argentina investment outlook - ey - united statesfi… · 4 argentina investment outlook: winds o...

TRANSCRIPT

Argentina InvestmentOutlook: Winds of Change

June, 2016

2 | Argentina Investment Outlook: Winds of Change

Table of Contents

Contacts

• Executive Summary

• Argentina’s political and macroeconomic environment• Current situation• Potential changes and new regulations imposed by the new government• Challenges

• Investment opportunities• Investments and transactions overview• Outlook on main Sectors • Investments and transactions rationale

• Why EY?

Eduardo CoduriCountry Managing Partner Office: 54 11 4318-1587Mail: [email protected]

Ignacio HecquetTransaction Advisory Services Leader - PartnerOffice: 54 11 4515-2614Mail: [email protected]

Carlos CasanovasTax Market Leader – PartnerOffice: 54 11 4318 1619Mail: [email protected]

Aldo PelessonAdvisory Leader – PartnerOffice: 54 11 4318 1784Mail: [email protected]

Fernando CoccaroAssurance Leader Deputy – PartnerOffice: 54 11 4510-2366Mail: [email protected]

Pablo MorenoMarkets Leader Argentina - PartnerOffice: 54 11 4510-2366Mail: [email protected]

3Argentina Investment Outlook: Winds of Change |

Executive Summary• Current political situation:

The candidate proposed by the opposing political party, Mauricio Macri, former Mayor of the City of Buenos Aires, won the presidential elections and took over on December 10th, 2015.

• Country economic overview:Economic activity: it will remain weak in 2016, but this trend is expected to be reverted and growing at a very dynamic pace from 2017 onwards.

Exchange rate: it was overvalued but recent measures were taken to correct the lag and also for the unification of the foreign exchange market.

Inflation rate: It has been high during the past ten years but, though still high for 2016, is expected to start decelerating from 2017 onwards.

Sovereign debt: The return to the international markets with a sale of sovereign bonds put an end to the default.

• Measures in progress:Reliable national statistics to measure inflation, poverty and unemployment.

Strengthening regional economies through abolishing taxes on exports, providing them more competitiveness regularizing the exchange rate over-appreciation and helping them with logistic costs through extensive infrastructure investment plans.

Recovery of the energy sector through rate adjustment that will allow investments.

Focus on investments promotion for infrastructure, improve service level, increase Central Bank reserves and increase genuine employment.

• Main challenges:Reduce fiscal deficit and inflation.

• Opportunities:Current asset values in Argentina are lower compared to local historical figures and to asset values of the region.

There are investment opportunities mainly in the following sectors: Infrastructure, Oil and gas, Renewable energy, Utilities, Mining, Agribusiness, Meat production, Knowledge-based services, and Banks.

4 | Argentina Investment Outlook: Winds of Change

Argentina’s political and macroeconomic environment

5Argentina Investment Outlook: Winds of Change |

Current situation: country overview• Argentina’s new administrationOn November 22nd, 2015 Argentine voters elected a new president who will hold office for the next four years as of December 10th. The elected president represents the opposition to the political cycle that ruled the country for the last twelve years. The incoming administration intends to strengthen local institutions and review policies in different areas: economy, healthcare, security, justice, foreign relations, etc., as well as analyze the implementation of new ones.

The current deteriorated macro-economic environment has conditioned the country’s performance in the last few years and, consequently, new regulations are expected to be enacted aimed at promoting the local and foreign investment needed to strengthen employment and improve the country’s infrastructure and thus facilitate the production of goods and services.

Economic and financial landscape of ArgentinaFrom 2011 to 2015, under second period of President Cristina Fernández de Kirchner, there was a sub-optimal performance in many of the macroeconomic variables that led to the current economic situation which the newly elected president is dealing with:

• a weak economic activity;

• a high level of inflation;

• a decline in trade surplus, despite the strong control of imports;

• an overvalued exchange rate with a foreign exchange control generating a wide gap with the parallel market;

• a growing fiscal deficit;

• a heavy drop in international reserves;

• limited access to external financing due to default impact.

6 | Argentina Investment Outlook: Winds of Change

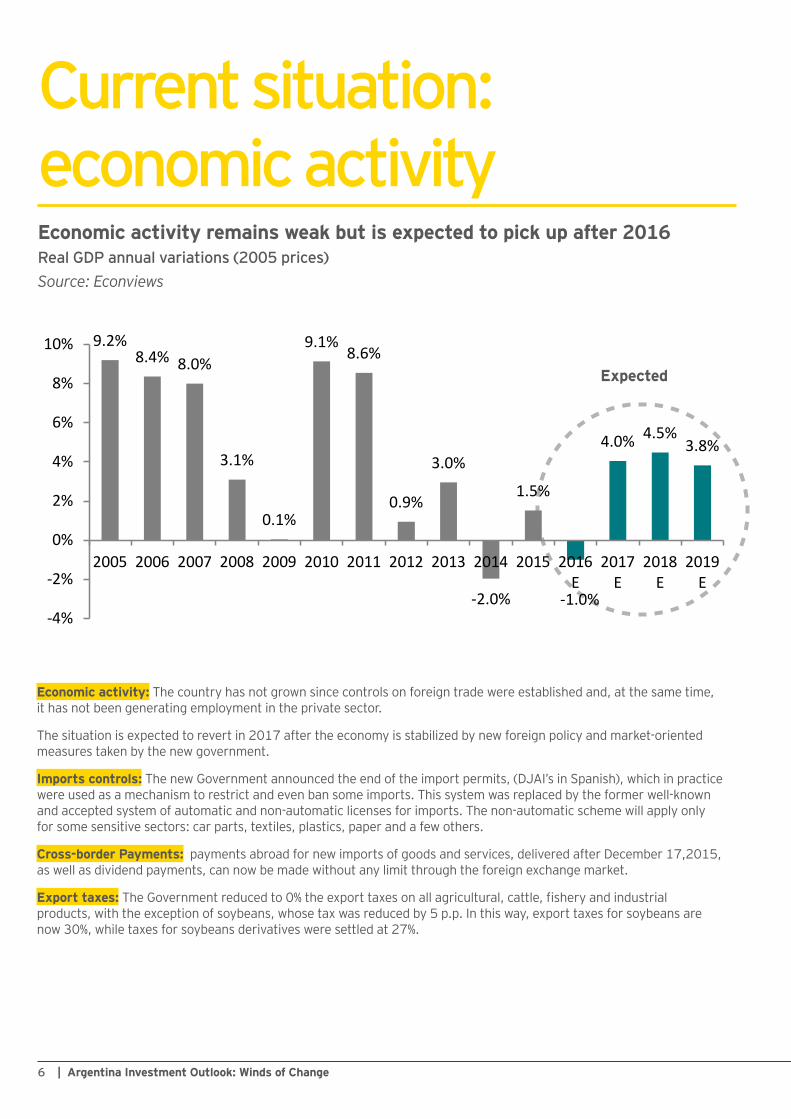

Current situation: economic activityEconomic activity remains weak but is expected to pick up after 2016Real GDP annual variations (2005 prices)Source: Econviews

Economic activity: The country has not grown since controls on foreign trade were established and, at the same time, it has not been generating employment in the private sector.

