annual results 2013 - finance.open.global · annual results 2013 valérie benvenuto ... guy...

TRANSCRIPT

Annual Results 2013

Valérie Benvenuto - Financial Director

Frédéric Sebag - Co-President

Guy Mamou-Mani - Co-President

Thursday 20th March 2014

Shangri-La Hotel

Contents

Financial Results

Summary & Perspectives

1

3

Introducing the Company 2

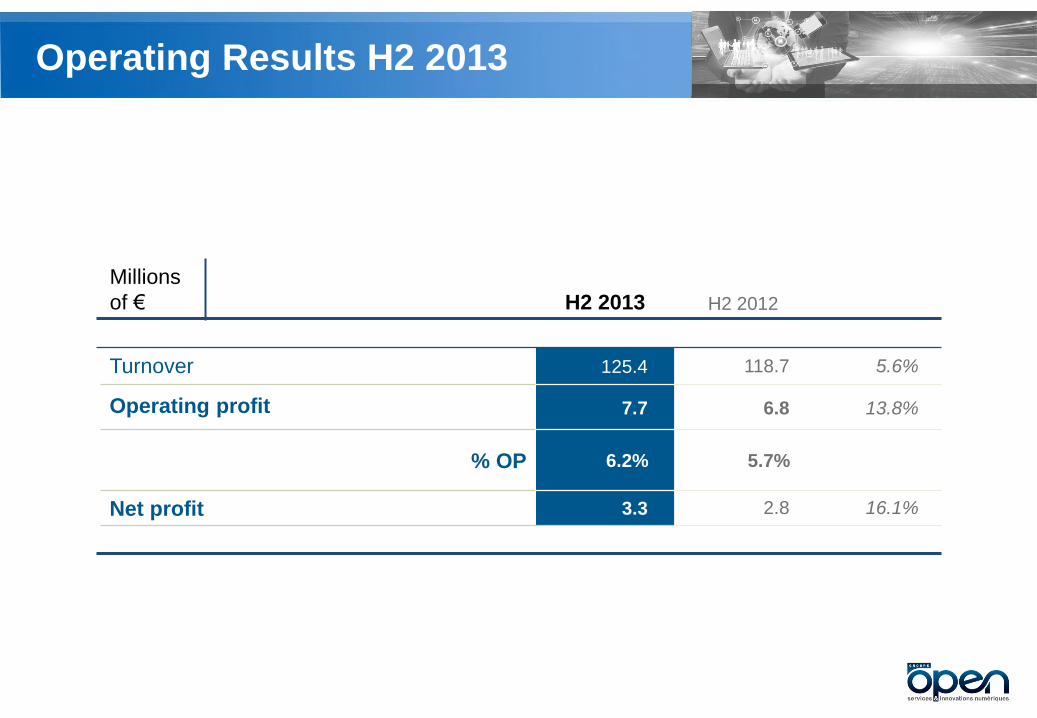

Operating Results H2 2013

H2 2013 H2 2012

Millions

of €

Turnover 125.4 118.7 5.6%

Operating profit 7.7 6.8 13.8%

% OP 6.2% 5.7%

Net profit 3.3 2.8 16.1%

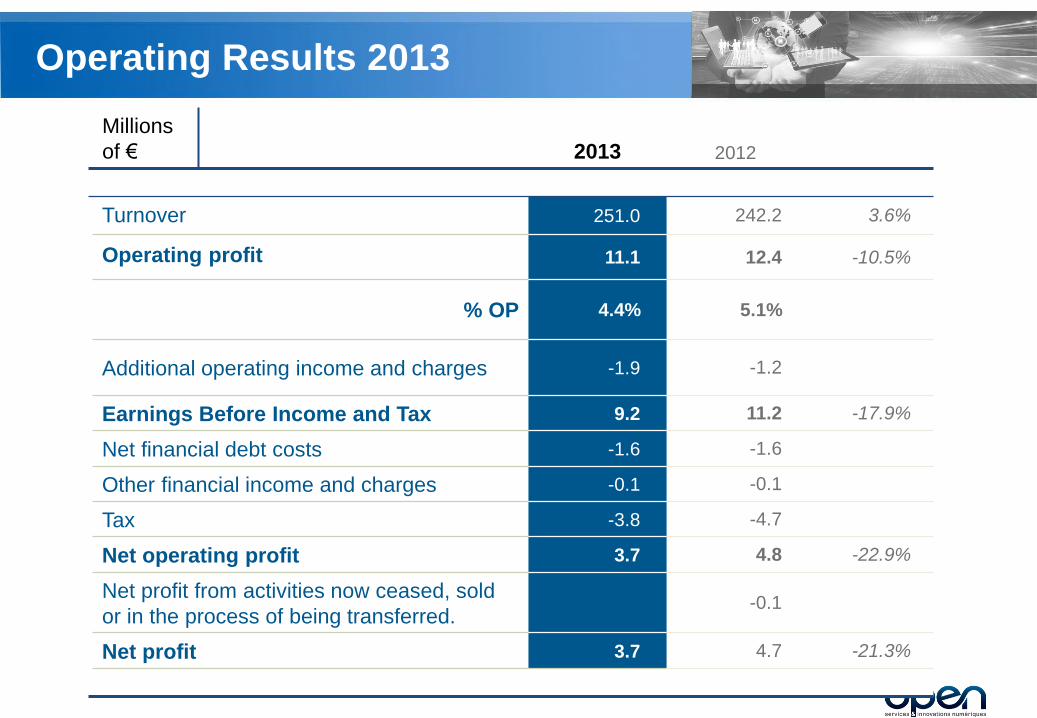

Operating Results 2013

2013 2012

Millions

of €

Turnover 251.0 242.2 3.6%

Operating profit 11.1 12.4 -10.5%

% OP 4.4% 5.1%

Additional operating income and charges -1.9 -1.2

Earnings Before Income and Tax 9.2 11.2 -17.9%

Net financial debt costs -1.6 -1.6

Other financial income and charges -0.1 -0.1

Tax -3.8 -4.7

Net operating profit 3.7 4.8 -22.9%

Net profit from activities now ceased, sold

or in the process of being transferred. -0.1

Net profit 3.7 4.7 -21.3%

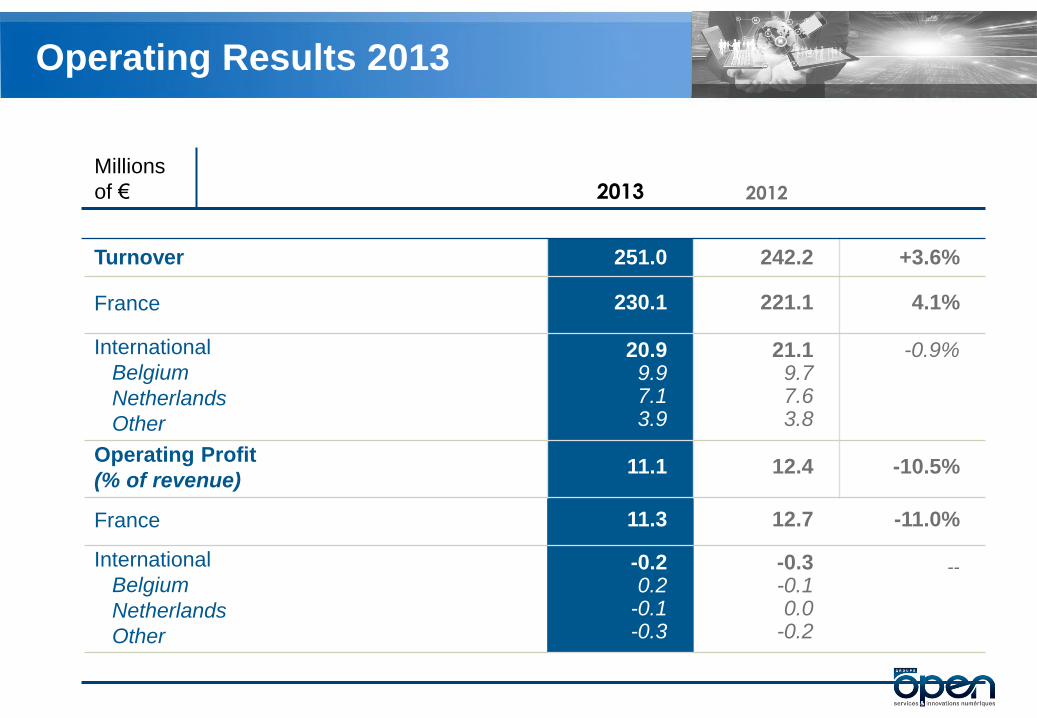

2013 2012

Millions

of €

Turnover 251.0 242.2 +3.6%

France 230.1 221.1 4.1%

International

Belgium

Netherlands

Other

