applied study of credit and financing … and finance... · · 2014-04-03commercial banks, micro...

TRANSCRIPT

i

This study has been realised with funding from the European Union

and from the Dutch Ministry for Development Cooperation - DGIS

APPLIED STUDY OF CREDIT AND FINANCING

OPPORTUNITIES FOR FARMERS IN

URBAN AND PERI-URBAN

FREETOWN

PAMELA KONNEH

Ministry of Agriculture Forestry

and Food Security (MAFFS)

November 2010

i

CONTENTS

List of Abbreviations ii.

Definition of Terms iii.

List of Tables iv. - v.

List of Figures vi.

Acknowledgements vii.

Abstract viii.

CHAPTER 1. Background and Introduction

Background, Problem Statement, Objectives of the Study,

Significance, Limitations, Hypothesis 1-3

CHAPTER 2. Literature Review 7-12

CHAPTER 3. Methodology

Study Area, Research Design, Population and Sampling Procedures,

Research Instruments, Data Analysis 13-25

CHAPTER 4. Institutions providing credit and finance in Western Area

Commercial Banks, Micro Finance Institutions, Government Institutions

and Local Authorities, Non Governmental Organisations 26-41

CHAPTER 5. Need Demand and Use of Credit and Finance by Poor Households

engaged in (peri) urban Agriculture

Characteristics of Poor Households engaged in (peri) urban Agriculture,

Access to and Use of Credit and Finance, Need and Demand for Credit

and Finance, Challenges to Access Financial Institutions 42-57

CHAPTER 6. Summary of Findings, Conclusion and Recommendations 58-66

References 67

Annex 1 Information Gathering Forms on Financial institutions

Annex 2 Questionnaire for poor households engaged in (peri) urban agriculture

Annex 3 Information Gathering Form on informal credit and finance (osusu and remittances)

ii

LIST OF ABBREVIATIONS

ARD - Association for Rural Development

BRAC - Bangladesh Rural Advancement Committee

CMC - Chiefdom Micro-credit Committee

COOPI - Cooperazione Internazionale

CSO - Central Statistics Officer

FAO - Food and Agriculture Organisation

FCC - Freetown City Council

FUPAP - Freetown Urban and Peri-urban Agricultural

Platform

GDP - Gross Domestic Product

GGEM - Gender and Grassroot Empowerment Movement

IDRC - International Development Research Centre

IPES - Promotion for Sustainable Development

IWMI - International Water Management Institute

LAC - Latin America and the Caribbean

LAPO - Lift Above Poverty Organisation

MAFFS - Ministry of Agriculture, Forestry and Food Security

MPSA CCO - Matila Prayas Savings and Credit Cooperative

NaCSA - National Commission for Social Action

NAFSL - National Association of Farmers Sierra Leone

NGOs - Non-Governmental Organisations.

PCIB - Philippines Commercial and Industrial Bank

RPSDP - Rural and Private Sector Development Project

RUAF - Resource centres for Urban Agriculture and Food

Security

SAPA - Social Action and Poverty Alleviation

UA - Urban Agriculture

UBA - United Bank for Africa

UMP - Urban Management Programme

UPA - Urban and Peri-urban Agriculture

VAM - Vulnerability Assessment Mapping

WARDC - Western Area Rural District Council

iii

DEFINITION OF TERMS

Agro-processing - Processing of agricultural products

Fisher folks - People involved in fishing activities

High Input Processors - People engaged in processing agricultural products

like cassava that require large quantity of resources for that

activity.

Long distance marketers - People engaged in trading of agricultural products

obtained from up country and elsewhere. They travel to market

places outside the city to buy produce to sell.

Low Input Processors - People engaged in processing of agricultural

products like vegetables that require small quantity of resources

for that activity.

Micro-credit Small loans provided for poor families to help them

engage in production activities

Micro-finance - A broader range of services (savings, loans

insurance, transfer of money etc.) because poor and very poor

people require a variety of financial products

Ornamental Producers - People engaged in raising and selling of flowers.

Osusu - Money put together by a group to help members. It

is rotational one receiving at a time promising to contribute for

others.

Respondents - Those people who answer questions from a

questionnaire.

Urban & Peri-urban

Agriculture - Agriculture practised in and around the city.

Urban Poor - Poor people living in the urban areas.

iv

LIST OF TABLES

Page Table 1 - Sample size determination and distribution of target population 20

in urban - and peri-urban areas.

Table 2 - Distribution of Credit and Finance Institutions 27

Table 3 - Descriptive Statistics of Challenges face by the banks. 30

Table 4 - Future Prospects for Financing UA by the banks. 31

Table 5 - Descriptive statistics on value of cumulated & outstanding 34

loans from Institutions.

Table 6 - Basic Information on Financial Institutions. 41

Table 7 - Descriptive Statistics on reasons for not pertaining to an 42

organization by respondents.

Table 8 - Descriptive Statistics of specific osusus use for UA by 43

respondents.

Table 8.1 - Details on the specific osusus use by respondents. 43

Table 9 - Description of remittances from relatives use by respondents. 45

Table 10 - Descriptive statistics of uses of credit and finance by respondents. 45

Table 11 - Percentage distribution of sex accessing credit and finance from 46

informal sources.

Table 12 - Percentage distribution of sex accessing credit and finance from 47

informal sources.

Table 13 - Percentage distribution of sex accessing credit and finance from 48

formal Sources.

Table 14 - Descriptive statistics of demand for credit by respondents. 49

Table 15 - Descriptive statistics of required time for credit by respondents. 50

v

Table 16 - Amount of credit received and amount demanded. 51

Table 17 - Challenges in accessing credit from multiple responses. 52

Table 18 - Recommended linkages of urban poor in agriculture with possible 57

financial institutions for accessing credit and finance.

vi

LIST OF FIGURES

Page

Figure 1 - Map of Sierra Leone showing Western Area - 14

Figure 2 - Map of Western Area showing Urban & Peri-Urban - 15

Areas

Figure 3 - Distribution of main occupation of respondents - 37

Figure 4 - Distribution of respondents by sex - 38

Figure 5 - Distribution of respondents by position in the - 39

household

Figure 6 - Distribution of respondents by belonging to a group - 40

Figure 7 - Percentage distribution of Informal sources of money - 42

for agricultural activities.

vii

ACKNOWLEDGEMENTS

I would like to thank COOPI Sierra Leone most sincerely for giving me the opportunity and financial

support for carrying out this study. I would also like to extend my gratitude to Mr. Tamba Dambabla of

SLARI for his reliable comments and inputs during the various stages of this study. I would like to

extend my gratitude to Mr. Richard Bockarie also of SLARI for taking the pains in editing this report.

I also thank FUPAP for their comments on the final version of this paper. I remain responsible for any

error in the paper.

viii

ABSTRACT

The study identified and assessed existing opportunities for financing small scale urban and peri- urban

agriculture and the needs and demand for finance from the urban poor engaged in urban agriculture,

agro-processing and marketing. .

The results of the study show that 14 out of the 27 formal finance institutions that exist are possible

financial sources for urban agriculture and provide finance opportunities for the urban poor engaged in

agriculture. Out of a sample of 269 respondents, 98.1% expressed the need and demand for credit and

finance for their activities. The groups of marketers and fisher folks interviewed also expressed a need

for credit and finance for expansion and improvement of their business.

The study concludes that in making credit available for urban agriculture, improving the lending terms

and conditions of the financial institutions, in favour of the urban poor engaged in agriculture would

facilitate their access to credit and finance.

Key words: Credit and finance, financial institutions, urban poor engaged in agriculture.

1

CHAPTER 1

BACKGROUND AND INTRODUCTION

Agriculture in and around the cities has been on the development agenda of many national and

international bodies in recent times. Sierra Leone is no exception to this development approach.

