anup p. shah - ctconline.org - anup p... · anup p. shah 20th june 2013 ... apollo tyres would be...

TRANSCRIPT

-Anup P. Shah

20th June 2013

Chamber of Tax Consultants

Int’l Tax RRC at Bengaluru

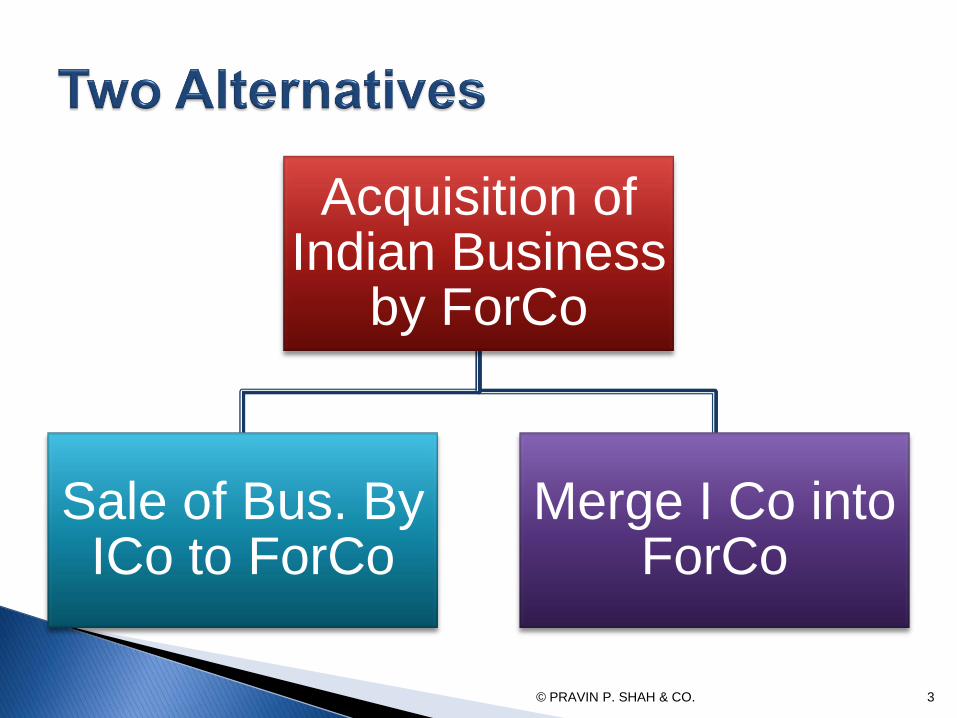

Acquisition of Indian Business

by ForCo

Sale of Bus. By ICo to ForCo

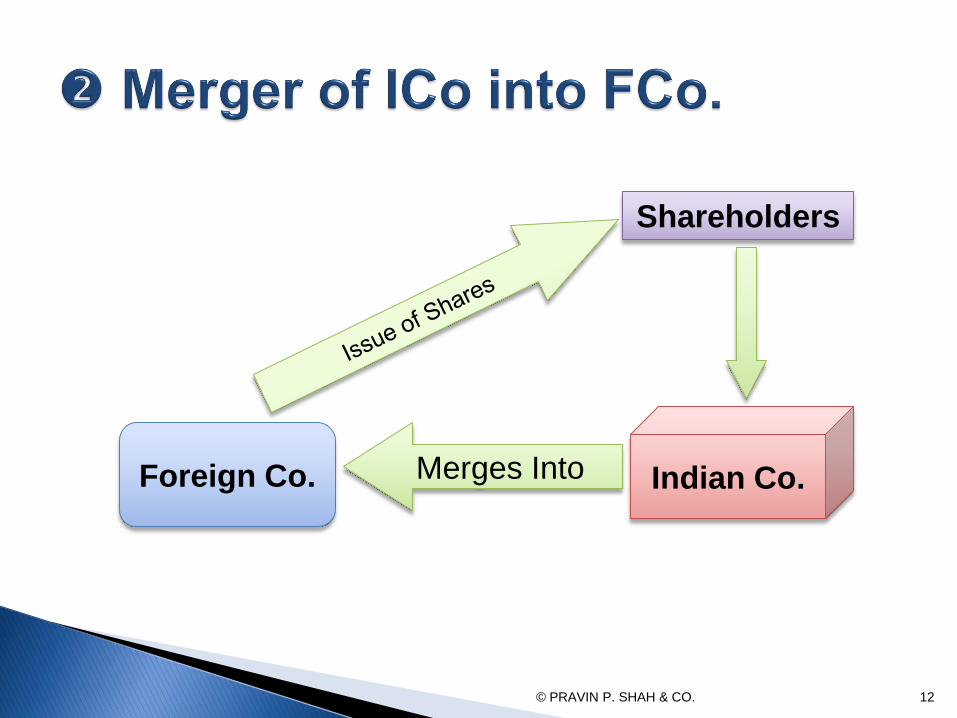

Merge I Co into ForCo

© PRAVIN P. SHAH & CO. 3

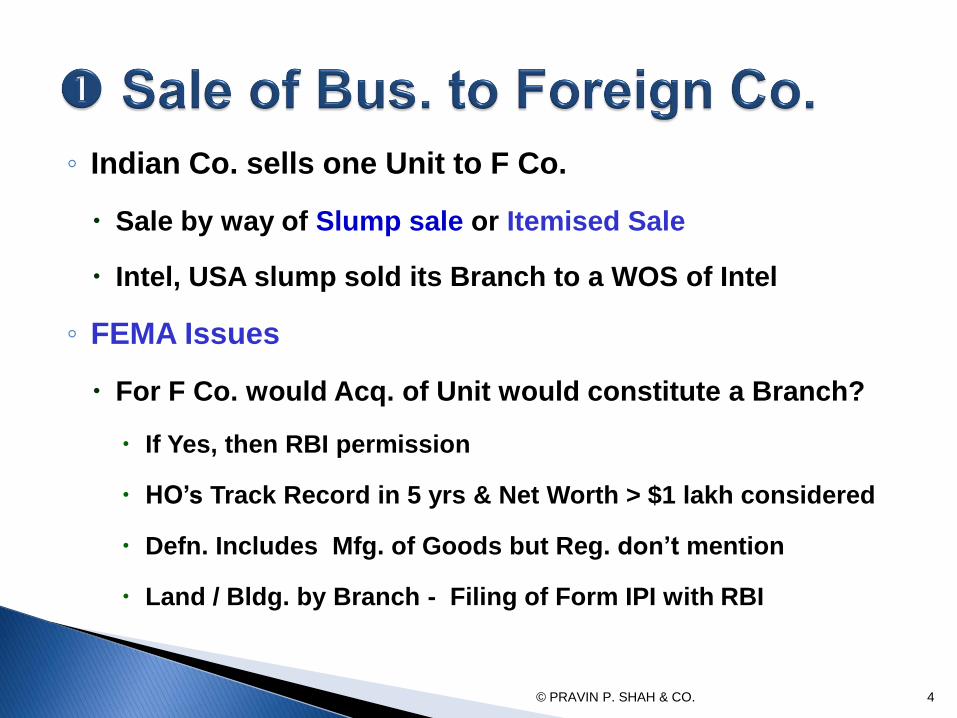

◦ Indian Co. sells one Unit to F Co.

Sale by way of Slump sale or Itemised Sale

Intel, USA slump sold its Branch to a WOS of Intel

◦ FEMA Issues

For F Co. would Acq. of Unit would constitute a Branch?

If Yes, then RBI permission

HO’s Track Record in 5 yrs & Net Worth > $1 lakh considered

Defn. Includes Mfg. of Goods but Reg. don’t mention

Land / Bldg. by Branch - Filing of Form IPI with RBI

© PRAVIN P. SHAH & CO. 4

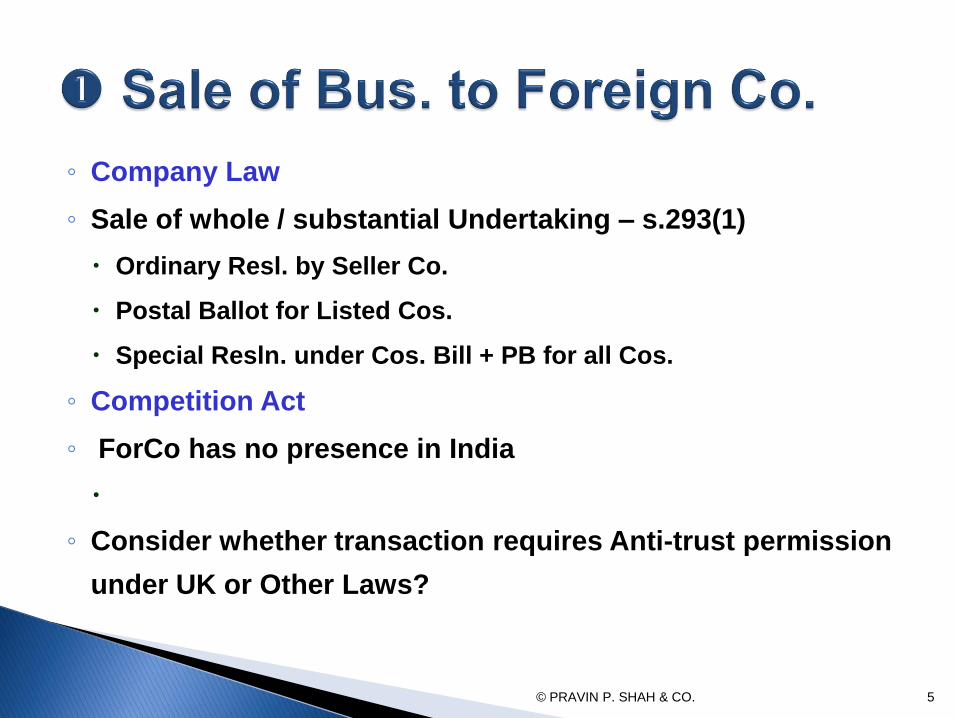

◦ Company Law

◦ Sale of whole / substantial Undertaking – s.293(1)

Ordinary Resl. by Seller Co.

Postal Ballot for Listed Cos.

Special Resln. under Cos. Bill + PB for all Cos.

◦ Competition Act

◦ ForCo has no presence in India

◦ Consider whether transaction requires Anti-trust permission

under UK or Other Laws?

© PRAVIN P. SHAH & CO. 5

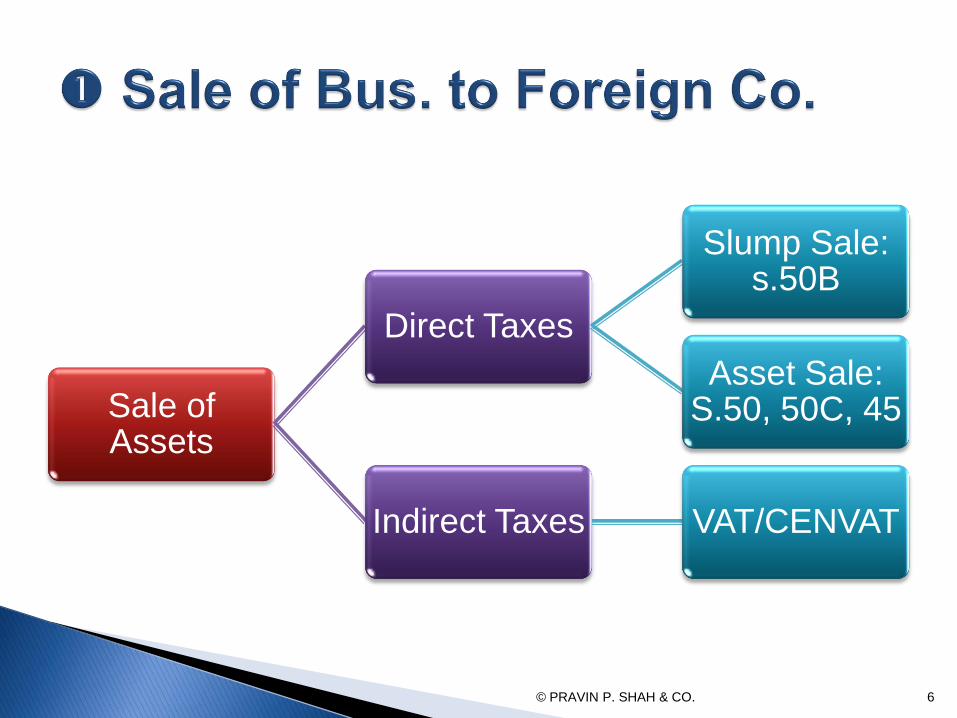

Sale of Assets

Direct Taxes

Slump Sale: s.50B

Asset Sale: S.50, 50C, 45

Indirect Taxes VAT/CENVAT

© PRAVIN P. SHAH & CO. 6

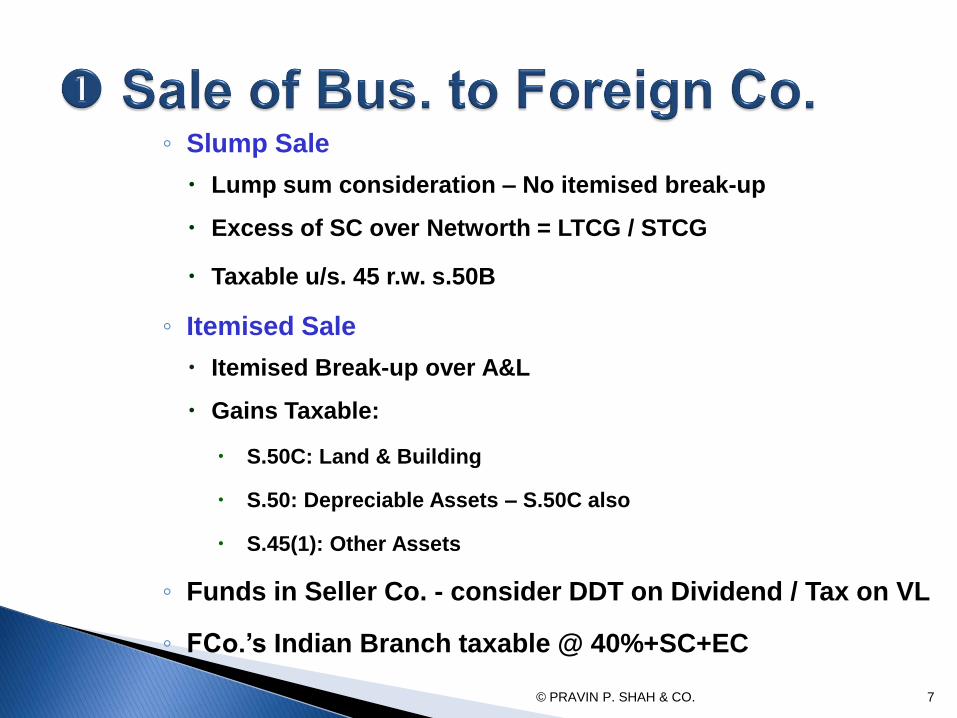

◦ Slump Sale

Lump sum consideration – No itemised break-up

Excess of SC over Networth = LTCG / STCG

Taxable u/s. 45 r.w. s.50B

◦ Itemised Sale

Itemised Break-up over A&L

Gains Taxable:

S.50C: Land & Building

S.50: Depreciable Assets – S.50C also

S.45(1): Other Assets

◦ Funds in Seller Co. - consider DDT on Dividend / Tax on VL

◦ FCo.’s Indian Branch taxable @ 40%+SC+EC

© PRAVIN P. SHAH & CO. 7

© PRAVIN P. SHAH & CO. 8

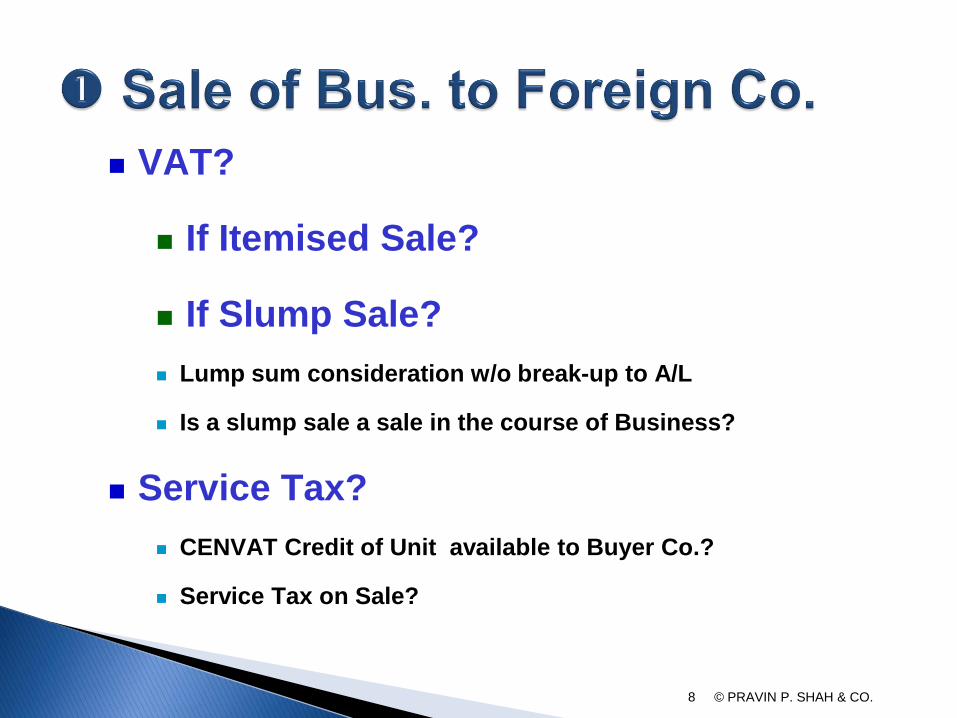

VAT?

If Itemised Sale?

If Slump Sale?

Lump sum consideration w/o break-up to A/L

Is a slump sale a sale in the course of Business?

Service Tax?

CENVAT Credit of Unit available to Buyer Co.?

Service Tax on Sale?

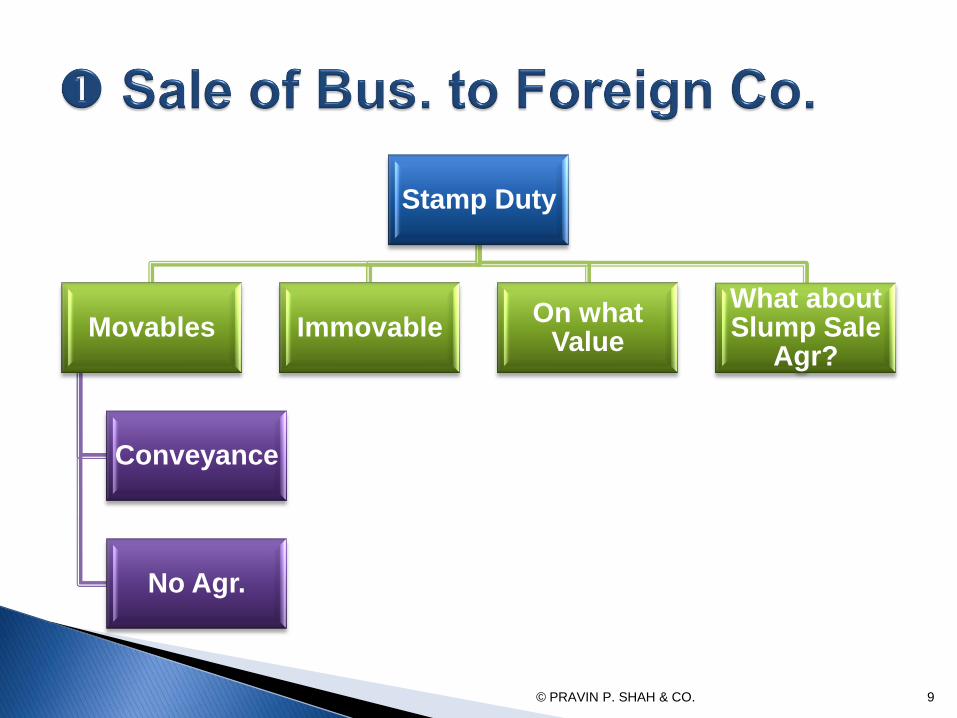

Stamp Duty

Movables

Conveyance

No Agr.

Immovable On what

Value

What about Slump Sale

Agr?

© PRAVIN P. SHAH & CO. 9

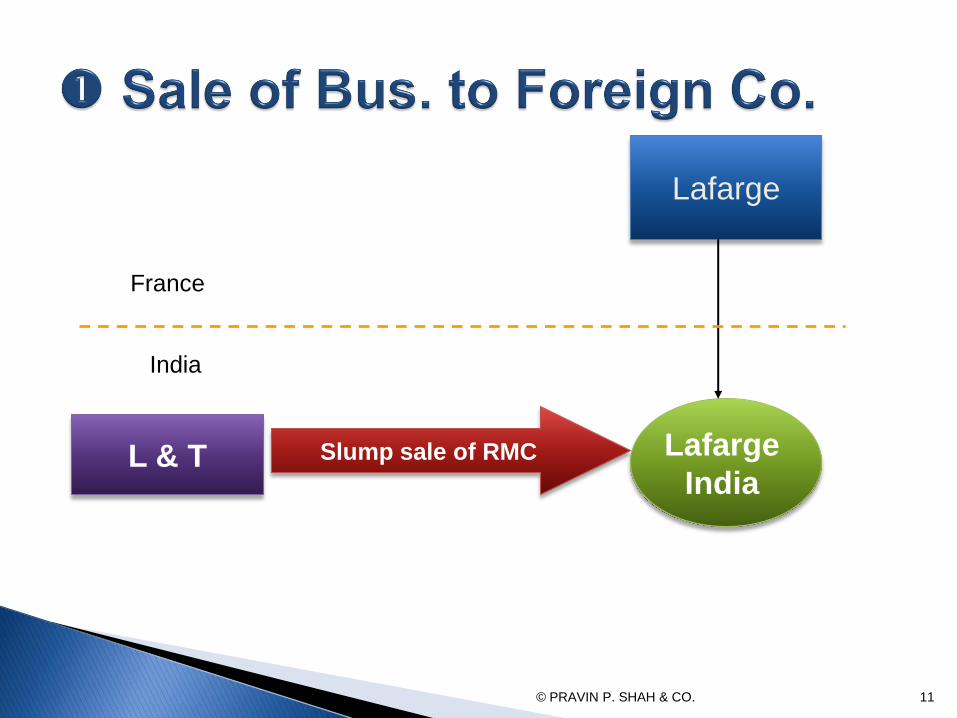

Instead of direct Acqn. FCo can consider having a

WOS which can acquire the Business

Example

L&T wanted to sell its Ready Mix Concrete (RMC)

Business

RMC was a unit within L&T

Lafarge of France was interested in buying this RMC unit

Agreement reached for $349 million

© PRAVIN P. SHAH & CO. 10

© PRAVIN P. SHAH & CO. 11

Lafarge

L & T Lafarge

India

France

India

Slump sale of RMC

© PRAVIN P. SHAH & CO. 12

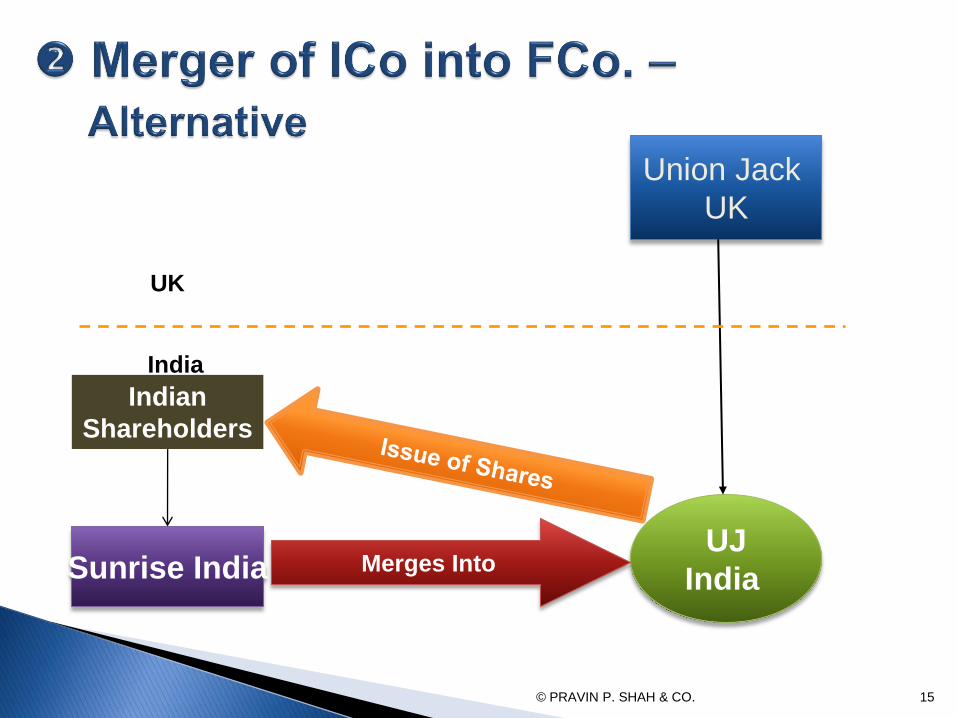

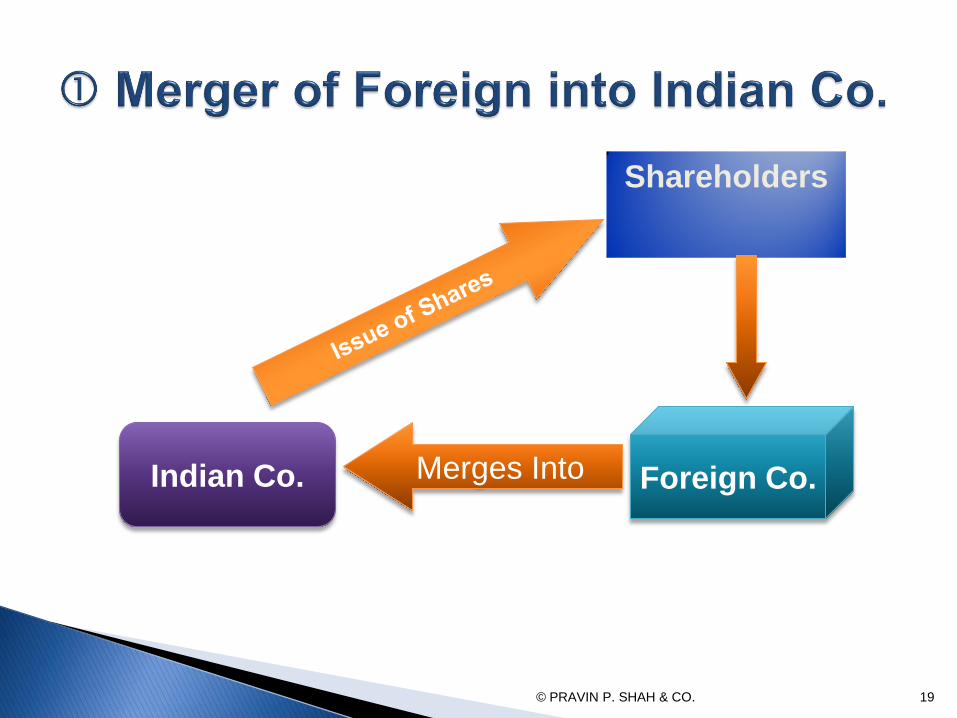

Foreign Co. Indian Co. Merges Into

Shareholders

◦ Can Sunrise (Indian Company) merge into Union

Jack (For Co) ?

◦ Can Union Jack issue its shares to shareholders of

Sunrise India?

◦ Is it possible u/s.394 of Companies Act?

Can Transferee Co. be a Foreign Co.?

◦

© PRAVIN P. SHAH & CO. 13

◦ Does the Companies Bill 2012 permit such a Merger?

◦ FEMA Regulations?

Can Indian Shareholders own shares in Foreign Co. by

way of merger

◦ Tax Exemption available?

