articles - icab.org.bd ltd and islami bank bangladesh ltd have been adjudged as the winners in the...

TRANSCRIPT

January - March 2013

BAN

K AU

DIT: H

OW

MU

CH

IS ENO

UG

H!

January - March 2013

Bank AuditHow much is Enough?

Editorial 2President’s Desk 3

ARTICLESGreen Banking and Sustainable Development: 5the Case of Bangladesh- Atiur Rahman Ph.D

Bank Audit – How Much should it be enough; 9in light of relevant Auditing Standards andAuditing Practice Statements- Sabbir Ahmed FCA

Audit of Local and International 15Commercial Banks:an overview of Practices and Procedures- M Jalal Hussain FCA

Profitability Trend in the Banking Sector of 22Bangladesh- a Comparative Study ofIslamic and Conventional Banks- Ishter Mahal1

- Benazir Rahman2

Laws and regulations for accounting system 36- Md Shahadat Hossain FCA

Recent Monetary Policy & Economic Trends 41- Ahmad Dawood FCA, FCMA

National Finance Performance & Stability 49- an Analysis to Reform & Retreat with Integrated Policy- Dipok Kumar Roy ACA

A Tribute to Late Mufazzal Hossain 71Chowdhury FCA- Parveen Mahmud FCA

Preparing Accountants for Future Challenges 77- ICAB President’s interview with the Daily Star

Proposals from ICAB on National Budget 792013-14

CONTENTS ISSN 1993-3649

"The opinions expressed in this publication are those of the respective authors themselves and do not necessarily reflect the views of the Editorial Board of the Institute of Chartered Accoun-tants of Bangladesh (ICAB) or the ICAB itself."

DISCLAIMER

Md. Abdus Salam FCAGopal Chandra Ghosh FCAAkhtar Sohel Kasem FCAMasih Malik Chowdhury FCANasir Uddin Ahmed FCASabbir Ahmed FCAMd. Sayeed Ahmed FCAMahmudul Hasan Khusru FCAMd. Abu Bakar FCAMd. Mahamud Hosain FCAMohammed Jashim Uddin FCASnehasish Barua FCAAjit Kumar Paul FCAMd. Abid Hossain Khan FCAMuhammmad Aminul Hoque ACAZareen Hosein ACAMd. Shahidul Islam ACADipok Kumar Roy ACAChairman DRC-ICABChairman CRC-ICAB

S M Abu Nayem Ahmed, pscSqn Ldr (Retd.)Senior Deputy Secretary-ICAB

EDITORIAL BOARD

ORIALEDIT

As the technological improvements and competitive environment changes, so is the risk of financial markets and economic fraud all around the world. As an answer to these new threats, the need to ensure transparent accounting and reporting standards cannot be overstated for the overall economic success of a country. To cope up, auditors need to adapt with the rapidly changing banking industry and the present concerns including: continuous auditing, regulatory changes, fraud, Enterprise Risk Management, social media and internet risks. Inview of this, the issue would offer an opportunity to gain insights into the current hidden and unknown facts and anomalies centering Bank that is haunting public perception with a sense of insecurity. The issues are not unknown to the world history. The best recognized bank offered best report even gave rise to corporate fraud shaking the country's financial sector. For our country, the dimension may vary compared to other modern economy. We tend to forget once it is over. The real perpetrator sometimes remains beyond touch.

On the recent financial irregularities of some

January - March 2013 The Bangladesh Accountant2

M. Farhad Hussain FCAChairman, Editorial Board

Companies; the issue has come forefront. It is surprising that how a company misappropriated more than Tk 2,500 crore from a Bank. The bank’s internal audit department could not spot any irregularity. This could have been otherwise, if the Banks would appoint the right professional in their branches. On the other hand, many thought that it is not possible to audit all the offices or branches of an office, company or bank. The audit is done randomly, on a risk-weighted basis. So, one is ikely to ponder about the process of bank audit; what and how much is feasible?

It is imperative to think about ‘Bank’s Audit in the present context as it is experiencing rising trend of financial frauds. The depositors are likely to lose their confidence in the banks as some major of irregularities in the banking sector has recently been surfaced by the newspapers’ and electronic media reports. New banks are in the line. In this context, the banks’ audit reports are considered very important to seal the possibility of recurrence of such misappropriation and to bring back people’s confidence.

As we know, in the present free trade market economy, the banking sector is the backbone of economy. Bank is the media to accelerate the trade and commerce including export and import of the country. In the global context, the role of banks is far-reaching and more penetrating in the economic

arena more than that of past. Bangladesh has a mixed banking system. Different types of audits have been carried out in the banks considering auditing rules. Every country has specific laws, rules and regulations on Banking Company. Generally, the Auditors follow the local and international standards and guide lines while conducting an audit of a bank. Recently, the Cabinet approved in principle the draft of the Bank Company (Amendment) Bill, 2013. I believe, it will strengthen the country's banking system. It is true that the Banks are facing unprecedented change in technology and regulation, Social networking, eBanking and regulatory reform are just a few of the current challenges bank auditors must tackle. Critical to the auditor’s ability to deal with these changes is probably a flexible audit plan and right input from management. Failure to deal with the malpractices can be fatal for the financial health of the country.

In fine, I would, as usual, look forward to feedbacks from our esteemed readers, the valuable suggestions and opinions would greatly help to add the quality of our journal.

Instilling more Trust

and Confidence

The Bangladesh Accountant January - March 2013 3

PRESIDENT’S DESK

As I take over the presidency, I consider it to be a sacred duty to uphold the interests of the Profession and contribute to the Accounting and private sector Auditing. We cannot stop till we get the result, we expect. To hold the continuity of our progress and advancement, I will not leave any dearth of my effort to discharge my function as the President of the Institute. I must be able to do justice to the trust and confidence bestowed upon me by the members.

In this quarter, I raised different pending issues with the Minister/Secretary/Officials of Regulatory Bodies and convey different contentious issues to them like utilization/ engagement of more Chartered Accountants in different Division/Bodies/Projects under the Ministries, allocation of land for ICAB Academic Campus, approval of the ICAB submitted Project proposal lying in the Planning Commission, engaging more Chartered Accountants in the banking sector etc. We pointed out contradiction between IFRSs & IASs and Bank Company Act, 1991 & some BRPD circulars of Bangladesh Bank which is required to be amended for the sake of exercising sound accounting practices in Bangladesh.

According to the proposal of Mr.

Wilson Vargheso, Senior Economist, Monetary and Capital Markets Development, Technical Assistance Division, International Monetary Fund (IMF), ICAB is working closely with Bangladesh Bank for the sake of strengthening the internal control of the central bank to arrange at least 6-months training for newly qualified CAs in Bangladesh Bank and other commercial banks to attract more CAs in the banking profession, encourage Bangladesh Bank to prefer accounting background professionals during their new recruitment etc. We truly believe that CA firms can play a significant role in thorough auditing the functions of the branches of the banks. It will undoubtedly, bring good result, if we could involve the adequate number of Chartered Accountants, aiming towards minimizing embezzlement/fraudulence.

As part of their expression of trust and confidence on ICAB, the NBR officials in this year also continued to take training on “Tax Audit for Tax Officials” for 5th batch and 6th batch in the month of January 2013 under the TACTS project in collaboration with DFID, a UK based development assistant partner. As we keep extending our good wishes and expertise cooperation, ICAB conducted

Training on ‘IFRS and IAS for Bangladesh Bank officials’ in the month of February and March 2013. ICAB, first time of its kind, organized this training and a total of 35 mid level Bangladesh Bank Officials Comprising Joint Directors, Deputy Directors and Assistant Directors participate in the training. Topics ranging from Financial Reporting, Financial Statements, Accounting Policy, Statement of Cash Flow and Adaptation of International Financial Reporting Standards are interacted on the 25-days training programme. ICAEW ACA Advanced Stage Classes, first time in Bangladesh held in the first quarter of 2013. We were encouraged that 32 ICAB Members registered to undergo these classes.

