assessment of participating banks microfinance performance based on mabs - eagle standards 2009...

TRANSCRIPT

Assessment of Participating Banks Microfinance Performance based on MABS - EAGLE Standards

2009 RBAP-MABS National Roundtable ConferenceMay 12-13, 2009

Hyatt Hotel and CasinoManila

Eulogio Martin O. MasilunganMonitoring & Research CoordinatorMABS

“What gets measured gets done.”

“What can’t be measured can’t be managed.”

Managing for Success

THE MABS-EAGLE Assessment

• The EAGLE assessment evaluates the performance of microfinance portfolio

• A management tool for monitoring and evaluating factors affecting a rural bank’s microfinance operations

• Has 5 performance areas with 13 indicators

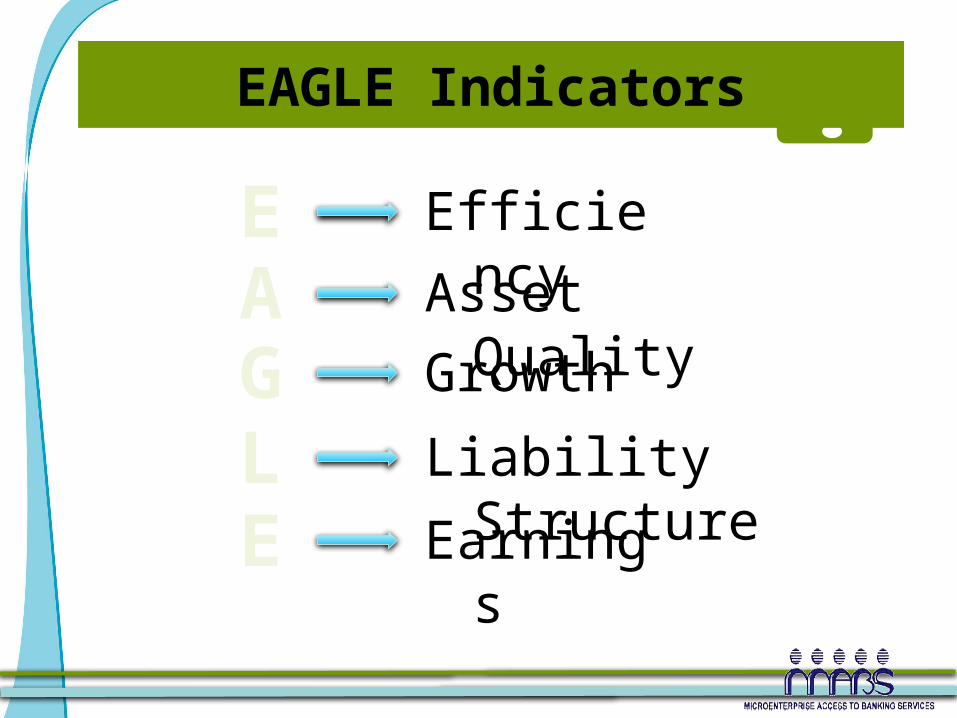

EAGLE Indicators

Efficiency

EAsset

QualityA

GrowthGLiability

StructureL

EarningsE

EAGLE Indicators

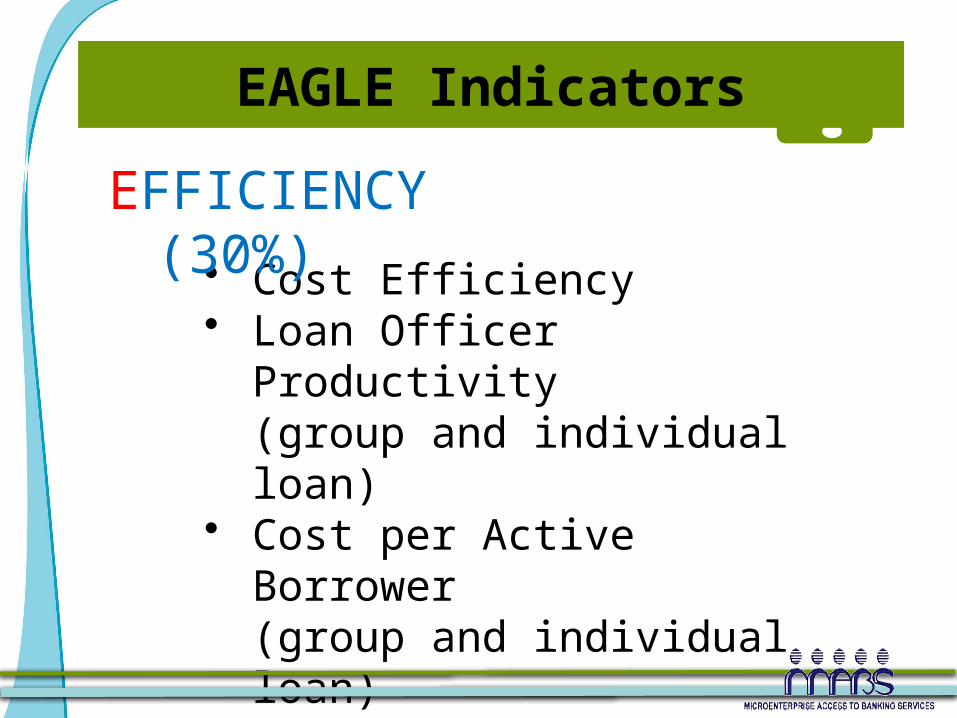

• Cost Efficiency• Loan Officer Productivity

(group and individual loan)

