assessing 30 listed belgian companies 2015transparencybelgium.be › images › slides ›...

TRANSCRIPT

1

ASSESSING 30 LISTED BELGIAN COMPANIES 2015

2

Responsible publisher: Transparency International Belgium VZW-ASBL, Nijverheidsstraat

10 rue de l‘Industrie, 1000 Brussels, Belgium. Date of publication: 18 December 2015,

www.transparencybelgium.be

Transparency International is the global civil society organization leading the fight against

corruption. Through more than 100 chapters worldwide and an international secretariat

in Berlin, Transparency International raises awareness of the damaging effects of corrup-

tion and works with partners in government, business and civil society to develop and im-

plement effective measures to tackle it.

Every effort has been made to verify the accuracy of the information contained in this re-

port. All information was believed to be correct at the date of our review (1-15 October

2015). Nevertheless, Transparency International cannot accept responsibility for the con-

sequences of its use for other purposes or in other contexts.

We would like to thank all individuals who contributed to the research, the review or the

drafting of the report: Karel Boone, Michael Clarke, Evert-Jan Lammers, Mathieu Maes,

Anja Siebel and David Szafran (for Transparency International Belgium) and Sophie

Delcoigne, Sarah Deom, Aloïs Moreau, Martin Tombal, Léopold Van Oost and Rafaël

Vansteenberghe (for Louvain School of Management).

3

CONTENTS

1. RESULTS AT A GLANCE

2. INTRODUCTION

3. SUMMARY

4. RECOMMENDATIONS

5. PROJECT RATIONALE AND METHODOLOGY

6. REPORTING ON ANTI-CORRUPTION PROGRAMMES

7. ORGANISATIONAL TRANSPARENCY

8. COUNTRY-BY-COUNTRY REPORTING

9. QUESTIONNAIRE

10. SCORES PER COMPANY

4

1. RESULTS AT A GLANCE

This Index is based on the unweighted average of results in all three categories

ACP = result for reporting on anti-corruption programmes

OT = result for organisational transparency

CBC = Country-by-country reporting

Domains BEL20 Other Average

1. Anti-corruption programmes (‘ACP’) 50% 24% 37%

2. Organizational transparency (‘OT’) 72% 74% 73%

3. Country-by-country reporting (‘CBC’) 11% 7% 9%

44% 35% 39%

5

2. INTRODUCTION

Transparency in Corporate Reporting: Assessing 30 Listed Belgian Companies 2015 provides

an evaluation of the transparency of reporting by 30 Belgian listed companies: 15 of the

BEL20 index and 15 smaller companies with international operations. The methodology

used (TRAC) focuses on three areas of reporting which are evolving very fast in the face of

rapidly changing public expectations of what constitutes good corporate practice: anti-

corruption programs, their organisational transparency (where and through what subsidiar-

ies they operate) and country-by-country reporting and countries.

The aim of this report is to encourage companies to align with developing reporting require-

ments rather than lag behind to await the inevitably slower developing statutory require-

ments. Leading from the front can be a competitive advantage, particularly in attracting in-

vestors and enhancing the public image. Being compliant with formal reporting require-

ments is not enough, companies increasingly need to anticipate change. This is as true of

their investor relations as it is of their business strategies.

The voluntary reporting that is described in this report today will be part of the formal re-

porting standards of tomorrow. Transparency International encourages companies to adopt

these standards now because it makes sense: their statements will be more convincing;

their standards will be more credible; their values can be linked to policies and procedures;

their vision is translated into strategy, policies and procedures. That is at the core of busi-

ness case of transparency in reporting on anti-corruption.

All the average scores are unweighted and must be interpreted with caution, not least be-

cause the relative importance of questions varies from company to company depending on

the extent of their international business and presence outside Belgium and business sec-

tors.

We would particularly like to thank the many companies which responded with useful com-

ments on the initial evaluations giving rise to fruitful exchanges of views. The more we can

dialog with companies in such a study the better and more useful the findings.

6

Transparency : “Characteristic of governments, companies, organisations and

individuals of being open in the clear disclosure of information, rules, plans,

processes and actions. As a principle, public officials, civil servants, the man-

agers and directors of companies and organisations, and board trustees have

a duty to act visibly, predictably and understandably to promote participation

and accountability and allow third parties to easily perceive what actions are

being performed.”

Bribery : ”The offering, promising, giving, accepting or soliciting of an ad-

vantage as an inducement for an action which is illegal, unethical or a breach

of trust. Inducements can take the form of gifts, loans, fees, rewards or other

advantages (taxes, services, donations, favours etc.).”

Corruption : “Corruption is the abuse of entrusted power for private gain. It

hits all the people whose live, livelihoods or happiness depend on the integ-

rity of those holding a position of authority.”

7

Summary

8

3. SUMMARY Overall

The following general trends and conclusions can be drawn from the TRAC-2015 review:

Firstly, companies improve their corporate reporting over time. This can be seen by com-

paring the scores from the companies that were also included in previous TRAC-studies.