The situation is expected to revert in 2017 after the economy is stabilized by new foreign policy and market-oriented measures taken by the new government.

Imports controls: The new Government announced the end of the import permits, (DJAI’s in Spanish), which in practice were used as a mechanism to restrict and even ban some imports. This system was replaced by the former well-known and accepted system of automatic and non-automatic licenses for imports. The non-automatic scheme will apply only for some sensitive sectors: car parts, textiles, plastics, paper and a few others.

Cross-border Payments: payments abroad for new imports of goods and services, delivered after December 17,2015, as well as dividend payments, can now be made without any limit through the foreign exchange market.

Export taxes: The Government reduced to 0% the export taxes on all agricultural, cattle, fishery and industrial products, with the exception of soybeans, whose tax was reduced by 5 p.p. In this way, export taxes for soybeans are now 30%, while taxes for soybeans derivatives were settled at 27%.

Expected

9.2%8.4% 8.0%

3.1%

0.1%

9.1%8.6%

0.9%

3.0%

-2.0%

1.5%

-1.0%

4.0% 4.5%3.8%

-4%

-2%

0%

2%

4%

6%

8%

10%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

2017E

2018E

2019E

7Argentina Investment Outlook: Winds of Change |

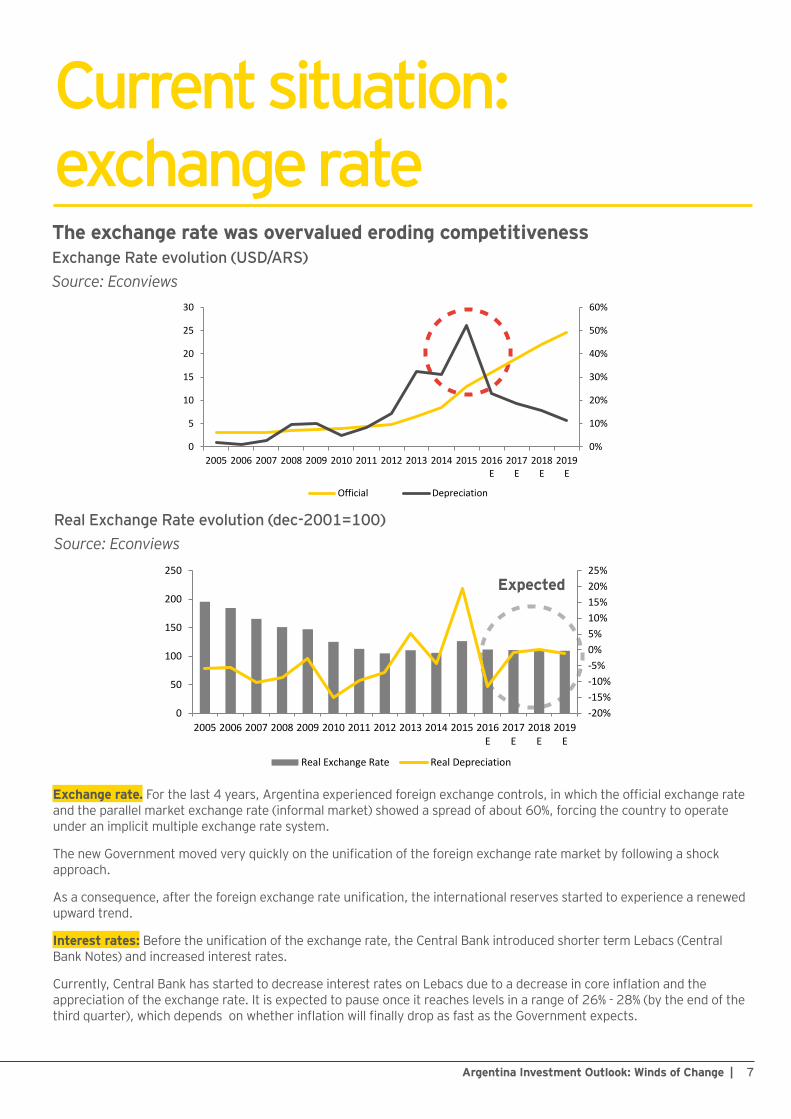

Current situation: exchange rateThe exchange rate was overvalued eroding competitivenessExchange Rate evolution (USD/ARS)Source: Econviews

Expected

Real Exchange Rate evolution (dec-2001=100)Source: Econviews

Exchange rate. For the last 4 years, Argentina experienced foreign exchange controls, in which the official exchange rate and the parallel market exchange rate (informal market) showed a spread of about 60%, forcing the country to operate under an implicit multiple exchange rate system.

The new Government moved very quickly on the unification of the foreign exchange rate market by following a shock approach.

As a consequence, after the foreign exchange rate unification, the international reserves started to experience a renewed upward trend.

Interest rates: Before the unification of the exchange rate, the Central Bank introduced shorter term Lebacs (Central Bank Notes) and increased interest rates.

Currently, Central Bank has started to decrease interest rates on Lebacs due to a decrease in core inflation and the appreciation of the exchange rate. It is expected to pause once it reaches levels in a range of 26% - 28% (by the end of the third quarter), which depends on whether inflation will finally drop as fast as the Government expects.

