assignment finance miss farah 2015

DESCRIPTION

ACCOUNTSTRANSCRIPT

EXECUTIVE SUMMARY

Tan Sri Dr Ahmad Tajuddin Ali

(Non-Independent Non-Executive Chairman)

Dato’ Wan Abdullah Wan Ibrahim

(Managing Director/Chief Executive Officer)

Dato’ Izzaddin Idris

(Non-Independent Non-Executive Director)

Md Ali Md Dewal

(Senior Independent Non-Executive Director)

Oh Kim Sun

(Independent Non-Executive Director)

Sheranjiv Sammanthan

(Non-Independent Non-Executive Director)

Professor Philip Sutton Cox

(Independent Non-Executive Director)

Lim Tian Huat

(Independent Non-Executive Director)

Dato’ Srikandan Kanagainthiram

(Independent Non-Executive Director)

YM Ungku Suseelawati Ungku Omar

(Independent Non-Executive Director)

1 | P a g e

EXECUTIVE SUMMARY

Y. Bhg. Tan Sri Dato’ Ir. (Dr) Wan Abdul

Rahman Bin Wan Yaacob

(Independent Non-Executive Chairman)

Y. Bhg. Tan Sri Dato’

Tan Boon Seng @ Krishnan

(Executive Deputy Chairman)

Y. Bhg. Dato’ Teh Kean Ming

(Chief Executive Officer & Managing Director)

Tan Gim Foo

(Deputy Chief Executive Officer &

Deputy Managing Director)

Y. Bhg. Datuk Yahya Bin Ya’ acob

(Senior Independent Non-Executive Director)

Y.Bhg. Tan Sri Abdul Halim Bin Ali

(Independent Non-Executive Director)

Y.Bhg. Datuk Oh Chong Peng

(Independent Non- Executive Director)

Y.Bhg. Datuk Hj Hasni Bin Harun

(Non-Executive Director)

2 | P a g e

UEM Land Berhad or now known as UEM Sunrise Berhad is a public company listed on

the Main Market of Bursa Malaysia Securities Berhad. It is the flagship Company for real estate

investment and property development businesses of UEM Group Berhad and Khazanah Nasional

Berhad which is an inversment holding arm of the Malaysia government. UEM Group is a whole

owned subsidiary by Khazanah, as a solid foundation.

As stated, UEM Sunrise Berhad which is the flagship for real estate and property

development has core competencies in macro township development, high-rise residential,

commercial, retail and integrated developments, as well as property management and project &

construction services. Making real estate and property development kind of field as the main

business of UEM Sunrise Berhad.

The Company, the master developer of Nusajaya is currently undertaking the

development of Nusajaya, one of the five flagship zones of Iskandar Malaysia, Johor into

Southeast Asia’s newest regional city. Upon completion, it will be the largest fully integrated

urban development in Southeast Asia that will provide significant investment, financial and

business opportunities to economic growth and development in the region. As being said out, the

development not only gave an impact to the company but also the surrounding of its activities

will received a huge positive impact upon the development itself.

Embracing innovation and technology, Nusajaya will be a role model of an economically,

socially and environmentally sustainable city for Southeast Asia. By doing so, other companies

can make this as a marking site on achieving greater success. With its modern infrastructure and

cutting edge architectural masterplan, the expected local and foreign investment inflows into

Nusajaya will propel economic growth and transform south Johor into an exciting centre of

economic development. This will be an historical moment where the development will make

south Johor into a place never think of.

3 | P a g e

Nusajaya spans close to 24,000 acres, with approximately 7,600 acres currently owned by

UEM Sunrise and at various stages of development. Nusajaya comprises a range of catalytic

developments including Kota Iskandar, the Johor State administrative centre which houses State

and Federal Government offices and others which development will be comprising mixed,

commercial projects with activity malls, campus offices, trade centres and residential

developments. Together with a mix of residential, commercial and industrial properties, hotels,

resorts and many other amenities, Nusajaya will emerge as a vibrant and dynamic destination

offering holistic and integrated lifestyle, with immense potential growth for investors. The

corporation is indeed making an income while pleasing the one’s connected.

Gerbang Nusajaya, the second phase development of Nusajaya is a 4,551 acre project

which will feature various catalytic developments including Nusajaya Tech Park, Motorsports

City, Signature Residences and Gerbang Nusantara. Gerbang Nusajaya will be developed over a

period of 25 years and will include components such as lifestyle & retail parks, campus offices &

industrial parks as well as residential precincts. Showing that the corporation can handle a long

term and huge project that will generate the income.

In the Central Region, UEM Sunrise is renowned for its award-winning, up-market high

rise residential projects as well as commercial developments largely in the Mont’Kiara enclave,

including 28 Mont’Kiara, Arcoris Mont’Kiara and Residensi22. It is also responsible for

introducing the concept of creative retail in Solaris Dutamas known as Publika. It is shown that

the corporation itself not only been active in business within the south region but also within the

central. On top of that handling a big project more than one at a time.

UEM Sunrise is also the owner of 98 acres of freehold site adjacent to the Central

Business District of Cyberjaya where Symphony Hills, an exclusive residential development and

the Country’s first Connected Intelligent Community resides, offering smart-home features and

community connectivity through high-speed broadband. UEM Sunrise has achieved a greater

concept of developing using the technology presently developed.

UEM Sunrise presence extends internationally into Vancouver, Canada via its mixed-use

development, Quintet and Aurora Melbourne Central in Melbourne, Australia. It also oversees

the sales and marketing of Khazanah and Temasek’s Marina One and DUO mixed-use

developments in Singapore. UEM Sunrise retains a landbank in Durban, South Africa.

4 | P a g e

IJM is one of Malaysia's leading conglomerates corporation ever established and is listed

on the Main Market of Bursa Malaysia Securities Berhad. Its core business activities are not sole

and encompass construction, property development, manufacturing and quarrying, infrastructure

concessions and plantations. Having a wide field of business showing the high generative income

obtain by the company which is why it IJM Corporation Berhad is listed on the Main Market of

Bursa Malaysia Securities Berhad.

Headquartered is located in Selangor, Malaysia, where the place itself is a strategic venue

which is one of the main core business state in Malaysia. IJM's regional aspirations have seen it

establish a growing presence in neighbouring developing markets with operations presently

spanning 10 countries, with primary focus in Malaysia, India, United Arab Emirates, China and

Indonesia. Going worldwide also expanding and fully utilize IJM Corporation Berhad on going

futher. IJM's phenomenal growth over the past three decades has been the result of its

unwavering focus on its core competencies, diversification into strategically related businesses

and selective expansion into new markets. While standing firm on the top, IJM Corporation

Berhad still aim to go higher in achieving their organizational goals.

Initially supporting in house needs, the Group's Industry Division quickly grew its operations

into scalable core activities focused on catering to demand from outside the Group. This was the

step on IJM expanding its business field. IJM continued to expand on its operations in this

division with strategic acquisitions such as the takeover of Industrial Concrete Products Berhad

in 2004 and successful market diversifications into China, India and Pakistan was a huge stone

step for IJM Corporation Berhad in standing where it is right now.

In April 2007, IJM acquired the Road Builder Group, its nearest competitor, to augment

its position as one of the country’s biggest builders. Making it to stand firm as one of the best

leading corporation in Malaysia. In addition to bolstering its construction order book, property

land bank and infrastructure portfolio, the enlarged Group enabled IJM to attain considerable

synergistic benefits, greater local prominence as well as attain a more sizeable balance sheet to

bid for larger jobs and facilitate its expansion into overseas markets. By doing so, the business of

5 | P a g e

IJM Corporation have extended to a whole new level where the corporation became larger and

achieving more business activities and projects throughout the years.

Leveraging on its construction expertise, the Group also owns and operates infrastructure

concessions to create long-term recurrent income streams. Initial advancements into concession

assets in Malaysia, however, proved elusive and, thus, an international focus was adopted. IJM's

involvement in overseas infrastructure privatisation schemes met with considerable success.

Amongst the corporation’s present investments in major overseas infrastructure projects are the

Western Access Tollway in Argentina, five tolled highways and the Gautami power plant in

India, and the Binh An water treatment concession in Vietnam. In Malaysia, the group owns and

operates three highways and port concessions from the RBH merger. IJM had previously

invested in and profitably sold several infrastructure assets in China. Making a stream of income

into IJM Corporation Berhad as an income that will always generate.

IJM's undertaking as a property developer began as a natural progression from its

experience in the construction business. The Group's property arm has since grown considerably.

IJM Land Berhad is one of the largest property developers in Malaysia with sprawling

townships, commercial buildings and high rise condominiums under development in key growth

areas throughout the country. Besides establishing itself as a reputable township developer in

India, IJM had also successfully undertaken ventures overseas in the past such as in Orlando

USA, Singapore and Australia. As stated showing that IJM also aim its business not only in

Malaysia but also in the foreign countries.

The Group also ventured into oil palm plantations in 1985 as a source of steady income to

cushion the cyclical nature of its core construction business. Where at that time the currency rate

of oil palm is high and demanding. This investment has since paid off handsomely towards the

corporation. Now listed on the Main Market of Bursa Securities, IJM Plantations Berhad has

contributed significantly to the Group's earnings over the years and has also accorded the Group

better resilience to weather macro-economic and input costs volatilities. Showing that the

Corporation itself is ready to dominate the oil palm plantation. It is currently expanding its

plantation operations throughout Indonesia in expanding the oil palm plantation business.

6 | P a g e

SUMMARY OF ANNUAL REPORT

Based on the income statement as 31st December, the operating revenue for 2010 is

RM471136000 while in 2011 is RM1703172000 and in 2012 is RM 1939676000. The highest

revenue for this company is in 2012 compare to the 2011 and 2010. The lowest revenue is in

2010 with RM 471136000, so this indicates that the company has improve its profitability by

increasing its sales revenue year by year.

Besides, the net profit for the year 2010 is RM 195537000, for 2011 is RM 302942000

and in 2012 is RM 447863000. As you can clearly see that in the year 2012 its net profit is

higher than both year which is 2011 and 2010. The highest is in 2012 with RM 447863000 and

the lowest is in 2010 with RM 195537000. This means that UEM Land increased their profit by

increasing its sales revenue in 2012 more than in 2011 and 2010.

Based on the Balance sheet as at 31st December, the total current assets in year 2010 is

RM 1782609000, in year 2011 is RM 3115162000 and in year 2012 is RM 4083978000. As you

can see the highest total assets is in year 2012 compare to 2011 and 2010. Between 2011 and

2010, the higher total assets is in 2011. In the year 2010, it has the lowest total assets than both

2011 and 2012. This show that this company has a good liquidity or which they can turned assets

into cash easily. Moreover, the non-current assets for UEM Land for the year 2010 is RM

2188524000 while in 2011 is RM4678595000 and in 2012 is RM5002507000. In 2012 the

company has higher non-current assets than in 2010 and 2011. The lowest non-current assets is

in 2010 with 2188524000, meaning UEM Land allocates the cost of the assets in 2012 is more

than 2011 and 2010 for which the assets will be used.

The non-current liability for 2010 is RM 569319000 and in year 2011 is RM 1772359000

whereas in 2012 is RM 1739978000. The lowest non-current liability is in 2010 with RM

569319000. The highest is in 2012 compare to both year in 2011 and 2010. These liabilities

7 | P a g e

represent in 2012 the money company owes is more than in 2011 and 2010. Furthermore, the

current liabilities in 2010 for UEM Land is RM 259864000, but in 2011 is RM 724785000 also

in 2012 is RM 1529472000. Hence, the highest current liabilities is in 2012 compared in 2011

and 2010. As for the lowest is in 2010. This shows that this company has grown in debt from

year to year.

8 | P a g e

SUMMARY OF ANNUAL REPORT

IJM Corporation which is one of the top corporation must have solid and stable foundation in

which they must up hold to. One of the few important prospect is net income of the firm itself.

For a big company as IJM Corporation, its net income had its ups and downs, where on 2010 its

net income had soar to 446 million. Where in the upcoming year which is 2011, the corporation’s

net income had fall back a little but went back up in the year of 2012. It can be seen that there’s a

fall of the net income in 2011 may due to the ineffectiveness and utilization of resource might be

not enough. The increased of the net income can be seen where from 304 million to 409 million

where there is an increase of 34.35% in its income growth between 2011 and 2012.

Other than that, revenue is a must watch figure in evaluating a company. As known

that revenue is corresponding with neither income nor profit, the graft line of the revenue is also

slightly the same. As stated, on 2010 the revenue of IJM Corporation Berhad had a revenue

worth of 4013 million where in 2011 the revenue of the firm had slightly decreased to 3721

million. But in the year of 2012, the corporation had stand tall again and made a revenue with the

amount of 4518 million. As well as the net income previously stated, the revenue is quite the

same where the revenue itself is align with the net income.

IJM Corporation a lot of assets which make it one if the stand tall firm in Malaysia.

The assets they had will always be used to generate more income for the upcoming future ahead.

The corporation itself own a sum of 12557 million of total asset in the year of 2010. The asset

had slightly went down the next upcoming year with the figure of 12554 million, showing that

there was an ineffective way in utilizing the assets. Following the next year which is 2012, the

total assets had rose up with a figure worth of 13891 million where it can be seen the way of the

corporation doing its activities do gave a positive return on them.

