anti fraud training course - home - avepa · anti fraud training course risks of fraud: measurement...

TRANSCRIPT

Anti Fraud training course

Risks of fraud: measurement models for and analysis supporting tools

Padova, May 6-26th 2015

This event is supported by the European Union Programme Hercule III (2014-2020). This programme is implemented by the European Commission.

It was established to promote activities in the field of the protection of the financial interests of the European Union. (for more information see http://ec.europa.eu/anti_fraud/about-us/funding/index_en.htm)'

Risks of fraud: measurement models for and analysis supporting tools

Padova, May 26th 2015

This document reflects the author’s view and the European Commission is not responsible for the views displayed in the publications and/or in conjunction with the activities for which the grant is used.

The information contained in this publication does not necessarily reflect the position or opinion of the European Commission.

Mr. Andrea Chiusani Mr. Luca MarzegalliMr. Piero Di MicheleMr. Marco Ferrara

Introduction to Data Analysis

Rules based analysis and Alerting tools

Models for Data Analysis

Dashboarding and decision process

eDiscovery

Link Analysis

Agenda

Introduction to Data Analysis

Why Fraud Data Analytics

Data Analytics (DA) is the science that dealswith examining the data (structured and rough)in order to draw conclusions on suchinformation.

Data Analytics is used in large companies andorganizations in order to support themanagement in identifying the best businessdecisions.

Data Analytics Object

spiegare causa-effetto dei fenomeni

Individuare un particolare problema

anticipare gli eventi che possono determinare il futuro di una azienda

Cause and Effect

Identify specific problem

Improve future actions

Anti fraud control through inspection of 100% of transactions

Automating the analysis of forensic auditors and fraud examiners

Retrospective and/or real time

Independently validate compliance with company code of conduct

Measures gap between policy and expectation vs. what really happens and report on control effectiveness

Detect risks as they happen - when they are less costly and less complex to prove, correct and remediate

Why Fraud Data Analytics

ERROR

WASTE MISUSE

ABUSE FRAUD

Detection

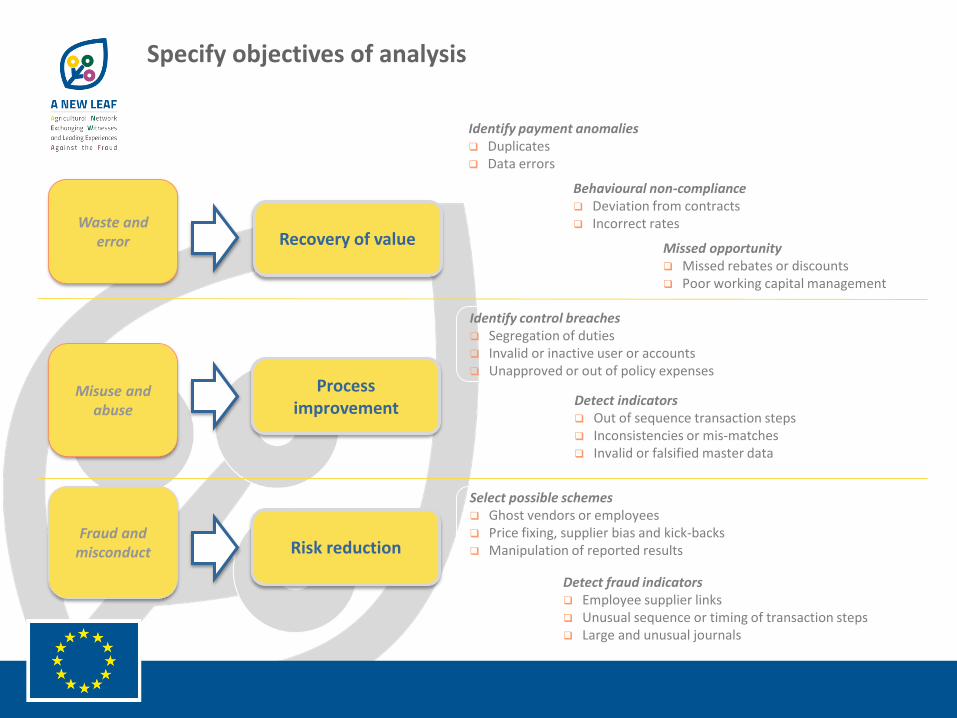

Recovery of valueWaste and

error

Identify payment anomalies Duplicates Data errors

Behavioural non-compliance Deviation from contracts Incorrect rates

Missed opportunity Missed rebates or discounts Poor working capital management

Misuse and abuse

Identify control breaches Segregation of duties Invalid or inactive user or accounts Unapproved or out of policy expenses

Detect indicators Out of sequence transaction steps Inconsistencies or mis-matches Invalid or falsified master data

Fraud and misconduct

Select possible schemes Ghost vendors or employees Price fixing, supplier bias and kick-backs Manipulation of reported results

Detect fraud indicators Employee supplier links Unusual sequence or timing of transaction steps Large and unusual journals

