annual report: 2013 - football.org.zwfootball.org.zw/posb/images/documents/posbannualreport.pdf ·...

TRANSCRIPT

Page | 1

Annual Report: 2013

VISION AND MISSION STATEMENT ..................................................................................... 2

GENERAL INFORMATION .................................................................................................... 3

BRANCH NETWORK ............................................................................................................. 4

CHAIRMAN‟S STATEMENT ................................................................................................... 7

CHIEF EXECUTIVE OFFICER‟S STATEMENT ......................................................................... 9

DIRECTORS‟ REPORT ......................................................................................................... 12

CORPORATE GOVERNANCE REPORT ............................................................................ 14

REPORT OF THE AUDITOR –GENERAL .............................................................................. 18

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME ................. 20

STATEMENT OF FINANCIAL POSITION .............................................................................. 21

STATEMENT OF CHANGES IN EQUITY .............................................................................. 22

STATEMENT OF CASH FLOWS ........................................................................................... 23

NOTES TO THE FINANCIAL STATEMENTS ……………………………………………..…… 24

Page | 2

VISION AND MISSION STATEMENT

“To be a world class Savings Bank catering for all”

“A Savings Bank which provides a broad range of quality, accessible and

affordable financial services.

Integrity

Innovation

Commitment

Excellence

OUR VISION

OUR MISSION STATEMENT

OUR VALUES

Page | 3

GENERAL INFORMATION

HEAD OFFICE AUDITORS Causeway Building Auditor General

Corner Central Avenue/ Third Street 48 Burroughs House

P.O. Box CY 1628, Causeway, Harare Fourth Street / George Silundika Ave

Telephone: 263-4-793831 / 729701 P.O. Box CY 143 Causeway

Fax: 263-04- 708537 / 730971 Harare

Website: www.posb.co.zw Telephone: 263-4-793611/4& 762817/8

Email: [email protected]

ATTORNEYS Mawere and Sibanda

Legal Practitioners

10th Floor Chiedza House

1st Street/ Nkwame Nkrumah Ave

Box CY1376, Harare

Telephone: 263-4-750843/ 750627

Email: [email protected]

BOARD OF DIRECTORS

Mr. I.P.Z. Ndlovu Acting Chairman

Mr. C.T. Nyamurova Member

Mr. O. Jambwa Member

Mr. A. Mpepu Member

Mr. A. Kandlela Chief Executive Officer

Mrs. P.M. Shuro Chief Accounting Officer

COMPANY SECRETARY

Mrs. D. Mapimhidze

EXECUTIVE MANAGEMENT

Mr. A. Kandlela Chief Executive Officer

Mrs. P.M. Shuro General Manager Finance and Administration

Mr. E. Chibvuri General Manager Banking Operations

Mr. W. Fungura General Manager Risk and Compliance

Mr. M. Kujeke Human Resources Executive

Mr. R. Gwendere Treasury Executive

Ms. L. Ngulube Information Technology Executive

Page | 4

RETAIL BRANCHES

Bindura Branch

111 Thurlows Ave

Farm & City Complex

Bindura

Telephone: 263-71-7481/7939

Gweru Branch

Corner 7th Street/Robert Mugabe

Gweru

Telephone: 263-054-220545/222798

Bulawayo Main Branch

Corner Main Street/L Takawira

Bulawayo

Telephone: 263-09-74023/79212

Halyet House Branch

Corner Josiah Tongogara Street/9th Ave

Bulawayo

Telephone: 263-09-76911/79205

Causeway Branch

Corner Central Ave/Third Street

Harare

Telephone: 263-4-735895

Harare Main

Mezzanine Floor, Harare Main Post Office

Cnr Innez Terrace/N. Mandela

Telephone: 263-4-773635

Chiedza Branch

68 Nkwame Nkrumah

Harare

Telephone: 263-703647/8

Highglen Branch

Shop Number 3

Highglen Shopping Centre

Telephone: 263-4-691920/692408

Chinhoyi Branch

135 Midway Street

Chinhoyi

Telephone: 263-67-25309

Kadoma Branch

28A, Herbert Chitepo Street

Kadoma

Telephone: 263-68-23488/23988

Chiredzi Branch

Old Mutual Shopping Complex

Chiredzi

Telephone: 263-031-2200/33

Karoi Branch

42 Fred Jameson Ave

Karoi

Telephone: 263-064-791/7911

Chitungwiza Branch

Chitungwiza Town Centre

Chitungwiza

Telephone: 263-70-21985/7

Kopje Plaza Branch

Corner Jason Moyo Ave/Rotten Row Rd

Harare

Telephone: 263-4-771865

Fort Street Branch

Corner Fort St/Dr Antony Taylor Avenue

Bulawayo

Telephone: 263-09-67328/64118

Kwekwe Branch

2 Kings Avenue

Kwekwe

Telephone: 263-055-24575/7

Gokwe Branch

Intermarket House

Gokwe Centre

Telephone: 263-059-2764/2798

Marondera Branch

Stand 1137, Second Street

Marondera

Telephone: 263-79-22980/2

BRANCH NETWORK

Page | 5

RETAIL BRANCHES (continued)

Gwanda Branch

169 Sandan Street

Gwanda

Telephone: 263-084-22433/22441

Rusape Branch

8 Manda Ave

Rusape

Telephone: 263-25-3092/3

Masvingo Branch

48 Hughes Road

Masvingo

Telephone: 263-039-264309/264311

Southerton Branch

Corner Highfield Rd/Lobengula Rd

Harare

Telephone: 263-4-620030/9

Mbare Branch

14808 Captain Tapfumaneyi Street

Mbare

Harare

Telephone: 263-4-771950

Victoria Falls Branch

1 Landela Complex

Victoria Fall

Telephone: 263-013-42631

Mutare Branch

Stand 4011 1st Avenue

Mutare

Telephone: 263-20-61766/66837

Westgate Branch

Shop MP1 Westgate Shopping Centre

Harare

Telephone: 263-4-334100/4

Mutoko Branch

Shop Number 1 Stand 46/47

BJ Shopping Mall

Oliver Newton Road

Mutoko

Telephone: 263-272-2748/2868/2896

Zvishavane Branch

Stand No 22-23

Robert Mugabe Way

Zvishavane

Telephone: 263-051-2383,2654/2056-7

Mvuma Branch

Slice Complex

580 Masvingo Road

Telephone: 263-32-0225

Nelson Mandela Branch

Corner N. Mandela / L. Takawira Street

Harare

Telephone: 263-4751513/511

Nkulumane Branch

Shop 9 Nkulumane

Bulawayo

Telephone: 263-084-22433/2241

Parirenyatwa Branch

Parirenyatwa Hospital

Mazowe street

Harare

Telephone: 263-4-795689

Page | 6

Esteem Banking Branches Ascot Shopping Centre (Bulawayo)

Bulawayo

Telephone: 263-09-64321/27

Exhibition Park (Harare)

Harare Show grounds

Telephone: 263-04-774172

Page | 7

CHAIRMAN’S STATEMENT Introduction

I am pleased to present the audited results of the People‟s Own Savings Bank for the year ended

December 31, 2013.

Operating environment and banking sector overview

The economy continued to face challenges in the year 2013, chiefly the persistent liquidity

crunch, lack of competitiveness of locally produced goods as well as infrastructure bottlenecks

around key economic enablers such as energy, transport and communication. These challenges

resulted in low capacity utilization, widespread company failures and rising unemployment.

The banking sector remained generally stable despite the various underlying macroeconomic

challenges and weaknesses specific to individual institutions. Total banking sector deposits which

stood at $3.81 billion at the beginning of the year closed the year at $4.73 billion thus registering a

growth of 24%. On the other hand, total credit to the private sector increased by only 4% from

$3.56 billion in January 2013 to $3.70 billion by year end. The performance in the banking sector is

consistent with the economic slowdown experienced over the same period. Annual inflation

which stood at 2.51% in January 2013 declined significantly to 0.33% by December 2013 with

growing fears of deflation. This is also a reflection of depressed demand, prevailing liquidity

shortages as well as weakening of the South African rand against the United States dollar thus

making imports cheaper.

