asset management industry sector presentation -...

TRANSCRIPT

Asset Management Industry

Sector Presentation

Mar 2015

Overview Regional IndustryGlobal Industry Domestic Industry

Outline

Global Dynamics

Regional Industry Dynamics | India

Domestic Industry

Overview Regional IndustryGlobal Industry Domestic Industry

Asset Management –

Global Trends

Overview Regional IndustryGlobal Industry Domestic Industry

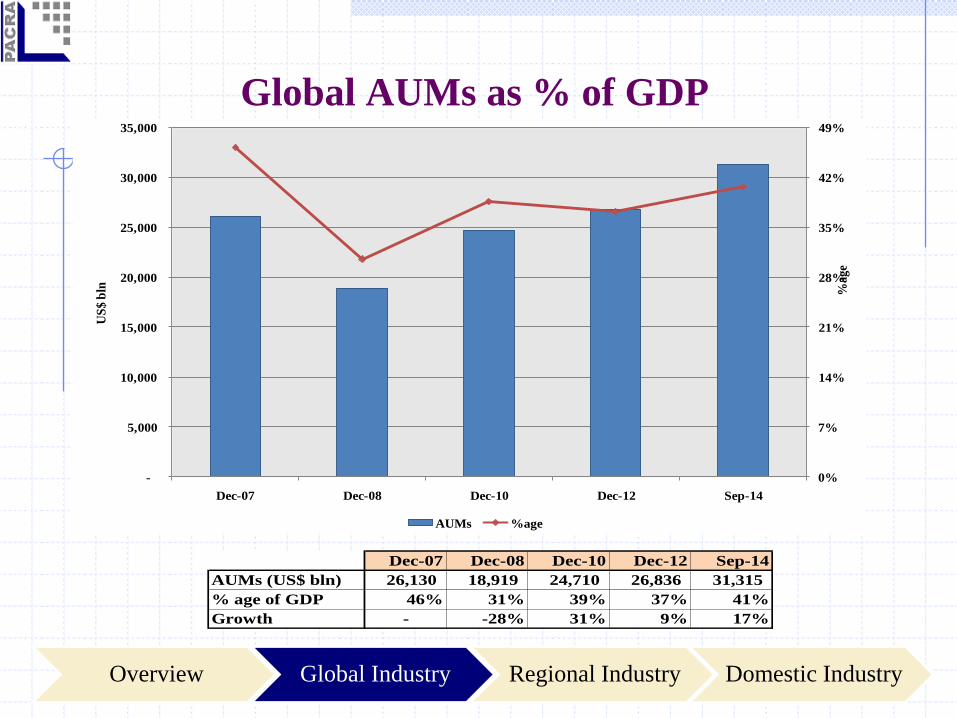

0%

7%

14%

21%

28%

35%

42%

49%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Dec-07 Dec-08 Dec-10 Dec-12 Sep-14

%age

US

$ b

lnGlobal AUMs as % of GDP

AUMs %age

Global AUMs as % of GDP

Overview Regional IndustryGlobal Industry Domestic Industry

Dec-07 Dec-08 Dec-10 Dec-12 Sep-14

AUMs (US$ bln) 26,130 18,919 24,710 26,836 31,315

% age of GDP 46% 31% 39% 37% 41%

Growth - -28% 31% 9% 17%

AUMs Regional Mix

56% 55% 56% 57%

33% 32% 31% 31%

11% 12% 12% 12%

0

7,000

14,000

21,000

28,000

35,000

Dec-08 Dec-10 Dec-12 Sep-14

0%

20%

40%

60%

80%

100%

US

$ b

ln

%a

ge

AUMs -Regional Mix

Americas Europe Asia and Pacific Africa AUMs

Overview Regional IndustryGlobal Industry Domestic Industry

33%

15%16%

36%

Europe

Luxembourg France Ireland Others

Country Wise AUM Split –Sep 14

57%31%

12%0%

The World

Americas Europe Asia and Pacific Africa

87%

6%6%1%

Americas

USA Brazil Canada Others

US$ 17.8tln

US$ 31.3tln

US$ 9.7tln

US$ 3.6tln US$ 0.14tln

Overview Regional IndustryGlobal Industry Domestic Industry

19%

5%

31%

5%

20%

5%

18%

4%

14%

4%

16%

20%

18%

18%

22%

18%

26%

18%

24%

20%

47%

41%

34%

41%

42%

40%

40%

38%

44%

37%

17%

34%

17%

36%

16%

37%

16%

40%

18%

40%

0%

20%

40%

60%

80%

100%

Split No. Split No. Split No. Split No. Split No.

