annual report 2005 - grenada co-op · pdf filetropicana inn conference room, ... making...

TRANSCRIPT

ANNUAL REPORT 2005

Grenada Co-operative Bank LimitedThere for all the people...all the time.

GRENADA CO-OPERATIVE BANK LIMITED

2 Annual Report 20052 Annual Report 2005

Annual Report and Financial Statements

September 30, 2005(expressed in Eastern Caribbean dollars)

To be the Leading Grenadian provider of

high quality financial and related services to

individuals and organisations in local

and international markets, maximizing

benefits for all Stakeholders

MISSION STATEMENT

3Annual Report 2005 3Annual Report 2005

Corporate Information 4

Notice/Agenda of Annual Meeting 5

Chairman’s Review 6-7

General Manager’s Report 8-13

Management Team 14-15

Board of Directors 16

Selected Financial Statistics 17

Auditors’ Report to the Shareholders 18

Balance Sheet 19

Statement of Changes in Equity 20

Statement of Income 21

Statement of Cash Flows 22

Notes to the Financial Statements 23-35

GRENADA CO-OPERATIVE BANK LIMITED

4 Annual Report 2005

Established 1932

Church Street, St. George’s , and

Branches at Grenville, Sauteurs and Spiceland Mall

Directors

C.A. St. Bernard, Esq., C.B.E., Q.C. - Chairman

Gordon V. Steele, Esq.

Derick Steele, Esq.

Richard Mc Intyre, Esq.

Lethon Herry, Esq.

Leslie Ramdhanny, Esq.

Darryl Brathwaite, Esq.

Manager/Secretary

Gordon V. Steele, Esq.

Auditors

Messrs. PricewaterhouseCoopers

Chartered Accountants

Solicitors

Messrs. Lewis & Renwick

A Member bank of the Caribbean Association of Indigenous Banks

5Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

Notice of Annual Meeting

Notice is hereby given that the Seventy-third Annual Meeting of the Company will be held at theTropicana Inn Conference Room, Lagoon Road, St. George’s, on Monday 30 January, 2006 at 4:45p.m.

AGENDA

1. To receive the audited financial statements for the year ended September 30, 2005 , together with the Chairman’s Review and General Manager’s Report thereon.

2. To announce a dividend for the year ended September 30, 2005.

3. To elect Directors.

4. To appoint auditors for the ensuing year. (Messrs. PricewaterhouseCoopers are due toretire and are eligible for re-appointment).

5. To consider any other business which may be given consideration at an annual meeting.

By order of the Board of Directors

Gordon V. SteeleSecretaryNovember 29, 2005

GRENADA CO-OPERATIVE BANK LIMITED

6 Annual Report 2005

THE ECONOMY

Rebuilding postHurricanes Ivan andEmily remained themain pre-occupation ofeconomic planners andbusiness leaders in2005. Fuelled primarilyby rebuilding of thehousing stock, growthin the constructionsector climbed to 30%,propelling real GDPgrowth to an estimated1.9%.

THE BANKING & FINANCIALSERVICES ENVIRONMENT

As players continue to improve theircompetitiveness, consumers enjoy commensuratebenefits of lower lending rates and better service. Atthe same time it is now very obvious that theeffective regulation of the sector ought not to bedelayed.

The New Banking Act, aimed at strengthening thestability of the banking sector having passed throughboth Houses of Parliament is expected to be passedinto law in 2006.

Also expected in 2006 is the passage of legislation toestablish the Grenada Authority for the Regulation ofFinancial Institutions.

Listings and trading on the Eastern CaribbeanSecurities Exchange and the Regional GovernmentSecurities Market continue to reflect positivedevelopments.

Compared with 2004, this year reflected lessbuoyancy in the level of activities in the bankingsector. Eastern Caribbean Central Bank statisticsshow that between September 2004 and September2005, loans and advances grew by 3.9% (2004:5.4%) while deposits expanded by 7.7% (2004: 12%).

BANK’S PERFORMANCE

Continuing the trend from previous years, the Bank,in 2005, produced commendable growth in assetsemployed and increased profits. Total assets of theBank have grown by $59.2m or 23% in 2005, animprovement over the $36.8m or 16% achieved in2004. For 2005 Income before Tax amounted to$5,637,693 - an improvement over the $4,037,225attained in 2004.

FUTURE PROSPECTS

An already difficult economic situation has beenexacerbated by rising oil prices. While thestrengthening of the global economy is good news,rising interest rates in the United States is not.Though commendable, the recent debt restructuringmust be accompanied by other restructuringmeasures to place the economy and the publicfinance on a sounder footing. In the final analysis oureventual recovery depends on the skill andcommitment of our people in forging and vigorouslyimplementing a strategy that is cohesive, transparentand all-inclusive.

