aurum webinar: indian defence offset program

TRANSCRIPT

IndianDefenseOffsetProgram

Challenges&Opportuni9es

December2016

1

• Thisdocument ispresentedsolelyforthe internaluseoftherecipienttowhomit ismarkedbyAurumEquityPartnersLLP(Aurum)andcannotbepublishedordisclosed inpartor inwholetoanythirdpartywithoutthespecificwri@en consent ofAurum. This document is incompletewithout reference to, and shouldbe viewedsolelyinconjuncEonwiththeverbalbriefing,asmayhavebeenprovided,byAurum.

• ThisdocumentshallbesubjecttothetermsofanyNonDisclosureAgreementthatmayhavebeenenteredinto

betweenAurumandtherecipienttowhomitismarked.

• InpreparingthisdocumentAurumhasrelieduponandassumed,withoutindependentverificaEon,theaccuracyandcompletenessofall informaEonavailablefrompublishedandpublicsourcesand/orprovidedto it forthepurposesofthisdocument.Accordingly,neitherAurumnoranyofitspartners,employees,affiliates,agentsoradvisorsmakeanyrepresentaEonastotheaccuracy,completeness,reasonablenessorsufficiencyofanyoftheinformaEon contained in this document, and none of them shall be liable for any loss or damage (direct orindirect)sufferedasaresultofrelianceuponany informaEoncontained inthisdocument,oranyomissionofanyinformaEonfromthisdocumentandanysuchliabilityisexpresslydisclaimed.

• Aurum has developed this document and all concepts, structures, recommendaEons and analyses areproprietarytoAurumandcannotbeusedwithouttheexpresswri@enconsentofAurum.

• ThisdocumenthasbeenpreparedforpreliminarydiscussionpurposesonlywithoutprejudiceandshouldnotbeconstruedasanofferorinvitaEontopurchaseorsellanysecuriEes,businesses,orassetsofanyenEtyreferredtointhisdocument.

Disclaimer

2

VikramBihaniPartner

Experience:

Vikram is an experienced investment banker with over 18 years and over 50transacEonsunderhisbelt.

Exper9se:

• VikramexcelsatfosteringanddevelopingrelaEonshipstoenableclientstomake informeddecisionsthroughtrustedadvice inacomplex internalandexternalenvironment.

• Deeprootedpassioninfosteringthestart-upeocsystem,abilitytoconnectwith growth oriented entrepreneurs through their life cycle from capitalraises,acquisiEonsandexits.

• DirectorandInvestmentCommi@eeMemberofTrivedaCapital,aUS$500millionrealestatefund

• Director,InvestorandMentorofTricogHealthServicesPvtLtd,apredicEvehealthcareanalyEcsfirm,fundedbysomeofIndia’sleadingventurecapitalfunds

• He is a member, and been a past president of the Entrepreneurs’OrganizaEonBangalore,theBangalorechapterofa11,000+memberglobalorganizaEoncomprisingsomeofleadingentrepreneursacrosstheworld.

WorkExperience:

Past:

• Co-Founder and Director ofMosaic Capital Services PvtLtd

• AmbitCorporateFinancePteLtd

3

SpeakerProfiles…

StrategicBusinessAdvisor–AerospaceandDefense,Automo9veandGeneralEngineering

VSunder

Experience:

Hehas,over25years,held severalposiEons includingbeing theCEOofJoint Ventures, Head Corporate Planning, Head Compliance, Legal andCompany Secretary and Group CFO of a large and diverse IndianmulEnaEonal.HehasservedontheboardsofmanycompaniesincludingListedcompaniesinIndiaandabroad.Exper9se:

• HeisanIndustryveteranandanInsEtuEonBuilder.• Hehasover25yearsof richexperience inareasofBanking,Financial

Services,Manufacturing,DesignandEngineeringService• He has been closely involved in establishing and expanding many

ventures across the Globe in diverse fields like Engineering,AutomoEve, Defense, Aerospace, Engineering Design Services,Biotechnology,HomelandSecurityandTradingAcEviEes.

• Apart from his experience in establishing and growing businessesorganically,hehasledacquisiEonsofbusinessesacrosstheGlobeandintegraEngthemwiththeexisEngIndianVentures.

• His team building and natural leadership skills have enabled him toidenEfy,leadandmentormanyyoungbusinessleadersthroughouthisprofessionalcareer.

• He is a Fellow Member of The InsEtute Of Company Secretaries ofIndia.

• He is a long-standing member of the WPO (World PresidentsOrganizaEon)-ApremierGlobalLeadershipOrganizaEon.

WorkExperience:PastPresident&GroupCFO-DynamaEcTechnologiesLtd

CurrentCo-founder&MDofMaFoiConnecEngDotsAdvisory(P)Ltd.

4

SpeakerProfiles…

AirMarshalMMatheswaranStrategicConsultancy-Defense&AerospaceBusiness

Experience:

AirMarshalMMatheswaran is the formerDeputyChiefof IntegratedDefenceStaff(‘DCIDS’),responsibleforPolicy,PerspecEvePlansandForceDevelopment.HereEredager39yearsofservicewiththeIAF.Commissionedasafighterpilotin1975,hehasextensiveexperienceinimportantprojectssuchastheLCAandKaveri.

HewasSeniorAdvisortoCMD,HALatBangalorefromMay2014toMay2015.Hewas"President,AerospaceBusiness"ofRelianceDefencefrom01Nov2015to31July2016atMumbai,helpingthe industrymajortosetup itsAerospaceVerEcal.

HeisacEveinacademicworkandpresentspapersininternaEonalconferences.HeisamemberoftheExecuEveCouncil,thegoverningbodyofIDSA(InsEtuteofDefenceStudiesandAnalysis),NewDelhi-anautonomousthinktankunderMOD. He isacEvewithvariousother think-tanksand insEtuEonssuchas ISA,USI,CAPS,ORF,andIISS.

Currently he is Strategic Advisor & Consultant for Defence & Aerospace toCyient,RelianceDefence,FICCIandDoctoral Faculty,PhDprogram,NavalWarCollege,Goaamongstothers.

5

AmitCowshishPartner,DuaAssociates

Experience:

Amit is a former Financial Advisor (AcquisiEon) and Member DefenceProcurementBoard,MoD.Duringhiscareerwith the IndianDefenceAccountsService, spanning 35 years, he worked in various capaciEes in the DefenceAccountsDepartmentandondeputaEonwiththeCVCandtheMoD.

