annual report and accounts 2004 - lavendon group limited · annual report and accounts 2004 la ve...

TRANSCRIPT

Lavendon Group plcAnnual Report and Accounts 2004

Lavendon Group plc

Annual Report and Accounts 2004Lavendon Group plc1 Midland Court, Central Park,

Lutterworth, Leicestershire LE17 4PN

Tel: 01455 558874 Fax: 01455 559569

Registered in England No. 2771891

www.lavendongroup.comwww.zooomrent.com

Contents01 Financial highlights02 Chairman’s statement04 Operational review08 Financial review10 Remuneration report 15 Directors’ report 18 Statement of directors’ responsibilities 19 Directors and advisers 20 Corporate governance26 Report of the Audit Committee27 Independent auditors’ report28 Consolidated profit and loss account29 Consolidated and parent

company balance sheets30 Consolidated cash flow statement 31 Notes to the financial statements50 Group five year financial history51 Notice and agenda of

annual general meeting54 Appendix: proposed Lavendon Group plc

Share Matching Plan 2005

Lavendon Group plc

Powered solutions for elevated work areas

What is powered access?

Powered access equipment is designed to enable people to worksafely, productively and comfortably at height. It can be used in a comprehensive range of applications, both inside and outsidebuildings and structures.

Traditional methods of getting people, their tools and equipmentup to an elevated work area include ladders, mobile accesstowers and scaffolding – all of which, if used incorrectly, maypose significant hazards in the workplace. In addition, they canbe time-consuming and costly to erect or reposition in use.

An increased focus on safety in the workplace is a major factorin the accelerating rate of penetration of powered accessequipment, which offers a safe, versatile and cost-effectivealternative to traditional methods. For example, in theconstruction industry falls account for over 50% of all fatalaccidents, and throughout Europe, legislation is beingprogressively tightened to help make it safer to carry out work at height. This campaign for improved safety will continue to drive market demand for powered access equipment acrossEurope as it has in the USA.

The main drivers of substitution for traditional access methods area:

• Commercial pressure to reduce project time scales – where speed, convenience and safety are prime concerns.

• Increasingly stringent health & safety legislation has led tohigher standards of repair and maintenance in the workplace,together with the need to conduct risk assessments on all work activities.

• A growing awareness of the benefits of powered access across a wide range of market sectors outside construction.

• Demonstrable cost-efficiency of powered access comparedwith methods such as aluminium towers and scaffolding, due to its low labour content.

Lavendon is the European market leader in the rental of self-propelled booms and scissor lifts (Mobile Elevating WorkPlatforms or “MEWPs”), with a growing fleet of the morespecialised truck-mounted access platforms. Across Europe andthe Middle East, the Company now operates a fleet of around10,700 machines from a network of over 85 depots.

Powered access machines are available for internal or externaluse. Battery-powered machines are used mainly inside existingbuildings, where users have a requirement for quiet, emission-free machines. Diesel-powered equipment is often usedexternally where its greater power and traction enables a stableworking platform in rugged terrain and difficult conditions.Boom and scissor lifts are self-propelled for easy positioning and the work platform can be raised and lowered either fromthe ground or the elevated work platform. Many models aredesigned to be driven safely in the elevated position, thusadding to their flexibility and increasing productivity.

Powered access equipment is regularly used in a growing anddiverse range of market sectors and applications including signerection, broadcasting, telecommunications, construction andcivil engineering, cleaning and inspection, building services,facilities management and industrial maintenance.

Lavendon Group is the European leader in the rental of powered access equipment.

The quality and diversity of the hire fleet, coupled with the professionalism and accessibility of the depotnetwork, provides an exceptional product range forcustomers and underpins the key operating strategiesof the Group.

Operational performance

2004 2003 +/-

Group turnover £108.0m £107.8m stable

Trading profit (EBITDA)– before exceptional operating costs £31.4m £35.6m down 12%– after exceptional operating costs £25.9m £34.8m down 26%

Net cash inflow from operating activities £29.1m £36.1m down 19%

Group operating profit/(loss)– before exceptional operating costs £5.8m £9.3m down 38%– after exceptional operating costs (£0.3m) £8.5m down 104%

Net borrowings £89.0m £109.5m down 19%

Free cash £20.9m 11.2m up 87%

Exceptional operating costs incurred in 2004 amount to £6.1 million (2003: £0.8 million).

EBITDA is Earnings Before Interest, Tax, Depreciation and Amortisation.

Financial highlights

Lavendon Group plc 2004 1

Free cash2004 2003

£million £million

Net cash inflow from operating activities 29.1 36.1Interest (5.4) (6.0)Taxation 0.5 (1.0)Dividends paid (2.6) (2.6)Capital expenditure (0.3) (4.7)Capital expenditure financed by hire purchase agreements (0.4) (10.6)

Net free cash 20.9 11.2

2 Lavendon Group plc 2004

Chairman’s statement

SummaryThe Group’s trading performance in 2004has been disappointing. A poor economicbackdrop in Germany aggravated by excessmachine capacity across Europe, led to asignificant reduction in Group profits.

In the UK, our response to these difficultcircumstances has been further investmentto improve our sales and customer servicecapabilities, to counter the competitivepressure experienced in the first quarter ofthe year. This investment successfullydelivered a resumption of revenue growth asthe year progressed, but conversion of theseincremental revenues into increased operatingprofits proved disappointingly slow, with onlyrelatively small benefits starting to accruetowards the end of the year.

As further market decline became apparentin Germany during the year, we undertook areappraisal of our combined German andAustrian operation. This led to theimplementation of a major restructuringprogramme to reduce the overall scale andcost of the business. Whilst we have retaineda market leading position in Germany, ourbusiness has been significantly downsized.The action taken has lowered the operatingcost base considerably, enabling the businessto weather better the present difficult tradingconditions and allowing it to respond moreefficiently to any improvement in theeconomic climate. As part of the restructuringprogramme, we have also disposed of ourbusiness in Austria since the year-end.

Some limited progress has been made inFrance, while Spain had a tough year as thepreviously robust construction market startedto weaken. In the Middle East both revenuesand operating profits increased as activitylevels in the region remained solid.

The decisions taken in the UK andparticularly Germany have resulted inconsiderable costs being incurred, boththrough increased operating costs andexceptional charges as well as generalbusiness disruption, the impact of whichhave been severely detrimental to theGroup’s results for 2004. These actions werenecessary to return the Group to a positionfrom which, once again, sustainableearnings growth should be achievable.

The Group has continued to generatesubstantial cash inflows, and with the limitedrequirement for capital expenditure in theyear, was able to reduce its debt levels monthon month throughout 2004. Further progressin reducing debt levels is expected in 2005.

We completed the refinancing of our bankfacilities in June and a new £85 millionfacility was put in place which will expire inJune 2009. This new facility provides thenecessary flexibility for the developmentof the Group going forward.

Financial resultsThe Group’s turnover for the year wasbroadly flat at £108.0 million (2003: £107.8million), producing an operating profit beforeexceptional costs of £5.8 million (2003: £9.3million). The operating loss after exceptionalcosts was £0.3 million (2003: profit of£8.5 million). Operating margins prior toexceptional costs were 5.4% (2003: 8.6%),while after exceptional costs a negativemargin of –0.3% was incurred (2003:profit margin of 7.9%).

Exceptional costs totalled £14.5 million(2003: £0.8 million). These comprised£6.1 million of exceptional operating costs,principally the professional fees associatedwith the refinancing of the Group’s debt

Lavendon Group plc 2004 3

“Our financial strength is firmly underpinned by the Group’s strongcash flows and reducing debt levels, attributes which allow us to lowerthe risk profile of the business through these tough trading periods.”

facilities and the costs incurred in Germanywith the goodwill write down and depotclosure programme, together with £8.4 millionof exceptional non-operating costs relatingto a provision made against German assetsidentified for disposal and the write down ofthe Austrian business to the value realisedfrom its disposal post the year-end.

Earnings before interest, tax, depreciation andamortisation (EBITDA) prior to exceptionalcosts declined to £31.4 million (2003: £35.6million) primarily as a result of the reducedoperating profits. After exceptional costs, theGroup’s EBITDA was £25.9 million (2003:£34.8 million). With a reduction of £0.6 million(2003: £1.3 million) in working capitalrequirements, the net operating cash flowprior to exceptional costs was £32.0 million(2003: £36.9 million). After exceptional coststhe net operating cash flow for the year was£29.1 million (2003: £36.1 million).