ROAD MAP TO ENHANCEDCORPORATE GOVERNANCE

Corporate governance has to do with the overallcontrol of activities in a corporation. It is concernedwith the long-term objectives and plans and theproper management structure to achieve them. Italso entails making sure that the structure functionsto maintain the corporate integrity, reputation andresponsibility to various stakeholders.

Our Board continues to build a commitment fordeveloping systems, policies and guidelines whichwill redound to long term efficiency, and effectivecontrol functions.

In June 2005 the Bank’s directors attended theDirectors and Chairperson training seminar held inSt. Lucia, organized by the Eastern CaribbeanSecurities Exchange. In the near term the Board willfocus on:-

CHAIRMAN'S REVIEW

C.A. St. Bernard, Esq., C.B.E.,Q.C., Chairman

7Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

i. Building directors’ capacity through directortraining

ii. Developing and utilizing formal assessmentinstruments to evaluate its own performance

iii. Implementing a formal system for the evaluationof senior managers’ performance

iv. Developing and utilizing formal assessmentinstruments to evaluate the ManagementControls for attaining the objectives in thestrategic plan.

FOLLOW-UP ON UNAUTHORIZEDTRANSACTIONS

The discovery of certain unauthorized transactionswas reported in 2004. Internal investigations, withthe assistance of external forensic auditors werecarried out in 2004/2005. The loss is $1.7m, all ofwhich has been accounted for.

British Solicitors Messrs. Thompson Snell &Passmore have been retained by the bank to assessthe potential for recovery of these amounts.

Additional controls have been implemented and are

CHAIRMAN'S REVIEW

regularly monitored to prevent further occurrences.

DIVIDEND POLICY

Given the performance of the Bank this year, the directors recommend a dividend of $0.14 per share. Thisamounts to $714,000.

The annexed Statement of Changes in Equity shows that: -

$

The net income for the Year amounts to 4,594,693

To which has been added Retained Earnings at the beginning of the Year 5,702,935

10,297,628

From which has been transferred to Statutory Reserves 918,939

Making available for distribution a total sum of 9,378,689

This amount the Directors recommend should be allocated as follows: -

To payment of dividends: 714,000

Retained Earnings at the end of the year 8,664,689

ACKNOWLEDGEMENTS

I would like to convey my sincerest appreciation and gratitude to my colleague directors whose dedicationcontinues to add value to our efforts at strengthening the bank and ensuring its sustained success. Tomanagement and staff I say thanks, on behalf of the Board, for your continued hard work and enthusiasm inadvancing the plans and programmes of the Bank.

C. A. St. Bernard

.........................................................

Chairman

BANK’S PERFORMANCE

Assets andLiabilities

Once again the Bank hasturned in quite animpressive performance.Despite the challengesposed by a recoveringeconomy, the Bank’sresults for asset growthand profits were betterthan 2004.

Stronger than last year,Assets employedrecorded a 23% or$59.2m expansion –(2004: 16% or $36.8m).

Growth in Customer Loans and Advances(gross) has been less buoyant than in 2004. Loansand Advances grew by $44.5m or 23.6% in 2005compared with $45.9m or 32.2% in 2004. LoanPortfolio growth is evidenced mainly in MortgageLoans which increased by $45.7m or 31% to$194.1m.

Some $1.1m was invested in Fixed Assets, mainlyinformation technology. To enhance customerservice, a new ATM was commissioned at the NISBuilding on Melville Street.

Total Customer Deposits displayed strongbuoyancy in 2005, expanding by $47.3m or 20%.The Bank’s deposit base now stands at $282.1m.Savings Deposits had a strong performanceclimbing some $14.8m or 15%. Strong growth wasalso attained in respect of Fixed Deposits ($14.8mor 15%); Current Accounts ($8.3m or 111%).

Income and Expenses

Ongoing application of sound Asset Liabilitymanagement strategies continue to impact positivelyon the Bank’s profitability. Net income after taxes for2005 amounted to $4.6m representing a $1.3m or39% increase over last year’s performance. Net aftertax earnings per share is at $0.90, a $0.25 or 38%increase over last year’s $0.65.

Due to the improved Asset Liability management,the ratio of interest earned to interest paid rose from2.63 in 2004 to 2.69 in 2005.

Interest income on Customer Loans and Advances in2005, rose by $4.1m (24%) climbing to $21.2m. Theinterest on investments and deposits held with otherbanks rose marginally to $3.5m, increasing by 4.6%or $157,632.

During 2005, interest expense rose by $1.4m or 17%.Non-interest expenses rose from $10.9m in 2004 to$12.3m in 2005, an increase of 13%.