• WhileservingwiththeMoDhewasassociatedwithfinancialandcontractualma@ers related to procurement of goods and services for the IndianNavy,CoastGuard,SpecialForcesandtheArmyOrdnance;healsohandleddefenceplansandbudgetfrom2005to2011

• AsFinancialAdvisor(AcquisiEon),hehandledallfinancialma@ersrelatedtocapitalprocurementsfortheservicesandtheCoastGuard

• He has chaired the commi@ee that reviewed and draged the DefenceProcurementManual,2009anditssupplementof2010

• Hewasco-chairoftheforumsetuptoreviewtheprogressofallprocurementcases under the Foreign Military Sales (FMS) programme of the USGovernment and was a member of the IndoRussian working group onprocurementrelatedissues

• HeisaDisEnguishedFellowattheInsEtuteforDefenceStudiesandAnalysesandaSeniorVisiEngFellowattheDelhiPolicyGroup

• Presently, he is also amember of the commi@ee set up by theMinistry ofDefencetorecommendseongupofadefenceprocurementorganisaEon

6

SpeakerProfiles

7

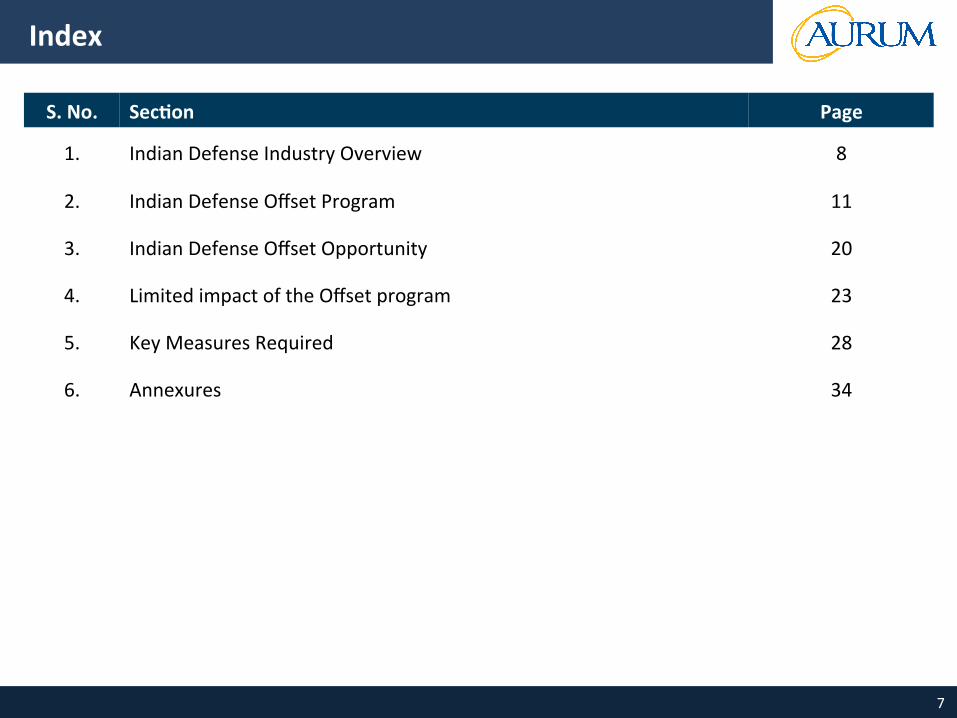

S.No. Sec9on Page

1. IndianDefenseIndustryOverview 8

2. IndianDefenseOffsetProgram 11

3. IndianDefenseOffsetOpportunity 20

4. LimitedimpactoftheOffsetprogram 23

5. KeyMeasuresRequired 28

6. Annexures 34

Index

8

IndianDefenseIndustryOverview1 SECTION

9

Indiaaccountsfor~2%oftheglobaldefensespend…

Source:MinistryofDefence,Govt.ofIndia,SIPRI*Figuresmaynotbecompa@blewitheachotherduetodifferencesinclassifica@on *OthersincludeOFs,DGQA,RR,NCC,MF,ECHS,etc

§ India is the 6th largest country in terms of defensespending, with the enEre defence sector, includingdefencepensions,accounEngfor2.4%ofIndia’sGDPin2016-17

§ India’s Defence budget for 2016-17: INR 2,491 bn(1.65%ofGDPin16-17)

§ Majorityofthedefensebudgetisallocatedforrevenueexpenditure (65%for theyear2016-17)andtheArmyreceivesthelargestallocaEon

§ OutlayoncapitalexpenditureasperbudgetesEmateshas decreased in 2016-17 budget for accommodaEngincreases in pay (7thCPC recommendaEons) andpension(OROP)

596

215

87 66 55 51 51 41

0.0%

4.0%

8.0%

12.0%

16.0%

-

200

400

600

USA China SaudiArabia

Russia UK India France Japan

MilitaryExpenditurebyCountry

MilitaryExpenditurein2015(USDbn) %ofGDP

113 125 134 152 163

80 78 95 95 86193 203

229 247 249

050100150200250300

2012-13 2013-14 2014-15 2015-16 2016-17

IndianDefenceBudget(INR‘000cr)

RevenueExpenditure CapitalExpenditure Total

52%

16%

21%

5%5%

Breakupof2016-17DefenseBudget

Army

Navy

AirForce

DRDO

Others*

10

..butisthelargestimporterofarmsintheworld

Source:SIPRI,DhirendraSinghCommiGeeReport2015,MinistryofDefense

14.0%

7.0%4.7% 4.6% 3.6% 3.4% 3.3% 2.9% 2.9% 2.6%

0.0%

5.0%

10.0%

15.0%

India SaudiArabia

China UAE Australia Turkey PakistanVietnam US SouthKorea

Top10ArmsImporter,2011-15(%ofGlobalShare)

§ Duetolackofindigenouslydesignedweapons,Indiahastoprimarily rely on imports for meeEng its defence capitalacquisiEonrequirements

§ Russia is thebiggest supplierof arms to India, thoughUSimportsinIndiahavestartedgrowingofflate

§ Goingforward,India’scapexspendisexpectedtogoupas~50%ofthecountry’sdefenceequipmentsareobsolete

70%

14%

5%12%

TopSuppliersofArmstoIndia(2011-15)

Russia US Israel Others

382

292262

-

100

200

300

400

500

FY14 FY15 FY16

ProcurementfromForeignVendorsbyIndianArmedForces(INRbn)

IndiashouldaccelerateitseffortstomanufactureinIndia,whichwillleadtoincreasedself-relianceinarmsprocurement,andsavepreciousforeignexchange–hencethefocuson“OffsetProgram”

11

IndianDefenseOffsetProgram2 SECTION

12

DefenseOffsets

Source:McKinsey,PublicSources

WhatareDefenseoffsets?

