are you saving enough for a brighter...

TRANSCRIPT

Regd. Office: 6th Floor, Vaman Centre, Makhwana Road, Off Andheri-Kurla Road, Near Marol Naka, Andheri (East), Mumbai 400 059. Reg. No. 109 Unique No.: 109N042V01ADV/02/08-09/3174 VER 2/JUNE /2009

Guaranteed Bachat Plan

Birla Sun Life Insurance

Encourages regular saving with guaranteeand opportunity to earn more

Are you saving enoughfor a brighter tomorrow?

Call Toll-free: 1-800-270-7000 www.birlasunlife.com sms ‘DHAN’ to 56161

BSLI GUARANTEED BACHAT PLAN

You are the head of your family and your family looks up to you for providing them their

dreams and their future. Your hard earned money may not be enough to meet all the

demands of today and tomorrow.

BSLI Guaranteed Bachat Plan, a non-participating endowment plan, is our answer to

many of your needs. The BSLI Guaranteed Bachat Plan offers:

Growth and Liquidity: The plan offers you a chance to earn survival benefit at the rdend of each policy year, from the 3 year onwards. The survival benefit can be

withdrawn by you or can be used to pay the premium dues

Guaranteed Returns: At maturity, your policy returns you an amount equal to your

Guaranteed Maturity Benefit, plus your survival benefits. The Guaranteed Maturity

Benefit is based on your current age and the policy term, and is greater than all

base premiums paid. The younger you are and the longer you wish to stay, the

higher is the guarantee

Increasing Life cover: Every policy anniversary, as a mark of loyalty, the plan

increases your existing cover by an amount equal to the annual base premium.

As a result, with successive years, your cover increases thus offering you

increasing safety

•

•

•

•

•

•

•

Early Exit Option: If ever you are required to exit this plan earlier, there is an early

exit option available, which reduces your Guaranteed Maturity Benefit and returns

you the reduced Guaranteed Maturity Benefit along with all your accumulated

survival benefit

We believe that, as a discerning customer, you deserve to get the best out of every

savings plan and we are happy to bring you BSLI Guaranteed Bachat Plan which

comes with unparalleled benefits never seen before.

This plan has been designed for you, if you are:

60 years of age or younger. This plan cannot be sold to less than 30 days old

babies

Looking to invest for more than 10 years subject to a minimum maturity age of

18 years. The maximum term for this product is [70 - your current age] subject to

a maximum of 40 years

Looking to invest at least Rs. 3,600 per annum. You can choose your annual

base premiums only in multiples of Rs. 1,200 per annum subject to maximum

annual base premium of Rs. 8,400

The survival benefit under BSLI Guaranteed Bachat Plan is linked to your annual

base premium.

Please note that you may choose to pay any premium in multiples of Rs. 1,200 per

annum over a minimum annual base premium of Rs. 3,600. You may also choose

to pay your premiums annually, half yearly, quarterly or monthly, as per your

convenience. Your annual premium will be multiplied by 0.510, 0.258 or 0.087,

in case if you opt for paying it half yearly, quarterly or monthly respectively.

Service Tax & Education Cess and any other applicable taxes will be added to your

premium and levied as per the extant tax laws.

IS BSLI GUARANTEED BACHAT PLAN RIGHT FOR ME?

PREMIUMS AND SURVIVAL BENEFIT BANDS

Annual Premium Annual Base Premium Survival Band Range Benefit

Band 1 Rs. 3,600 – Rs. 4,800 Base Survival Benefit

15% extra overBand 2 Rs. 6,000 – Rs. 8,400

Base Survival Benefit

BSLI GUARANTEED BACHAT PLAN

You are the head of your family and your family looks up to you for providing them their

dreams and their future. Your hard earned money may not be enough to meet all the

demands of today and tomorrow.

BSLI Guaranteed Bachat Plan, a non-participating endowment plan, is our answer to

many of your needs. The BSLI Guaranteed Bachat Plan offers:

Growth and Liquidity: The plan offers you a chance to earn survival benefit at the rdend of each policy year, from the 3 year onwards. The survival benefit can be

withdrawn by you or can be used to pay the premium dues

Guaranteed Returns: At maturity, your policy returns you an amount equal to your

Guaranteed Maturity Benefit, plus your survival benefits. The Guaranteed Maturity

Benefit is based on your current age and the policy term, and is greater than all

base premiums paid. The younger you are and the longer you wish to stay, the

higher is the guarantee

Increasing Life cover: Every policy anniversary, as a mark of loyalty, the plan

increases your existing cover by an amount equal to the annual base premium.

