assuring accurate reporting on irs form 990, schedule h · assuring accurate reporting on irs form...

TRANSCRIPT

Assuring Accurate Reporting on IRS Form 990,

Schedule H

Keith Hearle

President

Verité Healthcare Consulting, LLC

September 2015

© Verité Healthcare Consulting, LLC, 2015 2

Webinar Objectives

Discuss importance of accurate IRS Form 990,

Schedule H filings

Identify issue areas (e.g., examples of potential

under-reporting) and response strategies

Questions and answers

© Verité Healthcare Consulting, LLC, 2015 3

Brief History and Context

Concerns about tax-

exempt hospitals

Redesigned form 990 and Schedule H

PPACA:

new “501(r)” requirements

501(r) Implementing

rules

© Verité Healthcare Consulting, LLC, 2015 4

Schedule H Walk-Through

Part I: Financial Assistance and Certain Other Community Benefits at Cost

Part II: Community Building Activities

Part III: Bad Debt, Medicare, & Collection Practices

Part VI: Management Companies and Joint Ventures

Part V: Facility Information

Section A. Hospital Facilities

Section B. Facility Policies and Practices

Section C. Supplemental Information for Part V, Section B

Section D. Other Health Care Facilities (not hospitals)

Part VI: Supplemental Information

© Verité Healthcare Consulting, LLC, 2015 5

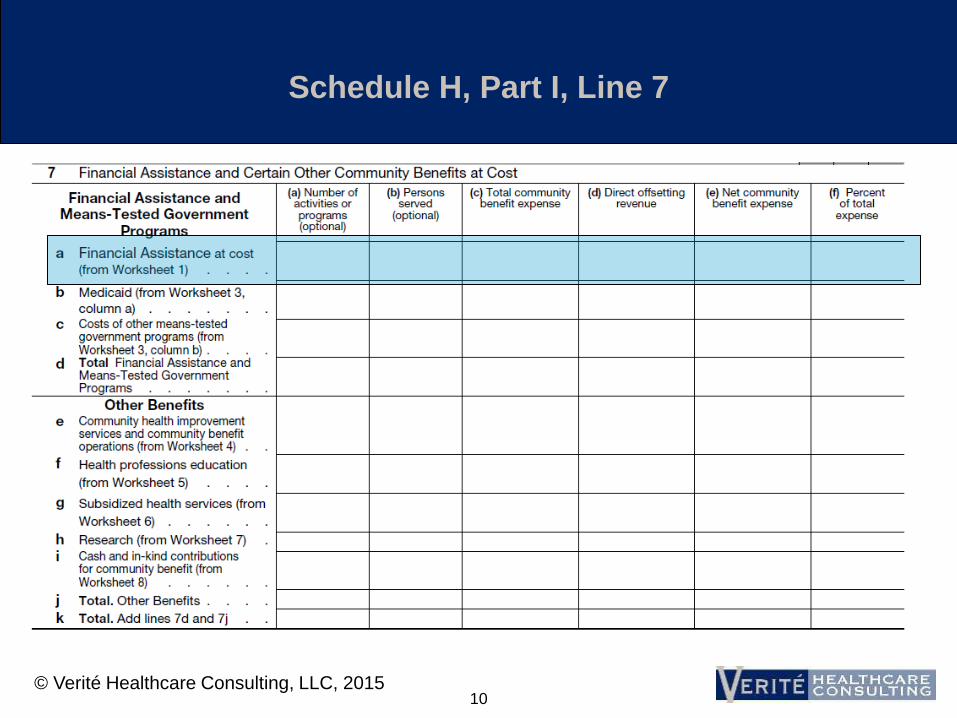

Schedule H, Part I, Line 7

© Verité Healthcare Consulting, LLC, 2015 6

IRS: What Counts as Community Benefit?

To count, a program or activity must respond to a demonstrated health/related community need and seek to achieve at least one community benefit objective:

• Improve Access to Health Services

• Enhance Public Health

• Advance Generalizable Knowledge

• Relief of a Government Burden to Improve Health

© Verité Healthcare Consulting, LLC, 2015 7

IRS: Programs that should not be counted

Activities or programs may not be reported:

• if they are provided primarily for marketing

purposes

• the program is more beneficial to the organization

than to the community; for instance,

– if the activity or program is designed primarily to

increase referrals of patients with third-party coverage,

– required for licensure or accreditation, or

– restricted to individuals affiliated with the organization.

© Verité Healthcare Consulting, LLC, 2015 8

Programs that should not be counted: additional

considerations (not in IRS Instructions)

An objective, “prudent layperson” would

question whether the program was established

primarily to benefit the community

The program represents a community benefit

that does not involve a reportable expense by

the organization, e.g.

• Benefits provided by employees on their own time

• Expense is not present in Form 990, Part IX

© Verité Healthcare Consulting, LLC, 2015 9

Programs that should not be counted: additional

considerations (not in IRS Instructions)

The initiative is designed only to benefit the

organization’s own patients or covered lives, e.g.