Due to the continued strength of the Group’scash flow and a limited capital expenditureprogramme, £20.9 million (2003: £11.2 million)of ‘free cash’(1) was generated in the year. Thissubstantial increase in the level of ‘free cash’ (1)

has enabled the Group to reduce its net debtlevels at the year-end to £89.0 million, after asmall adverse foreign exchange movement of£0.5 million, compared to £109.5 million at theend of 2003. The corresponding debt to equityratio was 118% (2003: 122%).

The Group’s pre-tax result before exceptionalcosts was breakeven (2003: a profit of £3.0million). After exceptional costs the lossbefore tax was £14.5 million (2003: a profitof £2.2 million). The loss per share beforeexceptional costs was 3.29 pence (2003:earnings of 4.83 pence) and after exceptionalcosts the loss per share was 34.49 pence(2003: earnings of 3.31 pence).

DividendWe reported in our pre-close trading updatein December 2004, that due to the impactof the exceptional costs on the Group’sdistributable reserves and the cash cost ofthis restructuring, the Board had decidednot to recommend the payment of a finaldividend for 2004.

The Board is hopeful that an improvedtrading performance in 2005 will enable theresumption of dividend payments.

OutlookThe generally weak levels of demand acrossmost of the European Industrial andCommercial construction sector, combinedwith the poor economic climate in Germany,is restricting the Group’s ability to deliversound financial performance. Nonetheless weremain confident that, over the medium term,the demand for powered access products willreturn to average growth trends considerablyabove that of general economic activity, andthat once this occurs, the profitability of theGroup will improve significantly.

Until the marketplace shows signs of asustained recovery, our efforts will be focusedon increasing the cost effectiveness of thebusiness, strengthening managementcapabilities and, through the use of enhancedIT systems, improving operational processes.

Our financial strength is firmly underpinnedby the Group’s strong cash flows andreducing debt levels, attributes which allowus to lower the risk profile of the businessthrough these tough trading periods, andwhich also ensure that the benefits of theGroup’s operational leverage are magnifiedonce demand levels improve.

Trading so far this year is in line with ourexpectations with the UK continuing thetrend of revenue growth year on year.Germany is completing the final elements ofits restructuring programme, which, althoughstill very early in the process, is deliveringperformance improvements.

David PriceChairman7 March 2005

(1) Free cash is defined as net cash inflow from continuingoperating activities less interest, taxation, dividends paid,and capital expenditure before inception of new hirepurchase agreements.

Free cash2004 2003

£million £million

Net cash inflow from operating activities 29.1 36.1Interest (5.4) (6.0)Taxation 0.5 (1.0)Dividends paid (2.6) (2.6)Capital expenditure (0.3) (4.7)Capital expenditure financed by hire purchase agreements (0.4) (10.6)

Net free cash 20.9 11.2

4 Lavendon Group plc 2004

Whilst market conditions continue to begenerally unfavourable, impeding our abilityto grow revenues, we have concentrated ourefforts on reshaping our business to ensurethat the future development of the Group isbased on solid foundations and that theadverse affects of current trading conditionsare minimised. By developing andimplementing enhanced IT and operationalsystems we have improved the economiesof scale available from centralising customerorder taking and transport co-ordinationfunctions, and at the same time increasedthe level of customer service that we offerto the marketplace. We have also, throughtight control of working capital and a limitedcapital expenditure programme, sought tomaximise cash flow to reduce our debt levels.

UKThe UK continues to be the Group’s largestand most important market and,consequently, the key focus, as we came intothe year, was to restore the business to bothrevenue and profit growth. To achieve thisaim substantial sums were invested duringthe first half of the year in marketing,telesales activities, strengthening customerservice centres, expanding the salesforce andimproving fleet availability. By the end of thefirst quarter, this investment had successfullyreversed a declining revenue trend allowingrevenues for the year to grow by 4% to£61.5 million (2003: £59.2 million). Althoughincremental operating profits from thisrevenue growth were being earned in the

final stages of the year, the extent of theinvestments made to improve customerservice standards meant that operatingprofits prior to exceptional costs declined to£7.4 million for the year as a whole (2003:£9.2 million). Operating margins prior toexceptional costs were 12% (2003: 16%).After exceptional costs, operating profitswere £5.3 million (2003: £8.8 million) withan operating margin of 9% (2003: 15%).

During the year, extensive upgrades to ourIT systems were made enabling improved,statistically based, pricing decisions to beapplied consistently across our depotnetwork. These enhancements are allowingadjustments to be made to product pricingwhich reflect the changing patterns ofdemand through the year, and are startingto deliver the expected benefits throughimproved hire rates.

The management structure of the UK hasbeen strengthened, through a combinationof external recruitment and targeted training.In August 2004, the UK senior managementteam was completed with the appointmentof Hugh Cole as Managing Director.

Although the short-term profitability ofthe UK business has been diluted by theinvestments made in the year, the operationis now in a robust shape and ready toimplement strategic decisions going forwardthat will deliver long-term growth andincreased profits.

Operational review

Lavendon Group plc 2004 5

“We have concentrated our efforts on reshaping our business to ensure that the future development of the Group is based on solid foundations and that adverse affects of current trading conditions are minimised.”

Top: Telescopic self-propelled boom lift assistingrestoration work on a lightship.Bottom: Steel erection at the new Coventry Arena, UK.

Germany and AustriaThe German marketplace remains depressedwith extremely testing trading conditions asa result of declining demand from theconstruction sector. Overall demand from thissector has reduced by some 28% since 2000,with the situation being exacerbated by thenon-construction related sectors also havingsubdued demand levels as a result of theprevailing economic climate.

Against this background, as 2004 progressed,it became increasingly clear that the Germanpowered access market was not experiencinga short-term correction between demandand the capability to supply, but wassuffering from a fundamental imbalancebetween these market forces. With theeconomic outlook at best forecasting stabilityor low growth, any demand led resolution ofthe situation was likely to take several years,and the correction of excess machinecapacity was only going to occur throughthe progressive non-replacement of retiringfleet, unless a significant number of rentalunits were removed from the marketplace byone or more main players.

As the strategic options to respond to thismarket situation were being evaluated,regional customer service centres werecreated to de-link the customer contact andorder placing from the local supplying depot,thereby enhancing customer retention in theevent of any future restructuring of theoperation. Once the review of the market

was completed, a more fundamentalrestructuring of the business was required andas a result the depot network was reducedfrom 44 to 24 depots, headcount by 80 and1,000 rental machines were removed from thefleet either by transfer to our operations inother countries or by being placed intostorage for disposal. These actions were takento ensure that the business is more closelyaligned to current market conditions.

As a result of this restructure the cost base ofthe German operation has been reduced by£5.25 million per annum, making the businessmore flexible to changing market conditionsand better able to defend market share fromprice-based competition. By removing 1,000rental units, the present over-capacity in themarketplace is partly addressed, thereby layingthe foundation for improved hire rates as theprice control systems, as implemented in theUK in 2004, are rolled out across the Germandepot network in 2005.

Of the 1,000 machines removed from themarket, 300 units have been transferred toFrance, the UK and the Middle East, with theremaining 700 units being placed into storagefor sale into the secondary market over thecoming 12-24 months with priority beinggiven to disposals into markets in which theGroup does not operate.

Revenues for the year declined by 9.6% to£28.3 million (2003: £31.3 million), producingan operating loss prior to exceptional costs

6 Lavendon Group plc 2004

of £3.4 million (2003: £1.9 million). Theexceptional operating costs totalled £4.0million and related to the restructuring ofthe operation and included depot closurecosts, termination of employee contracts,transport and storage of rental machines andthe write-off of the remaining goodwill.After exceptional operating costs, theoperating loss for the year was £7.4 million(2003: £2.2 million). In addition to theexceptional operating costs, non-operatingexceptional costs were incurred totalling£6.5 million relating to provisions madeagainst the rental units identified for disposal,to reflect their expected realisable value.

Whilst our Austrian operation was includedin the overall market review and was to bepart of the restructuring, an offer to acquirethe business was received from a third partyand accepted, with the sale being completedon 25 February 2005. The business was soldfor £2.65 million payable in cash, its netasset value. Revenues for the year were£2.1 million, (2003: £2.0 million), with anoperating loss of £0.3 million (2003: nil).Non-operating exceptional costs of £1.9million were incurred, which representedthe impairment charge required to reducethe net asset value of the business in linewith the agreed sale price.

