australian auditor independence...

TRANSCRIPT

Australian Auditor Independence Requirements

A Comparative Review

The Treasury

November 2006

© Commonwealth of Australia 2006

ISBN 0 642 74369 X

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission from the Commonwealth. Requests and inquiries concerning reproduction and rights should be addressed to the:

Commonwealth Copyright Administration Attorney-General’s Department Robert Garran Offices National Circuit Canberra ACT 2600 Or posted at:

http://www.ag.gov.au/cca

Consultation

Comments are sought on this comparative review by no later than 15 December 2006. Submissions should be sent by mail, fax or email to: The General Manager Corporations and Financial Services Division Department of the Treasury Langton Crescent PARKES ACT 2600

Facsimile: 02 6263 2770 Email: [email protected] Phone: 02 6263 3971

Confidentiality

All submissions will be treated as public unless the author clearly indicates to the contrary. A request made under the Freedom of Information Act 1982 for access to a submission marked confidential will be determined in accordance with that Act.

FOREWORD

Auditors perform a critical role in the efficient operation of capital markets. The audit function constitutes the principal external check on the integrity of financial statements and auditor independence is fundamental to the credibility and reliability of auditors’ reports.

The Australian Government significantly enhanced Australia’s auditor independence requirements with the comprehensive regime introduced by the Corporate Law Economic Reform Program (Audit Reform and Corporate Disclosure) Act 2004 which commenced on 1 July 2004.

The comparative review of Australian Auditor Independence Requirements compares the Australian requirements with those in Canada, the European Union, the United Kingdom and the United States. With the globalisation of capital markets and cross-border activities of companies and audit firms, it is now essential that the design of the regulatory framework in one jurisdiction should take account of developments in other jurisdictions.

The overall conclusion of the comparative review is that, notwithstanding differences in terminology, institutional arrangements and legal frameworks, there is a substantial underlying equivalence between the Australian requirements and ‘best practice’ standards adopted internationally.

I am pleased to release the comparative review of Australian Auditor Independence Requirements. A number of the key findings in the review are directly relevant to the Australian Government’s commitment to simplifying the regulatory system and reducing unnecessary or excessive red tape.

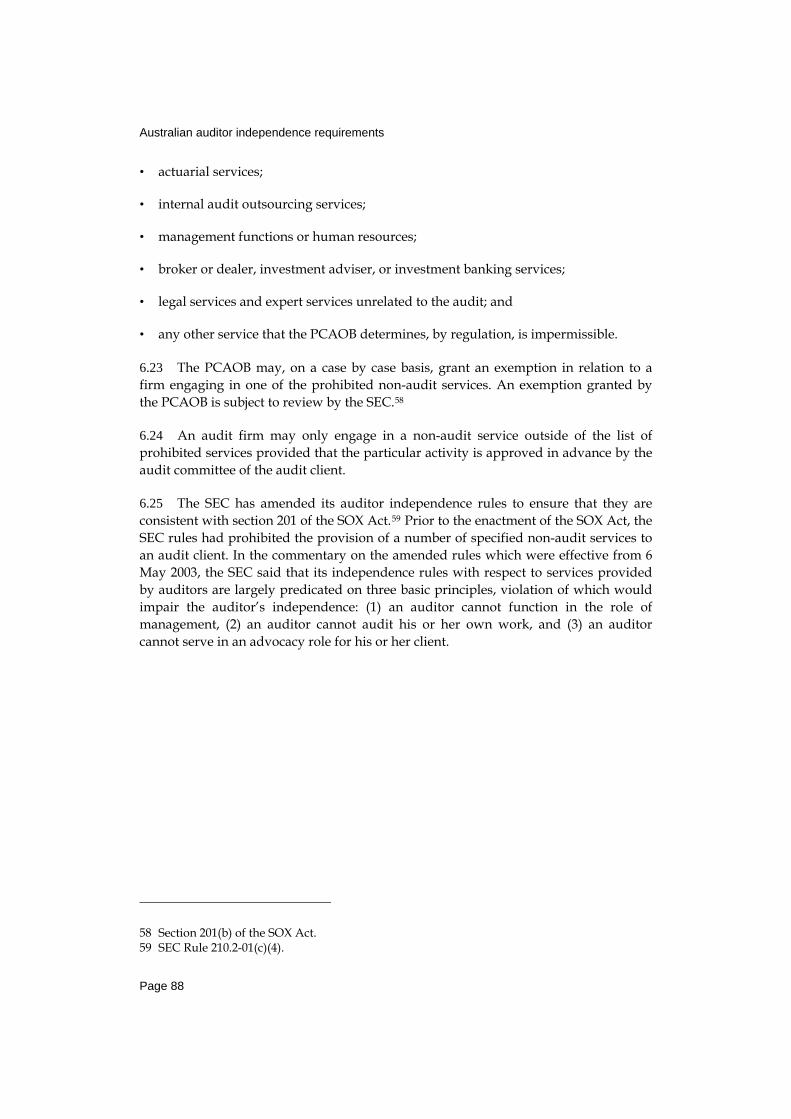

Among its key findings, the comparative review identifies the Australian multiple former audit firm partner restriction as having no overseas equivalent. The Australian Government announced in its response to the report of the Taskforce on Reducing Regulatory Burdens on Business that it will review this restriction by the end of 2006.

While the comparative review does not attempt to make policy recommendations, a number of the other key findings suggest that there may be scope, in line with overseas developments, to make further refinements which would result in a reduction in the compliance burden, without changing or weakening the existing, robust regulatory framework.

To this end, Treasury’s comparative review will make a significant contribution in factually informing the policy debate in Australia on auditor independence issues among key stakeholders.

Page iii

Treasury will be conducting a targeted consultative process with key stakeholders, including the Australian Securities and Investments Commission, the Financial Reporting Council, the major audit firms and the three main professional accounting bodies. I also invite other stakeholders to comment on the key findings in the comparative review.

Through stakeholder consultation, my intention is to identify any additional measures that could be included in the proposed Simpler Regulatory System Bill which is scheduled to be introduced into Parliament in 2007.

The Hon Chris Pearce MP Parliamentary Secretary to the Treasurer

Page iv

CONTENTS

FOREWORD ........................................................................................................ III

ABBREVIATIONS ................................................................................................VII

PART 1: INTRODUCTION .......................................................................................1 Background to the comparative review........................................................................... 1 Scope of the review......................................................................................................... 2

PART 2: EXECUTIVE SUMMARY ............................................................................5 Part 1: Introduction......................................................................................................... 5 Part 3: Auditor independence: policy goals, institutional arrangements and

legal framework .................................................................................................. 6 Part 4: General standard of auditor independence........................................................ 9 Part 5: Specific auditor independence requirements applying to employment,

financial and business relationships.................................................................10 Part 6: Provision of non-audit services ........................................................................13 Part 7: Employment restrictions applying to former audit partners and senior

audit personnel .................................................................................................15 Part 8: Auditor rotation .................................................................................................17 Conclusion.....................................................................................................................19

PART 3: AUDITOR INDEPENDENCE: POLICY GOALS, INSTITUTIONAL ARRANGEMENTS AND LEGAL FRAMEWORK..........................................................25 Introduction....................................................................................................................25 Loss of credibility in financial reporting has been the major policy driver of reforms ..........................................................................................................................25 International efforts to address crisis ............................................................................25 Australia ........................................................................................................................28 Canada ..........................................................................................................................33 European Union ............................................................................................................37 United Kingdom.............................................................................................................38 United States.................................................................................................................42