GRENADA CO-OPERATIVE BANK LIMITED

8 Annual Report 2005

Assets EmployedIn Millions of EC Dollars

2001 - 2005

GENERAL MANAGER'S REPORT

Gordon V. Steele, Esq.,General Manager

9Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

Loans & Advances(gross)

In Millions of EC Dollars2001 - 2005

DepositsIn Millions of EC Dollars

2001 - 2005

INCOME AFTER TAXES2001 - 2005

GENERAL MANAGER'S REPORT

HUMAN RESOURCEDEVELOPMENT

As the financial landscape changes rapidly,institutional strengthening through the building andenhancing of skills and abilities of our staff arepivotal to the long-term success of the Bank.

The Bank maintained its focus on employeedevelopment by retaining a balanced programme ofactivities in training, professional development andthe socializing among the staff.

Training…

The Bank continues to strive towards being alearning organization, with all training geared atpersonal development and enhanced bankperformance.

Some 40% of the staff members have undergonevarious forms of soft skills training during the yearviz Workplace Ethics, Art of Selling, and LeadershipStrengthening.

Further, 21% of the staff participated in technicaltraining, such as Insurance for Financial ServiceSector, Principles of Fraud, Risk Management &Basel II, Corporate Credit Appraisal Techniques,Corporate Credit Assessment, Debt Collection,among others.

Staff continue to pursue professional development

programmes with tertiary level institutions.Approximately 20% of the staff are also enrolled insuch programmes as the Associateship andFellowship programmes with the Institute of

Canadian Bankers, theB.Sc. ManagementStudies with theUniversity of the WestIndies and theDiploma in ProjectManagement with theInstitute of Business &Technology Inc. (St.Lucia).

Mrs. Hazel John andMr. Charmie Shearshave qualified asCertified ResidentialUnderwriters with theReal Estate Institute ofCanada.

On-line internetTraining, provided by

the US Graduate School of Banking of Wisconsin, is abudding tool for continuous training anddevelopment of staff members. This year, nine (9)employees who are Senior Managers and CreditOfficers, participated in Credit Risk ManagementTraining facilitated by the Graduate School ofBanking On-line Seminars.

Mrs. Ladyclair Noel and Ms. Ebernie Whyte both of

GRENADA CO-OPERATIVE BANK LIMITED

10 Annual Report 2005

Employees attending the Art of Selling Training, facilitated by La Touche & La Touche Consultancy.

Loans Officers: L to R: HazelWells-John, CRU and

Charmie Shears, AICB, CRU

L to R: Mrs. Ladychair Noel, AICB, andEbernie Whyte, AICB

GENERAL MANAGER'S REPORT

the Sauteurs Branch have completed the Institute ofCanadian Bankers’ Associateship programme. Theyjoin the 15% of the staff who are Associates of theInstitute of Canadian Bankers.

The Staff Christmas Cocktail replaced the usualAnnual Staff Banquet and Awards Ceremony, as theBank gave full consideration to the challenges of

Hurricane Ivan among others, which had impactedon employees and the institution as a whole.

The 2005 Family Fun Day staged in March at theVictoria Park, Grenville, was dubbed “the best ever”.Employees and their families engaged in obstacleraces, track and field competition and cricketmatches among other activities.

The Bank remains fully committed to fostering thekind of wholesome environment that all employeeswill enjoy working in, and from which customers willgain positive returns when doing business with us.

COMMUNITY OUTREACH

In 2005 the Bank continued to embrace its role as agood corporate citizen. Educational development hasalways been an area of emphasis and this year wecontinued to devote resources to support several on-going programs.

These include the following:

“Co-op Bank Julien Fédon Memorial Award”- Since 2001 in collaboration with the University ofthe West Indies and the Institute for People’sEnlightenment, the Bank has sponsored this highlycoveted award. This year the ‘Co-op Bank JulienFédon Memorial Award’ was presented to Dr. RonSookram, who is the fourth recipient and the secondGrenadian to have won this prestigious prize.

For the fourth year running, the Grenada BarAssociation (GBA) held its annual “Sir ArchibaldNedd Memorial Lecture” with the support of theBank. This year featured Hon. Mia Mottley Q.C.,Deputy Prime Minister and Attorney-General ofBarbados. Hon. Mia Mottley Q.C. delivered ascintillating lecture on the topic “The Relevance ofInsurance in Modern Caribbean Society: A criticallook at the insurance industry post Hurricane Ivan”.

Sports and Youth Development are two other areas

11Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

Men 400m relay brought out the athletic abilitiesof some of the male staff. Everyone enjoyed the famous “Musical Chairs”.

L to R: Mrs. Samantha Ince-John, Marketing Officer of theBank presenting certificate to Dr. Ron Sookram,

Julien Fedon Memorial Award winner.