As we hold our ties with the ICAEW, a learning partner of ICAB, we met ICAEW high officials and sought ICAEW’s support for strengthening our ties under World Bank financed Twinning Project on a range of issues like Updating the Curriculum of ICAB and Study Materials, ICAB Case Study Exam, arrangement of Workshop, updates of ICAB-ICAEW, joint Online IFRS Training and Certificate Programme, arrangement of tuition facilities for ICAB Members registered with ICAEW, publication of ICAEW

Md Abdus Salam FCAPresident, ICAB

January - March 2013 The Bangladesh Accountant4

Advanced Stage Study Manuals etc.

It is a matter of great pride that in the prestigious recent SAFA BPA Awards, beside other prizes, IDLC Finance Ltd and Prime Bank Ltd of Bangladesh won the first and second prize respectively on 'overall categories', while, Rupali Bank Ltd and Islami Bank Bangladesh Ltd have been adjudged as the winners in the category of 'Public Sector Banking Institutions' and 'SAARC Anniversary Awards for Corporate Governance', respectively. IDLC Finance Limited and Prime Bank Limited were adjudged as an ‘Overall Winner’ along with Sri Lanka Telecom. A total of 85 awards were given out, while Bangladesh won 19 awards and the remaining awards were shared between companies from India, Pakistan, Sri Lanka and Nepal. This is a manifestation of ICAB's sincere commitment which is paying dividend for holding the Best Annual Report, which is scrutinising and thereby best of the best receiving the SAFA Awards.

To heighten the professional image, I, as President of the

Institute, took the opportunity to speak on the country perspective of the theme 'Professionalism as a Tool to Economic Growth' in the ICAI International Conference titled “Accountancy Profession: Enablers of Economic Growth' hosted by Indian Institute.

ICAB is well aware of its true responsibility; the Institute submitted its primary observation on ‘Draft Company Bill 2013’ to the Ministry of Commerce of the Govt. of Bangladesh on 25 March 2013. ICAB Experts Team reviewed new ‘Draft Company Bill 2013’ prepared in Bengali and identified some clauses which would create complexity and broaden cost of business. ICAB also was critical that this might leave negative impact on the overall economic activities of the country, if enforced. ICAB team also identified some clauses of the new Act to be in duplication/contradictory to the existing laws/laws.

ICAB holds Continuation of training of its members on the urgent issues like ‘Harmonization of Financial Reporting and Audit Practices: Bangladesh Perspective’ in

February, 2013. ICAB organized a Members’ Conference titled ‘Harnessing Technology in CA Firms’ in February . Mr. Guru Parasad, Partner, Guru and Jana, Chartered Accountants, India, in his presentation described how to use the new information technology in CA Firms and projected some common delivery models for many business applications like customer Relation Management (CRM), Management Information Systems (MIS), Enterprise Resource Planning (ERP), Invoicing, Human Resource Management (HRM), Content Management (CM) and Service Desk Management. A CPD Seminar on ‘Recent Monetary Policy & Economic Trends’ was held in March 2013 by ICAB Chittagong Regional Office.

Now, let me be frank with all to acknowledge that the unrest and political impasse is harnessing us to take our activities in full swing. However, I re-assure that the path of progress and advancement; building more trust and confidence will not stop till we achieve our purpose.In fine, I hope that this issue of the journal addressed much needed issue, though sensitive one, to the readers and anyone reading it would be tremendously benefitted, undoubtedly.

I thank everyone associated with this publication.

The development strategies of Bangladesh Government, as laid down in the Perspective Plan and the Sixth Five Year Plan, clearly spell 'out the commitment of pursuing sustainable growth. The country's vulnerability to floods, cyclones and to the threat of inundation of large coastal areas from global warming driven sea level rise makes sustainability a prime development concern.

Over the past 4 decades since liberation, national income of Bangladesh has increased more than eighteen-fold, while the population has increased a little over two-fold. Real GDP growth averaged at around 6.0 percent annually over the last 10 years. Trade openness has integrated Bangladesh with global economy with trade/GDP ratio rising from around 20.0 percent during the 1970s and 1980s to more than 60 percent in FY12. Poverty has come down to around 30 percent of the population now, from around 57.0 percent in the 1990s.

As you all are aware that Bangladesh falls into the group of most climate change vulnerable countries in the world despite her insignificant share of global greenhouse gas (GHG) emission in comparison with other developing and developed countries. However,

Green Banking and Sustainable Development:the Case of Bangladesh

Atiur Rahman Ph.D

Bangladesh has made notable contribution towards establishing 'Green Climate Fund' alongside documenting the Renewable Energy Policy in 2008 & Environmental preservation Act in 1997. Accordingly, the government of Bangladesh has decided to produce 5 percent of total power generation from renewable energy sources like solar energy, air & waste by 2015 & 10 percent by 2020 with the above Policy & Act. To protect our environment from industrial pollution a guideline is formulated under this act, which requires Effluent Treatment Plant mandatory for those Industries that emit liquid effluent. Around 60 percent people in Bangladesh are outside of the electricity facility while around 90 percent are outside of the natural gas network. Renewable energy, especially solar energy and biogas can provide a sustainable and environment friendly solution to reduce the demand-supply gap of energy in the country.

BB has issued guidelines for environmental risk management and green banking in 2011 and is probably the only central bank, which has issued such an indicative guideline for green banking. The guidelines aim to ensure environment friendly business practices by banks and financial institutions, to incorporate environmental risks into Core Risk Management (CRM) and to promote

The Bangladesh Accountant January - March 2013 05

BB FORMULATED

GREEN BANKING POLICY

GUIDELINE IMPLEMENTED

IN 3 PHASES FROM 2011 TO

2013. BY FOLLOWING THESE

GUIDELINES, BANKS WILL

BENEFIT IN TERMS OF

IMPROVED CAMELS

RATING. BESIDES, BB WILL

DECLARE THE NAMES OF

THE TOP 10 BANKS

REGARDING THEIR

OVERALL PERFORMANCE IN

GREEN BANKING

ACTIVITIES AND WILL

ACTIVELY CONSIDER

GREEN BANKING

ACTIVITIES OF BANKS

WHILE ACCORDING

PERMISSION FOR OPENING

NEW BRANCH.

sustainable financial and economic growth. Bangladesh Bank has also issued a common format to all the commercial banks to report green banking activities including the extent of carbon footprint in a structured way. Banks and financial institutions enthusiastically responded to this 'Green Banking' drive. Now they regularly submit a quarterly report to Bangladesh Bank on their performance of green banking activities.

BB formulated green banking policy guideline implemented in 3 phases from 2011 to 2013. By following these guidelines, banks will benefit in terms of improved CAMELS rating. Besides, BB will declare the names of the top 10 banks regarding their overall performance in green banking activities and will actively consider green banking activities of banks while according permission for opening new branch. BB has decided to accord permission for SME branch subject to installation of solar panel in

January - March 2013 The Bangladesh Accountant06

place. Banks will also receive separate treatment in existing guidelines for Environmental Risks in computation of Adequate Capital by BB. To promote green energy, BB advised banks to facilitate clients to open L/Cs for installation of ETP in industrial units, to finance Solar Energy, Biogas and ETP projects, to comply with CSR guidelines for ingraining environmentally and socially responsible practices with the instructions stipulated in Green Banking Policy.

Besides these, BB introduced a Refinance Scheme (revolving) for Solar Energy, Biogas, and Effluent Treatment Plant (ETP) of Taka 200 Crore in August 2009. From this revolving fund, refinance facilities are allowed for banks/FIs against lending in the Solar Energy, Biogas Treatment Plant sectors on terms and conditions set forth in a BB's ACSPD Circular. By now, 27 banks & 1 Financial Institution have signed the participation agreement with BB to

The Bangladesh Accountant January - March 2013 07

avail the refinance facility for Solar Energy, Biogas & Effluent Treatment Plant. As per another ACD Circular, refinances were allowed at limited scale up to Taka 300 million from this fund to establish Hybrid Hoffman Kiln (HHK)/equivalent technology in brick manufacturing industry with a view to reduce carbon & suspended particulate matter in the atmosphere.

Notwithstanding the insignificant amount relative to the overall country's demand, the achievements of green banking in the renewable energy sector are worth mentioning.

As of December 2012:

• An amount of Tk. 103.72 million has been disbursed under the refinance program of Solar Home System (SHS) to establish 3763 units SHS. These solar home systems are situated at off-grid areas of the country benefiting at least 3763 families with the production capacity is 164100 KW/day.

