apoorva deshpande

TRANSCRIPT

A PROJECT REPORT

ON

“Matching the residential growth patterns with buyer preference (Pune).”

AT

JONES LANG LASALLE.

SUBMITTED TO

MAEER’s MIT SCHOOL OF BUSINESS

BY

APOORVA DESHPANDE

2804442

28TH PGDM

Under the esteemed guidance of

Prof. N.J. CHAVAN

MIT- SOB, PUNE

IN PARTIAL FULFILLMENT OF

POST GRADUATE DIPLOMA IN MANAGEMENT (PGDM)

2010-2012

1

Table of contents

Chapter No. Title Page No.

Declaration from student 4

Certificate from Company 5

Certificate from Guide 6

Acknowledgement 7

List of Tables 8

List of Graphs 9

Executive Summary 10-11

I Introduction 12- 30

1.1 Company profile

1.2 Objectives of the study

1.3 Limitations of Study

II Research Methodology 31- 35

2.1 Primary data

2.2 Secondary data

2.3 Sample design

2.4 Population

2.5 Sample size

2.6 Sampling method

2

2.7 Method of data collection

2.8 Instrument for data collection

III Theoretical Background 36- 40

IV Data Processing and Analysis 41- 72

V Management Lessons 73- 79

VI Findings 80- 82

VII Recommendations 83- 84

VIII Conclusions 85- 87

Bibliography 88- 89

3

DECLARATION

I, Ms. APOORVA M. DESHPANDE hereby declare that this project report is the record of

authentic work carried out by me during the period from 12 th May 2011 to 2nd July 2011 and has

not been submitted to any other University or Institute for the award of any degree / diploma etc.

Signature:

(APOORVA DESHPANDE)

Date:

4

5

6

ACKNOWLEDGEMENT

Completion of research and writing of the report is a satisfying event and the pleasant part is the

opportunity to thank those who inspired, contributed and cooperated to it.

I am thankful to Mr. Jai Singh, Residential head, Mr. Adhishesh Mitra, Capital markets

head and Mr. Sameer Gholve for their constant guidance and support throughout the duration

of the project. I would also like to thank all the staff at JLL for their cooperation.

I take the opportunity to offer my deep sense gratitude and reverence to Mr. N.J. Chavan, my

internal project guide for his beneficial co-operative help. His immense support has been a real

force behind completion of this project.

Last but not the least, I would like to thank all the respondents who spent their precious time to

answer the questions, without their support this project would not have been successfully

completed.

Apoorva Deshpande.

7

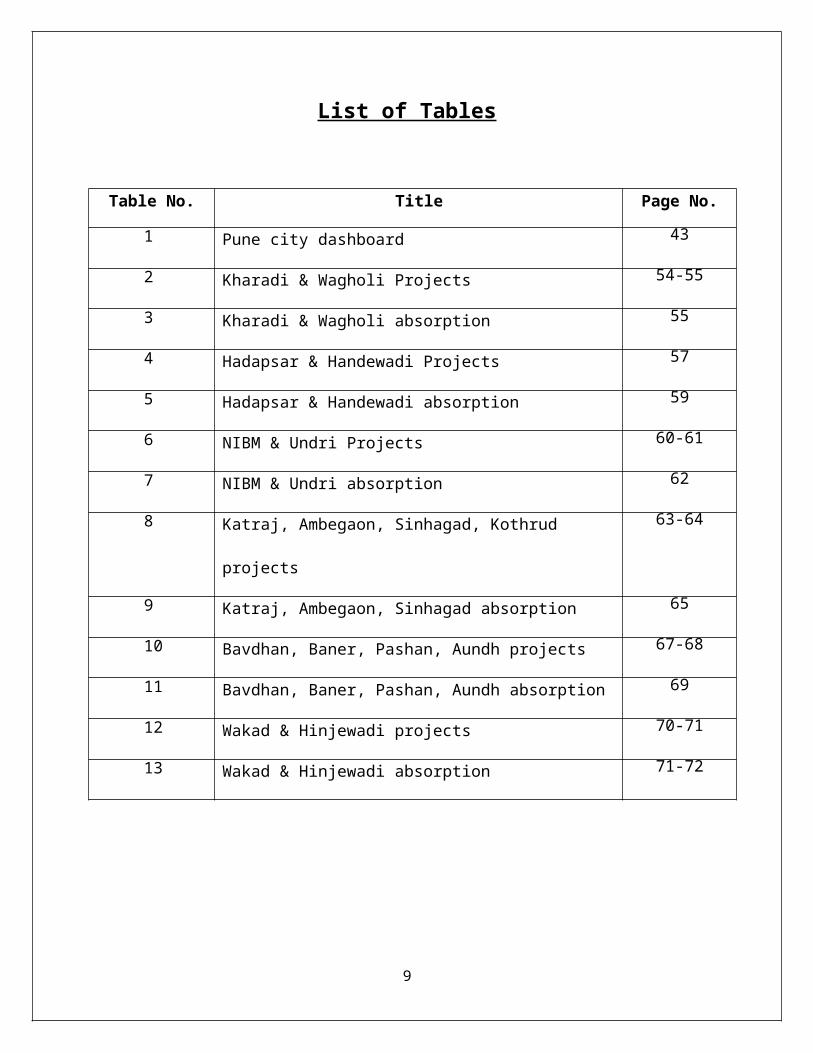

List of Tables

Table No. Title Page No.

1 Pune city dashboard 43

2 Kharadi & Wagholi Projects 54-55

3 Kharadi & Wagholi absorption 55

4 Hadapsar & Handewadi Projects 57

5 Hadapsar & Handewadi absorption 59

6 NIBM & Undri Projects 60-61

7 NIBM & Undri absorption 62

8 Katraj, Ambegaon, Sinhagad, Kothrud projects 63-64

9 Katraj, Ambegaon, Sinhagad absorption 65

10 Bavdhan, Baner, Pashan, Aundh projects 67-68

11 Bavdhan, Baner, Pashan, Aundh absorption 69

12 Wakad & Hinjewadi projects 70-71

13 Wakad & Hinjewadi absorption 71-72

List of Graphs

8

Graph No. Title Page No.

1 Population growth 44

2 Overall demand and supply 50

3 Kharadi & Wagholi availability 55

4 Kharadi & Wagholi absorption 56

5 Kharadi & Wagholi rate 56

6 Hadapsar & Handewadi availability 58

7 Hadapsar & Handewadi rate 58

8 Hadapsar & Handewadi absorption 59

9 NIBM & Undri availability 61

10 NIBM & Undri absorption 62

11 NIBM & Undri rate 62

12 Katraj, Ambegaon, Sinhagad availability 64

13 Katraj, Ambegaon, Sinhagad absorption 65

14 Katraj, Ambegaon, Sinhagad rate 66

15 Bavdhan, Baner, Pashan, Aundh availability 68

16 Bavdhan, Baner, Pashan, Aundh absorption 69

17 Bavdhan, Baner, Pashan, Aundh rate 69

18 Wakad & Hinjewadi availability 71

19 Wakad & Hinjewadi absorption 72

20 Wakad & Hinjewadi rate 72

EXECUTIVE SUMMARY

9

The objective of the project was matching the residential growth patterns with buyer preference

analysis in the city of Pune. The survey required a market research of builders and real estate

developers and in Pune and to collect information on various grounds in reference to the site

such as the type of offerings, number of apartments/ flats in the scheme, specific requirements,

the total ticket size, absorption rate, prevailing price per sq.ft, loading factor, location of the site,

etc.

The data collected was compiled in a proper format for the analysis of the most potential

upcoming zone in comparison to other zones in Pune.

The real estate sector is one of the unorganized sectors in India. In the recent past it has been

observed that the residential aspect of the real estate industry in India is highly potential, but

rather lacks a channelized manner of working. Thus the project title suggested by the company

was to capture the core demand and supply analysis in the residential sector for further research

analysis.

Due to limitations of geographical boundaries the research was limited to the city of Pune

including the suburbs. For the convenience of data collection and sampling process, the city was

divided into seven (7) zones; north, north east, east, south, south west, west and the central

business district.

Market research was done through the mode of survey.

The task at market research involved travelling across the city of Pune and interacting with the

developers, promoters and builders in regards to the upcoming residential projects by them in

various parts of the specified zones. Details of the residential projects were collected and

tabulated in a MS Excel sheet under various categories for the ease of segregation of the data.

10

The data consisted of the residential patterns in the city, pertaining to the size of the apartment,

row house and pent house, the cost, amenities provided and other aspects in regards to

construction development.

The total number of projects visited amounted to 107. A procedure of segmentation was done so

as to concentrate only on large projects that consisted of 50 apartments minimum.

In contrast to the market research carried out for the demand aspect, a questionnaire in form of

an enquiry form was distributed to potential customers (who are in search of an apartment, row

house or penthouse). The details were taken on the basis of the any particular area of residence

the customer would like to opt for, the budget, any pre- visited or finalized builder or project etc.

Further the data helped in analyzing the overall sales in the residential sector along with the

upcoming zone and the area in specific which was in demand. It also gave a clear picture of the

expenditure patterns of the consumer while purchasing or re- purchasing a house.

Both the demand and supply aspects have helped in analyzing the overall aspect of the

residential trends that has been observed in the city of Pune in the last one year (2010- 2011).

11

INTRODUCTION

1.1 COMPANY PROFILE

12

HISTORY AND EVOLUTION:

A Tale of Two Cities and Global Expansion52…

Jones Lang LaSalle’s history spans more than 200 years, but we’ll just give you the highlights:

1783: Richard Winstanley sets up shop as an auctioneer in London and is succeeded by his son

James in 1806.

1939: Through partnerships and mergers too numerous to mention, the Winstanley firm is now

known by the last names of its three principal members: Jones Lang Wootton (JLW) & Sons.

1945: In a London devastated by World War II bombings that destroyed property records, JLW

takes on the enormous job of documenting boundaries and ownerships of thousands of land

parcels. JLW secures licenses for development and agency appointments, which places it in an

enviable position as the city begins to rebuild in 1954.

1957: JLW begins its global expansion by opening offices in Australia, overcoming an initial

prognosis of "outlook favorable but problems formidable." Working from this base, the company

expands into New Zealand, Singapore, Kuala Lumpur, Hong Kong and Tokyo. Meanwhile, back

in Europe, JLW extends its activities into Scotland, Ireland and continental Europe.

1968: Across the Atlantic, in El Paso, Texas, a small group of professionals forms IDC Real

Estate with the goal of bringing much-needed professionalism to the marketplace. IDC quickly

outgrows its local market, moves to Chicago, eventually changes its name to LaSalle Partners

and becomes one of America’s leading real estate service firms. The firm becomes known for its

longstanding client relationships.

13

1975: JLW opens its first U.S. office in New York. Throughout the 1970s and 80s, both JLW

and LaSalle Partners extend their presence in new markets throughout Asia Pacific, Europe and

the Americas.

1997: LaSalle Partners completes its initial public offering of the company’s common stock.

1999: In the largest international real estate industry merger to date, JLW and LaSalle Partners

join forces and form Jones Lang LaSalle. The resulting company was—and still is—the leading

global commercial real estate services and investment management firm.

2006: The firm begins a period of strong growth both organically and through acquisitions.

Among four new firms joining the fold in 2006 is Spaulding and Slye, a major real estate player

on America’s east coast, plus other strong firms in England, Spain and markets in the Middle

East.

2007: Another busy expansion year sees 15 mergers and acquisitions including the transaction

that created Jones Lang LaSalle India, the largest real estate firm in India. We also acquire

Upstream, the leading sustainability consultancy in the UK, and a leading property advisor in the

Netherlands. The awards continue as well, highlighted by a top honor for our energy and

sustainability work from the U.S. Environmental Protection Agency.

2008: Acquisitions increase our presence in China, make us the largest retail advisor in

Germany, and allow us to expand our presence in Australia and Scotland. We are now the

leading real estate firm in Germany and the Netherlands, the two largest real estate markets in

Continental Europe. In the United States, we acquire The Staubach Company, a leader in tenant

representation. This acquisition significantly enhances our presence in key markets around the

United States, establishes us as the market leader in public sector services and adds scale to

many of our core businesses.

2011: We establish ourselves as the clear leader in the UK and continental Europe with the

acquisition of London-based King Sturge. The transaction gives us scale and depth of expertise

that greatly enhance our service delivery capabilities. This string of acquisitions supports our

strategy of being a consolidator within a consolidating industry. And we’re still winning awards,

including Fortune World’s Most Admired Companies in 2011.

14

ABOUT JONES LANG LASALLE:

Real Value

We are in business to create and deliver real value for clients, shareholders and our own people

in a complex world that is constantly changing.

Jones Lang LaSalle is a financial and professional services firm specializing in real estate

services. The firm offers integrated services delivered by expert teams worldwide to clients

seeking increased value by owning, occupying or investing in real estate. With 2010 global

revenue of more than USD 2.9 billion, Jones Lang LaSalle serves clients in 70 countries from

more than 1,000 locations worldwide, including 200 corporate offices. The firm is an industry

leader in property and corporate facility management services, with a portfolio of approximately

1.8 billion square feet worldwide. LaSalle Investment Management, the company’s investment

management business, is one of the worlds largest and most diverse in real estate with USD 45.3

billion of assets under management.

Jones Lang LaSalle has over 50 years of experience in Asia Pacific, with over 19,700 employees

operating in 78 offices in 13 countries across the region. The firm was named the Best Property

Consultancy in Asia Pacific at 'The Asia Pacific Property Awards 2011 in association with

Bloomberg Television'.

Jones Lang LaSalle is proud of the recognition we receive. These distinctions underscore our

position as the chosen real estate expert and strategic advisor for leading owners, occupiers and

investors worldwide.

15

SERVICES OFFERED:

Agency Leasing:

A strategic, proactive agency leasing approach for commercial property assets.

Commercial property leasing focused on forging long-term tenant relationships. Earning

successful returns on leased commercial property means more than filling space. It begins with a

firm grasp of what kind of space the most desirable tenants want and what they will pay for it.

And it’s followed by a marketing and agency leasing strategy that we’ll execute to mix the best

tenants at the best lease terms – and retain them for lasting value. Whether you’re an investor,

developer, property company or public entity, that’s the way we’ll go to work for you, in every

major market in the world. We’ll bring a strategic, proactive leasing approach to your

commercial real estate assets so that you can focus on continuous financial growth.

Capital Markets:

Uncovering value in your portfolio with real estate corporate finance.

Given the percentage of corporate budgets devoted to offices and other facilities, nothing

dominates a balance sheet more than real estate. Profitability equals your firm’s success in

16

aligning occupancy needs with financial objectives. The value is clear, but the path is complex.

Let Jones Lang LaSalle’s real estate corporate finance experts craft advanced strategies to get the

most out of your property. As the largest global professional services firm that is rooted firmly in

both real estate and the capital markets, we’ll work with you to uncover value in every facet of

your portfolio. There’s no need to shoot from the hip at emerging financial challenges. We’ll

develop corporate real estate finance strategies to align financing and occupancy decisions with

tax, financial reporting and treasury objectives.

Whether your charge involves a single property or a complex set of worldwide decisions, we’ll

assemble a collaborative corporate finance team that has delivered results in initiatives

comparable to yours.

Corporate Finance:

Let Jones Lang LaSalle’s real estate corporate finance experts craft advanced strategies to get the

most out of your portfolio or a single property.

Given the percentage of corporate budgets devoted to owning and managing offices and other

real estate assets, nothing dominates a balance sheet more. Profitability equals your firm’s

success in aligning occupancy needs with financial objectives and shareholder value enhanced by

sweating each asset optimally including real estate. The value is clear, but the path is complex.