Specify objectives of analysis

Process improvement

Risk reduction

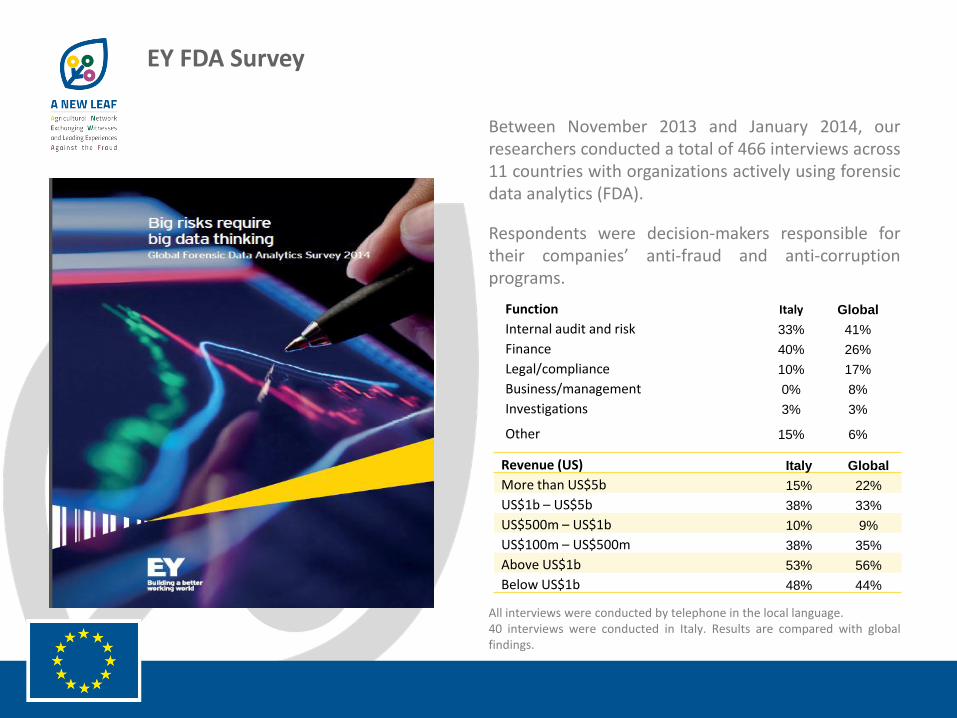

Between November 2013 and January 2014, ourresearchers conducted a total of 466 interviews across11 countries with organizations actively using forensicdata analytics (FDA).

Respondents were decision-makers responsible fortheir companies’ anti-fraud and anti-corruptionprograms.

All interviews were conducted by telephone in the local language.40 interviews were conducted in Italy. Results are compared with globalfindings.

Function Italy Global

Internal audit and risk 33% 41%

Finance 40% 26%

Legal/compliance 10% 17%

Business/management 0% 8%

Investigations 3% 3%

Other 15% 6%

Revenue (US) Italy Global

More than US$5b 15% 22%

US$1b – US$5b 38% 33%

US$500m – US$1b 10% 9%

US$100m – US$500m 38% 35%

Above US$1b 53% 56%

Below US$1b 48% 44%

EY FDA Survey

Forensic Data Analytics primary benefits

Global results

Italy Total TransportationConsumer

productsManufacturing

Financial

services

Life

sciencesMining

Oil and

gas

Technology,

communications

and entertainment

38 422 28 85 30 100 47 23 88 21

Spreadsheet tools such as

Microsoft Excel39% 65% 75% 79% 77% 55% 55% 57% 63% 62%

Database tools such as Microsoft

Access or Microsoft SQL Server26% 43% 39% 53% 37% 44% 43% 13% 42% 57%

Forensic analytics software (ACL,

IDEA)11% 26% 25% 21% 27% 24% 36% 26% 27% 24%

Statistical analysis and data mining

packages11% 11% 0% 11% 10% 14% 15% 4% 13% 14%

Continuous monitoring tools, which

may include governance risk and

compliance tools

24% 29% 25% 26% 27% 26% 36% 35% 35% 19%

Visualization and reporting tools 8% 12% 18% 16% 7% 11% 13% 4% 10% 10%

Big data technologies 0% 2% 4% 1% 0% 3% 4% 0% 2% 0%

Text analytics tools or keyword

searching24% 26% 14% 33% 37% 21% 28% 22% 25% 24%

Social media/web monitoring tools 16% 21% 18% 25% 23% 23% 21% 4% 17% 24%

Voice searching and analysis 0% 2% 0% 2% 0% 3% 4% 0% 1% 5%

Data Analytics tools used in organization

Focus on quick win: prioritize initial objectives of the project

Communicate: share information on early successes within the company and among the business units, in order to gain internal consensus

Go beyond rule based analytics

Deliveries take time: avoid the last minute rush

Data Analytics – Top 5 success factor

In Italy:

51% of people interviewed consider corruption as the main risk of fraud which they are exposed to

75% of italian companies use Forensic Data Analytics (FDA) tools in order to reduce the riskof fraud and corruption

According to 89% of the people surveyed, the benefits produced by FDA tools derive from «their capability to incercept potentially poor behaviour», hard to find by other means

70% of companies interviewed believe that new FDA technologies applied to large amountsof information (i.e. «Big Data») are gaining a central role in prevention and detection of suspect behaviours within the company.

