asia and pacific commission on agricultural · pdf fileasia and pacific commission on...

TRANSCRIPT

RAP/APCAS/14/13.2

1

Asia and Pacific Commission on

Agricultural Statistics

Twenty-fifth Session

Vientiane, Lao PDR, 18-21 February 2014

Agenda Item 13

Recent advancements in Agricultural Economic Statistics – Price and Investment domains

Contributed by: FAO Statistics Division

1. Price Statistics - Introduction

The 2007 food price crisis, with its implications for food security, underlined the

importance in improving the monitoring of agriculture and food price transmissions across the

value-chain. Though FAO is the main provider of internationally comparable data on agricultural

producer prices, the need to better monitor agriculture food price transmissions requires it expand

its previous work on agricultural prices in four key directions. These include: 1) improve the

coverage, frequency and timeliness of price statistics to measure farm to fork food and agriculture

prices; 2) improve dissemination and awareness of FAO price data by accompanying new data

releases with statistical analysis; 3) develop, evaluate and disseminate a new set of derived

indicators to better capture and monitor price dynamics, transmission and volatility; and 4)

consolidate and disseminate these price datasets and indicators in price profiles to provide quick

and easy access to price information for different geographic groupings.

This paper presents and describes the data currently collected on agricultural and food

prices, the new dissemination strategy, and new indicators and price profiles currently under

development. It also solicits discussion and advise from APCAS member countries on how to

January 2014 E

RAP/APCAS/14/13.2

2

improve underlying country-level data, and how FAO can best provide relevant and timely price

information and analytical products to member countries.

2. Setting the context – Key Uses of Price Statistics

Agricultural prices influence public and private decisions related to the type and volume of

agricultural policy and production, be it made by national governments, farmers and other agri-

businesses, or international organizations.

National governments use agriculture price data to develop, monitor and evaluate food price

subsidies as well as other agriculture support policies; to identify intra-country and international

comparative advantage in the type and composition of agricultural production; and to identify

population groups at risk as a result of price volatility or disruptions in the agriculture value-

chain. Price data is also used to estimate the value of agricultural output, intermediate inputs, and

agricultural value added, in both real and nominal terms, which in turn provides data essential for

productivity analysis.

Farmers and agri-businesses use price information to inform decisions about agricultural

production and composition; use and purchase of intermediate inputs, including feed, fertilizers,

labour and machinery; and borrowing, farm management and investment decisions.

International organizations use agricultural price data for similar analytical and policy

purposes as national governments. For their purposes, standardization in the methodologies

behind data collection helps ensure that cross-country comparisons are able to identify differences

in policies, environment, production, and productivity, and are not an artefact of differences in

definitions or the manner in which data are collected, estimated or disseminated1.

3. Current and planned work on Prices

a. Producer prices

FAO provides annual country-level data on producer prices for primary crop and livestock

products dating back to 19912; monthly producer prices beginning January 2010; and annual

producer price indexes (PPIs) for 1999 to 2011. FAO’s producer price database has the largest

coverage of producer prices in the world, with a coverage of approximately 150 countries and

about 200 commodities, representing roughly 97 percent of the world’s value of agricultural

production at 2004-2006 international dollar prices. Absolute producer prices are available in

local currency, standard local currency and US dollars, with continuous efforts made to expand

country coverage and improve data quality.

1 More details available in “Farm and input prices: collection and compilation”, FAO, 1980.

2 An older database (“Producer Price Archive”), with historical data from 1966 to 1990 is also available on

FAOSTAT. This database is not anymore maintained and updated.

RAP/APCAS/14/13.2

3

Producer prices, collected annually through a price questionnaire, refer to prices received by

farmers, known as “farm gate” or first-point-of-sale prices, when farmers participate in their

capacity as sellers of their own products. To maximize international comparability, countries are

requested to remain as close as possible to this concept. However, due to differences in data

collection infrastructure and capacity, countries do vary from this concept by collecting, instead,

wholesale or local market prices. While these may be good proxies of farm-gate prices when the

marketing chain is very limited, they tend to be poorer proxies in economies where transport and

commercial margins constitute a significant share of the final product price. At the far extreme,

some countries report retail prices, which are typically very poor proxies for producer prices.

