audit resolution under the uniform grant guidance presented by michael brustein, esq....

TRANSCRIPT

Audit Resolution Under the Uniform Grant Guidance

Presented byMichael Brustein, Esq.

[email protected] Jennifer Castillo, Esq.

[email protected] & Manasevit, PLLC

Fall Forum 2014

The Uniform Grant Guidance:

1) “Right-sizes the footprint of oversight and single audit requirements”

2) Focus audits where there is greatest risk of fraud, waste and abuse

Brustein & Manasevit, PLLC 2

Brustein & Manasevit, PLLC 3

HOW???

1. Makes single audits available online2. Encourages a cooperative approach to audit

resolution3. Raises threshold to $750,0004. Places focus on internal control deficiencies

that have been identified as material weaknesses

Brustein & Manasevit, PLLC 4

Internal control deficiencies remain a moving target

Brustein & Manasevit, PLLC 5

OMB / COFAR have not finalized guidance on oversight of single audit vs. pass-through

responsibility

Who is responsible for which internal controls?

Brustein & Manasevit, PLLC 6

Notice of Intent2-28-12

77 fr 11780

Compliance requirements will be “streamlined”

Brustein & Manasevit, PLLC 7

Audit focus should be on

• Allowable costs / activities• Eligibility• Reporting• Selection of subs• Monitoring• Cash management• Procurement

Brustein & Manasevit, PLLC 8

NPRM2-1-13

78 fr 7295• Proposed limiting audit review of

internal controls in compliance supplement from 14 to 7

Brustein & Manasevit, PLLC 9

The Proposed Seven Deadly Sins

1. Activities Allowed or Unallowed2. Allowable Costs (and Matching)3. Cash Management (Minimizing time)4. Eligibility5. Reporting (financial and performance)6. Subrecipient Monitoring7. Requirements Unique to the Program

Brustein & Manasevit, PLLC 10

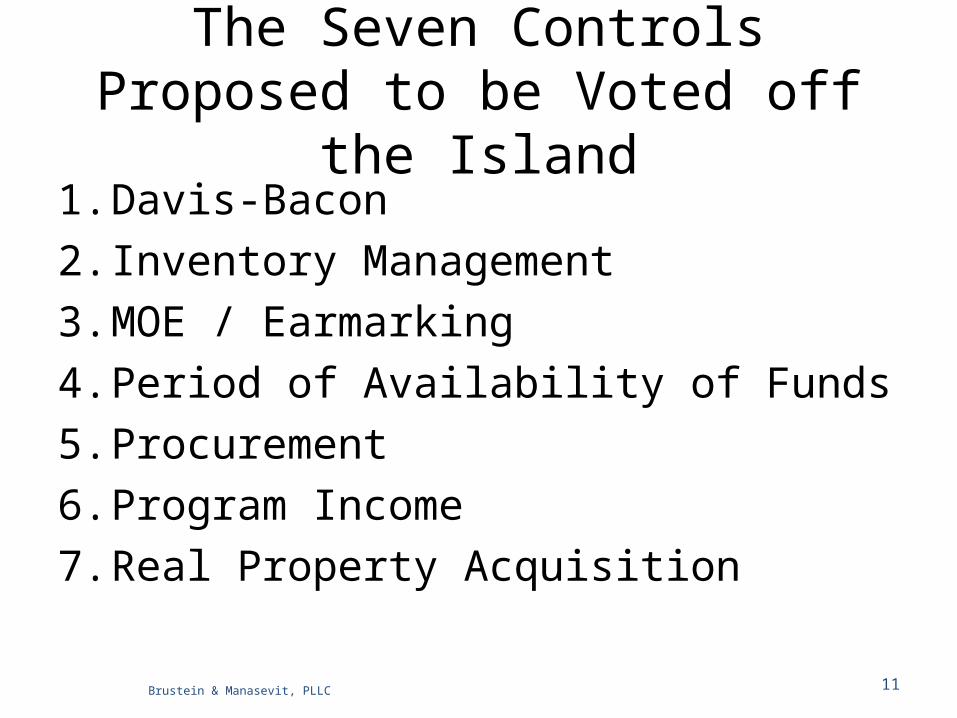

The Seven Controls Proposed to be Voted off the Island

1. Davis-Bacon2. Inventory Management3. MOE / Earmarking4. Period of Availability of Funds5. Procurement6. Program Income7. Real Property Acquisition

Brustein & Manasevit, PLLC 11

But who is responsible for oversight of these seven???