Financial highlights

The Bank witnessed a decline in profitability and recorded a loss of $0.209 million during the year

under review compared to a profit of $2.47 million in the prior year. The loss was mainly as a result

of the impact of the Memorandum of Understanding signed by banks and the Reserve Bank

which sought to reduce bank charges and interest rates, coupled by the increase in provisions for

impairment losses. The following highlights the Bank‟s performance;

Revenues for the year declined by 15% compared to last year.

Operating costs declined by 4% compared to last year.

Cost to income ratio for the year deteriorated from 89% in 2012 to 101% in 2013.

Total assets and deposits grew by 12% and13% respectively in the year under review.

The loan to deposit ratio declined from 59% in 2012 to 54% in 2013 as a result of the

cautious approach to lending.

Corporate governance

The board recognizes and subscribes to the principles of good corporate governance and strict

adherence thereof. The board is committed to the principle of openness, integrity and

accountability as required by good corporate governance guidelines. It will continue to uphold

the Bank‟s core values of integrity, innovation, commitment and excellence. During the year

under review, the Bank complied with regulatory requirements and central Bank directives, in all

material respects.

Corporate social responsibility

The People‟s Own Savings Bank will continue to be actively involved in the society in which it

operates. The Bank remains committed to supporting the less privileged and the socially

disadvantaged members of our community. During the year under review, the Bank continued to

be involved in various corporate social responsibility programmes in an effort to alleviate poverty

Page | 8

and enhance the well-being of the society in general. The Bank has been largely active in the

areas of education, health and other social fundraising activities.

Outlook

The Bank will continue to introduce new products particularly in the electronic space, with

greater emphasis on improved quality of service. Cost optimization will also remain an operating

imperative for the Bank. The People‟s Own Savings Bank shall continue to contribute to the

overall improvement in the growth of the country‟s economy by playing a key role in the banking

sector.

Appreciation

I wish to extend my appreciation to the Shareholder, Board, Chief Executive Officer,

Management and members of staff for their input during the year. My appreciation also goes to

all stakeholders, especially our customers for their unwavering support which enabled the Bank to

continue operations in 2013.

I.P.Z. NDLOVU

ACTING BOARD CHAIRMAN

Page | 9

CHIEF EXECUTIVE OFFICER’S STATEMENT General Overview

The financial sector remained crippled by tight liquidity conditions, volatile and transitory

deposits, high non-performing loans, limited activity on the interbank market, absence of lender

of last resort and low savings. Despite the foregoing the banking sector remained largely stable.

The Bank recorded a loss of $0.209 million for the financial year ended December 31, 2013. This

was mainly a result of the introduction of the Memorandum of Understanding (MoU) between the

Reserve Bank of Zimbabwe and banks in January 2013 which saw the Bank waiving charges on

all pensioners above the age of 60 years. This had a great impact as the Bank serves the largest

community of pensioners countrywide. Furthermore, the Bank had to increase its provisions for

impairment losses in order to cover its exposures and this, undoubtedly had a significant impact

on its financial performance. Despite the loss recorded for the year, the Bank was able to realign

its cost structure thus recording a decline in operating costs of 4%. Although the Bank‟s deposits

increased by 13%, the composition of the deposits remained unfavourable for long term lending

and investments. Lending business grew by a marginal 3% from last year, and this is reflective of

the tight liquidity conditions as well as the cautious approach adopted by most banks with

respect to lending.

Despite the foregoing, the Bank continued to be aggressive in deposit mobilization and business

development, focusing more on the mass market and small to medium enterprises. The Bank also

used its wide branch network to attract depositors.

Financial performance

The Bank witnessed a decline in profitability and recorded a loss of $0.209 million during the year

under review compared to a profit of $2.47 million in the prior year.

Total income declined by 15% from $22.73 million in 2012 to $19.21million in 2013 and this was

mainly as a result of the effects of the Memorandum of Understanding (MoU) between the

Reserve Bank and financial institutions in January 2013 which saw the sector recording a

significant decline in bank charges and lending rates. On a positive note, total costs declined by

4% as the Bank put in place effective cost cutting measures in an effort to reduce the decline in

performance caused by subdued income. Total assets grew by 12% from $80.57 million in 2012 to

$89.97 million by December 2013. On the same note, total deposits grew by 13% from $63.81

million in 2012 to $72.15 million by December 2013. The capital adequacy ratio at 13.55% exceeds

the prescribed minimum regulatory ratio of 12% and enables the Bank to meet all prudential

lending guidelines.

Corporate developments

The following highlights mark the operations of the Bank in the year under review;

Page | 10

Branch expansion

In an effort to bring convenience to our customers the Bank added 2 branches to its

stable, namely Mbare and Mvuma. The Harare Esteem branch and the Nelson Mandela

branch were renovated so as to improve on service delivery.

Upgrade of the core banking system

The Bank completed its upgrade of the core banking system in the first half of the year in

an effort to promote efficiency and reduce the cost of service delivery.

Enhancement of mobile banking

In the year under review, the Bank enhanced mobile banking for its customers which was

introduced in 2012. This will also enable the Bank to design products and pricing structures

which suit the low income groups.

Branch network

The Bank operated through its 34 branches country wide as well as 180 Zimpost outlets which

largely cover rural communities nationwide. The Bank has continued to witness increased level of

business activity being generated via the Zimpost agency as a result of deployment of Point of

Sale devices in 2012. This development has allowed faster and more efficient service delivery to

all our customers accessing our services from Zimpost outlets.

Training and development

The Bank continues to promote training and development to its employees by giving financial

support to members of staff undergoing career development programmes. Continuous

improvement remains the overall objective in terms of our Learning and Growth initiatives.

Risk management

The Bank acquired risk management software which was fully implemented by end of year 2013.

This will go a long way in ensuring effective management of all bank risks. The Modified,

Standardised approach of BASEL II was also fully implemented in compliance with Reserve Bank

of Zimbabwe regulations.

Strategic Alliances

Zimpost continues to be our key strategic partner in extending our delivery channels. In the period

under review, Zimpost handled an average of 7% of the Bank‟s business.

Legal Status

The Bank continues to be governed by the People‟s Own Savings Bank of Zimbabwe Act

{Chapter 24:22} of 1999 but under the supervision of the Reserve Bank of Zimbabwe.

Corporate Social Responsibility

POSB continues to be a responsible corporate citizen by playing a pivotal role in the communities

in which we exist. The following activities amongst others were undertaken in 2013;

Education

The Bank maintained its education support to financially disadvantaged students in the

form of full scholarships in all the country‟s ten provinces. The Bank was also involved in

reconstruction of some rural schools during the year.

Page | 11

Health

The Bank continued to support the health sector through provision of medical equipment,

linen and other ancillaries at major hospitals.

Rehabilitation of prisoners

POSB supported the rehabilitation of prisoners by providing them with farming tools to

enable them to do farming activities. This will go a long way in preparing the prisoners for

self-sustainment after serving their prison terms.

Other Charities

The Bank continues to work with a number of other organizations which are involved with

Charities in order to improve the well-being of communities.

Outlook

The People‟s Own Savings Bank is committed to maintaining its status as a savings bank thus its

vision remains: To be a world class Savings Bank catering for all. The Bank‟s strategy for 2014 is to

consolidate the branch network and to drive more utilization towards digital and electronic

platforms for improved service to our customers. To this end, the Savings Bank intends to provide

a wide range of usable financial services, support innovative business partnerships, support

financial literacy efforts and develop further information technology solutions for financial

inclusion.

Appreciation

I wish to extend my appreciation to the Shareholder, Board, Management and members of staff

for their sterling efforts during the past year. My appreciation also goes to all stakeholders,

especially our customers who have continued to conduct business with us in the year 2013.

A. KANDLELA

CHIEF EXECUTIVE OFFICER

Page | 12

DIRECTORS’ REPORT The People‟s Own Savings Bank Board is pleased to present the Annual Report and the Audited

Financial Statements for the year ended December 31, 2013.

Legal form

The People‟s Own Savings Bank is a corporate body established in terms of the People‟s Own

Savings Bank of Zimbabwe Act {Chapter 24:22} of 1999. It is broadly mandated to carry on the

business of a savings Bank, as well as offering Banking and financial services to the people of

Zimbabwe.

