asx / media release for personal use only · asx / media release 3 october 2011 ... of the worlds...

TRANSCRIPT

ASX / MEDIA RELEASE 3 October 2011 Allmine Group Limited (ASX:AZG) Annual Report The Directors of the Allmine Group Limited (Allmine or Allmine Group) are please to table the inaugural Annual Report post its official admission to the Australian Securities Exchange (ASX) on February 28, 2011.

Revenue $29,982,210 +23.9% EBITDA $5,038,280 +33.6% NPAT $3,612,881 +136.49% EPS¹ $0.03 +36.36%

¹ Note: EPS includes shares issued for the acquisition of Arccon (WA) Pty Limited which settled on 30 June 2011.

The Group has achieved a number of milestones since its admission to the ASX these include: Retirement of approximately A$10m in debt; The acquisition of the Karratha based mobile plant business Godfrey’s Fitting

Service (Godfreys) for A$1.8m; The acquisition of the Port Hedland based fixed plant maintenance business

Maxx Engineering Pty Ltd (Maxx Engineering) for $2.25m; The acquisition of Perth based mine design, engineering, procurement and

construction (EPC) company Arccon WA Pty Limited (Arccon) in an all scrip transaction of A$22.8m; and

Secured A$15m in bonding facilities to assist Arccon in delivering into its project pipeline.

The acquisitions of Godfrey’s and Maxx Engineering were bolt-on acquisitions to the Allmine Group’s Maintenance Division to strengthen and expand its maintenance division presence and service proposition to the Pilbara Region. Allmine Maintenance is a leading maintenance service provider across the Pilbara and Northern Territory mining precincts. The Arccon acquisition completed Allmine’s operating strategy of providing a “Life of Mine” service proposition to mineral resource owners, operators and service providers.

For

per

sona

l use

onl

y

The Allmine “Life of Mine” operating model provides services including; Pre-feasibility / Feasibility Assessment; Finance for approved projects; Design and Construction; and Fixed and mobile plant operations and maintenance.

The acquisition of Arccon has provided the Allmine Group with immediate scale, an earnings per share accretive acquisition and delivered a significant project pipeline. The founders and principals of Arccon, Mr Robert Wilde and Mr John McCowan, share in excess of 80 years’ experience in the mineral resources industry, having established Minproc Engineers in 1978, a highly successful mining design, engineering, procurement and construction (EPC) house (now Amec-Minproc). Allmine Group welcomes Mr Robert Wilde to the Board as an Executive Director. Arccon is a unique business in that it operates under Alliance Agreements with two of the worlds largest EPC contractors, the China domiciled China Metallurgical Corporation Ltd (MCC) and China Non-Ferrous Metal Industry’s Foreign Engineering and Construction Co. Ltd (NFC). MCC and NFC deliver substantial engineering capability and resources to enable Arccon to deliver large scale mining EPC projects. A key facet of the Alliance Agreement with NFC is the ability to deliver project finance to the project sponsors. In a world of capital constraint across equity and debt markets, Arccon’s ability to deliver a capital solution its project sponsors is a significant point of differentiation to its peers. Arccon has a significant project pipeline including: US$3bn in projects under Memorandum of Understanding with NFC; A$30m of general engineering works; and A$50m of work-in-progress via its 50% owned construction company,

Construction Industries Australia Ltd. The year ahead of us is extremely promising and exciting. -Ends-

For

per

sona

l use

onl

y

ALLMINE GROUP LIMITED

ACN: 128 806 271

FINANCIAL STATEMENTS FOR THE YEAR ENDED

30 June 2011

For

per

sona

l use

onl

y

2

ALLMINE GROUP LIMITED

ACN: 128 806 271

FINANCIAL STATEMENTS FOR THE YEAR ENDED

30 June 2011

For

per

sona

l use

onl

y

FINANCIAL REPORT

3

This financial report covers the Allmine Group Limited consolidated entity consisting of Allmine Group Limited and its subsidiaries. The financial report is presented in Australian currency unless otherwise stated. Allmine Group Limited is a company limited by shares, incorporated and domiciled in Australia. Its registered office is:

Allmine Group Limited 5 Westside Drive Laverton North VIC 3026

The financial report was authorised for issue by the Directors on 30 September 2011. The company has the power to amend and reissue the financial report.

For

per

sona

l use

onl

y

4

Contents Directors’ Report 5

Corporate Governance Report 12

Statement of Comprehensive Income 17

Statement of Financial Position 18

Statement of Changes of Equity 19

Statement of Cash Flow 20

Notes to Financial Statements 21

Directors’ Declaration 56

Shareholder Information 57

Corporate Directory 60

Auditor’s Independence Declaration 61

Independent Auditor’s Report 62

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

5

Your Directors present their report on the consolidated entity (referred to hereafter as the Group) consisting of Allmine Group Limited and the entities it controlled at the end of, or during, the financial year ended 30 June 2011. 1. General information

(a) Directors The following persons were Directors of Allmine Group Limited at any time during, or since the end of, the year:

Names Period as Director John Darling 30 April 2010 to present Kit Foo Chey 26 April 2010 to present Andrew Howard 29 July 2010 to present Scott Walkem 11 December 2007 to present Robert Wilde 30 June 2011 to present

(b) Company Secretary

. Mr Steve Welsh resigned from the position of Company Secretary on 29 July 2010 and Ms Sophie Karzis was appointed to the position of Company Secretary on 29 July 2010.

(c) Principal Activities

The Allmine Group is a mining service company that provides a “life of mine” service proposition to mine owners, mine operators and their subcontractors. The Groups principal focus is on mineral resource companies.

Allmine Group Limited operates two divisions:

(i) Engineering Division: Design, Engineering, Procurement and Construction via its wholly owned subsidiary Arccon (WA) Pty Ltd; and

(ii) Maintenance Division: Fixed and Mobile Plant maintenance for mining equipment.

The Engineering Division undertakes design, engineering and construction (“EPC”) projects across the globe. The Maintenance Division operates maintenance service centres across Perth, Leinster, Karratha, Port Hedland and Darwin. In addition to the service centres, the Maintenance Division provides mine-site labour hire, field service operations and the sale of after-market earthmoving components across Australia and Fiji.

2. Business Review

(a) Operating Results

The consolidated profit of the Group after providing for income tax amounted to $3,612,881 (2010 profit of $1,527,662).

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

6

(b) Review of Operations

Vision Our vision is for the Allmine Group is to be regarded as a leader and a preferred supplier of services to mineral resource companies via our “life of mine” operating model. Allmine will achieve this by: a) Putting our customers first; b) By offering high quality and value for money service; and c) Operating in an environment that is compliant to the highest standard of Occupational

Health and Safety. Recent Activities The Allmine Group was created to provide a “life of mine” service proposition principally to mineral resource companies. On 28 February 2011 Allmine Group Limited was officially admitted to the Australian Securities Exchange (“ASX”) with a capital raising of $10 million. The initial public offer proceeds were applied to retire debt, acquisition finance and for general working capital purposes. During the year, the Company has focused on the following activities:

• Official admission to the ASX. • Acquisition of the Karratha based mobile plant maintenance business Godfrey’s Fitting

Service for $1.8 million. • Acquisition of the Perth based mining EPC company Arccon (WA) Pty Ltd (“Arccon”) for

$22.8 million. • Retirement of approximately $10 million in group debt facilities. • The Company entered into a binding terms sheet to acquire the Port Hedland based mining

fixed plant maintenance business Maxx Engineering Pty Limited (“Maxx Engineering”) for $2.25 million.

(c) Dividends

No dividends were paid or declared since the start of the financial year (2010: no dividends).

3. Other items

(a) Significant Changes in State of Affairs

There were no significant changes in the Company’s state of affairs.

(b) Events Subsequent to Reporting Date

In the period subsequent to Reporting Date, the Group has undertaken a number of financing and other activities, as follows:

• Secured a $15 million bonding facility; • Undertaken a global refinance of $16million for the Group bonding and working capital

requirements; and

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

7

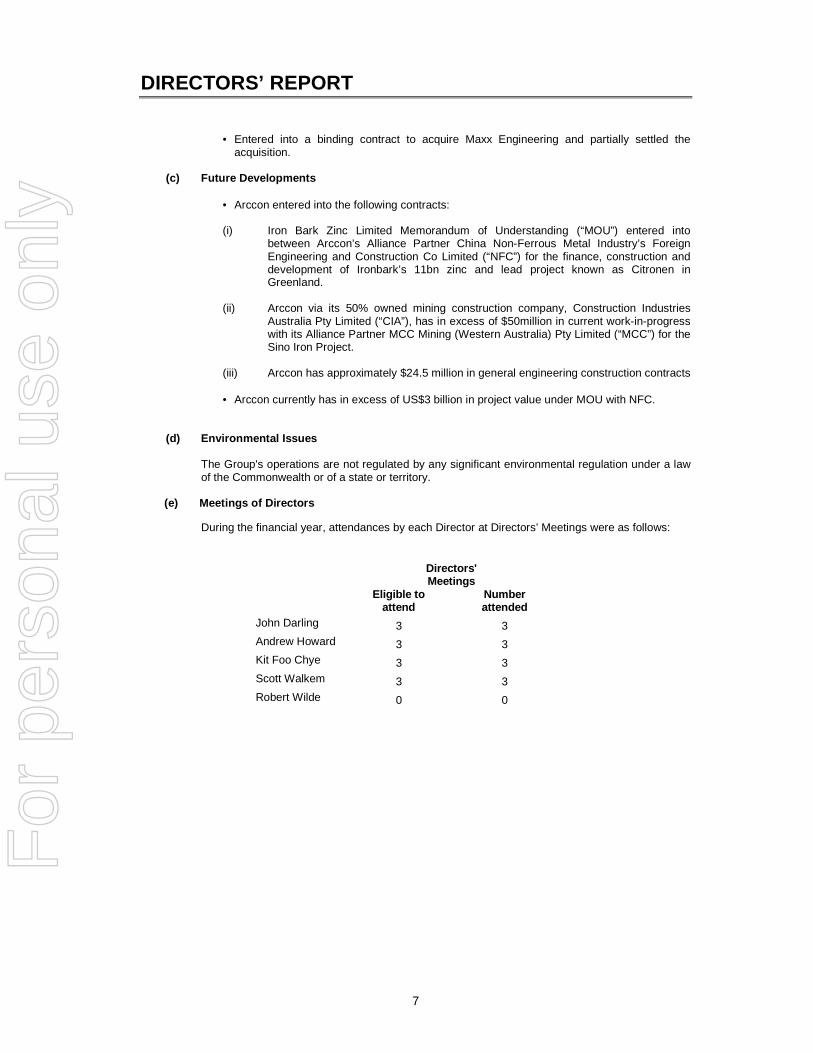

• Entered into a binding contract to acquire Maxx Engineering and partially settled the

acquisition.

(c) Future Developments

• Arccon entered into the following contracts: (i) Iron Bark Zinc Limited Memorandum of Understanding (“MOU”) entered into

between Arccon’s Alliance Partner China Non-Ferrous Metal Industry’s Foreign Engineering and Construction Co Limited (“NFC”) for the finance, construction and development of Ironbark’s 11bn zinc and lead project known as Citronen in Greenland.

(ii) Arccon via its 50% owned mining construction company, Construction Industries

Australia Pty Limited (“CIA”), has in excess of $50million in current work-in-progress with its Alliance Partner MCC Mining (Western Australia) Pty Limited (“MCC”) for the Sino Iron Project.

(iii) Arccon has approximately $24.5 million in general engineering construction contracts

• Arccon currently has in excess of US$3 billion in project value under MOU with NFC.

(d) Environmental Issues

The Group's operations are not regulated by any significant environmental regulation under a law of the Commonwealth or of a state or territory.

