audit firm size, industry specialization and earnings management

TRANSCRIPT

Tax Consulting and Reported Weaknesses in Internal Control

Randy ElderRandy ElderSyracuse UniversitySyracuse University

David HarrisDavid HarrisSyracuse UniversitySyracuse University

Jian ZhouJian ZhouSUNYSUNY--BinghamtonBinghamton

OutlineOutline

Broad perspective on Broad perspective on nonauditnonaudit servicesservicesPrevious literature and motivationPrevious literature and motivationHypothesesHypothesesData and resultsData and results

Why Examine Tax Why Examine Tax ConsultingConsulting??

PCAOB considered prohibiting tax consultingPCAOB considered prohibiting tax consulting–– Tax consulting issues at E&Y with Sprint, and KPMG Tax consulting issues at E&Y with Sprint, and KPMG

tax shelterstax shelters–– PCAOB restricted provision of abusive shelters and PCAOB restricted provision of abusive shelters and

consulting for key executivesconsulting for key executives

Tax Tax consulting consulting is a significant type of is a significant type of nonauditnonauditserviceservice and the eand the effect of ffect of nonauditnonaudit servicesservicesremainremain unresolvedunresolved

BackgroundBackgroundSOX codifies existing provisionsSOX codifies existing provisions–– Not all services are prohibitedNot all services are prohibited–– Only applies to public company audit clientsOnly applies to public company audit clients

Big 4 are still in the gameBig 4 are still in the game–– Deloitte still has a consulting practiceDeloitte still has a consulting practice–– KPMG advisory revenues grew 30% last yearKPMG advisory revenues grew 30% last year–– PwC will likely expand services after nonPwC will likely expand services after non--compete compete

expiresexpires–– Tax still a significant revenue sourceTax still a significant revenue source

Background TheoryBackground Theory

Audit QualityAudit Quality ((DeAngeloDeAngelo 1981) 1981) –– joint joint probability that auditor probability that auditor

will:will:–– Detect a misstatement (technical ability)Detect a misstatement (technical ability)–– Report the misstatement (independence)Report the misstatement (independence)

Tests have focused on independenceTests have focused on independence–– This has been especially true of effect of This has been especially true of effect of

nonauditnonaudit services services

Arguments for/against consultingArguments for/against consulting

ProPro –– Consulting services provide Consulting services provide knowledge spilloversknowledge spillovers–– Reduces cost of auditing and/or consulting Reduces cost of auditing and/or consulting

(efficiency)(efficiency)–– Provides knowledge useful to performance of Provides knowledge useful to performance of

auditing and/or consultingauditing and/or consultingConCon –– Consulting revenues increases the Consulting revenues increases the auditors economic dependence on the auditors economic dependence on the client, reducing auditor independenceclient, reducing auditor independence

Consulting and IndependenceConsulting and IndependenceEnron famously paid Andersen $52 million in 2000 Enron famously paid Andersen $52 million in 2000 -- $25 million for audit and $27 million for consulting$25 million for audit and $27 million for consultingHowever, pHowever, preponderance of research does not find reponderance of research does not find that nonthat non--audit services impairs independenceaudit services impairs independenceWhy this doesn’t matterWhy this doesn’t matter–– Concern is with both independence in fact and Concern is with both independence in fact and

appearanceappearance–– Consulting created appearance that independence was Consulting created appearance that independence was

impairedimpaired–– Therefore, finding of nonTherefore, finding of non--impairment probably not impairment probably not

sufficient to change status quo sufficient to change status quo

Independence evidence:Independence evidence: eearnings arnings mmanagementanagement

Conflicting results on the relationship between Conflicting results on the relationship between nonnon--audit service and auditor independence audit service and auditor independence measured by earnings management measured by earnings management –– Frankel et al. (2002) find a positive relation between Frankel et al. (2002) find a positive relation between

nonnon--audit services and earnings managementaudit services and earnings management–– Ferguson et al. (2004) also find for U.K. Ferguson et al. (2004) also find for U.K. Firms.Firms.–– Several U.S. studies find no relationSeveral U.S. studies find no relation