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

2017E

2018E

2019E

Official Depreciation

-20%-15%-10%-5%0%5%10%15%20%25%

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

2017E

2018E

2019E

Real Exchange Rate Real Depreciation

8 | Argentina Investment Outlook: Winds of Change

Current situation: inflationInflation will remain high in 2016 but it is expected to decelerate the coming yearsInflationSource: Econviews and INDEC

Expected

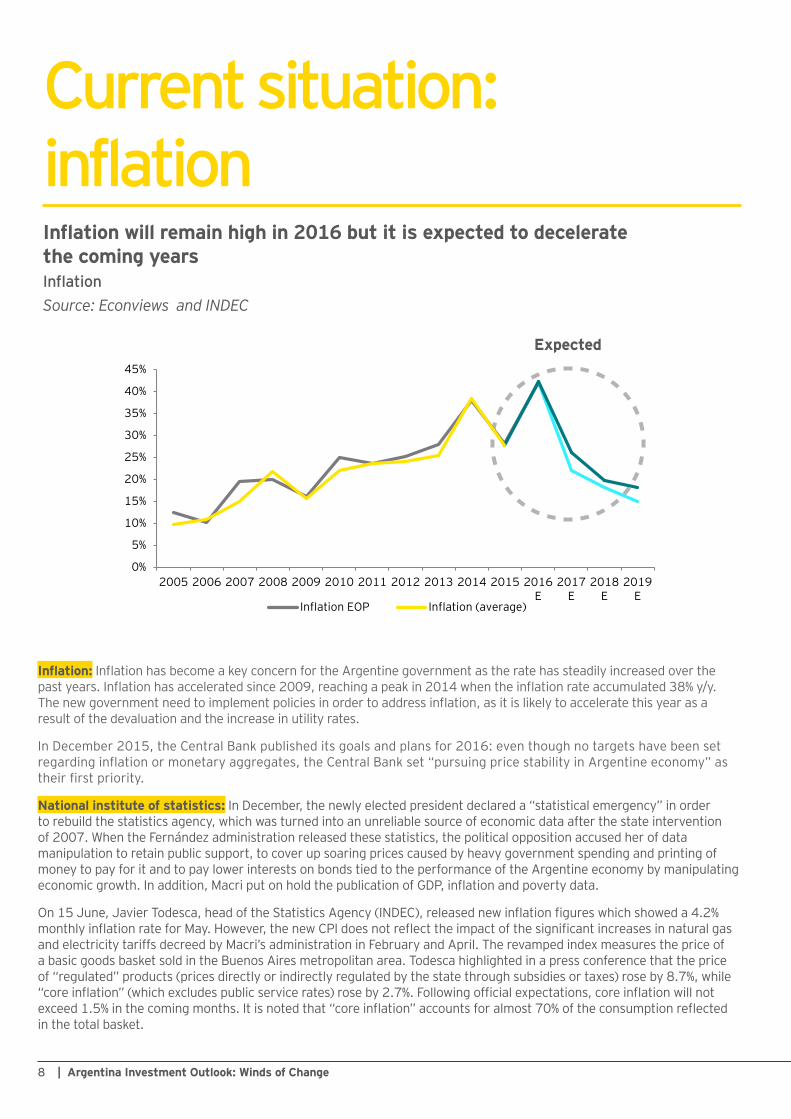

Inflation: Inflation has become a key concern for the Argentine government as the rate has steadily increased over the past years. Inflation has accelerated since 2009, reaching a peak in 2014 when the inflation rate accumulated 38% y/y. The new government need to implement policies in order to address inflation, as it is likely to accelerate this year as a result of the devaluation and the increase in utility rates.

In December 2015, the Central Bank published its goals and plans for 2016: even though no targets have been set regarding inflation or monetary aggregates, the Central Bank set “pursuing price stability in Argentine economy” as their first priority.

National institute of statistics: In December, the newly elected president declared a “statistical emergency” in order to rebuild the statistics agency, which was turned into an unreliable source of economic data after the state intervention of 2007. When the Fernández administration released these statistics, the political opposition accused her of data manipulation to retain public support, to cover up soaring prices caused by heavy government spending and printing of money to pay for it and to pay lower interests on bonds tied to the performance of the Argentine economy by manipulating economic growth. In addition, Macri put on hold the publication of GDP, inflation and poverty data.

On 15 June, Javier Todesca, head of the Statistics Agency (INDEC), released new inflation figures which showed a 4.2% monthly inflation rate for May. However, the new CPI does not reflect the impact of the significant increases in natural gas and electricity tariffs decreed by Macri’s administration in February and April. The revamped index measures the price of a basic goods basket sold in the Buenos Aires metropolitan area. Todesca highlighted in a press conference that the price of “regulated” products (prices directly or indirectly regulated by the state through subsidies or taxes) rose by 8.7%, while “core inflation” (which excludes public service rates) rose by 2.7%. Following official expectations, core inflation will not exceed 1.5% in the coming months. It is noted that “core inflation” accounts for almost 70% of the consumption reflected in the total basket.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

2017E

2018E

2019E

Inflation EOP Inflation (average)

9Argentina Investment Outlook: Winds of Change |

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

2017E

2018E

2019E

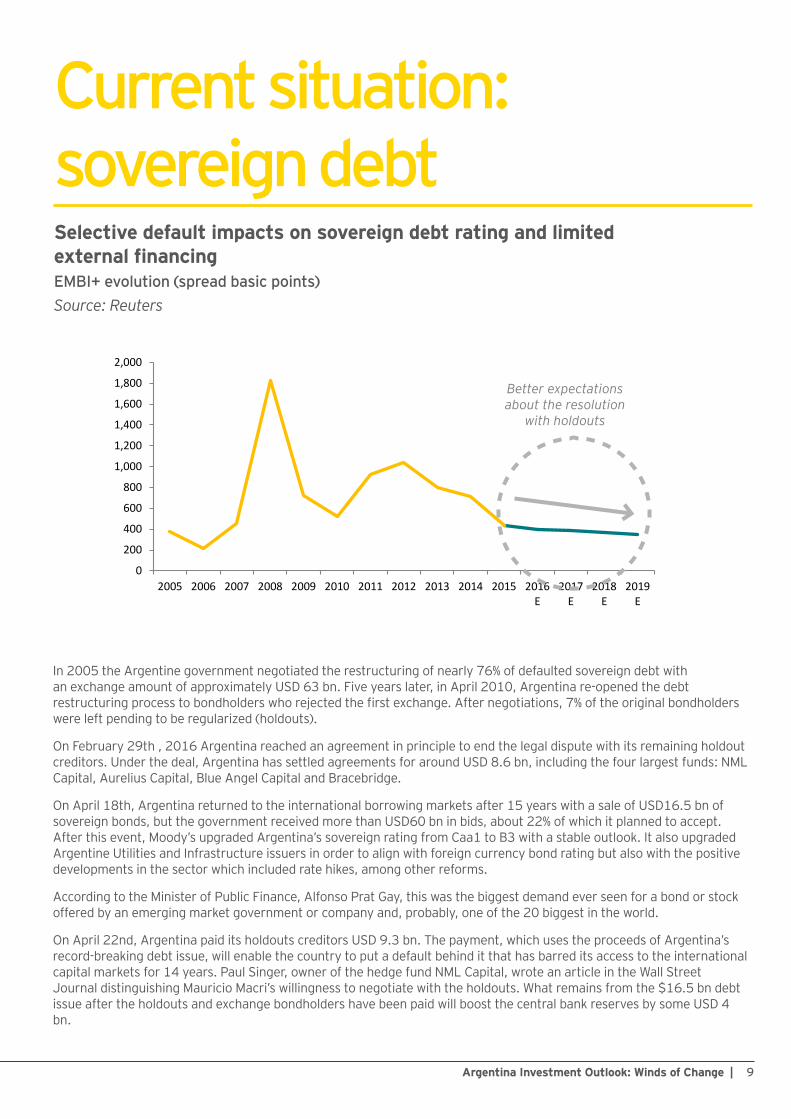

Current situation: sovereign debtSelective default impacts on sovereign debt rating and limited external financingEMBI+ evolution (spread basic points)Source: Reuters