In summarizing the financial data of a company, the liabilities is an important thing to

be look into. Basically liabilities is known as the loan of a company or one would say liability

but in business activities, the higher the liability, the more business activities the company own.

9 | P a g e

Making it seem as a high and active firm. On the year of 2010, the corporation have a liability

that reached 5596 million where it had slightly increased in 2011 from the previously stated to

5988 million. Another year a full prosperity where the liability of the year in 2011 had increased

dramatically to the point of 6852 million.

Earnings per share is an important thing to be looking at. IJM Corporation Berhad had

given their shareholders of earnings per share worth 25.21 cent for basic and 24.84 cent for fully

diluted. Moving to the next year onward, the earnings per share had slightly drop to 23.88 cent

for basic and 23.26 for fully diluted. This incident can give a quite waver for the corporation in

maintaining its shareholders. On the year of 2012, the corporation went berserk and had an

earnings of 29.84 cent for its basic earnings per share. This had given a great trust to the

company and also its shareholder on the increase rate of earnings per share.

10 | P a g e

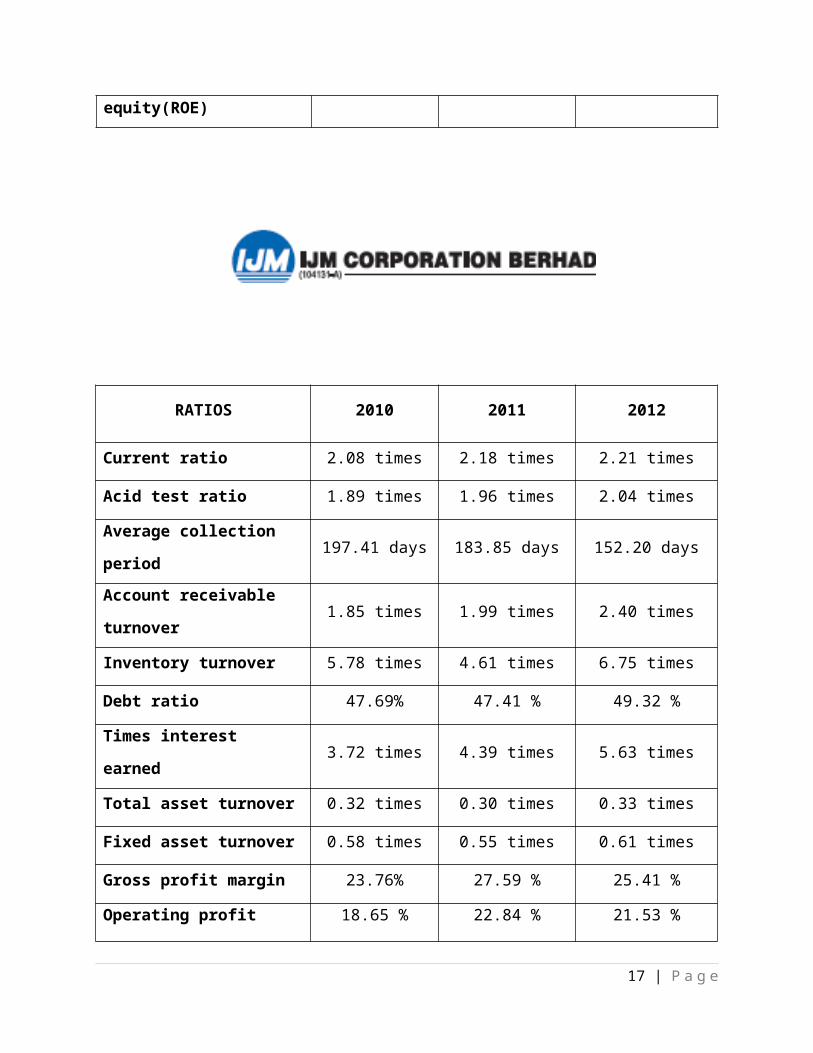

RATIOS 2010 2011 2012

Current ratio 6.86 times 4.30 times 2.67 times

Acid test ratio 6.70 times 4.13 times 2.59 times

Average collection period 354.00 days 217.70 days 337.14 days

Account receivable turnover 1.03 times 1.68 times 1.08 times

Inventory turnover 6.14 times 9.51 times 10.05 times

Debt ratio 20.88 % 32.04 % 35.98 %

Times interest earned 25.79 times 7.91times 13.93times

Total asset turnover 0.12 times 0.22 times 0.21 times

Fixed asset turnover 0.22 times 0.36 times 0.39 times

Gross profit margin 44.93 % 30.45 % 36.48 %

Operating profit margin 38.09 % 21.38 % 25.12 %

Net profit margin 41.54 % 17.79 % 23.09 %

Operating return on assets 5.38 % 5.22% 6.34 %

Return on equity(ROE) 6.23 % 5.85 % 7.86 %

11 | P a g e

RATIOS 2010 2011 2012

Current ratio 2.08 times 2.18 times 2.21 times

Acid test ratio 1.89 times 1.96 times 2.04 times

Average collection period 197.41 days 183.85 days 152.20 days

Account receivable turnover 1.85 times 1.99 times 2.40 times

Inventory turnover 5.78 times 4.61 times 6.75 times

Debt ratio 47.69% 47.41 % 49.32 %

Times interest earned 3.72 times 4.39 times 5.63 times

Total asset turnover 0.32 times 0.30 times 0.33 times

Fixed asset turnover 0.58 times 0.55 times 0.61 times

Gross profit margin 23.76% 27.59 % 25.41 %

Operating profit margin 18.65 % 22.84 % 21.53 %

Net profit margin 10.54 % 12.88 % 12.19 %

Operating return on assets 5.95 % 6.75 % 7.00 %

Return on equity(ROE) 6.55 % 7.36 % 7.91 %

12 | P a g e

RATIO ANALYSIS

(Trends Analysis)

Based on the liquidity ratio which is current ratio and Acid test ratio, In 2010, UEM Land

Holdings current ratio is greater compare to year 2011. The company in 2010 has 6.86 times

assets whereas in 2011 has 4.30 times assets. Meanwhile, in year 2012 the company recorded a

current ratio of 2.67 times. This shows a decreasing trends of current ratio for the three

consecutive years. Therefore, it shows that in 2010, UEM Land has more sufficient short- term

assets to settle short- term liabilities.

Acid test ratio for UEM Land Holdings in year 2010 is higher compare to year 2011. The

acid test ratio for the company in 2010 is 6.70 times and in 2011 is 4.13 times while in 2012 is

2.59 times. UEM Land in 2010 is more capable in paying its liabilities and obligations due to the

higher acid test ratio.

13 | P a g e

2010 2011 20120

1

2

3

4

5

6

7

8

Current ratio Acid test ratio

Year

Tim

es

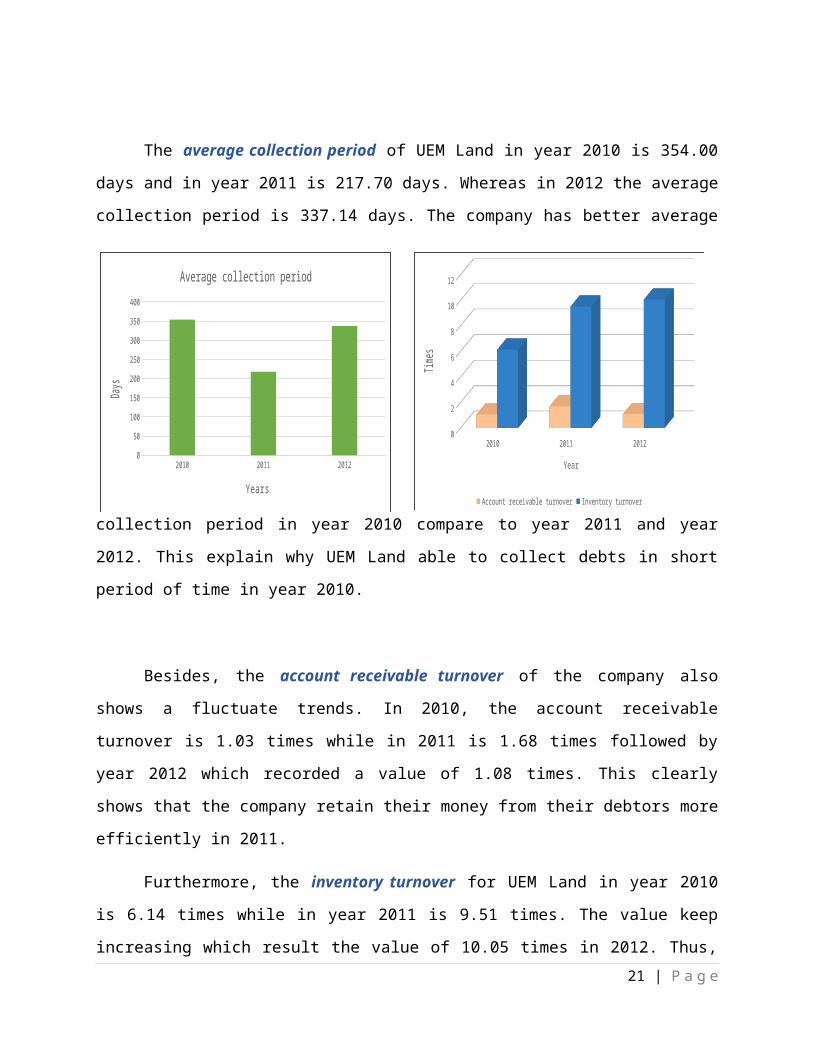

The average collection period of UEM Land in year 2010 is 354.00 days and in year

2011 is 217.70 days. Whereas in 2012 the average collection period is 337.14 days. The

company has better average collection period in year 2010 compare to year 2011 and year 2012.

This explain why UEM Land able to collect debts in short period of time in year 2010.

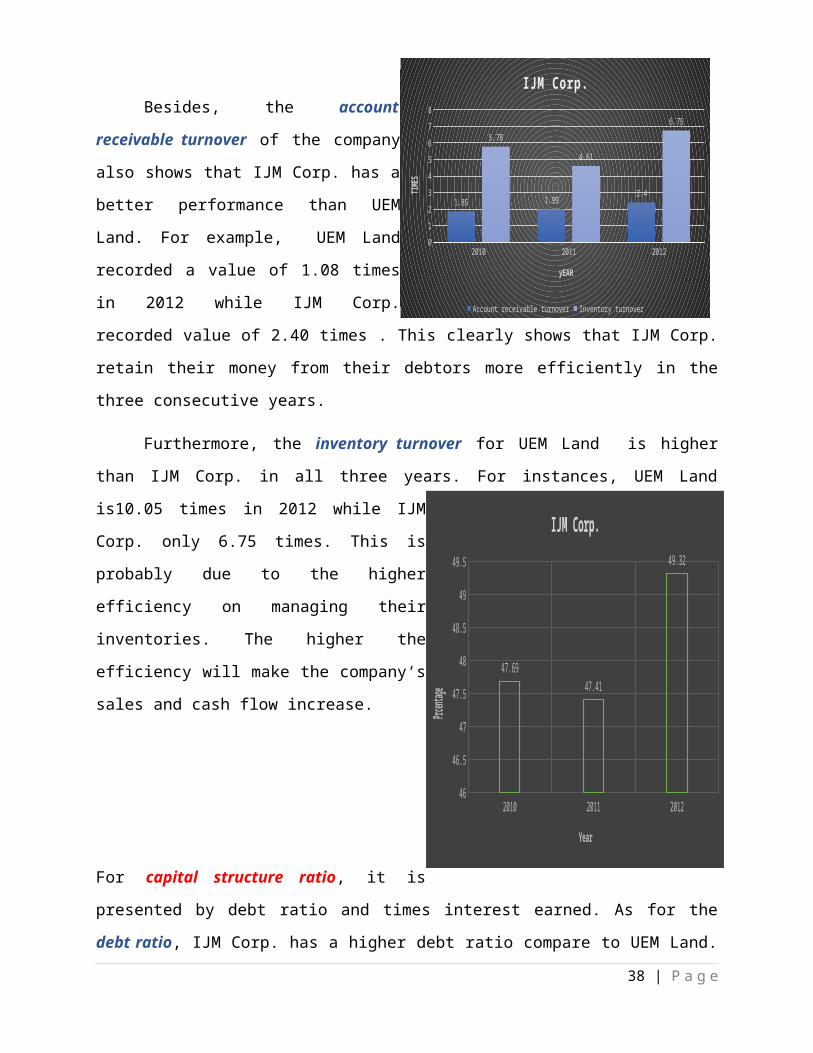

Besides, the account receivable turnover

1.03 times while in 2011 is 1.68 times followed by year 2012 which recorded a value of 1.08

times. This clearly shows that the company retain their money from their debtors more

efficiently in 2011.

Furthermore, the inventory turnover for UEM Land in year 2010 is 6.14 times while in

year 2011 is 9.51 times. The value keep increasing which result the value of 10.05 times in 2012.