FranceThe French market showed some signs ofrecovery in 2004 as demand levels startedto increase as the year progressed.

Our own operation reflected this marketrecovery as revenues in the second half ofthe year grew by 15%, to produce a totalrevenue for the year of £5.3 million (2003:£5.0 million), an increase of 6%. Theoperating loss for the year reduced to£0.6 million (2003: £0.7 million).

During the year the standard Group ITplatform was implemented to improveoperational control and managementinformation, and in the second half of theyear we decided to improve our position fora recovery in the market by opening a depotin Rouen and increasing the fleet by 120units, mainly transferred from Germany,bringing the total fleet to 750 units. Whilstthe expansion of the depot network producesa drag on profits in the short term, theincremental revenues earned, once the depotis established, will enable the business as awhole to move towards profitability.

SpainThe growth of the use of powered accessproducts in the Spanish market has beendriven by the expanding construction sectorover the last few years. This growth has beenconcentrated around the major cities, andSpain does not therefore have widespreaddepth and breadth of cross-industry sectordemand that exists in, for example, the UKand France. Consequently the health of thepowered access market is particularly sensitiveto the rate of growth in the constructionsector, which showed early signs of slowing

Operational review continued

S125 Boom lift with a working height of 40 metresassists installation of speakers & lighting at Sports Arena.

Lavendon Group plc 2004 7

during 2004, and is reflected in the declinein our revenues for the year to £3.6 million(2003: £3.7 million). The operating result forthe year was breakeven (2003: profit of£0.2 million).

To mitigate an expected further slowdown inthe construction market we are concentratingour activities in Madrid and Murcia where wehave strong market positions with a relativelystable demand base.

Middle EastOur Middle East business, recorded anotherexcellent trading performance, despite thesuspension of many customers’ projects inSaudi Arabia from the second quarter inlight of a number of terrorist incidents.

Revenues increased by 9% to £7.2 million(2003: £6.6 million), with operating profitsgrowing by 12% to £2.7 million (2003: £2.4million). These improved results were achieveddespite an adverse 8% year on year currencytranslation impact following the continuedweakness of the US dollar.

As we start 2005 there are encouraging signsof a resumption of many of the suspendedactivities in Saudi Arabia and, consequently,we are optimistic of another strongperformance in the year ahead.

SummaryThe past year has clearly been a difficultand disappointing year for the Group.Nevertheless by restructuring our operationsto be further in-line with current marketprospects and strengthening our operationalprocesses to improve customer service, weare well placed to deliver an improvedperformance. It is clear that without ourmany excellent and motivated employeesthe changes that have been made duringthe year would not have been possible,and considerable thanks are due to themfor their dedication and determination.

The year has started off in line with ourexpectations. The measures taken toimprove efficiency in the UK and mitigatethe impact of the poor economicenvironment in Germany should see theoverall Group make progress in 2005.

Kevin AppletonChief Executive7 March 2005

Chandeliers bedecked with gold and silver baublesare safely installed in shopping centres usingNationwide’s articulating boom lifts.

“It is clear that without our many excellent and motivatedemployees the changes that have been made during the year would not have been possible, and considerable thanks are due to them for their dedication and determination.”

8 Lavendon Group plc 2004

Financial review

Trading performanceThe turnover for the Group was stable for theyear at £108 million, with revenue growth inthe UK, France and the Middle East beingoffset by declines in Germany and Spain.

Prior to exceptional costs, the operatingprofits before interest tax, depreciation andamortisation declined to £31.4 million from£35.6 million in the previous year, due to thecombination of reduced operating profits andincreased losses from our main operations.

The Group’s depreciation and amortisationcharge for the year declined marginally to£25.6 million from £26.3 million in 2003, as aresult of currency fluctuations and a smallreduction in the size of the Group’s rentalfleet. As the average age of our rental fleetremains relatively young and still has sufficientcapacity to support anticipated revenuegrowth, the capital expenditure programmefor the year was tightly controlled with only£2.3 million being invested in fixed assets.

Operating profits after charging depreciationand amortisation, but before exceptionalcosts and interest charges, were £5.8 millioncompared to £9.3 million in 2003.

Exceptional operating costs totalling £6.1million were incurred in the year, mainlyrelating to the refinancing of the Group inthe first half of the year and the restructuringof our German operation involving the write-off of goodwill and an extensive depotclosure programme with associated employeetermination costs. In addition to theexceptional operating costs, non-operatingexceptional costs of £8.4 million wereincurred, relating to a provision made againstGerman assets identified for sale togetherwith the write down of the net assets of theAustrian business to the value realised fromits disposal post the year-end.

Interest charges decreased by £0.5 million to£5.8 million for the year, as the Group’s levelof borrowings continued to decline.

Although interest charges decreased, theextent of the decline in operating profits hasmeant that the Group produced a breakevenresult prior to tax and exceptional costs.After exceptional costs, the loss beforetaxation was £14.5 million. With the benefitof a net tax credit of £1.7 million, the lossafter tax was £12.8 million, compared to aprofit in 2003 of £1.2 million.

The loss per share after both tax andexceptional costs was 34.49p compared toearnings of 3.31p in the previous year. Priorto the effects of the exceptional costs, theloss per share was 3.29p against earningsof 4.83p in 2003.

Cash flow and financingThe net operating cash flow of the Groupprior to the impact of exceptional costs,remained strong at £32.0 million, compared to£36.9 million in 2003. After the cash effect ofthe exceptional costs are accounted for, thenet operating cash flow for the year was£29.1 million, against £36.1 million in 2003.

Although the cash inflow from operationsdeclined during the year, a reduced interestcharge, taxation refunds and limited capitalexpenditure, enabled the level of free cash toincrease significantly to £20.9 million from£11.2 million in 2003. Unlike in recent years,currency fluctuations only marginallytempered the effect that this free cash hadon reducing the Group’s level of borrowings,enabling net debt levels to reduce to £89.0million, a substantial decline from the £109.5million reported at the previous year-end.

As the Group’s requirement for capitalexpenditure in 2005 is again minimal, afurther significant decrease in net debtlevels is expected to be produced.

During the year, the Group completed therefinancing of its bank facilities and put inplace new facilities comprising of a €60.0million amortising term loan over five yearsto 30 June 2009, and a £45.0 million multicurrency revolving loan repayable 30 June2009. These facilities continue to be availableand all associated covenants have been met.

Financial riskThroughout the year, the Group’s approach tofinancial risk has remained consistent in itsaim to manage and mitigate the risks thatrelate to fluctuations in interest and foreignexchange rates, and to ensure that thenecessary funds are available to meet theGroup’s ongoing requirements.

Lavendon Group plc 2004 9

The risks are managed to reduce the overalllevel of uncertainty to which the Group isexposed, whilst providing the necessaryflexibility to meet the commercial needsof the business.

Interest rate riskThe Group has exposure to movements ininterest rates on its borrowings. This exposureis managed by a combination of fixed andfloating interest agreements. The mix of shortand long-term fixed interest rate agreementsallows the Group to smooth the impact ofinterest rate fluctuations by allowing somebenefit from rate reductions, whilst offeringsome protection against rate rises.

The fixed interest rate element of borrowingsat the end of the year was 58%, a smallincrease from the previous year, but remainingbroadly in line with the Board’s intention tomaintain an even split between fixed andfloating rate borrowings.

Based on the year-end mix and quantum ofborrowings, a movement in Euro interest baserates of 0.25% would increase or decrease theGroup’s annual interest costs by approximately£70,000, whilst a similar movement in Sterlinginterest base rates would increase or decreaseannual costs by £30,000.

Currency riskThe Group has international operations tradingin local foreign currencies. The fluctuation ofglobal exchange rates, particularly the Euro,can cause currency exposures to the Group’sconsolidated Sterling results.

The Group does not hedge the translationalexposure, believing the cost is notcommensurate with the risk. If the exchangerates prevailing at the year-end had appliedthroughout 2004, the earnings per share

would have decreased by 2.45 pence. Had theexchange rates at the previous year-endapplied throughout 2004, the earnings pershare would have decreased by 1.11 pence.

The Group manages its risk to transactionalcurrency exposures by, if circumstances aredeemed appropriate, taking forward coverwhere significant receipts or payments aredue. The remittance of funds between cross-border entities is minimised to reducetransaction exposure on earnings.