© PRAVIN P. SHAH & CO. 14

© PRAVIN P. SHAH & CO. 15

Union Jack

UK

Sunrise India UJ

India

UK

India

Merges Into

Indian

Shareholders

© PRAVIN P. SHAH & CO., CAs 16

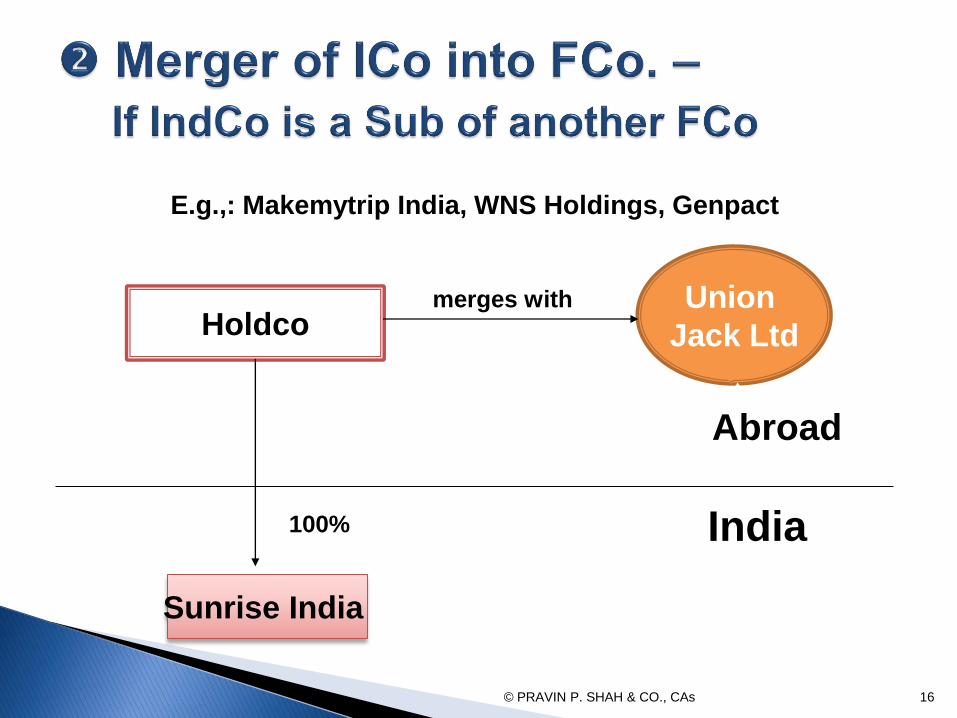

Holdco Union

Jack Ltd

Sunrise India

India

Abroad

merges with

100%

E.g.,: Makemytrip India, WNS Holdings, Genpact

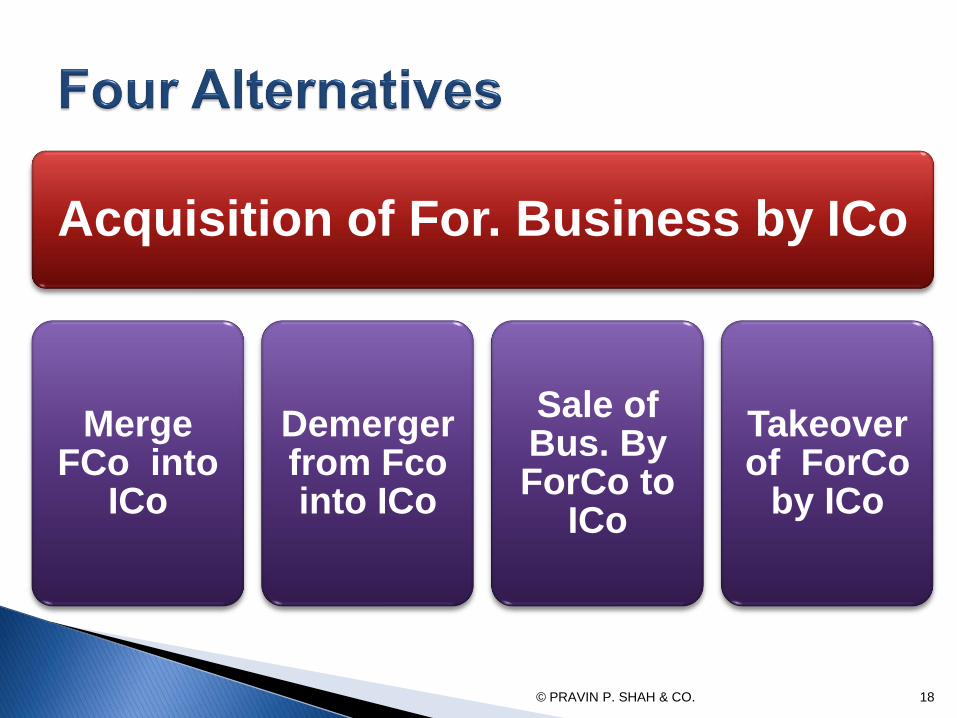

Acquisition of For. Business by ICo

Merge FCo into

ICo

Demerger from Fco into ICo

Sale of Bus. By ForCo to

ICo

Takeover of ForCo

by ICo

© PRAVIN P. SHAH & CO. 18

© PRAVIN P. SHAH & CO. 19

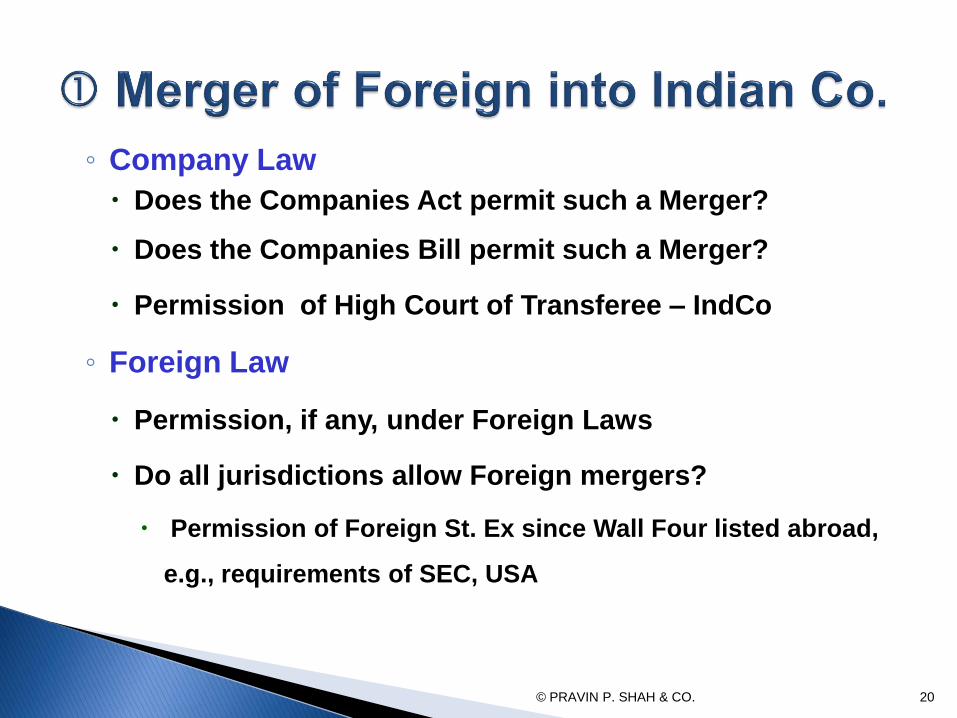

Indian Co. Foreign Co. Merges Into

Shareholders

◦ Company Law

Does the Companies Act permit such a Merger?

Does the Companies Bill permit such a Merger?

Permission of High Court of Transferee – IndCo

◦ Foreign Law

Permission, if any, under Foreign Laws

Do all jurisdictions allow Foreign mergers?

Permission of Foreign St. Ex since Wall Four listed abroad,

e.g., requirements of SEC, USA

© PRAVIN P. SHAH & CO. 20

Tax Implications?

◦ Can you merge under Income-tax

◦ Yes

◦ CGT by Fco for Business in India?

◦ No CGT by the Indian Shareholders holding shares in

Fco.- Conditions?

© PRAVIN P. SHAH & CO. 21

Other Laws

◦ FIPB’s approval required for merger

What if Foreign WOS merges into Indian HoldCo.?

E.g., Wipro’s Singaporean & Bermuda WOS with Wipro

◦ Do SEBI Takeover Regs. Apply?

◦ Permission of CCI

◦ If ICo is listed – SEBI Permission is required

Cl. 24 of Listing Agreement

© PRAVIN P. SHAH & CO. 22

© PRAVIN P. SHAH & CO. 23

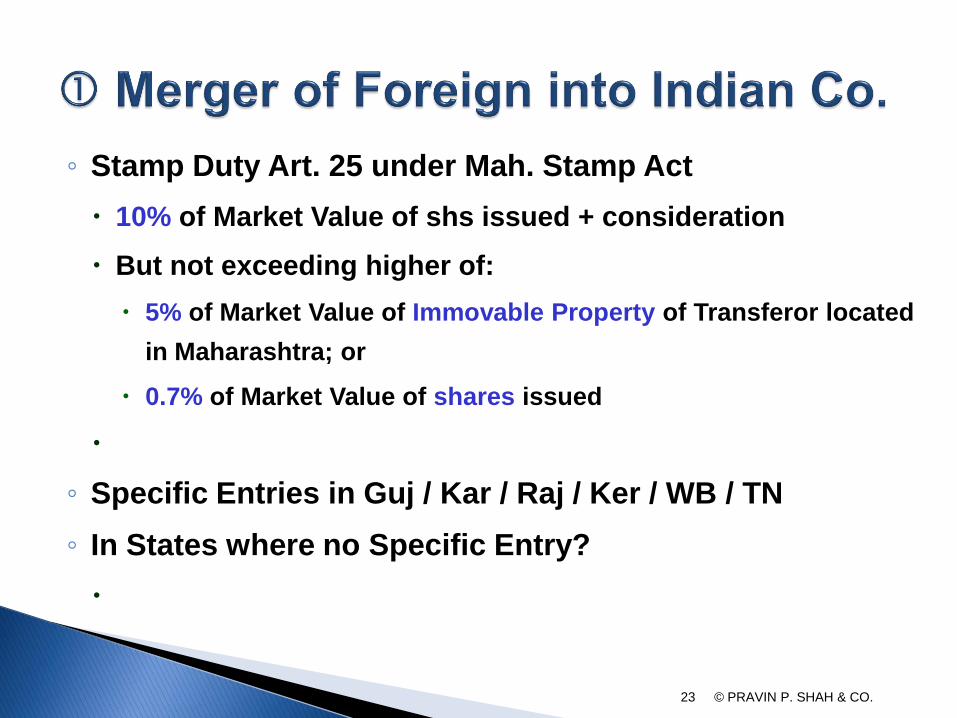

◦ Stamp Duty Art. 25 under Mah. Stamp Act

10% of Market Value of shs issued + consideration

But not exceeding higher of:

5% of Market Value of Immovable Property of Transferor located

in Maharashtra; or

0.7% of Market Value of shares issued

◦ Specific Entries in Guj / Kar / Raj / Ker / WB / TN

◦ In States where no Specific Entry?

© PRAVIN P. SHAH & CO., CAs 24

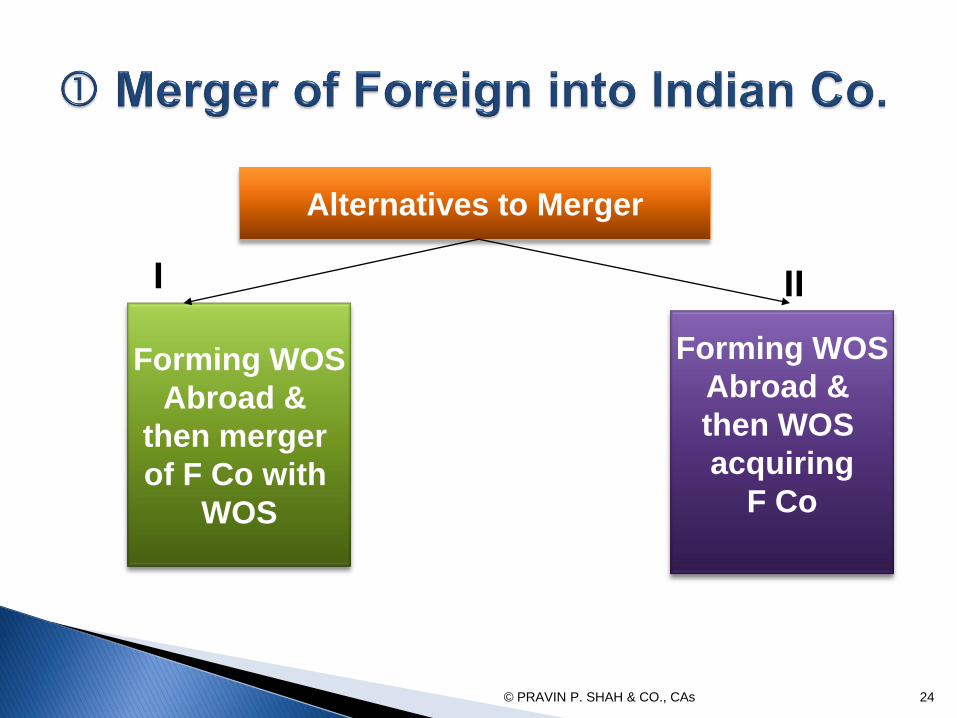

Alternatives to Merger

Forming WOS

Abroad &

then merger

of F Co with

WOS

Forming WOS

Abroad &

then WOS

acquiring

F Co

I II

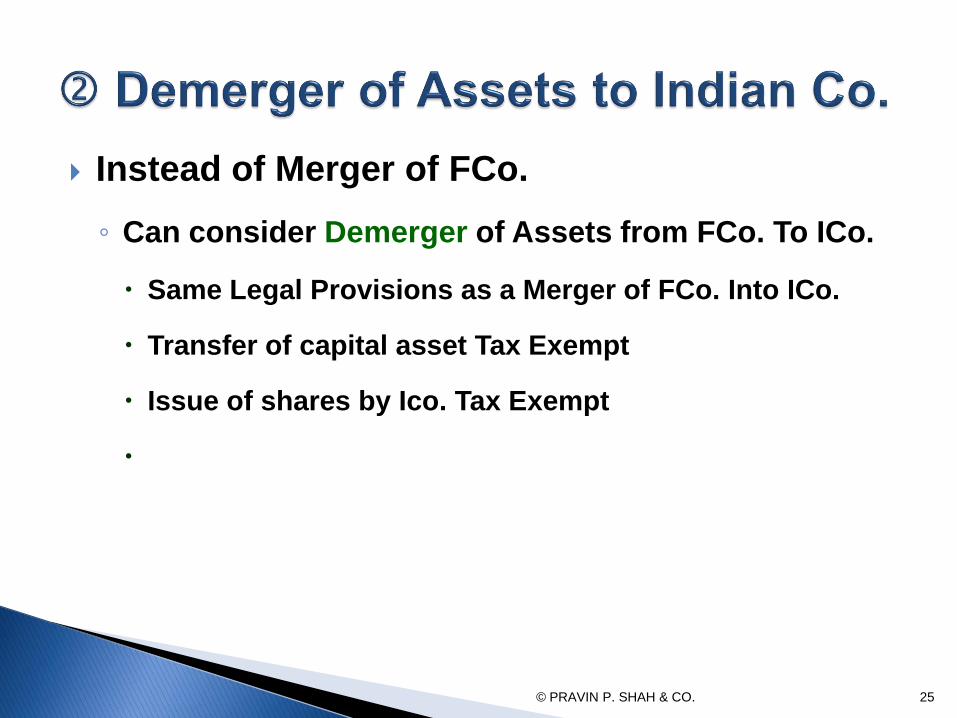

Instead of Merger of FCo.

◦ Can consider Demerger of Assets from FCo. To ICo.

Same Legal Provisions as a Merger of FCo. Into ICo.

