automotive human machine interface: bridging the gap between driver and car

TRANSCRIPT

Automotive Human Machine Interface –Bridging the Gap Between Driver and Car

Krishna Jayaraman, Research Associate

Automotive and Transportation Industry

29th September 201129th September 2011

Functional Expertise

� More than an year of automotive research experience, having worked on over three projects on a global scale. Specific expertise in:

- New market entry and diversification strategies

- New business model analysis and evaluation

- Competitive benchmarking and OEM strategy analysis

Industry Expertise

� Experienced in Automotive Infotainment and Telematics, specific expertise in:

- In-vehicle connectivity, interfacing of smartphone and other consumer electronics in car

- Infotainment and Navigation platforms

Today’s Presenter: Krishna Jayaraman

- Automotive Human machine interface

What I bring to the Team

� Understanding of the automotive infotainment market and growing trends in interiors and connectivity.

� Data analysis and representation, extensive presentation skills.

� Knowledge about dynamics between consumer electronics (smartphone) and automotive industry

Career Highlights

� Research Associate, tracking industry trends in Automotive Infotainment and Telematics.

� Engineering intern at Engine factory, Ministry of Defense, Chennai.

Education

Bachelors in Engineering in Mechanical Engineering, Anna University, Chennai

Krishna JayaramanResearch AssociateAutomotive & Transportation

Frost & SullivanSouth Asia Chennai, India

Agenda

Industry needs and HMI selection criteria 4

HMI Development Strategy 5

Elements of HMI 6

Industry Challenges 7

Key Market Trends 8

Overview of Central Displays 9

Overview of Head up Displays 10

Overview of Instrument Clusters 11

Connectivity and Revenue Generation models 12

Proliferating Industry Alliances 13

3

Proliferating Industry Alliances 13

Market expectations for Voice Control Interface and Multifunctional Knobs 14

Future HMI approach 15

Conclusions 16

Highlights of the Research 17

Highlights from Comfort and Convenience study, existing and future production plan 18-23

Existing and Upcoming Research 24

Next Steps 27

For Additional Information 30

Criteria for HMI DevelopmentHMI Development Must Cater to Consumers’ Safety, Comfort and Ease of Use

Fail-safeRelevant

Information

Increase Efficient

Needed to improve occupant safety

Particularly for safety and navigation

Ease of use System cost

Increase comfort

Preferencesfor HMI applications

Particularly in telematics and

infotainment

Efficient controls

Choice between different controls or a single control for

the system

Source: Frost & Sullivan

Critical to increase uptake rates

HMI Development StrategyDesigning a user friendly and intuitive HMI allowing personalization of information is the key focus

Evaluating user needs

ObjectivesDesigning user

interaction modulePrototyping, evaluation

and testingFinal implementation

Input Output

HMI

Logic

Evaluation of user demands and expectations.

Designing a safe, easy to use and reliable HMI multimodal HMI concept with proper split of functions keeping user needs in mind.

Designing layout of display, different menu structures, HMI logic, choosing input and output options for different in-vehicle functionalities.

Based on different criteria a prototype HMI is made and is evaluated in the testing environment.

After tests and evaluation, the designed HMI is implemented in the dashboard of car.

“More and more features inside the car, doesn’t really make sense because it will make driving more difficult. So a balanced distribution of functions should be made on different types of available HMI in order to make the system less complex and easy for the user” – Leading Tier 1 Supplier

Consumer feedback

Feedback from testing

Source: Frost & Sullivan

Elements of HMINatural speech, touch screens and handwriting recognition will gain prominence in coming years, 3D HMI and reconfigurable displays will be the preferred technologies

Output

Multifunctional/

Rotary Knob

Touch Screen, Touch pads/

Camera based visual inputs

Voice notifications and alerts

HMI Logic

Inp

ut Touch Screen, Touch pads/

Handwriting recognition

Steering wheel controls

Buttons on system/console

Voice commands

((( )))

((( )))

Central displays, HUDs, instrument

clusters and RSE displays

Haptic feedback for safety systems

Industry ChallengesDriver distraction focused information prioritization to be the key challenge

Industry Challenges

High cost

Smartphone interfacing

Prioritization and split of information content

Source: Frost & Sullivan

Industry Challenges

Interior space constraints

Driver distraction

Challenge from aftermarket products

Key Market TrendsVoice technology will be the next big thing, Multifunctional knobs to be prevalent in luxury segment

Initial acceptance in premium segment, will trickle down to mass market in future

Market primarily driven

Voice enabled telephony and media controls to notice high penetration

Negligible penetration, restricted to luxury segment

Market Trends – North AmericaMarket Trends – Europe

Most preferred type of HMI controlling almost all functionalities

Market primarily driven by premium automotive segment

Increasing need for HUDs and large central display screens

restricted to luxury segment

Functions like cruise control, telephony and media controls to be seen on steering wheel

High preference towards touch screens and large central displays

Central DisplaysDemand for central displays will be driven by infotainment functionalities

Music control

Radio

Local information

Navigation

Ce

ntra

l dis

pla

y

Safety andDAS

What level of functionality integration can be

expected?