Thus, 2012 recorded the highest inventory turnover compare to 2011 and 2010. This is probably

due to the higher efficiency on managing their inventories. The higher the efficiency will make

the company‘s sales and cash flow increase.

14 | P a g e

2010 2011 20120

2

4

6

8

10

12

Account receivable turnover Inventory turnover

Year

Times

2010 2011 20120

50

100

150

200

250

300

350

400

Average collection period

Years

Days

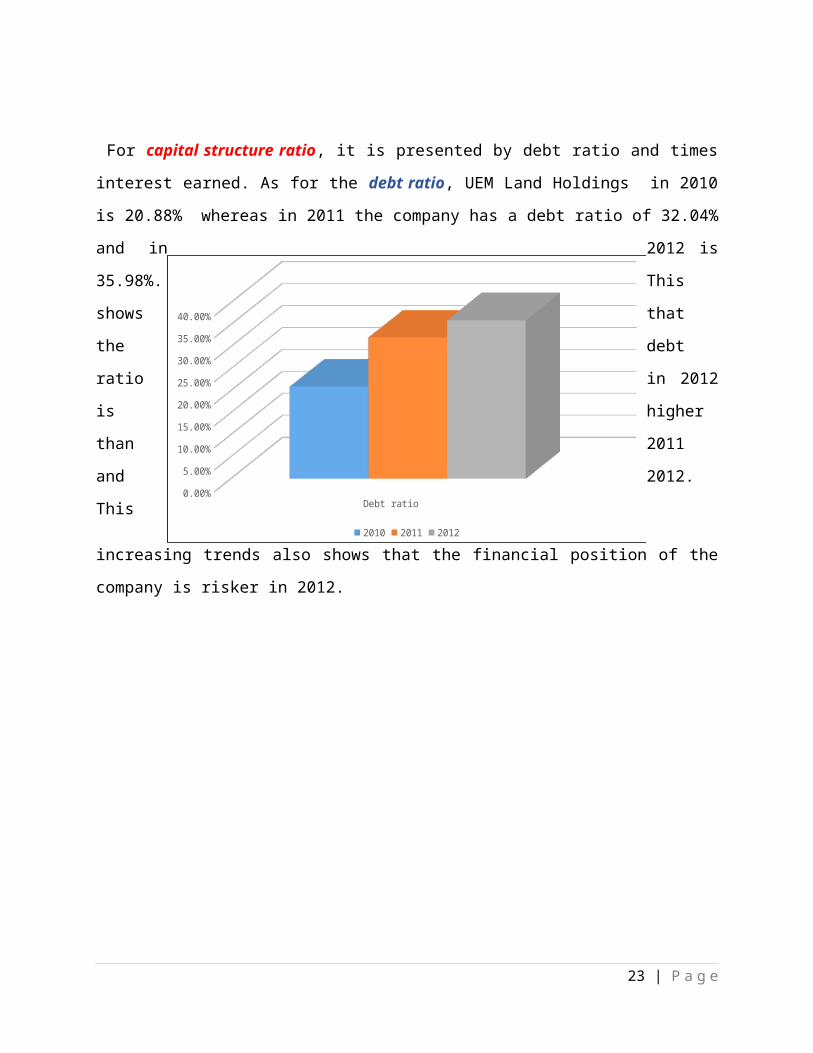

For capital structure ratio, it is presented by debt ratio and times interest earned. As for the debt

ratio, UEM Land Holdings in 2010 is 20.88% whereas in 2011 the company has a debt ratio of

32.04% and in 2012 is 35.98%. This shows that the debt ratio in 2012 is higher than 2011 and

2012. This increasing trends also shows that the financial position of the company is risker in

2012.

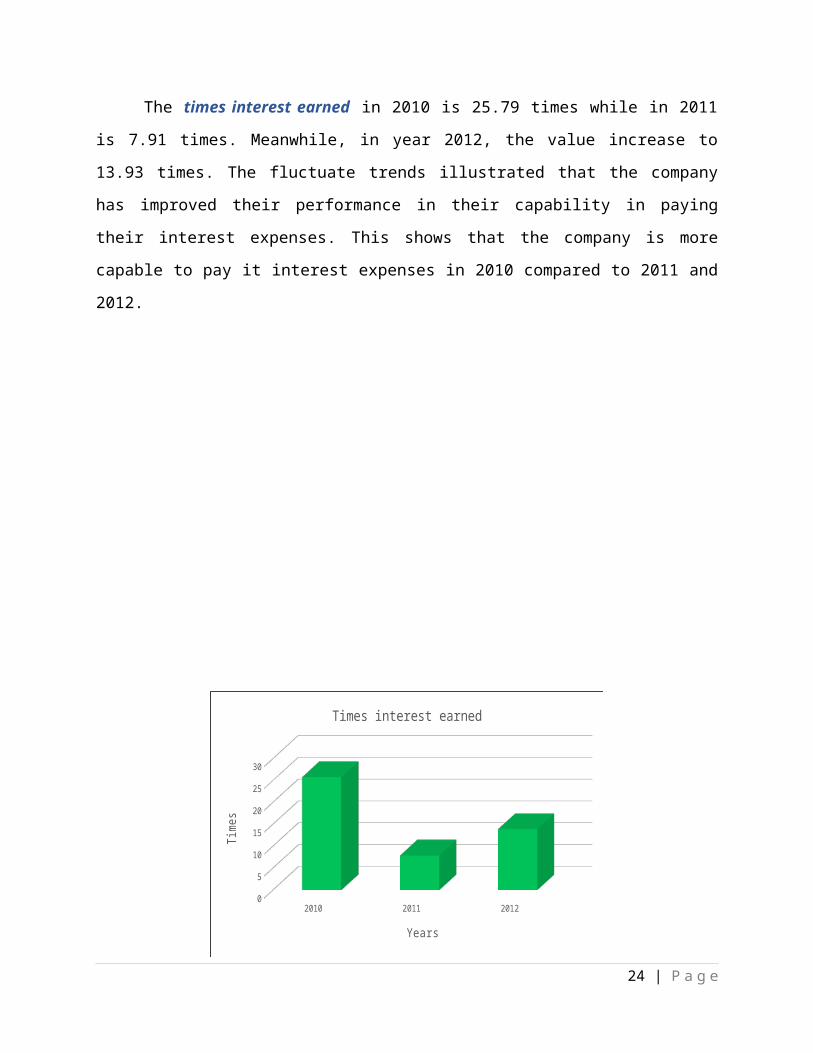

The times interest earned in 2010 is 25.79 times while in 2011 is 7.91 times. Meanwhile,

in year 2012, the value increase to 13.93 times. The fluctuate trends illustrated that the company

has improved their performance in their capability in paying their interest expenses. This shows

that the company is more capable to pay it interest expenses in 2010 compared to 2011 and 2012.

15 | P a g e

Debt ratio0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

2010 2011 2012

2010 2011 20120

5

10

15

20

25

30

Times interest earned

Years

Time

s

For the assets management ratio, it is presented by the total assets turnover and fixed assets

turnover. The total assets turnover in year 2010 is 0.12 times whereas in year 2011 is 0.22 times.

Besides, in 2012, the total assets turnover is 0.21 times. Thus, in year 2011 the assets turnover is

higher than year 2010 and 2012. This shows that in year 2011 the company uses its assets to

generate sales more efficiently.

As for the fixed assets turnover, in year 2010 recorded 0.22 times and in year 2011 is

0.36 times. Nevertheless, the value keep increasing in year 2012 which is 0.39 times. Thus, year

2012 has the highest fixed assets turnover.

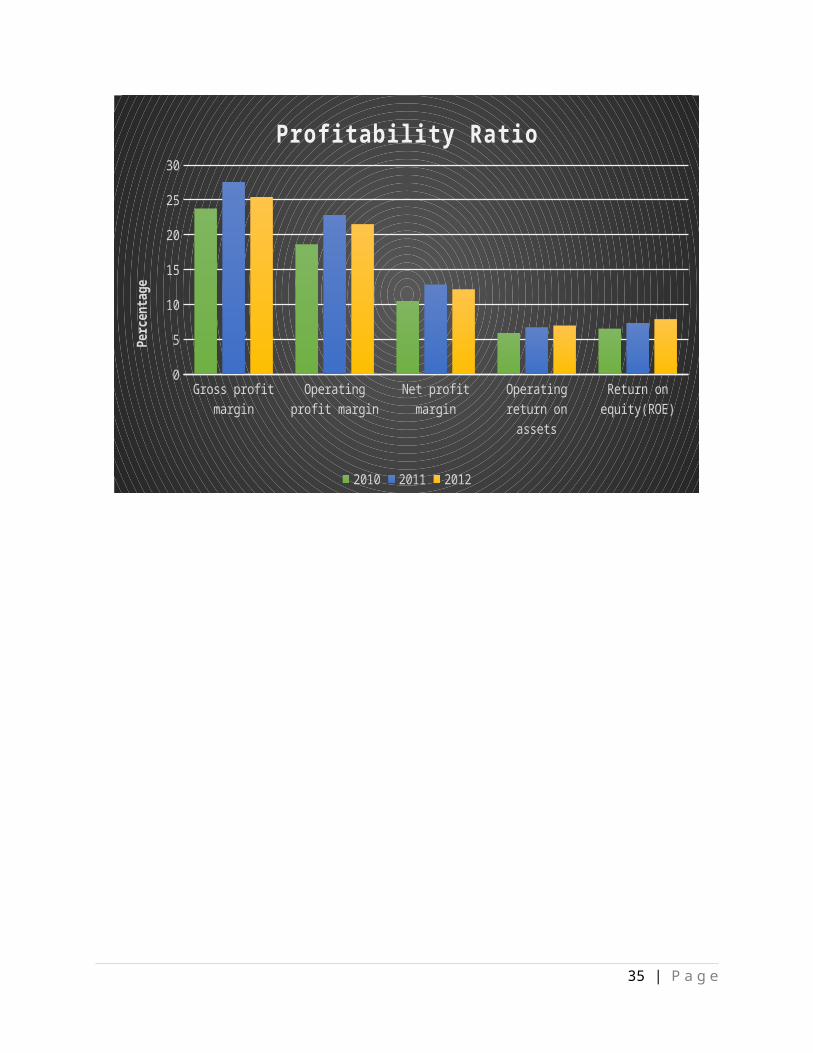

The profitability ratio is shown by the gross profit margin, operating profit margin, net profit

margin, operating return on assets and return on equity (ROE). For the gross profit margin, in

year 2010 recorded percentage of 4.93%, 30.45% in year 2011 and 36.48% in year 2012. The

operating profit margin at 2010 is 38.09% while in 2011 is at 21.38%. As for year 2012, the

percentage recorded is 25.12%. The net profit margin at 2010 is 41.54% and in 2011 is 17.79%

while in 2012 is 25.12% for UEM Land. Thus, year 2010 has the highest percentage for the three

ratio. This shows that the gross profit, operating profit and net profit generate per dollar of sales

is greater in 2010 compare to 2011 and 2012.

16 | P a g e

2010 2011 20120

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

Total asset turnover Fixed asset turnover

Years

Tim

es

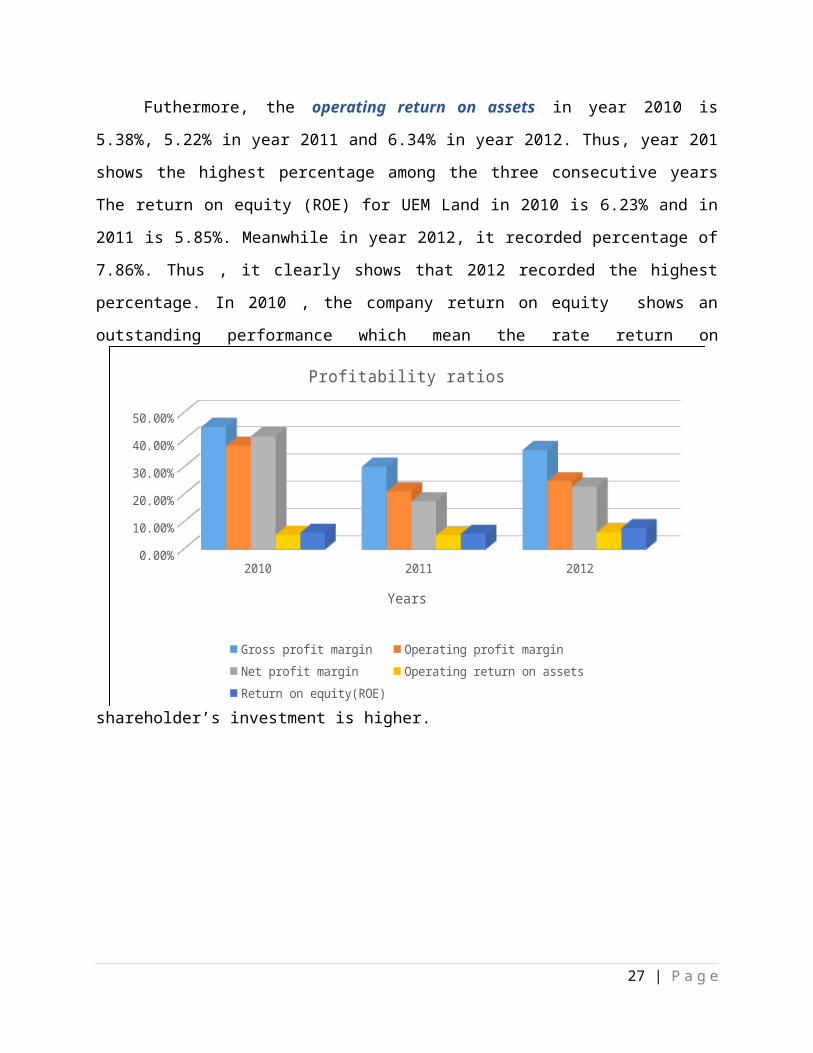

Futhermore, the operating return on assets in year 2010 is 5.38%, 5.22% in year 2011

and 6.34% in year 2012. Thus, year 201 shows the highest percentage among the three

consecutive years The return on equity (ROE) for UEM Land in 2010 is 6.23% and in 2011 is

5.85%. Meanwhile in year 2012, it recorded percentage of 7.86%. Thus , it clearly shows that

2012 recorded the highest percentage. In 2010 , the company return on equity shows an

outstanding performance which mean the rate return on shareholder’s investment is higher.

