appendix a mining industry profile - us epa a mining industry profile. ... the extraction and...

TRANSCRIPT

APPENDIX A

MINING INDUSTRY PROFILE

MINING INDUSTRY PROFILE

September 1997

TABLE OF CONTENTS

1. Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-1

2. Location of Mining Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-4

3. Mining Practices and Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-10

4. Mining and the Economy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-17

5. Inactive and Abandoned Mines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-20

6. Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-21

7. References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-23

MINING INDUSTRY PROFILE

September1997 A - 1

1. OVERVIEW

This overview provides summary information on 11 commodities (10 non-fuel and uranium) that are

produced from the most important metalliferous and fertilizer ores in the United States. The combined

value of these minerals (copper, gold, iron ore, lead, molybdenum, phosphate rock, platinum, potash, silver,

uranium, and zinc) was $12.15 billion in 1993, accounting for less than 1 percent of gross national product

(GNP) (U.S. Department of Commerce, 1994).

This appendix is intended to provide an overview of mining activities and the mining industry, not a

comprehensive examination. It is necessarily simplistic, but should give a snapshot of the industry as it

existed in 1992. This framework recognizes the dynamic nature of this vital industry and the market,

technological, and other factors that drive its performance, environmental and otherwise.

These metals and minerals are the primary raw materials used in many industrial applications and

thus are essential to the American and world economies. Copper, for example, is essential to the

electronics and construction industries, while iron ore provides the base material for the steel, automotive,

and transportation industries. Molybdenum is used in steel production, machinery, electrical and chemical

manufacturing. Potash and phosphate rock are used in fertilizers and chemical manufacturing. Gold, while

primarily used in jewelry and the decorative arts, is also used in the electronics industry and dentistry.

Table 1 provides a more detailed list of the consumptive uses for these minerals.

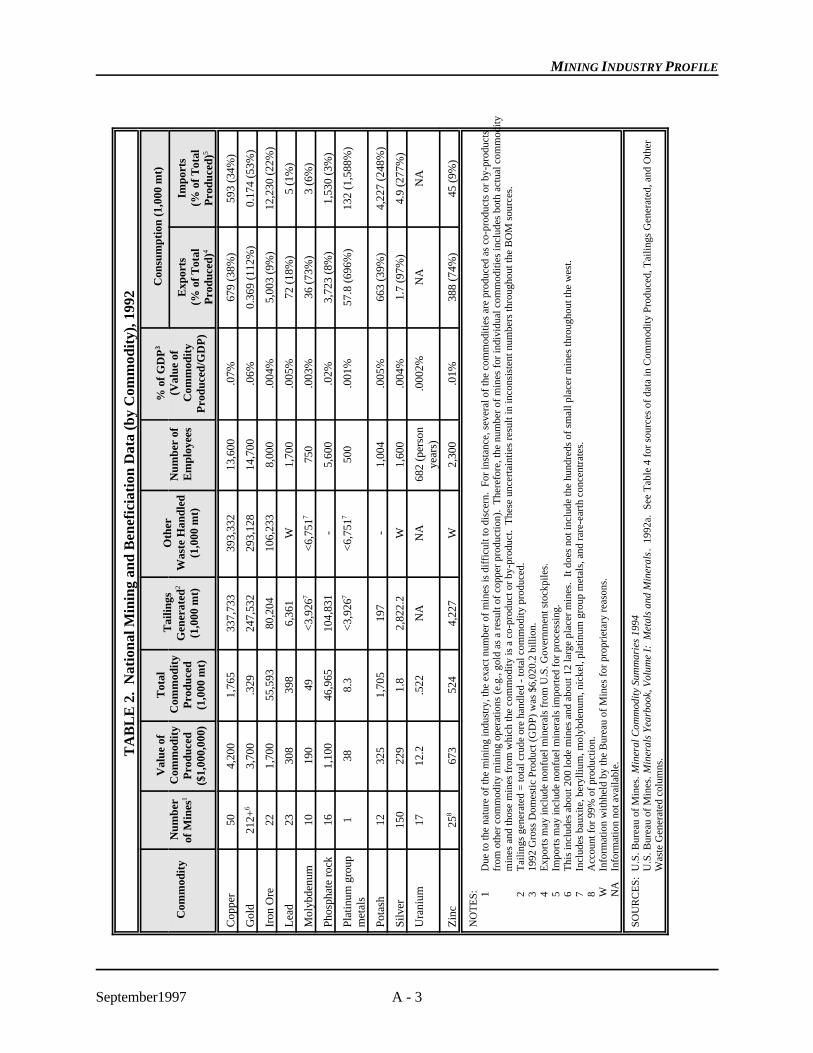

The minerals industry also contributes to the national economy by virtue of its production of exports

and its reduction of industrial dependence on certain minerals that the United States would otherwise

import. For example, the U.S. exports 8% of the lead and 75% of the molybdenum it produces.

Conversely, the U.S. imports 22% of the iron ore it consumes (Bureau of Mines, 1995). See Table 2 for

detailed national production data (including import and export information) for these minerals.

The extraction and beneficiation of these minerals necessarily lead to the generation of large quantities

of waste. Total waste (waste rock and tailings) produced during the extraction and beneficiation of

minerals can range from 10% of the total material removed from the earth (potash) to more than 99.99%

(gold). As for total amounts of waste generated in 1992, the gold mining industry generated about

540,661,000 metric tons and the copper mining industry generated 731,065,000 metric tons; potash, on the

other hand, generated 197,000 metric tons (Bureau of Mines, 1992a). To put these quantities in

perspective, about 200,000,000 metric tons of municipal solid waste are generated in the United States

each year.

MINING INDUSTRY PROFILE

September1997 A - 2

TA

BL

E 1

. N

umbe

r of

Min

es, T

otal

Pro

duct

ion

and

Use

s of

Com

mod

itie

s of

Con

cern

, 199

2

Com

mod

ity

Num

ber

of m

ines

1M

ajor

use

sT

otal

U.S

. min

epr

oduc

tion

(m

etri

c to

ns)

Pro

duct

ion

as %

of c

onsu

mpt

ion

Cop

per

50B

uild

ing

cons

truc

tion,

ele

ctri

cal a

nd e

lect

roni

c pr

oduc

ts, I

ndus

tria

lm

achi

nery

and

equ

ipm

ent,

tran

spor

tatio

n eq

uipm

ent,

and

cons

umer

and

gene

ral p

rodu

cts

1,76

5,00

075

%

Gol

d21

2+2

Jew

elry

and

art

s, in

dust

rial

(m

ainl

y el

ectr

onic

), d

enta

l32

930

0%

Iron

Ore

22St

eel

55,5

93,0

0074

%

Lea

d23

Tra

nspo

rtat

ion

(bat

teri

es, f

uel t

anks

, sol

der,

sea

ls, a

nd b

eari

ngs)

;el

ectr

ical

, ele

ctro

nic,

and

com

mun

icat

ions

use

s39

8,00

032

%

Mol

ybde

num

10Ir

on a

nd s

teel

pro

duct

ion,

mac

hine

ry, e

lect

rica

l, tr

ansp

orta

tion,

chem

ical

s, a

nd o

il an

d ga

s in

dust

ry u

ses

49,0

0028

7%

Phos

phat

e R

ock

16W

et-p

roce

ss p

hosp

hori

c ac

id, f

ertil

izer

s46

,965

,000

109%

Plat

inum

gro

upm

etal

s1

Aut

omot

ive,

ele

ctri

cal a

nd e

lect

roni

c, c

hem

ical

, den

tal,

med

ical

8,30

012

%

Pota

sh12

Fert

ilize

rs, c

hem

ical

man

ufac

turi

ng1,

705,

000

32%

Silv

er15

0Ph

otog

raph

ic p

rodu

cts,

ele

ctri

cal a

nd e

lect

roni

c, e

lect

ropl

ated

war

e, s

terl

ingw

are,

and

jew

elry

1,80

0N

A

Ura

nium

17E

nerg

y (f

uel r

ods)

522

NA

Zin

c25

3C

hem

ical

, agr

icul

tura

l, ru

bber

, and

pai

nt in

dust

ries

524,

000

41%

NO

TE

S: 1D

ue to

the

natu

re o

f th

e m

inin

g in

dust

ry, t

he e

xact

num

ber

of m

ines

is d

iffi

cult

to d

isce

rn.

For

inst

ance

, sev

eral

of

the

com

mod

ities

are

pro

duce

das

co-

prod

ucts

or

by-p

rodu

cts

from

oth

er c

omm

odity

min

ing

oper

atio

ns (

e.g.

, gol

d as

a r

esul

t of

copp

er p

rodu

ctio

n).