As FAO begins work on Cost of Production statistics and the Economic Accounts of

Agriculture (EAA), the proximity of price data to the producer price concept will become

increasingly important. Producer prices are an essential input into both statistical activities, and

both are used by policy makers to evaluate comparative advantage within their country and

against major competitors, in identifying productivity enhancing inputs, and in establishing

agricultural support policies.

b. Consumer prices, and regional and global price indexes

To extend statistical coverage of agricultural price statistics and better investigate price

transmission, in 2011 FAO began to disseminate country-level data on Consumer Price Indices

(CPI), using data compiled by the International Labour Organization (ILO), for the food and all-

items index, for about 140 countries3. Since August 2013, FAO also began publishing regional

and global food CPIs4. These indicators, compiled quarterly for FAO regions, add to the set of

regional indices from other data domains, such as production and trade. In the near future, these

set will be further enhanced with the addition of regional and global PPIs.

Such aggregate indicators help identify common trends across regions as well as country-

level differences, and the drivers behind both. They can also serve to identify leading indicators

of phenomenon such as food price hikes and food insecurity. For example, a comparison of the

historical trend in the FAO Food Price Index (FPI) against the global food CPI suggests the FPI is

a leading indicator of future consumer food price inflation, though the transmission is lagged,

incomplete and varies considerably across regions (Figure 1 and Section 4.c).

3 Some countries provide indices for urban or local areas only and a very limited number also provide categorical

disaggregation (low income vs. high income households, etc). 4 The data and corresponding analysis can be found in: www.fao.org/economic/ess/ess-economic/cpi/en/. Among

other organizations that produce regional Food CPIs, the ILO, the OECD and Eurostat’s indices have a more limited

regional disaggregation or country coverage. Furthermore, while all these organizations use GDP weights to

aggregate country data, FAO uses weights based on country population, which is best adapted to keep focus on food

security.

RAP/APCAS/14/13.2

4

Figure 1: The FPI as a leading indicator of the global food CPI5

In moving forward, these food CPIs will be complemented by regional and global PPIs.

Still under discussion are two important methodological questions: 1) the choice of weights

(population, GDP or other); and whether or not to produce global and regional PPIs at the

commodity level.

c. Mobile data collection and the AMIS project

Under a project to strengthen Agricultural Market Information Systems (AMIS), FAO is

developing a market monitor to track current and expected future trends in international markets.

The project will develop and adapt data and analysis tools, for use at the global and country level,

in sharing, analyzing and disseminating international and national data on market prices, as well

as crop production forecasts and food stock estimates. This, in turn, can help governments and

policy makers detect abnormal situations in agriculture markets, and monitor and evaluate impacts

such as futures exchanges, price transmission, and food security.

One component of the AMIS project includes the use of digital and geo-referenced

technologies, such as smart phones and mobile applications, to improve food price data collection.

The use of digital mobile technology exploits the opportunity for real time data, and the use of

ICT technology helps cost-effectively improve the speed of data collection, validation,

processing, analysis and dissemination. Another component of AMIS includes strengthening of

FAO’s existing on-line GIEWS Food Price Data and Analysis Tool, to monitor basic staple food

prices in 82 countries and conduct analysis of different data series in both nominal and real terms.

Bangladesh, India and Nigeria are among the country-level partners piloting this project.

5 The different scales on the left magnifies the food CPI to demonstrate the leading indicator aspect of the FPI; use of

the same scale on the right demonstrates that FPI volatility is mitigated at the consumer level.

-40%

-20%

0%

20%

40%

60%

0%

5%

10%

15%

20%

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

FAO Global Food CPI

FAO Food Price Index (right scale)

-40%

-20%

0%

20%

40%

60%

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

FAO Global Food CPI

FAO Food Price Index

RAP/APCAS/14/13.2

5

d. Price transmission and price volatility indicators

The understanding of how and to what extent price changes are transmitted from

international to national markets (horizontal transmission) and along agricultural and food value-

chains (vertical transmission) helps assess the exposition and vulnerability of market actors and

consumers to price shocks. Quantification of vertical price transmission provides a measure of

the size and speed of the pass-through of a price shock (producer level) to consumers (retail

level). For horizontal price transmission, it provides a measure of the impact of a change in

international prices on domestic prices (wholesale or retail level).