This is in line with the trend of increasing reporting on non-financial information.

Secondly the BEL20 companies do better than the smaller multinationals, even though

the differences are not as big as one might expect (average overall score: 44% vs 35%).

Thirdly, companies pay increasing attention to reporting on anti-corruption programmes

(37%) and on organizational transparency (73%). However, country-by-country reporting

at corporate level does not get the attention it deserves (9%).

Finally, the BEL20-companies may be twice as transparent on their anti-corruption poli-

cies as the smaller Euronext-companies (50% versus 24%) but in this domain they are

lagging behind the global average of 70% (1).

The results of this TRAC review vary considerably from company to company, often we be-

lieve as a reflection of the extent to which companies have international operations and

presences: Companies operating internationally on a large scale may be more frequently faced

with issues around bribery and corruption, not least the legal risks associated with ex-

ternal jurisdictions such as the US Department of Justice (DoJ) with the Foreign Corrupt

Practices Act (FCPA) and the UK’s Anti-Bribery legislation, now more vigorously pursued

by the Serious Fraud Office (SFO) as was recently demonstrated by their action against

Standard Bank for a case involving bribery in Tanzania. Companies with the bulk of

their operations centred in Belgium, appear to be less conscious of these risks, though

they still exist, at least as regards public disclosure of policies to combat corruption and

bribery.

Clearly too, companies with largely domestic operations are less likely to be pre-

occupied with disclosure around their corporate organisation and country-by-country

reporting.

(1) Transparency in Corporate Reporting, Transparency International, 2014 http://www.transparency.org/whatwedo/

publication/transparency_in_corporate_reporting_assessing_worlds_largest_companies_2014

9

Both these factors are reflected in the results as also companies’ appreciation of their sec-

toral exposure both as regards risks and public expectations.

The business environment in which companies now operate has been changing very rapidly

in recent years in response to a mixture of corporate failures, the financial crisis of 2008 and

the resultant increasing public scrutiny of the ethical stance of companies be it as regards

fighting corruption or perceived fairness in paying taxes. The range of corporate stakehold-

ers has widened considerably beyond just investors, employees, customers and suppliers.

Governments, politicians and the general public, particularly the younger generations, are

becoming more demanding. Recent cases such as those of GSK in China and Petrobras in

Brazil reinforce public expectations of more active corporate policies to fight bribery and

corruption. Reluctant or forced disclosure of corporate tax policies are leading to the rapid

moves towards Base Erosion Profit Shifting (BEPS) rules under pressure from the OECD and

G20 and even more rapid moves to country-by-country (CBC) reporting of tax and profits.

The EU Member States must transpose the Directive on disclosure of non-financial and di-

versity information by certain large companies into national laws before the end of 2016. It

is expected that the first company reports will be published in 2018 covering financial year

2017-2018.

The Directive introduces measures that will strengthen the transparency and accountability

of ‘public interest entities’ with more than 500 employees. They will be required to report

on new matters including anti-corruption and anti-bribery measures. They will be required

to describe their business model, outcomes and risks of the policies on the above topics,

and are encouraged to rely on recognized frameworks such as GRI’s Sustainability Reporting

Guidelines, the United Nations Global Compact (UNGC), the UN Guiding Principles on Busi-

ness and Human Rights, OECD Guidelines, and International Organization for Standardiza-

tion (ISO) 26000.

This Directive is part of the wider European Union’s initiative on Corporate Social Responsi-

bility which includes plans for a consistent approach to reporting to support smart, sustaina-

ble and inclusive growth in pursuit of the Europe 2020 objectives.

10

Anti-corruption programmes

In this section BEL20-companies do better than the smaller multinational companies in every

one of the 13 areas under scrutiny (average score: 50% versus 24%). The responses that we

have obtained from smaller multinational companies indicate that they do have relevant poli-

cies and procedures in place but are less inclined to publicly report on them.

For companies, the best protection against the risk of bribery and corruption must be a

comprehensive anti-corruption programme that is fully implemented and monitored on a

continuing basis. Such anti-corruption programmes need to be very clearly endorsed by the

Boards (tone at the top) as an integral part of the company’s ethical stance.

The publication of the key-elements of an anti-corruption programme demonstrates a com-

pany’s commitment to fighting corruption and increases its responsibility and accountability

to stakeholders. In addition, a strong and public commitment to a robust anti-corruption

programme has a positive impact on a company’s employees as it strengthens their anti-

corruption attitudes. Public reporting on anti-corruption programmes can also contribute to

positive changes as the process of reporting focuses the attention of the company on its

own practices and drives improvements in policies and programmes.

