annual report 2016 - greenergy report 2016_web... · £13.7 bn turnover £ 52.6 m ebitda...

TRANSCRIPT

ANNUAL REPORT 2016

USA

BRAZIL

CANADAUK FAR EAST/

CHINA

MIDDLE EAST

26Supply locations

24% Sales volume

increase in Canada

Domestic diesel supply

New petrol blending

joint venture

908 Shipments of fuel products

received

137 Train wagons importing fuel to the region

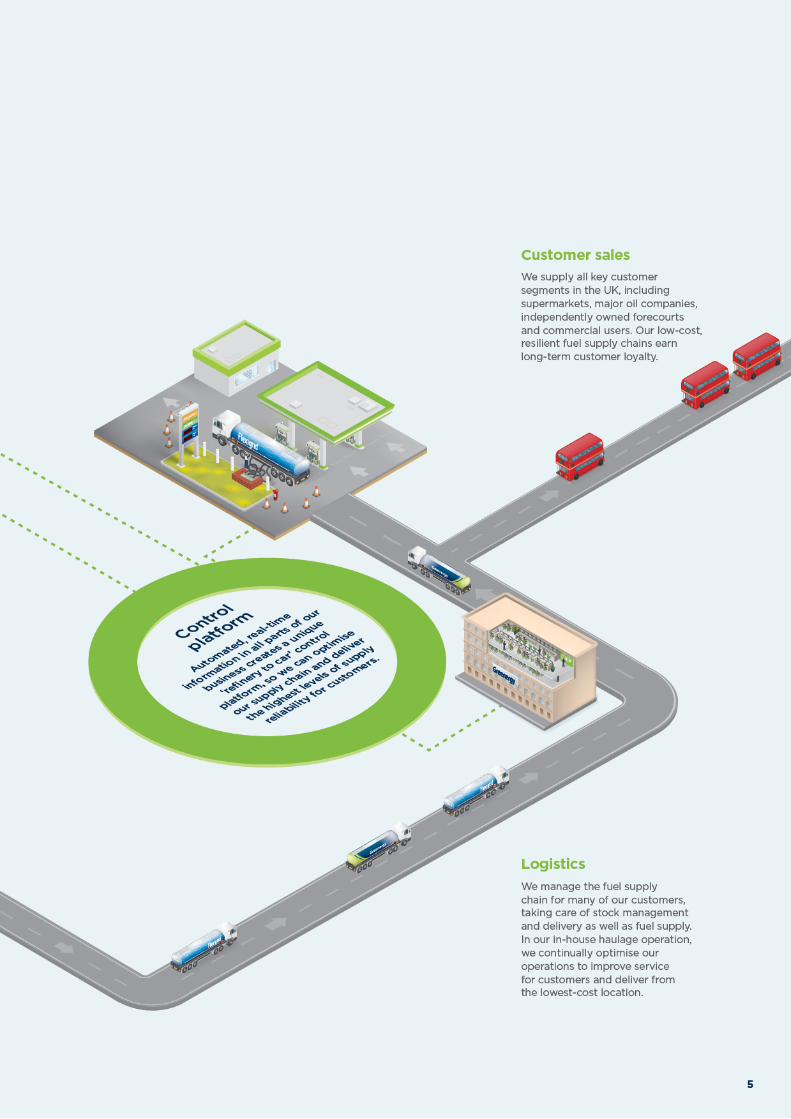

We are the UK’s leading supplier of road fuelWe are replicating our UK successes to grow internationally

18.1bn Litres of fuel

supplied globally

2016 Greenergy Annual Report2

Overview

£13.7bn

Turnover

£52.6m

EBITDA (pre-exceptionals)

£57.9m

Profit before tax

£15.7bn

£13.7bn

£14.1bn

FY14

FY16

FY15

£3.8m

£6.8mFY14

FY16 £57.9m

FY15

£23.5m

£52.6m

£30.3m

FY14

FY16

FY15

Financial Highlights Strategic Report

OverviewOur business model 4Our mission 6Strategic summary 8

Chairman’s Statement 10

Chief Executive’s Review 14

Health and Safety Safety record 22Approach 24

Market ReviewGlobal markets 28UK market 30Our other markets 32

Strategy in Action UK Fuels 36International Fuels 44Infrastructure 48Haulage 56

Key Performance Indicators Financial KPIs 59Service quality KPIs 60

Chief Financial Officer’s Review 62

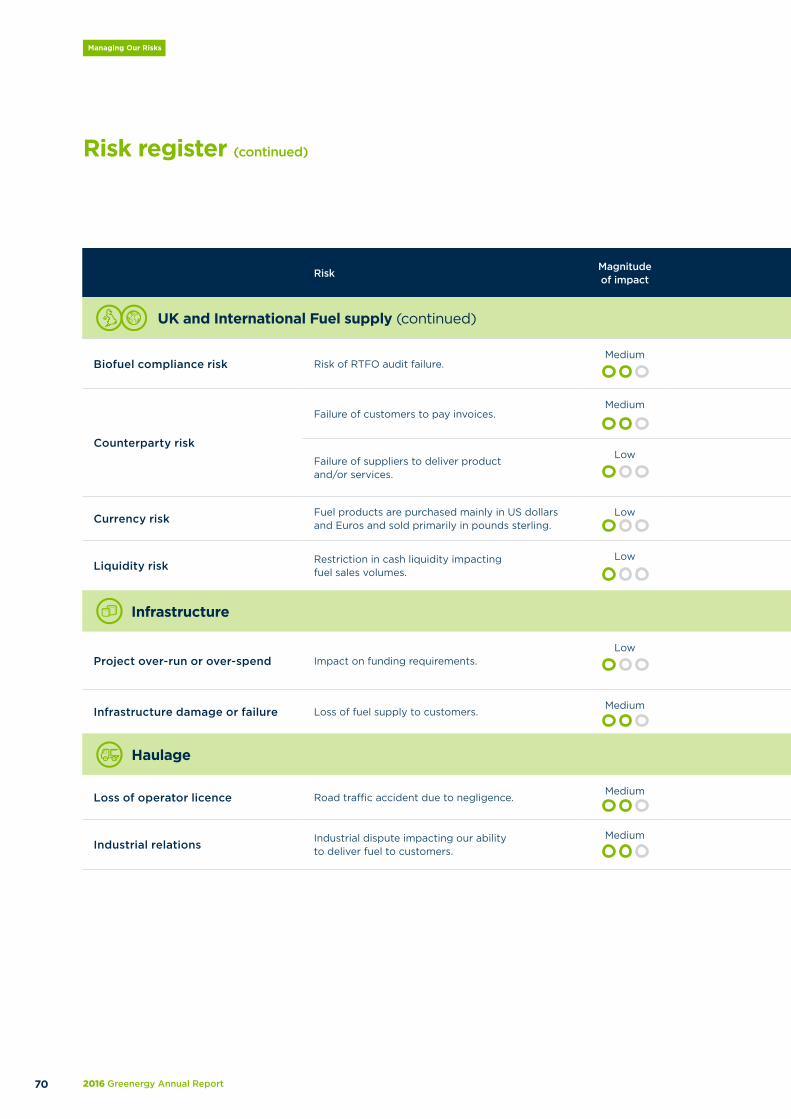

Managing Our RisksRisk overview 67Risk register 68Risk analysis 72

People and EnvironmentApprenticeships 80Employment 81Biofuel sustainability 82Carbon emissions 84Carbon savings from biofuel 85

Strategic Report 85

Governance

Board of Directors 88

Statement on corporate governance 90

Directors’ report 92

Financials

Independent auditors’ report 96

Consolidated income statement 97

Consolidated statement 98 of comprehensive income

Consolidated and Company 99 balance sheets

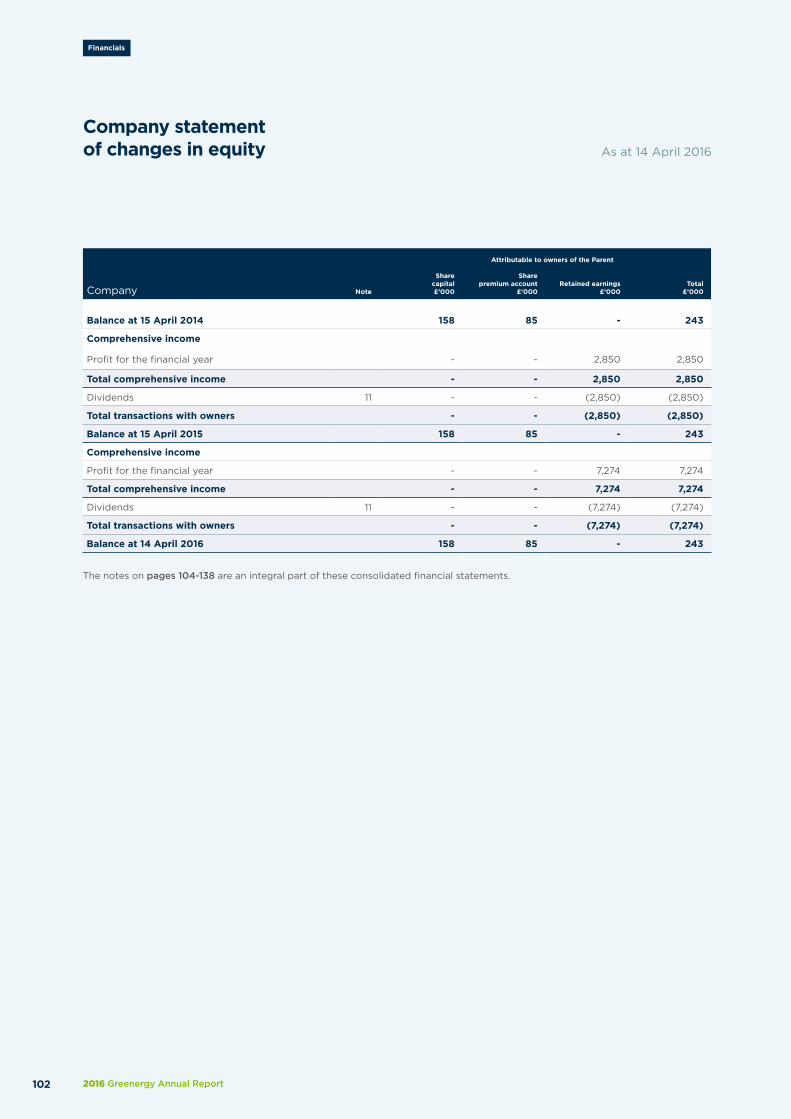

Consolidated statement 101 of changes in equity

Consolidated and Company 103 statements of cash flows

Notes to the financial statements 104

Officers and professional advisors 138

3

» Lowest cost» Highest reliability» Best systems and control» Easiest people to deal with» Most transparency.