PART 4: GENERAL STANDARD OF AUDITOR INDEPENDENCE ................................47 The auditor independence concept...............................................................................47 Australian and US ‘statute-based’ requirements...........................................................48 Canada ..........................................................................................................................51 European Union ............................................................................................................51 United Kingdom.............................................................................................................52

Page v

Australian auditor independence requirements

PART 5: SPECIFIC AUDITOR INDEPENDENCE REQUIREMENTS APPLYING TO EMPLOYMENT, FINANCIAL AND BUSINESS RELATIONSHIPS ...................................53 Restrictions on employment relationships ....................................................................53 Australia ........................................................................................................................54 Comparison between Australian and overseas employment relationship restrictions .....................................................................................................................58 Financial relationships...................................................................................................66 Prohibited business relationships..................................................................................79

PART 6: PROVISION OF NON-AUDIT SERVICES .....................................................83 Introduction....................................................................................................................83 Australia ........................................................................................................................84 Canada ..........................................................................................................................86 European Union ............................................................................................................86 United Kingdom.............................................................................................................86 United States.................................................................................................................87 Comparative table .........................................................................................................89 Concluding comments...................................................................................................91

PART 7: EMPLOYMENT RESTRICTIONS APPLYING TO FORMER PARTNERS OF AUDIT FIRMS AND SENIOR AUDIT PERSONNEL .................................................93 ‘Cooling-off’ periods ......................................................................................................93 Multiple former partner of audit firm/audit company director restriction........................99

PART 8: AUDITOR ROTATION............................................................................101 Introduction..................................................................................................................101 Australia ......................................................................................................................102 Canada ........................................................................................................................104 European Union ..........................................................................................................105 United Kingdom...........................................................................................................105 United States...............................................................................................................107 Concluding comments.................................................................................................108

Page vi

ABBREVIATIONS

AICPA The American Institute of Certified Public Accountants

APB Auditing Practices Board, UK

APESB Accounting Professional and Ethical Standards Board

APES 110 The Australian Code of Ethics for Professional Accountants APES 110

AQRB The Audit Quality Review Board

ASIC Australian Securities and Investments Commission

ASIC Act Australian Securities and Investments Commission Act 2001

CALDB The Companies Auditors and Liquidators Disciplinary Board

CICA Canadian Institute of Chartered Accountants

CPAB Canadian Public Accountability Board

CLERP 9 Act Corporate Law Economic Reform Program (Audit Reform and Corporate Disclosure) Act 2004

Corporations Act Corporations Act 2001

CSA Canadian Securities Administrators

EU European Union

EU Recommendation EU Recommendation: Statutory Auditors’ Independence in the EU: A Set of Fundamental Principles (May 2002)

FRC Financial Reporting Council

FRCUK Financial Reporting Council, UK

FRP Financial Reporting Panel

HIH HIH Insurance Limited

ICAA The Institute of Chartered Accountants in Australia

ICAEW The Institute of Chartered Accountants in England and Wales

ICAO The Institute of Chartered Accountants of Ontario

ICAO Rules The Rules of Professional Conduct adopted by the ICAO

IFAC International Federation of Accountants

IFAC Code Code of Ethics for Professional Accountants, IFAC

IOSCO International Organisation of Securities Commissions

Page vii

Australian auditor independence requirements

Abbreviations (continued)

ISB The Independence Standards Board, US

PCAOB Public Company Accounting Oversight Board

PIOB Public Interest Oversight Board

POB Professional Oversight Board, UK

NIA National Institute of Accountants

Ramsay report Review of the Independence of Australian Company Auditors (October 2001)

SEC Securities and Exchange Commission

SOX Act Sarbanes-Oxley Act of 2002

UK United Kingdom

US United States

Page viii

Part 1: Introduction

BACKGROUND TO THE COMPARATIVE REVIEW

1.1 The Financial Reporting Council’s (FRC) auditor independence functions are conferred on it under paragraphs 225(1)(c) and (d), and subsection 225(2B) of the Australian Securities and Investments Commission Act 2001 (ASIC Act).

1.2 Under subsection 225(1) of the ASIC Act, the FRC is required to monitor the effectiveness of auditor independence requirements in Australia and to give the Minister reports and advice about those requirements.

1.3 In addition, the FRC has been given a number of specific auditor independence functions under subsection 225(2B) of the ASIC Act. Paragraph 225(2B)(e) of the ASIC Act provides that these functions include, monitoring international developments in auditor independence, assessing the adequacy of the Australian auditor independence requirements provided for in the Corporations Act 2001 (the Corporations Act) and codes of professional conduct, in the light of those developments, and giving the Minister, and professional accounting bodies, reports and advice on any additional measures needed to enhance the independence of Australian auditors.

1.4 In view of its functions under paragraph 225(2B)(e) of the ASIC Act, the FRC sought Treasury’s assistance in undertaking a comparative review of the Australian auditor independence requirements with the equivalent requirements applying in Canada, the European Union, the United Kingdom, and the United States (the relevant overseas jurisdictions).

1.5 The Treasury agreed to assist the FRC in undertaking this comparative review in order to facilitate the preparation of the FRC’s 2005-06 Report on Auditor Independence. Auditor independence encompasses an extensive area and raises many complex issues. The new auditor independence regime in the Corporations Act was the most far-reaching and substantial measure included in the reforms introduced by the Corporate Law Economic Reform Program (Audit Reform and Corporate Disclosure) Act 2004 (the CLERP 9 Act).

Page 1

Australian auditor independence requirements

1.6 Treasury considers that the preparation of a comparative review is timely given that nearly five years have passed since a comparable exercise was undertaken by Professor Ian Ramsay in the review of the Independence of Australian Company Auditors (the Ramsay report1) and there have been two years of practical implementation since the commencement of the reforms. Treasury also proposes to use the comparative review for purposes of its central agency policy advisory role to the Government and in particular, the Treasurer and the Parliamentary Secretary to the Treasurer. Treasury will also be able to use the paper in its ongoing policy liaison responsibilities on behalf of the Government with other key stakeholders on auditor independence, such as ASIC, the major audit firms and the professional accounting bodies.

SCOPE OF THE REVIEW

1.7 Auditor independence is a complex and wide-ranging subject involving many difficult public policy decisions. In defining the scope of the review, Treasury has been selective in terms of:

• the independence topics covered in the review; and

• the jurisdictional focus of the review in relation to those overseas jurisdictions that have adopted federal systems of government.

1.8 In selecting the issues to be covered, we have concentrated on the following topics which we regard as core auditor independence requirements:

• General standard of auditor independence.

• Specific restrictions applying to employment, financial and business relationships.

• Provision of non-audit services.

• Employment restrictions applying to former audit partners and senior audit personnel.

• Auditor rotation.

1.9 In a comparative review of this sort, we also considered that it would be useful in a context setting sense, to examine, early in the review, the underlying policy goals, institutional arrangements and legal framework applying in each jurisdiction in relation to auditor independence.

1 Independence of Australian Company Auditors: Review of Current Australian Requirements and Proposals for Reform: Report to the Minister for Financial Services and Regulation: October 2001.

Page 2

Part 1: Introduction

1.10 Canada and the United States (US) have federal constitutions where the federal, provincial and state authorities have responsibility for audit regulation. The scope of the review in relation to these two federal jurisdictions has been limited:

• to the national system administered by the Canadian Public Accountability Board (CPAB), although the provincial requirements are addressed insofar as they impact on the CPAB framework; and

• to the federal securities regime in the US which includes the auditor independence rules of the Securities and Exchange Commission (SEC), the auditor independence requirements in the Sarbanes-Oxley Act 2002 (SOX Act) and the functions and role of the Public Company Accounting Oversight Board (PCAOB).