• An amount of Tk. 23.9 million disbursed for 8 solar energy driven irrigation pumps. No. of

beneficiary farmers are 618 and bringing 920 bighas of land under cultivation with uninterrupted water flow enhancing the productivity and cropping intensity. Besides, an amount of Tk. 248.80 million disbursed for establishing Solar PV Module Assembly Plant. In the sub sector of Integrated Cow Rearing and Biogas Plant, an amount of Tk. 262.13 million refinanced in 820 numbers of Integrated Cow Rearing and Biogas plant.

• An amount of Tk 90.36 million disbursed for establishing 8 ETP with effluent treatment capacity of 18000 cubic meter per day contributing significantly in limiting environmental pollutions, while an amount of Tk. 124.47 million disbursed for establishing Hybrid Hoffman Kiln (HHK) technology in 3 brick manufacturing industries which reduces carbon emission in the brick manufacturing plants.

I would like to take this opportunity to share the green initiatives taken by BB. The central bank of Bangladesh is responding to climate change in a diverse of

ways. With a move towards encouraging green banking in Bangladesh, BB installed a 8-kilowatt solar power system on its rooftop in March 2010, which has been providing necessary energy supply for the executive floor along with emergency security lights in the BB premises. This is now being extended to cover more areas. A recent initiative has been taken to convert the 30-storied building of the bank into a 'Green Building' with the modern facilities of rain water harvesting, waste water recycling and motion sensor energy efficient bulbs supported by window based solar panels. Besides, BB is arranging an international conference on 'Green Banking' jointly with IFC in March 2013 in line with the outcome document of Rio+20 called 'The Future We Want," and COP meetings of the UNFCCC, especially COP 18 including the 'Kyoto Protocol' in combating various vulnerabilities due to climate change.

Bangladesh Bank has been working for last four years to establish a completely IT based banking system in the country. Various IT based initiatives of BB have been helping to move

January - March 2013 The Bangladesh Accountant08

The Author is the Governor,Bangladesh Bank

towards the paperless green banking. In view of ensuring low-carbon green development without compromising the imperative of faster economic growth and social development, IT infrastructure of the financial sector has undergone vast improvements in recent years. It has been facilitating countrywide automated online connectivity of banks with the BB for supervisory reporting, National Payments Switch and fully automated inter bank clearing and settlement platforms for paper based and electronic fund transfers, and a credit information bureau accessible online by users.

Despite all these achievements, the prospect of achieving sustainable development is not free of challenges. Future challenges include formulation of sector specific environment polices, coordination among concerned authorities to build up a green economy, speeding up proper awareness and effective capacity building, application of quantitative approach for more justified ratings of banks. We envision Bangladesh as a mature advanced economy in 2050, with levels of human development and technological advancement sufficient to place her among

leading Asian nations in terms of financial prosperity as well as social and environmental responsibility.

To conclude, I would like to thank the organizer for initiating the discussion on such an important issue like green banking. I hope you all will have very productive deliberations and find this seminar very useful.

(The Article was presented in a seminar on 02 February 2013)

Introduction

I would like to start this article with a very famous quote that came to my attention many years ago while reading an interview of a Global Bank’s CEO. The quote I am referring here is “Banking is such a unique industry where you do not want your competitor to fail”. Honestly speaking it did not make much sense at that time. However, after working as a professional accountant for many years the perspective of the comment is quite vivid. Why it is so that a Bank would not like to see his fellow competitor Bank to fail? The simplest and shortest answer is “Banking business is based on Trust” and failure of a Bank severely dents that Trust and it affects not only other Banks but the whole economic systems bears the brunt.

It is an undeniable fact that Banks play a central role in the economy. They hold the savings of the public, provide a means of payment for goods and services and finance the development of business and trade. To perform these functions securely and efficiently, individual banks must command the confidence of the public and those with whom they do business. The stability of the banking system, both nationally and internationally, has therefore come to be recognized as a matter of general public interest. This

Bank Audit – How Much should it be enough;in light of relevant Auditing Standards and

Auditing Practice StatementsSabbir Ahmed FCA

public interest is reflected in the way banks in almost all countries, unlike most other commercial enterprises, are subject to multiple prudential supervisions by central banks and/or other specific official regulators/agencies.

As part of this confidence building measure on Banks, its financial statements are subject to audit by multiple auditors including external or statutory auditors. The external auditor conduct the audit in accordance with applicable ethical and auditing standards, including those calling for independence, objectivity, professional competence and due care, and adequate planning and supervision. The auditor’s opinion lends credibility to the financial statements and promotes confidence in the banking system.

However, what is also very important to note is the fact that the quality of the external auditor’s opinion would also be influenced by multiple elements, notable amongst those are the proper observance of various roles and responsibilities of not only external auditors but the following parties as well:

- the Bank’s Board of Directors (those charged with Governance);

- the Bank’s Management; and- the supervisor (i.e. Central Bank) and

other regulators.

The Bangladesh Accountant January - March 2013 09

THEY HOLD THE

SAVINGS OF THE PUBLIC,

PROVIDE A MEANS OF

PAYMENT FOR GOODS

AND SERVICES AND

FINANCE THE

DEVELOPMENT OF

BUSINESS AND TRADE. TO

PERFORM THESE

FUNCTIONS SECURELY

AND EFFICIENTLY,

INDIVIDUAL BANKS MUST

COMMAND THE

CONFIDENCE OF THE

PUBLIC AND THOSE WITH

WHOM THEY DO

BUSINESS. THE STABILITY

OF THE BANKING SYSTEM,

BOTH NATIONALLY AND

INTERNATIONALLY, HAS

THEREFORE COME TO BE

RECOGNIZED AS A

MATTER OF GENERAL

PUBLIC INTEREST.

The roles and responsibilities of the above parties could be different in various countries based on applicable law, regulation and custom, however it is true that proper observance of these roles and responsibilities by those parties would eventually support/complement fulfilment of each other’s duties and obligations.

Various auditing standards and audit practice statements provided guidance on respective roles and responsibilities of bank’s board of directors, management, banking supervisors and external auditors to avoid misconception about such roles that could lead to inappropriate reliance being placed by one party on the work of another. Those standards and statements also sets out responsibilities of the board of directors and management, essential features of the role of banking supervisors and external auditors and what should be the relationship between the banking supervisor and the bank’s external auditors. We shall

January - March 2013 The Bangladesh Accountant10

aim to analyze those roles and responsibilities before focusing in detail on what need to be considered by an external auditor at the time of doing the audit of a bank.

The Responsibility of the Bank’s Board of Directors and the Management

The primary responsibility for the conduct of the business of a bank is vested on the board of directors and the management appointed by it. This responsibility includes, among other things, ensuring that:

• Those entrusted with banking tasks have sufficient expertise and integrity and that there are experienced staff in key positions;

• Adequate policies, practices and procedures related to the different activities of the bank are established and complied with, including the following:

- The promotion of high ethical and professional standards.

- Systems that accurately identify and measure all material risks and adequately monitor and control these risks.

- Adequate internal controls, organizational structures and accounting procedures.

- The evaluation of the quality of assets and their proper recognition and measurement.

- “Know your customer” rules that prevent the bank being used, intentionally or unintentionally, by criminal elements.

- The adoption of a suitable control environment, aimed at meeting the bank’s prescribed performance, information and compliance objectives.

- The testing of compliance and the evaluation of the effectiveness of internal controls by the internal audit function.

• Appropriate management information and information technology systems are established;

• The bank has appropriate risk management policies and procedures;

• Statutory and regulatory directives, including directives regarding solvency and liquidity, are observed; and

• The interests not only of the shareholders but also of the depositors, employees and other creditors are adequately protected.

Management is responsible for preparing financial statements in accordance with the appropriate financial reporting framework and for establishing accounting procedures that provide for the maintenance of documentation sufficient to support the financial statements. This responsibility includes ensuring that the external auditor who examines and reports on the financial statements has complete and unhindered access to, and is provided with, all necessary information that can materially affect them and, consequently, the auditor’s report on them. Management also has the

responsibility to provide all information to the supervisory agencies that such agencies are entitled by law or regulation to obtain.

