asas perbankan islam - produk deposit

TRANSCRIPT

Produk Patuh Syariah

Differences Between Differences Between IslamicIslamic & Conventional & Conventional BankingBanking

Differences Between Differences Between IslamicIslamic & Conventional & Conventional BankingBanking

Islamic Banking Islamic Banking Restrict ionsRestrict ionsIslamic Banking Islamic Banking Restrict ionsRestrict ions

Contracts In Contracts In IslamicIslamic Banking BankingContracts In Contracts In IslamicIslamic Banking Banking

IslamicIslamic Deposit Product Deposit ProductIslamicIslamic Deposit Product Deposit Product

IslamicIslamic Financing Product Financing ProductIslamicIslamic Financing Product Financing Product

Implication of Implication of NonNon ShariahShariah Compliant CompliantImplication of Implication of NonNon ShariahShariah Compliant Compliant

Most Common Most Common Mistakes !Mistakes !Most Common Most Common Mistakes !Mistakes !

11

22

33

44

55

66

77

Differences Between Differences Between IslamicIslamic & Conventional & Conventional BankingBanking

Differences Between Differences Between IslamicIslamic & Conventional & Conventional BankingBanking

Islamic Banking Restrict ionsIslamic Banking Restrict ions

Contracts In Islamic BankingContracts In Islamic Banking

Islamic Deposit ProductIslamic Deposit Product

Islamic Financing ProductIslamic Financing Product

Implication of Non Shariah CompliantImplication of Non Shariah Compliant

Most Common Mistakes !Most Common Mistakes !

11

ISLAMIC & CONVENTIONAL ISLAMIC & CONVENTIONAL BANKING BANKING

ISLAMIC & CONVENTIONAL ISLAMIC & CONVENTIONAL BANKING BANKING

CONVENTIONALCONVENTIONALISLAMIC BANKINGISLAMIC BANKING

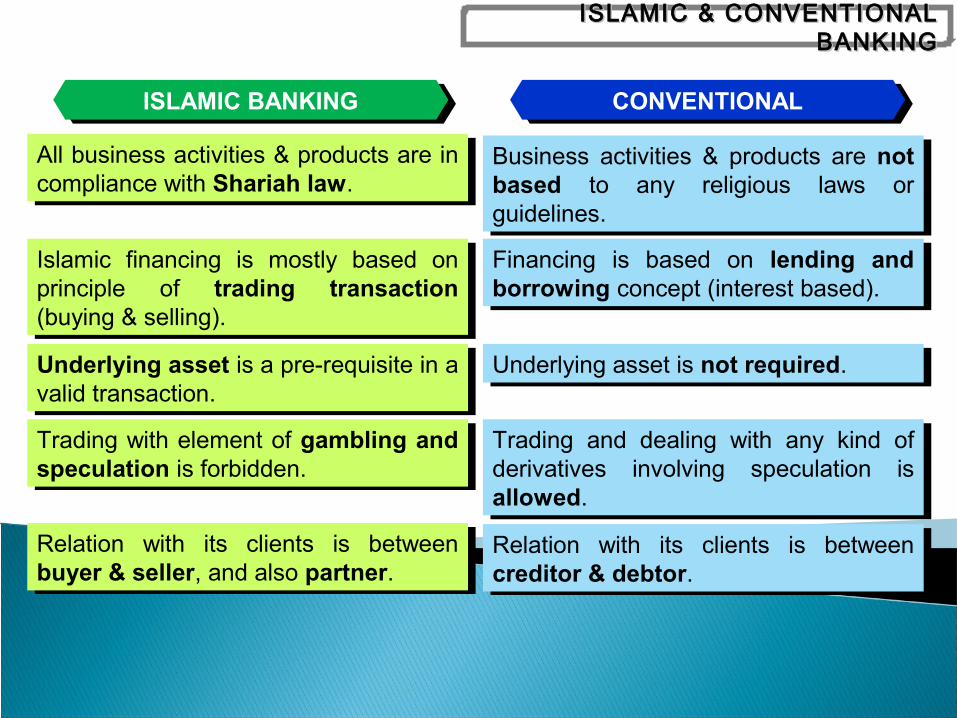

All business activities & products are in compliance with Shariah law.