Dec-07 Dec-08 Dec-10 Dec-12 Sep-14

Money Market Income Equity Others AUMs

Categories & Number of Funds

Overview Regional IndustryGlobal Industry Domestic Industry

14% 15% 12% 12% 15%

24% 24% 29%

10% 3%

44%48%

37%

45%

24%

18% 12%22%

32%

58%

0%

20%

40%

60%

80%

100%

World Americas Europe Asia & Pacific Africa

Regional Categorical Split

Money Market Income Equity Others

Regional Category Wise Split –Sep14

Overview Regional IndustryGlobal Industry Domestic Industry

Best & Worst Capital Markets -2014

Overview Regional IndustryGlobal Industry Domestic Industry

Rank CountryBest

Returns

1 Argentina 55%

2 China 43%

3 India 30%

4 Pakistan 26%

5 Turkey 25%

Rank CountryWorst

Returns

1 Russia -45%

2 Greece -27%

3 Nigeria -21%

4 Portugal -19%

5 Kuwait -14%

Rank Name Region CY13 CY14 Change1 BlackRock U.S. 4.32 4.65 8%

2 Vanguard Group U.S. 2.75 3.00 9%

3 State Street Global U.S. 2.34 2.40 2%

4 Allianz Group Germany 2.39 1.91 -20%

5 Prudential Financial U.S. 1.11 1.76 59%

6 AXA Group France 1.53 1.75 14%

7 Fidelity Investments U.S. 1.71 1.74 2%

8 J.P. Morgan Chase U.S. 1.60 1.70 6%

9 Bank of New York Mellon U.S. 1.58 1.70 7%

10 BNP Paribas France 1.33 1.52 15%

World’s Largest Asset Managers

figures in US$ tln

*the AUMs of top10 AMC comprise ~70% of global AUMs

Overview Regional IndustryGlobal Industry Domestic Industry

Overview Regional IndustryGlobal Industry Domestic Industry

India –Asset Management Industry

AUMs v/s Deposits

Overview Regional IndustryGlobal Industry Domestic Industry

Figures in US$ bln^ Mar-08 Mar-10 Mar-12 Mar-14 Dec-14

GDP 782 1,016 1,414 1,782 *1,856

Deposits 521 745 1,013 1,339 1,298

AUMs 79 96 92 129 165

^Exchange rate as published on oanda.com for 31-Dec-2014 (US$ 1 = INR 0.01569)

*Based on World Bank's forecast of 2014

Overview Regional IndustryGlobal Industry Domestic Industry

Categories & Number of Funds

18%

6%13%

6%14%

4%

16%

3%

17%

3%

44%

56%

51%

46%

50%62%

56%

68%48%

70%

31% 28%28%

35%

27% 23%20% 19%

27%19%

7% 10% 8%13% 9% 10% 7% 9% 7% 8%

0%

20%

40%

60%

80%

100%

Split No. Split No. Split No. Split No. Split No.

Mar-08 Mar-10 Mar-12 Mar-14 Dec-14

Money Market Income Equity Others

Mar-07 Mar-08 Mar-10 Mar-14 Dec-14

AUMs (US$ bln)^ 79 96 92 129 165

No. of Funds 15 14 21 26 29

^Exchange rate as published on oanda.com for 31-Dec-2014 (US$ 1 = INR 0.01569)