(e) Meetings of Directors

During the financial year, attendances by each Director at Directors’ Meetings were as follows:

Directors' Meetings

Eligible to

attend Number attended

John Darling 3 3 Andrew Howard 3 3 Kit Foo Chye 3 3 Scott Walkem 3 3 Robert Wilde 0 0

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

8

Remuneration Report – Audited This remuneration report sets out the remuneration information for each of the Group’s key management personnel including the directors. Role of the Remuneration Committee The remuneration Committee is a committee of the Board. It is primarily responsible for making recommendations to the Board in:

- non-executive directors fees; - executive remuneration (directors and other executives); and - the over-arching executive remuneration framework and incentive plan policies

Their objective is to ensure that remuneration policies and structures are fair and competitive and aligned with the long-term interests of the Company. The Corporate Governance Statement provides further information on the role of the Committee. Remuneration Policy The remuneration policy of Allmine has been designed to align key management personnel objectives with the shareholder and business objectives by providing a fixed remuneration component and offering specific medium term incentives based on key performance areas affecting the Group’s financial result. The Board of Allmine believes the remuneration policy to be appropriate and effective in its ability to attract and retain the best key management personnel to run and manage the Group, as well as create goal congruence between directors, executives and shareholders. Emoluments of directors and senior executives are set by reference to payments made by other companies of similar size in the industry and by reference to the skills and experience of those directors and executives. Non-Executive Directors The Group’s policy is to remunerate non-executive directors at market rates (for comparable companies) for time, commitment and responsibilities. Fees for non-executive directors are not linked to performance of the Group, however to align directors’ interests with shareholders’ interests, directors are encouraged to hold shares in the Group. The maximum aggregate amount of fees that can be paid to non-executive directors is subject to approval by shareholders at the Annual General Meeting Executive Directors Executive pay and rewards consist of a competitive level of base salary and some performance incentives. Medium to long term incentives may consist of options granted at the discretion of the Board, and which are subject to shareholder approval. Senior Executives Executive pay and reward consists of base salary and some performance incentives. Performance incentives to date have comprised cash bonuses recommended by the Chief Executive Officer and approved by the Board. Executive remuneration may be tailored to the executives’ discretion, through a combination of

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

9

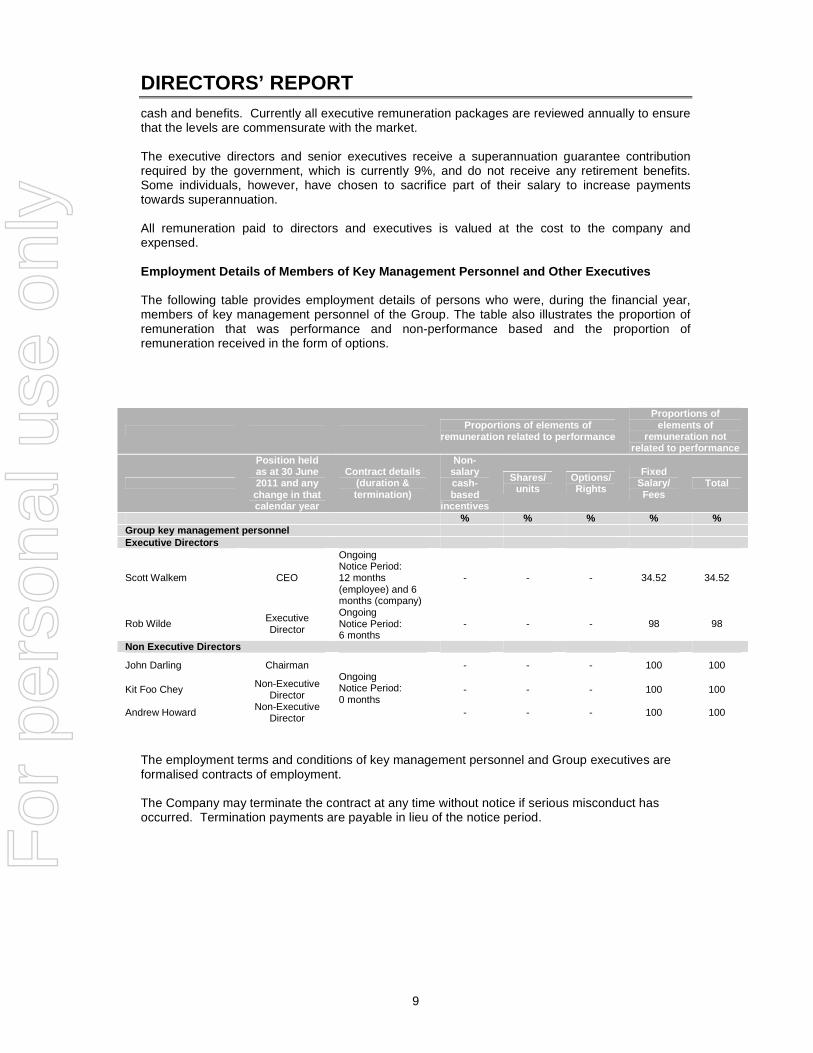

cash and benefits. Currently all executive remuneration packages are reviewed annually to ensure that the levels are commensurate with the market. The executive directors and senior executives receive a superannuation guarantee contribution required by the government, which is currently 9%, and do not receive any retirement benefits. Some individuals, however, have chosen to sacrifice part of their salary to increase payments towards superannuation. All remuneration paid to directors and executives is valued at the cost to the company and expensed. Employment Details of Members of Key Management Per sonnel and Other Executives The following table provides employment details of persons who were, during the financial year, members of key management personnel of the Group. The table also illustrates the proportion of remuneration that was performance and non-performance based and the proportion of remuneration received in the form of options.

Proportions of elements of remuneration related to performance

Proportions of elements of

remuneration not related to performance

Position held as at 30 June 2011 and any change in that calendar year

Contract details (duration & termination)

Non-salary cash-based

incentives

Shares/ units

Options/ Rights

Fixed Salary/ Fees

Total

% % % % % Group key management personnel Executive Directors

Scott Walkem CEO

Ongoing Notice Period: 12 months (employee) and 6 months (company)

- - - 34.52 34.52

Rob Wilde Executive Director

Ongoing Notice Period: 6 months

- - - 98 98

Non Executive Directors

John Darling Chairman - - - 100 100

Kit Foo Chey Non-Executive Director - - - 100 100

Andrew Howard Non-Executive Director

Ongoing Notice Period: 0 months

- - - 100 100

The employment terms and conditions of key management personnel and Group executives are formalised contracts of employment. The Company may terminate the contract at any time without notice if serious misconduct has occurred. Termination payments are payable in lieu of the notice period. F

or p

erso

nal u

se o

nly

DIRECTORS’ REPORT

10

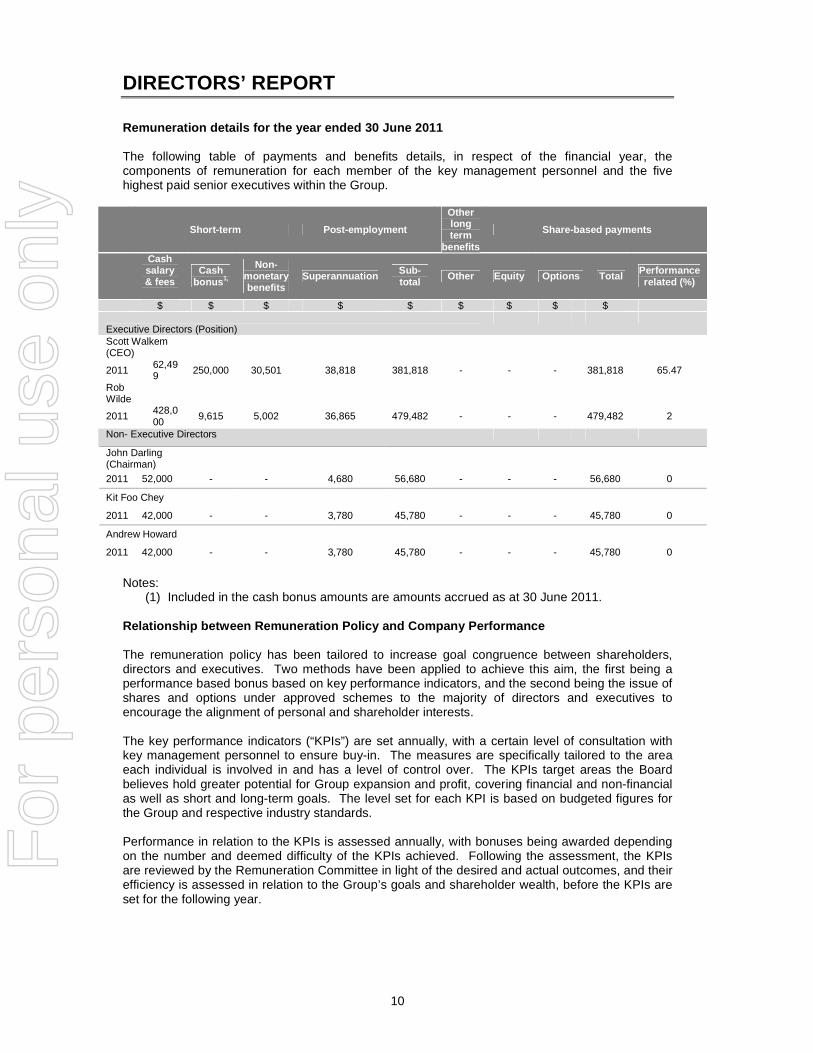

Remuneration details for the year ended 30 June 201 1 The following table of payments and benefits details, in respect of the financial year, the components of remuneration for each member of the key management personnel and the five highest paid senior executives within the Group.

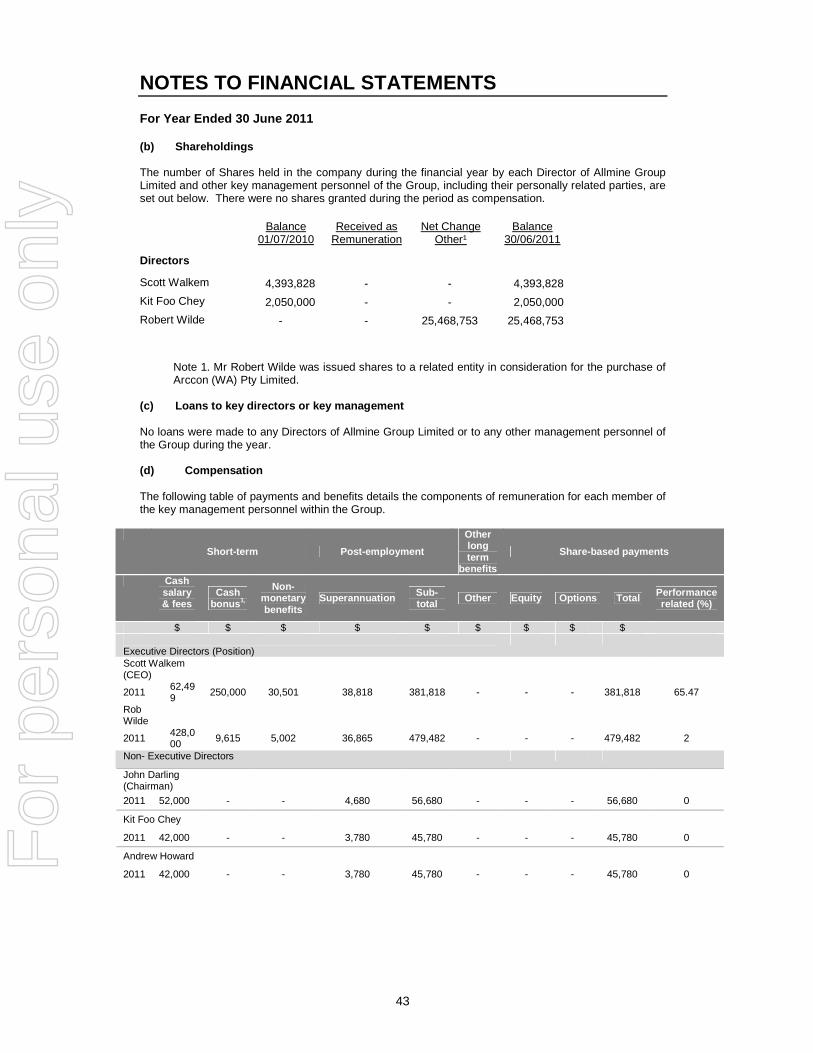

Short-term Post-employment

Other long term

benefits

Share-based payments

Cash salary & fees

Cash bonus 1,

Non-monetary benefits

Superannuation Sub-total Other Equity Options Total Performance

related (%)

$ $ $ $ $ $ $ $ $ Executive Directors (Position)

Scott Walkem (CEO)

2011 62,499 250,000 30,501 38,818 381,818 - - - 381,818 65.47

Rob Wilde

2011 428,000

9,615 5,002 36,865 479,482 - - - 479,482 2

Non- Executive Directors

John Darling (Chairman)

2011 52,000 - - 4,680 56,680 - - - 56,680 0

Kit Foo Chey

2011 42,000 - - 3,780 45,780 - - - 45,780 0

Andrew Howard

2011 42,000 - - 3,780 45,780 - - - 45,780 0

Notes:

(1) Included in the cash bonus amounts are amounts accrued as at 30 June 2011. Relationship between Remuneration Policy and Compan y Performance The remuneration policy has been tailored to increase goal congruence between shareholders, directors and executives. Two methods have been applied to achieve this aim, the first being a performance based bonus based on key performance indicators, and the second being the issue of shares and options under approved schemes to the majority of directors and executives to encourage the alignment of personal and shareholder interests. The key performance indicators (“KPIs”) are set annually, with a certain level of consultation with key management personnel to ensure buy-in. The measures are specifically tailored to the area each individual is involved in and has a level of control over. The KPIs target areas the Board believes hold greater potential for Group expansion and profit, covering financial and non-financial as well as short and long-term goals. The level set for each KPI is based on budgeted figures for the Group and respective industry standards. Performance in relation to the KPIs is assessed annually, with bonuses being awarded depending on the number and deemed difficulty of the KPIs achieved. Following the assessment, the KPIs are reviewed by the Remuneration Committee in light of the desired and actual outcomes, and their efficiency is assessed in relation to the Group’s goals and shareholder wealth, before the KPIs are set for the following year.

For

per

sona

l use

onl

y

DIRECTORS’ REPORT

11

Performance income as a proportion of total remuner ation Executive directors and senior executives may be paid performance based bonuses based on set monetary figures, rather than proportions of their salary. This has led to the proportions of remuneration related to performance varying between individuals. The Remuneration Committee has set these bonuses to encourage achievement of specific goals that have been given a high level of importance in relation to the future growth and profitability of the Group. The Remuneration Committee will review the performance bonuses to gauge their effectiveness against achievement of the set goals, and adjust any future years’ incentives as they see fit, to ensure use of the most cost effective and efficient methods. Corporate Governance The directors of the Company support and adhere to the principles of corporate governance, and recognise the need to achieve the highest possible standards of corporate behaviour and accountability. A review of the Company’s corporate governance practices was undertaken during the year. As a result, new practices were adopted and existing practices optimised to reflect best industry practice. Please refer to the Corporate Governance Statement contained in this report. Auditor’s Independence Declaration A copy of the auditor’s independence declaration as required under section 307C of the Corporations Act 2001 is set out on page 61. The Directors’ Report, incorporating the Remuneration Report, is signed in accordance with a resolution of the Board of Directors. Signed in accordance with a resolution of the Board of Directors:

Director………………………………… Dated this 30th day of September 2011.