As a result, with successive years, your cover increases thus offering you

increasing safety

•

•

•

•

•

•

•

Early Exit Option: If ever you are required to exit this plan earlier, there is an early

exit option available, which reduces your Guaranteed Maturity Benefit and returns

you the reduced Guaranteed Maturity Benefit along with all your accumulated

survival benefit

We believe that, as a discerning customer, you deserve to get the best out of every

savings plan and we are happy to bring you BSLI Guaranteed Bachat Plan which

comes with unparalleled benefits never seen before.

This plan has been designed for you, if you are:

60 years of age or younger. This plan cannot be sold to less than 30 days old

babies

Looking to invest for more than 10 years subject to a minimum maturity age of

18 years. The maximum term for this product is [70 - your current age] subject to

a maximum of 40 years

Looking to invest at least Rs. 3,600 per annum. You can choose your annual

base premiums only in multiples of Rs. 1,200 per annum subject to maximum

annual base premium of Rs. 8,400

The survival benefit under BSLI Guaranteed Bachat Plan is linked to your annual

base premium.

Please note that you may choose to pay any premium in multiples of Rs. 1,200 per

annum over a minimum annual base premium of Rs. 3,600. You may also choose

to pay your premiums annually, half yearly, quarterly or monthly, as per your

convenience. Your annual premium will be multiplied by 0.510, 0.258 or 0.087,

in case if you opt for paying it half yearly, quarterly or monthly respectively.

Service Tax & Education Cess and any other applicable taxes will be added to your

premium and levied as per the extant tax laws.

IS BSLI GUARANTEED BACHAT PLAN RIGHT FOR ME?

PREMIUMS AND SURVIVAL BENEFIT BANDS

Annual Premium Annual Base Premium Survival Band Range Benefit

Band 1 Rs. 3,600 – Rs. 4,800 Base Survival Benefit

15% extra overBand 2 Rs. 6,000 – Rs. 8,400

Base Survival Benefit

3

GROWTH & LIQUIDITY – THE POWER OF SURVIVAL BENEFITS

rdAt the end of every policy year, starting from the 3 year, you will earn a survival benefit

calculated as your total base premiums paid till date multiplied by:

4.25% + 60% of any excess of the GSec rate over 7.50%; or

4.25% – 75% of any excess of the 7.50% over the GSec rate

At the beginning of each policy year, your policy will be assigned the latest GSec rate

declared by us and your year-end survival benefit will be based on this GSec rate,

irrespective of any change in interest rates during the policy year.

stWe will declare the GSec rate at the beginning of each calendar quarter (the 1 of

January, April, July and October) and it will equal the average of the daily 10-year

Constant Maturity Treasury annual yields, as calculated by Bloomberg, recorded over

the last calendar quarter.

Your survival benefit is therefore based on the prevailing 10-year Government of India

Security at the beginning of the policy year. You will enjoy 60% of any upside interest

movement and be protected on the downside by having your survival benefit reduced

by only 75% of the downside interest movement. For example:

Your survival benefit will be increased by 15% at higher premiums for annual premium

band 2.

The survival benefit will be calculated at the end of every policy year and credited to

your policy's accumulated survival benefits. The accumulated survival benefits

balance is available for you to:

Make cash withdrawals, subject to a minimum of Rs. 2,500

Offset future premiums, provided your accumulated survival benefits are higher

than your annual premium

Any accumulated survival benefits will be payable on maturity, surrender or death.

•

•

•

•

GSec Rate Downside/Upside Adjustment Survival Benefit Rate

7.50% --- 4.25%

5.50% – 75% x 2.00% = – 1.50% 2.75%

9.50% + 60% x 2.00% = + 1.20% 5.45%

3

GROWTH & LIQUIDITY – THE POWER OF SURVIVAL BENEFITS

rdAt the end of every policy year, starting from the 3 year, you will earn a survival benefit

calculated as your total base premiums paid till date multiplied by:

4.25% + 60% of any excess of the GSec rate over 7.50%; or

4.25% – 75% of any excess of the 7.50% over the GSec rate

At the beginning of each policy year, your policy will be assigned the latest GSec rate

declared by us and your year-end survival benefit will be based on this GSec rate,

irrespective of any change in interest rates during the policy year.

stWe will declare the GSec rate at the beginning of each calendar quarter (the 1 of

January, April, July and October) and it will equal the average of the daily 10-year

Constant Maturity Treasury annual yields, as calculated by Bloomberg, recorded over

the last calendar quarter.

Your survival benefit is therefore based on the prevailing 10-year Government of India

Security at the beginning of the policy year. You will enjoy 60% of any upside interest

movement and be protected on the downside by having your survival benefit reduced

by only 75% of the downside interest movement. For example:

Your survival benefit will be increased by 15% at higher premiums for annual premium

band 2.