AshbaughAshbaugh et al. (2003)et al. (2003)Chung and Chung and KallapurKallapur (2003)(2003)Reynolds et al. (2002)Reynolds et al. (2002)Francis and Ke (2002)Francis and Ke (2002)

IIndependence ndependence eevidencevidence: other : other aspectsaspects

No evidence that No evidence that nonauditnonaudit services services affected propensity to issue going concern affected propensity to issue going concern opinions (opinions (DeFondDeFond et al. 2002)et al. 2002)

Little evidence that restatements are Little evidence that restatements are related to related to nonauditnonaudit services (Kinney et al. services (Kinney et al. 2004)2004)

Knowledge Spillovers Knowledge Spillovers -- PerformancePerformance

Audit firms argue that nonAudit firms argue that non--audit services:audit services:–– Can be performed at lower costCan be performed at lower cost–– Also allows for more effective performance of Also allows for more effective performance of

both servicesboth servicesPerformance data (or evidence of lower Performance data (or evidence of lower fees) will be necessary to justify change in fees) will be necessary to justify change in status quostatus quo

Knowledge Spillovers and FeesKnowledge Spillovers and Fees

SimunicSimunic (1984) identifies various plausible relations (1984) identifies various plausible relations between audit and between audit and nonauditnonaudit service feesservice fees

Audit Fee Consulting FeeAudit Fee Consulting Fee

Fixed cost Fixed costFixed cost Fixed costVariable cost Variable costVariable cost Variable cost

Knowledge Spillovers and FeesKnowledge Spillovers and Fees

Key PointsKey Points–– Early studies found positive relation between audit Early studies found positive relation between audit

and and nonauditnonaudit feesfees–– WhisenantWhisenant et al. (2003) find no significant relation et al. (2003) find no significant relation

using simultaneous equations of audit and using simultaneous equations of audit and nonauditnonauditfees, indicating no knowledge spilloversfees, indicating no knowledge spillovers

–– Little evidence that using your auditor for consulting Little evidence that using your auditor for consulting results in lower fees, although this is counterintuitiveresults in lower fees, although this is counterintuitive

–– Studies do not consider acquisition costs to clientStudies do not consider acquisition costs to client

Evidence from Evidence from Tax ServicesTax Services

Kinney et al. (2004) find some evidence Kinney et al. (2004) find some evidence that restatements are negatively related to that restatements are negatively related to tax servicestax servicesGleason and Mills (2007) find that Gleason and Mills (2007) find that auditorauditor--provided tax services are associated with provided tax services are associated with more accurate estimates of tax expensemore accurate estimates of tax expense–– Consistent with knowledge spillover and Consistent with knowledge spillover and

contrary to concerns about independence contrary to concerns about independence failurefailure

Internal Control ReportingInternal Control Reporting

Section 404 reports on internal control Section 404 reports on internal control provide a new reporting environment to provide a new reporting environment to test for potential lack of independence and test for potential lack of independence and knowledge spilloversknowledge spillovers

H1: There is no association between tax H1: There is no association between tax consulting and taxconsulting and tax--related related ICWsICWs

H2: There is no association between tax H2: There is no association between tax consulting and other consulting and other ICWsICWs

Possible Patterns of ResultsPossible Patterns of ResultsEffect of Tax Consulting on Effect of Tax Consulting on ICWsICWs