Year’s results

The financial results for the year ended December 31, 2013 are a reflection of the economic

slowdown over the period under review. The Bank‟s operating environment was haunted by

limited liquidity, transitory deposits as well as high default rate by borrowers. Total revenue

declined by 15% as a result of the implementation of the MoU where both interest rates and bank

charges were reduced, coupled with an increase in loan impairment provisions. On a positive

note, the Bank was able to reduce operating costs by 4% although this was not enough to cover

for the loss in revenue. The final result was therefore, a decline in profit by 108%. The following

shows the performance of the Bank in brief;

2013 2012 % change

Operating income 19,219,535 22,726,880 -15%

Operating expenses (19,428,900) (20,254,834) -4%

Net profit/(loss) (209,365) 2,472,046 -108%

Customer deposits 72,146,642 63,810,070 13%

Total assets 89,993,297 80,574,715 12%

Board members responsibility statement

The responsibility for the preparation and integrity of the financial statements that would fairly

present the state of affairs of the Bank at the end of the financial year lies with the Board. The

reports include the Statement of Financial Position, Statement of Profit or Loss and Other

Comprehensive Income, Statement of Changes in Equity and Statement of Cash flows for the

period, together with notes and other information contained in these reports. The financial

statements were prepared according to International Financial Reporting Standards.

In order to ensure integrity of the financial statements, the Board maintains adequate accounting

records and has put in place adequate internal controls and a robust risk management

framework in order to safeguard the assets of the Bank and to prevent and detect fraudulent

activities.

Page | 13

The Board has reassessed the operations of the Bank and is of the opinion that the Bank continues

to be a going concern. Accordingly the financial statements continue to be prepared on a

going concern basis. The financial statements on pages 20 to 64 were approved by the Board of

Directors on 18 March 2014.

Auditors The Auditor General continues to be the auditors of the Bank as provided for in section 34 of the

People‟s Own Savings Bank Act {Chapter 24:22} of 1999 and the Public Finance Management

Act [Chapter 22:19].

By order of the Board

IPZ NDLOVU

ACTING CHAIRMAN

A KANDLELA

CHIEF EXECUTIVE OFFICER

D. MAPIMHIDZE

COMPANY SECRETARY

Page | 14

CORPORATE GOVERNANCE REPORT The POSB Board recognizes the importance of good corporate governance and its impact on

the Bank‟s operations and ultimate performance. In this regard it focuses on attaining high

standards of corporate governance in line with the law, government policies, governance

guidelines and directives on Banks.

The Bank adopted and embarked on implementing the Corporate Governance Framework for

State Enterprises and Parastatals Guidelines issued in November 2010 by the Government of

Zimbabwe. Further, it regularly reviews its structures and policies to ensure continued adherence

to government policies, the RBZ corporate governance guidelines and or directives and

international best practices applicable to the Bank. The Board also recognizes that Zimbabwe as

a country has taken the upholding of good corporate governance practices seriously by

incorporating this as a national objective in the new constitution and remains cognisant of the

Bank‟s constitutional obligations in this regard. It thus continues to conduct business by observing

the highest standards of ethics and professional conduct through the governance structures

detailed below:

The Board

The Board comprises of four (4) independent non-executive directors and two (2) executive

directors, the Chief Executive Officer and the Chief Accounting Officer. The detailed

responsibilities of the Bank‟s Board include the following;

To set the Bank‟s direction/objectives;

To approve the Bank‟s policies;

To protect the interest of depositors and other stakeholders;

To align activities and behaviour to ensure the Bank operates in a safe and sound

manner, in compliance with applicable laws and regulations;

To articulate the strategy against which the success of the overall Bank and the

contribution of individuals is measured; and

To assign responsibilities and decision making authorities, incorporating a hierarchy of

required approvals from management to the board.

Board Committees and Meetings

The Board as a whole is responsible for the oversight of management on behalf of the

shareholder, the Government of Zimbabwe. To exercise its duties, the Board meets quarterly

through scheduled meetings, but may meet more frequently when the need arises. To assist the

Board in its oversight function, a number of Board Committees were established, in accordance

with section 14(i) of the People‟s Own Savings Bank Act {Chapter 24:22}. Details of the existing

Board Committees are outlined in the following paragraphs:

1. Board Audit Committee

The Board Audit Committee is authorized by the Board to review and assess recommendations

and reports of the finances, financial controls of the Bank and the internal audit function; and

where appropriate, make recommendations of its own to the Board regarding the financial

administration of the Bank.

Composition

Mr. I.P.Z. Ndlovu (Non- executive committee chairman)

Mr. A. Mpepu (Non- executive member)

Mr. O. Jambwa (Non -executive member)

Page | 15

The Chief Executive Officer, the Chief Accounting Officer and Head-Internal audit are not

members of the Board Audit Committee but can attend the Committee‟s meetings by invitation.

2. Board Credit and Investments Committee

The fundamental function of the Committee is to oversee the Bank‟s operations relating to credit,

market and liquidity risk, and in particular to ensure that the Bank has adequate funds to meet its

obligations. Furthermore the committee ensures that the Bank‟s lending policies are adequate

and that lending activities are conducted in accordance with established policies and

regulations.

The committee has the mandate over risks underwritten by the Bank in as far as they affect its

overall performance including particularly market risks and credit risks. The maintenance of safety

and procedures is a core objective of the Committee and to ensure this objective is aligned with

the Bank‟s need for consistent profits to finance operations, balanced with risk and other factors.

The Board Credit and Investments committee also ensures that the Bank has approved overall

lending policies in place and that lending activities are conducted in accordance with the

approved credit policies and regulations and that the policies are adequate. The committee is

also responsible for approval of loans to customers within its limit.

Composition

Mr. C.T. Nyamurova (Alt.) Mr I Mvere (Non- executive committee chairman)

Mr. O. Jambwa (Non- executive member)

Mr. A. Kandlela (Executive member)

Mrs. P.M. Shuro (Executive member)

Mr. E. Chibvuri (General manager banking operations)

Mr. R. Gwendere (Treasury executive)

3. Board Credit Review Committee

The Board Review Committee is tasked with the primary responsibility of monitoring the

performance of the loan book and ensuring that it is proficiently managed and appropriately

diversified to manage concentration risk. It also has the broad responsibility of ensuring that the

Bank‟s potential and specific bad debts are adequately provided for and that the total loan

book is in compliance with the lending guidelines and the Bank‟s credit policy. For segregation of

duties, the Board credit review committee acts as an independent committee carrying out

separate functions to those of the Board credit and investments committee, which is involved

partly, in the granting of credit.

Any member of the management team or Board Credit Committee involved in the sanctioning

of credit cannot be a member of the Board Credit Review Committee.

Composition

Mr. A. Mpepu (Non- executive committee chairman)

Mr. I.P.Z. Ndlovu (Non- executive member)

Mr. W. Fungura (General manager risk and compliance)