The Group’s aim is to both match itsinvestments with borrowings of the samecurrency, and service these borrowings fromcashflows in the appropriate currency whereavailable. This is managed by maintainingborrowing facilities in both the Group’s maintrading currencies of Sterling and the Euro.

Liquidity riskThe Group aims to achieve a balance betweencertainty of funding and a flexible costeffective borrowing structure. The currentcommitted bank facility, which forms 84% ofthe net indebtedness at the year-end, is notdue to finally mature until 2009, and this issupplemented by hire purchase and leasingcredit lines. To ensure a prudent approach istaken, the Group ensures that there aresufficient funds or credit lines available tosupplement internal cashflow to meet knownobligations in the next twelve months.

TaxationThe Group recorded a tax credit of £1.7 millionfor the year, compared to a charge of £0.9million in 2003.

Both the tax credit and the previous year’scharge reflect estimated liabilities for thecurrent year together with movements indeferred taxation balances, and are the

blended average of the effective tax ratesapplicable in the UK and the overseasoperations.

DividendsDue to the impact that the restructuringcharges have had on the Group’s distributablereserves together with the associated casheffect of this restructuring, the Board hasdecided not to recommend the payment ofa final dividend for 2004.

Going concernThe directors have acknowledged the latestguidance on going concern and have formeda judgment at the time of approving thefinancial statements, having made all relevantenquiries, that it has adequate resources atits disposal to continue its operations forthe foreseeable future.

International FinancialReporting StandardsPreparations for the move to reporting theGroup’s consolidated financial statementsin accordance with International FinancialReporting Standards (IFRS) are underway.The Group is confident that it will be able tomeet the reporting requirements under IFRSfor its Interim Report in 2005.

Alan MerrellGroup Finance Director7 March 2005

“As the Group’s requirement for capital expenditure in 2005 is again minimal, a further significant decrease in net debt levels is expected to be produced.”

10 Lavendon Group plc 2004

Auditable informationThe Remuneration Report has been audited by PricewaterhouseCoopers LLP as required by Schedule 7A to the Companies Act 1985. The sections on pages 11 and 12 disclosing target composition of directors’ performance related pay, directors’ service contracts, and thecompany performance comparative chart are unaudited.

Members of the Remuneration and Nomination CommitteeThe Remuneration and Nomination Committee (the ‘Committee’) comprised the two non-executive directors of the Company, JohnHeywood (Chairman of the Committee) and John Gordon, throughout the year. The terms of reference for the Committee are available on the Lavendon Group website (www.lavendongroup.com).

During 2004, the following parties provided material assistance to the Committee:

• Ashurst: legal advice on negotiation of the revised service contract for the Executive Chairman• Future Focus: executive pension scheme advice• M, M & K Limited: executive directors’ remuneration review• Odgers Ray & Berndtson: non-executive recruitment search

Both the non-executive directors are considered to be independent by the Company and both are members of remuneration committeeswith other companies.

Remuneration policyThe Committee is responsible for determining the remuneration packages of the executive directors of the Group. In doing so, theCommittee ensures that:

i. the Group’s executive directors are appropriately rewarded for their contributions to the Group;ii. account is taken of their individual responsibility and performance;iii. the remuneration packages reflect current market conditions in order to attract, retain and motivate executive directors of a high quality;iv. the Company complies with the Code of Best Practice set out in the Listing Rules of the UK Listing Authority and

the Committee has given full consideration to the Best Practice provisions outlined therein.

Directors’ remunerationThe emoluments of the individual directors were as follows:

Salary Benefits Performance related Total Pension and fees in kind payments remuneration contributions

2004 2003 2004 2003 2004 2003 2004 2003 2004 2003£000 £000 £000 £000 £000 £000 £000 £000 £000 £000

Executive directors:David Price 70 150 4 33 – – 74 183 28 80Kevin Appleton 165 165 14 14 – – 179 179 41 41Alan Merrell 145 145 18 17 30 – 193 162 36 36

380 460 36 64 30 – 446 524 105 157

Non-executive directors:John Gordon 25 25 – – – – 25 25 – –John Heywood 25 25 – – – – 25 25 – –

50 50 – – – – 50 50 – –

Total directors’ emoluments 430 510 36 64 30 – 496 574 105 157

Remuneration report

Lavendon Group plc 2004 11

Amounts shown as salary and fees relate to basic salary in the case of executive directors and fees in the case of non-executive directors.Benefits in kind relate principally to company cars, fuel for private motoring, private health insurance and disability cover.

On 1 January 2004 David Price formally adopted the role of part-time Executive Chairman.

The fees for non-executive directors were last revised on 10 October 2002 at the time that their service contracts were renewed. The Boarddetermined the fees payable with reference to the current market conditions at that time.

The targeted composition for achievement of full performance related pay of each director’s remuneration is as follows:

Non-performance related Performance related

David Price 100% 0%Kevin Appleton 50% 50%Alan Merrell 50% 50%John Gordon 100% 0%John Heywood 100% 0%

In 2003, Kevin Appleton and Alan Merrell, each voluntarily agreed to apply 50% of future post-tax bonuses in acquiring shares in theCompany. This is in accordance with the desire of the Remuneration Committee for executive directors to have a greater equity holding in the Company to increase the alignment of their interests with those of the shareholders.

Both Kevin Appleton and Alan Merrell can earn performance related payments under the Group’s Executive Director’s Bonus Scheme, whichis directly linked to the financial performance of the Group. In 2004 the targets set out in the Executive Directors’ Bonus Scheme were notachieved and consequently no bonus payments were earned.

During the year a discretionary payment of £30,000 was paid to Alan Merrell to recognise the efforts made in completing the refinancing of the Group’s bank facilities.

Directors’ service contractsIn keeping with recommended practices under the Combined Code, Lavendon Group’s policy on executive directors’ service contracts is that no notice period of employment should exceed twelve months duration. Contractual termination payments should not exceed a notice period equivalent of the directors’ service contract at the time of termination.

All of the current directors have service contracts with the Company. Details of these are as follows:

Contract Unexpired Notice Contractual Note date term period termination payments

David Price (i) 10 October 1996 Rolling contract 12 months 12 months current salaryKevin Appleton 1 January 2002 Rolling contract 12 months 12 months current salaryAlan Merrell 26 May 1998 Rolling contract 6 months 6 months current salaryJohn Gordon (ii) 10 October 2002 9 months Fixed term 6 months current salaryJohn Heywood (ii) 10 October 2002 9 months Fixed term 6 months current salary

Notes:(i) David Price was originally employed as Chairman of the Group on 12 December 1992. His current contract commenced on the date of the Company’s Listing

on the London Stock Exchange, and was revised with effect from 1 January 2004 to reflect the move to the role of part-time Executive Chairman.

(ii) John Gordon and John Heywood are serving their third terms of appointment with the Company. Their original contracts commenced on the date of the Company’s Listing on 10 October 1996.