For instance, the “Agriculture Sector Review of Sierra Leone” sponsored by the government of

Sierra Leone, FAO and World Bank recognised the importance of agriculture in and around the

cities i.e. Urban & Peri-urban agriculture in poverty alleviation and ensuring food security.

Consequently local and international Non-governmental Organisations (NGOs) initiated Urban

and Peri-urban programmes in Freetown. In 2006 to 2008 a major project title Freetown Urban

& Peri-urban Project (FUPAP), within the frame of the cities farming Network of Resource

Centres on Urban Agriculture and Food Security (RUAF) launched by the International Water

Management Institution (IWMI) responsible RUAF centre for Anglophone West Africa was

implemented by the Ministry of Agriculture, Forestry and Food Security.(MAFFS).

The project aimed at supporting city authorities in recognising the benefits of urban agriculture

and at the same time addressed food security, Urban Poverty and improved urban environmental

management. The outcome of this intervention has made city authorities become more aware of

the importance of urban agriculture including Freetown city and its environs, hence the need to

lay emphasis on and sustainably address the issue of urban food crisis and unemployment. This

notwithstanding, and for urban agriculture to develop fully as a productive force, it requires not

only political recognition or legitimacy but also financial support.

Several challenges constrain urban and peri-urban production (UPA) in Freetown and therefore

prevent the sector to achieve its full potential of contributing to the City‟s Gross Domestic

Product (GDP). Among these challenges includes the promotion of investment in and financing

urban agriculture.

Yves Cabannes (2004) stated that financial support can make a significant difference to poor

urban families who are involved in a diversity of activities such as production, agro-processing,

trading/marketing waste collection and recycling. These entrepreneurs require access to working

capital, but often face limited access to credit and investment schemes for urban agriculture.

2

The experience gained in the implementation of the pilot projects implemented in the Freetown

Urban Area by RUAF city partners in the years 2007 and 2008 showed that access to credit and

other sources of financing (e.g. subsidies, grants) are crucial to sustainably and meaningfully

develop agricultural production and or processing and marketing activities, as most of the

producers have limited or no access to credit and finance.

As in most cities in the developing world available loans are not adapted to the specific

conditions of the poor urban producers. Most of the available credits are either from institutions

financing rural agriculture that still not consider urban agriculture as an issue by itself or existing

credit programmes for the urban poor (e.g. micro-enterprises) are handled by those that hardly

have experience with financing agricultural activities. As a result, the lending conditions in terms

of collateral and guarantee are in effective unsustainable as most urban producers do not have

land use rights, amount of down payments, duration of the loan often not allowing longer term

investments and length of the grace period often both too short to be able to pay back, interest

rates often too high, process to disburse a loan often too lengthy and therefore costly.

So, not only do the urban producers face limited access to credit and investment schemes, but

also the information on those who do (such scheme) is even sparse or scarce. Evidence of the

benefits or urban agriculture is anecdotal and deals mainly with highly localised small scale

experiences.

Worse still, little is known about credit and finance interventions for UA in the Freetown urban

area and even elsewhere, that could benefit large numbers of producers, agro-processors and

marketers and thereby make urban agriculture a major contributor to more productive and

inclusive urban economies.

As a result, COOPI Sierra Leone in collaboration with the Freetown Urban and Per-urban

Agriculture Platform (FUPAP) set up a study group with its members drawn from the Ministry

of Agriculture, Forestry and Food Security, MAFFS, Concern World Wide, Sierra Leone,

Association for Rural Development ARD, and National Association of Farmers of Sierra Leone

NAFSL .The purpose was to find out and provide information and knowledge on credit and

finance interventions namely: “Applied Study of Credit and financing opportunities for farmers

in urban and peri-urban Freetown”

3

On this score, the paramount focus of this study hinges on finding out the current practices of

institutions and programmes that finance urban agriculture or other informal productive activities

like micro-enterprise development in and around the city of Freetown.

Chapter One of this work looks at introduction to the study, statement of the problem, objectives,

significance limitations and hypothesis of the study.

Chapter Two looks at literature review especially or relevant issues in financing and investment

for urban agriculture in other areas of the world.

Chapter Three reviews the methodology used to conduct the research is explained including the

parameters used to find existing credit and finance opportunities and other related issues as

demand/need for credit and finance urban by urban producers, agro-processors and marketers of

urban agriculture products.

Chapter Four presents analyzes and discuss the data collected about institutions providing credit

and finance in Western Area,

Chapter Five presents analyzes and discussions of the data gathered on needs demand and use of

credit and finance by poor households engaged in urban and peri-urban agriculture in and around

Freetown as well as the challenges they face in accessing formal credit and finance.

Finally, Chapter Six looks at the mis-match between credit and finance offer and demand, draws

the study conclusions and presents recommendations for credit and finance practices and

products which tailored on the needs and conditions of poor households engaged in (peri) urban

agriculture.

Statement of the problem

Generally speaking, the Sierra Leone economy is characterised by a high incidence of the

informal sector. Despite the introduction of credit facilities through the country by NGOs and

others, very little achievements have been made particularly as its impact has not been

meaningfully felt at grass roots level especially on urban and rural resource poor producers.

The situation is especially acute for the urban farmers who are the main producers and

contributors to the urban food security household.

4

Furthermore, limited income and lack of information on existing credit opportunities for urban

agriculture further restrict urban producers‟ access to credit and finance from financial

institutions and agencies.

Significantly, most of the urban producers in the developing world are agrarian. Therefore if the

quality of life of these people is to be improved, access to resources including land and other

related inputs, the availability of credit and finance intervention becomes a top priority.

In the urban and peri-urban Freetown, the low level of community financial assistance among

the urban producers, processors and marketers suggests that indeed access of credit and finance

is a major bottleneck for the development of agriculture in the sector. A relevant issue for

empirical investigation is therefore that of the factors behind the lack of access to credit and

finance for urban agriculture from financial institutions.

This study is therefore intended to investigate into:

1. The main features of existing finance institutions that offer the poor urban producers

processors and marketers access to their credit facilities in urban and peri-urban

Freetown.

2. The need and demand for credit and finance by resource poor urban producers from the

formal and informal credit sources.

Study Objectives

The overall aim of the study was to provide information knowledge and clear recommendations

that will serve to broaden collective and individual financial opportunities for poor urban and

peri-urban producers in and around Freetown and in the other RUAF partner cities.

The specific objectives were:

To identify and assess the current practices of institutions and programmes that finance urban

agriculture or other informal productive activities. (Like micro-enterprise development) in

the city and the existing opportunities, difficulties and bottlenecks encountered for financing

small scale urban and peri-urban agriculture.

To identify the needs and demands for finance from urban poor engaged in urban agriculture,

agro-processing or marketing.

5

To make recommendations that will facilitate the access of small scale urban producers to

finance.

Significance of the Study

The result of this study will serves as resource base material for research students of

Universities, teachers‟ training colleges, agriculture and NGO workers, extension agents and

financial institutions (banking and micro finance institutions). It also attempts to give a clear

picture of the financing and investment situation for urban agriculture in the urban and peri-

urban area of Freetown and also serve as baseline information for future studies and the design

and implementation of credit and finance programmes for urban poor engaged in agriculture, and

small-scale micro enterprises.

The recommendations serve as a guide to generate a better enabling environment for financing

urban agriculture through changes in the existing financial programmes that require institutional

changes and support from third parties (e.g. provision of guarantees, additional resources and

other risk reducing mechanisms).

The recommendations also provide advice to the NGOs, producers organisations involved in the

Freetown farmbul Farm Project in the urban and peri-urban areas of Freetown, thus giving

concrete workable solutions to meet the short term financial needs of the producers.

Limitations of the study

The study covers the urban and peri-urban areas of Western Area of Sierra Leone i.e. the

Freetown Municipality, York, Waterloo and Mountain Wards.