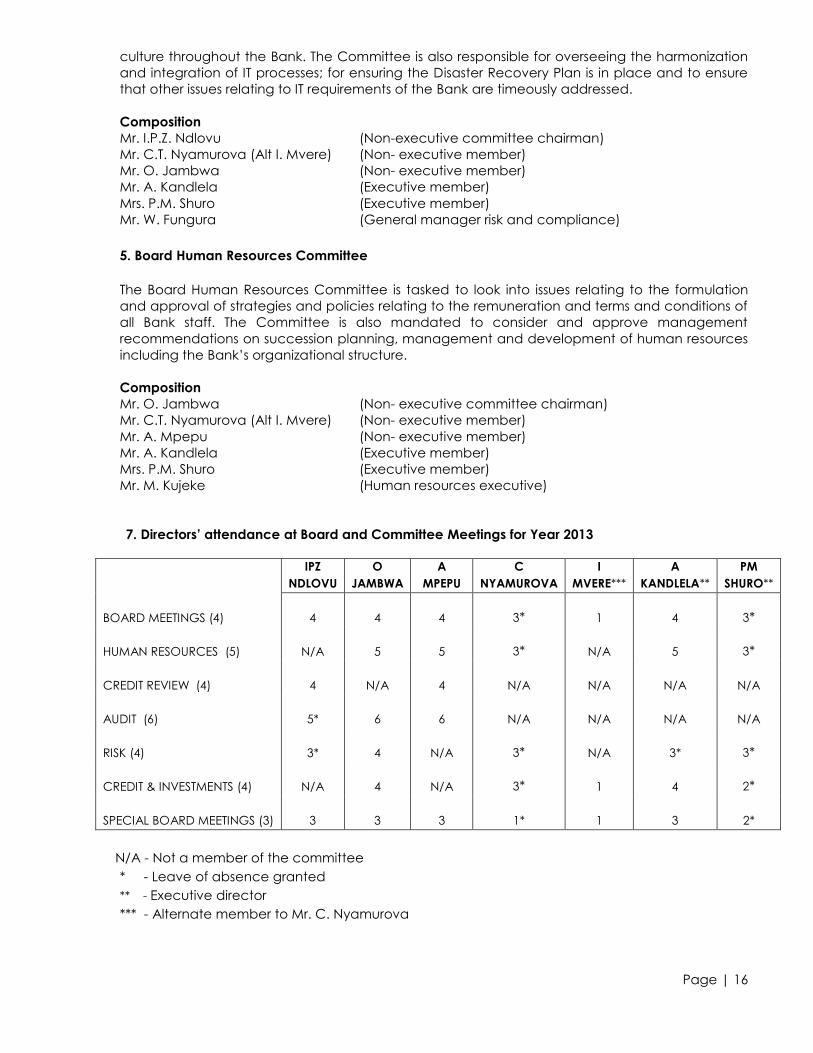

4. Board Risk and IT Management Committee

The Committee is responsible for overall identification, measurement, management and

monitoring of all risks facing the Bank. In the main, the risk management committee is responsible

for the formulation of high level risk management policies and for inculcating a risk management

Page | 16

culture throughout the Bank. The Committee is also responsible for overseeing the harmonization

and integration of IT processes; for ensuring the Disaster Recovery Plan is in place and to ensure

that other issues relating to IT requirements of the Bank are timeously addressed.

Composition

Mr. I.P.Z. Ndlovu (Non-executive committee chairman)

Mr. C.T. Nyamurova (Alt I. Mvere) (Non- executive member)

Mr. O. Jambwa (Non- executive member)

Mr. A. Kandlela (Executive member)

Mrs. P.M. Shuro (Executive member)

Mr. W. Fungura (General manager risk and compliance)

5. Board Human Resources Committee

The Board Human Resources Committee is tasked to look into issues relating to the formulation

and approval of strategies and policies relating to the remuneration and terms and conditions of

all Bank staff. The Committee is also mandated to consider and approve management

recommendations on succession planning, management and development of human resources

including the Bank‟s organizational structure.

Composition

Mr. O. Jambwa (Non- executive committee chairman)

Mr. C.T. Nyamurova (Alt I. Mvere) (Non- executive member)

Mr. A. Mpepu (Non- executive member)

Mr. A. Kandlela (Executive member)

Mrs. P.M. Shuro (Executive member)

Mr. M. Kujeke (Human resources executive)

7. Directors’ attendance at Board and Committee Meetings for Year 2013

IPZ

NDLOVU

O

JAMBWA

A

MPEPU

C

NYAMUROVA

I

MVERE***

A

KANDLELA**

PM

SHURO**

BOARD MEETINGS (4) 4 4 4 3*

1 4 3*

HUMAN RESOURCES (5) N/A 5 5 3*

N/A 5 3*

CREDIT REVIEW (4) 4 N/A 4 N/A

N/A N/A N/A

AUDIT (6) 5* 6 6 N/A

N/A N/A N/A

RISK (4) 3* 4 N/A 3*

N/A 3* 3*

CREDIT & INVESTMENTS (4) N/A 4 N/A 3*

1 4 2*

SPECIAL BOARD MEETINGS (3) 3 3 3 1*

1 3 2*

Key

N/A - Not a member of the committee

* - Leave of absence granted

** - Executive director

*** - Alternate member to Mr. C. Nyamurova

Page | 17

8. Management Committees

The Bank has put in place a number of management committees that assist in the management

of Board functions. The prominent management committees are briefly highlighted as follows:

8.1 Executive Committee (EC)

The Executive Committee has the mandate to manage the affairs of the Bank between meetings

of the Board. The Committee‟s main function is to review significant functions of the Bank and

recommend action as appropriate to the Board. The Executive Committee also handles matters

that are not assigned to any specific management committee and as may be delegated by the

Board.

Membership of the Executive Committee comprises the Chief Executive Officer as Chairman and

the Executive Management team. Non-Executive Board members and other managers may

attend Executive Committee meetings by invitation or as directed by the Board and/or any of

the Board Committees.

8.2 Management Assets/Liabilities Committee (ALCO)

The Bank has a management Assets/Liabilities Committee, which meets on a monthly basis to

review the product pricing, liquidity and market risks positions. The committee considers exposure

positions of the Bank and formulates strategies based on balanced risk and return on investments.

The committee also reviews the Bank‟s balance sheet and recommends the optimal asset and

liability mix which should be carried by the Bank.

8.3 Other prominent management committees

Other management committees that exist within the Bank include the Management Credit

Committee, Purchasing Committee and the IT Steering Committee. The IT Steering Committee is

mandated to oversee the IT processes and continuous improvement of IT systems and

procedures. The Purchasing committee oversees the purchase of all material capital and other

expenditure as guided by the State Procurement board to ensure compliance thereof and

effective cost monitoring.

Page | 18

All communications should be addressed to Reference: I/69/960

“The Auditor-General”

REPORT OF THE AUDITOR –GENERAL

TO

THE MINISTER OF FINANCE AND ECONOMIC DEVELOPMENT

AND

THE BOARD OF DIRECTORS

IN RESPECT OF THE FINANCIAL STATEMENTS FOR THE

PEOPLE’S OWN SAVINGS BANK

FOR THE YEAR ENDED DECEMBER 31, 2013

Report on the Financial Statements

I have audited the accompanying financial statements of the People‟s Own Savings Bank as set

out on pages 20 to 64, which comprise the statement of financial position as at December 31,

2013, and the statement of comprehensive income, the statement of changes in equity and

statement of cash flows for the year then ended, and the notes to the financial statements,

which include a summary of significant accounting policies and other explanatory notes.

Directors’ Responsibility for the Financial Statements

The Bank‟s directors are responsible for the preparation and fair presentation of these financial

statements in accordance with International Financial Reporting Standards (IFRS) and in the

manner required by the People‟s Own Savings Bank Act (Chapter 24:22). This responsibility also

includes: designing, implementing and maintaining internal controls relevant to the preparation

and fair presentation of financial statements that are free from material misstatement, whether

due to fraud or error; selecting and applying appropriate accounting policies; and making

accounting estimates that are reasonable in the circumstances.

Auditor’s Responsibility

My responsibility is to express an opinion on these financial statements based on my audit. I

conducted my audit in accordance with International Standards on Auditing. Those Standards

require that I comply with ethical requirements and plan and perform the audit to obtain

reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditor‟s

judgment, including the assessment of the risks of material misstatement of the financial

statements, whether due to fraud or error. In making those risk assessments, the auditor considers

internal control relevant to the entity‟s preparation and fair presentation of the financial

ZIMBABWE

P.O. Box CY 143, Causeway, Harare Telephone No.: 793611/3-4/762817/8/20-23

Telegrams: “AUDITOR”

706070/796312 E-mail: [email protected]

OFFICE OF THE AUDITOR-GENERAL

5th Floor, Burroughs House

48 George Silundika

Cnr. Fourth Street/ George Silundika Avenue

Harare

Page | 19

statements in order to design audit procedures that are appropriate in the circumstances, but

not for the purpose of expressing an opinion on the effectiveness of the entity‟s internal control.

An audit also includes evaluating the appropriateness of accounting policies used and the

reasonableness of accounting estimates made by management, as well as evaluating the

overall presentation of the financial statements.

I believe that the audit evidence I have obtained is sufficient and appropriate to provide a basis

for my audit opinion.

Opinion

In my opinion, the financial statements present fairly, in all material respects, the financial position

of the People‟s Own Savings Bank as at December 31, 2013, and its financial performance and its

cash flows for the year then ended in accordance with International Financial Reporting

Standards.

Report on other legal and regulatory requirements

In my opinion, the financial statements have, in all material respects, been properly prepared in

compliance with the disclosure requirements of the People„s Own Savings Bank Act (Chapter

24:22) and other relevant Statutory Instruments.

