annual report 2016 - patrimony1873.com report 2016. patrimony 1873 | 3 johannes blaeu (23 september...

TRANSCRIPT

ANCIENT ROOTS FOR NEW HORIZONS

Annual Report 2016

patrimony 1873 | 3

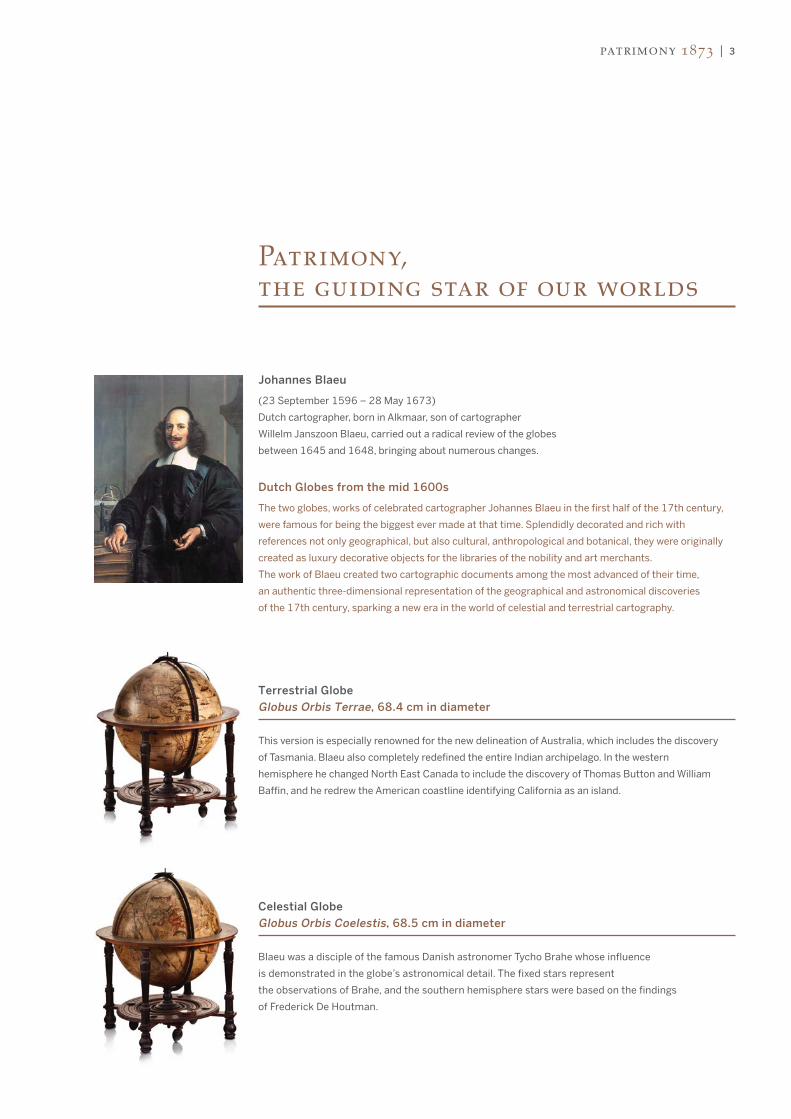

Johannes Blaeu

(23 September 1596 – 28 May 1673)

Dutch cartographer, born in Alkmaar, son of cartographer

Willelm Janszoon Blaeu, carried out a radical review of the globes

between 1645 and 1648, bringing about numerous changes.

Dutch Globes from the mid 1600s

The two globes, works of celebrated cartographer Johannes Blaeu in the first half of the 17th century,

were famous for being the biggest ever made at that time. Splendidly decorated and rich with

references not only geographical, but also cultural, anthropological and botanical, they were originally

created as luxury decorative objects for the libraries of the nobility and art merchants.

The work of Blaeu created two cartographic documents among the most advanced of their time,

an authentic three-dimensional representation of the geographical and astronomical discoveries

of the 17th century, sparking a new era in the world of celestial and terrestrial cartography.

Terrestrial GlobeGlobus Orbis Terrae, 68.4 cm in diameter

This version is especially renowned for the new delineation of Australia, which includes the discovery

of Tasmania. Blaeu also completely redefined the entire Indian archipelago. In the western

hemisphere he changed North East Canada to include the discovery of Thomas Button and William

Baffin, and he redrew the American coastline identifying California as an island.

Celestial GlobeGlobus Orbis Coelestis, 68.5 cm in diameter

Blaeu was a disciple of the famous Danish astronomer Tycho Brahe whose influence

is demonstrated in the globe’s astronomical detail. The fixed stars represent

the observations of Brahe, and the southern hemisphere stars were based on the findings

of Frederick De Houtman.

Patrimony, the guiding star of our worlds

patrimony 1873 | 5

TRADITION, DEDICATION, PROTECTION 7

PATRIMONY 1873 8

MANAGEMENT REPORT 2016 11

PATRIMONY 1873 ACCOUNTS 2016 15

BALANCE SHEET AS OF 31ST DECEMBER 2016 16

PROFIT AND LOSS STATEMENT 2016 17

PRESENTATION OF THE STATEMENT OF CHANGES IN EQUITY 18

NOTES TO THE PATRIMONY 1873 ACCOUNTS 19

1. Commentaries regarding the business activities 19

2. Accounting and valuation principles 19

3. Risk control and management 21

4. Information on the balance sheet 23

REPORT OF THE STATUTORY AUDITOR ON THE FINANCIAL STATEMENT 30

Contents

patrimony 1873 | 7

TRADITION, DEDICATION, PROTECTION

Patrimony 1873 is the response of the EFG Group to the changing needs of discerning

clients, with regard to the macro-economic and international regulatory environment in

constant evolution.

Patrimony 1873 is an independent wealth management Company, 100% owned by

BSI SA Lugano whose ultimate shareholder is EFG International AG, which represents its

Swiss tradition, its equidistance in respect to the world of banking and subsequent free-

dom of judgment, its dedication to clients and the precise knowledge of their values, as its

success factors.

Patrimony 1873 offers its clients a wide and specialized range of services aimed at the

protection and coordinated management of assets analyzed as a whole.

Patrimony 1873 received July 23rd, 2012 FINMA authorization to act in the capacity of

Securities Dealer.

Dear readers,

2016 was a very demanding year in many ways, yet we can claim we have been able to successfully

face the obstacles encountered on our journey.

With the acquisition of BSI Group by EFG International, successfully completed in October, Patrimony 1873

too has entered a new era.

Following the change in ownership of our controlling Company, at the end of 2016 changes occurred

at the top management of Patrimony 1873. A new board of directors has been appointed, with

the addition of three members of EFG International Group: Joachim H. Straehle, appointed Chairman,

Peter Fischer and Adrian Kyriazi appointed members. Moreover, Agostino Ferrazzini, former CEO

of Patrimony, has been appointed Deputy Chairman. Ermanno Gajo and Pierangelo Merati, former

members of the Board of Directors from 2013, have been confirmed in their roles. An important change

has also taken place in the Executive Committee with the appointment of Paolo Filippini, former CFO

of the Company, as new CEO.

We believe the strong commitment of EFG International, along with these changes, will lay the foundations

for a further development of Patrimony 1873 as independent wealth management Company.

A heartfelt thank you to the members of the outgoing Board of Directors who, in just four years and

with the Executive Committee, have succeeded in making Patrimony 1873 an important and recognized

reality of Ticino and the Swiss financial sector.

We now intend to ensure the continuity of the excellent work performed so far and to substantially

contribute to the growth of Patrimony 1873. The challenges ahead of us are many, but many are also

the opportunities and we are confident we will be able to respond to current and future customer

needs in the best possible way.

This year we also extend our heartfelt thankyou to all our customers for the trust they have

placed in us, customers to whom we renew our commitment towards professionalism and excellence.

We also wish to take this opportunity to thank our partners and all our employees.