• Cost per Active Borrower(group and individual loan)

EFFICIENCY (30%)

EAGLE Indicators

• PAR Over 7 Days• PAR Over 30 Days• Loan Loss Provision• Loan Loss Rate

ASSET QUALITY (30%)

EAGLE Indicators

• Growth in Active Borrowers

• Growth in Loan Portfolio

GROWTH IN PORTFOLIO (10%)

LIABILITY STRUCTURE (10%)

• Deposit to Loan RatioEARNINGS (20%)

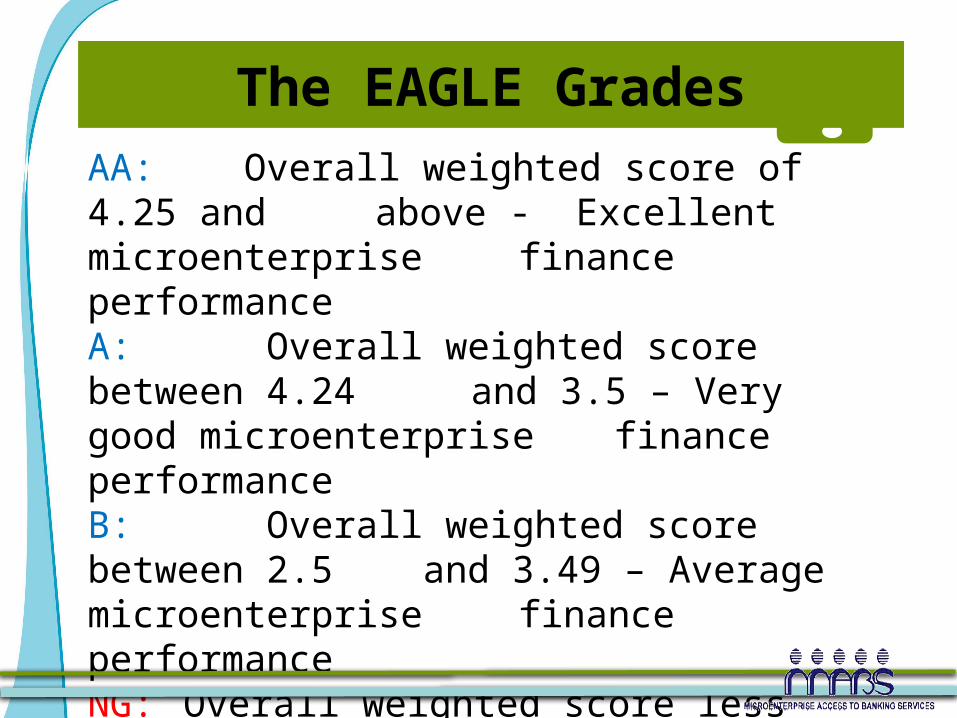

The EAGLE GradesAA: Overall weighted score of 4.25 and

above - Excellent microenterprise finance performanceA: Overall weighted score between 4.24

and 3.5 – Very good microenterprise finance performance

B: Overall weighted score between 2.5 and 3.49 – Average microenterprise finance performance

NG: Overall weighted score less than 2.49 – Below average performance

So, how did banks score for the period January to December 2008?