The survival benefit will be calculated at the end of every policy year and credited to

your policy's accumulated survival benefits. The accumulated survival benefits

balance is available for you to:

Make cash withdrawals, subject to a minimum of Rs. 2,500

Offset future premiums, provided your accumulated survival benefits are higher

than your annual premium

Any accumulated survival benefits will be payable on maturity, surrender or death.

•

•

•

•

GSec Rate Downside/Upside Adjustment Survival Benefit Rate

7.50% --- 4.25%

5.50% – 75% x 2.00% = – 1.50% 2.75%

9.50% + 60% x 2.00% = + 1.20% 5.45%

At your policy maturity, you will receive an amount equal to the Guaranteed Maturity

Benefit PLUS your accumulated survival benefits. The Guaranteed Maturity Benefit

(GMB) is linked to your age at entry and the policy term. To reiterate, the GMB is higher

for lower age and higher policy terms. Needless to say, you should start now and

save for as long as you can. Please refer to the table below for sample Guaranteed

Maturity Benefit per Rs. 1,200 annual base premium:

For exact Guaranteed Maturity Benefits at other combinations of your age and policy

term, please refer to our website or contact us.

There is a detailed illustration on the last page of the brochure which you mayrefer for ease of understanding.

The minimum life cover in this plan is five times the annual base premium. However, in

this policy, on every policy anniversary, your life cover will be increased by an amount

equal to your annual base premium.

In the case of the unfortunate event of death of the life insured, we will pay your nominee

an amount equal to 5 times your annual base premium plus all base premiums paid till

date (excluding the first year premium) PLUS all accumulated survival benefits.

Preponement of Maturity: In the unfortunate situation that you need to prepone

your maturity, you will receive your Guaranteed Maturity Benefit minus Early

Maturity Adjustment PLUS your accumulated survival benefits

•

Guaranteed

Maturity

Benefit

YOUR PREMIUMS ASSURED - THE POWER

OF GUARANTEED MATURITY BENEFIT

Guaranteed

Death

Benefit

SAFETY TO YOUR DREAMS – THE POWER

OF INCREASING LIFE COVER

Guaranteed

Surrender

Benefit

PREPONEMENT OF MATURITY AND

SURRENDER OF BENEFITS

Policy TermEntry Age

10 15 20 25 30

20 12,552 19,658 26,432 34,650 44,082

30 12,536 19,612 26,329 34,491 43,901

35 12,506 19,540 26,175 34,253 43,604

40 12,444 19,394 25,881 33,791 42,998

45 12,332 19,140 25,362 32,916 ---

50 12,139 18,700 26,071 --- ---

55 12,000 18,917 --- --- ---

60 12,000 --- --- --- ---

Annual Base 12,000 18,000 24,000 30,000 36,000Premiums Paid

This early maturity adjustment is equal to 1.2% for each year by which you want to

advance the maturity. There will be no deduction for early maturity after you havecompleted 20 policy years.

You cannot prepone your policy's maturity if your policy hasn't completed ten years.

Example: If a 25 years policy needs to be preponed to 15 years, your guaranteed

maturity amount will correspond to 15 years (not 25 years).

The early maturity adjustment of 1.2% will be applied on 5 years only as after 20

years there is no such deduction made i.e. 1.2% (20-15) years. This amounts to a

deduction of 6% from your guaranteed maturity amount.

Thus, you stand to receive 94% of Guaranteed Maturity Benefit corresponding to

15 years.

Surrender Benefits: In the unfortunate situation that you have to surrender

your policy before completion of 10 policy years, you will receive the base

premiums paid by you multiplied by a percentage as indicated below PLUS

accumulated survival benefits

Policy will acquire a surrender benefit only if premiums for full 3 years have been paid.

There is a detailed illustration on the last page of the brochure which you mayrefer for ease of understanding.

•

Policy Year of Surrender

0% 25% 30% 35% 45% 55% 65% 75% 85%

1-2 3 4 5 6 7 8 9 10

At your policy maturity, you will receive an amount equal to the Guaranteed Maturity

Benefit PLUS your accumulated survival benefits. The Guaranteed Maturity Benefit

(GMB) is linked to your age at entry and the policy term. To reiterate, the GMB is higher

for lower age and higher policy terms. Needless to say, you should start now and

save for as long as you can. Please refer to the table below for sample Guaranteed

Maturity Benefit per Rs. 1,200 annual base premium:

For exact Guaranteed Maturity Benefits at other combinations of your age and policy

term, please refer to our website or contact us.

There is a detailed illustration on the last page of the brochure which you mayrefer for ease of understanding.

The minimum life cover in this plan is five times the annual base premium. However, in

this policy, on every policy anniversary, your life cover will be increased by an amount

equal to your annual base premium.

In the case of the unfortunate event of death of the life insured, we will pay your nominee

an amount equal to 5 times your annual base premium plus all base premiums paid till

date (excluding the first year premium) PLUS all accumulated survival benefits.

