are you making a profit?. understand and utilize an income statement: understand the purpose of...

TRANSCRIPT

Income Statement

Are you making a profit?

Understand and utilize an income statement:

Understand the purpose of an income statement Be familiar with income statement terminology and structure Be familiar with cost and accrual methods of determining Net

Farm Income Understand the relationship with the balance sheet Be able to use the income statement for strategic purposes

Objectives

Use the income statement to determine the profit or loss

during an accounting period. Tells you the financial position of the business over a period of

time (generally your fiscal year). Return to Assets and Equity Return to Labor and Management Operating Profit Margin

Income Statement

Profit = Revenue – Expenses

Definitions: Revenue – Income earned during the accounting period

Commodity Sales, Inventories, Accounts Receivable Expenses – Cash or noncash expenses during the accounting

period Input Expenses, Depreciation, Accounts Payable, Accrued Interest &

Expenses

Income Statement Fundamentals

Income StatementGrant County Farms Co.

Year Ending December 31, 2013Revenue: Expenses: Cash crop sales Purchased feed and grainCash livestock sales Purchased market livestockInventory changes Other Operating Expenses:

Crops Seed and fertilizerMarket livestock Repairs, maintenance

Government payments Fuel and lubeChange in value of raised breeding stock Property taxesGain/loss from sale of culled breeding stock Hired laborChange in accounts receivable Utilities

Adjustments Total Revenue Accounts payable

Accrued expensesDepreciation

Total Operating Expenses Interest paidChange in interest payable

Total interest expense Total Expenses

Net Farm Income From Operations Gain/loss on sale of capital assets:

Machinery

Total Gain/Loss on capital assets Net Farm Income

Accrual-Adjusted Net Farm Income

The Farm Financial Standards Committee recommends that anyone using cash accounting convert net farm income to accrual-adjusted net farm income. More accurate Better for management purposes

Income Statement Adjustments

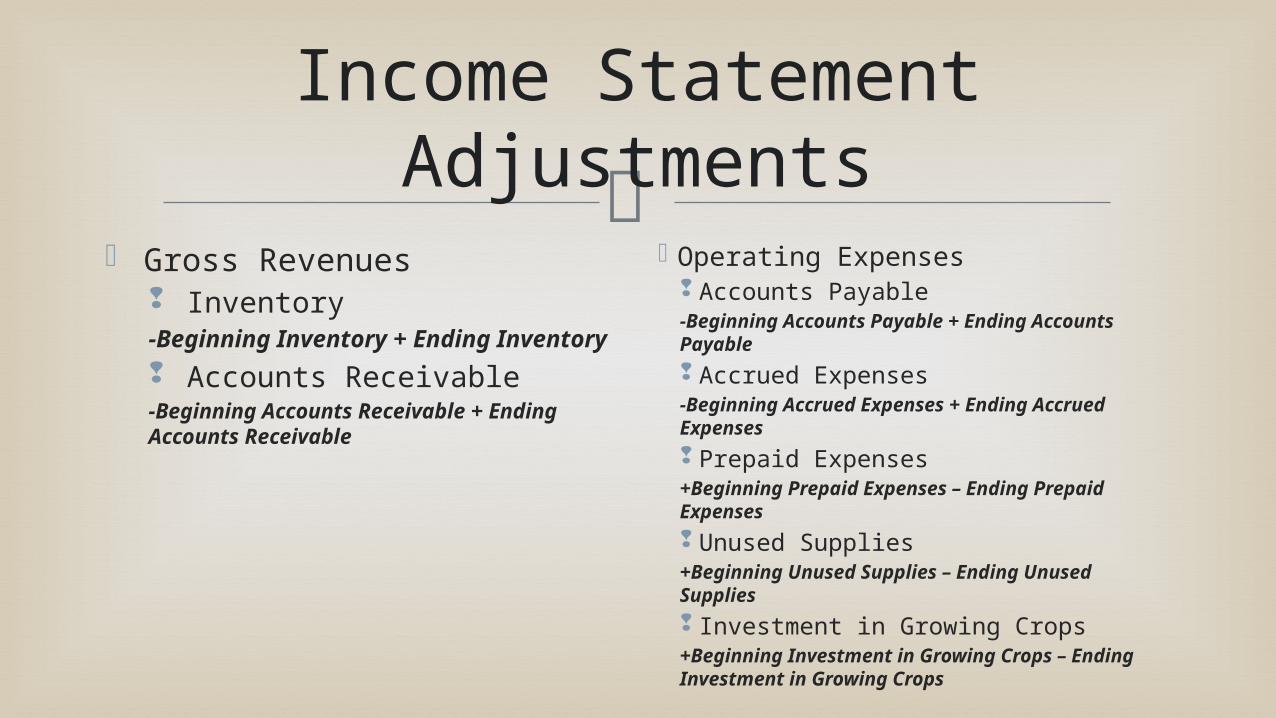

Gross Revenues Inventory-Beginning Inventory + Ending Inventory

Accounts Receivable-Beginning Accounts Receivable + Ending Accounts Receivable

Operating Expenses Accounts Payable-Beginning Accounts Payable + Ending Accounts Payable