Better expectations about the resolution

with holdouts

In 2005 the Argentine government negotiated the restructuring of nearly 76% of defaulted sovereign debt with an exchange amount of approximately USD 63 bn. Five years later, in April 2010, Argentina re-opened the debt restructuring process to bondholders who rejected the first exchange. After negotiations, 7% of the original bondholders were left pending to be regularized (holdouts).

On February 29th , 2016 Argentina reached an agreement in principle to end the legal dispute with its remaining holdout creditors. Under the deal, Argentina has settled agreements for around USD 8.6 bn, including the four largest funds: NML Capital, Aurelius Capital, Blue Angel Capital and Bracebridge.

On April 18th, Argentina returned to the international borrowing markets after 15 years with a sale of USD16.5 bn of sovereign bonds, but the government received more than USD60 bn in bids, about 22% of which it planned to accept. After this event, Moody’s upgraded Argentina’s sovereign rating from Caa1 to B3 with a stable outlook. It also upgraded Argentine Utilities and Infrastructure issuers in order to align with foreign currency bond rating but also with the positive developments in the sector which included rate hikes, among other reforms.

According to the Minister of Public Finance, Alfonso Prat Gay, this was the biggest demand ever seen for a bond or stock offered by an emerging market government or company and, probably, one of the 20 biggest in the world.

On April 22nd, Argentina paid its holdouts creditors USD 9.3 bn. The payment, which uses the proceeds of Argentina’s record-breaking debt issue, will enable the country to put a default behind it that has barred its access to the international capital markets for 14 years. Paul Singer, owner of the hedge fund NML Capital, wrote an article in the Wall Street Journal distinguishing Mauricio Macri’s willingness to negotiate with the holdouts. What remains from the $16.5 bn debt issue after the holdouts and exchange bondholders have been paid will boost the central bank reserves by some USD 4 bn.

10 | Argentina Investment Outlook: Winds of Change

-8.0%

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 E2017 E2018 E2019 E

Fiscal Surplus Fiscal Surplus without CB and ANSES

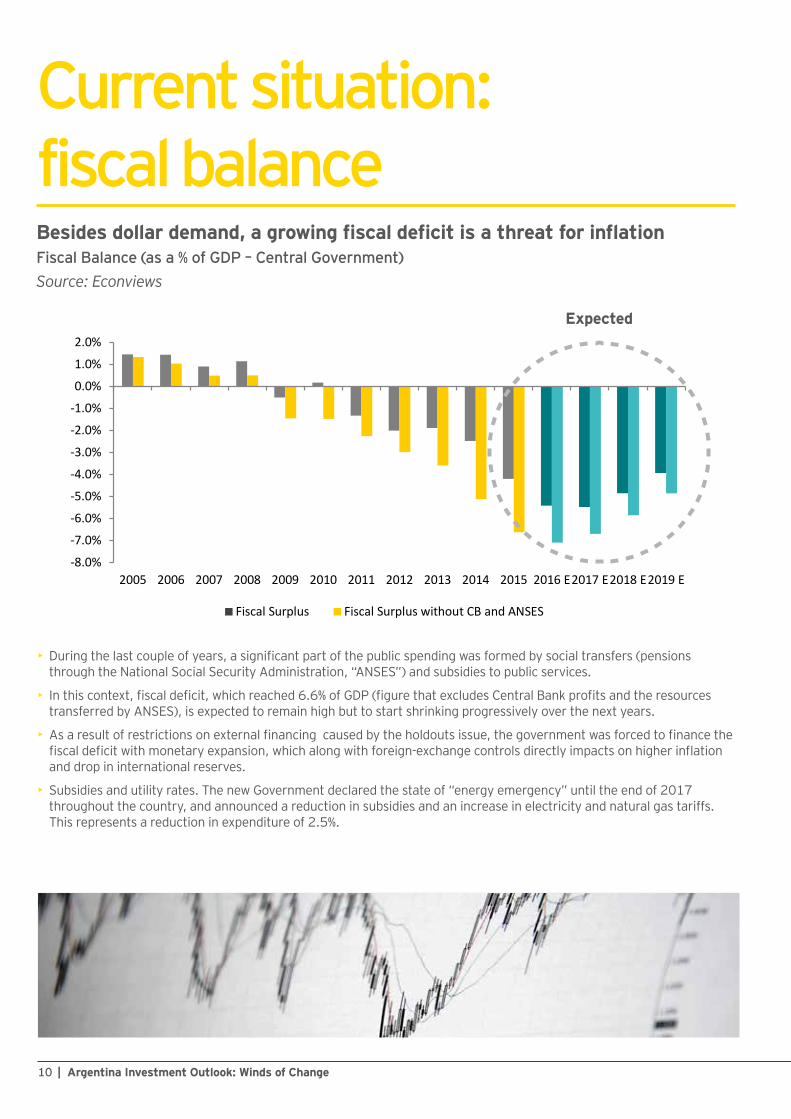

Current situation: fiscal balanceBesides dollar demand, a growing fiscal deficit is a threat for inflationFiscal Balance (as a % of GDP – Central Government)Source: Econviews

Expected

• During the last couple of years, a significant part of the public spending was formed by social transfers (pensions through the National Social Security Administration, “ANSES”) and subsidies to public services.

• In this context, fiscal deficit, which reached 6.6% of GDP (figure that excludes Central Bank profits and the resources transferred by ANSES), is expected to remain high but to start shrinking progressively over the next years.

• As a result of restrictions on external financing caused by the holdouts issue, the government was forced to finance the fiscal deficit with monetary expansion, which along with foreign-exchange controls directly impacts on higher inflation and drop in international reserves.