Tax nonTax non--TaxTaxICWsICWs ICWsICWs InterpretationInterpretation

-- None Knowledge SpilloversNone Knowledge Spillovers

-- -- Loss of independence Loss of independence oror

SelfSelf--selection by high selection by high quality firms quality firms

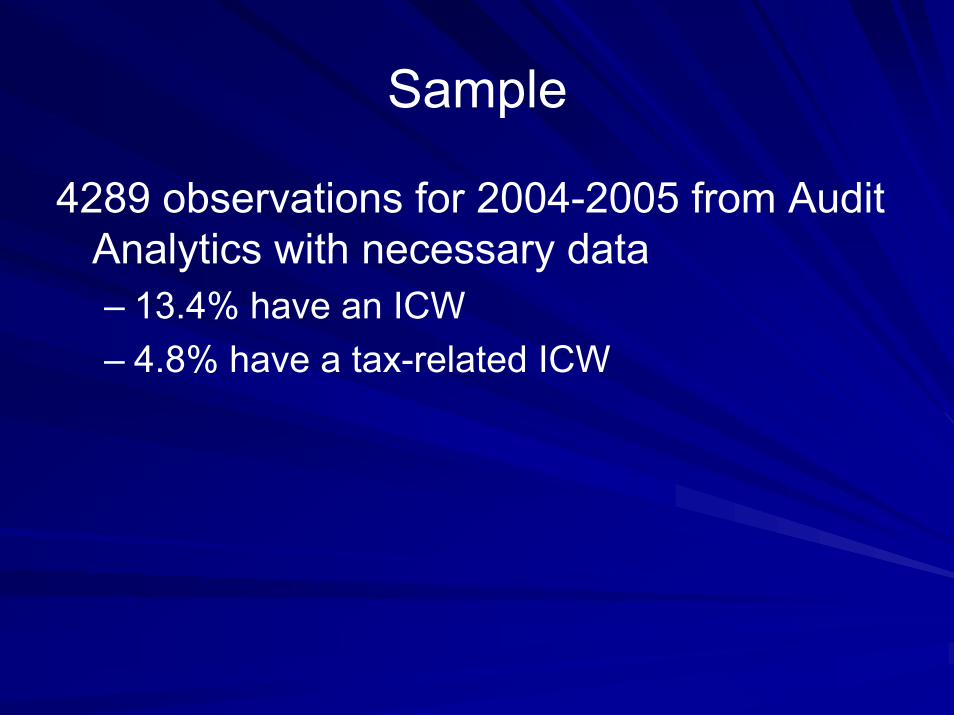

Sample

4289 observations for 2004-2005 from Audit Analytics with necessary data– 13.4% have an ICW– 4.8% have a tax-related ICW

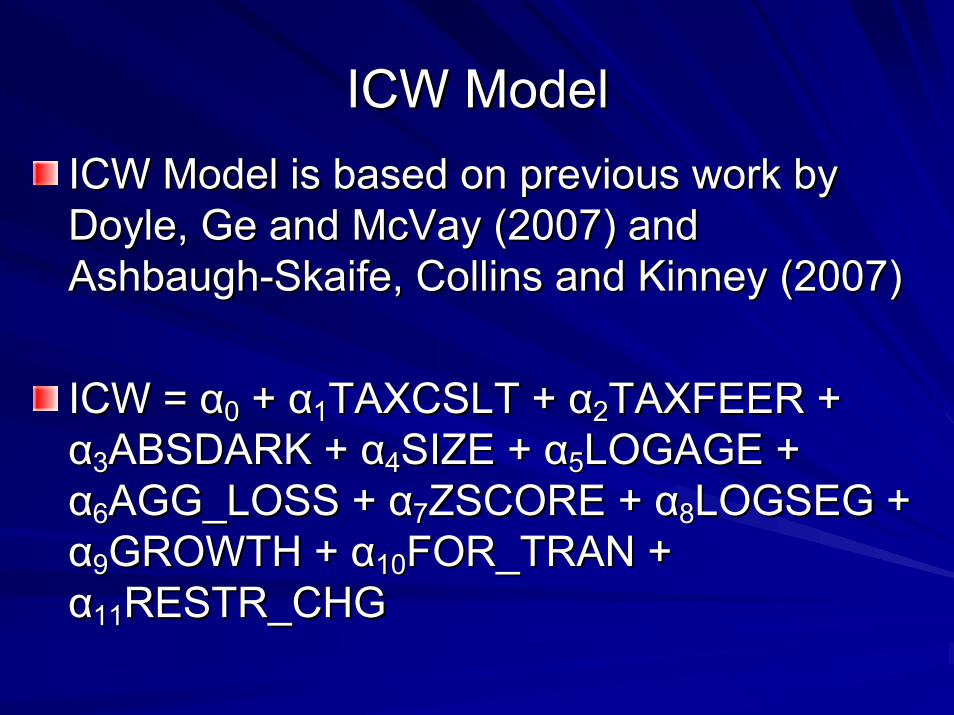

ICW ModelICW ModelICW Model is based on previous work by ICW Model is based on previous work by Doyle, Doyle, GeGe and and McVayMcVay (2007) and (2007) and AshbaughAshbaugh--SkaifeSkaife, , Collins and KinneyCollins and Kinney (2007)(2007)