The

refo

re, t

he n

umbe

r of

min

es f

or in

divi

dual

com

mod

ities

incl

udes

bot

h ac

tual

com

mod

ity m

ines

and

thos

e m

ines

fro

m w

hich

the

com

mod

ity is

a c

o-pr

oduc

t or

by-

prod

uct.

The

se u

ncer

tain

ties

resu

lt in

inco

nsis

tent

num

bers

thro

ugho

ut th

e B

OM

sou

rces

.2

Thi

s in

clud

es 2

00 lo

de m

ines

and

12

larg

e pl

acer

min

es.

It d

oes

not i

nclu

de th

e hu

ndre

ds o

f sm

all p

lace

r m

ines

thro

ugho

ut th

e w

est.

3

Acc

ount

for

99%

of

prod

uctio

n.

Sour

ces:

U

.S. B

urea

u of

Min

es.

Min

eral

Com

mod

ity S

umm

arie

s 19

94.

U.S

. Bur

eau

of M

ines

. M

iner

als

Year

book

, Vol

ume

I: M

etal

s an

d M

iner

als.

199

2U

.S. B

urea

u of

Min

es.

Min

eral

s Ye

arbo

ok, V

olum

e II

: A

rea

Rep

orts

: D

omes

tic.

1992

.

MINING INDUSTRY PROFILE

September1997 A - 3

TA

BL

E 2

. N

atio

nal M

inin

g an

d B

enef

icia

tion

Dat

a (b

y C

omm

odit

y), 1

992

Com

mod

ity

Num

ber

of M

ines

1

Val

ue o

fC

omm

odit

yP

rodu

ced

($1,

000,

000)

Tot

alC

omm

odit

yP

rodu

ced

(1,0

00 m

t)

Tai

lings

Gen

erat

ed2

(1,0

00 m

t)

Oth

erW

aste

Han

dled

(1,0

00 m

t)

Num

ber

ofE

mpl

oyee

s

% o

f G

DP

3

(Val

ue o

fC

omm

odit

yP

rodu

ced/

GD

P)

Con

sum

ptio

n (1

,000

mt)

Exp

orts

(% o

f T

otal

Pro

duce

d)4

Impo

rts

(% o

f T

otal

Pro

duce

d)5

Cop

per

504,

200

1,76

533

7,73

339

3,33

213

,600

.07%

679

(38%

)59

3 (3

4%)

Gol

d21

2+6

3,70

0.3

2924

7,53

229

3,12

814

,700

.06%

0.36

9 (1

12%

)0.

174

(53%

)

Iron

Ore

221,

700

55,5

9380

,204

106,

233

8,00

0.0

04%

5,00

3 (9

%)

12,2

30 (

22%

)

Lea

d23

308

398

6,36

1W

1,70

0.0

05%

72 (

18%

)5

(1%

)

Mol

ybde

num

1019

049

<3,

9267

<6,

7517

750

.003

%36

(73

%)

3 (6

%)

Phos

phat

e ro

ck16

1,10

046

,965

104,

831

-5,

600

.02%

3,72

3 (8

%)

1,53

0 (3

%)

Plat

inum

gro

upm

etal

s 1

388.

3<

3,92

67<

6,75

1750

0.0

01%

57.8

(69

6%)

132

(1,5

88%

)

Pota

sh12

325

1,70

519

7-

1,00

4.0

05%

663

(39%

)4,

227

(248

%)

Silv

er15

022

91.

82,

822.

2W

1,60

0.0

04%

1.7

(97%

)4.

9 (2

77%

)

Ura

nium

1712

.2.5

22N

AN

A68

2 (p

erso

nye

ars)

.000

2%N

AN

A

Zin

c25

867

352

44,

227

W2,

300

.01%

388

(74%

)45

(9%

)

NO

TE

S: 1D

ue to

the

natu

re o

f th

e m

inin

g in

dust

ry, t

he e

xact

num

ber

of m

ines

is d

iffi

cult

to d

isce

rn.

For

inst

ance

, sev

eral

of

the

com

mod

ities

are

pro

duce

d as

co-

prod

ucts

or

by-p

rodu

cts

from

oth

er c

omm

odity

min

ing

oper

atio

ns (

e.g.

, gol

d as

a r

esul

t of

copp

er p

rodu

ctio

n).

The

refo

re, t

he n

umbe

r of

min

es f

or in

divi

dual

com

mod

ities

incl

udes

bot

h ac

tual

com

mod

itym

ines

and

thos

e m

ines

fro

m w

hich

the

com

mod

ity is

a c

o-pr

oduc

t or

by-p

rodu

ct.

The

se u

ncer

tain

ties

resu

lt in

inco

nsis

tent

num

bers

thro

ugho

ut th

e B

OM

sou

rces

.2

Tai

lings

gen

erat

ed =

tota

l cru

de o

re h

andl

ed -

tota

l com

mod

ity p

rodu

ced.

319

92 G

ross

Dom

estic

Pro

duct

(G

DP)

was

$6,

020.

2 bi

llion

.4

Exp

orts

may

incl

ude

nonf

uel m

iner

als

from

U.S

. Gov

ernm

ent s

tock

pile

s.5

Impo

rts

may

incl

ude

nonf

uel m

iner

als

impo

rted

for

pro

cess

ing.

6T

his

incl

udes

abo

ut 2

00 lo

de m

ines

and

abo

ut 1

2 la

rge

plac

er m

ines

. It

doe

s no

t inc

lude

the

hund

reds

of

smal

l pla

cer

min

es th

roug

hout

the

wes

t.

7In

clud

es b

auxi

te, b

eryl

lium

, mol

ybde

num

, nic

kel,

plat

inum

gro

up m

etal

s, a

nd r

are-

eart

h co

ncen

trat

es.

8A

ccou

nt f

or 9

9% o

f pr

oduc

tion.

WIn

form

atio

n w

ithhe

ld b

y th

e B

urea

u of

Min

es f

or p

ropr

ieta

ry r

easo

ns.

NA

Info

rmat

ion

not a

vaila

ble.

SOU

RC

ES:

U.S

. Bur

eau

of M

ines

. Min

eral

Com

mod

ity S

umm

arie

s 19

94U

.S. B

urea

u of

Min

es. M

iner

als

Year

book

, Vol

ume

I: M

etal

s an

d M

iner

als.

199

2a.

See

Tab

le 4

for

sou

rces

of

data

in C

omm

odity

Pro

duce

d, T

ailin

gs G

ener

ated

, and

Oth

erW

aste

Gen

erat

ed c

olum

ns.

MINING INDUSTRY PROFILE

September1997 A - 4

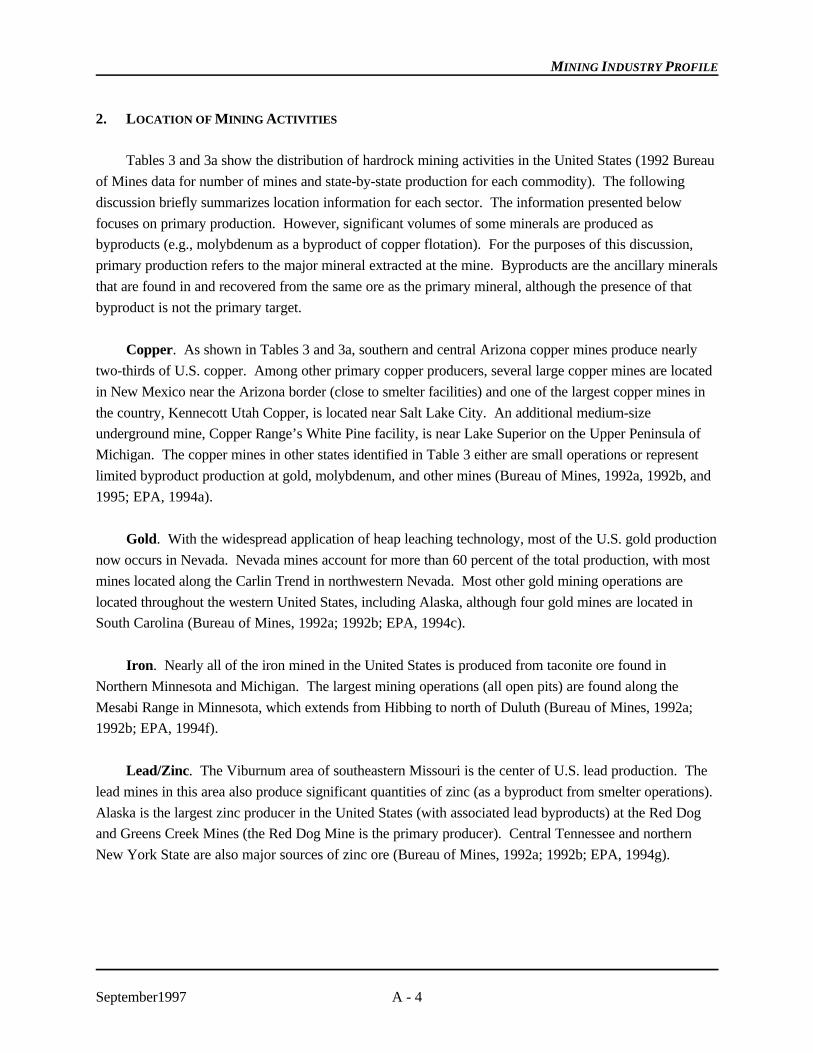

2. LOCATION OF MINING ACTIVITIES

Tables 3 and 3a show the distribution of hardrock mining activities in the United States (1992 Bureau