Our missionTo deliver long-term customer partnerships by being the fuel provider with the:

2016 Greenergy Annual Report6

Overview

7

UK Fuels p36

International Fuels p44

UK Fuels International Fuels Infrastructure Haulage

STRATEGIC ICONS

UK Fuels International Fuels Infrastructure Haulage

STRATEGIC ICONS

Our aim: Develop low-cost and resilient fuel supply chains to earn the long-term loyalty of our UK customers

Our aim: Expand internationally by replicating our UK successes in other markets

Highlights

» Continued development of our import capabilityto allow us to receive fuel on larger, lower-cost ships.

» Strong biodiesel manufacturing margins as a resultof greater raw material flexibility, improved reliabilityand increased output.

» Conclusion of long-term storage contractswith Navigator Terminals at strategic locations,including where we have petrol blending facilities.

» Growth in sales to independent forecourtoperators, including under our BrandedWholesaler agreement with Esso.

Highlights

» Successful start to our new Cargoflo rail-to-road supplylocation in Canada. This first-of-its-kind facility offersa low-cost distribution concept in a new location thatis convenient for our customers.

» First diesel imports into Brazil, marking the startof a fuel import and supply business in a new market.

» Planning for a new joint venture with the BahrainPetroleum Company (Bapco) to blend petrol to meetdomestic Bahraini demand and for import/export.

UK Fuels

International Fuels

Strategic summary

2016 Greenergy Annual Report8

Overview

Infrastructure p48

Haulage p56

UK Fuels International Fuels Infrastructure Haulage

STRATEGIC ICONS

UK Fuels International Fuels Infrastructure Haulage

STRATEGIC ICONS

Our aim: Acquire, regenerate and operate assets that support our supply chain objectives

Our aim: Make reliable and cost-efficient fuel deliveries to customers through our in-house haulage operation

Highlights

» Opening of Thames Oilport for diesel storageand completion of infrastructure that will be needed as we move on to a fully-fledged import and distribution terminal.

» Creation of Navigator Terminals to invest in fuel and chemical storage in the UK. This gives Greenergy greater influence at key supply locations in theUK and creates a platform for future growth that is underpinned by long-term investment income.

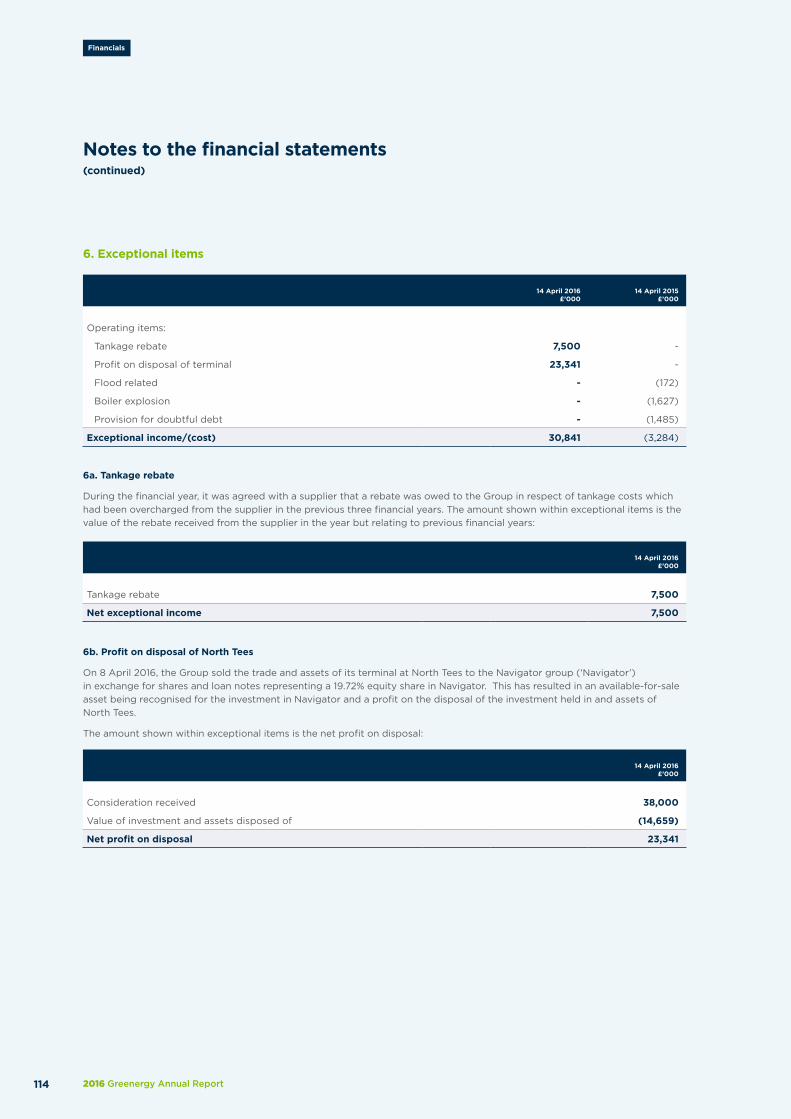

» Sale of Greenergy North Tees to Navigator Terminals after four years of regeneration.

Highlights

» Continued safe operations, with increased resourcingof driver training and an ever greater safety awarenessamongst drivers.

» Cost-efficiency improvements, with an expansionof our driver workforce leading to improved fleetutilisation and profitability.

Infrastructure Haulage

9

This was another strong year for the business, both financially and operationally. We completed strategically important infrastructure transactions and derived value from all parts of our supply chain to deliver our best-ever financial results.

2016 Greenergy Annual Report10

Chairman’s Statement

Paul LesterChairman

Health and Safety p20

Global markets p28

UK market p30

Chairman’s Statement

Market

The underlying changes in the UK fuels market continue to favour our business.

Road fuel demand in the UK continued to grow this period, up 2.1%. This is the third consecutive year of UK market growth, following a five-year period of decline. While diesel consumption rose by 4.3%, petrol demand declined by 1.5%, continuing the trend of the last decade, and by year-end diesel consumption reached 63% of total road fuel demand (FY15: 61.6%).

This trend means that the few remaining UK refineries are increasingly producing too much petrol and not enough diesel to meet the UK’s product demand profile, leaving the UK structurally short of diesel. As a result, in calendar year 2015, the UK again imported more fuel than it exported and, in spite of a temporary recovery in refinery production, net imports were at their highest level for more than 30 years.

UK refinery supply of petrol and diesel

This was the most successful year ever for the business financially. We have capitalised on our previous infrastructure investments and acquisitions to drive financial success.

Safety

We continue to identify, assess and mitigate the risks associated with our operations as our first priority. Our approach is founded on a culture of open and honest reporting and we encourage everyone working in the business to observe, report and respond to hazards, near misses and unwanted events, without fear of blame. This is an extension of the values of care and ownership which extend across the business.

We have also increased our focus on process safety at Group as well as site level, with continuous review and improvement of our safe operating standards, an extension of process safety training which included the Non-Executive Directors and completion of our first round of process integrity audits.

Oil prices continued to fall in the early part of this period, reaching a ten-year low of $27/barrel in January 2016 before recovering somewhat. This did not directly impact sales margins because customer pricing is based on spot market prices, our operating inventory is relatively constant and we remain hedged against price fluctuations.

Low crude oil prices drove an increase in refinery production globally, which in turn resulted in an abundance of refined products and contango market conditions for diesel. This made it profitable to store oil and created opportunities for us to bring redundant storage capacity back into operation in our own facilities, including at Thames Oilport.

We expect UK refinery production to continue to decline as refiners increasingly struggle to sell their surplus petrol in other markets and as competitive pressures grow from refiners in the US, Middle East and Asia. Greenergy is best-placed to make up the shortfall in domestic refinery production by supplying low-cost product imported from the most efficient producers around the world.

500

400

300

200

600

kb/d

Diesel

Petrol

2005 2010 2015 2020 F

11

Infrastructure p48

Corporate governance p91

Operational performance

We continued to explore new sales opportunities both within the UK and internationally, expanding our fuel sales in the UK and supplying diesel into Brazil for the first time. Our Canadian business delivered a profit after two years of development and investment.

Strategic investments

During the period we acquired Vopak’s one third share in the Thames Oilport joint venture with Shell. In addition, we co-founded Navigator Terminals with Macquarie Capital to acquire Vopak’s UK operating bulk fuel storage terminals as well as Greenergy’s North Tees Terminal. The establishment of Navigator provides a platform for continued growth in key infrastructure to support our business, both in the UK and abroad.

With our low-cost model, the scale of our operation and our import infrastructure, we are ideally placed to capture future opportunities created by a growing requirement for fuel imports, both in the UK and internationally.

The hidden highlight for me this year was the effectiveness of our control processes across all parts of the business. Market conditions were favourable and, with robust daily operations throughout the period, we consistently captured the opportunities that the market presented.

Financial performance

This was another strong year for the company, with EBITDA (excluding exceptionals) reaching £52.6m, and we derived value across all segments of our business. Financially we benefited from a global diesel surplus, keeping our supply costs low, as well as strong petrol blending and biofuel margins.

Supply chain and blend margins were strongest at locations where we have made infrastructural investment – a pay-back from our strategyover the last decade.

Corporate governance

We are committed to operating to high standards of corporate governance, measuring ourselves against the best publicly quoted companies. We will continue to review our processes in this context as the scale and breadth of our business grows.

This year saw a further increase in our risk management processes. We are increasingly fostering a risk awareness culture within our business, with constant activity to minimise risk across management levels and functions.