The evaluation of corporate reporting on anti-corruption programmes is based on 13 ques-

tions, which are derived from the UN Global Compact and Transparency International Re-

porting Guidance on the 10th Principle against Corruption. This tool, based on the Business

Principles for Countering Bribery, which were developed by Transparency International in

collaboration with a multi-stakeholder group, includes recommendations for companies on

how to publicly report on their anti-corruption programmes.

Organisational transparency

Most companies demonstrate high standards regarding organisational transparency (section

2) scoring an average of 72-74%, yet they are reluctant to disclose all countries in which they

have operational activities (13% or less).

Large multinational companies operate as complex networks of interconnected entities in-

volving subsidiaries, affiliates or joint ventures controlled to varying degrees by the parent

company. These can be registered and operate in several countries, including secrecy juris-

dictions or tax havens.

11

If companies choose not to disclose these structures and holdings it can be very difficult to

identify them and understand how they relate to each other. US regulators require the dis-

closure of material subsidiaries only, which may explain a poor performance of companies

with US subsidiaries in this section.

Organisational transparency is a prerequisite to effective country-by-country reporting as

the next section illustrates.

Country-by-country reporting

Scores in this section are mostly low (on average 7-11%), which is not surprising given that

moves to country-by-country reporting are very recent and the financial reports that have

been the subject of review are those from 2014. But it is clear that some companies are more

advanced than others.

Overall company performance is very weak.

Companies disclose financial information for selected countries only.

Revenues are the most-often disclosed data point; pre-tax profits are the least-disclosed.

Country-by-country reporting is an essential element of corporate transparency in order to

ensure a stronger accountability of multinational companies through an increased monitor-

ing by stakeholders and citizens, which will also help to reduce tax avoidance. Currently,

multinational companies publish their accounts by combining data about tax compliance

from multiple countries into one single aggregate report, making it difficult to distinguish

between the contributions they make to all the individual countries they operate in. As the

recent Luxleaks scandal brought to light, in most cases multinational companies are not

transparent regarding their structure and operations, and exploit loopholes in domestic and

international tax law that allow for ‘profit shifting’ from country to country, with the inten-

tion of reducing the taxes paid on profits.

Transfer pricing policies are not per se unacceptable but increasingly society demands trans-

parency as to their effect on taxes paid in the countries in which companies operate.

On the 8th of July 2015 the European Parliament voted in favour of measures to increase the

transparency of the finances of multinational corporations, requiring EU-based multination-

al companies to reveal details of tax payments to governments around the world, reporting

financial information on a country-by-country basis and to publicly disclose information re-

garding tax rulings.

12

Under the country-by-country provision multinational companies would be required to dis-close crucial information such as, among others, their turnover, number of employees, profit made, taxes paid and public subsidies received for all the countries in which they have an establishment.

13

Recommenda-

tions

14

4. RECOMMENDATIONS

This section contains recommendations to the companies and to the readers of this report.

Recommendations to companies

Most public companies have anti-corruption programs in place, but many of them do not see

the need to report on this extensively at corporate level. Leading companies do report on

such programs to increase awareness and reinforce the prevention (and early detection) of

misconduct and errors of judgement. These companies simply make internal policies and

procedures (or abstracts) available on their corporate websites. The high scores in this sec-

tion, such as AB Inbev, KBC and Solvay, may serve as examples.

Companies increasingly report on their non-financial performance: health, safety, environ-

ment, community, etc. In doing so they should explicitly reject all forms of corruption be-

cause of its impact on society and on corporate reputation. Companies can show responsi-

bility and demonstrate leadership by reporting on the key policies and procedures that they

have put in place. Only a minority of companies do so while our discussions with others give

us the impression that they could do better rather easily. Every day the media show us that

no sector of industry is free of corruption. Public companies should recognize the sense of

urgency and act.

Regarding organisational transparency, we see that companies generally do not disclose all

countries of operation. They typically argue that this information can be found on the web-

sites of their subsidiaries and that they do not want to report on items that they consider

insignificant. These companies do not encourage stakeholders in getting the right picture of

their risk management in relation to corruption. And foreign subsidiaries do not necessarily

provide such information either. Small countries can generate big problems. Companies

should convince the public that they are in-control, also with remote entities and in small

countries, through voluntary disclosure of the countries in which they have operational ac-

tivities.

In line with the previous recommendation companies should also report their revenues,

profits and taxes paid in every country of operation, the so-called country-by-country re-

porting. Only those companies that disclose the local impact of their business allow their

stakeholders to assess the adequacy of their anti-corruption programs.

15

Obviously reporting can only be an indication of the quality of the company’s risk manage-

ment. Risk management must be based on a clear corporate vision on the risk of corruption.

It must be driven by shared values and clear policies rather than reporting standards and

compliance. Public interest entities in general do comply with statutory reporting require-

ments. Although such an assessment cannot be made by looking at corporate reporting

alone, the absence of corporate reporting is a weakness and a missed opportunity to show a

company’s intentions at a corporate level.

