attitudes towards programmatic advertising - a deep dive into buy-side attitudes and adoption

TRANSCRIPT

x

Attitudes towards Programmatic Advertising

September 2016

A deep dive into buy-side attitudes and adoption

x

CONTENT

Introduction

Summary

Programmatic is mainstream

Drivers, Barriers and Business Impacts

Current Adoption and Strategies

Measurement and Data Strategy

Future of Programmatic

Contact

The following report provides further insight into the buy-side (advertisers and agencies) attitudes and

current adoption of programmatic advertising following the full report publication. The additional

data in this report includes a breakdown of advertiser and agency respondents by regions as listed

below:

Central and Eastern Europe: Bulgaria, Croatia, Czech Republic, Hungary, Poland, Romania, Russia,

Serbia, Slovakia, Slovenia, Turkey

Northern Europe: Norway, Sweden, Denmark, Finland

Southern Europe: Spain, Italy, Portugal , Greece

Western Europe: UK, France, Germany, Belgium, Switzerland, Netherlands, Austria, Ireland

INTRODUCTION

x

Programmatic is mainstream – majority of all buy-side stakeholders are investing in programmatic

Programmatic is increasingly seen as a strategic component of media planning and not longer just a place for remnant inventory

Programmatic strategies evolve as market mature and buy-side stakeholders are experimenting with hybrid and in-house models, however clients outsourcing to an agency still dominates

Buy-side stakeholders view skills and training as a key barrier to programmatic investment

The future of programmatic looks bright – the majority of buy-side stakeholders plan to increase their investment over the next 12 months

SUMMARY

PROGRAMMATIC IS MAINSTREAM

PROGRAMMATIC IS MAINSTREAM

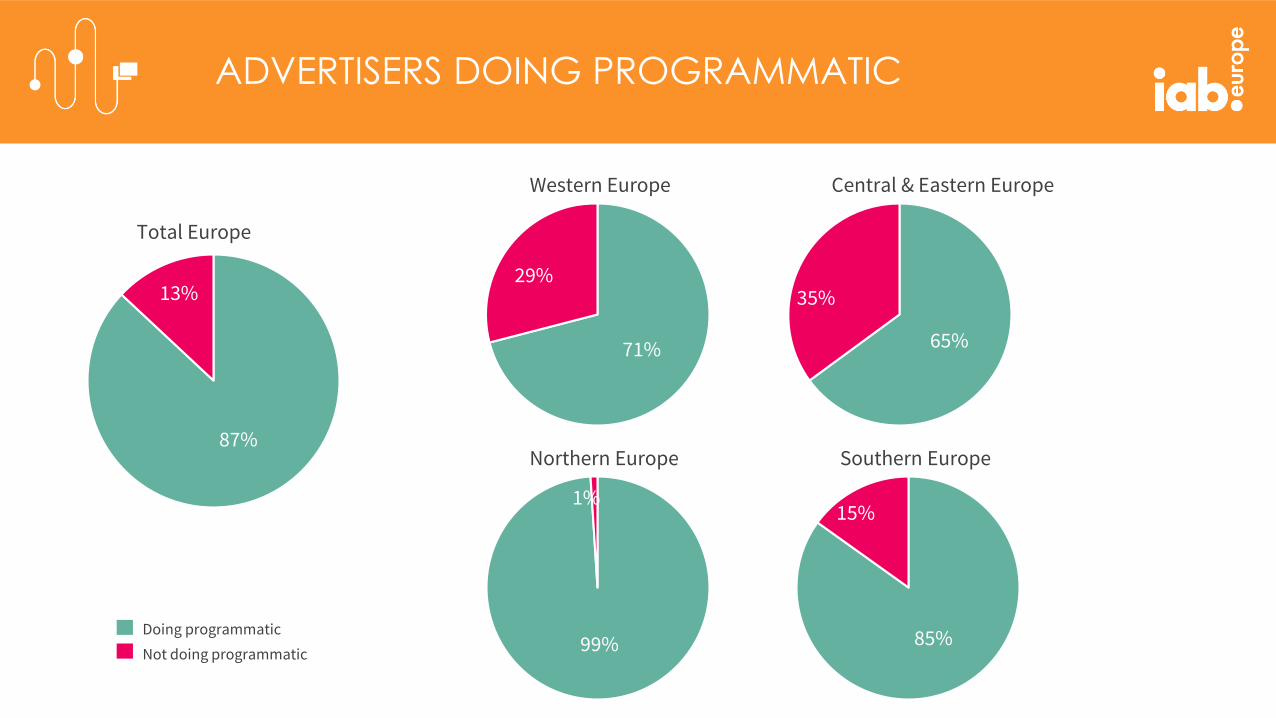

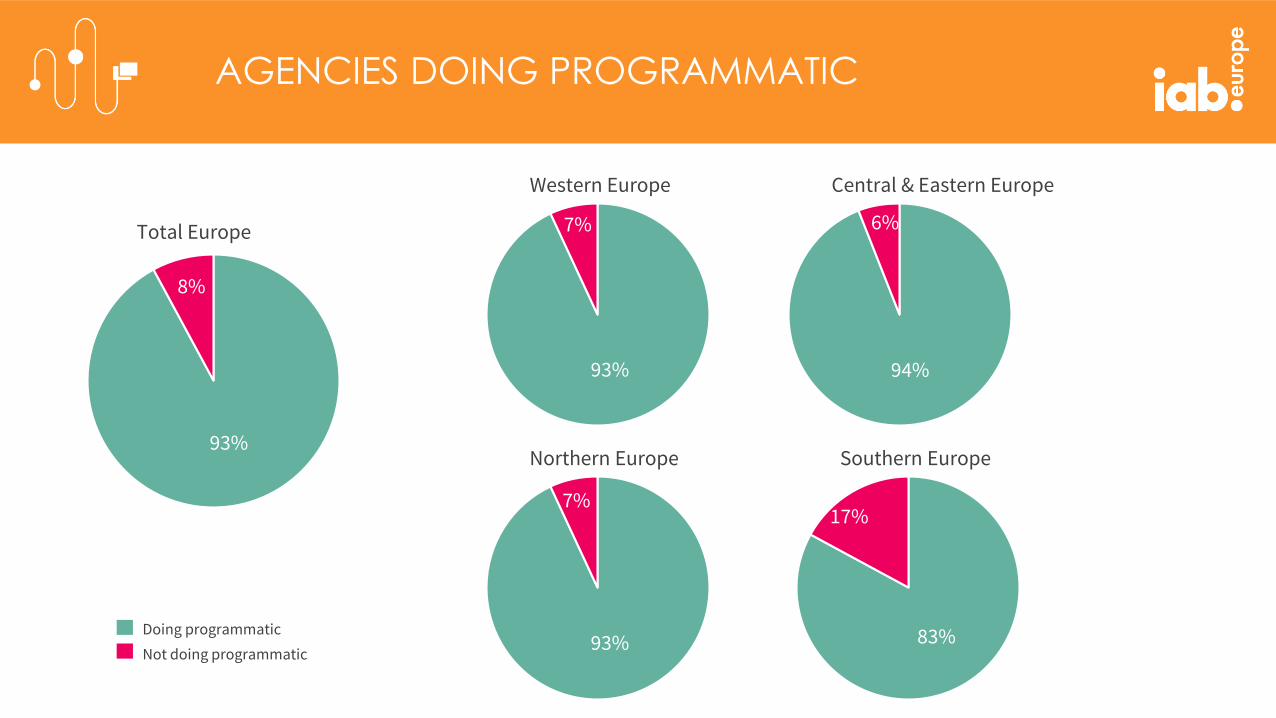

The survey highlights that programmatic is now mainstream - all buy-side stakeholders surveyed are investing in digital and now most are also deploying some form of programmatic advertising - 87% of advertisers, 93% of agencies.