Telephone

Vehicle diagnostics

Smartphoneapps

Internet

System Settings

TV tuner

Smartphone and USB interfacing

Ce

ntra

l dis

pla

y

Climatecontrols

“On the positive side, we see true color information representation, dynamics, andhighly sophisticated graphics. Display size also matters with respect to a moreappropriate size of the displayed information. On the negative side, we arechallenged by display packaging, power consumption and heat development “ –Tier 1 supplier

“On the positive side, we see true color information representation, dynamics, andhighly sophisticated graphics. Display size also matters with respect to a moreappropriate size of the displayed information. On the negative side, we arechallenged by display packaging, power consumption and heat development “ –Tier 1 supplier

Overview of Head up displaysHUDs are gaining prominence amidst issue of high cost

Virtual Image at bumper distanceWindshield

Why head up display?

Prioritization of information

Minimal driver distraction

Reduction in cost of electronics

favor customers

Brand differentiation tool

Safety mandates, legislations and

regulations

Is cost the

Driver

LC Display

Aspheric Mirror

FoldMirror

Source: Frost & Sullivan

Brand differentiation tool

High cost

Increased complexity of the system

“HUDs will be always limited to projecting information that is relevant while driving. Addition of infotainmentfunctionalities doesn’t make sense because driver gets distracted. HUDs will never replace the instrumentcluster in a driver’s dash board. ” - Leading Tier 1 Supplier

Is cost the primary barrier for

market uptake?

Instrument ClustersClusters go digital to prioritize information

Analog control

systems

Analog-Digital control systems

Fully digital control systems

3D interfaces and high graphics

2005 2010 2013 2017

Electromechanical instrument clusters Focus on graphical displays

ChallengesAdvantages

Needs

Widespread adoption of digital

instrument clusters, how is it

possible?

Source: Frost & Sullivan

Cloud based Vehicle based

Revenue Opportunity: HMI – Display

Apps

All Data accessed from CloudSmartphone / in-built modem used for connectivity

Revenue Opportunity: HMI - Display

Apps

Smartphone used for connectivity

Connectivity and Revenue Generation ModelsConnectivity is being provided by telecom operators, the only way OEMs can make money is through their HMI

Provider approach

Partial Intelligence in Car Smartphone based

Revenue Opportunity: App / embedded unit

Virtual skins loaded both on car and mobile phoneSmartphone provides connectivity

Revenue Opportunity: HMI - Display

Apps AppsApps

Source: Frost & Sullivan

Replicator approachEnabler approach

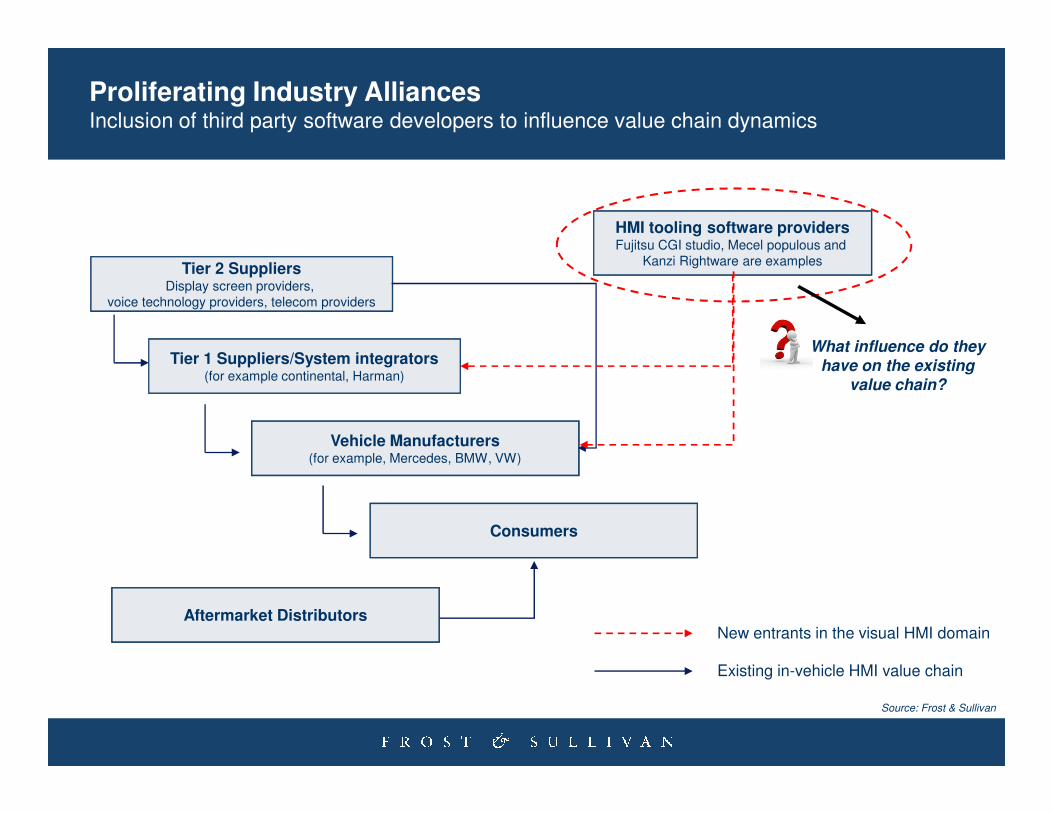

Proliferating Industry AlliancesInclusion of third party software developers to influence value chain dynamics

Tier 2 SuppliersDisplay screen providers,

voice technology providers, telecom providers

Tier 1 Suppliers/System integrators(for example continental, Harman)

HMI tooling software providersFujitsu CGI studio, Mecel populous and

Kanzi Rightware are examples

What influence do they have on the existing

value chain?