ICW = ICW = αα00 + + αα11TAXCSLTTAXCSLT + + αα22TAXFEER + TAXFEER + αα33ABSDARK + ABSDARK + αα44SIZE + SIZE + αα55LOGAGE + LOGAGE + αα66AGG_LOSS + AGG_LOSS + αα77ZSCORE + ZSCORE + αα88LOGSEG + LOGSEG + αα99GROWTH + GROWTH + αα1010FOR_TRAN + FOR_TRAN + αα1111RESTR_CHG RESTR_CHG

VariablesVariablesICW: ICW: 1 if the firm has a material internal control weakness; 0 otherw1 if the firm has a material internal control weakness; 0 otherwise.ise.OTHICW:OTHICW: NonNon--taxtax--related ICW.related ICW.TAXICW:TAXICW: TaxTax--related ICW.related ICW.TAXFEER:TAXFEER: Ratio of taxRatio of tax--related fees to total fees.related fees to total fees.TAXCLST:TAXCLST: 1 if tax1 if tax--related fees are reported; 0 otherwise.related fees are reported; 0 otherwise.ABSDARK:ABSDARK: DecileDecile rank of the absolute value of discretionary accruals.rank of the absolute value of discretionary accruals.SIZE:SIZE: Most recent three years average market valueMost recent three years average market valueLOGAGE: LOGAGE: Log of the number of years that the company has CRSP data Log of the number of years that the company has CRSP data AGG_LOSS: AGG_LOSS: 1 if the sum of earnings before extraordinary items for year t a1 if the sum of earnings before extraordinary items for year t and nd

year tyear t--1 is less than zero, 0 otherwise. 1 is less than zero, 0 otherwise. ZSCORE:ZSCORE: Altman ZAltman Z--score measure of financial distress score measure of financial distress LOGSEG: LOGSEG: Log of number of operating and geographic segmentsLog of number of operating and geographic segmentsGROWTH:GROWTH: Most recent three years’ sales growthMost recent three years’ sales growthFOR_TRAN:FOR_TRAN: 1 if the company has non1 if the company has non--zero foreign currency translation in zero foreign currency translation in

year t, 0 otherwise. year t, 0 otherwise. RESTR_CHG:RESTR_CHG: Aggregate restructuring charges in year t and tAggregate restructuring charges in year t and t--1 scaled by 1 scaled by

market capitalization in year t.market capitalization in year t.