Accrued Expenses-Beginning Accrued Expenses + Ending Accrued Expenses

Prepaid Expenses+Beginning Prepaid Expenses – Ending Prepaid Expenses

Unused Supplies+Beginning Unused Supplies – Ending Unused Supplies

Investment in Growing Crops+Beginning Investment in Growing Crops – Ending Investment in Growing Crops

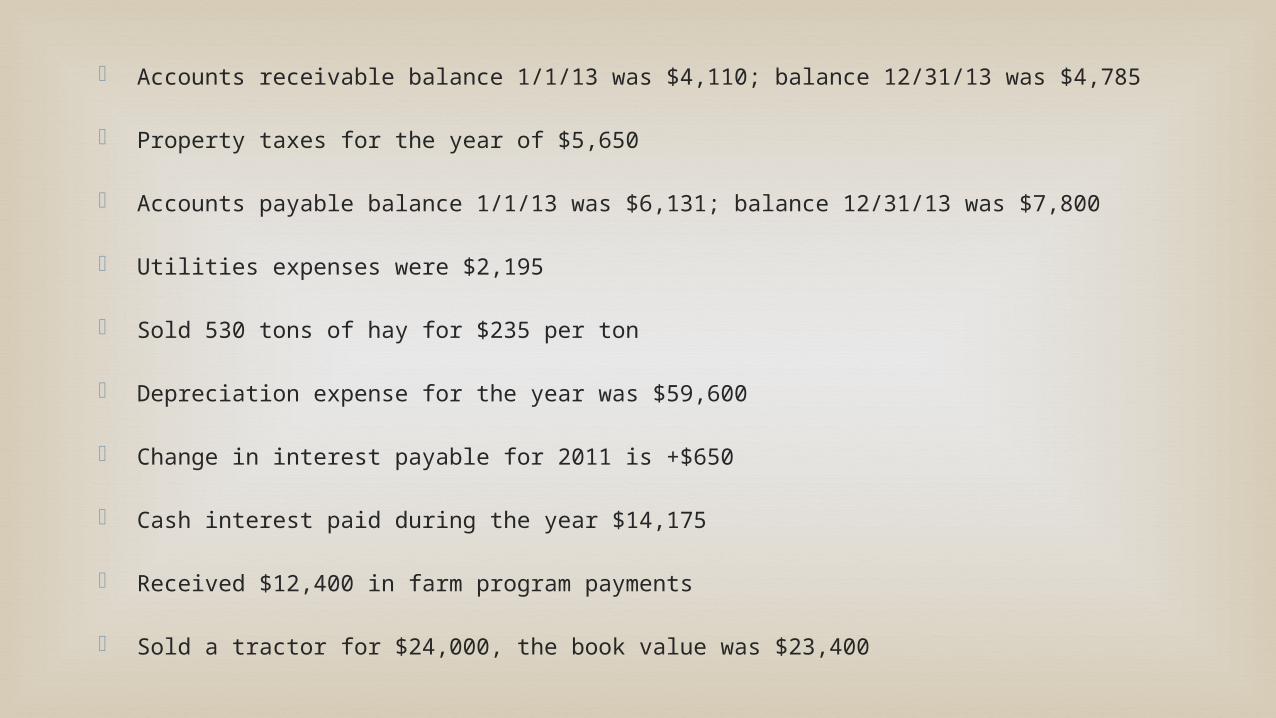

Accounts receivable balance 1/1/13 was $4,110; balance 12/31/13 was $4,785

Property taxes for the year of $5,650

