australia future oil and gas text · lng – continues to grow source: ... india source:abare. lng...

TRANSCRIPT

Australia – The Future for Oil and Gas

Philip AikenPresident and CEO BHP Billiton Petroleum

Asia Pacific Petroleum ConferenceSingapore, September 2003

Australia – historical production

Production profiles of individual Australian fields and cumulative production forecast at 50 per cent probability derived from industry data.

Source: T Powell AGSO 2001, ABARE

200

150

100

50

01967 1973 1979 1985 1991 1997 2003 2009

MMbo

e

Gippsland Basin Fields

Barrow Island Fields

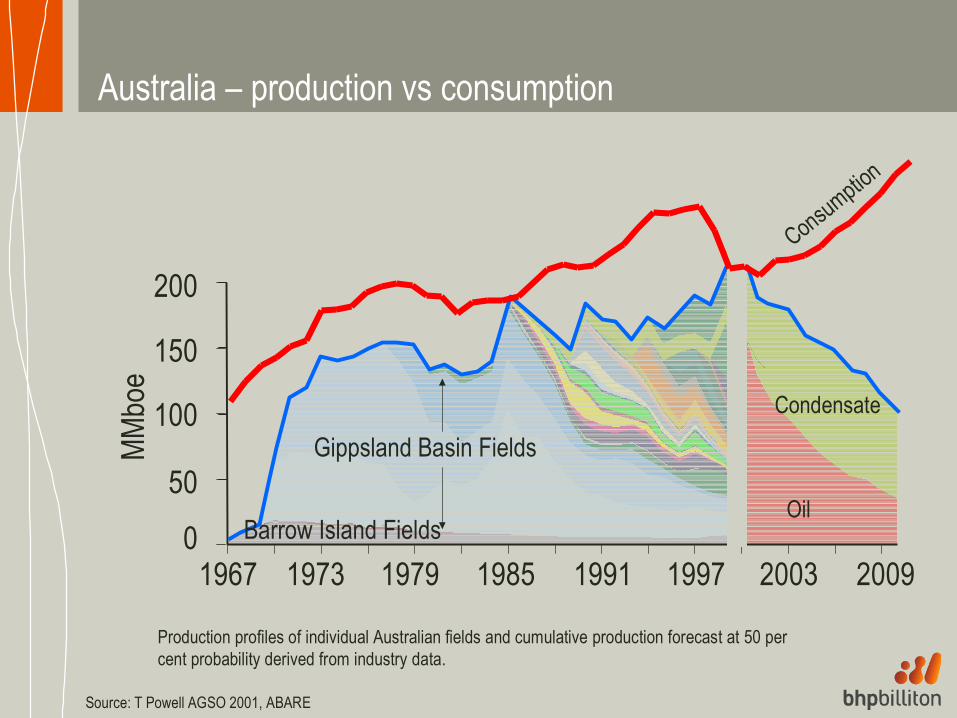

Australia – production vs consumption

Production profiles of individual Australian fields and cumulative production forecast at 50 per cent probability derived from industry data.

Source: T Powell AGSO 2001, ABARE

200

150

100

50

01967 1973 1979 1985 1991 1997 2003 2009

MMbo

e

Gippsland Basin Fields

Oil

Condensate

Consumption

Barrow Island Fields

Australia – some future liquids developmentsField name Product Liquids reserves Startup

Gorgon Gas/condensate 316 MMbbl 2009

Mutineer/Exeter Oil & Gas 120 MMbbl 2006

Stybarrow Oil & Gas Appraisal 2006

Enfield Oil & Gas 43 MMbbl 2005

Cliff Head Oil 25 MMbbl 2005

Yolla Gas/condensate 24.5 MMbbl 2004

Kipper Oil & Gas 13 MMbbl 2006

Egret Oil 11 MMbbl 2005

Source Wood Mackenzie, Nov 02.

Global Prospectivity – world undiscovered oil

Australia<1% of World Oil

Middle East & North Africa

Central & South America

Sub-Saharan Africa & Antartica

US

Europe

North America (excl U.S.)

Former Soviet Union

Asia Pacific (excl Australia)

Source: USGS

Global Materiality

0

1

2

3

4

0 0.5 1 1.5 2 2.5 3 3.5 4

Australia…not a place to rush to for oil

Fiscal Terms Increasingly Onerous

Incr

easin

g Po

litica

l Risk

.