12 Lavendon Group plc 2004

Remuneration reportContinued

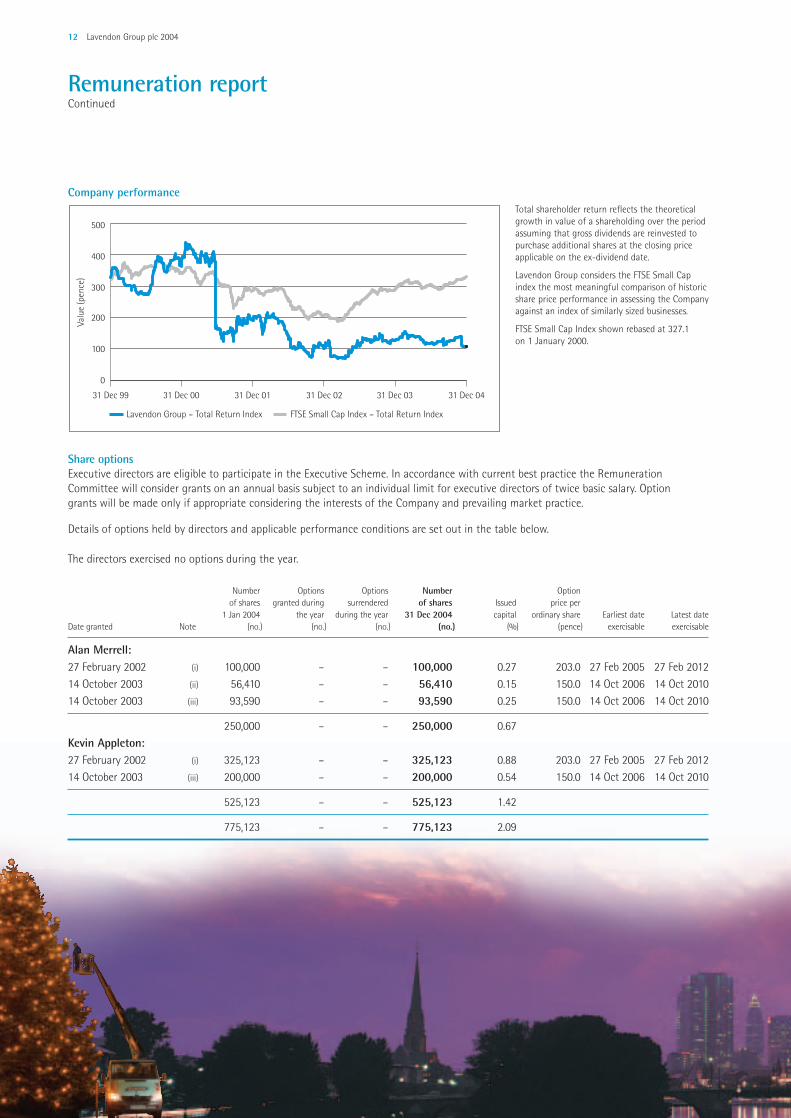

Company performance

Share optionsExecutive directors are eligible to participate in the Executive Scheme. In accordance with current best practice the RemunerationCommittee will consider grants on an annual basis subject to an individual limit for executive directors of twice basic salary. Optiongrants will be made only if appropriate considering the interests of the Company and prevailing market practice.

Details of options held by directors and applicable performance conditions are set out in the table below.

The directors exercised no options during the year.

Number Options Options Number Option of shares granted during surrendered of shares Issued price per

1 Jan 2004 the year during the year 31 Dec 2004 capital ordinary share Earliest date Latest dateDate granted Note (no.) (no.) (no.) (no.) (%) (pence) exercisable exercisable

Alan Merrell:27 February 2002 (i) 100,000 – – 100,000 0.27 203.0 27 Feb 2005 27 Feb 201214 October 2003 (ii) 56,410 – – 56,410 0.15 150.0 14 Oct 2006 14 Oct 2010 14 October 2003 (iii) 93,590 – – 93,590 0.25 150.0 14 Oct 2006 14 Oct 2010

250,000 – – 250,000 0.67Kevin Appleton: 27 February 2002 (i) 325,123 – – 325,123 0.88 203.0 27 Feb 2005 27 Feb 2012 14 October 2003 (iii) 200,000 – – 200,000 0.54 150.0 14 Oct 2006 14 Oct 2010

525,123 – – 525,123 1.42

775,123 – – 775,123 2.09

0

100

200

300

400

500

31 Dec 99 31 Dec 00

Lavendon Group – Total Return Index

31 Dec 01 31 Dec 02 31 Dec 03 31 Dec 04

FTSE Small Cap Index – Total Return Index

Valu

e (p

ence

)

Total shareholder return reflects the theoreticalgrowth in value of a shareholding over the periodassuming that gross dividends are reinvested topurchase additional shares at the closing priceapplicable on the ex-dividend date.

Lavendon Group considers the FTSE Small Capindex the most meaningful comparison of historicshare price performance in assessing the Companyagainst an index of similarly sized businesses.

FTSE Small Cap Index shown rebased at 327.1on 1 January 2000.

Lavendon Group plc 2004 13

Notes:(i) The options granted to Alan Merrell and Kevin Appleton on 27 February 2002 were exceptional grants made by deed (all other options have been granted under the terms

of the Executive Scheme). The options will not be exercisable unless growth in earnings per share (“EPS”) exceeds growth in the Retail Price Index (“RPI”) over theperformance period by at least an average of 8 per cent per annum in the case of Alan Merrell’s option and 3 per cent per annum in case of Kevin Appleton’s option. Theoptions will be exercisable in full if growth in EPS exceeds growth in RPI by at least an average of 12 per cent per annum in the case of Alan Merrell’s option, and 6 per centper annum in the case of Kevin Appleton’s option. Each option will be exercisable on a straight-line basis between nil and 100% between the two applicable percentagetargets. The performance target will be measured over an initial period of three financial years and may be achieved in each successive year thereafter provided that theperiod over which the performance target is measured will be extended to include each additional successive year up to the tenth anniversary of grant and the target willalways be measured from the fixed base of the financial year preceding the year of grant.

(ii) The option will not be exercisable unless growth in EPS exceeds growth in RPI over the performance period by an average of 3 per cent per annum. The option will beexercisable in full if annual growth in EPS exceeds growth in RPI by an average of at least 6 per cent. The option will be exercisable on a straight-line basis between nil and100% between the two percentage targets. The performance target will be measured over an initial three-year period and to the extent that it has not been met, will beretested annually over 0-4 years and 0-5 years, measured from the fixed base of the financial year immediately prior to grant. The option will lapse to the extent that the target has not been achieved by the end of the fifth year.

(iii) The options will not be exercisable unless compound growth in EPS over the performance period is at least an average of 20 per cent per annum. The options will be exercisablein full if compound growth in EPS is at least an average of 30 per cent per annum. The options will be exercisable on a straight-line basis between nil and 100% between these two percentage targets. The performance target will be measured over an initial three-year period and, to the extent that it has not been met, will be retested annuallyover 0-4 years and 0-5 years, measured from the fixed base of the financial year immediately prior to grant. The option will lapse to the extent that the target has not beenachieved by the end of the fifth year. If the Company is subject to a change of control prior to the publication of the Annual Report for the year ended 31 December 2005,these options will become exercisable on a straight-line, time-apportioned basis over the period from 31 December 2002. If the exit price on a change of control exceeds theNet Asset Value as disclosed in the latest Annual Report at that date then 100% of these options will vest irrespective of the average growth in EPS at that date.

Performance conditions of executive optionsIt is the Committee’s policy in setting performance conditions for executive options to set challenging targets in producing earnings pershare growth over the medium term that exceeds basic expectations. The three-year performance measurement encourages appropriatesustained growth in earnings and rewards loyal service by executives.

No other directors have been granted options in the shares of the Company.

The market price of the Company’s shares at 31 December 2004 was 112.5p; the range of market prices during the year was between 111.5p and 172.5p.

Long-term incentive schemesNo directors currently participate in long-term incentive schemes other than in share option schemes.

Subject to shareholder approval at the 2005 Annual General Meeting, executive directors will become eligible to participate in theLavendon Group plc Share Matching Plan 2005. The principal terms of the plan (including the performance conditions which are proposedfor the 2005 awards) are set out in the appendix to the Notice of the Annual General Meeting of the Company dated 7 March 2005 onpages 54 and 55 of this document.

The Remuneration Committee will consider grants on an annual basis and awards will only be made if appropriate considering the interestsof the Company and the prevailing market practice.

It is the Remuneration Committee’s policy in setting performance conditions for the Share Matching Plan to set challenging targets overthe medium term. The three year measurement rewards loyal service by executives. For the 2005 awards the Remuneration Committeeintends to use share price as the measure of performance in order to emphasise the importance of increasing shareholder value.

The Remuneration Committee has decided to recommend that executive directors be able to participate in both the executive option planand the Share Matching Plan in the belief that the combination of both plans will align the interests of these directors more closely withthose of shareholders.

14 Lavendon Group plc 2004

Remuneration reportContinued

Directors’ pension entitlementThe Company made pension contributions amounting to £28,000, being 40% of David Price’s basic salary during the year which was paidinto David Price’s personal pension plan.

The Company contributed 25% of Kevin Appleton’s basic salary to an Executive Pension Scheme. The contribution for 2004 totalled £41,250.

The Company contributed 25% of Alan Merrell’s basic salary to an Executive Pension Scheme. The contribution for 2004 totalled £36,250.

Directors’ interestsThe interests of the directors in the ordinary share capital of the Company are shown below:

Beneficial number of shares

31 December 2004 31 December 2003

David Price 2,853,706 3,553,706Kevin Appleton 10,000 10,000Alan Merrell 12,500 12,500John Gordon 52,623 52,623

John Heywood 70,000 70,000

All directors’ interests are beneficially held. On 1 April 2004, David Price sold 700,000 ordinary shares in the Company at a price of 150.0p per share. There has been no change in the directors’ interests in the ordinary share capital of the Company between 31 December 2004 and 7 March 2005.