For

per

sona

l use

onl

y

CORPORATE GOVERNANCE REPORT

12

The Board of Directors of Allmine Group Limited (the “Company” or “Allmine”) is responsible for the corporate governance of the Company. The Board guides and monitors the business and affairs of Allmine on behalf of the shareholders by whom they are elected and to whom they are accountable.

To ensure that the Board is well equipped to discharge its responsibilities, it has established guidelines for the nomination and selection of directors and for the operation of the Board.

COMPOSITION OF THE BOARD

The composition of the Board is determined in accordance with the following principles and guidelines:

• the Board should comprise at least three directors and it intends to establish a majority of

non-executive directors; • the Chairman should be a non-executive director; • the Board should comprise directors with an appropriate range of qualifications and expertise;

and • the Board shall meet at regular intervals and follow meeting guidelines set down to ensure all

directors are made aware of, and have available all necessary information, to participate in an informed discussion of all agenda items.

When a vacancy exists, through whatever cause, or where it is considered that the Board would benefit from the service of a new director with particular skills, the Board selects a candidate or panel of candidates with the appropriate expertise.

The Board then appoints the most suitable candidate, who must stand for election at the next general meeting of shareholders.

REMUNERATION COMMITTEE

The Company has in place a policy for an HR and Remuneration Committee. At present, this committee is made up of the full Board who undertake the necessary roles and responsibilities of the committee.

Remuneration levels are set by the Board in accordance with industry standards to attract suitable qualified and experienced directors and senior executives.

AUDIT COMMITTEE

The Company has in place a policy for an Audit, Risk and Compliance Committee. At present, this committee is made up of the full Board who undertake the necessary roles and responsibilities of the committee.

BOARD RESPONSIBILITIES

As the Board acts on behalf of and is accountable to the shareholders, it seeks to identify the expectations of the shareholders, as well as other regulatory and ethical expectations and obligations. In addition, the Board is responsible for identifying areas of significant business risk and ensuring arrangements are in place to adequately manage those risks. The Board seeks to discharge these responsibilities in a number of ways.

The responsibility for the operation and administration of the Company is managed by the Board and, where appropriate, delegated to the Chief Executive Officer, Chief Financial Officer or Company Secretary.

The Board ensures that any Company appointments, albeit officers, contractors and consultants are appropriately qualified and experienced to discharge their responsibilities, and that procedures are in place to assess the performance of any roles carried out by any officer, contractor and consultant to the Company.

For

per

sona

l use

onl

y

CORPORATE GOVERNANCE REPORT

13

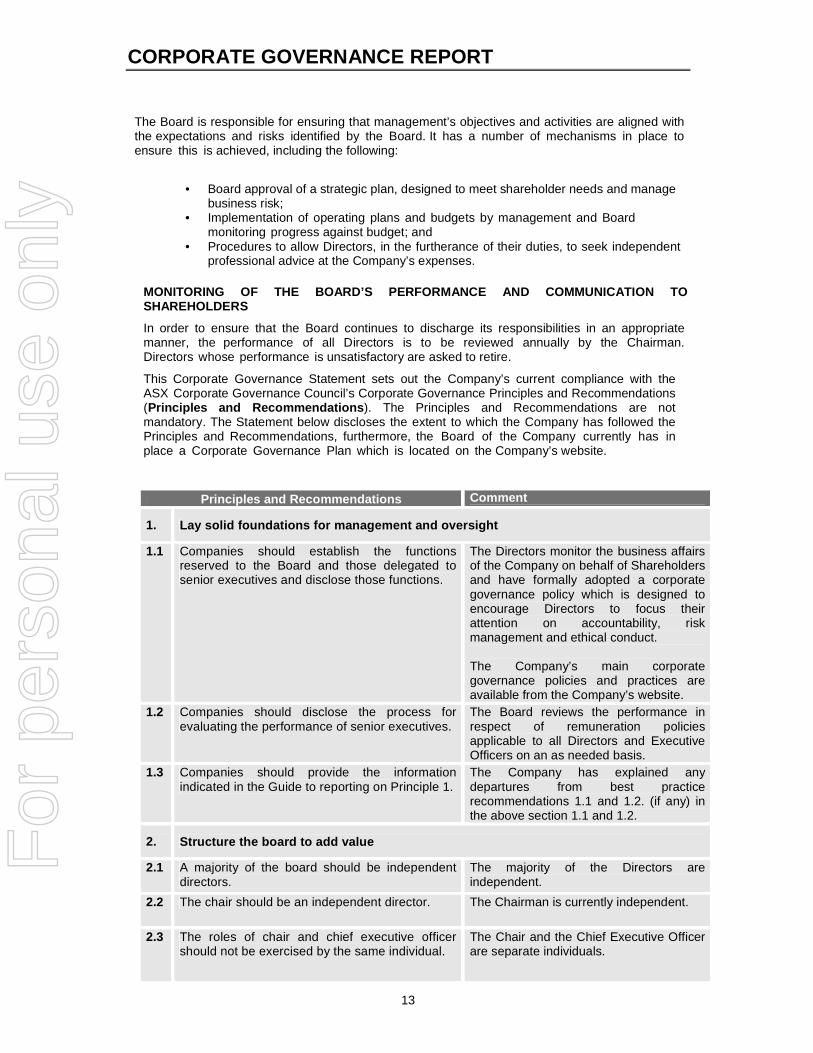

The Board is responsible for ensuring that management’s objectives and activities are aligned with the expectations and risks identified by the Board. It has a number of mechanisms in place to ensure this is achieved, including the following:

• Board approval of a strategic plan, designed to meet shareholder needs and manage business risk;

• Implementation of operating plans and budgets by management and Board monitoring progress against budget; and

• Procedures to allow Directors, in the furtherance of their duties, to seek independent professional advice at the Company’s expenses.

MONITORING OF THE BOARD’S PERFORMANCE AND COMMUNICA TION TO SHAREHOLDERS

In order to ensure that the Board continues to discharge its responsibilities in an appropriate manner, the performance of all Directors is to be reviewed annually by the Chairman. Directors whose performance is unsatisfactory are asked to retire.

This Corporate Governance Statement sets out the Company’s current compliance with the ASX Corporate Governance Council’s Corporate Governance Principles and Recommendations (Principles and Recommendations ). The Principles and Recommendations are not mandatory. The Statement below discloses the extent to which the Company has followed the Principles and Recommendations, furthermore, the Board of the Company currently has in place a Corporate Governance Plan which is located on the Company’s website.

Principles and Recommendations Comment

1. Lay solid foundations for management and oversight

1.1 Companies should establish the functions reserved to the Board and those delegated to senior executives and disclose those functions.

The Directors monitor the business affairs of the Company on behalf of Shareholders and have formally adopted a corporate governance policy which is designed to encourage Directors to focus their attention on accountability, risk management and ethical conduct. The Company’s main corporate governance policies and practices are available from the Company’s website.

1.2 Companies should disclose the process for evaluating the performance of senior executives.

The Board reviews the performance in respect of remuneration policies applicable to all Directors and Executive Officers on an as needed basis.

1.3 Companies should provide the information indicated in the Guide to reporting on Principle 1.

The Company has explained any departures from best practice recommendations 1.1 and 1.2. (if any) in the above section 1.1 and 1.2.

2. Structure the board to add value

2.1 A majority of the board should be independent directors.

The majority of the Directors are independent.

2.2 The chair should be an independent director. The Chairman is currently independent.

2.3 The roles of chair and chief executive officer should not be exercised by the same individual.

The Chair and the Chief Executive Officer are separate individuals.

For

per

sona

l use

onl

y

CORPORATE GOVERNANCE REPORT

14

2.4 The board should establish a nomination committee.

The Company has in place a policy for an HR & Remuneration Committee who perform the roles and responsibilities of a Nomination Committee. Currently this committee is made up of the Board of Directors.

2.5 Companies should disclose the process for evaluating the performance of the board, its committees and individual directors.

The HR & Remuneration Committee, currently made up of the Board, evaluate the performance of directors. The performance of all Executive Directors will be reviewed at least annually.

2.6 Companies should provide the information indicated in the Guide to reporting on Principle 2.

The Company will provide details of each Director, such as their skills, experience and expertise relevant to their position. The Company has provided an explanation of any departures from best practice recommendations 2.1, 2.2, 2.3, 2.4 and 2.5, (if any) in sections 2.1 to 2.5 above.

3. Promote ethical and responsible decision-making

3.1 Companies should establish a code of conduct and disclose the code or a summary of the code as to:

• the practices necessary to maintain confidence in the company’s integrity

• the practices necessary to take into account their legal obligations and the reasonable expectations of their stakeholders the responsibility and accountability of individuals for reporting and investigating reports of unethical practices.

The Company has a Code of Conduct as part of its Corporate Governance Plan that addresses these issues.

3.2 Companies should establish a policy concerning diversity and disclose the policy or a summary of that policy. The policy should include requirements for the board to establish measureable objectives for achieving gender diversity and for the board to assess annually both the objectives and progress in achieving them.

The Company has a Diversity and Equal Opportunities Policy as part of their Corporate Governance Plan.

3.3 Companies should disclose in each annual report the measureable objectives for achieving set by the board in accordance with the diversity policy and progress in achieving them.

The Company has not yet set measurable objectives however these will be considered by the Board. The Board will review progress against any objectives identified on an annual basis.

3.4 Companies should disclose in each annual report the proportion of women employees in the whole organisation, women in senior executive positions and women on the board.

The Company’s only office holding below the Board level, this being the position of Company Secretary.

3.5 Companies should provide the information indicated in the Guide to reporting on Principle 3.

The Board will include in the Annual Report each year:

• measurable objectives, if any, set by the Board; and

• progress against the objectives.

4. Safeguard integrity in financial reporting

For

per

sona

l use

onl

y

CORPORATE GOVERNANCE REPORT

15

4.1 The board should establish an audit committee. The Company has an Audit, Risk and Compliance Committee, currently made up of the Board.

4.2 The audit committee should be structured so that it:

• consists only of non-executive directors • consists of a majority of independent

directors • is chaired by an independent chair, who is

not chair of the board • has at least three members.

The Board of Directors, who make up the Committee, currently comprises one Non-Executive Chairman and two Non-Executive Directors, all of whom are independent. The majority of the committee are independent.

4.3 The audit committee should have a formal charter.

The formal charter can be found on the Company’s website.

4.4 Companies should provide the information indicated in the Guide to reporting on Principle 4.

The Company has explained any departures from best practice recommendations 4.1, 4.2 and 4.3 (if any) in the above sections 4.1 to 4.3 above.

5. Make timely and balanced disclosure

5.1 Companies should establish written policies designed to ensure compliance with ASX Listing Rule disclosure requirements and to ensure accountability at a senior executive level for that compliance and disclose those policies or a summary of those policies.

The Company has a continuous disclosure program in place designed to ensure the compliance with ASX Listing Rule on continuous disclosure and to ensure accountability at a senior executive level for compliance and factual presentation of the Company’s financial position.

5.2 Companies should provide the information indicated in Guide to Reporting on Principle 5.

The Company has provided an explanation of any departures from best practice recommendation 5.1 (if any) in section 5.1 above.

6. Respect the rights of shareholders

6.1 Companies should design a communications policy for promoting effective communication with shareholders and encouraging their participation at general meetings and disclose their policy or a summary of that policy.

The Company has in place a Market Disclosure and Communications Policy to encourage effective communication.

6.2 Companies should provide the information indicated in the Guide to reporting on Principle 6.

The Company has provided an explanation of any departures from best practice recommendation 6.1 (if any) in section 6.1 above.

7. Recognise and manage risk

7.1 Companies should establish policies for the oversight and management of material business risks and disclose a summary of those policies.

The Board is responsible for ensuring there are adequate policies in relation to risk management, compliance and internal control systems. In summary, the Company’s policies are designed to ensure strategic, operational, legal, reputational and financial risks are identified, assessed, effectively and efficiently managed and monitored to enable achievement of the Company’s business objectives.