1.11 The European Union has issued a Recommendation and a Directive in relation to the independence of statutory auditors. The review will focus on the EU Recommendation and Directive but will not extend to auditor independence requirements in each of the EU member states (other than the United Kingdom (UK)).

Page 3

Part 2: Executive Summary

PART 1: INTRODUCTION

Background to the comparative review

2.1 The Treasury agreed to undertake the comparative review in order to assist the FRC prepare the FRC’s 2005-06 Report on Auditor Independence. The review focuses on the independence requirements in Australia, Canada, the European Union, the United Kingdom and the United States (the relevant overseas jurisdictions).

2.2 The Treasury also proposes to use the comparative review for purposes of its central agency policy advisory role to the Government and in particular, the Treasurer and the Parliamentary Secretary to the Treasurer. The review will also inform Treasury in its ongoing policy liaison responsibilities on behalf of the Government with other key stakeholders on auditor independence, such as ASIC, the major audit firms and the professional accounting bodies.

Scope of the review

2.3 The new auditor independence regime in the Corporations Act was the most far-reaching and substantial measure introduced by the CLERP 9 Act. The review is timely because it is nearly five years since a comparable exercise was undertaken by the Ramsay report.

2.4 The review focuses on the following core elements of auditor independence:

• General standard of auditor independence.

• Specific restrictions applying to employment, financial and business relationships.

• Provision of non-audit services.

• Employment restrictions applying to former audit partners and senior audit personnel.

• Auditor rotation.

Page 5

Australian auditor independence requirements

PART 3: AUDITOR INDEPENDENCE: POLICY GOALS, INSTITUTIONAL ARRANGEMENTS AND LEGAL FRAMEWORK

2.5 For purpose of background and context setting of the review, we examined the policy goals, institutional arrangements and legal framework in relation to auditor independence in each of the jurisdictions covered by the review.

2.6 A major policy driver of the reforms that have taken place over the past five years in relation to auditor independence and audit regulation generally has been the loss of credibility in financial reporting that followed the collapse of Enron and other major companies from late 2001. The reforms relating to audit regulation, including auditor independence, were one component of broader corporate governance reforms introduced in the wake of the collapse of Enron and other corporate failures.

2.7 With the globalisation of capital markets, this was recognised as a world-wide crisis and important initiatives have been taken at the international level to address these problems. In this context, the review has recognised the important contributions that have been made by governmental authorities, such as the International Organisation of Securities Commissions (IOSCO) and by the international accounting profession such as the revised Code of Ethics adopted by the International Federation of Accountants (IFAC). Common themes identified in the work of these bodies is that there is a trend towards greater consistency in global regulatory standards, and a recognition of the need for greater international cooperation and for the pursuit of the public interest at the international level.

2.8 While the review has found that many of the core elements of the auditor independence requirements in each jurisdiction are similar, there are substantial differences in the institutional arrangements relating to audit regulation and the legal framework applicable to the auditor independence requirements.

• While Australia has a federal constitutional system, it has been able to achieve a national system of corporations regulation as a result of an agreement between the Australian Government and the governments of the States and Territories involving the referral of powers to the Federal Government.

– ASIC, the key corporate regulator, is a statutory body established under federal legislation. All the other bodies performing specified functions in relation to the audit regulatory framework, including the FRC, have also been established under the umbrella of the national corporations legislation.

– Another distinguishing feature of the Australian auditor independence requirements is that the detailed requirements have been enacted by the Federal Parliament in the Corporations Act. This implements a key aspect of the Ramsay report that most of the enhanced auditor independence requirements recommended in the review should be placed in the Corporations Act, within a co-regulatory model. The HIH Royal Commission report also made some

Page 6

Part 2: Executive Summary

important recommendations on the audit function and most of these recommendations were premised on the basis that they would be implemented in the Corporations Act.

• Canada’s audit oversight institutional framework has been strongly influenced by the division of powers between the federal and provincial jurisdictions under its federal constitutional system. In Canada, the Canadian provinces and territories are responsible for securities regulation. To ensure that Canada has a national approach to securities regulation, the provincial securities regulators have formed the Canadian Securities Administrators (CSA). The accounting profession is also regulated at the provincial level.

– To ensure a national approach to the oversight of the audits of publicly listed entities, the CSA, the Canadian Institute of Chartered Accountants (CICA) and the Federal Superintendent of Financial Institutions created the Canadian Public Accountability Board (CPAB) in 2003. The CPAB is a federal not-for-profit corporation. It was not possible to establish CPAB as a statutory body because of the federal-provincial jurisdictional arrangements in Canada.

– The auditor independence rules that apply within the CPAB oversight framework are the standards for auditor independence that have been adopted by the provincial Institutes of Chartered Accountants. The CSA and CICA have been active in ensuring that the provincial standards have adopted the IFAC Code as well as some of the auditor independence requirements under the US SOX Act. In contrast to the position in Australia, where ASIC is responsible for the enforcement of the auditor independence requirements, enforcement of the independence rules in Canada is the function of the provincial Institutes of Chartered Accountants as part of the self-regulation of their members.

– The provincial auditor independence rules are substantially uniform. For purposes of the review, we have focused on the Rules of Professional Conduct of the Institute of Chartered Accountants of Ontario (ICAO Rules).

• The European Union (EU) is a union of 25 independent states based on the European Communities and founded to enhance political, economic and social cooperation. Treasury included the EU in the review in order to obtain a window on European policy consideration in relation to the issue of the independence of the statutory auditor. We have not attempted to study the EU’s internal governance arrangements or the auditor independence regimes in the member states, other than the United Kingdom.

• The United Kingdom (UK) undertook a wide-ranging work program to review the UK’s regulatory practices for statutory audit and financial reporting following the collapse of Enron and other high profile companies from late 2001 onwards. The UK Government sought a ‘relatively light touch’ approach by building on the existing framework for the regulation of the statutory auditor which devolved to recognised supervisory bodies (professional accounting bodies) the day to day

Page 7

Australian auditor independence requirements

responsibility for ensuring the training and authorisation of registered auditors and the supervision of audit firms.

– The key reform proposal was to expand significantly the scope of the responsibilities and powers of the Financial Reporting Council (FRCUK) to create a unified, non-statutory regulator. The FRCUK’s functions are principally exercised by its five operating bodies.

: For purposes of the review, the most relevant operating body is the Auditing Practices Board (APB). The APB’s responsibilities in relation to the development of auditing and assurance standards have been extended to the development of ethical standards relating to the independence, objectivity and integrity of auditors. The recognised supervisory bodies have been required to adopt the APB’s Ethical Standards for Auditors for purposes of their professional conduct rules.

• Under the federal constitutional system in the United States, the auditor independence framework consists of a matrix of federal securities laws, professional conduct rules and state laws relating to the licensing and regulation of the practice of accounting. For purposes of the review, we have focussed primarily on the federal auditor independence requirements, and particularly the rules of the SEC which were made in 2001 and then further enhanced in 2003 following the enactment of the SOX Act. There are important similarities between the Australian and US auditor independence regimes. Australia and the US have both adopted independence requirements that have legislative backing. The key regulators, ASIC, the SEC and the PCAOB are manifestly independent from the accounting profession. There are however some important differences:

– In accordance with the ‘internal affairs’ doctrine in the US, the states govern internal corporate affairs, while the federal rule-makers, particularly through the SEC, govern the external trading of a company’s securities. This is unlike the national system of corporate regulation that has been achieved in Australia.