Recommendations to readers

The aim of this report is not to denounce companies that are not doing well enough in the

eyes of Transparency International. They are all compliant with statutory reporting require-

ments, well embedded in regulatory, supervisory and audit structures. Rather the voluntary

reporting that is described in this report will be part of the formal reporting standards of to-

morrow and Transparency International has played a leading role since its establishment in

1993.

Transparency International encourages companies to adopt these standards now because it

makes sense: their statements will be more convincing; their standards will be more credi-

ble; their values can be linked to policies and procedures; their vision is translated into strat-

egy, policies and procedures. That is at the core of the business case of transparency in re-

porting on anti-corruption.

16

Project rationale

and methodology

17

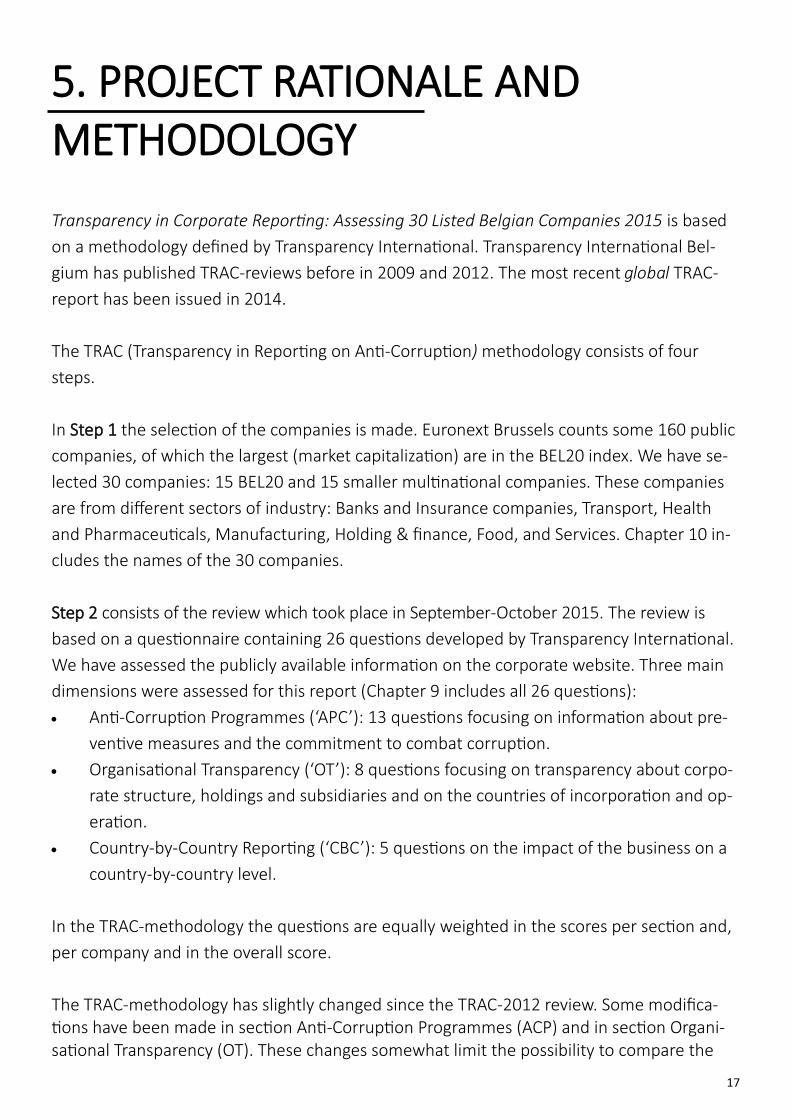

5. PROJECT RATIONALE AND METHODOLOGY

Transparency in Corporate Reporting: Assessing 30 Listed Belgian Companies 2015 is based

on a methodology defined by Transparency International. Transparency International Bel-

gium has published TRAC-reviews before in 2009 and 2012. The most recent global TRAC-

report has been issued in 2014.

The TRAC (Transparency in Reporting on Anti-Corruption) methodology consists of four

steps.

In Step 1 the selection of the companies is made. Euronext Brussels counts some 160 public

companies, of which the largest (market capitalization) are in the BEL20 index. We have se-

lected 30 companies: 15 BEL20 and 15 smaller multinational companies. These companies

are from different sectors of industry: Banks and Insurance companies, Transport, Health

and Pharmaceuticals, Manufacturing, Holding & finance, Food, and Services. Chapter 10 in-

cludes the names of the 30 companies.

Step 2 consists of the review which took place in September-October 2015. The review is

based on a questionnaire containing 26 questions developed by Transparency International.

We have assessed the publicly available information on the corporate website. Three main

dimensions were assessed for this report (Chapter 9 includes all 26 questions):

Anti-Corruption Programmes (‘APC’): 13 questions focusing on information about pre-

ventive measures and the commitment to combat corruption.