Let Jones Lang LaSalle’s real estate corporate finance experts craft advanced strategies to get the

most out of your portfolio or a single property. These strategies are tailored to suit corporate

looking to monetize or optimize their portfolios. As the largest global professional services firm

that is rooted firmly in both real estate and the corporate finance, we’ll work with you to uncover

value in every facet of your portfolio. Our corporate finance team can help evaluate real estate

and business objectives through various lenses to determine the most effective solutions and

implement them. We’ll develop and apply corporate real estate finance methods to align

financing and occupancy decisions with tax, financial reporting and treasury objectives.

Whether your portfolio involves a single location property or a complex set of worldwide

decisions, we’ll assemble a collaborative team that has delivered results. Our broad range of

offerings for various set of corporate includes:

17

• Sales lease back structuring & execution

• Transaction Structuring

• Fund raising (Equity or Debt)

• Mergers & Acquisitions

• Joint Ventures

• Portfolio / Single Asset Strategy

• Alternative Ownership Structures

• Accommodation Strategy

Corporate Solutions:

We know what it takes to make real estate outsourcing successful.

Jones Lang LaSalle pioneered the corporate real estate offering in Asia Pacific. Today, our

platform provides unmatched services across a single project, country or regional portfolio. Our

commitment to shaping our business around the needs of our clients and delivering on our

promises keeps us at the forefront of our industry. With real estate being one of the top three

costs in a company, having the right partner is critical in finding operational efficiencies. At the

heart of our clients’ success lays the collective expertise of our Corporate Solutions professionals

from around the world. Through our collaborative approach in understanding their needs, we

help bridge their goals and challenges. No single solution can address different circumstances.

By harnessing the power of an individual or integrated suite of our specialized services, we offer

clients winning strategies that help them maximize the performance of their real estate portfolio.

18

Facility Management:

Facility management providing maximum efficiency, safety and employee comfort.

Efficiency, cost savings and continuous improvement from facility management experts. In an

ideal world, real estate executives manage facilities that operate flawlessly, freeing them to focus

on real estate strategies that contribute to broader business and financial goals. In reality, many

spend much of their work day managing routine facility management and maintenance tasks. As

the world’s largest facilities management company, we know that the ideal can be real. We’ve

shown hundreds of the world’s best-known companies and institutions how to operate facilities

with maximum efficiency, safety and employee comfort—and dramatically reduce costs in the

process. Our facility management services typically show clients a 20 percent or more drop in

their overall facility operating expenses. What’s more, we expose our clients to all the best

practices we’ve honed while managing office, industrial, technical, manufacturing, critical

environments and one-of-a-kind facilities on five continents—often for the same company. Our

facility management professionals will apply their hands-on experience to drive maximum value

and efficiency in your commercial property portfolio.

Hotels:

19

Whether you’re a hotel owner, operator, investor, developer or financier, you strive to enhance

your operations and investments in an industry that gets more competitive every day. And real

estate is at the heart of it all. Jones Lang LaSalle Hotels can be your single check-in for building

profit with comprehensive hotel asset management and investment services. We are the first—

and largest—global hotel investment services firm to set up operations in India. . Our clients

look to us for advice and execution on everything from investment sales, capital raising and

valuation advice to asset management, operator selection and project development.

Land & Industrial Services:

Transactions related to land, being the pre-requisite for any real estate development, require

specialist advisory services that stem from a background of knowledge that provides critical

insights into the potential of projects that may be positioned on land at various locations and the

in-depth knowledge of local planning norms. Our land agency division leverages on the

knowledge gained from our internal consulting services, wherein there is a high degree of

exposure to various types of real estate markets in various locations across India, along with

identification of development opportunities right from their concept stage all across India. This

synergistic approach has benefited our clients, who range from land owners, developers,

corporates, and various funds seeking to invest in projects, including FII. This group seeks to

align expectations of various potential partners in the development of projects with the objective

of enabling high level of returns on investments for all partners along with an equitable

distribution of risks and project costs. Typically, our range of services include assisting

prospective purchasers in identification, evaluation, and purchase of land; assisting land owners

in disposal of their land holdings; facilitating investments for developers in various projects;

organizing opportunities for various investors seeking to invest in remunerative projects;

structuring joint ventures between landowners and developers/investors/end users; assisting

20

developers/corporate in divesting or investing in land portfolios; and assisting clients in

sourcing/disposal of ‘Transferable Development Rights’, among others.

Lease Administration:

Make informed decisions with our comprehensive lease administration and auditing solutions.

If your organization has a diverse and geographically dispersed real estate portfolio, it is critical

for you to have accurate, up-to-date portfolio information for strategic planning and mitigate the

risks and cost of missing a critical lease date. We can offer you a comprehensive lease

administration and auditing solution that facilitates quicker decision making and reduces risk.

We have experienced professionals with strong industry expertise that can deliver solutions that

meet your business needs. This is further supported by our award winning IT platform, One

View Lease Admin, which provides you with easy storage, retrieval and real-time access to

every detail of your portfolio. It also gives you a consolidated view of your total real estate

portfolio.

Project & Development Services:

Whether your organisation is relocating or expanding, you need the assurance of a service

provider that has the right experience and knowledge to overcome your unique challenges. No

21

other service provider has a stronger combination of global experience, local knowledge, best

practices and professional expertise to address your real estate project management needs.

Across the Asia Pacific, we have over 600 professionals in 26 offices that managed and advised

on over US$6.8 billion worth of capital expenditure in 2009, making us a leader in managing

projects that create real value for our clients. In India, we delivered our expertise on over 100

projects with sizes ranging from 1,000 to 2.1 million sq ft in the past year. You gain an

unparallel advantage of having greater control of outcomes through our suite of specialized

industry solutions – Hotel, Commercial, Education, Health, Infrastructure, Industrial, Residential

and Retail. Delivered through a specially selected team, we’ll work with you to set measurable

goals and achieve them throughout your project’s advisory, planning, design, and construction

phases.

Property and Asset Management:

Real Estate Intelligence Service:

In a dynamically growing market, your business needs to have a comprehensive view of the

machinations behind India’s fast paced real estate growth. REIS India is a subscription-based

research service designed to provide you with timely, accurate, insightful real estate intelligence

across India to enable you to make informed decisions. REIS India combines international

expertise with local knowledge and is backed by Jones Lang LaSalle’s award-winning research

platform. Real estate professionals across the globe have been relying on REIS in their decision-

making process for over two decades in Australia and New Zealand, and over a decade in Asia.

This service consists of comprehensive real estate data, analyses and forecasts for institutional

property players. The wide spectrum of outputs is prepared by a dedicated team of researchers

located across 10 offices in India. REIS would give your business access to accurate and timely

real estate market intelligence to help you make smart business decisions in a semi-transparent

22

and emerging market. In a competitive environment where information is power, REIS India

provides you with cutting-edge insights into India’s diverse and challenging real estate markets

through collation, analysis and forecasts of property market indicators and trends across all major

markets. Carefully prepared and constantly updated by Jones Lang LaSalle’s highly qualified

research professionals, REIS India enables you to identify opportunities and risks first-hand. We

gather on ground intelligence via regular collaboration with our colleagues working in areas such

as capital markets, leasing, consulting and valuation. REIS empower you with consistent and

complete data and analyses. It is supplemented by value-added services including client

briefings, presentations and rapid market updates.

Research:

Insight, interpretation and analysis tailored to your needs from our real estate research services.

Timely and informed research and analysis is an accepted prerequisite to successful decision

making. At Jones Lang LaSalle, our extensive market coverage, innovative analysis and

prescient forecasting is backed by the market knowledge and commercial acumen of real estate’s

most experienced research team. Our local, regional and global researchers are dedicated to

providing a seamless research service from local data sourcing and single assignment analysis

through to the construction of global investment, development and locational strategies. Our

research services are flexible, practical and backed by best in class proprietary data and

analytical models. Projects can be customized to address questions on sectors, geographies or

individual assets and we work with you in a manner that best fits with your organization. Please

contact the Jones Lang LaSalle commercial real estate market research services group for more

information.

23

Residential:

Experience and expertise gained through the various residential transactions on behalf of some of

the most active developers, corporate and individuals make us the unchallenged market leaders

in the residential domain. At Jones Lang LaSalle, our team of professionals dedicated to

residential real estate continuously keeps abreast of the ever-changing consumer needs. In

addition, we leverage our industry relationships to help developers achieving their sales goals,

maximize returns and speed up cash recovery.

Retail:

Shoppers change preferences and retailers change strategies. But we never waver in our

commitment to providing industry-leading real estate services for retail assets. As a recognized

leader in the global retail industry, Jones Lang LaSalle offers unparalleled knowledge and

experience. Our specialists provide comprehensive retail services built on a platform to exceed

the expectations of our owner, investor and occupier clients. With retail offices in 40 countries

around the globe, we manage nearly 250 million square feet of retail with more than 600

properties worldwide. We know that retail offerings and clients’ needs are constantly changing.

That’s why we offer a flexible, customized plan that will ensure that together, we’ll maximize

the highest potential of your asset or portfolio.

24

Strategic Consulting:

Many real estate initiatives are designed to get the immediate job done. But our commercial

property consultants deliver strategies that take a longer view. When real estate decisions align

with your organization’s broader business and financial objectives, it’s only natural that

expectations are soon exceeded. Our smart, innovative advice helps you gain a competitive

advantage and win senior management support for your real estate activities. Successful

strategies typically pay for their development costs many times over, and real estate savings of

10 percent to 15 percent are not unusual. Our professionals partner with you to create—and

execute—solutions that not only look good on paper, but work in practice. You’ll benefit from

our extensive commercial real estate experience helping companies from a broad range of

industries meet the challenges of mergers and acquisitions, identify innovative workplace

solutions, drive organizational change and engineer the financial optimization of their

commercial property.

Tenant Representation:

An effective and cost-efficient tenant representation services in New York, Newcastle, New

Delhi or anywhere in between. Whether your organization is relocating a single major office or

seeking a consistent strategy to acquire space and accommodate global expansion, you need a

commercial tenant representation firm that knows the territory. We serve as your strategic

advisor, lowering your real estate costs and occupancy risks while maximizing workplace

flexibility and productivity. We’ll analyze your business drivers and occupancy needs, identify

and evaluate appropriate options, and manage lease negotiations. In fact, we’ll be your on-call

expert for all your leasing and lease administration needs.

25

Transaction Management:

In recognition of this, Jones Lang LaSalle has a dedicated Transaction Management discipline

within its Tenant representation group. The primary function of the Transaction Management

team is to develop and implement processes and tools which support workflow management;

promoting cross training, skill sharing and continuous adoption of best practices into local

delivery teams. Our transaction management approach provides our corporate clients with:

• Deal Support – Working closely with local Tenant Representation teams, the Transaction

Manager initiates each project, sharing account protocols and processes and imparting captured

key learning’s which results in increased speed to market and internal efficiencies.

• Best Practices - Leveraging from the regional and global platforms, the Transaction

Manager is able to cascade best practice tools, policies and processes to drive continuous process

improvement and an innovative approach to your account.

• Market Trends Analysis – Through analysis of Lang LaSalle’s research offerings and

local market expertise, the Transaction Manager is able to identify market trends and create a

proactive portfolio strategy that allows you to minimize risk and focus more time on addressing

the needs of your internal stakeholders.

• Tailored Deliverables – Working with you, the Transaction Manager will develop

structured and specific portfolio reporting including; benchmark reporting against market,

competitor or industry and an operating report that identifies key market trends and themes and

the potential impact on your portfolio.

• Performance Measurement – Measuring performance on both individual assignments as

well as overall satisfaction ensures our clients receive services that consistently meet or exceed

26

defined metrics and expectations. These results are shared with the delivery teams to drive

training and development to ensure continuous improvement and enhance performance across

your account. Consistent performance and high levels of client satisfaction have resulted in over

90 strategic alliance partnerships. Across Asia Pacific, we provide exclusive transaction

management services for over 150 million square feet of office, retail and industrial space for

leading banking, technology, industrial and government organizations.

Warehousing and Logistics Solutions:

With new warehousing and logistics frontiers opening throughout India, local and multinational

companies are facing more challenges in selecting and managing the best locations. At Jones

Lang LaSalle, we understand the unique requirements of the supply chain industry. We have a

dedicated team of warehousing and logistics property experts who help clients achieve flexibility

and cost-efficiencies through quality advice. With over 49 years of experience in working with

high-profile logistics organisations across Asia Pacific, you can rely on us to deliver

sophisticated real estate solutions for your businesses.

CORPORATE SOCIAL RESPONSIBILITY:

As part of our commitment to create real value in a world that is constantly changing, we are

determined to be a good corporate citizen in every corner of our global community. We hold

ourselves accountable for the social, environmental and economic impact of our operations. We

design our policies and business practices to reflect the highest standards of corporate

governance, transparency and ethics. We support all aspects of the corporate social responsibility

agenda, but one area is particularly relevant for us. We have the skills and opportunity to help

minimize the significant impacts that real estate has on the environment. Our goal is to be the

27

unquestioned leader in the real estate industry in environmental sustainability and energy

management.

Environment: We are committed to being the real estate industry leader in environmental

sustainability and energy management, both for our clients and ourselves. Our capabilities give

us the opportunity to drive change that minimizes the impact of commercial real estate on the

environment.

Workplace: We focus on creating and maintaining a rewarding and welcoming workplace for

our people around the world. We strive to attract and retain the most talented individuals,

encouraging and enabling them to succeed.

Diversity: We foster an inclusive environment that values the richness of our differences and

reflects the diverse world in which we work. By cultivating a dynamic mix of people and ideas,

we enrich our service capabilities and the communities in which we operate.

Community and Society: We endeavor to be good citizens wherever we live and work.

ETHICS AND CORPORATE GOVERNANCE:

We are proud of our global reputation for uncompromising integrity, ethical conduct and

corporate governance. Our Code of Business Ethics and Vendor Code of Conduct are followed

by our own employees and everyone who does business on behalf of our firm. We are also

proud of the rigor and quality of the firm’s corporate governance and the benefits these policies

produce for our stakeholders.

• Code of Business Ethics:

Our Code of Business Ethics helps our people better understand the duties and responsibilities

associated with conducting business on behalf of Jones Lang LaSalle. The Code contains

sections that address our responsibilities to clients, business partners, shareholders, and the

communities and governments in the countries in which we do business. Members of our Board

of Directors fully support and mandate our compliance with the Code. Reports of possible

violations can be made to our global Ethics Hotline 24 hours a day, seven days a week.

28

• Vendor Code of Conduct:

We trust that our vendors, including firms and individuals who provide direct service to or

directly to our clients, will honor our commitment to integrity. While vendors are viewed as

independent entities, their business practices can reflect upon our brand and reputation. We

expect all vendors to embrace and adhere to our Vendor Code of Conduct.

1.2 OBJECTIVE OF THE STUDY

Real estate sector is one of the most unorganized sectors in India. The presence of small property

agents and real estate brokers poses a great challenge for the established institutions and MNC’s

to make their presence felt in the market. Thus, creating awareness among the masses is a tough

task posed in front of international property consultants.

There are two objectives of the study; primary and secondary. The primary objective

concentrates on the prime focus of the research carried out, while the secondary objective is a

supporting element.

Primary objective:

Studying the residential market in Pune – Development of the growth corridors.

1. Division of the city into zones.i.e, North, South, East and West.

2. Concentration on the development of the suburbs in the respective zones.

3. Research on the upcoming projects.

4. Feedback from the sales team.

29

Secondary objective:

Customer behavior and preferences

1. Customer feedback on the basis of absorption level.

1.3 LIMITATIONS OF THE STUDY:

The survey was divided in two categories Developers/ builders and customers. The method

adopted was a personal interaction with the developers and questionnaire (feedback form) for the

customers.