Data was collected from the urban poor engaged in production, processing and marketing

activities consisting of groups of vegetable, pig farmers selected randomly, ornamental

producers; low input processors of agricultural products like cassava leaves, pepper and

groundnut; short and long distance vegetable sellers and fishing communities in and around

Freetown. Also data was collected from farmers groups working with the Ministry of

Agriculture Forestry and Food Security already registered as farmer based organisations, since

there were no statistical information on the total farming population in the Freetown urban and

peri-urban areas and conducting a census would have been costly and time consuming.

It was also limited to the services of banking and financial institutions operating around

Freetown. The study was constrained with a lot of formalities in approaching the banking

6

institutions, and their code of conduct on the release of information. The exercise therefore took

more time than expected because each Institution had to be well informed before audience was

given to the researcher.

Assumption of the study

It was assumed that:

1. All respondents from which data was collected were true residents of the study area and

that;

2. the information given by the sample population was true

3. the sample population have or have not benefited from financial services in the study area.

Hypothesis of the study

The study tested the following hypothesis:

1. H0 = Urban poor engaged in production, processing and marketing

activities have knowledge of and access to credit and finance from financial

institutions.

= Financial institutions offer credit and finance for urban agriculture

2. Ha = Urban poor engaged in production, processing and marketing activities

have no knowledge of and no access to credit and finance from financial

institutions.

= Financial institutions do not offer credit and finance for urban

agriculture.

7

CHAPTER 2

LITERATURE REVIEW

Financial and investment for Urban Agriculture

The provision of credit and finance for urban agriculture has increasingly been regarded as an

important tool for raising the incomes of the urban producers mainly by mobilising resources to

more productive uses.

Despite the current difficulties in making credit and finance for urban agriculture available from

financial institutions, yet some innovative initiatives are taking place in various RUAF Partner

cities such as participatory budgeting, farmer savings and credit schemes, corporate

responsibilities, financing, public - private partnerships funding, micro-credit for urban

agriculture, subsidies in form of tax or fiscal incentives or exemptions etc, etc, though generally

only on a limited scale and serving therefore only a portion of the current needs for finance of

the urban producers.

In other cases where no direct financing for urban and peri-urban agriculture exists, other

financing sources (such as those for rural agriculture, urban micro-enterprise development and

marketing or other small scale urban productive activities) are being or could be directed towards

urban agriculture (Dr. Yves Cabannes 2006).

In recent past though, there has been an increased tendency to fund credit programmes in

developing countries aimed at small-scale enterprises (Daniels et al, 1995) .For instance ,a city

survey and evaluation of significant and diverse modalities of credit and investment provision to

urban agriculture was commissioned in 2002 and 2003 by UN-HABITAT, the Urban

Management Programme - Regional Coordination for Latin America and the Caribbean (UMP-

LAC), IPES – promotion for Sustainable Development, International Development Research

Centre (IDRC) and the International Network of Resource Centres on Urban Agriculture, and

Food Security (RUAF). Thirteen cases were commissioned and assessed giving innovative

experiences of credit and investment schemes, geographically representing various Africa, Latin

America, Asia and Europe. (Technical report on survey of city experiences 2002) - Rose Ngara -

Miray

The work revealed that urban and peri-urban agriculture is financed through a combination of

savings, subsidies/grants, credit (primarily micro-credits), or loans which are provided by

8

Banking institutions (Commercial) micro-finance institutions, NGO, government/or municipal

and self financed.

Savings and resource mobilisation

Urban farmers rely heavily and primarily on the mobilization of their own funds. Therefore, by

and large, urban agriculture for subsistence is self-financed. Mobilization of the financial

resource and savings is done through individual, family-based and collective savings of small

groups of producers that are community based.

Additionally, subsidies/grants for agriculture in the city are many times in different forms:

These include financial subsidies to the banking system, referred to as “Soft conditions for

Credit”,( subsidies directly to the farmer for main agricultural inputs/land, water, seed etc.) or

subsidies in the form of free technical assistance and training or support to obtain inputs as in the

case of Botswana, Nairobi Kenya; and subsidies to generate a facilitating environment

(transport) such as in St. Petersburg for agricultural production in and around the city.( Dr.Yves

Cabannes)

Credit either micro-or soft loan can be supported by international donors (as in Bulgaria),

National governments (Argentina), Federal or municipal governments, private banks, informal

private credit or NGOs and cooperatives (Sudan). Most of these existing finance and investment

schemes however are not accessible by the poor or other vulnerable groups as in Bulgaria. Poor

urban farmers usually cannot afford the requested collateral or the high interest rates.

Financial Institutions/Intermediaries

The analysis of all cases researched showed that a large number of actors are involved in

providing (sources) and managing funds (intermediaries) for urban and peri-urban agriculture.

Financial institutions/intermediaries transform available financial resources into loans that can be

directed to urban farmers in three typical situations:

Public financial institutions/intermediaries which include the national government and municipal

government as in Texaco (Mexico) and Rosario in Argentina.

Private & community-based institution that is credit and savings cooperatives as in Nepal.

9

Private banking system which include commercial banks and micro finance institutions.

Example of this is seen in Prove Pantanal (Brazil) and Botswana.

Municipal Financing/Intermediaries

The local government of Texaco, in the Metropolitan region set up an innovative agricultural

loans programme a few years ago. Resources from the central government were transferred to

the local government as part of the National Social Programme. The Texaco municipality

decided to transform these resources to limited and innovative sets of loans to agricultural

cooperatives (in particular for flower production) and to small solidarity groups of producers that

had not yet formed cooperatives as was the case with a group of rabbit keepers.

However, public resources and subsidies have been a crucial source of funds for facilitating the

access to credit of small urban farmers and for leveraging and channelling additional resources,

the dependence on public money has the risk of a sudden interruption to or closing of excellent

and economically successful urban agricultural activities. The case of Texaco for instance shows

the risk of depending on public resources as the urban agriculture programme was halted after a

change of local government.

As much as possible and in order to reduce the dependency of a credit system on political will, it

is fitting to build strong financial intermediary institutions that can lend and work with public

money, but will not depend on political orientations for the continuity. (Cabannes 2006).

An NGO can be a specialised financial intermediary with some outside help. For example

ACCION international is a U.S. - based non-profit consulting firm providing assistance to urban

micro-entrepreneurs in four foundations in the Latin American countries.

ACCION‟s clients, mostly market stall holders and street traders, and predominantly women are

organised into „Solidarity groups‟. A group of about five members‟ guarantees loans made to

each individual business. If one member does not pay, the rest must make up the repayment or

all members will be denied of access to credit. Pay back is usually weekly. Loans are generally

short-term from one month to six months and build slowly the capacity for absorbing credit

increases. The loan size is from $50 to $300 for micro-commerce and the smallest industries and

from $100 to $1,000 for micro industries and services. (Jeffry Ashe 1989 credit for the poor).

Thus, ACCION assisted programmes provide training and business orientation during meetings

so that business owners can tell each other how they have sorted out problems using peers to

10

train and encourage one another is effective and helps micro-business owner mange their

business as they expand.

One major strength of projects involving NGOs is that they provide services beyond credit; such

services may include technical assistance, village organising and linkage of community groups

with other agencies.

Private and community based financial institutions

In Nepal, in 1998, a cooperative body called the “Matila Prayas Savings & Credit Cooperative

Ltd. (MPSACCO) was set up to offer individual and peer lending for agricultural activities for

setting up shops and diary farming. The financial resources of the cooperative‟s members

generate from various savings such as regular compulsory or, voluntary monthly savings,

marriage and festival saving etc (Cabannes 2006).

This community-based banking facility is tailored to cultural and local practices and is different

from the conventional banking systems wherein savings are compulsory and pre-conditioned for

the poor for getting a loan (though the cooperative and the central government provide loan and

limited grants). Also, various economic institutions provided loans, occasional subsidies and

technical assistance to MPSACCO and its members.