Accounts payable balance 1/1/13 was $6,131; balance 12/31/13 was $7,800

Utilities expenses were $2,195

Sold 530 tons of hay for $235 per ton

Depreciation expense for the year was $59,600

Change in interest payable for 2011 is +$650

Cash interest paid during the year $14,175

Received $12,400 in farm program payments

Sold a tractor for $24,000, the book value was $23,400

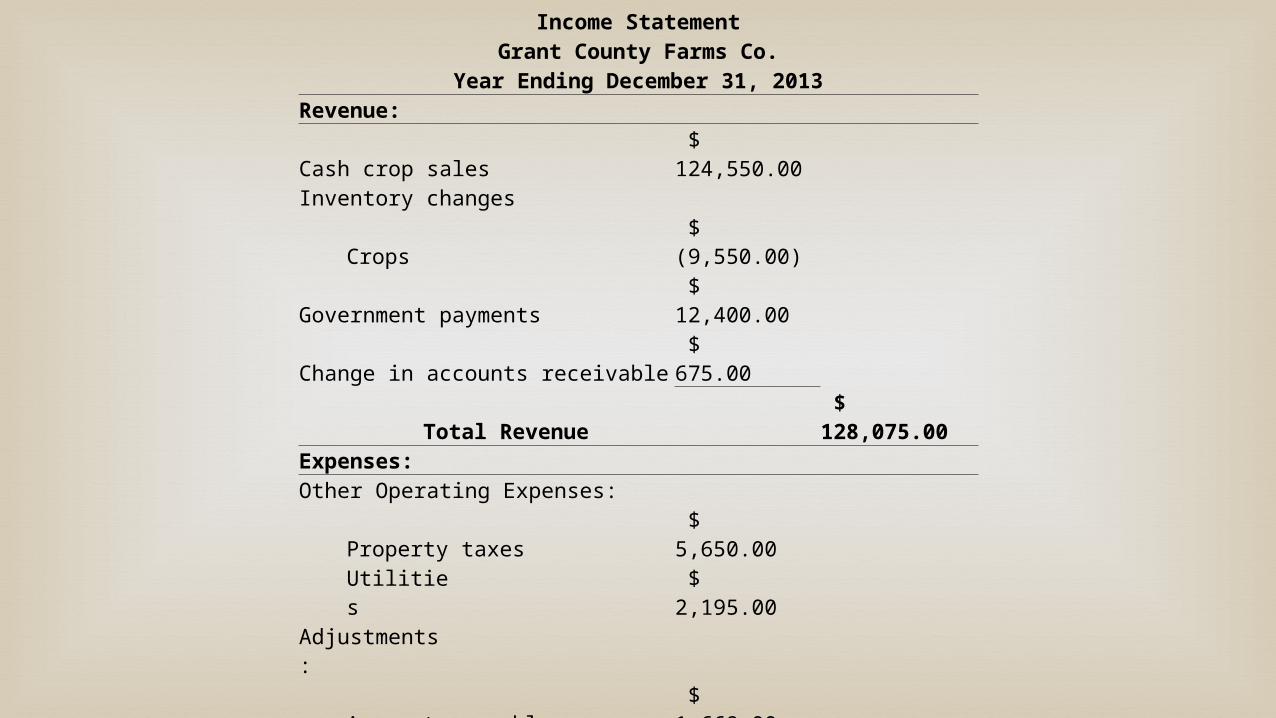

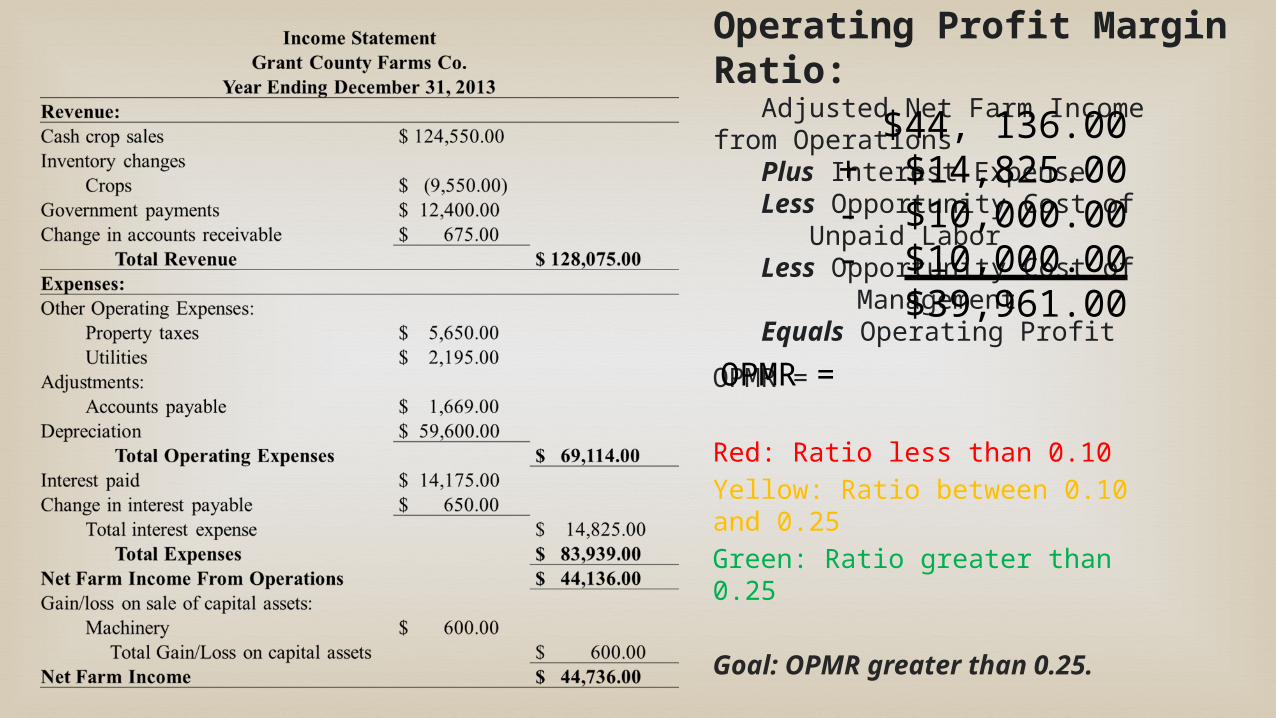

Income StatementGrant County Farms Co.