Source: Frost & Sullivan

Vehicle Manufacturers(for example, Mercedes, BMW, VW)

Consumers

Aftermarket Distributors

Existing in-vehicle HMI value chain

New entrants in the visual HMI domain

Overview of Total HMI MarketBasic voice interface to witness high penetration across all segments, advanced voice to favor mass market adoption in the future

0

20

40

60

80

100

Basic Voice Interface Advanced Voice Interface Multifunctional Knobs

Penetration of HMI interfaces in 2014

2017

~62%

~26%

~7%

~20%

~10%~6%

Ve

hic

le p

en

etr

atio

n(%

)

Ve

hic

le p

en

etr

atio

n(%

)

Ve

hic

le p

en

etr

atio

n(%

)

Automotive Human Machine Interface Market: Forecasts for Total HMI market (Europe), 2010,2014 and 2017

~38%

~17%~6%

2010

2010Basic Voice Interface Advanced Voice Interface Multifunctional Knobs

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

2017

Automotive Human Machine Interface Market: Forecasts for Total HMI market (North America), 2010,2014 and 2017

Note: Advanced voice includes basic voice package.

0

20

40

60

80

100

Basic Voice Interface Advanced Voice Interface Multifunctional Knobs

Penetration of HMI interfaces in 2014

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan

2017

~68%

~34%

~5%

~24%

~10%~4%

Ve

hic

le p

en

etr

atio

n(%

)

Ve

hic

le p

en

etr

atio

n(%

)

Ve

hic

le p

en

etr

atio

n(%

)

~43%

~20%~5%

Future HMI approachOEMs are reluctant about introducing a system fully dependent on smartphones

OEM controlled Filtering

Personalization of information display

New concepts like Eco route to

OEM control on the information content

HMI alone cannot reduce driver

Integration of DAS in the line of sight of driver

OEM controlled apps certification for in-vehicle use.

Filtering information

Where are the revenues coming

from?

New concepts like Eco route toinduce developments in visual HMI

Driver assistance

system

Infotainment system

udio isual aptic

HMI

Consumer electronics

To Driver

Approach to reduce distraction

HMI alone cannot reduce driverdistraction, integration of safetysystems with visual interfaces.

Conclusions HMI market is closely linked to consumer uptake rates of the optional packages

To develop a user interface that is simple, accessible,less distractive and affordable is the most significantchallenge. The location of user interface and the type ofinformation depending on the driving conditions are themain issues in the development of an efficient HMI.

Consumer demands for safety and conveniencealong with vehicle manufacturers’ strategy to realize their brand philosophy are likely to be the major driving forces of the automotive human machine interface market.

Brand differentiation

to be the major driver

Efficient

and cost-effective

HMI is the key

End Consumers to play an important

factor

Conclusions

Advanced and innovative HMI such as HUD are very expensive. Consumers find most of the innovative solutions as features that they are not willing to pay for. Thus, most of the solutions are limited to premium segment vehicles.

Conclusion from the Consumer Research

Source: Frost & Sullivan

Integration of the user interfaces of various comfortand safety systems into one single system throughlocalisation and multi-modality is a growingtrend as it reduces the number of interfaces andECUs needed for the system.

Localisation and multi-modality is

the trend

Highlights of the Research Service

�Detailed analysis of market and technology trends

of the European and North American automotive

HMI market.

�Revenues and unit shipments analysis of various

HMI technologies including voice control system,

haptic interface and visual interfaces.

�Consumer perceptions towards different HMI

technologies and their willingness to pay towards the

systems.

�Scenario analysis for unit and revenue forecasts for

various HMI technologies.

�OEM and supplier strategies on human machine

interface technologies, multi-modal HMI solutions.

�Drivers, restraints, industry challenges and their

impact analysis on automotive HMI.