Preponement of Maturity: In the unfortunate situation that you need to prepone

your maturity, you will receive your Guaranteed Maturity Benefit minus Early

Maturity Adjustment PLUS your accumulated survival benefits

•

Guaranteed

Maturity

Benefit

YOUR PREMIUMS ASSURED - THE POWER

OF GUARANTEED MATURITY BENEFIT

Guaranteed

Death

Benefit

SAFETY TO YOUR DREAMS – THE POWER

OF INCREASING LIFE COVER

Guaranteed

Surrender

Benefit

PREPONEMENT OF MATURITY AND

SURRENDER OF BENEFITS

Policy TermEntry Age

10 15 20 25 30

20 12,552 19,658 26,432 34,650 44,082

30 12,536 19,612 26,329 34,491 43,901

35 12,506 19,540 26,175 34,253 43,604

40 12,444 19,394 25,881 33,791 42,998

45 12,332 19,140 25,362 32,916 ---

50 12,139 18,700 26,071 --- ---

55 12,000 18,917 --- --- ---

60 12,000 --- --- --- ---

Annual Base 12,000 18,000 24,000 30,000 36,000Premiums Paid

This early maturity adjustment is equal to 1.2% for each year by which you want to

advance the maturity. There will be no deduction for early maturity after you havecompleted 20 policy years.

You cannot prepone your policy's maturity if your policy hasn't completed ten years.

Example: If a 25 years policy needs to be preponed to 15 years, your guaranteed

maturity amount will correspond to 15 years (not 25 years).

The early maturity adjustment of 1.2% will be applied on 5 years only as after 20

years there is no such deduction made i.e. 1.2% (20-15) years. This amounts to a

deduction of 6% from your guaranteed maturity amount.

Thus, you stand to receive 94% of Guaranteed Maturity Benefit corresponding to

15 years.

Surrender Benefits: In the unfortunate situation that you have to surrender

your policy before completion of 10 policy years, you will receive the base

premiums paid by you multiplied by a percentage as indicated below PLUS

accumulated survival benefits

Policy will acquire a surrender benefit only if premiums for full 3 years have been paid.

There is a detailed illustration on the last page of the brochure which you mayrefer for ease of understanding.

•

Policy Year of Surrender

0% 25% 30% 35% 45% 55% 65% 75% 85%

1-2 3 4 5 6 7 8 9 10

OTHER QUESTIONS THAT YOU MAY HAVE:

What will happen if, due to some reason, I am unable to pay my premium on time?

Can I get loans against my policy?

What are the tax benefits that I get on this policy?

What is the option that I have if in case I change my mind after buying the

policy?

If you are unable to pay the premium by the due date, you will be given a grace period

of 30 days and during this grace period, all coverages under your policy will continue.

If you do not pay your premium within the grace period, the following will be applicable:

(a) In case your policy has not acquired a surrender benefit, then all benefits under

your policy will cease immediately.

(b) In case your policy has acquired a surrender benefit, then your policy will be

continued on a reduced paid-up basis.

You can reinstate your policy for its full coverage within two-years from the due date

of the unpaid premium by paying all outstanding premiums together with interest as

declared by us from time to time and by providing evidence of insurability satisfactory

to us.

Yes, you are allowed to get policy loans once the policy acquires a surrender benefit.

The minimum policy loan is Rs. 5,000 and the maximum is 90% of the surrender

benefit. Interest, at a rate declared by us from time to time, will be charged against any

outstanding loans.

Any outstanding loan balance will be recovered by us from policy proceeds due for

payment and will be deducted before any benefit is paid under the policy.

You will be eligible for tax benefits under Section 80C and Section 10(10D) of the

Income Tax Act, 1961. Presently,

Under Section 80C, premiums up to Rs. 100,000 are allowed as a deduction from

your taxable income, each year

Under Section 10(10D), the benefits you receive from this plan are exempt from

tax, subject to mentioned exclusions

You will have the right to return your policy to us within 15 days from the date of receipt

of the policy. We will refund all premiums paid till date once we receive your written

notice of cancellation (along with reasons thereof) together with the original policy

documents. Depending on our then current administration rules, we may reduce

the amount of the refund by expenditures incurred by us in issuing your policy and

as permitted by the IRDA and in accordance to IRDA (Protection of Policyholders’

Interest) Regulations, 2002.

•

•

OTHER QUESTIONS THAT YOU MAY HAVE:

What will happen if, due to some reason, I am unable to pay my premium on time?

Can I get loans against my policy?

What are the tax benefits that I get on this policy?

What is the option that I have if in case I change my mind after buying the

policy?

If you are unable to pay the premium by the due date, you will be given a grace period

of 30 days and during this grace period, all coverages under your policy will continue.