– ASIC does not have the power to make rules of the kind made by the SEC or the PCAOB. In the US, the independent federal regulatory agencies, such as the SEC, have been granted extensive, quasi-legislative and quasi-judicial powers which have been held not to violate the separation of powers doctrine enshrined in the US constitution.

Page 8

Part 2: Executive Summary

Key finding 1 While many of the core elements of the auditor independence requirements, including their underlying policy objectives, in each jurisdiction are similar, the review has found substantial differences in the institutional arrangements and the legal framework applying to audit regulation in each jurisdiction. These differences can be explained by the unique combination of circumstances applying in each jurisdiction, including constitutional arrangements, history relating to the regulation of corporations and financial services and system of government.

Key finding 2 A distinguishing feature of the Australian auditor independence requirements compared with the overseas jurisdictions covered by the review, is that the detailed independence requirements have been enacted by the Federal Parliament in the Corporations Act to provide a comprehensive legislative code.

PART 4: GENERAL STANDARD OF AUDITOR INDEPENDENCE

2.9 The review discusses the widely accepted concept of independence which involves independence of mind and independence in appearance.

2.10 Both Australia and the US have adopted a general standard of auditor independence incorporating the concepts of independence of mind and appearance. The wording of the Australian general requirement of auditor independence is closely based on the SEC’s general standard. The Australian and SEC requirements are a cornerstone of their respective auditor independence regulatory frameworks.

2.11 Canada, the EU and the UK have not adopted a general standard of auditor independence along the lines of the Australian and SEC requirements. The review notes though that the UK’s APB Ethical Standard 1, in discussing the concept of ‘independence’, adopts language which limits the subjective application of the standard and, given that the standards are mandatory, looks very much like a general standard of independence.

Page 9

Australian auditor independence requirements

Key finding 3 Canada, the European Union and the UK have not adopted a general standard of auditor independence along the lines of the general requirement for auditor independence in the Corporations Act or the general standard in the SEC Rule in the US.

The Australian and SEC requirements are a cornerstone of their respective auditor independence regulatory frameworks. The Australian general requirement on auditor independence applies to all circumstances relating to an audit and is in addition to, and does not derogate from any other obligation imposed by the Corporations Act or a code of professional conduct.

PART 5: SPECIFIC AUDITOR INDEPENDENCE REQUIREMENTS APPLYING TO EMPLOYMENT, FINANCIAL AND BUSINESS RELATIONSHIPS

Employment and financial relationships

2.12 The existence of employment and financial relationships between an audit firm and an audit client can give the impression that an auditor is not independent of the client, irrespective of the actual situation. Where such relationships exist, there may be a range of circumstances which make it difficult for the auditor to adopt an unbiased approach to the audit engagement, with the result that the audit client could receive a more favourable audit report than the facts or circumstances justify.

2.13 The CLERP 9 Act substantially implemented the recommendations of the Ramsay report which sought to achieve ‘best practice’ restrictions on employment and financial relationships building on the existing requirements in the Corporations Act and drawing on recent overseas developments, particularly under the IFAC Code and the SEC Rules on auditor independence.

2.14 When comparing the Australian requirements with the overseas specific requirements, it is important to understand how the criminal liability rules in Australia operate in relation to audit firms where the partners of an audit firm can be made vicariously liable for a breach of the requirements. The review explains how these provisions operate and the way in which they have been designed to encourage a ‘culture of compliance’ within audit firms.

2.15 For purposes of its comparative analysis, Treasury adopted the methodology of comparing each prohibited employment and financial relationship in the Corporations Act with the corresponding restrictions in the relevant jurisdictions. We considered that this form of analysis was the only way we would be able to draw informed

Page 10

Part 2: Executive Summary

conclusions as to whether there is substantial equivalence between the Australian requirements and ‘best practice’ standards adopted internationally.

2.16 Our analysis is contained in the tables set out in Part 5 of the Review. Notwithstanding the fact that differences in terminology used in the various legislative and professional requirements make precise comparisons of the Australian and overseas requirements difficult, we believe that the analysis indicates clearly that there is a substantial underlying equivalence between the Australian requirements and those in the relevant overseas jurisdictions.

Key finding 4 The detailed comparative analysis undertaken by Treasury in relation to the specific employment and financial relationship restrictions in each jurisdiction, clearly indicates that there is substantial underlying equivalence between the Australian requirements and those in the relevant overseas jurisdictions.

2.17 We noted though that in relation to some of the employment and financial restrictions, the SEC has introduced a ‘covered person’ concept rather than applying an ‘all partner approach’. In commenting on the adoption of its final auditor independence rules in 2001, the SEC said that ‘we believe that independence will be protected and the rules will be more workable by focussing on those persons who can influence the audit, instead of all partners in an accounting firm’. Canada has also adopted a ‘restricted person’ regime, rather than an ‘all partner’ approach, in relation to financial relationships. The restrictions in the EU Recommendation apply to the statutory auditor and those persons in the firm in a position to influence the outcome of the audit, rather than an ‘all partner’ approach. The ‘covered person’ concept has not been applied under the auditor independence requirements in Australia and the UK. Australia and the UK have adopted an ‘all partner’ approach in relation to restrictions on financial investments but not in relation to loans and guarantees where a narrower range of prohibited relationships apply.

Page 11

Australian auditor independence requirements

Key finding 5 The review noted that the SEC auditor independence rules in the US have applied a ‘covered person’ test in relation to a number of the specific employment and financial relationship restrictions in place of an ‘all partner approach’. Canada has adopted an ‘all partner’ approach in relation to dual employment restrictions but has adopted a ‘restricted person’ regime in relation to financial relationship restrictions. The employment and financial relationship restrictions in the EU Recommendation apply to the statutory auditor and those persons in the firm in a position to influence the outcome of the audit, rather than an ‘all partner’ approach. The ‘covered person’ concept has not been adopted under the auditor independence requirements in Australia and the UK. Australia and the UK have adopted an ‘all partner’ approach in relation to dual employment restrictions and in relation to restrictions on financial investments. However, the restrictions in Australia and the UK relating to loans and guarantees have not adopted an ‘all partner’ approach.

Business relationships

2.18 The Government accepted the recommendation of the Ramsay report that detailed rules on close business relationships between an audit firm and the audit client be dealt with in the ethical rules of the professional accounting bodies. The general requirement on auditor independence in the Corporations Act also applies to business relationships between an auditor and audit client. The Australian Code of Ethics for Professional Accountants APES 110 (APES 110) was issued in June 2006 by the Accounting Professional and Ethical Standards Board. APES 110 reflects the latest revisions in the IFAC Code.

2.19 The requirements in Australia, Canada and the EU focus on the need for the financial interest created by the business relationship being immaterial and the relationship itself being insignificant to the audit firm and the audit client.

2.20 The requirements in the UK and the US will only permit purchase of goods and services in the ordinary course of business, in the case of the UK, and in the case of the US, the provision of professional services to the audit client or where the audit firm is a consumer in the ordinary course of business.

Page 12

Part 2: Executive Summary

Key finding 6 In Australia, detailed rules on close business relationships are contained in the professional conduct rules, although the general requirement on auditor independence in the Corporations Act would still apply to business relationships between the auditor and audit client. The Australian Code of Ethics for Professional Accountants APES 110 imposes restrictions on close business relationships between the auditor and audit client and requires that the financial interest is immaterial and clearly insignificant to the firm and the audit client. Close business relationships are also regulated under the auditor independence requirements applying in the other jurisdictions. The UK and US requirements will only permit the purchase of goods and services in the ordinary course of business, in the case of the UK, and in relation to the US, professional services to the audit client or where the audit firm is a consumer in the ordinary course of business.

