asymmetric information, delay costs and choice of w … · asymmetric information, delay costs and...

TRANSCRIPT

Asymmetric Information, Delay Costs and Choice of Workout

Under Financial Distress *

Sanjay Banerji

Deapartment of Finance and Economics

Durham Business School University of Durham

23-26 Old Elvet Durham, DH1 3HY United Kingdom Telephone: 44 191 334-6336 e-mail: [email protected] Pinaki Bose

Department of Economics Fogelman College of Business and Economics

University of Memphis Memphis, TN 38152 Phone: (901) 678-5528 email: [email protected]

JEL Classification Codes: G32, G33, D82

July 2006

Key words: financial distress, bankruptcy, bank refinancing, debt restructuring * We have benefited from comments and suggestions made by seminar participants at American University, Concordia University, McGill University, Karlsruhe Conference on Banking and Corporate Finance, the annual meeting of Canadian Economic Association held at University of British Columbia and European Financial Management Association conference at Basel. We would like to extend special thanks to Christian Ahlin, Sris Chatterjee, Tom Chemmanur, Adolfo DeMotta, Robert Hausewald, Robert Marquez, Michel Robe for their extensive comments and valuable suggestions. Errors belong to us.

2

Asymmetric Information, Delay Costs and Choice of Workout

Under Financial Distress Abstract:

We study the reorganization of a financially distressed firm when public debt-holders are

uninformed about future profitability of its continuation projects and costliness of public

workouts (higher legal fees and delays) determines their outside option in private

workout. Under perfect information, continuation via exchange offers dominates direct

refinancing by the bank. When information on the profitability of the continuation project

is private to the bank-firm coalition, exchange offers effect continuation only for projects

with very large NPV. Low NPV results in liquidation. For intermediate ranges of NPV,

the bank directly refinances the short-term public debt. Under private information, the

credibility requirement of exchange offers involves additional equity to the firm’s

shareholders, thereby causes redistributes wealth from large creditors. Our analysis

derives testable hypothesis relating the nature of workouts and the magnitude of equity

stake to magnitude of delay costs under public workouts and also shows that legal

reforms that reduces delay costs protects small debt holders and also benefits large

creditors by mitigating adverse effects of asymmetric information.

3

Introduction:

Inordinate delays under the court-supervised bankruptcy proceedings and privileged

information held by large stake holders in a financially distressed firm are two major

impediments towards a fair resolution of financial crisis. Though the problem is

pronounced everywhere, it is more so in emerging markets. While the average time for

resolution of bankruptcy is 20 months in United States, it may range from 3 to 7 years in

countries like Mexico, Peru, Thailand and India. (Source: World Bank Index of ‘’Doing

Business’’(2006). Another important feature is that large stake holders such as banks and

dominant share holders and other suppliers of monitored finance very often possess key

information about the possibility of survival of firm currently under crisis, which, small

investors lack, making all parties vulnerable in such situations (see Senbet and Seward

(1993) for extensive examples and discussions on this subject).

The primary objective of this paper is to explore the effects of these two factors, delays in

public workout and asymmetric information, on distribution of firm value to multiple

stakeholders during private workout launched by a large creditor in a financially

distressed firm. We also examine their impacts on the equilibrium outcome leading to

choice between different methods of financial restructuring such as exchange offers,

refinancing of loans or liquidation of the firm as a whole. Finally, we trace out the effect

of judicial reform curbing excessive delays in public workout on the expected pay-off to

both large as well as small creditors.

In order to analyze these issues in depth, we study an environment where a firm’s

shareholders has defaulted on loans to a large private debt holder, such as bank and small

and dispersed public debt holders. Corporate default has triggered a change of control

4

from shareholders of the firm to bank and the latter has to decide whether to continue the

firm as an ongoing entity with new and uncertain projects or to liquidate its assets. If the

bank opts for a continuation via private workout, it needs to restructure the public debt

either (1) by direct refinancing of outstanding dues of bond holders, or (2) by offering a

new security, of higher priority but with lower payout, in exchange for the existing debt.1

If the assets of the firm are liquidated, proceeds are distributed according to existing legal

norms and priority. The bank has then, to decide whether to continue or to liquidate and

in case of continuation, how much to offer to public debt holders in their claims to new

security.

We impose two assumptions that hold key to our results. First, if they find

exchange offers from the bank unacceptable, public debt holders can always resort to

court but resolution of final outcome under any form of restructuring via public workout

is more time consuming than the same under private workouts. Second, the bank, along

with dominant shareholder, due to their superior monitoring power and close association

with the firm, has better information regarding the probability of success of new projects

(hence, about the possibility of survival) which small and dispersed public debt holders

do not possess.2

1 Restructuring of the public debt in the United States is governed by the Trust Indenture Act of 1939 which requires approval by all bondholders to change principal, interests or maturity. Hence, publicly traded debt, if not directly refinanced, is almost always restructured through exchange offers where the existing bond holders tender their old bonds in return for new securities in the reorganized firm. Non-tendering debtholders maintain their claims so that the Act is not violated. See Gilson, John and Lang (1990), Chatterjee, Dhillon and Ramirez (1995). Similar types of arrangements are also used in many emerging markets. See Laporta and Lopez-de-Silanes (2001). 2 These assumptions are based on empirical foundation laid out by several papers. It is well known that banks tend to possess superior information about firms because they monitor the borrowing firm frequently as they hold larger stakes in them. On the other hand, public debt holders, each lending a ery small fraction of total loan, does not hold a stake large enough to collect information on his own. See, Rajan (1992), James 1995), Houston and Christopher (1996). On the other hand, Gilson, S.C (1993) Gilson, John and Lang (1990), Franks and Torus (1994), document that time resolution of bankruptcy under chapter 11 and legal costs therein are substantially larger than the same under private workout. For similar results in the

5

The presence of these twin distortions, legal delays and asymmetric information, creates

following trade-offs to bank who makes an exchange offer to uninformed public debt

holders. If resolution of financial distress is more time-consuming under public workout,

the public bond holders’ expected pay-off from this outside option shrinks. Since, in

equilibrium, the expected pay-off to bondholders must be the same in both private and

public work out, banks can offer terms of exchange equal to returns from outside options

and can extract surplus from public debt holders.

However, if public debt holders do not have access to private information regarding the

profitability of the continuation project, the bank may conceal favorable information and

offer lower terms of exchange for the existing bonds. We show that such a conflict could

be resolved if banks grant concessions to share holders in the form of offering a stake in

the reorganized firm as a part of signaling devise. That is, by observing terms of

exchange alone, dispersed bond holders can not figure out the true expected value of the

firm unless the bank incurs signaling cost of some form, implying that presence of

informational asymmetry forces the large creditor to concede some information rent to

dominant share holders.

While, on one hand, these trade-offs essentially imply that delay costs in court

supervised resolution of bankruptcy redistributes firm value from small creditors to bank,

informational asymmetry, on the other hand, hurts large creditors’ interests, while making

the defaulting share holders better off. If the bank refinances the short term public debt,

it could save the costs of splitting information rent but can not exploit the public debt

emerging markets and developing countries, see Laporta and Lopez-de-Silanes (2000) and Keefer and knack, (1995). The table 1 depicts delays and costs of public workout for a small sample of both developed and developing countries.

6

holders by offering lower terms of exchange as no new security is issued. We show that

depending upon the magnitude of delay costs and degree of informational asymmetry, the

private bank optimally chooses either exchange offers or refinancing of public debt.