Organisational Transparency (‘OT’): 8 questions focusing on transparency about corpo-

rate structure, holdings and subsidiaries and on the countries of incorporation and op-

eration.

Country-by-Country Reporting (‘CBC’): 5 questions on the impact of the business on a

country-by-country level.

In the TRAC-methodology the questions are equally weighted in the scores per section and,

per company and in the overall score.

The TRAC-methodology has slightly changed since the TRAC-2012 review. Some modifica-tions have been made in section Anti-Corruption Programmes (ACP) and in section Organi-sational Transparency (OT). These changes somewhat limit the possibility to compare the

18

In Step 3 the draft scores are sent to the participating companies, asking them for their

comments. Less than 25 percent of the companies have taken the opportunity to respond.

This took place in the month of November. One company has requested us to discuss our

findings in more detail in a personal meeting.

Step 4 consists of the drafting of the report, that contains all answers per question and per

company, as well as trends, conclusions and recommendations.

More detailed information on the TRAC-2015 methodology can be found at our website (1).

Every effort has been made to verify the accuracy of the information contained in this re-port. All information was believed to be correct at the date of our review (closing 15 Octo-ber 2015). Nevertheless, Transparency International Belgium cannot accept responsibility for the consequences of its use for other purposes or in other contexts. (1) www.transparency.org/corporate_reporting

19

REPORTING ON

ANTI-CORRUPTION

PROGRAMMES

20

5. Reporting on Anti-Corruption-

Programmes

6.1 Introduction

For companies, the best protection against the risk of corruption and bribery must be a

comprehensive anti-corruption programme that is fully implemented and monitored on a

continuing basis. Such anti-corruption programmes need to be very clearly endorsed by the

Boards (tone at the top) as an integral part of the company’s ethical stance.

The publication of the elements of an anti-corruption programme demonstrates a compa-

ny’s commitment to fighting corruption and increases its responsibility and accountability to

stakeholders. In addition, a strong and public commitment to a robust anti-corruption pro-

gramme has a positive impact on a company’s employees as it strengthens their anti-

corruption attitudes. Public reporting on anti-corruption programmes can also contribute to

positive changes as the process of reporting focuses the attention of the company on its

own practices and drives improvements in policies and programmes.

The evaluation of corporate reporting on anti-corruption programmes is based on 13 ques-

tions, which are derived from the UN Global Compact and Transparency International Re-

porting Guidance on the 10th Principle against Corruption. This tool, based on the Business

Principles for Countering Bribery, which were developed by Transparency International in

collaboration with a multi-stakeholder group, includes recommendations for companies on

how to publicly report on their anti-corruption programmes.

6.2 Results

Unweighted average cores BEL20

Other Average

Anti-corruption programmes (‘ACP’) 50% 24% 37%

21

In this section the companies from the BEL20 advance the smaller companies at Euronext

Brussels in every one of the 13 areas under scrutiny (average score: 50% versus 24%). The

responses that we have obtained from smaller multinational companies indicate that they

do have relevant policies and procedures in place but are less inclined to publicly report on

them.

The companies that may serve as an example here are KBC (92%) Solvay (88%) and AB Inbev

(85%). It is positive to see that 10 out of 15 companies from the BEL20-index have scores of

50% or more in this area.

Furthermore, the study suggests that those companies substantially focused on the Belgian

domestic market, make a lower assessment of their possible exposure to bribery and cor-

ruption. All, however, appear to be re-assessing their positions.

Companies in the BEL20-index

The highest score (80%) is obtained on question 2: “Does the company publicly commit to

be compliant with all relevant laws including anti-corruption law?”.

For the high-level questions (questions 1-4) the average score is slightly lower (63%) as not

all companies are explicit about their anti-corruption programmes or mention only anti-

bribery measures which is often defined as ‘gifts, hospitality and expenses’. The concept of

corruption is definitely broader than that.

This is also reflected in the scores on questions 9 and 13 showing that companies are less

inclined to report on facilitation payments or political contributions (37%). The same goes

for question 26 regarding reporting on community contributions (7%).

Some 40% of the companies report having training programs on anti-corruption for their

employees and directors.

Finally, the reporting on policies and procedures in relation to reporting channels (such as

hotlines and confidants) and the protection of whistleblowers (questions 10 and 11) scores

a promising average of 52%. Many more companies do have reporting channels but these

are only open to employees and therefore not included in their public reporting.

22

Other companies from Euronext Brussels

In the ACP-section (anti-corruption programmes) the smaller international companies are

lagging behind the companies from the BEL20-index. This goes for every one of the ques-

tions 1-13, but some differences stand-out.

As for the BEL20-group the smaller international companies obtain their highest score (53%)

on question 2 “Does the company publicly commit to be compliant with all relevant laws in-

cluding anti-corruption law?” In this domain this is the only question with an average score

above 50%.