Chairman’s Statement (continued)

2016 Greenergy Annual Report12

Chairman’s Statement

In its referendum on 23 June 2016 the UK voted to leave the European Union. Whilst the changes to the UK’s trading relationships are still uncertain, we do not anticipate any problematic outcomes for the business and are confident in our ability to manage the impact of any changes.

We have a track record of managing change effectively and, as an entrepreneurial business, are quicker than many of our competitors to identify and respond to opportunity. We are ready to capture any opportunities created by a UK Brexit to create value for the business.

Q&AHow will the UK’s referendum vote on EU membership affect Greenergy?

Outlook

Over the last decade we have positioned ourselves to take full advantage of underlying changes in the UK market caused by refinery closures. We have invested in the infrastructure we need to meet the UK’s growing fuel import requirements and to benefit from the availability of low-cost products sourced from global refiners.

Our participation within Navigator Terminals will allow us to develop existing assets to their fullest potential. It also creates a funding base for further acquisitions within the UK and to support our expansion in new markets.

13

Paul LesterChairman

Our infrastructure capability is important to our success, allowing us to access global markets and lowest-cost products to meet customers’ fuel requirements. Having completed strategically important infrastructure transactions, we now have greater control of key facilities to support future growth.

14

Chief Executive’s Review

2016 Greenergy Annual Report

Andrew OwensChief Executive

Health and safety p20

UK market p30

Global markets p28

Sales volume growthChief exec review

Sales volume growth

FY120

20

15

10

FY13 FY14 FY15 FY16

Bill

ion

litr

es

10.9

13.5 15

.0 15.6

5

18.1

Safety, health, environment and quality

We have continued to operate with safety and environmental care as our first priority in a culture of open and honest reporting. There were no RIDDOR dangerous occurrences this period and an improvement in the rate of RIDDOR reportable and lost-time injuries, but the number of minor injuries (not requiring time off work) increased. We continue to address this through increased discussion and awareness training.

Maintaining our focus on process safety at Group as well as at site and function level, we completed a single set of safe operating standards that define the expectations for the management of safety across the business. We will continue to develop and improve this going forward and to share learnings with our colleagues in Navigator.

Markets

Refinery expansion outside Europe resulted in a significant surplus of diesel globally. With our growing sales volume and deep-water import infrastructure, we were able to benefit from this global supply/demand imbalance by importing diesel on larger ships, strengthening our diesel margins.

Since January 2015 we have operated three petrol blending facilities in the UK. This gives us additional economies of scale and, with petrol demand falling in the UK and elsewhere in Europe, we were able to source competitively-priced petrol products for blending from European refiners which had limited alternative markets.

Results

Our global sales volume for the period totalled 18.1 billion litres, up 15% on the same period last year.

EBITDA (excluding exceptionals) amounted to £52.6m this period, significantly improved on FY15 (£30.3m). This was due to a combination of factors:

» Continued sales growthin the UK and internationally

» Strong purchase margins for diesel

» Strong petrol blend marginsthrough our in-houseblending operations

» Strong biodiesel manufacturingmargins driven by increasedproduction and supplychain flexibility

» Prior to the creation of NavigatorTerminals, infrastructureincome from third-partystorage at North Tees

» Continued unit cost reduction,to £6.67 per cbm excludingacquisitions (FY15: £6.79).

Chief Executive’s Review

15

13%

UK sales growth FY16

+11% FY15

UK Fuels p36

Opportunities in new regions

Q&ALooking ahead, how will this year’s financial performance be sustained?

International growth

UK Fuels

Our UK sales volume has continued to rise, up 13% in FY16. Additional volume has come both from increased business with existing customers and from new sectors, including sales growth to the independent forecourt sector. We will continue to explore opportunities to expand existing sales and to introduce new products at new locations.

We will also maintain our programme of infrastructure development. Further planned integration of Navigator facilities on Teesside and progress at Thames Oilport are expected to create further economies of scale and greater operational flexibility.

We are using our UK experience and capabilities to expand in new regions.

» We have developed a successful rail import modelin Canada, with flexible low-cost supply chains fromNorth America and Europe. We are now pursuingfurther sales growth at existing and new locations.

» We are exploring opportunities to expandour diesel import operations in Brazil.

» In the Middle East, we are bringing ourpetrol blending expertise into a new jointventure with Bapco, the national oil companyof the Kingdom of Bahrain.

16

Chief Executive’s Review

2016 Greenergy Annual Report

Our strategy is to grow profits in our core UK Fuels business by continuing to invest in infrastructure to deliver cost and operational efficiencies, while replicating our success by growing in international markets with similar import dynamics.

£57.9m

Profit before tax FY16

£3.8m FY15

Navigator fuel terminals

OtherInfrastructure

We partnered with Macquarie Capital to co-found Navigator Terminals. This strategic investment gives us greater influence over supply facilities that are key to our ongoing UK business. In addition, it provides access to long-term, low-cost capital to finance major infrastructure investments and facilitate future growth.

Thames Oilport continues to be a key development project, offering potential for sales growth and giving us the ability to receive products on larger ships, further improving our access to global markets. We now have a clear route-map to develop the terminal in phases.

Our strong financial performance this year and the transfer of Greenergy North Tees into Navigator Terminals will reduce our capital constraints going forward. We are now in a position to fund further acquisitions and infrastructure investments, either directly as Greenergy or within Navigator, to support our continued growth.

17

358Independently owned forecourts

298 FY15

UK Fuels p36

Strategy

UK FuelsWe have continued to grow our business in a highly competitive market place. Our UK market share for the period averaged 28% for fuel originated by Greenergy (FY15: 25%) and 35% including domestic third-party purchases (FY15: 32%).

Growth in UK petrol and diesel sales has primarily been from locations where we have made infrastructural investment and acquisition. These investments have allowed us to develop low-cost, global supply chains with which to compete successfully in the market. As our sales volume grows, we are increasingly developing economies of scale, to optimise our purchasing, receive product on larger ships and drive down unit costs.

We also increased sales to independent forecourt operators, including as part of our Branded Wholesaler agreement with Esso. This remains a relatively new area of business for us offering potential for long-term growth. As we begin to establish a reputation in the sector as a flexible and high service fuel supplier, the number of sites we were contracted to supply has increased, reaching 358 at year-end (FY15:298).

We made further upgrades and expanded capacity at our biodiesel manufacturing facilities, resulting in greater raw material flexibility, improved reliability and increased output. We also further diversified our supply chains for waste oils, to source from new markets globally and to purchase product in smaller containers. As a result, our biodiesel manufacturing operations made a significant additional contribution to profits this year. With our manufacturing operations producing more biodiesel than we require for our own blending, we also increased biodiesel sales to third parties.

We reconfigured operations as a sole user of the Navigator Thames terminal to improve efficiency. This has reduced variable costs and reduced waiting times for customers and for our in-house haulage operation. A long-term contract has been concluded with Navigator Terminals, to secure our continued access to this facility.

International FuelsIn Canada, we commenced fuel sales from a new location north of Toronto. Developed in partnership with Canadian National Railway, this is a first-of-its-kind rail-to-road Cargoflo facility that uses the train as the tank terminal. This offers a low-cost distribution concept in a new location that is convenient for our customers. Despite the loss of an important customer elsewhere, sales have been strong. Our Cargoflo rail-to-road facility in Toronto reached capacity within nine months of commissioning, enabling us to commit to expanding the facility in 2016.

We made our first diesel imports for sale within Brazil, a market historically supplied predominantly from domestic production. These imports leveraged long-standing relationships with storage companies and diesel users in Brazil and have taken advantage of trading windows created by lower international diesel prices, a favourable US Dollar-Real exchange rate and high domestic diesel prices within the Brazilian market. We expect the Brazilian market to continue to open up to competition as Petrobras focuses on other matters and we will explore opportunities to increase our involvement going forward.

We have used our infrastructure capability to deliver supply chain flexibility and resilience, allowing us to retain and win new business in our home market and internationally.

Chief Executive’s Review (continued)

18

Chief Executive’s Review

2016 Greenergy Annual Report

Thames Oilport p50

International Fuels p44

Post year-end we concluded a new joint venture between Greenergy and the Bahrain Petroleum Company (Bapco) to blend petrol to meet domestic Bahraini demand and for import/export. Bapco’s facilities are located on a trading channel in and out of the Arabian Gulf and form an ideal base for a new petrol blending operation.

InfrastructureIn this period we acquired Vopak’s shares and voting rights in Thames Oilport directly, giving us a two thirds shareholding in the joint venture with the remaining third held by Shell. As a separate transaction, we also established Navigator Terminals in partnership with Macquarie Capital, to acquire Vopak’s other UK assets as well as the operational storage assets of Greenergy North Tees. Both transactions are strategically important for Greenergy, giving us greater influence over infrastructure that is key to our continued success in the UK market.

I am pleased at the significant progress that has been made in the development of Thames Oilport during this period. Under the new ownership structure the regeneration of the terminal is being carried out in phases. In the first phase, we brought some 175k cbm of tankage back into use for diesel storage and restored pipeline connections from the tanks to the jetty. A further 32k cbm of diesel tankage is planned for our own use from Q3 2017. By storing diesel, we have benefited from contango market conditions to generate revenue in FY17 that can be re-invested.

The works completed so far have prepared infrastructure that will be needed in future stages in the development of Thames Oilport, as we move on to storage and road loading for diesel, gasoil and kerosene and, eventually, petrol. In preparation for these future works, we also recommenced our own petrol project development engineering.

Meanwhile, demolition of former refinery infrastructure has continued clearing land not required for an import terminal, allowing us to market it for alternative uses.

We made significant investment to upgrade our North Tees terminal following the acquisition from Petroplus in 2012. Most significantly, we integrated the terminal with the neighbouring Seals Sands petrol blending facility, allowing us to add petrol throughout and export by rail. This investment enabled us to maximise value through the sale of the facility to Navigator during the year and gives us a platform to further integrate with Seal Sands, also now owned by Navigator Terminals, to create a fuel and chemical storage hub in the North East.

HaulageOur in-house operation has again provided a safe and reliable operation, providing visibility, control and team spirit in this essential part of our supply chain.