�OEM and supplier profiles

�Regional differences in technology adoption and

take rates.Source: Frost & Sullivan

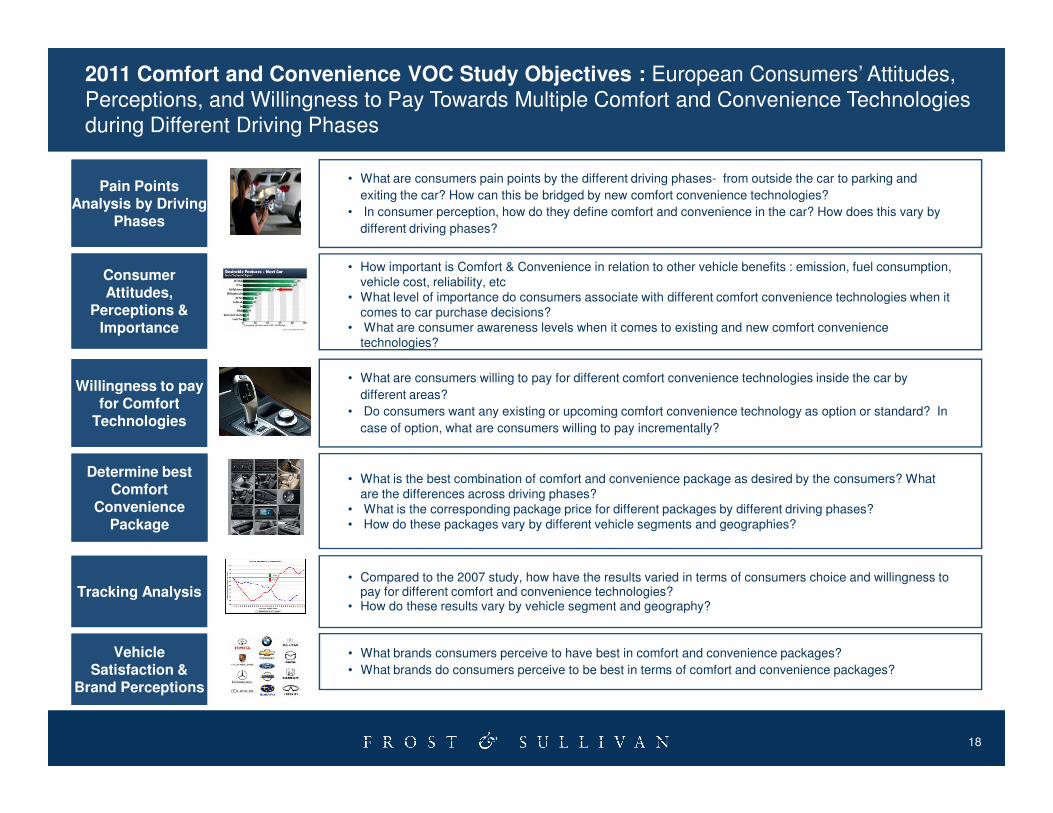

• What are consumers pain points by the different driving phases- from outside the car to parking and

exiting the car? How can this be bridged by new comfort convenience technologies?

• In consumer perception, how do they define comfort and convenience in the car? How does this vary by

different driving phases?

• How important is Comfort & Convenience in relation to other vehicle benefits : emission, fuel consumption, vehicle cost, reliability, etc

• What level of importance do consumers associate with different comfort convenience technologies when it comes to car purchase decisions?

• What are consumer awareness levels when it comes to existing and new comfort convenience technologies?

• What are consumers willing to pay for different comfort convenience technologies inside the car by

different areas?

• Do consumers want any existing or upcoming comfort convenience technology as option or standard? In

Pain Points Analysis by Driving

Phases

Consumer Attitudes,

Perceptions & Importance

Willingness to pay for Comfort

2011 Comfort and Convenience VOC Study Objectives : European Consumers’ Attitudes, Perceptions, and Willingness to Pay Towards Multiple Comfort and Convenience Technologies during Different Driving Phases

18

• Do consumers want any existing or upcoming comfort convenience technology as option or standard? In

case of option, what are consumers willing to pay incrementally?

• What brands consumers perceive to have best in comfort and convenience packages?

• What brands do consumers perceive to be best in terms of comfort and convenience packages?

• Compared to the 2007 study, how have the results varied in terms of consumers choice and willingness to pay for different comfort and convenience technologies?

• How do these results vary by vehicle segment and geography?

Vehicle Satisfaction &

Brand Perceptions

Tracking Analysis

• What is the best combination of comfort and convenience package as desired by the consumers? What are the differences across driving phases?

• What is the corresponding package price for different packages by different driving phases? • How do these packages vary by different vehicle segments and geographies?