17 | P a g e

2010 2011 20120.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

Profitability ratios

Gross profit margin Operating profit margin Net profit marginOperating return on assets Return on equity(ROE)

Years

RATIO ANALYSIS

(Trends Analysis)

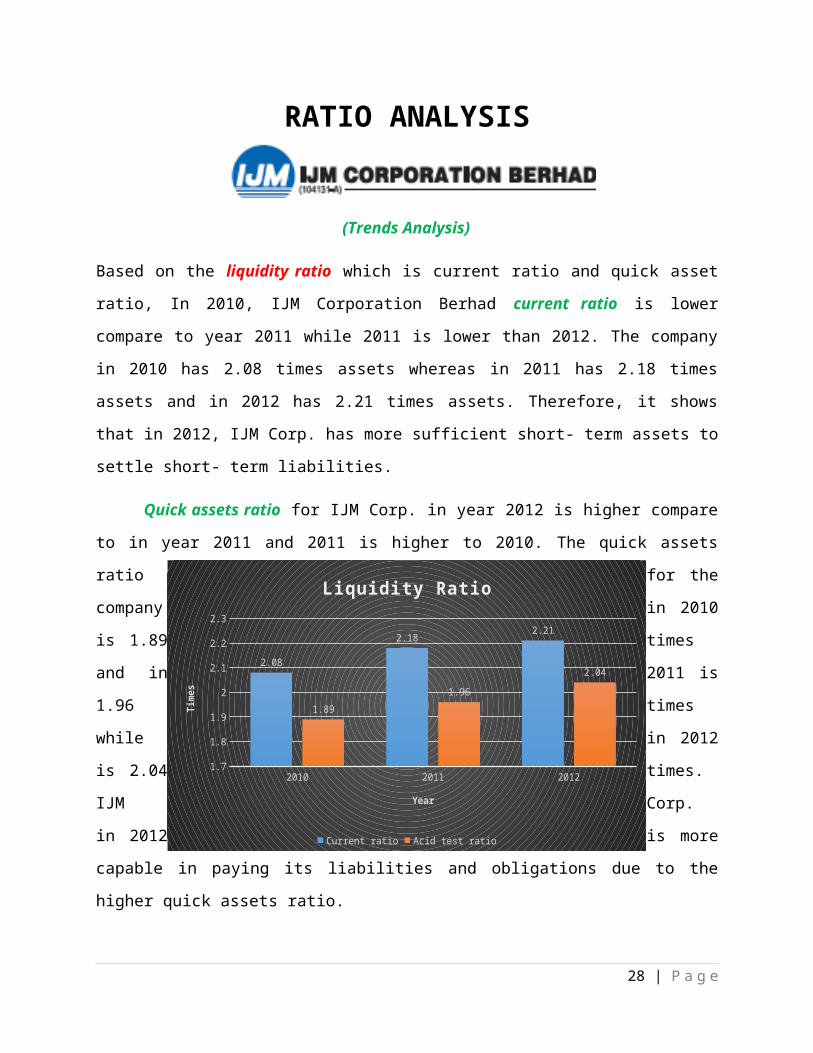

Based on the liquidity ratio which is current ratio and quick asset ratio, In 2010, IJM Corporation

Berhad current ratio is lower compare to year 2011 while 2011 is lower than 2012. The

company in 2010 has 2.08 times assets whereas in 2011 has 2.18 times assets and in 2012 has

2.21 times assets. Therefore, it shows that in 2012, IJM Corp. has more sufficient short- term

assets to settle short- term liabilities.

Quick assets ratio for IJM Corp. in year 2012 is higher compare to in year 2011 and 2011

is higher to 2010. The quick assets ratio for the company in 2010 is 1.89 times and in 2011 is

1.96 times while in 2012 is 2.04 times. IJM Corp. in 2012 is more capable in paying its liabilities

and obligations due to the higher quick assets ratio.

18 | P a g e

2010 2011 20121.7

1.8

1.9

2

2.1

2.2

2.3

2.08

2.182.21

1.89

1.96

2.04

Liquidity Ratio

Current ratio Acid test ratio

Year

Tim

es

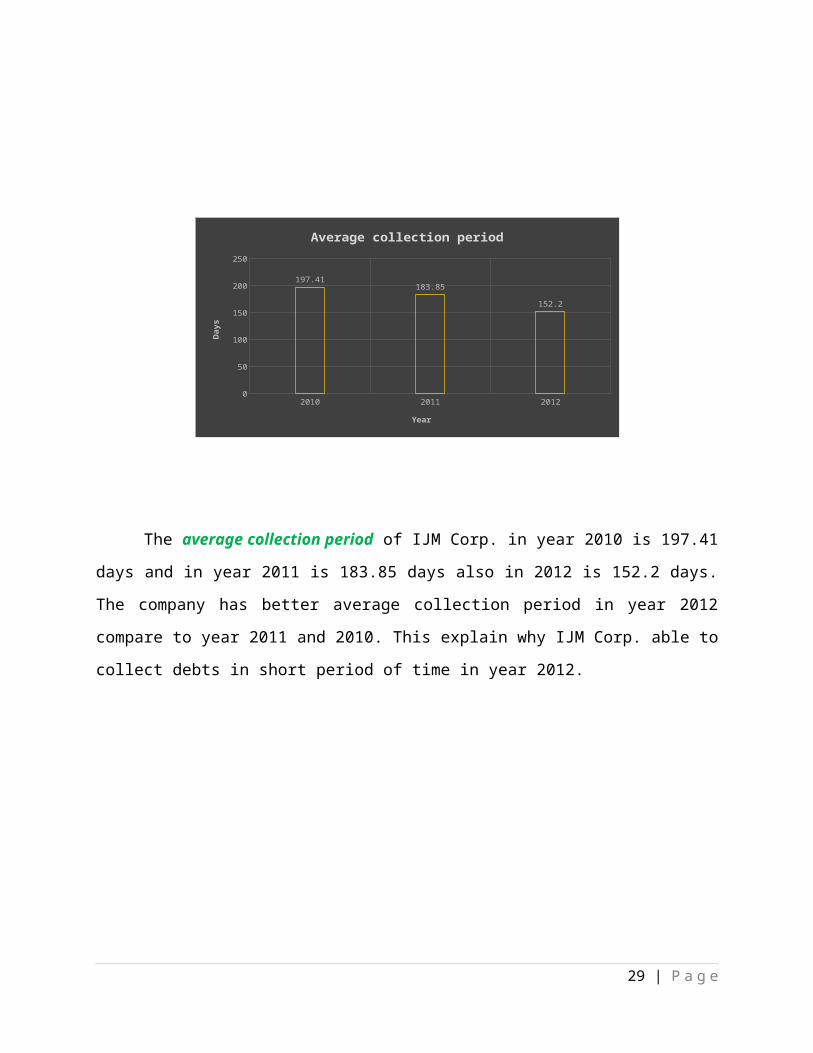

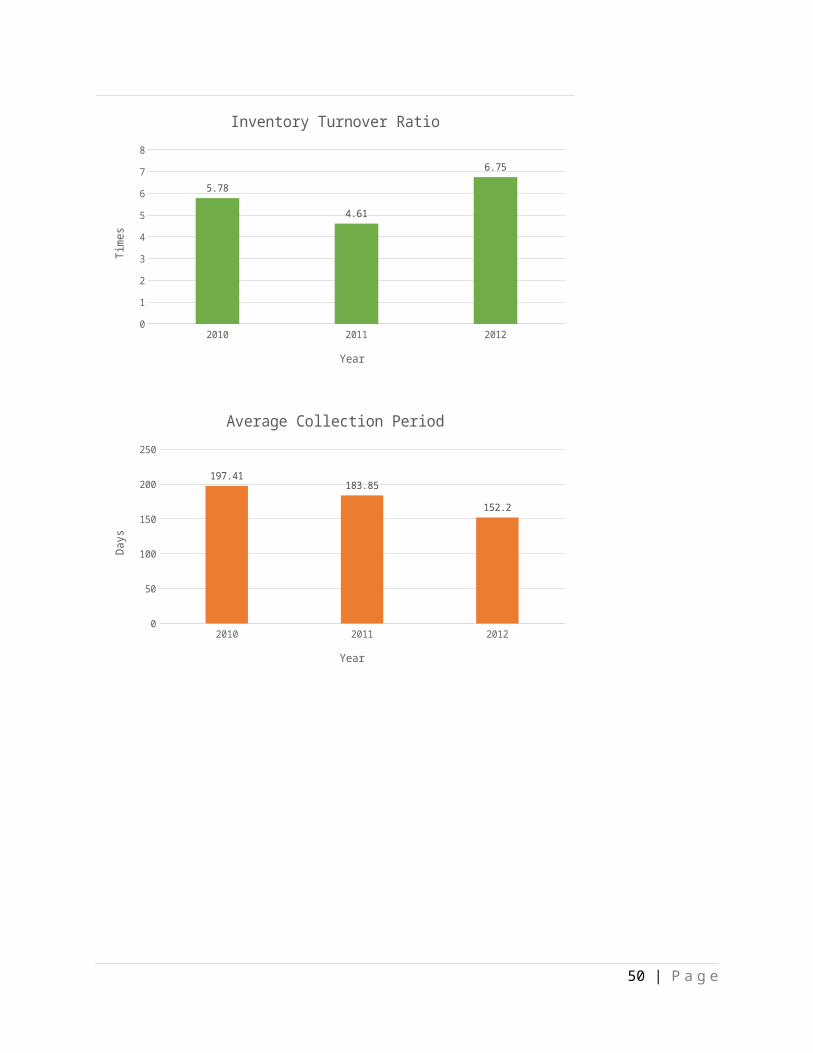

The average collection period of IJM Corp. in year 2010 is 197.41 days and in year 2011

is 183.85 days also in 2012 is 152.2 days. The company has better average collection period in

year 2012 compare to year 2011 and 2010. This explain why IJM Corp. able to collect debts in

short period of time in year 2012.

The account receivable turnover for the year 2010 is 1.85 times while the year 2011 is

1.99 times and in 2012 is 2.4 times. In 2012 the account receivable turnover is higher than in

2011 and 2010 so the company has better account receivables turnover than in year 2011 and

2010. This show that IJM Corp. able to roll over their debtors money faster.

Inventory turnover for IJM Corp. in year 2010 is 5.78 times, in year 2011 is 4.61 times

and in 2012 is 6.75 times. In year 2012 the inventory turnover is higher than 2011 and 2011 is

lower than 2010. This is probably due to the higher efficiency on managing their inventories.

The higher the efficiency will make the company‘s sales and cash flow increase.

19 | P a g e

2010 2011 20120

50

100

150

200

250

197.41183.85

152.2

Average collection period

Year

Day

s

2010 2011 20120

1

2

3

4

5

6

7

8

1.85 1.992.4

5.78

4.61

6.75

Account receivable turnover Inventory turnover

yEAR

TIMES

Based on the capital structure ratio, the debt ratio of IJM Corporation Berhad in 2010 is 47.69%

whereas in 2011 the company has a debt ratio of 47.41% while in year 2012 its debt ratio is

49.32%. This shows that the debt ratio in 2012 is higher than both 2011 and 2010 so this also

shows that the financial position of the company is riskier in 2012

The times interest earned in 2010 is 3.72 times while in 2011 is 4.39 times and in 2012 is

5.63 times. This shows that the company is more capable to pay it interest expenses in 2011

compared to 2010. Hence in 2012 the company is more capable to pay its interest in 2012 than in

2011. The company grow in a positive way year by year and the graph of IJM Corp. is expected

to increase in future year.