____________________, 2014. ______________________________________

M. CHIRI,

AUDITOR – GENERAL.

PEOPLE’S OWN SAVINGS BANK

Page | 20

Statement of profit or loss and other comprehensive income

For the year ended December 31, 2013

HISTORICAL COST

Notes Dec 13

US$

Dec 12

US$

Interest income

Interest expense

5

6

9,159,609

(2,762,853)

8,871,394

(2,303,524)

Net interest income

6,396,756 6,567,870

Increase in impairment losses on loans and advances

Net interest income after provisions

Fees and commission income

Dividend income

Fair value gain on investment properties

Other operating income

10.4

7

8

(3,032,745)

3,364,011

15,573,804

63,091

5,600

213,029

(728,459)

5,839,411

16,567,373

90,073

13,900

216,123

Net operating income

19,219,535 22,726,880

Operating expenses

9 (19,428,900) (20,254,834)

(Loss)/profit for the year (209,365) 2,472,046

Other comprehensive income

Items that will not be reclassified to profit or loss

Fair value gain on financial assets at fair value through other

comprehensive income

Revaluation gain of non-current assets

Items that will be reclassified to profit or loss

Total comprehensive income for the year

431,938

2,667

-

225,240

256,286

-

-

2,728,332

PEOPLE’S OWN SAVINGS BANK

Page | 21

Statement of financial position

As at December 31, 2013

HISTORICAL COST

Notes

Dec-13

US$

Dec-12

US$

ASSETS

Cash and balances with banks

10,858,680 8,535,385

Balances with the Central Bank

9,469,540 842,768

Financial assets at amortised cost 10 47,676,439 55,660,508

Financial assets at fair value through other

comprehensive income 11.1 3,235,524 2,667,392

Investment properties 11.2 177,000 225,000

Other assets 12 10,339,970 9,183,413

Property, plant and equipment 13 4,910,620 3,380,870

Intangible assets 14 3,325,524 79,379

TOTAL ASSETS 89,993,297 80,574,715

LIABILITIES

Customer deposits 15 72,146,642

63,810,070

Other liabilities 16 5,398,524 3,923,742

TOTAL LIABILITIES

77,545,166

67,733,812

EQUITY AND RESERVES

Share capital

Mark- to-market reserves

17.1

17.2

6,729,662

(526,475)

6,729,662

(958,413)

Revaluation reserve 2,667 -

Revenue reserves

6,242,277 7,069,654

TOTAL EQUITY AND RESERVES

12,448,131

12,840,903

TOTAL LIABILITIES, EQUITY AND RESERVES 89,993,297 80,574,715

……………………………. Chief Executive Officer (A. Kandlela) March 2014

…………………………… Acting Board Chairman (I.P.Z. Ndlovu) March 2014

PEOPLE’S OWN SAVINGS BANK

Page | 22

Statement of changes in equity

For the year ended December 31, 2013

HISTORICAL COST

Share

capital

Revenue

reserve

Mark- to-

market

reserve

Revaluation

reserves Total

US$ US$ US$ US$ US$

Balance at January 01, 2012

6,729,662 5,624,997 (1,214,699) - 11,139,960

Total comprehensive income

for the year -

2,472,046 256,286 - 2,728,332

Dividend - (1,027,389) - - (1,027,389)

Balance at December 31,

2012

6,729,662 7,069,654 (958,413) - 12,840,903

Total comprehensive

income/(loss) for the year - (209,365) 431,938 2,667 225,240

Dividend - (618,012) - - (618,012)

Balance at December 31,

2013

6,729,662 6,242,277 (526,475) 2,667 12,448,131

PEOPLE’S OWN SAVINGS BANK

Page | 23

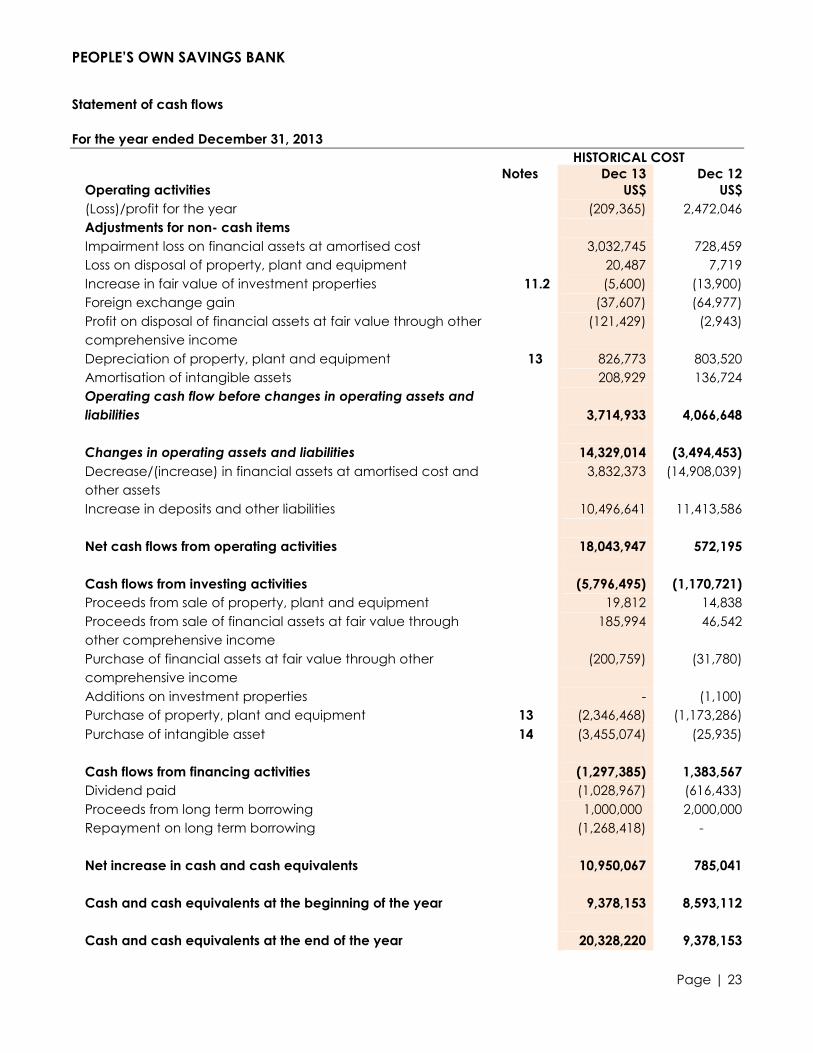

Statement of cash flows

For the year ended December 31, 2013

HISTORICAL COST

Notes Dec 13 Dec 12

Operating activities US$ US$

(Loss)/profit for the year (209,365) 2,472,046

Adjustments for non- cash items

Impairment loss on financial assets at amortised cost 3,032,745 728,459

Loss on disposal of property, plant and equipment 20,487 7,719

Increase in fair value of investment properties 11.2 (5,600) (13,900)

Foreign exchange gain (37,607) (64,977)

Profit on disposal of financial assets at fair value through other

comprehensive income

(121,429) (2,943)

Depreciation of property, plant and equipment 13 826,773 803,520

Amortisation of intangible assets 208,929 136,724

Operating cash flow before changes in operating assets and

liabilities

3,714,933

4,066,648

Changes in operating assets and liabilities 14,329,014 (3,494,453)

Decrease/(increase) in financial assets at amortised cost and

other assets

3,832,373 (14,908,039)

Increase in deposits and other liabilities 10,496,641 11,413,586

Net cash flows from operating activities 18,043,947 572,195

Cash flows from investing activities (5,796,495) (1,170,721)

Proceeds from sale of property, plant and equipment 19,812 14,838

Proceeds from sale of financial assets at fair value through

other comprehensive income

185,994 46,542

Purchase of financial assets at fair value through other

comprehensive income

(200,759) (31,780)

Additions on investment properties - (1,100)

Purchase of property, plant and equipment 13 (2,346,468) (1,173,286)

Purchase of intangible asset 14 (3,455,074) (25,935)

Cash flows from financing activities (1,297,385) 1,383,567

Dividend paid (1,028,967) (616,433)

Proceeds from long term borrowing 1,000,000 2,000,000

Repayment on long term borrowing (1,268,418) -

Net increase in cash and cash equivalents

10,950,067

785,041

Cash and cash equivalents at the beginning of the year 9,378,153 8,593,112

Cash and cash equivalents at the end of the year 20,328,220 9,378,153

Page | 24

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

1. REPORTING ENTITY AND ITS NATURE OF BUSINESS

The People‟s Own Savings Bank is a corporate body established in terms of section 3 of the

People‟s Own Savings Bank of Zimbabwe Act, [Chapter 24:22] of 1999, to provide savings,

Banking and financial services in Zimbabwe. The Bank accepts deposits that will accumulate

interest for the benefit of the depositors and all deposits are government guaranteed.