Private and Banking Institutions

In Brazil, the Prove Pantanal Institution provides credits and technical assistance to home-based

producers, so that they can add value to their agricultural family-based production by processing

primary produce and selling it to supermarkets. The credits provided by Prove are funds from the

central government resources, while the technical assistance comes from the state government

budget. The state government separated the technical assistance component from the

management of the credits and delegated the financial management to a bank operating within

the state. The bank authorises various loans and the borrowers to repay at the bank in a fairly

conventional way. Through this programme, the financial set-up has the opportunity to open the

doors of the banks to family-based urban farmers. If they repay their first loans, they will be in a

better position to apply for future loan from the bank beyond the subsidised PROVE credit line.

This programme also acts as a bridge between informal producers and the formal banking system

making it especially attractive. (Araujo, P.Szukala, S. Programma Prove Pantanal, Study case of

the IPES/UMP Research Programm-Cabannes, Y 2004a).

11

In Sierra Leone, in an economy marked by high incidence of the informal sector, the government

has identified the provision of micro-credit as a key mechanism to help reduce poverty. The

provision of financial services (savings insurance, loans) to low-income households aims at

enabling them to acquire capital, improve livelihood and generate employment.

In mid 2001, the government adopted a new approach to micro credit scheme through the Social

Action and Poverty Alleviation (SAPA) Programme of the National Commission for Social

Action (NaCSA) to manage the scheme country-wide with a sub committee from the Ministry of

Development & Economic Planning. Chiefdom Micro-Credit Committee (CMC), chaired by the

Paramount Chiefs, were established to supervise the scheme and loan Managers were appointed.

However, because of the difficulties caused by the slow economic activity and the lack of

mobility of loan monitors, the overall process was deemed satisfactory (NaSCA, 2002).

Although the availability of micro-credit from the banking system, NGOs, local associations and

cooperative remain limited, yet there are viable organisations and institutions in the country that

could lend and recover funds on a revolving basis even for the promotion of urban agriculture

Need and Demand for Credit and finance

Farmers both urban and rural feel the need to borrow. From a study on rural banking and credit

conducted in Sierra Leone (J.E. Bessel et al 1981) it was revealed that farmers have the desire to

borrow additional funds. They needed these funds (in order of priority) for hiring labour,

purchasing seeds, expansion of crops and livestock, trading, education and housing. James

Kamara in his survey reported that out of the 184 farmers interviewed, 183 expressed a desire to

borrow for several reasons: in expressing the desire to borrow additional funds from a bank, they

probably felt that it was an additional source of ready credit from an institution far away and

therefore they could ask for what they needed rather than what they could afford. Also farmers

may have exhausted that resources and therefore need to borrow from other sources even though

the repayments could be more than they can afford. Farmers need to and do borrow funds during

the planting season. When there is high demand for labour and during the time when farmers‟

savings are low. The amount that a farmer needs to borrow depends on the harvest in the

previous cycle. As indicated in the study approximately 40% of the total borrowing of farmers

was for production of which 28% was for labour and seeds and 60% for non-farm investment.

In short, farmers need credit and finance not only for production but also for investment in non-

farming activities. Therefore loans to farmers should be based on their needs rather than standard

packages.

12

The immediate potential demand for credit and finance for agriculture is restricted to traditional

practices. While there is a need to demand for credit in the form of available capital, affordable

for the poor urban producers, giving them the ability to use resource conserving farming

technology, grow higher value crops and raise higher value livestock, handle in safer ways inputs

and outputs as well acquire implements and equipment (Rose Ngara-Muraye Technical Report

2002), yet according to Malik (Malik et al, 1991) “Often socio-economic characteristics of the

borrowers (urban producers) of credit affect the demand for credit.

A potential borrower of credit will demand credit based on the need for it and the satisfaction to

be derived.

13

CHAPTER 3

RESEARCH METHODOLOGY

3.1 Study Area

The study was carried out in and around Freetown (urban & Peri-urban areas) of Western Area

as shown in Figure 1. The study was also carried out in various communities within the

Freetown Urban & Peri-urban Area. (Figure 2).

The study area is located in the Freetown municipality and peninsular within the Western Area

of Sierra Leone. It lies about 80 and 9

0 North of the equator and 4

0 and 5

0 West of Greenwich

Meridian. It is bounded on the West by the Atlantic Ocean, and extends through the peninsular

mountains. South & westwards, it is bounded by the Sierra Leone River (Rokel Estuary)

The Freetown Municipality is categorised into Urban East, Central and West. The Urban East

comprises Allen Town, Wellington, Calaba Town, Cline Town and Kissy. The Urban Central

comprises King Jimmy, Tower Hill, the central Business area, Brookfields, New England,

Dwarzack, Kroo Bay, Kroo Town Road and the Urban West comprises Tengbeh Town, Murray

Town, Aberdeen, Wilberforce, Lumley, Juba and Pottor Levuma. The Peri-urban Areas of

Freetown comprise the Thunder Hill, Mountain, York and Waterloo Wards. In the mountain

ward there are three (3) village areas: Regent, Leicester and Motaim. The Waterloo Ward has six

(6) village areas: Campbell Town, Lumpa, Benguema, Macdonald, Hastings and Waterloo. Also

the York Ward has seven (7) village areas: York, Kent, Goderich, Tombo, Sattia, Hamilton and

Banana Island.

14

Figure 1.

15

Figure 2.

Land Area & Physiography

The total land area of Western Area is 2,009sq. km of which Freetown Municipality is 82sq.km

(essay et al, 2006).

The cities of Freetown urban and peri-urban area is generally fairly steep and hills are drained by

a number of rocky seasonal flowing streams. It occupies narrow chain of hills approximately

37km long and 14m wide with average of peaks. The highest being the picket hill in the South

which rises to about 900m (Gywne-Jones et al, 1978). Where as much of the Freetown urban is

made up of semi circular hills, less than 300m high and interspersed by stream valleys from the

East to the West. The hills are well drained, where as there are waterlogged areas within the

raised beaches in the rainy season. The low lying beaches have badly drained stormy rainfed and

tidal flooded areas in the rainy season and daily throughout the seasons respectively (T.Winneba

Urban Agriculture Weekly Report, 2007).

16

Climate

Freetown urban and peri-urban area experiences hot and tropical climate with average

temperatures ranging between 230c and 34

0c with March and April being the hottest months and

August the coldest month. However, night temperatures in the interior can drop to as low as

140c during the period between December and February.

Two main seasons exist: the raining season running from May to November and the dry season

from December to April. Over half of the rainfall occurs between July & August. The highest

average annual rainfall is about 800mm occurring in August.

There is a short dry spell in September which farmers take advantage of, to dry some groundnut,

maize, spinach and krain krain seeds for second cropping in the uplands late in the month.

Vegetation characteristics

The climax vegetation of most of the Freetown Peri-urban Area forest is classified by White

(1993) as Guinea-Congolian rain forest of the hygrophilous coasted type. It has a close langay at

about 30m or more with emergent tree rising above this canopy. The drier rocky slopes and

summit support low shrub forest as their climax. The latent parts are covered by grassland since

the forest is too poor to support shrubs on high forest. The present vegetation of Freetown urban

and peri-urban area is mainly influenced by land use pattern which had resulted to biotic climatic

type of vegetation with patches of original montage forests in the reserve areas of mountain

ranges encircled by a secondary formation of farm bush in the slopes and base plateau,

exemplary only the narrow coastal strips between Juba and No.2 River villages on the Western

face and that between Kissy and Calaba Town where are found grass foundation.

Soils

The soils of the Freetown Urban and Peri-urban Area are feralitic in origin and are developed

under continuous high temperatures and constant leaching due to heavy rainfall, high rates of

run-off and rapid infiltration of water to the lower horizons. In the Greater Freetown Area most

of the soil in the highland and raised beach are greatly intent loams, and those in the low-lying

raised beaches comprise sandy loams and alluvium.

