apiv professional standards scheme...api / apiv expressly disclaims any and all liability for any...

TRANSCRIPT

Independent Objective Authoritative The home for property professionals in Australia

Anna ShinNational Manager, Compliance & Risk (APIV Ltd)

Independent Objective Authoritative The home for property professionals in Australia

APIV Professional Standards Scheme

8 February 2018

Disclaimer

Information provided in this document regarding the APIV Scheme is intended to be a general guide only. The information does not constitute professional or legal advice, and you should rely on your own enquiries and assessment.

You should carefully consider the appropriateness of this information to your circumstances and seek independent advice from brokers/financial/legal advisers before making any decisions.

API / APIV expressly disclaims any and all liability for any errors, omissions, defects or misrepresentations in the Information (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the content of this document.

Overview

1. Background

2. The APIV Scheme

3. How does it work?

4. Key compliance obligations

5. Membership Application Process

6. Claims and Notifications

7. API/APIV Update

1. Background

What is APIV Scheme?

• Created under PSL

• 1 of 19 Prof Stds Schemes

• Regulated by the Professional Standards Councils (PSC)

• Administered and monitored by APIV , including enforcing compliance obligations (e.g. audit, renewal, annual reporting to PSC)

• API monitors and enforces professional standards (e.g., m/ship requirements, CPD / complaints)

1. Background (cont.) – Role of PSC

• Key objectives of PSC (the regulator): Improve professional standards

Protect consumers

Help associations administer schemes

• PSC have powers to: Compel production of information

Approve, reject and revoke schemes

• PSC reports to Parliament annually APIV must report to PSC annually

1. Background (cont.) – Role of APIV• Improve professional standards through a compliant culture (eg. reinforce CPD

requirements, etc)

• Administer Scheme (administrative function):

Monitor and enforce compliance with PSL and APIV requirements o It is not the APIV’s role to advise Members as to their compliance obligations. Whilst the

APIV actively monitors or audits member compliance, the APIV does so to discharge its obligations as administrator of the Scheme. The APIV makes no representation or warranty to Members as to whether or not they are compliant at any particular point of time

o Only a Court can determine if member is compliant in context of claim

• Report to the PSC:

Annually on operation of Scheme, outcome of compliance monitoring, insurance market, trends in notifications/claims/complaints and risk management strategies adopted

Compliance breaches by members (on-going)

1. Background (cont.) - Benefits• Compliant members can 'cap' their liability to Monetary Ceiling in place at time

of act or omission

• Member of Scheme Approved by Independent Government Agency Leading to Affordability and availability of PI insurance

• Better business practices + improved professional standards: Complementary access to RICS Valuer Registration

proactive risk management / dynamic CPD programs (eg. ‘Insurance 101’)

codes of ethics

Leading to Affordability and availability of PI insurance

• Increased consumer protection insurance up to the monetary ceiling (cap) – will cover majority of claims

consumer confidence

2. The APIV Scheme

History of APIV Scheme

• Previous Scheme 1 Sep 2010 – 31 Aug 2016

• Current Scheme commenced on 1 Sep 2016. Will operate for 5 years subject to continued compliance

structured the same way as the current Scheme/same caps threshold for RPVs increased to $2M under new Scheme – see Appendix C to the Scheme

(Supervision Guidelines) Exemptions process tightened significantly

• The APIV Scheme commenced in Tasmania on 29 January 2018.

• Currently recognised in all jurisdictions

• Cap levels determined by PSC by reference to insurance claims data for past 10 years (actuarial advice). Set at level sufficient to cover most claims

2. APIV Scheme (cont.) - who needs to join?

An API member must join the Scheme, if he/she:

1. Ordinarily resides in a State / Territory in which APIV Scheme operates (i.e. anywhere except external Territories)

2. Undertakes valuations of real property; and

3. is any one of the following:

• Life Fellow (CPV)

• Fellow (CPV)

• Associate (CPV)

• Provisional (RPV)

(Sec. 38 of API Membership Policy)

2. APIV Scheme (cont.) - who else can join?

A RICS member may join, if he/she:

1. Undertake valuations of real property in Australia

2. Holds designation of AssocRICS, MRICS or FRICS; AND

3. Holds one of the following:

• Chartered level of Membership and is entitled to use the regulatory designation of ‘Registered Valuer’; OR

• Associate level of membership and is entitled to use the regulatory designation of ‘AssocRICS Registered Valuer’

2. APIV Scheme (cont.) - who else can join?

A company/firm may join, if it is:

• An insured entity which is constituted by, employs or contracts to, one or more API member(s) eligible to join the APIV Scheme;

OR

• Duly authorised by RICS to use the designation of ‘Regulated by RICS’ AND is an insured entity which is constituted by, employs or contracts to, one or more RICS member(s) eligible to join the APIV Scheme.