Thus, our model demonstrates the existence of a tension between the “cost convenience”

of exchange offers due to delay costs in alternative methods of restructuring , and the

splitting of informational rents associated under the presence of asymmetric information

determine methods of restructuring via their effects on distribution of firm value among

different participants.

In particular we show that firms with larger expected NPV (i.e, with higher

probability of success) of projects in the continuation phase, will opt for exchange offers

because they can afford to avoid signaling costs by offering a higher terms to public debt

holders in exchange offers. The firms, with intermediate values (moderate probability of

success) will choose the option of refinancing because costs of transmitting information

are large. If the expected NPV of the new project falls below a threshold, then assets of

the firm will be liquidated. We derive these threshold values for which the bank switches

from one method of workout to another and such threshold values depend on, delay costs

in public workouts, liquidation value of projects and degree of informational asymmetry.

Finally, we address a question directly linked to the arena of public policy that calls

for curbing delays in the process of public workouts. We show that such a policy, though

meant to protect small creditors, does not only improve the public debt holders’ return

by increasing the value of their outside options but it also helps large private creditor by

mitigating effects of asymmetric information. The underlying reason is that banks

needed to signal in the event of low firm value and lower terms of exchange offers

7

associated with it. However, with improved terms of exchange accompanied by legal

reforms aiming to slash time in bankruptcy proceedings under public workout, reduces

the need for signaling and saves their costs of splitting informational rent with

shareholders.

A deeper implication of this result is that an efficient public workout system not only

secures return of small investors in alternative workout system but also guards the large

creditors’ interests and helps to alleviate costs associated with information asymmetry in

financial market.3

The issues discussed in this paper are motivated by a large number of empirical

studies on corporate governance which had documented how weak laws for enforcing

creditors’ rights and inefficient bankruptcy procedures act as a barrier to the development

of financial markets, especially in the context of emerging markets. Creditors, large and

small, could be subject to expropriation of their wealth by managers and controlling

shareholders. La Porta, Lopez-de-Silanes (2001) and Laporta, Lopez-de-Silanes, F,

Shleifer, and Vishny,(1998) had analyzed bankruptcy rules and ability to enforce

financial contracts across 49 countries. Primary findings of these papers are that countries

with poor bankruptcy laws engender redistribution of wealth from creditors to dominant

shareholders and results in excessive costs of capital. See also Levine (1998), Levine and

Zervos (1998) for making analogous claims. The World Bank Index of ‘‘Doing

Business’’ also echoes similar conclusions and find that time for resolution of

3 Such legal reforms could be accomplished by either making simpler legal codes or through quicker

enforcement. A related point is that one time legal reforms have a far reaching impact on the dissipative signaling costs under asymmetric information and they improve their ex-ante incentive of banks to collect and process information and ultimately benefits the firm in lowering costs of capital. Though, we omit this result in our paper but it is a straightforward extension.

8

bankruptcy in different countries (measured in years) is positively related to costs of

bankruptcy (measured by percentage of the estate) and recovery rates of the creditors

(measured in cents per dollar). (See the table 1)

There are three main contributions of this paper in relation to the extant literature on

restructuring of debt under financial distress. First, existing literature discusses debt

renegotiations either under private or under public workout. (Gertner and Scharfstein

(1991), Brown, Mooriadian and James (1993) for private workout and Eraslan and

Yilmaz (2005) for public workouts). Our paper deals with the resolution of financial

distress under private workout but outcome in public workout, such as Chapter 11 code

of Bankruptcy, exerts influence the equilibrium pay-off to all types of creditors.

Simultaneous presence of two different systems of workouts implies that inefficiencies in

the alternative system should spill into the other. The empirical literature in both

developed and developing countries document that small investors very often receive

deteriorating terms of exchange under private workout which is very often attributed to

monopolistic power of large creditors. . See Gilson, John and Lang (1990), Chatterjee,

Dhillon and Ramirez (1995) and Laporta and Lopez-de-Silanes (2001) for small

creditors’ pay-off under private workout. Our paper suggests that such distressed

exchange offers in private workout emanate more from inefficient and time-consuming

legal system than from monopoly of the large investors.

Second, the existing literature discusses on either refinancing or exchange offers, we

focus on firms’ choice between them as well as liquidation and to what extent such a

choice is determined by redistribution of firm value between the parties due to the

presence of asymmetric information and delay costs in public workouts. For example,

9

Bulow and Shoven (1978), White (1980), Giammarino, R (1989) and others discuss only

refinancing as a method of restructuring of public debt while Gertner and Scharfstein

(1991), Brown, Mooriadian and James (1993) focus only on exchange offers but none of

the papers cited above deals with how banks choose one method of restructuring of debt

in preference over others.

Third, most of the current literature brings the issue of security design in the context of

resolution of financial distress. For example, Eraslan and Yilmaz (2005) show in the

context of Chapter 11 debt restructuring, preservation of priorities among the junior and

senior claim holders resolves inefficiencies due to asymmetric information as well as

conflicts of interests between them. Brown, Mooriadian and James (1993) focus

exchange offers in private workout and deal with the issuance of new debt and equity as

signalling mechanisms. While the common theme in ours and these papers is asymmetric

information, this paper brings the issue of conflict and redistribution among of wealth

between bondholders and shareholders, with shareholders retaining a stake in the

reorganized firm and not with the issue of design of securities. There is a substantive

evidence that shareholders receive a stake in the reorganized firm resulting in violations

of absolute priority rules (APR). See Eberhart, Moore and Roenfeldt (1991), Franks and

Torous (1994) and Betker (1995). The existing literature dealing with such violations of

APR, take the event as exogenous and are concerned with its effects on issues such as

rationing of credit, risk-taking or investment decisions not its relation to bondholders’

pay-off.4 This literature presumes existence of a firm-bank coalition during debt

4 APR violations occur when junior claim holders like shareholders receive some pay-off before senior stakeholders (creditors) are paid in full. See Berkovitch, Israel and Zender (1998) for the effects of APR violations on investment incentives, Longhofer (1997) on rationing of credit and Bebchuk (2001) on the choice of risky projects by shareholders.

10

renegotiations but we establish that such a coalition could form endogenously when the

bank acts as an informed principal in private workout. 5

The rest of the paper is organized as follows. In section 2, we outline the basic

model. Section 3 analyzes the benchmark case of complete and symmetric information.

Section 4 constitutes the core of the paper where we study the optimality of the two

different options of debt restructuring in the presence of asymmetric information, and

derive our results. The empirical implications and conclusions are presented in section 5.

2. The Model:

The firm is currently in financial distress. The face value of the bank debt is B,

which is due in period 1. The total volume of public debt is D , of which Dλ is due this

period (period 1), while D)λ( −1 is due in period 2 (the last period). Financial distress

implies that the current assets of the firm – of liquidation value L – is strictly less than

the current liabilities DλB + . Liquidation involves the bank getting bL , while the public

debt holders get dL , where LLL db =+ . The division of L may be determined by a

sharing rule, or by the court.6

5 Under asymmetric information, bank’s role in our set- up is similar to an “informed principal” who can grant some ” information rents” to agents in order to send a credible message to other parties. See Maskin and Tirole (1990) and (1992 ) for a general analysis of issues on the ‘’informed principal’’ relevant to this paper, Tirole (2005, Chapter 6) for some applications to Corporate Finance and Beaudry (1994 ) for an application of this issue in the context of a worker and firm where an informed principal concedes some information rent to agents. 6 In keeping with the literature (see Houston and Christopher; 1996; Welch, 1997), we regard the bank as the senior-most creditor while granting the bondholders some share in case of liquidation. The shareholders of the firms are lowest in the order of priority.