• Subsidies and utility rates. The new Government declared the state of “energy emergency” until the end of 2017 throughout the country, and announced a reduction in subsidies and an increase in electricity and natural gas tariffs. This represents a reduction in expenditure of 2.5%.

11Argentina Investment Outlook: Winds of Change |

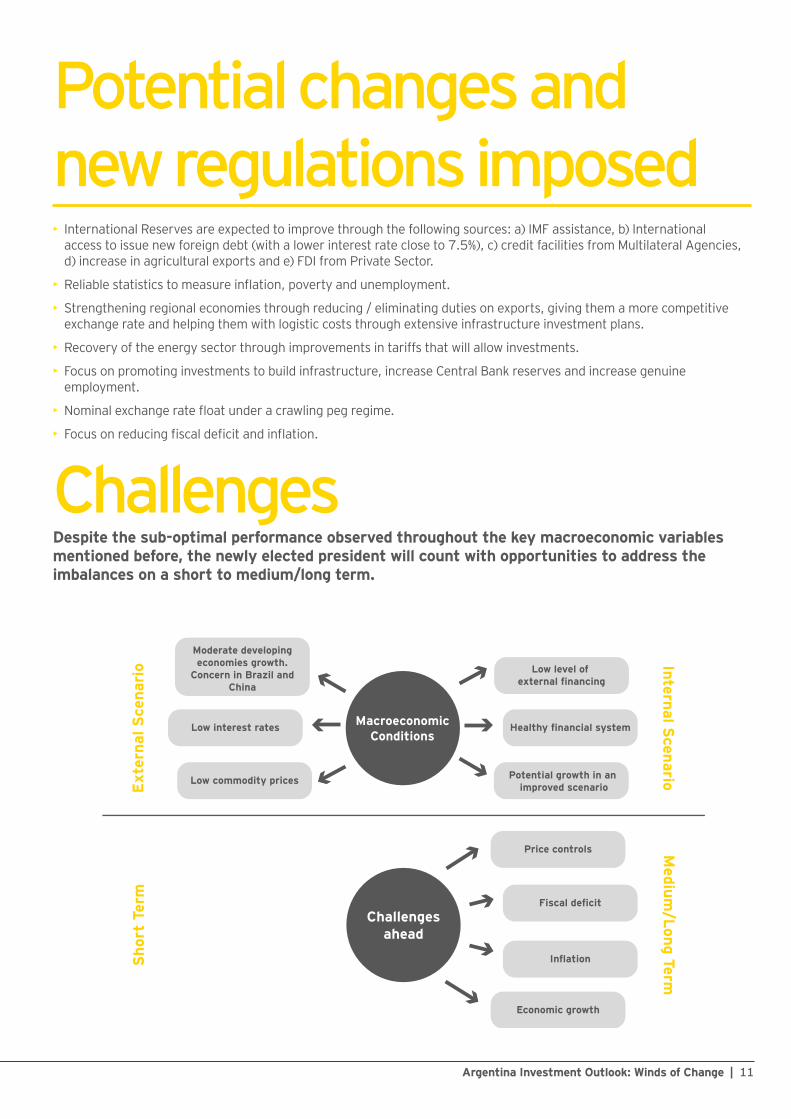

Potential changes and new regulations imposed• International Reserves are expected to improve through the following sources: a) IMF assistance, b) International

access to issue new foreign debt (with a lower interest rate close to 7.5%), c) credit facilities from Multilateral Agencies, d) increase in agricultural exports and e) FDI from Private Sector.

• Reliable statistics to measure inflation, poverty and unemployment.

• Strengthening regional economies through reducing / eliminating duties on exports, giving them a more competitive exchange rate and helping them with logistic costs through extensive infrastructure investment plans.

• Recovery of the energy sector through improvements in tariffs that will allow investments.

• Focus on promoting investments to build infrastructure, increase Central Bank reserves and increase genuine employment.

• Nominal exchange rate float under a crawling peg regime.

• Focus on reducing fiscal deficit and inflation.

ChallengesDespite the sub-optimal performance observed throughout the key macroeconomic variables mentioned before, the newly elected president will count with opportunities to address the imbalances on a short to medium/long term.

Low commodity prices

Low interest rates

Moderate developing economies growth.