Transfer of capital asset Tax Exempt

Issue of shares by Ico. Tax Exempt

© PRAVIN P. SHAH & CO. 25

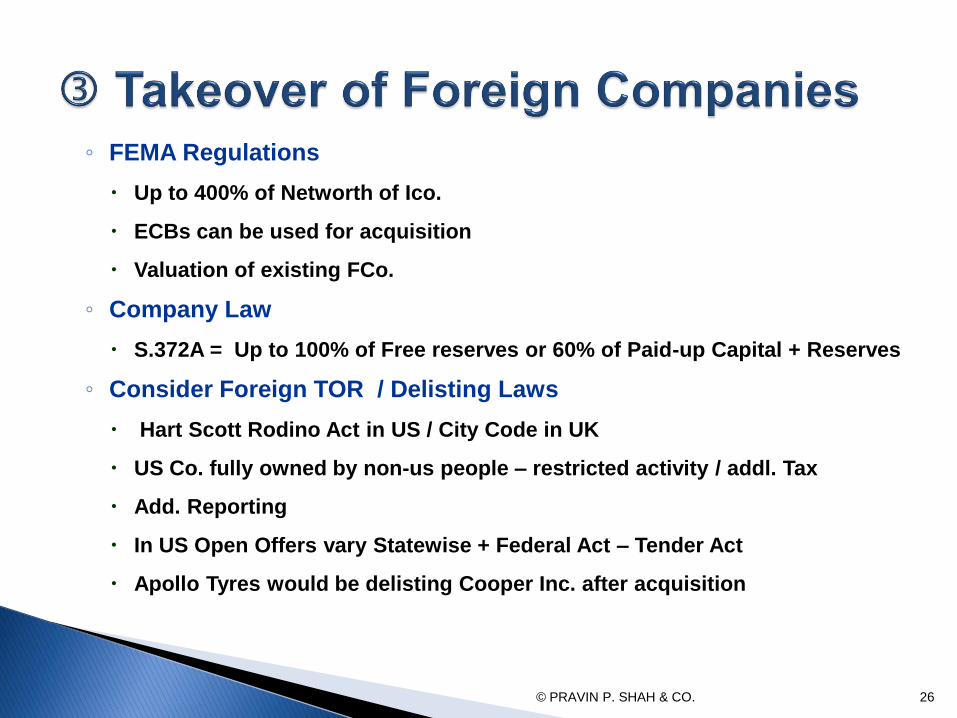

◦ FEMA Regulations

Up to 400% of Networth of Ico.

ECBs can be used for acquisition

Valuation of existing FCo.

◦ Company Law

S.372A = Up to 100% of Free reserves or 60% of Paid-up Capital + Reserves

◦ Consider Foreign TOR / Delisting Laws

Hart Scott Rodino Act in US / City Code in UK

US Co. fully owned by non-us people – restricted activity / addl. Tax

Add. Reporting

In US Open Offers vary Statewise + Federal Act – Tender Act

Apollo Tyres would be delisting Cooper Inc. after acquisition

© PRAVIN P. SHAH & CO. 26

◦ Income-tax

S.56(2)(viia) applicable on acquisition of listed FCo.?

S.14A Disallowance for Interest?

Whether s.14A applicable for overseas investments?

© PRAVIN P. SHAH & CO. 27

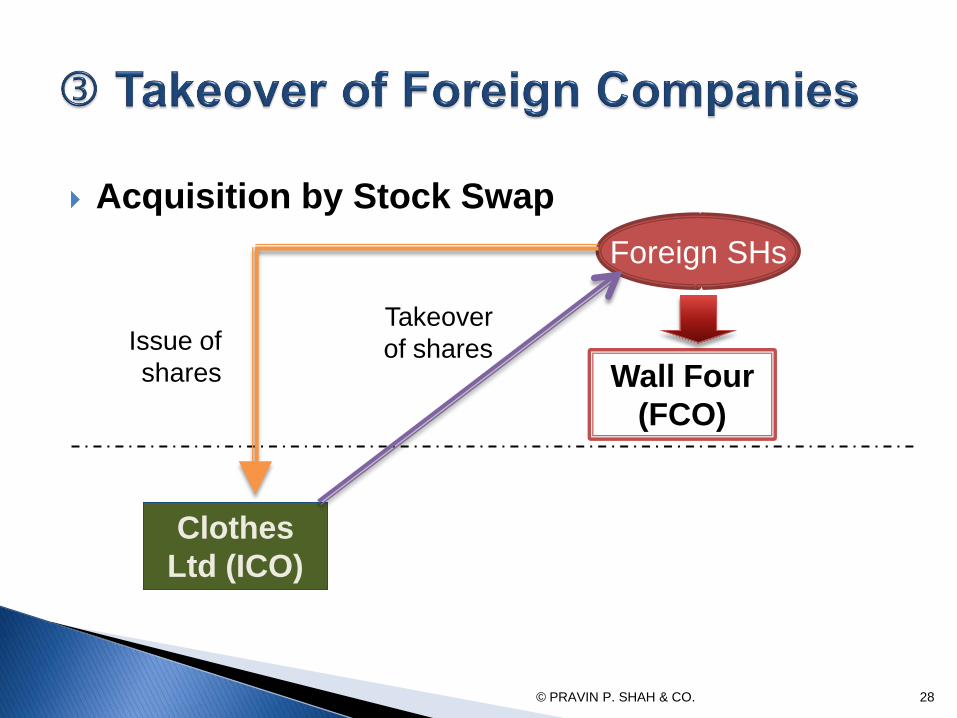

Acquisition by Stock Swap

© PRAVIN P. SHAH & CO. 28

Clothes

Ltd (ICO)

Wall Four

(FCO)

Foreign SHs

Issue of

shares

Takeover

of shares

Overseas Direct Invst. by Share Swap:

◦ ICo issues its shares in return for shares of FCo

◦ Auto Route for Outbound

◦ Valuation of FCo by Invst Banker – No specific method

◦ FIPB permission for Inward Invst. Leg

Consideration Other than Cash

◦ Undertaking from NR Shs.

Sale of ICo shs. to be as per FEMA Regs. only

© PRAVIN P. SHAH & CO. 29

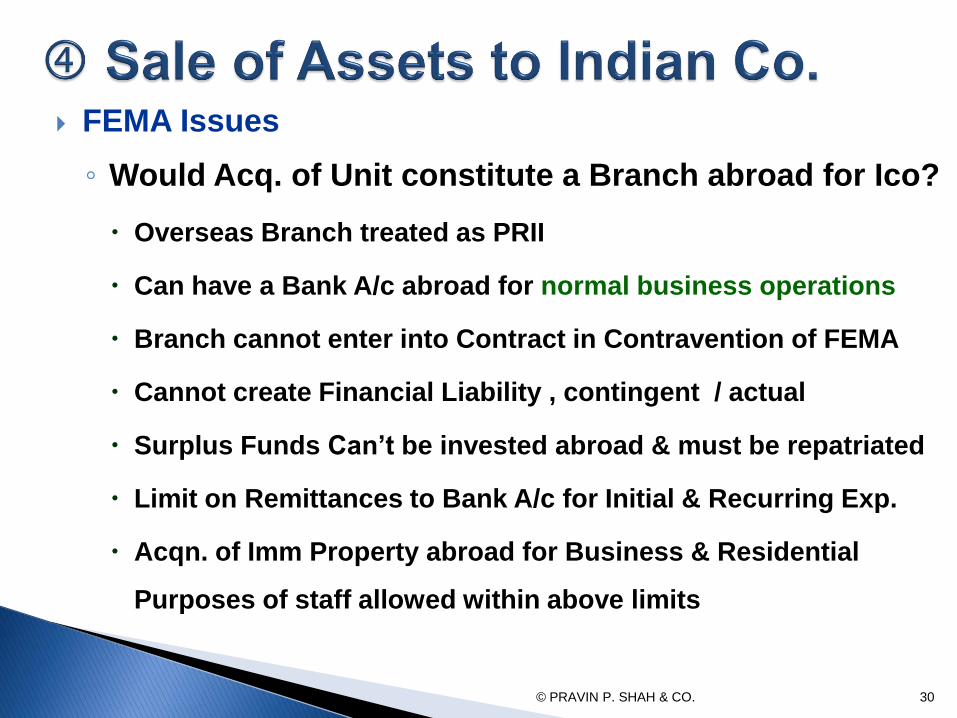

FEMA Issues

◦ Would Acq. of Unit constitute a Branch abroad for Ico?

Overseas Branch treated as PRII

Can have a Bank A/c abroad for normal business operations

Branch cannot enter into Contract in Contravention of FEMA

Cannot create Financial Liability , contingent / actual

Surplus Funds Can’t be invested abroad & must be repatriated

Limit on Remittances to Bank A/c for Initial & Recurring Exp.

Acqn. of Imm Property abroad for Business & Residential

Purposes of staff allowed within above limits

© PRAVIN P. SHAH & CO. 30

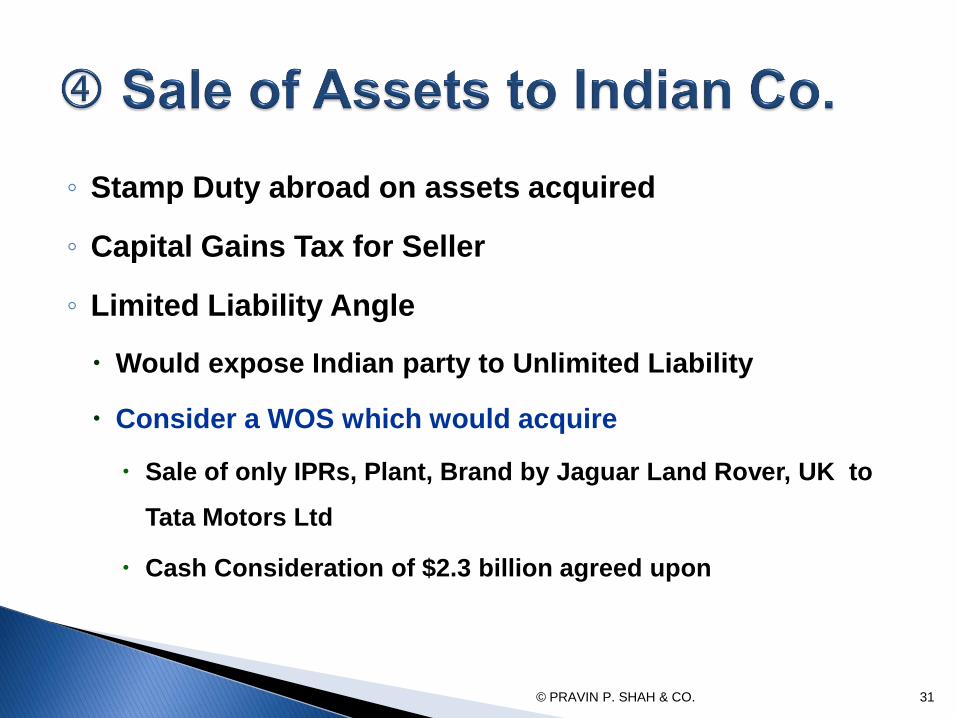

◦ Stamp Duty abroad on assets acquired

◦ Capital Gains Tax for Seller

◦ Limited Liability Angle

Would expose Indian party to Unlimited Liability

Consider a WOS which would acquire

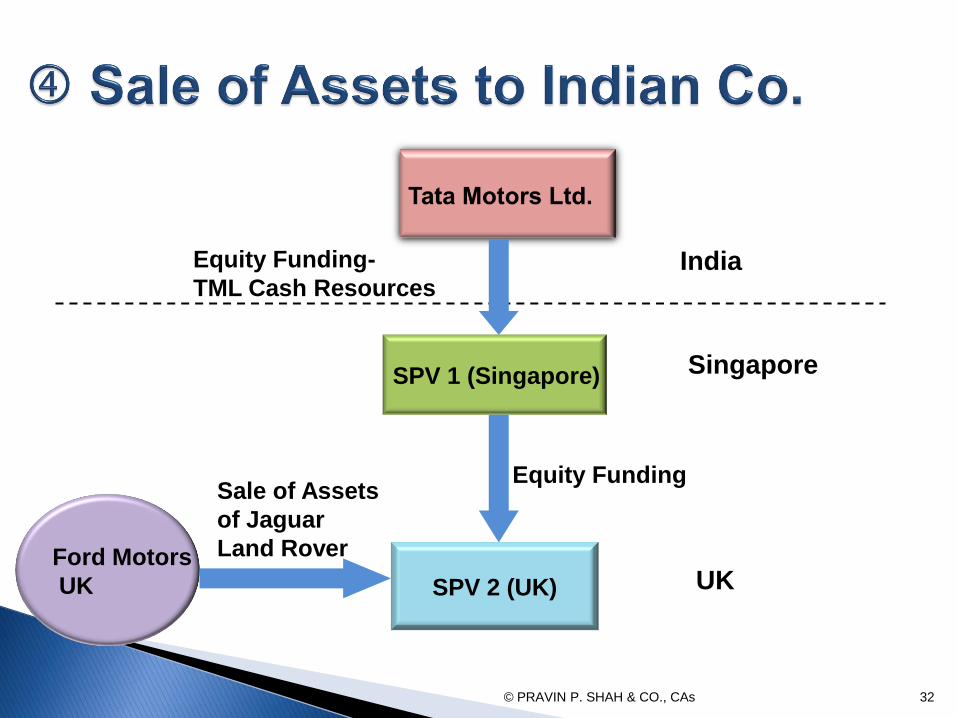

Sale of only IPRs, Plant, Brand by Jaguar Land Rover, UK to

Tata Motors Ltd

Cash Consideration of $2.3 billion agreed upon

© PRAVIN P. SHAH & CO. 31

© PRAVIN P. SHAH & CO., CAs 32

SPV 2 (UK)

Ford Motors

UK

Sale of Assets

of Jaguar

Land Rover

India

Singapore SPV 1 (Singapore)

Equity Funding

Equity Funding-

TML Cash Resources

UK

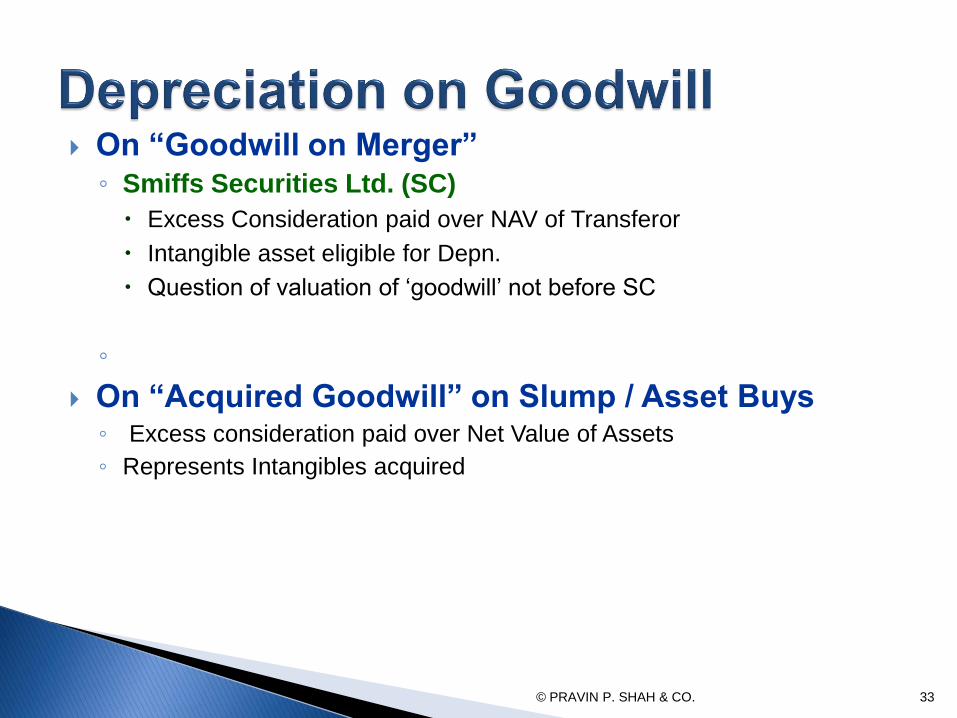

On “Goodwill on Merger” ◦ Smiffs Securities Ltd. (SC)

Excess Consideration paid over NAV of Transferor

Intangible asset eligible for Depn.