11

The firm may, instead, be reorganized, with the bank playing a governing role. If

reorganization (via a private workout) is successful, the continuation project yields a

stochastic return. This is represented by the probability distribution }:{ 2,1,0 tppp over

the discrete support of the vector of non-negative yields { 210 y,y,y } where 012 yyy >> .

Without any loss of generality, we assume that 0y = 0. Throughout our analysis, 2y will

be taken to represent a level of return that is high enough to satisfy all dues at the end of

period 2. 1y represents a low but strictly positive yield – one where the firm is unable to

repay all its creditors in full. Consequently, the state of nature where 1y is produced will

necessitate the implementation of some sharing rule between the bank and bondholders.

Later, we shall introduce specific assumptions involving the magnitude of 1y within the

context of each type of workout.

In this model, t is a parameter that affects the probability distribution of the

returns in the various states of nature. For the sake of expositional simplicity, we assume

that t affects the probability of the highest return 2y in a multiplicative way so that the

likelihood of occurrence of 2y is 2tp and the probability of 1y and 0y are 1p and

121 ptp −− , respectively. In the later section of the paper, t will be the source of

information asymmetry in our analysis.7

As mentioned in the introduction, continuation of the firm and private workout

between the bank, bondholders and the shareholders involves one of two alternatives:

either (i) the bank refinances the current financial liabilities of the firm by repaying Dλ

7 Our conclusions below are fairly general and are robust with respect to such assumptions on technology and the nature of uncertainty. We made these assumptions in order to preserve simplicity of the exposition. Our main propositions in this paper depend only on a “single-crossing” (refereed to in footnote 14 below) condition which is fairly standard in the literature.

12

to the public debt holders, and rolling over its own debt B, or (ii) the bank-firm coalition

restructures the public debt by making an exchange offer that will be described in the

following sections. For expositional convenience, we assume that the continuation project

does not require any new investment and that all other assets of the firm, except the

return iy , atrophies to zero by the end of the second period.

To specify the previously mentioned inadequacy of 1y , we initially assume that

1y BD +−< )1( λ (1)

This assumption implies that if the bank refinances and rolls over its own debt to the next

period, the firm defaults in discharging its debt obligations if continuation yields 1y . We

assume that, in this case, the return is split between the bank and the public bondholders,

with the share of the latter being σ ≥ 0 (which may be determined by an equal sharing

rule, or otherwise). In addition, we also assume that, in any workout, the minimum that

the shareholders must receive for continuation is x*. This is usual and realistic in many

situations.8

3. Benchmark Model: Perfect Information:

Suppose that the realization of t is observed by all concerned parties prior to any

private workout, and that the bank opts for continuation. Continuation involves either a

restructuring of the public debt (when the bank offers a new debenture of higher seniority

in exchange for the existing bonds), or refinancing (i.e. repayment of all period 1 dues by

the bank itself). In this section, we adapt the analysis of Gertner and Scharfstein (1991)

to the present model to demonstrate that, in the absence of asymmetric information, the

8 We may regard x* as the reservation payoff of the shareholders under the chapter 11 proceedings of bankruptcy. If the firm is reorganized under chapter 11, shareholders usually obtain some equity stakes as the court favors equity holders due to equity maintenance value.

13

bank may prefer exchange offers as a method of restructuring the public debt to

refinancing.

3.1 Refinancing by the Bank

Suppose, first, that the bank refinances by repaying the short-term public debt and

rolling over B. In this case, the bank does not need to provide more that the reservation

equity stake to the shareholders. Furthermore, as mentioned in the previous section, the

bank-firm coalition is able to pay all its outstanding dues if y2 is produced in period 2. If

the project generates the low return y1, assumption (1) implies that the entire yield is split

between the bank and the public bondholders. The assumed sharing rule yields 1(1 )yσ−

to the bank. Its continuation payoff is then given by

DypxDytpRF λσλ −−+−−−= 1122 )1(*])1([ (2)

where *x represents the payment to the shareholders. As junior claimants, shareholders

receive a payoff only if the return is high enough to repay the creditors in full.

3.2 Exchange offers

Next, we consider the alternative of restructuring the public debt via an exchange

offer. Suppose that the bank offers α$ of senior debt for $1 of the existing debt of both

maturities, and postpones repayment of its own debt till period 2. Thus, in return for

tendering their old bonds, bondholders receive a package of new securities that enjoy

more seniority but receive a lower cash payout. Such an exchange offer will not violate

the Trust Indenture Act if the new bonds are offered without extinguishing the old bonds.

14

For simplicity of exposition, we assume that the new debt is senior to all other

debts.9 Suppose that all public debt holders tender their bonds. According to the terms of

the new debt, the bank will pay Dαλ to the bondholders at the end of period 1. In period

2, the new debt has the highest priority, and will be repaid first. Other creditors will

receive payments only when there is a surplus left over after repayment of the new debt.

We shall, as before, suppose that 2y is large enough for all creditors to be repaid in full.

However, we assume that

BDy <−−< )1(0 1 λα (3)

i.e., if 1y is produced, only the debtors with the highest priority – the holders of the new

bond - are paid in full. Tendering an old bond of face value $1 results the following

expected pay-off:

λλα −++ 1)(([ 12 ptp )]

Consider, on the other hand, the consequences of holding out for a possessor of an

original bond of face value $1. The yield 2y is high enough for her to be repaid in full.

But in case of a cash flow of 1y , assumption (3) implies that the residual Dy )1(1 λα −−

is inadequate for this purpose. In this event, the payment to a bondholder that holds out

will be the consequence of bargaining over the splitting of the residual with the bank. Let

ρ represent what this bondholder receives when 1y is produced. With costly bargaining

and in face of the superior bargaining power of the bank vis-à-vis the atomistic

bondholder, it is quite reasonable to expect that ρ will be less than what she would have

9 While this assumption is usual in the literature, and also realistic, our analysis and its conclusions will be robust to certain variations of this seniority, and to the consideration of a range of exchange offers that may be predicated on the maturity of the original debt, subject to appropriate restrictions. Our treatment of exchange offers follows Gromb’s exposition of the topic in the conext of financial distress. See Gromb (2000)

15

received if continuation had yielded the return 1y in the absence of exchange offers.

Later in this section we present a simple analysis that formalizes the determination of ρ as

the outcome of bargaining under threat of litigation between the bank and a single

bondholder.

The expected pay-off from holding out with an existing bond of $1 face value is

then:

ρλλ 12 )1( ptp +−+ (4)

Assuming that all bondholders tender, an atomistic individual has no incentive to hold out

as long as

ρλλλλα 1212 )1()]1)(([ ptpptp +−+≥−++

or, if

),()1)((

)1(

12

12 ραλλρλλα t

ptp

ptp=

−+++−+

≥ (5)

It is easy to see that α(t, ρ) in increasing in both t and ρ.