Concern in Brazil and China

Potential growth in an improved scenario

Healthy financial system

Low level of external financing

Exte

rnal

Sce

nari

o Internal Scenario

Inflation

Economic growth

Fiscal deficit

Price controls

Sho

rt T

erm

Medium

/Long Term

12 | Argentina Investment Outlook: Winds of Change

Investment Opportunities

13Argentina Investment Outlook: Winds of Change |

Investment Opportunities:Investments and Transactions Overview

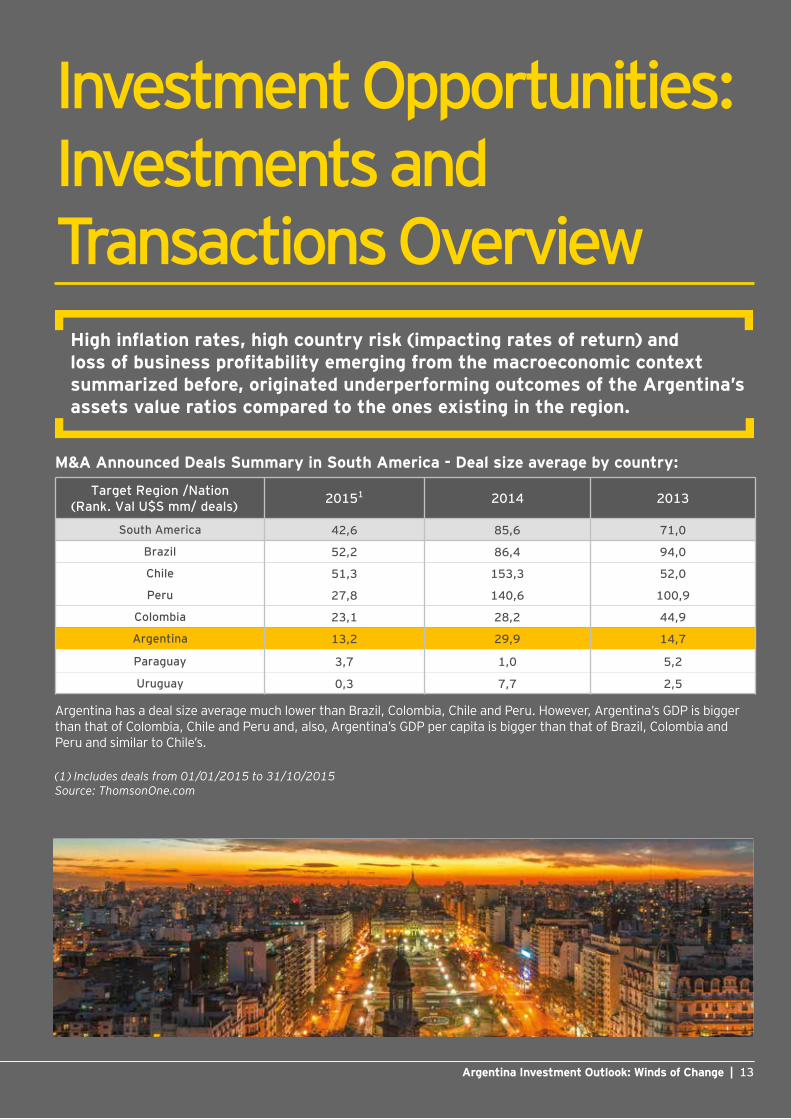

High inflation rates, high country risk (impacting rates of return) and loss of business profitability emerging from the macroeconomic context summarized before, originated underperforming outcomes of the Argentina’s assets value ratios compared to the ones existing in the region.

M&A Announced Deals Summary in South America - Deal size average by country:

Target Region /Nation (Rank. Val U$S mm/ deals) 20151 2014 2013

South America 42,6 85,6 71,0

Brazil 52,2 86,4 94,0

Chile 51,3 153,3 52,0

Peru 27,8 140,6 100,9

Colombia 23,1 28,2 44,9

Argentina 13,2 29,9 14,7

Paraguay 3,7 1,0 5,2

Uruguay 0,3 7,7 2,5

Argentina has a deal size average much lower than Brazil, Colombia, Chile and Peru. However, Argentina’s GDP is bigger than that of Colombia, Chile and Peru and, also, Argentina’s GDP per capita is bigger than that of Brazil, Colombia and Peru and similar to Chile’s.

(1) Includes deals from 01/01/2015 to 31/10/2015Source: ThomsonOne.com

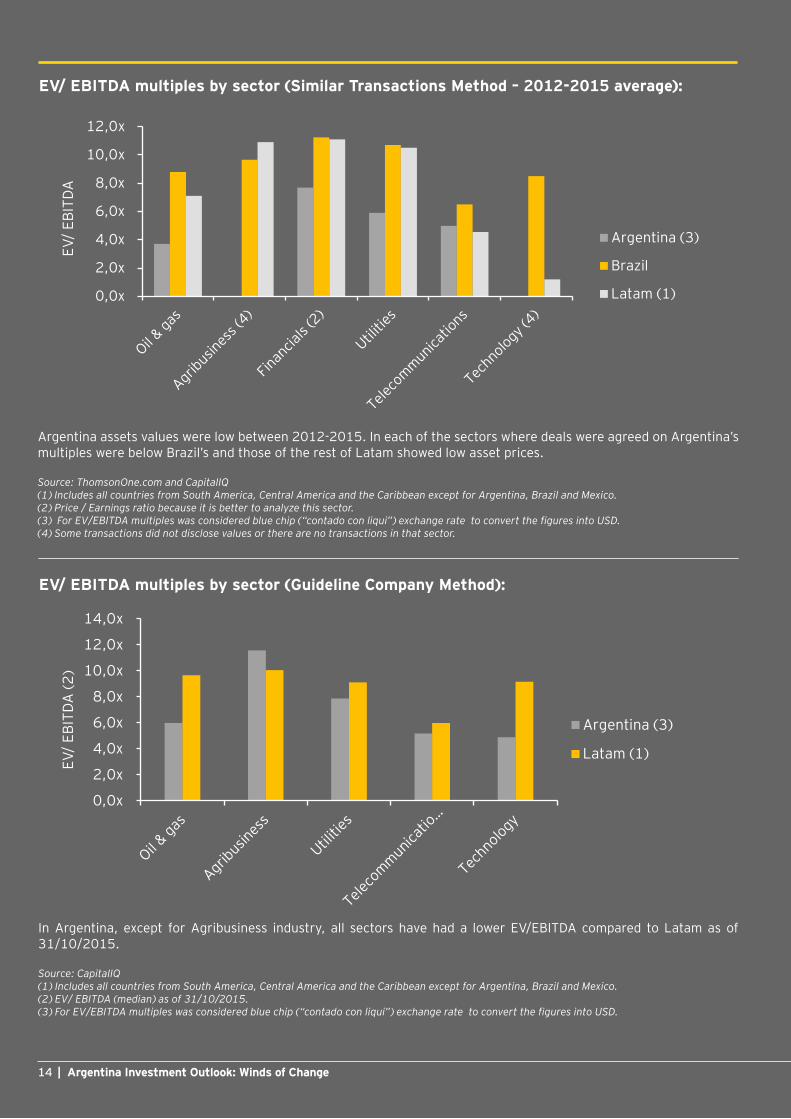

EV/ EBITDA multiples by sector (Similar Transactions Method – 2012-2015 average):

0,0x

2,0x

4,0x

6,0x

8,0x

10,0x

12,0x

Argentina (3)

Brazil

Latam (1)

EV/

EBIT

DAEV

/ EB

ITDA

(2)

Argentina assets values were low between 2012-2015. In each of the sectors where deals were agreed on Argentina’s multiples were below Brazil’s and those of the rest of Latam showed low asset prices.

Source: ThomsonOne.com and CapitalIQ(1) Includes all countries from South America, Central America and the Caribbean except for Argentina, Brazil and Mexico.(2) Price / Earnings ratio because it is better to analyze this sector.(3) For EV/EBITDA multiples was considered blue chip (“contado con liqui”) exchange rate to convert the figures into USD.(4) Some transactions did not disclose values or there are no transactions in that sector.

In Argentina, except for Agribusiness industry, all sectors have had a lower EV/EBITDA compared to Latam as of 31/10/2015.

Source: CapitalIQ(1) Includes all countries from South America, Central America and the Caribbean except for Argentina, Brazil and Mexico.(2) EV/ EBITDA (median) as of 31/10/2015.(3) For EV/EBITDA multiples was considered blue chip (“contado con liqui”) exchange rate to convert the figures into USD.

EV/ EBITDA multiples by sector (Guideline Company Method):

0,0x

2,0x

4,0x

6,0x

8,0x

10,0x

12,0x

14,0x

Argentina (3)

Latam (1)

14 | Argentina Investment Outlook: Winds of Change

15Argentina Investment Outlook: Winds of Change |

Sect

ors’

Outlo

ok

During the last years, the political and economic conditions established an uncertain and risky scenario for businesses in Argentina. As we have seen from recent transactions, these conditions have caused asset prices in Argentina to be very low compared to those of the rest of LATAM region. In this new scenario of improved conditions and expectations, asset prices that are still underpriced represent a great opportunity for investors.