§ CompensaEonarrangementsrequiredbythegovernmentasacondiEonofthepurchaseofgoodsandservicesfromnon-domesEcsuppliers

§ Offsetscantakeeitheroftwoforms:directoffsets(agreementswhicharedirectlyrelatedtothedefenseproductsbeingsold)andindirectoffsets

§ GovernmentstypicallygiveoffsetpackagesasignificantweightagewhenevaluaEngcompeEngbidsfromvariousforeignsuppliers

§ OffsetobligaEonsaremostlyfulfilledthroughawardof“credits”.Creditsmaybeearnedusinga“mulEplier,”oranincenEvethatreflectsthecountry’sdesiretodirectfundingorservicestowardparEcularsectorsoriniEaEves.

BenefitsofOffsetprograms

§ GovernmentscountonthelocalinvestmentsandtechnologytransferthatoffsetsgeneratetojusEfythecapitalexpendituresrequiredfortheirdefenseupgrades

§ Forglobaldefencecompanies,offsetshelpthemtapdifficulttoaccessmarketsthroughtheirindustrialrelaEonshipswithlocalpartners(forjointproducEonordevelopment)

RisksinOffsetAgreements

§ OffsetscanposelegalandreputaEonalrisksforthecontractorswhichactimproperlyinfulfillingtheiroffsetobligaEons

§ AnotherriskoverthelongtermisincreasedcompeEEonfromcompaniesthathavegainedkeycapabiliEesthroughoffsets

13

IndianDefenseOffsetPolicy

Source:MinistryofDefence*Norevisionin2013butchangesin2012wereincorporatedin2013

§ The DefenceOffset policy,was formally announced for the first Eme in 2005. Over the period 2005-2016, theDefenceOffsetGuidelineshavebeenrevisedmulEpleEmesbasedonfeedbackfromvariousstakeholders.

§ Defence Offsets Management Wing (DOMW) under the Department of Defence ProducEon is responsible forformulaEonofDefenceOffsetGuidelines

RevisionsinDefenseOffsetGuidelinesovertheyearsCurrentDefenseOffsetGuidelines(asperDPP2016)§ The currentDPP2016 lays down various categories of procurementprocessesnamely, in priority, Buy Indian –

IDDM(IndigenouslyDesigned,Developed&Manufactured),BuyIndian,Buy&Make(Indian),Buy&Make(Global)andBuyGlobal*

§ The Offset clause is applicable for ‘Buy (Global)’ or ‘Buy and Make’ categories of procurements where theindicaEvecostofacquisiEonisINR2,000croresormore

§ 30% of the es9mated cost of the acquisi9on in ‘Buy (Global)’ category acquisi9ons and 30% of the foreignexchangecomponentin‘BuyandMake’categoryacquisi9onswillbetherequiredvalueoftheoffsetobliga9ons

§ TheoffsetcondiEonformsapartoftheRFPandsubsequentlyofthemaincontract.Aseparateoffsetcontractisexecutedsimultaneouslywiththemaincontract.

2005 2006 2008 2011 2012 2013 2016

*DetailsofcategoriesofprocurementunderDPP2016providedinAnnexureI

14

DefenseOffsetEcosystem

Source:DPP2013

IndianOffsetPartner(IOP)

ForeignOEM/Vendor

Regulators

AvenuesforDischargeofOffsetObliga9ons

§ DirectPurchase/Exports§ FDI§ Investmentinkind-TOT§ Investmentinkind-Others§ GovernmentInsEtuEons§ DRDO

§ MinistryofDefense§ DIPP

§ DefensePSUs§ OrdnanceFactories§ DRDO§ PrivatePlayers

TierIsub-vendor

DischargeofOffsetObliga9ons

§ VendorResponsibility§ Periodfordischarge§ Performancebond§ MandatoryOffsets§ OffsetcreditsforTOT§ OffsetBanking§ MulEpliers§ ValuaEonofOffsets

ManagementofOffsets

§ Acquisi9onWing-ResponsiblefortechnicalandcommercialevaluaEonofoffsetproposals

§ DOMW-FormulaEonofDefenceOffsetGuidelinesandallma@ersrelaEngtopostcontractmanagement

RequirementfromIOP§ IncludeIndianenterprisesand

insEtuEonsandestablishmentsengagedinmanufactureofeligibleproductsand/orprovisionofeligibleservices,includingDRDO

§ IOPshallcomplywiththeguidelines/licensingrequirementssEpulatedbyDIPP

§ TheOEM/vendor/Tier-Isub-vendorisfreetoselectIOPforimplemenEngtheoffsetobligaEon,providedtheIOPhasnotbeenbarredbyMOD

15

Avenuesfordischargeofoffsetobliga9ons

Source:DPP2013

• Directpurchaseof,orexecuEngexportordersfor,eligibleproductsmanufacturedby,orservicesprovidedbyIndianenterprises,i.e.DefencePublicSectorUndertakings,OrdnanceFactoryBoardandprivateandpublicsectorIndianenterprises.

DirectPurchase/Exports

• ForeignDirectInvestmentinjointventureswithIndianenterprises(equityinvestment)forthemanufactureand/ormaintenanceofeligibleproductsandprovisionofeligibleservicesFDI

• Investmentin‘kind’intermsoftransferoftechnology(TOT)toIndianenterprisesforthemanufactureand/ormaintenanceofeligibleproductsandprovisionofeligibleservices

• Thiscouldbethroughjointventuresorthroughthenon-equityrouteforco-producEon,co-developmentandproducEonorlicensedproducEonofeligibleproductsandeligibleservices

Investmentinkind-TOT

• Investmentin‘kind’inIndianenterprisesintermsofprovisionofequipmentthroughthenon-equityrouteforthemanufactureand/ormaintenanceofeligibleproductsandprovisionofeligibleservices(excludingTOT,civilinfrastructureandsecondhandequipment)

Investmentinkind-Others

• Provisionofequipmentand/orTOTtoGovernmentinsEtuEonsandestablishmentsengagedinthemanufactureand/ormaintenanceofeligibleproductsandprovisionofeligibleservices,includingDRDO