EY FDA Survey – Italian market

Rules based analysis and Alerting tools

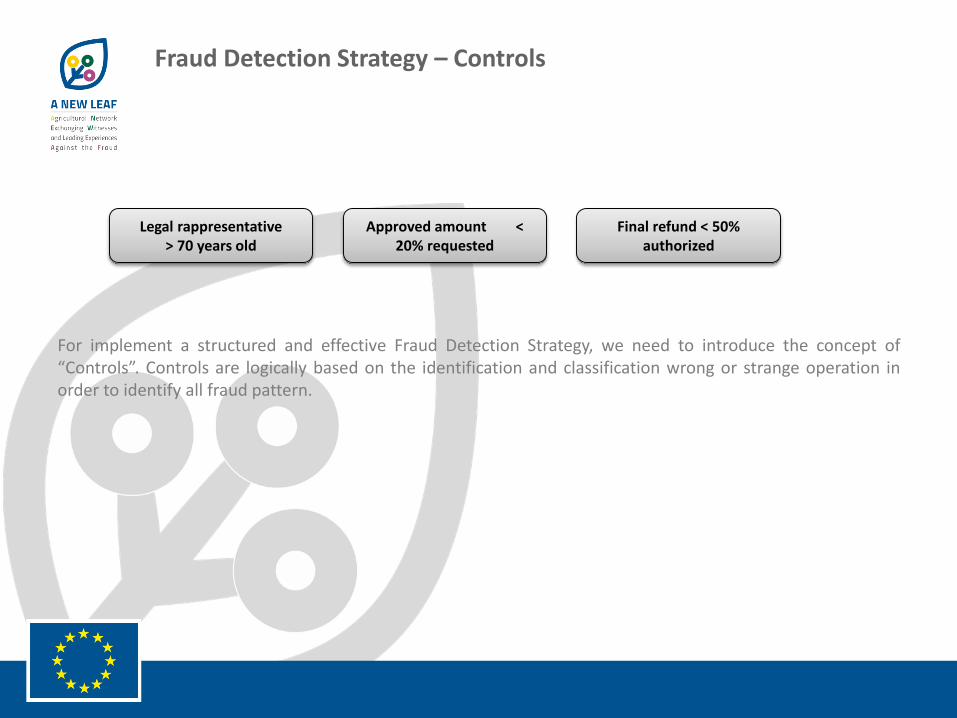

Fraud Detection Strategy – Controls

Legal rappresentative > 70 years old

Approved amount < 20% requested

Final refund < 50% authorized

For implement a structured and effective Fraud Detection Strategy, we need to introduce the concept of“Controls”. Controls are logically based on the identification and classification wrong or strange operation inorder to identify all fraud pattern.

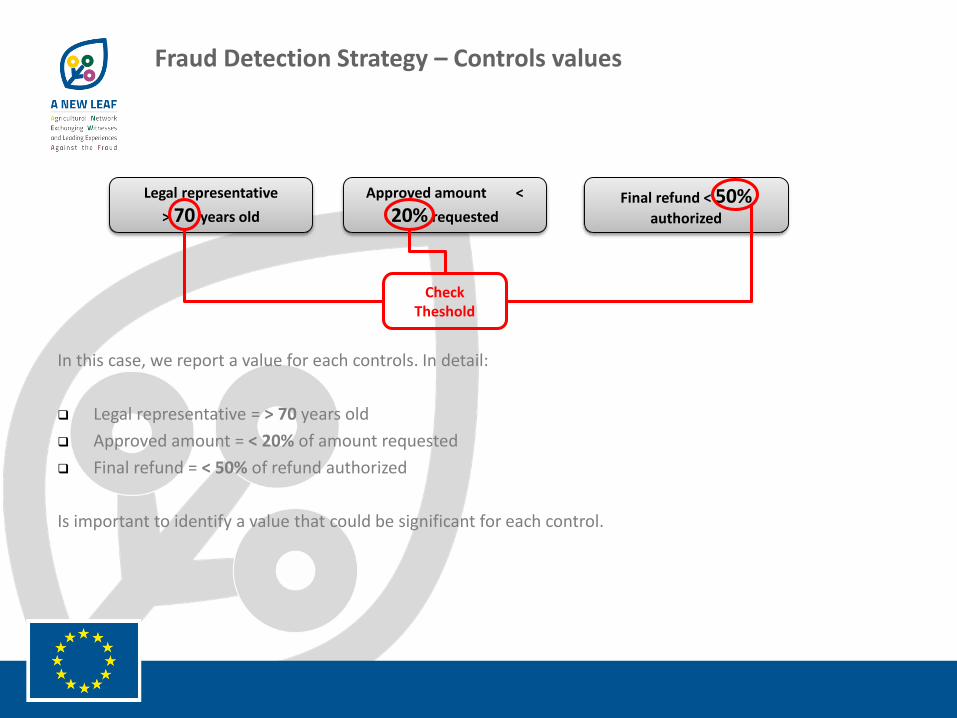

Fraud Detection Strategy – Controls values

Legal representative

> 70 years old

Approved amount <

20% requestedFinal refund < 50%

authorized

Check Theshold

In this case, we report a value for each controls. In detail:

Legal representative = > 70 years old

Approved amount = < 20% of amount requested

Final refund = < 50% of refund authorized

Is important to identify a value that could be significant for each control.

Fraud Detection Strategy – Measure

Scoring Overall

Legal representative > 70 years old

Approved amount < 20% requested

Final refund < 50% authorized

Measure TOT 100

30 60 10

For each control, in order to calculate the math formulas, could be assigned a specific value. In this example weassigned:

Legal representative > 70 years old = 30

Approved amount < 20% of amount requested = 60

Final refund < 50% of refund authorized = 10

The total of all control’s value is 100.