Relatively fertile soils are found at the middle and lower course of the mainstream villages

where eroded soils rich in slit and clay from the hills and mountains are deposited. It is within

these areas that farming crops is practiced.

17

Population

There are dynamics in the population of the Freetown urban and peri-urban area. The population

in the entire Western Area has increased from 554.243 in 1985 to 1,134.132 in 2004 (CSO,

2004) Freetown Peri-urban area has 361,259 (VAM survey 2005) and Freetown Urban has a

population of 772,873 consisting 15.5 percent of the National figure of 4,976,871 in 2004

(Thomas et al, 2006 Sesay et al, 2006)

Economic activities

The main economic activities of the populace in the study area are agriculture, trading, coastal

sea fishing fuel wood/charcoal collection and mining particularly sand and stones and office

work.

There are two types of farming: upland in which crops like cassava, groundnut vegetables and

rice are grown under shifting cultivation system; Swamp/lowland cultivation in which rice is

grown in the rainy season and vegetables in the dry season.

The main farming activity is vegetable growing in small farm holdings and backyard gardening,

pig and poultry production. Cereals (rice and maize) are seasonally in a subsistence manner.

Marketing/trading of agricultural products such as fruits and vegetables cassava, palm oil is

actively done mostly by women.

Also most of the active labour forces are engaged in tertiary livelihood strategies like processing

of food stuff and local vegetables in the market centres.

3.2 Research Design

The study was designed to gather qualitative and descriptive statistics from service providers

(lenders) of financial institutions and from producers groups (vegetable, pig and ornamental,

fish) and individual processors and marketers of agricultural products, receiving credit/finance

from formal and informal credit institutions as well as those who did not. The formal financial

institutions considered in this study were the Banks, Micro-finance institutions, NGOs

(development financing organisations) and the central and local government institutions.

(Ministry of Agriculture, Forestry and Food Security, Freetown City Council and Western Area

Rural District Council) Informal finance has been used to refer to all transactions, loans and

savings outside the regulation of a central monetary or financial market authority. (Adams and

Von Pischke, 1992; Aryeetey and Udry, 1997). The informal financial institutions in this study

18

consisted of self savings; remittance from relatives, rotating saving and credit schemes (Thrift

and credit, Osusu), pre-financing by input providers/traders and money lenders.

The survey was carried out during March 2010 in the financial institutions, producers sites &

market centres in the urban and peri-urban areas of Freetown: Urban East and West, Mountain,

Waterloo and York Wards.

The target population were service providers of institutions providing finance and credit and

small scale urban entrepreneurs engaged in farming, marketing and primary processing of

agricultural products who were therefore selected as the Units of study.

Data used in the study are primary data collected directly from the target population with the use

of structured questionnaires and focus group discussions. The structured questionnaires were

developed to collect information from financial institutions and the small scale enterprises.

The information collected from the financial institutions indicate a profile of the institutions and

information collected from the small scale urban entrepreneurs indicate

their responses on access to credit and finance and the views on need and demand for credit and

finance for agricultural activities.

The data collected was translated into qualitative statistics, which was analysed using descriptive

statistics. The statistical information of the survey was presented in tables and graphs.

3.3 Population and Sampling Procedures

The population selected for the study were service providers (lenders) of financial institutions;

(Banks, Micro-finance, NGOs, Central & Local Government) small scale entrepreneurs in

groups of farmers organisations involved in the production of vegetable, pig, ornamental and

aquaculture, processing and marketing of agro-products (e.g. vegetables, cassava, groundnut, hot

pepper etc.) in the urban and peri-urban Freetown in Western Area of Sierra Leone. The data

collection process required a preliminary survey in order to construct the sampling frame and

draw up a sample. A pilot survey was conducted for this purpose during the last week of

February. With the help of the Ministry of Finance, all financial institutions operating within

Freetown were identified. A population of small scale farmers (vegetable, pig, ornamentals and

aquaculture) and processors and marketers were also identified in the study area with the help of

the district offices of the Ministry of Agriculture, Forestry and Food Security and the Sierra

Leone Petty Traders Union. This included both credit and non credit users. Since there is no

official register of individual processors and marketers operating in the market centres, listing

19

was done in each market centre. Also there were no statistical information on the total farming

population in the study; therefore a list of farmers groups was obtained from those working with

the Ministry of Agriculture.

A sample size for such category of entrepreneur was determined using the small sample formula

of Cochan (1963) showing relationship between the sample size and the total population.

No sample was taken from the financial institutions that were identified through the help of

Ministry of Finance. Hence, all of them were investigated.

Sample Size Determination and Selection of Members of target population in the Urban

and Per-urban of the Western Area

To determine the sample sizes (n) of the target population for the administration of the

questionnaire, the formula given below that was propounded by Cochran (1963) will be used:

2

1 eN

Nn

Where the level of precisions for 90% confidence

Where n is the sample size, N is the population to be sampled and e is the level of precision

(which, in this case is the 90% confidence level)

Appling the formula for:

2

1 eN

Nn

Where n = sample size of the membership of the target population.

N = total membership of target population in the sample area for both Urban and Peri-Urban .

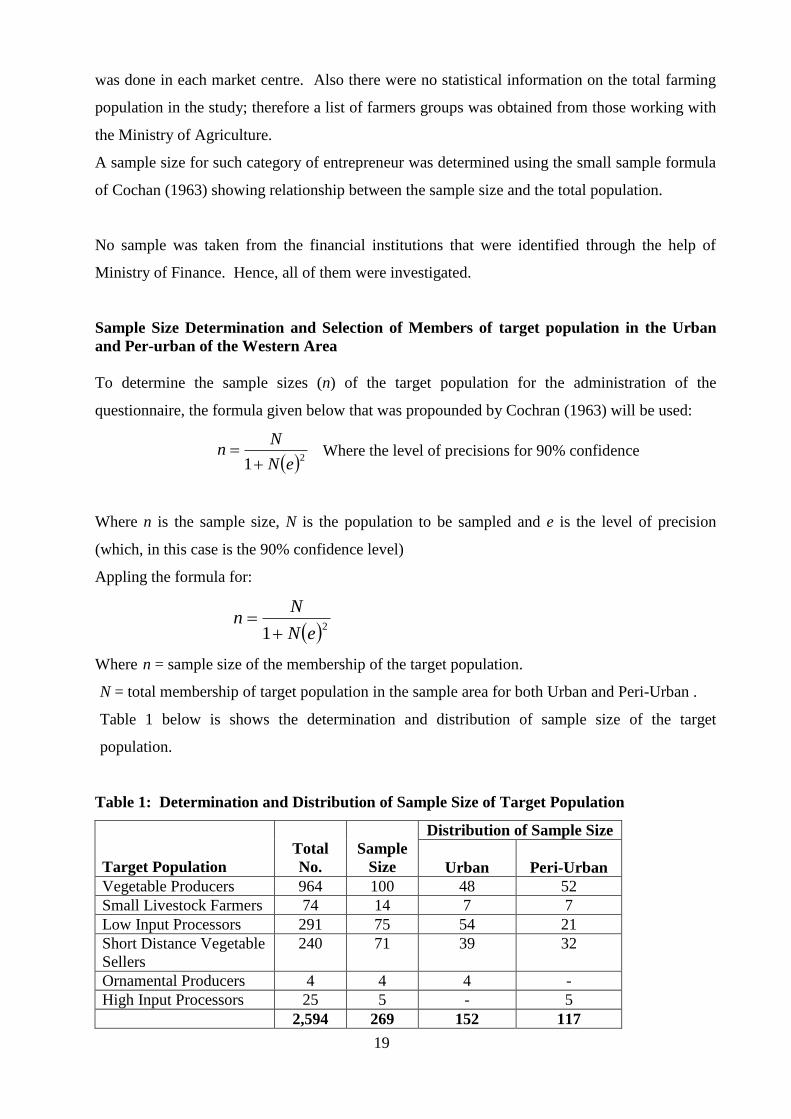

Table 1 below is shows the determination and distribution of sample size of the target

population.