For

per

sona

l use

onl

y

CORPORATE GOVERNANCE REPORT

16

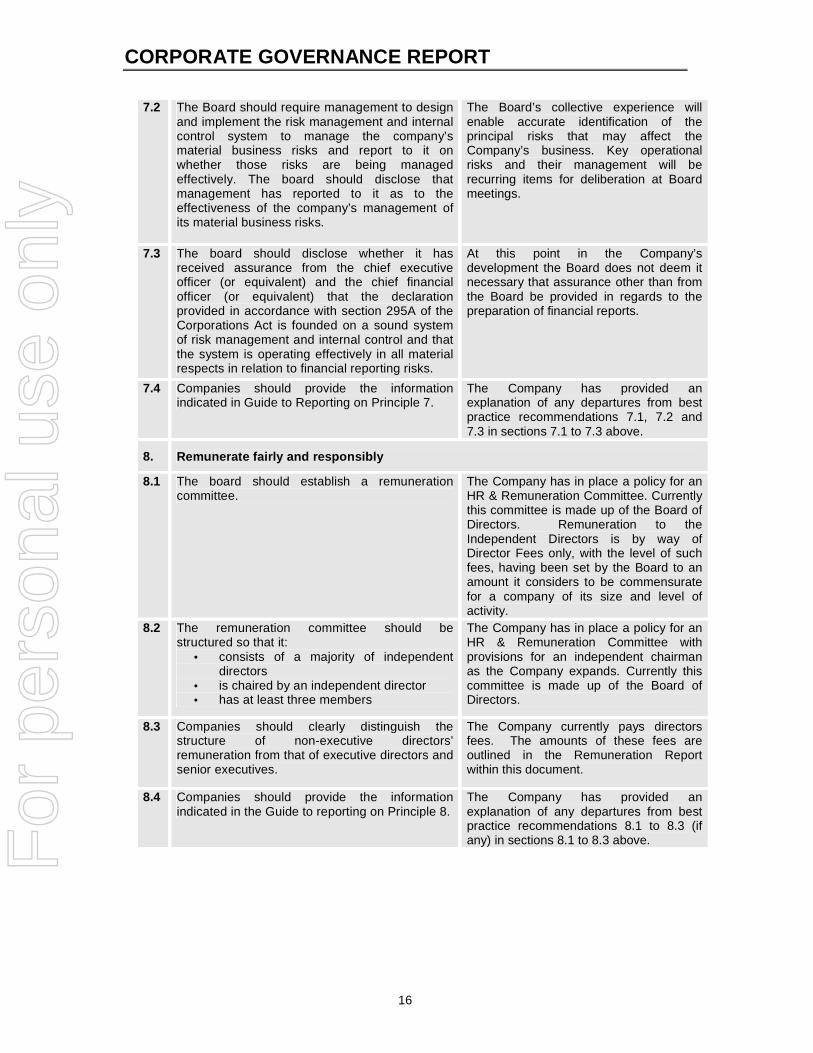

7.2 The Board should require management to design and implement the risk management and internal control system to manage the company’s material business risks and report to it on whether those risks are being managed effectively. The board should disclose that management has reported to it as to the effectiveness of the company’s management of its material business risks.

The Board’s collective experience will enable accurate identification of the principal risks that may affect the Company’s business. Key operational risks and their management will be recurring items for deliberation at Board meetings.

7.3 The board should disclose whether it has received assurance from the chief executive officer (or equivalent) and the chief financial officer (or equivalent) that the declaration provided in accordance with section 295A of the Corporations Act is founded on a sound system of risk management and internal control and that the system is operating effectively in all material respects in relation to financial reporting risks.

At this point in the Company’s development the Board does not deem it necessary that assurance other than from the Board be provided in regards to the preparation of financial reports.

7.4 Companies should provide the information indicated in Guide to Reporting on Principle 7.

The Company has provided an explanation of any departures from best practice recommendations 7.1, 7.2 and 7.3 in sections 7.1 to 7.3 above.

8. Remunerate fairly and responsibly

8.1 The board should establish a remuneration committee.

The Company has in place a policy for an HR & Remuneration Committee. Currently this committee is made up of the Board of Directors. Remuneration to the Independent Directors is by way of Director Fees only, with the level of such fees, having been set by the Board to an amount it considers to be commensurate for a company of its size and level of activity.

8.2 The remuneration committee should be structured so that it:

• consists of a majority of independent directors

• is chaired by an independent director • has at least three members

The Company has in place a policy for an HR & Remuneration Committee with provisions for an independent chairman as the Company expands. Currently this committee is made up of the Board of Directors.

8.3 Companies should clearly distinguish the structure of non-executive directors’ remuneration from that of executive directors and senior executives.

The Company currently pays directors fees. The amounts of these fees are outlined in the Remuneration Report within this document.

8.4 Companies should provide the information indicated in the Guide to reporting on Principle 8.

The Company has provided an explanation of any departures from best practice recommendations 8.1 to 8.3 (if any) in sections 8.1 to 8.3 above. F

or p

erso

nal u

se o

nly

STATEMENT OF COMPREHENSIVE INCOME

17

For the Year Ended 30 June 2011

Consolidated 2011 2010 $ $ Note

Revenue 5 29,982,210 24,197,994 Cost of sales 17,553,511 13,312,959 Gross profit 12,428,699 10,885,035 Administrative expenses 4,278,740 4,232,776 Depreciation and amortisation expense 813,394 749,178 Finance expenses 1,418,583 1,511,452 Marketing expenses 57,684 120,892 Occupancy expenses 881,243 1,110,519 Other expenses 2,172,752 1,651,522

Profit before income tax 2,806,303 1,508,696

Income tax benefit / (expense) 7 806,578 18,966

Profit from continuing operations 3,612,881 1,527,662

Profit for the period 3,612,881 1,527,662

Profit is attributable to:

Equity holders of the parent 3,612,881 1,527,662

Cents Cents

Earnings per share for profit from continuing operations

Basic earnings per share $0.030 $0.022

Diluted earnings per share $0.020 $0.016

The above statements should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

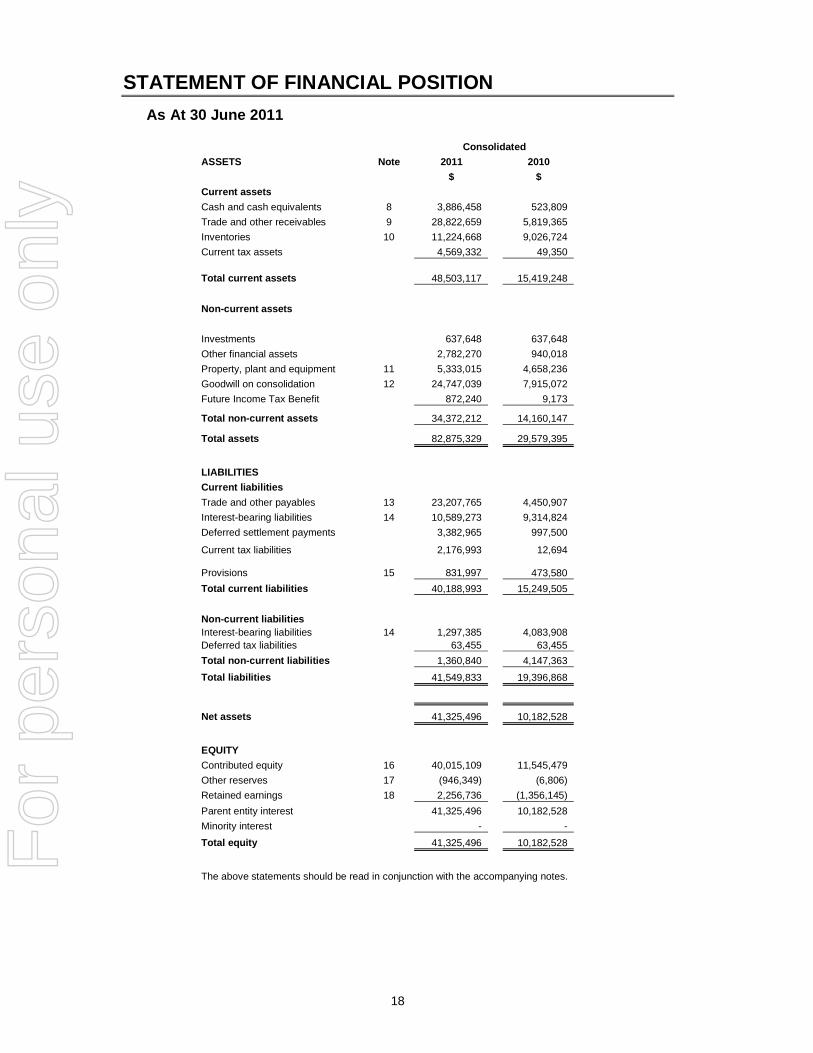

STATEMENT OF FINANCIAL POSITION

18

As At 30 June 2011

Consolidated

ASSETS Note 2011 2010

$ $

Current assets

Cash and cash equivalents 8 3,886,458 523,809

Trade and other receivables 9 28,822,659 5,819,365

Inventories 10 11,224,668 9,026,724

Current tax assets 4,569,332 49,350

Total current assets 48,503,117 15,419,248

Non-current assets

Investments 637,648 637,648

Other financial assets 2,782,270 940,018

Property, plant and equipment 11 5,333,015 4,658,236

Goodwill on consolidation 12 24,747,039 7,915,072

Future Income Tax Benefit 872,240 9,173

Total non-current assets 34,372,212 14,160,147

Total assets 82,875,329 29,579,395

LIABILITIES

Current liabilities

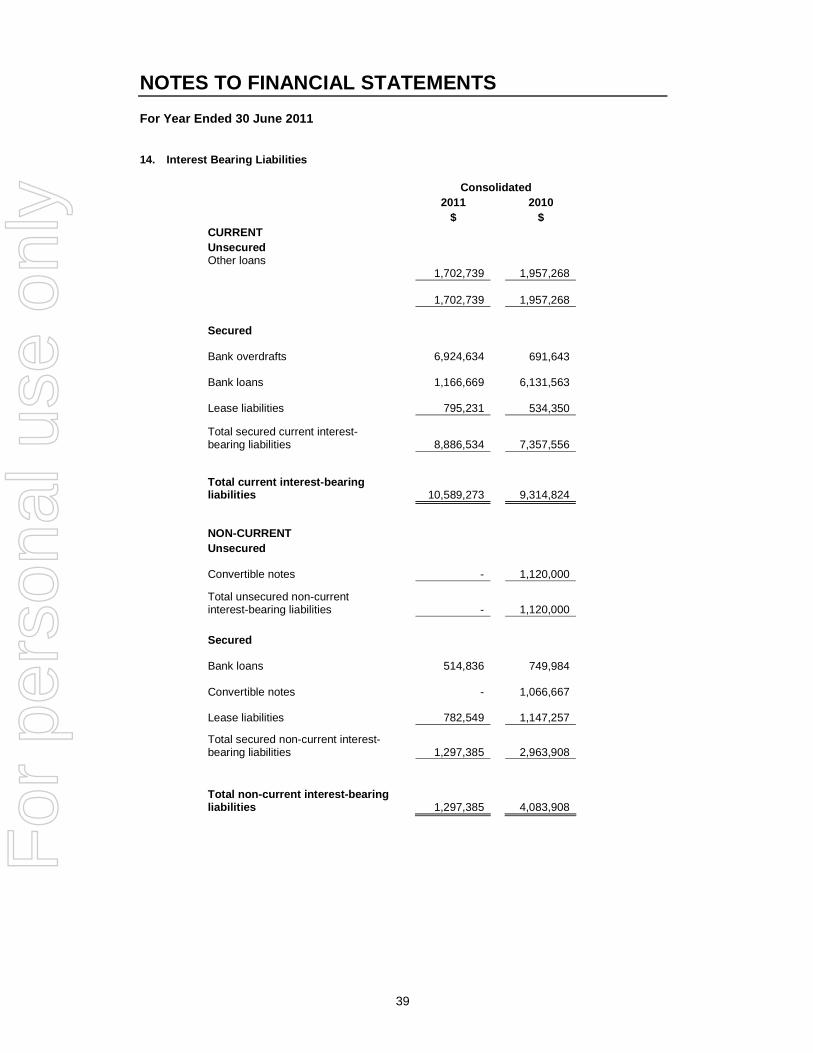

Trade and other payables 13 23,207,765 4,450,907

Interest-bearing liabilities 14 10,589,273 9,314,824

Deferred settlement payments 3,382,965 997,500

Current tax liabilities 2,176,993 12,694

Provisions 15 831,997 473,580

Total current liabilities 40,188,993 15,249,505

Non-current liabilities Interest-bearing liabilities 14 1,297,385 4,083,908 Deferred tax liabilities 63,455 63,455

Total non-current liabilities 1,360,840 4,147,363

Total liabilities 41,549,833 19,396,868

Net assets 41,325,496 10,182,528

EQUITY

Contributed equity 16 40,015,109 11,545,479

Other reserves 17 (946,349) (6,806)

Retained earnings 18 2,256,736 (1,356,145)

Parent entity interest 41,325,496 10,182,528

Minority interest - -

Total equity 41,325,496 10,182,528

The above statements should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

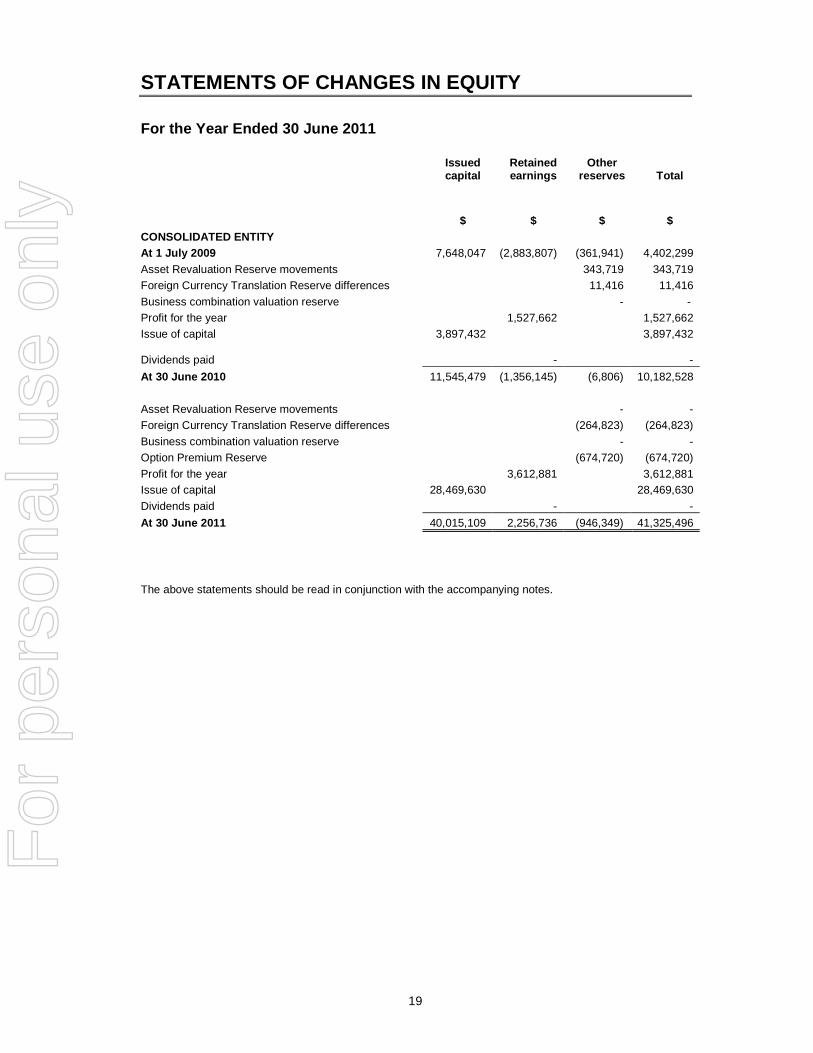

STATEMENTS OF CHANGES IN EQUITY

19

For the Year Ended 30 June 2011

Issued capital

Retained earnings

Other reserves Total

$ $ $ $ CONSOLIDATED ENTITY At 1 July 2009 7,648,047 (2,883,807) (361,941) 4,402,299

Asset Revaluation Reserve movements 343,719 343,719 Foreign Currency Translation Reserve differences 11,416 11,416