John HeywoodChairman of the Remuneration and Nomination Committee

7 March 2005

Lavendon Group plc 2004 15

Directors’ report

Your directors present their report and financial statements of the Group for the year ended 31 December 2004.

Principal activitiesThe principal activity of the Group is the rental of powered access equipment. Powered access equipment is used to provide temporaryaerial access for people in a broad range of applications: in industrial repair and maintenance, construction, telecommunications, outsidebroadcasting, sign erection and highway maintenance. These activities are undertaken both in the UK and overseas.

Review of the businessA review of the business, together with an outlook for the future development of the Group, is contained in the Chairman’s Statement andthe Operational and Financial Reviews.

Financial resultsThe financial results for the year are set out in the consolidated profit and loss account on page 28. The consolidated loss for the year of £13,595,000 (2003: £1,346,000) will be transferred from reserves. The position at the end of the year is set out in the consolidated balancesheet on page 29.

DividendThe directors do not recommend a final dividend for the year, consequently the total dividend for the year is 2.25p per ordinary share.

DirectorsThe present directors of the Company are shown on page 19. Information on the directors’ interests in the ordinary shares of theCompany during 2004 is set out in the Remuneration Report on pages 10 to 14.

No director has, or has had, any beneficial interest in any transaction of significance which has been effected by any Group company at any time during the year.

The Company has maintained insurance throughout the year to cover all directors against liabilities in relation to the Company and its subsidiary undertakings.

EmployeesThe Group pursues a policy of employee communication through regular team briefings and newsletters. Personal employee development isencouraged through the structure provided by the Investors in People National Standard. Employee involvement in the financial performance of the Group is encouraged through a comprehensive range of well established profit share programmes. Furthermore, all employees who workover 25 hours per week are eligible for the grant of share options when they achieve two years service with the Group.

It is the policy of the Group that disabled people, whether registered or not, should receive full and fair consideration for all job vacanciesfor which they are suitable applicants. Employees who become disabled during employment will be retained wherever possible andretrained if necessary. The Group is prepared to modify procedures or equipment wherever this is practicable, to allow full use to be madeof an individual’s abilities.

The Board has issued a statement of business operations and culture detailing the Group’s commitment to ensuring that all employeescomply with all applicable laws and regulations, support a culture of honesty and integrity, conduct operations in an ethical andprofessional manner, and act at all times to prevent impropriety, discrimination, bribery and corruption. The Board has also approved theimplementation of independent reporting procedures across the Group’s operations to assist employees in upholding these standards andto further facilitate communications throughout the organisation.

EnvironmentThe Group’s policy is to harmonise its business operations with environmental best practice to minimise its impact on both its social andnatural surroundings, where this is operationally feasible. This practice is embodied within the Group’s Quality accreditation and Healthand Safety Policies and compliance is monitored by field based Systems auditors. As part of this process, maintenance of the rental fleetis of a high and regular standard to minimise noise and emission pollution. Consumable recycling and waste disposal are undertakendiligently and fuel oils are stored safely.

16 Lavendon Group plc 2004

Directors’ reportContinued

Fixed assetsDuring the year the Group’s total capital expenditure on tangible fixed assets amounted to £2,317,000. Details of this expenditure,and all other fixed asset movements, are set out in notes 15, 16 and 17 to these financial statements.

Issue of share capitalBy resolutions passed on 6 May 2004 the directors were:

i. generally and unconditionally authorised for the purposes of Section 80 of the Companies Act 1985 (the ‘Act’) to exercise all the powers of the Company to allot relevant securities up to an aggregate nominal amount of £123,344 and

ii. empowered, pursuant to Section 95 of the Act, to allot shares for cash up to an aggregate nominal amount of £18,501 (being 5 per centof the Company’s issued share capital at that time) as if Section 89 of the Act did not apply with regard to pre-emption rights.

These authorities expire at the conclusion of the Annual General Meeting, and your directors propose that renewal should be sought. Suchproposals are set out as resolutions 6 and 7 in the Notice of the Annual General Meeting on page 51. Details of any movements in sharecapital during the year are set out in note 24 to these financial statements.

Share option schemesThe Company established two share option schemes on admission of its ordinary shares to the Official List of the London Stock Exchangeon 10 October 1996, namely:

i. the Lavendon Group 1996 Company Share Option Plan (the ‘Employee Scheme’); andii. the Lavendon Group 1996 Unapproved Executive Share Option Scheme (the ‘Executive Scheme’).

Options are normally granted under the terms of the schemes on the day following the announcement of the Group’s interim and annualfinancial results each year at an option price equal to the mid-market quoted share price derived from the London Stock Exchange DailyOfficial List at the close of trading on the preceding day.

The value of options granted to any individual during the year is subject to an individual limit such that the aggregate exercise price of alloptions granted during the year cannot exceed 200 per cent of basic annual salary in the case of a director, or 100 per cent in case of anyother employee.

Options are granted subject to the following performance targets:

The Executive Scheme:An option will not be exercisable unless growth in Earnings Per Share (“EPS”) exceeds growth in the Retail Price Index (“RPI”) over theperformance period by an average of 3 per cent per annum. The option will be exercisable in full if growth in EPS exceeds growth in RPI by an average of at least 6 per cent per annum. The option will be exercisable on a straight line basis between these two percentage levels.

The Employee Scheme:An option will be exercisable in full if growth in EPS exceeds growth in RPI over the performance period by an average of at least 3 per cent per annum.

All performance targets are measured over an initial three year period and to the extent that they are not met, will be retested. In the caseof an option granted in the period to 31 August 2003 the target may be achieved on a three-year rolling basis up to the tenth anniversary of grant in the case of the Employee Scheme, and the seventh anniversary in the case of the Executive Scheme. Any options granted afterthis date will be capable of being retested annually over 0-4 years and 0-5 years, provided that the target will always be measured from thefixed base of the financial year immediately prior to grant and the option will lapse to the extent that the target has not been achieved by the end of the fifth year.

Lavendon Group plc 2004 17

Details of options granted to executive directors are disclosed separately in the Remuneration Report on pages 10 to 14.

Details of all other share options granted to date under the terms of the schemes are shown below:

Ordinary Option Options Options Options not Optionsshare options Issued price per exercised since lapsed since exercisable at exercisable at

granted capital ordinary share date of grant date of grant 31 Dec 2004 31 Dec 2004Date granted Note (no.) (%) (pence) (no.) (no.) (no.) (no.)

i. The Employee Scheme:11 October 1996 121,370 0.33 140.5 74,973 36,101 – 10,296 27 March 1997 10,256 0.03 236.5 3,994 3,555 – 2,707 2 September 1997 23,302 0.06 242.5 10,078 8,128 – 5,09616 March 1998 21,216 0.06 381.5 2,931 17,475 – 810 24 August 1998 25,732 0.07 407.5 – 22,592 – 3,140 16 March 1999 (1) 37,220 0.10 329.5 – 34,981 2,239 –24 August 1999 (1) 33,454 0.09 407.5 – 31,159 2,295 –9 March 2000 (1) 44,270 0.12 410.5 – 40,957 3,313 –15 August 2000 (1) 30,832 0.08 463.5 – 27,212 3,620 –14 March 2001 (1) 41,584 0.11 510.0 – 34,022 7,562 –6 September 2001 (1) 86,055 0.23 208.5 – 41,338 44,717 –26 February 2002 114,114 0.31 203.0 – 42,045 72,069 –5 September 2002 227,392 0.61 127.5 – 99,566 127,826 –5 March 2003 287,038 0.78 90.0 – 86,990 200,048 –5 September 2003 185,304 0.50 136.0 – 49,176 136,128 –14 October 2003 46,963 0.13 150.0 – 5,172 41,791 –3 March 2004 137,237 0.37 160.0 – 20,679 116,558 –8 September 2004 244,194 0.66 120.0 – 2,375 241,819 –

1,717,533 4.64 91,976 603,523 999,985 22,049

ii. The Executive Scheme:11 October 1996 – 14 March 2001 (2) 700,324 1.89 140.5-510.0 61,489 638,835 – –26 February 2002 167,375 0.45 203.0 – 57,244 110,131 – 5 September 2002 25,000 0.07 127.5 – – 25,000 –5 September 2003 65,000 0.18 136.0 – 25,000 40,000 –14 October 2003 114,739 0.31 150.0 – – 114,739 –3 March 2004 157,623 0.42 160.0 – – 157,623 –8 September 2004 50,000 0.14 120.0 – – 50,000 –

1,280,061 3.46 61,489 721,079 497,493 –

Note:(1) Options granted under the terms of the Employee Scheme in the period March 1999 to September 2001 inclusive have not achieved the required performance criteria to

31 December 2004 and remain unexercisable at this date.

(2) Options granted under the terms of the Executive Scheme between 11 October 1996 and 14 March 2001 have been fully exercised or lapsed at 31 December 2004.