We recruited more drivers into the business this period in order to deliver more fuel and created cost efficiencies by improving the utilisation of our vehicle fleet. The number of drivers we employed on average across the year increased to 285 (FY15: 261).

Outlook

Our business has again proved robust to changing market conditions. Our continuing success stems from our import model, which enables us to optimise our purchasing in response to global market trends.

As we expand within the UK and internationally, we will continue to prioritise infrastructure development in order to develop further supply chain flexibility and operational efficiencies.

19

Andrew OwensChief Executive

We continue to focus on safety across our business as our number one priority.

Health and Safety

20

Health and Safety

2016 Greenergy Annual Report

21

Barbara LeadbetterHead of Process Integrity

‘‘Our Process Integrity committee ensures that health and safety issues are addressed openly and are resourced appropriately. The Committee brings together Executive Directors, terminal and manufacturing plant managers and our SHEQ team.

’’

Safety record

Our health and safety reporting is open and transparent.

There was a further reduction in the rate of RIDDOR reportable and lost time injuries this period. However the rate of minor injuries (not requiring time off work) increased and is being addressed through increased discussion and awareness workshops.

There were no RIDDOR dangerous occurrences.

There were seven separate RIDDOR reportable injuries across the business:

» One in our fuel terminal operations, being a twisted ankle

» Six in our haulage operations, of which two resulted from slips and trips, two from manual lifting, one from running and one from banging an elbow exiting a vehicle.

22

Health and Safety

2016 Greenergy Annual Report

Incident rate per 100,000 hours worked

FY14-15

0

0.16 0.65

1.1

2.4

18.2

172.3

Incident rate per 100,000 hours worked

FY15-16

Incident rate per 100,000 hours worked

FY15-16

occurrence

0

0.0 0.53

0.98

3.9

16.8

213.0

injury

Fatalities

Fatalities

RIDDOR dangerous occurrence or injury

RIDDOR dangerous occurrence or injury

Lost time injury

Lost time injury

Minor injuries

Minor injuries

Near misses

Near misses

Hazard observations

Hazard observations

Group safety record FY16

Definitions RIDDOR dangerous occurrence: an incident with a high potential to cause death or serious injury (as defined by the RIDDOR regulations).

RIDDOR or lost time injury: an injury resulting in an absence from work beyond the shift in which the injury was sustained or one which led to significant injury such as a fracture or serious burns.

Minor injury: an injury which is not RIDDOR reportable and does not require time off work or restricted work duties.

Near misses: an unplanned event that did not result in injury, illness, damage or non-compliance but which had the potential to do so.

Hazard observations: an ‘act’ or a ‘condition’ that has the potential to cause injury, loss or damage.

23

213 486Hazard observations across business

Customer site risk assessments completed

per 100,000 hours worked in FY16

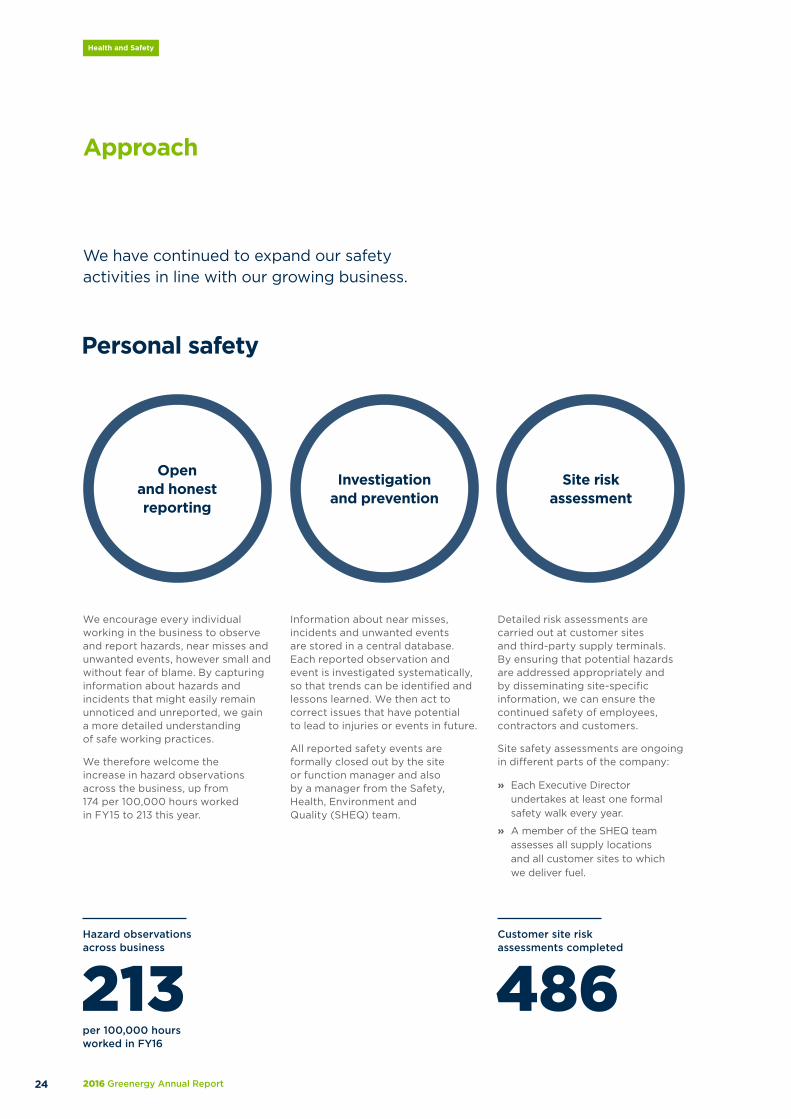

Open and honest reporting

Investigation and prevention

We have continued to expand our safety activities in line with our growing business.

Approach

Personal safety

We encourage every individual working in the business to observe and report hazards, near misses and unwanted events, however small and without fear of blame. By capturing information about hazards and incidents that might easily remain unnoticed and unreported, we gain a more detailed understanding of safe working practices.

We therefore welcome the increase in hazard observations across the business, up from 174 per 100,000 hours worked in FY15 to 213 this year.

Information about near misses, incidents and unwanted events are stored in a central database. Each reported observation and event is investigated systematically, so that trends can be identified and lessons learned. We then act to correct issues that have potential to lead to injuries or events in future.

All reported safety events are formally closed out by the site or function manager and also by a manager from the Safety, Health, Environment and Quality (SHEQ) team.

Detailed risk assessments are carried out at customer sites and third-party supply terminals. By ensuring that potential hazards are addressed appropriately and by disseminating site-specific information, we can ensure the continued safety of employees, contractors and customers.

Site safety assessments are ongoing in different parts of the company:

» Each Executive Director undertakes at least one formal safety walk every year.

» A member of the SHEQ team assesses all supply locations and all customer sites to which we deliver fuel.

Site risk assessment

24

Health and Safety

2016 Greenergy Annual Report

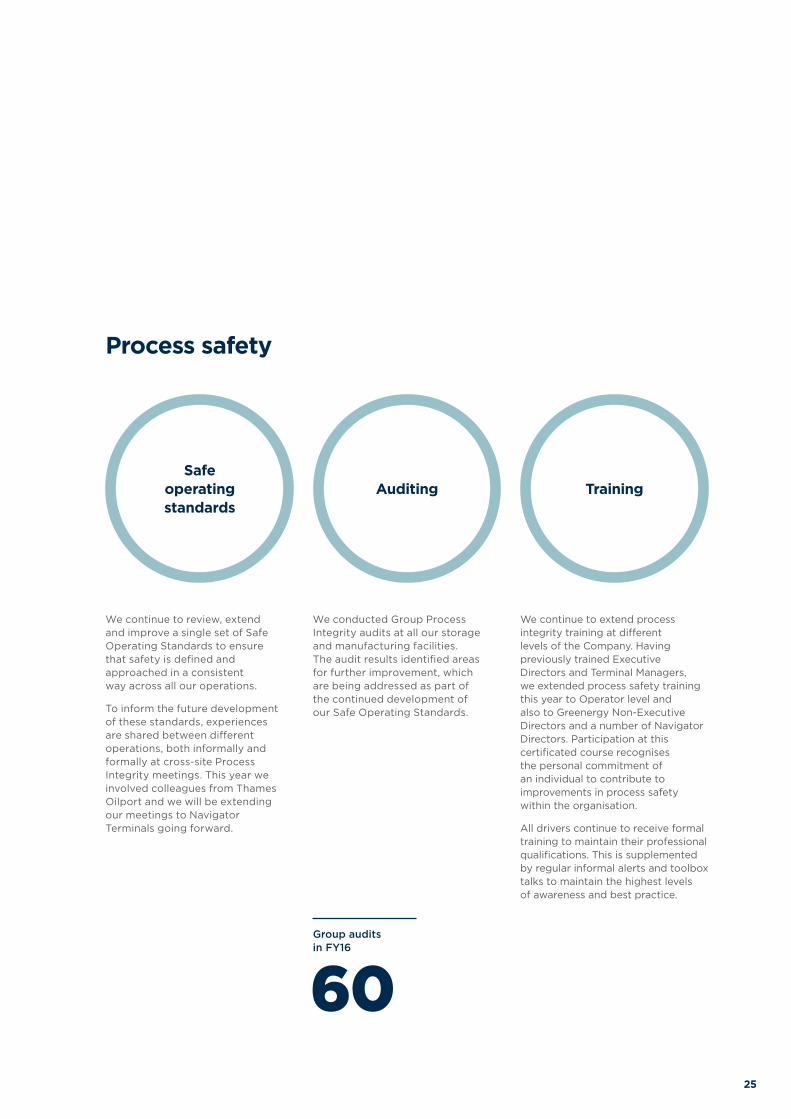

60Group audits in FY16

Safe operating standards

Auditing

Process safety

We continue to review, extend and improve a single set of Safe Operating Standards to ensure that safety is defined and approached in a consistent way across all our operations.

To inform the future development of these standards, experiences are shared between different operations, both informally and formally at cross-site Process Integrity meetings. This year we involved colleagues from Thames Oilport and we will be extending our meetings to Navigator Terminals going forward.