Business combination valuation reserve - - Profit for the year 1,527,662 1,527,662 Issue of capital 3,897,432 3,897,432

Dividends paid

-

-

At 30 June 2010 11,545,479 (1,356,145) (6,806) 10,182,528

Asset Revaluation Reserve movements - - Foreign Currency Translation Reserve differences (264,823) (264,823)

Business combination valuation reserve - - Option Premium Reserve (674,720) (674,720)

Profit for the year 3,612,881 3,612,881 Issue of capital 28,469,630 28,469,630

Dividends paid - -

At 30 June 2011 40,015,109 2,256,736 (946,349) 41,325,496

The above statements should be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

STATEMENT OF CASH FLOW

20

For the Year Ended 30 June 2011

Consolidated 2011 2010 $ $ Note

Cash flows from operating activities

Cash receipts from customers 25,810,218 26,617,793

Cash paid to suppliers and employees (24,298,313) (26,038,471)

Interest received 72,997 4,811 Interest paid (1,239,249) (1,323,852) Income taxes paid (17,726) -

Net cash inflow/(outflow) from operating activities 24 327,927 (739,719)

Cash flows from investing activities

Acquisition of subsidiary, net of cash acquired (19,106,265) -

Purchase of property, plant and equipment (275,245) (1,607,156)

Purchase of intangible assets (1,591,042) - Purchase of other financial assets (71,279) -

Proceeds from sale of property, plant and equipment 38,183 -

Loans to related parties - -

Net cash inflow/(outflow) from investing activities (21,005,648) (1,607,156)

Cash flows from financing activities

Proceeds from issue of shares 28,469,630 3,692,180 Proceeds from borrowings - 2,050,000 Repayment of borrowings (10,364,329) (3,250,00)

Net cash inflow/(outflow) from financing activities 18,105,301 2,492,180

Net (decrease)/increase in cash and cash equivalents (2,622,101) 145,305

Net foreign exchange differences (248,241) 11,416

Cash and cash equivalents at beginning of period (167,834) (324,555)

Cash and cash equivalents at end of period 8 (3,038,176) (167,834)

The above statements should be read in conjunction with the accompanying notes.

F

or p

erso

nal u

se o

nly

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

21

1. Statement of Significant Accounting Policies

The principal accounting policies adopted in the preparation of the financial report are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

(a) Basis of preparation

This general purpose financial report has been prepared in accordance with the Australian Accounting Standards (AASBs) (including Australian Accounting interpretations) adopted by the Australian Accounting Standards Board (AASB), and the Corporations Act 2001. Compliance with IFRS Australian Accounting Standards include Australian equivalents to International Financial Reporting Standards (AIFRS). Compliance with AIFRS ensures that the consolidated financial statements and notes of Allmine Group Limited comply with International Financial Reporting Standards (IFRS) and interpretations adopted by the International Accounting Standards Board (IASB).

Historical Cost Convention These financial statements have been prepared under the historical cost convention other than for items required to be brought to account at fair value as stated throughout. Critical Accounting Estimates The preparation of financial statements in conformity with AIFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Group’s accounting policies.

(b) Principles of Consolidation

Subsidiaries The consolidated financial statements incorporate the assets and liabilities of all subsidiaries of Allmine Group Limited (''company'' or ''parent entity'') as at 30 June 2011 and the results of all subsidiaries for the year then ended. Allmine Group Limited and its subsidiaries together are referred to in this financial report as the Group or the consolidated entity. Subsidiaries are all those entities over which the Group has the power to govern the financial and operating policies, generally accompanying a shareholding of more than one half of the voting rights. The existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing whether the Group controls another entity. Subsidiaries are fully consolidated from the date on which control is transferred to the Group. The accounting policies of subsidiaries have been changed where necessary to align them with the policies adopted by the Group. The purchase method of accounting is used to account for the acquisition of subsidiaries by the Group (refer to Note 1(d)). Intercompany transactions, balances and unrealised gains on transactions between Group companies are eliminated. Unrealised losses are also eliminated unless the transaction provides evidence of the impairment of the asset transferred. Accounting policies of subsidiaries have been changed where necessary to ensure consistency with the policies adopted by the Group.

Investments in subsidiaries are accounted for at cost in the parent financial statements of Allmine Group Limited.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

22

(c) Going Concern

As a growing business the Group has experienced an operating profit of $3,612,881. The Directors believe that the Group will be able to access sufficient sources of funds and, accordingly, have prepared the financial report on a going concern basis. At this time, the Directors are of the opinion that no asset is likely to be realised for an amount less than the amount at which it is recorded in the financial report at 30 June 2011. Accordingly, no adjustments have been made to the financial report relating to the recoverability and classification of the asset carrying amounts or the amount and classification of liabilities that might be necessary should the Group not continue as a going concern.

(d) Business Combinations

The purchase method of accounting is used to account for all business combinations, including business combinations involving entities or businesses under common control, regardless of whether equity instruments or other assets are acquired. Cost is measured as the fair value of the assets given, equity instruments issued or liabilities incurred or assumed at the date of exchange plus costs directly attributable to the acquisition. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date, irrespective of the extent of any minority interest. The excess of the cost of acquisition over the fair value of the Group’s share of the identifiable net assets acquired is recorded as goodwill (refer to Note 1(j)). If the cost of acquisition is less than the Group's share of the fair value of the identifiable net assets of the subsidiary acquired, the difference is recognised directly in the statement of comprehensive income, but only after a reassessment of the identification and measurement of the net assets acquired. Where settlement of any part of cash consideration is deferred, the amounts payable in the future are discounted to their present value as at the date of exchange. The discount rate used is the Company’s incremental borrowing rate, being the rate at which a similar borrowing could be obtained from an independent financier under comparable terms and conditions.

(e) Segment Reporting

A business segment is identified for a group of assets and operations engaged in providing products or services that are subject to risks and returns that are different to those of other business segments. A geographical segment is identified when products or services are provided within a particular economic environment subject to risks and returns that are different from those of segments operating in other economic environments (refer to Note 4).

(f) Comparative Figures

When required by Accounting Standards, comparative figures have been adjusted to conform to changes in presentation for the current financial year.

(g) Foreign Currency

Transactions in foreign currencies are translated to Australian dollars (the functional currency) at exchange rates at the dates of those transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated to Australian dollars at the foreign exchange rate at that date. The foreign currency gain or loss on monetary items is the difference between amortised cost in Australian dollars at the beginning of the period, adjusted for effective interest and payments during the period, and the amortised cost in Australian dollars translated at the exchange rate at the end of the period. Foreign currency differences arising on retranslation are recognised in results.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

23

(h) Financial Instruments

A financial instrument is recognised if the Group becomes a party to the contractual provisions of the instrument. Financial assets are derecognised if the Group’s contractual rights to the cash flows from the financial assets expire or if the Group transfers the financial asset to another party without retaining control or substantially all risks and rewards of the asset. Regular purchases and sales of financial assets are accounted for at trade date, ie. the date the Group commits itself to purchase or sell the asset. Financial liabilities are derecognised if the Group’s obligations specified in the contract expire or are discharged or cancelled. Held-to-Maturity Investments If the Group has positive intent and ability to hold debt securities to maturity, then they are classified as held-to-maturity. Held-to-maturity investments are measured at amortised cost using the effective interest method, less any impairment losses. Available-For-Sale Financial Assets Any such assets subsequently acquired would, subsequent to initial recognition, be measured at fair value and changes therein, other than impairment losses (see Note 1(k)) and foreign exchange gains and losses on available-for-sale monetary items are recognised directly in a separate component of equity. When an investment is derecognised, the cumulative gain or loss in equity would be transferred to results. Financial Assets at Fair Value through Profit or Loss An instrument is classified at fair value through profit or loss if it is held for trading or is designated as such upon initial recognition. Financial instruments are designated at fair value through profit or loss if the Group manages such investments and makes purchase and sale decisions based on their fair value in accordance with the Group’s documented risk management or investment strategy. Any such assets subsequently acquired would be measured at fair value, with changes therein recognised in profit or loss, and attributable transaction costs on initial recognition brought to account in profit or loss when incurred. Other Other non-derivative financial instruments are measured at amortised cost using the effective interest method, less any impairment losses.

Trade & Other Receivables

Trade receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision for impairment. Trade receivables are generally due for settlement within 30 days from month end. Collectability of trade receivables is reviewed on an ongoing basis. Debts which are known to be uncollectible are written off. A provision for impairment of trade receivables is established when there is objective evidence that the Group will not be able to collect all amounts due according to the original terms of the receivables. Significant financial difficulties of the debtor, probability that the debtor will enter bankruptcy or financial reorganisation, and default or delinquency in payments (more than 30 days overdue) are considered indicators that the trade receivable is impaired. The amount of the provision is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the original effective interest rate. Cash flows relating to short term receivables are not discounted if the effect of discounting is immaterial. The amount of the provision is recognised in the statement of comprehensive income in other expenses.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

24

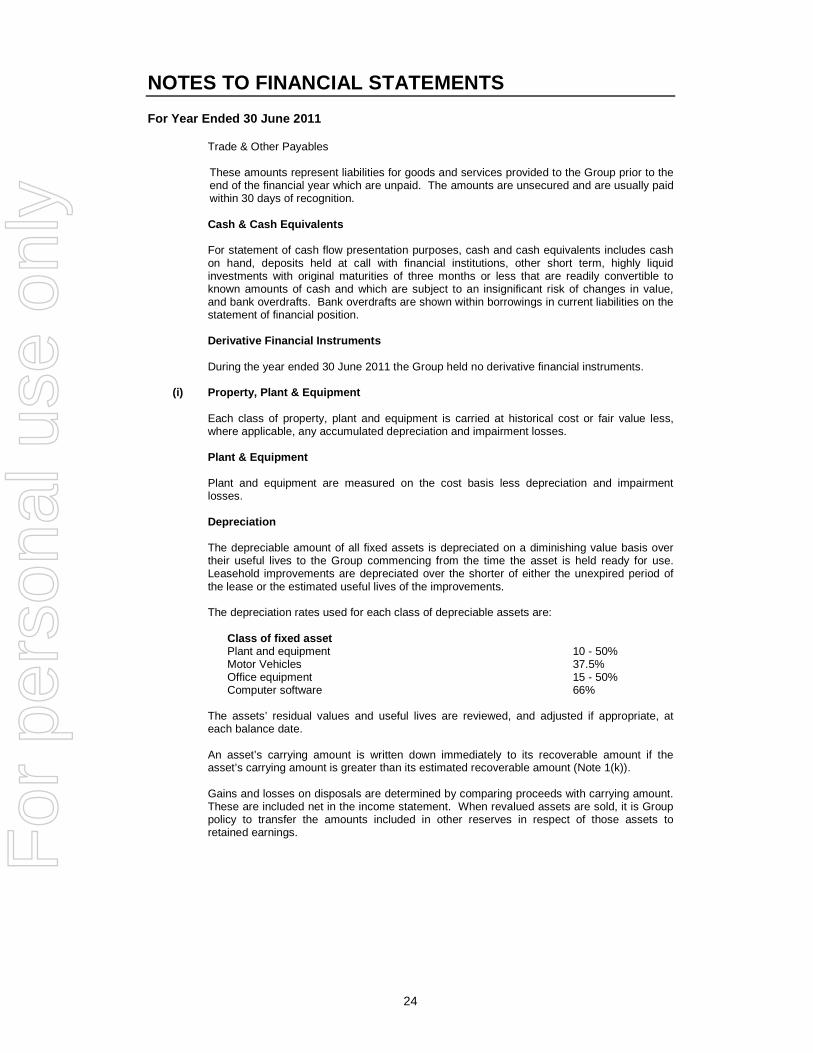

Trade & Other Payables

These amounts represent liabilities for goods and services provided to the Group prior to the end of the financial year which are unpaid. The amounts are unsecured and are usually paid within 30 days of recognition.