Substantial shareholdingsAt 28 February 2005 the following interests in the ordinary share capital of the Company had been notified:

Name % interest

M&G Investment Management Limited 14.98Cycladic Capital Management Limited 12.93Goldman Sachs International 8.97

The directors are not aware of any changes in these substantial shareholdings up to 7 March 2005.

The interests of the directors in the ordinary share capital of the Company are set out in the Remuneration Report on pages 10 to 14.

18 Lavendon Group plc 2004

Directors’ reportContinued

Charitable donationsCharitable donations amounting to £6,479 (2003: £6,298) were made during the year. There were no donations to political parties duringthe year.

Post balance sheet eventOn 25 February 2005 the Group disposed of its Austrian subsidiary. Details of the sale are given in note 30.

Policy on payment of suppliersThe Company’s creditor payment period at 31 December 2004 was Nil days (2003: Nil) as the Company had no trading activities.

AuditorsA resolution to reappoint our auditors, PricewaterhouseCoopers LLP, will be proposed at the Annual General Meeting, including authorityfor the directors to fix their remuneration.

By order of the Board

Alan MerrellSecretary

7 March 2005

Statement of directors’ responsibilities

The directors are required by the Companies Act 1985 to prepare financial statements for each financial year which give a true and fair viewof the state of affairs of the Company and the Group as at the end of the financial year and of the Group’s profit or loss for that period.

The directors are also responsible for ensuring the keeping of proper accounting records which disclose with reasonable accuracy thefinancial position of the Company and the Group, and they have a general responsibility to safeguard the assets of the Company and theGroup, and to prevent and detect fraud and other irregularities.

The directors confirm that suitable accounting policies, consistently applied and supported by reasonable and prudent judgements andestimates, have been used in the preparation of the financial statements, and that applicable accounting standards have been followed.

The directors have acknowledged the latest guidance on going concern and have formed a judgement at the time of approving thefinancial statements, having made all relevant enquiries, that the Group has adequate resources at its disposal to continue its operationsfor the foreseeable future.

By order of the Board

Alan MerrellSecretary

7 March 2005

Lavendon Group plc 2004 19

Directors and advisers

DirectorsDavid Price, aged 59, ChairmanDavid Price has been Chairman of the Group since it was established in 1992 and until January 2002 also held the role of Chief Executive.Prior to establishing Lavendon he held various senior management positions, both in the UK and overseas, with GKN plc. In particular,in 1986 he became Chairman and Chief Executive of the building services division of GKN plc where he established powered accessbusinesses in Australia, USA and the UK. His role as Executive Chairman became part-time with effect from January 2004.

Kevin Appleton, aged 44, Chief ExecutiveKevin Appleton was appointed Chief Executive to the Group in January 2002. He has spent most of his senior management career withinthe international logistics and materials handling industry. Most recently he was the Managing Director for the European business ofDexion Group Limited.

Alan Merrell, aged 44, Group Finance DirectorAlan Merrell has been Group Finance Director since May 1998. He qualified as a Chartered Accountant in 1984. Prior to joining the Grouphe had spent the previous 12 years in the transportation industry with TNT Post Group where he held a number of financial roles, both inthe UK and overseas, before becoming Finance Director for its international business operation.

John Gordon, aged 65, Senior Non-Executive Director, Chairman of Audit Committee, member of Remuneration and Nomination CommitteeJohn Gordon qualified as a Chartered Accountant in 1965 before commencing a career in corporate finance in the City which culminated inhis being Head of Corporate Finance at Capel-Cure Myers and then at Beeson Gregory Limited before his retirement in March 1996. He iscurrently non-executive Chairman of UCM Group plc and Epic Group plc. He is also a non-executive director of Alizyme plc and ImprintSearch and Selection plc where he also serves as Chairman of both the Remuneration and Audit Committees at both companies.

John Heywood, aged 67, Non-Executive Director, Chairman of Remuneration and Nomination Committee, member of Audit CommitteeJohn Heywood was formerly Managing Director of Jardine Matheson and Company Limited and a director of various public and privatecompanies in the Far East, Middle East, South Africa and the USA. He is also a non-executive director of F&C Asset Management plc,where he also serves on the Remuneration and Audit Committees.

Secretary and Registered OfficeAlan Merrell, 1 Midland Court, Central Park, Lutterworth, Leicestershire LE17 4PN

Advisers

AuditorsPricewaterhouseCoopers LLP, Cornwall Court, 19 Cornwall Street, Birmingham B3 2DT

Solicitors Ashurst, Broadwalk House, 5 Appold Street, London EC2A 2HA

BankersBank of Scotland, 1 Bede Island Road, Bede Island Business Park, Leicester LE2 7EA

StockbrokersEvolution Securities Limited, 100 Wood Street, London EC2V 7AN

RegistrarsCapita Registrars, The Registry, 34 Beckenham Road, Beckenham, Kent BR3 4TU

Public RelationsWeber Shandwick Square Mile, Fox Court, 14 Grays Inn Road, London WC1X 8WS

20 Lavendon Group plc 2004

Corporate governance

Statement of appliance of corporate governance policies and the combined codeThe directors believe as a Board that their principal function is to deliver sustainable wealth to the Group’s investors, and that this shouldbe achieved within the acknowledged corporate governance guidelines. The directors confirm that they have continued to ensure that theGroup applies and maintains the principles of good corporate governance, in so far as is practicable and appropriate for a public companyof this size.

The directors have set out below the means by which they apply current best practice corporate governance procedures within the Groupand the extent of that compliance with the Listing Rules of the UK Listing Authority (12.43A) relating to the provisions of the Principles ofGood Governance and Code of Best Practice (the ‘Combined Code’ – as revised in 2003).

In particular, during their review, the directors have acknowledged the latest guidance on going concern and have formed a judgement at the time of approving the financial statements, having made all relevant enquiries, that the Group has adequate resources at its disposalto continue its operations for the foreseeable future.

A DirectorsA1 The Board

The Board of directors currently comprises three executive and two non-executive directors all of whom served a full year in officeduring 2004. The responsibilities of each director and the identity of the senior non-executive director are detailed on page 19 of thefinancial statements.

1.1 The members currently comprising the Board provide the Group with a range of industry, financial and commercial knowledge andexperience. This combination of skills and interests facilitates the Board in formulating the decisions and strategies which the Groupadopts and ensures that all directors are able to make a significant and individual contribution to all such matters. Biographical details ofeach director, including current directorships held in other non-Group companies, are detailed on page 19 of the financial statements.

The Company maintains a schedule of matters reserved for decisions by the full Board which incorporates release of a number ofcorporate and statutory disclosures (including the Annual Report itself), approval of major operating strategies, composition of relevantCommittees and management structures, and policies relating to ethical, health and safety matters.

The directors provide effective leadership and control of the Group by means of regular Board meetings throughout the year. Relevantpapers are circulated to all members of the Board on a timely basis and in advance of each meeting and the quantity and focus of suchinformation is reviewed on an ongoing basis. Directors provide feedback to management to continually enhance reporting formats andcontent of Board papers and, in addition, make individual enquiries of management wherever necessary to ensure that they are in receiptof all relevant information to allow the appropriate decisions to be made with regard to Group matters. The Chairman also holds strategyand review meetings with the executive directors at other intervals throughout the year.

The Group appoints employees in key executive positions throughout the business to provide strong management teams in its maincountries of trade. These management teams comprise both local directors and senior management whose aim is to deliver expectedfinancial performance and to develop and implement both operational and non-operational improvements within their businesses.These management teams report directly to executive Board directors and a formal Group Executive Committee meets on a regularbasis to receive the key reports from each country of operation and each business functional unit. This facilitates the day-to-daymanagement of the subsidiaries concerned by supporting a devolved process of decision-making which in turn allows the GroupBoard to focus resources more efficiently within the Group.