3.3 Determination of ρ

Suppose that, in period 1, the bank introduces exchange offers to restructure the public

debt, and that one (or some) bondholders hold out. At the end of period 2 let the firm’s

realized cash flow be 1y so that firm is again on the verge of bankruptcy. The bank

proposes the payment of ρ to a holder of an original bond of face value of $1. The

bondholder could, then, litigate to claim a higher amount. It is reasonable to suppose that

maximum amount of claim that a bondholder may either justify, or expect to be awarded

by the court, is what she would have recovered in the same state of nature if continuation

16

had taken place in the absence of any exchange offer. Recall that in the alternative

scenario all bondholders receive a total of 1yσ when 1y is produced, whereupon D

yσ 1 is

the amount paid to the owner of a bond of face value $1.

Denote D

yσµ 1= . In our analysis µ represents is the amount that the litigating

bondholder can expect from the court. The court can either grant µ to the bondholder or

it can alternatively reject her proposal and accept the proposal offered by the bank. We

assume that the court, under chapter 11, accepts the bondholder’s proposal with

probability qso that the probability of rejection is (1-q ).

It is well known that court-supervised public workouts involve delay costs (and

possibly other legal expenditures). We assume that such costs are proportional to the

amount expected by the litigating bondholder, i.e. that the original claim of $1 from a

public workout is worthγ (with 0 < γ < 1) to her.10 Then, by litigating, the payoff that

that this bondholder expects to recover in the event of bankruptcy at the end of period 2 is

will be given by ])1([ ρµγ qq −+ . Hence, in equilibrium, bank would propose a ρ such

that ρ = ])1([ ρµγ qq −+ , whereupon

)]q(γ

µqγρ

−−=

11 (6)

10 Alternatively, we could analyze with differential costs of time for resolution of financial distress under

private work out and chapter 11 bankruptcy. In that case, p

c

γγγ = , where subscripts (c) and (p) stand for

chapter 11 and private workouts. So long as 1<γ (see the footnote below), our results will hold with the

burden of extra notations.

17

From the above analysis, ρ emerges as a function of the delay (and other) costs, and the

probability of acceptance of the bondholders proposal.11

3.4 Optimal Debt Restructuring under Symmetric Information

We now compare the continuation payoff to the bank-firm coalition under the

exchange offers (denotedER ) to the corresponding payoff from refinancing by the bank

itself. The following proposition captures the effect of delay costs and the NPV of the

continuation project on the nature of continuation opted for by the bank:

Proposition 1: If 1t t≥ , i.e. the NPV of the second period project is high enough for

continuation. As long as the costs arising from delays and disputes in the resolution of

financial distress are greater in a public workout than in a private workout )10( << γ ,

the bank strictly prefers restructuring of the public debt via exchange offers to direct

refinancing.

Proof: In an exchange offer, the bank will optimally offer )(tαα = as given by (5) and

avoid the holdout problem.12 With the new bond having the highest priority, RE is given

by:

DDypxDytpRE αλλαλα −−−+−−−= ])1([*])1([ 1122 (7a)

which, using (5) may be expressed as

11 Gilson, John and Lang (1990) finds in their sample that while the average time spent by the companies in chapter 11 was more than 20 months, the similar time length in private work outs was about 15 months. If the opportunity costs of waiting is even moderately estimated to be proportional to the time elapsed, then,

75.=γ

12 Although, we restrict ourselves to a specific form of exchange offer given by (5), our analysis is robust to other forms of exchange offers that involve a combination of both junior and senior securities. This particular formulation captures reductions in overall debt )(α and its relationship to weak bargaining

power of a single bondholder )(ρ in a simple manner. Our results below will remain unchanged even if

we proceed with a more complicated arrangement but algebra will be more tedious.

18

−+−= 1122 *][ ypxytpRE Dptp ])1([ 12 ρλλ +−+ (7b)

Recall that the bank’s expected pay-off under direct refinancing of short-term public

debt, as given by (2) is

DypxDytpRF λσλ −−+−−−= 1122 )1(*])1([

Hence,

][][ 11

1 ρµρσ−=−=− Dp

D

yDpRR FE

Using (6) and the above expression, we get

0)]1(1

)1(1 >

−−−=−

qDpRR FE γ

µγ (8)

Furthermore, since RE is increasing in t, the bank will not liquidate if t is high enough

such that RE ≥ Lb. Inspection of (7a) reveals that if Lb is strictly greater than

DDyp αλλα −−− ])1([ 11 , then the bank prefers liquidation for sufficiently low values of

t. Thus, there may exists 1t t= at which RE = Lb. The bank liquidates if t is lower than 1t .

At 1t t≥ , the NPV of the continuation project is high enough to make the private workout

preferable to liquidation. //

Proposition 1 implies that the bank will never opt for direct refinancing of outstanding

dues. However, this is too strong a result that holds only when the NPV of the

continuation project is public information to all parties. As we will demonstrate in the

next section, if the realized value of t is not observed by the bondholders, both forms

private workouts are possible.

19

4. Debt Restructuring with Information Asymmetry:

We now assume that the realized value of t is observed only by the bank-firm

coalition. The public bondholders do not directly observe t. This information asymmetry

does not affect the payoff of the bank when it effects continuation through refinancing.

However, since α(t), as given by (5), is increasing in t, it can be in the bank’s interest to

underreport t. In such a situation, we demonstrate that the bank may signal that its

exchange offer is credible by awarding a higher share of the surplus to the existing

shareholders. In other words, a private workout involving an equity stake( )x t that may

be higher than x* can convey information about the magnitude of t to the bondholders.

The present section analyses the nature of the separating equilibrium involving

exchange offers at the appropriate values of α(t). We initially confine our attention to the

discrete case where t may take one of two possible values and derive the necessary

results. The discrete case makes transparent the intuition behind the signalling behaviour.

Our analysis is subsequently extended to the case where t varies over a continuum.

4.1. The Discrete Case

The value of t is realized in period 1 prior to any private workout, and may be

either lt with probability θ , or ht with probability 1-θ , where lt < ht . As mentioned,

only the bank-firm coalition observes the realization of t . Throughout the rest of our

analysis, we assume that. 10 << γ so that, under conditions of perfect information, the

bank prefers exchange offers to direct refinancing. The introduction of asymmetric

information, as we demonstrate in this section, may change the bank’s choice of workout.

20

Let the private workout involving the exchange offer α to the bondholders and the

equity stake x to the shareholders be represented by the pair ),( xα . Given a realized

value of t , the bank’s expected payoff from this workout is

DptpypxytptxRE )]1)(([][);,( 121122 λλαα −++−+−= (9)

Suppose that the bank offers ),( ii xα when itt = , for li = or .h In a separating

equilibrium, ),(),( hhll xx αα ≠ , i.e. the offers are distinct with respect to t. Furthermore,

each offer is a credible signal of the it it is associated with. This implies that the bank is

unable to profit from manipulating the signal, i.e. incur a strict gain from offering

)x,α( jj when itt = for .ji ≠ This is ensured by the following condition:

);,();,( ijjE

iiiE txRtxR αα ≥ (10a)

for hlji ,, = and ji ≠ .