Year Ending December 31, 2013Revenue: Cash crop sales $ 124,550.00 Inventory changes

Crops $ (9,550.00)Government payments $ 12,400.00 Change in accounts receivable $ 675.00

Total Revenue $ 128,075.00 Expenses: Other Operating Expenses:

Property taxes $ 5,650.00 Utilities $ 2,195.00

Adjustments:Accounts payable $ 1,669.00

Depreciation $ 59,600.00 Total Operating Expenses $ 69,114.00

Interest paid $ 14,175.00 Change in interest payable $ 650.00

Total interest expense $ 14,825.00 Total Expenses $ 83,939.00

Net Farm Income From Operations $ 44,136.00 Gain/loss on sale of capital assets:

Machinery $ 600.00 Total Gain/Loss on capital assets $ 600.00

Net Farm Income $ 44,736.00

Return to Assets:Adjusted Net Farm Income from OperationsLess Opportunity Cost of Unpaid LaborLess Opportunity Cost of ManagementEquals Return to Assets

ROA =

Red: Ratio less than 0.01Yellow: Ratio between 0.01 and 0.05Green: Ratio greater than 0.05

Goal: ROA greater than 0.05.

$44, 736.00- $10,000.00- $10,000.00

$24,736.00

ROA =

Return to Equity:Adjusted Net Farm Income from OperationsLess Opportunity Cost of Unpaid LaborLess Opportunity Cost of ManagementEquals Return to Equity

ROE =

No rule of thumb. It is best to compare with similar operations. Want ROE > ROA.

Goal: ROE greater than _____.

$44, 736.00- $10,000.00- $10,000.00

$24,736.00

ROE = 11

Operating Profit Margin Ratio:

Adjusted Net Farm Income from Operations

Plus Interest ExpenseLess Opportunity Cost of

Unpaid LaborLess Opportunity Cost of

ManagementEquals Operating Profit

OPMR =

Red: Ratio less than 0.10Yellow: Ratio between 0.10 and 0.25Green: Ratio greater than 0.25

Goal: OPMR greater than 0.25.

$44, 136.00+ $14,825.00- $10,000.00- $10,000.00

$39,961.00

OPMR =

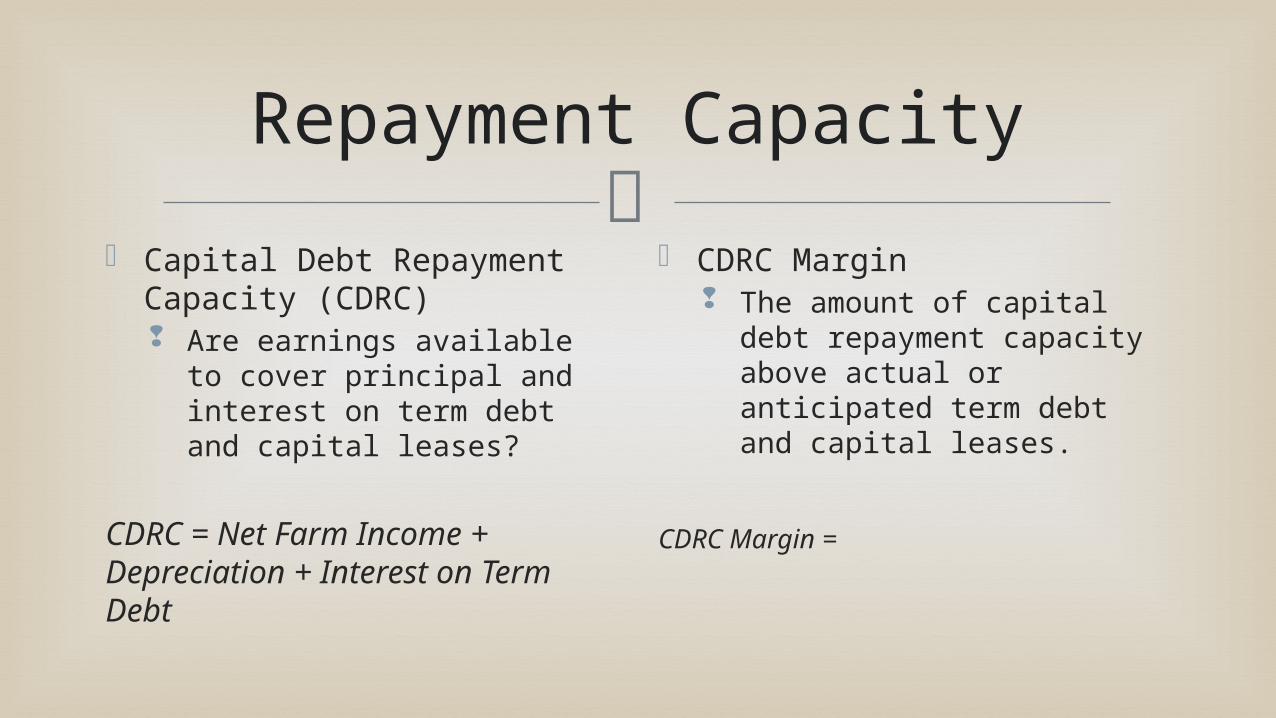

Repayment Capacity

Capital Debt Repayment Capacity (CDRC) Are earnings available to

cover principal and interest on term debt and capital leases?