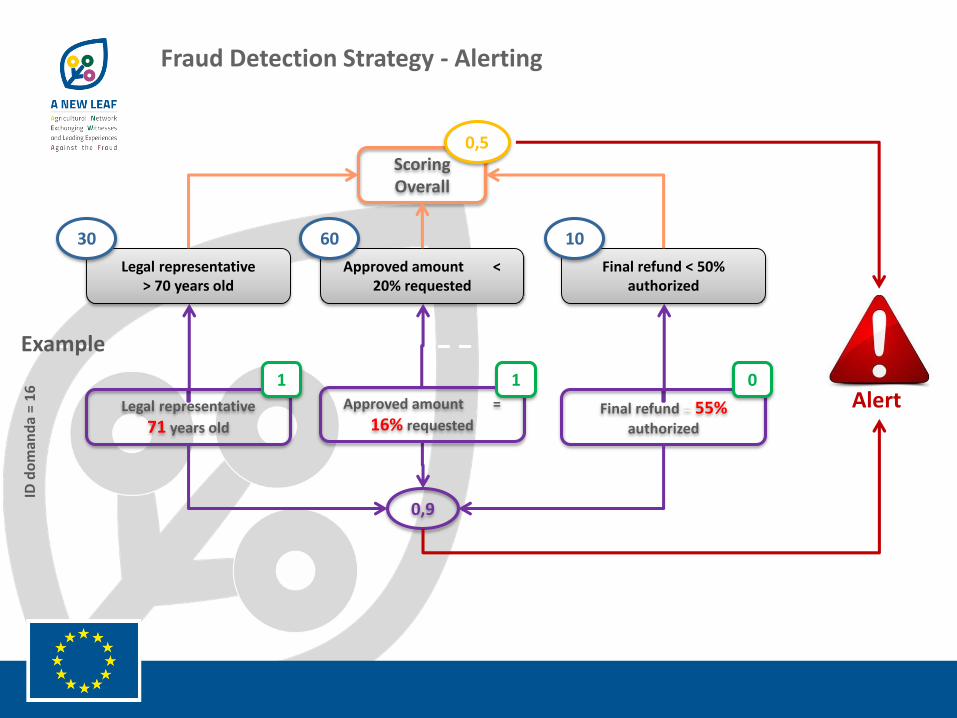

Fraud Detection Strategy – Alert threshold

Scoring Overall

Legal representative > 70 years old

Approved amount < 20% requested

Final refund < 50% authorized

30 60 10

0,5Alert

Threshold

For the scoring overall, could be assigned a value that separate the alert threshold operation. If the value ofspecific controls are wired than the level designed, so the system has an alert.

Fraud Detection Strategy – Example values

Scoring Overall

Legal representative > 70 years old

Approved amount < 20% requested

Final refund < 50% authorized

30 60 10

Legal representative

71 years old

1

Final refund = 55%authorized

Example

ID d

om

and

a =

16

Approved amount = 16%requested

1 0

0,5

1 = True0 = False

Fraud Detection Strategy – Example result

Scoring Overall

Legal representative > 70 years old

Approved amount < 20% requested

Final refund < 50% authorized

30 60 10

Legal representative

71 years old

1

Final refund = 55%authorized

(1x30) + (1x60) + (0x10)

100

Example

ID d

om

and

a =

16

Approved amount =

16% requested

1 0

0,5

0,9

Fraud Detection Strategy - Alerting

Scoring Overall

Legal representative > 70 years old

Approved amount < 20% requested

Final refund < 50% authorized

30 60 10

Legal representative

71 years old

1

Final refund = 55%authorized

Example

ID d

om

and

a =

16

Approved amount =

16% requested

1 0

0,5

0,9

Alert

Excel example: data

Excel example: formulas

Excel example: conditional formatting

Excel example: output and alarm overall

ALERTING

Advanced Graph and Chart

False Positive – The importance of analysis

Allowed FraudAll request

ID Request: 1

. . . .

ID Request: 2

ID Request: 3

ID Request: 1

ID Request: 2

ID Request: 3

False Positive – Misuse detection

Fraud

Alert

You have to define as unacceptable behavior and identify the misuse.

ID Request: 3

False Positive – Anomaly detection

Allowed

Alert

You have to define as acceptable behavior and identify, logically, the other one.

ID Request: 1

ID Request: 2

False Positive and False Negative

Allowed FraudAllowed Fraud

Misuse detectionAnomaly detection

False Positive : an acceptable behaviour give an alarm

False Negative: an unacceptable behavior don’t give an alarm

False negative

False positive

False positive

False negative

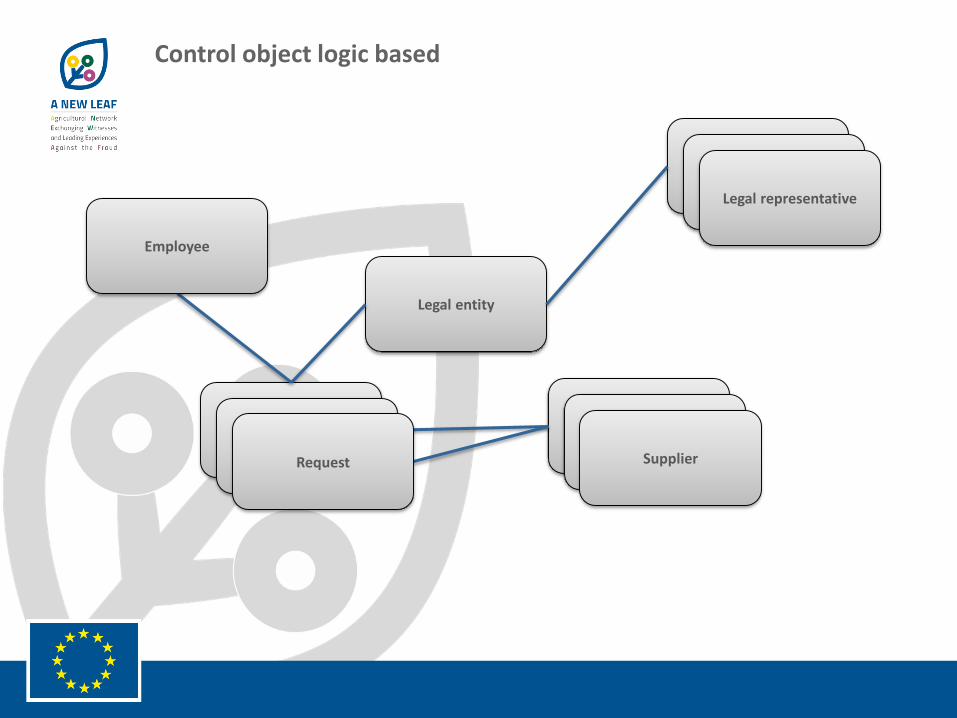

Legal entity

Legal representative

SupplierRequest

Employee

Control object logic based

Legal entity

Legal representative

SupplierRequest

Employee

Control object logic based: example

There are legal representatives that request more than one question?

There is a vendor that appears to only one question, and that has never seen for any other questions?