Question of valuation of ‘goodwill’ not before SC

◦

On “Acquired Goodwill” on Slump / Asset Buys ◦ Excess consideration paid over Net Value of Assets

◦ Represents Intangibles acquired

© PRAVIN P. SHAH & CO. 33

© PRAVIN P. SHAH & CO. 35

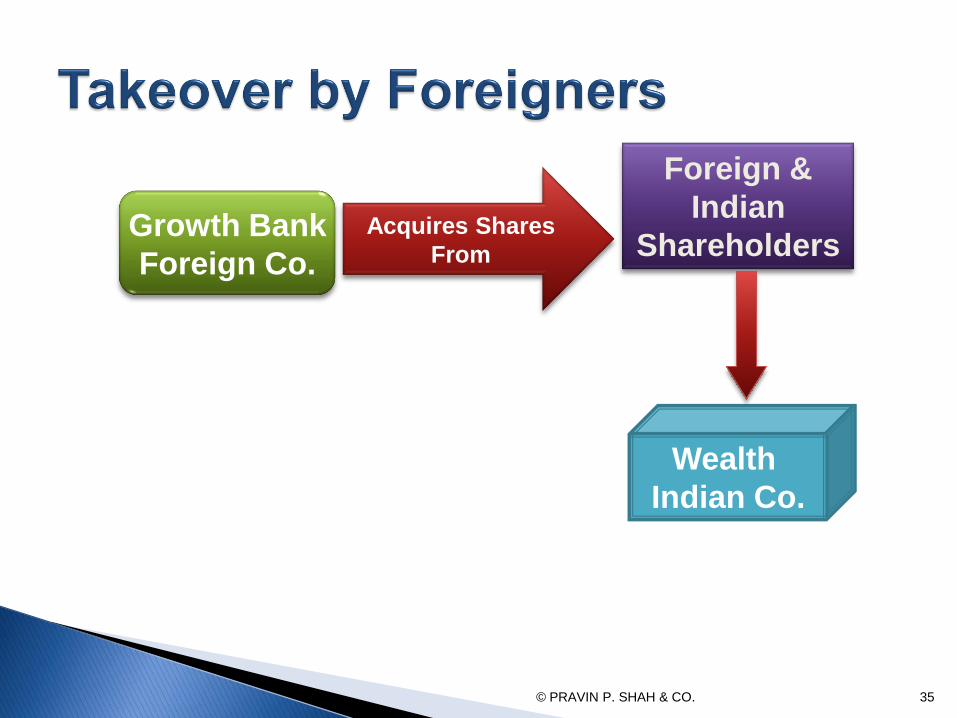

Growth Bank

Foreign Co.

Wealth

Indian Co.

Foreign &

Indian

Shareholders Acquires Shares

From

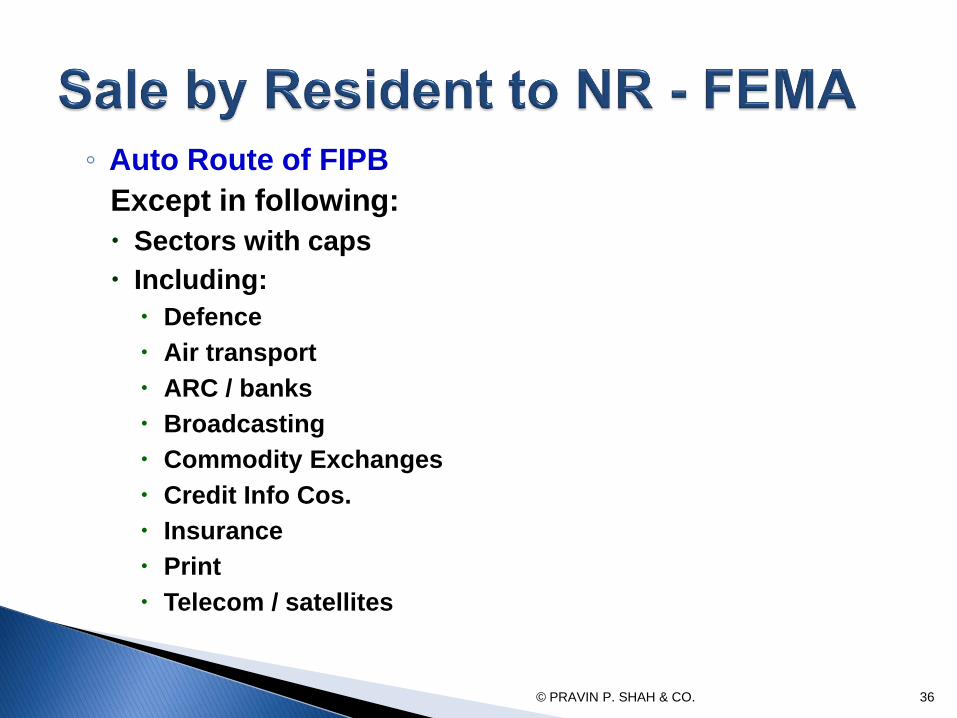

◦ Auto Route of FIPB

Except in following:

Sectors with caps

Including:

Defence

Air transport

ARC / banks

Broadcasting

Commodity Exchanges

Credit Info Cos.

Insurance

Telecom / satellites

© PRAVIN P. SHAH & CO. 36

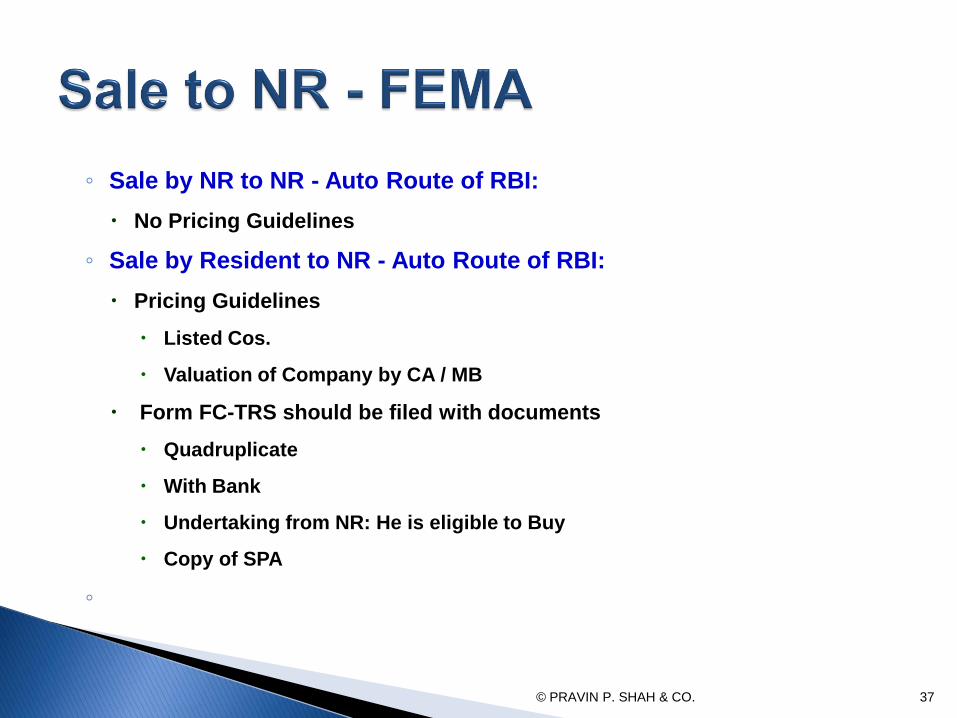

◦ Sale by NR to NR - Auto Route of RBI:

No Pricing Guidelines

◦ Sale by Resident to NR - Auto Route of RBI:

Pricing Guidelines

Listed Cos.

Valuation of Company by CA / MB

Form FC-TRS should be filed with documents

Quadruplicate

With Bank

Undertaking from NR: He is eligible to Buy

Copy of SPA

◦

© PRAVIN P. SHAH & CO. 37

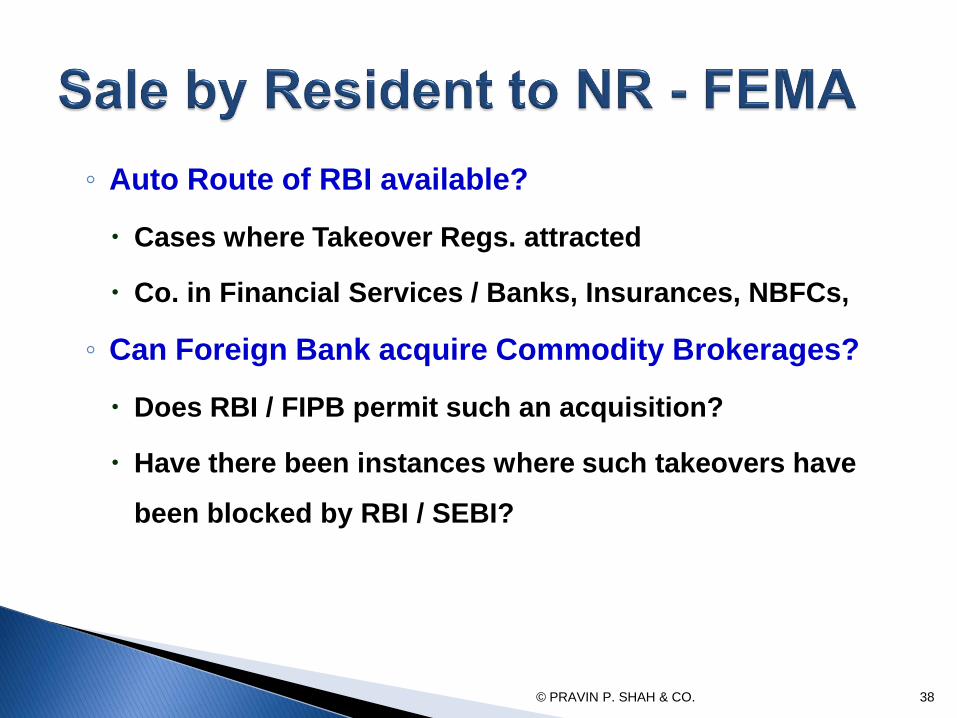

◦ Auto Route of RBI available?

Cases where Takeover Regs. attracted

Co. in Financial Services / Banks, Insurances, NBFCs,

◦ Can Foreign Bank acquire Commodity Brokerages?

Does RBI / FIPB permit such an acquisition?

Have there been instances where such takeovers have

been blocked by RBI / SEBI?

© PRAVIN P. SHAH & CO. 38

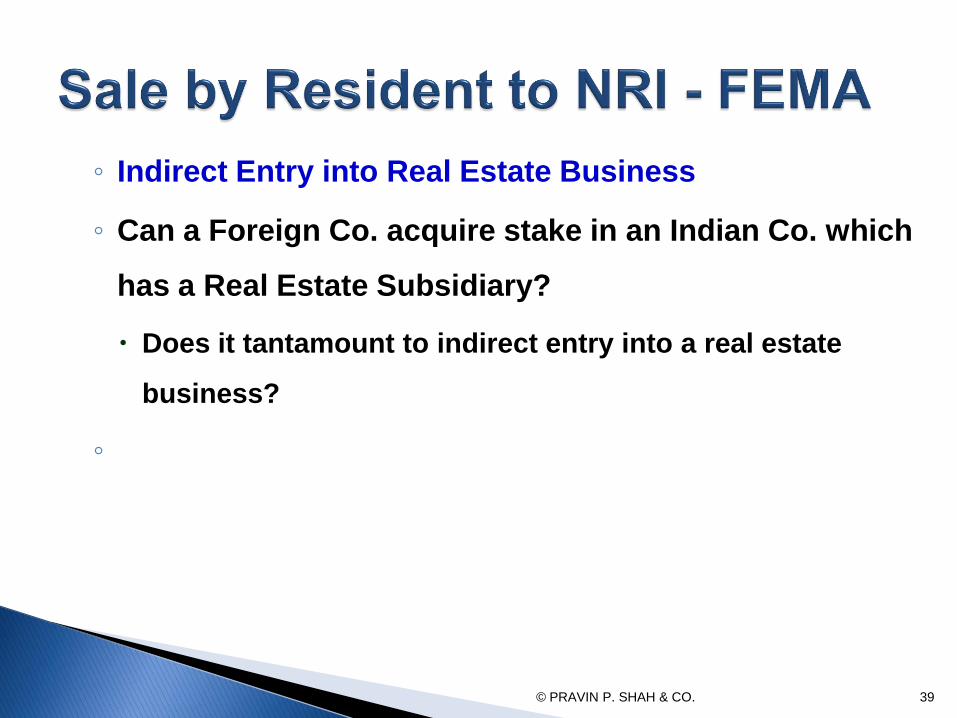

◦ Indirect Entry into Real Estate Business

◦ Can a Foreign Co. acquire stake in an Indian Co. which

has a Real Estate Subsidiary?

Does it tantamount to indirect entry into a real estate

business?