Pass-Through

Brustein & Manasevit, PLLC 12

And where will the resources come from?

Brustein & Manasevit, PLLC 13

Final Guidance

“While most commenters were in favor of the proposed reduction of the number of types of compliance requirements in the compliance supplement, many voiced concern about the process that would implement such changes”

– 78 CFR 78608

Brustein & Manasevit, PLLC 14

• No changes made at this time • COFAR recommends further

outreach

Brustein & Manasevit, PLLC 15

May 2014 Compliance Supplement

Silent

Brustein & Manasevit, PLLC 16

OMB / COFAR FAQ 8/14/14

Look to the 2015 Compliance Supplement on the streamlining of compliance requirements

(P. 15)

Brustein & Manasevit, PLLC 17

• While final chapter is yet to be written, we recommend every non-federal entity has fundamental understanding of the following four legal authorities

Brustein & Manasevit, PLLC 18

1. Uniform Guidance – Subpart F2. Compliance Supplement3. Generally Accepted Government Auditing

Standards (Yellow Book)4. EDGAR / GEPA Enforcement Provisions

Brustein & Manasevit, PLLC 19

UNIFORM GUIDANCE SUBPART F

Brustein & Manasevit, PLLC 20

Federal Agency Responsibility

• Cognizant agency for audit– TA to auditees– Quality control– Advice to auditors– Notice to auditors of audit deficiencies – Coordinate management decisions

Brustein & Manasevit, PLLC 21

Federal Agency Responsibilities

• Awarding agency responsibility– Ensure completion of audits – timely– TA to auditees and auditors– Follow up – ensure corrective action– Management decision– Monitor corrective action– Use CAROI

Brustein & Manasevit, PLLC 22

CAROI

• Cooperative Audit Resolution Oversight Initiative–Developed with ED and pilot states–Adopted by ED as standard audit

resolution

Brustein & Manasevit, PLLC 23

CAROI

Historically:Rejected by most other agencies LaborAgricultureHealth Human Services

Brustein & Manasevit, PLLC 24

Uniform Grant Guidance Applies CAROI

• To all federal agencies • Government wide policy

Brustein & Manasevit, PLLC 25

CAROI 200.25

• Audit and follow up that promotes prompt corrective action

• Improve communication• Foster collaboration• Promote trust• Develop federal – non federal agency

understanding

Brustein & Manasevit, PLLC 26

CAROI (cont.)

• Basis– Leadership commitment to program

integrity– Partnership, federal

• Non federal and auditors– Focus

• Current conditions and cooperative action

Brustein & Manasevit, PLLC 27

CAROI (cont.)

• Message:– Continued failure to correct unacceptable

Brustein & Manasevit, PLLC 28

CAROI (cont.)

• Prompt corrective action as shown by audits

–Federal agencies offer–Appropriate relief Past

non-compliance

Brustein & Manasevit, PLLC 29

CAROI (cont.)

• Federal agency responsibilities 200.513– Use CAROI to improve outcomes

• Audit resolution• Follow up• Corrective action

Brustein & Manasevit, PLLC 30

CAROI (cont.)

Management DecisionAudit finding sustained or not sustainedReasons for decisionExpected action

Repayment?Corrective actionAppeal available6 months of filing with Federal Audit Clearing House

(FAC)

Brustein & Manasevit, PLLC 31

The Office of Management and Budget (OMB) A-133 Compliance

SupplementWhat is it?