Whilst almost everyone is investing in programmatic now the majority of buying and selling is still manual. Over two thirds of agencies state that more than 20% of this digital advertising is traded via manual processes.

ADVERTISERS DOING PROGRAMMATIC

87%

13%

Total Europe

Not doing programmatic

Doing programmatic

71%

29%

Western Europe

65%

35%

Central & Eastern Europe

99%

1%

Northern Europe

85%

15%

Southern Europe

AGENCIES DOING PROGRAMMATIC

93%

8%

Total Europe

Not doing programmatic

Doing programmatic

93%

7%

Western Europe

94%

6%

Central & Eastern Europe

93%

7%

Northern Europe

83%

17%

Southern Europe

PROGRAMMATIC DRIVERS, BARRIERS AND BUSINESS

IMPACTS

EFFICIENCY AND COST ARE DOMINANT IN

DRIVING BUY-SIDE ADOPTION

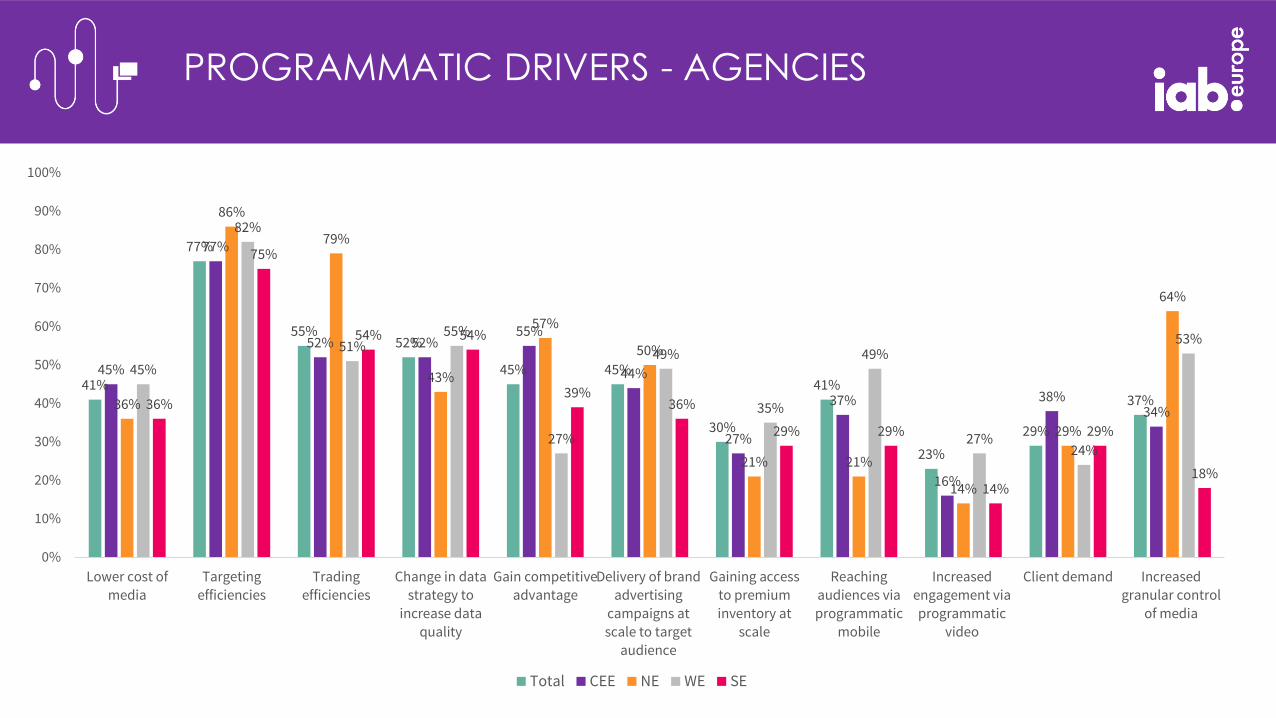

Gaining efficiencies stood out as a key motivation for the industry to invest in programmatic in 2015, this driver is still dominant in 2016 particularly for buy-side stakeholders. Advertisers and agencies seek targeting efficiencies, agencies also want to gain trading and operational efficiencies.

Mobile wasn’t factored highly in 2015, however now almost a third of advertisers and over 40% of agencies are investing in programmatic to reach mobile audiences. Programmatic video is also considered highly by advertisers in Western Europe and is creeping onto the agenda of those in CEE markets.

Delivery of brand advertising campaigns at scale is also important to advertisers, especially in the Northern and Western European markets.