Table 1 – Descriptive Statistics

Variable Mean Std Dev Median

ICW 0.134 0.341 0.000

OTHICW 0.114 0.317 0.000

TAXICW 0.048 0.213 0.000

TAXFEER 0.090 0.099 0.058

TAXCSLT 0.822 0.383 1.000

ABSDARK 5.499 2.872 5.000

SIZE 3713.270 9846.350 739.746

LOGAGE 2.483 0.953 2.485

AGG_LOSS 0.244 0.429 0.000

ZSCORE 4.649 5.860 3.233

LOGSEG 1.317 0.961 1.386

GROWTH 0.211 0.408 0.117

FOR_TRAN 0.337 0.473 0.000

RESTR_CHG 0.005 0.016 0.000

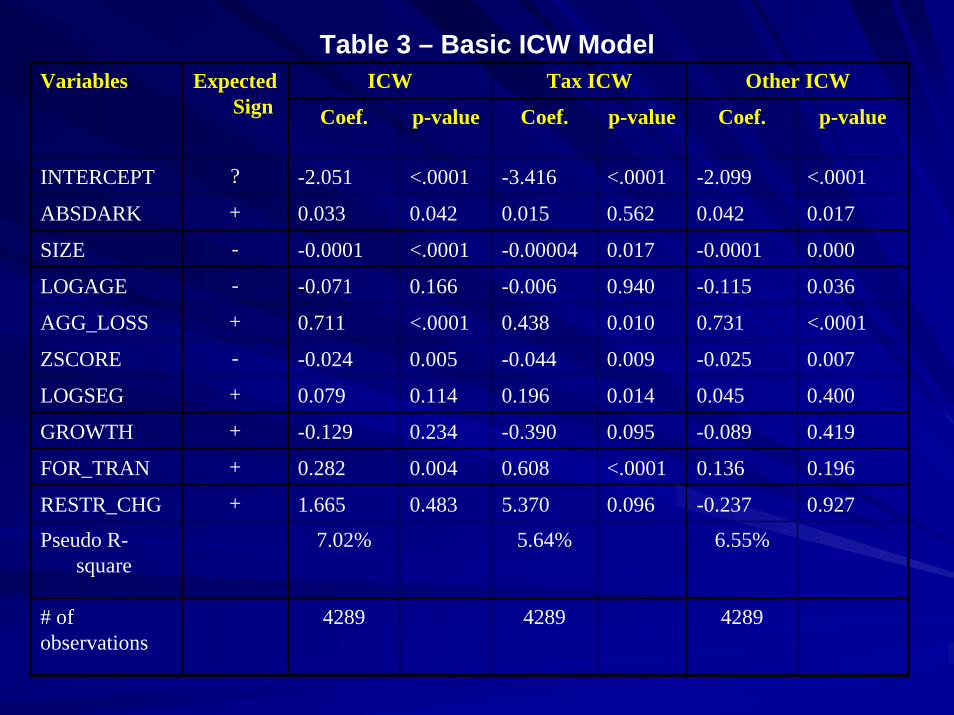

Table 3 – Basic ICW ModelICW Tax ICW Other ICW

Coef. p-value Coef. p-value Coef. p-value

INTERCEPT ? -2.051 <.0001 -3.416 <.0001 -2.099 <.0001

ABSDARK + 0.033 0.042 0.015 0.562 0.042 0.017

SIZE - -0.0001 <.0001 -0.00004 0.017 -0.0001 0.000

LOGAGE - -0.071 0.166 -0.006 0.940 -0.115 0.036

AGG_LOSS + 0.711 <.0001 0.438 0.010 0.731 <.0001

ZSCORE - -0.024 0.005 -0.044 0.009 -0.025 0.007

LOGSEG + 0.079 0.114 0.196 0.014 0.045 0.400

GROWTH + -0.129 0.234 -0.390 0.095 -0.089 0.419

FOR_TRAN + 0.282 0.004 0.608 <.0001 0.136 0.196

RESTR_CHG + 1.665 0.483 5.370 0.096 -0.237 0.927

Pseudo R-square