Who does it apply to?

• Expend more than $500k ($750k under Uniform Grant Guidance)

• Covers 150 major programs

Brustein & Manasevit, PLLC 33

Why is the Compliance Supplement important?

How is the Document Organized? • Part 1 – Background, Purpose, and

Applicability• Part 2 – Matrix of Compliance

Requirements• Part 3 – Compliance Requirements• Part 4 – Agency Program Requirements• Part 5 – Clusters of Programs• Part 6 – Internal Control• Part 7 – Guidance for Auditing Programs

Not Included in the Compliance Supplement

Brustein & Manasevit, PLLC 35

Part 4: Agency Program Requirements

Brustein & Manasevit, PLLC 36

The most useful portion for federal education grant recipients is the agency- specific section

on the Department of Education

Example: Title I, Part A of the ESEA I.Program Objectives: The objective of this program is to improve the teaching and learning of children who are at risk of not meeting challenging academic standards and who reside in areas with high concentrations of children from low-income families. II.Program Procedures

I. Describes ESEA flexibility, Sources of Governing requirements, availability of other program information

III.Compliance Requirements

Brustein & Manasevit, PLLC 37

Example: CAREER AND TECHNICAL EDUCATION—BASIC GRANTS TO STATES (Perkins IV)

Program Objectives: Perkins IV provides grants to States and outlying areas to develop the career, technical, vocational, and academic skills of secondary students and postsecondary students …I.Program Procedures: II.Compliance Requirements:

I. Matching, Level of Effort, Earmarking I. Level of Effort – Maintenance of Effort

Brustein & Manasevit, PLLC 38

Example: 21 Century Learning Centers

I. Program Objectives: The objective of this program is to establish or expand community learning centers that provide students with academic enrichment opportunities along with activities designed to complement the students’ regular academic program.

II. Program Procedures: I. ESEA Flexibility is Referenced II. Source of Governing RequirementIII. Availability of other Program Information

III. Compliance RequirementsBrustein & Manasevit, PLLC 39

PART 6: Internal Control Five Components of Internal Control that

should reasonably assure compliance with the requirements of Federal laws,

regulations and program compliance requirements

• Control Environment • Risk Assessment • Control Activities • Information and Communication • Monitoring Brustein & Manasevit, PLLC 40

2014 Compliance Supplement

Changes from the 2013 Version

What are the next steps for the Compliance

Supplement?

The GAO Yellow Book

Generally Accepted Government Auditing Standards

Who does it apply to?

• Single auditors• OIG auditors

Brustein & Manasevit, PLLC 44

Why is the Yellow Book Important?

“We conducted this audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objective.” LAUSD OIG Audit report

Noncompliance with the auditing standards may result in failure to establish prima facie case (case dismissed!)

Colorado / Houston PDLs

Brustein & Manasevit, PLLC 45

Auditor Findings

How Often is the Yellow Book Updated and How is it Organized?

• Yellow book last updated in 2011• Organization

– Financial audits– Attestation engagements– Performance audits

Brustein & Manasevit, PLLC 47

High Standards for Auditors

High Standards for Auditors

Continued…

Assess condition or activity for threats to independence

Assess safeguard(s) effectiveness

Identify and apply safeguard(s)

Assess threat for significance

Is threat significant?

Threat identified?

Is threat eliminated or reduced to an acceptable level?

Yes

Yes

Document nature of threat and any safeguards applied

Yes

No

Independence impairment; do

not proceed

No

Is threat related to a nonaudit service?

Is the nonaudit service specifically prohibited in GAGAS paragraphs

3.36 or 3.49 through 3.58?No

No

Yes

Yes

Proceed

Proceed

Proceed

No

Conceptual Framework for Independence

Brustein & Manasevit, PLLC 50

Important Provisions

What may cause finding?

Internal control deficiencies Fraud and illegal acts AbuseViolations of contracts or grant agreements

Brustein & Manasevit, PLLC 51

What happens when an auditors identify findings?