PROGRAMMATIC DRIVERS - ADVERTISERS

53%

76%

29% 30%26%

49%

22%

30%

19%23%

68%

74%

26%21%

16%

37%

5%

21%

16% 16%

33%

67%

0% 0%

33%

67%

0% 0% 0%

33%

64%

71%

43%

50%

29%

57%

14%

29%

36%

14%

27%

82%

9%

36%

27%

45%

27%

45%

9%

0%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Lower cost of

media

Targeting

efficiencies

Trading

efficiencies

Change in data

strategy to

increase data

quality

Gain competitive

advantage

Delivery of brand

advertising

campaigns at

scale to target

audience

Gaining access to

premium

inventory at scale

Reaching

audiences via

programmatic

mobile

Increased

engagement via

programmatic

video

Increased granular

control of media

Total CEE NE WE SE

PROGRAMMATIC DRIVERS - AGENCIES

41%

77%

55%52%

45% 45%

30%

41%

23%

29%

37%

45%

77%

52% 52%55%

44%

27%

37%

16%

38%34%

36%

86%

79%

43%

57%

50%

21% 21%

14%

29%

64%

45%

82%

51%55%

27%

49%

35%

49%

27%24%

53%

36%

75%

54% 54%

39%36%

29% 29%

14%

29%

18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Lower cost of

mediaTargeting

efficienciesTrading

efficienciesChange in data

strategy to

increase data

quality

Gain competitive

advantageDelivery of brand

advertising

campaigns at

scale to target

audience

Gaining access

to premium

inventory at

scale

Reaching

audiences via

programmatic

mobile

Increased

engagement via

programmatic

video

Client demand Increased

granular control

of media

Total CEE NE WE SE

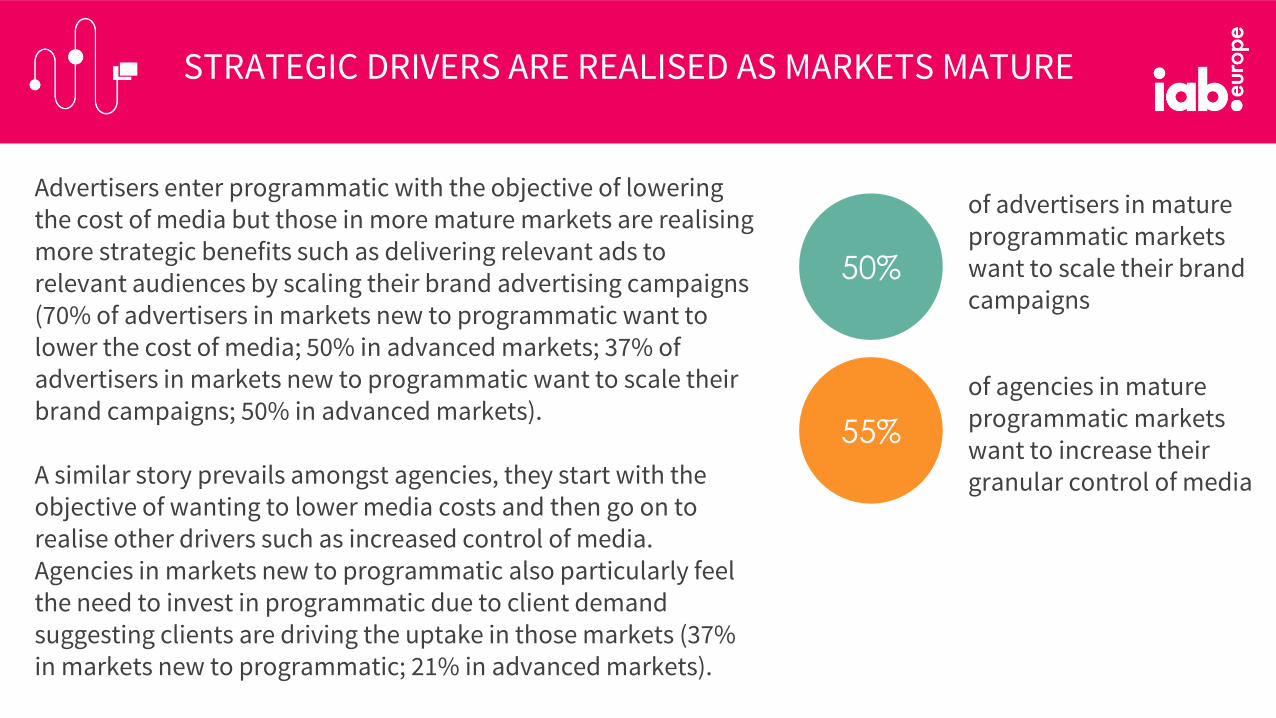

50%

of advertisers in mature programmatic markets want to scale their brand campaigns

of agencies in mature programmatic markets want to increase their granular control of media

Advertisers enter programmatic with the objective of lowering the cost of media but those in more mature markets are realising more strategic benefits such as delivering relevant ads to relevant audiences by scaling their brand advertising campaigns (70% of advertisers in markets new to programmatic want to lower the cost of media; 50% in advanced markets; 37% of advertisers in markets new to programmatic want to scale their brand campaigns; 50% in advanced markets).

A similar story prevails amongst agencies, they start with the objective of wanting to lower media costs and then go on to realise other drivers such as increased control of media. Agencies in markets new to programmatic also particularly feel the need to invest in programmatic due to client demand suggesting clients are driving the uptake in those markets (37% in markets new to programmatic; 21% in advanced markets).

55%

STRATEGIC DRIVERS ARE REALISED AS MARKETS MATURE

SUCCESS IN PROGRAMMATIC DEMANDS THE

RIGHT EXPERTISE

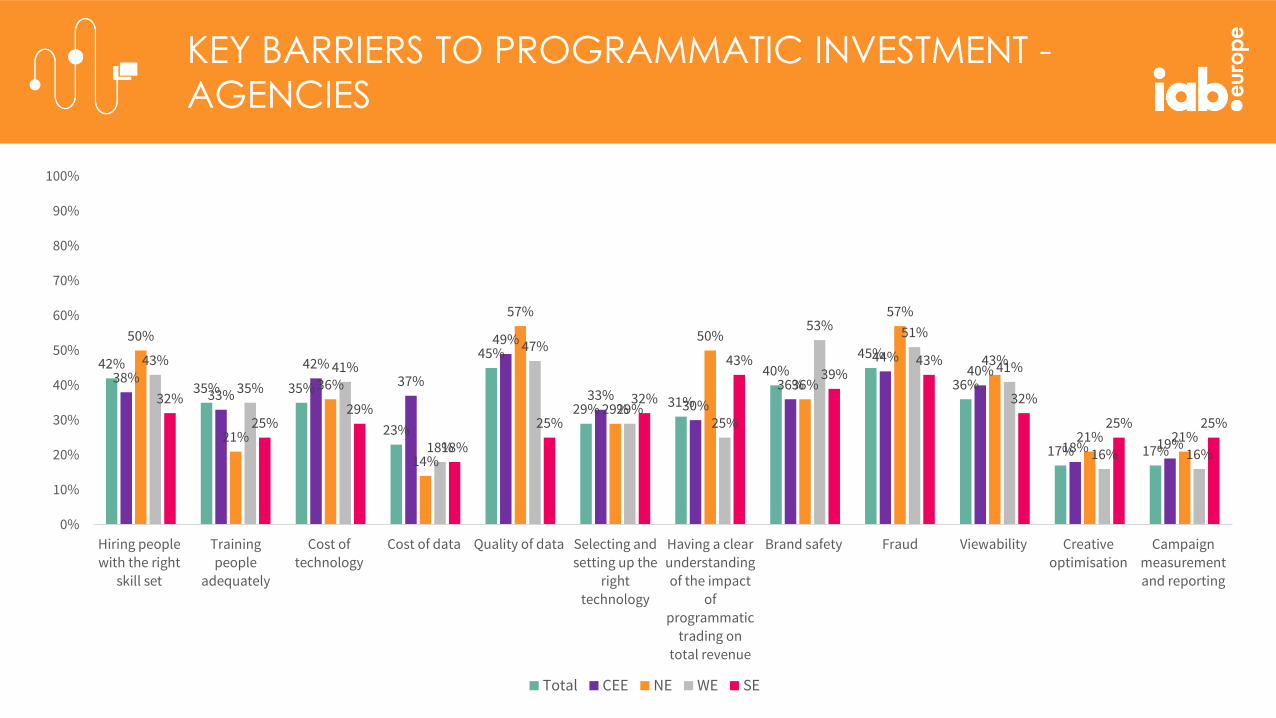

Skills and hiring people with the right skillset are still key barriers to investing in programmatic suggestingthat stakeholders have some way to go in finding people with the right skills and implementing trainingprograms.