We conducted Group Process Integrity audits at all our storage and manufacturing facilities. The audit results identified areas for further improvement, which are being addressed as part of the continued development of our Safe Operating Standards.

We continue to extend process integrity training at different levels of the Company. Having previously trained Executive Directors and Terminal Managers, we extended process safety training this year to Operator level and also to Greenergy Non-Executive Directors and a number of Navigator Directors. Participation at this certificated course recognises the personal commitment of an individual to contribute to improvements in process safety within the organisation.

All drivers continue to receive formal training to maintain their professional qualifications. This is supplemented by regular informal alerts and toolbox talks to maintain the highest levels of awareness and best practice.

Training

25

Market Review

Globally, the supply of refined products exceeded demand. However, in the markets where we supply fuel, supply/demand imbalances resulted in a structural requirement for fuel imports.

26

Market Review

2016 Greenergy Annual Report

27

We used our deep-water import infrastructure to source diesel not required regionally in Asia, the Middle East and the US. With expansion of the refining sector in these countries expected to continue, access to these markets will continue to be strategically important.

Middle East

+2.7m b/d

China

+2.4m b/d

Other Asia

+1.65m b/d

Europe

–0.1m b/d

North America

+1.15m b/d

Expected change in regional refining capacity 2015–2021*

Global markets

Higher refinery utilisation rates combined with refinery expansion in Asia, North America and the Middle East resulted in an oversupply of diesel. We were able to access this low-cost diesel through our deep-water import terminals.

28

Market Review

2016 Greenergy Annual Report

370

450

430

410

390

$/t

on

ne

Contago price structure

Jan 2017 Nov 2017

ICE Diesel Future Price, 14 April 2016

May 2016

370

450

430

410

390

$/t

on

ne

Contago price structure

Jan 2017 Nov 2017

ICE Diesel Future Price, 14 April 2016

May 2016

Contango price structure

Increased refinery production

Brent crude oil prices fell to their ten year low of $27/barrel in January 2016 before recovering somewhat. However, product prices remained buoyant relative to crude, pushing up refining margins and refinery utilisation rates, particularly in the first half of FY16. At the same time, refinery expansion continued in Asia, the Middle East and North America.

These factors together resulted in a 2mb/d increase in global refinery production in 2015 compared with the previous calendar year*.

Supply/demand imbalances

The growth in refinery production was not matched by demand growth (up 1.6mb/d in 2015*). With most new refinery capacity set up for higher diesel yields, the increase in refinery production was stronger for diesel than for petrol. Demand growth, on the other hand, was primarily for petrol, driven by lower fuel prices in North America and increased vehicle ownership in China and India.

This created a global surplus of diesel particularly, resulting in:

» A significant increase in storage of products globally and, by December 2015, a seasonal record of diesel stocks in Europe*

» Contango market conditions for diesel.

* Source: IEA

The over-supply of diesel resulted in contango market conditions this year, meaning that prompt prices were lower than forward prices.

The level of contango was sufficient to cover tankage and working capital costs and therefore it was advantageous to store products.

This expedited the development of Thames Oilport within the joint venture and we brought into use an initial 175cbm tankage for diesel storage. Elsewhere, most of our storage capacity is fully utilised for our ongoing fuel supply commitments, but we did bring into use additional tankage for contango storage at Navigator North Tees.

We expect to continue to benefit from contango market conditions during FY17.

A contango market

29

Net petroleum product imports into the UK market

(15)

(10)

(5)

5

0

10

15

2004 2006 2008 2010 2012 2014 2016 F 2018 F 2020 F

Mill

ion

to

nn

es

Net imports

Net exports

Declining UK refinery production

UK refinery production declined in 2015, continuing the trend of the last decade. The causes of declining refinery output remain unchanged:

» Competition from larger and lower-cost refiners in other regions

» A mismatch between UK refined products and consumption patterns. UK refiners produce a surplus of petrol and a deficit of diesel relative to domestic consumption and are constrained by their ability to sell surplus petrol internationally.

We expect UK refinery utilisation rates to decline further until 2020.

Diesel demand growth

Demand for road fuel in the UK increased 2.1% overall in the financial year. Once again all of that growth was in diesel demand, up 4.3% (FY15: up 3.3%), with petrol demand falling by 1.5% (FY15: down 2.5%). This is an ongoing trend caused by continuing dieselisation of the car fleet and by the improving fuel efficiency of petrol-engined vehicles. By the end of this financial year diesel accounted for 63% of road fuel consumption (FY15: 61.6%) with petrol accounting for just 37% of the market (FY15: 38.4%). This growth in diesel demand relative to domestic refinery production is expected to continue to drive the UK’s import requirements.

UK market

Rationalisation of UK refinery capacity has made the UK structurally reliant on imports to meet its fuel requirements. We are well positioned to meet this shortfall with supply through our import terminals.

30

Market Review

2016 Greenergy Annual Report

The UK was a net importer of petroleum products in 2015 by 9.3m tonnes. This is the highest annual figure since 1984, when industrial action in the coal sector led to greater demand for oil products for electricity generation.

With our access to import infrastructure and our low-cost model, we have the capacity to meet the UK’s growing import requirements.

Insight

The UK’s growing reliance on fuel imports

31

EASTERNCANADA

BRAZIL

MIDDLEEAST

Growing regional production deficit

as a result of refinery closure, population growth and a strong

economy

Commenced diesel supply as the

Brazilian market opens up to external

competition

Joint venture to meet petrol

demand in India, China

and Middle East

Our other markets

Our international expansion is in markets with import requirements.

32

Market Review

2016 Greenergy Annual Report

International Fuels p44

International Fuels p44

International Fuels p44

Supply chain flexibility

Changing regional dynamics

Petrol blending

Brazil

Historically domestic petrol and diesel supply has been almost exclusively from Petrobras, but this market is increasingly opening to outside competition. Petrobras’ position has been diminished by the ongoing corruption scandal, with refinery projects cancelled and a lack of investment in alternative supply. At the same time, road fuel demand is growing due to increasing vehicle ownership and a return to economic growth.

This year we commenced diesel imports into Brazil, having previously been an ethanol exporter. As the country’s requirement for fuel imports grows, there is potential to increase our infrastructure and fuel supply position in this market.

Middle East

We negotiated a petrol blending joint venture in the Kingdom of Bahrain which will be formed shortly after year-end.

Eastern Canada

We supply fuel in the Eastern provinces of Canada, which account for 65% of Canadian road fuel demand. This region is an import market in which:

» Refinery production has declined following refinery closures in 2010 (Dartmouth) and 2013 (Montreal).

» Road fuel demand has been robust due to population and economic growth.

This period we imported fuel from Western Canada and the US Mid-West, where refinery production increased due to the availability of low-cost crude oil produced from fracking. Refineries in these areas are landlocked and, unable to export by sea, sought markets elsewhere in North America.

This represents a change from 2014 and 2015, when most of the petrol we supplied in Canada originated in Europe.

33

Strategy in Action

Our strategy is to grow our core UK fuels business, replicate our successes internationally and continue to invest in strategic infrastructure and operations.

2016 Greenergy Annual Report34

Strategy In Action

35

Strategy in actionFuel sales by customer segment

12%

23%

17%

48%

Fuel sales by customer segment

UK Fuels International Fuels Infrastructure Haulage

STRATEGIC ICONS

‘‘Competition in the UK road fuel market was again intense. We bought well to reduce product costs and delivered strong manufacturing margins, allowing us to continue to retain and win new business. We maintain our focus on cost reduction and service quality in order to deliver a compelling customer offer and maintain our loyal customer base.

’’

Aim: Develop low-cost and resilient fuel supply chains to earn the long-term loyalty of our UK customers

Caroline LumbardUK Trading Director

Hypermarkets Independents

Oil majors Other

UK Fuels

2016 Greenergy Annual Report36

Strategy In Action

Ross

Clydebank

TeessideSeal Sands

North Tees

Thames Oilport

Thames

Cardi�

Plymouth

With our own import infrastructure in key demand regions and lifting rights at inland locations, we have a unique national supply capability.

Greenergy stock-managed terminals

Biofuel manufacturing facilities

Areas of population density

Supply locations

Our UK supply locations and facilities

Infrastructure p48

37

UK Fuels (continued)

Strategic priority 1 Source diesel from the lowest-cost global producers

With the expansion of the global refining sector and a growth in global diesel production ahead of demand, there was a rise in diesel imports into Europe from the Middle East and the Baltics. This increased the availability of diesel in the European market.

With an ownership interest in the UK’s only deep-water road fuel jetties, at Navigator North Tees and Thames Oilport, we were able to purchase lowest-cost diesel both from within the European market and direct from global producers, giving us supply chain flexibility and strong purchase margins.

Strategic priority 2 Blend petrol from component products

We operate sophisticated petrol blending systems at three UK locations, being Navigator Thames, Navigator Seal Sands and Inter-Terminals Seal Sands (effective January 2015). The operation of three facilities this year created greater operational flexibility.

Blend margins were strong due to an over-supply of petrol products in the European market. Although naphtha, typically one of our main petrol blend components, was expensive relative to petrol, other blend products that had historically been exported to the USA became available at favourable prices.

Global market review p28

Our import infrastructure enabled us to take advantage of global oversupply of refined products, to source products from lowest-cost producers wherever they are.

Petrol blend margins

By purchasing petrol blend components, typically from outside the UK, and combining them to make UK-specification petrol we:

» Generated purchase and blend margins by blending component products for less than the market value of the finished petrol

» Controlled the supply reliability and quality of the petrol we supplied

» Produced customer-specific petrol grades, such as high octane fuels.

2016 Greenergy Annual Report38

Strategy In Action UK Fuels

Size of ships importing Greenergy fuel into the UK

25,000

20,000

0

15,000

5,000

10,000

Ave

rgae

car

go

siz

e (c

bm

)

700

680

660

540

640

620

580

560

600

Nu

mb

er o

f sh

ips

FY11 FY12 FY16FY15FY13 FY14

Number of cargoes

Average ship size

21,068

11,777

We have an ownership interest in two of the UK’s deep-water road fuel jetties, at Navigator North Tees and Thames Oilport. These give us the ability to import fuel on larger ships and buy direct from producers in the US, Middle East or Asia, when this is the lowest-cost option.