J.H. Straehle P. Filippini

Chairman CEO

Patrimony 1873

patrimony 1873 | 9

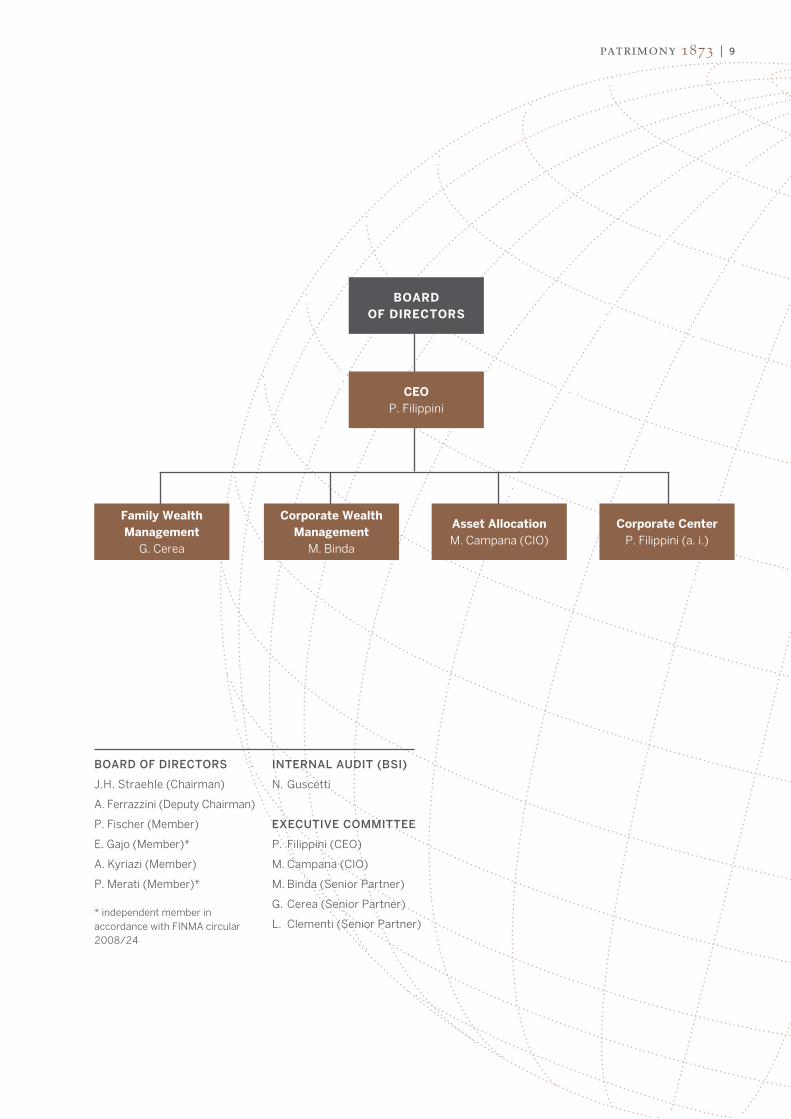

BOARD OF DIRECTORS

J.H. Straehle (Chairman)

A. Ferrazzini (Deputy Chairman)

P. Fischer (Member)

E. Gajo (Member)*

A. Kyriazi (Member)

P. Merati (Member)*

* independent member in accordance with FINMA circular 2008/24

INTERNAL AUDIT (BSI)

N. Guscetti

EXECUTIVE COMMITTEE

P. Filippini (CEO)

M. Campana (CIO)

M. Binda (Senior Partner)

G. Cerea (Senior Partner)

L. Clementi (Senior Partner)

Corporate Wealth Management

M. Binda

Family Wealth Management

G. Cerea

Asset AllocationM. Campana (CIO)

Corporate CenterP. Filippini (a. i.)

CEOP. Filippini

BOARD OF DIRECTORS

patrimony 1873 | 11

Management Report 2016

MACRO ECONOMIC BACKGROUND AND FINANCIAL MARKET

2016 was marked by a nervous start, as the Federal Re-serve had just raised interest rates in December 2015 and was preparing to raise them further in 2016, revers-ing the monetary policy despite fears of a global reces-sion. However, these expectations were disregarded and Fed has only raised rates once in December. The second part of the year saw three events which have surprised the world. First, the United Kingdom voted its exit from the European Union in a referendum. Secondly, Donald Trump was elected as President of the United States with a very expansionary economic program, based on investments on infrastructures and tax cuts to be financed by increasing the deficit, and which will lead to a higher growth in aggregate demand and an increased inflation. Finally, the agreement be-tween OPEC countries on oil production cut. After two years of overproduction and low prices, the agreement has in fact pushed the price of oil to its highest levels in over a year.Meanwhile, geopolitical tensions heightened with the launch of a huge offensive against Isis. This resulted in a large flow of migrants towards Europe in search of humanitarian protection, a fact that has encouraged the growth of populist parties across Europe and makes the political situation of major European coun-tries uncertain, a few months away from important elec-tions.

With regards to the equity markets, 2016 got off to a bad start, with stock markets dragged down by fears of a global recession. They then reversed course follow-ing the prudent attitude of the Fed and the ultra-expan-sionary behaviour of the ECB. Despite a few shocks, the markets ended the year in positive territory, al-though performance was mixed across the world. Some emerging markets played the leading role, fol-lowed by the Anglo-Saxon ones, primarily the United States, while in continental Europe, Germany and France went well, Italy and Spain less well. Switzerland ended the year negatively, held back by the disappoint-ing performance of pharmaceutical and banking stocks.

As for the bond market, performance was moderately positive in 2016. Central banks’ interventionist policies in developed countries and the renewed confidence in emerging markets have supported all fixed income segments. The macroeconomic outlook changed in the latter part of the year and this had strong implications on the bond market. The best prospects of inflation and the newly found sustainability in growth led to a less ex-pansionary monetary policy, resulting in a sharp rise in yields on all maturities and markets.

On the currency markets, 2016 saw increased volatil-ity and just a few recognizable trends. One of these was the rise of the US dollar against developed countries’ currencies and, most importantly, against those of emerg-ing countries.The Swiss Franc remains strong and could remain so for several quarters as a results of high political uncer-tainty in Europe. Looking at 2017, the macroeconomic and geopolitical picture remains extremely controversial. The global eco-nomic recovery, with growth estimated at +3,3% for 2017, remains below the average long term values, de-spite the cost of money and energy are still historically very low. The recovery of commodities and the price of money at its absolute minimum have increasingly fa-voured developing countries more than advanced coun-tries, in contrast to what was expected at the beginning of the year.As said, the recovery of the raw materials listing, oil first and foremost, as well as the rising cost of labour in the United States and in some important emerging countries are a clear sign that the long period of deflation is nearing its conclusion.

ACTIVITY REPORT

2016 was a year of major changes. Events that reached our shareholder, in particular the communications of FINMA, the Swiss Financial Market Supervisory Au-thority, had an impact also on the development pro-jects of Patrimony 1873. Nevertheless, our Company’s open-architecture model proved once again to be ef-fective and allowed us to successfully overcome the many challenges we faced, as well as to provide our customers with quality products and services. The arrival of EFG International, the new owner of the BSI Group, allowed Patrimony 1873 to revamp its strategy, strengthening internal expertise and reassuring custom-ers and employees and we believe that, thanks to the adopted measures, 2017 will be a year of activity revival to the benefit of our customers and staff.

patrimony 1873 | 13

FINANCIAL DATA

The financial results of Patrimony 1873 for 2016 are pos-itive. The Company has a license as securities dealer and thus the main activity remains asset management. At year-end, Patrimony 1873 Assets under Management (AuM) amounted to CHF 5.9 billion (2015: CHF 6.5 billion). This reduction is due to the combination of various negative factors coupled with the appreciation of the Swiss Franc over major currencies. As at 31.12.2016, total revenues amounted to CHF 28.5 million (2015: 33.8 million) and the main item is represented by commission and servic-es. Operating expenses amount to CHF 19.6 million (2015: 19.3 million) stable in respect to the previous year. Operating result thus amounted to CHF 6.5 mil-lion (2015: CHF 14.7 million), while net profit amounted to CHF 7.1 million (2015: CHF 12.1 million).As at 31.12.2016, total assets amounted to CHF 81.5 million (2015: CHF 101.4 million). At the end of the year under review, the Company had equity before appropria-tion of profit of CHF 32.1 million (2015: 35.1 million) and a Total Capital Ratio of 42,2% (2015: 40.8%), which shows that despite a difficult 2016 due to external events, the Company has strengthened its financial solidity.