Buy-side stakeholders are also concerned with many of the industry’s hot topics: data quality; fraud; brandsafety and viewability, particularly those in Northern Europe. Agencies perceive fraud as a higher risk thando advertisers and so this may be why they are taking more proactive steps with data (see section 6)

Advertisers in Western Europe perceive with campaign measurement and reporting as a barrier suggestingthey want to see improvements in this area.

KEY BARRIERS TO PROGRAMMATIC INVESTMENT -

ADVERTISERS

31%

21% 20% 19%

37%

27%31% 30%

26%30%

17%

27%

37%

26% 26%

11%

32%

26% 26%21%

16%

26%

11%

26%

33%

0% 0% 0% 0% 0%

33% 33% 33%

100%

33%

0%

21% 21% 21%

14%

57%

29%

21% 21%

36%

29%

21%

43%

9%

18%

0%

18%

36%

27% 27% 27%

18%

36%

9%

27%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Hiring people

with the right

skill set

Training

people

adequately

Cost of

technology

Cost of data Quality of data Selecting and

setting up the

right

technology

Having a clear

understanding

of the impact

of

programmatic

trading on total

revenue

Brand safety Fraud Viewability Creative

optimisation

Campaign

measurement

and reporting

Total CEE NE WE SE

KEY BARRIERS TO PROGRAMMATIC INVESTMENT -

AGENCIES

42%

35% 35%

23%

45%

29% 31%

40%45%

36%

17% 17%

38%33%

42%37%

49%

33%30%

36%

44%40%

18% 19%

50%

21%

36%

14%

57%

29%

50%

36%

57%

43%

21% 21%

43%

35%

41%

18%

47%

29%25%

53% 51%

41%

16% 16%

32%

25%29%

18%

25%

32%

43%39%

43%

32%

25% 25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Hiring people

with the right

skill set

Training

people

adequately

Cost of

technology

Cost of data Quality of data Selecting and

setting up the

right

technology

Having a clear

understanding

of the impact

of

programmatic

trading on

total revenue

Brand safety Fraud Viewability Creative

optimisation

Campaign

measurement

and reporting

Total CEE NE WE SE

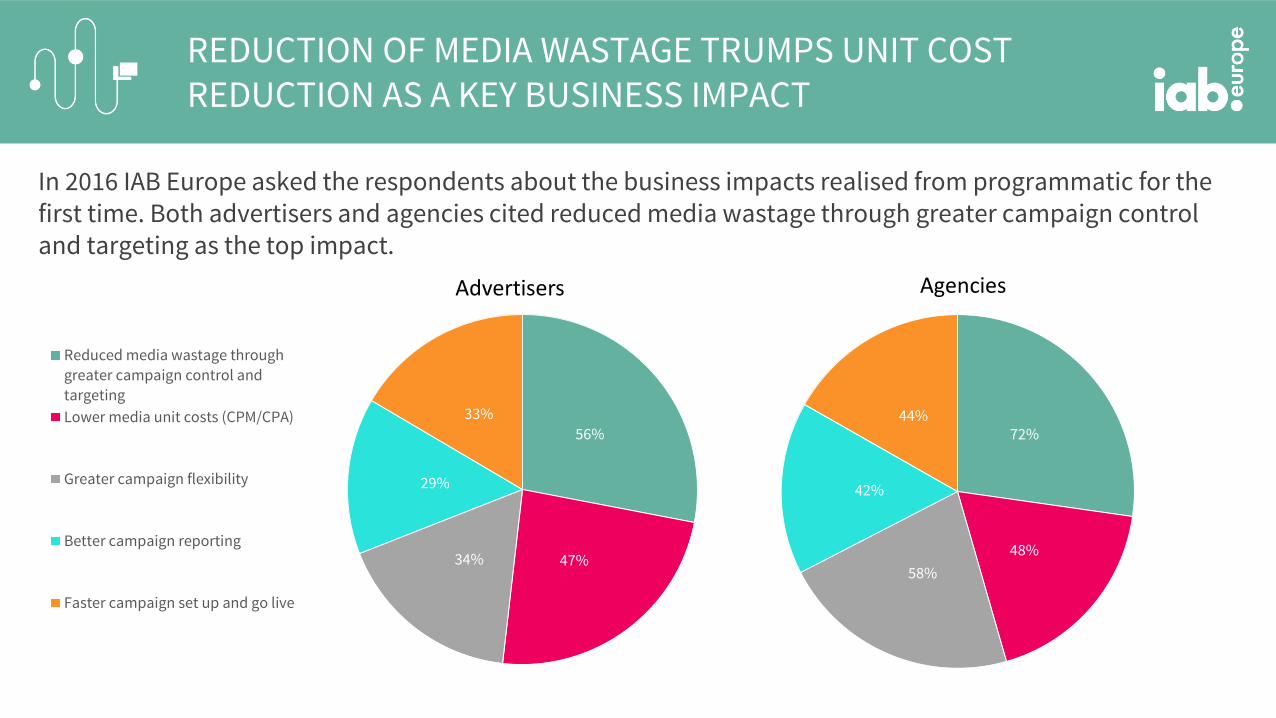

REDUCTION OF MEDIA WASTAGE TRUMPS UNIT COST REDUCTION AS A KEY BUSINESS IMPACT

In 2016 IAB Europe asked the respondents about the business impacts realised from programmatic for the first time. Both advertisers and agencies cited reduced media wastage through greater campaign control and targeting as the top impact.

56%

47%34%

29%

33%

Reduced media wastage through

greater campaign control and

targeting

Lower media unit costs (CPM/CPA)