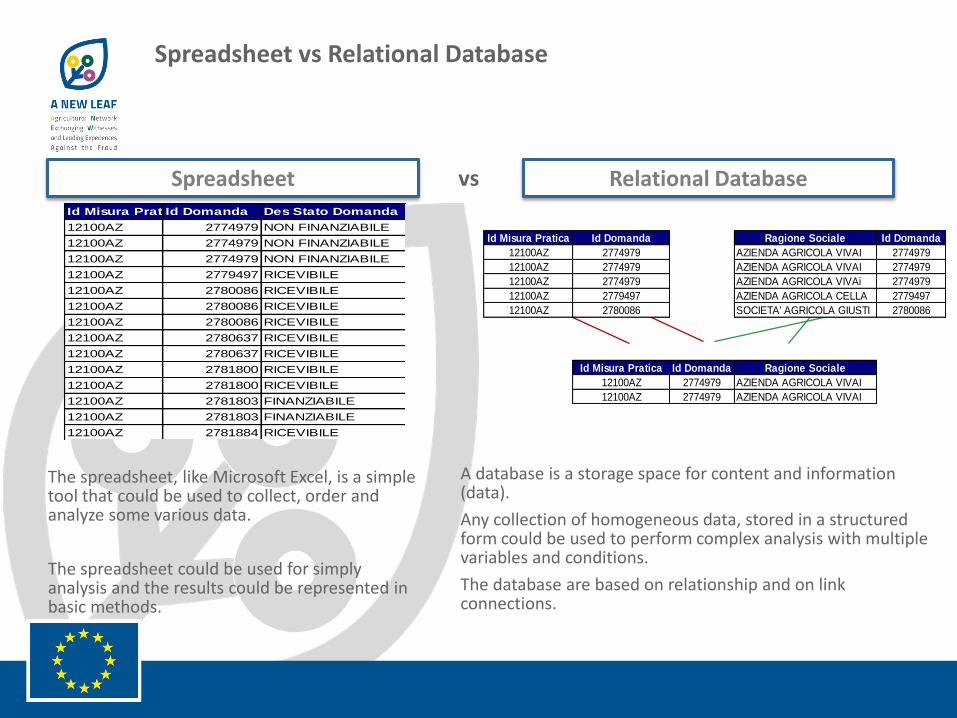

Spreadsheet vs Relational Database

SpreadsheetId Misura PraticaId Domanda Des Stato Domanda Ente Delegato Cuaa Ragione Sociale Indirizzo Sede Legale Cap Sede LegaleDescr Comune Sede LegaleDescr Provincia Sede Legale

12100AZ 2774979 NON FINANZIABILE SPORTELLO UNICO DI ROVIGO DSRFPP77M03H620A AZIENDA AGRICOLA VIVAI DE SERO FILIPPO VIA VERDI GIUSEPPE 113 45010 VILLADOSE ROVIGO

12100AZ 2774979 NON FINANZIABILE SPORTELLO UNICO DI ROVIGO DSRFPP77M03H620A AZIENDA AGRICOLA VIVAI DE SERO FILIPPO VIA VERDI GIUSEPPE 113 45010 VILLADOSE ROVIGO

12100AZ 2774979 NON FINANZIABILE SPORTELLO UNICO DI ROVIGO DSRFPP77M03H620A AZIENDA AGRICOLA VIVAI DE SERO FILIPPO VIA VERDI GIUSEPPE 113 45010 VILLADOSE ROVIGO

12100AZ 2779497 RICEVIBILE SPORTELLO UNICO DI VENEZIA CLLMLE57R09H823U AZIENDA AGRICOLA CELLA EMILIO VIA M POLO 9 30027 SAN DONA' DI PIAVE VENEZIA

12100AZ 2780086 RICEVIBILE SPORTELLO UNICO DI TREVISO 04172990261 SOCIETA' AGRICOLA GIUSTI - DAL COL S.R.L. VIA ZILIO N 1 31041 CORNUDA TREVISO

12100AZ 2780086 RICEVIBILE SPORTELLO UNICO DI TREVISO 04172990261 SOCIETA' AGRICOLA GIUSTI - DAL COL S.R.L. VIA ZILIO N 1 31041 CORNUDA TREVISO

12100AZ 2780086 RICEVIBILE SPORTELLO UNICO DI TREVISO 04172990261 SOCIETA' AGRICOLA GIUSTI - DAL COL S.R.L. VIA ZILIO N 1 31041 CORNUDA TREVISO

12100AZ 2780637 RICEVIBILE SPORTELLO UNICO DI PADOVA TMBNZR64T31E682R TAMBARA NAZZARENO VIA GARZAN 621 37040 ZIMELLA VERONA

12100AZ 2780637 RICEVIBILE SPORTELLO UNICO DI PADOVA TMBNZR64T31E682R TAMBARA NAZZARENO VIA GARZAN 621 37040 ZIMELLA VERONA

12100AZ 2781800 RICEVIBILE SPORTELLO UNICO DI VERONA FRGMSM70C25H783B FRIGOTTO MASSIMO VIA G AROLDI N 22 37032 MONTEFORTE D'ALPONE VERONA

12100AZ 2781800 RICEVIBILE SPORTELLO UNICO DI VERONA FRGMSM70C25H783B FRIGOTTO MASSIMO VIA G AROLDI N 22 37032 MONTEFORTE D'ALPONE VERONA

12100AZ 2781803 FINANZIABILE SPORTELLO UNICO DI PADOVA BLLNTN80M18L364P BELLOMI ANTONIO VIA SANTA GIUSTINA 11 37031 ILLASI VERONA

12100AZ 2781803 FINANZIABILE SPORTELLO UNICO DI PADOVA BLLNTN80M18L364P BELLOMI ANTONIO VIA SANTA GIUSTINA 11 37031 ILLASI VERONA

12100AZ 2781884 RICEVIBILE SPORTELLO UNICO DI TREVISO 04030120267 IRIS VIGNETI SOC.SEMPLICE SOCIETA' AGRICOLAVIA GRAVE 1 SANTA MARIA DI PIAVE31010 MARENO DI PIAVE TREVISO