Management is also responsible for the establishment and the effective operation of a permanent, continuous and adequate internal audit function that should also be independent of the organizational activities it audits or reviews and every day internal control process. Every activity and every division, subsidiary or other component of the banking organization should fall within the scope of the internal audit function’s review and the internal audit function should be adequately staffed with persons of the appropriate skills and technical competence who are free from operating responsibilities.

The Role of the Banking Supervisor (i.e. Central Bank)

The key objective of prudential supervision is to maintain stability and confidence in the financial system, thereby reducing the risk of loss to depositors and other creditors. In addition, supervision also is often directed toward verifying compliance with laws and regulations governing banks and their activities. Although these compliance requirements may differ from country to country but the following basic requirements are ordinarily found in most systems of supervision:

• The bank must have suitable shareholders and members of the board (this notion includes integrity and standing in the business community as well as the financial strength of all major shareholders).

The Bangladesh Accountant January - March 2013 11

January - March 2013 The Bangladesh Accountant12

by regulators in that country (i.e. the Bank Company Act 1991).

As stated earlier, the auditor’s opinion helps to establish the credibility of the financial statements. The auditor’s opinion, however, should not be interpreted as providing assurance on the future viability of the bank or an opinion as to the efficiency or effectiveness with which the management has conducted the affairs of the bank, since these are not objectives of the audit.

The auditor designs audit procedures to reduce to an acceptably low level the risk of giving an inappropriate audit opinion when the financial statements are materially misstated. The auditor assesses the inherent risk of material misstatements occurring (inherent risk) and the risk that the entity’s accounting and internal control systems will not prevent or detect and correct material misstatements on a timely basis (control risk). Based on the assessment of inherent and control risk, the auditor carries out substantive procedures to reduce the overall audit risk to an acceptably low level.

The auditor considers how the financial statements might be materially misstated and considers whether fraud risk factors are present that indicate the possibility of fraudulent financial reporting or misappropriation of assets. The auditor designs audit procedures to reduce to an acceptably low level the risk that misstatements arising from fraud and error that are material to the financial statements taken as a whole are not detected.

What are the additional audit risk factors

As all we know, Banks have the following characteristics that

• The bank’s management must be honest and trustworthy and must possess appropriate skills and experience to operate the bank in a sound and prudent manner.

• The bank’s organization and internal control must be consistent with its business plans and strategies.

• The bank should have a legal structure in line with its operational structure.

• The bank must have adequate capital to withstand the risks inherent in the nature and size of its business.

• The bank must have sufficient liquidity to meet outflows of funds.

• The bank must have a robust risk management framework to cover various banking risks, such as credit risk, market risk (including interest and foreign exchange risk), liquidity and funding risk, operational risk, legal risk and reputational risk and regularly monitor, measure and limit its risk exposures to the prescribed internal and external limits.

• The bank is applying right methods and fair judgments to calculate specific and general allowances that are adequate to absorb estimated credit losses, on a timely basis, in accordance with appropriate policies and procedures. In addition, the supervisor also seeks to ensure that credit risk is adequately diversified by means of rules to limit exposures, whether in terms of individual borrowers, industrial or commercial sectors or particular countries or economic regions. Although it

may not be the banking supervisor’s role to direct banks’ lending policies, but it is essential for the supervisor to be confident that the bank has adopted a sound system for managing credit risk.

• The development of sophisticated real-time computerized information systems has greatly improved the potential for control, but in turn has brought with it additional risks arising from the possibility of computer failure or fraud. The introduction of electronic commerce has also introduced significant new risks and requires, in turn, additional controls. From supervisory point of view these are very critical element.

• Supervisors are concerned to ensure that the quality of management is adequate for the nature and scope of the business and try to understand management’s business plans and strategies and how it expects to achieve them. Similarly, the supervisor seeks to discover whether the bank is properly equipped to carry out its functions in terms of the skills and competence of its staff and the equipment and facilities at its disposal.

The Role of the Bank’s External Auditor

The objective of an audit of a bank’s financial statements by an external auditor is to enable an independent auditor to express an opinion as to whether the bank’s financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework (i.e. Bangladesh Financial Reporting Standards) and in accordance with any relevant regulations laid down

The Bangladesh Accountant January - March 2013 13

generally distinguish them from most other commercial enterprises and hence external auditors need to consider appropriate additional audit procedures:

• They have custody of large amounts of monetary items, including cash and negotiable instruments, whose physical security has to be safeguarded during transfer and while being stored. They also have custody and control of negotiable instruments and other assets that are readily transferable in electronic form. The liquidity characteristics of these items make banks vulnerable to misappropriation and fraud. Banks therefore need to establish formal operating procedures, well-defined limits for individual discretion and rigorous systems of internal control.

• They often engage in transactions that are initiated in one jurisdiction, recorded in a different jurisdiction and managed in yet another jurisdiction.

• They operate with very high leverage (that is, the ratio of

capital to total assets is low), which increases banks’ vulnerability to adverse economic events and increases the risk of failure.

• They have assets that can rapidly change in value and whose value is often difficult to determine. Consequentially a relatively small decrease in asset values may have a significant effect on their capital and potentially on their regulatory solvency.

• They generally derive a significant amount of their funding from short term deposits (either insured or uninsured). A loss of confidence by depositors in a bank’s solvency may quickly result in a liquidity crisis.

• They have fiduciary duties in respect of the assets they hold that belong to other persons. This may give rise to liabilities for breach of trust. They therefore need to establish operating procedures and internal controls designed to ensure that they deal with such assets only in accordance with the terms on which the assets

were transferred to the bank.

• They engage in a large volume and variety of transactions whose value may be significant. This ordinarily requires complex accounting and internal control systems and widespread use of information technology (IT).

• They ordinarily operate through networks of branches and departments that are geographically dispersed. This necessarily involves a greater decentralization of authority and dispersal of accounting and control functions, with consequential difficulties in maintaining uniform operating practices and accounting systems, particularly when the branch network transcends national boundaries.

• Transactions can often be directly initiated and completed by the customer without any intervention by the bank’s employees, for example over the Internet or through automatic teller machines (ATMs).

• They often assume significant commitments without any

The Author is a Fellow CharteredAccountant and Director,Hoda Vasi Chowdhury & Co.

January - March 2013 The Bangladesh Accountant14

When I was discussing the draft of this article with a very senior chartered accountant with few decades of experience in bank audit, he jokingly told me that some people may interpret this article as my effort to defend auditors or dilute auditor’s responsibilities by highlighting roles of other stakeholders. Although his comment was a lighthearted one without much seriousness attached to it, but taking the hint, for the purpose of this article, I have extensively used relevant auditing standards and audit practice statements in its original form without much alteration. This way I have attempted to eliminate subjectivity and reflected what requires as per standards for a bank audit that can be termed as sufficient and appropriate. As this article has already highlighted, fulfilling of all requisite roles and responsibilities by only the auditor would not result in sufficient and appropriate audit if all other stakeholders are not fulfilling their mutual responsibilities.

No doubt time has come for self assessment by auditors as to whether they are performing Bank audits as required by standards or this has become just a routine matter. At the same time it also needs to be ensured that all other stakeholders are also fulfilling their respective responsibilities as without which an audit would not be adequate (i.e. sufficient and appropriate).

initial transfer of funds other than, in some cases, the payment of fees/margins. These commitments may involve only memorandum accounting entries. Consequently their existence may be difficult to detect.

• They are regulated by governmental authorities, whose regulatory requirements often influence the accounting principles that banks follow. Non-compliance with regulatory requirements, for example, capital adequacy requirements, could have implications for the bank’s financial statements or the disclosures therein.

• Customer relationships (i.e. loans, deposits) that the auditor, assistants, or the audit firm may have with the bank might affect the auditor’s independence in a way that customer relationships with other organizations would not.

• They generally have exclusive access to clearing and settlement systems for checks, fund transfers, foreign exchange transactions, etc.

• They are an integral part of, or are linked to, national and international settlement systems and consequently could pose a systemic risk to the countries in which they operate.

• They may issue and trade in complex financial instruments, some of which may need to be recorded at fair values in the financial statements. They therefore need to establish appropriate valuation and risk management procedures. The effectiveness of these procedures depends on the appropriateness of the

methodologies and mathematical models selected, access to reliable current and historical market information, and the maintenance of data integrity.