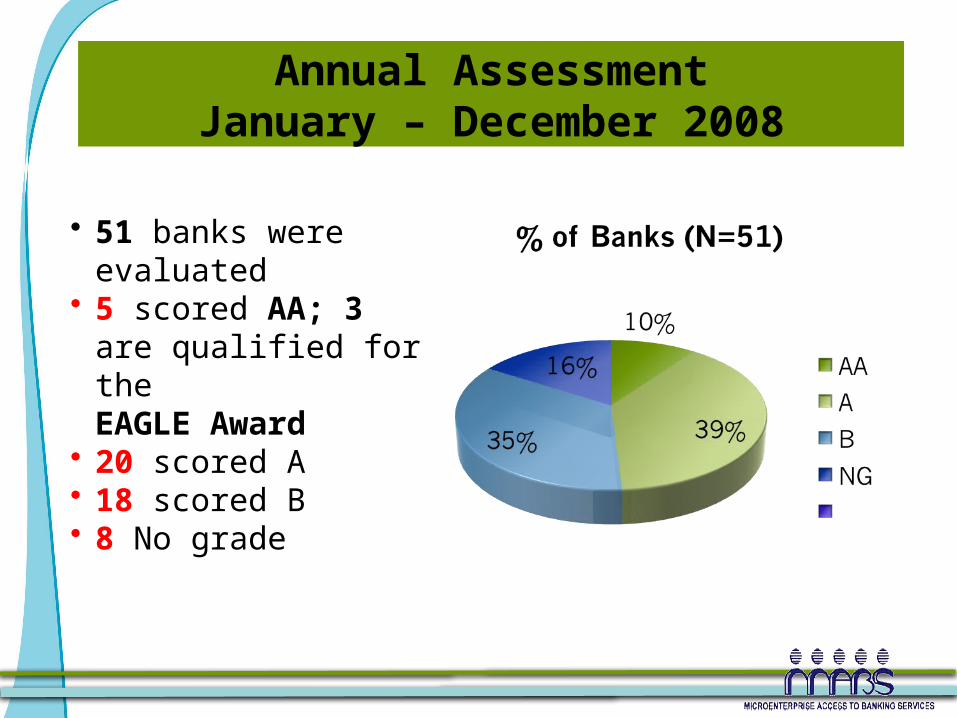

Annual AssessmentJanuary – December 2008

• 51 banks were evaluated

• 5 scored AA; 3 are qualified for the EAGLE Award

• 20 scored A• 18 scored B• 8 No grade

Measuring EFFICIENCY

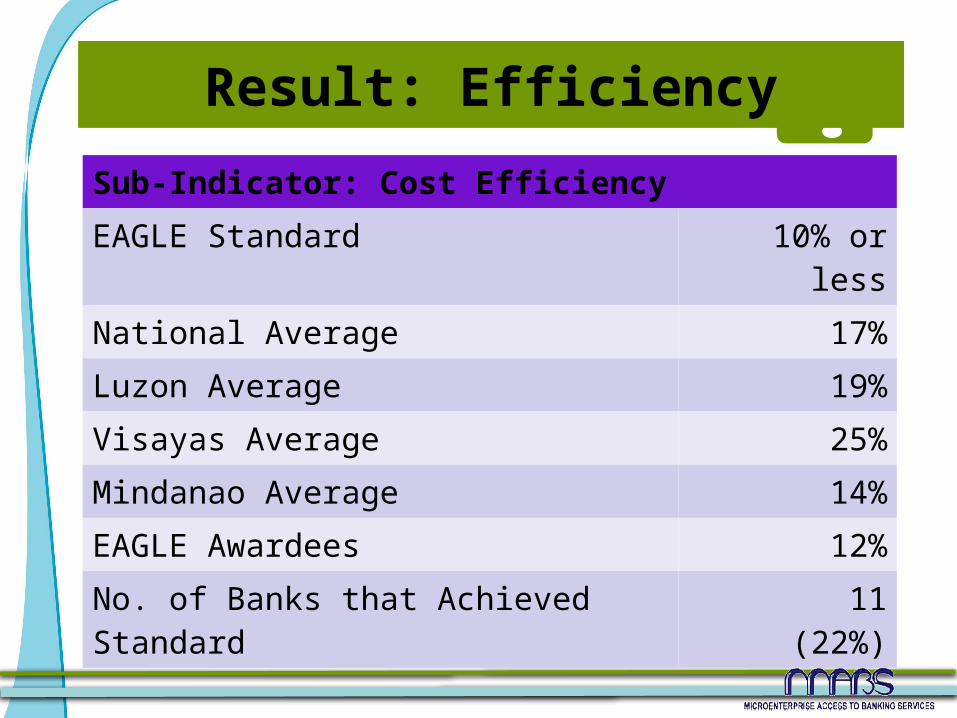

Result: Efficiency

Sub-Indicator: Cost Efficiency

EAGLE Standard 10% or less

National Average 17%

Luzon Average 19%

Visayas Average 25%

Mindanao Average 14%

EAGLE Awardees 12%

No. of Banks that Achieved Standard

11(22%)