PART 6: PROVISION OF NON-AUDIT SERVICES

2.21 The Australian APES 110 has noted that audit firms have traditionally provided audit clients a range of non-audit services that are consistent with the firm’s skills and expertise. The fundamental concern raised by those who oppose the provision on non-audit services is that when an audit firm provides non-audit services to a client it is serving two different sets of clients: management in the case of non-audit services and the audit committee, the shareholders and all those who rely on the audited financial statement in the case of the audit. In serving these different clients, it is argued that the audit firm is subject to conflicts of interest.

2.22 The fundamental policy issue confronting policy makers is whether to ban some or all non-audit services or whether to allow non-audit services provided auditors are made aware of the potential threats to their independence and require safeguards to be put in place in order to minimise these threats to acceptable levels. When a threat cannot be reduced to an acceptable level, the auditor should either resign from the audit or refrain from providing the non-audit service.

2.23 The Australian Government decided not to impose a legislative ban on non-audit services when the CLERP 9 Act reforms were introduced. The Ramsay report noted that it had not uncovered any evidence to suggest that there were systemic failures within the accounting profession in complying with the ethical rules for providing non-audit services to clients.

2.24 Canada, the EU, and the UK have adopted a similar approach to Australia. The US on the other hand, prohibits eight specific categories of non-audit services and requires that any other non-audit services must be pre-approved by the audit client’s audit committee.

Page 13

Australian auditor independence requirements

2.25 The review compares the specific non-audit services that are either banned in the US, or discussed in terms of threats to independence and the safeguards that need to be taken. The review found that the coverage of specific non-audit services in APES 110 is substantially similar to those identified in the other jurisdictions, except the EU which is not as comprehensive. We noted however that Canada, the UK and the US specifically address actuarial services which are not specifically covered in APES 110. The general requirement on auditor independence in the Corporations Act also applies to the provision of non-audit services by an auditor to an audit client.

Key finding 7 Australia has not imposed a legislative ban on non-audit services. Canada, the European Union and the United Kingdom have adopted a similar approach to Australia. In the US, the Sarbanes-Oxley Act prohibits eight specific categories of non-audit services and requires that any other non-audit services must be pre-approved by the audit client’s audit committee.

Key finding 8 The coverage of specific non-audit services in the Australian Code of Ethics for Professional Accountants APES 110 is substantially similar to those identified in the other jurisdictions, except the EU which is not as comprehensive. The review noted, however, that Canada, the UK and the US specifically address actuarial services which are not specifically covered in Australia’s APES 110. The general requirement on auditor independence in the Corporations Act also applies to the provision of non-audit services by an auditor to an audit client.

2.26 Tax services are not prohibited in any of the jurisdictions. We noted though that in the UK the potential threats that can arise from the provision of tax services are analysed in detail under an ethical standard (APB Ethical Standard 5). This compares with the position adopted under APES 110 which states that generally tax services do not create any auditor independence threats.

Key finding 9 Tax services are not prohibited in any of the jurisdictions, including the US. The Australian Code of Ethics for Professional Accountants APES 110 states that generally tax services do not create any auditor threats. This can be compared with the treatment of tax services in the UK under APB Ethical Standard 5 where the potential threats that can arise from the provision of tax services are analysed in detail.

2.27 IOSCO is currently undertaking a detailed survey of the regulation of non-audit services in various jurisdictions. IOSCO is aware that jurisdictions have differing views as to which non-audit services might give rise to an actual or perceived conflict of interest. Differing interpretations can raise important issues for corporations and audit firms that operate on a global basis. ASIC considers that in light of these cross border

Page 14

Part 2: Executive Summary

issues, the IOSCO study of the regulation on non-audit services will be useful to IOSCO members in determining how best to deal with independence requirements, not only in their local jurisdictions, but also in a global context.

Key finding 10 IOSCO is currently undertaking a detailed survey of the regulation of non-audit services in various jurisdictions. IOSCO is aware that jurisdictions have differing views as to which non-audit services might give rise to an actual or perceived conflict of interest. Where different interpretations occur, this raises important issues for corporations and audit firms that operate on a global basis. ASIC considers that the IOSCO study will be useful to IOSCO members in determining how best to deal with auditor independence requirements in relation to non-audit services, not only in their local jurisdictions, but also in a global context.

PART 7: EMPLOYMENT RESTRICTIONS APPLYING TO FORMER AUDIT PARTNERS AND SENIOR AUDIT PERSONNEL

‘Cooling-off periods’

2.28 Objectivity and independence may be threatened where an officer or employee of an audit client who is in a position to exert direct and significant influence over the preparation of the financial statements has recently been a partner in the audit firm or a member of the audit engagement team.

2.29 Australia and each of the other jurisdictions have addressed these concerns by requiring a ‘cooling-off’ period between the partner’s or professional employee’s departure from the firm and his or her joining the audit client. There are however, subtle differences between the requirements in each jurisdiction. These differences are analysed in the review.

2.30 The two year ‘cooling-off’ period in Australia is similar to the periods in the other jurisdictions although in Canada, the period is only one year. The SOX Act also refers to one year but the way the provision is drafted, the period in fact is longer than one year but not more than two years.

2.31 The obligation under the Australian restriction is placed on the former partner while in other jurisdictions the burden falls on the audit firm as it is not regarded as being independent if the ‘cooling-off’ restriction is breached. The Australian position is explained by the fact that breach of the restriction is a criminal offence and it would not be appropriate to prosecute the firm after the partner has resigned from the firm.

Page 15

Australian auditor independence requirements

Key finding 11 The obligation under the Australian restriction is imposed on the former partner because it would be inappropriate to impose a criminal sanction on the audit firm after a former partner has resigned from the firm and is beyond the control of the firm. The restriction in the relevant overseas jurisdictions falls on the audit firm because the firm is not regarded as being independent of the audit client if the ‘cooling-off’ restriction is breached.

2.32 The Australian two year ‘cooling-off’ period applies to a former partner who was a member of the audit team, regardless as to when the partner participated as a member of the audit team. Canada, the UK and the US place a limit on the time of participation in an audit prior to the partner’s date of departure.

2.33 However, the scope of the Australian requirement only applies to a partner or director of an authorised audit company who has been a professional member of the audit team. The UK requirement extends beyond membership of the audit team to other partners in the ‘chain of command’. The US requirement is even more extensive and applies to any person who participated ‘in any capacity’ in the audit.

Key finding 12 The Australian ‘cooling-off’ period restriction applies to a former partner of the firm who was a member of the audit team, regardless as to how far back the partner’s participation on the audit team took place. Canada, the UK and the US place a limit on the time of participation in an audit prior to the partner’s date of departure from the firm.

Key finding 13 In contrast to key finding 12, the scope of the Australian ‘cooling-off’ period only applies to a partner or director of an authorised audit company who has been a professional member of the audit team. The UK requirement includes other partners in the ‘chain of command’. The US requirement is even more extensive and applies to any person who participated ‘in any capacity’ in the audit.

Multiple former partner of audit firm/audit company director restriction

2.34 Section 324CK of the Corporations Act implements a recommendation of the HIH Royal Commission that a prohibition be introduced preventing more than one former partner of an audit firm, or director of an audit company, at any time becoming an officer of the audit client.