7.02% 5.64% 6.55%

# of observations

4289 4289 4289

Variables Expected Sign

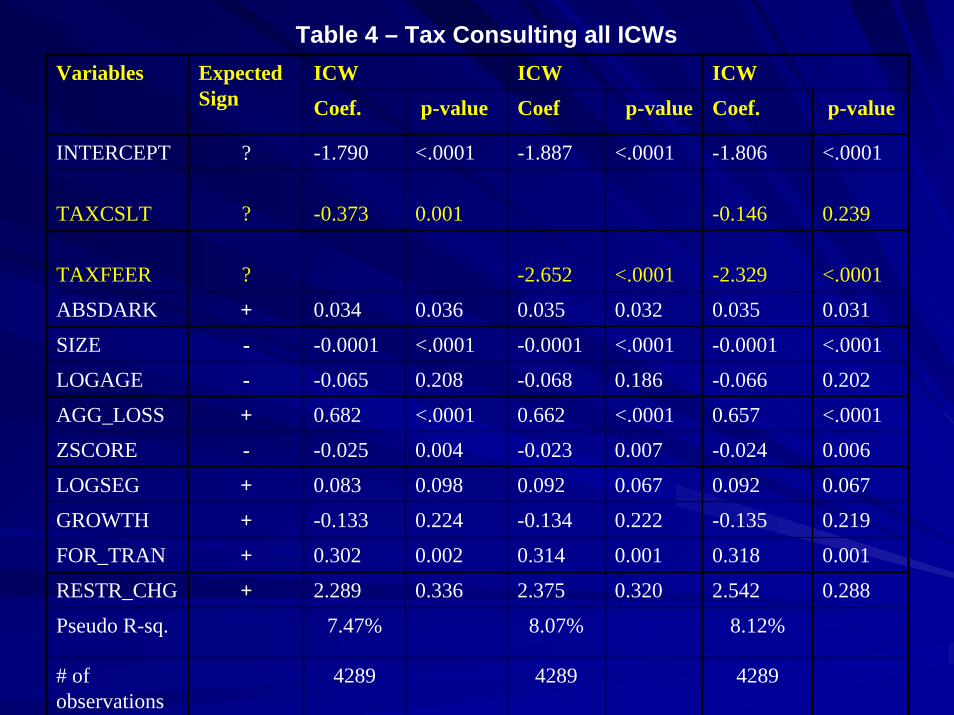

Table 4 – Tax Consulting all ICWsICW ICW ICW

Coef. p-value Coef p-value Coef. p-value

INTERCEPT ? -1.790 <.0001 -1.887 <.0001 -1.806 <.0001

TAXCSLT ? -0.373 0.001 -0.146 0.239

TAXFEER ? -2.652 <.0001 -2.329 <.0001

ABSDARK + 0.034 0.036 0.035 0.032 0.035 0.031

SIZE - -0.0001 <.0001 -0.0001 <.0001 -0.0001 <.0001

LOGAGE - -0.065 0.208 -0.068 0.186 -0.066 0.202

AGG_LOSS + 0.682 <.0001 0.662 <.0001 0.657 <.0001

ZSCORE - -0.025 0.004 -0.023 0.007 -0.024 0.006

LOGSEG + 0.083 0.098 0.092 0.067 0.092 0.067

GROWTH + -0.133 0.224 -0.134 0.222 -0.135 0.219

FOR_TRAN + 0.302 0.002 0.314 0.001 0.318 0.001

RESTR_CHG + 2.289 0.336 2.375 0.320 2.542 0.288

Pseudo R-sq. 7.47% 8.07% 8.12%

# of observations

4289 4289 4289

Variables Expected Sign

TAX ICW TAX ICW TAX ICW

Coeff. p-value Coeff. p-value Coeff. p-value

INTERCEPT ? -3.314 <.0001 -3.369 <.0001 -4.204 <.0001

TAXCSLT?

0.091 0.659 0.216 0.321

TAXFEER ? -1.636 0.049 -1.805 0.049 -0.642 0.494

OTHICW?