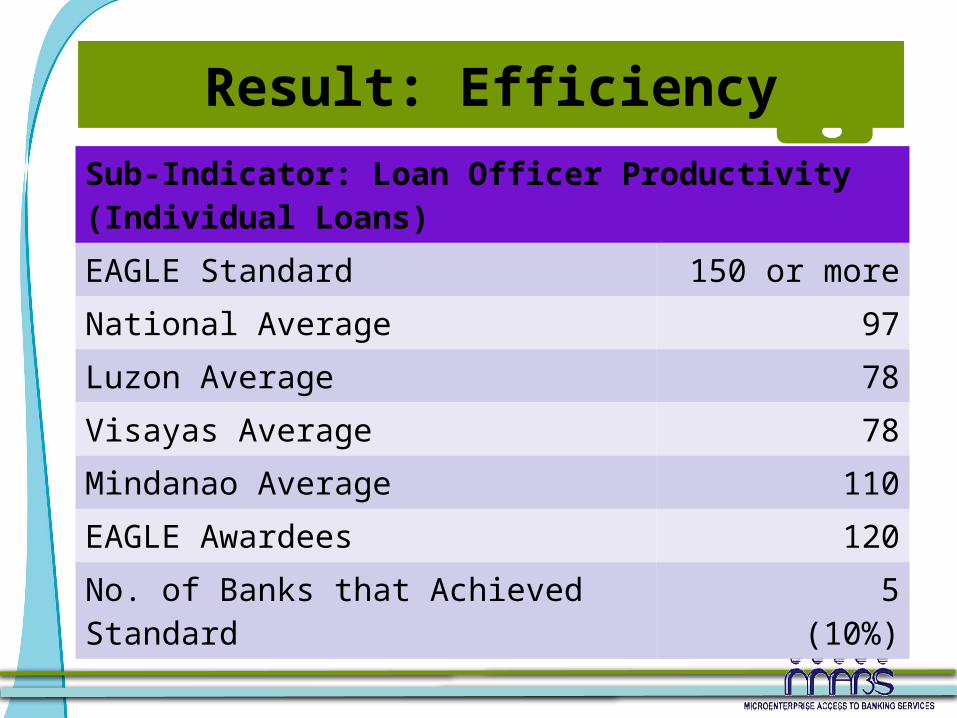

Result: EfficiencySub-Indicator: Loan Officer Productivity (Individual Loans)

EAGLE Standard 150 or more

National Average 97

Luzon Average 78

Visayas Average 78

Mindanao Average 110

EAGLE Awardees 120

No. of Banks that Achieved Standard

5(10%)

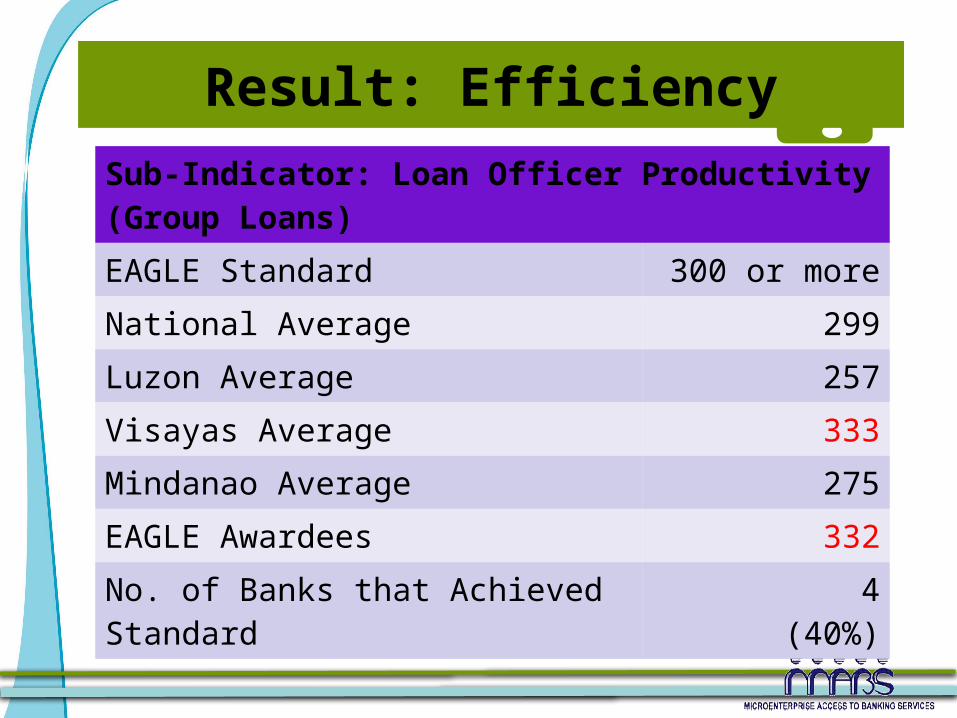

Result: EfficiencySub-Indicator: Loan Officer Productivity (Group Loans)

EAGLE Standard 300 or more

National Average 299

Luzon Average 257

Visayas Average 333

Mindanao Average 275

EAGLE Awardees 332

No. of Banks that Achieved Standard

4(40%)