All business activities & products are in compliance with Shariah law.

Business activities & products are not based to any religious laws or guidelines.

Business activities & products are not based to any religious laws or guidelines.

Islamic financing is mostly based on principle of trading transaction (buying & selling).

Islamic financing is mostly based on principle of trading transaction (buying & selling).

Financing is based on lending and borrowing concept (interest based).

Financing is based on lending and borrowing concept (interest based).

Underlying asset is a pre-requisite in a valid transaction.

Underlying asset is a pre-requisite in a valid transaction.

Underlying asset is not required.Underlying asset is not required.

Trading with element of gambling and speculation is forbidden.

Trading with element of gambling and speculation is forbidden.

Trading and dealing with any kind of derivatives involving speculation is allowed.

Trading and dealing with any kind of derivatives involving speculation is allowed.

Relation with its clients is between buyer & seller, and also partner.

Relation with its clients is between buyer & seller, and also partner.

Relation with its clients is between creditor & debtor.

Relation with its clients is between creditor & debtor.

ISLAMIC & CONVENTIONAL ISLAMIC & CONVENTIONAL BANKINGBANKING

Differences Between Islamic & Conventional Banking

Differences Between Islamic & Conventional Banking

Islamic Banking Islamic Banking Restrict ionsRestrict ionsIslamic Banking Islamic Banking Restrict ionsRestrict ions

Contracts In Islamic BankingContracts In Islamic Banking

Islamic Deposit ProductIslamic Deposit Product

Islamic Financing ProductIslamic Financing Product

Implication of Non Shariah CompliantImplication of Non Shariah Compliant

Most Common Mistakes !Most Common Mistakes !