• Programs to prevent or reduce readmissions for

discharged patients

• Programs to reduce PMPM costs for patients/

members for whom the organization bears risk (or

might participate in shared savings)

9

© Verité Healthcare Consulting, LLC, 2015 10

Schedule H, Part I, Line 7

© Verité Healthcare Consulting, LLC, 2015 11

Reporting Strategies:

Financial Assistance

Assess ratio of bad debt to charity over time

Adjust Financial Assistance Policies:

• Include medical indigency (catastrophic) provisions

• Include presumptive eligibility

• Assure discounts align with Final Rule requirements

Use predictive modeling for accounts with bad debt and without completed applications (“the unknowns”)

Accelerate decision-making process

Reverse self-pay discounts for accounts with any financial assistance

11

© Verité Healthcare Consulting, LLC, 2015 12

Ratio of Patient Care Cost to Charges

12

© Verité Healthcare Consulting, LLC, 2015 13

Reporting Strategies:

Ratio of Patient Care Cost to Charges

Accuracy Strategies:

• Adjust the ratio so that community benefit expenses

are not double counted

– Only adjust the numerator of the ratio for amounts that are in

total operating expense

Maximization Strategies:

• Cost out “nonpatient care activities” rather than using

“other operating revenue” as a proxy

• Consider using a “more accurate cost accounting

method,” as allowed by instructions

13

© Verité Healthcare Consulting, LLC, 2015 14

Schedule H, Part I, Line 7

© Verité Healthcare Consulting, LLC, 2015 15

Reporting Strategies:

Medicaid and Other Means Tested Government

Programs

Include both Medicaid fee for service and Medicaid managed

care activities – from all states

Align offsetting revenue with GAAP financial statements, but

exclude direct GME revenue and include any IME

Include expense of provider tax, fees, assessments used to

maximize federal Medicaid matching funds

Assure that Medicaid managed care recipients are accounted

for as Medicaid

Use “most accurate” cost accounting method

Discussion: how to handle DSRIP revenues and program

expenses

15

© Verité Healthcare Consulting, LLC, 2015 16

Schedule H, Part I, Line 7

© Verité Healthcare Consulting, LLC, 2015 17

Community Health Improvement Categories

Community health education outreach

Community-based clinical services where there is no patient bill

Health care support services, e.g.:

• Enrollment assistance for Medicaid and other government-funded health

programs for lower-income people

• Cost of software tools that support decision making for granting financial

assistance at the beginning of the revenue cycle

• Transportation to improve access for lower-income people (not to increase

referrals)

Social and environmental improvement activities (e.g., removing

lead, violence prevention, eliminating food deserts)

17

© Verité Healthcare Consulting, LLC, 2015 18

Community Benefit Operations Categories

Community health needs assessments

Community benefit program administration

Activities associated with fundraising or grant-

writing for community benefit programs

18

© Verité Healthcare Consulting, LLC, 2015 19

Reporting Strategies:

Community Health Improvement Services (and

Operations)

Assure that all programs and activities that can be

reported are identified (comprehensive inventory)

Assess whether certain community building programs

(Part II) qualify as community health improvement (Part

1, Line 7e)

Assure that total expense includes both direct cost and

indirect cost

Include an auditable portion of “system-office” cost

(management fee/corporate allocation) in “community

benefit operations”

19

© Verité Healthcare Consulting, LLC, 2015 20

Schedule H, Part I, Line 7

© Verité Healthcare Consulting, LLC, 2015 21

Reporting Strategies:

Health Professions Education

Assure Schedule H incorporates a full inventory of

all reportable health professions education programs

Assess transactions (flows of funds) between

teaching hospital and medical school (and other

affiliates) to assure that all health professions

education expense is identified

Do not include Medicare and Medicaid “Indirect

Medical Education” reimbursement in offsetting

revenue

21

© Verité Healthcare Consulting, LLC, 2015 22

Schedule H, Part I, Line 7

© Verité Healthcare Consulting, LLC, 2015 23

Subsidized Health Services

“Subsidized health services” means clinical services

provided despite a financial loss to the organization.

• The financial loss is measured after removing losses,

measured by cost, associated with bad debt, charity

care, Medicaid and other means-tested government

programs.

In addition, in order to qualify as a subsidized health

service, the organization must provide the service

because it meets an identified community need.