Determine best Comfort

Convenience Package

for Comfort Technologies

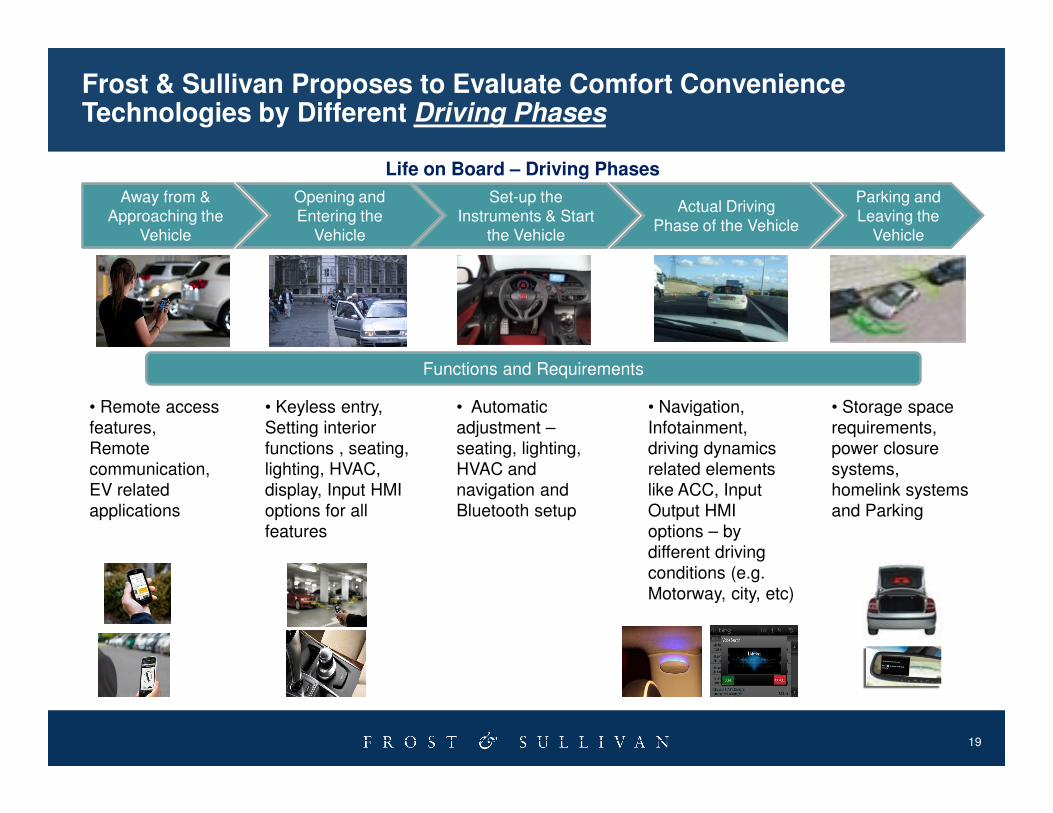

Away from & Approaching the

Vehicle

Opening and Entering the

Vehicle

Set-up the Instruments & Start

the Vehicle

Actual Driving Phase of the Vehicle

Parking and Leaving the

Vehicle

Life on Board – Driving Phases

Functions and Requirements

• Remote access • Keyless entry, • Storage space • Navigation, • Automatic

Frost & Sullivan Proposes to Evaluate Comfort Convenience Technologies by Different Driving Phases

19

• Remote access features, Remote communication, EV related applications

• Keyless entry, Setting interior functions , seating, lighting, HVAC, display, Input HMI options for all features

• Storage space requirements, power closure systems, homelink systems and Parking

• Navigation, Infotainment, driving dynamics related elements like ACC, Input Output HMI options – by different driving conditions (e.g. Motorway, city, etc)

• Automatic adjustment –seating, lighting, HVAC and navigation and Bluetooth setup

ComfortConvenience Area

Current Features Expected Future Features

Vehicle Access and Security

� Passive Keyless Entry� Remote Keyless Entry � Smart car key� Remote communication app – pre-conditioning � Remote Communication App – Vehicle Finder� Remote door lock unlock� Smart key fob - with Near Field Communication� Integration of Key Fob with smartphone application� Fingerprint recognition

�Under Vehicle Surveillance Systems� Enhanced command/control of all vehicle functions� Notification of vehicle security and diagnostic alerts� Eco-scores� Matching driving history/patterns with Picture ID of driver� Linkage to OEM Web portals for maintenance reminders � Automatic opt-in marketing data on vehicle usage and driver preferences� Control of vehicle functions remotely with graphical confirmation (e.g. doors, windows, engine start, HVAC, seat, navigation, audio)� Reconfiguration of vehicle preference settings easily and remotely

Lighting �Interior Ambient Lighting with Accent colors �Welcome and departure lighting

Existing and Upcoming Technology Elements in Different Comfort and Convenience Domains (not exhaustive and to be finalised with clients)

20

Lighting �Interior Ambient Lighting with Accent colors�Interior LED lighting electronics, for steering, switches & controls �Door ajar warning light �Play Protection

�Welcome and departure lighting �Fiber Optic 3D Light Guide �Climatised/ Personalized Ambient Lighting - White LED with light guide/curtain�Automatic Mood Lighting

HVAC �Automatic A/C�Individual Occupant Air-conditioning (Multi-Zone)�Direct Heating and Cooling of passengers (Through Seat)� Odor / Dust Control (anti-microbial/moisture resistant technology

�HMI (Speech recognition for A/c control� Smartphone apps for HVAC activation�Physiologically controlled A/c

Seats �Thermal sensors �Front seats with Luxury Massage function � Shoulder, lumbar, lateral and thigh support �Self-limiting Seat Heaters �Seat Position Memory

�Intelligent seats with sensing technologies�Humidity Control �Active Headrests �Integrated Child Seat (ICS) � Anti-whiplash seats� Multi Contour Backrest

ComfortConvenience Area

Current Features Expected Future Features

HMI , Cockpit, Displays and Instrument Clusters

� Touchscreen display -Resistive and Capacitive� Steering wheel controls � Multifunction switches � Voice Control – TTS and Advanced Voice Control� Mechanical switches� Fingerprint recognition� Driver d�Dual view displays� LED backlit displays – OLED � Touchscreen displays – capacitive, resistive� Head-up Displays� Drowsiness vibration alert

� Gesture control� Retina watch� Handwriting recognition� Proximity buttons� Holographic switches� Adaptive and programmable switches� Voice assisted ambient lighting� Nokia terminal mode� Hand-head gesture recognition� Emotion recognition� 3D Displays� Reconfigurable instrument cluster� AMOLED and PMOLED Displays� Holographic displays

Existing and Upcoming Technology Elements in Different Comfort and Convenience Domains (not exhaustive)

21

� Holographic displays� 10’ plus touch screens� Integrated center stack

Remote Access & Communication

�Remote light and horns operation� Remote immobilization� Remote vehicle status checks – oil level, etc

�Vehicle Diagnostics�Remote interior settings – seats, lights, temperature

Multimedia & Infotainment

�Embedded navigation system� Docked PND systems� Smartphone integration – wired, wireless� Bluetooth telephony� Rear seat entertainment – roof mounted, rear seat� Advanced audio system – speakers ,amplifiers

�Smartphone integration – terminal mode type solutions� Tablet based rear seat entertainment – e.g. Blackberry playbook� Mobile hotspot in car – internet access for passengers� 10” plus display screen� Application store & downloads to car

Other Key Areas � Roof (Sun roof, panoramic roof, etc)� Power closure systems� Homelink solutions� Space (Storage, leg room, etc)� NVH (Internal, external)

� Future NVH (brand specific noise, premium sound quality, etc)� Proximity sensing power closure systems� User programmable power closure controls