Price volatility indicators, on the other hand, matter both because they provide a statistical

measure of price variability in agricultural and food markets, an indicator of prevailing market

conditions, and a signal of the need for specific types of policy intervention. At the

upstream/producer level, a high level of price volatility may indicate that commodity supply is

insufficient to cover demand and/or that producers are exposed to price fluctuations in agricultural

inputs (e.g. fuel, feed, etc.), which are transmitted to output prices. At the downstream/retail

level, price volatility may be caused by a high rate of transmission of producer or international

commodity prices to the retail level, possibly reflecting short value-chains. High price volatility

can have several adverse impacts: lower levels of investment by producers uncertain about future

revenues; less adaption of consumption behavior by consumers facing unclear price signals; and

reduced effectiveness of agriculture and food policy interventions including price supports,

strategic stocks, and regulation of commodity derivatives markets. The extent to which variability

in producer prices is transmitted to food consumer prices essentially depends on the length of the

value-chain, on the market power of each actors of the chain, on the nature of the demand for that

commodity or product and on the existence of possible substitutes.

FAO is currently developing, testing and evaluating price transmission coefficients and

price volatility indicators, based on a limited set of commodities and countries. These indicators

would be first available at country-level, and then extend to higher levels of geography.

These price transmission indicators, developed using econometric models, show price

transmission is lowest in developed economies characterized by extended food value-chains and a

high share of processed products in households’ food baskets. Over the long term, North America

and Europe see only 30% of price increases of primary products on international markets

transmitted to domestic consumer food prices; while the price transmission is 50% in Latin

RAP/APCAS/14/13.2

6

America and Asia, and almost complete in Eastern and Western Africa. For Eastern Africa, more

than 10% of the shock is passed-on after 4 months, and 20% after 8 months (Figure 2).

RAP/APCAS/14/13.2

7

Figure 2: Response of regional food CPIs to a 1% shock in the FAO FPI

While these results suggest that price transmission is intrinsically linked to the

characteristics of food value-chains and to the composition of food baskets, which is confirmed by

other studies, they should be interpreted with caution for the following reasons. First, policy

interventions - such as minimum or maximum purchase prices, export or import restrictions, and

production and consumption subsidies - alter the degree of pass-through and may result in

weakened transmission or inconclusive estimates. Second, these results measure price

transmission between a limited number of internationally traded commodities and average food

consumer prices at the regional level, and these may differ for specific countries and/or specific

commodities. Third, the transmission does not yet take into account some important explanatory

variables, such as food import dependency, region-specific food commodity baskets, or structural

breaks in price co-movements. Fourth, more robust estimation of vertical price transmission

suffers from the lack of available data across the value-chain, which requires a sufficient number

of price quotations at the producer, wholesale and retail levels for the same or similar commodity;

while horizontal transmission is best estimated for specific markets at the local level, where

information is seldom available.6

Price volatility indicators, still under discussion, should capture the magnitude of consumer

prices change overtime, giving equal weight to increases and decreases. These indicators can be

standard statistical measures of observed volatility or dispersion (i.e. standard deviation, range,

interquartile range, or median of absolute deviations from the median); or from the modeling of

the volatility process (example in Box 1).

6 Faminow, M.S. and Bruce L. Benson. Spatial Economics: Implications for Food Market Response to Retail Price

Reporting. Journal of Consumer Affairs, V19:1, pp 1-19, 1985.

0%

20%

40%

60%

80%

100%

120%

140%

0 10 20 30 40 50 60 70

Lon

g-te

rm t

ran

smis

sio

n e

last

icit

y

Number of months needed to reach 20% transmission

South-Eastern Asia

Western Africa

Southern Africa

North America Europe

North AfricaSouthern Asia

Central AmericaSouth America

Eastern Africa

SLOW + LOW TRANSMISSION

FAST + HIGH TRANSMISSION

SLOW + HIGH

TRANSMISSION

FAST + LOW

TRANSMISSION

RAP/APCAS/14/13.2

8

Box 1: Volatility indicators based on the modeling of the volatility process

The price of a commodity or a group of commodities at one point in time can be decomposed into

its expected mean given the information available up to the preceding period and a random term.