Lugano, 11th April 2017

For the Board For the ExecutiveOf Directors Committee

J.H. Straehle (Chairman) P. Filippini (CEO)

M. Campana (CIO) M. Binda (Senior Partner) G. Cerea (Senior Partner) L. Clementi (Senior Partner)

patrimony 1873 | 15

Accounts 2016

BALANCE SHEET AS OF 31ST DECEMBER 2016

in SFR 1’000Note 31.12.2016 31.12.2015 Variation in %

Assets

Liquid assets 4’481 8’846 -49%

Amounts due from banks 4.9 76’656 92’300 -17%

Amounts due from customers 4.1 / 4.9 63 1 6’200%

Accrued income and prepaid expenses 84 124 -32%

Tangible fixed assets 4.2 48 - 100%

Other assets 4.3 172 107 61%

Total assets 81’504 101’378 -20%

Total subordinated claims - - -

of which subject to mandatory conversion and/or debt waiver - - -

Liabilities

Amounts due to banks 4.9 27’694 25’077 10%

Amounts due in respect of customer deposits 16’125 34’556 -53%

Accrued expenses and deferred income 5’242 6’465 -19%

Other liabilities 4.3 303 217 -40%

Provisions - - -

Reserves for general banking risks 4.6 1’540 1’540 0%

Company capital 4.7 5’000 5’000 0%

Statutory retained earnings reserve 2’500 2’297 9%

Profit carried forward 16’023 14’137 13%

Profit 7’077 12’089 -41%

Total liabilities 81’504 101’378 -20%

Total subordinated liabilities - - -

of which, subject to mandatory conversion and/or debt waiver - - -

Off-balance sheet transactions

Irrevocable commitments 4.1 46 52 -12%

patrimony 1873 | 17

PROFIT AND LOSS STATEMENT AS OF 31ST DECEMBER 2016

in SFR 1’000Note 2016 2015 Variation in %

Result from interest operations

Interest and discount income 33 38 -13%

Interest expense -11 -6 83%

Gross result from interest operations 22 32 -31%

Changes in value adjustments for default risks and losses from interest operations - -

Subtotal net result from interest operations 22 32 -31%

Result from commission business and services

Commission income from securities trading and investment activities 11’573 10’262 13%

Commission income from other services 14’895 24’459 -39%

Commission expense -418 -666 37%

Subtotal result from commission business and services 26’050 34’055 -23%

Result from trading activities and the fair value option 6.1 61 27 126%

Other result from ordinary activities

Other ordinary income - 2 100%

Other ordinary expenses -31 -118 74%

Subtotal other result from ordinary activities -31 -116 73%

Net operating result 26’102 33’998 -23%

Operating expenses

Personnel expenses 6.2 -14’396 -13’679 5%

General and administrative expenses 6.3 -5’169 -5’572 -7%

Subtotal operating expenses -19’565 -19’251 2%

Value adjustments on participations and depreciation and amortisation of tangible fixed assets and intangible assets 4.2 -5 - 100%

Changes to provisions and other value adjustments, and losses -16 -13 23%

Operating result 6’516 14’734 -56%

Extraordinary income 6.4 2’439 161 1’415%

Taxes 6.5 -1’878 -2’806 -33%

Profit/loss (result of the period) 7’077 12’089 -41%

Appropriation of profit

Profit 7’077 12’089 -41%

Profit carried forward 16’023 14’137 13%

Balance sheet profit 23’100 26’226 -12%

Proposal of the Board of Directors

Ordinary dividend on share capital 7’000 10’000 -

Allocation to general legal reserve - 203 -67%

Balance to be carried forward 16’100 16’023 13%

Total 23’100 26’226 78%

PRESENTATION OF THE STATEMENT OF CHANGES IN EQUITY

in SFR 1’000

Companycapital

Capitalreserve

Statutory retainedearnings

reserve

Reserves for general

bankingrisks

Voluntaryretained earningsreserves

and profit/loss carried

forward

Own shares(negative

item)

Result of the

period Total

Equity at start of current period 5’000 - 2’297 1’540 14’137 - 12’089 35’063

Appropriation of profit 2015 - - - - - - - -

– Assigment to statutory retained earnings reserve - - 203 - - - -203 -

– Retained earnings - - - - 1’886 - -1’886 -

– Dividend - - - - - - -10’000 -10’000

Profit / loss (result of the period) - - - - - - 7’077 7’077

Equity at end of current period 5’000 - 2’500 1’540 16’023 - 7’077 32’140

patrimony 1873 | 19

NOTES TO THE PATRIMONY 1873 SA ACCOUNTS

The following notes are referred to the situation as at 31st December 2016.

1. COMMENTARIES REGARDING THE BUSINESS ACTIVITIES

GENERAL INFORMATIONPatrimony 1873 SA, Lugano (hereinafter “The Company”), is 100% owned by BSI SA, Lugano, whose ultimate share-holder is EFG International AG, Zurich (EFG). EFG is a private banking group offering private banking and asset management services. It operates in around 40 locations worldwide, with about 3’500 employees. Its registered shares (Symbol: EFGN) are listed on the SIX Swiss Exchange. At the end of 2016, the staff of the Company converted to full-time equivalent (FTEs), is 45.9 (2015: 50.0). The Com-pany does not have participations.

MAIN ACTIVITIES The Company offers its services to discerning and so-phisticated, private and institutional clients both domes-tic and international, in compliance with the regulatory framework of the destination countries. As a wealth man-agement Company of the EFG Group, Patrimony 1873 SA offers a wide range of services for the protection, global management and risk management of complex and diverse assets at an international level. Moreover, as an independent centre of expertise, Patrimony 1873 SA can receive client mandates to achieve specific objec-tives, by identifying, selecting, and coordinating profes-sional service providers.

BALANCE SHEET TRANSACTIONSBalance sheet transactions have a marginal role. However, the results from operating commissions and services greatly contribute to the operating incomes of the Compa-ny. Bank deposits are made only at leading Swiss institu-tions or OECD countries.

OUTSOURCINGPatrimony 1873 outsources to BSI SA the internal audit, development and maintenance of its IT environment, back office activities and accounting. The Company com-plies with the legal provisions on outsourcing contained in FINMA circular 08/7.

VALUE ADDED TAX (VAT) Patrimony 1873 belongs to the VAT group of BSI SA and is thus jointly and severally liable for commitments aris-ing from this tax.

2. ACCOUNTING AND VALUATION POLICIES

GENERAL PRINCIPLESThe accounting, balance sheet entry and valuation criteria conform to the provisions of the Swiss Code of Obligations, the Swiss Banking Law and the Directives of the Swiss Fi-nancial Market Supervisory Authority FINMA.

RECORDING OF TRANSACTIONSAll transactions are recorded in the books of the Company on the execution date.

INDIVIDUAL ASSESSMENTThe assets and liabilities as well as off-balance operations are individually evaluated.

CONVERSION OF CURRENCYForeign currency transactions are recorded at the exchange rate of the trade date, and revaluations are recorded into the profit and loss account. Foreign currency denominated bal-ance sheet items are converted into Swiss francs at the rate of the balance sheet closing date. Conversion differences are booked directly within the Company shareholders’ equity.

Exchange rates used for the main currencies:

31.12.2016 31.12.2015 AVG 2016 AVG 2015

USD/CHF 1.019 0.995 0.989 0.964

EUR/CHF 1.074 1.084 1.091 1.064

JPY/CHF (100) 0.870 0.827 0.908 0.797

GBP/CHF 1.254 1.476 1.330 1.470

CASH AND OTHER LIQUID ASSETS, MONEY MARKET PAPERS, DUE FROM BANKS AND LIABILITIESThese items are recorded in the balance sheet at the nom-inal value or purchase cost. Any discounts are recorded in the appropriate liabilities items.