of Mines data for number of mines and state-by-state production for each commodity). The following

discussion briefly summarizes location information for each sector. The information presented below

focuses on primary production. However, significant volumes of some minerals are produced as

byproducts (e.g., molybdenum as a byproduct of copper flotation). For the purposes of this discussion,

primary production refers to the major mineral extracted at the mine. Byproducts are the ancillary minerals

that are found in and recovered from the same ore as the primary mineral, although the presence of that

byproduct is not the primary target.

Copper. As shown in Tables 3 and 3a, southern and central Arizona copper mines produce nearly

two-thirds of U.S. copper. Among other primary copper producers, several large copper mines are located

in New Mexico near the Arizona border (close to smelter facilities) and one of the largest copper mines in

the country, Kennecott Utah Copper, is located near Salt Lake City. An additional medium-size

underground mine, Copper Range’s White Pine facility, is near Lake Superior on the Upper Peninsula of

Michigan. The copper mines in other states identified in Table 3 either are small operations or represent

limited byproduct production at gold, molybdenum, and other mines (Bureau of Mines, 1992a, 1992b, and

1995; EPA, 1994a).

Gold. With the widespread application of heap leaching technology, most of the U.S. gold production

now occurs in Nevada. Nevada mines account for more than 60 percent of the total production, with most

mines located along the Carlin Trend in northwestern Nevada. Most other gold mining operations are

located throughout the western United States, including Alaska, although four gold mines are located in

South Carolina (Bureau of Mines, 1992a; 1992b; EPA, 1994c).

Iron. Nearly all of the iron mined in the United States is produced from taconite ore found in

Northern Minnesota and Michigan. The largest mining operations (all open pits) are found along the

Mesabi Range in Minnesota, which extends from Hibbing to north of Duluth (Bureau of Mines, 1992a;

1992b; EPA, 1994f).

Lead/Zinc. The Viburnum area of southeastern Missouri is the center of U.S. lead production. The

lead mines in this area also produce significant quantities of zinc (as a byproduct from smelter operations).

Alaska is the largest zinc producer in the United States (with associated lead byproducts) at the Red Dog

and Greens Creek Mines (the Red Dog Mine is the primary producer). Central Tennessee and northern

New York State are also major sources of zinc ore (Bureau of Mines, 1992a; 1992b; EPA, 1994g).

MINING INDUSTRY PROFILE

September1997 A - 5

TA

BL

E 3

. L

ocat

ion

of M

inin

g A

ctiv

itie

s, 1

992

Stat

e

Cop

per

Gol

dIr

on O

reL

ead

Pho

spha

te R

ock

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

#m

ines

1%

U.S

.P

rodu

ctio

n

Uni

ted

Stat

es50

1,76

5,00

0m

etri

c to

ns21

2+3

329

met

ric

tons

2255

,593

,000

met

ric

tons

2330

8,00

0m

etri

c to

ns16

46,9

65,0

00m

etri

c to

ns

Ala

ska

131.

5%2

15.6

%

Ari

zona

1665

.3%

142.

1%1

W

Cal

ifor

nia

1910

%N

AW

Col

orad

o22

W7

1.2%

2W

Flor

ida

968

.6%

Idah

o32

W11

1%1

W7

11.1

%

Illin

ois

1W

Mic

higa

n3

W2

23.2

%

Min

neso

ta7

76.2

%

Mis

sour

i2

0.6%

NA

0.03

%7

75.6

%

Mon

tana

3W

94.

3%1

W2

W1

NA

Nev

ada

1W

6161

.7%

New

Mex

ico

712

%5

W2

W

New

Yor

k2

Nor

th C

arol

ina

1W

Ore

gon

10.

01%

2W

Sout

h C

arol

ina

42.

1%

Sout

h D

akot

a5

5.8%

1W

Ten

ness

ee2

W

Tex

as2

W

(con

tinue

d)

MINING INDUSTRY PROFILE

September1997 A - 6

TA

BL

E 3

. L

ocat

ion

of M

inin

g A

ctiv

itie

s, 1

992

(con

tinu

ed)

Stat

e

Cop

per

Gol

dIr

on O

reL

ead

Pho

spha

te R

ock

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

min

es1

% U

.S.

Pro

duct

ion

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

Uni

ted

Stat

es50

1,76

5,00

0m

etri

c to

ns21

2+3

329

met

ric

tons

2255

,593

,000

met

ric

tons

2330

8,00

0m

etri

c to

ns16

46,9

65,0

00m

etri

c to

ns

Uta

h1

W2

W1

NA

Ver

mon

tN

AW

Was

hing

ton

42.

7%1

W

NO

TE

S: NA

= I

nfor

mat

ion

not a

vaila

ble.

W =

Inf

orm

atio

n w

ithhe

ld b

y th

e B

urea

u of

Min

es f

or p

ropr

ieta

ry r

easo

ns.

1D

ue to

the

natu

re o

f th

e m

inin

g in

dust

ry, t

he e

xact

num

ber

of m

ines

is d

iffi

cult

to d

isce

rn.

For

inst

ance

, sev

eral

of

the

com

mod

ities

are

pro

duce

d as

co-

prod

ucts

or

by-

prod

ucts

fro

m o

ther

com

mod

ity m

inin

g op

erat

ions

(e.

g., g

old

as a

res

ult o

f co

pper

pro

duct

ion)

. T

here

fore

, the

num

ber

of m

ines

for

indi

vidu

al c

omm

oditi

es in

clud

es b

oth

actu

al c

omm

odity

min

es a

nd th

ose

min

es f

rom

whi

ch th

e co

mm

odity

is a

co-

prod

uct o

r by

-pro

duct

. T

hese

unc

erta

intie

s re

sult

in in

cons

iste

nt n

umbe

rs th

roug

hout

the

BO

M s

ourc

es.

2A

t all

of th

ese

min

es, c

oppe

r is

pro

duce

d as

a b

ypro

duct

of

othe

r co

mm

odity

ope

ratio

ns.

3T

his

incl

udes

abo

ut 2

00 lo

de m

ines

and

abo

ut 1

2 la

rge

plac

er m

ines

. It

doe

s no

t inc

lude

the

hund

reds

of

smal

l pla

cer

min

es th

roug

hout

the

wes

t.

SOU

RC

ES:

U.S

. Bur

eau

of M

ines

. Min

eral

Com

mod

ity S

umm

arie

s 19

94.

U.S

. Bur

eau

of M

ines

. Min

eral

s Ye

arbo

ok, V

olum

e I:

Met

als

and

Min

eral

s. 1

992.

U.S

. Bur

eau

of M

ines

. Min

eral

s Ye

arbo

ok, V

olum

e II

: A

rea

Rep

orts

: D

omes

tic.

1992

.

MINING INDUSTRY PROFILE

September1997 A - 7

TA

BL

E 3

a. L

ocat

ion

of M

inin

g A

ctiv

itie

s, 1

992

Stat

e

Mol

ybde

num

Pla

tinu

m2

Pot

ash

Silv

erU

rani

umZ

inc

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

Uni

ted

Stat

es10

349

,000

met

ric

tons

18,

300

met

ric

tons

121,

705,

000

met

ric

tons

150

1,80

0 m

etri

cto

ns17

522

met

ric

tons

2552

4,00

0m

etri

c to

ns

Ala

ska

1515

.8%

347

.5%

Ari

zona

5W

159.

2%

Cal

ifor

nia

NA

W2

W14

1%

Col

orad

o2

W4

W1

NA

Flor

ida

24N

A

Idah

o1

W12

14.1

%2

NA

Illin

ois

NA

NA

NA

NA

Mic

higa

n1

W1

NA

Min

neso

taN

A1.