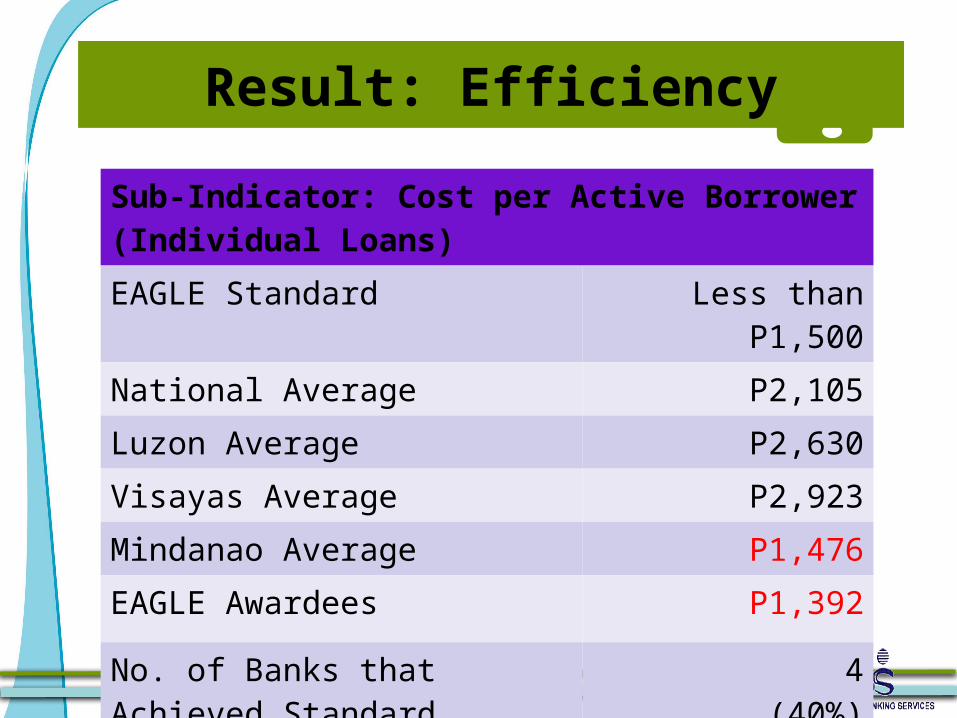

Result: Efficiency

Sub-Indicator: Cost per Active Borrower (Individual Loans)

EAGLE Standard Less than P1,500

National Average P2,105

Luzon Average P2,630

Visayas Average P2,923

Mindanao Average P1,476

EAGLE Awardees P1,392

No. of Banks that Achieved Standard

4(40%)

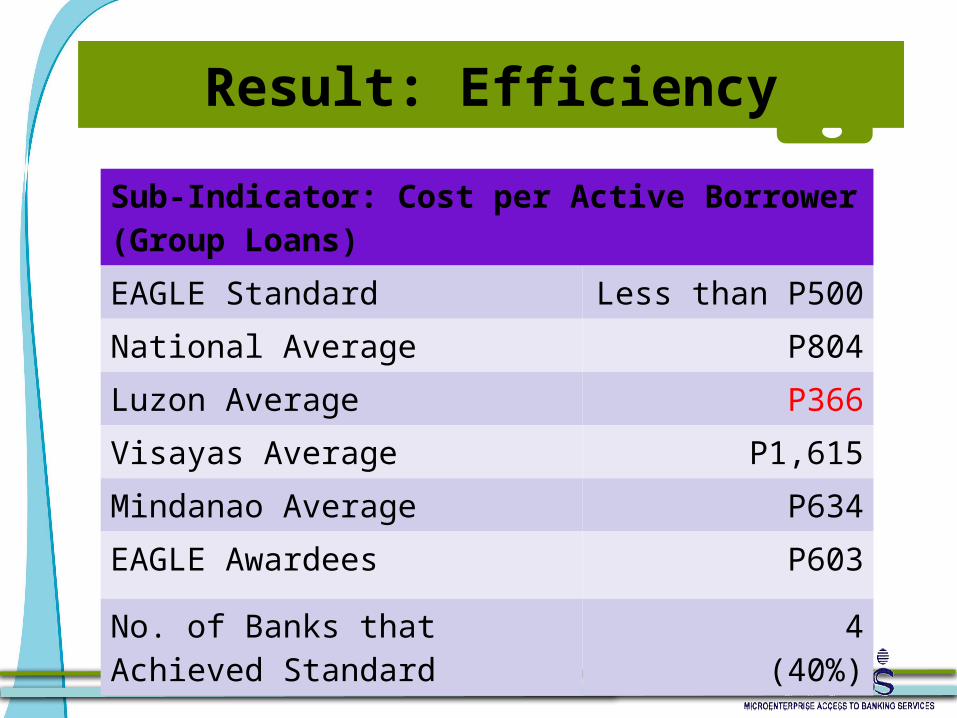

Result: Efficiency

Sub-Indicator: Cost per Active Borrower (Group Loans)

EAGLE Standard Less than P500

National Average P804

Luzon Average P366

Visayas Average P1,615

Mindanao Average P634

EAGLE Awardees P603

No. of Banks that Achieved Standard

4(40%)

MeasuringASSET QUALITY

Result: Asset Quality

Sub-Indicator: PARR > 7 days

EAGLE Standard 5% or less

National Average 10%

Luzon Average 9%

Visayas Average 21%

Mindanao Average 9%

EAGLE Awardees 3%

No. of Banks that Achieved Standard

22(43%)