20.9 9.9 7.1 3.9

21.1 9.7 7.6 3.8

-0.9%

Operating Profit

(% of revenue) 11.1 12.4 -10.5%

France 11.3 12.7 -11.0%

International

Belgium

Netherlands

Other

-0.2 0.2

-0.1 -0.3

-0.3 -0.1 0.0

-0.2

--

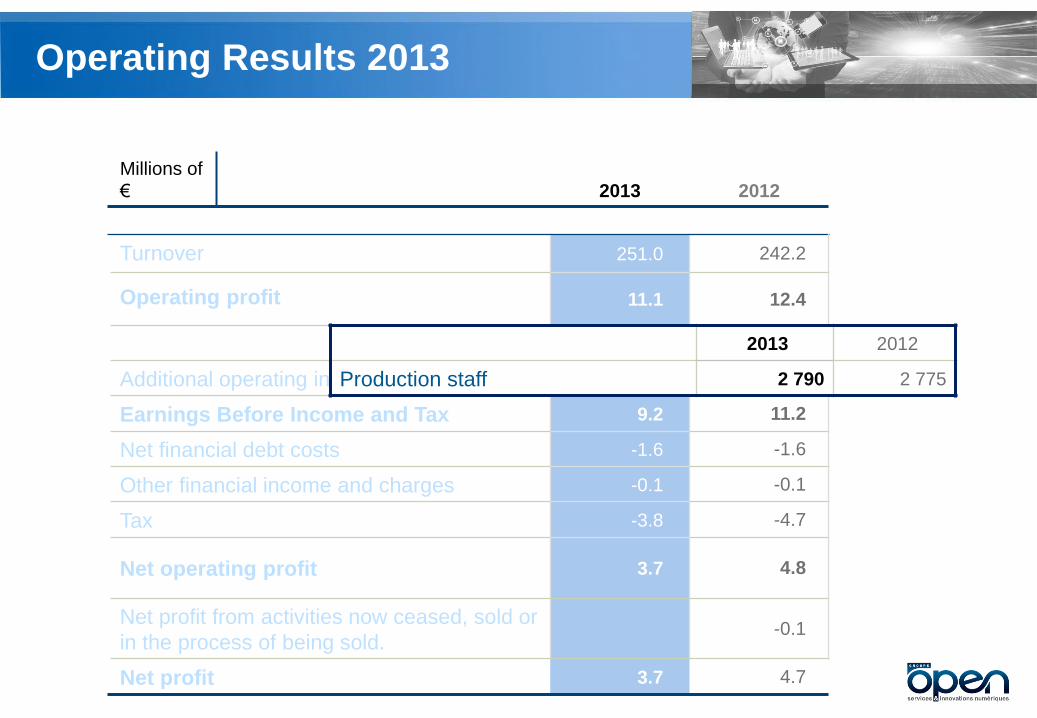

Operating Results 2013

Operating Results 2013

2013 2012

Millions of

€

Turnover 251.0 242.2

Operating profit 11.1 12.4

% OP 4.4% 5.1%

Additional operating income and charges -1.9 -1.2

Earnings Before Income and Tax 9.2 11.2

Net financial debt costs -1.6 -1.6

Other financial income and charges -0.1 -0.1

Tax -3.8 -4.7

Net operating profit 3.7 4.8

Net profit from activities now ceased, sold or

in the process of being sold. -0.1

Net profit 3.7 4.7

2013 2012

Production staff 2 790 2 775

Operating Results 2013

2013 2012 M€

Turnover 251.0 242.2

Operating profit 11.1 12.4

% OP 4.4% 5.1%

Additional operating income and charges -1.9 -1.2

Earnings Before Income and Tax 9.2 11.2

Net financial debt costs -1.6 -1.6

Other financial income and charges -0.1 -0.1

Tax -3.8 -4.7

Net operating profit 3.7 4.8

Net profit from activities now ceased, sold

or in the process of being sold. -0.1

Net profit 3.7 4.7

2013 2012

Restructuring costs -2.2 -1.1

Other 0.3 -0.1