Greater campaign flexibility

Better campaign reporting

Faster campaign set up and go live

72%

48%

58%

42%

44%

Advertisers Agencies

CURRENT ADOPTION & STRATEGIES

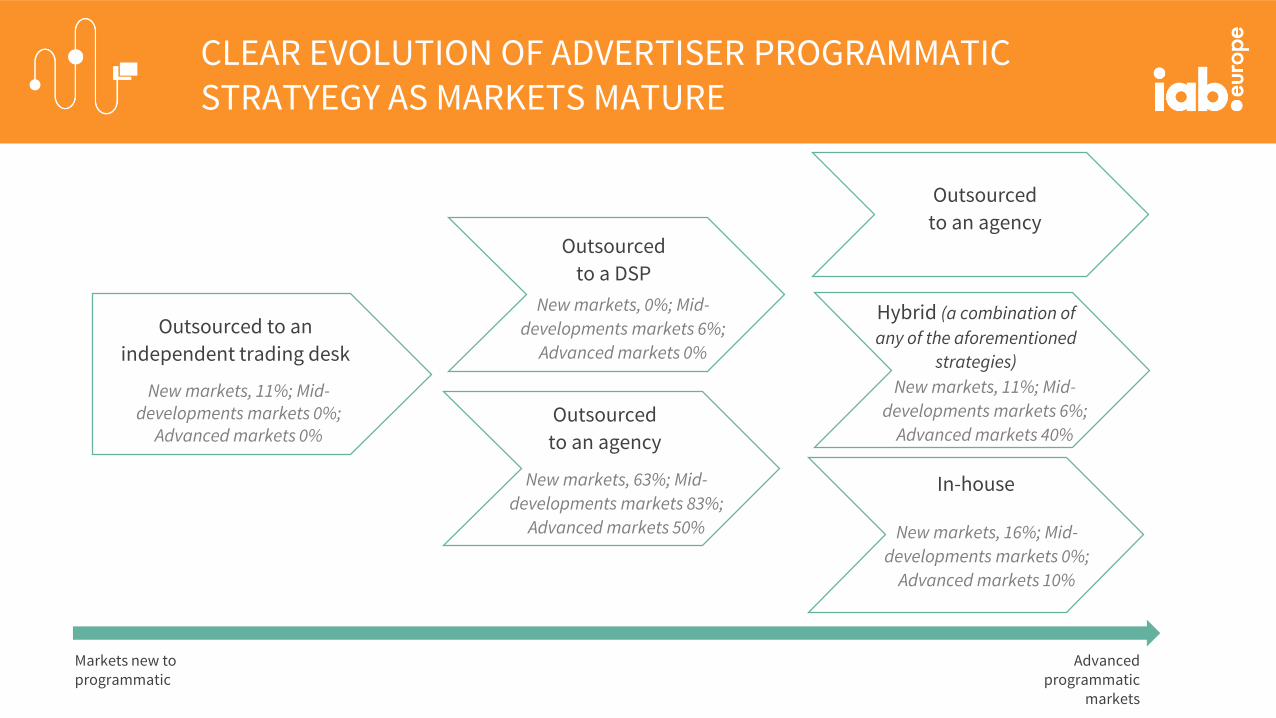

CLEAR EVOLUTION OF ADVERTISER PROGRAMMATIC STRATYEGY AS MARKETS MATURE

The survey showed us that there is a clear evolution of advertiser programmatic strategy as markets mature

Buyers start with an independent specialist perhaps looking for an independent managed service with flexibility and control, then move to an agency or DSP to provide a managed service with media buying expertise and finally in mature markets end up with an agency or hybrid model, but in the main still rely on agencies. More information on these operational models can be found in section 2.2 of the IAB Europe Road to Programmatic white paper.

Despite the challenges to the agency trading desk model, for example advertiser in-house buying, it remains the predominant way in which agencies build the skills to execute programmatic buying effectively, almost a third do have a hybrid model suggesting the trading desks will become part of a wider programmatic strategy. Advertisers in Northern Europe are more likely to experiment with a hybrid model. Agencies are more likely to use a DSP or independent trading desk than advertisers directly.

Outsourced to an

independent trading desk

Outsourced

to a DSP

Outsourced

to an agency

Outsourced

to an agency

Hybrid (a combination of

any of the aforementioned

strategies)

In-house

Markets new to programmatic

Advanced programmatic

markets

New markets, 11%; Mid-developments markets 0%;

Advanced markets 0%

New markets, 0%; Mid-

developments markets 6%;

Advanced markets 0%

New markets, 63%; Mid-

developments markets 83%;

Advanced markets 50%

New markets, 11%; Mid-

developments markets 6%;

Advanced markets 40%

New markets, 16%; Mid-

developments markets 0%;

Advanced markets 10%

CLEAR EVOLUTION OF ADVERTISER PROGRAMMATIC STRATYEGY AS MARKETS MATURE

OPERATIONAL MODELS - ADVERTISERS

Graphs showing operational models by market

63%

3%1%

16% 16%

63%

11%

0%

16%

11%

33%

0% 0% 0%

67%64%

0% 0%

14%

21%

91%

0%

9%

0% 0%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Outsourced to an agency Outsourced to an independent

trading deskOutsourced to a DSP In-house operations Hybrid model (more than one of the

above)

Total CEE NE WE SE

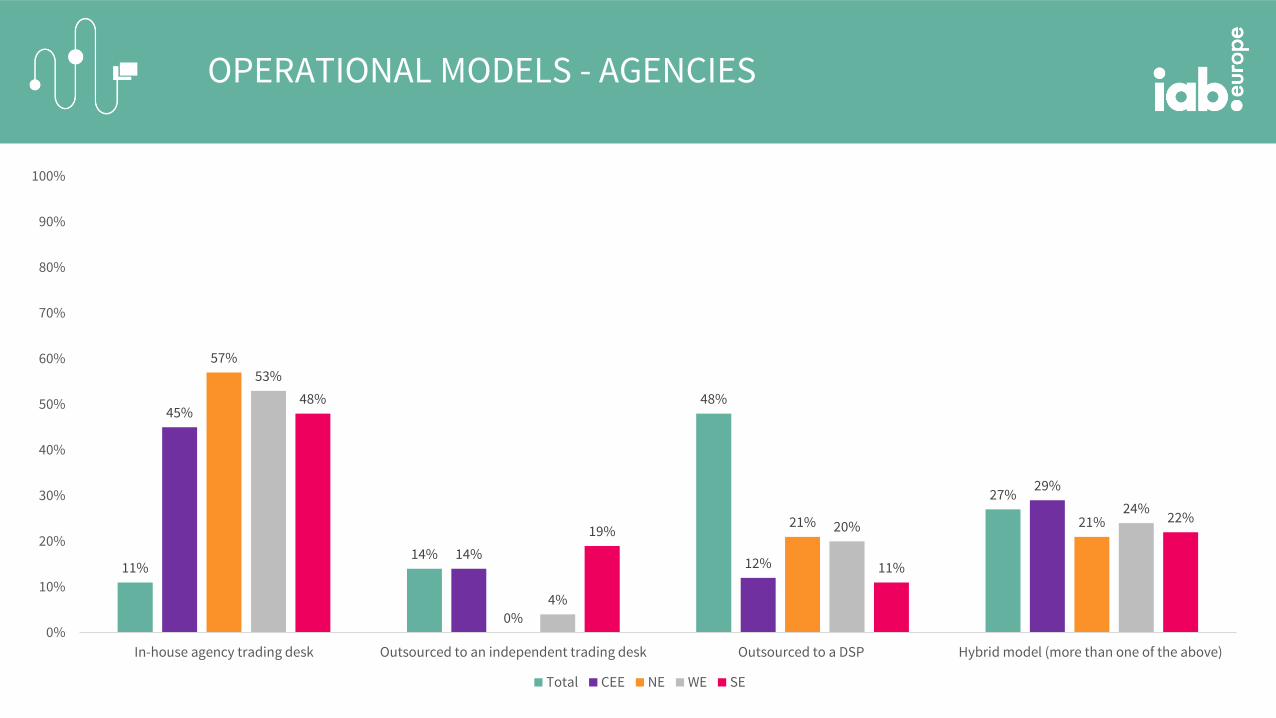

OPERATIONAL MODELS - AGENCIES

11%14%

48%

27%

45%

14%12%

29%

57%

0%

21% 21%

53%

4%

20%24%

48%

19%

11%

22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

In-house agency trading desk Outsourced to an independent trading desk Outsourced to a DSP Hybrid model (more than one of the above)

Total CEE NE WE SE

IAB Europe wanted to understand whether those stakeholders who do not currently have an in-house model areconsidering one and what were their reasons for doing so or not doing so.