Cash & Cash Equivalents

For statement of cash flow presentation purposes, cash and cash equivalents includes cash on hand, deposits held at call with financial institutions, other short term, highly liquid investments with original maturities of three months or less that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value, and bank overdrafts. Bank overdrafts are shown within borrowings in current liabilities on the statement of financial position. Derivative Financial Instruments

During the year ended 30 June 2011 the Group held no derivative financial instruments.

(i) Property, Plant & Equipment

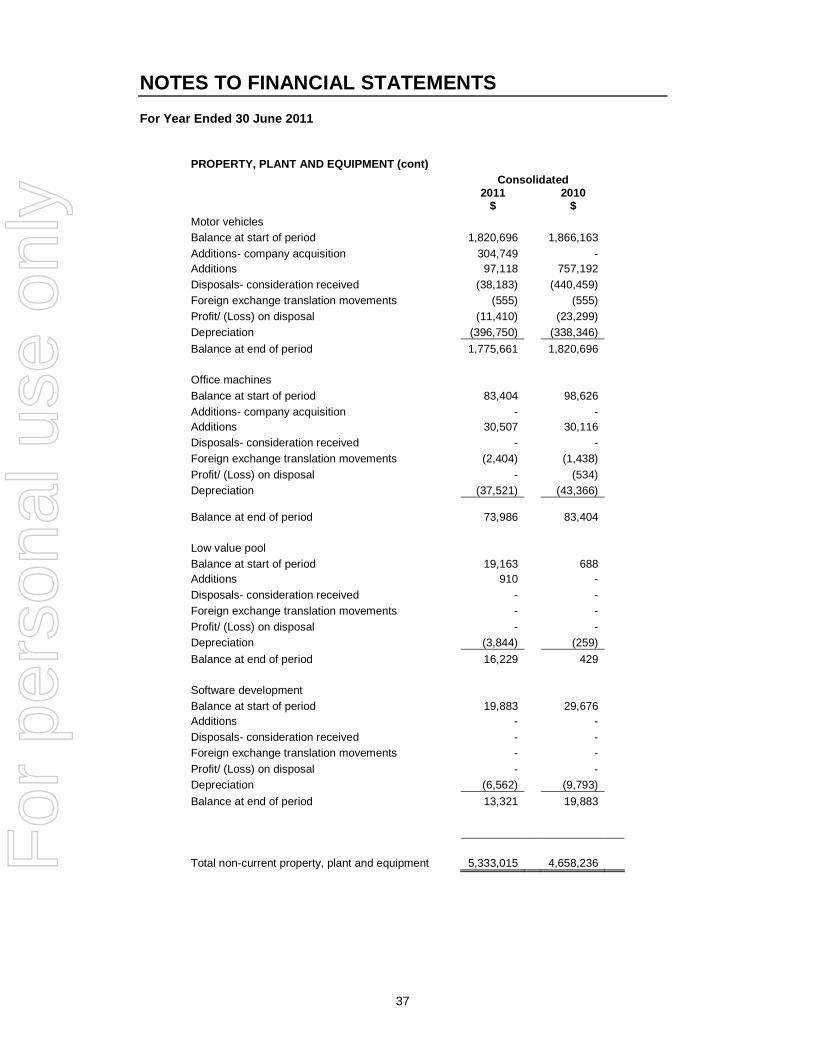

Each class of property, plant and equipment is carried at historical cost or fair value less, where applicable, any accumulated depreciation and impairment losses. Plant & Equipment Plant and equipment are measured on the cost basis less depreciation and impairment losses. Depreciation The depreciable amount of all fixed assets is depreciated on a diminishing value basis over their useful lives to the Group commencing from the time the asset is held ready for use. Leasehold improvements are depreciated over the shorter of either the unexpired period of the lease or the estimated useful lives of the improvements. The depreciation rates used for each class of depreciable assets are:

Class of fixed asset Plant and equipment 10 - 50% Motor Vehicles 37.5% Office equipment 15 - 50% Computer software 66%

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at each balance date. An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount (Note 1(k)). Gains and losses on disposals are determined by comparing proceeds with carrying amount. These are included net in the income statement. When revalued assets are sold, it is Group policy to transfer the amounts included in other reserves in respect of those assets to retained earnings.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

25

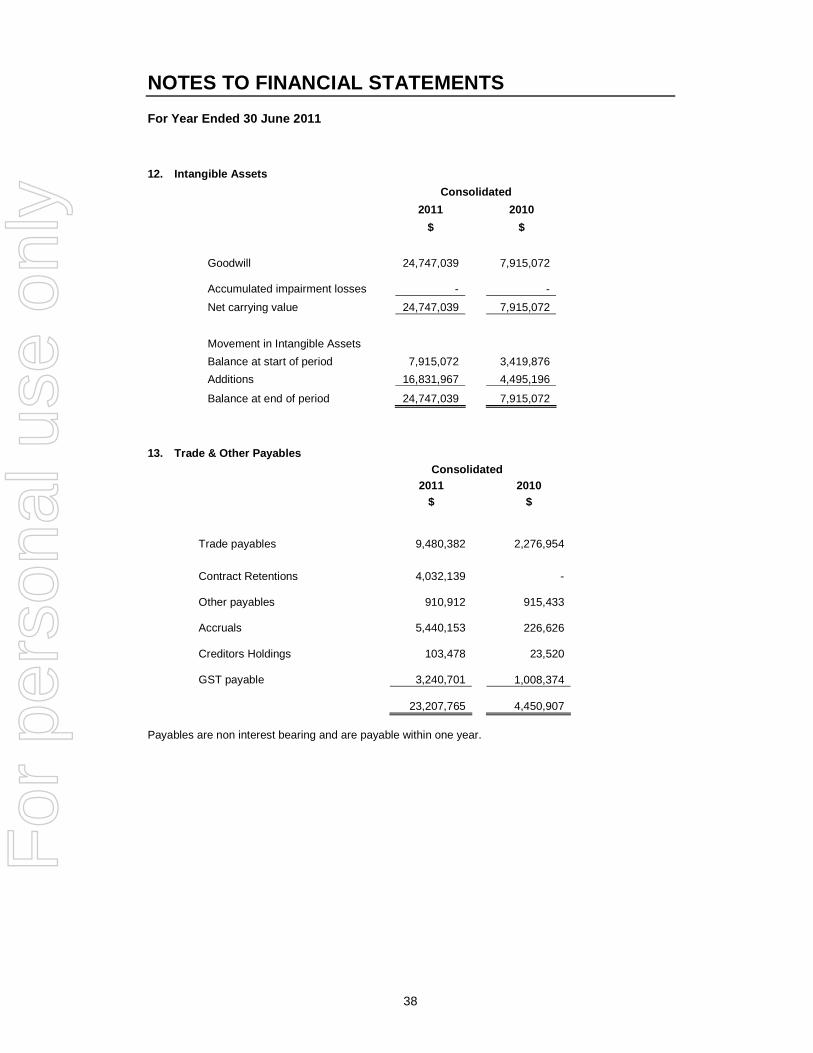

(j) Intangible Assets

Goodwill Goodwill represents the excess of the cost of an acquisition over the fair value of the Group’s share of the net identifiable assets of the acquired subsidiary at the date of acquisition. Goodwill on acquisitions of subsidiaries is included in intangible assets. Goodwill is tested for impairment annually or more frequently if events or changes in circumstances indicate that it might be impaired, and is carried at cost less accumulated impairment losses. Gains and losses on the disposal of an entity include the carrying amount of goodwill relating to the entity sold.

(k) Impairment of Assets

Financial Assets Financial assets are assessed at each reporting date to determine whether there is any objective evidence that they are impaired. A financial asset is considered to be impaired if objective evidence indicates that one or more events have had a negative effect on the estimated future cash flows of that asset. An impairment loss in respect of a financial asset measured at amortised cost is calculated as the difference between its carrying amount and the present value of the estimated future cash flows discounted at the original effective interest rate. An impairment loss in respect of an available-for-sale financial asset is calculated by reference to its fair value. Individually significant financial assets are tested for impairment on an individual basis. The remaining financial assets are assessed collectively in groups that share similar credit risk characteristics. All impairment losses are recognised in profit or loss. Any cumulative loss in respect of an available-for-sale financial asset recognised previously in equity is transferred to profit or loss. An impairment loss is reversed if the reversal can be related objectively to an event occurring after the impairment loss was recognised. For financial assets measured at amortised cost and available-for-sale financial assets that are debt securities, the reversal is recognised in profit or loss. For available-for-sale financial assets that are equity securities, the reversal is recognised directly in equity. Non-Financial Assets

An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. For the purposes of assessing impairment, assets are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows from other assets or groups of assets (cash generating units). Non financial assets other than goodwill that suffered impairment are reviewed for possible reversal of the impairment at each reporting date.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

26

(l) Finance Income and Expenses

Finance income comprises interest income on funds invested (including available-for-sale financial assets), gains on the disposal of any available-for-sale financial assets, changes in the fair value of financial assets at fair value through profit or loss, and gains on hedging instruments that are recorded in profit or loss. Interest income is recognised as it accrues in profit or loss, using the effective interest method. Finance expenses comprise interest expense on borrowings, unwinding of the discount on provisions, changes in the fair value of financial assets at fair value through profit or loss, and impairment losses recognised on financial assets. Borrowing costs directly attributable to the acquisition or production of assets that necessarily take a substantial period of time to prepare for their intended use or sale are added to the cost of those assets, until such time as the assets are substantially ready for their intended use or sale. All other borrowing costs are recognised in profit or loss using the effective interest method. Foreign currency gains and losses are reported on a net basis.

(m) Provisions

Provisions are recognised when the Group has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources will be required to settle the obligation and the amount has been reliably estimated. Where there are a number of similar obligations, the likelihood that an outflow will be required in settlement is determined by considering the class of obligations as a whole. A provision is recognised even if the likelihood of an outflow with respect to any one item included in the same class of obligations may be small. Provisions are measured at the present value of management’s best estimate of the expenditure required to settle the present obligation at the balance date. The discount rate used to determine the present value reflects current market assessments of the time value of money and the risks specific to the liability. The increase in the provision due to the passage of time is recognised as interest expense.

(n) Employee Benefits

Wages & Salaries and Annual Leave Liabilities for wages and salaries, including non monetary benefits and annual leave expected to be settled within 12 months of the reporting date are recognised in provisions in respect of employees' services up to the reporting date and are measured at the amounts expected to be paid when the liabilities are settled. Long Service Leave

The liability for long service leave is recognised in the provision for employee benefits and measured as the present value of expected future payments to be made in respect of services provided by employees up to the reporting date. Consideration is given to expected future wage and salary levels, experience of employee departures and periods of service. Expected future payments are discounted using market yields at the reporting date on national government bonds with terms to maturity and currency that match, as closely as possible, the estimated future cash outflows.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

27

Defined Contribution Plans A defined contribution plan is a post-employment benefit plan under which an entity pays fixed contributions into a separate entity and will have no legal or constructive obligation to pay further amounts. Obligations for contributions to defined contribution plans are recognised as a personnel expense in profit or loss when they are due.

(o) Revenue

Revenue is measured at the fair value of the consideration received or receivable. Amounts disclosed as revenue are net of returns, trade allowances and duties and taxes paid. Revenue is recognised for the major business activities as follows: � Sale of goods is for sales of current inventory; and � Service revenue is for services rendered and recognised as work is performed for the

customer.

(p) Goods & Services Tax (GST)

Revenues, expenses and assets are recognised net of the amount of associated GST, unless the GST incurred is not recoverable from the taxation authority. In this case it is recognised as part of the cost of acquisition of the asset or as part of the expense. Receivables and payables are stated inclusive of the amount of GST receivable or payable. The net amount of GST recoverable from, or payable to, the taxation authority is included with other receivables or payables in the statement of financial position. Cash flows are presented on a gross basis. The GST components of cash flows arising from investing or financing activities which are recoverable from, or payable to the taxation authority, are presented as operating cash flow.

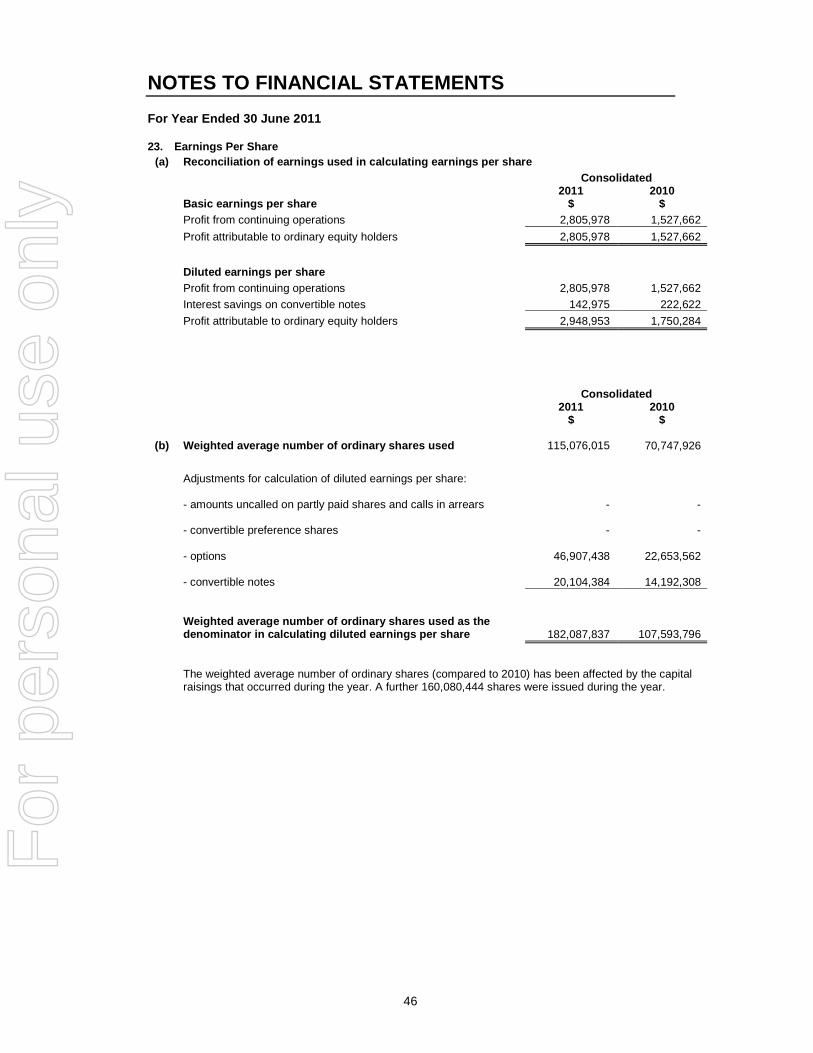

(q) Earnings per Share

Basic Earnings Per Share Basic earnings per share is calculated by dividing the profit attributable to equity holders of the company, excluding any costs of servicing equity other than ordinary shares, by the weighted average number of ordinary shares outstanding during the financial year, adjusted for bonus elements in ordinary shares issued during the year.