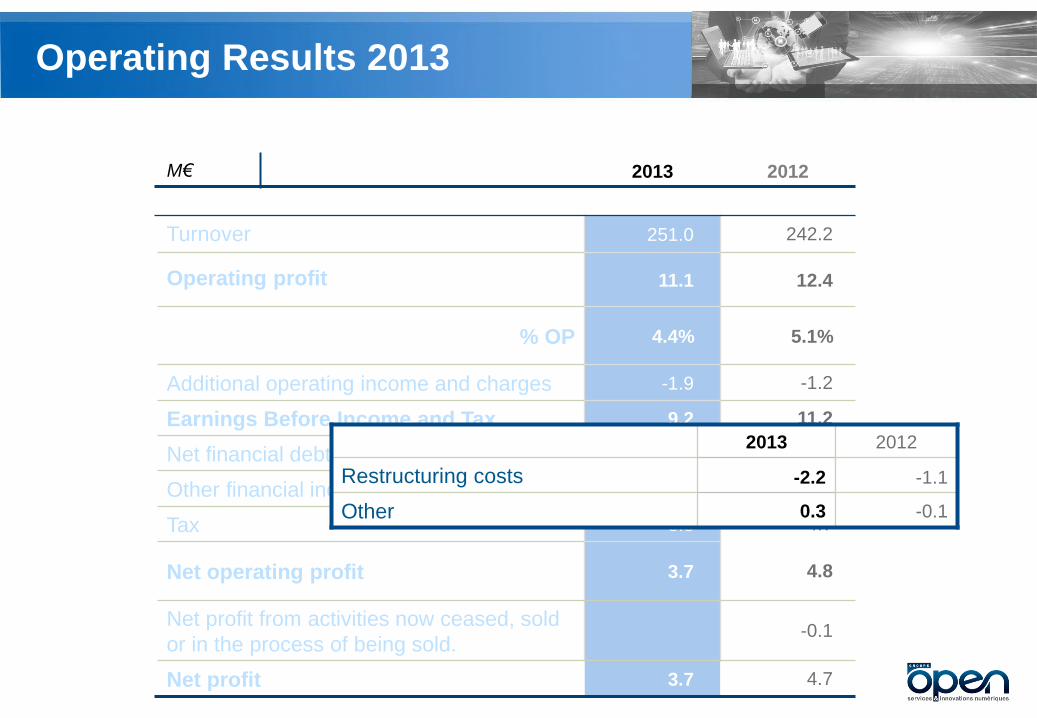

Operating Results 2013

2013 2012 M€

Turnover 251.0 242.2

Operating profit 11.1 12.4

% OP 4.4% 5.1%

Additional operating income and charges -1.9 -1.2

Earnings Before Income and Tax 9.2 11.2

Net financial debt costs -1.6 -1.6

Other financial income and charges -0.1 -0.1

Tax -3.8 -4.7

Net operating profit 3.7 4.8

Net profit from activities now ceased, sold

or in the process of being sold. -0.1

Net profit 3.7 4.7

2013 2012

Interests on loans -1.6 -1.8

Other 0.2

Operating Results 2013

2013 2012 M€

Turnover 251.0 242.2

Operating profit 11.1 12.4

% OP 4.4% 5.1%

Additional operating income and charges -1.9 -1.2

Earnings Before Income and Tax 9.2 11.2

Net financial debt costs -1.6 -1.6

Other financial income and charges -0.1 -0.1

Tax -3.8 -4.7

Net operating profit 3.7 4.8

Net profit from activities now ceased,

sold or in the process of being sold. -0.1

Net profit 3.7 4.7

2013 2012

Local corporation tax -3.1 -2.8

Corporation tax -0.7 -1.9

Operating Results 2013

2013 2012

Millions

of €

Turnover 251.0 242.2 3.6%

Operating profit 11.1 12.4 -10.5%

% OP 4.4% 5.1%

Additional operating income and charges -1.9 -1.2

Earnings Before Income and Tax 9.2 11.2 -17.9%

Net financial debt costs -1.6 -1.6