8%

Mis

sour

iN

AN

A4

8.4%

Mon

tana

1W

110

0%9

10.9

%1

3.9%

Neb

rask

a2

35%

Nev

ada

134

.1%

New

Mex

ico

1W

684

%1

10%

New

Yor

k1

NA

2W

Nor

th C

arol

ina

Ore

gon

1.0

6%

(con

tinue

d)

MINING INDUSTRY PROFILE

September1997 A - 8

TA

BL

E 3

a. L

ocat

ion

of M

inin

g A

ctiv

itie

s, 1

992 (

cont

inue

d)

Stat

e

Mol

ybde

num

Pla

tinu

m2

Pot

ash

Silv

erU

rani

umZ

inc

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

#m

ines

1%

U.S

.P

rodu

ctio

n#

min

es1

% U

.S.

Pro

duct

ion

Uni

ted

Stat

es10

349

,000

met

ric

tons

18,

300

met

ric

tons

121,

705,

000

met

ric

tons

150

1,80

0 m

etri

cto

ns17

522

met

ric

tons

2552

4,00

0m

etri

c to

ns

Sout

h C

arol

ina

3N

A

Sout

h D

akot

a4

0.3%

Ten

ness

eeN

AN

A10

W

Tex

as2

NA

Uta

h1

W3

W4

W1

NA

Ver

mon

t

Was

hing

ton

4W

1N

A

Wyo

min

g2

>12

%5

NO

TE

S: NA

= I

nfor

mat

ion

not a

vaila

ble.

W =

Inf

orm

atio

n w

ithhe

ld b

y th

e B

urea

u of

Min

es f

or p

ropr

ieta

ry r

easo

ns.

1D

ue to

the

natu

re o

f th

e m

inin

g in

dust

ry, t

he e

xact

num

ber

of m

ines

is d

iffi

cult

to d

isce

rn.

For

inst

ance

, sev

eral

of

the

com

mod

ities

are

pro

duce

d as

co-

prod

ucts

or

by-p

rodu

cts

from

othe

r co

mm

odity

min

ing

oper

atio

ns (

e.g.

, gol

d as

a r

esul

t of

copp

er p

rodu

ctio

n).

The

refo

re, t

he n

umbe

r of

min

es f

or in

divi

dual

com

mod

ities

incl

udes

bot

h ac

tual

com

mod

ity m

ines

and

thos

e m

ines

fro

m w

hich

the

com

mod

ity is

a c

o-pr

oduc

t or

by-p

rodu

ct.

The

se u

ncer

tain

ties

resu

lt in

inco

nsis

tent

num

bers

thro

ugho

ut th

e B

OM

sou

rces

. 2

The

num

bers

for

pla

tinum

incl

ude

all t

he p

latin

um-g

roup

met

als.

Tho

se m

etal

s in

clud

e pl

atin

um, p

alla

dium

, rho

dium

, rut

heni

um, i

ridi

um, a

nd o

smiu

m.

3O

f th

e 10

mol

ybde

num

min

es, o

nly

thre

e ar

e in

bus

ines

s to

min

e m

olyb

denu

m.

The

oth

er s

even

pro

duce

mol

ybde

num

as

a re

sult

of o

ther

com

mod

ity o

pera

tions

. O

f th

e th

ree

true

mol

ybde

num

min

es, t

wo

are

loca

ted

in C

olor

ado

and

one

in I

daho

.4

Ura

nium

was

pro

duce

d at

thes

e tw

o si

tes

as a

byp

rodu

ct o

f ph

osph

ate

proc

essi

ng.

5O

ne o

f th

e tw

o m

ines

in th

e st

ate

repo

rted

pro

duct

ion

of 6

1 m

etri

c to

ns o

f ur

aniu

m.

Prod

uctio

n da

ta f

or th

e ot

her

min

e w

as n

ot a

vaila

ble.

SOU

RC

ES:

U.S

. Bur

eau

of M

ines

. Min

eral

Com

mod

ity S

umm

arie

s 19

94.

U.S

. Bur

eau

of M

ines

. Min

eral

s Ye

arbo

ok, V

olum

e I:

Met

als

and

Min

eral

s. 1

992.

U.S

. Bur

eau

of M

ines

. Min

eral

s Ye

arbo

ok, V

olum

e II

: A

rea

Rep

orts

: D

omes

tic.

1992

.

MINING INDUSTRY PROFILE

September1997 A - 9

Phosphate Rock. The Tampa/Bartow area of central Florida is the major phosphate rock producing

area of the United States. The recent introduction of a heavy media separation process at IMC’s Four

Corners mine has led to possibly increased phosphate recovery from types of ore that previously could not

be beneficiated (i.e., the potential for additional production in the area). Beyond the Florida operations,

TexasGulf operates a large phosphate facility along the North Carolina coast near New Bern, and smaller

phosphate mines are located in Idaho, Montana, and Utah (Bureau of Mines, 1992a; 1992b; EPA, 1994h).

Molybdenum. Recent market conditions have limited molybdenum production in the United States,

especially primary production. In 1994, Cyprus’ Henderson Mine in central Colorado was the only active

primary molybdenum operation in the country (compared with three in 1992). Byproducts represent the

remainder of U.S. production, mostly as a byproduct of copper ore flotation at mines and mills in Arizona

and Utah (Kennecott) (Bureau of Mines, 1992a and 1992b).

Platinum. Only one platinum mine is active in the United States, the Stillwater Mine operated by the

Stillwater Mining Company near Nye, Montana (Bureau of Mines, 1992a and 1992b).

Potash. New Mexico produced almost all potash produced in the United States in 1992. In the state,

five producers operated six mines, all of which mined potash in underground bedded ore zones. The other

potash-producing states (California, Michigan, and Utah) produced potash by two-well solution mining,

solar evaporation, and selective crystallization (Bureau of Mines, 1992a and 1992b).

Silver. Silver is mined primarily in the Western United States both through primary and byproduct

production. Primary silver production generally occurs in Montana, Idaho, and Nevada. Silver is also

recovered as a byproduct from copper, lead/zinc, and gold production. In Alaska, silver is a significant

byproduct at the Green Creek and Red Dog Mines. In Nevada, much of the total silver production is

derived as a byproduct of the state’s extensive gold mining industry (Bureau of Mines, 1992a and 1992b;

EPA, 1994 and 1994c).

Uranium. The total amount of uranium produced in 1992 (522 metric tons) was more than 70

percent less than the quantity produced in 1991 and the lowest amount produced since 1951. The

decreased demand for uranium (and the resulting decrease in price) shut down several mines and put others

on standby. According to the Bureau of Mines, Nebraska produced nearly 35 percent of the uranium

produced in the United States. Texas was second producing more than 12 percent. Of the 17 mines in

operation in 1992, five were conventional mines (both underground and open pits), four were in situ, and

eight were reported as “other” (heap leach, mine water, mill tailings, or low-grade stockpiles). In Florida,

uranium has also been produced as a byproduct of phosphoric acid production (Bureau of Mines, 1992a

and 1992b; EPA, 1994 and 1994j; U.S. Department of Energy, 1993).