In the present context, utilizing (9), (10a) may be elaborated as

Dpptypxypt hhhh ]))(1[()( 121122 λλα ++−−+−

≥ Dpptypxypt hllh ]))(1[()( 121122 λλα ++−−+− (10b)

in the case where .hi = For li = , the corresponding condition is

Dpptypxypt llll ]))(1[()( 121122 λλα ++−−+−

≥ Dpptypxypt lhhl ]))(1[()( 121122 λλα ++−−+− (10c)

In addition, iα must also be high enough to prevent the holdout problem, i.e. ),( ii tαα ≥

for lhi ,= , where

)1)((

)1()(

12

12

λλρλλα

−+++−+

=ppt

pptt

i

ii (11)

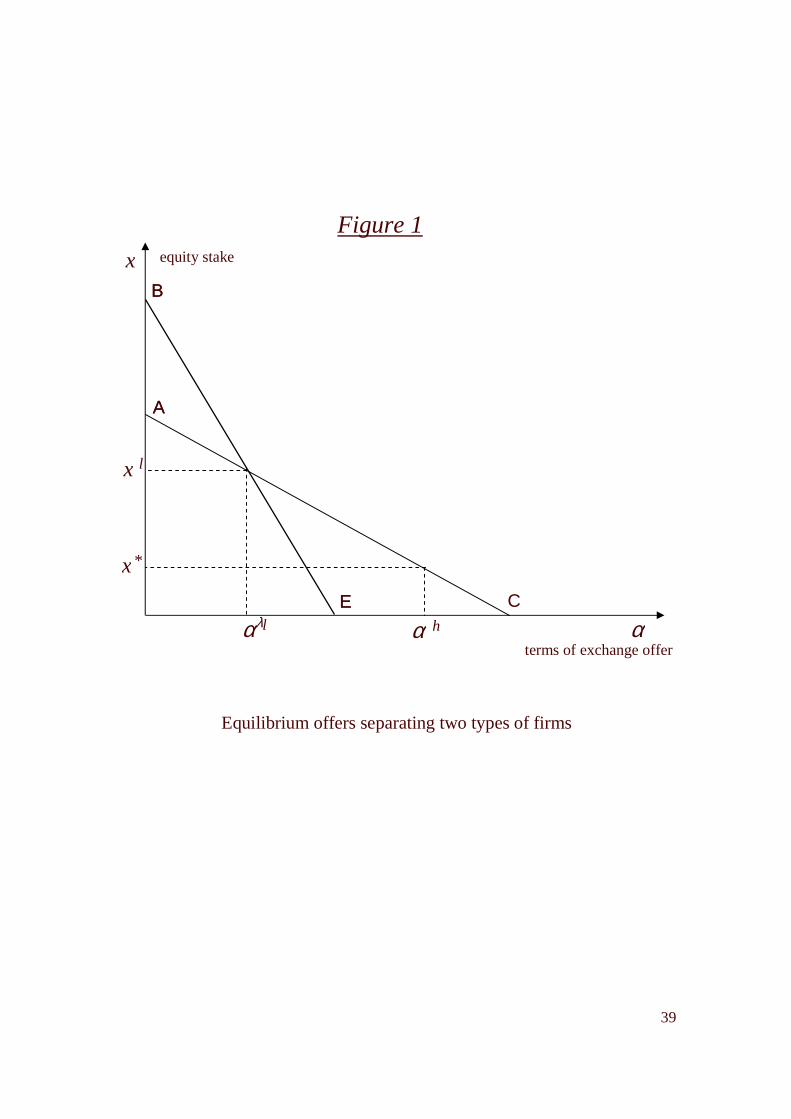

[Figure 1 about here]

21

The nature of the separating equilibrium is depicted in Figure 1 which represents

the contour curves for );,( iiiE txR α in the ),( xα plane. A contour curve represents all

),( xα that yield the same expected payoff to the bank for a given value of t. It is easy to

see that the contour curves are linear, and that13

02

>= ttanconsRE

t

x

δαδδ

implying that a lower value of t results in a steeper curve – as in figure 1. Since ER is strictly

decreasing in α and x , a lower contour curve represents a higher expected payoff for the

bank.

From (7), it is evident that )()( hl tt αα < . This means that the exchange offer

represented by )( htα will credibly represent ht and x does not need to be higher than x*

for signalling purposes, i.e. *).),((),( xtx hhh αα = The private workout represented by

*)),(( xt lα will, however, not be a credible reflection of lt , since the bank has the

incentive to gain from understating t by deviating to such as offer when .htt =

Consider the contour curve AC represented by

)*;),(();,( hhE

hE txtRtxR αα = (12)

[Figure 2 is about here]

13 The condition 02

>= ttanconsRE

t

x

δαδδ

is very often referred to as “single-crossing” or sorting condition in

the information economics literature and is widely used in games of incomplete information. See Tirole (2005). Though, our paper deals with a linear technology and multiplicative uncertainty, conclusions below are robust with alternative specifications as long as this assumption is maintained.

22

This curve represents workouts that yield the same expected payoff as received by the

bank from offering *)),(( xt hα when .htt = It is easy to see that, given the realization of

lt , the offer ))(),((),( lxtx lll αα = will be credible. The offer ),( ll xα is given by the

intersection of AC and the steeper indifference curve BE that represents a constant

continuation payoff of the bank in the event of .ltt = From figure 1 it is clear that, when

,htt = a switch from ),( hh xα to ),( ll xα leaves the expected payoff unchanged. Also,

when ltt = , switching to ),( hh xα will move the bank to a contour curve that is higher

than BE. This implies a strict decrease in its payoff. Thus, ),( hh xα and ),( ll xα satisfy

both (10b) and (10c), and there is no incentive to gain from deviating. Furthermore, of

all private workouts that credibly signal tl, ),( ll xα is the one that yields the highest

expected payoff to the bank. ),( hh xα and ),( ll xα , therefore, constitute a separating

equilibrium.14

In this separating equilibrium, *xxl > , implying that the shareholders receive an

equity stake in the reorganized firm that is strictly greater that the reservation level that is

obtained under perfect information. Information asymmetry leads to a trade-off between

α and x that is, in essence, an APR violation as well as redistribution of surplus from

creditors to shareholders. When ,ltt = the bank offers a higher stake to shareholders,

who are lowest in the order of seniority, since this makes the lower terms of the exchange

14 No pooling equilibrium exists in this model. When the same workout ),( xα is offered in both states of

nature, there is another workout involving some ))(,( lααα ∈′ that is profitable when ltt = , but not

when .htt = The demonstration of this result is omitted from the paper for sake of brevity, but is available from the authors upon request. Also, this equilibrium is supported by the following out-of the–

equilibrium belief of bondholders: For any choice of ,hαα ≥ the firm belongs to the type ht and for

,hαα < the message must have been sent by the low type.

23

offer credible to the bondholders. That is, better firms need not incur any cost because a

higher exchange offer is credible but the lower offer is not, so that the burden of proof

and signalling costs are borne out only by the firms with poorer realization of t .

The discrete case analysed above establishes the link between the NPV of the

continuation project and the terms of credible private workouts involving exchange offers

that may be offered to bondholders. The intuition here is straightforward: under

asymmetric information any credible reduction in the terms of exchange offers must be

accompanied by costly concessions from the bank - in the form of higher equity stakes to

the shareholders. The necessity of offering a higher share of the residual surplus to

shareholders at a lower value of t adversely affects the continuation payoff of the bank,

and may result in situations where the bank prefers to refinance rather than restructure the

public debt. We explore this possibility in the next subsection, where t is assumed to vary

over a continuum. The relevant algebra is presented in the appendix and in the text, we

discuss the intuitions behind results based on the discreet case.