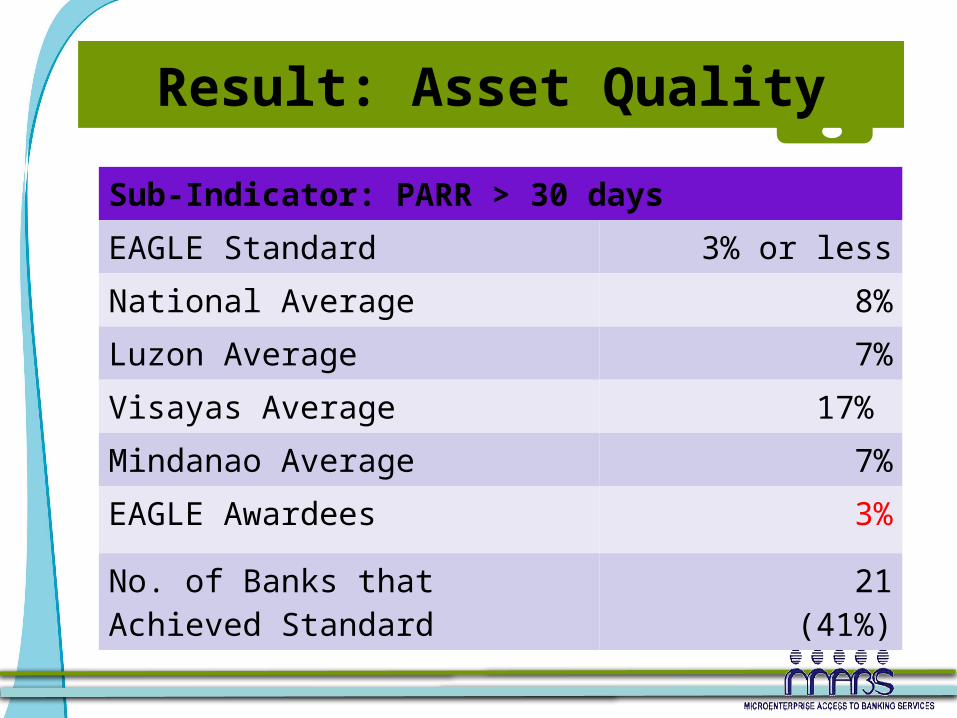

Result: Asset Quality

Sub-Indicator: PARR > 30 days

EAGLE Standard 3% or less

National Average 8%

Luzon Average 7%

Visayas Average 17%

Mindanao Average 7%

EAGLE Awardees 3%

No. of Banks that Achieved Standard

21(41%)

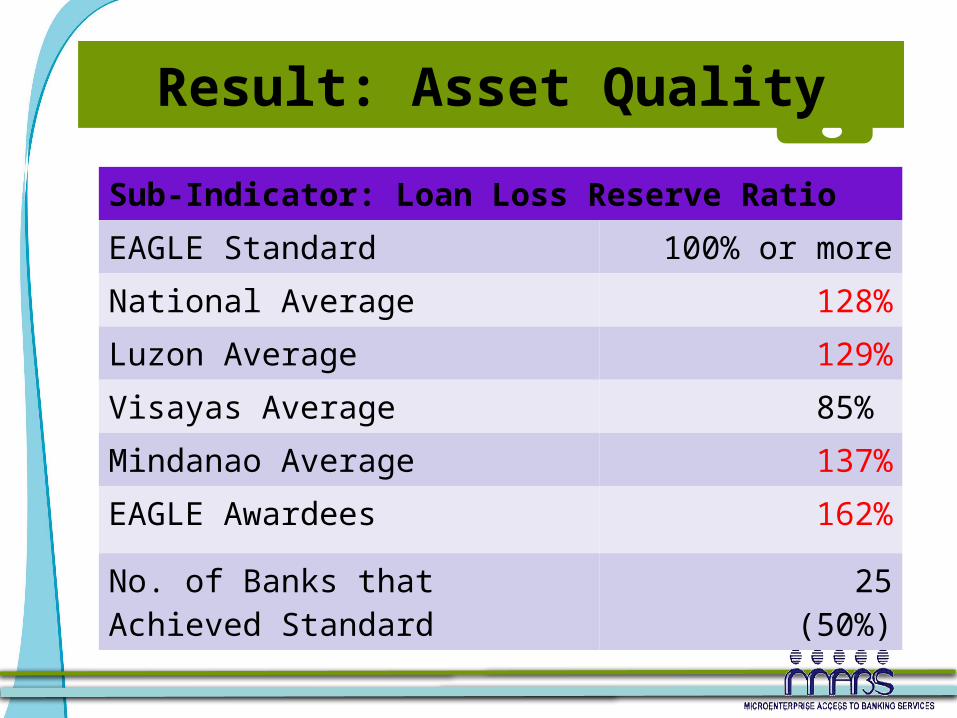

Result: Asset Quality

Sub-Indicator: Loan Loss Reserve Ratio

EAGLE Standard 100% or more

National Average 128%

Luzon Average 129%

Visayas Average 85%

Mindanao Average 137%

EAGLE Awardees 162%

No. of Banks that Achieved Standard

25(50%)