12100AZ 2781884 RICEVIBILE SPORTELLO UNICO DI TREVISO 04030120267 IRIS VIGNETI SOC.SEMPLICE SOCIETA' AGRICOLAVIA GRAVE 1 SANTA MARIA DI PIAVE31010 MARENO DI PIAVE TREVISO

12100AZ 2781884 RICEVIBILE SPORTELLO UNICO DI TREVISO 04030120267 IRIS VIGNETI SOC.SEMPLICE SOCIETA' AGRICOLAVIA GRAVE 1 SANTA MARIA DI PIAVE31010 MARENO DI PIAVE TREVISO

12100AZ 2782362 FINANZIABILE SPORTELLO UNICO DI TREVISO BNTLDA58A23I124R BONOTTO ALDO VIA FERRAREZZA 18 31020 VILLORBA TREVISO

12100AZ 2782362 FINANZIABILE SPORTELLO UNICO DI TREVISO BNTLDA58A23I124R BONOTTO ALDO VIA FERRAREZZA 18 31020 VILLORBA TREVISO

vs Relational Database

The spreadsheet, like Microsoft Excel, is a simple tool that could be used to collect, order and analyze some various data.

The spreadsheet could be used for simply analysis and the results could be represented in basic methods.

A database is a storage space for content and information (data).

Any collection of homogeneous data, stored in a structured form could be used to perform complex analysis with multiple variables and conditions.

The database are based on relationship and on link connections.

Id Misura Pratica Id Domanda Ragione Sociale Id Domanda

12100AZ 2774979 AZIENDA AGRICOLA VIVAI 2774979

12100AZ 2774979 AZIENDA AGRICOLA VIVAI 2774979

12100AZ 2774979 AZIENDA AGRICOLA VIVAi 2774979

12100AZ 2779497 AZIENDA AGRICOLA CELLA 2779497

12100AZ 2780086 SOCIETA' AGRICOLA GIUSTI 2780086

Id Misura Pratica Id Domanda Ragione Sociale

12100AZ 2774979 AZIENDA AGRICOLA VIVAI

12100AZ 2774979 AZIENDA AGRICOLA VIVAI

Relational Databases - Introduction

Relational databases are category of databases (actually the most common at the moment) in which the dataare stored in tables, originally called relations.

A table is a collection of related data entries and it consists of columns and rows.

A database contains one or more tables, and each table contains rows (records) of data

ID FIRST_NAME LAST_NAME CITY COUNTRY Height

1 Albert Lucas London England 184

2 Beatrice Monroe New York USA 171

3 Charles Jones New York USA 176

4 Diane Mc Gregor New York USA 165

For instance, the table above contains 4 records, each one of those having 6 fields.

In order to interact with a relational database systems, that is to insert and retrieve data, we have to use aspecific programming language. To this purpose, most of databases uses SQL (Standard Query Language).

SQL provides the syntax to create, retrieve, update or delete a piece of information

Databases are specifically designed for dealing with large amounts of data

• They use scripting languages specific for data manipulation

• They provide features for mission critical aspects such as security, efficiency, reliability, fault tolerance,data consistency, backup, etc.

Why databases are useful

However, most of business applications use a database system and the use of databases is the key for dataanalytics.

Nevertheless, when the amount of information grows, using spreadsheets becomes particularly difficult, oreven unfeasible.

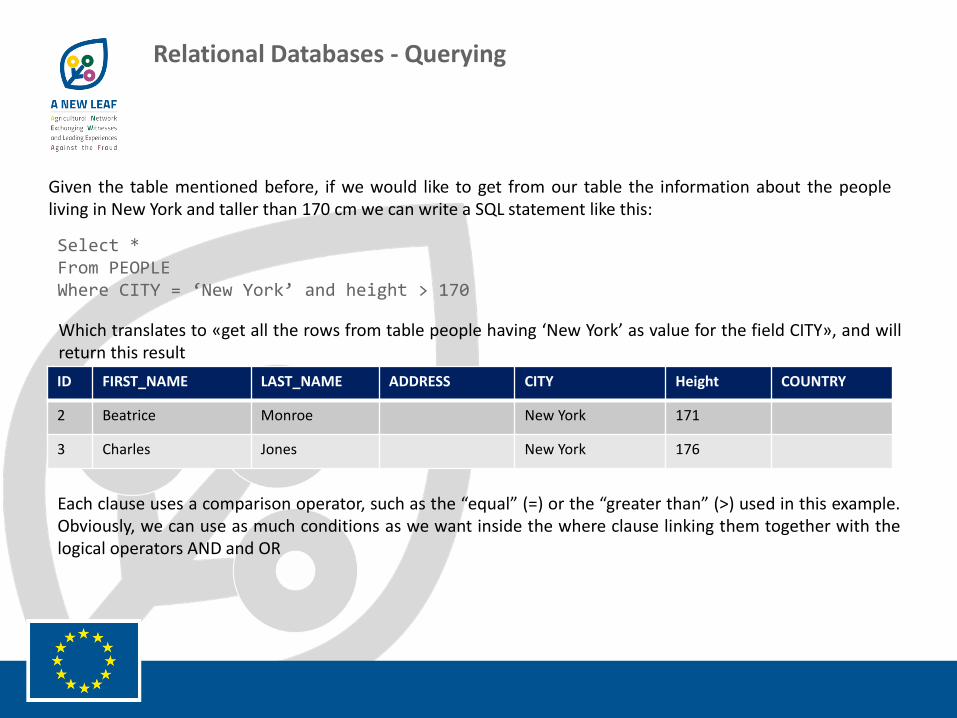

Relational Databases - Querying

Given the table mentioned before, if we would like to get from our table the information about the peopleliving in New York and taller than 170 cm we can write a SQL statement like this:

Each clause uses a comparison operator, such as the “equal” (=) or the “greater than” (>) used in this example.Obviously, we can use as much conditions as we want inside the where clause linking them together with thelogical operators AND and OR

Select *From PEOPLEWhere CITY = ‘New York’ and height > 170

Which translates to «get all the rows from table people having ‘New York’ as value for the field CITY», and willreturn this result

ID FIRST_NAME LAST_NAME ADDRESS CITY Height COUNTRY

2 Beatrice Monroe New York 171

3 Charles Jones New York 176

Relational Databases – Joining tables

However, one of the key principles of a databasesis to have multiple tables, in order to organize theinformation in an efficient and effective manner.