Almost three quarters of agencies who do not currently have an in-house model are considering one, as they migrateaway from I/O media buying.

Advertisers continue to rely on their agencies; three quarters of advertisers who do not currently have an in-housemodel are not considering one, this has increased from 54% in 2015. Interestingly though, those that are consideringin-house are most likely doing so to reduce agency costs. However in-house is more likely to be considered byadvertisers in advanced markets; 67% of advertisers in advanced markets are considering an in-house model but only12% of those in markets new to programmatic share this view.

OPERATIONAL MODELS ARE CHANGING

Bringing programmatic in-house means full control over what happens with our

most valuable good: the data of our customers. Setting up an in-house solution first

and foremost requires education on programmatic, in order to get the various

functions that need to be involved on board. Once the set-up is complete, it is a

great way to foster cross-functional collaboration while providing our customers

with personalised advertising

Henrik Schulte,

Media Strategy Manager EMEA, Schneider Electric

We are migrating programmatic expertise into client teams as programmatic

evolves from point solutions on a plan to the method to execute a consumer

centric communication plan. We still focus on the same questions, of whom do we

want to reach, what do we want to achieve, how do we measure success, which

message and format will resonate and which media placements have the highest

impact – but now we answer those questions in much more granular buying

decisions, based on much more data and leveraging much more sophisticated tools.

Oliver Gertz, Managing Director Interaction, EMEA and

Programmatic Lead Global Clients , Mediacom

MEASUREMENT AND DATA STRATEGY

PROGRAMMATIC IS A KEY ELEMENT OF MEDIA PLANNING

75% 70%

Advertisers Agencies

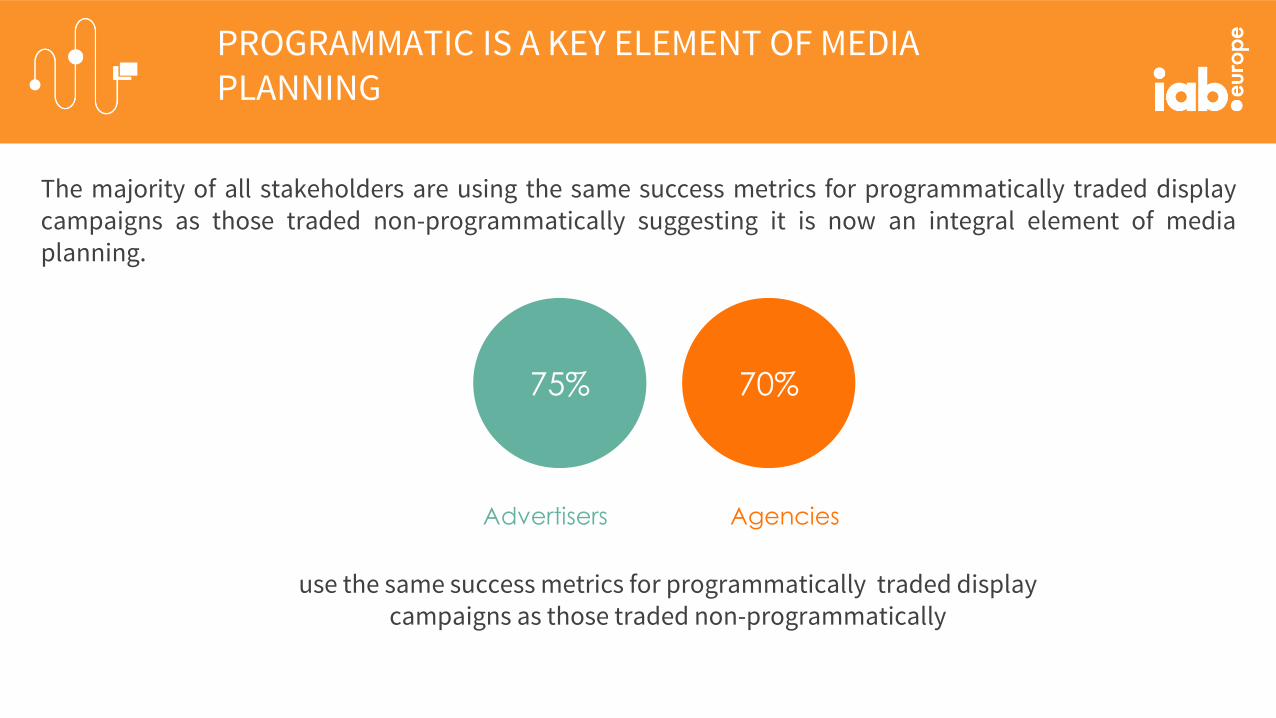

use the same success metrics for programmatically traded display campaigns as those traded non-programmatically

The majority of all stakeholders are using the same success metrics for programmatically traded displaycampaigns as those traded non-programmatically suggesting it is now an integral element of mediaplanning.