The Bank‟s head office is at Causeway Building, Corner 3rd Street/Central Avenue, Harare,

Zimbabwe.

2. BASIS OF PREPARATION

2.1 Statement of compliance

The financial statements for the year ended December 31, 2013 have been prepared in

accordance with applicable International Financial Reporting Standards (IFRS) and the

International Financial Reporting Interpretations Committee (IFRIC) interpretations promulgated

by International Accounting Standards Board (IASB) which include standards and interpretations

approved by the IASB, International Accounting Standards (IAS) as well as Standing

Interpretations Committee (SIC) and other relevant statutory requirements.

The Bank‟s financial statements for the year ended December 31, 2013 were authorized for issue

in accordance with a resolution of the directors on 18 March 2014.

2.2 Basis of measurement

The financial statements have been prepared on a historical cost basis except for the following

items:

Financial assets measured at fair value with changes presented in other comprehensive

income,

Investment properties measured at fair value,

Financial assets at amortised cost and

Financial liabilities measured at amortised cost.

2.3 Functional and presentation currency

The Bank‟s financial statements are presented in United States dollar, which is the Bank‟s

functional currency.

2.4 Use of significant accounting judgements, estimates and assumptions

The preparation of the Bank‟s financial statements requires management to make judgements,

estimates and assumptions that affect the reported amounts of income, expenses, assets and

liabilities. However, uncertainty about these assumptions and estimates could result in outcomes

that require a material adjustment to the carrying amount of the asset and liability affected in

future periods.

Page | 25

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

In the process of applying the Bank‟s accounting policies, management has made the following

judgements, estimates and assumptions which have the most significant effect on the amounts

recognized in the financial statements:

2.4.1 Useful lives and residual values of property, plant and equipment

The Bank assesses useful lives and residual values of property, plant and equipment each year

taking into account past experience and technology changes. The depreciation rates are set

out in note 3.7.2 and no changes to these useful lives have been considered necessary during

the year.

2.4.2 Allowances for credit losses

The specific counterparty component of the total allowances for impairment applies to financial

assets evaluated individually for impairment and is based upon management‟s best estimate of

the present value of the cash flows that are expected to be received. In estimating these cash

flows, management makes judgements about a counterparty‟s financial situation and the net

realizable value of any underlying collateral. Each impaired asset is assessed on its merits, and

the workout strategy and estimate of cash flows considered recoverable are independently

approved by the credit risk function.

Collectively assessed impairment allowances cover credit losses inherent in portfolios of loans

and advances and investment securities measured at amortised cost with similar credit risk

characteristics when there is objective evidence to suggest that they contain impaired financial

assets, but the individually impaired items cannot yet be identified.

In assessing the adequacy of provision, both specific and general, the Bank is guided by BASEL II

provisioning guidelines as provided by the Reserve Bank of Zimbabwe which are considered as

minimum requirements. At its discretion, using professional judgement, the Bank may raise

additional provisions over and above those prescribed to ensure adequate provisioning.

Management considers factors such as credit quality, portfolio size, concentrations and

economic factors to assess the need for collective loss allowances. In order to estimate the

required allowance, assumptions are made to define the way inherent losses are modeled and

to determine the required input parameters, based on historical experience and current

economic conditions. The accuracy of the allowances depends on the estimates of future cash

flows for specific counterparty allowances and the model assumptions and parameters used in

determining collective allowances.

Page | 26

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

2.5 New and amended standards and interpretations adopted

The accounting policies adopted are consistent with those of the previous financial year, except

for the following new and amended IFRS and IFRIC interpretations adopted in 2013:

IFRS 9 Financial instruments : Classification and measurement

IFRS 9 is a new standard that forms the first part of a three- part project to replace IAS 39

Financial Instruments: Recognition and Measurement. It applies to classification and

measurement of financial assets and financial liabilities as defined in IAS 39. The adoption of IFRS

9 has an effect on classification and measurement of the Bank‟s financial assets, but has

potentially no impact on classification of financial liabilities. The Bank has assessed the impact

that this standard has on its financial position and performance and has concluded that this has

an effect on classification but not on measurement of financial assets.

IFRS 9 is applicable for accounting periods on or after 1 January 2015, but early adoption is

permitted and the Bank has early adopted this standard.

IFRS 13 Fair value measurement

IFRS 13 replaces guidance on fair value measurement in existing IFRS accounting literature with a

single standard.

The IFRS defines fair value, provides guidance on how to determine fair value and requires

disclosures about fair value measurements. It does not change the requirements regarding

which items should be measured or disclosed at fair value.

IFRS 13 applies where another IFRS requires or permits fair value measurements or disclosures

about fair value measurements. With some exceptions, the standard requires entities to classify

these measurements into a „fair value hierarchy‟ based on the nature of inputs:

• Level 1 - quoted prices in active markets for identical assets or liabilities that the entity can

access at the measurement date;

• Level 2 - inputs other than quoted market prices included within Level 1 that are observable

for the asset or liability, either directly or indirectly; and

• Level 3 - unobservable inputs for the asset or liability.

IFRS 13 is effective for accounting periods beginning on or after January 1, 2013 and the Bank

has adopted it.

2.6 New and amended standards and interpretations not yet effective

Standards issued but not yet effective up to the date of issuance of the Bank‟s financial

statements are listed below. This listing is of standards and interpretations issued, which the Bank

reasonably expects to be applicable at a future date. The Bank intends to adopt those

standards when they become effective.

Page | 27

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

IAS 32 Financial instruments: Presentation – Offsetting financial assets and financial liabilities

Amendments to IAS 32 require entities to disclose gross amounts subject to rights of set-off,

amounts set off in accordance with the accounting standards followed and the related net

credit exposure. This information will help investors understand the extent to which an entity has

set off in its statement of financial position and the effects of rights of set-off on the entity‟s rights

and obligations.

This standard is effective for accounting periods beginning 1 January 2014, however early

adoption is permitted.

IAS 36 Impairment of assets

Amendments to this standard require entities to disclose additional information about fair value

measurement when the recoverable amount of impaired assets is based on fair value less costs

of disposal. Moreover the amendment requires entities to disclose the discount rates used in the

current and previous measurements if the recoverable amount of impaired assets based on fair

value less costs of disposal was measured using a present value technique.

This standard is effective for accounting periods beginning 1 January 2014, however early

adoption is permitted.

3 SIGNIFICANT ACCOUNTING POLICIES

The accounting policies set out below have been applied consistently to all years presented in

the financial statements.

3.1 Inventory

Inventories are measured at the lower of cost and net realizable value. The cost of inventories

comprises all costs of purchase, cost of conversion and other costs incurred in bringing the

inventories to their present location and condition. Net realizable value is the estimated selling

price in the ordinary course of business less estimated costs of completion and the estimated

costs necessary to make the sale.

3.2 Taxation

The Bank is exempted from tax in terms of the Income Tax Act, Chapter 23:06.

Page | 28

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

3.3 Interest income and interest expense

Interest income or expenses are recognized in the statement of profit or loss and other

comprehensive income using the effective interest method. The effective interest rate is the rate

that exactly discounts estimated future cash payments or receipts through the expected life of

the financial asset or financial liability (or where appropriate, a shorter period) to the carrying

amount of the financial asset or financial liability. When calculating the effective interest rate,

the Bank estimates future cash flows considering all contractual terms of the financial instrument,

but not future credit losses.

Transaction costs include incremental costs that are directly attributable to the acquisition or

issue of a financial asset or liability.

Interest income and expense presented in the statement of profit or loss and other

comprehensive income is interest on financial assets and financial liabilities measured at

amortised cost calculated on an effective interest basis.