The entire survey was completely carried out according to the flow as per decided plan. There

were a few hurdles in the process of my survey.

1. It was difficult to obtain appointments and availability with the developers/ builders.

2. The marketing and sales personnel lacked the basic knowledge.

3. Some people were not able to give complete information due to professional constraints.

4. Repeat visits were required at some sites, due to unavailability of the staff.

30

2. RESEARCH METHODOLOGY

31

2.1 PRIMARY DATA:

In the research process primary data was used on a large extent. Personal Survey and telephonic

Survey method through certain mandated questions were done, in reference to the supply

analysis. A feedback was used to get the response of buyers/ customers, in reference to the

demand analysis. For this purpose I have contacted respondents personally to get the feedback

forms filled.

2.2 SECONDARY DATA:

The secondary data source used in the form of overall industry details and the ongoing sites in

the respective zones through newspaper and internet sites, etc.

32

2.3 SAMPLE DESIGN:

Sample design covers the method of selection, the sample structure and plans for analyzing and

interpreting the results. Sample designs can vary from simple to complex and depend on the type

of information required and the way the sample is selected.

2.4 POPULATION:

The population selected was of all the ongoing residential projects in the segregated respective

zones. There was no such biased behavior done in the selection of all the projects targeted in any

particular zone.

33

2.5 SAMPLE SIZE:

I have used the statistical approach of sample size determination, which is based on well-defined

principles. A sample size of one hundred and five (105) was taken into account. All the 105

sample data was gathered and arranged in a manner where the entire information was accessible.

2.6 SAMPLING METHOD:

The Quota Sampling method was used by me for the project analysis. Aim is to obtain a sample

that is "representative" of the overall population; the population is divided ("stratified") by the

most important variables (e.g. income,. age, location) and a required quota sample is drawn from

each stratum.

This is the reason only residential projects with a total unit size of minimum 50 were considered.

34

2.7 METHOD OF DATA COLLECTION:

Structured interview

- The interviewer has a standard set / sequence of questions that are asked of all

candidates.‡

- Interviewers read the questions exactly as they appear on the survey questionnaire.

Personal survey was done to obtain response from respondents conveniently available. I have

prepared a structured, non-disguised set of questionnaires. The questionnaire prepared collected

different types of questions.

2.8 INSTRUMENT FOR DATA COLLECTION:

A questionnaire with a set of well defined questions was the instrument of data collection that

was used so as to facilitate the research process.

35

3. THEORETICAL BACKGROUND

36

Market Research

According to Philip Kotler, “Research is the systematic design, collection, analysis and reporting

of data and findings relevant to a specific marketing situation facing the company.

We can say that research is both problem solving and problem oriented. The research process

involves a number of inter related activities which overlap and each step has some influence over

the following steps followed by me in the research of this project. The steps are as followed:

1. Formulating the research problem.

2. Choice of research design.

3. Determining sources of data.

4. Designing data collection forms.

5. Determining sampling decisions.

6. Organizing and conducting the field survey.

7. Processing and analyzing the collected data.

8. Preparing the research report.

1. Formulating Research Problem:

The first step in research process is formulating a research problem. It is important stage in

applied research. It is rightly said, “A problem well defined is half solved”.

Once two or more problems are identified the question should be concerned with is- which of the

problem is to be selected? This is necessary because I am not in a position to take up all the

problems on account of limited time. So I have selected a problem, which gives maximum net

worth of research.

2. Research Design:

According to Green and Tull, “Research design in the specification of methods and procedures

for acquiring the information needed. It is the overall operational patterns or framework of the

37

project that stipulates what information is to be collected from which sources by what

procedures”

Research design is a plan, structure and strategy of investigation conceived so as to obtain

answers to research question and to control variance. A research design specifies the methods

and procedures for conducting a particular study. Broadly speaking, research design can be

grouped in three different categories:

Exploratory research

Descriptive research

Casual research

As my research is based on survey of the ongoing residential sites, I have used DESCRIPTIVE

RESEARCH design. I have used Personal Survey Method and telephonic Survey Method of

Descriptive Research Design. Respondents are contacted personally and through telephone

interviewed through questionnaire. I have selected descriptive research design because,

exploratory research design helps in exploring a problem or situation to provide insights and

understanding; and causal research design helps to obtain evidence of cause and effect

relationship, and hence, the use of the descriptive research design in the project is appropriate.

3. Determining Source of Data:

This step includes specifying the various sources of data used by the researcher in collecting the

factors that affect antivirus buyers.

Basically the sources of data are divided into two main categories:

(i) Primary Sources of Data.

(ii) Secondary Sources of Data.

Primary data is the data collected by the researcher at the time of research; its main purpose is to

serve the findings of the research and is collected for the first time. Secondary data is the data

already collected by someone for his/her purpose of study.

38

4. Designing Data Collection Form:

For the study survey method was employed as majority of details, which were collected, were

primary in nature. Personal survey was done to obtain response from respondents conveniently

available, with the help of well-structured questionnaire. I have prepared a structured, non-

disguised type of questionnaire.

5. Determining Sampling Design and Sampling Size:

Once the researcher has decided to carry out a field survey he has to decide whether it is to be a

census survey or sample survey. When decision is in favor of a sample survey has been taken, it

is necessary to have a clear definition of the population for which the sample is to be drawn, and

before deciding on the type of sample design is to be used. First, a broad choice is to be made

between probability and non-probability sampling. There are two approaches for sample size i.e.

practical approach and statistical approach.

6. Organizing and Conducting Field Survey:

Having prepared the questionnaire and selecting sample design and size of sample, the next step

is to organize and conduct the field survey. Two important aspects should be looked into:

interviewing and supervision of fieldwork. The task of interviewing seems to be simple but, in

reality, it is one of the most difficult tasks in research. Supervision of fieldwork is equally

important to ensure timely and proper completion of field survey. Neglecting these aspects

would result in interviewing errors, which, in turn, would undermine the utility of survey.

The researcher then has to organize and conducted the survey by interviewing and supervision of

fieldwork. It is one of the most difficult tasks in marketing research because respondents are

many times busy with their work and some respondents are unwilling to give response due to

various constraints. Thus personal survey takes more time.

39

7. Processing and Analyzing the Collected Data:

In order to derive meaningful results from the statistical tables, the researcher may use one or

more techniques to analyze the collected data and to tabulate it in a proper way. Such analyses

use a variety of techniques to determine important relationship among several variables. The data

primarily collected by questionnaire are represented by questionnaire in tabulation forms and the

findings are represented as the Graphics.

8. Preparing the Research Report:

After the data had been analyzed and conclusion reached, the researcher has to report his

findings to the management. The reporting has to be done in a clear manner so that the chances

of any misunderstandings can be managed. The essence of a good research report is that it

effectively communicates its research findings. The researcher has to exercise the entire course

to make the report useful and worthwhile document for management.

40

4. DATA PROCESSING AND ANALYSIS

41

Pune

PUNE CITY OVERVIEW

Snapshot

Pune (180 31' N, 730 51' E), a leading city within the state of Maharashtra, is located

approximately 170 kilometres southeast of Mumbai. Rising 560m above sea lea, Pune is situated

on the Deccan Plateau where it is surrounded by hills, leading to its moderate climate. The city

is positioned near the confluence of the Mula and Mutha rivers with two additional rivers, the

Pavna and Indrayani, transversing its north-western outskirts.

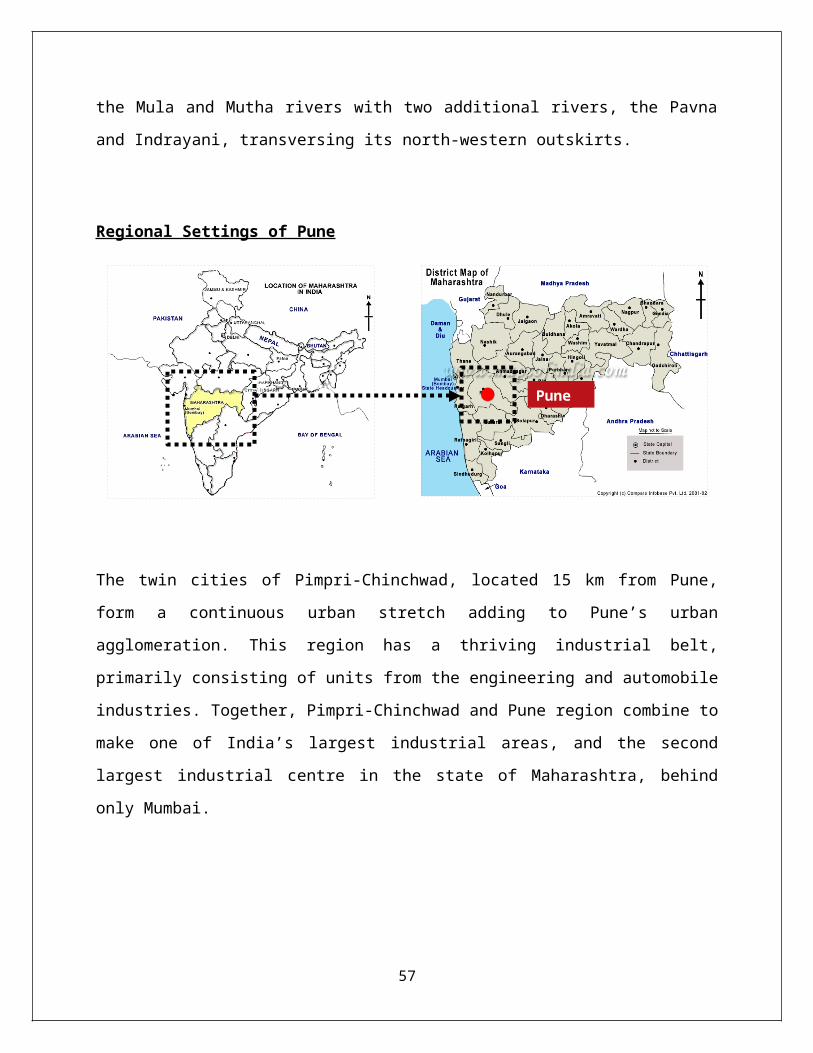

Regional Settings of Pune

The twin cities of Pimpri-Chinchwad, located 15 km from Pune, form a continuous urban stretch

adding to Pune’s urban agglomeration. This region has a thriving industrial belt, primarily

consisting of units from the engineering and automobile industries. Together, Pimpri-Chinchwad

and Pune region combine to make one of India’s largest industrial areas, and the second largest

industrial centre in the state of Maharashtra, behind only Mumbai.

42

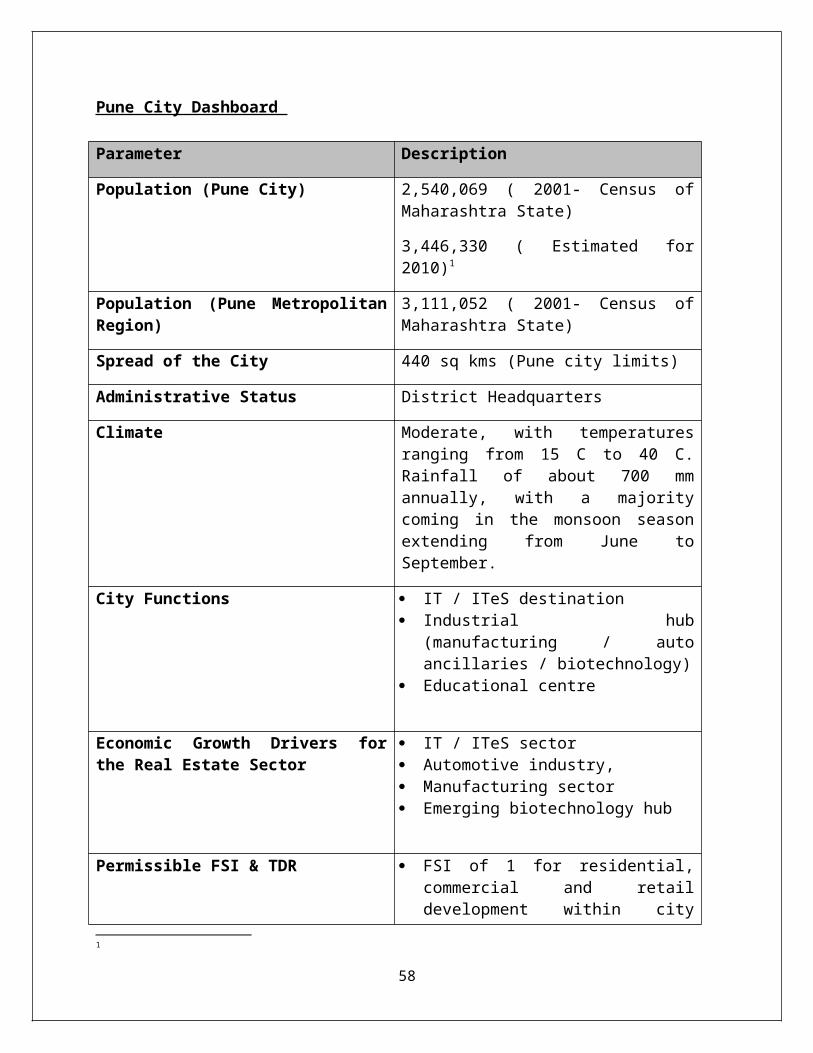

Pune City Dashboard

Parameter Description

Population (Pune City) 2,540,069 ( 2001- Census of Maharashtra State)

3,446,330 ( Estimated for 2010)1

Population (Pune Metropolitan Region) 3,111,052 ( 2001- Census of Maharashtra State)

Spread of the City 440 sq kms (Pune city limits)

Administrative Status District Headquarters

Climate Moderate, with temperatures ranging from 15 C to 40 C. Rainfall of about 700 mm annually, with a majority coming in the monsoon season extending from June to September.