Table 1: Determination and Distribution of Sample Size of Target Population

Target Population

Total

No.

Sample

Size

Distribution of Sample Size

Urban

Peri-Urban

Vegetable Producers 964 100 48 52

Small Livestock Farmers 74 14 7 7

Low Input Processors 291 75 54 21

Short Distance Vegetable

Sellers

240 71 39 32

Ornamental Producers 4 4 4 -

High Input Processors 25 5 - 5

2,594 269 152 117

20

Vegetable Producers

The sample selection of the vegetable producers was done in a way that bias was not introduced;

on reaching the area where the farmer groups whose members are to be interviewed are located

for both Urban and Peri-Urban, the first farmer group contacted was interviewed, then the

second, the third and so on. At most five members were interviewed in a farmer group. If up to

four members of a group were not present at the

period of the interview, other members of another farmer group present were interviewed to

complete the four.

A vegetable farmer in his local hot pepper production plot at Regent Village

Small Scale Livestock Farmers

The survey frame of the small scale livestock farmers consists of all the small scale livestock

farmers in the Urban and Peri-Urban areas of the western area.

We consider 20% of the total small scale livestock farmers to be taken as the sample size and

this sample size is proportional distributed among the areas. Twenty percent of the total number

of small scale livestock farmers is approximately 12.

The number of small scale farmers in each of the areas were randomly selected and interviewed.

Low Input Processors

The survey frame of the low input processors consists of all the low input processors in the

Urban and Peri-Urban areas of the western area.

The distribution of the low input processors is already shown in table 1.

The selection of the processors to be interviewed was done randomly from the list of the low

input processors.

21

Peri-urban food processors grinding groundnut and cassava leaves at the Waterloo market

centre

High Input Processors

The survey frame of the high input processors consists of all the high input processors in

Waterloo Ward in the Peri-urban area. The total number of high input processors in the Waterloo

Ward is 25.

We consider 20% of the total high input processors to be taken as the Sample Size. Twenty

percent of the total high input processors are approximately 5.

The number of high input processors in Waterloo Ward in the Peri-urban area were randomly

selected and interviewed.

High input food processors processing cassava into bread in the peri-urban area at

Waterloo village.

22

Short Distance Vegetable Sellers

The survey frame of the short distance vegetable sellers consists of all the Short distance

vegetable sellers in the Urban and Peri-Urban areas of the western area.

The distribution of the Vegetable sellers is shown in Table 1

The selection of the short distance sellers to be interviewed was done randomly from the list of

the short distance sellers.

Vegetable (plasas) sellers selling in the peri-urban area.

Ornamentals Plants and Flowers Producers

In this survey, producers of ornamental plants and flowers were also interviewed. However since

there were only four in the area, all of them were interviewed.

Long Distance Marketers

Focus group discussion was also used to obtain information from the long distance marketers.

Since there are only two big marketing centers for the long distance marketers, two focus group

discussions were done; one in each of the market centre.

23

Aquaculture (Fish)

For the purpose of this survey, information was got from the fishing communities through focus

group discussions.

Twenty percent of the fishing communities were selected at random and focus group discussion

were done in the selected communities. There are 16 fishing communities; one in the Urban area

and 15 in the Peri-Urban area. Twenty percent of the 17 fishing communities is approximately 4.

Therefore the one community in the urban area was selected and three were randomly selected

from Peri-Urban area.

Tokeh fishermen undertaking fishing along the village beach in the community.

3.4 Research Instruments

Structured questionnaires were developed with a focus on the research objectives of the study to

be achieved. Questionnaires were used to obtain relevant information of the study. A pilot test

was conducted to verify the validity and reliability of the questionnaire. The questionnaire was

later modified for the final implementation. This was to ensure that the questionnaire was free

from errors and the questions would give the appropriate information for achieving the

objectives of the study. Data collection was carried out by the researcher and members of the

study team from the stakeholder institutions. Data collectors were given a day training on how to

24

collect valid and reliable data. Focus group discussions were also conducted and held with four

fishing communities and two communities of long distance marketers in order to obtain

information on credit and finance.

The items on the questionnaires focused on the specific variables of the study: Existing financial

institutions and demand for credit and finance. The items on the questionnaire for existing

financial institutions were further categorized into four (4) parts namely: basic data, financial

products for agriculture factors/challenges in financing small scale urban agriculture and future

prospects for financing urban agriculture.

Basic data: Information collected in this section was based on the name and type of institution,

year of creation, operational areas within the study area.

Financial products: Information collected in this area was based on the products offered by the

financial institutions and available for agriculture, conditions and terms of access; minimum and

maximum value of the products.

Factors/challenges in financing small scale urban agriculture: Information collected in this

area was based on main factors that hamper financing of small scale producers and what might

be done to foster financing of urban agriculture.

Further prospects for financing urban agriculture: Information in this area was based on the

institutions expectations regarding financing urban agriculture with regards to volume, type of

financing and conditions.

Also additional information was collected from the financial institutions involved in financing

UA and the target population.

The information collected from the institutions financing UA include: origin of financial

resources, value of cumulated loans given, value of outstanding loans and financial assistance to

the urban poor farmers.

The items on the questionnaire focusing demand for credit and finance were also categorized

into six (6) sections namely: Basic data, occupation, access to credit and finance, need for credit

and finance, demand for credit and finance and challenges in accessing credit and finance.

Section 1 Basic data:

Information collected in this section was based on the respondent‟s name, sex, address, religion,

ethnicity and membership in farmers‟ organisation or traders‟ union.

25

Section 2 Occupation:

Information collected in this section was based on respondent‟s engagement in agricultural

activity:

Section 3 Access to credit

Information collect in this section was based on the respondent‟s way and means of financing his

or her activity.

Section 4 Need for credit and finance

Information collected in this section was based on respondent‟s financing needs to undertake his

or her activity.

Section 5 Demand for credit and finance

Information collected in this section was based on the respondent‟s demand for credit and

finance to improve and expand his or her activity.

Section 6 Challenges in accessing credit and finance

Information collected in this section was based on the respondent‟s (1) Problems encountered to

access credit and finance from financial institutions. (2) Views on possible solutions to the

problems encountered in accessing credit and finance.

Also additional information on the type of osusus and remittances channels and practices

were also collected as follows: size of the osusu groups, duration of the cycle, value of savings,

kind of relative, estimated amount received, channel of receiving money, conditions for

remittances and frequency of money remitted

3.5 Data Analysis

The data collected from the survey was analysed using statistical description represented in

graphs and tables. The figures illustrate the outcome of the study. Discussion of the result of the

findings in relation to the objectives stated form part of the analysis. Highlights of the

implications of the findings were included in the discussions. Finally, summary of findings and

recommendations was given.

26

CHAPTER 4

INSTITUTIONS PROVIDING CREDIT AND FINANCE IN WESTERN AREA

This chapter and next present the results of this study. This Chapter examines the existing

financial institutions that provide credit and finance facilities in the urban and peri-urban

Freetown for producers, processors and marketers. The next Chapter assesses the need and

demand for credit and finance from financial institutions by the urban poor engaged in

production, processing and marketing activities in and around Freetown.

The study shows that there exist a number of credit institutions that provide credit and finance in

the study area. These institutions include commercial banks, micro-finance institutions, central

government ministries, local councils and NGOs. From the inventory survey, there are twenty-

seven of such, thirteen commercial banks, eight micro-finance, three NGOs and three

government institutions. As shown in the table below commercial banks are the principal service

provider of credit and finance and accounts for 48% of all credit and financing.