DUE FROM CUSTOMERSLoans to customers are recorded in the balance sheet at their nominal value, less any value adjustment for uncer-tain debts.

ACCRUALS AND DEFERRALSInterest income, interest expenses and all other income and expenses not settled during the accounting period are ac-crued or prepaid in order to match the correct profit and loss period.

FIXED ASSETSFixed asset acquisitions are capitalized and valued at their purchase price if their intended use is for more than one accounting period and their purchase price exceeds a min-imum of CHF 5’000. Thereafter, fixed assets are recorded at their purchase price less accumulated depreciation. De-preciation is calculated on the basis of the asset’s expect-ed useful life.

PENSION PLANSThe accounting complies with Swiss GAAP AAR 16 re-lating to the presentation of accounts. Further details are provided in point 4.4 in the notes to the Company account.

TAXESTaxes relating to the current accounting period are esti-mated in accordance with local tax legislation and record-ed as costs for the period to which they relate. Direct taxes on current year profits payable, but not yet paid, are re-corded as “accrued expenses”. The accounting is in com-pliance with ARR 11 relating to the presentation of ac-counts. The reserve for general banking risks is taxed and the consequent tax expense is reported as “Accrued ex-pense and deferred income”.

VALUE ADJUSTMENTS AND PROVISIONSSpecific provisions and value adjustments are made with respect to all identified risks in accordance with the prin-ciple of prudence. The value of such items is deducted from the balance sheet assets to which they relate. Value adjustments and provisions proving to be financially un-necessary during the financial year are released and

credited to the profit and loss statement. Provisions for latent risk or other risks are booked as liabilities in the balance sheet under “Value adjustment and provisions”.

RESERVES FOR GENERAL BANKING RISKSThis item was created in accordance with FINMA direc-tives on the presentation of accounts. Movements in the reserves for general banking risks are posted to “Changes in reserves for general banking risks”.

CONTINGENT LIABILITIES, IRREVOCABLE COMMITMENTS, CONTINGENT LIABILITIES FOR CALLS AND MARGIN LIABILITIESOff-balance sheet items are stated at nominal value. Any provisions for identified risks are included under “Value adjustments and provisions”. Following the application of the banking agreement on deposit guarantees, an irrevo-cable commitment of CHF 46’000 was booked as commu-nicated by the Supervisory Authority.

CLIENT ASSETSThe value of clients’ assets under management is calculat-ed with reference to the total value of all client positions at year-end. Assets managed by the Company but deposited at third party banks are also included.

MATERIAL EVENTS AFTER THE BALANCE SHEET DATEAfter the balance sheet date, no event took place that would lead to a correction of the financial statements.EFG International SA, in the context of the Group re-structuring, has bought from BSI SA the participation in Patrimony 1873, SA with effective date 22 of March 2017.

3. RISK CONTROL AND MANAGEMENT

PRINCIPLESRisk management is an integral part of the business poli-cy of the Company. In compliance with applicable laws and regulatory requirements, the Company has estab-lished a structure of risk control and management.

STRUCTURE AND RESPONSIBILITIES The Company has a risk management and internal con-trols structure appropriate to the size and complexity of the business activities. These include processes and con-trols that ensure the delegation of powers and the sepa-ration of critical functions.

patrimony 1873 | 21

• The Board of Directors monitors whether the Company has a clear process of global risk management, ap-proves risk policies and limits, and is informed quarter-ly in writing about all risk situations of the Company.

• The Executive Committee is responsible for imple-menting the risk management process throughout the entire organization by defining the principles, risk strat-egies and policies, global limits and authorities ap-proved by the Board of Directors.

• Risk Management and Internal Control Units conduct various independent controls, intervening directly in cases of non-compliance with limits, and reports regu-larly to the Executive Committee on the risk status. The Internal Control Unit provides and monitors data related to commercial performances, and reports regularly to the Executive Committee. The Risk Management Unit analyzes and consolidates the data and the risk informa-tion at a Company level and produces a quarterly “Glob-al Risks Report” for the Executive Committee and Board of Directors. Finally, the Risk Management and Internal Control Units assume the second-level controls activi-ties for the Family Wealth Management, Asset Alloca-tion and Corporate Wealth Management.

• Legal & Compliance is responsible for the manage-ment of the legal and reputational risks, and for ensur-ing that the Company complies with regulatory and le-gal requirements.

• Client Compliance is the unit in charge for the fight against money laundering and terrorism financing. In this area of interest is in charge of managing reputational risk, compliance with legal regulations and compliance with the standard and market conduct rules.

CREDIT RISKS Credit risk is the risk that a counterparty’s creditworthiness deteriorates and the counterparty becomes insolvent or does not pay back its liabilities. Credit risk also includes oth-er risk categories such as counterparty risk, delivery risk, concentration risk and country risk. The Company has set out various internal and Group policies that define risk gov-ernance principles, the method of calculation and risk limi-tation. The Company measures the credit risk and, through a system of limits, defines the maximum risk exposure to groups of counterparties and monitors compliance with regulatory requirements related to large exposures. The Risk Management unit carries out the independent con-trols. The Company does not currently provide lending ac-tivities to customers and does not own a property portfolio.

MARKET RISKS Market risk is the risk of losses arising from unexpected changes in interest rates, exchange rates, share prices, the prices of precious metals and commodities, as well as the corresponding expected volatility.

The Company carries out trading operations for the clients using all financial products and their derivatives. The Com-pany has established an Asset Allocation Committee which is responsible for investment decisions with particular at-tention to the portfolio structure, the selection of instru-ments as well as the risk-return of different risk profiles.

OPERATIONAL RISKS Operational risk is the risk of loss resulting by the inadequa-cy or failure of processes, people and systems or from exter-nal events. Operational risks also include compliance risks, legal risks and reputational risks. The operational risk man-agement of the Company is under the responsibility of the Risk Management and Internal Controls units, and is mainly based on the collection and analysis of centralized operating losses, on the identification and analysis of the inherent risks in the processes and the management of corrective meas-ures. The Company creates provisions for events that could generate a financial loss. The use and monitoring of some risk indicators selected by the Risk Management and Inter-nal Controls allow advanced assessment of any increase in the level of the risk within the Company.

CONTROL LEVEL STRUCTURE The Company’s risk mitigation controls have a three level structure. • First level controls are performed by the line and are

basic for carrying out operational activities. The pur-pose is to ensure correct execution.

• Second level controls monitor and ensure that activities are correctly carried out by the operational units. These controls are carried out by the Risk Management, Internal Control and Legal & Compliance units which are inde-pendent from the monitored unit.

• Third level controls are conducted to verify the correct implementation and the effectiveness of the first level and second level controls. They are carried out by the Group Internal Audit unit.