If you do not pay your premium within the grace period, the following will be applicable:

(a) In case your policy has not acquired a surrender benefit, then all benefits under

your policy will cease immediately.

(b) In case your policy has acquired a surrender benefit, then your policy will be

continued on a reduced paid-up basis.

You can reinstate your policy for its full coverage within two-years from the due date

of the unpaid premium by paying all outstanding premiums together with interest as

declared by us from time to time and by providing evidence of insurability satisfactory

to us.

Yes, you are allowed to get policy loans once the policy acquires a surrender benefit.

The minimum policy loan is Rs. 5,000 and the maximum is 90% of the surrender

benefit. Interest, at a rate declared by us from time to time, will be charged against any

outstanding loans.

Any outstanding loan balance will be recovered by us from policy proceeds due for

payment and will be deducted before any benefit is paid under the policy.

You will be eligible for tax benefits under Section 80C and Section 10(10D) of the

Income Tax Act, 1961. Presently,

Under Section 80C, premiums up to Rs. 100,000 are allowed as a deduction from

your taxable income, each year

Under Section 10(10D), the benefits you receive from this plan are exempt from

tax, subject to mentioned exclusions

You will have the right to return your policy to us within 15 days from the date of receipt

of the policy. We will refund all premiums paid till date once we receive your written

notice of cancellation (along with reasons thereof) together with the original policy

documents. Depending on our then current administration rules, we may reduce

the amount of the refund by expenditures incurred by us in issuing your policy and

as permitted by the IRDA and in accordance to IRDA (Protection of Policyholders’

Interest) Regulations, 2002.

•

•

TERMS AND CONDITIONS

Refund of Premiums upon Death

Prohibition of Rebates – Section 41 of the Insurance Act, 1938

Non-Disclosure – Section 45 of the Insurance Act, 1938

We will only refund base premiums paid to date in the event the life insured dies by

suicide, whether medically sane or insane, within one year after the issue or

reinstatement date, whichever is later.

We will only refund base premiums paid to date in the event the life insured dies before th the policy anniversary coinciding with or immediately following the 5 birthday of the

life insured.

No person shall allow or offer to allow, either directly or indirectly, as an inducement to

any person to take or renew or continue an insurance in respect of any kind of risk

relating to lives or property in India, any rebate of the whole or part of the commission

payable or any rebate of the premium shown on the policy, nor shall any person taking

out or renewing or continuing a policy accept any rebate, except such rebate as may

be allowed in accordance with the published prospectuses or tables of the insurer.

No policy of life insurance effected after the coming into force of this act shall, after

the expiry of two years from the date on which it was effected be called in question

by an insurer on the ground that statement made in the proposal or in any report

of a medical officer, or referee, or friend of the life insured, or in any other document

leading to the issue of the policy, was inaccurate or false, unless the insurer shows

that such statement was on a material matter or suppressed facts which it was

material to disclose and that it was fraudulently made by the policyholder and that

the policyholder knew at the time of making it that the statement was false or that it

suppressed facts which it was material to disclose.

Provided that nothing in this section shall prevent the insurer from calling for proof of

age at any time if he is entitled to do so, and no policy shall be deemed to be called in

question merely because the terms of the policy are adjusted on subsequent proof

that the age of the life insured was incorrectly stated in the application.

TERMS AND CONDITIONS

Refund of Premiums upon Death

Prohibition of Rebates – Section 41 of the Insurance Act, 1938

Non-Disclosure – Section 45 of the Insurance Act, 1938

We will only refund base premiums paid to date in the event the life insured dies by

suicide, whether medically sane or insane, within one year after the issue or

reinstatement date, whichever is later.

We will only refund base premiums paid to date in the event the life insured dies before th the policy anniversary coinciding with or immediately following the 5 birthday of the

life insured.

No person shall allow or offer to allow, either directly or indirectly, as an inducement to

any person to take or renew or continue an insurance in respect of any kind of risk

relating to lives or property in India, any rebate of the whole or part of the commission

payable or any rebate of the premium shown on the policy, nor shall any person taking

out or renewing or continuing a policy accept any rebate, except such rebate as may

be allowed in accordance with the published prospectuses or tables of the insurer.

No policy of life insurance effected after the coming into force of this act shall, after

the expiry of two years from the date on which it was effected be called in question

by an insurer on the ground that statement made in the proposal or in any report

of a medical officer, or referee, or friend of the life insured, or in any other document

leading to the issue of the policy, was inaccurate or false, unless the insurer shows

that such statement was on a material matter or suppressed facts which it was

material to disclose and that it was fraudulently made by the policyholder and that

the policyholder knew at the time of making it that the statement was false or that it

suppressed facts which it was material to disclose.