4.2. The Continuum Case

We extend our analysis to the case where t is distributed uniformly over the

interval ],[ tt . In the separating equilibrium where the bank makes the exchange offer

that is represented by )(tα (as given by (11)), let the corresponding equity stake to the

shareholders be ).(tx Clearly, (α(t), x(t)) ≠ (α(t´), x(t´)) if t ≠ t´ for the terms of the

private workout to serve as distinct signals for each t. As in the previous section, there

24

will be a trade-off between a lower )(tα and a higher value of )(tx for credible

representation of the bank’s private information to the shareholders.

Suppose that the bank attempts to under-represent t following its realization by

making the exchange offer )(t ′α and offering the shareholders the equity stake)(tx ′ ,

where tt <′ . Then, the bank obtains the payoff

DtptppytxytpttxtRE )]1)(()[()]([]);(),([ 12122 λαλα −′++−+′−=′′ (14)

In a separating equilibrium, such a misrepresentation must not be profitable to the bank.

Thus, t′ must maximize (14) at t′ = t. As is standard in the analysis of such situations,

this implies the following first-order condition15

0=′

′′

′=tt

E

tδ

]t);t(x),t(α[Rδ (15)

From the solution to the differential equation (15), we obtain the equilibrium )(tx , while

)(tα is given by (11). We present the necessary algebra in the appendix. )(tx emerges

as a decreasing function of t, denoting that the shareholders, as junior claimants receive

an increasingly higher than reservation share of the residual surplus (generated only when

the continuous project yields y2) at lower values of t. However, as we demonstrate, if

x(t)) is too high, the bank may prefer to effect continuation by direct refinancing.

Propositions 2 below demonstrate the relationship between )(tx and )(tα that gives rise

redistribution of wealth from creditors to share holders and 3 and 4 below formalise

between relationship between the magnitude of t and the bank’s choice of workout

between the alternatives of liquidation, refinancing and exchange offers.

15 Our analysis of the separating equilibrium (done in detail in the appendix) primarily follows Mailath (1987).

25

Proposition 2: The shareholders expected pay-off is inversely related and public debt

holders’ pay-off is positively related to t.

The proof of this result is given in the appendix but the essence of the proof can

be grasped in the discreet case analyzed in Figure 1. In equilibrium, both offers are on

curve AC, (Figure 1) and (10b) holds with a strict equality. Utilizing this, and the fact

that *xxh = , we can derive

212 )]1)(()[(*

pt

Dpptxx

hhlhl λλαα −++−+=

when, using (11), we can derive

2 1 2 1

2 1 2 1

(1 ) (1 )- 0

( )(1 ) ( )(1 )

h lh l

h l

t p p t p p

t p p t p p

λ λ ρ λ λ ρα αλ λ λ λ

+ − + + − +− = >+ + − + + −

Since lh αα − is strictly decreasing in ,lt lx will be higher the lower is the magnitude of lt .

The main message of this result is that asymmetric information forces creditors concede

surplus to share holders but firms with higher upside potential, such transfer of wealth

will be smaller.16

Proposition 3: In a separating equilibrium, the equity stake to the shareholder and the

exchange offer are given by the following:

( )( ) ln ) *

(

t at b Qx t x

t at b b

+= + + and 2 1

2 1

(1 )( )

( )(1 )

tp pt

tp p

λ λ ραλ λ

+ − +=+ + −

where, DpQ ]1)[(1(1 ρλλ −−−= , 1(1 )b p λ= − and )1(2 λλ −+= pa

Proof: Follows from (2) and the solution to the differential equation given in (15).

16 The necessity of offering a higher equity stake to shareholders at lower values of t lowers adversely affects the continuation payoff of the bank, and may result in situations where the bank prefers to refinance rather than restructure the public debt. Note that in the case of refinancing the bank will offer x*. Thus, under asymmetric information, there may exist values of tl for which proposition 1 of the previous section may no longer be valid. This is explored further in the next sets of propositions.

26

(see appendix).

From the explicit form of )(tx in proposition 3, we can see the extent of violation

of the Absolute Priority Rule, i.e. the extent to which the shareholders, as the most junior

claimants, receive equity stakes in excess of the reservation level *x in a private

workout. x(t), and the associated exchange offerα (t), are related to each other via key

parameters such as (i) t, which is the determinant of the NPV of continuation project; and

(ii) ρ , which can be a proxy for costs due to delays in public workouts.

Our analysis, so far, has focused on the mechanism of exchange offers. However,

as indicated earlier, there may be situations where the bank prefers refinancing to

restructuring the public debt. We now turn to the determination of the relationship

between the realized value of t and the optimal form of workout that is chosen by the

bank. Proposition 2 suggests that, for the low values of t, )(tx may impose too large a

cost of exchange offers on the banks. At a lower realization of t, the bank-firm coalition

has to concede a large information rent to shareholders in form of a high x(t), and this can

result in the bank preferring refinancing options to exchange offers. Furthermore, if t is

too low, continuation may not be optimal irrespective of the type of workout chosen, and

the bank would favour liquidation.

Recall that liquidation implies a payoff of bL to the bank. As before, we assume

that bargaining between the bank and the bondholders results in the latter obtaining the

same shareσ of the liquidated assets, i.e. LLb )1( σ−= . Proposition 3 now formalizes

the above argument involving the choice of workouts, and derives the critical values of t

that demarcates the regions of the alternative continuation decisions by the bank.

[Figure 2 about here]

27

Proposition 4: For realizations of t in the interval 1[ , ]t t , bank liquidates the firm. It opts

for reorganization via direct refinancing if the realized value of t falls within the interval

),( 21 tt . If ],[ 2 ttt ∈ the bank resorts to a private workout involving exchange offers.

Thus, shareholders receive an additional surplus if t ∈ ),( 2 tt . The critical values of t are

1 11

2 2

(1 )[ ]

[ (1 ) *]

L p y Dt

p y D x

σ λλ

− − +=− − −

, and x

pDyt

.][ 112

ρσ −=

Proof: The formal derivation is in the appendix. Here, we present the intuition with the

help of figure 2. The horizontal curve lR represents the bank’s pay-off from liquidation,

while FR is the expected pay-off under refinancing. The convex curve ER is the bank’s

expected pay-off under restructuring via exchange offers. As figure 2 demonstrates, lR

initially dominates both ER and FR . Thus, for 1t t< the firm is liquidated because the

bank’s share of the liquidation value is strictly higher than the optimal return from

continuation, i.e. Fb RL)σ(L >−= 1 . For intermediate values of t continuation is

preferred, but the information costs, as represented by the excess of )(tx over *x are

large. With asymmetric information, the difference between the pay-offs from exchange

offers and refinancing is:

*])([)]1(1

)1(21 xtxtp

qDpRR FE −−

−−−=−

γµγ

(16)

The first component is same expression on the R.H.S. of (8) that, under perfect

information, represents the entire difference between RE and RF. It is strictly positive due

to higher delay costs associated with public restructuring. The existence of asymmetric

information now adds a second component to the difference in the two payoffs: the

information rent conceded to shareholders in form of the expected surplus over and above

28

x*. This may be too high at a lower value of t to cause the R.H.S. of (16) to be negative,

whereupon refinancing is the more attractive choice even if γ <1. As t increases, ( )tα

increases at a decreasing rate while )(tx decreases at an increasing rate, causing ER to be

higher than FR beyond .2t

These threshold values of t are endogenously determined by the parameters in our

model. As is evident from proposition 3 and 4, the choice of workout depends on the

distribution of pay-off among shareholders and public debt holders (( )x t , ( )tα ) which in

turn is determined by parameters such as delay costs, the degree of asymmetric

information, maturity of the public debt and liquidation value of the project. These

parameters will impact on the pay-off to share holders and on the terms of exchange

offered to the bondholders.