City Functions IT / ITeS destination Industrial hub (manufacturing / auto

ancillaries / biotechnology) Educational centre

Economic Growth Drivers for the Real Estate Sector

IT / ITeS sector Automotive industry, Manufacturing sector Emerging biotechnology hub

Permissible FSI & TDR FSI of 1 for residential, commercial and retail development within city limits (outside core – gaothan areas)

FSI of 2 is granted for IT / ITeS buildings (STPI sanctioned buildings)

TDR of 0.4 is allowed in certain zones Additional TDR of 0.2 could be allowed

(over and above of the 0.4 TDR – as mentioned above) for slum redevelopment

City’s Demographic Profile

1

43

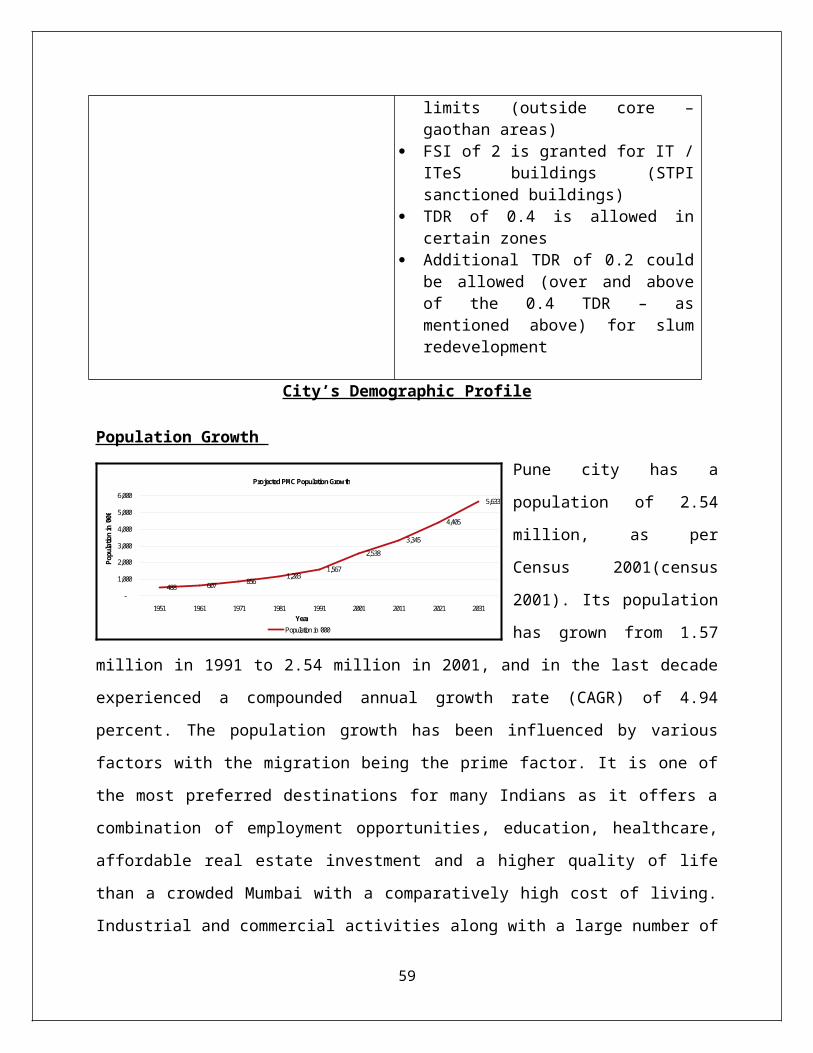

Population Growth

Pune city has a population of

2.54 million, as per Census

2001(census 2001). Its

population has grown from 1.57

million in 1991 to 2.54 million

in 2001, and in the last decade

experienced a compounded

annual growth rate (CAGR) of 4.94 percent. The population growth has been influenced by

various factors with the migration being the prime factor. It is one of the most preferred

destinations for many Indians as it offers a combination of employment opportunities, education,

healthcare, affordable real estate investment and a higher quality of life than a crowded Mumbai

with a comparatively high cost of living. Industrial and commercial activities along with a large

number of educational centres in Thus, Pune attracts a large floating population from all over

India into the city. Rapid growth of the city can mainly be attributed to industrialization of Pune

Municipal Corporation (PMC)/ Pimpri-Chinchwad Municipal Corporation (PCMC) after 1960

and expansion of the information technology (IT) industry in the last decade.

According to the population census 2001, Pune’s population is estimated at around 5.6 million

by end 2031 (fig 1.2a). The average population density for PMC, in 2007 was recorded to be

12,173 persons/sq km, in 2011 it is projected to be approx. 13,718 persons/sq km , in 2021,

approx. 18,064 persons/sq km, and in 2031, it is projected to be approx. 23,102 persons/sq km.

Linkages and Connectivity

Pune has excellent road, rail and air connectivity with most major cities in India. It is well

connected by three national highways (NH-4, NH-50 & NH-9) and one expressway (Mumbai –

Pune) to major urban centers in the western, central and southern parts of the country. Express

and long-distance rail connectivity is already established to Mumbai, Delhi, Hyderabad,

Chennai, Miraj- Kolhapur, and Goa. Pune International Airport, located in the northeastern

quadrant of the city, is located on an Indian Air Force base and is presently used for civil

purposes catering to both international and domestic flights.

Road Connectivity

44

Projected PMC Population Growth

488 607 8561,203

1,567

2,538

3,345

4,405

5,633

-

1,000

2,000

3,000

4,000

5,000

6,000

1951 1961 1971 1981 1991 2001 2011 2021 2031Year

Pop

ulat

ion

in '0

00

Population in '000

The city of Pune is situated on the confluence of National Highways (NH), which includes NH-4

connecting Mumbai in the north and Bangalore to the south, NH-50 leading to Nashik and NH-9

connecting to Sholapur and Hyderabad. As the names of these transportation corridors suggest,

Pune is well connected through a network of national highways to major cities including

Mumbai (163 km), Nashik (202 km), Nagpur (880 km), Bangalore (835 km), Chennai (1,166

km) and Hyderabad (548 km). State Highways connect Pune to smaller prominent centers in

vicinity. Key State Highways are SH-60 (Pune–Ahmednagar), SH-64 (Pune–Saswad) and SH-57

(Pune–Pirangut).

Rail Connectivity

The city of Pune has four major train stations: Pune Junction, Shivajinagar Station, Pimpri and

Chinchwad. Pune Junction is a major rail node where a majority of trains halt to connect

passengers by broad gauge line to Mumbai, Bangalore, Chennai, Hyderabad and Delhi. In

addition, Pune suburban trains also run from Pune Junction to the industrial towns of Khadki,

Pimpri and Chinchwad.

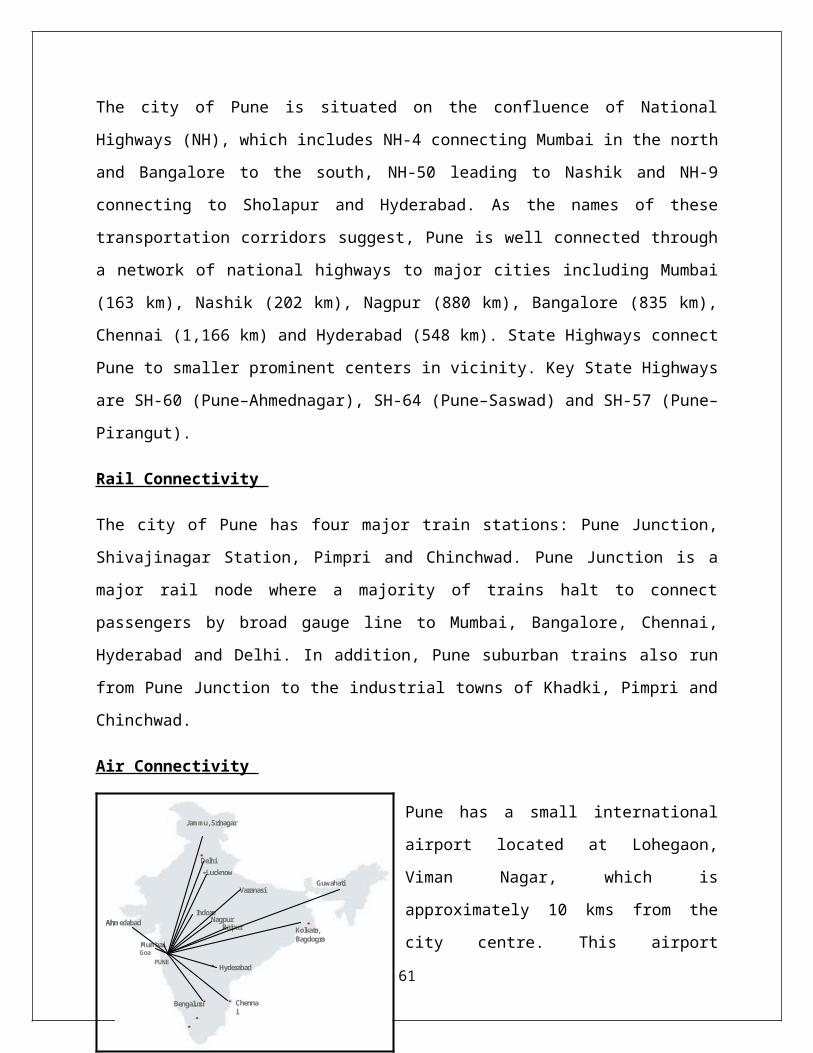

Air Connectivity

Pune has a small international airport located at

Lohegaon, Viman Nagar, which is

approximately 10 kms from the city centre. This

airport provides domestic connectivity to major

metros including New Delhi, Mumbai,

Bangalore, Kolkata, Chennai and Hyderabad, as

well as to other cities within India. More than 50

daily flights connect Pune to the rest of the

country. In addition to this, Pune International

Airport also provides air connectivity to foreign

destinations including Dubai and Frankfurt.

Economic Base and Economic Activities

While the city is reputed for its educational institutions, Pune’s economic base has traditionally

been anchored by the strong presence of the engineering and automobile sectors. Economic

45

Jammu, Srinagar

Delhi

Kolkata, Bagdogra

Mumbai

PUNEHyderabad

Chennai

Bengaluru

Nagpur

Goa

Indore

RaipurAhmedabad

Lucknow

VaranasiGuwahati

Jammu, Srinagar

Delhi

Kolkata, Bagdogra

Mumbai

PUNEHyderabad

Chennai

Bengaluru

Nagpur

Goa

Indore

RaipurAhmedabad

Lucknow

VaranasiGuwahati

activity in the city is rooted by the presence of corporate giants like Bajaj, TELCO, Fiat, General

Motors and Bharat Forge. Over the years, this has helped consolidate Pune's position as the

'Detroit of India'.

In recent times, Pune has emerged as a preferred IT destination in India. Major IT domestic and

international players including Infosys, Wipro, TCS and Syntel have set up operations in Pune

and are increasing business at a significant pace.

Prominent IT/ITeS Destination

Pune was one of the prominent cities in India to capitalize on the IT / ITeS boom that started in

late 1990s, and it has continued to remain on the forefront of this industry. Progressive state

government policies and efforts by the Maharashtra Industrial Corporation (MIDC) in creating

enclaves at Hinjewadi, Kharadi and Talawade have been successful in making land and other

required infrastructure available to domestic and multi-national companies for setting up their

office campuses in Pune.

Today Pune has a large and thriving IT/ITeS industry with major domestic software players such

as TCS, Wipro, Infosys, Mahindra British Telecom, Mastek and PCS having established their

base in the city. Major global players such as HSBC Global Technology, Sakaen, Avayay, T-

Systems, Syntel, Cognizant, IBM and EDS also have also a significant presence in the city.

The IT / ITeS industry has established itself in Pune along two broad locations:

North-Western Corridor comprising primarily the Hinjewadi region. This region

primarily houses the campus style development of major IT players like Infosys, Wipro,

TCS, Cognizant, KPIT, Persistent Systems. Also it houses a majority of Pune’s existing

and upcoming IT SEZ by major developers including DLF, Paranjape, Embassy Group,

Kumar Builders and Ascendas.

Eastern Corridor comprising areas such as Kalyani Nagar, Yerwada, Viman Nagar,

Kharadi, Hadapsar and Fursungi. This region houses some of the most prominent existing

and upcoming IT parks in the city with the likes of Magarpatta Cybercity, K Raheja’s

46

Commerzone, Vascon’s Weikfield IT Park, Kumar Builder’s Cerebrum IT Park and

Panchsil’s Tech Park.

Automotive hub

The growth story of Pune as a major automobile hub can be dated back to 1965 with the

establishment of commercial motor vehicle units of Telco in Pimpri-Chinchwad. Later the city

also witnessed the entry of auto majors such as Tata Motors and Bajaj Auto. This resulted in

setting up of numerous auto ancillary industries that catered to the outsourcing requirements of

these automobile manufacturers. Today, Pune is home to major automotive companies ranging

from two-wheelers and auto rickshaws (Bajaj Auto, Kinetic Motor Company) to cars

(Volkswagen, General Motors, Tata Motors, Mercedes-Benz), tractors (John Deere), tempos,

excavators (JCB) and trucks (Force Motors). Most of these industries are located in the suburban

areas of Pimpri-Chinchwad, Chakan and Talegaon.

Engineering industry

One of the first major industries to be set up in Pune was Kirloskar Oil Engines Limited during

the 1960’s in Pimpri Chinchwad. MIDC set up a large industrial estate on 4,000 acres of land at

Bhosari. This development led to a spate of engineering ancillary industries being set up in

Pimpri-Chinchwad which further spurred the economic and physical development of this region.

The major engineering goods manufactured in Pune essentially include forges (Bharat Forge),

truck transmissions systems, clutches & hydraulic components (Eaton Corporation) and engines

(Kirloskar Oil Engines, Cummins). Other major notable engineering goods manufacturers in

Pune are Alfa Laval, Thyssen Krupp, Black & Veatch and Saint-Gobain Sekurit (automotive

safety glass). In addition to these large players, many small and medium-sized companies are

also active in Pune, producing components for larger companies and creating unique components

for the Indian marketplace. Electronic goods and consumer durables are also manufactured in

and around Pune. Key companies from this segment which have operations in Pune include

National Panasonic, Whirlpool Corporation and the LG Group, located in the Ranjangaon

industrial area in Eastern Pune. Food giants like Frito Lay and Coca Cola also have food

processing plants located in Pune.

Pune Residential Sector Overview

47

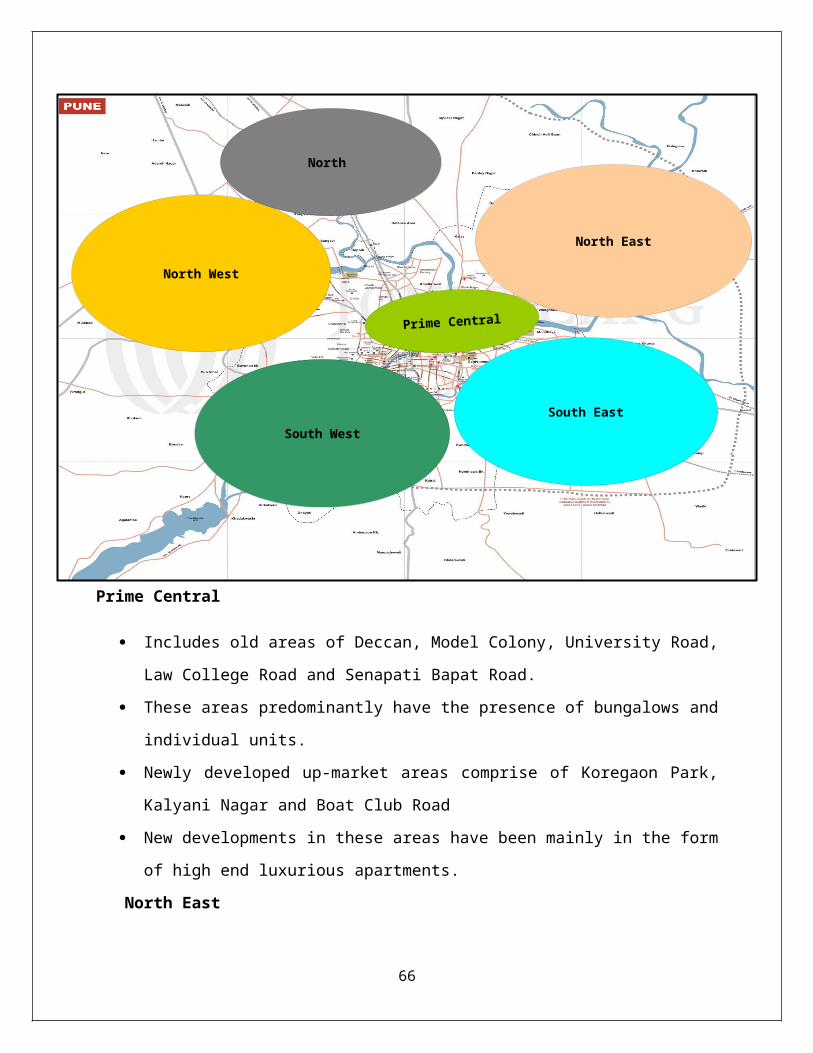

Prime Central

North West

South West

North East

South East

North

Residential Micro Market description

Prime Central

Includes old areas of Deccan, Model Colony, University Road, Law College Road and

Senapati Bapat Road.