Size of the button reflects average discovery size (MMboe, 1995-1999)

Australia

Russia

Nigeria

NorwayBrazil

UK

AngolaIndonesia

ColombiaTurkey

Algeria

Libya

China

Pakistan

US

Source: IHS Energy Group/Wood Mackenzie

0

2000

4000

6000

8000

10000

12000

1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000

Rese

rves

Add

ition

s ( M

Mboe

)

0

20

40

60

80

100

120

140

Num

ber o

f Well

s per

Yea

r

Australia – maturity in shallow waters

Oil

Oil & Condensate

Wells

Australia – activity in maturing areas

But these are unlikely to yield material quantities of hydrocarbons…

• Shallow water basins are well explored

• Infill exploration close to infrastructure will continue

– ‘new’ technology application (3D seismic)

– incremental reserves• New plays in existing shallow water

– eg. Enfield area in WA-271-P

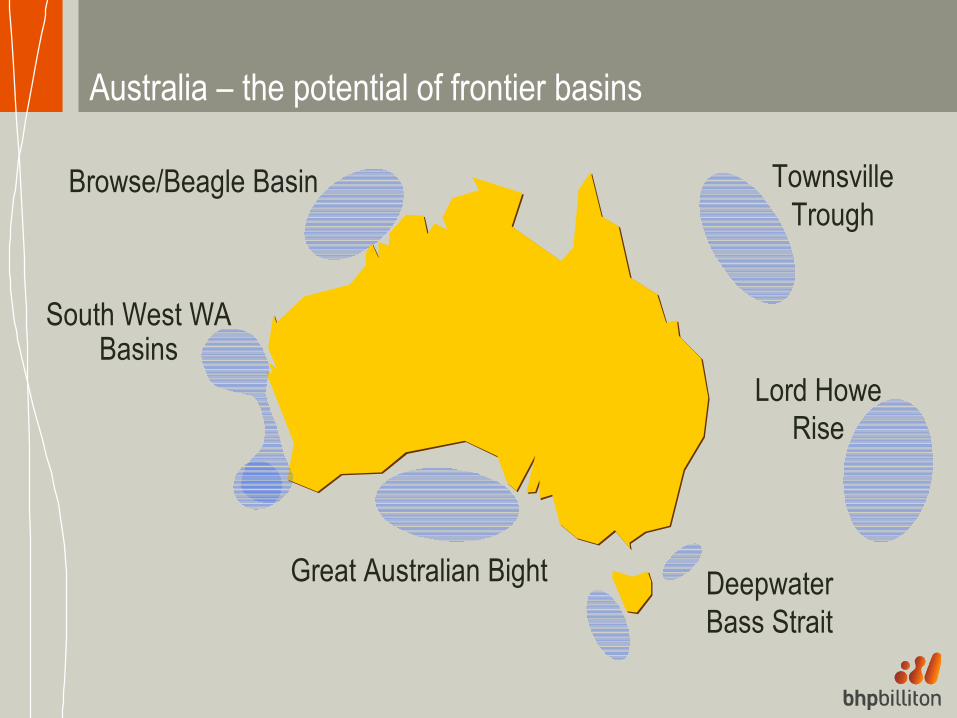

Browse/Beagle Basin

Great Australian Bight DeepwaterBass Strait

Lord Howe Rise

TownsvilleTrough

South West WA Basins

Australia – the potential of frontier basins

Responses:• Funding for technical data• Review of fiscal terms

Australia – oil Trends in industry:• Declining liquids production• Industry focus is diverging

- Minors focus on mature areas, generally smaller prizes- Majors focus on larger opportunities

• Australia regarded as maturing, and lacking prospectivity• Some untested frontier areas, mainly offshore

Australia – history of gas production

Domestic

Export

0

200

400

600

800

1000

1200

1400

1600

1973-74 1976-77 1979-80 1982-83 1985-86 1988-89 1991-92 1994-95 1997-98 2000-01

PJ

Includes: Gippsland, Cooper, Carnarvon, and other

Source: AGA

Gas consumption by State*

New South Wales

Victoria

Queensland Western Australia

South Australia

Northern Territory

0

200

400

600

800

1000

1200

1969 1973 1977 1981 1985 1989 1993 1997 2001

PJ

* Includes ethane, non-commercial natural gas and methane produced from other than natural gas fields. ** Includes ACT. Source: AGA