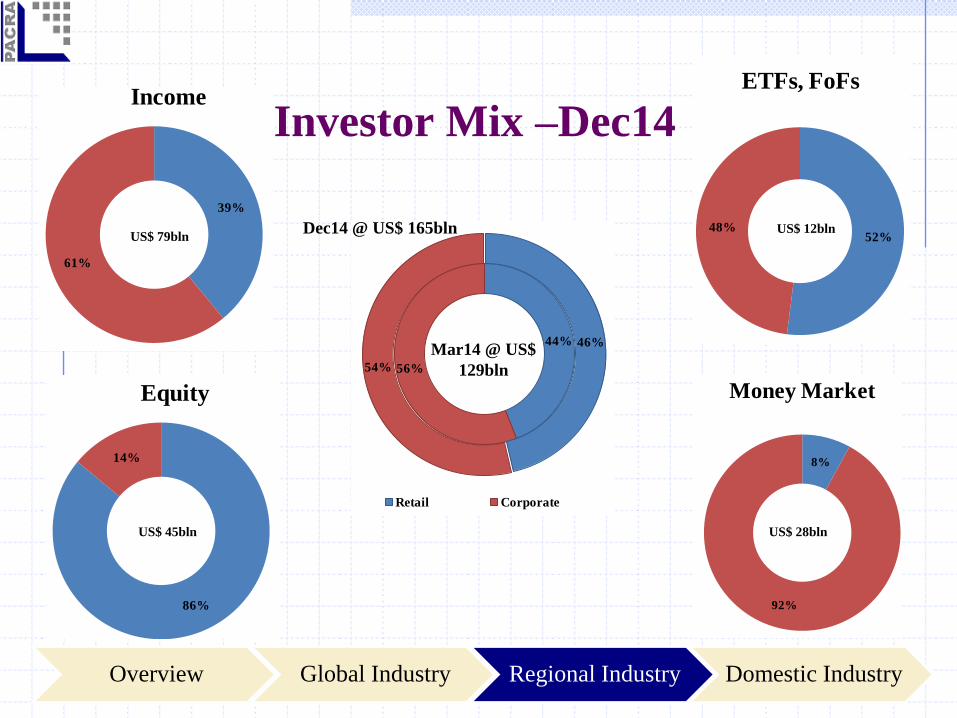

Investor Mix –Dec14

44%

56%

46%

54%

Retail Corporate

Mar14 @ US$

129bln

Dec14 @ US$ 165bln

86%

14%

Equity

52%48%

ETFs, FoFs

8%

92%

Money Market

39%

61%

Income

Overview Regional IndustryGlobal Industry Domestic Industry

US$ 79bln

US$ 45bln US$ 28bln

US$ 12bln

Largest Indian Asset Managers

Overview Regional IndustryGlobal Industry Domestic Industry

*As of Dec14, there are 45 AMCs functioning in India

AUMs Mkt. sh AUMs Mkt. sh AUMs Mkt. sh1 HDFC Mutual Fund 16 12% 18 12% 24 14%

2 ICICI Prudential Mutual Fund 14 11% 17 12% 21 12%

3 Reliance Mutual Fund 15 12% 17 12% 20 11%

4 Birla Sun Life Mutual Fund 12 9% 14 10% 17 10%

5 UTI Mutual Fund 11 8% 12 8% 14 8%

6 SBI Mutual Fund 9 7% 10 7% 11 7%

7 Franklin Templeton Mutual Fund 7 5% 7 5% 10 6%

8 IDFC Mutual Fund 5 4% 7 5% 8 4%

9 Kotak Mahindra Mutual Fund 6 4% 5 4% 6 4%

10 DSP BlackRock Mutual Fund 5 4% 5 4% 6 3%

Others 30 23% 32 22% 37 21%

Total (US$bln) 129 143 175

S/No. AMCMar-13 Mar-14 Dec-14

Overview Regional IndustryGlobal Industry Domestic Industry

Pakistan –Asset Management Industry

Overview Regional IndustryGlobal Industry Domestic Industry

Figures in PKR bln Jun-08 Jun-10 Jun-12 Jun-14 Dec-14

GDP 9,922 13,844 20,047 25,402 *26,088

Deposits 3,832 4,661 6,403 8,082 8,342

AUMs 341 234 409 428 471

*Based on the World Bank's forecast for 2014

3%2% 2% 2% 2%

39%

34%32% 32% 32%

0%

10%

20%

30%

40%

50%

-

100

200

300

400

500

Jun-08 Jun-10 Jun-12 Jun-14 Dec-14

%a

ge

PK

R b

ln

AUMs AUMs as % of GDP Deposits as % of GDP

AUMs v/s Deposits

Regulatory Environment

Overview Regional IndustryGlobal Industry Domestic Industry

FY14 FY15 FY14 FY15 FY14 FY15 FY14 FY15

Banks 35.0% 35.0% 35.0% 35.0% 12.5% 12.5% 12.5% 12.5%

Corporates 10.0% 12.5% 8.0% 12.5% - 10.0% - -

Individuals 10.0% 12.5% 8.0% 12.5% - 10.0% - -

Capital Gain Tax on Money Market & Income Funds

Investor0-6 months 6-12 months 1-2 years 2 years +

FY14 FY15 FY14 FY15

Banks 25% 25% 10% 10%

Corporates 10% 25% 10% 10% - 12.5%

Individuals 10% 10% 10% 10% - 12.5%

StockInvestor

Tax on Cash Dividend

Money Market &

Income

Asset Management Services PKR 200mln

Advisory Services PKR 30mln

Minimum Capital Requirement

Category Wise Split

Overview Regional IndustryGlobal Industry Domestic Industry

36%

19%

34%

19%

28%

19%

28%

19%25%

19%

13%

22%

13%

21%

15%

21%

15%

22%15%

21%

34%

26%

35%

26%

36%

25%

36%

24%

37%

23%

1%

5%

3%

5%

4%

5%

4%

5%

5%

5%

8%

6%

9%

7%

10%

7%

9%

8%

11%

10%

7%

24%

6%

23%

7%

24%

8%

22%

7%

22%

0%

20%

40%

60%

80%

100%

Split No. Split No. Split No. Split No. Split No.