2. The APIV Scheme (cont.) – Exemptions?

• Limited circumstances set out in APIV Exemptions Policy (eg., ADI/government employees or non-practising)

• Must provide evidence

• Application must be approved by APIV/APIV Board

What if I am eligible to join, but I do not want to?

• Breach of s.38 of API's Membership Policy

• API membership status may be affected

3. How does the Scheme work?

Pleaded as a defence at commencement of proceedings

To limit liability, Members must satisfy Court that:

• they have a current PI policy insuring them against the ‘occupational liability’ to which the cause of action relates

• the amount payable under the PI policy is not less than the amount of the monetary ceiling applicable at time of the act/omission which gave rise to the claim

• they have met their compliance obligations

PI insurance is “claims made” – Critical for Members to maintain a PI policy with sufficient limit of indemnity to cover the highest Monetary Ceiling applicable at any time in the past (or, at least, for the last seven years).

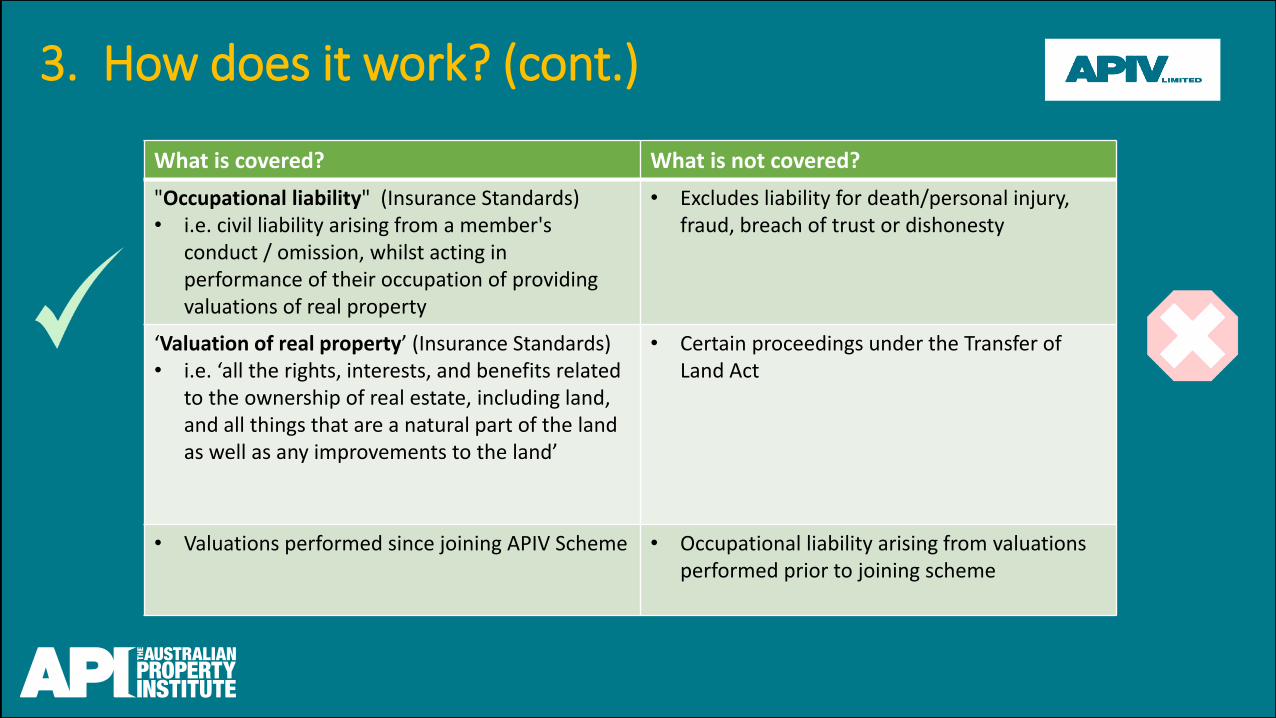

3. How does it work? (cont.)

What is covered? What is not covered?