22

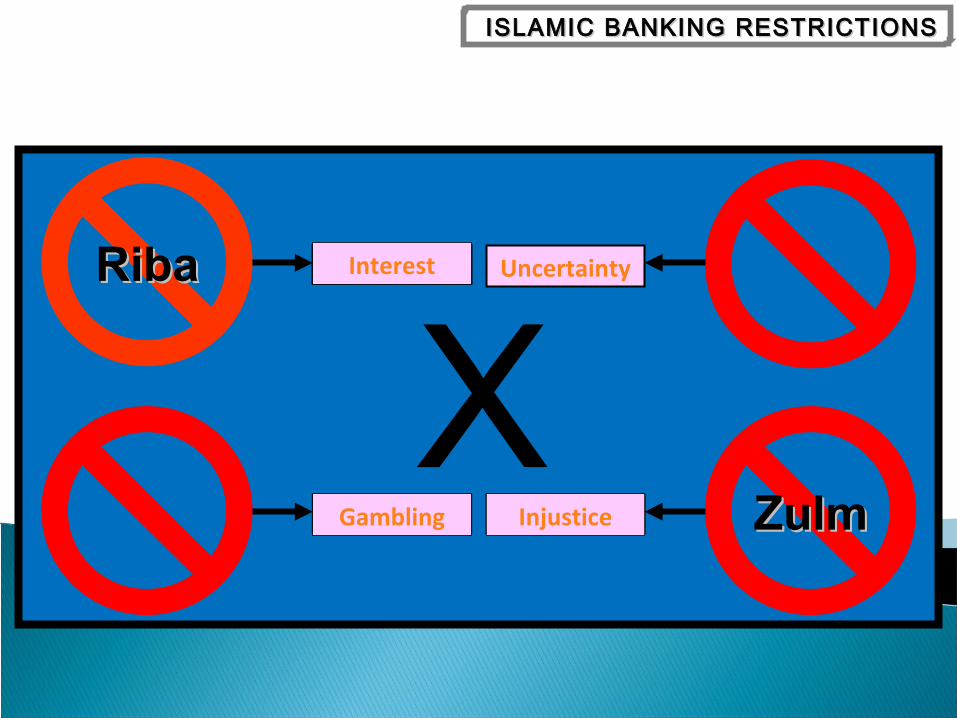

ISLAMIC BANKING ISLAMIC BANKING RESTRICTIONRESTRICTION

ISLAMIC BANKING ISLAMIC BANKING RESTRICTIONRESTRICTION

GhararGhararUncertainty

XMaysirMaysir__________ ZulmZulm__________

RibaRiba __________Interest

Gambling Injustice

ISLAMIC BANKING RESTRICTIONSISLAMIC BANKING RESTRICTIONS

Differences Between Islamic & Conventional Banking

Differences Between Islamic & Conventional Banking

Islamic Banking Restrict ionsIslamic Banking Restrict ions

Contracts In Contracts In IslamicIslamic Banking BankingContracts In Contracts In IslamicIslamic Banking Banking

Islamic Deposit ProductIslamic Deposit Product

Islamic Financing ProductIslamic Financing Product

Implication of Non Shariah CompliantImplication of Non Shariah Compliant

Most Common Mistakes !Most Common Mistakes !

33

CONTRACTS IN ISLAMIC CONTRACTS IN ISLAMIC BANKINGBANKING

CONTRACTS IN ISLAMIC CONTRACTS IN ISLAMIC BANKINGBANKING

3 Categories of Contracts in Islamic Banking3 Categories of Contracts in Islamic Banking

joint ventureMudharabah cost plus sale

Bai’ Bithaman Ajil

Bai’ InahBai’ Dayn

agency

CONTRACTS IN ISLAMIC BANKINGCONTRACTS IN ISLAMIC BANKING

Differences Between Islamic & Conventional Banking

Differences Between Islamic & Conventional Banking

Islamic Banking Restrict ionsIslamic Banking Restrict ions

Contracts In Islamic BankingContracts In Islamic Banking

IslamicIslamic Deposit Product Deposit ProductIslamicIslamic Deposit Product Deposit Product

Islamic Financing ProductIslamic Financing Product

Implication of Non Shariah CompliantImplication of Non Shariah Compliant

Most Common Mistakes !Most Common Mistakes !