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

Money Market Income Equity Capital Protected Government Bond Others

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

AUMs (PKR bln) 413 448 428 437 471

No. of Funds 195 200 203 209 215

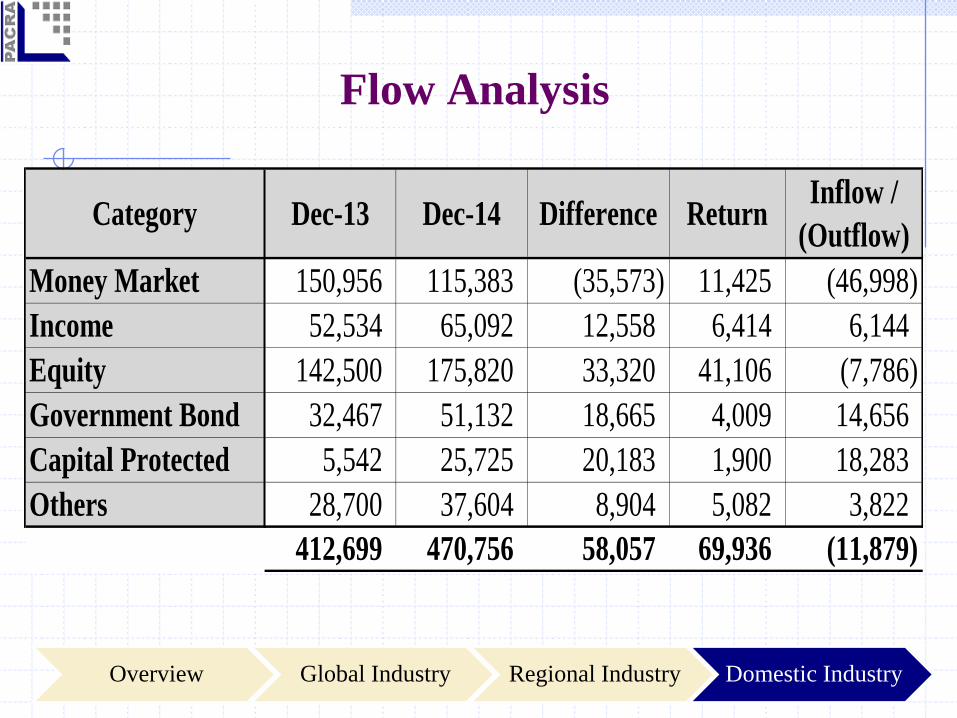

Flow Analysis

Overview Regional IndustryGlobal Industry Domestic Industry

Money Market 150,956 115,383 (35,573) 11,425 (46,998)

Income 52,534 65,092 12,558 6,414 6,144

Equity 142,500 175,820 33,320 41,106 (7,786)

Government Bond 32,467 51,132 18,665 4,009 14,656

Capital Protected 5,542 25,725 20,183 1,900 18,283

Others 28,700 37,604 8,904 5,082 3,822

412,699 470,756 58,057 69,936 (11,879)

Category Dec-13 Dec-14 Difference ReturnInflow /

(Outflow)

*As of Jan15, there are 23 AMCs functioning in Pakistan. The top 10 AMCs represent ~86% of

the total domestic AUMs.

Overview Regional IndustryGlobal Industry Domestic Industry

Total Mkt.sh

1 NIT 99 20%

2 Meezan 66 13%

3 UBL 60 12%

4 NAFA 53 11%

5 MCB-AH 48 9%

6 Allied 32 6%

7 PICIC 28 6%

8 HBL 20 4%

9 Atlas 17 3%

10 JS 11 2%

Others 69 14%

Total 505

Jan-15AMCS/No.