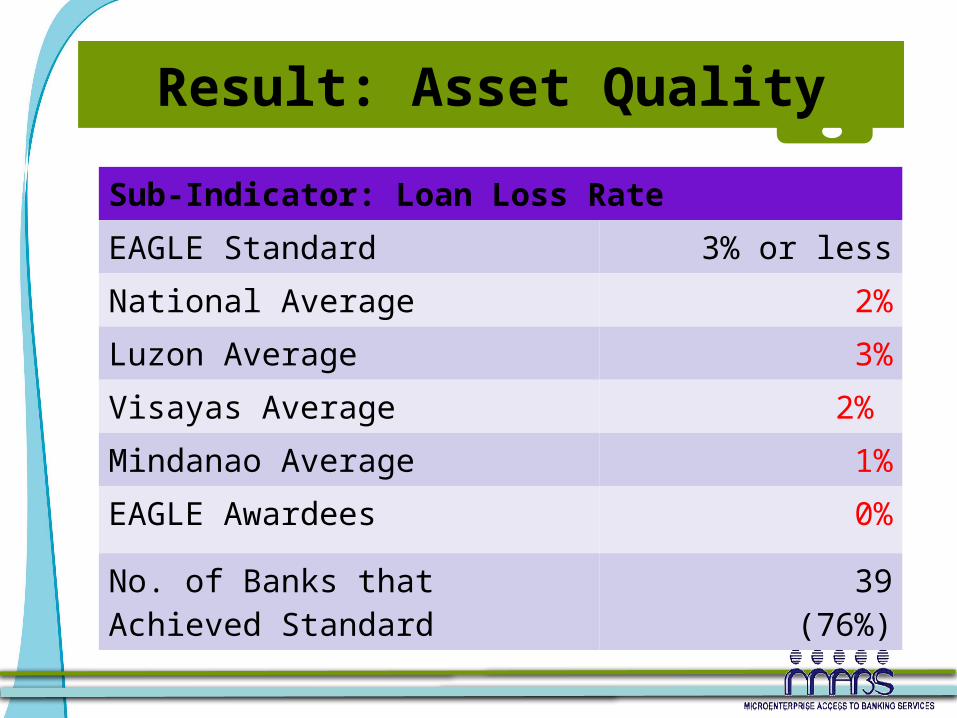

Result: Asset Quality

Sub-Indicator: Loan Loss Rate

EAGLE Standard 3% or less

National Average 2%

Luzon Average 3%

Visayas Average 2%

Mindanao Average 1%

EAGLE Awardees 0%

No. of Banks that Achieved Standard

39(76%)

MeasuringGROWTH

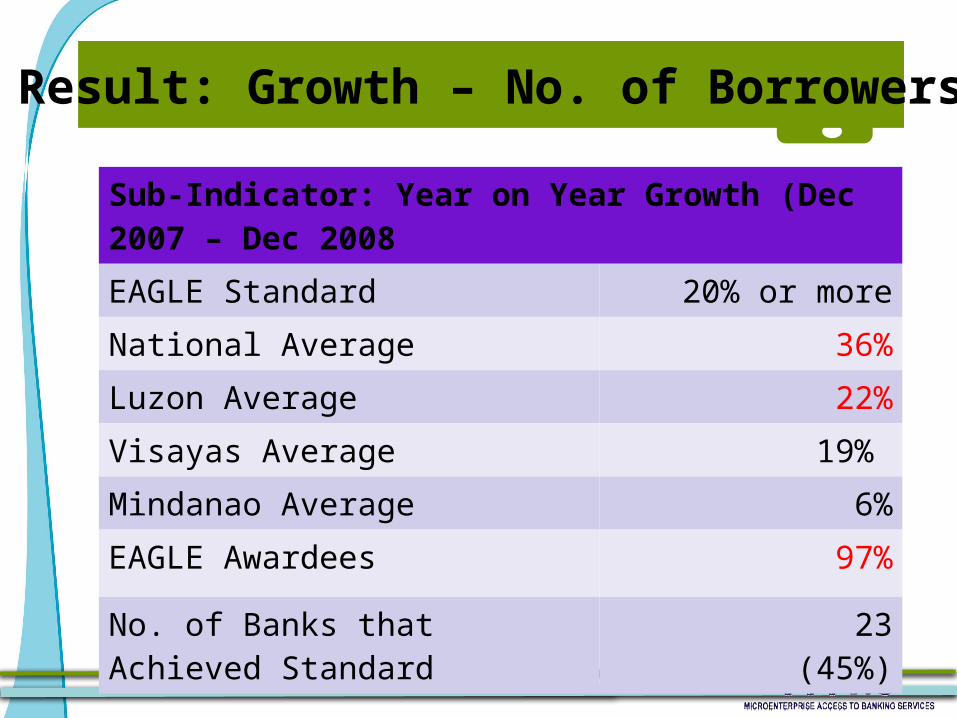

Result: Growth – No. of Borrowers

Sub-Indicator: Year on Year Growth (Dec 2007 – Dec 2008

EAGLE Standard 20% or more

National Average 36%

Luzon Average 22%

Visayas Average 19%

Mindanao Average 6%

EAGLE Awardees 97%

No. of Banks that Achieved Standard

23(45%)