This random term represents the unexpected shocks that affect prices and, in the case of

commodity prices in particular, are likely to be correlated over time. These so-called GARCH

processes (Generalized Autoregressive Conditional Heteroscedasticity) can be reproduced by

setting and estimating the structure of this autocorrelation. In its simplest version, this approach

can be expressed mathematically by:

[1],

[2].

where and are independently and identically distributed random terms and the conditional

standard error.

The coefficients of equation [2] are generally determined by Maximum Likelihood Estimation

(MLE), after setting initial values for the conditional variance. The conditional variance is then

estimated iteratively over the whole period.

e. Price profiles and other analytical products

FAO has begun quarterly dissemination of regional and global food CPIs accompanied by a

statistical analysis and media release to promote awareness of its new data series. As FAO

progressively expands its price data and indicators, it plans to integrate and present them in

country, regional and global price profiles. Country profiles would show country specific

information on producer prices (absolute levels and indices), consumer prices (indices) and price

transmission coefficients; while regional and global profiles would present regional and global

PPIs and food CPIs, and average price levels for select commodities. Some possible mock-ups

are provided below, for discussion.

RAP/APCAS/14/13.2

9

Country Profiles - Producer prices

Price indicators

5 largest increases

5 largest decreases

Global Profile - Producer Prices

Price indicators

Livestock (avg. 2011 prices, I$/t)

Vegetables (avg. 2011 prices, I$/t)

Cereals (avg. 2011 prices, I$/t)

0

20

40

60

80

100

120

140

160

180

Agricultural GDP Deflator

Agricultural Producer Price Index

27.5%

28.0%

28.5%

29.0%

29.5%

30.0%

30.5%

31.0%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

0

20

40

60

80

100

120

140

160

180

Agricultural GDP Deflator-World

Agricultural Producer Price Index-World

0

500

1,000

1,500

2,000

2,500

Indigenous Cattle Meat

Indigenous Goat Meat

Indigenous Pigmeat

Indigenous Chicken Meat

0

20

40

60

80

100

120

140

160

180

200

Wheat Rice, Paddy Barley Maize

0

20

40

60

80

100

120

140

160

180

200

Wheat Rice, Paddy Barley Maize

RAP/APCAS/14/13.2

10

4. Investment Statistics - Introduction

Raising agricultural productivity is critical to increasing the real incomes necessary for

better access to food7. In turn, increasing capital stock per worker, often known as the capital-

labour ratio, or degree of capital intensity, is a critical to increasing agricultural productivity. In

many instances, the income gap between high-income and low-income countries has widened as a

result of low capital-labour ratios in low-income countries. This reflects both the higher relative

costs of capital compared to labour in low-income countries, but more importantly, weaker credit

markets that make it more difficult for agricultural producers to finance capital investments.

As shown in Figure 2, developing countries exhibit a strong positive correlation between

investment in agriculture, as measured by capital accumulation, and hunger reduction, measured

by the World Food Summit (WFS) goal to eradicate hunger and reduce the number of

undernourished. The graph shows that all countries with the largest setback vis-à-vis the WFS

goal, except DPR Korea, had a negative annual growth rate in Agricultural Capital Stock (ACS)

per worker in agriculture for 1990-2005, while the opposite occurred in countries with the greatest

progress towards the WFS goal.

Figure 2: Annual rates of ACS growth (1990-2005): best and worst performing countries

Source: Von Cramon-Taubadel et al. (2009)

To support analysis of ACS, and its’ associated sources of investment financing, FAO

Statistics Division (ESS) is developing a new and more robust methodology to measure ACS , a

new global Investment Dataset comprised of five main elements - Credit to Agriculture,

Government Expenditures on Agriculture, Official Development Assistance to Agriculture,

7 For a review of the magnitude of, trends in, and data gaps pertaining to investment in agriculture, see ESA Working

Paper No.11-19 Financial Resource Flows to Agriculture (http://www.fao.org/docrep/015/an108e/an108e00.pdf) and

the 2012 State of Food and Agriculture (http://www.fao.org/publications/sofa/en/)

RAP/APCAS/14/13.2

11

Foreign Direct Investment in Agriculture, and Foreign Remittances, and country-level profiles on

both growth in agricultural capital stock and its financing sources. A key feature of this initiative

is the harmonization of FAO work with that of other international organizations that are

compiling relevant datasets, as presented in the following sections. The FAOSTAT’s framework

of agricultural investment flows is illustrated in the following hierarchical chart.