BRAND AWARENESS CLOSES IN ON THE CLICK

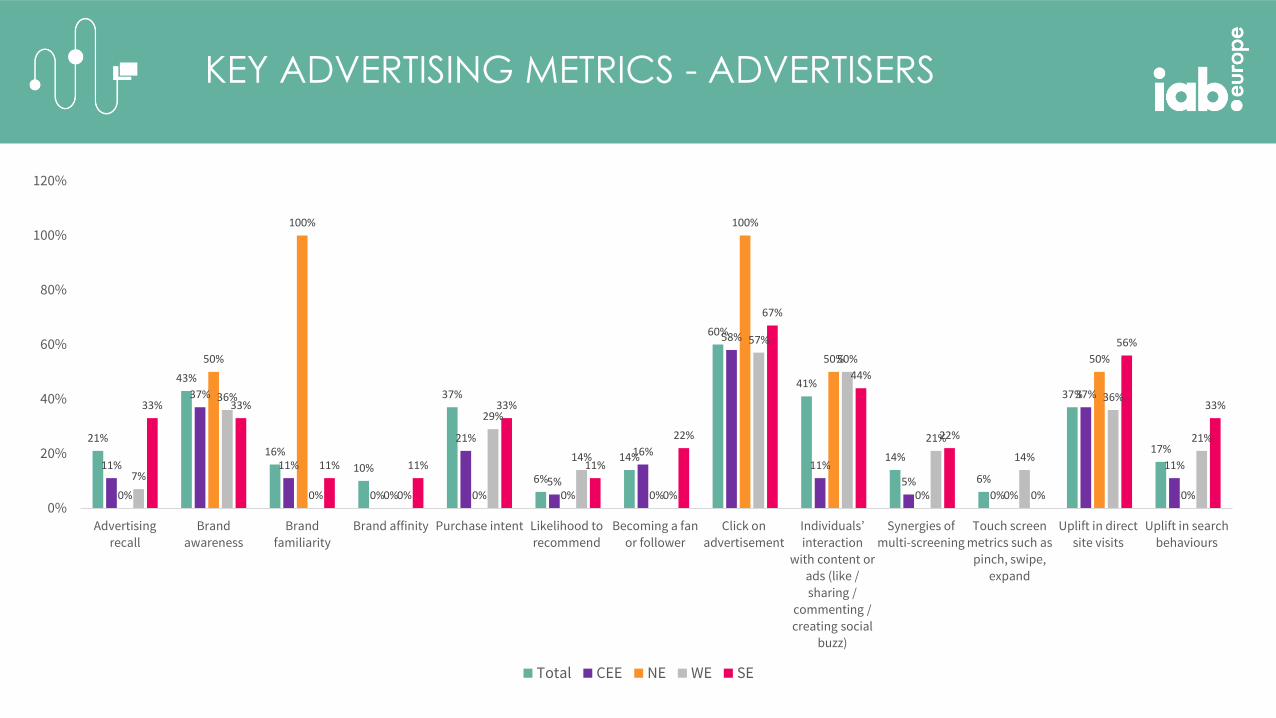

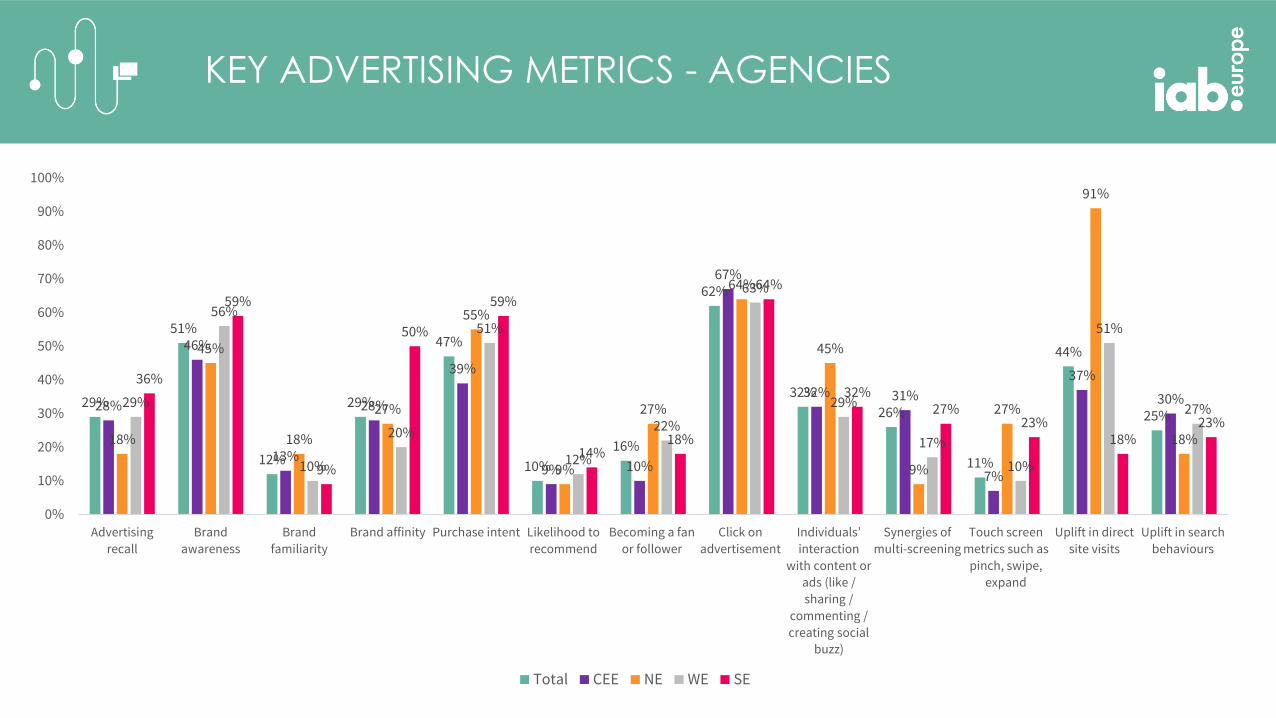

IAB Europe asked about which advertising effectiveness metrics are used to evaluate programmatically traded display campaigns for the first time in 2016. whilst the results show that click on advertisement is still widely used, brand awareness and purchase intent metrics follow closely behind suggesting maturing measurement strategies.

Agencies in Southern European markets are more likely to use brand metrics than other European regions.

21%

43%

16%

10%

37%

6%

14%

60%

41%

14%

6%

37%

17%

11%

37%

11%

0%

21%

5%

16%

58%

11%

5%0%

37%

11%

0%

50%

100%

0% 0% 0% 0%

100%

50%

0% 0%

50%

0%

7%

36%

0% 0%

29%

14%

0%

57%

50%

21%

14%

36%

21%

33% 33%

11% 11%

33%

11%

22%

67%

44%

22%

0%

56%

33%

0%

20%

40%

60%

80%

100%

120%

Advertising

recall

Brand

awareness

Brand

familiarity

Brand affinity Purchase intent Likelihood to

recommend

Becoming a fan

or follower

Click on

advertisement

Individuals’

interaction

with content or

ads (like /

sharing /

commenting /

creating social

buzz)

Synergies of

multi-screening

Touch screen

metrics such as

pinch, swipe,

expand

Uplift in direct

site visits

Uplift in search

behaviours

Total CEE NE WE SE

KEY ADVERTISING METRICS - ADVERTISERS

29%

51%

12%

29%

47%

10%

16%

62%

32%

26%

11%

44%

25%28%

46%

13%

28%

39%

9% 10%

67%

32% 31%

7%

37%

30%

18%

45%

18%

27%

55%

9%

27%

64%

45%

9%

27%

91%

18%

29%

56%

10%

20%

51%

12%

22%

63%

29%

17%

10%

51%

27%

36%

59%

9%

50%

59%

14%18%

64%

32%27%

23%18%

23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Advertising

recall

Brand

awareness

Brand

familiarity

Brand affinity Purchase intent Likelihood to

recommend

Becoming a fan

or follower

Click on

advertisement

Individuals’

interaction

with content or

ads (like /

sharing /

commenting /

creating social

buzz)