These areas predominantly have the presence of bungalows and individual units.

Newly developed up-market areas comprise of Koregaon Park, Kalyani Nagar and Boat

Club Road

New developments in these areas have been mainly in the form of high end luxurious

apartments.

North East

48

Includes areas of Viman Nagar, Wadgaon Sheri, Nagar Road, Kharadi, Vishrantwadi,

Mundhwa and Wagholi

One of recently developed residential areas in Pune.

Development in this area can be primarily attributed to massive growth in IT/ITeS sector

on Nagar Road stretch including areas of Kharadi, Viman Nagar, Yerwada and Kalyani

Nagar.

Moreover proximity of this region to the Pune’s Airport at Lohegaon and central areas

has also contributed to the growth of this region.

Today it is one of the most vibrant regions in the city in terms of real estate development,

primarily in commercial (IT/ITES), retail and hospitality.

South East

This micro-market comprises two major residential catchments: the entire Magarpatta

Road along with Hadapsar, Manjri and Fursungi and other one including Wanowrie,

Salunke Vihar, NIBM Road along with Undri, Kondwa and Mohammedwadi.

The IT development within Magarpatta Township, together with the industrial units in

Hadapsar, primarily drives the residential demand along Magarpatta Road and Hadapsar.

With Wanowrie, Salunke Vihar Road and NIBM Road almost saturated, the focus has

shifted to Undri, Kondwa and Mohammedwadi. The working population in the CBD and

Magarpatta generally resides in this residential pocket within this micro-market.

North West

Includes the areas of Aundh, Baner, Balewadi, Bavdhan, Wakad, Pimple Saudagar,

Pimple Nilkah and Pimple Gaurav and Hinjewadi.

Initially better connectivity of certain areas like Aundh, Baner and Balewadi with the

Mumbai-Pune Expressway and presence of industrial units in Northern Pune led to

residential developments in early 1990’s.

Over the last decade, particularly in the later half of 2000, areas such as Wakad, Pimple

Saudagar, Pimple Nilakh and Pimple Gaurav have emerged as hub of affordable housing

category due to large availability of land parcels and their proximity to Hinjewadi IT

Park.

South West

49

Fig 2.2a New Launches & Absorption

0

5,000

10,000

15,000

20,000

25,000

30,000

2005 2006 2007 1H 08 3Q08-1Q09 2Q09-4Q09 1Q10-3Q10Year

Uni

ts

New Launches Absorption

Includes the areas of Kothrud, Warje, Karve Road, Katraj, Sinhagad Road.

This region in Pune as predominantly been a residential area with negligible commercial

developments.

The region also comprises shopping centers, restaurants and high-density residential

housing complexes.

This area houses some of the major educational institutes in the city and its proximity to

the city centre with good connectivity also adds to its advantage.

North

The North micro-market comprises Pimpri, Chinchwad, Akrudi, Bhosari and Chakan,

Ravet, Alandi and Nigdi. It is one of the cheapest micro-markets in the city.

This region has a thriving industrial belt comprising mainly of engineering and

automobile industries. As land pressure in the city has risen, this industrial hub is

gradually being transformed into a residential area.

Its proximity to Hinjewadi IT Park and to establishments of industrial units in Chakan

and Bhosari drives the residential demand in this precinct.

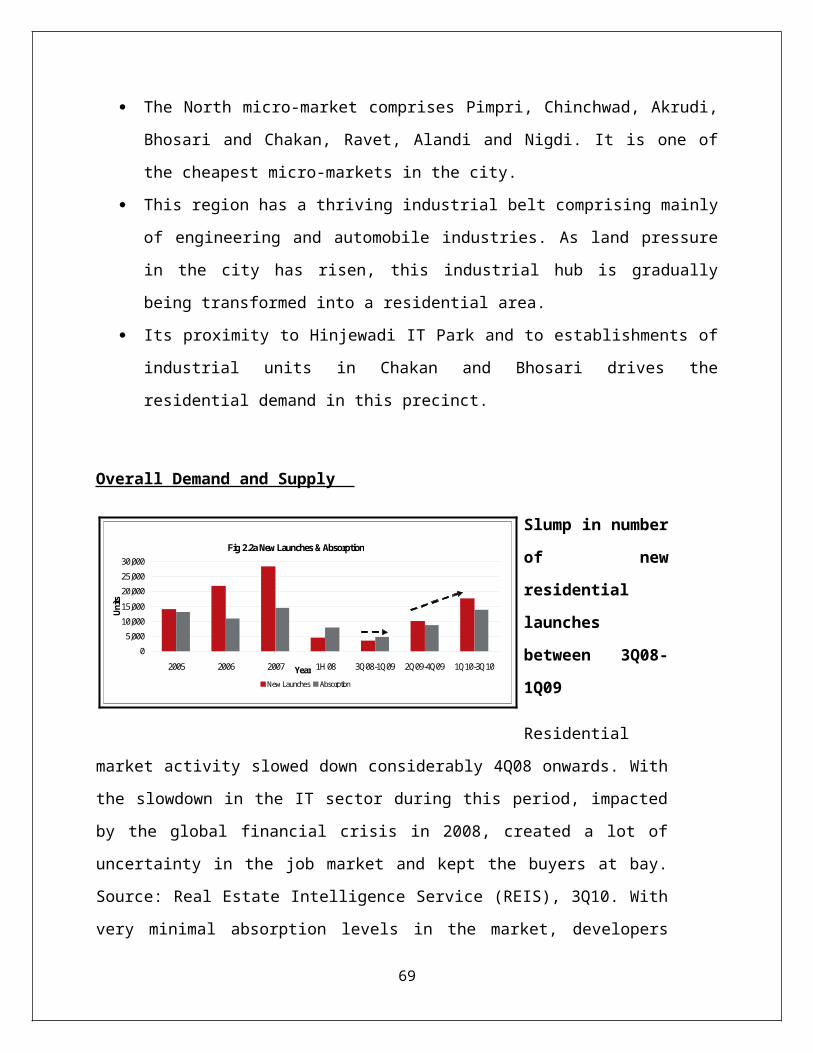

Overall Demand and Supply

Slump in number of

new residential

launches between

3Q08-1Q09

Residential market

activity slowed down

considerably 4Q08

onwards. With the slowdown in the IT sector during this period, impacted by the global

financial crisis in 2008, created a lot of uncertainty in the job market and kept the buyers

at bay. Source: Real Estate Intelligence Service (REIS), 3Q10. With very minimal

absorption levels in the market, developers had to delay the launch of their projects. As a

result only 2,355 new residential units were launched in 2H08 out of the total 6,900 units

50

launched during 2008 and only 1,142 units got launched in 1Q09 out of the total 11,214

units launched in 2009.

Developers focus on the affordable category housing led to gradual revival of

residential sector in 2009.

Developers primarily focused on affordable housing launches in 2009, both in terms of

specifications and capital values, which played a pivotal role in improving the overall

demand for housing sector in the city. Capitalizing on lower capital values and improved

demand in first few quarters of 2009, Pune witnessed a huge supply of 11,214 units during

the year compared to just 6,900 units in year 2008.

Steady recovery of the residential sector since 2H09. Residential affordability increased in

2009, primarily due to rational mortgage rates and reduced residential prices. Several banks

lowered the home loan rates from 12-13% in 2008 to 8.5-9% in 2009. Moreover the average

capital values in the city fell about 10-25% from their peak values of 2Q08. The confluence

of price correction and lowered mortgage rates led to a rise in affordability of buyers. Also

developers’ focus primarily on the affordable housing segment throughout the year 2009

played a pivotal role in improving the overall demand for housing sector in the city. The

average quarterly absorption which was recorded at approximately 2,000 units between the

period 2Q08-2Q09 had almost doubled and stood at approximately 4,000 units over the last

one year since 3Q09, clearly indicating the improved sentiments among the buyer as well as

the investor communities. With the improving economic conditions as evident from the

increased absorption of office space in the year 2010, the employment security has also

strengthened resulting in increased absorption levels in year 2010. As compared to 10,187

units absorbed in 2009, the first three quarters of 2010 alone has witnessed absorption of

approximately 13,900 units.

Residential micro market description:

Pune has a vast land bank.

It can be divided into 6(Six) micro markets, such as:

51

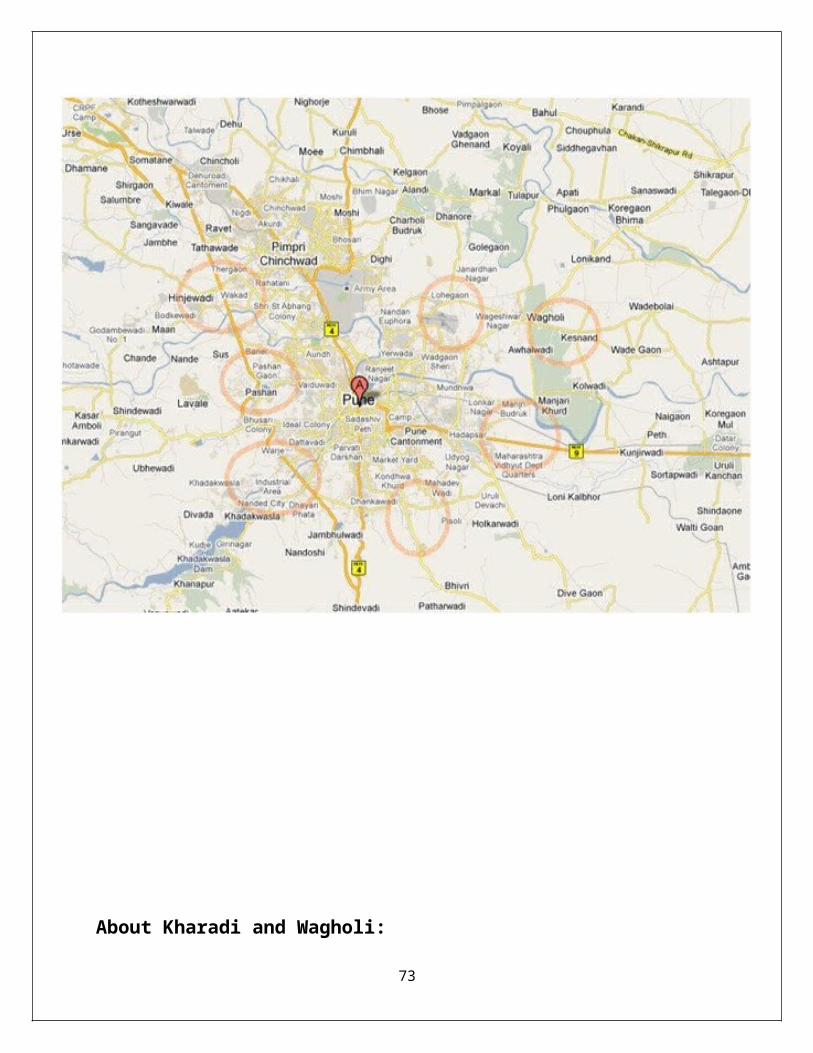

1. Kharadi and Wagholi

2. Hadapsar and Handewadi

3. Undri, NIBM and Kondhwa

4. Katarj, Ambegaon, Sinhagad road, kothrud and Warje

5. Bhavdhan, Pashan, Baner, Balewadi and Aundh

6. Wakad and Hinjewadi.

Pune residential sector overview:

52

About Kharadi and Wagholi:

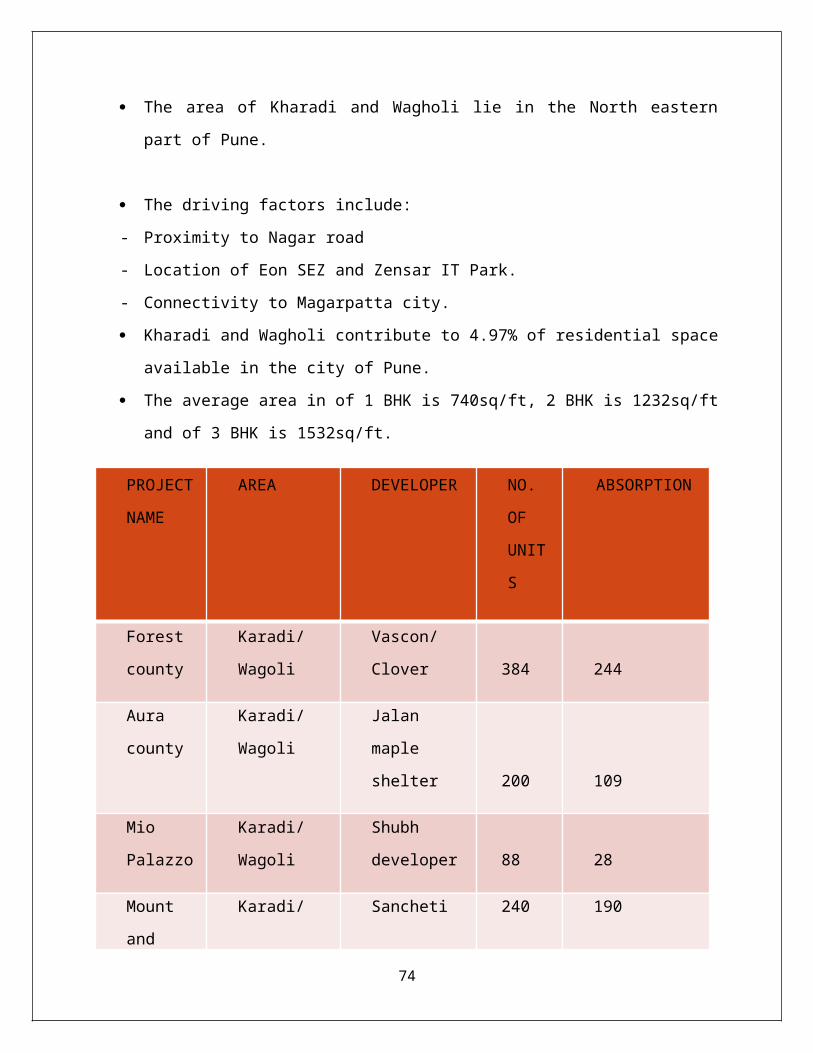

The area of Kharadi and Wagholi lie in the North eastern part of Pune.

53

The driving factors include:

- Proximity to Nagar road

- Location of Eon SEZ and Zensar IT Park.

- Connectivity to Magarpatta city.

Kharadi and Wagholi contribute to 4.97% of residential space available in the city of

Pune.

The average area in of 1 BHK is 740sq/ft, 2 BHK is 1232sq/ft and of 3 BHK is 1532sq/ft.

PROJECT

NAME

AREA DEVELOPER NO.