3.4 Fees and commission income and expense

Fees and commission income and expense that are integral to the effective interest rate on a

financial asset or liability are included in the measurement of the effective interest rate.

The Bank earns fees and commission from a diverse range of services it provides to its customers.

Fees earned for the provision of services over a period of time are accrued over that period of

time.

Loan commitment fees for loans that are likely to be drawn down and other credit related fees,

for example loan establishment fees, are deferred and recognized over the duration of the loan.

When it is unlikely that the loan will be drawn down, the loan commitment fees are recognized

over the commitment period on a straight line basis. Other fees and commission expense relate

mainly to transaction and service fees, which are expensed as the services are received.

3.5 Dividends

Dividend income is recognized when the Bank‟s right to receive income is established. Usually

this is the ex-dividend date for equity securities. The Bank also recognises a liability to make cash

or non-cash dividend distributions to equity holders when the distribution is authorised and

approved by the shareholders. A corresponding amount is recognized directly in equity.

Page | 29

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

3.6 Financial Instruments: Financial assets and liabilities

3.6.1 Classification

The Bank‟s accounting policies provide scope for assets and liabilities at inception into different

accounting categories in certain circumstances.

The Bank has classified its financial assets in the following categories:

Cash and cash equivalents

Financial assets measured at amortised cost and,

Financial assets at fair value through other comprehensive income.

3.6.1.1 Cash and cash equivalents

Cash and cash equivalents include cash and balances with banks, unrestricted balances held

with the Central Bank, unrestricted balances held with other banks and any highly liquid

financial asset used by the Bank in the management of its short term commitments.

3.6.1.2 Financial assets at amortised cost

Financial assets at amortised cost include, loan and advances as well as repurchase agreement

assets.

Loans and advances

Loans and advances include non-derivative financial assets with fixed or determinable

payments that are not quoted in an active market, other than:

Those that the Bank intends to sell immediately or in the near term and those that the

Bank upon initial recognition designates as at fair value through profit or loss.

Those that the Bank, upon initial recognition, designates as available for sale.

Those for which the Bank may not recover substantially all of its initial investment, other

than because of credit deterioration.

After initial measurement, loans and advances are subsequently measured at amortised cost

using the effective interest rate less allowance for impairment. Amortised cost is calculated by

taking into account any discount or premium on acquisition and fees and costs that are an

integral part of effective interest rate. The amortization is included in „Interest income‟.

The Bank reviews its individually significant loans and advances at each statement of financial

position date to assess whether an impairment loss should be recorded in the statement of

comprehensive income.

Page | 30

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

Repurchase agreement assets (Money market investment)

Repurchase agreement assets are non-derivative financial assets with fixed or determinable

payments and fixed maturities, which the Bank has the intention and ability to hold to maturity.

After initial measurement, repurchase agreement assets are subsequently measured at

amortised cost using effective interest rate, less impairment. Amortised cost is calculated by

taking into account any discount or premium on acquisition and fees that are an integral part of

the effective interest rate. The losses arising from impairment of such investments are recognized

in the statement of profit or loss and other comprehensive income.

If the Bank were to sell or reclassify more than an insignificant amount of held to maturity

financial assets before maturity, the entire category would be tainted and would have to be

reclassified as available for sale. Furthermore, the Bank would be prohibited from classifying any

financial assets as held to maturity during the following two years.

3.6.1.4 Financial assets at fair value through other comprehensive income

Equity investments classified as financial assets at fair value through other comprehensive

income are those which are neither classified as held for trading nor designated at fair value

through profit or loss.

At initial recognition, an entity may make an irrevocable election to present in other

comprehensive income subsequent changes in the fair value of an investment in an equity

instrument that is not held for trading.

When the investment is disposed of, the cumulative gain or loss previously recognized in equity is

recognized in the Statement of profit or loss and other comprehensive income in „Other

operating income‟. Where the Bank holds more than one investment in the same security they

are deemed to be disposed of on a first-in-first-out basis. The Bank assesses at each statement of

financial position date whether there is objective evidence that an investment is impaired.

In the case of equity investment classified as financial assets at fair value through other

comprehensive income, objective evidence of impairment include „prolonged‟ or „significant‟

decline in the fair value of the investment below its cost. The Bank treats „significant‟ generally as

40% and prolonged generally as greater than twelve months. When there is evidence of

impairment, the cumulative loss measured as the difference between the acquisition cost and

the current fair value, less any impairment loss on that investment previously recognized in the

statement of other comprehensive income, is removed from equity and recognized in the

statement of profit or loss.

Page | 31

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

Impairment losses on equity investments are not reversed through the statement of profit or loss

and other comprehensive income; increases in fair value after impairment are recognized in

other comprehensive income.

3.6.2 Measuring and determining fair values

IFRS 13 introduces a new definition of fair value as “The price that would be received to sell an

asset or paid to transfer a liability in an orderly transaction between market participants at the

measurement date. The definition provides more clarity on the following:

Fair value is exit price rather than a transaction price (entry price). However, there is a

presumption that the transaction price equal fair value unless there are exceptions like

the transaction is distressed, forced sale or transactions are between related parties.

Fair value is determined at measurement date and it is therefore a current price based

on prevailing market conditions at that date.

The Bank measures fair values using the following fair value hierarchy that reflects the

significance of the inputs used in making the measurements:

Level 1: Quoted market prices (unadjusted) in an active market for an identical

instrument.

Level 2: Valuation techniques based on observable inputs, either directly or indirectly.

This category includes instruments valued using quoted market prices in active markets

for similar instruments; quoted prices for identical or similar instruments in markets that are

considered less than active or other valuation techniques where all significant inputs are

directly or indirectly observable from market data.

Level 3: Valuation techniques using significant unobservable inputs. This category

includes all instruments where the valuation technique includes inputs not based on

observable data and the unobserved inputs have a significant effect on the instrument‟s

valuation. This category includes instruments that are valued based on quoted prices for

similar instruments where significant unobservable adjustments or assumptions are

required to reflect differences between the instruments.

Fair value of financial assets and financial liabilities that are traded in active markets are based

on quoted market prices or dealer price quotations. For all other financial instruments, the Bank

determines fair values using valuation techniques.

Page | 32

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

3.6.3 Impairment of financial assets

The Bank assesses at each statement of financial position date whether there is any objective

evidence that a financial asset or group of financial assets is impaired. A financial asset or a

group of financial assets is deemed to be impaired if, and only if, there is objective evidence of

impairment as a result of one or more events that has occurred after the initial recognition of the

asset (as an incurred „loss event‟) and that loss event or events have an impact on the

estimated future cash flows of the financial asset or the group of financial assets that can be

reliably estimated.

Evidence of impairment may include indications that the borrower or a group of borrowers is

experiencing significant financial difficulty, the probability that they will enter Bankruptcy or

other financial reorganization, default or delinquency in interest or principal payments and

where observable data indicates that there is a measurable decrease in the estimated future

cash flows, such as changes in arrears or economic conditions that correlate with defaults.

3.6.4 De-recognition of financial instruments

A financial asset or where applicable a part of a financial asset or part of a group of similar

financial assets is derecognized when:

The rights to receive cash flows from the asset have expired

The Bank has transferred its rights to receive cash flows from the asset or has assumed an

obligation to pay the received cash flows in full without material delay to a third party

under a „pass through‟ arrangement and either:

The Bank has transferred substantially all the risks and rewards of the asset, or the Bank

has neither transferred nor retained substantially all the risks and rewards of the asset, but

has transferred control of the asset.

When the Bank has transferred its rights to receive cash flows from an asset or has entered into a

pass-through arrangement, and has neither transferred nor retained substantially all the risks and

rewards of the asset nor transferred control of the asset, the asset is recognized to the extent of

the Bank‟s continuing involvement in the asset. In this case, the Bank also recognizes an

associated liability. The transferred asset and the associated liability are measured on a basis

that reflects the rights and obligations that the Bank has retained.

A financial liability is de-recognized when the obligation under the liability is discharged,

cancelled or expires. Where an existing financial liability is replaced by another from the same

Page | 33

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

lender on substantially different terms, or the terms of an existing liability are substantially

modified, such an exchange or modification is treated as a de-recognition of the original liability

and the recognition of the new liability. The difference between the carrying value of the

original financial liability and the consideration paid is recognized in profit or loss.