For example we might have a second tablecontaining the phone numbers:

Select FIRST_NAME, LAST_NAME, PHONE_TYPE, PHONE_NUMBERFrom PEOPLE as P join PHONE_BOOK as BON PEOPLE.PERSON_ID = B.PERSON_ID

In order to associate the owner’s name to eachphone number we can write a SQL statementcontain a JOIN instruction:

PHONE_ID PERSON_ID PHONE_TYPE PHONE_NUMBER

1 1 Mobile_business 122548215

2 1 Mobile_personal 445431287

3 2 Home_personal 245482136

4 4 Mobile_business 545825315

5 4 Home_personal 785453568

FIRST_NAME LAST_NAME PHONE_TYPE PHONE_NUMBER

Albert Lucas Mobile_business 122548215

Albert Lucas Mobile_personal 445431287

Beatrice Monroe Home_personal 245482136

Diane Mc Gregor Mobile_business 545825315

Diane Mc Gregor Home_personal 785453568

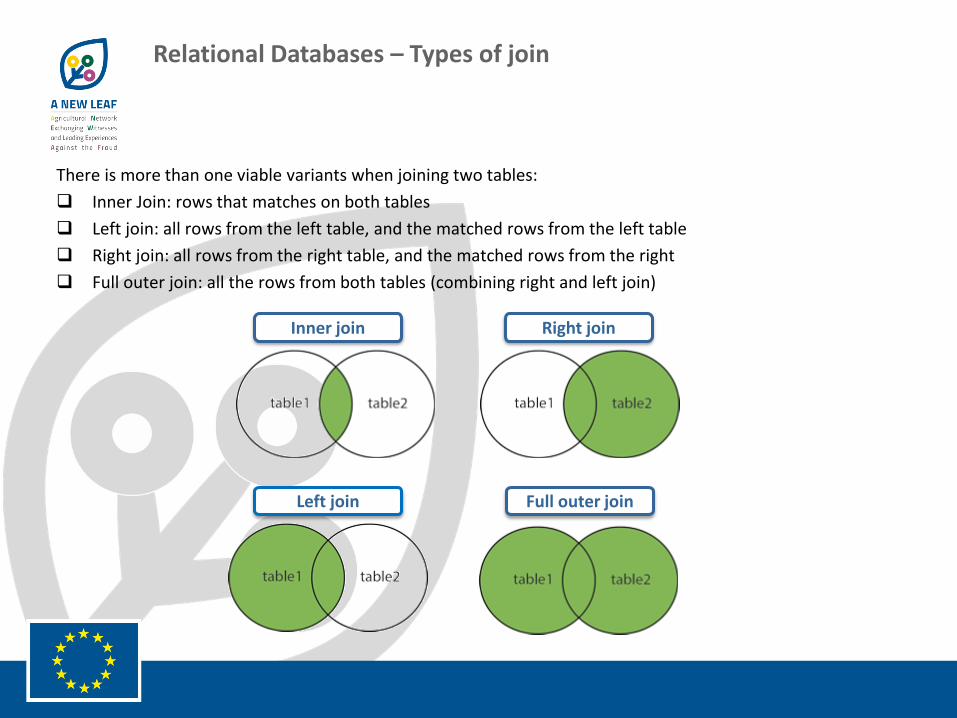

There is more than one viable variants when joining two tables:

Inner Join: rows that matches on both tables

Left join: all rows from the left table, and the matched rows from the left table

Right join: all rows from the right table, and the matched rows from the right

Full outer join: all the rows from both tables (combining right and left join)

Relational Databases – Types of join

Inner join Right join

Left join Full outer join

Relational Databases – Aggregate functions

Aggregation is a common operation when dealingwith data. Considering those data, we could needfor example to compute the total amount.

To this purpose we can use the aggregate functionsum(<field>):

PURCHASE_ID PURCHASE_TYPE AMOUNT DATE

1 cat_1 1000 2015/02/10

2 cat_3 1500 2015/03/16

3 cat_1 700 2015/02/22

4 cat_2 1400 2015/03/07

5 cat_3 400 2015/04/27

6 cat_3 1850 2015/05/08

7 cat_2 975 2015/05/21

Select SUM(AMOUNT)From PURCHASES

This translates to «sum all the values of the field AMOUNT», andproduces the result on the right.

TOT_AMOUNT

7825

SQL provides a large number of aggregate functions, like min,max, avg, stdev, etc.