Provided that nothing in this section shall prevent the insurer from calling for proof of

age at any time if he is entitled to do so, and no policy shall be deemed to be called in

question merely because the terms of the policy are adjusted on subsequent proof

that the age of the life insured was incorrectly stated in the application.

BIRLA SUN LIFE INSURANCE – A COMING TOGETHER OF VALUES

Birla Sun Life Insurance Company Limited is a joint venture between The Aditya Birla

Group, one of the largest business houses in India and Sun Life Financial Inc.,

a leading international financial services organization. The local knowledge of the

Aditya Birla Group combined with the expertise of Sun Life Financial Inc., offers a

formidable protection for your future.

The Aditya Birla Group has a turnover of close to Rs. 119,000 crores, with a market stcapitalization of Rs. 133,875 crores (as on 31 March, 2008). It has over 100,000

employees across all its units worldwide. It is led by its Chairman - Mr. Kumar Mangalam

Birla. Some of its key companies are Hindalco, Grasim and Aditya Birla Nuvo.

Sun Life Financial Inc. and its partners, have operations in key markets worldwide.

These include Canada, the United States, the United Kingdom, Hong Kong, the

Philippines, Japan, Indonesia, India, China, and Bermuda. Sun Life Financial Inc. has stassets under management of over US$ 404.7 billion (as on 31 March, 2008).

It is a leading performer in the life insurance market in Canada.

Birla Sun Life Insurance (BSLI) has been operating for 9 years. It has contributed

significantly to the growth and development of the life insurance industry in India.

It pioneered the launch of Unit Linked Life Insurance plans amongst the private

players in India. It was the first player in the industry to sell its policies through the

Bancassurance route and through the Internet. It was the first private sector player

to introduce a Pure Term plan in the Indian market. BSLI has covered more than

2 million lives since it commenced operations and its customer base is spread

across more than 1500 towns and cities in India. The company has a capital base of stRs. 1274.5 crores as on 31 March, 2008.

BIRLA SUN LIFE INSURANCE – A COMING TOGETHER OF VALUES

Birla Sun Life Insurance Company Limited is a joint venture between The Aditya Birla

Group, one of the largest business houses in India and Sun Life Financial Inc.,

a leading international financial services organization. The local knowledge of the

Aditya Birla Group combined with the expertise of Sun Life Financial Inc., offers a

formidable protection for your future.

The Aditya Birla Group has a turnover of close to Rs. 119,000 crores, with a market stcapitalization of Rs. 133,875 crores (as on 31 March, 2008). It has over 100,000

employees across all its units worldwide. It is led by its Chairman - Mr. Kumar Mangalam

Birla. Some of its key companies are Hindalco, Grasim and Aditya Birla Nuvo.

Sun Life Financial Inc. and its partners, have operations in key markets worldwide.

These include Canada, the United States, the United Kingdom, Hong Kong, the

Philippines, Japan, Indonesia, India, China, and Bermuda. Sun Life Financial Inc. has stassets under management of over US$ 404.7 billion (as on 31 March, 2008).

It is a leading performer in the life insurance market in Canada.

Birla Sun Life Insurance (BSLI) has been operating for 9 years. It has contributed

significantly to the growth and development of the life insurance industry in India.

It pioneered the launch of Unit Linked Life Insurance plans amongst the private

players in India. It was the first player in the industry to sell its policies through the

Bancassurance route and through the Internet. It was the first private sector player

to introduce a Pure Term plan in the Indian market. BSLI has covered more than

2 million lives since it commenced operations and its customer base is spread

across more than 1500 towns and cities in India. The company has a capital base of stRs. 1274.5 crores as on 31 March, 2008.

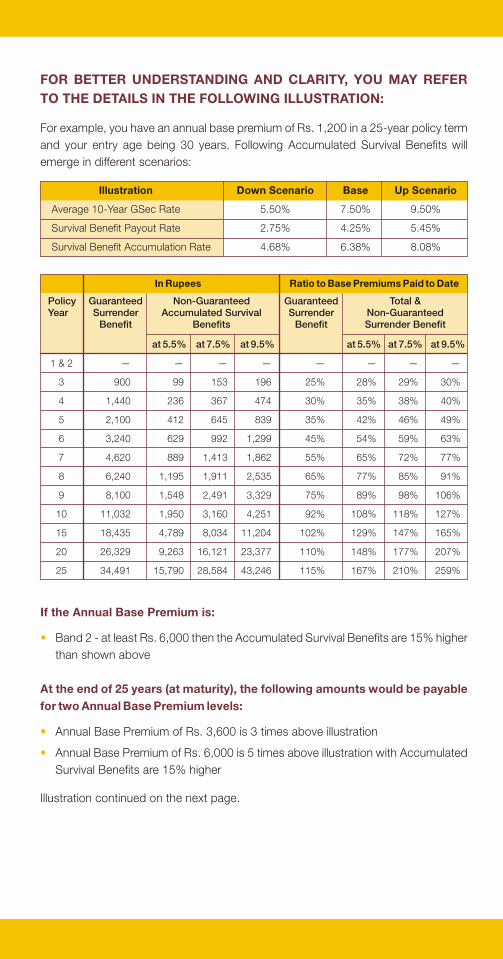

FOR BETTER UNDERSTANDING AND CLARITY, YOU MAY REFER

TO THE DETAILS IN THE FOLLOWING ILLUSTRATION:

If the Annual Base Premium is:

At the end of 25 years (at maturity), the following amounts would be payable

for two Annual Base Premium levels:

For example, you have an annual base premium of Rs. 1,200 in a 25-year policy term

and your entry age being 30 years. Following Accumulated Survival Benefits will

emerge in different scenarios:

Band 2 - at least Rs. 6,000 then the Accumulated Survival Benefits are 15% higher

than shown above

Annual Base Premium of Rs. 3,600 is 3 times above illustration

Annual Base Premium of Rs. 6,000 is 5 times above illustration with Accumulated

Survival Benefits are 15% higher

Illustration continued on the next page.

•

•

•

Illustration Down Scenario Base Up Scenario

Survival Benefit Payout Rate 2.75% 4.25% 5.45%

Survival Benefit Accumulation Rate 4.68% 6.38% 8.08%

Average 10-Year GSec Rate 5.50% 7.50% 9.50%

In Rupees Ratio to Base Premiums Paid to Date

Guaranteed Non-Guaranteed Guaranteed Total &Year Surrender Accumulated Survival Surrender Non-Guaranteed

Benefit Benefits Benefit Surrender Benefit

at 5.5% at 7.5% at 9.5% at 5.5% at 7.5% at 9.5%

1 & 2 — — — — — — — —

3 900 99 153 196 25% 28% 29% 30%

4 1,440 236 367 474 30% 35% 38% 40%

5 2,100 412 645 839 35% 42% 46% 49%

6 3,240 629 992 1,299 45% 54% 59% 63%

7 4,620 889 1,413 1,862 55% 65% 72% 77%

8 6,240 1,195 1,911 2,535 65% 77% 85% 91%

9 8,100 1,548 2,491 3,329 75% 89% 98% 106%

10 11,032 1,950 3,160 4,251 92% 108% 118% 127%

15 18,435 4,789 8,034 11,204 102% 129% 147% 165%

20 26,329 9,263 16,121 23,377 110% 148% 177% 207%

25 34,491 15,790 28,584 43,246 115% 167% 210% 259%

Policy

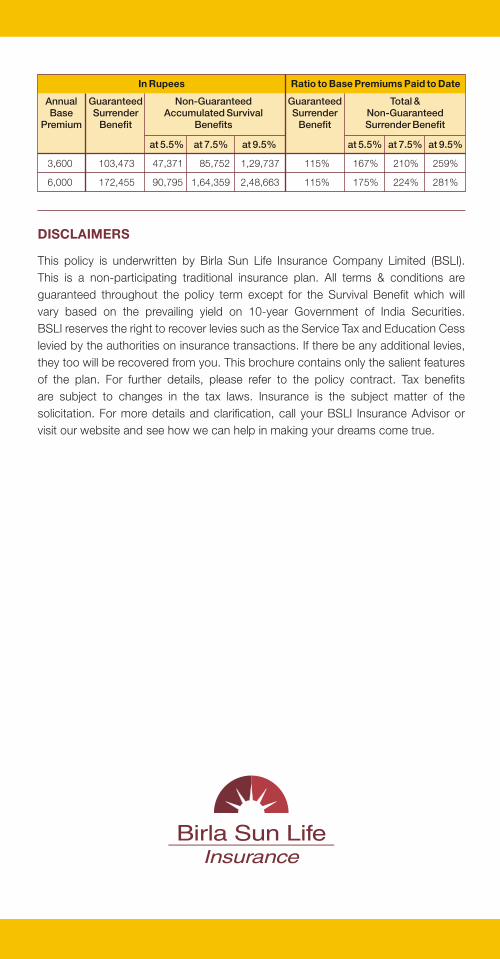

DISCLAIMERS

This policy is underwritten by Birla Sun Life Insurance Company Limited (BSLI).

This is a non-participating traditional insurance plan. All terms & conditions are

guaranteed throughout the policy term except for the Survival Benefit which will

vary based on the prevailing yield on 10-year Government of India Securities.