The following is a summary of the most promising sectors in Argentina.

Infrastructure and Development of Regional economies Argentina is implementing the most ambitious plan in the history of the country, fostering growth and development. The aims of this plan are: enhance productive corridors, develop domestic air market, create new opportunities, improve the quality of public transport and diversify logistics matrix. More than USD 75 bn of investments are expected in the following categories: Roads and Highways (USD 25 bn); Water and Sewage (USD 20 bn), Railway Freight Lines (USD 15 bn), Real Estate and Housing (USD 10 bn), Cellular Networks (USD 5 bn); and, Airports and Ports (USD 2 bn).

Macri’s administration has defined specific programs in relation to this ambitious plan. The Belgrano Plan, aiming at building infrastructure and encouraging industry development in ten of Argentina’s underdeveloped northern provinces, includes an investment of USD 16 bn over the course of 10 years, “historical reconstruction fund” of ARS 50 bn to be used in 4 years, housing for 250,000 families, and the construction of 1,400 child care centers. The Inter-American Development Bank (IADB) is going to finance this plan and help the Government meet its goals of improving infrastructure and reducing poverty.

The Government also announced the construction of transport tunnels beneath the Andes seeking to improve the volume of exports from Argentina, Brazil, Paraguay and Uruguay to the Pacific through better logistic connection with Chile. It also announced its commitment to the completion of the civil works such as the path of the oil, Añelo hospital, roads, housing and infrastructure links and the sewage treatment plant effluent of Rincon de los Sauces, agreed upon in the YPF-Chevron agreement, totaling AR$ 1,000 million.

Oil and gas Regardless of low international prices, development of hydrocarbons is still considered a great opportunity for the economy since Argentina has one of the main shale oil and shale gas reservoirs in the world. The discovery of Vaca Muerta and partnerships between YPF and foreign companies have further improved the grounds for the development of the sector.

On March 11, 2016 the energy ministry said the exporters of heavy crude from Argentina will receive a USD 7.50 per barrel subsidy from the government as long as international prices remain under USD 47.50 per barrel. The policy was announced as Argentina’s new government seeks foreign investment to help jumpstart a stagnant economy.

Investments in unconventional are expected to reach over USD 20 bn.

16 | Argentina Investment Outlook: Winds of Change

Renewable energyWith just 295 MW of installed wind capacity at the end of 2014 and just 10 MW of installed solar PV capacity and heavily dependent on home-produced fossil fuels, which have been kept artificially cheap by government subsidies, wind and solar together produce less than 0.5% of Argentina’s power mix.

According to a research from the US’ National Renewable Energy Research Laboratory (NREL), Argentina’s gross solar resource could amount to as much as 7853 TWh/y, the 11th highest in the world. But the biggest opportunity for Argentina lies in wind power, possessing one of the world’s most promising wind resources.

In October 2015, the previous administration passed the Renewable Energy Law (27.091) and, in March 2016, the law’s regulatory decree (531) was published. The law sets renewable energy consumption targets (8% by the end of 2017, rising by 4% every two years to reach 20% by 2025). According to the CADER (Cámara Argentina de Energía Renovable), Argentina’s renewable energy chamber, the country will need 7 GW of new installed capacity by 2021. Around 2-3 GW will be necessary to meet the 8% target (requiring USD5 bn in capital investment), and 10GW to meet the 20% target (requiring a total USD15-20 bn in capital investment).

It also establishes a government trust fund, Fondo para el Desarrollo de Energías Renovables (FODER), to support financing for new renewables projects or expanding existing ones. Capital for this fund is expected to come from the national treasury, consumers, individual investors, pension funds and the recovery of principal and interest of loans granted.

Decree 531 proposes the following tax benefits: accelerated depreciation on assets, value-added tax rebate available on the purchase, manufacture and import of new capital equipment and construction; non-operating losses may be rolled for 10 fiscal years, exemption from corporate tax on assets-generated dividends (upon reinvestment in infrastructure); among others.

The first tender for renewable energy (RenovAr) has been launched with the objective to add to the country’s energy supply 1 GW of power within two years, with an estimated USD 1,500 -2,000 million of investment. Through the auction, the country will add to the grid: 600 MW from wind energy, 300 MW from solar energy, 65MW from biomass, 20 MW from small dams and 15 MW from biogas.

Utilities / Hydro, Thermal and Nuclear Power The subsidy policy, along with the refusal to grant rate increases to utilities’ companies became two of the most important political statements for the “kirchnerismo”. Macri’s government is set to gradually raise these prices in order to partially rebuild earnings of companies and promote investments.

The government declared an electricity emergency in December 2017. As a result of this, Energy and Mining Minister, Juan José Aranguren, cut electricity subsidies.

Recently, the national government launched an auction for thermal generation for the wholesale market. The deal of USD 170 million signed between YPF and General Electric for the construction of an electric generator plant in the northern province of Tucuman is the most important of those selected in the bidding process. The plant will have a capacity of 260 MW and would provide 10,000 direct and indirect jobs in the coming years. Miguel Gutierrez, president of YPF, said that the company is moving toward being an integral energy company.

As part of the energy plan 2015-2019, the government has developed preliminary plans for diversifying the country’s energy matrix by 2025. Around 8 GW will be necessary to meet the 43% target in thermal power, 1.5 GW in nuclear power to reach the target of 10%, and, 3 GW in hydro power to meet the 27% target.

Investments in hydro and thermal power are expected to reach above USD 20 bn.

MiningOn February 2016, Argentine President Mauricio Macri eliminated a 5% tax imposed by the previous administration on mining exports. In Argentina there is around USD14.5bn in mining projects pending and the changes Macri is implementing could see investment start to flow as the business environment improves for miners. The opportunities are not only in the most traditional metals like gold, silver or copper. Lithium and potassium also offer enormous opportunities for future development.

Sect

ors’

Outlo

ok

17Argentina Investment Outlook: Winds of Change |

Agribusiness

Agribusiness is considered a critical engine for the country and to ensure the rebound of this sector, the Government eliminated the export taxes on all agricultural, cattle, fishery and industrial products, with the exception of soybeans, whose tax was reduced by 5 p.p., export taxes for soybeans are now set at 30%, and taxes for soybeans derivatives at 27%.