Governmentins9tu9ons

• TechnologyAcquisiEonbytheDefenceResearchandDevelopmentOrganizaEoninareasofhightechnologyDRDO

§ MandatoryOffsets:Ø Aminimum70percentoftheoffsetobligaEonmustbedischargedbyanyoneoracombinaEonofDirectPurchase/Exports,FDI,

“InvestmentinKind-TOT”or“InvestmentinKind-Others”Ø WherethedischargeofoffsetobligaEonsisproposedintermsof“InvestmentinKind-Others”,thevendorisrequiredtobuyback

aminimum40%oftheeligibleproductand/orservice(byvalue)withinthepermissibleperiodfordischargeofoffsetobligaEons

§ OffsetCreditsforToT:WherethedischargeofoffsetobligaEonsisproposedintermsof“InvestmentinKind-TOT”,theoffsetcreditforTOTshallbe10%ofthevalueofbuybackduringtheperiodoftheoffsetcontract,totheextentofvalueaddiEoninIndia

16

DischargeofOffsetObliga9ons(1/2)

Source:DPP2013

VendorResponsibility

§ TheVendoroftheequipmentunderthemainprocurementcontractresponsibleforthefulfilmentofoffsetobligaEons

§ TheVendorcanallowhisTier-1sub-vendorsunderthemainprocurementcontracttodischargeoffsetobligaEons,totheextentoftheirworkshare(byvalue),onbehalfofthemainvendor

§ But,overallresponsibilityandliabilityforthefulldischargeofoffsetobligaEonsconEnuetoremainwiththemainvendor

PeriodforOffsetDischarge

§ OffsetobligaEonsaretobedischargedwithinaEmeframethatcanextendbeyondtheperiodofthemainprocurementcontractbyamaximumperiodoftwoyears

§ Theperiodofthemaincontractincludestheperiodofwarrantyoftheequipmentbeingprocuredunderthemaincontract

PerformanceBond

§ WhentheperiodfordischargeofoffsetobligaEonsexceedstheperiodofthemainprocurementcontract,thevendorisrequiredtofurnishanaddiEonalPerformanceBondtoDOMWintheformofaBankGuaranteecoveringthefullvalueoftheun-dischargedoffsetobligaEons

§ ThisPerformanceBondshallbereducedannually,unElfullexEncEon,basedontheproratavalueofthedischargedoffsetobligaEonacceptedbytheDOMW.TheaddiEonalPerformanceBondshallbesubmi@edsixmonthspriortoexpiryofthemainPerformance-cum-WarrantyBond

17

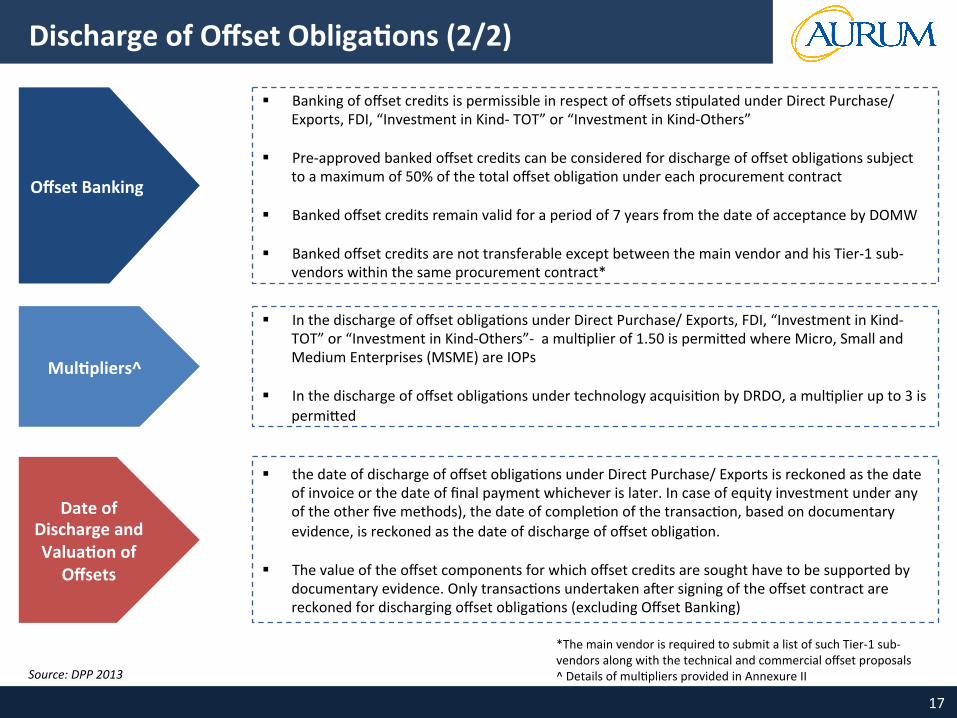

DischargeofOffsetObliga9ons(2/2)

Source:DPP2013

OffsetBanking

§ BankingofoffsetcreditsispermissibleinrespectofoffsetssEpulatedunderDirectPurchase/Exports,FDI,“InvestmentinKind-TOT”or“InvestmentinKind-Others”

§ Pre-approvedbankedoffsetcreditscanbeconsideredfordischargeofoffsetobligaEonssubjecttoamaximumof50%ofthetotaloffsetobligaEonundereachprocurementcontract

§ Bankedoffsetcreditsremainvalidforaperiodof7yearsfromthedateofacceptancebyDOMW

§ BankedoffsetcreditsarenottransferableexceptbetweenthemainvendorandhisTier-1sub-vendorswithinthesameprocurementcontract*

Mul9pliers^

§ InthedischargeofoffsetobligaEonsunderDirectPurchase/Exports,FDI,“InvestmentinKind-TOT”or“InvestmentinKind-Others”-amulEplierof1.50ispermi@edwhereMicro,SmallandMediumEnterprises(MSME)areIOPs

§ InthedischargeofoffsetobligaEonsundertechnologyacquisiEonbyDRDO,amulEplierupto3ispermi@ed

DateofDischargeandValua9onof

Offsets

§ thedateofdischargeofoffsetobligaEonsunderDirectPurchase/Exportsisreckonedasthedateofinvoiceorthedateoffinalpaymentwhicheverislater.Incaseofequityinvestmentunderanyoftheotherfivemethods),thedateofcompleEonofthetransacEon,basedondocumentaryevidence,isreckonedasthedateofdischargeofoffsetobligaEon.