Other financial income and charges -0.1 -0.1

Tax -3.8 -4.7

Net operating profit 3.7 4.8 -22.9%

Net profit from activities now ceased, sold or in the

process of being sold. -0.1

Net profit 3.7 4.7 -21.3%

Balance sheet 2013

M€

2013 2012

Goodwill 102.0 102.0

Intangible assets 0.6 0.8

Non-current assets 109.2 109.4

Liquid assets 24.8 24.8

Current assets 86.9 81.4

Total ASSETS 196.1 190.8

2013

2012

Equity 93.9 93.2

Financial debts 21.4 19.2

Non-current liabilities 10.8 21.3

Current liabilities 91.4 76.3

Factoring 5.5 4.8

Total LIABILITIES 196.1 190.8

31/12/13 31/12/12

Gearing 2% 0%

Cash flow

2013

2012 M€

Net cash flow generated by activities 3.0 14.1

Net cash flow from investments -1.2 -2.6

Net cash flow from financing operations -5.1 -8.1

Variation in net liquid assets -3.3 3.4

Cash and cash equivalents at opening 24.3 20.9

Cash and cash equivalents at close 21.0 24.3

Introducing the company Frédéric Sebag, Co-President Valérie Benvenuto – Financial Director

Guy Mamou-Mani – Co-President

Thursday 20th March 2014

Shangri-La Hotel

Sommaire

The Digital Age

Positioning and Assets

Focus 2014

1

3

4

Digital Transformation in Business 2

The Digital Age

Connected

devices

PC

Tablet