4. INFORMATION ON THE BALANCE SHEET

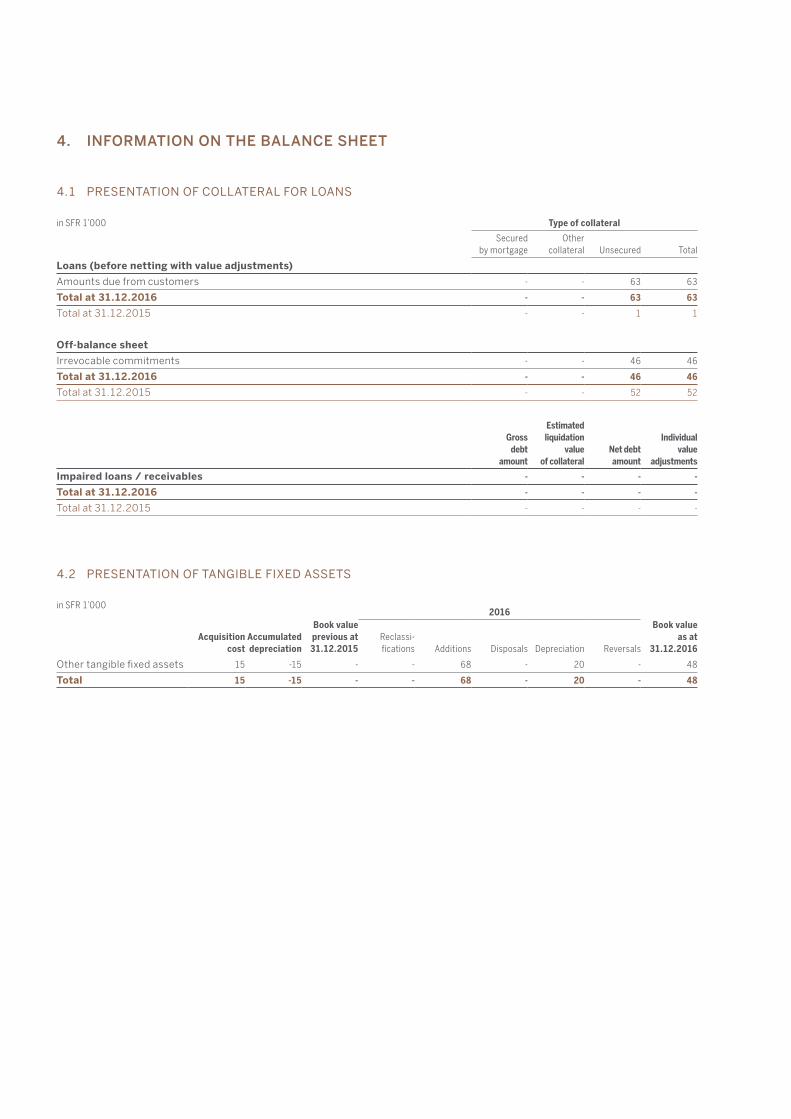

4.1 PRESENTATION OF COLLATERAL FOR LOANS

in SFR 1’000 Type of collateral

Secured by mortgage

Other collateral Unsecured Total

Loans (before netting with value adjustments)

Amounts due from customers - - 63 63

Total at 31.12.2016 - - 63 63

Total at 31.12.2015 - - 1 1

Off-balance sheet

Irrevocable commitments - - 46 46

Total at 31.12.2016 - - 46 46

Total at 31.12.2015 - - 52 52

Grossdebt

amount

Estimated liquidation

valueof collateral

Net debt amount

Individual value

adjustments

Impaired loans / receivables - - - -

Total at 31.12.2016 - - - -

Total at 31.12.2015 - - - -

4.2 PRESENTATION OF TANGIBLE FIXED ASSETS

in SFR 1’000

Acquisitioncost

Accumulateddepreciation

Book value previous at 31.12.2015

2016Book value

as at 31.12.2016

Reclassi-fications Additions Disposals Depreciation Reversals

Other tangible fixed assets 15 -15 - - 68 - 20 - 48

Total 15 -15 - - 68 - 20 - 48

patrimony 1873 | 23

4.3 BREAKDOWN OF OTHER ASSETS AND OTHER LIABILITIES

in SFR 1’000 Other assets Other liabilities

31.12.2016 31.12.2015 31.12.2016 31.12.2015

Compensation account - - - -

Deferred income taxes recognised as assets - - - -

Amount recognised as assets in respect of employer contribution reserves - - - -

Amount recognised as assets relating to other assets from pension schemes - - - -

Negative goodwill - - - -

Tax asset/liability 71 83 130 139

Other 101 24 173 78

Total 172 107 303 217

4.4 DISCLOSURE OF LIABILITIES RELATING TO OWN PENSION SCHEMES, AND NUMBER AND NATURE OF EQUITY INSTRUMENTS OF THE COMPANY HELD BY OWN PENSION SCHEMES

in SFR 1’00031.12.2016 31.12.2015

Commitment to Pension Institution

Commitment to Pension Institution - -

Disclosures on the economic situation of own pension schemes

The “Fondazione di previdenza di BSI SA” (Foundation) provides

pension insurance to all employees of Patrimony, with the ex-

ception of interns, trainees, volunteers and collaborators with

fixed-term contract exceeding three months or an advisory

mandate. Employees with a fixed-term employment contract

exceeding three months or a temporary or permanent advisory

mandate have occupational pension insurance with a primary

pension institution.

The Foundation, which guarantees occupational pension contri-

butions in compliance with the Swiss Federal Law on Occupa-

tional Retirement, Survivors and Disability Pension Plans (LPP)

and its ordinances, is based on a defined-contribution system,

according to which the old-age pension is calculated by applying

the conversion rate to the individual savings accumulated until

retirement.

On the contrary, contributions for disability and death are deter-

mined based on the last salary paid before the occurrence of the

insured event.

The “Fondo complementare di previdenza BSI SA” (Fund) con-

sists of a defined-contribution supplementary plan. The Fund in-

sures employees already covered by the Foundation, whose annu-

al insured salary is above four times the maximum AVS retirement

pension or whose entry benefit generated a purchase surplus.

The statutory retirement age is set at 64 for both the Founda-

tion and the Fund.

As at 31.12.2016, the responsible actuary determined the pen-

sion funds and actuarial provisions applying the technical rate of

2.5% and the 2015 LPP generational technical bases year 2017.

On the basis of these actuarial estimates, coverage at

31.12.2016 stands at 100.9% (unaudited) for the Foundation

(31.12.2015: 101%, technical rate 2.75%, 2010 LPP genera-

tional tables year 2016) and 102.3% (unaudited) for the Fund

(31.12.2015: 104.8%, technical rate 2.75%, 2010 LPP genera-

tional tables year 2016).

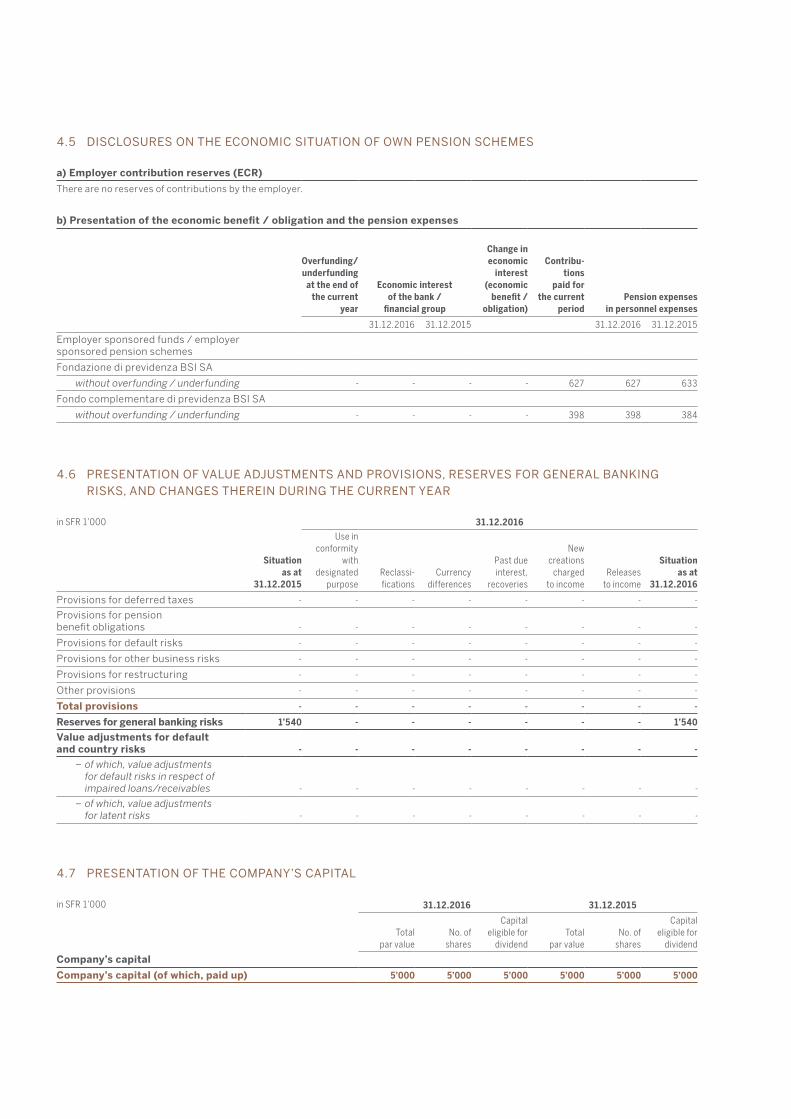

4.5 DISCLOSURES ON THE ECONOMIC SITUATION OF OWN PENSION SCHEMES

a) Employer contribution reserves (ECR)