Figure 1. FAOSTAT’s Agricultural Investment Data Framework8

5. Current and planned work on Investment

a. AGRICULTURAL CAPITAL STOCK

FAO’s previous database on ACS was based on FAOSTAT’s physical inventories, which

included the following components: land development, plantation crops, machinery and

equipments, livestock, and structures for livestock. These data excluded the forestry and fishery

subsectors and greenhouse production structures, mainly due to lack of information. The more

significant problem in the ACS database, however, came from limitations in the underlying data

sources, much of which was found in agricultural machinery and equipment data, the

methodology of which is currently being reviewed.

To build a more robust global ACS database, the Statistics Division of FAO (ESS) will

develop a methodology based on national accounts information, and draw on national accounts

data and estimates compiled by the UN Statistics Division and the OECD. To estimate capital

stock data for the agriculture, forestry and fisheries sectors from a national accounts perspective,

it will use country-level data and estimates of the following variables: value-added, gross output,

gross fixed capital formation (GFCF), capital stock, employment and labour compensation. As a

result, the revised methodology would enable FAO to better estimate agricultural capital stock

8 This framework could be further expanded by including other financing sources as Tax Expenditures (Marginal Tax

Revenue Forgone) in Public Domestic or Savings and Firm Product Financing in Private Domestic.

Agricultural Capital Formation (ACF)

ACFt = ACSt – ACSt-1

Domestic Flows

Private Domestic

Credit, Private Equities,

Remittances

Public Domestic

Government Expenditure

Foreign Flows

Private Foreign

Foreign Direct Investment

Foreign Remittances

Public Foreign

ODA + Other Official Flows

RAP/APCAS/14/13.2

12

encompassing agriculture, forestry, and fishing activities more broadly, and thereby enabling

better analysis of productivity and investment financing in the broad agricultural sector.

In addition to improving data on capital stock/physical investment, ESS is also expanding its

coverage of sources of investment financing, looking at both public and private sources, as well as

domestic and foreign sources, as outlined in Figure 1. This is a critical first step in assessing how

the composition of financing sources impacts total investment in agriculture, as well as investment

across different sizes and types of agricultural producers.