For the high-level questions (questions 1-4) the average score is only 33% as the majority of

companies are not explicit about their anti-corruption programmes or mention only anti-

bribery measures which they give a narrow definition.

Only 18% of the smaller international companies report that their anti-corruption programs

explicitly apply to others than employees and directors, for example agents, contractors, ad-

visors, representatives and intermediaries (questions 5 and 6). Some 30% does conform that

it is applicable to employees and directors.

Only 13% of the smaller multinationals report having training programs on anti-corruption

for their employees and directors.

Finally, the reporting on policies and procedures in relation to reporting channels and the

protection of whistleblowers (questions 10 and 11) have an average score of only 20%.

Reporting channels are recognised as an effective tool to be informed of any misbehaviour

that is not getting addressed in day-to-day communication. It is clear to see that serious im-

provements can be made in all of the above areas.

For companies with staff numbers over 500 the reporting requirements are changing funda-

mentally and at a rapid pace. All companies in our selection should demonstrate a sense of

urgency and respond clearly and explicitly in relation to their anti-corruption programmes,

especially for the 13 issues covered in the ACP-section.

Transparency international has traditionally been monitoring and advising the larger multi-

national companies (BEL20) whereas the other companies underwent their first TRAC-

review in 2015. This may explain in part the lower scores of the latter group.

23

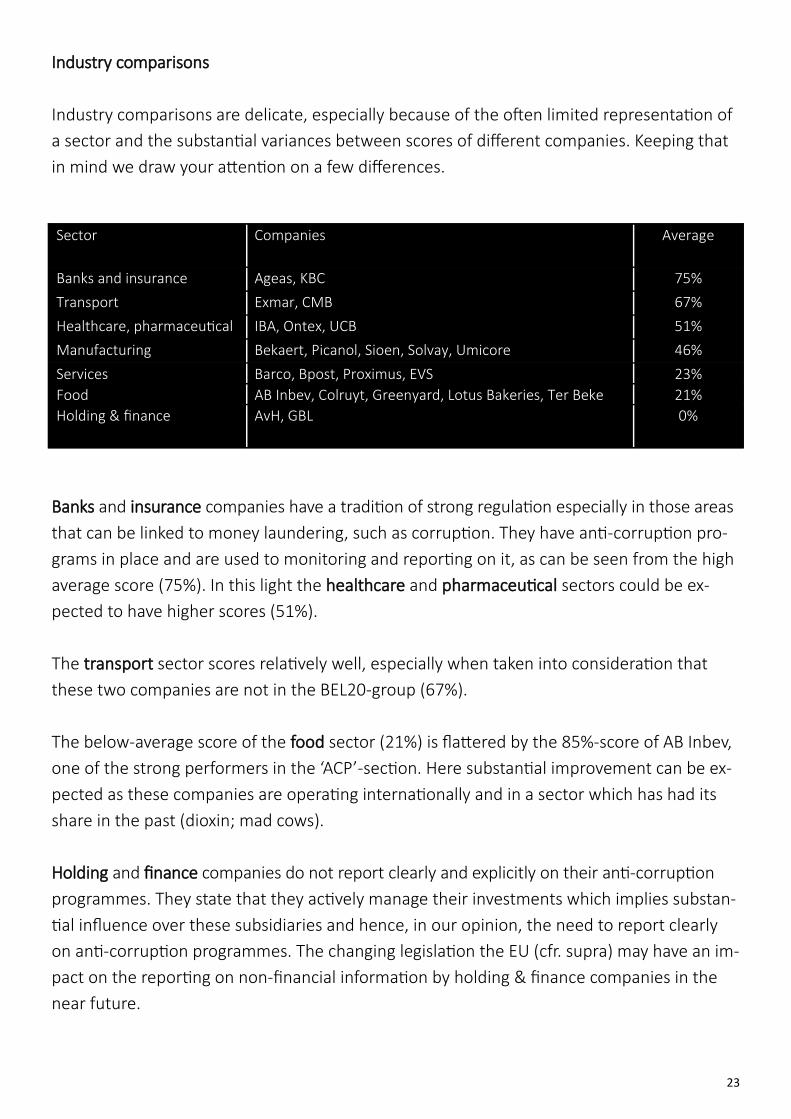

Industry comparisons

Industry comparisons are delicate, especially because of the often limited representation of

a sector and the substantial variances between scores of different companies. Keeping that

in mind we draw your attention on a few differences.

Banks and insurance companies have a tradition of strong regulation especially in those areas

that can be linked to money laundering, such as corruption. They have anti-corruption pro-

grams in place and are used to monitoring and reporting on it, as can be seen from the high

average score (75%). In this light the healthcare and pharmaceutical sectors could be ex-

pected to have higher scores (51%).

The transport sector scores relatively well, especially when taken into consideration that

these two companies are not in the BEL20-group (67%).