◦

© PRAVIN P. SHAH & CO. 39

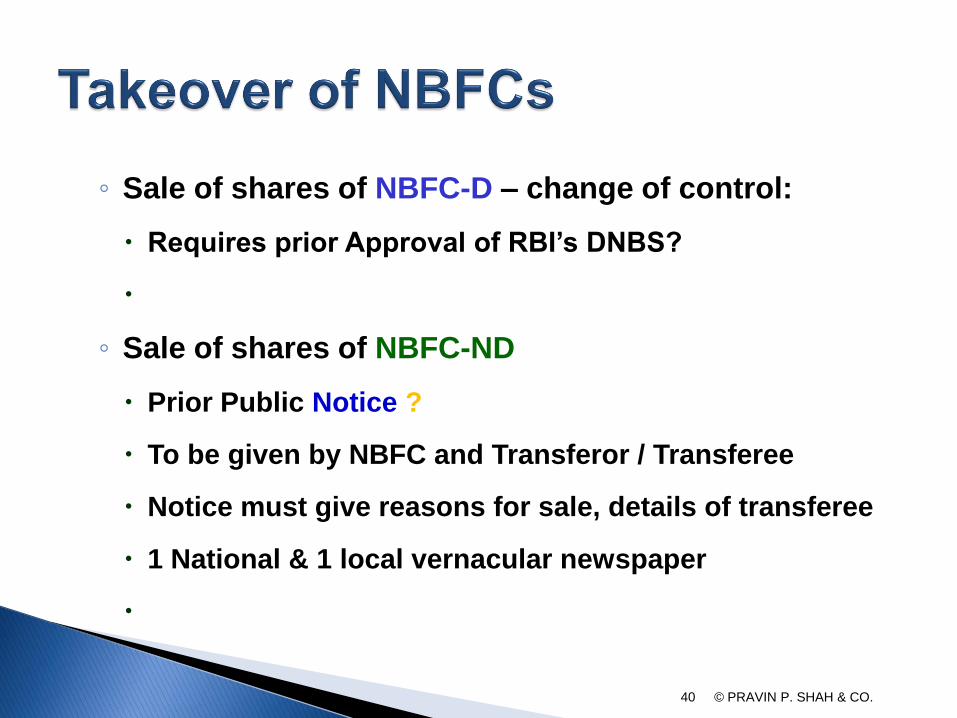

◦ Sale of shares of NBFC-D – change of control:

Requires prior Approval of RBI’s DNBS?

◦ Sale of shares of NBFC-ND

Prior Public Notice ?

To be given by NBFC and Transferor / Transferee

Notice must give reasons for sale, details of transferee

1 National & 1 local vernacular newspaper

© PRAVIN P. SHAH & CO. 40

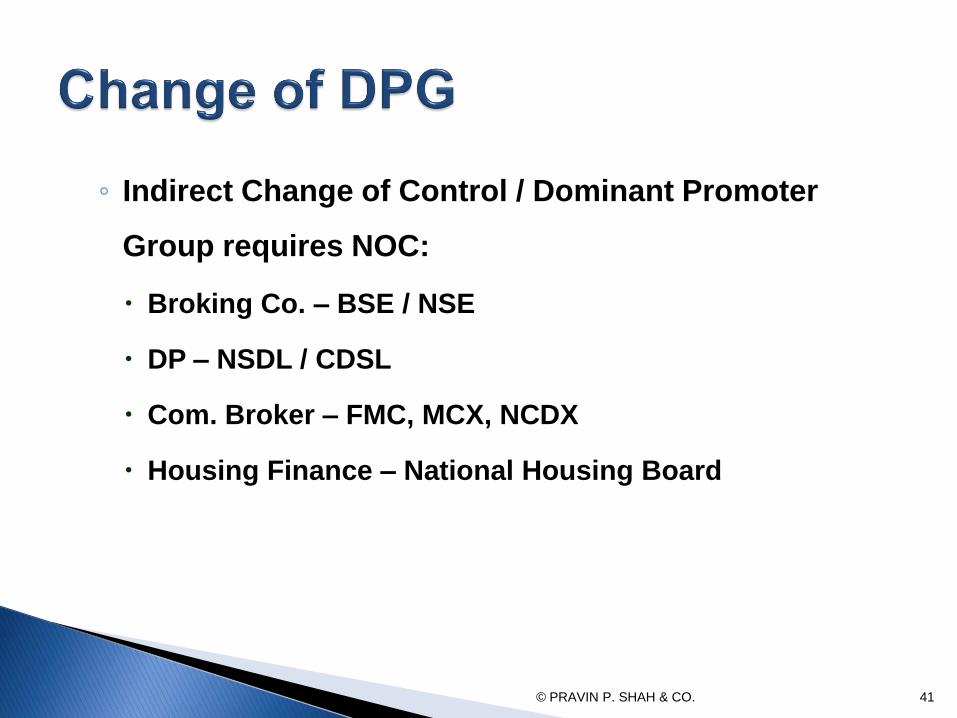

◦ Indirect Change of Control / Dominant Promoter

Group requires NOC:

Broking Co. – BSE / NSE

DP – NSDL / CDSL

Com. Broker – FMC, MCX, NCDX

Housing Finance – National Housing Board

© PRAVIN P. SHAH & CO. 41

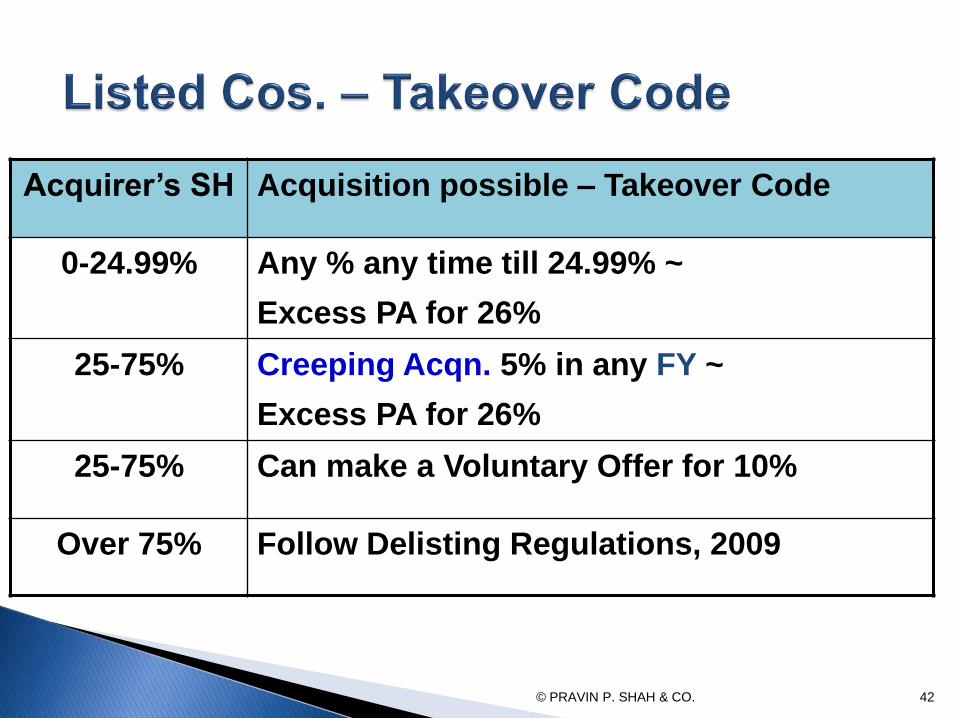

Acquirer’s SH Acquisition possible – Takeover Code

0-24.99% Any % any time till 24.99% ~

Excess PA for 26%

25-75% Creeping Acqn. 5% in any FY ~

Excess PA for 26%

25-75% Can make a Voluntary Offer for 10%

Over 75% Follow Delisting Regulations, 2009

© PRAVIN P. SHAH & CO. 42

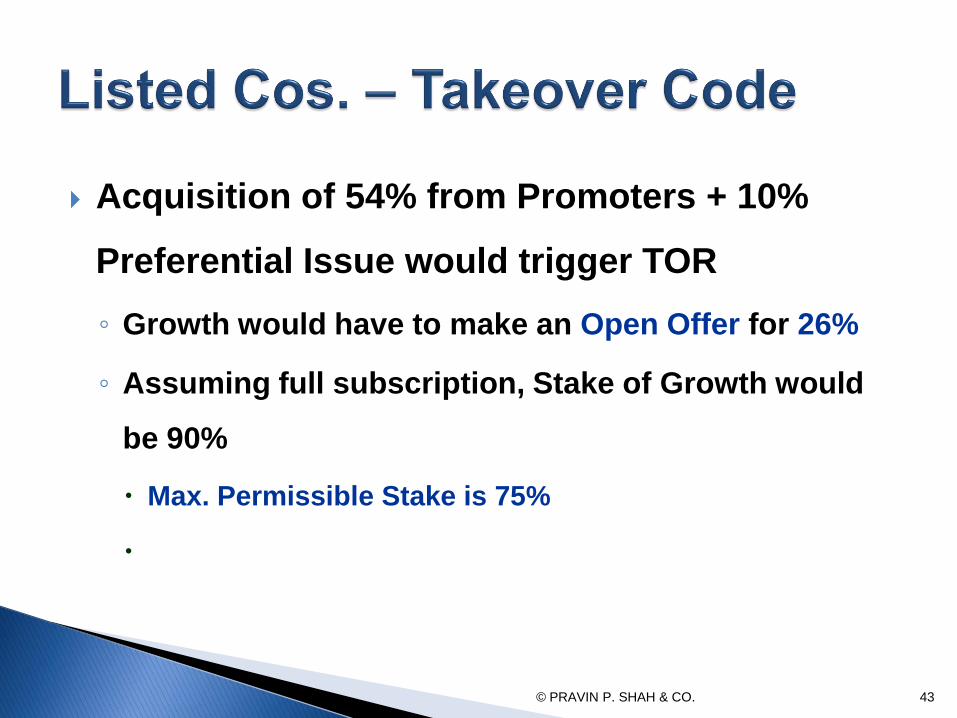

Acquisition of 54% from Promoters + 10%

Preferential Issue would trigger TOR

◦ Growth would have to make an Open Offer for 26%

◦ Assuming full subscription, Stake of Growth would

be 90%

Max. Permissible Stake is 75%

© PRAVIN P. SHAH & CO. 43

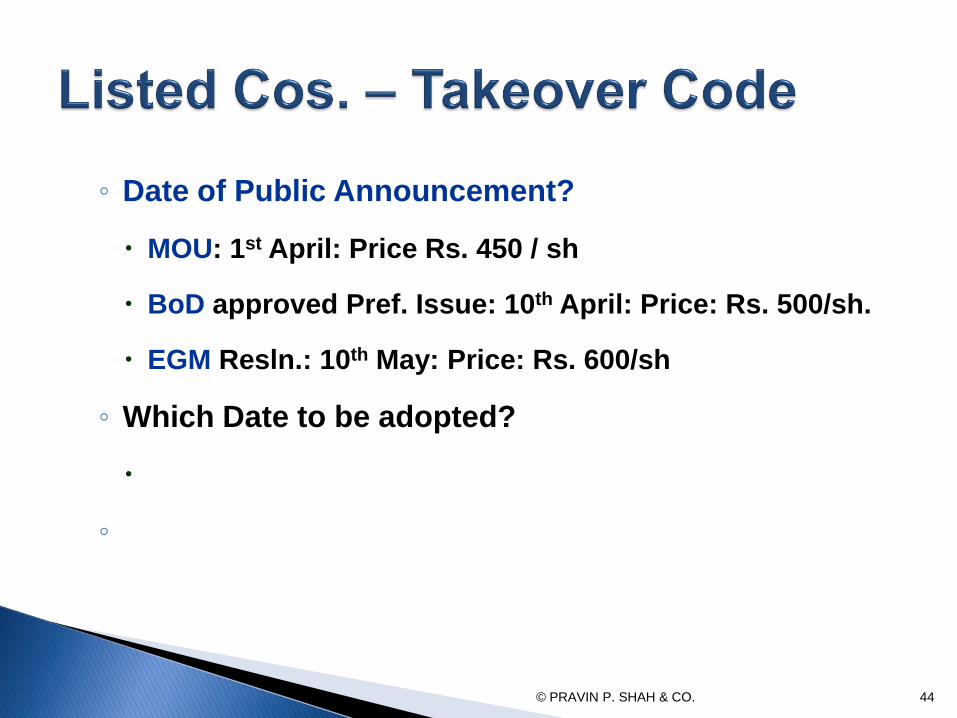

◦ Date of Public Announcement?

MOU: 1st April: Price Rs. 450 / sh

BoD approved Pref. Issue: 10th April: Price: Rs. 500/sh.

EGM Resln.: 10th May: Price: Rs. 600/sh

◦ Which Date to be adopted?

◦

© PRAVIN P. SHAH & CO. 44

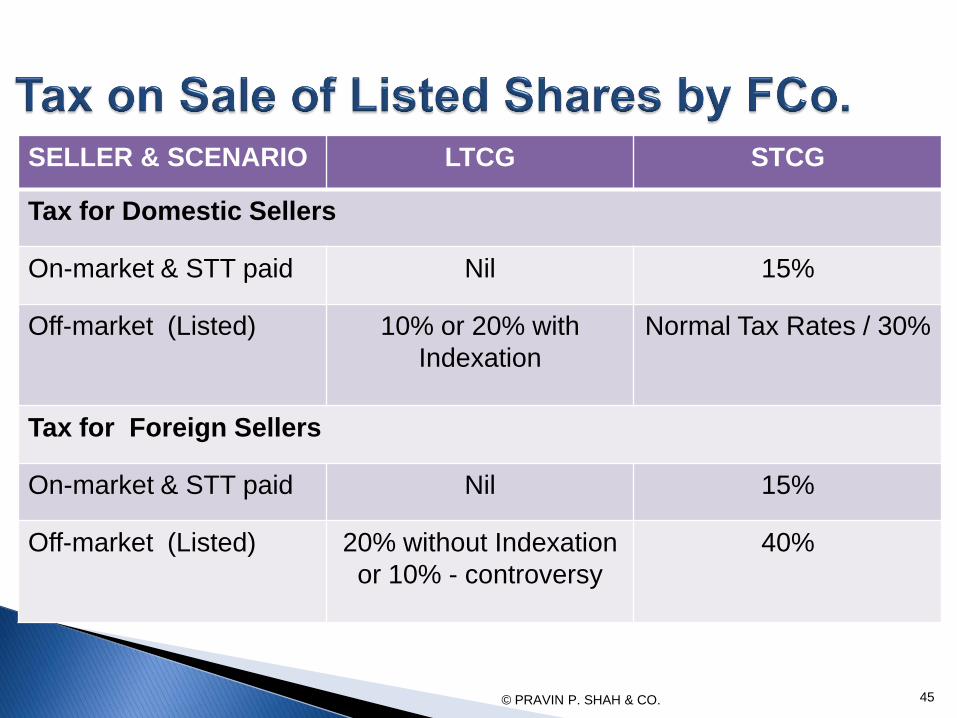

SELLER & SCENARIO LTCG STCG

Tax for Domestic Sellers

On-market & STT paid Nil 15%

Off-market (Listed) 10% or 20% with

Indexation

Normal Tax Rates / 30%

Tax for Foreign Sellers

On-market & STT paid Nil 15%

Off-market (Listed) 20% without Indexation

or 10% - controversy

40%

© PRAVIN P. SHAH & CO. 45

Controversy

Foreign Sellers selling Listed Shs. on off-market basis

◦ Q. Concessional rate of 10% available to FCo? (s.112)

Mum ITAT – No in BASF AG (Mum)

Mum ITAT – Yes in Chicago Pneumatic Tool Company (Mum)

AAR – Yes in Timken / McLeod Russel / Fujitsu Services Ltd

AAR – No in Cairns UK, Castleton Investment

Judicial Controversy?