Synergies of

multi-screening

Touch screen

metrics such as

pinch, swipe,

expand

Uplift in direct

site visits

Uplift in search

behaviours

Total CEE NE WE SE

KEY ADVERTISING METRICS - AGENCIES

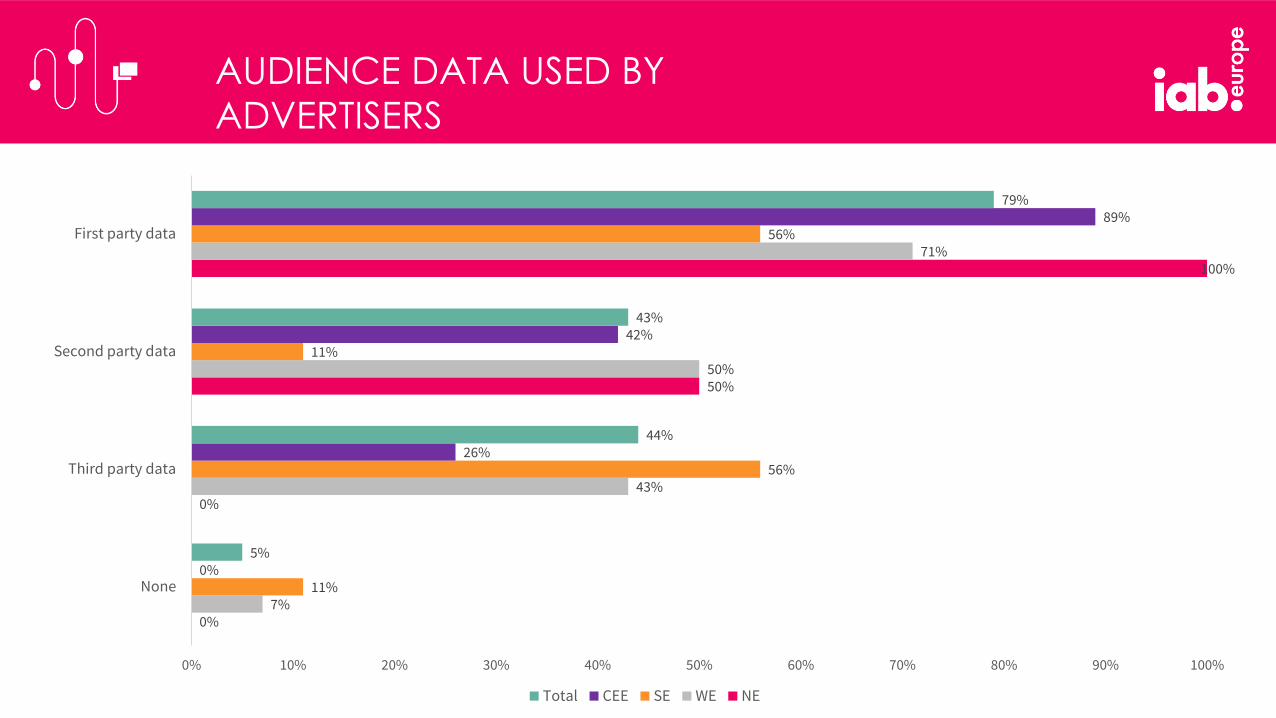

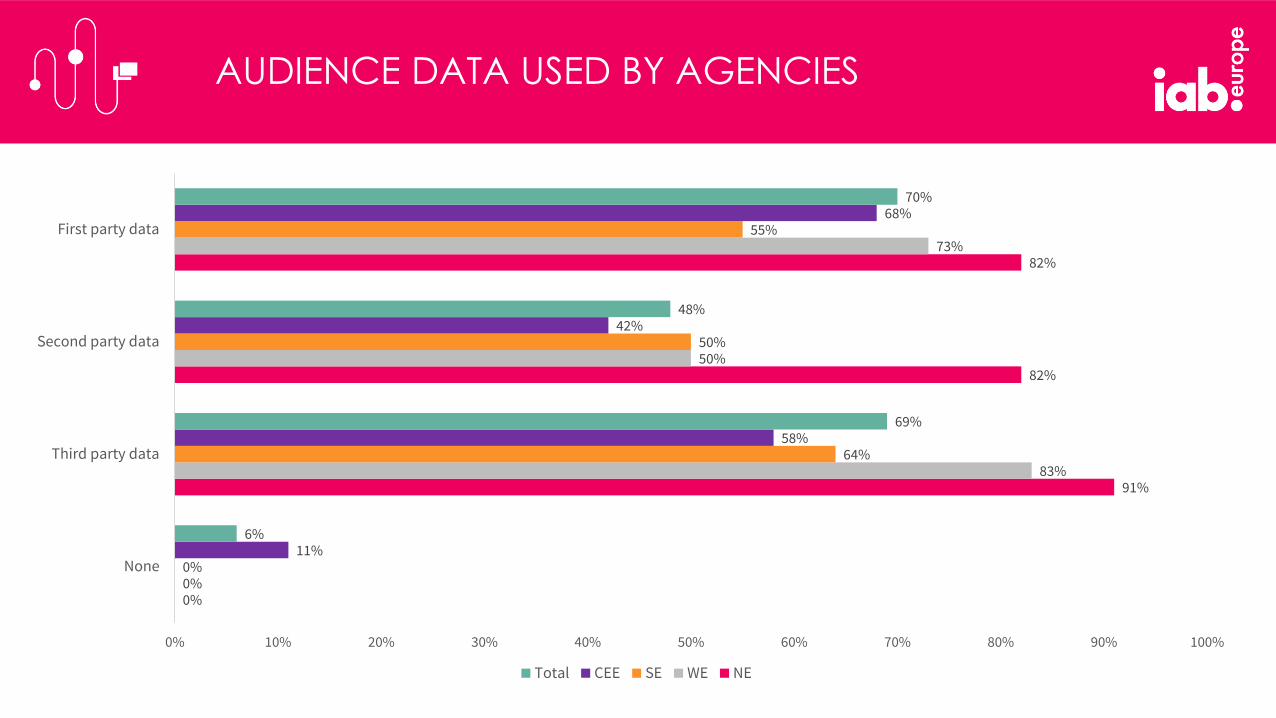

FIRST PARTY DATA DOMINATES

The majority of all stakeholders are currently leveraging first party data for their programmatic

campaigns. Agencies show signs of more mature data strategy via data integration and on boarding of

third party data whilst advertisers are utilising their first party data.

AUDIENCE DATA USED BY

ADVERTISERS

0%

0%

50%

100%

7%

43%

50%

71%

11%

56%

11%

56%

0%

26%

42%

89%

5%

44%

43%

79%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

None

Third party data

Second party data

First party data

Total CEE SE WE NE

AUDIENCE DATA USED BY AGENCIES

0%

91%

82%

82%

0%

83%

50%

73%

0%

64%

50%

55%

11%

58%

42%

68%

6%

69%

48%

70%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

None

Third party data

Second party data

First party data

Total CEE SE WE NE

FUTURE OF PROGRAMMATIC

Advertisers

94%

Agencies

97%

INVESTMENT IN PROGRAMMATIC IS SET TO

CONTINUE TO INCREASE

Percentage of stakeholders that cite an increase in programmatic over the next 12 months

CEE – 100%NE – 100%WE – 79%SE – 88%

CEE – 96%NE – 100%WE – 100%SE – 100%

Similar to last year programmatic trading revenues and investments are set to increase, regardless of market or stakeholder type. There is little difference in optimism regarding the expected increase of programmatic trading investments and revenues; over 90% of all stakeholders cite an increase in the next 12 months.

IAB Europe is the voice of digital business and the leading European-level industry association

for the digital advertising ecosystem.

@iabeurope

/iab-europe

www.iabeurope.eu

For more information on the Attitudes to Programmatic Advertising Research please contact Marie-Clare:

THANK YOU