44

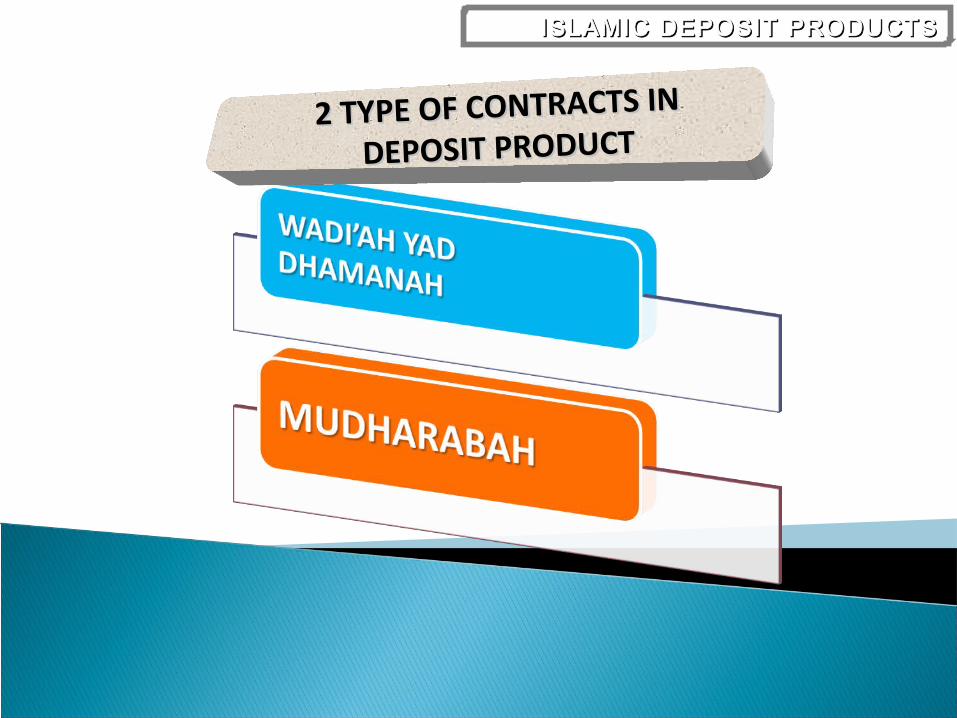

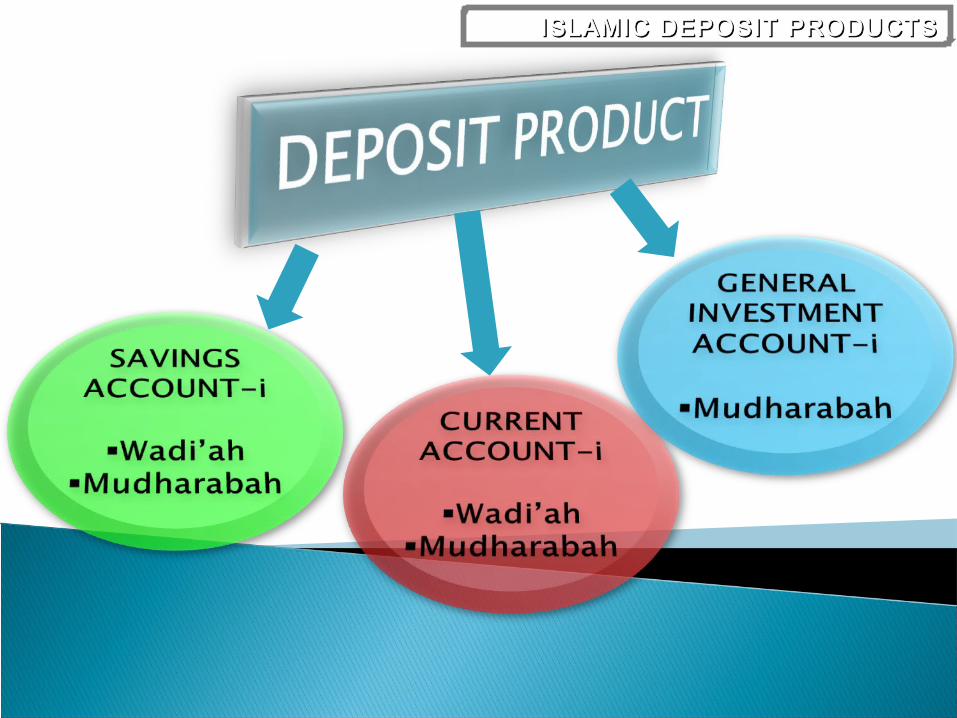

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

2 TYPE OF CONTRACTS IN 2 TYPE OF CONTRACTS IN

DEPOSIT PRODUCTDEPOSIT PRODUCT

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

16

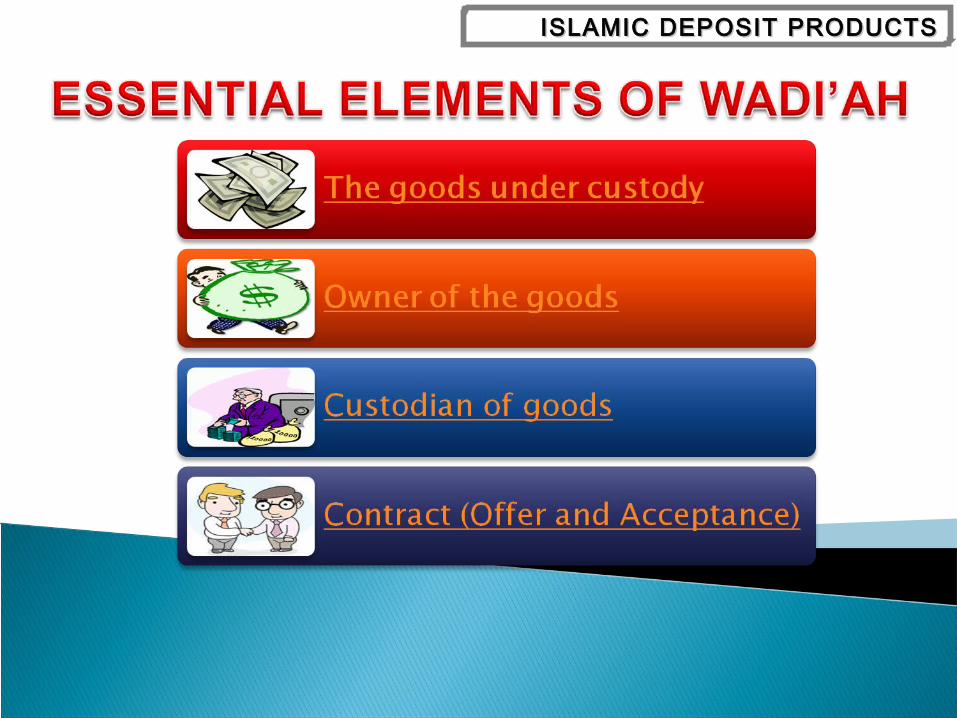

WADI’AH YAD DHAMANAH(Guaranteed Safe Custody)WADI’AH YAD DHAMANAH(Guaranteed Safe Custody)

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

HIBAHHIBAH

1. A authorises B to safekeep his goods / moneyA grants B to utilise the money

2. B utilize the money in business / project3. All the profit earned belongs to B4. B can give Hibah (gift) to A based on his discretion

AA

BB

13

2

PROFIT100 %

WADI’AH YAD DHAMANAH(Guaranteed Safe Custody)WADI’AH YAD DHAMANAH(Guaranteed Safe Custody)

4

BUSINESS

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

CURRENT / SAVINGS ACCOUNT-i

WADI’AH YAD DHAMANAHWADI’AH YAD DHAMANAH

* Yellow indicate Shariah principle being applied

1. Customer deposit money with Bank for the purpose of safekeeping & convenienceCustomer grants Bank to utilize the money

2. Bank utilize the money in investment / financing3. All the profit generated belongs to Bank4. Bank give Hibah (gift) to Customer as a token of appreciation based on its discretion

BANK (Custodian)

CUSTOMER (Owner of Fund)