Select SUM(AMOUNT), min(AMOUNT), max(AMOUNT)From PURCHASES

TOT_AMOUNT MIN_AMOUNT MAX_AMOUNT

7825 400 1850

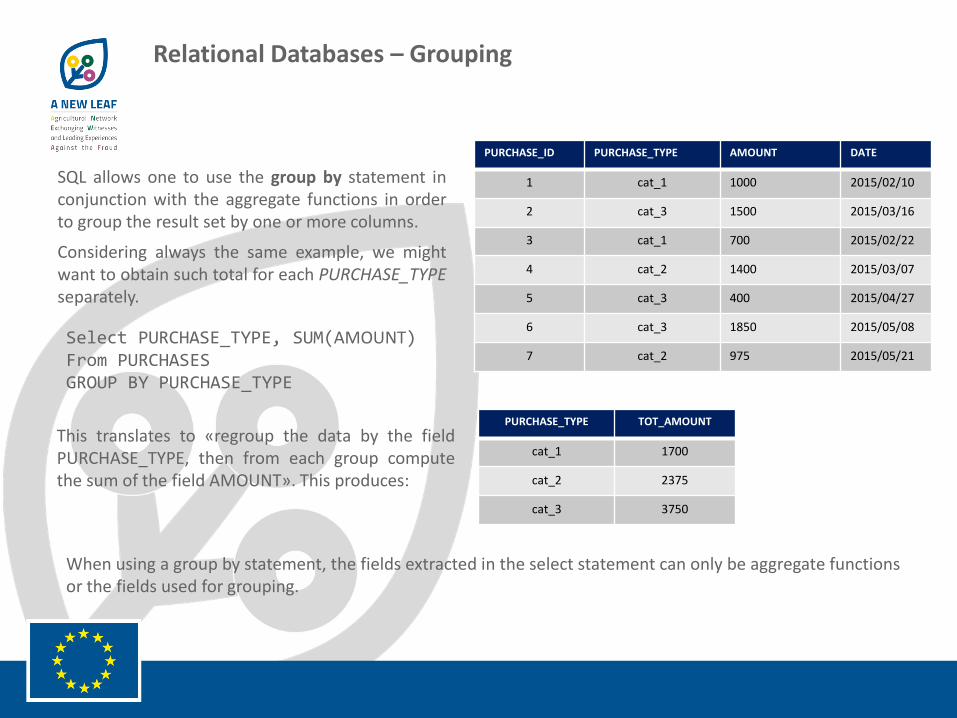

Relational Databases – Grouping

SQL allows one to use the group by statement inconjunction with the aggregate functions in orderto group the result set by one or more columns.

Considering always the same example, we mightwant to obtain such total for each PURCHASE_TYPEseparately.

PURCHASE_ID PURCHASE_TYPE AMOUNT DATE

1 cat_1 1000 2015/02/10

2 cat_3 1500 2015/03/16

3 cat_1 700 2015/02/22

4 cat_2 1400 2015/03/07

5 cat_3 400 2015/04/27

6 cat_3 1850 2015/05/08

7 cat_2 975 2015/05/21Select PURCHASE_TYPE, SUM(AMOUNT)From PURCHASESGROUP BY PURCHASE_TYPE

This translates to «regroup the data by the fieldPURCHASE_TYPE, then from each group computethe sum of the field AMOUNT». This produces:

PURCHASE_TYPE TOT_AMOUNT

cat_1 1700

cat_2 2375

cat_3 3750

When using a group by statement, the fields extracted in the select statement can only be aggregate functionsor the fields used for grouping.

Dashboarding and decision process

DashboardingIntroduction to Tableau

Tableau Software is designed to quickly analyze, visualize and share information. You can work with data, movefrom simple to complex visualizations and combine them in interactive dashboards.

Tableau applies label, color, shape and size to visualizations using the view cards.

Dashboarding The Marks Card and Buttons

Dashboarding Example dashboard

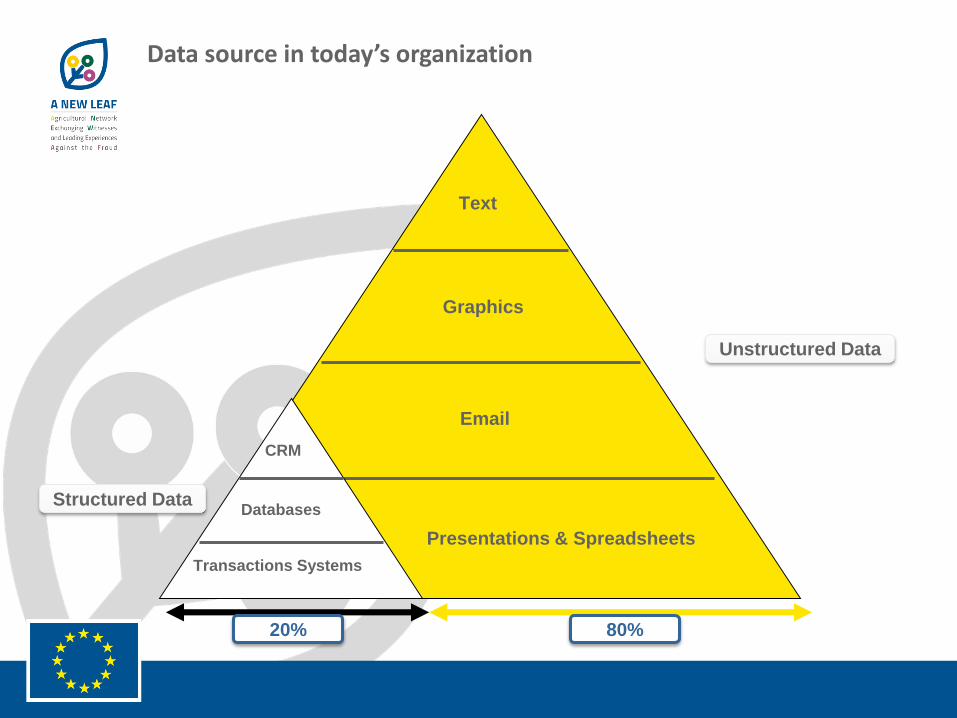

Structured and Unstructured Data

Data source in today’s organization

Text

Graphics

Presentations & Spreadsheets

20% 80%

CRM

Databases

Transactions Systems

Structured Data

Unstructured Data

20% 80%

Electronic Discovery: the process of identifying, managing, preserving, processing, analyzing, reviewing producing and presenting of electronically stored information, usually in the context of an investigation or litigation.

Project Management

Experience

Not Relevant

RelevantCustodians

Keywords

Date range

Validation and cleansing

Metadata and text extraction

De-duplication

Quality control

Exception reporting

Robust processHighly trained personnel

Tracking and reporting

eDiscovery

Fraud Data Analytics eDiscovery

Link Analisys

Output Output

Analysis of the relationships between the identified findings and reconstruction of dependencies.

Data Sources: anomalous transactions , relevant documents

Next frontier – Link Analysis