20 | P a g e

2010 2011 201246

46.5

47

47.5

48

48.5

49

49.5

47.6947.41

49.32

Debt ratio

Year

Prce

ntag

e

2010 2011 20120

1

2

3

4

5

6

3.72

4.39

5.63

Times interest earned

Year

times

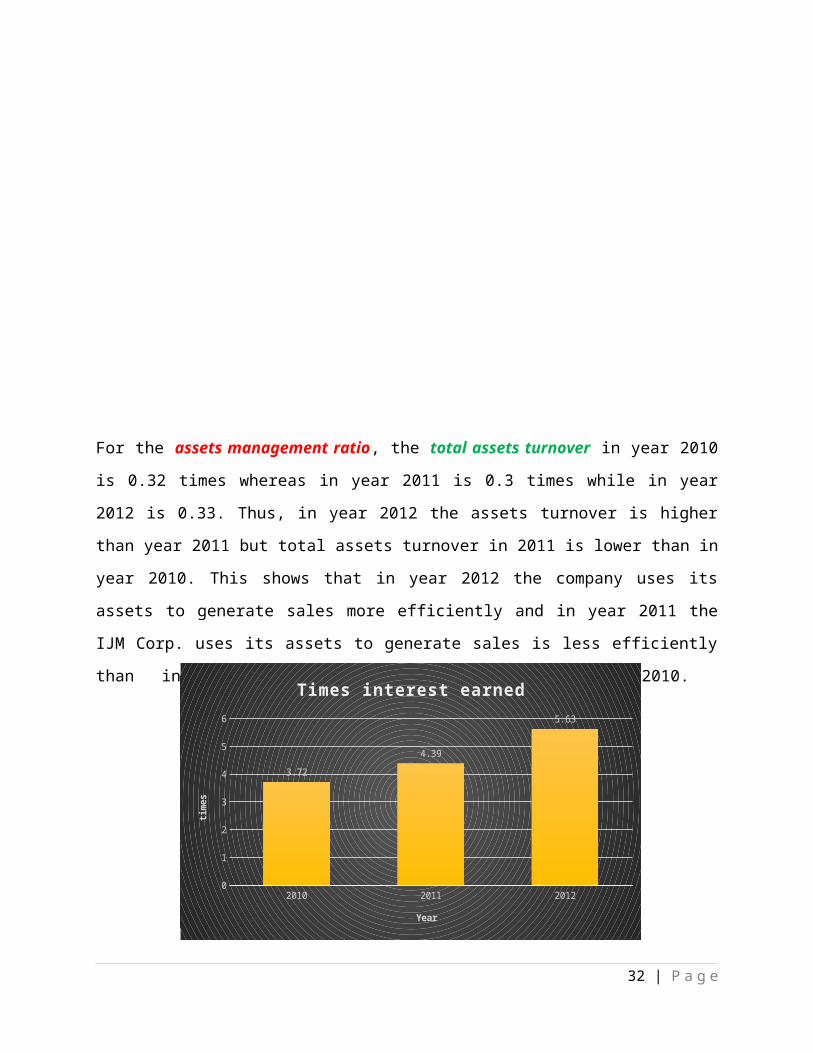

For the assets management ratio, the total assets turnover in year 2010 is 0.32 times whereas in

year 2011 is 0.3 times while in year 2012 is 0.33. Thus, in year 2012 the assets turnover is higher

than year 2011 but total assets turnover in 2011 is lower than in year 2010. This shows that in

year 2012 the company uses its assets to generate sales more efficiently and in year 2011 the IJM

Corp. uses its assets to generate sales is less efficiently than in 2010.

Fixed assets turnover in year 2010 is 0.58 times, in 2011 is 0.55 times and in year 2012

is 0.61 times. IJM Corp. presented that in year 2012 is higher fixed assets turnover than in both

2011 and 2010. So, in 2012 is the highest fixed assets turnover that is 0.61 times. The company

assets grow more in 2012.

Based on the profitability ratio, IJM Corporation Berhad in 2011 is greater and better than 2010

and 2012 but in 2012 the profitability ratio is better than in 2010. This is shown by the gross

profit margin, operating profit margin and net profit margin. The gross profit margin, operating

profit margin and net profit margin is fluctuated. The gross profit margin in year 2010 is lower

than 2011 which is 23.76% in year 2010 while 27.59% in year 2011. In year 2012, it is 25.41%

which is lower than 2011. The operating profit margin at 2010 is 18.65% while in 2011 is at

22.84% and in 2012 is 21.53%. The net profit margin at 2010 is 10.54% and in 2011 is 12.88%

whereas in 2012 is 12.19% for IJM Corp. This shows that the gross profit, operating profit and

net profit generate per dollar of sales is fluctuate in 2010 to 2012.

21 | P a g e

2010 2011 20120

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.32 0.30.33

0.580.55

0.61

Assets Management Ratio

Total asset turnover Fixed asset turnover

Year

Tim

es

The return on equity (ROE) for IJM Corp. in 2010 is 6.55% and in 2011 is 7.36% while

in year 2012 is 7.91%. In 2012 , the company return on equity shows an outstanding

performance which mean the rate return on shareholder’s investment is higher.

Besides, the operating return on assets in 2012 is greater than 2011 and in the year 2011

is higher than 2010 where in year 2012 the operating return on assets is 7% whereas in 2011 is

6.75% and in year 2010 is 5.95% only.

Gross profit margin Operating profit margin

Net profit margin Operating return on assets

Return on equity(ROE)

0

5

10

15

20

25

30

Profitability Ratio

2010 2011 2012

Perce

ntag

e

22 | P a g e

RATIO ANALYSIS

UEM LAND HOLDINGS VS IJM CORPORATION BERHAD

(Cross-sectional Analysis)

Based on the liquidity ratio which is current ratio and acid test ratio, In 2012, UEM Land

Holdings current ratio is greater compare to IJM Corp.Berhad. UEM Land has 2.67 times

assets whereas IJM Corp.has 2.21 times assets. This performance is also the same as in 2010 and

2011 which shows that UEM Land has higher current ratio. Therefore, it shows that UEM Land

has more sufficient short- term assets to settle short- term liabilities.

Likewise, acid test ratio for UEM Land in year 2012 is higher compare to IJM Corp. The

acid test ratio for the UEM Land in 2012 is 2.59 times and IJM Corp.is 2.04 times. This

outstanding performance by UEM Land are similar in year 2010 and 2011 with a higher acid test

ratio compare to IJM Corp. Therefore, UEM Land is more capable in paying its liabilities and

obligations due to the higher acid test ratio.

23 | P a g e

2010 2011 20120

1

2

3

4

5

6

7

8

UEM Land

Current ratio Acid test ratio

Year

Times

2010 2011 20121.7

1.8

1.9

2

2.1

2.2

2.3

2.08

2.182.21

1.89

1.96

2.04

IJM Corp.

Current ratio Acid test ratio

Year

Times

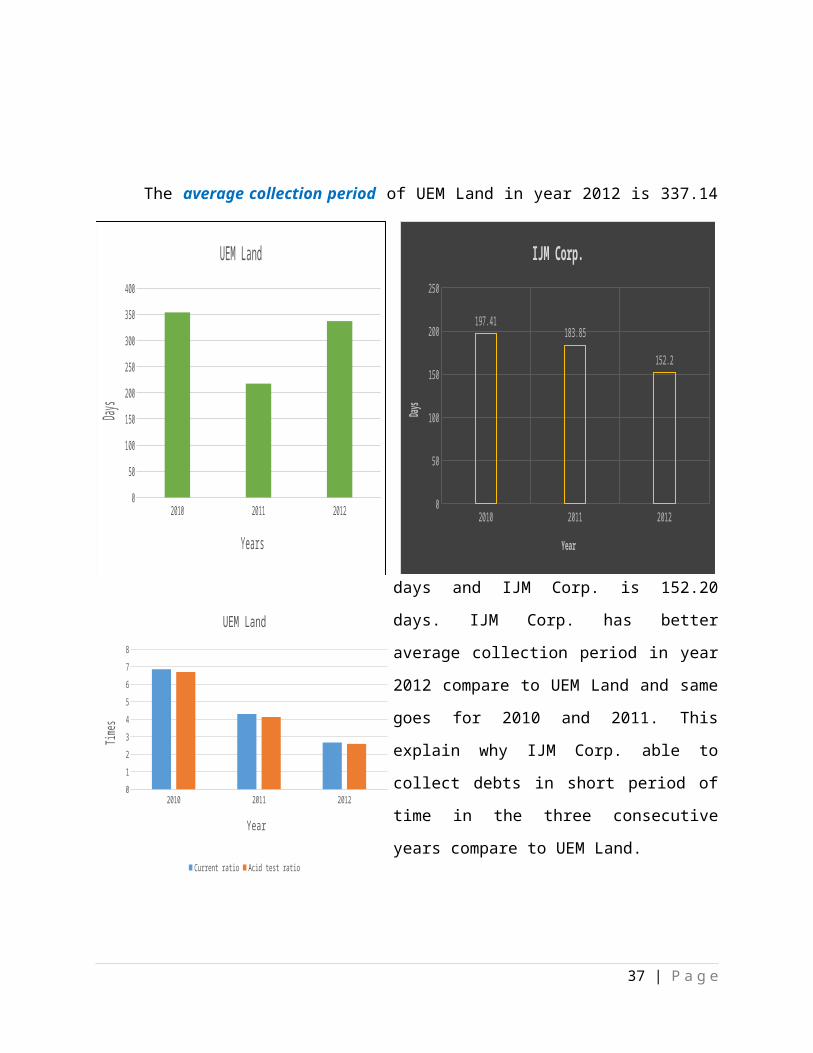

The average collection period of UEM Land in year 2012 is 337.14 days and IJM Corp.

is 152.20 days. IJM Corp. has better average collection period in year 2012 compare to UEM

Land and same goes for 2010 and 2011. This explain why IJM Corp. able to collect debts in

short period of time in the three consecutive years compare to UEM Land.

Besides, the account receivable turnover of the company also shows that IJM Corp. has

a better performance than UEM Land. For example, UEM Land recorded a value of 1.08 times

in 2012 while IJM Corp. recorded value of 2.40 times . This clearly shows that IJM Corp. retain

their money from their debtors more efficiently in the three consecutive years.

Furthermore, the inventory turnover for UEM Land is higher than IJM Corp. in all three

years. For instances, UEM Land is10.05 times in 2012 while IJM Corp. only 6.75 times. This is

probably due to the higher efficiency on managing their inventories. The higher the efficiency

will make the company‘s sales and cash flow increase.

24 | P a g e

2010 2011 20120

50

100

150

200

250

300

350

400

UEM Land

Years

Days

2010 2011 20120

50

100

150

200

250

197.41183.85

152.2

IJM Corp.

Year

Days

For capital structure ratio, it is presented by debt ratio and times interest earned. As for the debt

ratio, IJM Corp. has a higher debt ratio compare to UEM Land. For example in 2012, UEM

25 | P a g e

2010 2011 20120

2

4

6

8

10

12

UEM Land

Account receivable turnover Inventory turnover

Year

Times

2010 2011 20120

1

2

3

4

5

6

7

8

1.85 1.992.4

5.78

4.61

6.75

IJM Corp.

Account receivable turnover Inventory turnover

yEAR

TIMES

Debt ratio0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

UEM Land

2010 2011 2012

2010 2011 201246

46.5

47

47.5

48

48.5

49

49.5

47.6947.41

49.32

IJM Corp.

Year

Prcentag

e

The times interest earned of UEM Land is better than IJM Corp. For example, UEM

Land recorded a value of 13.93 times while IJM Corp. only 5.63 times in year 2012.This shows

that the UEM Land is more capable to pay it interest expenses in 2010 compared to 2011 and

2012.

For

the

assets management ratio, it is presented by the

total assets turnover and fixed assets turnover. The total assets turnover and fixed assets

turnover of IJM Corp. is better than UEM Land. For example, in 2012 UEM Land recorded 0.21

times while IJM Corp. recorded 0.33 times for total assets turnover . Meanwhile, For fixed assets

turnover, IJM Corp. recorded value of 0.61 times and UEM Land recorded value of 0.39 times

in 2012.

26 | P a g e

2010 2011 20120

5

10

15

20

25

30

UEM Land

Years

Times

2010 2011 20120

1

2

3

4

5

6

3.72

4.39

5.63

IJM Corp.

Year

times

2010 2011 20120

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

Total asset turnover Fixed asset turnover

Years

Times

2010 2011 20120

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.32 0.30.33

0.580.55

0.61

IJM Corp.

Total asset turnover Fixed asset turnover

Year

Times

The profitability ratio is shown by the gross profit margin, operating profit margin, net profit

margin, operating return on assets and return on equity (ROE). For the gross profit margin,

36.48% in year 2012 by UEM Land while IJM Corp. recorded percentage of 25.41% . The

operating profit margin of UEM Land as for year 2012, is 25.12% while IJM Corp. only

21.53% The net profit margin of UEM Land in 2012 is 25.12% while IJM Corp. only 12.19%.

Thus, UEM Land has the highest percentage for the three ratio and three consecutive years. This

shows that the gross profit, operating profit and net profit generate per dollar of sales is greater

by UEM Land compare to IJM Corp.

However, the operating return on assets and return on equity (ROE) of IJM Corp. is

higher than UEM Land. IJM Corp. return on equity shows an outstanding performance which

mean the rate return on shareholder’s investment is higher

Gross profit margin Operating profit margin

Net profit margin Operating return on assets

Return on equity(ROE)

0

5

10

15

20

25

30

IJM Corp.