Table 2: shows distribution of Credit and Finance Institutions

Institution No. Percentage

Commercial Bank 13 48.2

Micro-finance 8 29.6

NGOs 3 11.1

Governmental (Local & Central 3 11.1

Total 27 100

4.1 Commercial Banks and their Financing Practices

The thirteen commercial banks that are operating are: First International Bank, Union Trust

Bank, Rokel Commercial Bank, Eco Bank, Access Bank, Standard Chartered Bank, United Bank

for Africa UBA - SL, Skye Bank, Zenith Bank Ltd, International Commercial Bank, Guaranty

Trust Bank and Sierra Leone Commercial Bank.

Majority of these banks started operations from the late 90‟s up to now; the oldest in 1894 and

that is the Standard Chartered Bank. The banks provide credit loans including overdraft

advances and amortise to a wider range of beneficiaries which include farmers/farmers groups,

small and medium entrepreneurs, importers, exporters, corporate borrowers, traders, fisherfolks,

27

legal companies and employees of credible institutions. First International Bank, Access Bank,

Zenith Bank and Guaranty Trust Bank specifically offer financial assistance to farmers and

fisherfolks.

All the banks provide financial services for either agriculture and or trading with the majority

(eight banks) for Production, Marketing and agro-processing. These banks are First

International, Union Trust, Eco Bank, Access, Standard Chartered, Zenith Bank, Guaranty Trust

and Sierra Leone Commercial Bank. The United Bank for Africa UBA, Skye Bank,

International Commercial Bank and Bank PHB Sierra Leone do not provide financial services

for agriculture in and around Freetown.

It means that, in the area of credit and financing opportunities for agriculture and according to

the study, commercial banks can provide financial assistance for urban agriculture.

The loan terms and conditions of the banks vary from one bank to the other. Collateral is

required in various forms depending on the bank. Most of the banks require guarantee including

personal guarantee except for Access and Standard Chartered.

From the study, no loan terms and conditions were set by United Bank for Africa UBA, Skye

Bank, Bank PHB Sierra Leone and Zenith Bank since they do not offer loans for urban

agriculture.

The minimum amount of loans offered by the banks varies and range from five hundred

thousand Leones (Le500,000), offered by Eco Bank to five hundred millions Leones (Le500m)

offered by Zenith Bank The maximum amount of loans range from one million five hundred

thousand (Le1.5m) offered by Eco Bank to one and the half billion Leones (Le1.5B) which is

offered by Access Bank.

It means that agriculture in around the Freetown city can be financed for small scale enterprises

as well as for large investments through the Commercial Banks. The Rokel Commercial Banks

are negotiable on a case by case basis.

Interest rates charged by the banks range from fifteen percent (15%) offered by First

International Bank and Guaranty Bank to forty seven percent (47%) offered by First

International Bank and Eco Bank. However, most of the banks charge between twenty and

twenty-five percent (20%-25%) interest rates. The highest interest rate of forty to forty-seven

percent is charged by First International Bank and Eco Bank. In respect of the loan terms and

conditions of the banks, it implies that large amount of loans are or can be offered for agriculture

28

but with high interest rates, and the collateral and guarantee required actually would stand in the

way of smallholder and the poor in obtaining credit.

Down payment is not a requirement for most of the banks except for Rokel Commercial Bank

which requires down payment depending on level of comment and the type of financial product.

Loan repayment period range from one day up to seven years depending on the loan amount.

First International bank allows seven (7) years repayment period because of the Agriculture Hire

Purchase Scheme for farm machinery, tractors it offers, whereas Eco bank allows a day up to

eighteen (18) months because it offers small credit (micro-credit).

The repayment period therefore depends on the size of the loan offered by the banks that is, for

small amounts, the repayment period is short and for large amounts the period is long.

Grace period for loan repayment varies with the banks but range from two (2) to three (3)

months.

However, some banks like Access bank, International Commercial Bank and Guaranty Bank do

not have grace period.

For Standard Chartered Bank the grace period is negotiable and it varies for Union Trust Bank,

Rokel Commercial Bank, and Sierra Leone Commercial Bank as it is applied wherever possible.

In short, the grace period a bank allows is a necessity for loan repayment but may or may not

suit the interest of the target group (urban farmers). Accessing loans from the banks involves the

following: application from the customer, appraisal or review of application, discussion on loan

terms and conditions, approval or acceptance and disbursement. For Guaranty Bank, Zenith

Bank, Sierra Leone Commercial Bank and International Commercial Bank the process is short

and requires just application from the customers.

The challenges the banks face in giving out loans for agriculture from the multiple responses

include the following as outlined in the table below:

Table: 3- Descriptive Statistics of Challenges face by the banks.

Challenges Faced By Banks Count %

In Security of land tenure 2 10

No mechanism in the city to get secure land 4 20

Late payment of loans 2 10

29

Formal deed require for credit 5 25

Lack of savings account 3 15

Beneficiaries in ability to handle & manage

loans

1 5

Lack of legislation 3 15

Total 20 100

It is seen that the problems of formal deed required for in credit, no mechanism in the Freetown

City to get secure land, lack of savings account legislation (in ranking order) are faced by banks.

The perception of the banks with regards to what might be done to foster financing urban

agriculture are that proper mechanism or law for land tenure system should be put in place by

government, reduction of risk entailed in informal businesses through business development,

increased commitment of the beneficiary farmers towards repayment of loans.

First International Bank, Union Trust Bank, Eco Bank, Access Bank, Standard Chartered Bank,

Bank PHB Sierra Leone and Sierra Leone Commercial Bank intend to finance agriculture

(production, marketing, marketing and agro-processing) in and around the Freetown City while

the other remaining six (6) banks have no intention.

Future prospects of the banks for financing urban agriculture from the multiple responses are

outlined below:

Table: 4. Future Prospects for Financing UA by the banks

Future Prospects for financing UA Count

Involvement in agric hire purchase through individual and group loan offer 1

Access to farm – sites, assumed markets and readiness of the beneficiaries to pre

finance the business

1

Required business plans for viability and profitability management potentials and loan

security

2

Finance those already involved in agriculture activities 1

Advance loans to agric groups guaranteed by agro-project funds 1

Finance those that fall under the normal banking consideration 1

Total 7

30

Of the Seven Banks that intend to financial Urban Agriculture one of them, that is, First

International Bank would want to involve in agriculture hire purchase scheme through individual

and group loan offer. Two of the banks Eco Bank, and Standard Chartered would require

business plans for viability and profitability management potentials and loan security. Union

Trust Bank will require the Bank‟s access to beneficiaries‟ farm sites, assumed matters and

readiness of beneficiaries to pre-finance the business for financing Urban Agriculture.

Only one bank, PHB Sierra Leone that intends to finance beneficiaries already involved in

agricultural activities and those with security from Government or Insurance Company, where as

another bank that is the Access Bank, will advance loans to agricultural groups guaranteed by

agro- project funds. The Sierra Leone Commercial bank also indicates that they will finance

beneficiaries that fall under the normal banking consideration for production and agro-

processing.

In addition, the banks intend to provide loans based on requests, individual‟s business plan

projection for procurement of agricultural inputs and machinery.

4.2 Micro Finance Institutions and their Financing practices

The eight micro-finance institutions studied are:

Lift above Poverty Organisation LAPO, Luma Micro Finance Trust, Salone Micro-Finance

Trust, Finance Salone, Hope Micro-finance, BRAC micro-finance (SL) limited, Gender and

Grass root Empowerment Movement GGEM Micro-finance Services Limited and Association

for Rural Development ARD.

Almost all of the micro-finance institutions started operations in the city between 2002 - 2009,

but Association for Rural Development ARD started in 1986. The micro-finance institutions

offer micro-credit to women traders, monthly salary earners, and vegetable sellers for agriculture

and mainly petty trading and also as salary loan.

Only four of these institutions (LUMA, Salone micro-finance, Finance Salone, Hope micro

finance) offer assistance for urban agriculture mainly marketing and agro-processing. LUMA

and Hope Micro finance offer financial assistance also for production.

The Lift above Poverty Organisation LAPO, BRAC micro finance Limited, GGEM and ARD do

not fund urban agriculture.