Further planned development of Navigator and Thames Oilport facilities will allow us to increase our long-haul imports in future.

Deep-water fuel imports

39

423m

Third-party biodiesel sales in litres

FY12 FY13 FY14*

*A�ected by floodingFY15 FY16

cbm

Strategy in actionBiodiesel production

FY12 FY13 FY14*

*A�ected by floodingFY15 FY16

cbm

Strategy in actionBiodiesel production

UK Fuels (continued)

Strategic priority 3 Biofuel manufacturing and supply

Biodiesel manufacturing

We own two of Europe’s largest waste-to-biodiesel production facilities, having purchased the right to operate our second facility in January 2015.

Further upgrades at both facilities resulted in greater raw material flexibility, improved reliability and increased output. In particular, we installed a new refinery distillation column at our Teesside facility, increasing capacity, and built facilities to receive waste oils in smaller containers, allowing us to purchase from suppliers without bulk storage. This has allowed for further diversification of our global waste oil supply chains and reduced raw material costs.

Transfer of knowledge and experience between both facilities also created cost savings and production efficiencies, including through allocation of raw materials with different quality characteristics to the most appropriate site.

Biodiesel production

Biofuel sales to third parties

Our biofuel sales focus on matching the right product with the right customer, recognising the specific sustainability requirements of different customers and markets. By applying our sustainability expertise across different continents, we maximise the value of biofuel we supply.

Biodiesel sales to third parties grew significantly this year from new storage arrangements in Rotterdam. These included biodiesel manufactured in our UK facilities and not required for our own blending.

Ethanol sales to other oil companies in the UK, Europe and the USA also grew. We used our sustainability expertise to source products meeting different customer requirements. As our ethanol origination grows and we buy from multiple parties, we were increasingly able to optimise our purchasing to benefit from market opportunities.

Generation and sale of RTFO certificates

We blend biofuel into the fuel we supply in order to meet UK biofuel supply obligations and generate Renewable Transport Fuel Obligation (RTFO) certificates which can be sold to other oil companies.

Demand for RTFO certificates fell this year and the volume of our certificate sales was lower. However, we expect demand to increase from April 2017 when a change in legislation is expected to increase RTFO biodiesel inclusion mandates.

In the first full year of operating a second biodiesel manufacturing facility, our own biodiesel production increased by 75%. We also grew biodiesel sales to third parties from new storage arrangements in Rotterdam.

2016 Greenergy Annual Report40

Strategy In Action UK Fuels

Strategic priority 4 Create cost and operating efficiencies

Fuel storage

We concluded long term storage contracts on the Thames and Teesside as part of our participation in Navigator Terminals, securing our long-term access to these strategically important import locations.

As a sole user of the Thames terminal we further reconfigured operations to create operating efficiencies. By re-utilising pipelines we were able to discharge ships more quickly, cutting ship-related costs and reducing our use of other higher-cost terminals.

Service quality KPIs p60

Under-utilised third-party tankage arrangements at Eastham were terminated and we now supply customers from lower-cost locations. We continue to review all our third-party tankage arrangements based on regional supply requirements.

Supply from the lowest- cost supply location

The terminal or refinery that is closest to a customer site is not necessarily the lowest-cost supply location. Therefore we use our own LP programme to calculate product and haulage costs from different supply locations on a daily basis and schedule deliveries accordingly. By optimising delivery patterns to customers in this way, we generated significant cost savings this year.

We also reconfigured road loading facilities, significantly reducing waiting times for customers and for our in-house haulage operation.

‘‘Each month we look back at how successful we have been in implementing the lowest-cost supply option, comparing with a theoretical optimum. By analysing patterns, we have learned new ways of cutting costs and improving efficiency.

’’ Nuno Do ValleGroup Optimisation Analyst

41

UK Fuels (continued)

Strategic priority 5 Grow in new markets

Independent forecourt sector

Over the last decade major oil companies have significantly scaled back their UK downstream operations, selling or closing refineries and disposing of company-owned sites. The independent forecourt sector has grown as a result and the market continues to open up to fuel suppliers such as Greenergy.

We have developed an innovative supply offer which gives forecourt operators a choice of forecourt brands, including the Esso, Nisa or operators’ own brands, combining competitively priced fuel with the highest standards of supply reliability and customer service.

We plan to: » Commence fuel sales from Thames Oilport

» Create cost efficiencies through increased use of larger ships

» Further optimise biodiesel manufacturing operations

» Continue to expand sales to the independent forecourt sector.

In a major enhancement to our customer offer, we developed a new fuel card scheme which was piloted after year-end.

Sales growth in other sectors

Sales growth was also achieved in other parts of our UK business:

» Spot sales, to customers buying on the day rather than under a long-term contract, were up 51% on FY15 following the introduction of a sales force dedicated to this part of our business.

» We significantly expanded sales from Ross, a new supply location that we took on in January 2015.

» We began selling kerosene from North Tees and Ross.

» Increased sales of gasoil, up 45% on FY15.

2016 Greenergy Annual Report42

Strategy In Action UK Fuels

164

298

358

FY14

FY15

FY16

We have further expanded our fuel supply to independent forecourt operators, including as part of our Branded Wholesaler agreement with Esso.

The number of independently-owned forecourts we were contracted to supply increased to 358 at year-end (Esso: 269; Nisa: 7; other: 82).

Case Study

Independent forecourts

43

Sales volume in Canada

244

400 49

4

0

500

400

300

Mill

ion

litr

es

100

200

FY14FY13 FY15 FY16

UK Fuels International Fuels Infrastructure Haulage

STRATEGIC ICONS

Aim: Expand internationally by replicating our UK experience in other markets

CanadaSales growth

BrazilFirst diesel imports

Middle EastNew petrol blending in Bahrain

International Fuels

44

Strategy In Action

2016 Greenergy Annual Report44

Strategy In Action Rail-to-road facility Canada

We plan to: » Increase sales from existing locations

» Develop further rail-to-road supply locations

» Develop deep-water import capability in the east of Canada

» Further develop our logistics capability in the US Mid-West.

Our Canadian business has established itself as a low-cost and reliable provider of fuels in the Ontario and Quebec regions of Canada, with a unique supply chain concept. The business made its first positive contribution to consolidated EBITDA this period, in only its second full year of operation.

Strategic priority 1 Develop low-cost supply chains from North America and Europe

A priority this year was to diversify our product sourcing in order to reduce reliance on local refiners and increase supply optionality, minimise product costs and deliver improved supply resilience for customers.

We developed alternative sources of supply from North America, establishing new flexible supply partnerships with refiners in the US Mid-West. As part of this, we took on new tankage arrangements in the US Mid-West to enable us to load product from refinery pipelines onto railcars for delivery to our supply locations in Canada. To support these relationships, we moved our US office from Georgia to Houston.

Strategic priority 2 Expand our supply footprint and increase sales

Sales commenced from our innovative new rail-to-road facility north of Toronto, developed in partnership with Canadian National Railway. This facility allows petrol and diesel to be loaded directly from railcars onto trucks and makes use of existing rail infrastructure to create a new supply location in a heavily congested area.

The rail-to-road concept, known as Cargoflo, was received well by the market and our sales from the facility were strong. Following year-end we commenced an expansion project at our Toronto facility, doubling its capacity. We have also completed engineering studies to bring two new facilities to market in FY17.

Our sales volume in Canada increased 24% compared with FY15.

The number of railcars that we operate increased to 137 (FY15:116) while lease costs per railcar fell.

We continued to import petrol from Europe, although this year our petrol blending facilities were fully utilised in meeting our UK supply commitments.

Canada

45

We negotiated a new joint venture with Bahrain Petroleum Company, the national oil company of the Kingdom of Bahrain, to create a regional petrol blending hub in the Middle East.

Strategic priority 3 Develop new relationships in the Middle Eastern market

Planning was completed this period for a new joint venture between Greenergy and Bahrain Petroleum Company (Bapco) to blend petrol to meet domestic Bahraini demand and for import/export, which was announced post year-end.

The joint venture, called Bahrain Gasoline Blending (BGB), combines Bapco’s infrastructure and refinery petrol production with Greenergy’s expertise in blending, terminal operation and trading.

Middle East

BGB will blend petrol components produced by Bapco’s refining operations and purchased from third parties. It intends to sell finished-grade petrol to Bapco and to customers in the region and further afield.

‘‘Our new gasoline blending joint venture, Bahrain Gasoline Blending, is a further area for expansion for us, allowing us to bring our experience and expertise to bear in a new market.

’’ Tirath MagdaniChief Executive, Greenergy Asia

International Fuels

46

Strategy In Action

2016 Greenergy Annual Report

We made our first diesel imports for domestic sale within Brazil, delivering competitive pricing in a market that has historically been closed to us.

Strategic priority 4 Increase domestic sales into Brazil

This period we imported diesel into Brazil for the first time, supplying fuel wholesalers through existing tankage at Santos in the centre south and new storage arrangements in Paranagua in the south.

The Brazilian diesel market has historically been supplied predominantly from domestic production, but this has failed to keep up with rising fuel demand. With domestic (regulated) diesel prices higher than international prices in the second half of this year, we were able to make our first in a series of diesel imports.

We plan to:

Middle East

» Develop new dedicated blending facilities within the joint venture to process a wider variety of petrol components

Brazil

» Explore opportunities to expand our fuel supply

» Expand our access to infrastructure in the long term.

Brazil

As an exporter of ethanol over ten years, we have developed long-standing relationships with storage companies in Brazil. Access to infrastructure, and therefore market entry, is difficult but we were able to leverage existing relationships to establish a diesel import operation in a short space of time.

We will consider opportunities to expand our position in Brazil, to meet the country’s growing requirements for fuel imports on a larger scale.

47

UK Fuels International Fuels Infrastructure Haulage

STRATEGIC ICONS

Navigator p52

Thames Oilport p50

‘‘We significantly extended our ownership of fuel infrastructure in the UK this year, taking a majority shareholding in Thames Oilport and, through Navigator, purchasing Vopak’s UK storage facilities. These transactions give us greater influence over infrastructure that is important to our future success.

We are now in a position to fund further infrastructure investment and acquisition, either directly as Greenergy or within Navigator, to support our continued growth.