2010 2011 2012

Pe

rce

nta

ge

27 | P a g e

2010 2011 20120.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

UEM Land

Gross profit margin Operating profit margin Net profit marginOperating return on assets Return on equity(ROE)

Years

28 | P a g e

CASH CONVERSION CYCLE

2010 2011 2012

Inventory Turnover

Ratio

6.14 times 9.51 times 10.05 times

Inventory

Conversion Period

59.45 days 38.38 days 36.32 days

Average Collection

Period

354.00 days 217.70 days 337.14 days

Account Payable

Deferral Period

413.45 days 256.08 days 373.46 days

Operating Cycle 218.99 days 158.94 days 211.11 days

Cash Conversion

Cycle

194.46 days 97.14 days 162.35 days

29 | P a g e

YEAR

DETAIL

2012 2013 20140

2

4

6

8

10

12

1412.49

9.8

11.46

Inventory Turnover Ratio

Year

Tim

es

30 | P a g e

2012 2013 20140

5

10

15

20

25

30

35

40

29.22

37.24

31.85

Inventory Conversion Period

Year

Days

2012 2013 20140

5

10

15

20

25

30

11.31

27.47

10.95

Average Collection Period

Year

Days

2012 2013 20140

10

20

30

40

50

60

70

40.53

64.71

42.8

Operating Cycle

Year

Days

31 | P a g e

2012 2013 201425

25.5

26

26.5

27

27.5

26.2

27.19

25.8

Account Payable Deferral Period

Year

Days

2012 2013 20140

5

10

15

20

25

30

35

40

14.33

37.52

17

Cash Conversion Cycle

Year

Days

32 | P a g e

Inventory Turnover

Inventory Conversion Period

Average Collection Period

Operating Cycle

AccountPayable Deferral Period

Cash Coversion Cycle

0 10 20 30 40 50 60 70

11.46

31.85

10.95

42.8

25.8

17

9.8

37.24

27.47

64.71

27.19

37.52

12.49

29.22

11.31

40.53

26.2

14.33

Analysis

2012 2013 2014

The operating cycle of UEM Land was longer in 2012 than in 2011 but the longest operating

cycle was in 2010. It shows that UEM Land had improvement in managing its working capital in

2011 than in 2010. However, the operating cycle in 2012 increase from 256.08 days to 373.46

days. EUM Land operating cycle in 2011 has the lowest record in these 3 years of operating

which is the best of these 3 years.

For inventory conversion period, UEM Land experienced a slightly decreasing in number

of days taken to sell their inventories over these 3 years from 2010 till 2012. Sales of EUM Land

is increase from 2010 till 2012 based on inventory conversion period, the inventories became

faster to convert into sales. Therefore, the best inventory conversion period was 2012.

In 2011, the chart shows that the average collection period for EUM Land is shorter than

2010. In 2011, it clearly shows that EUM Land able to collect from their account receivable

efficiently but in 2012 EUM Land had some problem in collecting debt from their account

receivable as the average collection period increase from 217.7 days to 337.14 days.

33 | P a g e

For account payable deferral period, 2011 has the lowest days among these 3 years. 2012 has

higher days than 2011 in paying its supplier but lower days than 2010. The average number of

days taken to pay its suppliers in 2010 is the highest among these 3 years which is the worst.

Conclusion, 2011 has the best account payable deferral period as the lowest days is the best.

34 | P a g e

CASH CONVERSION CYCLE

2010 2011 2012

Inventory Turnover

Ratio

5.78 times 4.61 times 6.75 times

Average Collection

Period

197.41 days 183.85 days 152.20 days

Account Payable

Deferral Period

201.49 days 222 days 193.40 days

Inventory

Conversion Period

63.15 days 78.16 days 54.10 days

Operating Cycle 260.56 days 262.01 days 206.30 days

Cash Conversion

Cycle

59.07 days 40.01 days 12.90 days

35 | P a g e

YEAR

DETAIL

36 | P a g e

2010 2011 20120

1

2

3

4

5

6

7

8

5.78

4.61

6.75

Inventory Turnover Ratio

Year

Times

2010 2011 20120

50

100

150

200

250

197.41183.85

152.2

Average Collection Period

Year

Days

37 | P a g e

2010 2011 2012175

180

185

190

195

200

205

210

215

220

225

201.49

222

193.4

Account Payable Deferral Period

Year

Days

2010 2011 20120

10

20

30

40

50

60

70

80

90

63.15

79.18

54.1

Inventory Conversion Period

Year

Days

38 | P a g e

2010 2011 20120

50

100

150

200

250

300

260.56 263.03

206.3

Operating Cycle

Year

Days

2010 2011 20120

10

20

30

40

50

60

70

59.07

41.03

12.9

Cash Conversion Cycle

Year

Days

39 | P a g e

I nv en t o r y T

u r n o v er Rati o

Av er ag e Co l l

ec tio n Pe r i o

d

Ac c o u n t Pa y ab l e

Defe

r r a l P e r i o

d

I nv en t o r y C

o n v er s i on P

er i od

Op er ati n g C

y c l e

C a sh Co n v er s i o

n Cy c l e5

.78

19

7.4

1

20

1.4

9

63

.15

26

0.5

6

59

.07

4.6

1

18

3.8

5

22

2

79

.18

26

3.0

3

41

.03

6.7

5

15

2.2

19

3.4

54

.1

20

6.3

12

.9

Chart Title2010 2011 2012

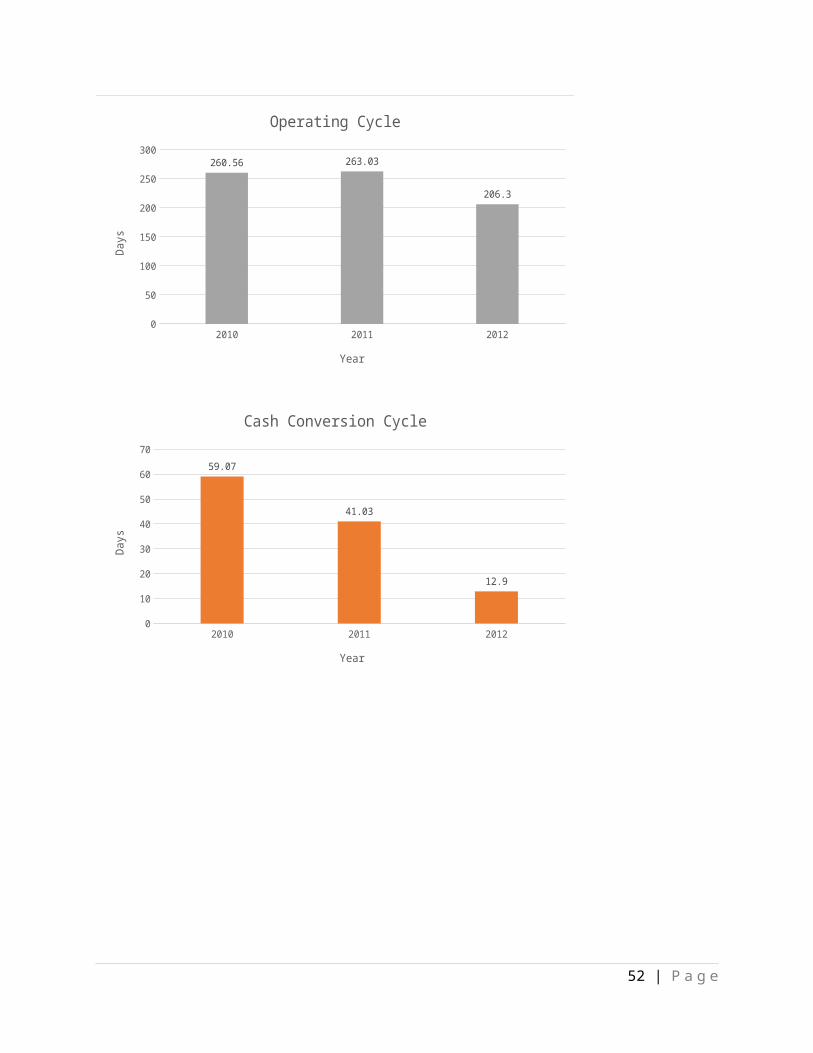

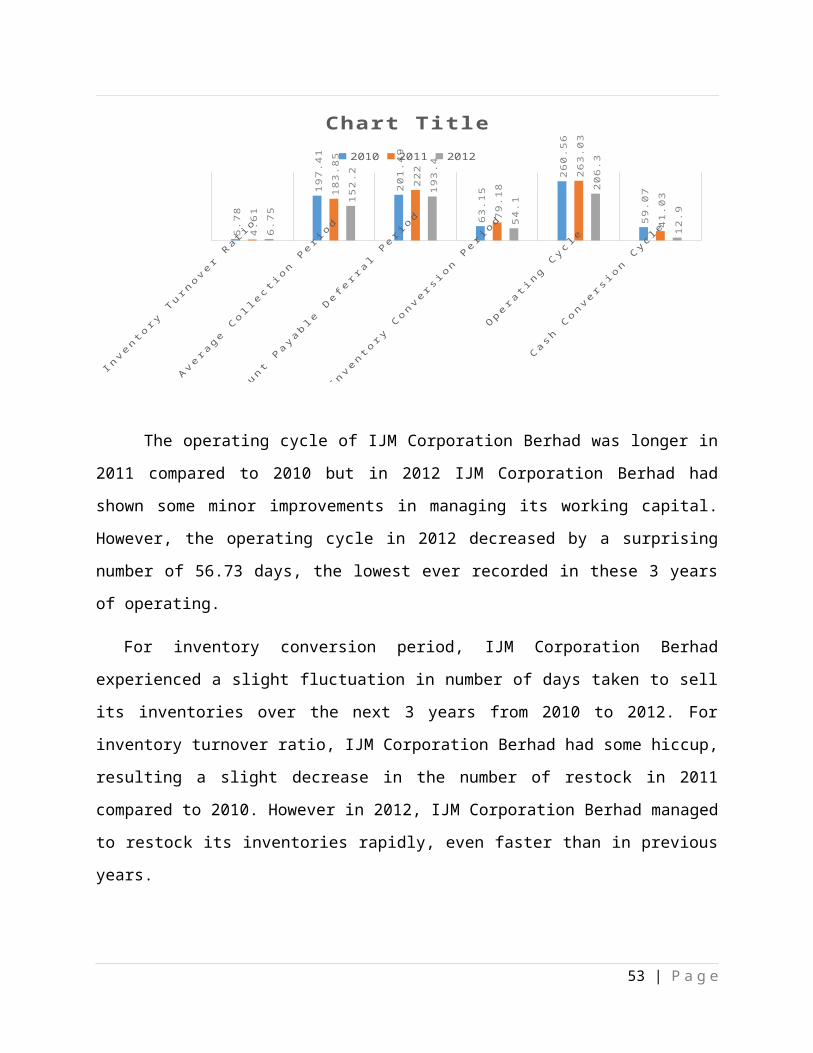

The operating cycle of IJM Corporation Berhad was longer in 2011 compared to 2010 but

in 2012 IJM Corporation Berhad had shown some minor improvements in managing its working

capital. However, the operating cycle in 2012 decreased by a surprising number of 56.73 days,

the lowest ever recorded in these 3 years of operating.

For inventory conversion period, IJM Corporation Berhad experienced a slight fluctuation in

number of days taken to sell its inventories over the next 3 years from 2010 to 2012. For

inventory turnover ratio, IJM Corporation Berhad had some hiccup, resulting a slight decrease in

the number of restock in 2011 compared to 2010. However in 2012, IJM Corporation Berhad

managed to restock its inventories rapidly, even faster than in previous years.

In 2011, the chart shows that the average collection period for IJM Corporation Berhad is

shorter compared to 2010. It clearly shows that IJM Corporation Berhad was able to collect from

their account receivable efficiently. Maintaining the record, in 2012, IJM Corporation Berhad

was even more efficient in collecting debt from its account receivables, proving the statement is

its shorter average number of days compared to year 2011 and 2010.

For accounts payable deferral period, from 2010 to 2012, the average number of days taken

to pay its suppliers fluctuate, but managed to score the lowest days in 2012 which had given IJM

Corporation Berhad trade credit to finance the firm.

40 | P a g e

CONCLUSION

Based on the financial position of both company , it can conclude that UEM Land has a better overall performance compare to IJM Corp. UEM Land is more liquid from IJM Corp. except for the average collection period and account receivable turnover ratio. As for the capital structure ratio, IJM Corp. is much more riskier than UEM Land while for assets management ratio, IJM Corp. shows a better performance. UEM Land as the best financial position in year 2010 while IJM Corp in year 2012.

Besides, the cash conversion cycle of IJM Corp. is much more better than UEM Land. UEM Land has better cash conversion cycle in year 2011 while IJM Corp. in year 2012. This is due to the low period of cash conversion cycle which illustrates how fast a company can convert resource inputs into cash flows.

41 | P a g e

RECOMMENDATION

From the point of view of a bankers the company that deserves additional capital is UEM Land

Holdings because it has a better performance than IJM Corp. Based on the capital structure ratio,

UEM Land are more capable to pay their interest expenses and debt . Thus, the bank are more

confident in giving loan to this company . Besides, this company is more liquid. So, it can

convert its assets to money in much more shorter period. The increasing revenue in three

consecutive years really shows that the company are really on track. The IJM Corp. does not

deserve additional capital because its financial position is more riskier.