Page 16

Part 2: Executive Summary

2.35 The restriction has been criticised by the accounting profession because of its potential negative impact on the employment market and recruiting practices of audit firms. The report of the Taskforce on Reducing Regulatory Burdens on Business has recommended that the Australian Government should review the multiple former audit partner restriction.

2.36 Treasury is unaware of any equivalent requirement in the overseas jurisdictions covered in the comparative review. However, we note that the HIH Royal Commission Report linked the recommendation to the fact that there were three former partners of Andersen appointed to the board of HIH.

2.37 The Government has announced that it will review the multiple former audit partner restriction by the end of 2006.2

Key finding 14 The report of the Taskforce on Reducing Regulatory Burdens on Business has recommended that the Australian Government should review the multiple audit firm partner restriction. While Treasury is unaware of an equivalent restriction in any of the relevant overseas jurisdictions, the existing restriction implements a recommendation of the HIH Royal Commission which concluded that the cumulative effect of three former partners of HIH’s auditor, Andersen, being appointed to the board of HIH, resulted in the perception that Andersen was not independent of HIH.

The Australian Government has announced that it will review the multiple former audit firm partner restriction by the end of 2006.

PART 8: AUDITOR ROTATION

2.38 The IFAC Code notes that using the same senior audit personnel on an audit engagement over a long period of time may create a familiarity threat. One of the safeguards that the IFAC Code recommends to address this threat is to rotate senior audit personnel off the audit team.

2.39 The review discusses the auditor rotation requirements in Australia and the other relevant overseas jurisdictions. The approach taken in each jurisdiction can be summarised as follows:

• All the jurisdictions covered in the review applied the rotation requirements to the lead engagement auditor and the review auditor.

2 Australian Government’s Response to the Rethinking Regulation Task Force report: 15 August 2006.

Page 17

Australian auditor independence requirements

• The length of time an auditor is allowed to remain on an audit engagement before being required to rotate is addressed in the following way:

– In Australia, the basic rule is that the lead and review auditors must rotate after five successive years and also may not audit a particular audit client for more than five out of seven successive financial years.

– Canada, the UK and the SEC Rules require rotation after five successive years.

– The EU Recommendation requires rotation after seven years.

• The following ‘time-out’ periods apply before a ‘rotated’ auditor is allowed to resume involvement with the same audit client:

– Australia and the EU have adopted a two year time-out period.

– Canada, the UK and the SEC have adopted a five year time-out period.

• The requirements in Australia, Canada, the UK and the SEC only apply to listed companies (‘reporting issuers’ in Canada and ‘issuers’ under the SEC Rules).

• Under the SEC Rules, audit firms with fewer than five audit clients who are ‘issuers’ for purpose of the securities laws and which have less than ten partners, are exempt from the rotation requirements provided the PCAOB conducts a review at least once every three years of each of the firm’s audit client engagements.

Key finding 15 While Australia and the relevant overseas jurisdictions have all adopted auditor rotation requirements, there are subtle differences between the requirements adopted in each jurisdiction. None of the jurisdictions require audit firm rotation.

The auditor rotation requirements in each jurisdiction extend to the lead engagement auditor and the review auditor.

Australia, Canada, the UK and the SEC Rules in the US, require rotation after five successive years. Australia has an additional requirement that a lead or review auditor may not audit a particular audit client for more than five out of seven successive years. The EU requires rotation after seven years.

Australia and the EU have adopted a two year time-out period before a ‘rotated’ auditor is allowed to resume involvement with the same audit client. Canada, the UK and the SEC have adopted a five year time-out period.

Only the SEC Rules provide an exemption from the rotation requirements for smaller audit firms (fewer than five audit clients and less than ten audit partners) provided the PCAOB conducts a review at least once every three years of each of the firm’s audit client engagements.

Page 18

Part 2: Executive Summary

CONCLUSION

2.40 Audited financial statements play a key role in relation to the efficiency of capital markets and the independent auditor constitutes the principal external check on the integrity of financial statements. Australia and all the relevant overseas jurisdictions recognise that auditor independence is fundamental to the credibility and reliability of auditor’s reports.

2.41 Our overall conclusion is that the comparative review that Treasury has undertaken establishes conclusively that, notwithstanding differences in terminology, institutional arrangements and legal frameworks, there is a substantial underlying equivalence between the Australian requirements and ‘best practice’ standards adopted internationally. The key findings do, however, identify some important areas where the approach by particular jurisdictions on a specific issue has diverged.

Conclusion Treasury’s overall conclusion is that notwithstanding differences in terminology, institutional arrangements and legal frameworks, there is a substantial underlying equivalence between the Australian auditor independence requirements and ‘best practice’ standards adopted internationally.

2.42 The key findings of the review are detailed below.

Key finding 1 While many of the core elements of the auditor independence requirements, including their underlying policy objectives, in each jurisdiction are similar, the review has found substantial differences in the institutional arrangements and the legal framework applying to audit regulation in each jurisdiction. These differences can be explained by the unique combination of circumstances applying in each jurisdiction, including constitutional arrangements, history relating to the regulation of corporations and financial services and system of government.

Key finding 2 A distinguishing feature of the Australian auditor independence requirements compared with the overseas jurisdictions covered by the review, is that the detailed independence requirements have been enacted by the Federal Parliament in the Corporations Act to provide a comprehensive legislative code.

Page 19

Australian auditor independence requirements

Key finding 3 Canada, the European Union and the UK have not adopted a general standard of auditor independence along the lines of the general requirement for auditor independence in the Corporations Act or the general standard in the SEC Rule in the US.

The Australian and SEC requirements are a cornerstone of their respective auditor independence regulatory frameworks. The Australian general requirement on auditor independence applies to all circumstances relating to an audit and is in addition to, and does not derogate from any other obligation imposed by the Corporations Act or a code of professional conduct.

Key finding 4 The detailed comparative analysis undertaken by Treasury in relation to the specific employment and financial relationship restrictions in each jurisdiction clearly indicated that there is substantial underlying equivalence between the Australian requirements and those in the relevant overseas jurisdictions.

Key finding 5 The review noted that the SEC auditor independence rules in the US have applied a ‘covered person’ test in relation to a number of the specific employment and financial relationship restrictions in place of an ‘all partner approach’. Canada has adopted an ‘all partner’ approach in relation to dual employment restrictions but has adopted a ‘restricted person’ regime in relation to financial relationship restrictions. The employment and financial relationship restrictions in the EU Recommendation apply to the statutory auditor and those persons in the firm in a position to influence the outcome of the audit, rather than an ‘all partner’ approach. The ‘covered person’ concept has not been adopted under the auditor independence requirements in Australia and the UK. Australia and the UK have adopted an ‘all partner’ approach in relation to dual employment restrictions and in relation to restrictions on financial investments. However, the restrictions in Australia and the UK relating to loans and guarantees have not adopted an ‘all partner’ approach.

Page 20

Part 2: Executive Summary

Key finding 6 In Australia, detailed rules on close business relationships are contained in the professional conduct rules, although the general requirement on auditor independence in the Corporations Act would still apply to business relationships between the auditor and audit client. The Australian Code of Ethics for Professional Accountants APES 110 imposes restrictions on close business relationships between the auditor and audit client and requires that the financial interest is immaterial and clearly insignificant to the firm and the audit client. Close business relationships are also regulated under the auditor independence requirements applying in the other jurisdictions. The UK and US requirements will only permit the purchase of goods and services in the ordinary course of business, in the case of the UK, and in relation to the US, professional services to the audit client or where the audit firm is a consumer in the ordinary course of business.