There are no reserves of contributions by the employer.

b) Presentation of the economic benefit / obligation and the pension expenses

Overfunding/ underfunding

at the end of the current

year

Economic interest of the bank /

financial group

Change in economic

interest (economic

benefit / obligation)

Contribu-tions

paid for the current

periodPension expenses

in personnel expenses

31.12.2016 31.12.2015 31.12.2016 31.12.2015

Employer sponsored funds / employer sponsored pension schemes

Fondazione di previdenza BSI SA

without overfunding / underfunding - - - - 627 627 633

Fondo complementare di previdenza BSI SA

without overfunding / underfunding - - - - 398 398 384

4.6 PRESENTATION OF VALUE ADJUSTMENTS AND PROVISIONS, RESERVES FOR GENERAL BANKING RISKS, AND CHANGES THEREIN DURING THE CURRENT YEAR

in SFR 1’000 31.12.2016

Situation as at

31.12.2015

Use in conformity

with designated

purposeReclassi-fications

Currency differences

Past due interest,

recoveries

New creations

charged to income

Releases to income

Situation as at

31.12.2016

Provisions for deferred taxes - - - - - - - -

Provisions for pension benefit obligations - - - - - - - -

Provisions for default risks - - - - - - - -

Provisions for other business risks - - - - - - - -

Provisions for restructuring - - - - - - - -

Other provisions - - - - - - - -

Total provisions - - - - - - - -

Reserves for general banking risks 1’540 - - - - - - 1’540

Value adjustments for default and country risks - - - - - - - -

– of which, value adjustments for default risks in respect of impaired loans/receivables - - - - - - - -

– of which, value adjustments for latent risks - - - - - - - -

4.7 PRESENTATION OF THE COMPANY’S CAPITAL

in SFR 1’000 31.12.2016 31.12.2015

Total par value

No. of shares

Capitaleligible for

dividendTotal

par valueNo. of

shares

Capitaleligible for

dividend

Company’s capital

Company’s capital (of which, paid up) 5’000 5’000 5’000 5’000 5’000 5’000

patrimony 1873 | 25

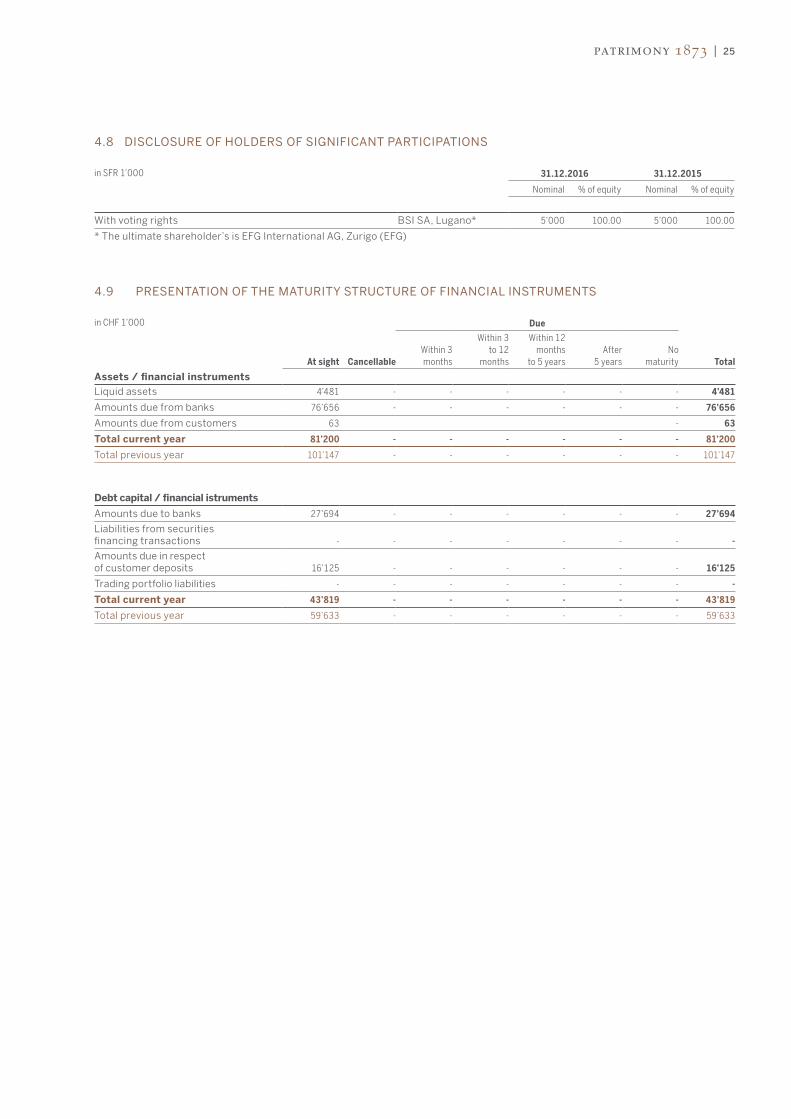

4.8 DISCLOSURE OF HOLDERS OF SIGNIFICANT PARTICIPATIONS

in SFR 1’000 31.12.2016 31.12.2015

Nominal % of equity Nominal % of equity

With voting rights BSI SA, Lugano* 5’000 100.00 5’000 100.00

* The ultimate shareholder’s is EFG International AG, Zurigo (EFG)

4.9 PRESENTATION OF THE MATURITY STRUCTURE OF FINANCIAL INSTRUMENTS

in CHF 1’000

At sight Cancellable

Due

TotalWithin 3 months

Within 3 to 12

months

Within 12 months

to 5 yearsAfter

5 yearsNo

maturity

Assets / financial instruments Liquid assets 4’481 - - - - - - 4’481

Amounts due from banks 76’656 - - - - - - 76’656

Amounts due from customers 63 - 63

Total current year 81’200 - - - - - - 81’200

Total previous year 101’147 - - - - - - 101’147

Debt capital / financial istruments

Amounts due to banks 27’694 - - - - - - 27’694

Liabilities from securities financing transactions - - - - - - - -

Amounts due in respect of customer deposits 16’125 - - - - - - 16’125

Trading portfolio liabilities - - - - - - - -

Total current year 43’819 - - - - - - 43’819

Total previous year 59’633 - - - - - - 59’633

4.10 PRESENTATION OF ASSETS AND LIABILITIES BROKEN DOWN BY THE MOST SIGNIFICANT CURRENCIES FOR THE COMPANY

CHF USD EUR GBP Other Total

Assets

Liquid assets 4’225 7 245 4 - 4’481

Amounts due from banks 38’691 1’840 35’659 73 393 76’656

Amounts due from customers 13 - 50 - - 63

Financial investments 84 - - - - 84

Tangible fixed assets 48 - - - - 48

Other assets 138 24 - 3 7 172

Total assets shown in balance sheet 43’199 1’871 35’954 80 400 81’504

Delivery entitlements from spot exchange, forward forex and forex options transactions - - - - - -

Total assets 43’199 1’871 35’954 80 400 81’504

Liabilities

Amounts due to banks 4’897 350 22’382 57 8 27’694

Amounts due in respect of customer deposits 916 1’502 13’323 13 371 16’125

Accrued expenses and deferred income 5’242 - - - - 5’242

Other liabilities 302 - 1 - - 303

Reserves for general banking risks 1’540 - - - - 1’540

Bank’s capital 5’000 - - - - 5’000

Statutory capital reserve 2’500 - - - - 2’500

Profit carried forward 16’023 - - - - 16’023

Profit (result of the period) 7’077 - - - - 7’077

Total liabilities shown in the balance sheet 43’497 1’852 35’706 70 379 81’504

Delivery obligations from spot exchange, forward forex and forex options transactions - - - - - -