"Occupational liability" (Insurance Standards)• i.e. civil liability arising from a member's

conduct / omission, whilst acting in performance of their occupation of providing valuations of real property

• Excludes liability for death/personal injury, fraud, breach of trust or dishonesty

‘Valuation of real property’ (Insurance Standards)• i.e. ‘all the rights, interests, and benefits related

to the ownership of real estate, including land, and all things that are a natural part of the land as well as any improvements to the land’

• Certain proceedings under the Transfer of Land Act

• Valuations performed since joining APIV Scheme • Occupational liability arising from valuations performed prior to joining scheme

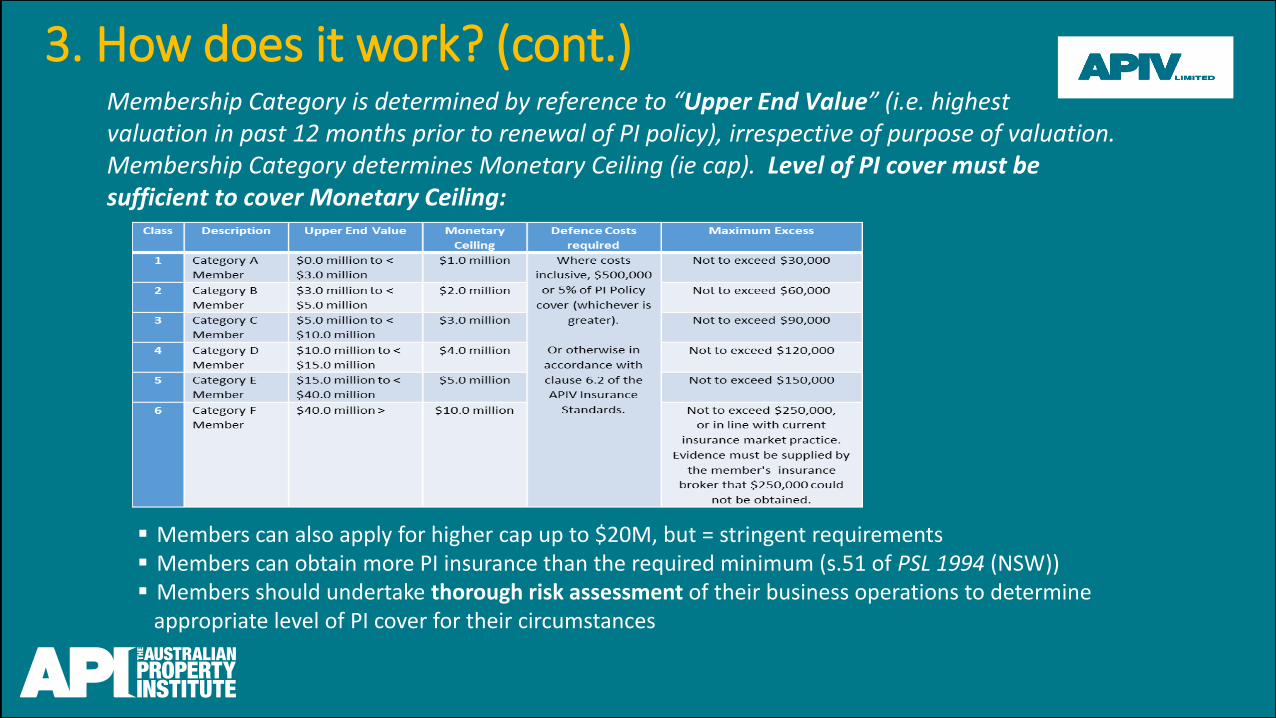

3. How does it work? (cont.) Membership Category is determined by reference to “Upper End Value” (i.e. highestvaluation in past 12 months prior to renewal of PI policy), irrespective of purpose of valuation. Membership Category determines Monetary Ceiling (ie cap). Level of PI cover must be sufficient to cover Monetary Ceiling:

Members can also apply for higher cap up to $20M, but = stringent requirements Members can obtain more PI insurance than the required minimum (s.51 of PSL 1994 (NSW)) Members should undertake thorough risk assessment of their business operations to determine

appropriate level of PI cover for their circumstances

3. How does it work? (cont.)

Borrower defaults & property sold by Lender

Firm values property for lender Lender/LMI sues Firm

2012

Valuation performed

2016Lender suffers loss

2018Claim is made

Scheme applicable is at time of valuation (ie., 2012)

Policy on foot in 2018 will respond to claim.Need PI insurance cover at the time of

Claim (ie., 2018), which is sufficient to cover Monetary Ceiling at time of valuation (i.e.