In view of the above, it is agreeable that in addition to the usual competency of auditing and accounting standards, statutory or external audit of a Bank also require additional knowledge and understanding on areas like banking products/services, various macro and micro economic indicators, applicable regulations etc.

Also equally important to note that an auditor can only effectively discharge their responsibilities when other functionaries like board, management and regulator/supervisors are also properly and diligently following their own roles and responsibilities. If any one party is falling behind in following its roles and responsibilities the work of other would suffer.

Conclusion

The key theme of this issue of the Bangladesh Accountant is very topical, as hardly any single day has been passed during the last few months where not only business and finance section, but even headlines of local dailies were not free from news about banking sector in Bangladesh. Many of those articles also touched upon the performance of external auditors in their audit of banks. Therefore, an attempt has been made through this article to reflect respective roles and responsibilities of auditors as well as other stakeholders like board, management and supervisors for the conduct of a successful audit as all are quite interrelated.

Introduction

Commercial Bank (Bank), either local or international, is required to be incorporated under the laws of the land where they are incorporated as “Banking Companies”. Every country has its specific laws, rules and regulations on how to incorporate Banking Company, how it will be run, what are the requirements for audit, who will conduct the audit, what guidelines are to be followed and so on. Generally the Auditors follow the local and international standards and guide lines while conducting an audit of a commercial bank. There are different types of audit of banks: internal, external, statutory, special and compliance audit. External audit may be from the Central Bank, from the government auditors, from the management on specific purposes, from the parliamentary audit committee. Bank audit is completely different and unique in itself because banking businesses are different from other ordinary businesses. The importance of banks’ audit has been increased tremendously after the Global Financial and Economic Crisis started from the giant economy of the United States since 2007. In Bangladesh, special audit consideration has been provided by various authorities including the stakeholders, the central bank and the government, after the

Audit of Local and InternationalCommercial Banks:

an overview of Practices and ProceduresM Jalal Hussain FCA

exposure of Sonali Bank’s (a local state owned commercial bank) loan scandal with Hall Mark Group of Industries and Destiny Group of industries.

Why Bank audit is different from other business entities?

Commercial banks have the following distinctiveness which generally distinguishes them from most other commercial enterprises:

• Commercial banks of any country need special license from the Central Bank to run the operations of the bank and strictly follow the rules, regulations and guidelines of the Central bank.

• They are the custodian of large volumes of monetary items, including cash and negotiable instruments, whose physical security has to be assured. This applies both to the storage and the transfer of monetary items and makes banks vulnerable to misappropriation and fraud. Banks therefore need to establish and upgrade formal operating procedures, well defined limits for individual discretion and effective systems of internal control.

The Bangladesh Accountant January - March 2013 15

IN MANY CASES OF AUDIT: INTERNAL, EXTERNAL, STATUTORY AND OTHER TYPES, FAIL TO DETECT AND CONTROL FRAUD, ERRORS, NEGLIGENCE, MISAPPROPRIATION OF FUND, LOAN SCAMS, ETC. IN LARGE BANKS. IN BANGLADESH, AUDIT JOBS ARE CONDUCTED BY VARIOUS AUDITORS AND THERE ARE INTERNAL CONTROL SYSTEMS IN EXISTENCE BUT THE LOAN SCAMS OF HALL MARK AND DESTINY GROUPS PROVE THAT BOTH INTERNAL CONTROL AND VARIOUS AUDITS FAIL TO CONTROL AND PREVENT THE EMBEZZLEMENT OF HUGE FUND. FROM THE VARIOUS ANALYSIS AND INVESTIGATION IT IS EVIDENCED THAT THERE ARE MANY LAPSES AND WEAKNESSES IN THE INTERNAL CONTROL SYSTEMS OF BANKS WHICH ARE NOT DETECTED WHILE CONDUCTING AUDITS BY THE AUDITORS.

• Banks engage in a large volume and variety of transactions both in terms of quantity and value. This necessarily requires strong internal control and in particular, the Bank’s management information system and related business processes relevant to financial reporting and widespread use of electronic data processing.

• Banks normally operate through a wide network of branches and departments which are geographically located in different parts of the country. This necessarily involves a greater decentralization of authority and dispersal of financial reporting and internal control functions, with consequent difficulties in maintaining uniform operating practices and information systems, particularly when the branch network covers national and international boundaries.

• Banks often times assume significant commitments without any transfer of funds. These items, normally called “off-balance-sheet” items, may not involve accounting entries and consequently the failure to record such items may be difficult to detect.

• They are regulated by governmental authorities and the resultant regulatory requirements often influence generally accepted accounting principles and auditing practices within the Banking sector.

Why special audit considerations arise in the audits of banks?

As mentioned earlier, Banks do business transactions which are different from other commercial

January - March 2013 The Bangladesh Accountant16

enterprises; special considerations are required for the following reasons:

• Since Banks operate the businesses where risks are involved in many ways, special concentration of auditors have become material;

• the particular nature of the business risks associated with the transactions undertaken by banks;

• the scale of banking operations and the resultant significant exposures which can arise within short periods of time;

• the extensive dependence on computerized systems to process transactions;

• the outcome of the regulations in the various jurisdictions in which they operate; and

• the ongoing development of new products and banking practices which may not be matched by the concomitant development of accounting principles and auditing practices.

International and Local Standards for conducting audit of Banks:

The International Auditing Practices Committee (IAPC) of the International Federation of Accountants (IFAC) issues standards (ISAs) on generally accepted auditing practices and on related services and on the form and content of the auditor’s reports. These standards are intended to improve the degree of uniformity of auditing practices and related services throughout the world. In addition to the international standards, there are various standards framed by the local authorities, need to be followed by the auditors. In addition, Banks are required to follow the local standards,

The Bangladesh Accountant January - March 2013 17

procedures and programs as embodied by the local authorities and the central banks.

Why reliance on the Internal Control System of banks is so important?

Effective internal control system in banking sector is a must. A system of effective control is a choleric and diagnostic component of bank management and a foundation for the safe and sound operation of banking organizations. A system of strong internal controls can help ensure that the goals and objectives of a banking organization will be met, that the bank will achieve long-term profitability targets, and maintain reliable financial and managerial reporting. Such a system can also help ensure that the bank will comply with laws and regulations

as well as policies, plans, internal rules and procedures, and decrease the risk of unexpected losses or damage to the bank’s reputation due to corruption, baloney and malpractices by the employees of the bank.

Establishing degree of Reliance on Internal control:

Management’s responsibilities include the maintenance of adequate internal control, the selection and application of accounting policies, and the safeguarding of the assets of the entity.

The auditor is required to obtain a sufficient understanding of the internal control to plan the audit and develop an effective audit approach. After obtaining the understanding, the auditor should

consider the assessment of control risk to determine the appropriate detection risk to accept for the financial statement assertions and to determine the nature, timing and extent of substantive procedures for such assertions. Where the auditor assesses control risk at a lower level, substantive procedures would normally be less extensive than would otherwise be required and may also differ as to their nature and timing. Identifying, documenting and testing the operating effectiveness of control procedures

Who is responsible to introduce effective and strong internal control system in banking industries? The answer is simply the Board of Directors of the bank. The Board of Directors of a bank provides governance, guidance and oversight to senior management. Board members

January - March 2013 The Bangladesh Accountant18

should be professional, objective, capable, and inquisitive, with a knowledge or expertise of the activities of and risks run by the bank. The Board should consist of some members who are independent from the daily management of the bank. A strong, active board, particularly when coupled with effective upward communication channels and capable financial, legal, and internal audit functions, provides an important mechanism to ensure the correction of problems that may diminish the effectiveness of the internal control system. The Board of Director should realize the importance of effective internal control system as banks handle billions of Taka of money that belongs to individual depositors, businesses and other entities. Internal bank controls ensure that account holders can safely deposit money into banks without having to contend with the risk that a bank employee might misuse the money or put it in jeopardy by recklessly

investing it. Additionally, bank internal controls are necessary to ensure that the bank employees comply with the laws of the land and the rules, regulations issued by banks and the central bank.