31

With terms & conditions for the micro-credit, most institutions require collateral of ten to fifteen

percent (10% - 15%). Only BRAC micro-finance Limited does not have terms and conditions

for the micro-credit because it does not provide finance for urban agriculture.

All the institutions require guarantee in the form of group solidarity except for LAPO which

does not require this.

The minimum value of the micro-credit that the institutions offer is between three hundred

thousand (Le300, 000) and five hundred thousand Leones (Le500,000).

LAPO offers two hundred and ten thousand Leones (Le210, 000) as minimum and three hundred

thousand Leones as maximum.

The maximum value offer is between five hundred thousand to four million Leones. The Salone

micro-finance trust gives one million (Le1m) Leones as maximum amount for micro-credit

whereas Finance Salone gives four million Leones (Le4m).

Interest rate charge per year is thirty to thirty-six percent (30% – 36%) and per month is (two and

the half to three percent (2.5% - 3%).

When comparing the interest rates of the banks and micro institutions the highest rate for the

banks is forty-seven percent (47%) and that of the micro finance institutions is thirty six percent

(36%). On the average the interest rate of the banks is thirty one percent (31%) and for the MFIs

thirty six percent (36%) This can be attributed to the fact that the MFIs obtain loans from the

banks for subsequent disbursement to beneficiaries and would require paying interest.

The micro finance institutions do not require any down payment for the micro-credit provided.

Repayment period is between one (1) month to one (1) year, but some institutions allow four (4)

to five (5) months.

Accessing micro credit from the institutions requires the following steps: sensitization of

beneficiaries, application from beneficiaries, and verification by the institutions, approval and

disbursement.

All the micro finance institutions stated that they face no challenges in giving out micro credit

except that some of them LUMA and Salone Micro Finance Trust may require adequate funds to

meet the demand of the beneficiaries.

Almost all of them do intend to finance urban agriculture except for Hope micro-finance and

Association for Rural Development ARD. They intend to provide finance under these

considerations:-

32

LAPO, LUMA and Salon Micro Finance Trust indicate that beneficiaries to be finance

should be the right kind of clients engaged in agricultural business

Salon micro- Finance Trust indicates that beneficiaries should exist in groups with

government and National Associations of Farmers Sierra Leone NAFSL as third party

LAPO and Finance Salone will finance beneficiaries who have the capacity to provide

the required collateral.

Under future prospects for financing urban agriculture Salone Micro Finance Trust intend to

provide finance for inputs (seed, fertilizer) and processing machines. GGEM Micro Finance

Services Limited intends to give small loans for short term cropping. Finance Salone, Luma

Micro Finance Trust and LAPO will finance marketing of produce and agro-processing business.

It is seen that micro-finance institutions are possible financing sources for urban agriculture as

they are already providing and intend to provide financial assistance for urban agriculture.

The micro-credit provided by these institutions is small enough to meet the short term financial

needs of the urban poor engaged in production, marketing and processing. Group solidarity is a

strong guarantee for accessing micro-credit loans and therefore the urban farmers, marketers and

processors must be organized in functional groups.

The short repayment period does not permit any down payment although interest rates are high

with an average of 31 % for the banks and 33 % for the MFIs.

Value of cumulated and outstanding loans from banks and MFIs.

Table 5 Descriptive statistics on value of cumulated & outstanding loans from

Institutions

Financial Institution

Total value

cumulated Loans

Le’000m

Total value

outstanding of

Loans

Le’000m

Percentage

of

Outstanding

Loans

Access Bank 2,000,000 - 0

First International

Bank

8,500,000 3,500,000 41.2

Finance Salone

Limited

1,600,000 640,000 40

Luma Micro-finance

Trust

99,661 66,440 67

33

Hope Micro-Finance

Services

1,500,000 1,100,000 73.3

Salone Micro-Finance

Trust

775,900 460,651 59.3

Total 14,475,561 5,767,091 39.8

Information was also obtained from the institutions on the value of cumulated loans that were

disbursed and outstanding loans to be recovered from the beneficiaries. It was found that only

two banks and four MFIs have given credit and finance to the urban poor engaged in agricultural

activities. A total of 14 .4 billion Leones have been given out especially for marketing and agro-

processing with a little for producing. However a total of 5.7 billion Leones are outstanding

about 39.8 % to be collected within the given time that the repayment period. These funds have

been given by various donors for instance Salone Micro finance trust has received funds from K

IVA an American based organization and partly from UNIDO;LUMA from CORDAID , Eco

Bank and Rokel Commercial Bank; Finance Salone from American Refugee Council and Hope

Micro finance trust from World Hope International United States of America.

4.3 Government Institutions and Local Authorities and their Financing practices

The Government Institutions that operate in the study area provide finance and credit for urban

and peri-urban agriculture are the Ministry of Agriculture, Forestry and Food Security MAFFS,

the Local Councils, Freetown City and Western Area Rural District Council. There is also the

Rural and Private Sector Development Project (world bank funded) jointly implemented by the

Ministry of Trade and Industry and the Ministry of Agriculture, Forestry and Food Security,

(MAFFS) providing finance for peri-urban agriculture.

Ministry of Agriculture Forestry and Food Security (MAFFS)

The MAFFS has been in operation in the entire Western Area providing extension

Services to urban and peri-urban farmers. Such services include input supply in the form of

seeds, fertilizer, tools, livestock treatment with veterinary drugs and vaccines and training. Funds

were provided by the central government to finance these activities for the farmers.

Freetown City Council (FCC)

In 2006, funds for agriculture were devolved from the Central Government (MAFFS) to the

Councils FCC for the implementation of devolved agricultural functions in the form of tied

grants. The grants are used to finance small projects purely production designed by MAFFS and

FCC for urban farmers.

34

There are no terms and conditions for the grant except that the beneficiaries (urban farmers) are

organized into functional groups inorder to benefit from such assistance.

The amount of grant allocated from Central Government MAFFS to FCC for 2010 is Le132,

921.351M .The grant funding by MAFFS through FCC is on-going.

The Challenges faced by the Council are lack of meaningful implementation of agricultural

projects and programmes and also the 2009 remittance of funds does not meet the planned

budget of the programmes.

Western Area Rural District Council (WARDC)

The Western Area Rural District Council Started operations in 2004 by the Local Government

Act in the Western Area Rural District which is the peri- urban area of Freetown. In 2006 funds

from the central Government through the Ministry of Agriculture was remitted to WARDC to

support small scale farmers within the peri urban area in the form of production inputs like seeds

cassava and sweet potato cuttings and fertilizer and small hand tools including veterinary drugs

and vaccines for livestock treatment. The Council aims at promoting small scale farmers in food

security within the frame work of the Poverty Reduction Strategy Paper pillar 2 (PRSP 11).

The amount of grant remitted to the council by the central government is thirty five million

Leones (Le35M) minimum and maximum one hundred million Leones (Le 100M).

The challenges the council faces are lack of cooperation from the farming communities and

inadequate funds to fully and effectively support the farmers. The council therefore requests the

central government to increase the grant allocation in order to empower farmers in the district.

Rural and Private Support Development Project (RPSDP)/ MAFFS/MTI

The Rural and Private Support Project RPSDP of MAFFS & the Ministry of Trade and Industry

(MTI) started operations in 2008 in the Western Area Rural District part of which forms the peri-

urban areas. (Mountain, waterloo, York)

This project provides grants to farmers groups, traders in agricultural products purely for

marketing and agro-processing activities. The project does not fund production.

The terms and conditions of the project for grant assistance are group solidarity as a guarantee,

group registration with WARDC and group savings account. The minimum value of the grant

provided is five thousand dollars ($5,000) the maximum is forty thousand dollars ($40,000).

(One dollar $1 is equivalent to four thousand Leones Le4, 000).

35

To access the grant, it requires application from the beneficiary group, group project proposal,

approval by a coordination committee and disbursement.