Mobile

Objects

INDIVIDUAL

Data

Produced Accessible Analysed Implemented

Uses

Social

Collaborative

Share

Responsibility

Commerce

The implementation of

new uses

of digital technologies

to boost

value creation

From a business perspective

The Digital Age

Digital Transformation in Business

Helping a business make its Digital Transformation

means implementing

SMAC Technologies and related practices

in the following areas:

* Social Mobility Analytics Cloud

CO

MPA

NY

CONNECTED

PRODUCTS/SERVICES CUSTOMER

RELATIONS

BRAND (E-reputation)

PROCESSES (staff / ecosystem)

By treating data as a precious resource

(information).

Digital Transformation in Business

The heart of this transformation: Information Systems

which correspond to the company’s market / sector priorities

Flexibility and

rationalisation

Modernising IT sourcing methods:

combined ordering, target-based

contracts leading to full outsourcing

of Application Services and

Infrastructure Services

Technological

Breakthroughs

Social (collaborative)

Mobility

Big Data (Analytics)

Cloud

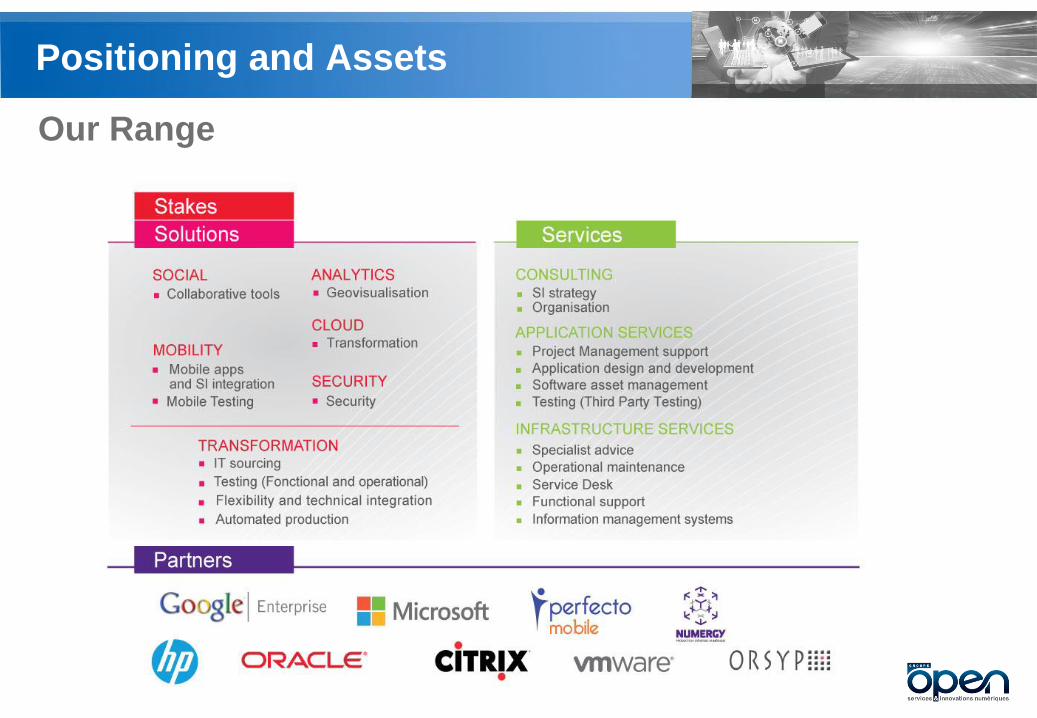

Positioning and Assets

Boosting SI performance for Open clients means providing industry-leading digital

services in:

Top 500 businesses in

France and Benelux

Positioning and Assets

Our Range

Test

Comprehensive

run-through

Industrial methods

Safety certification

Multiple

configurations

Tester différemment

Development

Methodology,

expert analysis

Security

SI Integration

Fabriquer l’expérience numérique

Advice

Audit,

Workshops,

Priority analysis,

Positioning,

Mobile strategy

Imaginer la mobilité

Hébergement

Supervision.

Administration.

IT Support

Resource

management

Decommissioning

Maintenir et anticiper

Design

Latest technology,

Ergonomy

Design

Choice of mobile

platforms (Terminal. OS. Format)

Créer les services

Deployment

Distribution

Ensuring the

security of the

application & data

Selective roll-out

Déployer sur toutes les plateformes

Positioning and Assets

Close-up: Mobility Imagining new

forms of

mobility

Creating

services

Crafting the

digital

experience

Testing with a

difference

Deploying the

solution across

all platforms

Maintenance

and forward

planning

Positioning and Assets

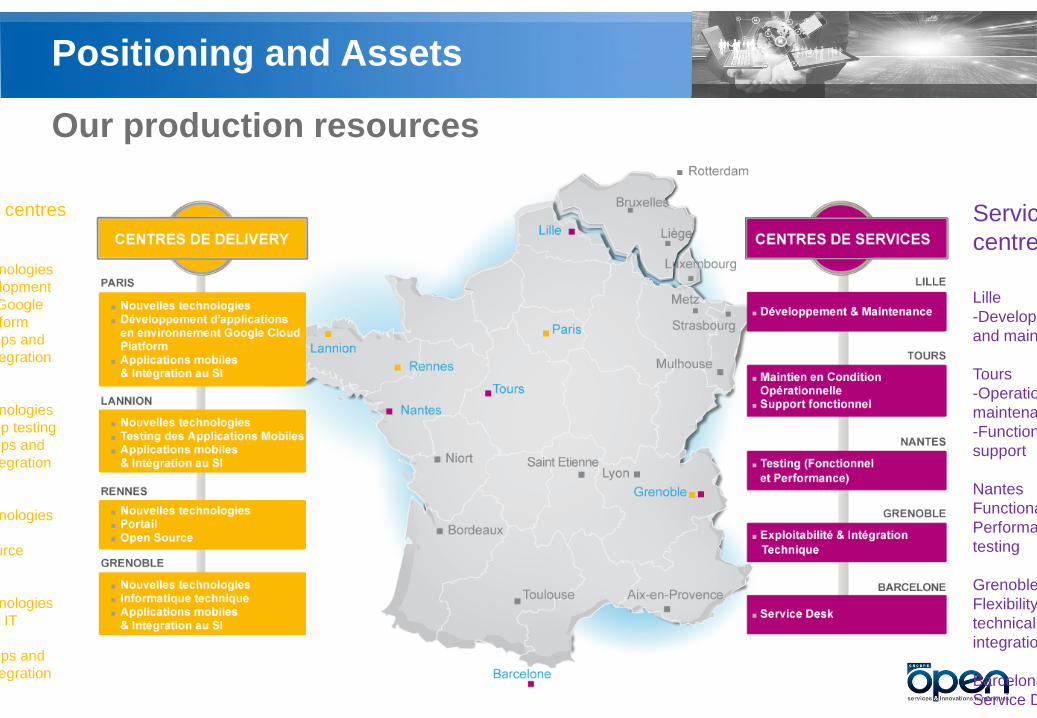

Our production resources

Delivery centres

Paris

-New technologies

-App development

using the Google

Cloud platform

-Mobile apps and

system integration

Lannion

-New technologies

-Mobile app testing

-Mobile apps and

system integration

Rennes

-New technologies

-Portals

-Open Source

Grenoble

-New technologies

-Technical IT

systems

-Mobile apps and

system integration

Service

centres

Lille

-Development

and maintenance

Tours

-Operational

maintenance

-Functional

support

Nantes

Functional and

Performance

testing

Grenoble

Flexibility and

technical

integration

Barcelona

Service Desk

Positioning and Assets

Clients – Industrial Transformation

Positioning and Assets

Clients – Digital Transformation

CO

MPA

NY

CONNECTED

PRODUCTS/SERVI

CES

CUSTOMER

RELATIONS

BRAND (E-reputation)