Since our model emphasizes on the delay costs of public workout, we will

examine, next, the impact of reduction of delay costs on the distribution of pay-off to

creditors and its consequent effects on the choice of restructuring. The following

propositions summarize its effects on those variables.:

Proposition 5: A decrease in the delay costs, represented by an increased value of ρ in

our model, leads to an decrease equity stakes and an improvement in the terms of

exchange for the bondholders.

Proof: By differentiating ( )x t and ( )tα , as given in the proposition (3), with respect to ρ, we

get: 0)(

)( <

++−=

batt

btatx

δρδ

and 0)1)(( 12

1 >−++

=λλδρ

δαptp

p//

29

Proposition 6: A reduction in delay costs causes larger number of firms to switch from the

option of refinancing to exchange offer 1

2

x D p

x t

δ ρ ρδρ

<

The proposition 5 carries an important result for policy implications. As stated in the

introduction of the paper that various authors have called for reforms in the bankruptcy

rules that protect small investors and a very important issue in that debate is how to

reduce delay costs that hurt primarily small and dispersed creditors. The proposition 5

states that such reforms aiming to make small investors secure their rights also help the

large creditor to retain a part of information rent. The intuitive reason is that large

informed creditors incur costs of signalling when they offer a lower terms in exchange

offers. However, with diminishing delay costs, public debt holders fare better in

exchange offers which reduces the need to incur signalling costs.

5. Testable Implications:

Our conclusions have several testable propositions and policy implications. While some

of them, such as APR violations and distressed exchange offers, agree with the existing

literature, the following are new and specific to the model.

(a) The proposition 2 suggests that the magnitude of shareholders’ stakes in the

reorganized firms and the terms of exchange (the amount of reduction in the face

value of the current debt) offered to public debt holders are inversely related

under asymmetric information. The testable implication of this result is that more

profitable projects leave smaller equity stakes to shareholders but better terms of

exchange to public debt holders. Hence, wealth transfer from bond holders to

30

shareholders and banks is relatively smaller (larger) for firms with greater

(smaller) upside potentials.

(b) The great the delays in public workout system, the smaller the pay-off to the

public debt holders as well as banks in private negotiations. While this one

accords with casual empiricism (see table 1), one needs to carry out empirical

tests to examine validity of the proposition.

(c) The testable implication of propositions 5 and 6 are that (i) the likelihood of

distressed exchange decreases with the reduction of delay costs and if the

outstanding amount of debt is very large, then we are more likely to observe

exchange offers as a form of restructuring as opposed to refinancing. For

example, the propositions all together suggest that exchange offers are likely to be

observed in OECD countries more than in emerging markets as delay costs in

public workout are lower in the former.

5. 1. Conclusion

In times of financial distress, workouts between the major claimants frequently lead to a

restructuring of the public debt of corporations. Restructuring usually takes the form of

either exchange offers or direct refinancing by the bank. Terms of exchange offers in

private workout very often reflect the bargaining power of bondholders, determined by

how much they can get from the chapter 11 bankruptcy, which serves as outside option to

public debt holders. Finally, very often, in a private workout the junior-most

claimholders, such as the shareholders of the corporation, receive substantial equity

stakes in the reorganized firms, indicating a violation of the priority rule. In this paper,

31

we develop an analysis that demonstrates that these features are interrelated and are

affected by transfer of wealth between various stake holders due existence of asymmetric

information across creditors, inherent delay costs. In this sense, the present analysis

provides endogenous explanations of influences that have been empirically observed in

the literature and in our future work, we would extend our analysis to endogenous

composition and maturity structure of debt. .

32

Mathematical Appendix:

Proposition 2:

Let the expected pay-off function of the type t bank that offers a reduction of the face

value of public debt from $1 to )1($ <α in the continuation stage be:

DtDtypxtxDtytptxttRE λαλαλαα )(])1)(([*])()1)(([)](),(,[ 1122 −−−+−−−−=′′ (1A)

Where, jy = cash flow from the project 2 in the state j=1,2,

)1)((

)1()(

12

12

λλρλλα

−+++−+=

ptp

ptpt

is the exchange offer by the type t bank to public debt holders, and =)(tx Equity stake

to shareholders.

The incentive compatibility condition requires that

0)](),(,[ =′′′ =′ ttE txtt

t

R αδ

δ ⇒

Dtppt

t

t

txtp )]1)(([(

)()(212 λλ

δδα

δδ −++=−

.

t

t

tp

Dtpp

t

tx

δδαλλ

δδ )()]1)(([()(

2

21 −++−= (2A)

The derivative of )]([ tα is given by :

0)]1)(([

]1)[(1()(2

12

21 >−++

−−−=λλ

ρλλδ

δαptp

pp

t

t

(3A)

and plugging its value in (2A), we get:

0)]1)(([

]1)[(1()(

122

21 <−++−−−−=

λλρλλ

δδ

ptptp

pp

t

tx

(4A)

33

Proposition 3:

The equation (4A) used in the proof of the proposition 2 can be rewritten as:

)]1([)1(

]1)[(1()(

22

1

1

λλλρλλ

δδ

−++−−−−−=

pttp

p

t

tx (5A)

The differential equation (4A) assumes the following form:

2

( )x t Q

t at bt

δδ

= −+

;

where, D)ρλ)(λ(pQ −−−= 111 , 1(1 )b p λ= − and )1(2 λλ −+= pa

The solution is given by:

Cb

Q

bat

ttx lnln)( +

+−= (6A)

where Cln is a constant and its value is determined by the condition that the highest type

need not signal. Hence, *)( xtx = . Using this information, we can write the equation (5A) as:

*)(

)(ln)( x

b

Q

btat

batttx +

++=

Finally, in this equilibrium, the out-of-equilibrium messages are *x x> and ( )x x t< .

Application of intuitive criterion would require the investors’ belief (ξ ) about the type ( )t

after observing a message( )x be ( , ) 1t xξ = for *x x> and ( , ) 1t xξ = for ( )x x t< and such

beliefs do not provide the incentive for any type to defect and thus gives rise to a unique

separating equilibrium.

34

Proposition 4:

For a given realization of t , the firm-bank coalition will decide whether they are going to

liquidate the firm or to reorganize and if in the event of reorganization, they have to opt

between exchange offers and direct repayment of short-term debt. The coalition would choose

an option that maximizes the expected pay-offs, given by the following function:

},,.{ Efl RRRMaxR = , where

LRl )1( σ−= (we assume that the sharing rule implies Lb = (1 – σ)L)

DypxDytpRF λσλ −−+−−−= 1122 )1(*])1([ and

DDypxDytpRE αλλαλα −−−+−−−= ])1([])1([ 1122

The figure 2 illustrates the expected pay-off functions. The function )( lR is independent of t

and is the horizontal line in the figure. The function )( FR is an upward sloping straight line

because 0*])1([ 22 >−−−= xDypt

RF λδ

δ and .0

2

2

=t

RF

δδ

On the other hand, =t

RE

δδ

0])]1(*[ 22 >−−− Dxyp λα

])1([22

2

tD

t

xp

t

RE

δδαλ

δδ

δδ −+−=

Dpt

t

t

p)]1([(

)([ 1

2 λλδ

δα −+−=

0)]1)(([

]1)[(1()]1((

212

211

2 >−++

−−−−+−=λλ

ρλλλλptp

ppDp

t

p

35

The first equality is the envelope theorem, the second equality uses the incentive

compatibility condition and third equality uses the equation (3A). Hence, the curve is convex.