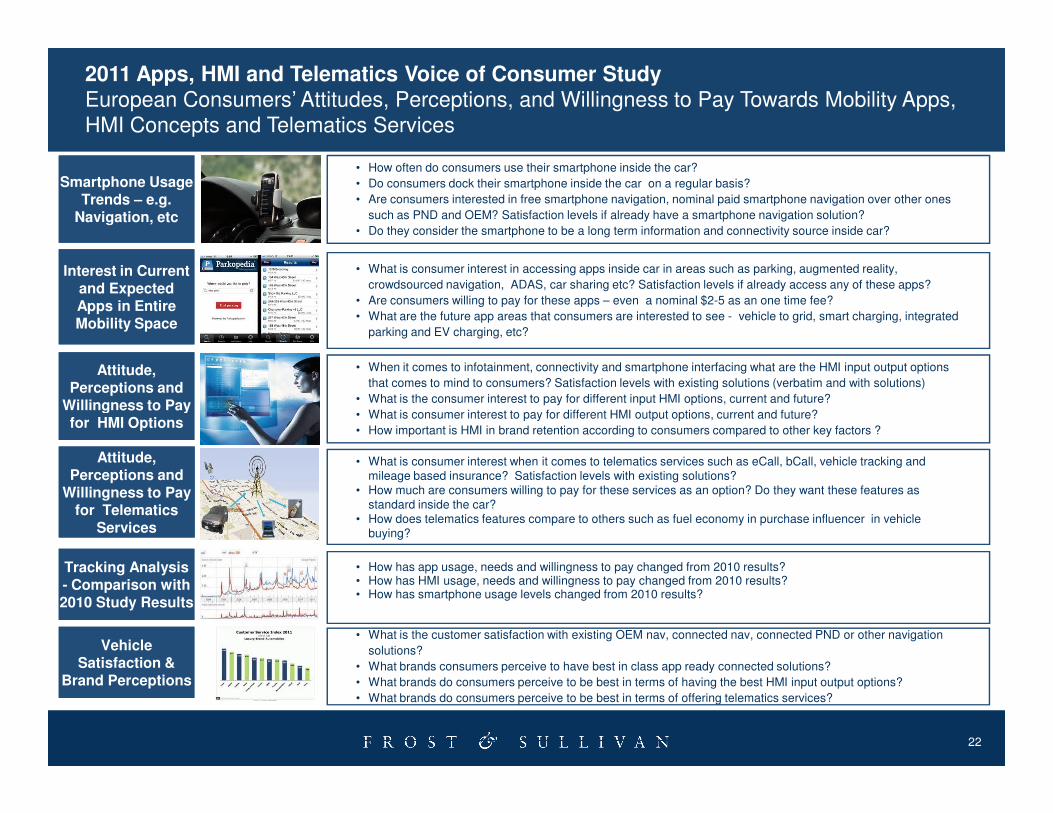

• How often do consumers use their smartphone inside the car?

• Do consumers dock their smartphone inside the car on a regular basis?

• Are consumers interested in free smartphone navigation, nominal paid smartphone navigation over other ones

such as PND and OEM? Satisfaction levels if already have a smartphone navigation solution?

• Do they consider the smartphone to be a long term information and connectivity source inside car?

• What is consumer interest in accessing apps inside car in areas such as parking, augmented reality,

crowdsourced navigation, ADAS, car sharing etc? Satisfaction levels if already access any of these apps?

• Are consumers willing to pay for these apps – even a nominal $2-5 as an one time fee?

• What are the future app areas that consumers are interested to see - vehicle to grid, smart charging, integrated

parking and EV charging, etc?

• When it comes to infotainment, connectivity and smartphone interfacing what are the HMI input output options

that comes to mind to consumers? Satisfaction levels with existing solutions (verbatim and with solutions)

• What is the consumer interest to pay for different input HMI options, current and future?

Smartphone Usage Trends – e.g.

Navigation, etc

Interest in Current and Expected Apps in Entire Mobility Space

Attitude, Perceptions and

Willingness to Pay

2011 Apps, HMI and Telematics Voice of Consumer StudyEuropean Consumers’ Attitudes, Perceptions, and Willingness to Pay Towards Mobility Apps, HMI Concepts and Telematics Services

22

• What is consumer interest to pay for different HMI output options, current and future?

• How important is HMI in brand retention according to consumers compared to other key factors ?

• What is the customer satisfaction with existing OEM nav, connected nav, connected PND or other navigation

solutions?

• What brands consumers perceive to have best in class app ready connected solutions?

• What brands do consumers perceive to be best in terms of having the best HMI input output options?

• What brands do consumers perceive to be best in terms of offering telematics services?

• How has app usage, needs and willingness to pay changed from 2010 results? • How has HMI usage, needs and willingness to pay changed from 2010 results?• How has smartphone usage levels changed from 2010 results?

Vehicle Satisfaction &

Brand Perceptions

Tracking Analysis - Comparison with 2010 Study Results

• What is consumer interest when it comes to telematics services such as eCall, bCall, vehicle tracking and mileage based insurance? Satisfaction levels with existing solutions?

• How much are consumers willing to pay for these services as an option? Do they want these features as standard inside the car?

• How does telematics features compare to others such as fuel economy in purchase influencer in vehicle buying?