’’ Chris BrookhouseInfrastructure Director

Aim: Acquire, regenerate and operate assets that support our supply chain objectives

Infrastructure

48

Strategy In Action

2016 Greenergy Annual Report48

Strategy In Action

Strategic priority 1 Regenerate legacy infrastructure to increase value

Thames Oilport

This period we purchased Vopak’s shares in Thames Oilport and Thames Enterprise Park, giving us two thirds of the joint venture with the remaining one third held by Shell. Chris Brookhouse, Director of Infrastructure at Greenergy, continues as Chief Executive of the joint venture.

With the new shareholder structure streamlining decision-making and reducing ongoing overhead costs, significant progress was made on site this period. In the first step to full commercial operations, an initial 175k cbm of tankage was engineered and commissioned this period and oil was received into Thames Oilport for the first time.

Thames Oilport p50

Navigator p52

Creation of an integrated infrastructure hub on Teesside

We continued work to integrate Navigator fuel facilities on Teesside.

Planning work was completed for a new diesel pipeline between the Navigator North Tees and Seal Sands facilities and work began on site shortly after year-end. North Tees has a deep-water jetty, allowing us to import diesel on large ships from the lowest-cost global producers. By linking with the Navigator Seal Sands facility, where we utilise sophisticated petrol blending facilities and supply ‘retail mix’ (petrol and diesel on the same road tanker), we aim to create economies of scale, reducing shipping-related costs and improving purchase margins.

49

Infrastructure

Connected to the UKOP pipeline, giving the potential to move fuel inland

to other areas of significant demand

Deep-water jetty able to receive

long-haul diesel ships and connect with the Middle Eastern, Asian

and US markets

Strategically important location

with a rapidly growing population, rising fuel demand and

limited suitable fuel infrastructure

The opening of Thames Oilport

50

Strategy In Action

2016 Greenergy Annual Report

Phase 2Road & pipeline

connections

Phase 3Blending

Phase 1Diesel

storage

KENT

ESSEX

LONDON

M25

M25

We have agreed a route-map to progress Thames Oilport in phases, to create a fully-fledged import terminal. The facility has now opened for diesel storage and we are moving on to road loading and storage for other products.

The ongoing development of Thames Oilport continues to be a priority for Greenergy.

51

Strategy In Action Infrastructure

Strategic priority 2 Increase income from rental of storage or sale of assets to third parties

Creation of Navigator Terminals to own and operate bulk storage facilities in the UK

We co-founded a new oil and chemical storage company called Navigator Terminals Ltd in partnership with Macquarie Capital. Navigator’s first two acquisitions were the purchase of:

» Vopak’s UK storage facilitiesat West Thurrock on the Thames,Seal Sands on Teesside andWindmill at Barry, near Cardiff

» The operational assetsof Greenergy North Tees,also in the UK.

These acquisitions give Navigator an initial storage capacity of more than 1.5m cbm, making it the UK’s largest independent storage provider in the oil and chemicals sectors and providing long-term investment income for Greenergy as a Navigator shareholder.

Sale of Greenergy North Tees to Navigator

The sale of Greenergy North Tees to Navigator generated significant value that is recognised in our exceptional profits for the year, reflecting the additional capability added to the facility since we acquired it in 2012 from the administrators of Petroplus:

» New petrol storage facilities

» Rail loading facilities to enableonward distribution of petrolto other UK locations by rail

» Pipeline links withadjacent terminals to createcost efficiencies

» Increased tank utilisation

» Jetty modifications creatinggreater operational flexibilityfor discharge of large ships.

Our third-party storage agreements for crude oil and kerosene transferred to Navigator Terminals from 8 April 2016 as part of the sale of the North Tees facility. We will benefit in the future from these and from third-party storage agreements at other Navigator facilities through our shareholding in Navigator.

52

Strategy In Action

2016 Greenergy Annual Report

Our participation in Navigator ensures our continued access to the infrastructure assets that currently underpin our UK supply position. It gives us greater flexibility at these facilities, ensuring we will be best placed to deliver low-cost and resilient fuel supply for our customers in the long-term.

As an infrastructure investment company, Navigator will also provide a vehicle to fund further infrastructure acquisitions supporting our continued growth in the fuels sector both in the UK and abroad.

Case Study

Creation of Navigator Terminals

53

Strategic priority 3 Operate fuel infrastructure to meet regional demand

Our participation in Navigator gives us a stake in fuel blending and storage facilities formerly owned and operated by Vopak, as well as a continuing interest in our North Tees facility. These facilities are located in areas of high fuel demand and where we have significant customer fuel supply commitments.

We also continued to operate our Plymouth facility safely and efficiently, in compliance with post-Buncefield environmental and safety standards.

We plan to:» Progress the development of Thames Oilport,

introducing road loading facilities and connectionsto the UKOP pipeline in the latter part of FY17

» Maximise our use of tankage at Thames Oilportfor diesel storage

» Further develop Navigator facilities to create costand operating efficiencies, including continuedintegration of Navigator North Tees and Seal Sands.

Infrastructure

Strategic priority 2 (continued)

Increase income from rental of storage or sale of assets to third parties

Create value from former refinery land at Thames Enterprise Park

At Thames Enterprise Park, the joint venture partners offered for sale former refinery land that is not required for the import terminal at Thames Oilport, to be used for industrial development. Discussions to sell the land at Thames Enterprise Park to a third-party stalled post year-end when the exclusive prospective buyer informed us that, due to the state of the debt markets

after the UK’s referendum on EU membership, they were unable to continue with the transaction on the terms offered. In light of these developments the joint venture has begun a process to identify alternative deal structures which will enable Thames Enterprise Park to realise a value through either sale or development of the land.

54

Strategy In Action

2016 Greenergy Annual Report

55

‘‘We have continued to expand our haulage capability within Greenergy Flexigrid to meet our growing supply requirements in the UK.

We have recruited more drivers in order to improve efficiency and built strong foundations for further growth.

’’

Aim: Make reliable and cost-efficient fuel deliveries to customers through our in-house haulage operation

Tim DavisonChief Executive, Greenergy Flexigrid

2016 Greenergy Annual Report56

Strategy In Action

Haulage

285

6.4bn

Number of drivers (year average)

Litres of fuel delivered

+9% FY15

+10% FY15

UK Fuels International Fuels Infrastructure Haulage

STRATEGIC ICONS

Strategic priority 1 Ensure a safe operation

We seek to ensure that drivers, vehicles and equipment are prepared for all foreseeable hazards.

Our resourcing of driver training increased this period in order to provide formal and informal training and assessment, over and above legal requirements. We began providing individual, data-based feedback to drivers on safer, more efficient driving styles.

All drivers are encouraged to report hazards, however small. The frequency of reporting in our in-house operation increased to 396 hazard observations per 100,000 hours worked (FY15: 338), reflecting a growing safety awareness amongst our drivers.

Strategic priority 3 Create an inclusive employee relations environment

We continue to focus on maintaining an active dialogue with our drivers, to ensure effective teamwork and shared goals. A quarter of the shares in Greenergy Flexigrid are held by a drivers’ trust on behalf of our drivers. The number of drivers benefiting from this trust increased significantly this year.

Strategic priority 2 Efficient use of resources

By increasing our in-house driver force to over 300 by year-end (year average: 285), we have been able to move more volume onto our own fleet than ever before, giving improved efficiency and profitability.

We improved the cost-efficiency of our operation by:

» Expanding our driver workforcein order to maximise the volumeof fuel delivered using ourin-house fleet

» Bringing a larger proportion of ourin-house fleet into 24/7 operation

» Working proactively and on a dailybasis to minimise the numberof vehicles that are off-road.

We plan to:» Make further improvements in fleet utilisation

» Improve communication with customerson truck arrival times

» Increase fleet availability through more effectivemanagement of service providers

» Review planning and scheduling platforms

» Improve the review process with third-party providers.

57

Key Performance Indicators

This year we achieved our best ever results as we converted opportunity into financial success.

58

Key Performance Indicators

2016 Greenergy Annual Report

Teesside biodiesel plant UK

15bn

18.1bn

15.6bn

KPI s sales volume

FY15

FY14

FY16

15.7bn

13.7bn

14.1bn

Financial KPI s turnover

FY15

FY14

FY16

6.8m

57.9m

3.8m

Financial KPI s pro�t before tax

FY15

FY14

FY16

23.5m

52.6m

30.3m

Financial KPI s EBITDA excluding exceptionals

FY15

FY14

FY16

Financial KPIs

Our sales volume grew 15% this year as a result of continued growth in our UK business as well as expansion in Canada and Brazil.

18.1bn

Sales volume in litres

Turnover decreased because of lower oil prices, whilst sales volumes increased. Market prices were lower overall this period, resulting in lower revenue per litre of fuel sold to customers.

Turnover

EBITDA grew due to increased sales volume, reduced supply chain costs as well as an improved contribution from our international businesses.

Profit before tax was affected by lower depreciation charges following asset sales, reduced interest costs in line with lower oil prices and exceptional income of £30.8m.

£52.6m £57.9m

EBITDA (pre-exceptionals) Profit before tax

£13.7bn

59

Invoice accuracyOn-time deliveries

97

95

98

96

100

May 15 Apr 16

99% Average99

Per

cent

age

97

95

98

96

100

99

May 15 Apr 16

Per

cent

age

99.57% Average

Service quality KPIs

We measure our operational efficiency through many KPIs. We publish three key KPIs that underpin our mission to be the fuel supplier with the lowest-cost, highest reliability and best systems and control.

99.0%

99.6%

On-time deliveries

Invoice accuracy

99.1% FY15

99.6% FY15

On-time deliveries

The complexity of our delivery operations increased further this year as we expanded our UK sales, including to the independent forecourt sector. We made 10% more customer deliveries in this period than in FY15 and delivered to 214 more sites. Despite this, the reliability of our operation remained high, with 99% of our deliveries made within the delivery window agreed with the customer.

Invoice accuracy

Our invoice accuracy is a measure of the quality of the information flow throughout our business.

In order to improve the efficiency and accuracy of our processes, we continue to automate our invoicing wherever possible. The proportion of invoices that were automatically generated this period was 93%, unchanged from last year.