Key finding 7 Australia has not imposed a legislative ban on non-audit services. Canada, the European Union and the United Kingdom have adopted a similar approach to Australia. In the US, the Sarbanes-Oxley Act prohibits eight specific categories of non-audit services and requires that any other non-audit services must be pre-approved by the audit client’s audit committee.

Key finding 8 The coverage of specific non-audit services in the Australian Code of Ethics for Professional Accountants APES 110 is substantially similar to those identified in the other jurisdictions, except the EU which is not as comprehensive. The review noted, however, that Canada, the UK and the US specifically address actuarial services which are not specifically covered in Australia’s APES 110. The general requirement on auditor independence in the Corporations Act also applies to the provision of non-audit services by an auditor to an audit client.

Key finding 9 Tax services are not prohibited in any of the jurisdictions, including the US. The Australian Code of Ethics for Professional Accountants APES 110 states that generally tax services do not create any auditor threats. This can be compared with the treatment of tax services in the UK under APB Ethical Standard 5 where the potential threats that can arise from the provision of tax services are analysed in detail.

Page 21

Australian auditor independence requirements

Key finding 10 IOSCO is currently undertaking a detailed survey of the regulation of non-audit services in various jurisdictions. IOSCO is aware that jurisdictions have differing views as to which non-audit services might give rise to an actual or perceived conflict of interest. Where different interpretations occur, this raises important issues for corporations and audit firms that operate on a global basis. ASIC considers that the IOSCO study will be useful to IOSCO members in determining how best to deal with auditor independence requirements in relation to non-audit services, not only in their local jurisdictions, but also in a global context.

Key finding 11 The obligation under the Australian restriction is imposed on the former partner because it would be inappropriate to impose a criminal sanction on the audit firm after a former partner has resigned from the firm and is beyond the control of the firm. The restriction in the relevant overseas jurisdictions falls on the audit firm because the firm is not regarded as being independent of the audit client if the ‘cooling-off’ restriction is breached.

Key finding 12 The Australian ‘cooling-off’ period restriction applies to a former partner of the firm who was a member of the audit team, regardless as to how far back the partner’s participation on the audit team took place. Canada, the UK and the US place a limit on the time of participation in an audit prior to the partner’s date of departure from the firm.

Key finding 13 In contrast to key finding 12, the scope of the Australian ‘cooling-off’ period only applies to a partner or director of an authorised audit company who has been a professional member of the audit team. The UK requirement includes other partner’s in the ‘chain of command’. The US requirement is even more extensive and applies to any person who participated ‘in any capacity’ in the audit.

Key finding 14 The report of the Taskforce on Reducing Regulatory Burdens on Business has recommended that the Australian Government should review the multiple audit firm partner restriction. While Treasury is unaware of an equivalent restriction in any of the relevant overseas jurisdictions, the existing restriction implements a recommendation of the HIH Royal Commission which concluded that the cumulative effect of three former partners of HIH’s auditor, Andersen, being appointed to the board of HIH, resulted in the perception that Andersen was not independent of HIH.

The Australian Government has announced that it will review the multiple former audit firm partner restriction by the end of 2006.

Page 22

Part 2: Executive Summary

Key finding 15 While Australia and the relevant overseas jurisdictions have all adopted auditor rotation requirements, there are subtle differences between the requirements adopted in each jurisdiction. None of the jurisdictions require audit firm rotation.

The auditor rotation requirements in each jurisdiction extend to the lead engagement auditor and the review auditor.

Australia, Canada, the UK and the SEC Rules in the US, require rotation after five successive years. Australia has an additional requirement that a lead or review auditor may not audit a particular audit client for more than five out of seven successive years. The EU requires rotation after seven years.

Australia and the EU have adopted a two year time-out period before a ‘rotated’ auditor is allowed to resume involvement with the same audit client. Canada, the UK and the SEC have adopted a five year time-out period.

Only the SEC Rules provide an exemption from the rotation requirements for smaller audit firms (fewer than five audit clients and less than ten audit partners) provided the PCAOB conducts a review at least once every three years of each of the firm’s audit client engagements.

Conclusion Treasury’s overall conclusion is that notwithstanding differences in terminology, institutional arrangements and legal frameworks, there is a substantial underlying equivalence between the Australian auditor independence requirements and ‘best practice’ standards adopted internationally.

Page 23

Part 3: Auditor independence: Policy goals, institutional arrangements and legal framework

INTRODUCTION

3.1 A sound knowledge of the auditor independence requirements applying in each jurisdiction is not possible without an understanding of the institutional arrangements and the legal framework within which those requirements operate.

3.2 While many of the core elements of the auditor independence requirements in each jurisdiction are similar, there are substantial differences between the jurisdictions in terms of the legal framework and institutional arrangements that have been adopted.

LOSS OF CREDIBILITY IN FINANCIAL REPORTING HAS BEEN THE MAJOR POLICY DRIVER OF REFORMS

3.3 Concerns about the credibility of financial reporting and the audit function surfaced during the 1997 Asian financial crisis when major companies in apparent sound financial health dramatically collapsed or went into deep financial distress. This was perceived though, as largely an Asian phenomenon. It was not until the jolt of the collapse of the US Corporation, Enron in late 2001, and subsequent failures of other high profile companies, that a worldwide debate on the crisis affecting financial reporting and the audit function was triggered, and led to the introduction of substantial reforms in relation to financial disclosure and the regulation of auditors.

INTERNATIONAL EFFORTS TO ADDRESS CRISIS

3.4 While the regulatory framework in relation to corporate disclosure and the effectiveness of the audit function operates primarily at the national level, it is important to acknowledge the multilateral action that has been initiated at the international level.

3.5 There is a current trend towards greater consistency in global regulatory standards as evidenced by work undertaken, for example, by the International Organisation of Securities Commissions (IOSCO), the International Monetary Fund and the World Bank.

Page 25

Australian auditor independence requirements

3.6 IOSCO has released a range of best-practice standards and principles which provide an international benchmark for the development of securities and corporate regulatory standards. IOSCO’s Principles of Auditor Independence and the Role of Corporate Governance in Monitoring an Auditor’s Independence3 notes that ‘the importance of auditor independence standards that are reasonable and enforceable has been underlined by several significant corporate failures in which questions have been raised about the quality of financial reporting and, in particular, the independence of the auditor’.

3.7 The International Federation of Accountants4 (IFAC) represents 163 member organisations in 120 countries. IFAC is widely recognised as the voice of the international accounting profession. An important part of IFAC’s mission is to develop and promote adherence to high quality professional standards in the areas of auditing, education, ethics and public sector financial reporting. The following IFAC initiatives are worth noting in the context of the international measures that have been taken to enhance auditor independence and audit quality standards:

• IFAC’s International Ethics Standards Board for Accountants updated the Code of Ethics for Professional Accountants (the IFAC Code) in June 2005. The IFAC Code emphasises five fundamental values which are integrity, objectivity, professional competence, due care, confidentiality and professional behaviour. The IFAC Code contains a conceptual framework which identifies threats to these values and the safeguards that could be taken to address these threats. This conceptual framework forms the basis of the auditor independence rules adopted by each of the professional body members of IFAC. All IFAC member organisations must ensure that they adopt auditor independence rules that are no less stringent than those laid down in the IFAC Code. For purposes of Treasury’s comparative review, the standards set by the IFAC Code are particularly important in those jurisdictions where the auditor independence rules of recognised professional bodies constitute the primary auditor independence requirements for the particular jurisdiction.