The below-average score of the food sector (21%) is flattered by the 85%-score of AB Inbev,

one of the strong performers in the ‘ACP’-section. Here substantial improvement can be ex-

pected as these companies are operating internationally and in a sector which has had its

share in the past (dioxin; mad cows).

Holding and finance companies do not report clearly and explicitly on their anti-corruption

programmes. They state that they actively manage their investments which implies substan-

tial influence over these subsidiaries and hence, in our opinion, the need to report clearly

on anti-corruption programmes. The changing legislation the EU (cfr. supra) may have an im-

pact on the reporting on non-financial information by holding & finance companies in the

near future.

Sector Companies Average

Banks and insurance Ageas, KBC 75%

Transport Exmar, CMB 67%

Healthcare, pharmaceutical IBA, Ontex, UCB 51%

Manufacturing Bekaert, Picanol, Sioen, Solvay, Umicore 46%

Services Barco, Bpost, Proximus, EVS 23%

Food AB Inbev, Colruyt, Greenyard, Lotus Bakeries, Ter Beke 21%

Holding & finance AvH, GBL 0%

24

Organisational

Transparency

25

7. Organisational transparency (‘OT’)

7.1 Introduction

Large multinational companies operate as complex networks of interconnected entities in-

volving subsidiaries, affiliates or joint ventures controlled to varying degrees by the parent

company. These can be registered and operate in several countries, including secrecy juris-

dictions or tax havens. If companies choose not to disclose these structures and holdings it

can be very difficult to identify them and understand how they relate to each other.

Organisational transparency is important for many reasons, not least because company

structures can be made deliberately opaque for the purpose of hiding the proceeds of cor-

ruption. More fundamentally, it is important because it allows local stakeholders to know

which companies are operating in their territories, are bidding for government licences or

contracts, or have applied for or obtained favourable tax treatment. It also informs local

stakeholders about which international networks these companies may belong to and how

they are related to other companies operating in the same country. In addition, through full

disclosure of corporate holdings, stakeholders, including investors, can gain more complete

knowledge of financial flows such as intra-company transfers and payments to govern-

ments. Organisational transparency allows citizens to hold companies accountable for the

impact they have on their communities.

To assess organisational transparency, Transparency International researchers consulted

publicly available documents such as annual reports and stock exchange filings for infor-

mation about company subsidiaries, affiliates, joint ventures and other holdings. The infor-

mation sought included corporate names, percentages of ownership by the parent compa-

ny, countries of incorporation and the countries in which the companies operate.

7.2 Results

Unweighted average scores BEL20

Other Average

Organizational transparency (‘OT’) 72% 74% 73%

26

Virtually all companies disclose their fully consolidated subsidiaries, the percentage of

shares held and the countries of incorporation of these subsidiaries (93%-95%). For non-

fully disclosed subsidiaries the score of this information is somewhat lower (70%-73%).

However, companies generally do not disclose all the countries in which they have opera-

tional activities (0%-8%). The relatively good score for Organisational transparency is a pre-

requisite to effective country-by-country reporting as the next section illustrates. The coun-

try of operation is important therein, and therefore companies need to be more clear and

transparent as to their countries of operation. The information is readily available in the or-

ganization and can be easily provided at corporate level. Also remote subsidiaries and small

countries can provoke big problems to corporates and deserve to be included in anti-

corruption programmes and related reporting.

Differences between the companies in the BEL20-index and the other companies from the

Euronext Brussels are limited and not considered worth analysing further.

27

Country

By

Country

reporting

28

8. COUNTRY-BY-COUNTRY

8.1 Introduction

The third section of the report assessed the level of country-by-country reporting on basic

financial data. The main objective of the CBC-section is for companies to display the profits

they earn abroad and the amount of taxes relating thereto. Currently, companies publish

their accounts by combining data about tax compliance from multiple countries into one

single report making it difficult to distinguish between the contributions they make to all the

individual countries they operate in.

This section is likely to become very important in the future as the European Parliament vot-

ed in favour of measures to increase the transparency of EU-based multinational companies

on the 8th of July 2015. The measures aim to reveal details of tax payments to governments

around the world.

The measures voted by the Parliament are now being reviewed by the Commission and

Council. This could become an EU law, forcing multinational EU-based companies to comply

with the CBC reporting standards.

In addition, country-by-country reporting provides investors with more comprehensive fi-

nancial information about companies and helps them address investment risk more effec-

tively. The publication of key financial data provides citizens with the opportunity to under-

stand the activities of a particular company in their country and to monitor the appropriate-

ness of their payments to governments.

29

8.2 Results

The scores in this section are low: 11% for the BEL20 and 7% for the smaller multinational

companies. The only company with an average score greater than 50% is KBC (60%), fol-

lowed by Solvay and Sioen (each 40%).

Only three companies disclose pre-tax income or income taxes for all countries.

This is an area that will receive much attention during the coming years due to the changing

legislation regarding country-by-country reporting (cfr. Supra).