© PRAVIN P. SHAH & CO. 46

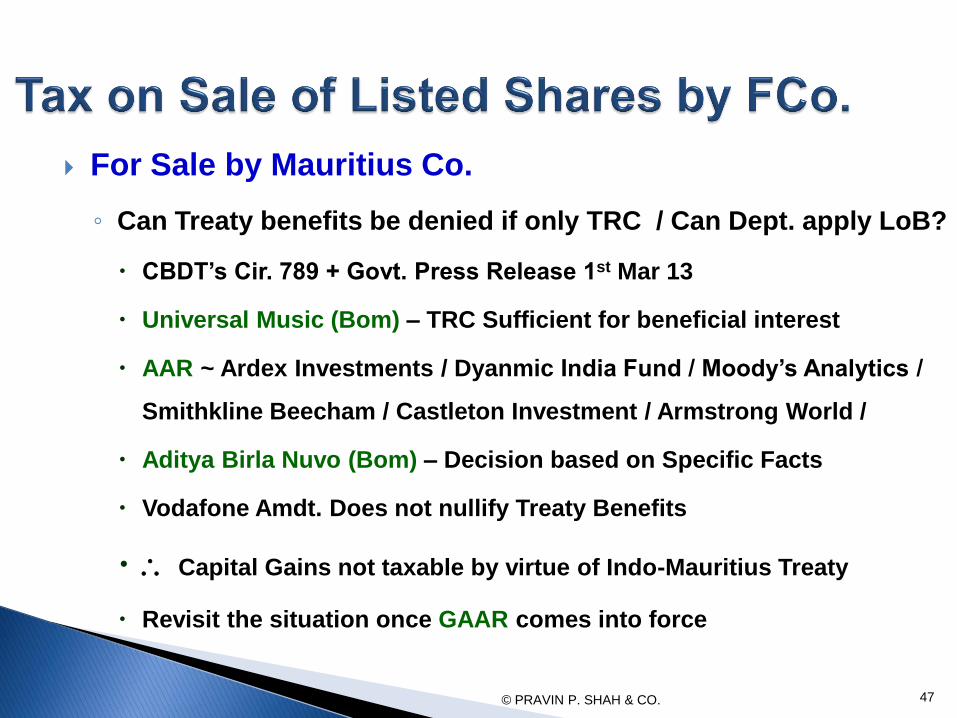

For Sale by Mauritius Co.

◦ Can Treaty benefits be denied if only TRC / Can Dept. apply LoB?

CBDT’s Cir. 789 + Govt. Press Release 1st Mar 13

Universal Music (Bom) – TRC Sufficient for beneficial interest

AAR ~ Ardex Investments / Dyanmic India Fund / Moody’s Analytics /

Smithkline Beecham / Castleton Investment / Armstrong World /

Aditya Birla Nuvo (Bom) – Decision based on Specific Facts

Vodafone Amdt. Does not nullify Treaty Benefits

Capital Gains not taxable by virtue of Indo-Mauritius Treaty

Revisit the situation once GAAR comes into force

© PRAVIN P. SHAH & CO. 47

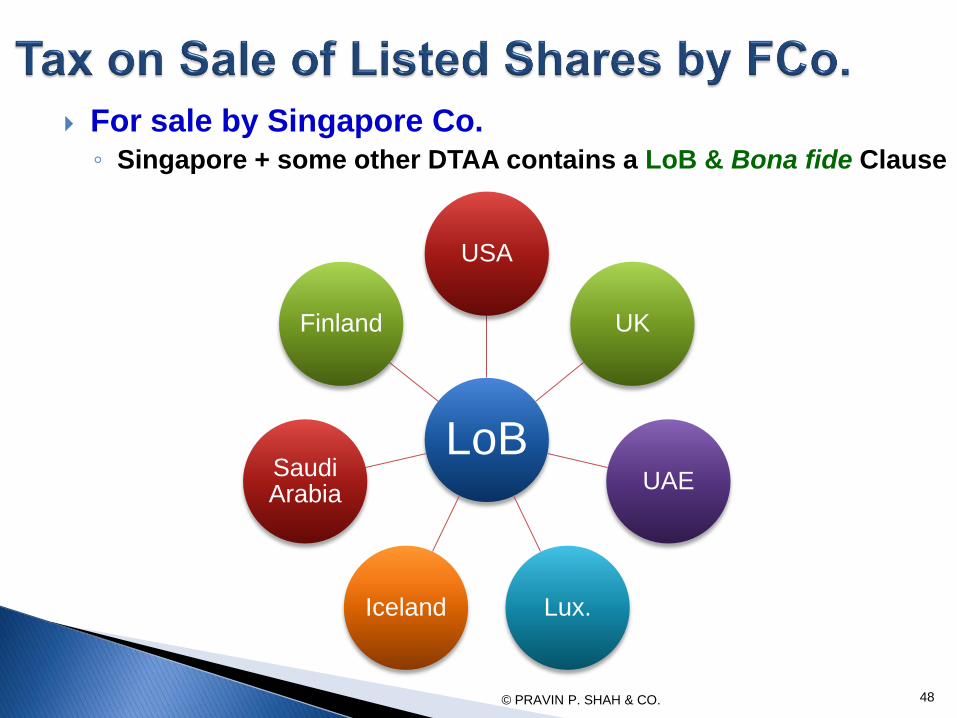

For sale by Singapore Co. ◦ Singapore + some other DTAA contains a LoB & Bona fide Clause

© PRAVIN P. SHAH & CO. 48

LoB

USA

UK

UAE

Lux. Iceland

Saudi Arabia

Finland

If at all Tax payable by FCo.

◦ Both Buyer and Seller Located Abroad

Payment received abroad but shares located in India

Would Foreign Buyer have to deduct tax at source on payments

made to Foreign Seller?

◦

© PRAVIN P. SHAH & CO. 49

If at all Tax payable by FCo.

◦ Can AO impute CG if sale price lower than DCF Valn. Under FEMA

Guidelines?

◦ If Sale to Associate Enterprises

DCF can be used for determining ALP?

Can Auto Approval of RBI be considered as deemed ALP?

© PRAVIN P. SHAH & CO. 50

MAT

◦ Is It applicable on Sale of Shares by Foreign Cos.?

Does MAT only apply to Indian Cos.?

Does it apply to Foreign Cos. only if they have a PE?

© PRAVIN P. SHAH & CO. 51

Return

◦ Foreign Seller has to file a Return in India even though no

tax liability

◦ Necessary to have all facts in a wide amplitude

◦ AAR ~ VNU International / Dana Corp., Castleton

Investment Ltd.

Stamp Duty

◦ Transfer Deed @ 0.25% if not in demat form

◦ If SPA executed Addl. Duty?

© PRAVIN P. SHAH & CO. 52

◦ Can Growth AG set up an Indian WOS to buy Wealth?

FDI in WOS requires FIPB Approval

Status of WOS?

Leveraging debt?

Downstream Invst. Provisions if O& C by NRs

Comply with Sectoral Caps, Pricing, Reporting conditions

Can Fco issue its own shares as consideration to SH of

Ico?

© PRAVIN P. SHAH & CO. 53

◦ Conditions for repatriation of FDI Funds by Real estate co.

Minimum Capitalisation - Met

3 years lock-in: Expire on Oct 2013

50% of Project must be developed?

◦ Can Hyper (NR) sell to another NR during lock-in Period?

No outflow /remittance from Indian Co. Space

Is lock-in qua Investor or qua Investment?

© PRAVIN P. SHAH & CO. 55

Can Hyper (NR) sell to Promoter (Domestic Investor) in 3 years?

Can Hyper’s shareholder (Cipher) sell the shares of Hyper to

Viber (another NR) before 3 years?

No transaction at Indian level

Transfer of Foreign Investor offshore

For such Indirect transfers consider impact of Amendment to s.9 –

Vodafone.

© PRAVIN P. SHAH & CO. 56

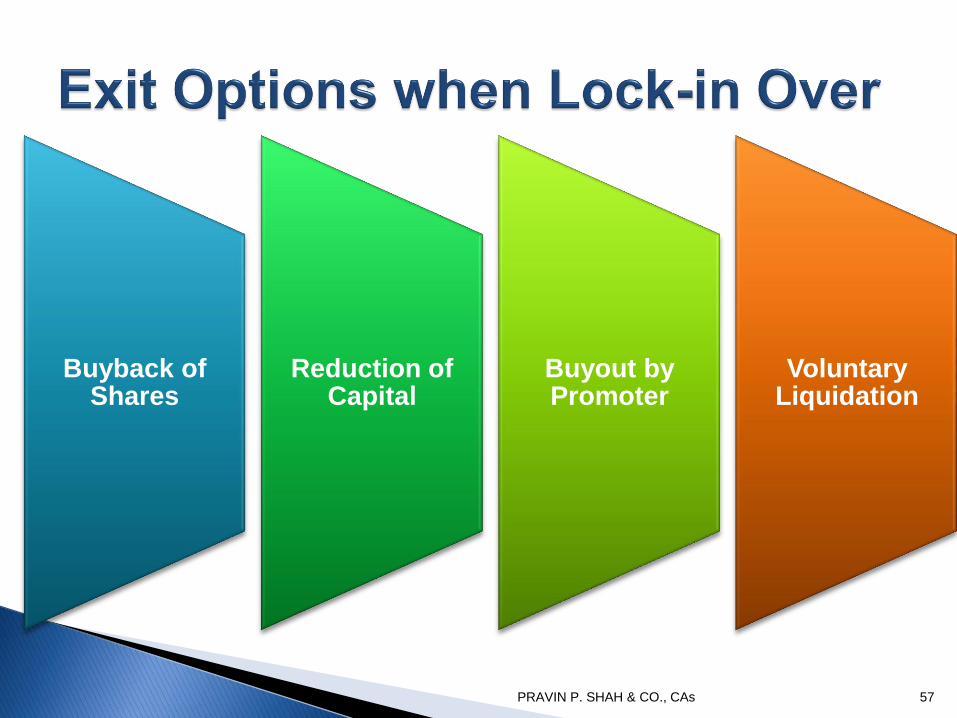

PRAVIN P. SHAH & CO., CAs 57

Buyback of Shares

Reduction of Capital

Buyout by Promoter

Voluntary Liquidation

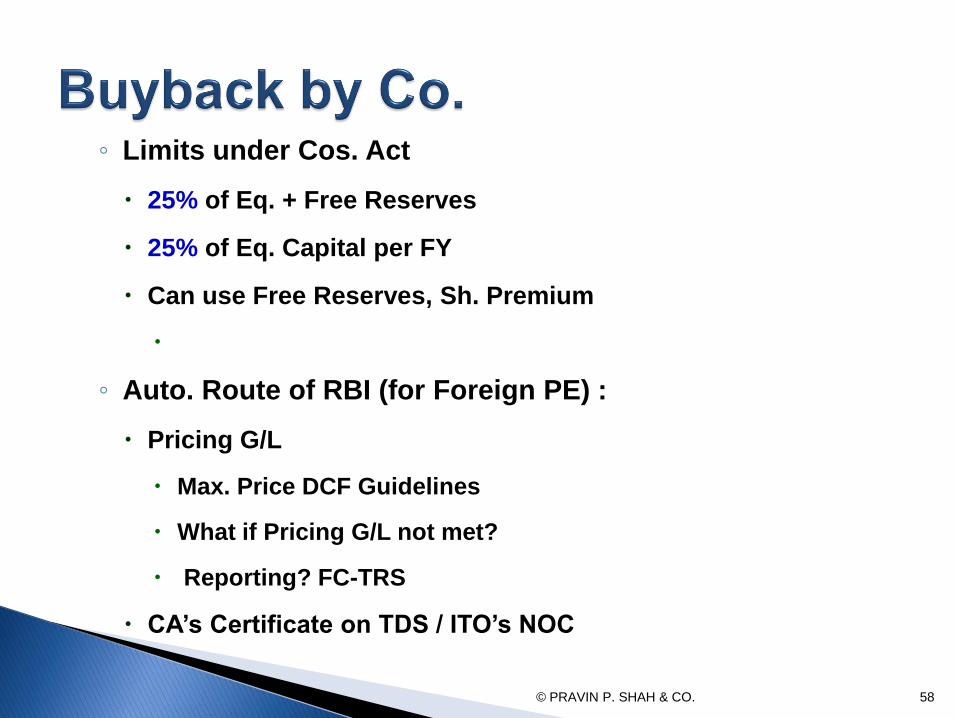

◦ Limits under Cos. Act

25% of Eq. + Free Reserves

25% of Eq. Capital per FY

Can use Free Reserves, Sh. Premium

◦ Auto. Route of RBI (for Foreign PE) :

Pricing G/L

Max. Price DCF Guidelines

What if Pricing G/L not met?