2012)

An example

Compliance for duration of Scheme

Liability capped at Monetary Ceiling in place at time of

valuation (ie., 2012)

3. How does it work? (cont.) – Change in Categories

Membership Category may change from time to time depending on Upper End Value. There are risks members need to consider:

• If a member exceeds the Upper End Value of their Category, they:

o will automatically move to higher Category at next renewal of PI policy

o must increase their PI insurance ON OR BEFORE next renewal of PI policy

o should maintain the higher level of PI cover for at least 7 years (even if they subsequently move down to a lower Membership Category)

• Members should carefully consider the implications of exceeding their Upper End Value - prior to accepting instructions

• If a member fails to increase PI cover on or before date of renewal of PI policy, they may not be able to cap their liability for valuations completed when their PI limit was not compliant(even if otherwise compliant)

Going up

3. How does it work? (cont.) – Change in Categories

• If Members do valuations that fall within a lower Membership Category, they:

o will automatically go down to appropriate lower Membership Category at the next PI policy renewal

o should maintain a PI policy with a limit of indemnity sufficient to cover the highest Monetary Ceiling applicable at any time in the past (or, at least, for the last seven years)

o should seek legal/insurance advice to ensure that they have sufficient cover

• If Members don't maintain cover at the higher level for at least 7 years, may not be able to rely on the cap (even if otherwise compliant) and hence are potentially exposed to an uninsured risk

• Risk can be mitigated by ensuring sufficient cover is maintained for at least 7 years

Going down

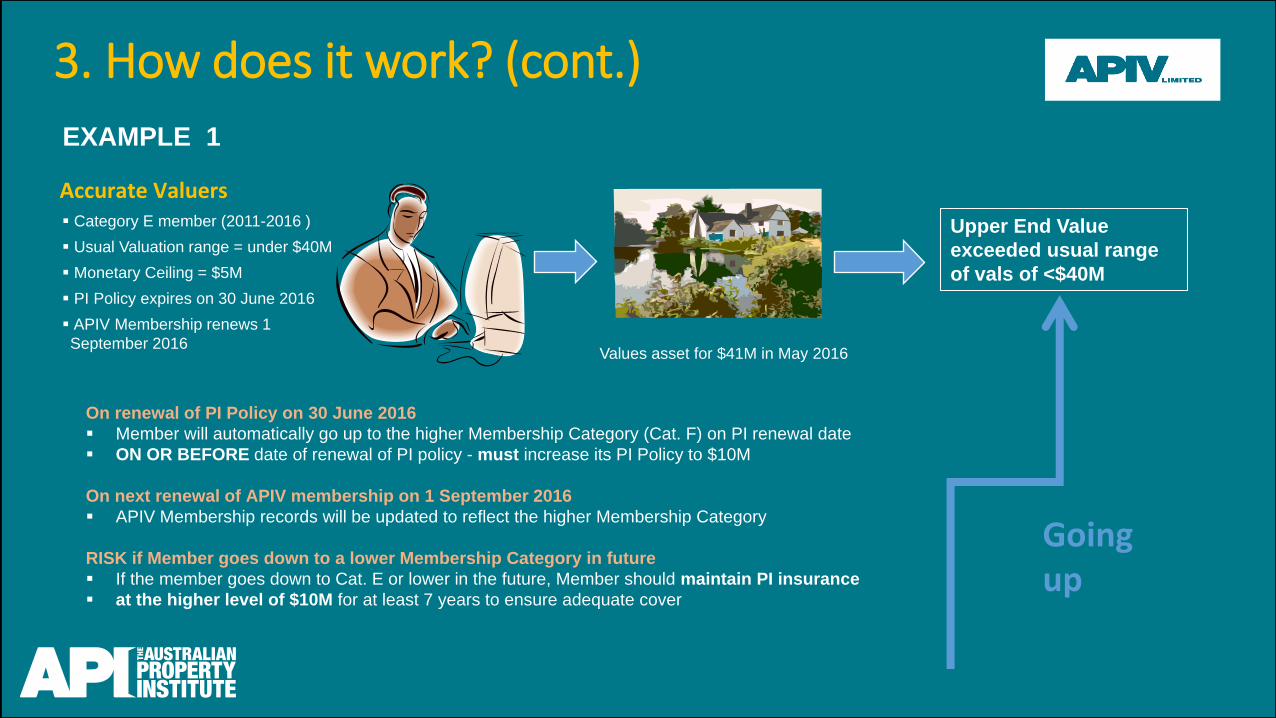

Accurate Valuers Category E member (2011-2016 )