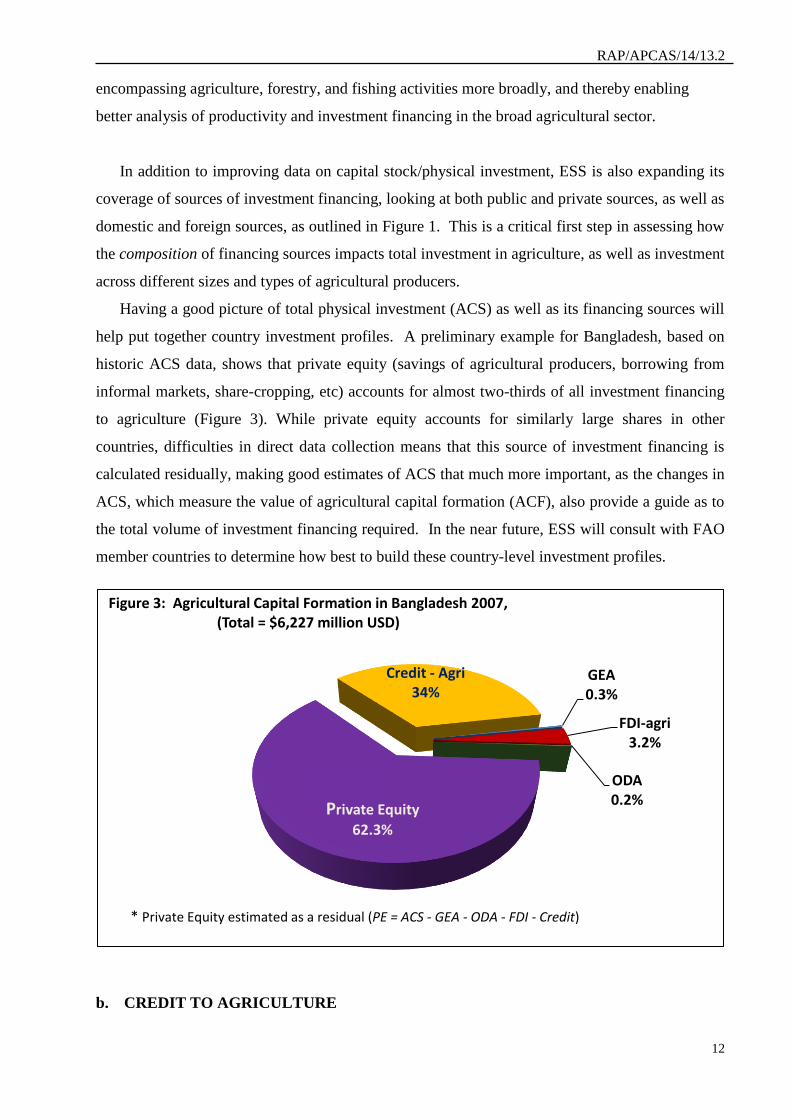

Having a good picture of total physical investment (ACS) as well as its financing sources will

help put together country investment profiles. A preliminary example for Bangladesh, based on

historic ACS data, shows that private equity (savings of agricultural producers, borrowing from

informal markets, share-cropping, etc) accounts for almost two-thirds of all investment financing

to agriculture (Figure 3). While private equity accounts for similarly large shares in other

countries, difficulties in direct data collection means that this source of investment financing is

calculated residually, making good estimates of ACS that much more important, as the changes in

ACS, which measure the value of agricultural capital formation (ACF), also provide a guide as to

the total volume of investment financing required. In the near future, ESS will consult with FAO

member countries to determine how best to build these country-level investment profiles.

b. CREDIT TO AGRICULTURE

GEA 0.3%

FDI-agri 3.2%

ODA 0.2%

Private Equity

62.3%

Credit - Agri 34%

Figure 3: Agricultural Capital Formation in Bangladesh 2007, (Total = $6,227 million USD)

* Private Equity estimated as a residual (PE = ACS - GEA - ODA - FDI - Credit)

RAP/APCAS/14/13.2

13

The extent to which formal private sector credit markets provide investment financing has a

direct and positive correlation with growth in agricultural capital stock, and in turn, with

agricultural productivity growth. This occurs because financial institutions in formal credit

markets are better able to diversify and absorb risks across time, across borrowers, and across

sectors, thereby lowering financing costs to borrowers, and better allocating savings. This source

of financing is of particularly importance in sectors, such as agriculture, where producers face

high risks not only in terms of the timing between the need to finance investments and the

realization of income to repay loans, but also from the significant supply-side uncertainties that

arise from climate and weather conditions (droughts, floods, etc), price volatility of their output,

and the impact of pests and disease, which affect the volume and quality of their output.

Data on formal credit extended to agriculture ― including finance to corporations and firms

for onward financing to farmers, agricultural cooperatives and agri-related businesses ― is

generally available through monetary and financial statistics. This data, which serves as a

benchmark indicator of formal domestic private sector investment activity, is being developed by

FAO’s Statistics Division into a comprehensive credit to agriculture dataset, harvesting official

data from Central Banks websites. Data challenges exist for countries that lack legislative

reporting requirements for this type of data, or where reported data lack the necessary level of

sector detail. Across all countries, a significant challenge also exists in differentiating agricultural

loans for investment purposes, and those for consumption purposes.

c. GOVERNMENT EXPENDITURES ON AGRICULTURE

Although the private sector mobilizes most investment financing in agriculture, the public

sector ― general government units and public (financial and nonfinancial) corporations ― also

plays a role. The efficiency of these expenditures, whether measured in relation to agricultural

GDP, to total government outlays, or the agricultural labour force, remains a key element of the

overall policy mix. Well targeted government expenditures can create a conducive environment

for private investment (economic incentives) and can ensure sufficient availability of public goods

(basic rural infrastructure and market openness), particularly when these investments address

market failures.