2.531 <.0001

ABSDARK + 0.016 0.543 0.016 0.543 -0.004 0.871

SIZE - -0.00004 0.020 -0.00004 0.019 -0.00002 0.126

LOGAGE - -0.003 0.970 -0.004 0.956 0.027 0.742

AGG_LOSS + 0.407 0.017 0.411 0.016 0.092 0.614

ZSCORE - -0.043 0.010 -0.043 0.010 -0.038 0.038

LOGSEG + 0.205 0.010 0.205 0.011 0.200 0.016

GROWTH + -0.398 0.090 -0.397 0.091 -0.471 0.066

FOR_TRAN + 0.629 <.0001 0.626 <.0001 0.605 0.000

RESTR_CHG + 5.769 0.074 5.663 0.081 5.772 0.108

Pseudo R-square 5.94% 5.95% 22.82%

# of observations 4289 4289 4289

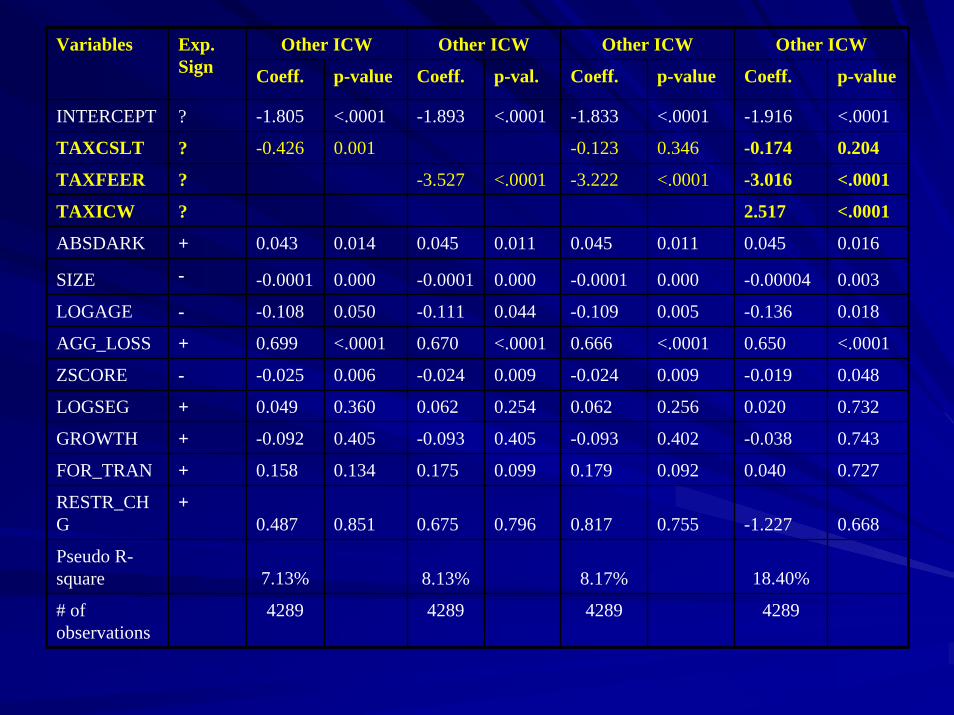

Variables Exp. Sign

Other ICW Other ICW Other ICW Other ICW

Coeff. p-value Coeff. p-val. Coeff. p-value Coeff. p-value

INTERCEPT ? -1.805 <.0001 -1.893 <.0001 -1.833 <.0001 -1.916 <.0001

TAXCSLT ? -0.426 0.001 -0.123 0.346 -0.174 0.204

TAXFEER ? -3.527 <.0001 -3.222 <.0001 -3.016 <.0001

TAXICW ? 2.517 <.0001

ABSDARK + 0.043 0.014 0.045 0.011 0.045 0.011 0.045 0.016

SIZE - -0.0001 0.000 -0.0001 0.000 -0.0001 0.000 -0.00004 0.003

LOGAGE - -0.108 0.050 -0.111 0.044 -0.109 0.005 -0.136 0.018

AGG_LOSS + 0.699 <.0001 0.670 <.0001 0.666 <.0001 0.650 <.0001

ZSCORE - -0.025 0.006 -0.024 0.009 -0.024 0.009 -0.019 0.048

LOGSEG + 0.049 0.360 0.062 0.254 0.062 0.256 0.020 0.732

GROWTH + -0.092 0.405 -0.093 0.405 -0.093 0.402 -0.038 0.743

FOR_TRAN + 0.158 0.134 0.175 0.099 0.179 0.092 0.040 0.727

RESTR_CHG

+0.487 0.851 0.675 0.796 0.817 0.755 -1.227 0.668

Pseudo R-square 7.13% 8.13% 8.17% 18.40%

# of observations

4289 4289 4289 4289

Variables Exp. Sign

Results

The extent, but not the existence of tax The extent, but not the existence of tax consulting is associated with a reduced consulting is associated with a reduced likelihood of a taxlikelihood of a tax--related ICW related ICW (but not after controlling for other ICW)The extent, but not the existence of tax The extent, but not the existence of tax consulting is also associated with a consulting is also associated with a reduced likelihood of nonreduced likelihood of non--tax tax ICWsICWsResults are more consistent with reduced Results are more consistent with reduced independence than knowledge spilloversindependence than knowledge spillovers

PlansPlans

Gathering data on the nature of the tax Gathering data on the nature of the tax ICWsICWsFurther sensitivity analysis based on the Further sensitivity analysis based on the extent of the tax consultingextent of the tax consultingUse path analysis to test whether both Use path analysis to test whether both independence effects (for firmindependence effects (for firm--level level ICW) and spillover effects (for tax ICW) ICW) and spillover effects (for tax ICW) existexist