From the point of view of an investors, UEM Land in a good investment because based on the

return on equity, its shows an increasing trends. Thus, it illustrates that the company has manage

to increase the rate of return of the shareholder investment. Although IJM Corp. shows a better

result, but the company make less profit. Thus in future may result in lack of income in the

company.

42 | P a g e

REFERENCES

1. http://www.uemsunrise.com/pdf/UEMLAND_AR2012.pdf 2. http://www.uemsunrise.com/pdf/UEMLAND_AR2011.pdf 3. http://www.financialreport.biz/File/AR/2011/7/29/3336%20-%202152222830876.pdf 4. http://www.financialreport.biz/File/AR/2012/7/30/3336%20-%202152178469349.pdf

43 | P a g e

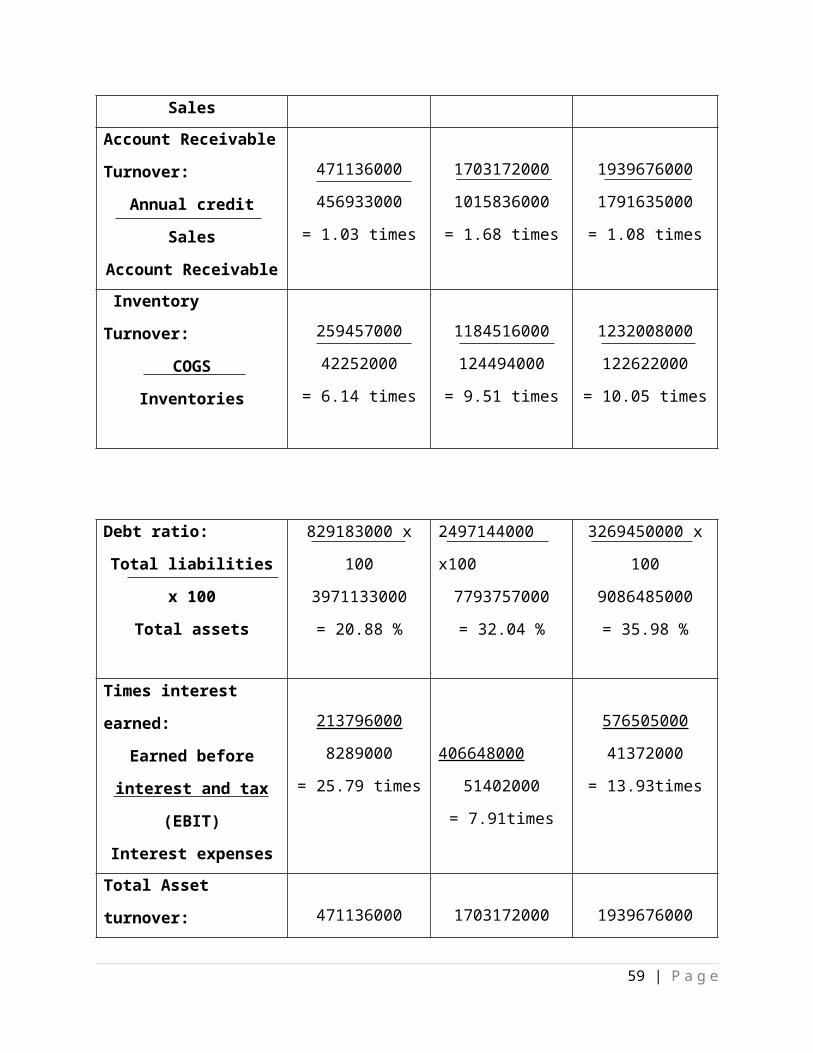

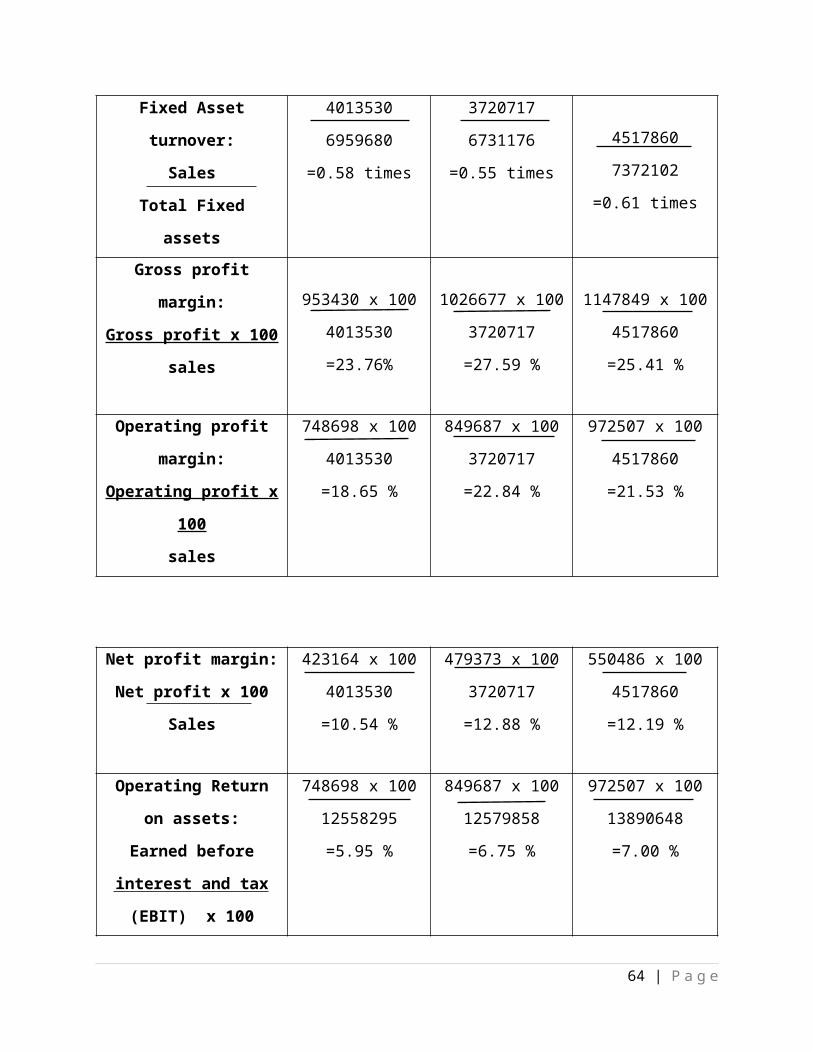

Calculation

RATIOS 2010 2011 2012

Current ratio:

Current Assets

Current Liabilities

1782609000

259864000

= 6.86 times

3115162000

724785000

= 4.30 times

4083978000

1529472000

= 2.67 times

Quick assets ratio:

(Current Assets–Stock)

Current Liabilities

(1782609000 -

42252000)

259864000

= 6.70 times

(3115162000 -

124494000)

724785000

= 4.13 times

(4083978000 –

122622000)

1529472000

= 2.59 times

Average collection

period:

Account Receivable x 365

Annual credit Sales

456933000 x 365

471136000

= 354.00 days

1015836000 x 365

1703172000

= 217.70 days

1791635000 x 365

1939676000

= 337.14 days

Account Receivable

Turnover:

Annual credit Sales

Account Receivable

471136000

456933000

= 1.03 times

1703172000

1015836000

= 1.68 times

1939676000

1791635000

= 1.08 times

Inventory Turnover:

COGS

Inventories

259457000

42252000

= 6.14 times

1184516000

124494000

= 9.51 times

1232008000

122622000

= 10.05 times

44 | P a g e

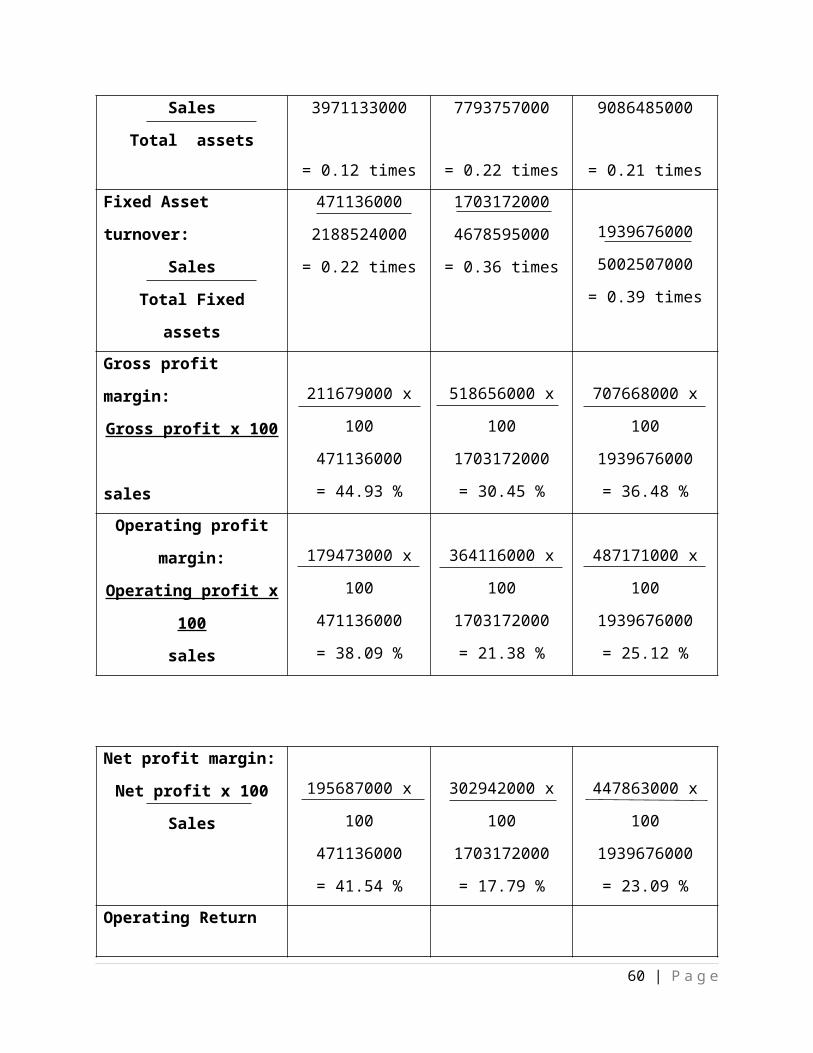

Debt ratio:

Total liabilities x 100

Total assets

829183000 x 100

3971133000

= 20.88 %

2497144000 x100

7793757000

= 32.04 %

3269450000 x 100

9086485000

= 35.98 %

Times interest earned:

Earned before interest

and tax (EBIT)

Interest expenses

213796000

8289000

= 25.79 times

406648000

51402000

= 7.91times

576505000

41372000

= 13.93times

Total Asset turnover:

Sales

Total assets

471136000

3971133000

= 0.12 times

1703172000

7793757000

= 0.22 times

1939676000

9086485000

= 0.21 times

Fixed Asset turnover:

Sales

Total Fixed assets

471136000

2188524000

= 0.22 times

1703172000

4678595000

= 0.36 times

1939676000

5002507000

= 0.39 times

Gross profit margin:

Gross profit x 100

sales

211679000 x 100

471136000

= 44.93 %

518656000 x 100

1703172000

= 30.45 %

707668000 x 100

1939676000

= 36.48 %

Operating profit margin:

Operating profit x 100

sales

179473000 x 100

471136000

= 38.09 %

364116000 x 100

1703172000

= 21.38 %

487171000 x 100

1939676000

= 25.12 %

45 | P a g e

Net profit margin:

Net profit x 100

Sales

195687000 x 100

471136000

= 41.54 %

302942000 x 100

1703172000

= 17.79 %

447863000 x 100

1939676000

= 23.09 %

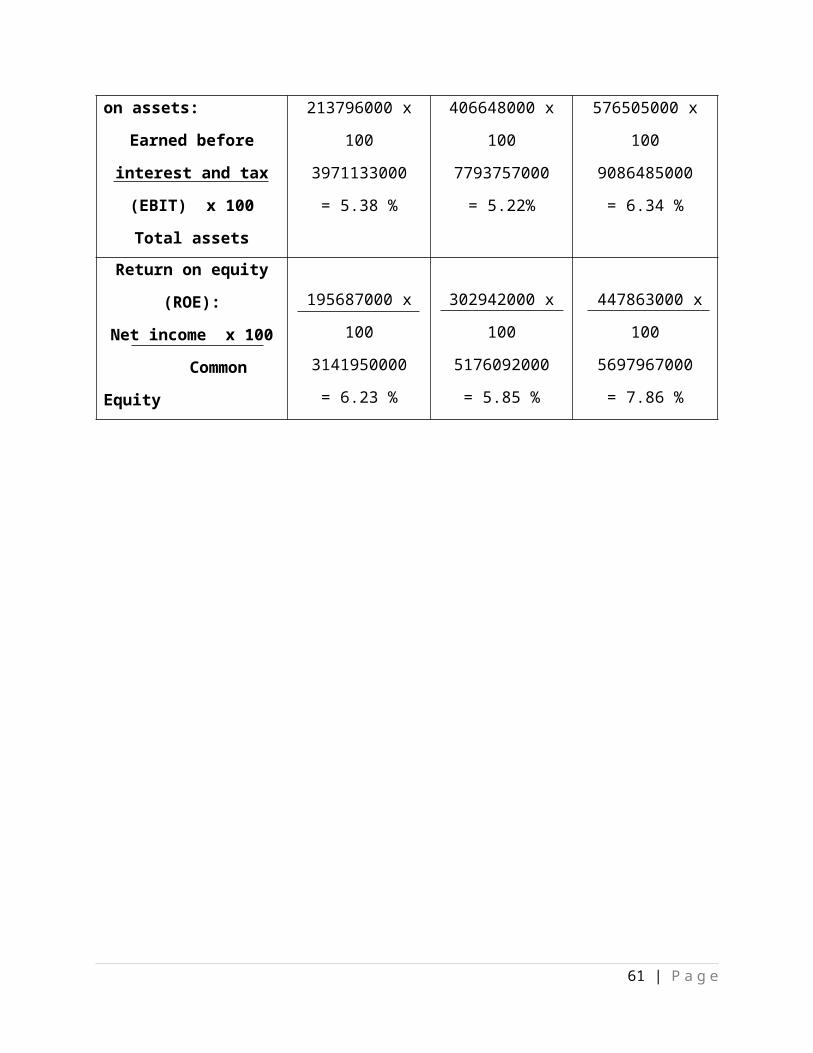

Operating Return on

assets:

Earned before interest

and tax (EBIT) x 100

Total assets

213796000 x 100

3971133000

= 5.38 %

406648000 x 100

7793757000

= 5.22%

576505000 x 100

9086485000

= 6.34 %

Return on equity (ROE):

Net income x 100

Common Equity

195687000 x 100

3141950000

= 6.23 %

302942000 x 100

5176092000

= 5.85 %

447863000 x 100

5697967000

= 7.86 %

46 | P a g e

Calculation

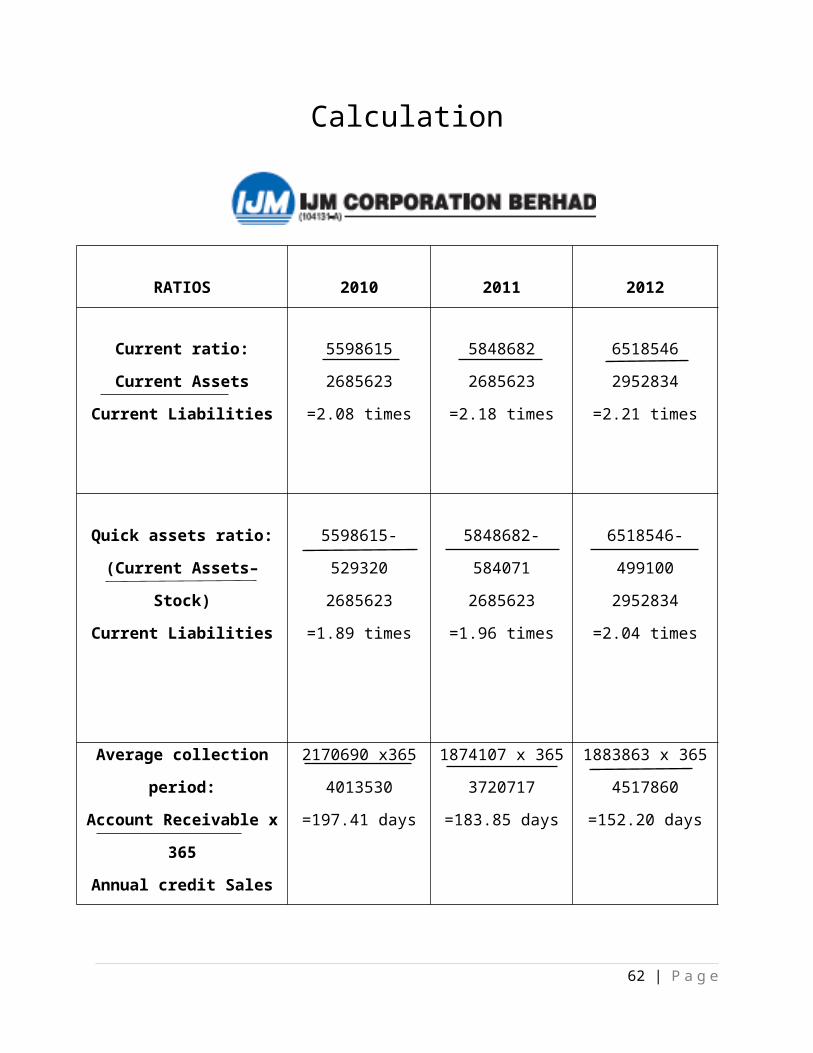

RATIOS 2010 2011 2012

Current ratio:

Current Assets

Current Liabilities

5598615

2685623

=2.08 times

5848682

2685623

=2.18 times

6518546

2952834

=2.21 times

Quick assets ratio:

(Current Assets–Stock)

Current Liabilities

5598615-529320

2685623

=1.89 times

5848682-584071

2685623

=1.96 times

6518546-499100

2952834

=2.04 times

Average collection period:

Account Receivable x 365

Annual credit Sales

2170690 x365

4013530

=197.41 days

1874107 x 365

3720717

=183.85 days

1883863 x 365

4517860

=152.20 days

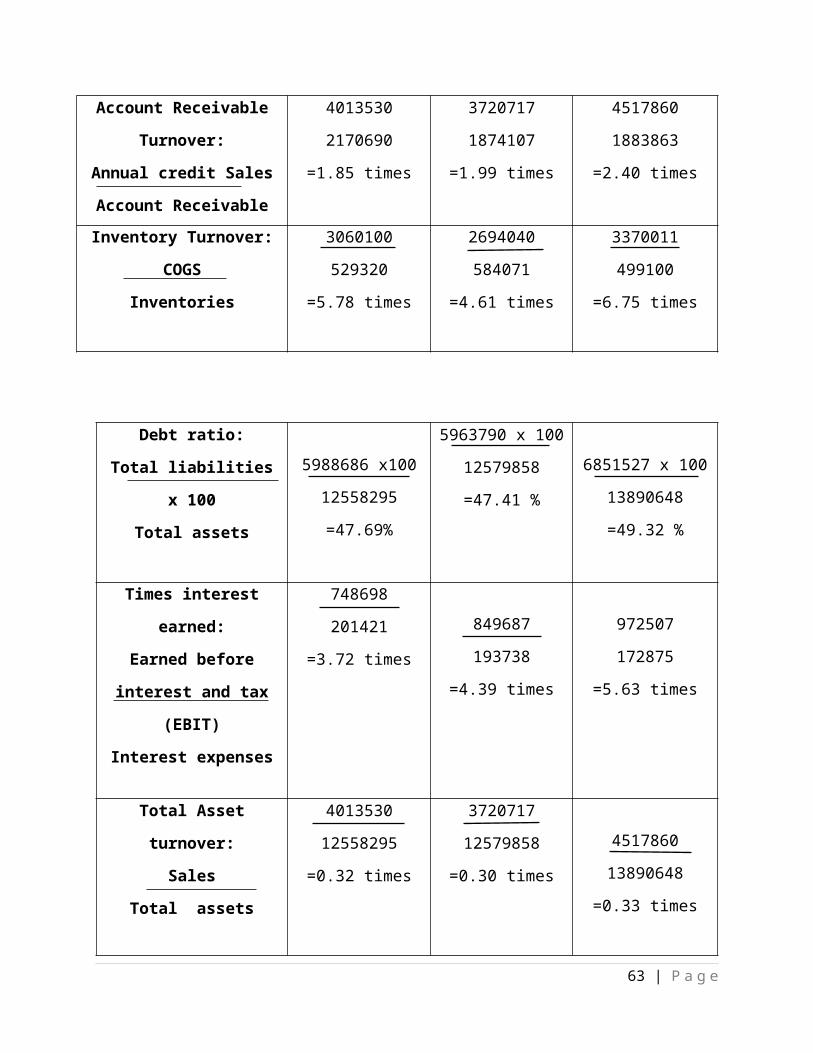

Account Receivable

Turnover:

Annual credit Sales

Account Receivable

4013530

2170690

=1.85 times

3720717

1874107

=1.99 times

4517860

1883863

=2.40 times

Inventory Turnover:

COGS

Inventories

3060100

529320

=5.78 times

2694040

584071

=4.61 times

3370011

499100

=6.75 times

47 | P a g e

Debt ratio:

Total liabilities x 100

Total assets

5988686 x100

12558295

=47.69%

5963790 x 100

12579858

=47.41 %

6851527 x 100

13890648

=49.32 %

Times interest earned:

Earned before interest

and tax (EBIT)

Interest expenses

748698

201421

=3.72 times

849687

193738

=4.39 times

972507

172875

=5.63 times

Total Asset turnover:

Sales

Total assets

4013530

12558295

=0.32 times

3720717

12579858

=0.30 times

4517860

13890648

=0.33 times

Fixed Asset turnover:

Sales

Total Fixed assets

4013530

6959680

=0.58 times

3720717

6731176

=0.55 times

4517860

7372102

=0.61 times

Gross profit margin:

Gross profit x 100

sales

953430 x 100

4013530

=23.76%

1026677 x 100

3720717

=27.59 %

1147849 x 100

4517860

=25.41 %

48 | P a g e

Operating profit margin:

Operating profit x 100

sales

748698 x 100

4013530

=18.65 %

849687 x 100

3720717

=22.84 %

972507 x 100

4517860

=21.53 %

Net profit margin:

Net profit x 100

Sales

423164 x 100

4013530

=10.54 %

479373 x 100

3720717

=12.88 %

550486 x 100

4517860

=12.19 %

Operating Return on

assets:

Earned before interest

and tax (EBIT) x 100

Total assets

748698 x 100

12558295

=5.95 %

849687 x 100

12579858

=6.75 %

972507 x 100

13890648

=7.00 %

Return on equity (ROE):

Net income x 100

CommonEquity

423164 x 100

6457359

=6.55 %

479373 x 100

6516907

=7.36 %

550486 x 100

6957698

=7.91 %

49 | P a g e

Calculation

CASH CONVERSION CYCLE

2010 2011 2012

Inventory Turnover

Ratio:

COGS

Inventory

259457000

422252000

= 6.14 times

1184516000

124494000

= 9.51 times

1232008000

122622000

= 10.05 times

Inventory

Conversion Period:

365

Inventory Turnover

Ratio

365

6.14

= 59.45 days

365

9.51

= 38.38days

365

10.05

= 36.32 days

Average Collection

Period:

Account Receivables

+Annual Credit Sales

456933000

471136000

365

= 354.00 days

1015836000

1703172000

365

= 217.70 days

1791635000

1939676000

365

50 | P a g e

YEAR

DETAIL

365 = 337.14 days

Operating Cycle:Inventory Conversion

Period

+

Average Collection

Period

59.45 + 354.00

= 413.45 days

38.38 + 217.70

= 256.08 days

36.32 + 373.14

= 373.46 days

Account Payable

Deferral Period:

365

COGS

Accounts Payables

365

259457000

155669000

= 218.99 days

365

1184516000

515787000

= 158.94 days

365

1232008000

712587000

= 211.11 days

Cash Conversion

Cycle:

Operating Cycle

-

Account Payable

Deferral Period

413.45 – 218.99

= 194.46 days

256.08 – 158.94

= 97.14 days

373.46 – 211.11

= 162.35 days

Calculation

CASH CONVERSION CYCLE

51 | P a g e

2010 2011 2012

Inventory Turnover Ratio:

COGSInventory

3060100000529320000

=5.78 times

2694040000584071000

=4.61 times

3370011000499100000

=6.75 times

Average CollectionPeriod:

Account Receivables+Annual Credit Sales

365

21706900004013530000

365

=197.41 days

18741070003720717000

365

=183.85 days

18838630004527860000

365

=152.20 days

Account Payable Deferral Period:

365COGS

Accounts Payables

36530601000001689300000

=201.49 days

36527297030001660175000

=222 days

36533700110001785685000

=193.40 days

Inventory Conversion Period:

365Inventory Turnover

Ratio

3655.78

=63.15 days

3654.67

=78.16 days

3656.75

=54.10 days

Operating Cycle:Inventory Conversion

Period+

63.15 + 197.41

=260.56 days

78.16 + 183.85

=262.01 days

54.10 + 152.20

=206.30 days

52 | P a g e

YEAR

DETAIL

Average Collection Period

Cash Conversion Cycle:

Operating Cycle-

Account Payable Deferral Period

260.56 – 201.49

=59.07 days

262.01 – 222

=40.01 days

206.30 – 193.40

=12.90 days

53 | P a g e

Annual Report UEM Land

54 | P a g e

55 | P a g e

56 | P a g e

57 | P a g e

58 | P a g e

59 | P a g e

Annual Report IJM Corp.

60 | P a g e

61 | P a g e

62 | P a g e

63 | P a g e

64 | P a g e