HIBAHHIBAH

3 100 %

4

PROFIT

INVESTMENT

2

1

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

The banks safekeep the money and pays it back to depositor in demand.

Banks does not promise a fixed return, but has discretion to provide depositors with hibah (gift).

Banks is allowed to utilise the fund.

CURRENT / SAVINGS ACCOUNT-i

WADI’AH YAD DHAMANAHWADI’AH YAD DHAMANAH

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

21

MUDHARABAH(Profit Sharing & Loss Bearing)

MUDHARABAH(Profit Sharing & Loss Bearing)

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

LOSS

1. A authorises B to invest his funds based on Mudharabah contract2. B invests the fund in business / project3. Profit will be shared between fund provider and entrepreneur /

Loss will be borne only by fund provider

AA

BB

MUDHARABAH(Profit Sharing & Loss Bearing)

MUDHARABAH(Profit Sharing & Loss Bearing)

1 3

2BUSINESS

PROFIT

BusinessOutcomeX %

Y %

100%

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

1. Customer deposit money with Bank and authorises Bank to invest his funds with agreed PSR (e.g 30:70) based on Mudharabah contract

2. Bank invests the fund in investment or financing3. Profit will be shared between Bank and Customer /

Loss will be borne only by Customer

BANK (Entrepreneur)

CUSTOMER (Capital Provider)