MINING INDUSTRY PROFILE

September1997 A - 10

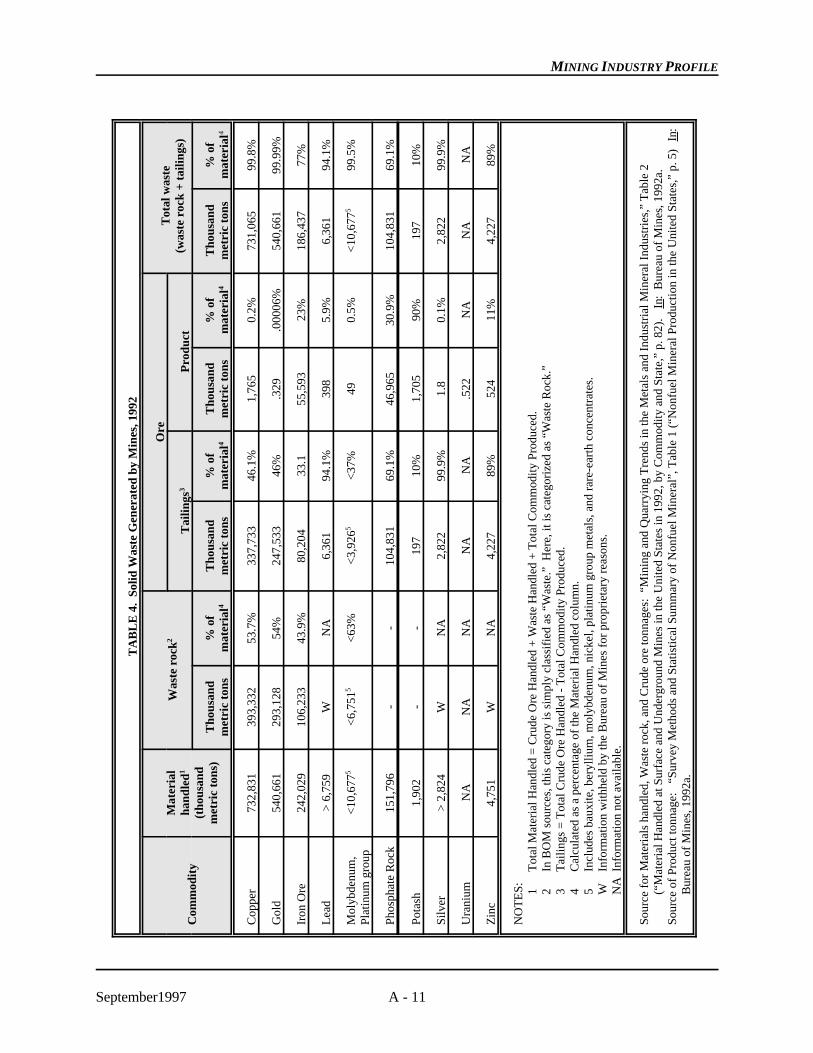

3. MINING PRACTICES AND PRODUCTS

Overall, as shown in Table 4, hardrock mining operations handle large quantities of material, the vast

majority of which becomes waste in most industry sectors. Although it varies by commodity, the amount

of product per ton of ore is generally very small for most of these commodities. Overall, the quantities and

characteristics of the wastes are largely beyond the control of the industry, since they are the direct product

of the material being mined.

Conventional underground and surface mining techniques account for most of the hardrock mining in

the United States. Until recent decades, nearly all mining occurred underground, but with the advent of

large earthmoving equipment and cheaper energy sources, surface mining has become prevalent in most

industry sectors. The relatively lower cost of surface mining has allowed much lower-grade ores to be

exploited economically in some industry sectors (EPA, 1994). In addition, in situ leaching has been used

for about two decades in uranium and copper mining.

Primary iron and phosphate ores are mined almost exclusively by surface mining methods. Open pit

mining is also the predominant extraction method used in primary gold and copper production, although

there are several significant exceptions. For example, Homestake’s facility in Lead, South Dakota, and

Copper Range’s White Pine mine in Michigan are large underground gold and copper mines, respectively.

An additional mining practice used during the past 20 years in the copper and uranium sectors is in situleaching. Lead/zinc and the only platinum mine in the United States, on the other hand, are industry sectors

where nearly all primary production occurs at underground mines (Bureau of Mines, 1993; 1992a; 1992b).

The major wastes generated by mines include mine water, waste rock, tailings, and overburden. Mine

water is produced when the water table is higher than the underground mine workings or the depth of an

open pit surface mine. When this occurs, the water must be pumped or drained out of the mine.

Alternatively, water may be pumped from wells surrounding the mine to create a cone of depression in the

ground water table, thereby reducing infiltration. Mine water may be used in milling operations as makeup

water, used for dust suppression, or discharged. When mining ends and pumping stops, groundwater will

usually recover to its pre-mining level, although this can take decades or centuries.

Surface mines generate greater volumes of waste rock than underground operations. Waste rock is

typically managed in angle-of-repose piles, either within or near the pit/mine. Waste rock also can be used

on-site for road construction, in tailings dams, and to backfill mined-out areas. The differentiation between

waste rock and ore (i.e., the cutoff grade) is generally an economic distinction, and can vary significantly

over time depending on economic conditions; thus, what is disposed as waste rock (or sub-ore) at one time

during a mine’s life may be ore at another time. In addition, the development of new technologies can lead

to economically viable mineral recovery from historic waste rock piles. Sub-ore is often stored in

freestanding piles until economic conditions favor its beneficiation or until the mine reaches the end of its

active life (EPA, 1994).

MINING INDUSTRY PROFILE

September1997 A - 11

TA

BL

E 4

. So

lid W

aste

Gen

erat

ed b

y M

ines

, 199

2

Com

mod

ity

Mat

eria

lha

ndle

d1

(tho

usan

dm

etri

c to

ns)

Was

te r

ock2

Ore

Tot

al w

aste

(was

te r

ock

+ t

ailin

gs)

Tai

lings

3P

rodu

ct

Tho

usan

dm

etri

c to

ns%

of

mat

eria

l4T

hous

and

met

ric

tons

% o

fm

ater

ial4

Tho

usan

dm

etri

c to

ns%

of

mat

eria

l4T

hous

and

met

ric

tons

% o

fm

ater

ial4

Cop

per

732,

831

393,

332

53.7

%33

7,73

346

.1%

1,76

50.

2%73

1,06

599

.8%

Gol

d54

0,66

129

3,12

854

%24

7,53

346

%.3

29.0

0006

%54

0,66

199

.99%

Iron

Ore

242,

029

106,

233

43.9

%80

,204

33.1

55,5

9323

%18

6,43

777

%

Lea

d>

6,7

59W

NA

6,36

194

.1%

398

5.9%

6,36

194

.1%

Mol

ybde

num

,Pl

atin

um g

roup

<10

,677

5<

6,75

15<

63%

<3,

9265

<37

%49

0.5%

<10

,677

599

.5%

Phos

phat

e R

ock

151,

796

--

104,

831

69.1

%46

,965

30.9

%10

4,83

169

.1%

Pota

sh1,

902

--

197

10%

1,70

590

%19

710

%

Silv

er>

2,8

24W

NA

2,82

299

.9%

1.8

0.1%

2,82

299

.9%

Ura

nium

NA

NA

NA

NA

NA

.522

NA

NA

NA

Zin

c4,

751

WN

A4,

227

89%

524

11%

4,22

789

%

NO

TE

S: 1T

otal

Mat

eria

l Han

dled

= C

rude

Ore

Han

dled

+ W

aste

Han

dled

+ T

otal

Com

mod

ity P

rodu

ced.

2In

BO

M s

ourc

es, t

his

cate

gory

is s

impl

y cl

assi

fied

as

“Was

te.”

Her

e, it

is c

ateg

oriz

ed a

s “W

aste

Roc

k.”

3T

ailin

gs =

Tot

al C

rude

Ore

Han

dled

- T

otal

Com

mod

ity P

rodu

ced.

4C

alcu

late

d as

a p

erce

ntag

e of

the

Mat

eria

l Han

dled

col

umn.

5In

clud

es b

auxi

te, b

eryl

lium

, mol

ybde

num

, nic

kel,

plat

inum

gro

up m

etal

s, a

nd r

are-

eart

h co

ncen

trat

es.

WIn

form

atio

n w

ithhe

ld b

y th

e B

urea

u of

Min

es f

or p

ropr

ieta

ry r

easo

ns.

NA

Info

rmat

ion

not a

vaila

ble.

Sour

ce f

or M

ater

ials

han

dled

, Was

te r

ock,

and

Cru

de o

re to

nnag

es:

“Min

ing

and

Qua

rryi

ng T

rend

s in

the

Met

als

and

Indu

stri

al M

iner

al I

ndus

trie

s,”

Tab

le 2

(“M

ater

ial H

andl

ed a

t Sur

face

and

Und

ergr

ound

Min

es in

the

Uni

ted

Stat

es in

199

2, b

y C

omm

odity

and

Sta

te,”

p. 8

2).

In:

Bur

eau

of M

ines

, 199

2a.

Sour

ce o

f Pr

oduc

t ton

nage

: “

Surv

ey M

etho

ds a

nd S

tatis

tical

Sum

mar

y of

Non

fuel

Min

eral

”, T

able

1 (

“Non

fuel

Min

eral

Pro

duct

ion

in th

e U

nite

d St

ates

,” p

. 5)

In:

B

urea

u of

Min

es, 1

992a

.

MINING INDUSTRY PROFILE

September1997 A - 12

Waste rock piles are generally designed to drain freely to minimize the potential for unstable

conditions. Therefore, these piles are often located in natural drainages and now frequently have drainage

systems installed during construction (e.g., French drains). Due to the potential for contamination of water

flowing over or through waste rock piles, many mining facilities are now installing systems or taking steps

to prevent or reduce the infiltration of precipitation. Contamination from piles may include sediments and

solids, and also acid mine drainage or toxic pollutant loadings, depending upon the mineralogy of the waste

rock. Systems used to reduce or prevent drainage into, or over, waste rock piles include uphill diversions,

sloped and compacted surfaces, drains, and covers (EPA, 1994).