Diluted Earnings Per Share

Diluted earnings per share adjusts the figures used in the determination of basic earnings per share to take into account the after income tax effect of interest and other financing costs associated with dilutive potential ordinary shares and the weighted average number of shares assumed to have been issued for no consideration in relation to dilutive potential ordinary shares.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

28

(r) Income Tax

The income tax expense or revenue for the period is the tax payable on the current period’s taxable income based on the national income tax rate for each jurisdiction adjusted by changes in deferred tax assets and liabilities attributable to temporary differences and to unused tax losses. Deferred income tax is provided in full, using the liability method, on temporary differences arising between the tax bases of assets and liabilities and their carrying amounts in the consolidated financial statements. However, the deferred income tax is not accounted for if it arises from initial recognition of an asset or liability in a transaction other than a business combination that at the time of the transaction affects neither accounting nor taxable profit or loss. Deferred income tax is determined using tax rates (and laws) that have been enacted or substantially enacted by the balance date and are expected to apply when the related deferred income tax asset is realised or the deferred income tax liability is settled. Deferred tax assets are recognised for deductible temporary differences and unused tax losses only if it is probable that future taxable amounts will be available to utilise those temporary differences and losses. Deferred tax liabilities and assets are not recognised for temporary differences between the carrying amount and tax bases of investments in controlled entities where the parent entity is able to control the timing of the reversal of the temporary differences and it is probable that the differences will not reverse in the foreseeable future. Deferred tax assets and liabilities are offset when there is a legally enforceable right to offset current tax assets and liabilities and when the deferred tax balances relate to the same taxation authority. Current tax assets and tax liabilities are offset where the entity has a legally enforceable right to offset and intends either to settle on a net basis, or to realise the asset and settle the liability simultaneously. Current and deferred tax balances attributable to amounts recognised directly in equity are also recognised directly in equity. Tax Consolidation Legislation

Allmine Group Limited and its wholly owned Australian controlled entities have implemented the tax consolidation legislation.

The head entity, Allmine Group Limited, and the controlled entities in the tax consolidated group account for their own current and deferred tax amounts. These tax amounts are measured as if each entity in the tax consolidated group continues to be a stand alone taxpayer in its own right. In addition to its own current and deferred tax amounts, Allmine Group Limited also recognises the current tax liabilities (or assets) and the deferred tax assets arising from unused tax losses and unused tax credits assumed from controlled entities in the tax consolidated group.

(s) Leases

Leases of fixed assets where substantially all the risks and benefits incidental to the ownership of the asset, but not the legal ownership that are transferred to entities in the Group are classified as finance leases. Finance leases are capitalised by recording an asset and a liability at the lower of the amounts equal to the fair value of the leased property or the present value of the minimum lease payments, including any guaranteed residual values. Lease payments are allocated between the reduction of the lease liability and the lease interest expense for the period. Leased assets are depreciated on a diminishing value basis over the shorter of their estimated useful lives or the lease term. Lease payments for operating leases, where substantially all of the risks and benefits remain

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

29

with the lessor, are charged as expenses in the periods in which they are incurred.

(t) New Accounting Standards & AASB Interpretations

No presently existing new standards or interpretations are expected to have any material impact on the Group.

2. Critical Accounting Estimates & Judgements

Estimates and judgements are continually evaluated and are based on historical experience and other factors, including expectations of future events that may have a financial impact on the entity and that are believed to be reasonable under the circumstances.

3. Financial Risk Management

Overview The Company and the Group have exposure to the following risks from their use of financial instruments:

• credit risk; and

• liquidity risk; and

• market risk; This note presents information about the Company’s and Group’s exposure to each of the above risks, their objectives, policies and processes for measuring and managing risk, and the management of capital. Further quantitative disclosures are included throughout this financial report. The Board of Directors has overall responsibility for the establishment and oversight of the risk management framework and setting risk management policies. Risk management policies are established to identify and analyse the risks faced by the Company and Group, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly to reflect changes in market conditions and the Company’s and Group’s activities. The Company and Group, through training and management standards and procedures appropriate for the Group, aim to develop a disciplined and constructive control environment in which all employees understand their roles and obligations. The board oversees how management monitors compliance with the Company’s and Group’s risk management policies and procedures and reviews the adequacy of the risk management framework in relation to the risks faced by the Company and Group. Being a relatively small organisation, there is no formal Audit Committee but the Board act in this capacity. Credit Risk Credit risk is the risk of financial loss to the Group if a customer or counterparty to a financial instrument fails to meet its contractual obligations, and arises principally from the Group’s receivables from customers. For the Company, this is also the major source of credit risk. Trade and Other Receivables The Company’s and Group’s exposure to credit risk is influenced mainly by the individual characteristics of each customer. The demographics of the Group’s customer base minimises any influence on credit risk. The Company has a credit policy under which potential new customers are analysed individually for creditworthiness before payment terms are offered. As the Group’s revenue has been derived principally from “sale of goods” and “fee for service” activities pre-agreed contractual terms, credit limits are analysed first. If payment is not received within agreed credit terms, services may be suspended pending clearance of the outstanding balance.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

30

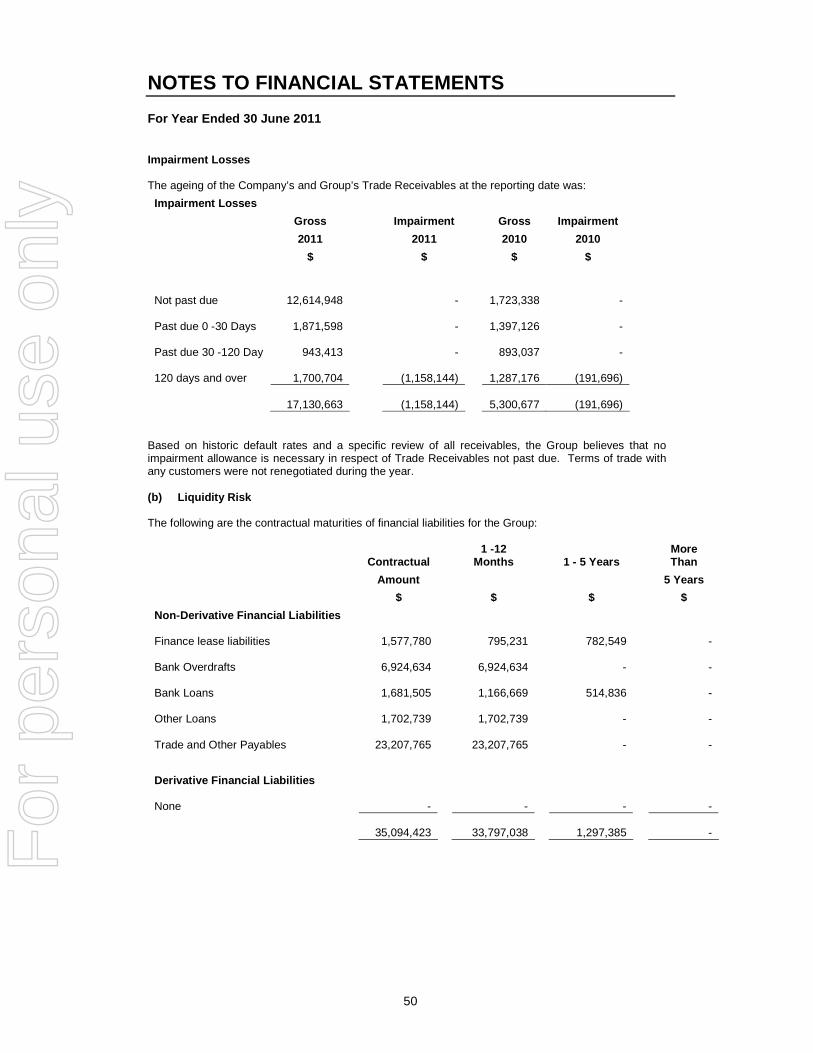

The typical trend of the industry is for trade receivables to not be collected until 60 – 90 days. Most of the Group’s operating revenue is from customers that tend to not pay within the required 30 day terms however material losses have rarely been experienced. In monitoring credit risk, each customer is assessed individually rather than grouping customers according to credit characteristics. The Company and Group have reviewed the outstanding trade and other receivables at year end, The Company and Group have assessed a quantum of provision for impairment is required which has been booked in the accounts. All other amounts are considered to be collectible.

Liquidity Risk Liquidity risk is the risk that the Group will not be able to meet its financial obligations as they fall due. The Group’s approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Group’s reputation. Through its ongoing capital initiatives, the Group aims to ensure it has sufficient cash reserves to meet operating expenses. Regular cash flow forecasts are prepared to monitor the cash position. The non-payment of contractual progress payments within time periods specified within the contract, withholding of retention sums and completion bonds respond both liquidity and finance risk for Group companies. The provision of engineering services by Arccon involves risks arising from completed projects not performing in accordance with stipulated design specifications; for example, a plant designed to extract minerals from ore may not achieve stipulated hourly throughput because of design errors. Group companies are able to insure against such risks through professional indemnity insurance but such occurrences frequently result in extended negotiations with clients and the Group’s insurers as well as receivables being disputed by clients. The construction industry involves similar risk. Although Group companies do not provide architectural or design services, clients sometimes attribute delays in completion, cost overruns or design faults to the construction company and refuse to pay outstanding progress claims and/or to release completion bonds and retention monies. In response, the Group companies may need to enter into conciliation and arbitration proceedings or to undertake legal action. In both circumstances described above, clients may suffer liquidity issues resulting from industrial action, construction delays due to unseasonal weather or natural disasters, inability to obtain required raw material or other circumstances resulting in non-payment of progress billings within stipulated contract terms, the non-release of completion bonds or withholding of retention monies. At balance date, the Parent Entity’s available lines of finance were secured over the assets of principal shareholders. It is proposed Allmine will replace the existing security providers. Market Risk

Market risk is the risk that changes in market prices, such as foreign exchange rates, interest rates, and equity prices will affect the Group’s income or the value of its holdings of financial instruments. The objective of market risk management is to manage and control market risk exposures within acceptable parameters, while optimising the return. The Group is exposed to market risk. The Wildkat business has a major exposure to currency risk in relation to purchases of stock that are denominated in a currency other than Australian dollars. Historically, most of Wildkat’s stock was acquired globally with the USD and EUR being the main currencies purchased. However, the industry tends to pass on any foreign exchange differences onto the customer. This policy was reviewed during the year with the decision made to reduce market risk and to procure the majority of Wildkat’s stock from domestic suppliers. The other Group members have minimal exposure to market risk, with most stock being purchased from domestic suppliers.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

31

Arccon is also exposed to market risks. The market segments to which the Group provides services; mining engineering and construction and commercial construction are highly cyclical in nature and significantly dependant on external influences including the availability of credit, rental prices and vacancy levels for commercial property, the demand for, and prices of, mineral commodities and the availability of a skilled workforce. Further, during periods of reduced activity in the Group’s market segments, there is strong competition from competitors who are concerned to maintain their market share. To address these risks, the Group maintains a highly experienced and well-qualified management group with a strong national and international reputation for industry excellence. The Group also has Alliance Agreements with two China domiciled engineering, procurement and construction company in the world, China Metallurgical Group Corporation (“MCC”) and China Non-Ferrous Metal Industry’s Foreign Engineering and Construction Co. Ltd (“NFC”). MCC and NFC are two of the largest mining engineering construction companies in the world. Capital Management The Board’s policy is to maintain a sufficiently strong capital base so as to maintain investor, creditor, and market confidence and to sustain future progress on the Group’s operations. As the Group has grown rapidly throughout the year as a result of acquisitions, the cash position remains tight. As a result, the Group continues to evaluate financing alternatives. There were no changes to the Group’s approach to capital management during the year. Neither the Company nor any of its subsidiaries are subject to externally imposed capital requirements.