Usual Valuation range = under $40M

Monetary Ceiling = $5M

PI Policy expires on 30 June 2016

APIV Membership renews 1

September 2016

3. How does it work? (cont.)

Values asset for $41M in May 2016

On renewal of PI Policy on 30 June 2016

Member will automatically go up to the higher Membership Category (Cat. F) on PI renewal date

ON OR BEFORE date of renewal of PI policy - must increase its PI Policy to $10M

On next renewal of APIV membership on 1 September 2016

APIV Membership records will be updated to reflect the higher Membership Category

RISK if Member goes down to a lower Membership Category in future

If the member goes down to Cat. E or lower in the future, Member should maintain PI insurance

at the higher level of $10M for at least 7 years to ensure adequate cover

Upper End Value

exceeded usual range

of vals of <$40M

Going up

EXAMPLE 1

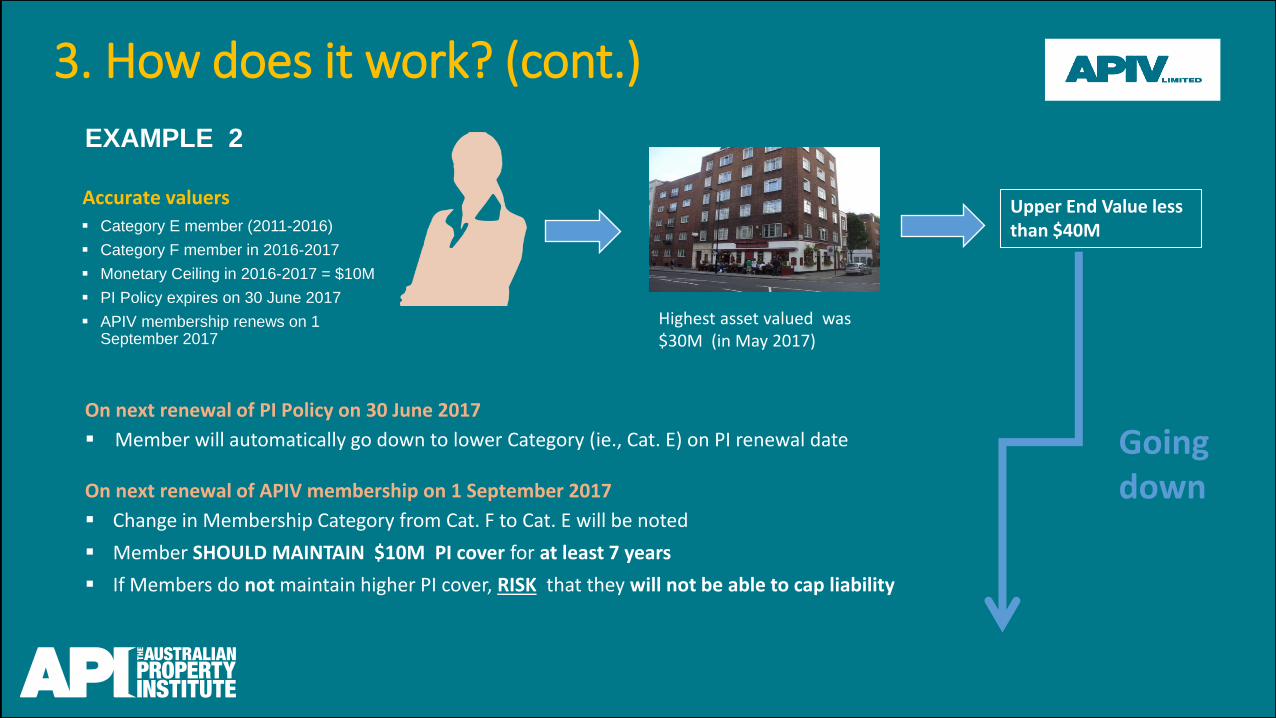

Accurate valuers

Category E member (2011-2016)

Category F member in 2016-2017

Monetary Ceiling in 2016-2017 = $10M

PI Policy expires on 30 June 2017

APIV membership renews on 1 September 2017

On next renewal of PI Policy on 30 June 2017

Member will automatically go down to lower Category (ie., Cat. E) on PI renewal date