Except for the gold and copper sectors, in which leaching is increasingly prevalent, beneficiation of

most other metal and phosphate ores occurs by conventional milling technologies. These include crushing,

grinding, autoclaving, roasting, chlorination, calcining, and reagent flotation, by which a chemical reagent

causes the target mineral to stick to air bubbles. In these cases, the ore is crushed and ground and the

target mineral(s) are recovered, leaving very fine “tailings” as a waste to be disposed of. Tailings can be

dewatered and disposed of in piles or used as backfill in the mine; more commonly, they are pumped as a

slurry (typically 30 to 65 percent solids) to impoundments. In tailings impoundments, the solid component

of the tailings settles out behind embankments and the ponded water is either reused in the process or

discharged to surface water. The volumes of water discharged and reused are dependent on site-specific

conditions, including water availability and evaporation rates. Tailings embankments/dams can be

constructed of concrete, earthen materials, and/or waste rock or tailings (EPA, 1994 and 1994e; Bureau of

Mines, 1995).

Table 5 is a summary of mining methods and beneficiation waste management practices for the

various industry sectors.

While conventional flotation involves a wide range of flotation reagents (oils, xanthates, lime, etc.),

depending on the industry sector and site-specific geology residual reagents comprise a diminishing fraction

of the total amount of waste. One exception is in the phosphate industry where flotation occurs in

conjunction with “washing” stages that use both ammonia and sulfuric acid; even there, at least one

company now uses a substitute reagent that both increases recovery efficiency and reduces the toxicity of

discharges (EPA, 1994 and 1994h).

Cyanidation technologies, some of which have been available for more than 100 years, are widely

used for gold beneficiation. Higher-grade ores (“higher-grade” is relative; the highest grades are generally

in the tenths of an ounce of gold per ton of ore) are crushed and ground, then the ore slurry passes through

a series of tanks or vats that contain a sodium cyanide solution that dissolves the gold values; then the gold

is recovered from the solution via Merrill-Crowe zinc precipitation or carbon adsorption, electrowinning,

melting, and refining. The slurry of fine tailings is then disposed of, typically in impoundments (EPA,

1994, 1994c, and 1994i).

MINING INDUSTRY PROFILE

September1997 A - 13

TA

BL

E 5

. P

redo

min

ant

Min

ing

Met

hods

and

Was

te M

anag

emen

t P

ract

ices

Com

mod

ity

Num

ber

ofm

ines

1P

redo

min

ant

min

ing

met

hods

Pre

dom

inan

t B

enef

icia

tion

Met

hods

Maj

or b

enef

icia

tion

was

tem

anag

emen

t pr

acti

ces

Zin

c25

Und

ergr

ound

Flot

atio

nT

ailin

gs im

poun

dmen

ts

Cop

per

50U

nder

grou

nd, o

pen

pit,

in s

ituFl

otat

ion,

Lea

chin

g, S

X/E

WT

ailin

gs im

poun

dmen

ts, s

pent

ore

dum

ps

Iron

22U

nder

grou

ndG

ravi

ty, m

agne

tic s

epar

atio

n, f

lota

tion

Tai

lings

impo

undm

ents

Gol

d20

0 lo

deM

ost o

pen

pit

Seve

ral u

nder

grou

ndC

yani

datio

n: h

eap,

tank

, vat

leac

hing

Tai

lings

impo

undm

ents

(ta

nk, v

at),

dum

ps a

nd h

eaps

(he

aps)

, spe

nt o

redu

mps

100s

pla

cer

Ope

n pi

t, dr

edge

, etc

.G

ravi

ty, s

ome

cyan

idat

ion

Tai

lings

bac

k in

to m

ine

cut

Mol

ybde

num

10U

nder

grou

ndO

pen

pit

Flot

atio

nT

ailin

gs im

poun

dmen

ts

Lea

d23

Und

ergr

ound

Flot

atio

nT

ailin

gs im

poun

dmen

ts

Phos

phat

e16

Mos

t by

surf

ace

min

ing

Flot

atio

n, h

eavy

med

ia s

epar

atio

nB

ackf

illin

g an

d cl

ay p

onds

Plat

inum

1U

nder

grou

ndFl

otat

ion

Tai

lings

impo

undm

ent

Pota

sh6

Und

ergr

ound

, sol

utio

n m

inin

g,la

ke b

rine

Flot

atio

n, h

eavy

med

ia s

epar

atio

n,di

ssol

utio

n -

recr

ysta

lizat

ion

Silv

er15

0O

pen

pit,

unde

rgro

und,

pla

cer,

by-

prod

uct

Flot

atio

n (b

ase

met

al o

res)

, Sm

eltin

g(c

oppe

r or

es),

Cya

nida

tion

(gol

d/ s

ilver

ores

), p

reci

pita

tion

(silv

er o

res)

Tai

lings

impo

undm

ents

Tai

lings

use

d as

bac

kfill

Not

e: 1

Due

to th

e na

ture

of

the

min

ing

indu

stry

, the

exa

ct n

umbe

r of

min

es is

dif

ficu

lt to

dis

cern

. Fo

r in

stan

ce, s

ever

al o

f th

e co

mm

oditi

es a

re p

rodu

ced

asco

-pro

duct

s or

by-

prod

ucts

fro

m o

ther

com

mod

ity m

inin

g op

erat

ions

(e.

g., c

oppe

r as

a r

esul

t of

gold

pro

duct

ion)

. T

here

fore

, the

num

ber

of m

ines

for

indi

vidu

al c

omm

oditi

es in

clud

es b

oth

actu

al c

omm

odity

min

es a

nd th

ose

min

es f

rom

whi

ch th

e co

mm

odity

is a

co-

prod

uct o

r by

-pro

duct

. T

hese

unce

rtai

ntie

s re

sult

in in

cons

iste

nt n

umbe

rs th

roug

hout

the

BO

M s

ourc

es.

Sour

ce:

Var

ious

MINING INDUSTRY PROFILE

September1997 A - 14

Lower grade gold ore (down to two hundredths of an ounce of gold or less per ton of ore), which may

be crushed, is piled onto lined “pads,” and a “barren” cyanide solution is applied to the surface. The

cyanide solution percolates through the heap, dissolving gold values. This “pregnant” solution is recovered

from the base of the heap, gold is recovered from the solution, and the “barren” solution is refortified with

cyanide and reapplied. The pregnant and barren solutions are generally stored in lined ponds. Following

leaching, spent ore may either be left in place (with new ore added over it) or removed for disposal (after

detoxification/neutralization) in a spent ore pile/dump. Where spent ore is managed in place, neutralization

of the residual cyanide occurs after the heap has reached the maximum height (EPA, 1994, 1994c, and

1994i).

The process of using cyanide to extract gold works most effectively on oxide ores. (Oxide ores are

those exposed to weathering and the action of water, and that have little or no sulfur content.) As the sulfur

content of the ore increases, the efficiency of gold recovery decreases. As shallow oxide deposits are mined

out, gold mines are beginning to extract ores with ever higher concentrations of sulfur bearing minerals. In

response, operators are treating these sulfide ores with a variety of techniques to reduce their sulfur content.

Such techniques include roasting and biological treatment. The trend towards greater exploitation of

sulfide ores is of concern in that these ores contain potentially acid generating sulfide minerals, as does the

waste rock (EPA, 1994c and 1994i).

In addition, copper ores are increasingly being leached, primarily in very large dumps (e.g., Cyprus

Minerals Col, ASARCO, Inc., and Magma Copper Co.) but also in situ. Leaching of copper ores has

occurred since the 1950s and 1960s, but the use of dump leaching for copper recovery has only become

viable during the past decade, with the acceptance of solvent extraction/electrowinning (SX/EW)

technology. In this process, oxide ores and low grade sulfide ore (those that cannot be economically milled

and recovered by flotation) are placed in lined heaps or unlined dumps, typically with no crushing or

grinding. Leaching solution is applied to the surface and collected at the base. Ore can also be leached insitu, with leach solution injected into the ore body through wells and recovered in underground workings or

through recovery wells. The pregnant solution from these leach operations is collected and conveyed to the

SX plant, where the copper is extracted by a proprietary organic chemical dispersed in a kerosene diluent.

The copper is then extracted from the organic base with a strong sulfuric acid solution that then becomes

the electrolyte for electrowinning. In the electrowinning tankhouse, the copper is plated out of solution onto

a cathode suitable for sale. The entire SX/EW process is almost exclusively closed-looped. For low-grade

sulfide ores, water is the lixiviant; for oxide ores, sulfuric acid is used to make up leaching solution. To

facilitate collection of pregnant solution, dump leach units are typically located within a pit or a natural

drainage. Dump leach units (and in situ operations) are not always designed to ensure maximum collection

of pregnant solution; there are technological limits to containment, but the more important factor is the

balance struck between the economics of facility design/construction and the anticipated efficiency of

solution recovery. (Another factor, state regulation, is increasingly important: Arizona’s new regulations,

for example, have led to increased attention on improving solution containment there (EPA, 1994 and

1994a).)