Australia – progressive inter-linking of markets

• 10 Years Ago – Bass Strait gas sold in

Victoria– Cooper Basin sold in NSW

& South Australia• Now

– Eastern Gas Pipeline– Tasmania supply - July

2002– South Australia pipeline to

be completed by 2004– Other interconnection

proposals– Timor Sea & PNG

discussion

Proposed Pipeline

SA

Vic

NSW

Qld

Bass Strait

Cooper Basin

Minerva

SeaGasPipeline

TGP

EGP

PNG

Timor Sea

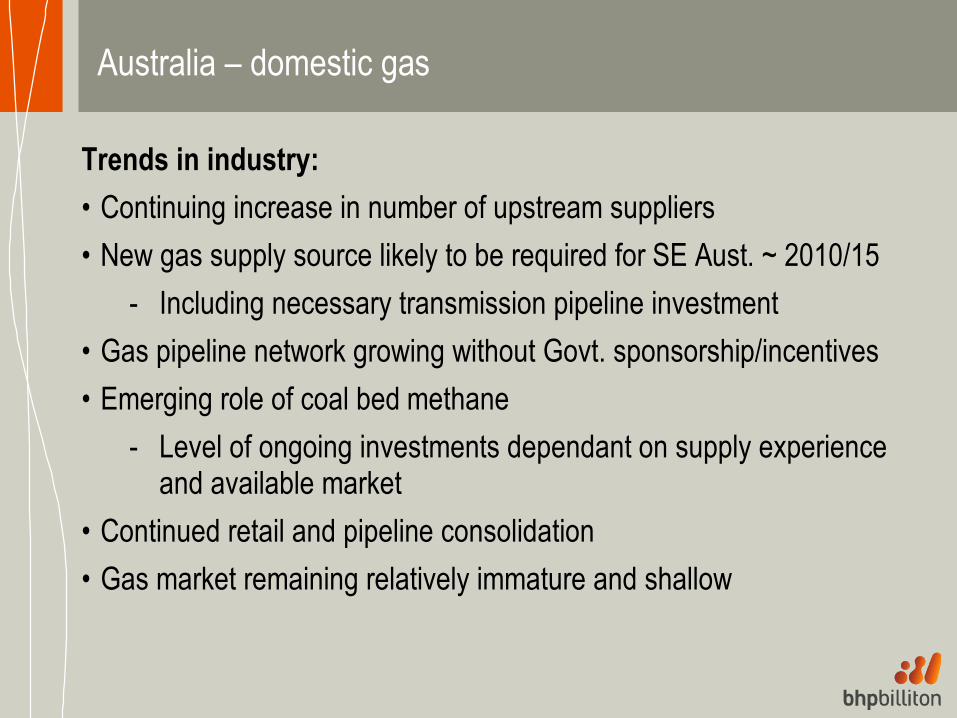

Australia – domestic gas

Trends in industry:• Continuing increase in number of upstream suppliers• New gas supply source likely to be required for SE Aust. ~ 2010/15

- Including necessary transmission pipeline investment• Gas pipeline network growing without Govt. sponsorship/incentives• Emerging role of coal bed methane

- Level of ongoing investments dependant on supply experience and available market

• Continued retail and pipeline consolidation• Gas market remaining relatively immature and shallow

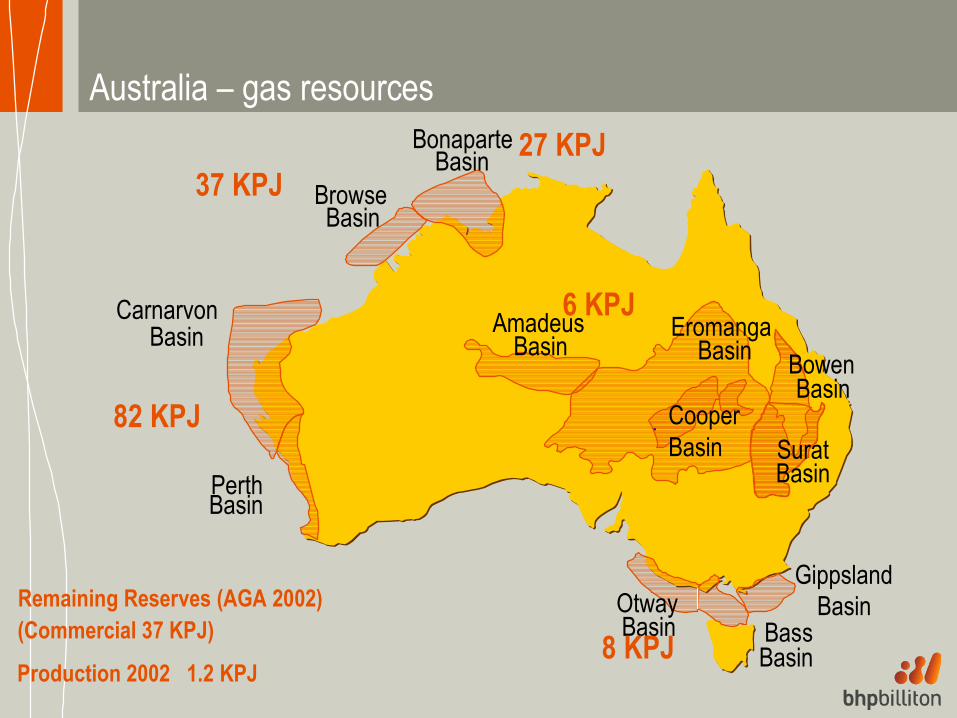

Australia – gas resources

CarnarvonBasin

PerthBasin

AmadeusBasin

BonaparteBasin

BrowseBasin

EromangaBasin

CooperBasin

GippslandBasinOtway

Basin

SuratBasin

BowenBasin

BassBasin

82 KPJ

6 KPJ

8 KPJRemaining Reserves (AGA 2002)(Commercial 37 KPJ)

Production 2002 1.2 KPJ

37 KPJ27 KPJ

Major Gas Trade MovementsTrade flows (billion cubic metres)