Pakistan’s Largest Asset Managers

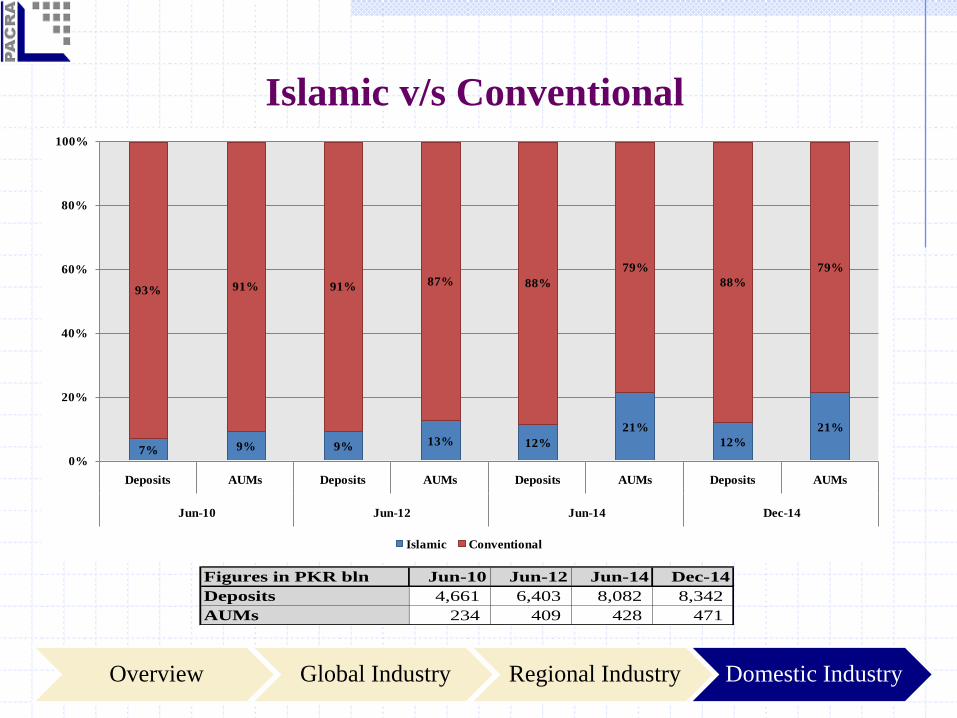

Islamic v/s Conventional

Overview Regional IndustryGlobal Industry Domestic Industry

7% 9% 9% 13% 12%

21%

12%

21%

93% 91% 91% 87% 88%

79%

88%

79%

0%

20%

40%

60%

80%

100%

Deposits AUMs Deposits AUMs Deposits AUMs Deposits AUMs

Jun-10 Jun-12 Jun-14 Dec-14

Islamic Conventional

Figures in PKR bln Jun-10 Jun-12 Jun-14 Dec-14

Deposits 4,661 6,403 8,082 8,342

AUMs 234 409 428 471

Separately Managed Accounts

Overview Regional IndustryGlobal Industry Domestic Industry

No. of Accounts Jun-11 Jun-12 Jun-13 Jun-14 Dec-14

Discretionary Portfolios 104 136 248 492 28

Non Discretionary Portfolios 19 21 28 26 539

123 157 276 518 567

10,793 14,255

23,267

35,857

44,048 24,199

30,148

33,217

36,258

37,781

-

17,000

34,000

51,000

68,000

85,000

Jun-11 Jun-12 Jun-13 Jun-14 Dec-14

PK

R m

ln

Discretionary Portfolios Non Discretionary Portfolios

Key Findings

Domestic AMC market comparative size reflecting gap with global and

regional markets.

AUMs concentrated with few large AMCs in line with the global and regional

trends.

Investors preference towards Fixed Income Funds as compared to equity funds

in contrast to the global trend.

Investor facilitation and technological advancement lacks quality in

comparison to banking sector resulting in reduced retail penetration.

Transition of AUMs towards longer duration funds from Money Market

Funds.

Islamic Funds & Separately Managed Accounts gaining momentum

Innovative products help in increasing AUM base.

Overview Regional IndustryGlobal Industry Domestic Industry

Bibliography

1. http://www.pionline.com

2. http://www.efama.org

3. http://www.ici.org

4. http://www.ipe.com

5. http://www.ey.com/

6. http://www.pwc.com/

7. https://www.deloitte.com

8. http://www.kpmg.com

9. http://money.cnn.com/interactive/investing/best-performing-global-markets/

10. https://www.amfiindia.com/

11. http://www.mufap.com.pk/

12. http://www.rbi.org.in

13. http://www.imf.org/

14. http://secp.gov.pk/

15. http://www.li.com.pk/

16. http://www.sbp.org.pk/

17. http://www.towerswatson.com/

18. http://www.worldbank.org/

DISCLAIMERPACRA has used due care in preparation of this document. Our information has been obtained

from sources we consider to be reliable but its accuracy or completeness is not guaranteed.

The information in this document may be copied or otherwise reproduced, in whole or in part,

provided the source is duly acknowledged. The presentation should not be relied upon as

professional advice.

Analysts Rai Umar Zafar

Manager Ratings

+92 42 3586 9504

Suffiyan Saleem

Senior Financial Analyst

+92 42 3586 9504

Saad Khan

Associate Analyst

+92 42 3586 9504