Attitude, Perceptions and

Willingness to Pay for Telematics

Services

Willingness to Pay for HMI Options

2012

Strategic Analysis of OE and Aftermarket Automotive Telematics Market Including Services such as Emergency/Breakdown Assistance, Stolen Vehicle Tracking, Usage-based Insurance in Europe and North America

2012

Strategic Analysis of OE and Aftermarket Automotive Telematics Market Including Services such as Emergency/Breakdown Assistance, Stolen Vehicle Tracking, Usage-based Insurance in Russia and Brazil

2012

Strategic Update of the In-Car Audio Systems and Accessories Market including Speakers, Amplifiers, Aux-in Features and Sound Processing Technologies in Europe and North America

2012Executive Analysis of Smartphone Interface Technologies such as Mirrorlink and its Impact in the European and North American Market

• Location-based

services

• GPS / Navigation

systems

• Infotainment systems

• Wireless

Telematics, HMI, Connectivity and Navigation Related Upcoming Research – 2012

23

2012 Impact in the European and North American Market

2012Strategic Analysis of Remote Vehicle Diagnostics Services in Passenger Vehicles in EU and NA

2012 Strategic Analysis of the Electronic Toll Collection Market in Europe and North America

2012Global OEM Benchmarking Study on Connected Telematics and Infotainment Offerings and Strategies

2012Strategic Dashboard for Passenger Vehicle Telematics , Infotainment and Connectivity in Europe, North America and China – 2012 Edition

• Wireless

Communication /

Bluetooth

• CV Telematics

• RVD

3G, GPRS. HSDPA, UMTS, WiFi

Forthcoming* Draft titles subject to change based on other customer feedback as well

2011Key Trends and Forecasts of Navigation Systems and Telematics Services in China, India and Select APAC Markets

2011Key Trends and Forecasts of Navigation Systems and Telematics Services in North and Latin American Markets

2011Key Trends and Forecasts of Navigation Systems and Telematics Services in Western and Eastern European Markets including Russia

2011Strategic Analysis of European and North American Automotive Human Machine Interface Market -Part 2 Display and Instrument Clusters

2011Connectivity, App Stores and Cloud-based Delivery Platforms - Future of Connected Infotainment and Telematics Market

Strategic Analysis of Global Automotive Market for IT Mobility Platforms

• Location-based

services

• GPS / Navigation

systems

• Infotainment systems

• Wireless

Telematics, HMI, Connectivity and Navigation Related Existing and Upcoming Research – 2010 and 2011

24

2011Strategic Analysis of Global Automotive Market for IT Mobility Platforms Billing and Smart Charging are Two Key Opportunity Areas in the EV Infrastructure Segment

2011Strategic Analysis of European and North American Automotive Human Machine Interface Market -Part 1 Steering Wheel Controls, Voice Interfaces and Multifunctional Switches

2010Executive Analysis of European Consumers’ Awareness and Preferences for Usage of Smartphone Apps Inside and Outside Car

2010Strategic Analysis of the Impact of Smartphones and Apps on the European and North American Infotainment Market

2010Strategic Analysis of the North American Market for Telematics-Enabled Usage-based Insurance Market

2010 Strategic Analysis of North American Embedded-Connected Hybrid Telematics Market

2010 Strategic Analysis of the European Market for Telematics -enabled Usage-based Insurance

2010 Automotive Telematics Application Stores – Will it Succeed like the Apple App Store Concept

• Wireless

Communication /

Bluetooth

• CV Telematics

• RVD

3G, GPRS. HSDPA, UMTS, WiFi

Forthcoming

Existing

• Location-based

services

• GPS / Navigation

systems

• Infotainment systems

• Wireless

2009 Strategic Analysis of European and North American Green Telematics Market for Passenger Vehicles

2009 Global Trend Analysis of Passenger Vehicle Telematics and Infotainment Systems – 2009 Edition

2009 Strategic Dashboard for Automotive Telematics and Infotainment Systems - Q2 2009 Edition

2009 Strategic Analysis of European Market for Low Cost OEM Navigation Systems

2009 Strategic Analysis of the European Automotive Human Machine Interface Market

2009 Strategic Analysis of Automotive Telematics Market for Wireless and Connectivity Technologies

2008Comparative Analysis of European, North American, Chinese, South Korean and Indian Telematics Markets