In assessing the appropriateness of the individual internal controls used to ensure that all transactions are properly recorded, the auditor will need to take into account a number of factors which are especially important in a banking environment. These are as follows:

• Banks deal in large volumes of transactions, which can individually and cumulatively involve large amounts of money. Accordingly, the bank will need to have balancing and reconciliation procedures which are operated within a time-frame that provides the ability to detect errors and discrepancies so that they can be investigated and corrected with a minimal risk of loss to

the bank. Such procedures may be operated hourly, daily, weekly, or monthly, depending on the volume, nature of the transaction, level of risk, and transaction settlement time-frame.

• Many of the transactions entered into by banks are subject to particular accounting rules. It will therefore be necessary to have control procedures in place to ensure those rules are applied in a manner and in a time-frame which results in the generation of accounting entries that may be required for the preparation of appropriate financial information for management and external reporting. Examples of such control procedures are those which result in the market revaluation of foreign exchange and security purchase and sale commitments so as to ensure that all unrealized profits and losses are recorded.

• Many transactions entered into by banks are not disclosed in the balance sheet or even in the notes to the financial statements. Accordingly, control procedures must be in place to ensure that such transactions are recorded and monitored in a manner which provides management with the required degree of control over them and which allows for the prompt determination of any change in their status which needs to result in the recording of a profit or loss.

• New financial products and services are constantly being developed by banks. The auditor needs to obtain

The Bangladesh Accountant January - March 2013 19

reasonable assurance that necessary revisions are made in accounting procedures and related internal controls.

• End of day balances may not be indicative of the volume of transactions processed through the systems or of the maximum exposure to loss during the course of a business day. This is particularly relevant in executing and controls in these areas must take into account the ability to maintain control during the period of maximum volumes or maximum financial exposure.

• The majority of banking

transactions must be recorded in a manner which is capable of being verified both internally and by the bank’s customers and counterparties. The level of detail to be recorded and maintained on individual transactions must allow for bank management, transaction. Counter parties, and the bank’s customers to verify the accuracy of the amounts. An example of such a control is the continuous verification of foreign exchange trade tickets by having an independent employee match them to incoming confirmations from counterparties.

Why audit is not enough to detect and control fraud in banks?

Although the audit of banks are conducted by the professionals, experts with due consideration to internal control systems in banking businesses, there are lots of frauds, misappropriation and misuse of fund, loans scam and on and on remain unearthed and uncovered around the modern world. In many cases of audit: internal, external, statutory and other types, fail to detect and control fraud, errors, negligence, misappropriation of fund, loan scams, etc. in large banks. In Bangladesh, audit jobs are conducted by various auditors and there are internal control

January - March 2013 The Bangladesh Accountant20

systems in existence but the loan scams of Hall Mark and Destiny Groups prove that both internal control and various audits fail to control and prevent the embezzlement of huge fund. From the various analysis and investigation it is evidenced that there are many lapses and weaknesses in the internal control systems of banks which are not detected while conducting audits by the auditors. Loopholes in the existing legal system help the loan defaulters and the criminals to escape punishment. Banks, in most of the cases, fail to realize loan from the defaulting borrowers as the borrowers come out by using the legal network without paying back the loan amount. As a result the amount of classified loans increases every year.

In USA the SEC has recently charged three former executives of a bank, Tier OneBank, responsible for a fraudulent scheme.

New charges were also brought against its auditors. The SEC’s

investigation found that the auditors failed to appropriately scrutinize management’s estimates of TierOne’s allowance for loan and lease losses (known as ALLL). Due to the financial crisis and problems in the real estate market, this was one of the highest risk areas of the audit, yet the auditors failed to obtain sufficient evidence supporting management’s estimates of fair value of the collateral underlying the bank’s troubled loans. Instead, they relied on stale information and management’s representations, and they failed to heed numerous red flags when issuing unqualified opinions on TierOne’s 2008 financial statements and the bank’s internal controls over its financial reporting.

According to the SEC’s order, the internal controls identified and tested by the auditing engagement team did not effectively test management’s use of stale and inadequate appraisals to value the collateral underlying the bank’s troubled loan portfolio. For

example, the auditors identified TierOne’s Asset Classification Committee as a key ALLL control. But there was no reference in the audit work papers to whether or how the committee assessed the value of the collateral underlying individual loans evaluated for impairment, and the committee did not generate or review written documentation to support management’s assumptions. Given the complete lack of documentation, the auditors had insufficient evidence from which to conclude that the bank’s internal controls for valuation of collateral were effective. The SEC’s order alleges that the auditors engaged in improper professional conduct as defined in the securities laws. A hearing will be scheduled before an administrative law judge to determine whether the allegations contained in the order are true and what, if any, remedial sanctions are appropriate. The judge is expected to issue an initial decision within 300 days from the date of service of the order (Topbeancounter | January 10, 2013).

Conclusion:

It has become conspicuously evident that the banks are in no way obviated of corrupt and fraudulent practices after all. Abundant facts in the recent studies attest to this claim. The banking sector in particular has become a terrain for various appalling corrupt and fraudulent practices. In addition, the recent studies noted that the internal mechanisms in the banks are not sufficient to guarantee transparent and accountable service in the conduct of official business in the sector. Mere conventional audit is not enough to protect the banking industries from entwine of corruption and fraud. The audit procedures, plans and programs of

The Author is the Group FinancialController of a private Group ofIndustries and Fellow CharteredAccountant of ICAB

The Bangladesh Accountant January - March 2013 21

the auditors need to be reorganized to cope with modern complicated and electronic banking system. Auditors should give more emphasis on the internal control system and evaluate the effectiveness of the system. The stakeholders and the management of the bank must establish and upgrade the transparency and accountability in the banking operation and management system. Accountability and transparency are celestially

considered to be the most important contraptions for protecting banks from irregularities, frauds and mismanagement. It is copacetic from the present world economic scenarios that the more economically developed countries have track record of strong and effectual transparency and accountability in banking sector economy. The legal systems of the developing economies like Bangladesh need to be amended to

enable the banks to realize the default loans and the defaulters get punishment and cannot escape punishment by using the laws of the land.

Abstract

Profitability is the ultimate test of managements’ operating effectiveness and success of a financial institution. However, profit is one of the quantitative elements which reflect the bank performance story. Baking industry of Bangladesh has developed tremendously. Among contributory financial organizations both conventional and Islamic banks of Bangladesh are making significant contribution in economic development of Bangladesh. But both types of bank need to ensure sustainability along with the profitability by maintaining adequate liquidity. In the recent years banks are developing at a high growth rate. Both of these banks are concentrated in their profitability trend for better sustainability. Profitability depends on the overall performance efficiency of the bank. The study shows a comparative study between conventional and Islamic banking system of Bangladesh and reveals the competitive scenario for both sectors.

Introduction

Banking is the backbone of national economy. All sorts of economic and financial activities revolve round the axis of banks. In the global context, the role of banks is far-reaching and more penetrating

Profitability Trend in the Banking Sector ofBangladesh- a Comparative Study of

Islamic and Conventional Banks1Ishter Mahal | 2Benazir Rahman

in the economic and fiscal discipline, trade, commerce, industry, export and import. Banks are the only media through which both national and international trade and commerce emanated. Bangladesh has a mixed banking system comprising nationalized, private and foreign commercial banks. Bangladesh Bank is the central bank of the country and is in charge of monetary policies of the Government and all commercial banks.