23

© Verité Healthcare Consulting, LLC, 2015 24

Reporting Strategies:

Subsidized Health Services

Include subsidized health services, if any are

reportable during the tax year

• Requires annual assessment using cost accounting

information

Do not report services with gains during the tax

year (even if previously reported)

Rely on “most accurate” cost accounting

methodology available

24

© Verité Healthcare Consulting, LLC, 2015 25

Schedule H, Part I, Line 7

© Verité Healthcare Consulting, LLC, 2015 26

Reporting Strategies:

Research

Assure all research studies funded by a tax-exempt

source (creating expense on the books of the

organization filing Schedule H) have been identified

Base indirect costs on NIH guidelines and not the

actual, indirect cost factor negotiated between the

organization and NIH

Consider which entity (EIN) should bear the cost of

research studies

26

© Verité Healthcare Consulting, LLC, 2015 27

Schedule H, Part I, Line 7

© Verité Healthcare Consulting, LLC, 2015 28

Cash and In-Kind Contributions

“Cash and in-kind contributions” means

contributions made by the organization to health

care organizations and other community groups

that are restricted, in writing, to one or more of

the community benefit activities described in the

Table in Part I, line 7 (or the Worksheets

thereto).

Do not include amounts involving a quid pro quo

arrangement.

28

© Verité Healthcare Consulting, LLC, 2015 29

Reporting Strategies:

Cash and In-Kind Contributions

Place restrictions on cash contributions

Include the value of time spent by staff

supporting community health work as in-kind

donation

Assure that all contributions being made by the

system and its affiliates are accounted for as

expense by the hospital organization(s)

Describe unrestricted donations/sponsorships in

Part VI

29

© Verité Healthcare Consulting, LLC, 2015 30

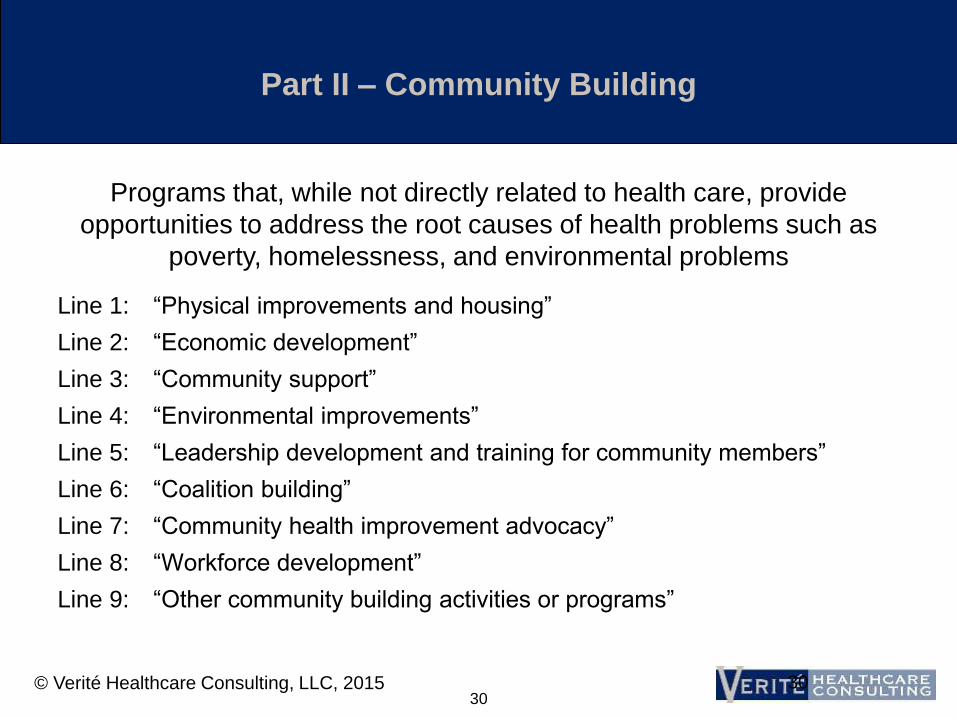

Part II – Community Building

Line 1: “Physical improvements and housing”

Line 2: “Economic development”

Line 3: “Community support”

Line 4: “Environmental improvements”

Line 5: “Leadership development and training for community members”

Line 6: “Coalition building”

Line 7: “Community health improvement advocacy”

Line 8: “Workforce development”

Line 9: “Other community building activities or programs”

Programs that, while not directly related to health care, provide

opportunities to address the root causes of health problems such as

poverty, homelessness, and environmental problems

30

© Verité Healthcare Consulting, LLC, 2015 31

Community Building, Continued

Change to Community Building instructions:

• 2010: “Report in this part … activities … to

protect health or safety, and that are not

reportable in Part I or III …”

• 2011: “Some community building activities may

also meet the definition of community benefit. Do

not report in Part II community building costs that

are reported on Part I, line 7 … as … a

community health improvement service

reportable on Part I, Line 7e”

31

© Verité Healthcare Consulting, LLC, 2015 32

Contact Information

Keith Hearle

President Verite Healthcare Consulting, LLC

Alexandria, VA

www.veriteconsulting.com

© Verité Healthcare Consulting, LLC, 2015 33

Questions

33

Healthcare Association of New York State www.hanys.org

HANYS’ Contacts

Schedule H Analysis: • Bob McLeod

• Pam Payette [email protected]

Community Health • Sue Ellen Wagner

• Donna Evans [email protected]

34