In this context, wheat will be one of producers’ larger bets. Historically, wheat was seen as the crop to turn into cash at the end of the year.

According to experts, by eliminating/reducing the taxes, total annual production could boost from 100 millions to 180 million tons of grain and soybeans by 2025. Investments in land development with irrigation are expected to be over USD 8 bn and forestry and pulp industry of over USD 2.5 bn.

Meat productionMeat production, currently underdeveloped, could become a genuine new source of foreign exchange since the sector has a strong orientation towards international trade and is highly reputed around the world. Restrictions imposed by the “kirchnerismo” caused the sector to shrink but new foreign trade policies should enable it to regain previous output levels as it becomes easier to import or retain heifers.

Investments in food industrialization are expected to be over USD 0.5 bn and in animal protein (beef, pork, poultry) of over USD 5 bn.

Knowledge-based services Knowledge-based services is a field characterized by a highly qualified labor force and the use of advanced technologies, which also enable the provision of long distance services, such as business services (accounting, finance, HR, etc.), health (telemedicine and diagnostics, medical tourism, etc.), creative industries (audiovisual, advertising, architecture, etc.) and computer (software development, computer services, application development, networking, video, animation, etc.), among others.

These sectors experienced rapid growth by leveraging the services offshoring boom that occurred globally and cheaper labor cost after the devaluation of 2001. It also promised to continue to grow fast and above GDP, taking into account the comparative advantages of Argentina in this sector, a skilled labor with competitive salaries.

Investments of over USD 2 bn are expected in this sector.

BanksEven though Banks are expected to be subjected to new and stricter regulations, they face a favorable scenario for growth. The ratio of loans to GDP is 15% while that of the rest of the region is close to 38%. If Argentina were to equate its leverage ratio to that of the region, it would have to double its loan value. In other words, it has the potential to double the size of the system.

With interest rates raising above 32% annually, investors are returning to the argentine peso as it offers a positive real rate of return.

Sect

ors’

Outlo

ok

18 | Argentina Investment Outlook: Winds of Change

Investments and Transactions RationaleCurrent acquisition rationale for investors in Argentina:

• Highly attractive assets value compared with other countries in the region. High room to capture value in the future.

• Many family-owned middle-market companies

• Great need for infrastructure development

• A wealth of raw material, workforce highly-skilled and competitive with good level of education and a human development indicator significantly above the Latin American average

• New professional and market-oriented government

• Access to MERCOSUR: Non-tariff barriers with other South American countries. Argentina, Brazil, Paraguay and Uruguay – which are plenary members – with associated countries such as Bolivia, Chile, Colombia, Ecuador, Peru and Venezuela

• Certain industries with high growth potential. The sectors providing the best opportunities are: Infrastructure, Oil and gas, Renewable energy, Utilities, Mining, Agribusiness, Meat production, Knowledge-based services, and Banks.

Sect

ors’

Outlo

ok Public – Private Partnerships Bill• At the 14th Latin American Infrastructure Leadership Forum, the Minister of Interior Affairs, Public

Works and Housing, Rogelio Frigerio, said that the government faces “the most ambitious infrastructure development plan in history” and estimated that the objective is to invest 6 percentage points of GDP per year.

• “With that goal ahead, the Minister highlighted, we are creating the conditions for the private sector to regain trust in the country and to help us trace a path of growth with genuine and high quality job creation.”

• To reach an annual growth level of 4% or 5%, sustainable over many years, it is necessary to invest at least 5 points of GDP in infrastructure which would represent an investment of USD 26,500 million per year. Frigerio admitted the country is far from that goal because investment in recent years was less than 3 points of GDP. Concerning the situation inherited from the previous government, Frigerio recalled that, in the first quarter, the current administration had to update the enormous existing debt related to projects of national and province infrastructure which amounted to nearly USD 10,000 million.

• In the coming weeks, the government will send a bill in Congress to promote public-private partnerships hoping to increase investment. With the initiative, Mauricio Macri’s administration expects to capture USD 5,000 million during the first year, to be allocated to infrastructure and services, productive investment, applied research and / or technological innovation. According to Reyser, Macri’s adviser on foreign investment, “this need to be seen as an additional source of financing that can generate efficiency and transparency in infrastructure projects”.

• The draft bill lays down a general regulatory framework that allows the private sector to partner with the State for investment projects through different mechanisms to be defined for each particular initiative. The State may obtain a majority or minority stake in the project through funding, granting of permits and guarantees or some other configuration. Also, both parts may become partners and take the same risks giving private companies the opportunity to finance those projects at lower costs.

19Argentina Investment Outlook: Winds of Change |

Our purpose: committed to building a better working world• At EY, we are committed to building a better working world with increased trust and confidence in business, sustainable

growth, development of talent in all its forms, and greater collaboration.

• We want to build a better working world through our own actions and by engaging with like-minded organizations and individuals. This is our purpose and why we exist as an organization.

• EY headcount is around 210,000 employees all over the world and with combined global revenues of US$27.4b, EY’s financial success allows us to make investments in our people and business.

• We are a global organization, unified in our approach. Our global structure means we can respond faster than our competitors. We can access the right people and assemble high-performing teams to deliver exceptional client service worldwide.

• EY is located in more than 700 offices in more than 150 countries. Our 28 Regions are grouped into four Geographic Areas: Americas; Europe, Middle East, India and Africa; Asia-Pacific; Japan. This structure is streamlined allowing us to provide exceptional client services wherever in the world our clients do business.

EY in Argentina • Throughout more than 50 years of continual growth

in Argentina, EY is a leading professional services firm with over 2,100 employees. With offices in Buenos Aires and Cordoba and over 1,000 clients, we play a lead role in the business world and in our community.

• EY multidisciplinary teams are formed by professionals with vast and proven experience in their fields, who share a comprehensive vision of their task. They are doubly specialized: by service line and by industry. That enables us to offer unique solutions to our clients.

TAS Team• We help to create social and economic value for

our clients by helping them make more informed decisions about strategically managing capital and transactions.

• We advise on strategies to raise, invest, optimize and preserve capital. Our teams bring together transaction professionals across functional areas, sectors and geographies to evaluate your Capital Agenda.

• Our goal is to help businesses achieve the best capital performance, deliver value to stakeholders and meet strategic corporate objectives.

2100employeesBuenos & Cordoba

Why EY?

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Pistrelli, Henry Martin y Asociados S.R.L. is a client-serving member firm of Ernst & Young Global Limited operating in Argentina.

© 2016 EYGM Limited. All Rights Reserved.

EYG no. CE0944ED NoneThis material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com/ccb