OF

UNITS

ABSORPTION

Forest

county

Karadi/Wagoli Vascon/Clover

384 244

Aura

county

Karadi/Wagoli Jalan maple

shelter 200 109

Mio

Palazzo

Karadi/Wagoli Shubh

developer 88 28

Mount and

glory

Karadi/Wagoli Sancheti

developer 240 190

Renaissant Karadi/Wagoli Alcon 264 162

Ozone Karadi/Wagoli Raviraj Group 120 68

Tuscan

Estate

Karadi/Wagoli Kolte Patil

group 48 36

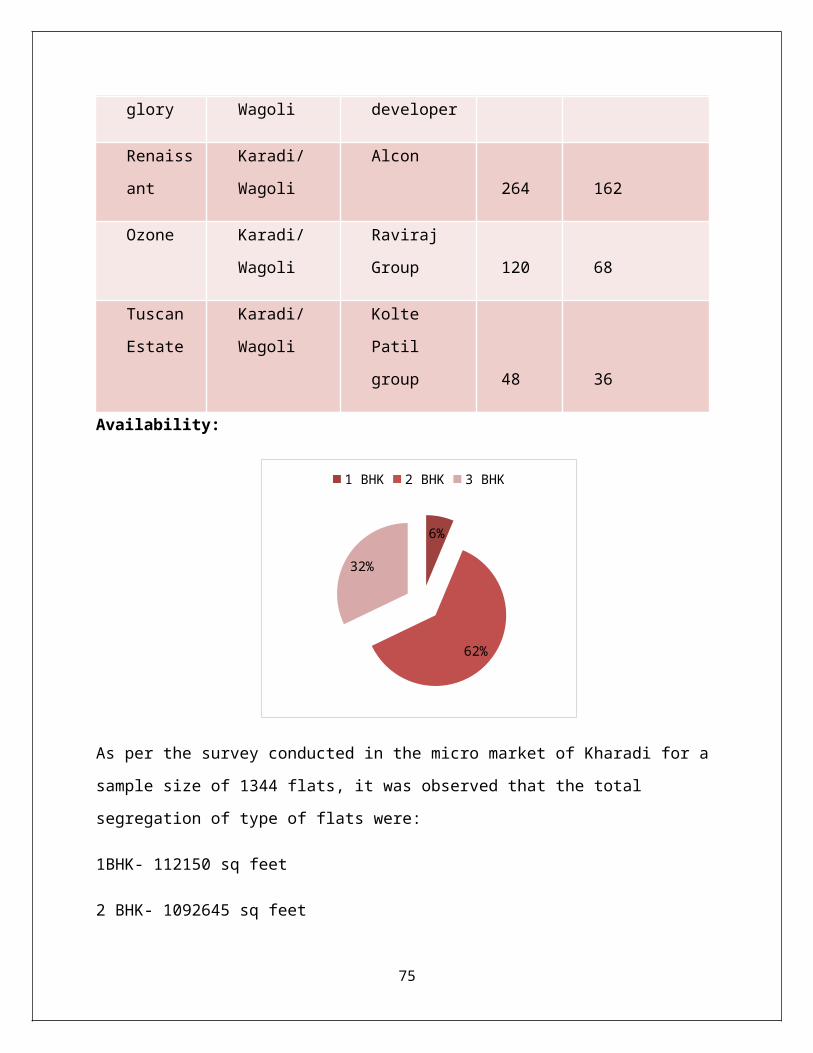

Availability:

54

6%

62%

32%

1 BHK 2 BHK 3 BHK

As per the survey conducted in the micro market of Kharadi for a sample size of 1344 flats, it

was observed that the total segregation of type of flats were:

1BHK- 112150 sq feet

2 BHK- 1092645 sq feet

3 BHK- 569990 sq feet

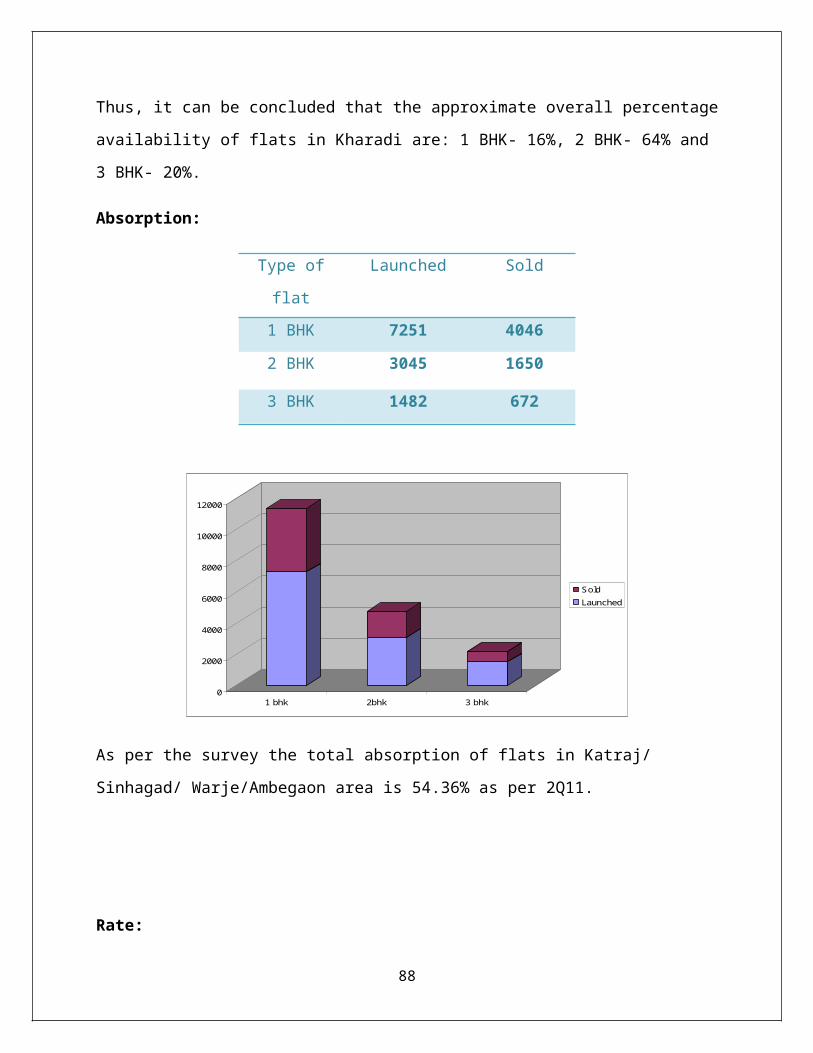

Thus, it can be concluded that the approximate overall percentage availability of flats in Kharadi

are: 1 BHK- 6%, 2 BHK- 62% and 3 BHK- 32%.

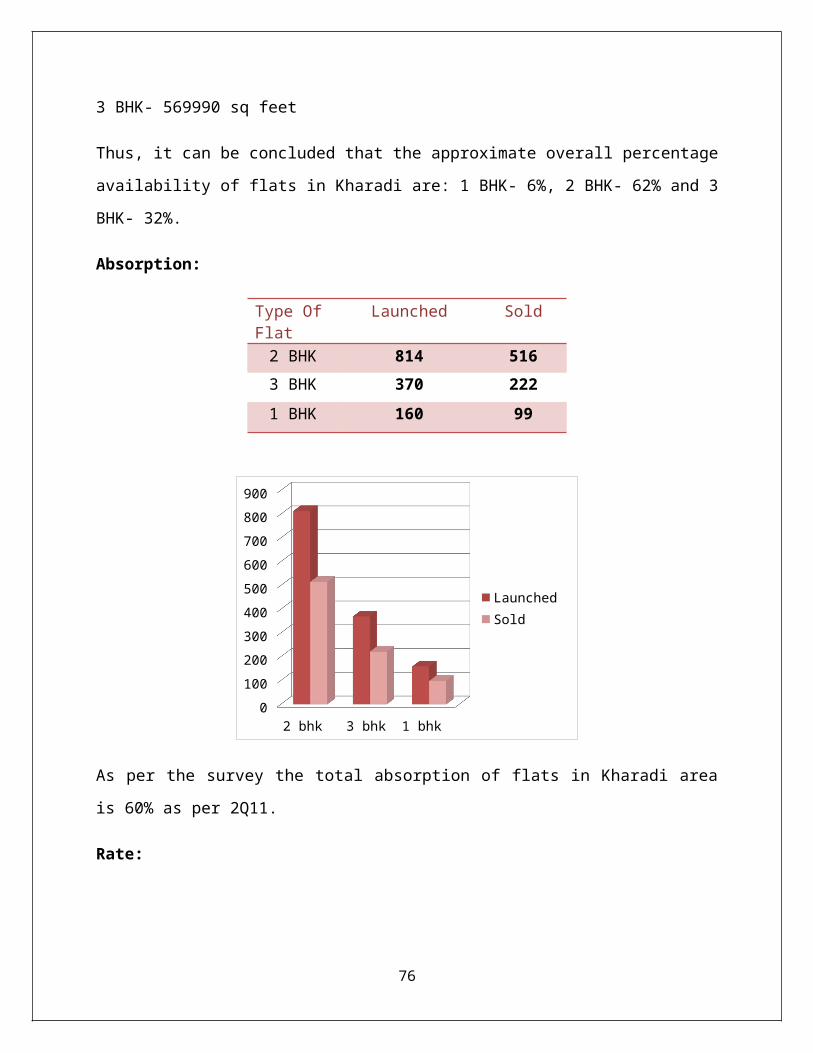

Absorption:

Type Of Flat

Launched Sold

2 BHK 814 516

3 BHK 370 222

1 BHK 160 99

55

2 bhk 3 bhk 1 bhk 0

100

200

300

400

500

600

700

800

900

Launched Sold

As per the survey the total absorption of flats in Kharadi area is 60% as per 2Q11.

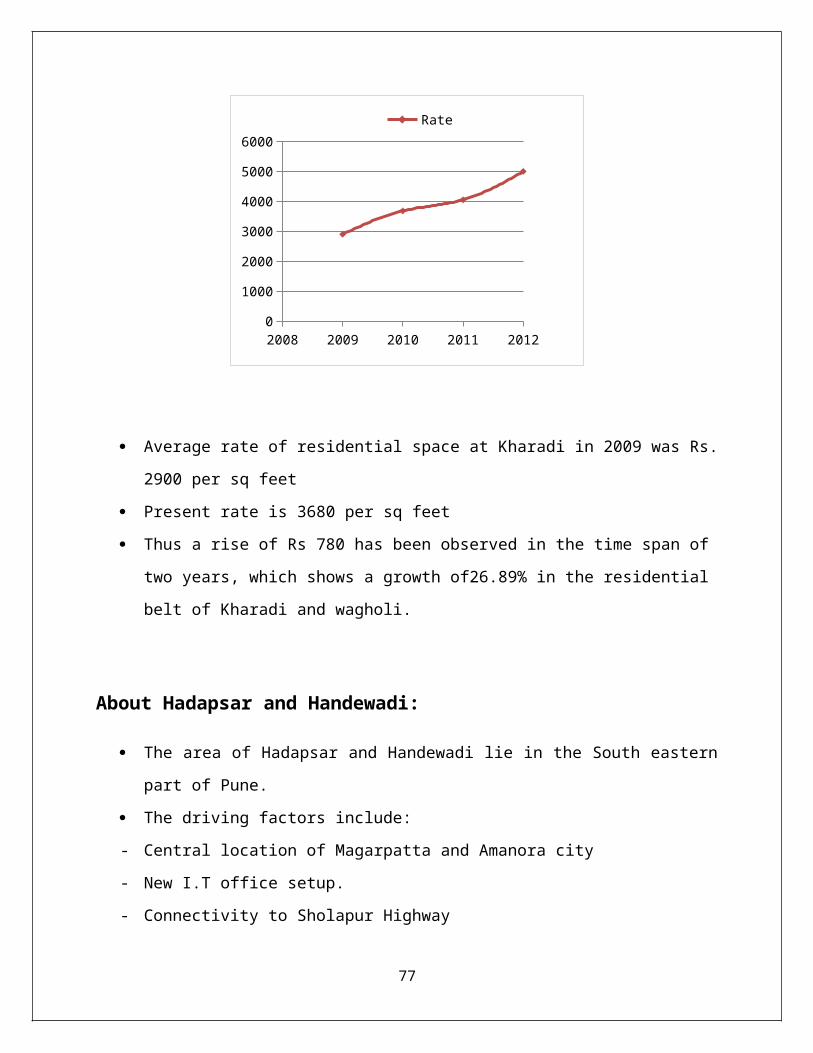

Rate:

2008 2009 2010 2011 20120

1000

2000

3000

4000

5000

6000

Rate

Average rate of residential space at Kharadi in 2009 was Rs. 2900 per sq feet

Present rate is 3680 per sq feet

Thus a rise of Rs 780 has been observed in the time span of two years, which shows a

growth of26.89% in the residential belt of Kharadi and wagholi.

56

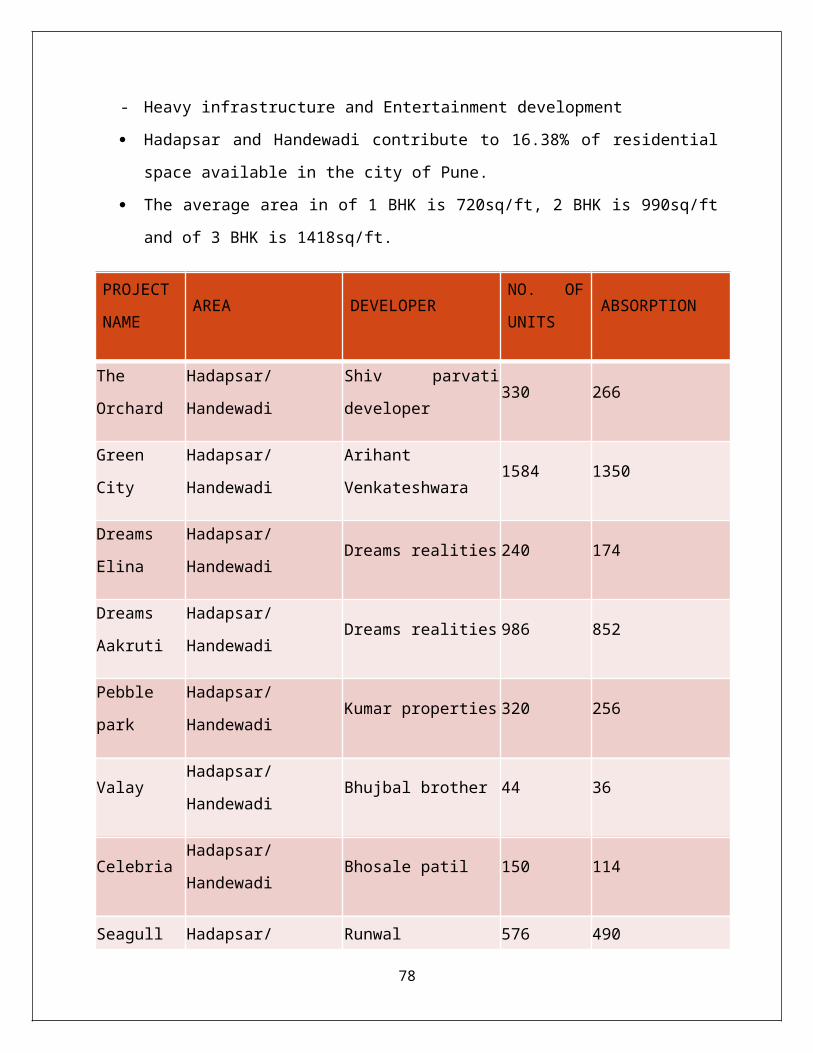

About Hadapsar and Handewadi:

The area of Hadapsar and Handewadi lie in the South eastern part of Pune.

The driving factors include:

- Central location of Magarpatta and Amanora city

- New I.T office setup.

- Connectivity to Sholapur Highway

- Heavy infrastructure and Entertainment development

Hadapsar and Handewadi contribute to 16.38% of residential space available in the city

of Pune.

The average area in of 1 BHK is 720sq/ft, 2 BHK is 990sq/ft and of 3 BHK is 1418sq/ft.