PROCESSES (staff / ecosystem)

Focus 2014

Structuring our activities around our growth drivers

Industrial

Transformation

Turnover

Operating Profit

Digital

Transformation

Turnover

Operating Profit

Summary & Perspectives Guy Mamou-Mani, Co-Président Valérie Benvenuto, Financial Director

Frédéric Sebag, Co-President

Thursday 20th March 2014

Shangri-La Hotel

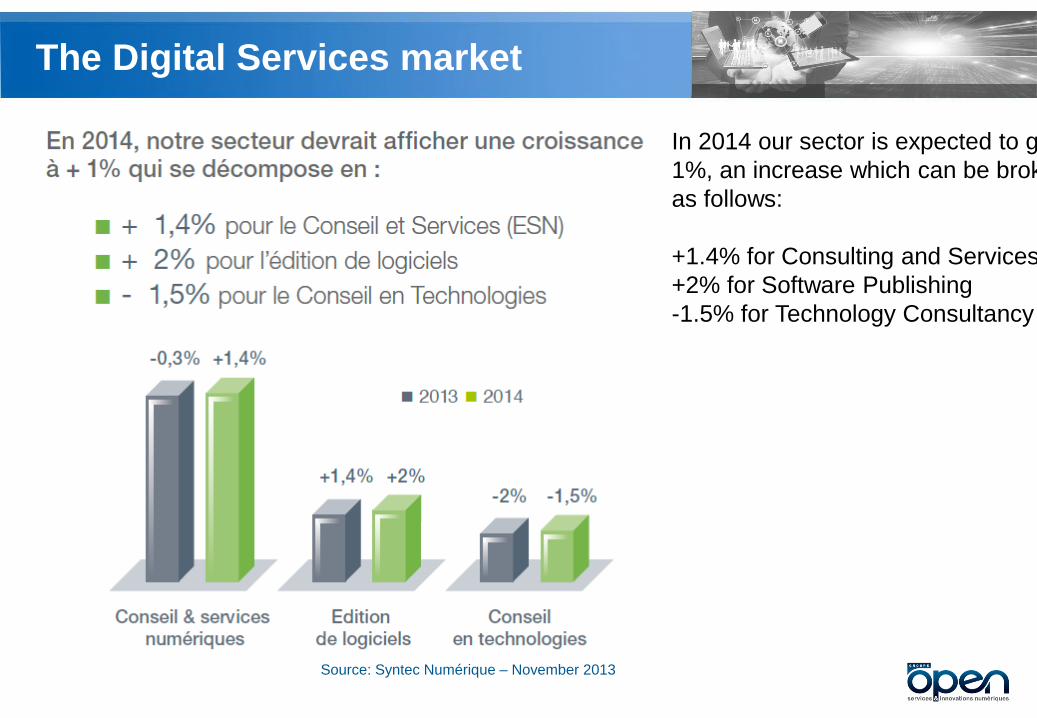

The Digital Services market

Source: Syntec Numérique – November 2013

In 2014 our sector is expected to grow by

1%, an increase which can be broken down

as follows:

+1.4% for Consulting and Services

+2% for Software Publishing

-1.5% for Technology Consultancy

The SMAC market

Digital transformation, at the heart of our growth perspectives

20% increase in revenue, 18% reduction in costs

10% annual growth in the ‘Portal’ and ‘Collaborative Tools’ sectors between

now and 2015

42% growth in the Business Network market between now and 2016

138 billion mobile application downloads

268 billion downloads predicted in 2017. Source: Cabinet Gartner

49 %

average growth rate for

Cloud infrastructures

between now and 2017

The Big Data market is

growing 6 times

faster than the IT

market as a whole

Positioning

A Responsible & Innovative Digital Services Provider

leading the way in

Industrial and Digital Transformation

for businesses in France and Benelux

Excellence underpinned by five core values and a strong CSR policy

Pertinence Audacity Ethics & Responsibility Passion Commitment

The 5 priorities of our CSR policy

INDUSTRIAL PERFORMANCE

AN AMBITIOUS INNOVATION STRATEGY

‘BETTER LIVING WITH OPEN’