Unweighted average scores BEL20

Other Average

Country-by-country reporting (‘CBC’) 11% 7% 9%

30

9. Questionnaire

The TRAC-2015 review is based on the following questionnaire:

I. Corporate reporting on anti-corruption programmes (Section ‘ACP’)

1. Does the company have a publicly stated commitment to anti-corruption?

2. Does the company publicly commit to be compliance with all relevant laws, in-

cluding anti-corruption law?

3. Does the company leadership (senior member of management or board)

demonstrate support for anti-corruption?

4. Does the company’s code of conduct / anti-corruption policy explicitly apply to

all employees and directors?

5. Does the company’s anti-corruption policy explicitly apply to persons who are

not employees but are authorised to act on behalf of the company or repre-

sent it (for example: agents, advisors, representatives or intermediaries)?

6. Does the company’s anti-corruption programme apply to non-controlled per-

sons or entities that provide goods or services under contract (for example:

contractors, subcontractors, suppliers)?

7. Does the company have in place an anti-corruption training programme for its

employees and directors?

8. Does the company have a policy on gifts, hospitality and expenses?

9. Is there a policy that explicitly prohibits facilitation payments?

10. Does the programme enable employees and others to raise concerns and re-

port violations (of the programme) without risk of reprisal?

11. Does the company provide a channel through which employees can report sus-

pected breaches of anti-corruption policies, and does the channel allow for

confidential and/or anonymous reporting (whistle blowing)?

12. Does the company carry out regular monitoring of its anti-corruption pro-

gramme to review the programme’s suitability, adequacy and effectiveness,

and implement improvements as appropriate?

13. Does the company have a policy on political contributions that either prohibits

such contributions or if it does not, requires such contributions to be publicly

disclosed?

31

III. Country-by-Country Reporting (Section ‘CBC’)

22. Does the company disclose its revenues/sales in country X?

23. Does the company disclose its capital expenditure in country X?

24. Does the company disclose its pre-tax income in country X?

25. Does the company disclose its income tax in country X?

26. Does the company disclose its community contribution in country X?

The TRAC-methodology provides further instructions as well as scoring-criteria for every question to ensure consistent application by the researchers.

32

10. Scores per company

ACP: Anti-corruption programmes. OT:Organisational transparency. CBC: Country-by-country reporting.

Sections: * ACP OT CBC Average Company Responded

BEL20 AB Inbev 85% 75% 0% 53%

Ageas 58% 25% 0% 28%

Ackermans en van H. 0% 75% 0% 25%

Bekaert 73% 75% 10% 53%

Bpost 15% 75% 20% 37% Y

Cofinimmo 65% 100% 10% 58%

Colruyt 8% 75% 10% 31%

D’ieteren 23% 75% 0% 33%

Engie 77% 31% 10% 39%

GBL 0% 75% 0% 25%

KBC 92% 100% 60% 84%

Proximus 31% 75% 0% 35% Y

Solvay 88% 75% 40% 68% Y

UCB 77% 75% 0% 51% Y

Umicore 50% 75% 0% 43%

Average 50% 72% 11% 44%

Euronext Barco 62% 75% 0% 46%

CFE 0% 75% 0% 25%

CMB 54% 75% 0% 43%

EVS 0% 75% 0% 25%

Exmar 81% 75% 0% 52%

Greenyard 0% 75% 10% 28%

IBA 46% 75% 0% 40%

Lotus Bakeries 4% 88% 30% 40% Y

Nyrstar 58% 19% 0% 25%

Ontex 31% 100% 0% 44% Y

Picanol 0% 75% 0% 25%

Sioen 15% 75% 0% 43%

Sipef 0% 75% 10% 28% Y

Ter Beke 8% 75% 10% 31%

Vande Velde 0% 75% 0% 25%

Average 24% 74% 7% 35%

Average 37% 73% 9% 39%

33

Create change with us

Engage

More and more people are joining the fight against corruption, and the discussion is grow-

ing. Stay informed and share your views on our website and blog, and social media.

Volunteer

With an active presence in more than 100 countries around the world, we’re always look-

ing for passionate volunteers to help us increase our impact. Check out our website for the

contact details for your local organisation.

Donate

Your donation will help us provide support to thousands of victims of corruption, develop

new tools and research, and hold governments and businesses to their promises. We want

to build a fairer, more just world. With your help, we can.

Young TIB

We draw your attention to our Young TIB group that has been established in 2015 and ac-

tively engages in our organisation, research and advocacy.

Join us

Facebook: https://www.facebook.com/TransparencyInternationalBelgium?fref=ts

Facebook (Young TI) https://www.facebook.com/youngTIbelgium/?fref=ts

Twitter https://twitter.com/TIBelgium

Website www.transparencybelgium.be

Offices

Transparency International Belgium VZW-ASBL

Nijverheidsstraat 10 rue de l‘Industrie

1000 Brussels

Belgium