MINING INDUSTRY PROFILE

September1997 A - 15

Mineral processing operations generally follow beneficiation and include techniques that often change

the chemical make-up of the ore or mineral by chemical attack or digestion, electrolytic refining, and

pyrometallurgical/thermal processes. In contrast to extraction and beneficiation wastes, processing

operations generate waste streams that generally bear little or no resemblance to the materials that entered

the operation.

When mineral processing operations are co-located with extraction and beneficiation operations,

commingling of extraction and/or beneficiation and mineral processing wastes (both Bevill and non-Bevill)

may occur. Most often, the volume of processing waste is very small compared with the total waste

quantity managed on-site (e.g., co-disposing a few thousand tons per year of wastewater treatment sludge

with millions of tons of mill tailings). In these cases, management of the mixed waste streams usually

occurs in a land disposal unit, such as a tailings pond or other surface impoundment, or, in some industry

sectors, a gypsum stack.

Environmental Performance

Mining operations can be and have been sources of widespread environmental impacts, with more

than 60 sites on the National Priorities List. During the past 20 years, however, there has been significant

improvement in environmental performance at many hardrock mining operations. This is due to many

factors:

! Increasing environmental awareness and commitment to environmental protection by many miningcompanies.

! Better techniques to predict and detect potential environmental effects before damage occurs.

! Continually developing technologies to prevent, mitigate, or remediate environmental impacts.

! Broader state and federal regulatory requirements, including post-mining liability.

Many of the largest mining companies have set up extensive environmental programs. They have

begun to incorporate environmental concerns into all phases of mining operations, from exploration to

mining planning, through development, operations, closure and reclamation. At some mines, management

performance standards now include environmental accomplishments. Other mining companies have set up

comprehensive environmental auditing programs. Therefore, environmental costs are now being

characterized during the earliest stages of mine planning as part of the economic evaluation of recovering

target minerals (EPA, 1994).

The most significant environmental threats posed by mine sites are often complex and highly

dependent on site-specific factors. Acid generation potential and water balances, for example, can be very

MINING INDUSTRY PROFILE

September1997 A - 16

difficult to predict, but also can be very difficult, and expensive, to deal with once problems occur. Poor

understanding of water balances, or site hydrology, can contribute to making uninformed decisions about

control technologies, and that in turn can result in environmental problems. During the past decade,

predictive tools have been greatly improved; this reduces uncertainty and provides more reliable

information to develop and carry out mitigation measures. Uncertainty does remain, though, and

unanticipated environmental impacts continue to occur at some sites, which emphasizes the need for

continued development and refinement of site characterization and mine planning tools (EPA, 1994 and

1994k).

Along with better predictive tools, technologies also continue to be developed to reduce potential

environmental threats and address impacts where they do occur. Mining companies have learned to build

better, more efficient, and more environmentally safe operations. Advances in liner and other containment

systems, piping and spill control, and reclamation techniques are all examples of such improvements. It is

important to recognize that the economic costs of environmental controls are a significant element, as is the

concentration of the target mineral in the ore body, in the planning and economic evaluation of a site for

mine development and operation. Environmental controls must be affordable, cost-effective, and meet

certain standards. Where there are potential or actual releases to the environment, treatment and remedial

technologies also continue to evolve. For example, nearly 20 years ago, the Homestake Mining Company

developed an innovative biotreatment technology for cyanide destruction at the company’s gold mine in

Lead, South Dakota. Other biotechnologies are being started and improved for cyanide heap leach

detoxification and acid drainage control, among other environmental applications. Information

management and process controls are also improving environmental performance at many mine and mill

sites. By better classifying ore grades and by improving mineral recovery from ore, mines and mills can

improve productivity and thus generate somewhat less waste rock or tailings for every pound of metal

recovered. (Better classification and recovery, however, have finite limits imposed by the absolute amount

of the valuable mineral in the ore and the technologies that are available for recovery.) Because of the high

waste-to-product ratios and the volume of wastes generated, however, any improvement in recovery can

reduce wastes by substantial amounts (but generally only by small proportions) (EPA, 1994 through

1994k).

Historic mining operations were often unregulated, resulting in extensive uncontrolled environmental

releases. In recent decades, particularly since the early 1970s, state and federal agencies have established

broad regulatory requirements that generally address all phases of mine operations. During mine planning,

operators may be required to complete baseline studies and assess the potential effects of and risks

associated with proposed operations. Mine units frequently have to meet specific design standards (liner

requirements, stability standards, overflow protection, etc.). Environmental statutes and regulations, such

as the Clean Water Act, Clean Air Act and corresponding state requirements, are intended to address

environmental releases. Bonding requirements are imposed to ensure that reclamation will be successfully

completed. In some states, bonding also serves to protect against environmental problems.

MINING INDUSTRY PROFILE

September1997 A - 17

4. MINING AND THE ECONOMY

All non-fuel mineral beneficiation and extraction activities accounted for approximately 0.23% of

GNP (Commerce, 1995a) and 0.85% of total employment (Commerce, 1995c) at the national level in 1993.

In contrast, the manufacturing industries accounted for 17.63% of GNP (Commerce, 1995a) and 19.2% of

total employment (Commerce, 1995c) during the same year. The apparently small portion of the national

economy attributed to mining can be traced to several factors: 1) the national economy of the United States

is the largest, and most diverse, in the world; 2) improvements in productivity, technology, and

mechanization have reduced the need for a large workforce; and 3) the mining sector of the economy has

not grown at the same rate as other major sectors of the economy (U.S. Department of Commerce, 1995a).

Although basic non-fuel metal mining occupies a statistically small position in the overall national

economy, the mining sector provides basic raw materials for major sectors of the U.S. economy, and thus is

more important then the mere numbers suggest. Copper is essential to the electronics and construction

industries. Iron ore provides the base material for the steel, automotive, and transportation industries.

Molybdenum is used in steel production, machinery, electrical and chemical manufacturing. Potash and

phosphate rock are used in fertilizers and chemical manufacturing. Gold, while primarily used in jewelry

and the decorative arts, is also used in the electronics industry and dentistry. These minerals are essential

to the operation of a modern, industrialized economy. Without a domestic iron ore industry for example,

the unit cost to produce automobiles in the United States would be significantly different. Copper,

molybdenum, phosphate rock, gold, silver, lead, and zinc play similar roles. The amount of raw materials

produced by the U.S. mining industry has provided and will continue to provide raw materials necessary to

drive the diverse U.S. economy.

Other important contributions of the minerals industry to the national economy are its value as a

producer of exports, and in reducing industrial dependence on certain minerals that would otherwise be

imported. For example, in 1994 the United States exported 8% of the lead and 75% of the molybdenum it

produced. Conversely, the United States imported 22% of the iron ore it consumed in 1994.

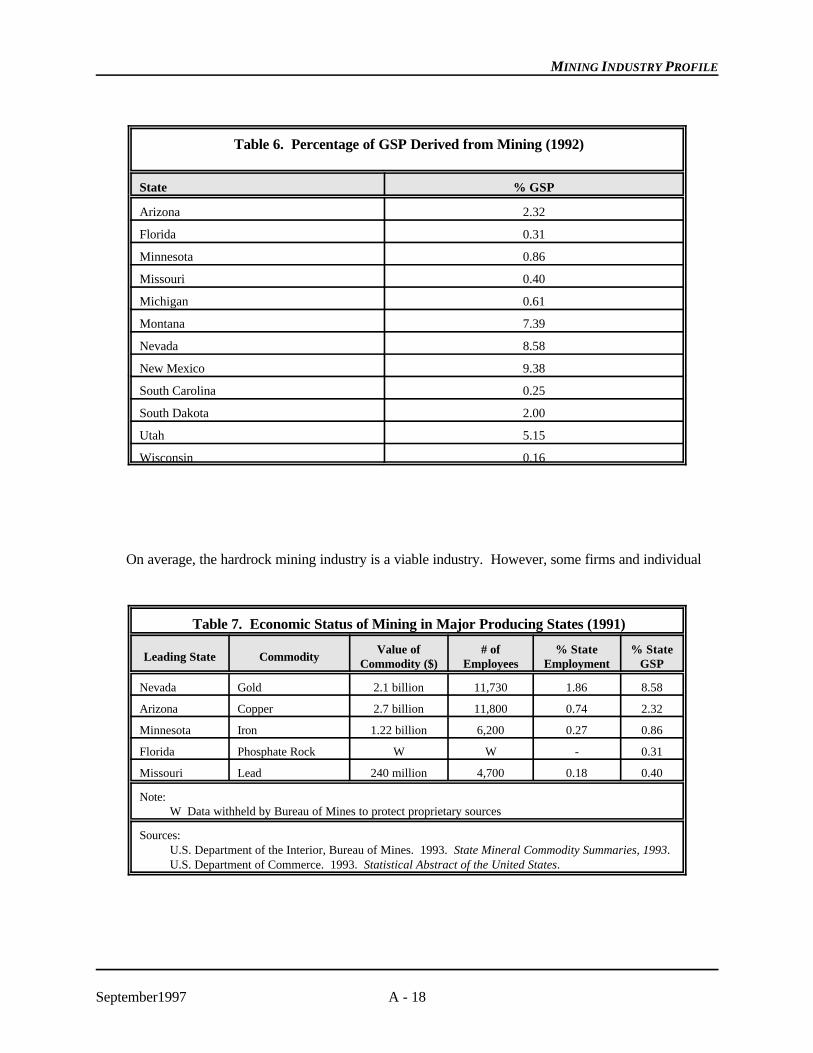

While mining is a small part of the national economy, the importance of mining to state economies