BSLI reserves the right to recover levies such as the Service Tax and Education Cess

levied by the authorities on insurance transactions. If there be any additional levies,

they too will be recovered from you. This brochure contains only the salient features

of the plan. For further details, please refer to the policy contract. Tax benefits

are subject to changes in the tax laws. Insurance is the subject matter of the

solicitation. For more details and clarification, call your BSLI Insurance Advisor or

visit our website and see how we can help in making your dreams come true.

In Rupees Ratio to Base Premiums Paid to Date

Annual Guaranteed Non-Guaranteed Guaranteed Total &Base Surrender Accumulated Survival Surrender Non-Guaranteed

Premium Benefit Benefits Benefit Surrender Benefit

at 5.5% at 7.5% at 9.5% at 5.5% at 7.5% at 9.5%

3,600 103,473 47,371 85,752 1,29,737 115% 167% 210% 259%

6,000 172,455 90,795 1,64,359 2,48,663 115% 175% 224% 281%

FOR BETTER UNDERSTANDING AND CLARITY, YOU MAY REFER

TO THE DETAILS IN THE FOLLOWING ILLUSTRATION:

If the Annual Base Premium is:

At the end of 25 years (at maturity), the following amounts would be payable

for two Annual Base Premium levels:

For example, you have an annual base premium of Rs. 1,200 in a 25-year policy term

and your entry age being 30 years. Following Accumulated Survival Benefits will

emerge in different scenarios:

Band 2 - at least Rs. 6,000 then the Accumulated Survival Benefits are 15% higher

than shown above

Annual Base Premium of Rs. 3,600 is 3 times above illustration

Annual Base Premium of Rs. 6,000 is 5 times above illustration with Accumulated

Survival Benefits are 15% higher

Illustration continued on the next page.

•

•

•

Illustration Down Scenario Base Up Scenario

Survival Benefit Payout Rate 2.75% 4.25% 5.45%

Survival Benefit Accumulation Rate 4.68% 6.38% 8.08%

Average 10-Year GSec Rate 5.50% 7.50% 9.50%

In Rupees Ratio to Base Premiums Paid to Date

Guaranteed Non-Guaranteed Guaranteed Total &Year Surrender Accumulated Survival Surrender Non-Guaranteed

Benefit Benefits Benefit Surrender Benefit

at 5.5% at 7.5% at 9.5% at 5.5% at 7.5% at 9.5%

1 & 2 — — — — — — — —

3 900 99 153 196 25% 28% 29% 30%

4 1,440 236 367 474 30% 35% 38% 40%

5 2,100 412 645 839 35% 42% 46% 49%

6 3,240 629 992 1,299 45% 54% 59% 63%

7 4,620 889 1,413 1,862 55% 65% 72% 77%

8 6,240 1,195 1,911 2,535 65% 77% 85% 91%

9 8,100 1,548 2,491 3,329 75% 89% 98% 106%

10 11,032 1,950 3,160 4,251 92% 108% 118% 127%

15 18,435 4,789 8,034 11,204 102% 129% 147% 165%

20 26,329 9,263 16,121 23,377 110% 148% 177% 207%

25 34,491 15,790 28,584 43,246 115% 167% 210% 259%

Policy

DISCLAIMERS

This policy is underwritten by Birla Sun Life Insurance Company Limited (BSLI).

This is a non-participating traditional insurance plan. All terms & conditions are

guaranteed throughout the policy term except for the Survival Benefit which will

vary based on the prevailing yield on 10-year Government of India Securities.

BSLI reserves the right to recover levies such as the Service Tax and Education Cess

levied by the authorities on insurance transactions. If there be any additional levies,

they too will be recovered from you. This brochure contains only the salient features

of the plan. For further details, please refer to the policy contract. Tax benefits

are subject to changes in the tax laws. Insurance is the subject matter of the

solicitation. For more details and clarification, call your BSLI Insurance Advisor or

visit our website and see how we can help in making your dreams come true.

In Rupees Ratio to Base Premiums Paid to Date

Annual Guaranteed Non-Guaranteed Guaranteed Total &Base Surrender Accumulated Survival Surrender Non-Guaranteed

Premium Benefit Benefits Benefit Surrender Benefit

at 5.5% at 7.5% at 9.5% at 5.5% at 7.5% at 9.5%

3,600 103,473 47,371 85,752 1,29,737 115% 167% 210% 259%

6,000 172,455 90,795 1,64,359 2,48,663 115% 175% 224% 281%

Call Toll-free: 1-800-270-7000 www.birlasunlife.com sms ‘DHAN’ to 56161

Regd. Office: One Indiabulls Centre, Tower 1, 15th & 16th Floor, Jupiter Mill Compound,841, Senapati Bapat Marg, Elphinstone Road, Mumbai 400 013. Reg. No. 109 Unique No.:109N042V01 ADV/02/08-09/3174 VER 2/SEPT/2009