§ Thevalueoftheoffsetcomponentsforwhichoffsetcreditsaresoughthavetobesupportedbydocumentaryevidence.OnlytransacEonsundertakenagersigningoftheoffsetcontractarereckonedfordischargingoffsetobligaEons(excludingOffsetBanking)

*ThemainvendorisrequiredtosubmitalistofsuchTier-1sub-vendorsalongwiththetechnicalandcommercialoffsetproposals^DetailsofmulEpliersprovidedinAnnexureII

18

RecentAmendmentsinDefenseOffsetPolicy(1/2)

KeyIssue RecentAmendmentinOffsetPolicy

Unrealis9coffsetoffersandinflexibility

forsuppliers

§ Timelagbetweensubmissionofoffsetoffers,finalizaEonandimplementaEonoftheoffsetcontracts

§ SuppliersfacedifficulEesinprovidingupfrontspecificdescripEonofproducts,workshare,yearlydischargescheduleandsupporEngdocumentstoestablisheligibilityofIOPs

§ Pre-ContractStage:VendorsnowhavetheopEon,tosubmitdetailedoffsetproposalsatalaterstage.ThevendorcanfinalizeitsIOPsandoffsetproductdetailseitherattheEmeofseekingoffsetcreditsor1yearpriortotheintendedoffsetdischargethroughtheIOP

§ Post-ContractStage:Enablingprovisionshavealsobeenprovidedatthepost-contractstageforchangeinIOP/offsetcomponentandre-phasingwithintheperformanceperiod,andaprovisionhasbeenintroducedallowingaddressingofsupplier'srequeststochangetheIOPortheiroffsetcomponentasperrequirementduringtheperiodofthecontract

Exchangeratevaria9onduringcourseofoffsetdischarge

§ ExchangeRateVariaEon(ERV)hasbeenmadeapplicableforRupeecontractswithIndianvendorsbasedonRFPsissuedunderallcategoriesofcapitalacquisiEonswherethereisanimportcontent.

§ However,ERVclausewillnotbeapplicabletocontractswherethedeliveryperiodislessthan1yearandtherateofexchangeiswithinthebandof+/-2.5%

1

2

19

RecentAmendmentsinDefenseOffsetPolicy(2/2)

KeyIssue RecentAmendmentinOffsetPolicy

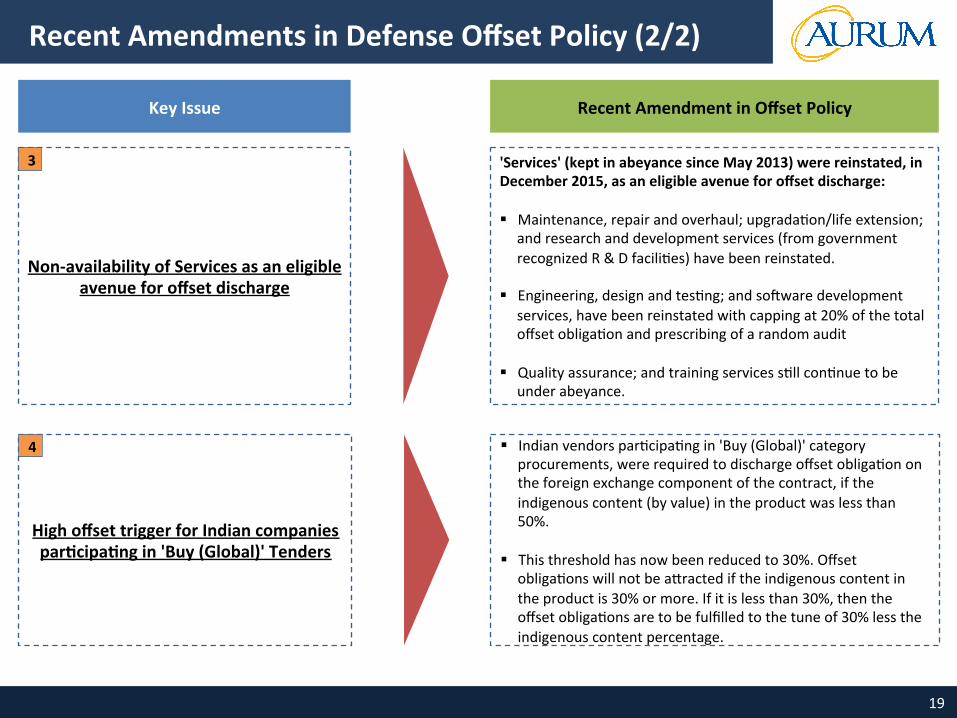

Non-availabilityofServicesasaneligibleavenueforoffsetdischarge

'Services'(keptinabeyancesinceMay2013)werereinstated,inDecember2015,asaneligibleavenueforoffsetdischarge:

§ Maintenance,repairandoverhaul;upgradaEon/lifeextension;andresearchanddevelopmentservices(fromgovernmentrecognizedR&DfaciliEes)havebeenreinstated.

§ Engineering,designandtesEng;andsogwaredevelopmentservices,havebeenreinstatedwithcappingat20%ofthetotaloffsetobligaEonandprescribingofarandomaudit

§ Qualityassurance;andtrainingservicessEllconEnuetobeunderabeyance.

HighoffsettriggerforIndiancompaniespar9cipa9ngin'Buy(Global)'Tenders

§ IndianvendorsparEcipaEngin'Buy(Global)'categoryprocurements,wererequiredtodischargeoffsetobligaEonontheforeignexchangecomponentofthecontract,iftheindigenouscontent(byvalue)intheproductwaslessthan50%.

§ Thisthresholdhasnowbeenreducedto30%.OffsetobligaEonswillnotbea@ractediftheindigenouscontentintheproductis30%ormore.Ifitislessthan30%,thentheoffsetobligaEonsaretobefulfilledtothetuneof30%lesstheindigenouscontentpercentage.