Total liabilities 43’497 1’852 35’706 70 379 81’504

Net position per currency -298 19 248 10 21 -

5. INFORMATION ON THE OFF BALANCE SHEET BUSINESS

5.1 BREAKDOWN OF FIDUCIARY TRANSACTIONS

in SFR 1’000

31.12.2016 31.12.2015

Fiduciary investments with group companies and linked companies 3’764 6’875

Total 3’764 6’875

patrimony 1873 | 27

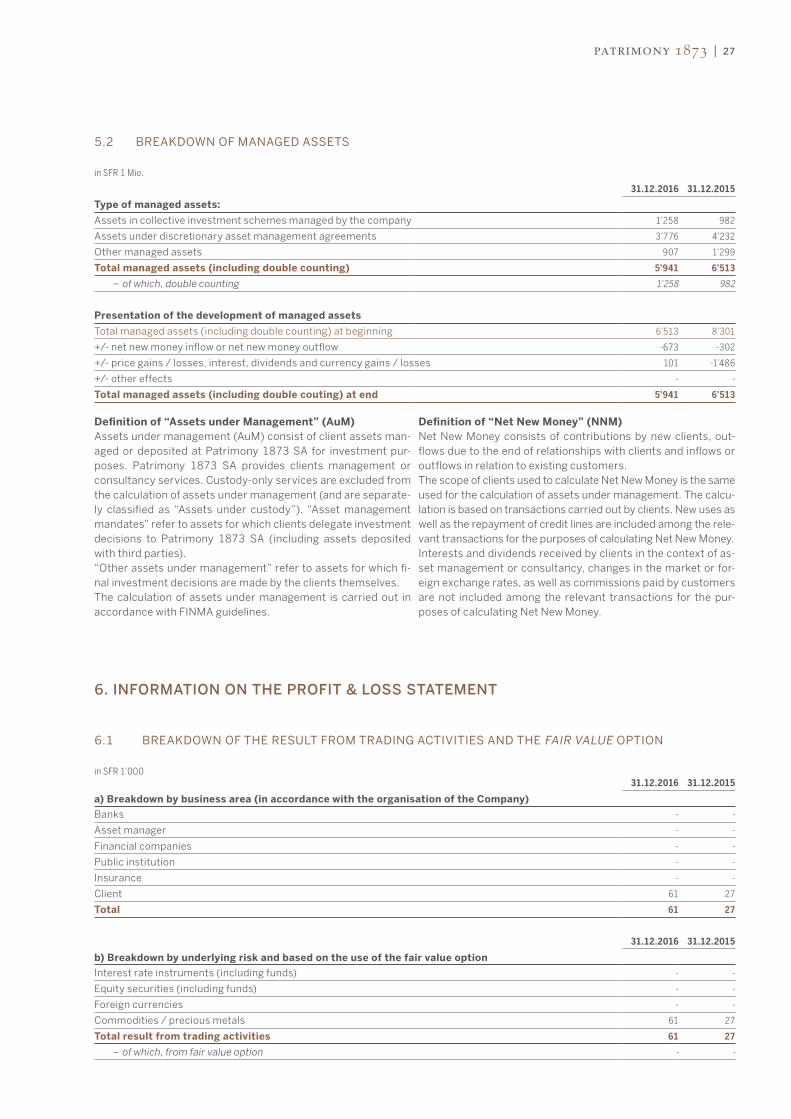

5.2 BREAKDOWN OF MANAGED ASSETS

in SFR 1 Mio.

31.12.2016 31.12.2015

Type of managed assets:

Assets in collective investment schemes managed by the company 1’258 982

Assets under discretionary asset management agreements 3’776 4’232

Other managed assets 907 1’299

Total managed assets (including double counting) 5’941 6’513

– of which, double counting 1’258 982

Presentation of the development of managed assets

Total managed assets (including double counting) at beginning 6’513 8’301

+/- net new money inflow or net new money outflow -673 -302

+/- price gains / losses, interest, dividends and currency gains / losses 101 -1’486

+/- other effects - -

Total managed assets (including double couting) at end 5’941 6’513

Definition of “Assets under Management” (AuM)Assets under management (AuM) consist of client assets man-aged or deposited at Patrimony 1873 SA for investment pur-poses. Patrimony 1873 SA provides clients management or consultancy services. Custody-only services are excluded from the calculation of assets under management (and are separate-ly classified as “Assets under custody”). “Asset management mandates” refer to assets for which clients delegate investment decisions to Patrimony 1873 SA (including assets deposited with third parties).“Other assets under management” refer to assets for which fi-nal investment decisions are made by the clients themselves.The calculation of assets under management is carried out in accordance with FINMA guidelines.

Definition of “Net New Money” (NNM)Net New Money consists of contributions by new clients, out-flows due to the end of relationships with clients and inflows or outflows in relation to existing customers.The scope of clients used to calculate Net New Money is the same used for the calculation of assets under management. The calcu-lation is based on transactions carried out by clients. New uses as well as the repayment of credit lines are included among the rele-vant transactions for the purposes of calculating Net New Money.Interests and dividends received by clients in the context of as-set management or consultancy, changes in the market or for-eign exchange rates, as well as commissions paid by customers are not included among the relevant transactions for the pur-poses of calculating Net New Money.

6. INFORMATION ON THE PROFIT & LOSS STATEMENT

6.1 BREAKDOWN OF THE RESULT FROM TRADING ACTIVITIES AND THE FAIR VALUE OPTION

in SFR 1’00031.12.2016 31.12.2015

a) Breakdown by business area (in accordance with the organisation of the Company)

Banks - -

Asset manager - -

Financial companies - -

Public institution - -

Insurance - -

Client 61 27

Total 61 27

b) Breakdown by underlying risk and based on the use of the fair value option

31.12.2016 31.12.2015

Interest rate instruments (including funds) - -

Equity securities (including funds) - -

Foreign currencies - -

Commodities / precious metals 61 27

Total result from trading activities 61 27

– of which, from fair value option - -

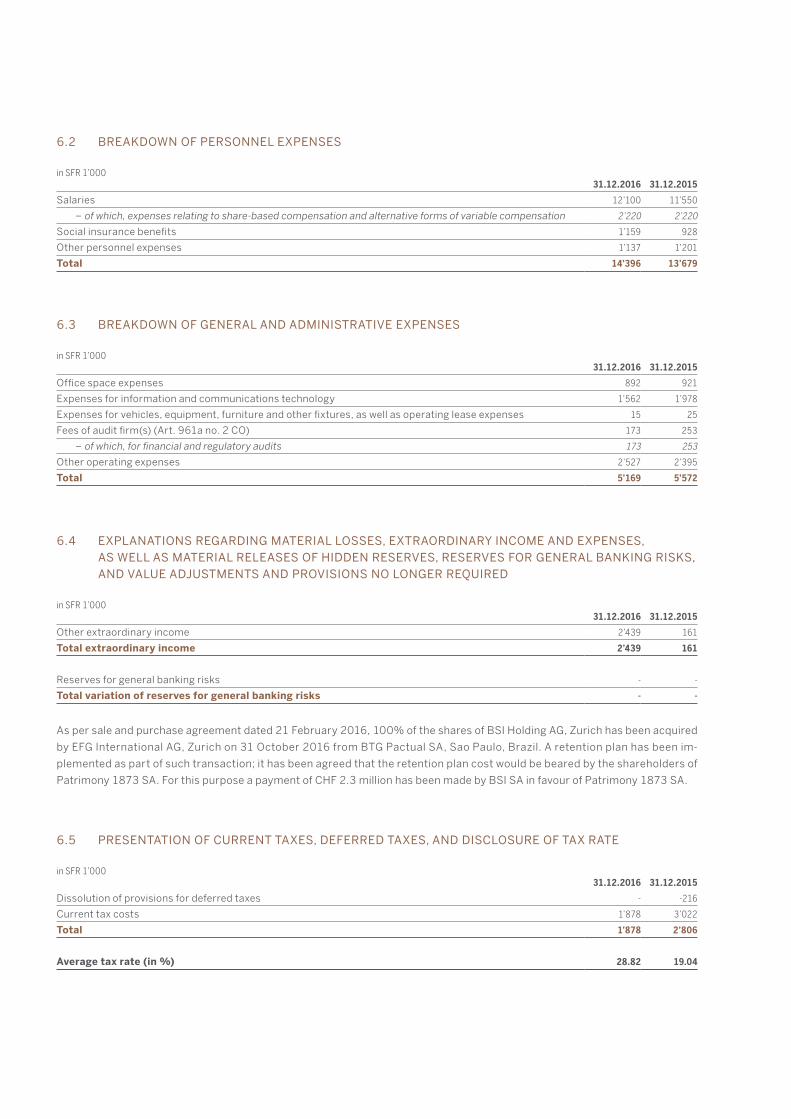

6.2 BREAKDOWN OF PERSONNEL EXPENSES

in SFR 1’00031.12.2016 31.12.2015

Salaries 12’100 11’550

– of which, expenses relating to share-based compensation and alternative forms of variable compensation 2’220 2’220