CDRC = Net Farm Income + Depreciation + Interest on Term Debt

CDRC Margin The amount of capital debt

repayment capacity above actual or anticipated term debt and capital leases.

CDRC Margin =

Case Studies

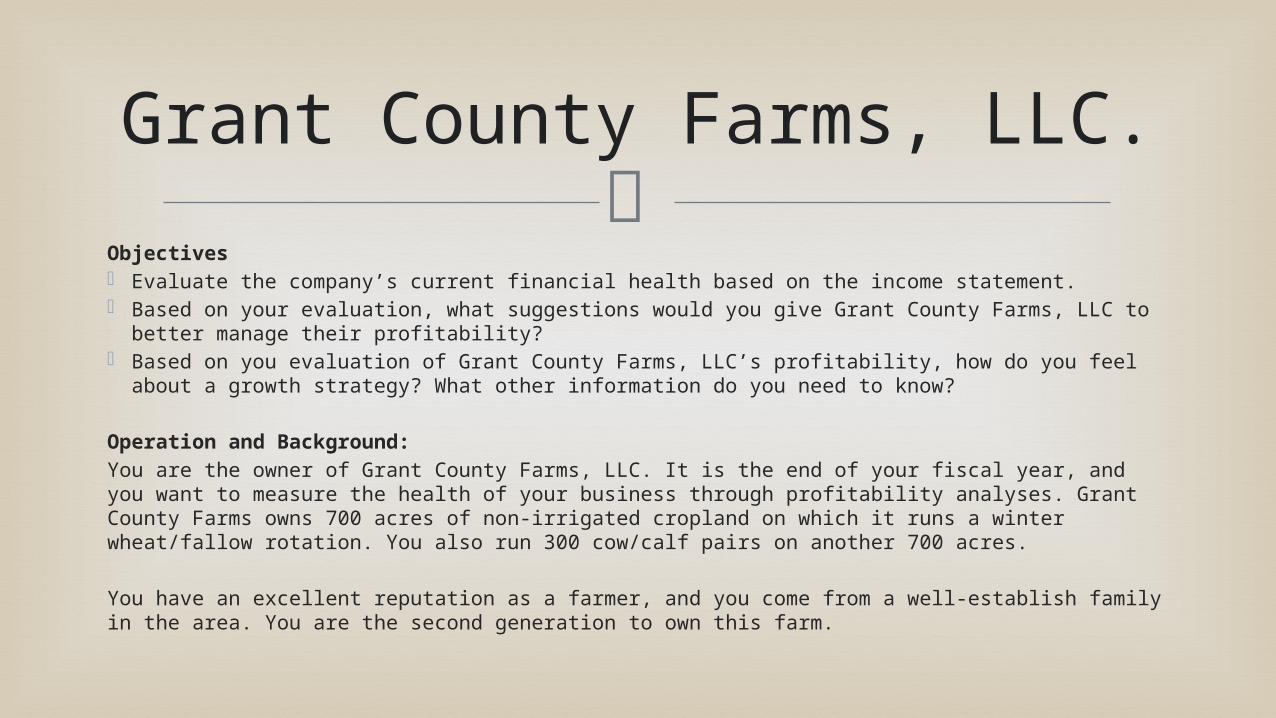

Grant County Farms, LLC.

Objectives Evaluate the company’s current financial health based on the income statement. Based on your evaluation, what suggestions would you give Grant County Farms, LLC to better

manage their profitability? Based on you evaluation of Grant County Farms, LLC’s profitability, how do you feel about a

growth strategy? What other information do you need to know? Operation and Background:You are the owner of Grant County Farms, LLC. It is the end of your fiscal year, and you want to measure the health of your business through profitability analyses. Grant County Farms owns 700 acres of non-irrigated cropland on which it runs a winter wheat/fallow rotation. You also run 300 cow/calf pairs on another 700 acres.

You have an excellent reputation as a farmer, and you come from a well-establish family in the area. You are the second generation to own this farm.