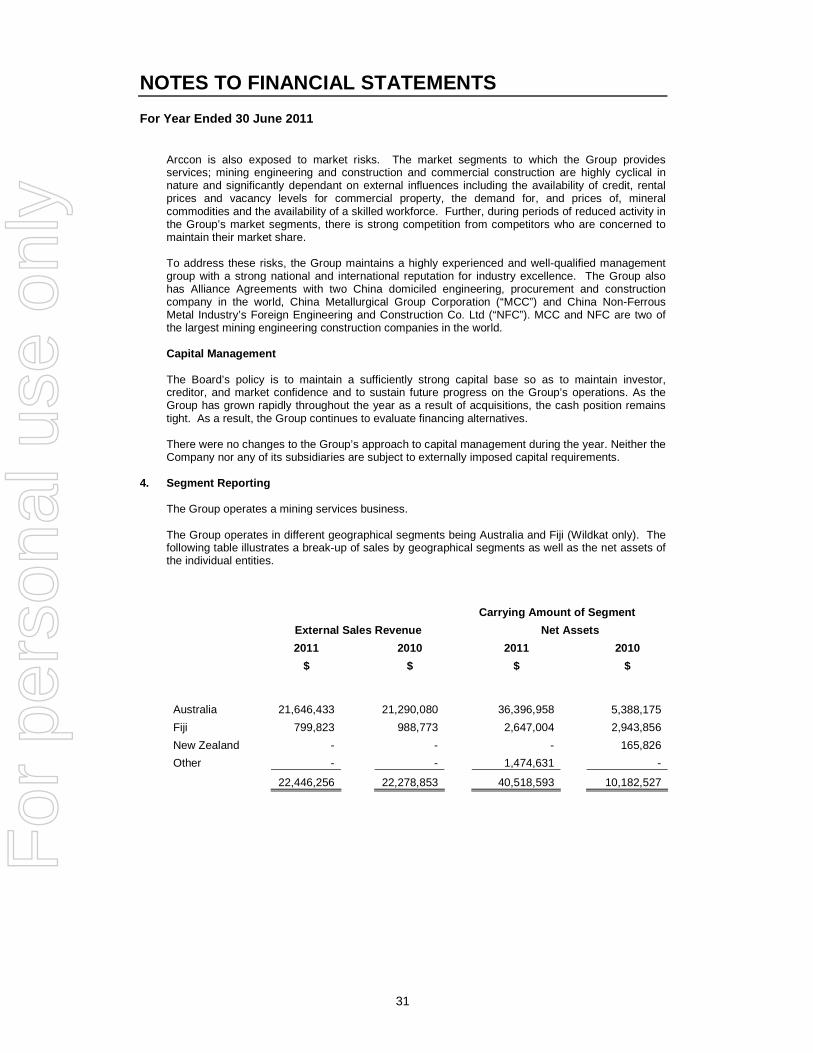

4. Segment Reporting

The Group operates a mining services business. The Group operates in different geographical segments being Australia and Fiji (Wildkat only). The following table illustrates a break-up of sales by geographical segments as well as the net assets of the individual entities.

Carrying Amount of Segment

External Sales Revenue Net Assets

2011 2010 2011 2010

$ $ $ $

Australia 21,646,433 21,290,080 36,396,958

5,388,175

Fiji 799,823 988,773 2,647,004 2,943,856

New Zealand - - - 165,826

Other - - 1,474,631 -

22,446,256 22,278,853 40,518,593 10,182,527

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

32

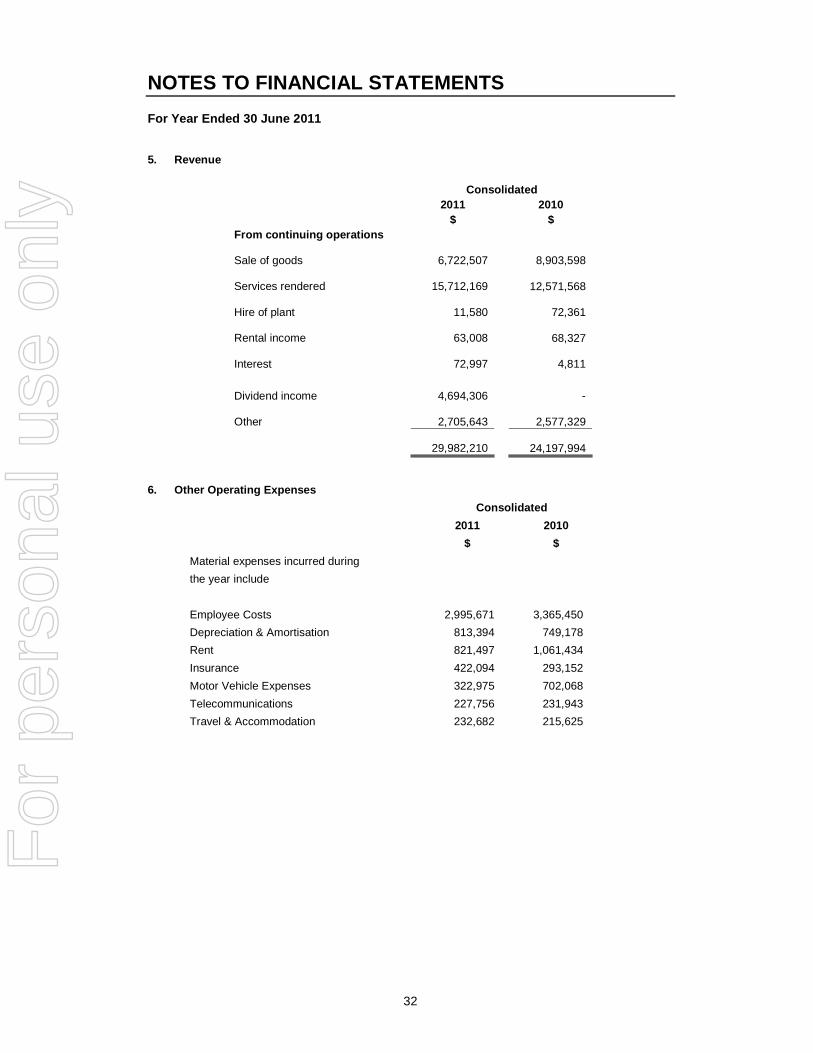

5. Revenue

Consolidated 2011 2010 $ $ From continuing operations

Sale of goods 6,722,507

8,903,598

Services rendered 15,712,169

12,571,568

Hire of plant 11,580

72,361

Rental income 63,008

68,327

Interest 72,997

4,811 Dividend income 4,694,306 -

Other 2,705,643

2,577,329

29,982,210

24,197,994 6. Other Operating Expenses

Consolidated

2011 2010

$ $

Material expenses incurred during

the year include

Employee Costs 2,995,671 3,365,450

Depreciation & Amortisation 813,394 749,178

Rent 821,497 1,061,434

Insurance 422,094 293,152

Motor Vehicle Expenses 322,975 702,068

Telecommunications 227,756 231,943

Travel & Accommodation 232,682 215,625

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

33

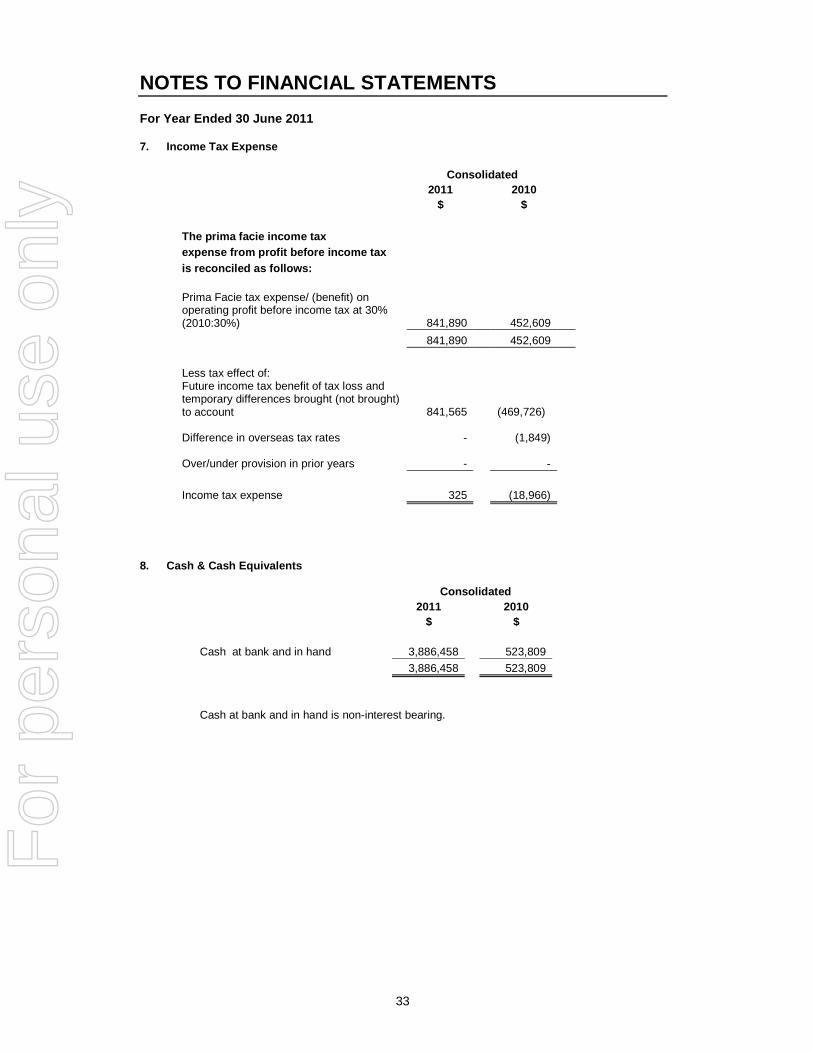

7. Income Tax Expense

Consolidated 2011 2010 $ $ The prima facie income tax expense from profit before income tax is reconciled as follows: Prima Facie tax expense/ (benefit) on operating profit before income tax at 30% (2010:30%) 841,890 452,609

841,890 452,609

Less tax effect of: Future income tax benefit of tax loss and temporary differences brought (not brought) to account 841,565

(469,726)

Difference in overseas tax rates -

(1,849)

Over/under provision in prior years -

-

Income tax expense 325 (18,966)

8. Cash & Cash Equivalents

Consolidated 2011 2010 $ $ Cash at bank and in hand 3,886,458 523,809

3,886,458 523,809

Cash at bank and in hand is non-interest bearing.

For

per

sona

l use

onl

y

NOTES TO FINANCIAL STATEMENTS For Year Ended 30 June 2011

34

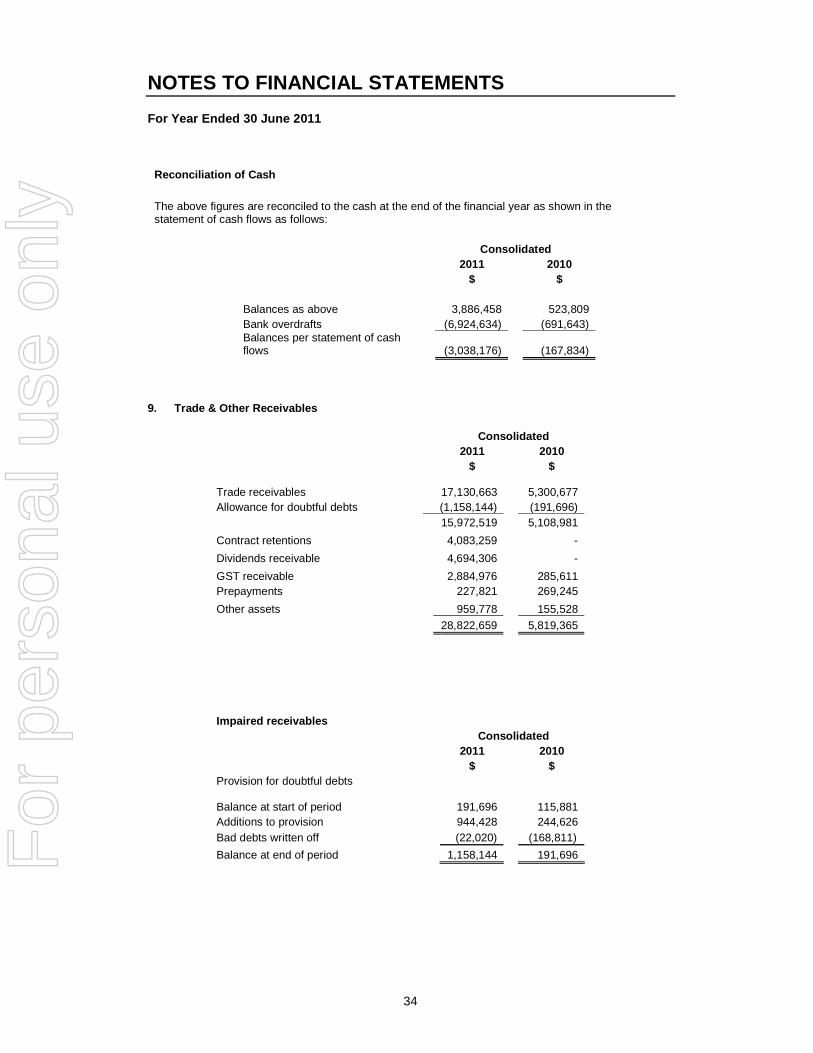

Reconciliation of Cash

The above figures are reconciled to the cash at the end of the financial year as shown in the statement of cash flows as follows:

Consolidated 2011 2010 $ $ Balances as above 3,886,458 523,809 Bank overdrafts (6,924,634) (691,643) Balances per statement of cash flows (3,038,176) (167,834)

9. Trade & Other Receivables