•Condition •Effect •Cause •Criteria •Recommendation

Brustein & Manasevit, PLLC 52

EDGAR GEPA Audit Resolution and Enforcement

Brustein & Manasevit, PLLC 53

ED Programmatic Components (OCFO, OESE, OSERS, OPE, OCTAE)

• Review all external audits (OIG and Single Audits)

Brustein & Manasevit, PLLC 54

• Audits are recommendation to management

• Management sustains or rejects audit findings

Brustein & Manasevit, PLLC 55

• Management sustains audit liability in a Program Determination Letter (PDL)

Brustein & Manasevit, PLLC 56

Audit Violations Deemed Significant

Brustein & Manasevit, PLLC 57

Significant Violations

1. Time Distribution2. MOE3. Supplement, Not Supplant4. Unallowable Expenses

Brustein & Manasevit, PLLC 58

Significant Violations

5.Procurement Irregularity6.Ineligible Students7.Lack of Accountability for Equipment/Materials

Brustein & Manasevit, PLLC59

Significant Violations8. Lack of Appropriate Record

Keeping9. Record Retention Problems10.Late or no Submission of

Required Reports, Inaccuracies, Inconsistence

11.Audits of Subrecipient Unresolved

Brustein & Manasevit, PLLC 60

Significant Violations

12.Lack of Subrecipient Monitoring13.Drawdown before they are needed or more than 90 days after the end of funding period14.Large Carryover Balances15.Lack of valid, reliable or complete performance data

Brustein & Manasevit, PLLC 61

Triggers EDGAR / GEPA Procedures34 CFR Part 81

Brustein & Manasevit, PLLC 62

AUDIT DEFENSE AND RESOLUTION

Brustein & Manasevit, PLLC 63

Common Defenses

• Harm to the Federal interest• Equitable offset• Statute of limitations

Brustein & Manasevit, PLLC 64

Harm to the Federal Interest 34 CFR 81.32 and Appendix

• “A recipient that made an unallowable expenditure or otherwise failed to account properly for funds shall return an amount that is proportional to the extent of the harm its violation caused to an identifiable federal interest associated program…”

Brustein & Manasevit, PLLC 65

ALJ Decisions - Reconstruction• Application of the New York State

Department of Education (April 21, 1995)– After-the-fact affidavits and other pertinent

documentation are admissible as evidence.• Consolidated Appeals of the Florida

Department of Education (June 26, 1990)– Accepted affidavits completed by

supervisors years later as credible and useful evidence.

Brustein & Manasevit, PLLC 66

Equitable Offset

In effect, an equitable offset permits the substitution of any costs paid under the grant that are subsequently disallowed with otherwise allowable expenditures paid by the grantee, and thereby reduces or eliminates a liability due to ED.

Application of Pittsburg Pre-School Community Council, Docket No 09-20-R,

May 16, 2012

Brustein & Manasevit, PLLC 67

Statute of LimitationsNo recipient under an applicable program shall be liable to return funds which were expended in a manner not authorized by law more than 5 years before the recipient received written notice of a preliminary departmental decision.

20 USC 1234a(k); 34 CFR 81.31(c)

For purposes of measuring the statute of limitations, funds are “expended” as of the date of obligation.

Brustein & Manasevit, PLLC 68

DisclaimerThis presentation is intended solely to provide general information and does not constitute legal advice or a legal service. This presentation does not create a client-lawyer relationship with Brustein & Manasevit, PLLC and, therefore, carries none of the protections under the D.C. Rules of Professional Conduct. Attendance at this presentation, a later review of any printed or electronic materials, or any follow-up questions or communications arising out of this presentation with any attorney at Brustein & Manasevit, PLLC does not create an attorney-client relationship with Brustein & Manasevit, PLLC. You should not take any action based upon any information in this presentation without first consulting legal counsel familiar with your particular circumstances.

Brustein & Manasevit, PLLC 69