3

4

20

IndianDefenseOffsetOpportunity3 SECTION

21

CurrentStatusoftheOffsetProgram

Source:MinistryofDefence

NumberofContracts

OffsetValue(USDmn)

%ofTotal

AirForce 16 3,904 79%

Navy 6 886 18%

Army 3 180 4%

TOTAL 25 4,970 100%

OffsetContractssignedbyMoD9llOctober2014§ Firstoffsetcontractwassignedin2007

§ AsperMinistryofDefense, ithasoverallsigned29offsetcontractsworthUSD6.13bnEllMay06,2016whichhavetobedischargedEll2022

§ Offset obligaEons to be discharged in respect ofdefencecontractssignedwasUSD~2.23bnby31stDecember2015

§ Vendors have reported discharge claims worthUSD~1.78bn*throughtheirquarterlyreports

46%

16%

34%

4%

OffsetBreakup-ByGeography(TillOctober2014)

USA

Russia

Europe

Israel

*Subjecttoaudit

40%

33%

27%

OffsetBreakup-BySector(TillOctober2014)

DefensePSUs

LargeIndustries

SMEs

22

Es9matedDefenseOffsetOpportunity(FY17-FY22)

Par9culars FY17-FY22 Remarks

IndianDefenceSpend(USDbn) 412 Defensebudgettobecome2.25%ofIndia’sGDP

CapexSpendas%ofDefenceSpend 49% CapextoOpexmixexpectedtoimproveinnext5yearsfromthecurrentlevel

EsEmatedCapexSpend(USDbn) 201

EsEmatedNewArmamentSpend(USDbn) 171 NewArmamentSpendesEmatedat85%ofoverallcapexspend

Importsas%ofNewArmamentSpend 55% Importpartofcapexspendisexpectedtoreduceovernext5yearswithIndia’sfocusonindigenizaEon“MakeinIndia”

ImportedEquipmentSpend(USDbn) 94^

Offsetas%ofImports 30%

AddressableOffsetOpportunity(USDbn) 28

AverageOffsetOpportunityperyear(USDbn)* 5.6

Source:FICCI

ExchangeRate:USD1=INR67*Timinguncertainfortheseoffsets

^AsperDPP2016,onlyacquisi@oncontracts>INR2000crore(USD~300mn)eligibleforoffsets

Basedonsimplis9cassump9ons,itises9matedthatUSD~6bninaddi9onaloffsetopportuni9eswillbegeneratedforIndianplayersduringtheperiodFY17-FY22;howeveramorerealis9cexpecta9onbasedoncurrentexperience

makesusbelievethattheEs9matedCapexSpendwillnotcrossUSD100bnoverthenext5years

23

LimitedImpactoftheOffsetProgram4 SECTION

24

TherehasbeengrowthinA&DExportssince2007……

Source:Interna@onalTradeCentre

*ITC(HS)Codesarebroad-basedandinclusiveoffewnon-defenceitemsalsoDoesnotincludeservices,inlandandcoastalsecurity

83 96 80 61 200 69 379

1,614 1,3131,998

2,6642,039

4,805 4,448

-1,0002,0003,0004,0005,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

IndiaExportsofA&DEquipment(USDmn)*

Total

ITC-93

ITC-8906

ITC-88

ITC-8710

ITCHSCode CategoryDescrip9on

8710 TanksandotherarmouredfighEngvehicles

88 Aircrag,spacecrag,andpartsthereof

8906 Vessels,incl.warshipsandlifeboats

93 ArmsandammuniEon;partsandaccessoriesthereof

§ Itemseligibleforoffsetdischargebroadlyfallunder4categoriesunderITCHSclassificaEon-93,8906,88and8720

§ GrowthinexportsofA&DequipmentfromIndiahascoincidedwiththepromulga9onofoffsetpolicysince2005

§ ExportsunderITCHSCode88,whichcaterto‘aircrag,spacecragandparts’,accountfor85%shareofexportsin2015

§ However,majorityofexportsunderthiscategoryconsEtutesofcivilianaircragsandrelatedcomponentssentabroadforMRO

25

butmostlyaircrarpartsarebeingexported….

Source:Interna@onalTradeCentre

Country-wiseExportstoCountrieswithOffsetLiabili9esunderITCHSCodes8802and8803in2015Country Exportsunder

ITCHS8802ExportsunderITCHS8803

USDmn USDmnUSA 101 374UK 6 216France 2 130Russia - 95Israel - 55Switzerland - 25Italy - 11Others 2,329 326Total 2,438 1,299

§ Valueofexportsunderthetwoheads,8802and8803,accountedfor~84%ofthetotalA&Dexportsin2015

§ Category8802refersto“poweredaircragsincludinghelicopters,aeroplanes,spacecragincl.satellitesandspacecraglaunchvehicles”while8803referto“partsofaircragandspacecrag“

§ Majority of exports to the countries having offset discharge liabili9es are in the category 8803, implying mostly parts andcomponentsarebeingexportedtothesecountriesbyIndiansuppliers

§ Substan9alriseinexportsundercategory8803tocountrieswithoffsetliabilityfrom2007onwards,furtherreinforcesthatoffsetshaveresultedinsubstan9alincreaseinIndianexportsofaircrarpartstothesecountries

50 37 42 46204

621476

1,0049101,066

902 844 906

-200400600800

1,0001,200

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

IndiaExportsunderITCHSCode8803(USDmn)

USA UK France Russia Israel Switzerland Italy Total

26

…andthereisnegligibleFDIfromOffsetssofar

Source:DIPP,MinistryofDefense

§ AsperDIPP,IndiahasreceivedFDIworthonlyUSD~5mninDefenseIndustriesfromApr-2000toSep-2016.

§ Thislackofinterestcanbea@ributedmajorlyto26%limitonFDIinDefenceIndustrieswhichwasinplaceEllAugust2014.However,thereisnotasingleinflowwhichwasbroughtinbycompanieshavingoffsetliabilitywithMoD

§ TheGovernmenthasliberalizedFDIpolicyprovisionsindefencesectorvide.PressNote.5(2016Series)on24thJune,2016

§ AsperthenewFDIpolicy,foreigninvestmentupto49%ispermi@edunderautomaEcrouteandbeyond49%throughGovernmentapprovalroutewhereveritislikelytoresultinaccesstomoderntechnologyorforotherreasonstoberecorded

§ SinceopeningofdefencesectorforFDI,36FDI/JVproposalshavebeenapprovedformanufactureofvariouslicensabledefenceitemsElldate.AgerthenoEficaEonofrevisedFDIpolicyinJune2016,6proposalshavebeenreceivedbytheFIPBElldate.

56,080

24,250 22,050 21,169 15,793

5-

20,000

40,000

60,000

Services ConstrucEon ITSogware&Hardware

Telecom Automobile Defence

Cumula9veFDIInflows(USDmn)inIndiafromApril2000-September2016

TherehasbeennegligibleFDIwhichhascomeintoIndiaonaccountofOffsets.ImpactofincreaseinFDIcapto100%onthedischargeofoffsetobliga9onsremaintobeseen.