The share of government expenditures on agriculture (GEA) is not related in any simple way

to the size of the agricultural sector, and depends inter alia on the overall importance given to

economic functions in governments’ budgets. By bringing together the data on agriculture's shares

in GDP and overall government expenditure we can construct an "agricultural orientation index"

by dividing the agricultural expenditure share of total government expenditures by the agriculture

RAP/APCAS/14/13.2

14

share of GDP, which reflects the relative importance that government places on its agricultural

sector. In Bangladesh, for example, the agriculture share of GDP was significantly higher than

the agricultural share of government expenditures (Figure 4), leading to an agricultural orientation

index up to 5% from 2001 to 1007, rising steadily to 15% in 2011 following the food price crisis.

Despite the need for comprehensive time series data on government expenditures on

agriculture and rural development, such data remain scarce. To address this gap and ensure

comparable data aligned with international standards, ESS, in collaboration with the IMF

Statistics Department, developed a Government Expenditures on Agriculture questionnaire based

on the Government Finance Statistics Manual, 2001 (GFSM 2001) methodology. ESS launched

this questionnaire globally in 2012, requesting additional detail on the agriculture subsectors of

agriculture, forestry and fisheries, as well as data on environmental protection. The questionnaire

also looks for additional detail on recurrent and capital expenditures, in order to proxy the amount

of expenditures allocated for investment. The second annual global data collection is currently

underway.

.

d. OFFICIAL DEVELOPMENT ASSISTANCE TO AGRICULTURE

Official Development Assistance to Agriculture (ODA) from major bilateral and multilateral

donors is an important complement to domestic sources of agricultural financing. To obtain this

data, ESS harvests data from the OECD’s Creditor Reporting System (CRS), which records ODA

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0%

5%

10%

15%

20%

25%

30%

35%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Figure 4: Government Expenditure on Agriculture - Bangladesh

GEA as % of Total Government Outlays (Left Axis)

Agriculture Value Added as % of GDP (Left Axis)

Agricultural Orientation Index (Right Axis)

RAP/APCAS/14/13.2

15

and Other Official Flows (OOF) at the project level. By extracting the subset of the data relevant

for agriculture, rural development and food security, ESS is able to obtain necessary data without

creating duplication across international organizations, or imposing additional response burden on

countries. Where data gaps exist, ESS will work with the OECD to identify and address these

gaps. The first comprehensive ODA to agriculture data will be available in FAOSTAT in the near

future.

e. FOREIGN DIRECT INVESTMENT

A fourth source of agricultural investment financing comes from foreign direct investment

(FDI). A host of factors, including spikes in food and fuel prices, a desire by countries dependent

on food imports to secure food supplies in the face of uncertainty, and speculation on land and

commodity price increases, recently prompted a sharp increase in investment involving significant

use of agricultural land, water, and forested areas in developing and transition countries. In the

coming year, ESS will work with data from UNCTAD to develop a database on FDI to

agriculture, and examine data gaps and challenges, along with strategies to address them.

f. FOREIGN REMITTANCES

A fifth source of investment financing comes from foreign remittances, or the money sent to

home countries by migrants. Last October the World Bank estimated that developing countries

would receive $414 billion US in foreign remittances in 2013, an increase of 6.3% over the

previous year. To put this in perspective, foreign remittances to Tajikstan would account for half

of its GDP, and for three times the FDI to India, which received $71 billion in remittances. As

such, foreign remittances are important due to their size, but also because they act as an automatic

economic stabilizer, rising in value when domestic currency weakens. A challenge that faces ESS

in including this source of investment financing is the determination of the share goes towards

financing agriculture, and the subset that finances agricultural investment.

6. INVITATIONS TO APCAS MEMBER COUNTRIES

APCAS member countries are requested to provide comments and feedback on these existing and

new lines of work, and suggestions on improvements and opportunities for collaboration in the

domains of price and investment statistics.

Questions, inputs and advice can be e-mailed to Ms. Dubey ([email protected]),

Franck Cachia ([email protected]) or Fabiana Cerasa ([email protected])