Profit to Equity

The relationship between your balance sheet and income statement

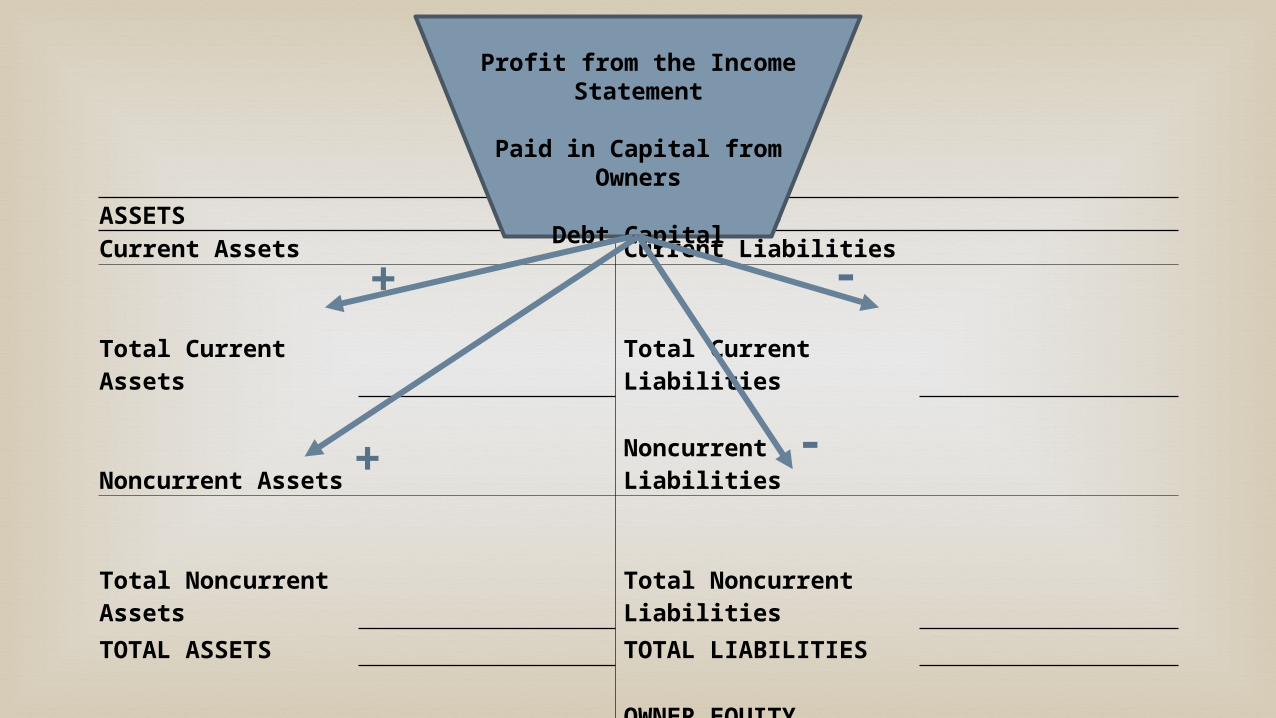

Balance Sheet for ABC Farms Co.

December 31, 20XX

ASSETS LIABILITIESCurrent Assets Current Liabilities

Total Current Assets Total Current Liabilities

Noncurrent Assets Noncurrent Liabilities

Total Noncurrent Assets Total Noncurrent Liabilities

TOTAL ASSETS TOTAL LIABILITIES OWNER EQUITY

Total Equity

Total Liabilities and OE

Profit from the Income Statement

Paid in Capital from Owners

Debt Capital

+

+ -

-

Managing Your Balance Sheet

Profit comes into the business: Fund growth Replace fixed assets Leverage/deleverage Increase liquidity Distribute to owners

Increase risk bearing ability through equity distribution

Liquidity Ratios

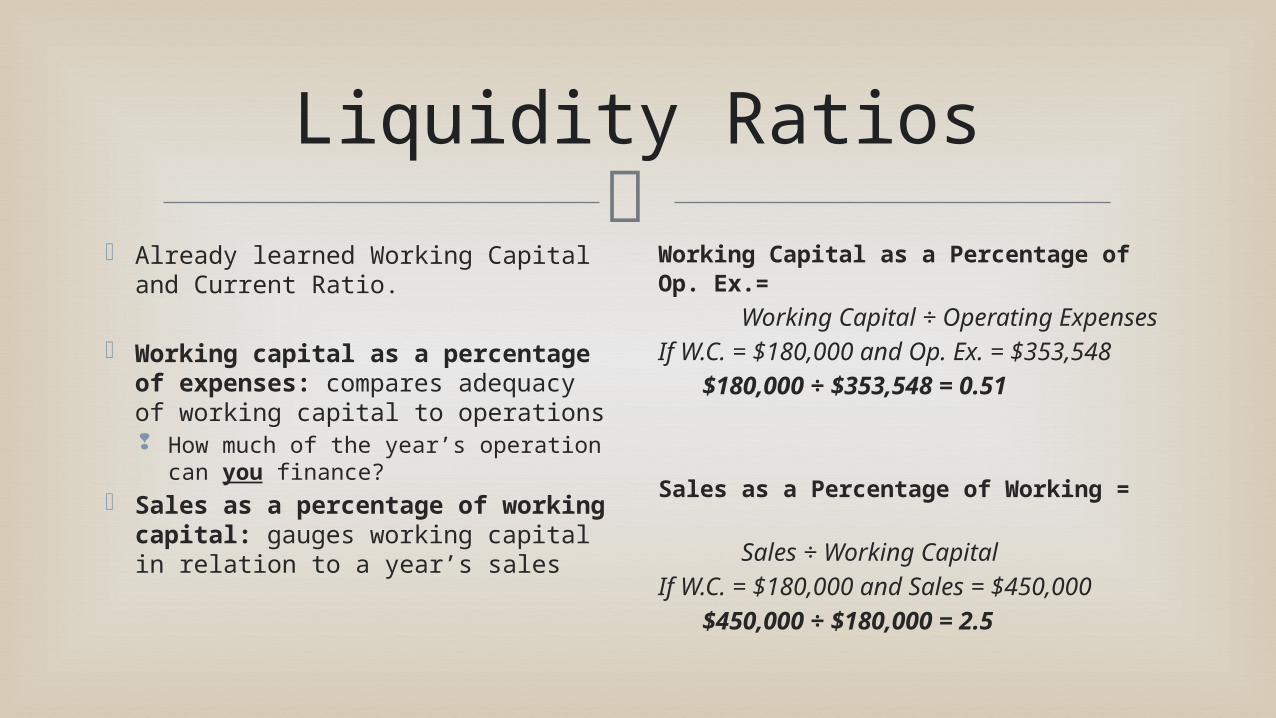

Already learned Working Capital and Current Ratio.