Social insurance benefits 1’159 928

Other personnel expenses 1’137 1’201

Total 14’396 13’679

6.3 BREAKDOWN OF GENERAL AND ADMINISTRATIVE EXPENSES

in SFR 1’00031.12.2016 31.12.2015

Office space expenses 892 921

Expenses for information and communications technology 1’562 1’978

Expenses for vehicles, equipment, furniture and other fixtures, as well as operating lease expenses 15 25

Fees of audit firm(s) (Art. 961a no. 2 CO) 173 253

–ofwhich,forfinancialandregulatoryaudits 173 253

Other operating expenses 2’527 2’395

Total 5’169 5’572

6.4 EXPLANATIONS REGARDING MATERIAL LOSSES, EXTRAORDINARY INCOME AND EXPENSES, AS WELL AS MATERIAL RELEASES OF HIDDEN RESERVES, RESERVES FOR GENERAL BANKING RISKS,

AND VALUE ADJUSTMENTS AND PROVISIONS NO LONGER REQUIRED

in SFR 1’00031.12.2016 31.12.2015

Other extraordinary income 2’439 161

Total extraordinary income 2’439 161

Reserves for general banking risks - -

Total variation of reserves for general banking risks - -

As per sale and purchase agreement dated 21 February 2016, 100% of the shares of BSI Holding AG, Zurich has been acquired

by EFG International AG, Zurich on 31 October 2016 from BTG Pactual SA, Sao Paulo, Brazil. A retention plan has been im-

plemented as part of such transaction; it has been agreed that the retention plan cost would be beared by the shareholders of

Patrimony 1873 SA. For this purpose a payment of CHF 2.3 million has been made by BSI SA in favour of Patrimony 1873 SA.

6.5 PRESENTATION OF CURRENT TAXES, DEFERRED TAXES, AND DISCLOSURE OF TAX RATE

in SFR 1’00031.12.2016 31.12.2015

Dissolution of provisions for deferred taxes - -216

Current tax costs 1’878 3’022

Total 1’878 2’806

Average tax rate (in %) 28.82 19.04

patrimony 1873 | 29

CAPITAL PLANNING (Unaudited) Since 2013, capital requirements are calculated accord-ing to Basel 3. At the end of 2015 the constraints speci-fied by the Ordinance on Capital Adequacy (CAO) have been respected both in terms of the minimum capital and concentration risk. Quantitative information on cap-ital and credit risks is provided in the attached tables. In accordance with the FINMA guidelines on capital buffer and capital planning, and in consideration of the size of the risks to which the Company is exposed (category 5), it was defined that the new free surplus buffer, above the basic capital adequacy requirements during favourable periods, should be set at the minimum of 31.2%. Addi-tional information about the calculation methods used by the Company is provided below.

• Credit risk The maximum limits on large exposures indicated by

the Ordinance on Capital Adequacy (CAO, Art. 95 et seq.) have been met. There are no groups with risk-weighted assets, calculated in accordance with art. 95 CAO, over 10% of eligible capital. As indicated in art. 99 of the related ordinance, the intra-group positions can be totally excluded from the limits stated in art.97.

• Market Risk Patrimony 1873 applies the standard approach to the

calculation of capital requirements for market risk. As at 31.12.2016 these requirements amount to less than 1% of the available eligible capital.

• Operational Risk To calculate the regulatory requirement for operational

risks, the Company uses the basic indicator approach, weighting gross revenues with 15% factor as defined in the FINMA circular 2008/21. As at 31.12.2016 the reg-ulatory capital for the Company operating risk amount-ed to CHF 5.4 million (2015: 5.4 million), which is about 21% (2015: 21%) of the available eligible capital.

INFORMATION CONCERNING EQUITY CALCULATIONIn relation to the publication requirements of the Basel III, reinforced by FINMA Circular 2016/1 “Disclosure – banks”, here below the required information.

31.12.2016

Capital Requirements

Minimal capital requirements ratio (CET1) 32.98%

Additional capital requirements ratio (T1) 32.98%

Minimal and all additional capital requirements ratio 32.98%

Capital ratio determining capital adequacy target 10.50%

Leverage ratio 29.70%

PricewaterhouseCoopers SA, via della Posta 7, casella postale, CH-6901 Lugano, Switzerland Telefono: +41 58 792 65 00, Fax: +41 58 792 65 10, www.pwc.ch

PricewaterhouseCoopers SA is a member of the global PricewaterhouseCoopers network of firms, each of which is a separate and independent legal entity.

Report of the statutory auditor to the General Meeting of Patrimony 1873 SA Lugano Report of the statutory auditor on the financial statements As statutory auditor, we have audited the financial statements of Patrimony 1873 SA, which comprise the balance sheet, income statement, statement of changes in equity and notes (pages 15 to 28), for the year ended 31 December 2016. Board of Directors' responsibility The Board of Directors is responsible for the preparation of the financial statements in accordance with the requirements of Swiss law and the company’s articles of incorporation. This responsibility includes designing, implementing and maintaining an internal control system relevant to the preparation of financial statements that are free from material misstatement, whether due to fraud or error. The Board of Directors is further responsible for selecting and applying appropriate accounting policies and making accounting estimates that are reasonable in the circumstances. Auditor's responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Swiss law and Swiss Auditing Standards. Those standards require that we plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers the internal control system relevant to the entity’s preparation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control system. An audit also includes evaluating the appropriateness of the accounting policies used and the reasonableness of accounting estimates made, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements for the year ended 31 December 2016 comply with Swiss law and the company’s articles of incorporation. Other matter The financial statements of Patrimony 1873 SA for the year ended 31 December 2015 were audited by another firm of auditors whose report, dated 17 March 2016, expressed an unmodified opinion on those statements.

patrimony 1873 | 31

Report on other legal requirements We confirm that we meet the legal requirements on licensing according to the Auditor Oversight Act (AOA) and independence (art. 728 CO and art. 11 AOA) and that there are no circumstances incompatible with our independence. In accordance with art. 728a paragraph 1 item 3 CO and Swiss Auditing Standard 890, we confirm that an internal control system exists which has been designed for the preparation of financial statements according to the instructions of the Board of Directors. We further confirm that the proposed appropriation of available earnings complies with Swiss law and the company's articles of incorporation. We recommend that the financial statements submitted to you be approved. PricewaterhouseCoopers SA

Omar Grossi

Yousuf Khan

Audit expert Auditor in charge

Audit expert

Lugano, 11 April 2017

Via Peri 21b, CH-6901 Lugano

Tel. + 41(0)91 912 72 72

Fax + 41 (0)91 912 72 70

This document is for purely informative purposes and in no

way represents an offer, invitation or recommendation to

buy or sell certain products or services, which are subject to

change without obligation of prior notification.

Patrimony 1873 Ltd is authorized to operate in Switzerland

as a securities dealer and, as such, is regulated by the Swiss

Financial Market Supervisory Authority (FINMA).

Patrimony 1873 Ltd is not authorized to act as a

securitiesdealer in other countries and is not authorized

to promote or advertise its products and financial

services in these countries. In some countries certain

products and services are subject to legal restrictions;

information about these products is understood to

be intended for those countrieswhere these restrictions

do not apply.

www.patrimony1873.com