60

Key Performance Indicators

2016 Greenergy Annual Report

22:27Average loading time Thames Terminal

14.41%

Number of trucks taking more than 30 minutes to load

26:14 FY15 27.42% FY15

We seek to minimise delays for trucks when collecting fuel from our terminals in order to improve our own, and our customers’ operational efficiency. Particular attention is paid to our busiest site at West Thurrock on the Thames estuary, where peak-time queuing has occurred in the past as a result of increased demand following the closure of the former Coryton refinery.

This period we completed a number of steps to improve operational flexibility at the facility, which have resulted in a significant reduction in waiting times for customers.

Case Study

Operational efficiency: Loading times

61

After an extended period of investment and expansion, we delivered a strong financial performance in all areas of the business this year. We benefited from our investments through cost optimisation and sales growth and improved margins.

62

Chief Financial Officer’s Review

2016 Greenergy Annual Report

Stephen McCaffreyChief Financial Officer

Chief Financial Officer’s Review

Realising investments

We have made significant investments over recent years to create cost efficiencies and prepare for expansion, both within the UK and internationally. We used our underlying infrastructure assets this year to source product from the lowest-cost global producers, resulting in improved margins and sales growth.

The establishment of Navigator Terminals will ensure our continued access to infrastructure that is strategically important to our UK business, allowing us to continue to source lowest-cost product and make petrol manufacturing margins. By selling our North Tees facility into Navigator Terminals, we realised a significant gain from our capital investments at this facility over the past three years. In addition, this will deliver us an annuity return from the investment we now hold in Navigator Terminals.

Biodiesel manufacturing margins were improved this year and production was up 75% following the purchase of our second biodiesel manufacturing facility in 2015. We have developed new cost savings and production efficiencies across both of our sites and made upgrades to improve supply chain flexibility and reduce raw material costs. All the biodiesel we blend into our fuel in the UK is waste-based and is now produced from our own facilities.

Our fuel supply business in Canada, which we established as a start-up in 2012, also performed well, with strong sales growth and diversification of our supply chain to minimise product costs and improve supply resilience for customers. Our Canadian business made a positive contribution to EBITDA for the first time this year.

Asset sales and an improved contribution from our overseas businesses complemented our strong underlying growth in the UK.

63

UK Fuels p36

Infrastructure p48

CFO reviewTurnover

FY120

16

10

FY13 FY14 FY15 FY16

Bill

ion

4

6

8

14

12

18

2

CFO reviewhistoric prices for diesel,

petroland brent

01.14200

300

1200

120

700

01.1507.14 07.15 01.16

400

500

600

800

900

1000

1100

20

30

50

40

60

70

80

90

100

110

140

130

Bre

nt

cru

de

futu

res

US

$ /

bar

rel

Die

sel /

pet

rol p

rice

US

$ /

to

nn

e

In a similar pattern to last year, turnover was down due to lower fuel retail prices. Sales volume has continued to grow, reaching 18.1bn litres this year.

This period we made our first infrastructure sale, delivering value from our investment over the last three years.

Chief Financial Officer’s Review (continued)

Performance

Our performance was strong in a low-price environment. Brent crude reached its ten year low of $27/barrel in January 2016 before recovering somewhat. With Rotterdam market prices for petrol and diesel following crude oil down, revenue per litre of fuel supplied was lower. Our business model is not affected by the underlying oil price, with margins remaining unaffected, but our turnover was down slightly due to falling prices and in spite of growing sales volume.

Profit before tax was £57.9m (FY15: £3.8m). This was driven by:

» Increased sales volume

» Improved margin drivenby economies of scale inour supply chain, particularlyin locations where we havemade infrastructure investments

» Operational and cost efficiencies,resulting in continued reductionin unit costs excluding acquisitionsto £6.67 per cbm of fuelsupplied (FY15: £6.79)

» Upgrades to our biodieselmanufacturing facilities resultingin lower raw material costs,improved reliability andincreased production

» Positive contributionsfor our Brazilian andNorth American businesses

» Exceptional incometotalling £30.8m.

EBITDA (pre-exceptionals) was £52.6m (FY15: 30.3m).

Exceptional items

We are reporting two exceptional items resulting from the creation of Navigator Terminals, which amounted to £30.8m.

Value from the sale of Greenergy North Tees to Navigator is reported as an exceptional non-cash item, reflecting the additional capability added to the facility since we acquired it in 2012 from the administrators of Petroplus.

As part of the finalisation of the Navigator transaction, we also reached agreement with the previous owners to rebate us for excess throughput charges which had impacted our earnings over the last three years.

Sales volume (litre)

Platts Petrol

Turnover (£)

Platts Diesel

Brent Crude

64

Chief Financial Officer’s Review

2016 Greenergy Annual Report

Financing our business

We continue to work closely with our banking group to ensure they have an effective understanding of our business and especially any significant activities or transactions that have taken place.

Our main working capital facility was extended this year with some important modifications to reflect the changing needs of the business. Given the reduction in oil prices we slimmed down the size of the facility from $1bn to $750m which still leaves us with a comfortable level of headroom to accommodate growth and unforeseen price fluctuations. We also reduced the number of syndicate banks to reflect the smaller size of the facility. The facility itself has continued to operate well and our banks continue to be supportive.

The Group’s total cash outflow from operations has been impacted during the year by two significant unusual adverse working capital movements. Firstly a £23m outflow arising from our decision to build a longer term stock position to take advantage of the contango in the market. And secondly the settlement of an unusually high 2015 year-end creditor balance which had arisen as a result of a change to the Group’s VAT registration. If the impact of these one-off items is eliminated then the adjusted cash outflow from operations for the year is £34m which is consistent with the normal working capital movements we expect to experience within the business.

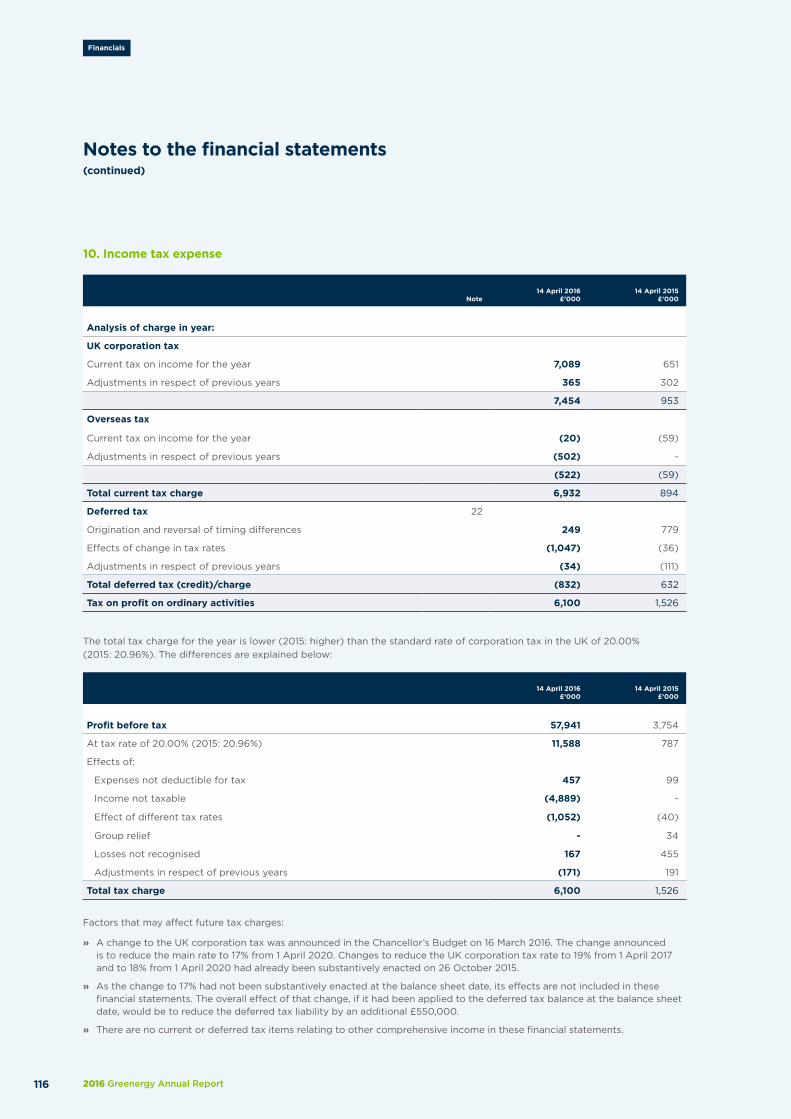

TaxationThe Group’s corporation tax charge for the year was £6.1m (FY15: £1.5m) representing an effective rate of 11% (FY15: 41%).

As noted above, current year results have been positively impacted by the profit realised on disposal of our North Tees terminal. Due to the nature of this transaction, the profit on disposal is deemed to be non-taxable. As a result, we are able to retain all of the profit within the Group, which improves our effective tax rate for the year.

Accounting and control environmentAs the business has continued to expand and evolve, the flexibility of our control environment has remained high on our agenda.

The sustained volatility in product prices during the year has continued to require rigorous application of hedging strategies. I am pleased to report that the falling fuel prices have once again had a minimal effect on our profits, which is testament to the robustness of our controls in this area.

Post balance sheet eventDuring the year, the joint venture partners at Thames Enterprise Park offered for sale former refinery land that is not required for the import terminal at Thames Oilport to be used for industrial development.

An agreement for sale was reached and the associated assets were classified as held for sale at year-end. Discussions to sell the land at Thames Enterprise Park to a third-party stalled post year-end when the exclusive prospective buyer informed us that due to the state of the debt markets after the UK’s referendum on EU membership, they were unable to continue with the transaction on the terms offered.

In light of these developments the joint venture has begun a process to identify alternative deal structures which will enable Thames Enterprise Park to realise a value which exceeds the asset carrying value through either sale or development of the land. This process will ultimately lead to a determination during FY17 of whether the classification as held for sale and the asset carrying values remain appropriate. These developments are considered a non-adjusting post balance sheet event and therefore any accounting implications will be recognised in the financial statements of future periods.

Earnings per share