LOSS1 3

2

INVESTMENT

PROFIT

BusinessOutcomeX %

Y %

100%

CURRENT / SAVINGS ACCOUNT-i, GIA-i

MUDHARABAHMUDHARABAH

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

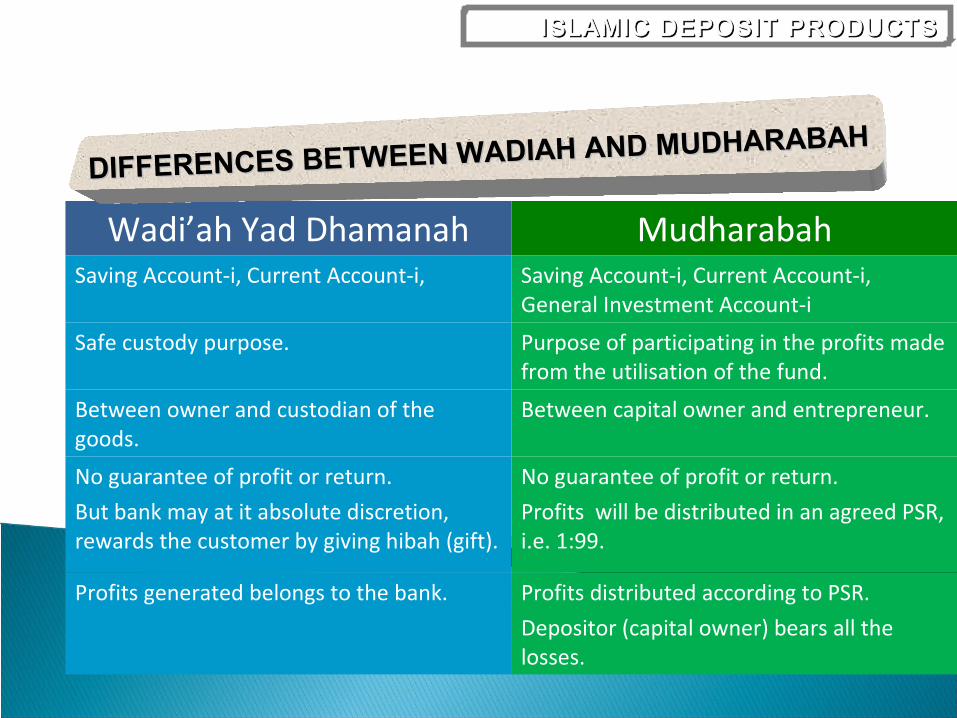

Wadi’ah Yad Dhamanah MudharabahSaving Account-i, Current Account-i, Saving Account-i, Current Account-i,

General Investment Account-i

Safe custody purpose. Purpose of participating in the profits made from the utilisation of the fund.

Between owner and custodian of the goods.

Between capital owner and entrepreneur.

No guarantee of profit or return.

But bank may at it absolute discretion, rewards the customer by giving hibah (gift).

No guarantee of profit or return.

Profits will be distributed in an agreed PSR, i.e. 1:99.

Profits generated belongs to the bank. Profits distributed according to PSR.

Depositor (capital owner) bears all the losses.

DIFFERENCES BETWEEN WADIAH AND MUDHARABAHDIFFERENCES BETWEEN WADIAH AND MUDHARABAH

ISLAMIC DEPOSIT PRODUCTSISLAMIC DEPOSIT PRODUCTS

Differences Between Islamic & Conventional Banking

Differences Between Islamic & Conventional Banking

Islamic Banking Restrict ionsIslamic Banking Restrict ions

Contracts In Islamic BankingContracts In Islamic Banking

Islamic Deposit ProductIslamic Deposit Product

IslamicIslamic Financing Product Financing ProductIslamicIslamic Financing Product Financing Product

Implication of Non Shariah CompliantImplication of Non Shariah Compliant

Most Common Mistakes !Most Common Mistakes !

55

Q & A Q & A