PROJECT

NAMEAREA DEVELOPER

NO. OF

UNITS ABSORPTION

The Orchard Hadapsar/Handewadi Shiv parvati developer 330 266

Green City Hadapsar/Handewadi Arihant Venkateshwara 1584 1350

Dreams Elina Hadapsar/Handewadi Dreams realities 240 174

Dreams

AakrutiHadapsar/Handewadi Dreams realities 986 852

Pebble park Hadapsar/Handewadi Kumar properties 320 256

Valay Hadapsar/Handewadi Bhujbal brother 44 36

Celebria Hadapsar/Handewadi Bhosale patil 150 114

Seagull Hadapsar/Handewadi Runwal 576 490

Availability:

57

18%

75%

6%

1 bhk 2 bhk 3 bhk

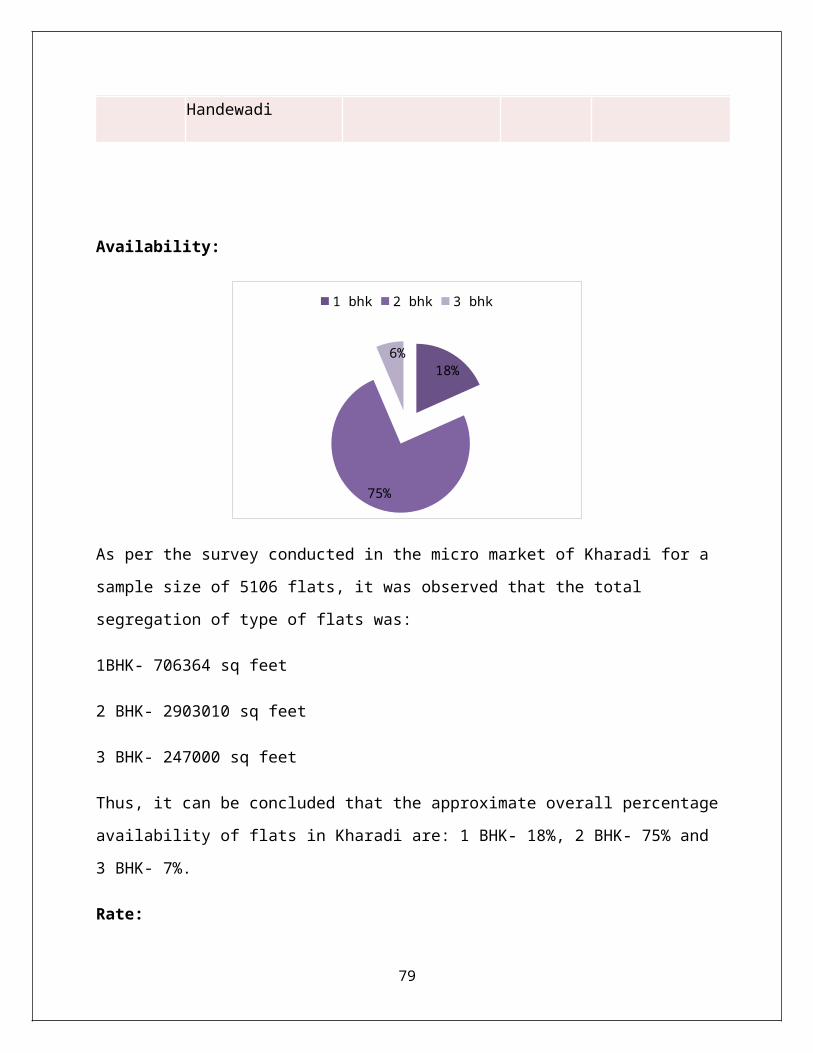

As per the survey conducted in the micro market of Kharadi for a sample size of 5106 flats, it

was observed that the total segregation of type of flats was:

1BHK- 706364 sq feet

2 BHK- 2903010 sq feet

3 BHK- 247000 sq feet

Thus, it can be concluded that the approximate overall percentage availability of flats in Kharadi

are: 1 BHK- 18%, 2 BHK- 75% and 3 BHK- 7%.

Rate:

2006 2008 2010 2012 20140

500

1000

1500

2000

2500

3000

3500

4000

Rate

58

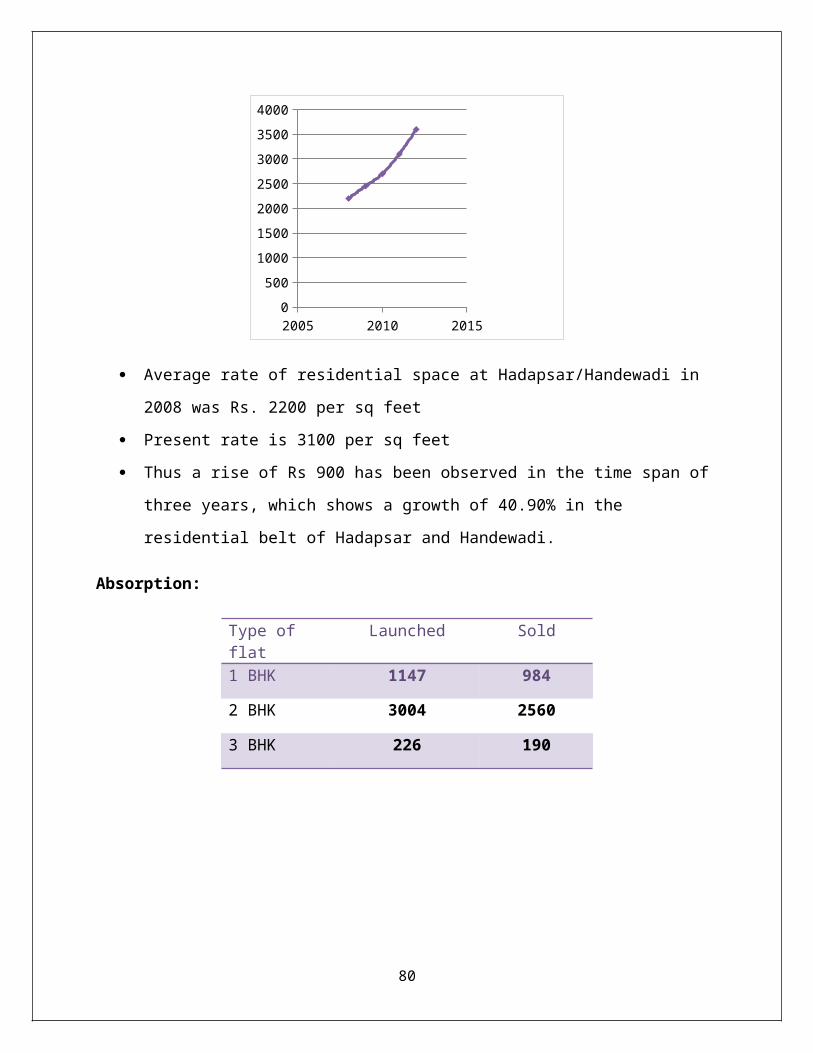

Average rate of residential space at Hadapsar/Handewadi in 2008 was Rs. 2200 per sq

feet

Present rate is 3100 per sq feet

Thus a rise of Rs 900 has been observed in the time span of three years, which shows a

growth of 40.90% in the residential belt of Hadapsar and Handewadi.

Absorption:

Type of flat Launched Sold

1 BHK 1147 984

2 BHK 3004 2560

3 BHK 226 190

1 bhk 2bhk 3 bhk0

1000

2000

3000

4000

5000

6000

SoldLaunched

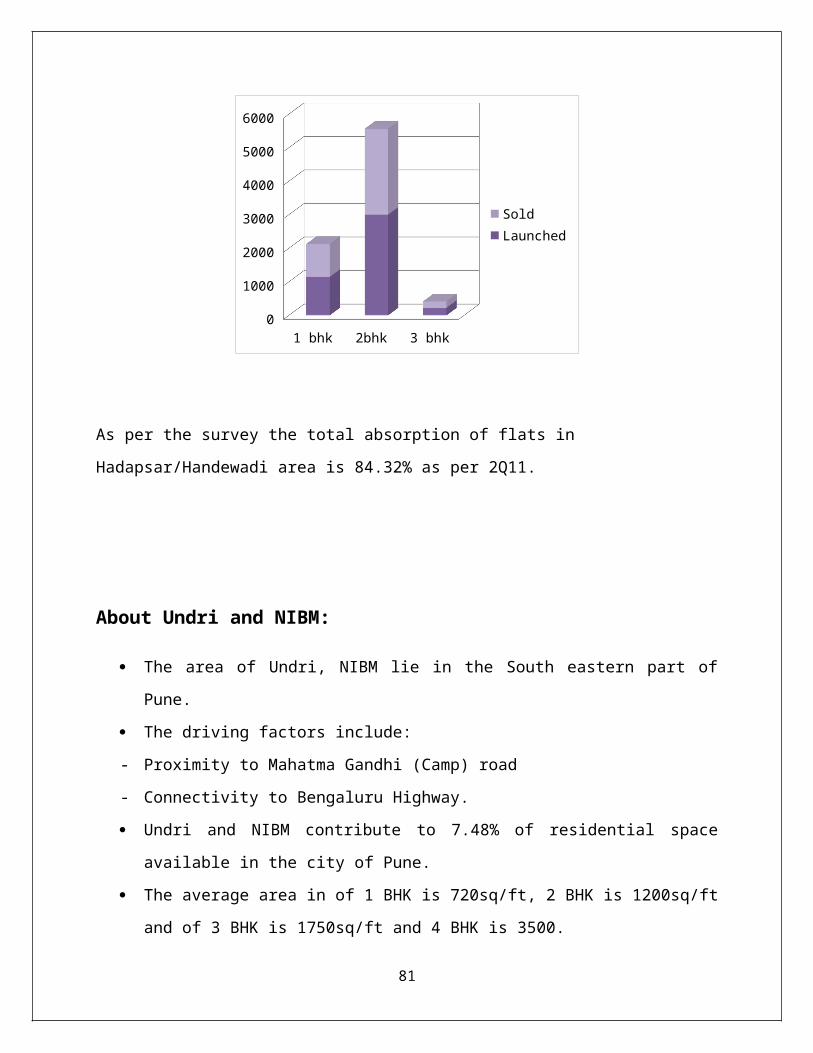

As per the survey the total absorption of flats in Hadapsar/Handewadi area is 84.32% as per

2Q11.

59

About Undri and NIBM:

The area of Undri, NIBM lie in the South eastern part of Pune.

The driving factors include:

- Proximity to Mahatma Gandhi (Camp) road

- Connectivity to Bengaluru Highway.

Undri and NIBM contribute to 7.48% of residential space available in the city of Pune.

The average area in of 1 BHK is 720sq/ft, 2 BHK is 1200sq/ft and of 3 BHK is 1750sq/ft

and 4 BHK is 3500.

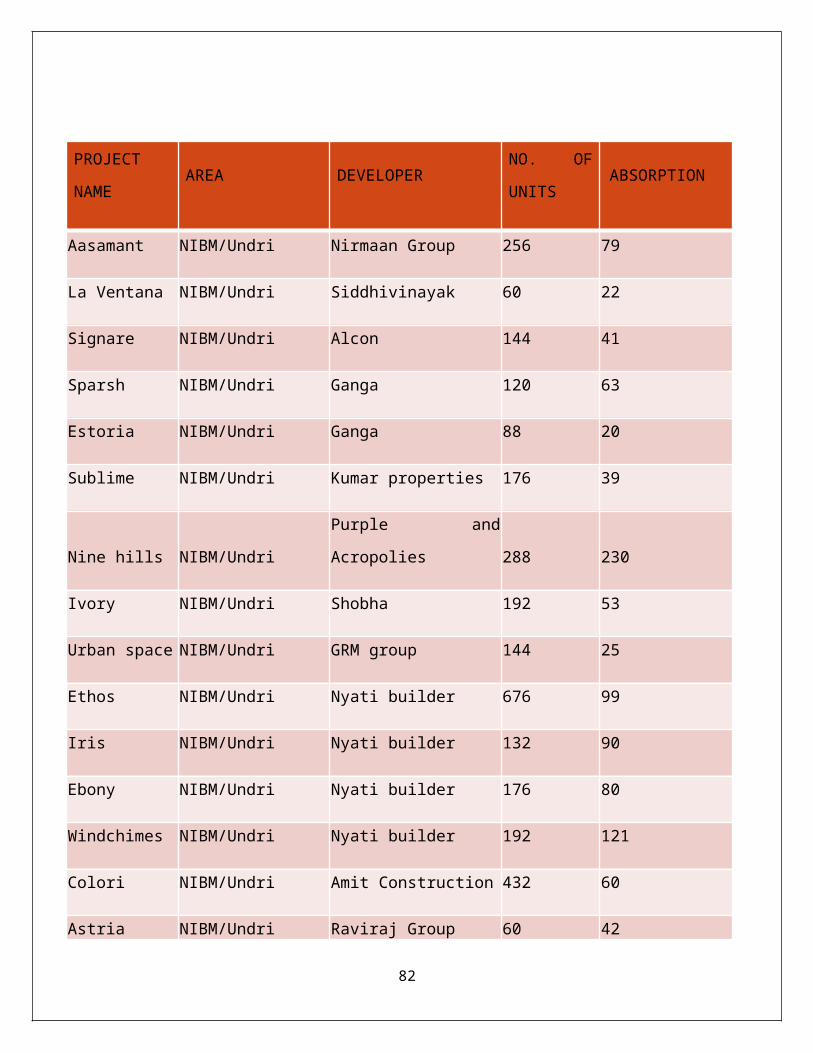

PROJECT

NAMEAREA DEVELOPER

NO. OF

UNITS ABSORPTION

Aasamant NIBM/Undri Nirmaan Group 256 79

La Ventana NIBM/Undri Siddhivinayak 60 22

Signare NIBM/Undri Alcon 144 41

Sparsh NIBM/Undri Ganga 120 63

Estoria NIBM/Undri Ganga 88 20

Sublime NIBM/Undri Kumar properties 176 39

Nine hills NIBM/Undri Purple and Acropolies 288 230

Ivory NIBM/Undri Shobha 192 53

Urban space NIBM/Undri GRM group 144 25

Ethos NIBM/Undri Nyati builder 676 99

Iris NIBM/Undri Nyati builder 132 90

Ebony NIBM/Undri Nyati builder 176 80

60

Windchimes NIBM/Undri Nyati builder 192 121

Colori NIBM/Undri Amit Construction 432 60

Astria NIBM/Undri Raviraj Group 60 42

Sangria NIBM/Undri Marvel and ganga 668 420

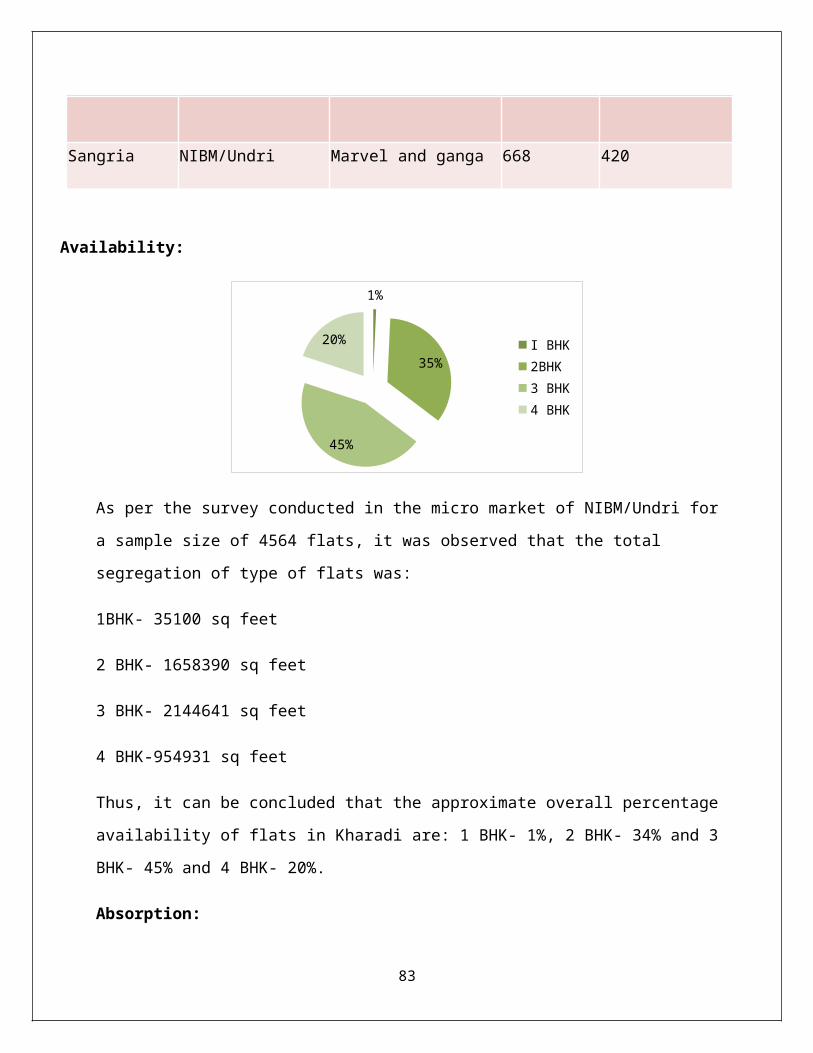

Availability:

1%

35%

45%

20%I BHK2BHK3 BHK4 BHK

As per the survey conducted in the micro market of NIBM/Undri for a sample size of 4564 flats,

it was observed that the total segregation of type of flats was:

1BHK- 35100 sq feet

2 BHK- 1658390 sq feet

3 BHK- 2144641 sq feet

4 BHK-954931 sq feet

Thus, it can be concluded that the approximate overall percentage availability of flats in Kharadi

are: 1 BHK- 1%, 2 BHK- 34% and 3 BHK- 45% and 4 BHK- 20%.