Reporting? FC-TRS

CA’s Certificate on TDS / ITO’s NOC

© PRAVIN P. SHAH & CO. 58

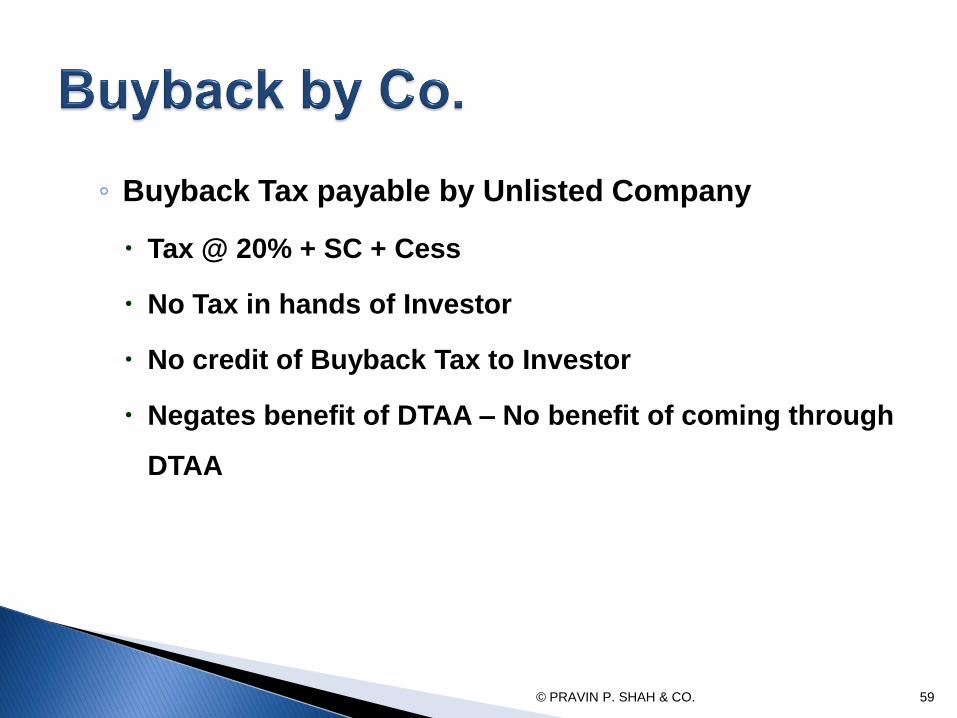

◦ Buyback Tax payable by Unlisted Company

Tax @ 20% + SC + Cess

No Tax in hands of Investor

No credit of Buyback Tax to Investor

Negates benefit of DTAA – No benefit of coming through

DTAA

© PRAVIN P. SHAH & CO. 59

Reduction of shares held by PE / FDI alone

◦ Shares cancelled and consideration paid

◦ Court process u/s. 100 of Companies Act

◦ Selective Reduction possible

◦ Auto Route of RBI subject to Pricing Guidelines

© PRAVIN P. SHAH & CO. 60

Reduction @ Price not higher than DCF Valuation

Tax consequences

Co. liable to pay DDT up to Accumulated Profits

Excess of consideration over Cost & Dividend = LTCG

No tax on Cap Gains if Treaty benefits available to Mauritian

Investor

Bennett Coleman (Mum SB) – No Cap Gain or Loss

© PRAVIN P. SHAH & CO. 61

Automatic Route of RBI

Pricing Guidelines:

◦ Valuation- Not higher than? DCF

◦ Reporting requirements? FC-TRS

CA’s Certificate on TDS / ITO’s NOC

© PRAVIN P. SHAH & CO. 62

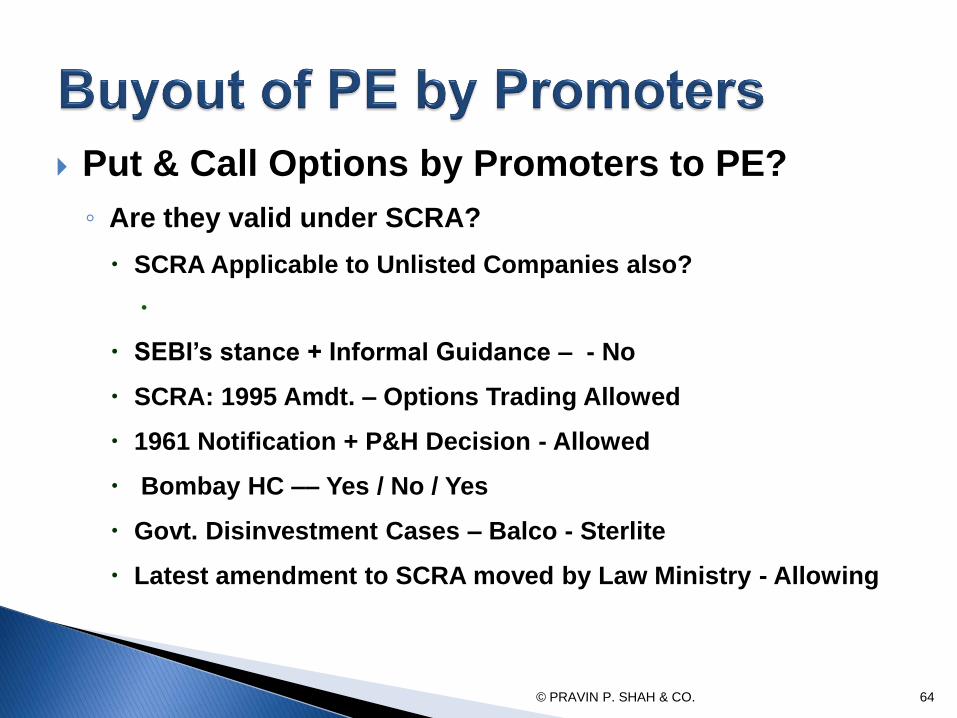

Put & Call Options by Promoters to PE?

◦ Are they valid under FEMA?

RBI’s stance – Indirect ECB – Thus, Not Allowed

CFDIP – Amdt. & Deletion

What if Fixed Price Exit

Not Allowed by RBI

What if subject to Pricing G/L – Should be permissible

© PRAVIN P. SHAH & CO. 63

Put & Call Options by Promoters to PE?

◦ Are they valid under SCRA?

SCRA Applicable to Unlisted Companies also?

SEBI’s stance + Informal Guidance – - No

SCRA: 1995 Amdt. – Options Trading Allowed

1961 Notification + P&H Decision - Allowed

Bombay HC –– Yes / No / Yes

Govt. Disinvestment Cases – Balco - Sterlite

Latest amendment to SCRA moved by Law Ministry - Allowing

© PRAVIN P. SHAH & CO. 64

Pre-emptive

RoFR

Tag Along

Drag Along

Russian Roulette

Texas Shoot Out

Dutch Auction

© PRAVIN P. SHAH & CO. 65

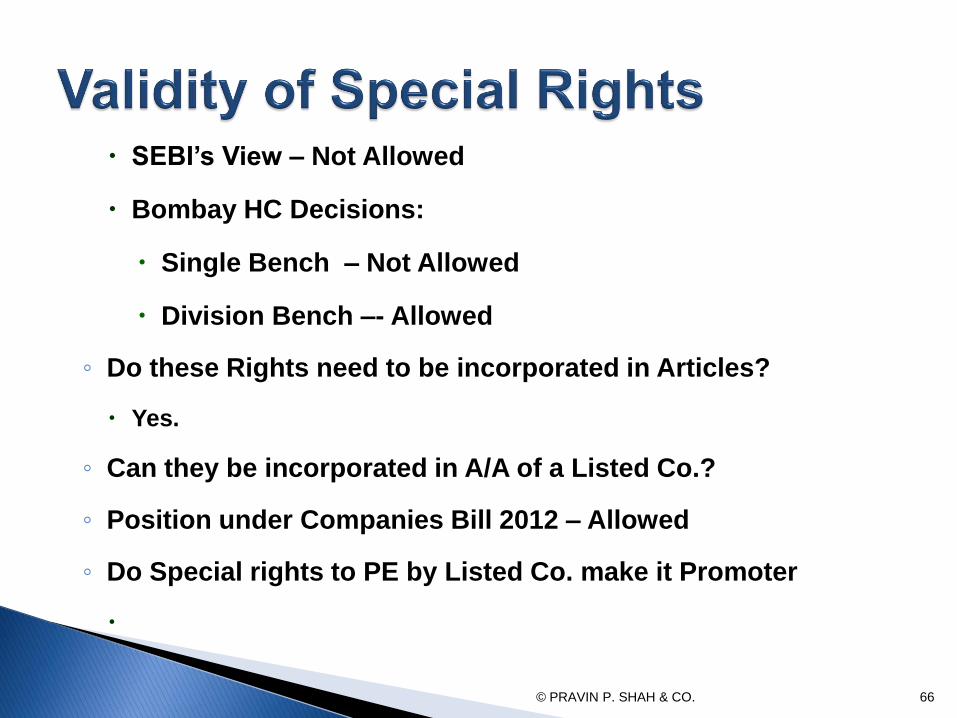

SEBI’s View – Not Allowed

Bombay HC Decisions:

Single Bench – Not Allowed

Division Bench –- Allowed

◦ Do these Rights need to be incorporated in Articles?

Yes.

◦ Can they be incorporated in A/A of a Listed Co.?

◦ Position under Companies Bill 2012 – Allowed

◦ Do Special rights to PE by Listed Co. make it Promoter

© PRAVIN P. SHAH & CO. 66

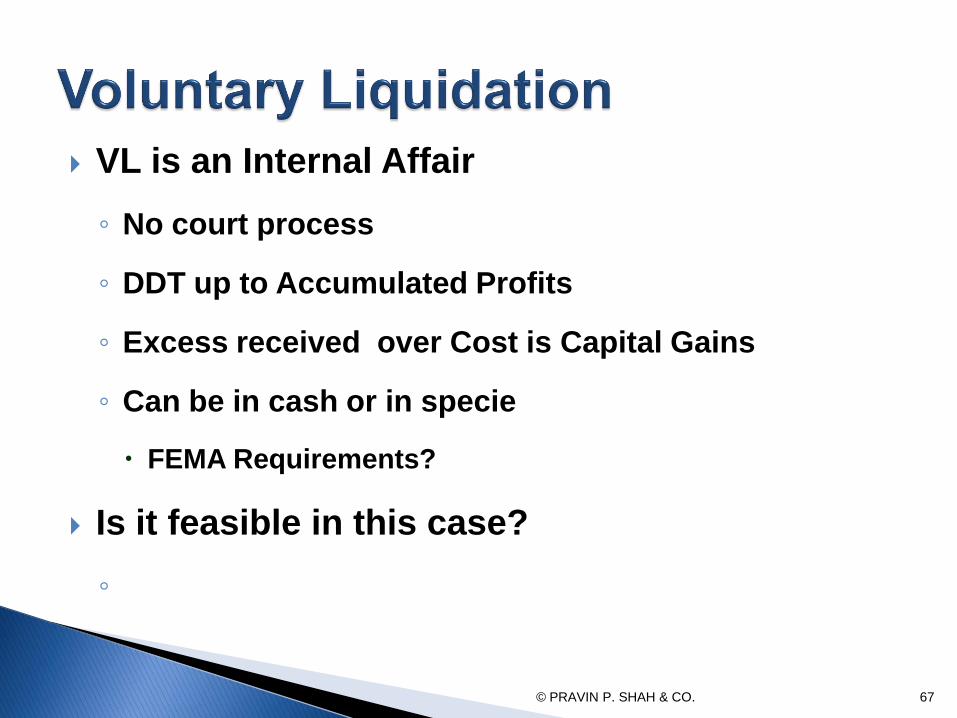

VL is an Internal Affair

◦ No court process

◦ DDT up to Accumulated Profits

◦ Excess received over Cost is Capital Gains

◦ Can be in cash or in specie

FEMA Requirements?

Is it feasible in this case?

◦

© PRAVIN P. SHAH & CO. 67

© PRAVIN P. SHAH & CO. 69

Foreign Group Holding Co.

Listing abroad – NYSE, Euronext, FTSE, AIM

Better valuation – Makemytrip, WNS, Genpact

Can retain funds abroad

◦ Most Important Pre-requisite

Who would be the Promoter of Foreign Holdco?

Holdco should not be wholly C&M not in India

© PRAVIN P. SHAH & CO. 70

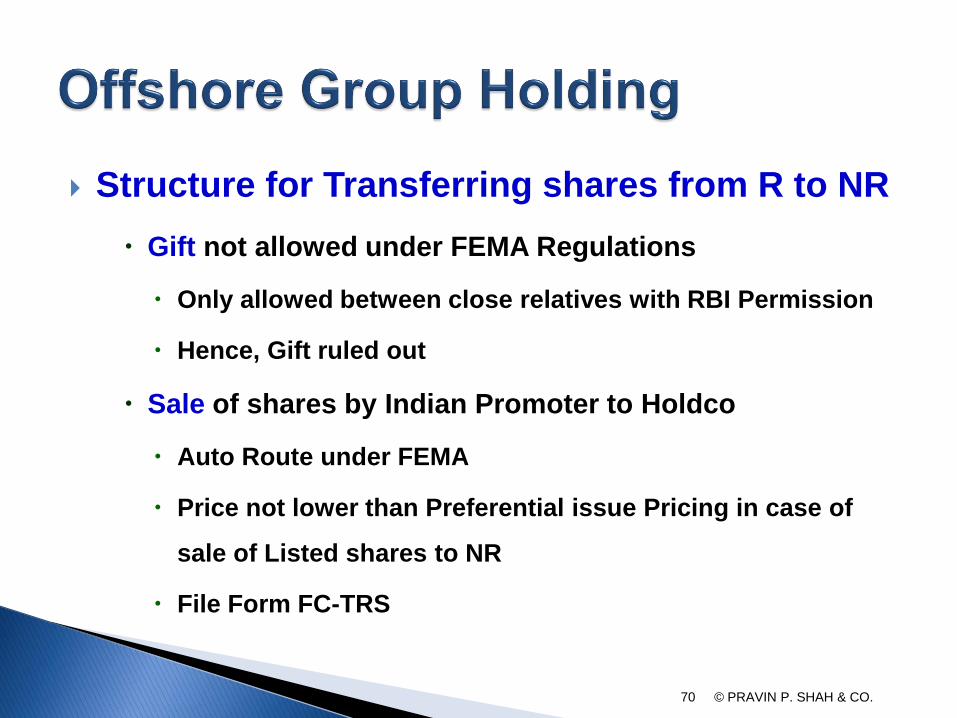

Structure for Transferring shares from R to NR

Gift not allowed under FEMA Regulations

Only allowed between close relatives with RBI Permission

Hence, Gift ruled out

Sale of shares by Indian Promoter to Holdco

Auto Route under FEMA

Price not lower than Preferential issue Pricing in case of

sale of Listed shares to NR

File Form FC-TRS

© PRAVIN P. SHAH & CO. 71

Sale of shares by Indian Promoter to Holdco

Can Listed Shares be sold on floor of St. Ex.?

If yes, then no Tax on LTCG to seller

If Off-market sale @ FMV

Tax on Resident Seller

© PRAVIN P. SHAH & CO. 72

Sale of shares by Indian Promoter to Holdco

Can promoter sell @ below FMV

Stamp Duty @ 0.25% if not in demat form

If SPA executed Addl. Duty in Maharashtra

© PRAVIN P. SHAH & CO. 73

Takeover Code implications

Transfer of shares held by Mr. A or his Investment Cos.

to Holdco entirely held by him

Consider Exemptions u./R. 10(1)(a)

Or else approach SEBI for Specific Exemption u/R11(1)

© PRAVIN P. SHAH & CO. 74

© PRAVIN P. SHAH & CO. 75

© PRAVIN P. SHAH & CO. 76