27

HistoricalReasonsforLimitedImpactofOffsetProgram

§ RigidityoftheOffsetPolicycombinedwithaweakgovernancestructurewherethereisnostrategicdirecEonandnomajorpowergiventotheDOMWisamajorhindrance

§ LackofamulE-EerecosystemlikeintheautomoEvesectorhasreducedthescopeforoutsourcingbyglobalmajors

§ ExisEngsupplychainisdominatedbysmallplayersdevelopedbythePSUswhohadamonopolyinthismarket;smallplayerssufferfromlackofcapital,technologyandprocesscapabiliEestoserviceglobalmajors

§ LackofpaEentcapitaltosupportthelonggestaEonperiods–asignificantfeatureofthissector;financialsourcesofcapitalsuchasprivateequityandventurecapitaldonotenteratanearlystageduetolonggestaEonperiodofprojects

§ Lackofcoordinatedeffortsamongstmechanicalengineering,electronics,designandtheinformaEontechnologysectorssoastoofferacompletesoluEontocustomers;acoordinatedapproachcanenablebuildingofenErepla}ormswhichwill,apartfromaddingvalue,buildvolumeinthissector

§ LackofIndustrialclusterslikeinautomoEveandothersectors;globally,largescaleindustrialgrowthhashappenedwhentheyhaveadopteda'clusterapproach’

§ NonavailabilityofrawmaterialsourceswithinthecountryandconEnuedrelianceonimports

28

OpportunityAhead5 SECTION

29

Opportuni9esAhead…

Source:SIPRI,IndianBudgetDocuments,FICCI

§ AsperareportbyFICCI,acombinaEonoffactorssuchasoffsets,outsourcing,defensecapitalexpenditurespends,etccoulddrivethedefensespendfrom$6billioninFY14toanesEmated$41billionbyFY22asbelow:

30

Opportuni9esAhead…

Source:KPMGReport2015

§ Expenditureoncapitalequipmentbyallsegmentsofthearmedforcestogathersteam;itisexpectedthatcapitalexpenditurewillriseto50%ofdefenseexpenditureasagainst35%currentlyandrevenueexpenditurewilldeclinecorrespondingly;somehighEcketitemsofimmediatepriorityarelistedbelow:

Air>USD30billion

Naval>USD22billion

Land>USD16billion

Rafale,AvroReplacementProgram,PilatusTrainerAircrag,LightUElityHelicopter,SukhoiFighterJet,TejasLCA,KamovHelicopters

SoldierasaSystemProgram,InfantryCombatVehicle,M777UltraLightHowitzers,LightArmoredMulEpurposeVehicle,ThermalImagingSightsforT-72tanks

Submarines(Project75I),IndigenousAircragCarrier(INS–Vishal),MulERoleFrigates(Project17A),LandingPla}ormDocks,Corve@es(Warships–Project28A)

31

Opportuni9esAhead…

§ Astrongeco-systemisbeingcreatedforaerospace&defenseinIndia:§ LargebusinessgroupssuchasTata’s,AdityaBirla,Reliance,L&T,etcareusingtheircorecompetenciesto

enterthedefenseindustrychallengingthelargebureaucraEcPSUs§ CompaniessuchasM&M&BharatForgethathavebeeninautocomponentsarelookingtomoveupthe

valuechaininaerospace&defenseandthistrendisfindfavorwithmidsizedautocomponentcompanieswhoareusingcapabiliEessuchasQuality(QS-ISOcerEficaEon,ProductCapabiliEes(smallcarmanufacturinginIndia),availabilityofskilledmanpowerandproximitytokeymarketsasafoundaEonformovingintotheaerospace&defensesector;

§ Emergenceofclustersdedicatedtoaerospace&defenseasshownbelow.

32

Opportuni9esAhead…

§ OtherfactorscontribuEngtolargeanEcipatedgrowthaheadinclude:

§ LiberalizaEonoftheoffsetnormsandprocurementprocessesofPSUsdrivenbytheGovernment's'MakeInIndia'iniEaEvehasenthusedlargerprivatesectorplayerstoenterthissector

§ LargeglobalcompaniessuchasThyssenKruppseongupwarehousesinIndia,easingthesupplyofcriEcalrawmaterial

§ SkilldevelopmentiniEaEveshavestartedbuildinghumanresourcecapacity

§ Theglobalsocio-poliEcalclimate,especiallywithChinaandPakistan;DonaldTrump’selecEontothePresidencyofUSAandhisequaEonwithPuEnofRussiacouldbeabenefittoIndiaaswellasweimport70%ofourarmsfromRussia

§ India’scurrentfiscalposiEonwithPublicDebttoGDPraEoseenascomfortable,couldspurdefensespendingoncapitalexpenditure

33

ThankYou

ContactPersons:

SanjayBansalFounder&ManagingPartnerAurumEquityPartnersLLPTel:+911244424477Mob:+919811010810Email:sanjaybansal@aurumequity.comVikramBihaniPartnerAurumEquityPartnersLLPTel:+918067205598Mob:+919886409387Email:[email protected]

34

Annexures6 SECTION

35

6A AnnexureI:ImpactofRecentEvents

36

RafaleDealwithFrance

Source:PublicSources

RafaleDealPar9culars Value

ContractSize(INRbn) 590

OffsetClauseofRafaleDeal 50%

OffsetOpportunity(INRbn) 295

OffsetDischargePeriod(years) 7

AnnualOffsetOpportunity(INRbn) 42

USD~630mnofannualoffsetopportunityavailabletoIndianDefenseindustryfromtheRafaledealovernext7years

§ IndiasignedEuro7.87billion (Rs59,000crore)agreementwithFranceforpurchaseof36RafalefighteronSeptember23,2016

§ TheoffsetclauseofRafaledealisa50%investmentcommitmentfromtheFrenchindustryinIndia

§ TheoffsetswillbecarriedoutbyFrenchcompanyDassaultandits vendors- Safran, Thales and MBDA, all part of the Rafaleproject

§ Asper thecontract,Dassault is in chargeofmeeEng theoffsetobligaEons and has to share details of all its partners andplannedworkwithinoneyearofsigningthecontract

§ ~74%ofthe50%offsetvalueshouldbeexportedfromIndia§ RelianceDefencehasalreadyformedaJVwithDassaultSystems

“DassaultRelianceAerospace”forexecuEonofoffsetobligaEonsØ Dassault expected to make aerostructures, engine parts and

electronicsattheReliancefacilityinNagpurØ Aimtomake50%ofRafalepartsinIndia

§ Besides the investment commitment, there is a 6% technologysharingcomponentaswell