Working capital as a percentage of expenses: compares adequacy of working capital to operations How much of the year’s operation

can you finance? Sales as a percentage of

working capital: gauges working capital in relation to a year’s sales

Working Capital as a Percentage of Op. Ex.= Working Capital ÷ Operating ExpensesIf W.C. = $180,000 and Op. Ex. = $353,548

$180,000 ÷ $353,548 = 0.51

Sales as a Percentage of Working = Sales ÷ Working CapitalIf W.C. = $180,000 and Sales = $450,000

$450,000 ÷ $180,000 = 2.5

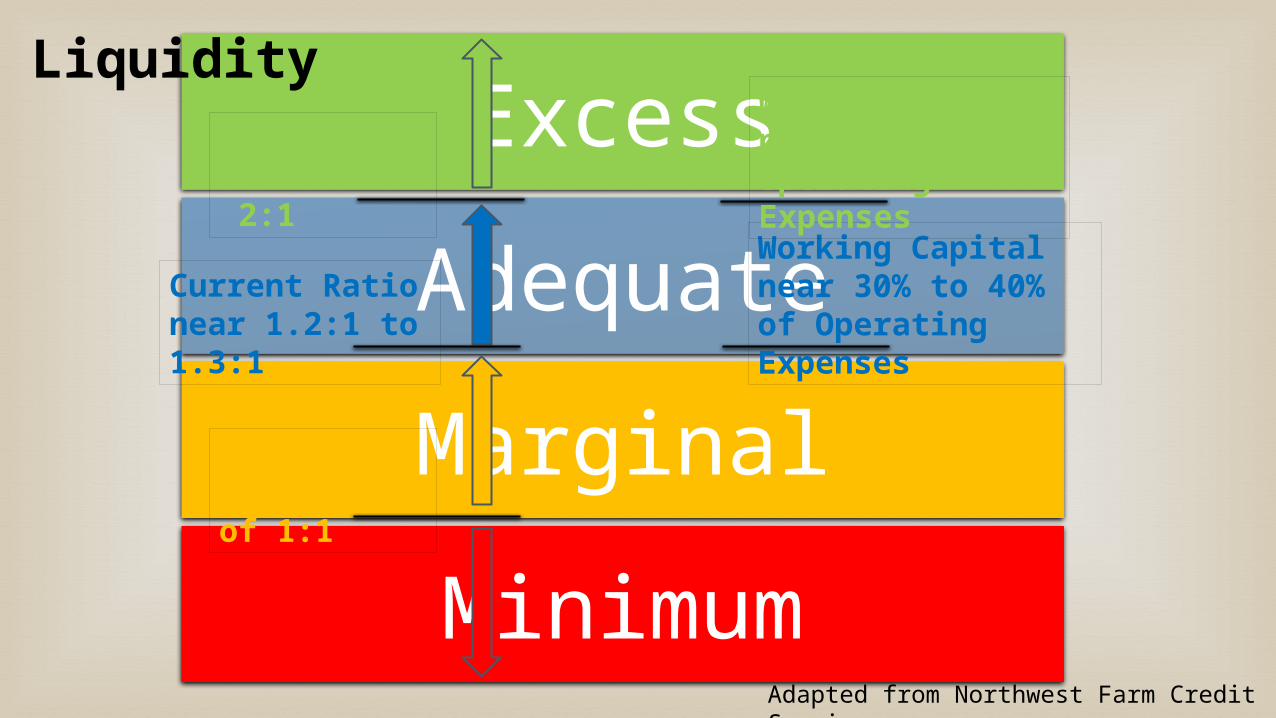

Excess

Adequate

Marginal

Minimum

Current Ratio near 2:1

Current Ratio near 1.2:1 to 1.3:1

Current Ratio near of 1:1

Working Capital near 30% to 40% of Operating Expenses

Working Capital near 50% of Operating Expenses

Liquidity

Adapted from Northwest Farm Credit Services

Solvency Ratios

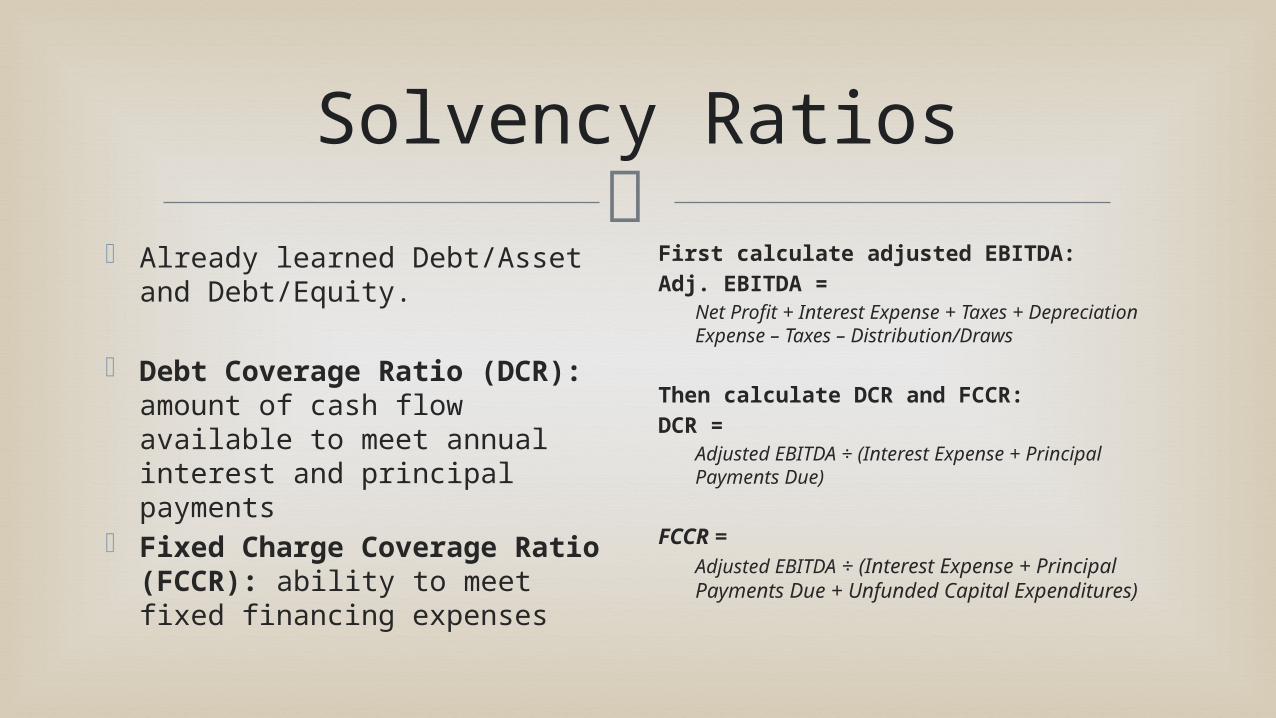

Already learned Debt/Asset and Debt/Equity.

Debt Coverage Ratio (DCR): amount of cash flow available to meet annual interest and principal payments

Fixed Charge Coverage Ratio (FCCR): ability to meet fixed financing expenses

First calculate adjusted EBITDA:Adj. EBITDA =

Net Profit + Interest Expense + Taxes + Depreciation Expense – Taxes – Distribution/Draws

Then calculate DCR and FCCR:DCR =

Adjusted EBITDA ÷ (Interest Expense + Principal Payments Due)

FCCR = Adjusted EBITDA ÷ (Interest Expense + Principal Payments Due + Unfunded Capital Expenditures)

Maximum

Marginal

Sustainable

Strategic

Debt/Asset Ratio:Dairy 50%Orchards 50%Irrigated Crops 45%Dry Crops 40%Livestock 40%

Debt/Asset Ratio:Dairy 35%Orchards 35%Irrigated Crops 35%Dry Crops 25%Livestock 25%