• IFAC established the Public Interest Oversight Board5 (PIOB) in February 2005, to oversee IFAC’s standard-setting activities. The establishment of the PIOB was the result of a collaborative effort by the international financial regulatory community (IOSCO, the Basel Committee on Banking Supervision, the International Association of Insurance Supervisors, the World Bank and the Financial Stability Forum) working with IFAC, to ensure that auditing and assurance, ethics and educational standards for the accounting profession are set in a transparent manner that reflects the public interest. It was mutually recognised that high quality, transparent standard-setting processes with public and regulatory input, together with regulatory monitoring and public interest oversight, are necessary to enhance the quality of external audits of entities.

3 A Statement of the Technical Committee of IOSCO: October 2002: www.iosco.org. 4 Background information on IFAC is available on its website www.ifac.org. 5 Further background information on the PIOB is available on its website: www.ipiob.org.

Page 26

Part 3: Auditor independence: Policy goals, institutional arrangements and legal framework

• Another noteworthy initiative by IFAC was to establish a Task Force on Rebuilding Public Confidence in Financial Reporting.6 The Task Force was commissioned to provide an international perspective on the causes of the loss of credibility in financial reporting and corporate disclosure and to recommend causes of action to restore credibility. The Task Force reported in July 2003. The key recommendations of the Task Force were built on three basic assumptions:

– the financial credibility of financial reporting is both a national issue in each country and an international issue, with action required at both levels;

– to improve the credibility of financial reporting, action will be necessary at all points along the information supply chain that delivers financial reporting to the market. In this context, the Task Force made a number of recommendations relating to audit independence and audit effectiveness through greater attention being given to audit control processes; and

– integrity, both individual and institutional, is essential for effective remedial action. The Task Force said that failure to recognise the primacy of integrity was a major contributor to the financial scandals of recent years.

3.8 The worldwide reform measures introduced to strengthen auditor independence rules and audit quality processes must also be considered in the context of the institutional reforms that governments have made at the national level to enhance auditor independence and audit quality.

• The PIOB explained these institutional developments in its First Public Report issued on 16 May 2006:

National audit regulators and oversight authorities have become a very important institutional feature of the regulatory landscape. This has been the result of many national responses to the same proximate causes that spearheaded the creation of the international PIOB: corporate scandals and audit failures. In some cases these new national authorities wield standard-setting powers while in others they do not. Such authorities constitute a new reality in the world architecture of regulation.

• IOSCO has noted that there is a growing consensus that ‘the adequacy and effectiveness of audit firms’ internal systems and processes relating to independence must be assessed and evaluated by an external oversight system’.7

6 The report of the Task Force was published by IFAC in 2003 and is available on the IFAC website, op. cit. 4. Professor Ian Ramsay was a member of the Task Force.

7 op. cit. 3 at page 4.

Page 27

Australian auditor independence requirements

AUSTRALIA

Legislative requirements

3.9 The CLERP 9 Act established a comprehensive statutory regime on auditor independence8, substantially implementing the recommendations of the Ramsay report and some of the relevant recommendations of the HIH Royal Commission.9

3.10 The Government decided to commission the review by Professor Ramsay in 2001 because there was a generally accepted view that the Australian auditor independence requirements could no longer be regarded as best practice, having fallen behind equivalent requirements in the US and Europe. Auditor independence issues had also been raised in the publicity relating to a number of corporate failures during the first half of 2001. Shortly before the Ramsay report was released in October 2001, HIH Insurance Ltd (HIH) was placed into final liquidation on 27 August 2001. The collapse of HIH represents the largest corporate failure experienced in Australia.

3.11 While the Ramsay report was adopted by the Government as the basic blueprint for the auditor independence reforms in the CLERP 9 Act, the development of these reforms was also informed by overseas developments from late 2001 following the collapse of Enron and other high profile companies in the US and Europe and the detailed recommendations in relation to the audit function contained in the report of the HIH Royal Commission which was completed in April 2003.

3.12 A salient feature of the Ramsay report was that the great majority of the detailed auditor independence requirements which it proposed were recommended to be included in the Corporations Act. Similarly, most of the recommendations that the HIH Royal Commission made in relation to auditor independence, involved the making of amendments to the Corporations Act. In other words, both the Ramsay report and the HIH Royal Commission recommended that most of the enhanced auditor independence rules should have the force of law within the framework of the Corporations Act.

8 Most of the auditor independence requirements are contained in Division 3 of Part 2M.4 of the Corporations Act.

9 The HIH Royal Commission: The failure of HIH Insurance: Volume 1: A corporate collapse and its lessons. Published by the Australian Government in April 2003: www.hihroyalcom.gov.au.

Page 28

Part 3: Auditor independence: Policy goals, institutional arrangements and legal framework

3.13 The inclusion of the auditor independence rules in the Corporations Act, has resulted in the Parliament enacting the detailed requirements. This can be contrasted with the position in the relevant overseas jurisdictions:

• the federal auditor independence regime in the US, which also has a statutory basis, relies primarily on the detailed rules made by the SEC10 and the rules and standards made by the PCAOB11 (the SOX Act contains prescriptive requirements in relation to audit committees, auditor rotation and non-audit services, but even in these cases, they require supporting rules being made by the SEC);

• in Canada, the detailed auditor independence requirements rely primarily on the rules in the professional codes of ethics of the provincial Institutes of Chartered Accountants which have adopted the IFAC conceptual framework approach;

• in the UK, the recognised professional accounting bodies have been required to adopt, for purposes of the auditor independence requirements in their respective codes of ethics, the ethical standards issued by the Auditing Practices Board12 (APB) (one of the UK Financial Reporting Council’s (FRCUK) operating bodies); and

• the EU has adopted in its Directive and Council Recommendation on the independence of the statutory auditor, a principles-based approach within a conceptual framework similar to the IFAC approach.

3.14 Another consequence of including the detailed auditor independence requirements in the Corporations Act, is that, in framing each auditor independence requirement, it is necessary to determine the persons who should be made liable in the event of a contravention of a particular requirement. As the liability rules under the criminal law apply differently depending on whether the auditor is an individual auditor (sole proprietor), a firm or an authorised audit company, the auditor independence regime in the Corporations Act deals with each of these forms of audit practice separately, even though the underlying auditor independence concept is the same.

• As an example, we explain how the liability rules operate in relation to the specific employment and financial relationship restrictions in Part 5 of the review because an understanding of the liability rules applicable to the specific auditor independence requirements is essential to a proper understanding of how the auditor independence obligations operate from a compliance perspective.

• To facilitate our analysis of the detailed auditor independence requirements in the comparative review, we focus primarily on the rules applicable in Australia to an

10 Information on the SEC’s functions and role are available on the SEC website www.sec.gov. 11 Information about the PCAOB’s functions and role are available on the PCAOB website

www.pcaobus.org. 12 The APB’s Ethical Standards are available on the APB website www.org.uk/apb/.

Page 29

Australian auditor independence requirements

audit firm and only mention the application of a particular rule to an individual auditor or an authorised audit company where this may warrant some special consideration.

Rules of professional conduct

3.15 The Ramsay report described the pre-CLERP 9 Act regulatory environment for the independence of auditors as co-regulatory. The Ramsay report recognised that prior to the CLERP 9 reforms, the major regulatory role was played by the professional accounting bodies through their professional requirements and the code of ethics.

3.16 While the Ramsay report recommended the substantial strengthening of the auditor independence requirements in the Corporations Act, one of the key objectives contained in the report was to continue the co-regulatory environment.