Now-a-days Commercial banks play a key role in the economic development of a nation through mobilization of savings and allocation of credit to productive sectors. Nevertheless, directed and inefficient credit allocation by the commercial banks of Bangladesh in various economic sectors without adequate credit appraisal and monitoring, ultimately led to the widespread loan delinquency, and deteriorating health of the entire financial system. The commercial banking system dominates Bangladesh's financial sector. There are 54 banks performing their functions in Bangladesh excluding Bangladesh Bank. Out of these, 4 are nationalized commercial banks, 29 are private commercial banks (conventional), 7 Islamic banks, 9 are foreign commercial banks and 5 are specialized development banks. These banks are offering a variety

January - March 2013 The Bangladesh Accountant22

AFTER ANALYZING THE AVERAGE PROFITABILITY RATIOS IT IS FOUND THAT BOTH THE SECTORS ARE DOING WELL BUT THEIR CLASSIFIED LOANS/INVESTMENTS AMOUNT SHOULD BE MAINTAINED AT A TOLERABLE LEVEL. AFTER THE COMPARATIVE STUDY IT IS FOUND THAT PROFITABILITY TREND OF SELECTED ISLAMIC BANKS ARE HIGHER BUT AVERAGE PROFITABILITY RATIOS OF CONVENTIONAL BANKS SHOWS BETTER POSITION. THOUGH ISLAMIC BANKS’GROWTH RATE IS BETTER BUT CONVENTIONAL BANKS’ RATIOS ARE IN BETTER POSITION. IT MAY BECAUSE OF THESE BANKS HAVE BETTER RISK MANAGEMENT TECHNIQUES AND ALSO DIVERSIFIED RANGE OF INVESTMENTS. IN SHORT, IT CAN BE SAID THAT BOTH SYSTEMS HAVE DIFFERENT COMPETITIVE ADVANTAGES IN THEIR FIELD WHICH INFLUENCE THEIR PROFITABILITY.

of products to their clients. In doing their business most crucial part is to manage their credit efficiently as their profit mostly depends on the proper management of credit. The next session will focus on literature review, third session focuses on company analysis, fourth session will include the analysis part and fifth session will focus on conclusion.

Objective

Broad Objective

The main objective is to focus on the profitability trend of both Conventional and Islamic banking system in Bangladesh taking 5 banks from each category and comparing them by applying appropriate tools.

Specific Objectives

The specific objectives of this paper are the following:

To study the Overall profitability trend of both Islamic banks and Conventional banks in Bangladesh based on their 5 years‘ performance of selected banks.

To find out the impact of profitability of these banks to the overall banking sector in last 5 years.

To show the impact of deposits and Loans/investments on profitability of banks selected from two sectors through regression analysis for 5 banks from each sector.

To show a comparative analysis of two sectors of banking in the light of selected 10 banks.

To point out the lacking that reflects in different banks’ performance.

To focus on factors influencing the growth as well as profitability of these two sectors of banking.

Limitation of the study

Privacy of Information: All the 10 banks selected as a sample are prominent banks of Bangladesh. For maintaining privacy, only limited information was available to use in the project. Another limitation of this study is bank’s policy of not disclosing some data and information for obvious reason, which could be very much useful.

Time Limitation: Such short time period of 3-months is not enough to learn everything about banking sector. Time limitation will also hinder the study.

Data Collection: collecting data through all the filtering and getting approval to use these data was difficult. The main constraint of the study is limited access to information, which has hampered the scope of analysis required for the study.

Sampling Problem: We have just worked with 10 banks amongst all the commercial banks which is so small as a sample.

Literature Review

Bader et al (2008) measured and compared the cost, revenue and profit efficiency of 43 Islamic and 37 conventional banks over the period 1990-2005 in 21 countries using Data Envelopment Analysis. They assessed the average and overtime efficiency of those banks based on their size, age, and region using static and dynamic panels and suggested that there are no significant differences between the overall efficiency results of conventional versus Islamic banks. Abdul & Azmi (2011) found in their

The Bangladesh Accountant January - March 2013 23

January - March 2013 The Bangladesh Accountant24

any differences of profit rate on investments of Islamic Bank against fixed lending rate of local conventional banks, foreign conventional banks and state owned commercial banks in Bangladesh. Analysis revealed that the foreign commercial banks charged the highest rate on the borrowers during the selected periods. It has also been found that there is a significant difference in mean return among Islamic banks, local conventional banks, foreign conventional banks and state owned commercial banks.

Selection of Banks / Samples

In this study the focal point is to make a comparative analysis between conventional and Islamic banking sector. For the study purpose we have selected 10 banks of Bangladesh as our sample; 5 banks from each sector. This study will focus on the profitability trend of these two sectors in the light of recent (2006-2011) 5 year’s performance of selected 10 banks. For the research selected banks are as follows-

study that while there are no significant difference in profitability during these two periods, Bank Islam Malaysia Berhad (BIMB) is relatively more liquid and less risky as compared to conventional banks. On top of that, basic modes of Islamic banking, i.e. mudharabah and musyarakah, are not of significant financing portfolio for Bank Islam Malaysia Berhad (BIMB). Usman & Khan (2012) have done a research on Financial Performance of Islamic and Conventional Banks of Pakistan and concluded that Islamic banks have high growth rate and profitability over the conventional banks. Moreover the Islamic banks have high liquidity power over conventional banks. Alani, Yaacob & Hamdan (2013) mentioned in their research perhaps the most important of the current analysis used in traditional banks are irrelevant in assessing the efficiency of the financial performance of Islamic banks because of their privacy. They urged researchers to focus on formulation of new analysis tools with focusing on Islamic banks.

Hanif (2011) depicted based on his research Islamic banking is very much practiced like modern conventional banking with certain restrictions imposed by Sharia and

addresses the large number of business requirements successfully hence perceiving Islamic banking as totally foreign to business world is not correct. Islamic banking is not a mere copy of conventional practices rather major differences exist in the operations of Islamic Financial Institutions (IFIs) in comparison with conventional banking. IFIs have succeeded in creating trust in the eyes of depositors and receive deposits on profit and loss sharing basis however investment and financing options available to Islamic banks are limited in comparison of conventional banks.

Shamsher, Taufiq & Khaled measured and compared the cost and profit efficiency of 80 banks in 21 of Organization of Islamic Conference (OIC) countries: comprising of 37 conventional banks and 43 Islamic banks, using the Stochastic Frontier Approach (SFA). The findings suggest that there are no significant differences between the overall efficiency results of conventional versus Islamic banks. However, there is substantial room for improvement in cost minimization and profit maximization in both banking systems. Kabir, Hafiz and Musa (2012) did a study which was an attempt to find whether there are

Conventional Banks

Islamic Banks

The Bangladesh Accountant January - March 2013 25

Comparison between Conventional & Islamic Banking in Bangladesh

After ananlyzing the recent 5 year’s senario of selected 10 banks we have got following result;

General Distinctions

Conventional Banks Islamic BanksDistinction of Product /Service :Principles of business

Deals with man-made principles or principles provided by BB .

Deals with Shariah based principles o n the basis of Islamic Shariah under the supervision of BB.

Variation in goals

Conventional goals are almost similar as Islamic ones in case of profitability & improving shareholder’s earnings. But now these banks are also concentrated in CSR such as environment consciousness and developing advanced technology as well.

Islamic banks mainly providing concentration on improving profit margin as well as increasing shareholder’s equity. But now these banks also improving their technology and concentrated in CSR activities but these are left behind than conventional ones.

Variation in Deposit

Conventional banks maintains following schemes generally but used different names for the schemes to distinguish from each other’s products Fixed Deposit (FDR) Savings or Short notice Deposit(SND) Current Deposit(CD)

Islamic banks receive deposits under two principles: Al-Wadeeah principle Mudaraba prin ciple

Other Facilities

Conventional banks believe in Letter of Credit ( L/C) most .

Islamic banks issues letter of guarantee most.

Business Efficiency:Profitability Profitability of conventional banks depends

on Loans and investments both.Profitability of Islamic banks depends on only investments sectors.

Liquidity & Solvency

These banks have to maintain more SLR that is 19% now.

These banks have to maintain SLR 10.5% which is lower than conventional ones.

Sources of Funds

Conventional banks use deposits as a core source of banks in exchange of fixed deposit interest.

Islamic banks also collect funds through deposits on the basis of profit & loss Sharing (PLS).

Uses of Funds These banks mainly invest in loans & advances as a core function of the banks & also invest in many sectors on term basis.

These banks mainly invest as per Islamic Shariah.

Business development

The growth profile of selected conventional banks indiates better positon.

Growth rate of selected Islamic banks are higher than the conventional ones.

Efficiency &Productivity

The selected conventional banks shows efficiency and productivity in the recent years.

The selected Islamic banks also shows better efficiency & productivity in the recent years. But the growth of these banks are higher than conventional ones.

Commitment to Economy &Community

These banks are in better situation as they have handsome amount that is invested in long-term investments.

Islamic banks are not an exeption.