Absorption:

61

Type of flat Launched Sold

1 BHK 1147 984

2 BHK 1106 605

3 BHK 929 430

4 BHK 264 224

1 bhk 2bhk 3 bhk 4 Bhk

0

500

1000

1500

2000

2500

SoldLaunched

As per the survey the total absorption of flats in NIBM/Undri area is 84.32% as per 2Q11.

Rate:

20062007

20082009

20102011

20122013

0500

100015002000250030003500400045005000

Rate

Average rate of residential space at NIBM/Undri in 2008 was Rs 2600 per sq feet

Present average rate is 3840 per sq feet

Thus a rise of Rs 1240 has been observed in the time span of three years, which shows a

growth of 47.96% in the residential belt of NIBM/Undri.

62

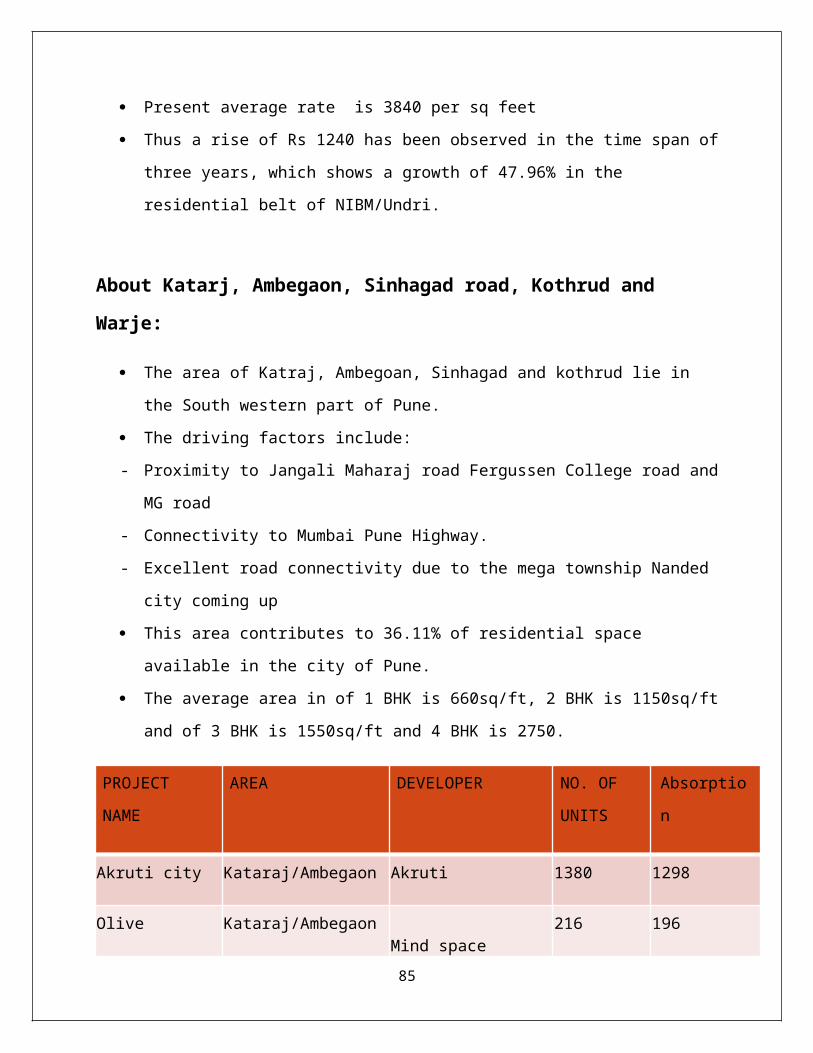

About Katarj, Ambegaon, Sinhagad road, Kothrud and Warje:

The area of Katraj, Ambegoan, Sinhagad and kothrud lie in the South western part of

Pune.

The driving factors include:

- Proximity to Jangali Maharaj road Fergussen College road and MG road

- Connectivity to Mumbai Pune Highway.

- Excellent road connectivity due to the mega township Nanded city coming up

This area contributes to 36.11% of residential space available in the city of Pune.

The average area in of 1 BHK is 660sq/ft, 2 BHK is 1150sq/ft and of 3 BHK is 1550sq/ft

and 4 BHK is 2750.

PROJECT

NAME

AREA DEVELOPER NO. OF

UNITS

Absorption

Akruti city Kataraj/Ambegaon Akruti 1380 1298

Olive Kataraj/Ambegaon Mind space reality 216 196

Lake Vista Kataraj/Ambegaon

shree Venkatesh

buildcon 200 76

Garden View Kataraj/Ambegaon Tyagi/mittals/trimurti 704 690

Eros Kataraj/Ambegaon Paramount 264 262

Bloomfield Kataraj/Ambegaon Amit Construction 466 319

Kalpataru Sihagard/Warje Rajlaxmi 162 95

Samarth Puram Sihagard/Warje Shree Saarth builders 60 27

63

Vasant vihar Sihagard/Warje Savitri developer 116 46

Oakwood County Sihagard/Warje Darode Jog 168 162

Amrutvel Sihagard/Warje Laxmi builders 152

Arcdia Sihagard/Warje Balark developers 188 30

Miami Sihagard/Warje Majestique 224 31

Amrut Ganga Sihagard/Warje Goelganga 168 142

Ganga Bhagyoday Sihagard/Warje Goel ganga 132 68

Nanded City Sihagard/Warje Magarpatta City 5160 2874

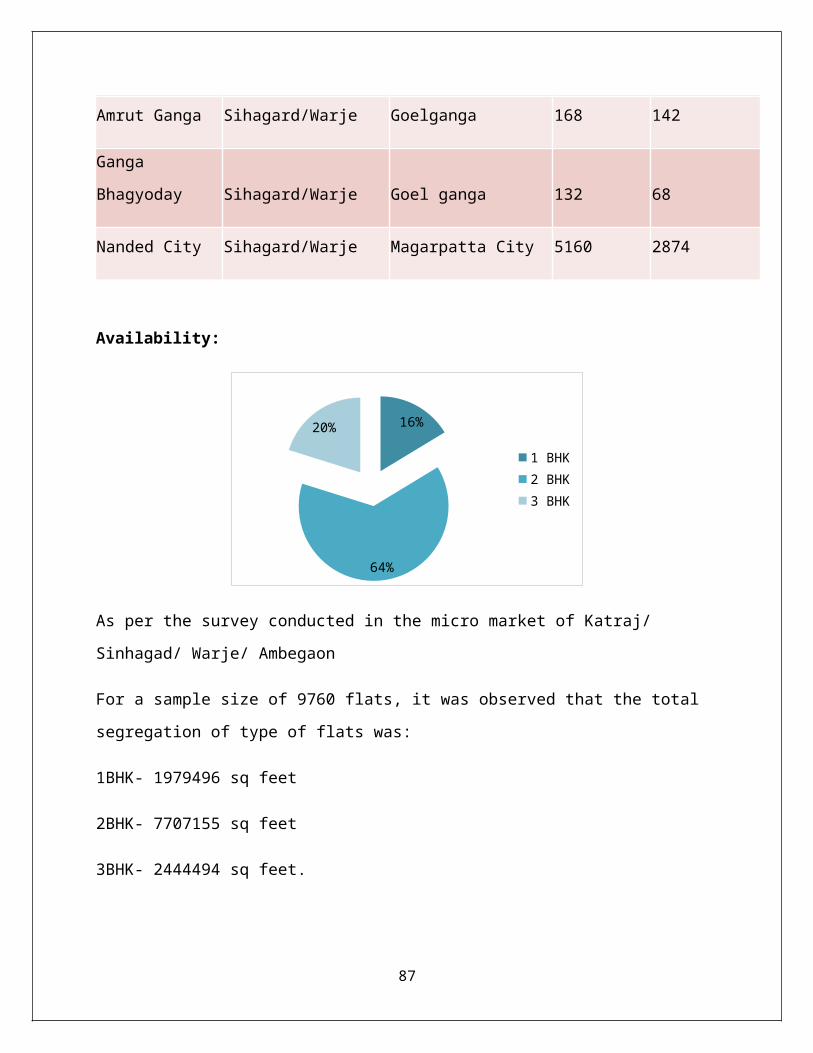

Availability:

16%

64%

20%

1 BHK2 BHK3 BHK

As per the survey conducted in the micro market of Katraj/ Sinhagad/ Warje/ Ambegaon

For a sample size of 9760 flats, it was observed that the total segregation of type of flats was:

1BHK- 1979496 sq feet

64

2BHK- 7707155 sq feet

3BHK- 2444494 sq feet.

Thus, it can be concluded that the approximate overall percentage availability of flats in Kharadi

are: 1 BHK- 16%, 2 BHK- 64% and 3 BHK- 20%.

Absorption:

Type of flat Launched Sold

1 BHK 7251 4046

2 BHK 3045 1650

3 BHK 1482 672

0

2000

4000

6000

8000

10000

12000

1 bhk 2bhk 3 bhk

Sold

Launched

As per the survey the total absorption of flats in Katraj/ Sinhagad/ Warje/Ambegaon area is

54.36% as per 2Q11.

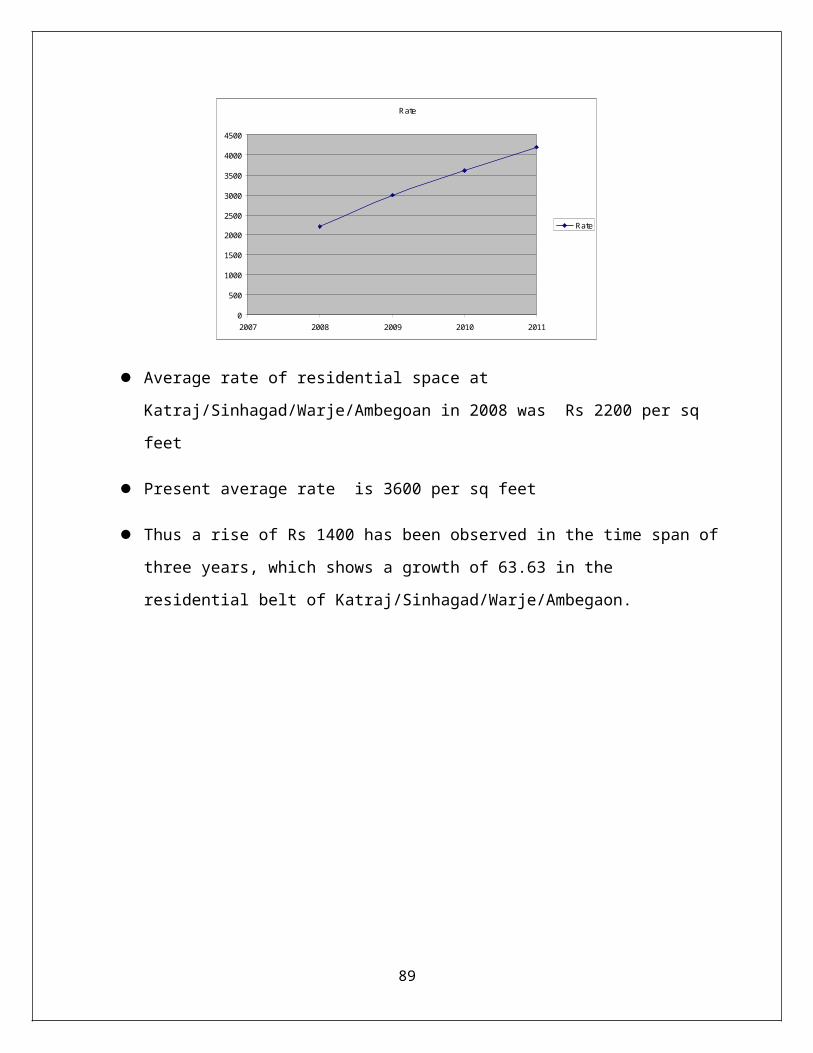

Rate:

65

Rate

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2007 2008 2009 2010 2011

Rate

Average rate of residential space at Katraj/Sinhagad/Warje/Ambegoan in 2008 was Rs

2200 per sq feet

Present average rate is 3600 per sq feet

Thus a rise of Rs 1400 has been observed in the time span of three years, which shows a

growth of 63.63 in the residential belt of Katraj/Sinhagad/Warje/Ambegaon.

About Bhavdhan, Pashan, Baner, Balewadi and Aundh:

66

The area of Bhavdhan, Pashan, Baner and Aundh lie in the North western part of Pune.

The driving factors include:

- Proximity to Hinjewadi IT park road

- Connectivity to Mumbai-Pune Highway.

- Good planned area

- Centrally located between Pune central and Hinjewadi

It contributes to 73.45% of residential space available in the city of Pune.

The average area in of 1 BHK is 620sq/ft, 2 BHK is 1250sq/ft and of 3 BHK is 1650sq/ft

and 4 BHK is 2500.

PROJECT NAME

AREA DEVELOPER NO. OF UNITS ABSORPTION

Skyi Irish Bhavdhan Skyi developer 86 30

Zinnea Bhavdhan Surana Associates 129 114

Pebbles Bhavdhan Rainbow group 188 94

Rohan Ishan Bhavdhan Rohan Builder 63 59

Eva Bhavdhan Anshul Realties 60 51

Dreams Belle Vue Bhavdhan Dreams realities 96 98

Esplanade Bhavdhan Nyati builder 253 210

Viva hallmark BhavdhanVivaswaraj developers 330 192

Orvi Balewadi Sai Samruddhi 96 82

Crest Avenu Balewadi Kiriti developer 96 38

Vatika Balewadi Bhujbal brother 180 132

Kool homes Balewadi kool home 176 132

Aura Balewadi Bhandari Associates 176 143

43 Balewadi 192 0

Stop Balewadi 60 51

Amit Balewadi Amit Construction 140 138

Eiffel greens Balewadi Eiffel builders 192 160

Alcon county Aundh Pride purple group 192 88