1.2 The Chairman, David Price, reduced his previous full-time commitment in assuming the position of part-time Executive Chairmanfrom 1 January 2004. Kevin Appleton holds the position of Chief Executive Officer.

John Gordon has been designated the Senior Independent Director

The Remuneration and Nomination Committee comprises the two non-executive directors and its remit includes the responsibilityrelating to decisions of nominating and appointing new directors. John Heywood is the Chairman of the Remuneration andNomination Committee.

Lavendon Group plc 2004 21

The Audit Committee comprises the two non-executive directors and its remit includes the responsibility relating to appointment ofauditors, policy on procurement of other non-audit services and internal monitoring and reporting procedures. John Gordon is theChairman of the Audit Committee.

During 2004, the Board held 8 formal meetings. The attendance of each director at these meetings is shown in the table below:

Director K A Appleton J E Gordon J A Heywood A S Merrell D L Price

Attended in person 8 8 8 8 8Apologies given – – – – –

1.3 The Chairman is given the opportunity to meet at least annually with the non-executives separately from the other directors in orderto review the contributions and performance of all individuals comprising the Board. Further details of this process are given in A.6.1below. This process was approved during 2004 and a formal review of the Board’s performance has been undertaken.

1.4 Minutes of Board meetings are agreed by all directors ensuring that the Company maintains appropriate records of all relevant matters.

1.5 The Company reviews conduct and liability issues as part of its annual risk review and mitigates these exposures where possible.

A2 Segregation of duties2.1 The Board has a part-time Executive Chairman and a Chief Executive Officer enabling separation of the appropriate shareholder

interests from the day-to-day operational requirements of the business. Each has clear lines of responsibilities and reporting whichhave been agreed by the Board.

2.2 The incumbent Chairman was appointed directly to this role in 1996 at the time of the Company’s flotation.

A3 Board balance and independence3.1 The two non-executive directors constitute in excess of one third of the total Board members. The non-executive directors are

considered to provide a strong and independent monitor on the performance of both the Group and its executive management,thereby performing an essential role in safeguarding investors’ interests.

3.2 The Board believes that both non-executive directors are independent within the guidance of the Combined Code as they have noconflicting business interests with the Group, they are remunerated on a fixed salary basis only and have adequate and unfetteredaccess to consultation with internal management and with professional external advisors to the Group. Their backgrounds in industryand finance make them suitably qualified to provide sufficient input and guidance to adequately perform their required duties, both tothe Board, and as members of both the Audit, and Remuneration and Nomination Committees.

3.3 Significant shareholders in the Company are offered the opportunity to meet with the senior independent director of the Companyannually at which time any concerns may be raised separately from the other Board directors. In addition, both the non-executivedirectors ensure that they are available for questions from individual shareholders on the day of the Annual General Meeting.

A4 Appointments to the Board4.1 The Remuneration and Nomination Committee comprises the two non-executive directors of the Company and has written terms of

reference. These terms of reference are published for information purposes on the Group’s website (www.lavendongroup.com). BothCommittee members are considered to be independent.

During 2004, the Remuneration and Nomination Committee held 2 formal meetings. The attendance of each director at thesemeetings is shown in the table below:

Director J E Gordon J A Heywood

Attended in person 2 2Apologies given – –

22 Lavendon Group plc 2004

Corporate governanceContinued

4.2 The incumbent non-executive directors currently hold appointments for a term period of three years ending on 9 October 2005.This is the second reappointment under three-year contracts of both directors following their initial appointments by the Board on 10October 1996. Fees for the non-executives are determined by the Board. The reappointment or rotation of non-executive directors isaddressed after giving due consideration to their qualifications, continuing independence, and willingness to accept reappointment.

As the current non-executive directors will have each completed nine years continuous service during 2005, the NominationCommittee has recommended that the Board develop succession plans for when the non-executive directors reach the end of theirthird term of appointment on 9 October 2005. The Board has accepted the Committee’s recommendation and has appointed anindependent executive recruitment agency to commence the search for two replacement non-executive directors.

4.3 The Chairman currently holds no other roles which are considered to impair or conflict with his abilities to serve the Company appropriately.

4.4 The terms and conditions of appointment of the non-executives are available for inspection at the Company’s registered office andduring the Company’s Annual General Meeting each year.

4.5 The work of the Nomination Committee is detailed in a separate Remuneration Report on pages 10 to 14 of the financial statements.

A5 Information and professional development5.1 The Group has agreed procedures for the directors to take any professional independent or individual advice as may be necessary in

carrying out their duties. New directors are offered training and advice tailored to their needs upon appointment to the Board and alldirectors have continuing access to such support as and when it is required.

5.2 The joint role of Finance Director and Company Secretary, held by Alan Merrell, ensures that the directors have ready access to theCompany Secretary in all relevant matters and that compliance with Board procedures is maintained.

A6 Performance evaluation6.1 Following the recommendations introduced in the Revised Combined Code the Board has completed an evaluation for 2004 of the

performance of the Board, its Committees and each director. The directors completed detailed appraisals on matters relevant to theBoard, its Committees and director performance. A report was presented to and reviewed by the Board and various action plans arebeing developed in response to its recommendations. The Board intends to carry out further performance evaluations on an annual basis.

A7 Re-election7.1 In accordance with the Articles of the Company a maximum of one third of the directors offer themselves for re-election each year

subject that each director shall stand for re-election within a time period not exceeding three years from the date of their previous re-election. This year Kevin Appleton retires by rotation and will seek re-election. Biographical details and the Annual General Meetingparticulars are detailed on page 19 and on pages 51, 52 and 53 of the financial statements respectively.

7.2 No non-executive directors retire by rotation at the Annual General Meeting in 2005.

B RemunerationThe Remuneration Committee considers it is currently complying in full with the relevant provisions of the Combined Code and outlinesits procedures and guidelines in a separate Remuneration Report on pages 10 to 14 of the financial statements. Details of the directors’remuneration and interests in shares during 2004 are included within this Report. In addition the Committee, in line with considered bestpractice, will invite the members of the Company to vote on the Remuneration Report at the Company’s Annual General Meeting on28 April 2005, details of which are given on pages 51, 52 and 53 of the financial statements respectively.

C Accountability and auditC1 Financial reporting1.1 The directors and auditors set out their respective responsibilities for preparing and reviewing the accounts in the Statement of

directors’ responsibilities on page 18 and in the Independent auditors’ report on page 27 of the financial statements respectively.

Lavendon Group plc 2004 23

1.2 The directors have acknowledged the latest guidance on going concern and have formed a judgement at the time of approving thefinancial statements, having made all relevant enquiries, that the Group has adequate resources at its disposal to continue itsoperations for the foreseeable future.

C2 Internal control2.1 The directors operate a system of internal controls within the Group that exist to minimise or control business risks in order to

safeguard investors’ interests. The Board has overall responsibility for ensuring that the Group maintains a system of internal controlsthat will provide them with reasonable, but not absolute, assurance of the reliability of the financial information used within thebusiness and for external publication, as well as safeguarding the assets of the Group against unauthorised use or disposition.

Although no system of internal controls can provide absolute assurance against material misstatement, loss or mismanagement of theGroup’s assets, the systems in place are designed to identify to the directors matters which require attention on a timely basis so thatthey may be considered and dealt with appropriately.

The directors have considered the systems of internal control in operation during the past financial year and are able to report theirfindings under the following headings:

Control environmentThere is a clearly defined organisational structure that allows the Group’s objectives to be planned, communicated, executed, controlledand monitored. The Group is committed to employing suitably qualified staff so that the appropriate level of authority can bedelegated to ensure the efficient management of the business. The main UK operating subsidiary was accredited with the Investors inPeople award in June 1996 in recognition of its achievements in supporting a culture of ability and progression for its staff. Duringreview in 2004 the appropriate body has recommended that this accreditation be renewed.

Identification and evaluation of business risks and control objectivesThe identification and evaluation of financial business risks facing the Group are reviewed and approved at Board level as part of thedevelopment of the annual operating and budgetary plans. For other non-financial business risks the Board meets annually to formallyconsider and review the extent and nature of the major perceived risks to the business and the effectiveness of its internal controls insafeguarding against these risks. In addition, appropriate control policies are continually monitored and developed to manage any newareas of risk identified. These policies are communicated and enforced throughout all appropriate areas of the organisation.