Comparative Financial Analysis(Statistical Calculation & its Interpretation)

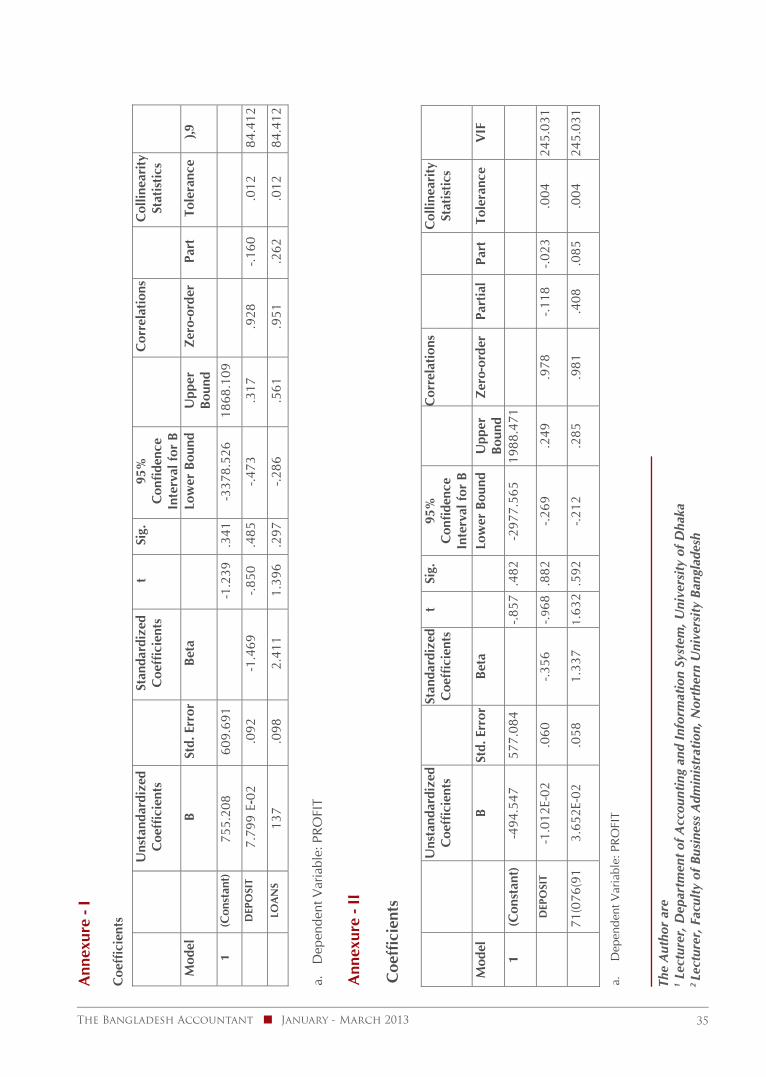

Multiple Regression-1 (For Conventional banks): For the regression analysis we have selected following variables;

Net Profit After Tax- Dependent Variable (Y)Deposits- Independent variable (X1)Loans & Advances- Independent variable (X2)

January - March 2013 The Bangladesh Accountant26

Descriptive Statistics

Mean Std. Deviation

N

PROFIT 1174.9340 882.2125 5DEPOSIT 48719.0000 16612.7650 5

LOANS 41720.5640 15484.9360 5

Variables Entered/RemovedModel Variables

EnteredVariables Removed

Method

1 LOANS, DEPOSIT

. Enter

a. All requested variables entered.b. Dependent Variable: PROFIT

Model SummaryR R2 Adjusted R2 Std. Error of

the EstimateChange Statistics

Model R2Change F Change df1 df2 Sig. F Change1 .964

a .929 .859 331.6207 .929 13.154 2 2 .071

a. Predictors: (Constant), LOANS, DEPOSIT

CorrelationsPROFIT DEPOSIT LOANS

Pearson Correlation

PROFIT 1.000 .928 .951

DEPOSIT .928 1.000 .994LOANS .951 .994 1.000

Sig. (1-tailed) PROFIT . .012 .007DEPOSIT .012 . .000LOANS .007 .000 .

N PROFIT 5 5 5DEPOSIT 5 5 5LOANS 5 5 5

Coefficient of correlation (R):

It measures the degree of relationship between the dependent and independent variables. Here, R = 0.964 indicates that there is a positive correlation between the variables.If the independent variable increases then this will result the dependent variable increase accordingly.

Coefficient of Determination(R2):

R2 shows the proportion of the variability in the dependent variable that can be explained by the estimated multiple regression equation.Here R2 is equal to 0.929 (92.9% expressed in percentage) indicates 92.9% of the variability in Profit after tax is explained by the input variables.

Adjusted R2:

Here Adj. R2= 0.859. R square shows the proportion of variability in the dependent variable that can be explained by multiple regressions. Adjusted R Square is the actual variability which is adjusted for both the independent variables. It is actual R2 needed when we add the second independent variable. It is found

after the analysis that the proportion is 0.859 or 85.90%.

Standard Error of Estimate:

Standard error of estimate denotes the error of overall estimation of the multiple correlations. Here the error is 331.6207 which indicate the variability between the expected and actual value.

ANOVAModel Sum of Squares df Mean Square F Sig.

1 Regression 2893250.743 2 1446625.372 13.154 .071Residual 219944.545 2 109972.273

Total 3113195.288 4a. Predictors: (Constant), LOANS, DEPOSITb. Dependent Variable: PROFIT

t-Test:

t- Test is used to determine whether each of the independent variable is significant. We refer to each of the separate T Test for each of the independent variable as a test for individual significance.

All the t values of our variables are (-1.239), (-0.850) and 1.396 and using α =.50, t0.25 = 0.816

Since 1.239>0.816 we reject H0: ß1=0

Since 0.850>0.816 we reject H0: ß2=0

Similarly 1.396>0.816 we reject H0: ß3=0

Hence there is a significant relationship between PAT and deposits & Loans at significance level of 0.50.

Regression Analysis:

Here,

Dependable Variable-Profit after Tax (PAT)

Independent Variables-Deposits (X2)

Loans & Advances (X3)

Findings:From the output above we can bring out an equation that is like:

Y= a+β2X2+β3X3

PAT =-755.208-7.799 Deposits +0.137Loans & Advances

Here (-7.799) represent an estimate of the changes corresponding to single quantity changes in deposit volume which is in inverse relation that for 1 increasing or decreasing arrangement with deposit volume results 7.799 decrease or increase the PAT.Similarly 1 increasing or decreasing arrangement with loans

Here

Sum of squares due to regression, (SSR) = 2893250.743Sum of square due to error, (SSE) = 219944.545Total sum of square (SST) = 3113195.288

F-Test:

The F Test is used to determine whether a significant relationship prevails between the dependent variable and independent variables. It is considered as the test for overall significance. Here the hypothesis for the F test is deemed as there is no significant relationship between dependent and independent variables. The alternative hypothesis is vice versa.

Therefore the null hypothesis is:

Ho: ß1 = ß2 = 0

Ha: one of the parameters is not equal to zero

If null hypothesis is rejected we can conclude that the overall relationship between Y(PAT) and independent variables X1(Deposits) & X2 (Loans) is significant.

Test Statistic, F= MSR/MSE 13.154And the given table value is 9.00 with the level of significance,

α= 0.10As 13.154 is higher than table value so we certainly derive that the null hypothesis is rejected. So, the overall relationship is significant.

The Bangladesh Accountant January - March 2013 27

Calculation of Coefficient –Annexure I

Coefficient CorrelationsModel LOANS DEPOSIT

1 Correlations LOANS 1.000 -.994DEPOSIT -.994 1.000

Co variances LOANS 9.679E-03 -8.968E-03DEPOSIT -8.968E-03 8.409E-03

a. Dependent Variable: PROFIT

Collinearity Diagnostics

a. Dependent Variable: PROFIT

Eigen value Condition Index

Variance Proportion

sModel Dimensio

n(Constant) DEPOSIT LOANS

1 1 2.937 1.000 .01 .00 .002 6.280E-02 6.838 .63 .00 .003 5.426E-04 73.565 .36 1.00 1.00

& advances results 0.137 likelihood to increase or decrease the PAT which is in positive relationship. (-0.755.208) represent the value of β1 which is constant coefficient that shows the reduction of PAT when two independent variables are zero (0).