varies widely (See Table 6). Of the twelve states producing significant amounts of minerals, there exists a

large difference in the percentage of GSP (gross state product) contributed by mining. Generally, states

with large, diverse economies (Florida, Missouri) reflect the same trend as is evidenced at the national

level: mining is responsible for a very small percentage of GSP. This is even true in Arizona, which is

ranked first in terms of dollar value of copper produced, yet whose mining sector accounts for “only”

2.32% of GSP. However, in states with smaller, less diverse economies, mining has a much greater role in

the state economy. This is notable in Montana and New Mexico, where mining accounts for 7.39% and

9.38% of GSP, respectively (U.S. Department of Commerce, 1995b). Mining at the state level is similarly

important to overall employment. As shown in Table 7, the percentage of state employment in the mining

sector is small in the five states that are the major producers of their respective commodities.

MINING INDUSTRY PROFILE

September1997 A - 18

Table 6. Percentage of GSP Derived from Mining (1992)

State % GSP

Arizona 2.32

Florida 0.31

Minnesota 0.86

Missouri 0.40

Michigan 0.61

Montana 7.39

Nevada 8.58

New Mexico 9.38

South Carolina 0.25

South Dakota 2.00

Utah 5.15

Wisconsin 0.16

Table 7. Economic Status of Mining in Major Producing States (1991)

Leading State CommodityValue of

Commodity ($)# of

Employees% State

Employment% State

GSP

Nevada Gold 2.1 billion 11,730 1.86 8.58

Arizona Copper 2.7 billion 11,800 0.74 2.32

Minnesota Iron 1.22 billion 6,200 0.27 0.86

Florida Phosphate Rock W W - 0.31

Missouri Lead 240 million 4,700 0.18 0.40

Note: W Data withheld by Bureau of Mines to protect proprietary sources

Sources:U.S. Department of the Interior, Bureau of Mines. 1993. State Mineral Commodity Summaries, 1993.U.S. Department of Commerce. 1993. Statistical Abstract of the United States.

On average, the hardrock mining industry is a viable industry. However, some firms and individual

MINING INDUSTRY PROFILE

September1997 A - 19

mines, particularly small ones, have financial difficulties. Assessing the financial health of individual

commodities is difficult because many firms produce various commodities from various countries. Reports

by Standard and Poor’s, Moody’s and the Value Line assess the finances for the mining companies, which

includes non-American holdings. In addition, publicly available financial statements for companies are

consolidated, and include the assets, liabilities, and operating accounts of the parent company and its

subsidiaries. This creates a problem in trying to understand the financial health of the American hardrock

mining industry because the consolidated financial statements include financial information from operations

outside of the United States. Therefore, it becomes a problem in distinguishing the financial health of the

American mining industry from the world’s mining industry.

The discussion below covers the major industry sectors, as reported by Standard & Poor’s, Moody’s,

and the Value Line. Individual commodities not discussed indicates that Standard & Poor’s or Moody’s

did not compile information. Note that the latest financial information reported by Standard & Poor’s,

Moody’s, and the Value Line includes information ending before the economic recovery of the mid-1990s.

It should also be noted that the industry’s, and individual companies’, financial health can be quite volatile

over relatively short periods of time, so the discussion that follows is necessarily only a snapshot in time.

Copper. Three financially viable producers dominate the copper mining industry (ASARCO

Incorporated, Cyprus Amax Mining Company, and Phelps Dodge). However, other firms are not as

financially healthy. From 1989 to 1992, the copper mining industry was characterized by decreasing

operating revenues, net income (including some companies with negative net income), asset-use efficiency,

average share prices, and earnings per share. Short-term and long-term liabilities have increased for some

companies but are stable. Overall the industry is financially secure.

Lead and Zinc. For purposes of its analysis, Standard & Poor’s combined the lead and zinc

industries. Leading lead producers include The Doe Run Company, ASARCO, and Cominco, while

leading zinc producers include Cominco, Doe Run, Jersey Miniere Zinc, and the Green Creek mine

(Kennecott, Hecla, and others). From 1988 to 1991, decreasing operating revenues, net income (including

some companies with negative net income), asset-use efficiency, average share prices, and earnings per

share characterized the lead and zinc mining industry. The industry began a modest improvement in 1992.

Short-term and long-term liabilities have remained constant, but decreasing sales has reduced the industry’s

ability to meet short-term and long-term obligations. Companies focusing on the lead and zinc industry

may be problematic.

Gold. The gold mining industry is dominated by a few firms (Barrick Gold Corporation, Echo Bay

Mines Limited, Homestake Mining, Lac Minerals Limited, and Newmont Mining Corporation) that are

gaining an increasing portion of the market share. None of these firms have a problem meeting either

short- or long-term debt. Decreasing operating revenues, net income and increasing liability characterize

smaller firms. In the gold mining industry, the major producing companies are financially strong, although

other firms within the industry are not as healthy and some have a problem meeting short-term debt.

MINING INDUSTRY PROFILE

September1997 A - 20

Silver. Many companies that produce gold also produce silver. Therefore, much said about gold can

also be repeated for silver. However, Standard & Poor’s classifies a few firms as primarily silver

producers (Coeur d’Alene Mines Corporation, Hecla Mining Corporation, and Sunshine Mining

Company). Net income for silver producers has continued to decline with the three major silver producers

having negative net income during 1991 and 1992. However, the companies do not have liquidity

problems. Based on current ratios (current assets divided by current liabilities), the three companies have

had consistently large cash reserves.

Miscellaneous sectors. In the metals-miscellaneous category, Standard & Poor’s used financial data

from several selected companies that mine diverse commodities. On average, for the companies in the

miscellaneous category sales, operating income, profit margin, cash flow, and earnings have all decreased.

All of the indicators started to decrease in 1988 and continued until 1992. However, based on measures of

liquidity for selected companies there does not appear to be a problem meeting short- and long-term

liabilities.

Capital Expenditures for Pollution Abatement. The U.S. Bureau of the Census does not separate

capital expenditures for pollution from companies identified by SIC codes 10, 11, 12, or 14, but reports

them together (those SIC codes include metal mining, industrial minerals mining, and coal mining). In

1991, capital expenditures for pollution abatement equipment was a combined $273.6 million for these four

major groups. This included expenditures of $117.5 million for air pollution control, $119.6 million for

water pollution control, and $38.5 million for solid waste control (U.S. Department of Commerce, 1993).

5. INACTIVE AND ABANDONED MINES

The number of inactive and abandoned mines in the United States is simply not known. (Although

“inactive and abandoned mines,” or IAMs, has become a commonly used term, the mines so categorized

may be better described as abandoned mines; most mines that are temporarily inactive are still considered

“active” by state and federal regulators.) Many federal agencies and others have made estimates of the

number of mines, with little consistency and unknown accuracy. There are several areas of agreement

among most sources and commentators. First, nearly all agree that the total number of abandoned mines is

very large. In addition, there is some agreement that only a minority cause environmental damages--the

size of the minority is uncertain, however. Also, many have noted that some mines pose a threat to safety

but otherwise pose little or no risk to human health or the environment. Finally, there is also some

agreement that the costs of remediation dwarfs available resources, at whatever level.

Major areas of disagreement include the extent to which resources should be devoted to detailed

inventories instead of remediation (the ultimate issue is how sites should be ranked), what the cleanup goals

should be, and who should be the responsible party (e.g., federal or private land owners or prior

claimants/lessees). If additional resources were made available for remediation, the major issue would

likely become establishing priorities among sites (Frieders and Raney, 1994).