On next renewal of APIV membership on 1 September 2017

Change in Membership Category from Cat. F to Cat. E will be noted

Member SHOULD MAINTAIN $10M PI cover for at least 7 years

If Members do not maintain higher PI cover, RISK that they will not be able to cap liability

Upper End Value less than $40M

Highest asset valued was $30M (in May 2017)

3. How does it work? (cont.)

Going down

EXAMPLE 2

4. Key compliance obligations Members are responsible for determining applicable compliance obligations and ensuring compliance

Members must comply with:

• APIV Insurance Standards

• Other APIV Scheme obligations (eg., Supervision Guidelines, etc)

• PSL requirements (e.g., disclosure obligations, reporting obligations, etc)

"Liability limited by a scheme approved under Professional Standards Legislation"

• Report certain matters to APIV on on-going basis (e.g. notifications, claims, settlements, complaints, etc.)

• Comply with API’s CPD requirements

• Renew APIV membership annually, including compliance checks

• Respond to surveys and audit requests

4. Key compliance obligations (cont.)Key requirements of the ‘Insurance Standards’:

• PI limit must be same or greater than Monetary Ceiling (cap)

• With respect to defence costs:

Must either have defence costs 'in addition' or, if inclusive, $500k defence costs cover in addition; or

Make asset declaration/s

• Minimum 1 automatic reinstatement

• Excess must be less than the applicable Maximum Excess

• Endorsements/Exclusions in Standard 7, if reasonably available;

• Retroactive date to inception of APIV Membership

• Run-off cover for 7 years (if reasonably available), unless exempt

• Must ensure all eligible employees/sub-contractors join Scheme

4. Key compliance obligations (cont.)

Key compliance obligations Consequences of failure to comply

Disclosure obligations • Offence under PSL carrying penalties• Potentially, inability to plead cap (specifically in

Vic, Qld & NT)• Disciplinary action by APIV

Non-compliance with Scheme requirements

• APIV may commence disciplinary action • APIV may terminate APIV membership • API may terminate API membership• APIV required to report non-compliance to the

PSC, which may take further action

Consequences of non-compliance

5. Membership Application Process1. Business Owners:

• Complete Membership Application Form for your firm and employees

• If running business in a corporate structure, the corporate employer must join as an APIV member as well as the eligible individual members

• Evidence of compliant PI insurance policy

• Payment of Invoice

2. Employees – Check with relevant person (eg. Director or Compliance Manager) at work regarding your application

3. Fees:• Joining Fee – $297 per person and per company

• Renewal Fee – $242 per person and per company

6. Claims and Notifications reported to APIV in 2017

• 16 claims and 45 notifications reported to APIV in 2017

• 80% of Member Firms confirmed that PI insurance was easy to purchase in 2017

• The tail of the claims (i.e. time taken between val date & notification date to insurer) – a median of 3.5 years

7. API and APIV Updates

RICS / API Strategic Alliance

• APIV Scheme open to eligible RICS valuers

• Mandatory participation in RICS Valuer Registration

• Alignment of API Valuation Standards with RICS Redbook

• One Professional Pathway for valuer profession

7. API and APIV Updates (cont.)

Scheme Amendments

1. Scheme Review in conjunction with RICS

• Removal of Membership Categories?

• Changes to how a Monetary Ceiling is determined

Upper End Value – Average of 5 or 10 highest valuations

7. API and APIV Updates (cont.)

Scheme Amendments

2. Reviewing Scheme to better deal with “low” risk valuations

• Feedback from Insurers – Generally agreeable with the concept, however, need to carefully consider what it means to be ‘low-risk’

• Feedback from PSC – Generally agreeable with the concept, provided insurance stakeholders are in agreement with the APIV’s proposal

7. API and APIV Updates (cont.)

Scheme Amendments

2. Reviewing Scheme to better deal with “low” risk valuations

• Val of RP undertaken in capacity as arbitrator

• Val of RP undertaken for purpose of providing a binding determination as an expert where ‘hold harmless’ agreement has been signed

• Val of RP for purpose of financial reporting, rating and taxing, or resumption

• Val of RP for purpose of providing expert evidence before court/tribunal

• Val of RP for purpose of advising on insurable value of RP in connection with purchase of insurance

• All other Val of RP = NOT low risk

Questions?

Key contact

Anna Shin

National Manager, Compliance and Risk (APIV Ltd)

(03) 9644 7505

Further information and resources can also be found on the API website: http://www.api.org.au/