2008 Strategic Analysis of European Market for ADAS Systems Using Digital Maps

2008 Executive Update of European Passenger Vehicle Telematics and Infotainment Markets

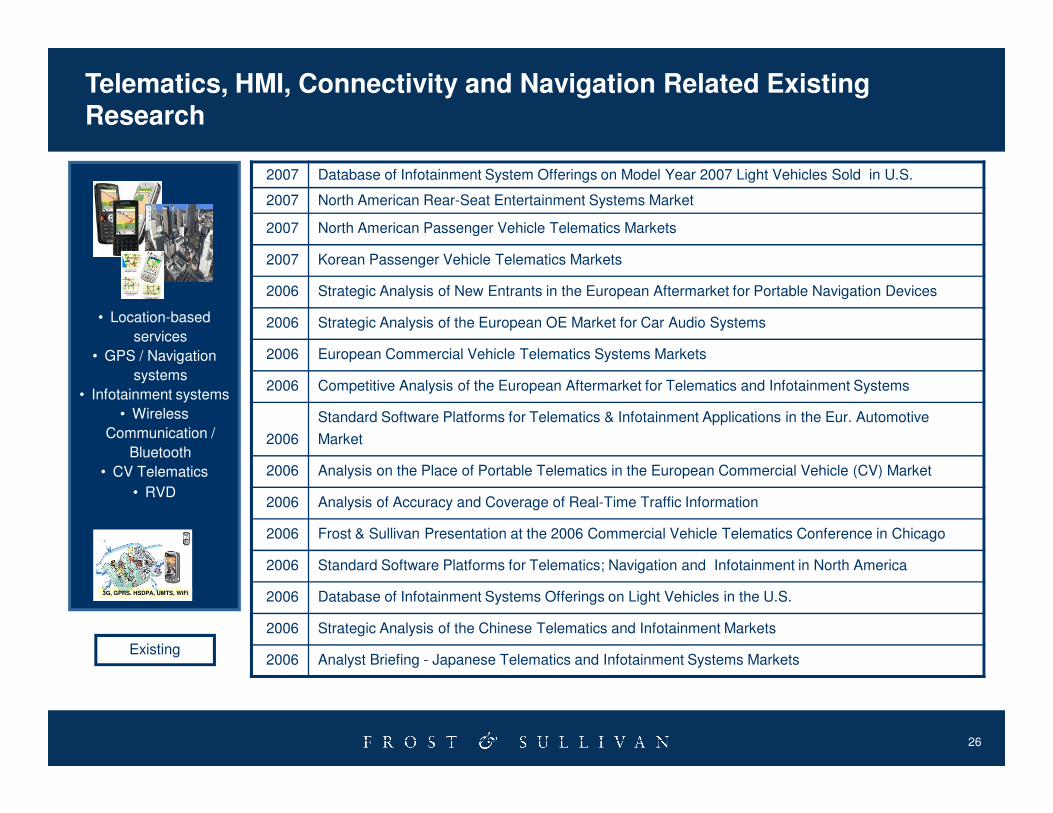

Telematics, HMI, Connectivity and Navigation Related Existing Research

25

• Wireless

Communication /

Bluetooth

• CV Telematics

• RVD

3G, GPRS. HSDPA, UMTS, WiFi

2008 Executive Update of European Passenger Vehicle Telematics and Infotainment Markets

2008 An Update of European Markets for Telematics Based Pay-As-You-Drive Vehicle Insurance

2008 Strategic Analysis of European Markets for Stolen Vehicle Tracking Systems

2008 Strategic Analysis of the European Markets for eCall and bCall Systems

2008 European Aftermarket for Access and Security Systems

2007 Strategic Analysis of the European Markets for Telematics Based Car Insurance Systems

2007 Global Trends Analysis of the Telematics and Infotainment Markets for Passenger Vehicles

2007 Strategic Analysis of Continental Automotive Systems' Telematics Business Unit

2007 Strategic Re-evaluation of the European Markets for Telematics and Infotainment Systems

2007 Strategic Analysis of the North American OE Car Audio System Markets

2007 Analysis of the North American Automotive Navigation Systems Market

Existing

2007 Database of Infotainment System Offerings on Model Year 2007 Light Vehicles Sold in U.S.

2007 North American Rear-Seat Entertainment Systems Market

2007 North American Passenger Vehicle Telematics Markets

2007 Korean Passenger Vehicle Telematics Markets

2006 Strategic Analysis of New Entrants in the European Aftermarket for Portable Navigation Devices

2006 Strategic Analysis of the European OE Market for Car Audio Systems

2006 European Commercial Vehicle Telematics Systems Markets

2006 Competitive Analysis of the European Aftermarket for Telematics and Infotainment Systems

• Location-based

services

• GPS / Navigation

systems

• Infotainment systems

• Wireless

Telematics, HMI, Connectivity and Navigation Related Existing Research

26

2006

Standard Software Platforms for Telematics & Infotainment Applications in the Eur. Automotive

Market

2006 Analysis on the Place of Portable Telematics in the European Commercial Vehicle (CV) Market

2006 Analysis of Accuracy and Coverage of Real-Time Traffic Information

2006 Frost & Sullivan Presentation at the 2006 Commercial Vehicle Telematics Conference in Chicago

2006 Standard Software Platforms for Telematics; Navigation and Infotainment in North America

2006 Database of Infotainment Systems Offerings on Light Vehicles in the U.S.

2006 Strategic Analysis of the Chinese Telematics and Infotainment Markets

2006 Analyst Briefing - Japanese Telematics and Infotainment Systems MarketsExisting

• Wireless

Communication /

Bluetooth

• CV Telematics

• RVD

3G, GPRS. HSDPA, UMTS, WiFi

Next Steps

� Request a proposal for Growth Partnership Services or Growth Consulting Services to support you and your team to accelerate the growth of your company. ([email protected])

� Join us at our annual Growth, Innovation, and Leadership 2012: A Frost & Sullivan Global Congress on Corporate Growthoccurring 15 – 16 May, 2012 (www.gil-global.com)

27

� Register for Frost & Sullivan’s Growth Opportunity Newsletter and keep abreast of innovative growth opportunities (www.frost.com/news)

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

What would you like to see from Frost & Sullivan?

28

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

http://twitter.com/frost_sullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

For additional information

Katja FeickCorporate Communications

Automotive & Transportation

+49 (0) 69 [email protected]

Cyril Cromier

Sales Director

Automotive & Transportation Europe

+31 (1) 42 81 22 44

Praveen Chandrasekar

Program Manager

Automotive & Transportation

+91-44-66814129

Franck Leveque

Vice President – Growth Consulting

Automotive & Transportation Europe

+49 (0)69 770 33 21