DELIVERING EXCELLENCE FOR OUR CLIENTS

OUR RESPONSIBILITY PROMISE

Summary & Perspectives

Finalising the transformation of the Open Group to reflect the

evolution of the market

A remarkable second half of 2013, with increases in both turnover and

profit

Every reason to expect similar operating profit

as that seen in H2 2013

Staff figures positive

Strong dynamic in first months of 2014

Summary & Perspectives

Objectives: substantial growth in both

Turnover and Operating Profit

In 2014

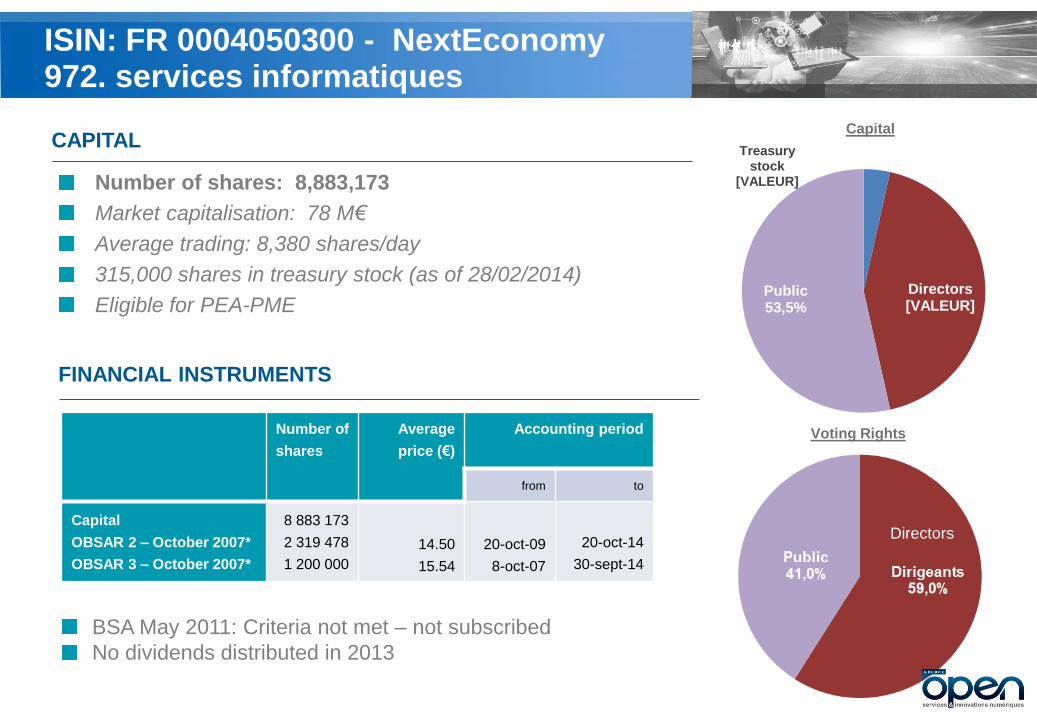

ISIN: FR 0004050300 - NextEconomy 972. services informatiques

Number of shares: 8,883,173

Market capitalisation: 78 M€

Average trading: 8,380 shares/day

315,000 shares in treasury stock (as of 28/02/2014)

Eligible for PEA-PME

CAPITAL

FINANCIAL INSTRUMENTS

Number of

shares

Average

price (€)

Accounting period

from to

Capital

OBSAR 2 – October 2007*

OBSAR 3 – October 2007*

8 883 173

2 319 478

1 200 000

14.50

15.54

20-oct-09

8-oct-07

20-oct-14

30-sept-14

Capital

Voting Rights

Treasury stock

[VALEUR]

Directors [VALEUR]

Public 53,5%

BSA May 2011: Criteria not met – not subscribed

No dividends distributed in 2013

Directors

Annual Results 2013

Thank you for listening

Thursday 20th March 2014

Shangri-La Hotel