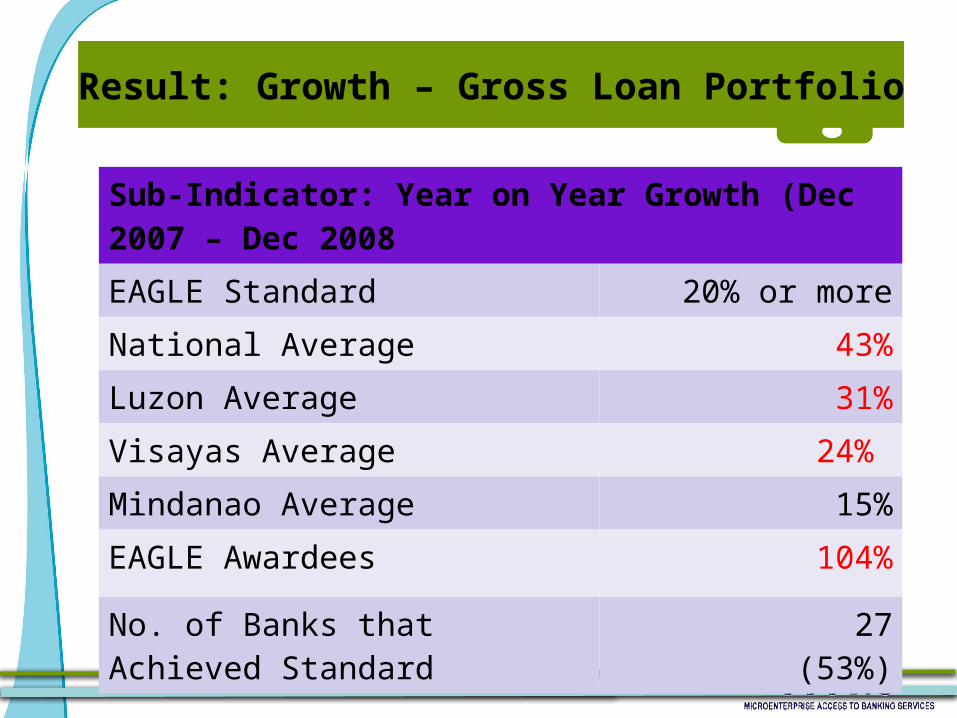

Result: Growth – Gross Loan Portfolio

Sub-Indicator: Year on Year Growth (Dec 2007 – Dec 2008

EAGLE Standard 20% or more

National Average 43%

Luzon Average 31%

Visayas Average 24%

Mindanao Average 15%

EAGLE Awardees 104%

No. of Banks that Achieved Standard

27(53%)

MeasuringLIABILITY

STRUCTURE

Result: Deposit to Loan Ratio

Sub-Indicator: Deposit to Loan Ratio

EAGLE Standard 100% or more

National Average 101%

Luzon Average 122%

Visayas Average 111%

Mindanao Average 83%

EAGLE Awardees 88%

No. of Banks that Achieved Standard

20(40%)

MeasuringEARNINGS

Result: Earnings

Sub-Indicator: Earnings

EAGLE Standard 35% or more

National Average 38%

Luzon Average 36%

Visayas Average 19%

Mindanao Average 41%

EAGLE Awardees 55%

No. of Banks that Achieved Standard

32(63%)

BEST PRACTICES

• Allot a day a week for promotional activities such as barangay visits, distribution of flyers and community events

• Ask AOs to work on Saturdays if there are PAR problems and low intake of new clients

• Ask AOs to prepare weekly prospects list

• Niche marketing – TODA members

Best Practices

AREAS FOR IMPROVEMENT

• Non-functioning MIS resulted in non monitoring of PAR status

• Loan Supervisors are not given authority to address delinquency issues (no delegation of authority)

• Inflexible products (fixes loan amount, terms, etc.)

• Poor customer service (long waiting lines, not enough chairs, unfriendly staff)

Areas for Improvement

• No incentives for MF borrowers who maintain high savings balance (e.g., lower interest rate, better payment terms, etc.)

Areas for Improvement

Continue

Doing Well by Doing Good

and

See You All at the

MABS EAGLE Awards

tonight!