DCR 1.2:1

DCR 1:1

Leverage

Adapted from Northwest Farm Credit Services

FCCR 1:1

FCCR 1.2:1

Guidelines for Using Ratios

Compare, compare, compare… Industry Historical information Business lifecycle

Consider the whole picture.

Case Studies

Jack & Jill Ranch Co.

Objectives: Evaluate the company’s current financial health based on the financial statements. Understand the impact of growth on the company’s financial position. Based on your evaluation of Jack & Jill Ranch Co.’s financial position, how do you feel about their growth

strategy? How do you feel that can prepare for growth?

Operation and Background: Jack & Jill Ranch Co. farm 400 acres of irrigated crop ground. They rent 100 acres and own 300 acres. 300 acres are planted to timothy hay, and the additional 100 acres are used to pasture their seedstock cattle operation. The owners of Jack & Jill Ranch Co. would like to expand their operation. They have the opportunity to purchase a neighboring 100 acres.

Growth Opportunity:Jack & Jill Ranch have the opportunity to purchase an additional 100 acres of excellent hay ground. They would like to offer $4,000 per acre. If purchased, this ground would be used to expand their timothy hay enterprise.

Homework

Complete an income statement for your farm.

Calculate your ROA and ROE.

Set targets for ROA, ROE, and OPMR.

Take a minute to write down one or two ideas or takeaways

from this lesson.

One Minute Takeaway

Sieverkropp Consulting LLC.

Contact: Elizabeth Sieverkropp [email protected] (509) 398-6858

Website: www.sieverkroppconsulting.com

Training Program Homepage:www.sieverkroppconsulting.com/fsa-borrower-training-program-homepage