3.6.5 Re-negotiated loans

Where possible, the Bank seeks to restructure loans rather than to take possession of collateral.

This may involve extending the payment arrangements and the agreement of new loan

conditions. Once the terms have been renegotiated, any impairment is measured using the

effective interest rate as calculated before the modification of terms and the loan is no longer

considered past due. Management continually reviews renegotiated loans to ensure that all

criteria are met and that future payments are likely to occur. The loans continue to be subject to

an individual or collective impairment assessment, calculated using the loan‟s original effective

interest rate.

3.6.6 Off-setting financial instruments

Financial assets and financial liabilities are offset and the net amount is reported in the

statement of financial position if, and only if, there is a currently enforceable legal right to offset

the recognized amounts and there is an intention to settle on a net basis, or to realize the asset

and settle the liability simultaneously.

3.7 Property, plant and equipment

3.7.1 Recognition and measurement

IAS 16 provides entities with the option of accounting for its property, plant and equipment at

revaluation model or cost model subsequent to initial recognition. The revaluation model is a fair

value based model within the scope of IFRS 13. Revalued amount is described as fair value at

the date of the revaluation less any subsequent accumulated depreciation and subsequent

accumulated impairment losses. IAS 16, paragraph 34 still allows an entity to continue with the

policy of determining revalued amounts at regular intervals even after adoption of IFRS 13.

The Bank is only required to apply IFRS 13 if the fair value of a revalued asset differs materially

from its carrying amount. Frequent revaluations are unnecessary for items of property, plant and

equipment with only insignificant changes in fair value. As such, the Bank‟s items of property,

plant and equipment are measured at cost less accumulated depreciation and accumulated

impairment losses. Cost includes expenditures that are directly attributable to the acquisition of

the asset. The cost of self-constructed assets includes the cost of raw materials and direct labour,

any other costs directly attributable to bringing the assets to a working condition for their

Page | 34

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

intended use, the costs of dismantling and removing the items and restoring the site on which

they are located and capitalized borrowing costs. Purchased software that is integral to the

functionality of the related equipment is capitalized as part of that equipment. When parts of an

item of property, plant and equipment have different useful lives, they are accounted for as

separate items of property, plant and equipment.

The gain or loss on disposal of an item of property, plant and equipment is determined by

comparing the proceeds from disposal with the carrying amount of the item of property, plant

and equipment, and is recognized in the statement of profit or loss and other comprehensive

income.

3.7.2 Depreciation

Depreciation is recognized in the statement of profit or loss and other comprehensive income on

a straight line basis over the estimated useful lives of each part of item of property, plant and

equipment since this most closely reflects the expected pattern of consumption of the future

economic benefits embodied in the asset.

The estimated useful lives are as follows:

Motor Vehicles 5 years

Computer Equipment 3 years

Furniture, Fittings and Fixtures 10 years

Office Equipment 4 years

Buildings 40 years

Land is not depreciated. Depreciation methods, useful lives and residual values are re-assessed

at each reporting date and adjusted if appropriate.

3.7.3 Reclassification to investment property

When the use of property changes from owner-occupied to investment property, the property is

re-measured to fair value and re-classified as investment property. Any gain arising on re-

measurement is recognized in the statement of profit or loss and other comprehensive income

to the extent that it reverses a previous impairment loss on the specific property, with any

remaining gain recognized in other comprehensive income and presented in revaluation

reserve in equity. Any loss is recognized immediately in the statement of profit or loss and other

comprehensive income.

Page | 35

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

3.7.4 Subsequent costs

The cost of replacing a component of an item of property and equipment is recognized in the

carrying amount of the item if it is probable that the future economic benefits embodied within

the part will flow to the Bank and its cost can be measured reliably. The carrying amount of the

replaced part is derecognized. The costs of the day to day servicing of property, plant and

equipment are recognized in the statement of profit or loss and other comprehensive income.

3.8 Investment properties

Investment properties are properties held either to earn rental income or for capital

appreciation or for both, but not for sale in the ordinary course of business, use in production or

supply of goods or services or for administrative purposes.

Investment properties are measured initially at cost, including transaction costs. Subsequent to

initial recognition, investment properties are stated at fair value, which reflect market conditions

at the reporting date. Gains and losses arising from changes in the fair values of investment

properties are included in the statement of profit or loss and other comprehensive income in the

period in which they arise. Fair values are evaluated annually by an accredited external,

independent valuer, applying a valuation model recommended by the International valuation

standards committee.

Investment properties are derecognized when either they have been disposed of or when the

investment property is permanently withdrawn from use and no future economic benefit is

expected from its disposal. The difference between the net disposal proceeds and the carrying

amount of the asset is recognized in the statement of profit or loss and other comprehensive

income in the period of de-recognition.

Transfers are made to or from investment property only when there is a change in use. For a

transfer from investment property to owner-occupied property, the deemed cost for subsequent

accounting is the fair value at the date of change in use. If owner-occupied property becomes

an investment property, the Bank accounts for such property in accordance with the policy

stated under property and equipment up to the date of change in use.

3.9 Intangible assets - computer software

An intangible asset is recognized only when its cost can be measured reliably and it is probable

that the expected future economic benefits that are attributable to it will flow to the Bank.

Software acquired separately is measured on initial recognition at cost. Following initial

Page | 36

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

recognition, it is carried at cost less any accumulated amortization and accumulated

impairment losses.

The useful lives of intangible assets are assessed as either finite or infinite. The Bank only has

intangible assets with finite useful lives. These assets are amortised over the useful economic life

and assessed for impairment whenever there is an indication that the intangible asset may be

impaired. The amortization period and the amortization method for an intangible asset with a

finite useful life are reviewed at least at the end of each reporting period. Changes in the

expected useful life or the expected pattern of consumption of future economic benefits

embodied in the asset is accounted for by changing the amortization period or method, as

appropriate, and are treated as changes in accounting estimates. The amortization expense on

intangible assets with finite lives is recognized in the statement of profit or loss and other

comprehensive income.

Amortisation is recognized in the statement of profit or loss and other comprehensive income on

a straight line basis over the useful life of the software, from the date it is available for use since

this most closely reflects the expected pattern of consumption of the future economic benefits

embodied in the asset.

Amortisation methods, useful lives and residual lives are reviewed at each financial year-end

and adjusted if appropriate. The estimated economic useful life applied is as follows:

Ethix core banking system 10 years

Other software (Risk and Treasury) 10 years

3.10 Provisions

A provision is recognized if, as a result of a past event, the Bank has a present legal or

constructive obligation that can be estimated reliably, and it is probable that an outflow of

economic benefits will be required to settle the obligation and reliable estimate can be made

of the amount of the obligation. The expenses relating to any provision is presented in the

statement of profit or loss and other comprehensive income.

3.11 Employee benefits

3.11.1 Defined benefit plans

A defined benefit plan is a post-employment benefit plan other than a defined contribution

plan. The Bank‟s net obligation in respect of defined benefit pension plans is calculated by

estimating the amount of future benefit that employees have earned in return for the service in

Page | 37

PEOPLE’S OWN SAVINGS BANK

Notes to the financial statements

For the year ended December 31, 2013

the current and prior periods; that benefit is discounted to determine its present value. Any

unrecognized past service costs and the fair value of any plan assets are deducted.

3.11.2 Termination benefits

Termination benefits are recognized as an expense when the Bank is committed demonstrably,

without realistic possibility of withdrawal, to a formal detailed plan to either terminate

employment before the normal retirement date, or to provide termination benefits as a result of

an offer made to encourage voluntary redundancy. Termination benefits for voluntary

redundancies are recognized if the Bank has made an offer of voluntary redundancy, it is

probable that the offer will be accepted, and the number of acceptances can be estimated

reliably.

3.11.3 Short term employee benefits

Short term employee benefit obligations are measured on an undiscounted basis and are

expensed as the related service is provided. A liability is recognized for the amount expected to

be paid under short-term cash bonus if the Bank has a present legal or constructive obligation to

pay this amount as a result of past service provided by the employee and the obligation can be

estimated reliably.

3.12 Share capital and reserves

3.12.1 Share capital

The Bank‟s authorized share capital is determined by the board which can increase or decrease