Ø France likely to help India revive the unsuccessful KaveriengineprojectforindigenousTejasaircrag,and

Ø TransferadvancedtechnologytoDRDO

37

IncreaseincontractcostthresholdinDPP2016

Source:ASSOCHAMIndia,DPP2016

AsperDPP2016§ Theoffsetclausewouldbeapplicablefor‘Buy(Global)’or‘BuyandMake’categoriesofprocurementswherethe

indicaEvecostofacquisiEonisRs.2000Croresormore,asonthedateofaccordofAoN.§ However,DACmayconsiderparEalorfullwaiverofoffsetclause.§ IncaseofawaiverforaparEcularacquisiEoncase,eligible/selectedIndianvendorsneedtobeexemptedfromthe

correspondingICsEpulaEons

LikelyPosi9veImpact§ ManagementandmonitoringbytheMoDwill

becomemoreefficientasthenumberofprogrammesdecreases

§ PosiEvefromforeignOEMsperspecEvelookingtoinvestinIndiandefenseopportuniEes

LikelyNega9veImpact§ Increaseinthresholdwillreducethenumberof

projectseligibleforoffsetsandhencequantumofoffsetsflowingintothecountry

§ DetrimentaltotheMakeinIndianarraEvewhichpromotesdevelopmentoflocalindustryandploughingbackofcapitalintothecountry

38

6B AnnexureII:CategoriesunderDPP2016

39

CategoriesofProcurementunderDPP2016

Source:DPP-2016

Indecreasingorderofprioritytheprocurementofdefenceequipment,underDPP2016arecategorizedasfollows:

• ‘Buy(Indian-IDDM)’categoryreferstotheprocurementofproductsfromanIndianvendormeeEngoneofthetwocondiEons:productsthathavebeenindigenouslydesigned,developedandmanufacturedwithaminimumof40%IndigenousContent(IC)oncostbasisofthetotalcontractvalue;or,productshaving60%IConcostbasisofthetotalcontractvalue,whichmaynothavebeendesignedanddevelopedindigenously

Buy(Indian-IDDM)

• ‘Buy(Indian)’categoryreferstoprocurementofproductshavingaminimumof40%IConcostbasisofthetotalcontractvalue,fromanIndianvendor

Buy(Indian)

• ‘Buy&Make(Indian)’categoryreferstoaniniEalprocurementofequipmentinFullyFormed(FF)stateinquanEEesasconsiderednecessary,fromanIndianvendorengagedinaEe-upwithaforeignOEM,followedbyindigenousproducEoninaphasedmannerinvolvingToTofcriEcaltechnologiesasperspecifiedrange,depthandscopefromtheforeignOEM.Underthiscategoryofprocurement,aminimumof50%ICisrequiredoncostbasisofthe‘Make’porEonofthecontract.

BuyandMake(Indian)

• ‘Buy&Make’categoryreferstoaniniEalprocurementofequipmentinFullyFormed(FF)statefromaforeignvendor,inquanEEesasconsiderednecessary,followedbyindigenousproducEonthroughanIndianProducEonAgency(PA),inaphasedmannerinvolvingToTofcriEcaltechnologiesasperspecifiedrange,depthandscope,tothePA

BuyandMake

• ‘Buy(Global)’categorizaEonreferstooutrightpurchaseofequipmentfromforeignorIndianvendors.Incaseofforeignvendors,GovernmenttoGovernmentroutemaybeadopted,forequipmentmeeEngstrategic/longtermrequirements.

Buy(Global)

40

6C AnnexureIII:Mul9pliers

41

AnnexureII:Mul9pliers

Source:DPP-2013

Defini9onofMicro,SmallandMediumEnterprises§ Inthecaseofenterprisesengagedinmanufactureofgoods:

Ø AmicroenterpriseisthatwhereinvestmentinplantandmachinerydoesnotexceedINR2.5million;Ø AsmallenterpriseisthatwhereinvestmentinplantandmachineryismorethanINR2.5millionbutdoesnot

exceedINR50million;andØ AmediumenterpriseisthatwhereinvestmentinplantandmachineryismorethanINR50millionbutdoes

notexceedINR100million

§ Inthecaseofenterprisesengagedinprovidingservices:Ø AmicroenterpriseisthatwhereinvestmentinequipmentdoesnotexceedINR1million;Ø AsmallenterpriseisthatwhereinvestmentinequipmentismorethanINR1millionbutdoesnotexceed

INR20million;andØ AmediumenterpriseisthatwhereinvestmentinequipmentismorethanINR20millionbutdoesnot

exceedINR50million

Mul9plierforTechnologyAcquisi9onbyDRDO§ MulEplierof2.0isapplicablewhenthetechnologyisofferedforusebyIndianArmedForcesonlybutwithoutany

restricEononthenumbersthatcanbeproduced§ MulEplierof2.5isapplicablewhenthetechnologyisofferedforuseonlyinIndianMarketbutforbothmilitary

andcivilapplicaEonsandwithoutanyrestricEononthenumbersthatcanbeproduced§ MulEplierof3.0isapplicablewhenthetechnologyisofferedwithoutanyrestricEonandwithfullandunfe@ered

rights,includingrighttoexport

42

6D AnnexureIV:Abbrevia9ons

43

Abbrevia9ons

bn Billion MF MilitaryFarms

CPC CentralPayCommission mn Million

DGQA DirectorateGeneralQualityAssurance MOD MinistryofDefence

DIPP DepartmentOfIndustrialPolicy&PromoEon NCC NaEonalCadetCorps

DOMW DefenceOffsetsManagementWing OEM OriginalEquipmentManufacturer

DPP DefenceProcurementProcedure OF OrdnanceFactory

DRDO DefenceResearchandDevelopmentOrganisaEon OROP OneRankOnePension

ECHS Ex-ServicemenContributoryHealthScheme PA ProducEonAgency

FDI ForeignDirectInvestment RFP RequestforProposal

FF FullyFormed RR RashtriyaRifles

GDP GrossDomesEcProduct SIPRI StockholmInternaEonalPeaceResearchInsEtute

IC IndigenousContent TOT TransferofTechnology

IDDM IndigenouslyDesignedDevelopedandManufactured UK TheUnitedKingdom

INR IndianRupee USA UnitedStatesofAmerica

IOP IndianOffsetPartner USD UnitedStatesDollar