Source: BP Statistical Review of World Energy 2002

4.87 109.02

4.28 30.59

12.36

48.3

20.24.2

10.9338.31

75.65

4.6

2.62

6.75

20.073.63

5.3

6.896.67

8.3

15.273.04

2.6 8.25.36 10.05

22.743.7

USACanadaMexicoSth & C AmericaEuropeFormer Soviet UnionMiddle EastAfricaAsia PacificNatural GasLPG

Atlantic Basin

Asia-Pacific

0

50

100

150

200

250

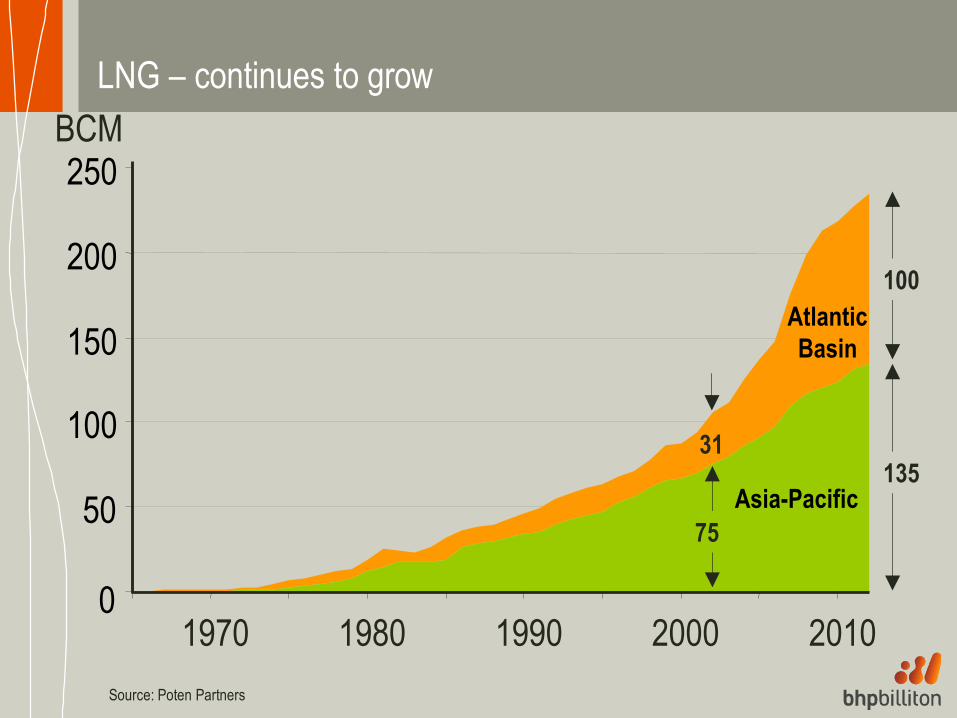

LNG – continues to grow

Source: Poten Partners

BCM

1970 1980 1990 2000 2010

135

75

100

31

LNG – world imports, 2002 (million tonnes)

5.2North & South

America

28.5

Europe

17.6

Korea 5.1Taiwan

53.1

Japan

Source: ABARE

LNG – supply to Asia, 2002 (million tonnes)

USA

1.2UAE

4.6

Qatar

11.2

Oman

4.8

Malaysia

14.9Brunei

6.6

Australia

7.3

Indonesia

25.1

Source: ABARE

LNG – Asian demand projections (million tonnes per annum)

2001

2010

2015

2015 high

55.262.8

6572.9

Japan

16.725 31.6 34.8

Korea

4.7 9.513.5 14.9

Taiwan

1018 20

China

5 7.5 12.5

IndiaSource:ABARE

LNG – capacity expansion plans

0

30

60

90

120

150

2003 2005 2007 2009 2011 2013 2015

Projected demand

Projected new capacity

Mt/pa

Existing capacity

Source: ABARE

LNG – market dynamics

Trends in industry:

• Fierce producer competition is lowering prices and margins

• Cost base of liquefaction is reducing

• LNG moving to “commodity status” in global market

• New LNG markets slow to materialise

• US emerging as a market

• Around 2010, expect another Australian producer of LNG other than NWS

Summary

• Australia will need to compete for exploration dollars

• Domestic gas market is immature but developing

• Australia positioned to supply growing LNG market