From the figure 2, it follows that lR and FR intersect at1t where,

1 11

2 2

(1 )[ ]

[ (1 ) *]

L p y Dt

p y D x

σ λλ

− − +=− − −

and FR and ER curve intersect at 2t where

x

pDyt

.][ 112

ρσ −= .

Hence, the firms having the realization of )(t in the interval of 1[ , ]t t are liquidated while those

in the interval of 1 2[ , ]t t undergo direct refinancing of the public debt. In the range of 1[ , ]t t ,

banks prefer exchange offers.

36

References Beaudry, Paul (1994) “When an Informed Principal May Leave Rents to an Agent” International Economic Review, 35, 821-832. Bebchuk, Lucian Arye, (2002) “Ex Ante Costs of Violating Absolute Priority in Bankruptcy” Journal of Finance, vol. 57, no.1, pp. 445-460. Berkovitch, Israel and Zender (1998) “The Design of Bankruptcy law: A Case for Management Bias in Bankruptcy Reorganizations” Journal of Financial and Quantitative Analysis, vol. 33, no. 4, pp. 441- 464. Betker, Brian L (1995) “Management Incentives, Equity’s Bargaining Power and Deviations from Absolute Priority in Chapter 11 Bankruptcies” Journal of Business, Vol. 68, pp. 161-183. Brown, David, James Christopher and Mooradian (1993) “The Information Content of Distressed Restructuring involving Public and Private Debt Claims”. Journal of Financial Economics,33, pp. 93-118 Bulow, J.I. and J.B, Shoven , (1978) “ The Bankruptcy Decision,” Bell Journal of Economics, vol. 9, pp. 437-456. Chatterjee, S, U.S Dhillon, and G. Ramírez, (1995) “Coercive tender and exchange offers in distressed high-yield debt restructurings An empirical analysis” Journal of Financial Economics, vol. 38, no. 3, pp. 333-360. Eberhart, Allan, Moore, W.T and Roenfeldt (1991) “Security Pricing and Deviations from the Absolute Priority Rule in Bankruptcy Proceedings” Journal of Finance, vol. 45, pp. 1457-1469. Eraslan, H.H.K and Yilmaz, B (2005) ‘‘ Deliberation and Proposal Design in Bankruptcy’’, working paper, Wharton School, University of Pennsylvania Franks, Julian and Torous, Walter (1994) “A Comparison of Financial Recontracting in Distressed Exchanges and Chapter 11 Reorganizations” Journal of Financial Economics, vol. 35, pp. 349-370. Giammarino, R (1989) “ The Resolution of Financial Distress” Review of Financial Studies, vol. 2, pp. 25-47. Gertner, R and D. Scharfstein (1991) “A Theory of Workouts and Effects of Reorganization Law,” Journal of Finance, vol. 46, no. 4, pp. 1189-1222.

37

Gilson, S.C, (1990) “Bankruptcy, Boards, Banks, and Blockholders - Evidence on Changes in Corporate Ownership and Control when Firms Default” Journal of Financial Economics, vol.27, pp. 355-387. Gilson, S.C, Kose John, and L. Lang (1990) “Troubled Debt Restructurings: An Empirical Study of Private Reorganization of Firms in Default” Journal of Financial Economics, vol. 27, pp. 315-353. Gilson, S.C (1993) “Managing Default: Some Evidence on how Firms Choose between Workouts and Chapter 11” p.645-653 in The New Corporate Finance, where Theory Meets Practice, edited by Donald Chew Jr., McGraw Hill Gromb, Denis (2000) ‘‘Lecture Notes on Financial Distress’’ London Business School‘ http://faculty.london.edu/dgromb/assets/documents/sample.pdf Houston, Joel and Christopher James (1996) “Bank Information Monopolies and the Mix of Private and Public Debt Claims” Journal of Finance, vol. 51, pp. 1863-1889.

John, K, Ambarish R and Williams J (1987) "Efficient Signalling with Dividends and Investments," The Journal of Finance, Vol. 42, No. 2.

James, Christopher (1995) “Bank Debt Restructuring and the Composition of Exchange Offers in Financial Distress” The Journal of Finance, vol. 50, pp. 711-727. Keefer, P and knack, S (1995). Institutions and Economic Performances: Cross-Country Tests Using Alternative Alternative Institutional Measures’’ Economics and Politics, 7(13): 207-27 Laporta, R and Lopez-de-Silanes, F, Shleifer, A and Vishny, R (1998) ‘‘Law and finance. Journal of Political Economy 106, pp. 1113–1155. Laporta, R and Lopez-de-Silanes, F (2001) ‘’Creditor Protection and Bankruptcy Law and Reform’’ pp 65-90 in Resolution of Financial Distress: An International Perspective on the Design of Bankruptcy Laws edited by Claessens,S, Djankov,S and Mody, A. . WBI Development Studies. Longhofer, Stanley (1997) “Absolute Priority Rule Violations, Credit Rationing and Efficiency” Journal of Financial Intermediation, vol. 6, pp. 249-267. Mailath, G (1987) “ Incentive Compatibility in Signalling Games with Continuum of Types” Econometrica ,55, 1349-1366. Maskin, Eric and Tirole, Jean (1990) “ The Principal-Agent Relationship with an Informed Principal, I: The Case with Private Values.” Econometrica, 58.379-409.

38

Maskin, Eric and Tirole, Jean (1992) “ The Principal-Agent Relationship with an Informed Principal, II: Common Values.” Econometrica, 60, 1-42. Senbet, L and Seward, J (1995) ‘’ Financial Distress, Bankruptcy and Reorganization" in Finance Handbooks in Operations Research and Management Science {Elsevier Science), Vol. 9, eds., R. Jarrow, et al., pp. 921-961. Tirole, Jean (2005) “The Theory of Corporate Finance’’ MIT Press. Welch, I (1997) “Why is Bank Debt Senior? A Theory of Asymmetry and Claim Priority based on Influence Costs,” Review of Financial Studies, vol. 10, pp. 1203-1236. Weiss, L (1990) “Bankruptcy Resolution: Direct Costs and Violation of Priority Claims”, Journal of Financial Economics, vol. 27, pp. 285 –314. White, M.J (1980) “ Public Policy Towards Bankruptcy: Me-First and Other Priority Rules” Bell Journal of Economics, vol. 11, pp. 550- 564.

39

equity stake

terms of exchange offer

Equilibrium offers separating two types of firms

l αλ

l x

* x

h α

x

A

E C

B

A

E

B

Figure 1

α

40

Expected payoffs of the bank-firm coalition and the choice of methods of workout.

t t2 t1

Figure 2

Rl, RE, RF

RE

RF

Rl

41

Source: Doing Business in 2006: Creating jobs. World Bank Publications

http://www.doingbusiness.org/documents/DoingBusines2006_fullreport.pdf

Table 1