GENERAL MANAGER'S REPORT

where the Bank places emphasis and has extended continued support.The Bank has been the title sponsor of the Grenada Union of Teachers(G.U.T) Primary School Athletic Championships in St. Andrew’s andSt. Patrick’s for the second consecutive year and is proud to beinvolved in the nurturing and development of these fledgling athletes.

The Bank was pleased to demonstrate its commitment to theperforming arts through its sponsorship of the musical play “Ay YaYai Ivan”. The play was first staged a mere three months followingHurricane Ivan whilst many of the performers, as well as the vastmajority of the population, still had no electricity or water and were‘under tarpaulin’ in damaged homes. A repeat performance was stagedin August 2005 and it has commenced a North American tour.

CONCLUSIONS

Like many others, our team faces what is emerging to be a difficult andchallenging environment. However, having regards for the plannedprograms, our strengths and capabilities, the Board of Directors isoptimistic that we can successfully build on the achievements of 2005.

GRENADA CO-OPERATIVE BANK LIMITED

12 Annual Report 2005

L to R: Mr. Gordon V. Steele, General Manager, Grenada Co-operative Bank Ltd., Hon. Mia Mottley Q.C., Deputy Prime Ministerand Attorney-General of Barbados and Mr. Ruggles Ferguson, president, Grenada Bar Association.

GENERAL MANAGER'S REPORT

Mr. Alleyne Francique, World 400mChampion presenting trophy to

an outsanding athelete at theSt. Andrew’s Games.

ELECTION OF DIRECTORS AND APPOINTMENT OF AUDITORS

The directors retiring are Messrs. C.A. St. Bernard and Leslie Ramdhanny, who being eligible, offerthemselves for re-election.

The retiring auditors, Messrs PricewaterhouseCoopers, Chartered Accountants, offer themselves for re-appointment.

APPRECIATION

On behalf of the Board of Directors and myself I wish to place on record our appreciation of the services ofthe Management and staff for their devotion to duty and hard work during the year under review.

Gordon V. Steele

General Manager

13Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

GENERAL MANAGER'S REPORT

GRENADA CO-OPERATIVE BANK LIMITED

14 Annual Report 2005

Gordon V. Steele, Esq.,Managing Director

Floyd Dowden, AICB,Manager,

Banking Operations

Richard Duncan, B.Sc., M.A.,CGA, AICB, Manager

Finance & Corporate Affairs

Julia Lawrence, B.S., MBA-IBF, Internal Auditor

Florence Williams, B.S.,Manager, Credit

Mondelle Squires-Francis,B.Sc., Human Resources

Officer

Peter Antoine, B.Sc., AICB,Senior Programme &

Research Officer

THE

MANAGEMENT

TEAM

Samantha Ince-John, B.Sc.,Marketing Officer

David Flemming, Senior Information Technology Officer

Shane Regis, AICB, Senior Operations Officer

Cynthia Davidson,Branch Manager,

Spiceland Mall

Ann Williams, Branch Manager,

Grenville

Denby De Freitas, Credit Consultant

Clifford Bhola, AICB,Branch Manager, Sauteurs

Jennifer Gulston-Gittens, B.S.,Senior Credit Officer

THE

MANAGEMENT

TEAM

15Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

C.A. St. Bernard, Esq., C.B.E.,Q.C., Chairman

Gordon V. Steele, Esq.,General Manager/Managing Director

Derick Steele, Esq. Richard Mc Intyre, Esq.

Lethon Herry, Esq. Leslie L. Ramdhanny, Esq. Darryl Brathwaite, Esq.

BOARD OFDIRECTORS

GRENADA CO-OPERATIVE BANK LIMITED

16 Annual Report 2005

17Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

GRENADA CO-OPERATIVE BANK LIMITED

Auditors’ Report

18 Annual Report 2005

November 29, 2005

Auditors’ Report

To the Shareholders ofGrenada Co-operative Bank Limited

We have audited the accompanying balance sheet of Grenada Co-operative Bank Limited as ofSeptember 30, 2005 and the related statements of changes in equity, income and cash flows for theyear then ended. These financial statements are the responsibility of the bank’s management. Ourresponsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with International Standards on Auditing. Those standardsrequire that we plan and perform the audit to obtain reasonable assurance about whether thefinancial statements are free of material misstatement. An audit includes examining, on a test basis,evidence supporting the amounts and disclosures in the financial statements. An audit also includesassessing the accounting principles used and significant estimates made by management, as well asevaluating the overall financial statement presentation. We believe that our audit provides areasonable basis for our opinion.

In our opinion, the financial statements present fairly, in all material respects, the financial position ofthe bank as of September 30, 2005 and the results of its operations and its cash flows for the yearthen ended in accordance with International Financial Reporting Standards.

PricewaterhouseCoopersChartered Accountants

GRENADA CO-OPERATIVE BANK LIMITED

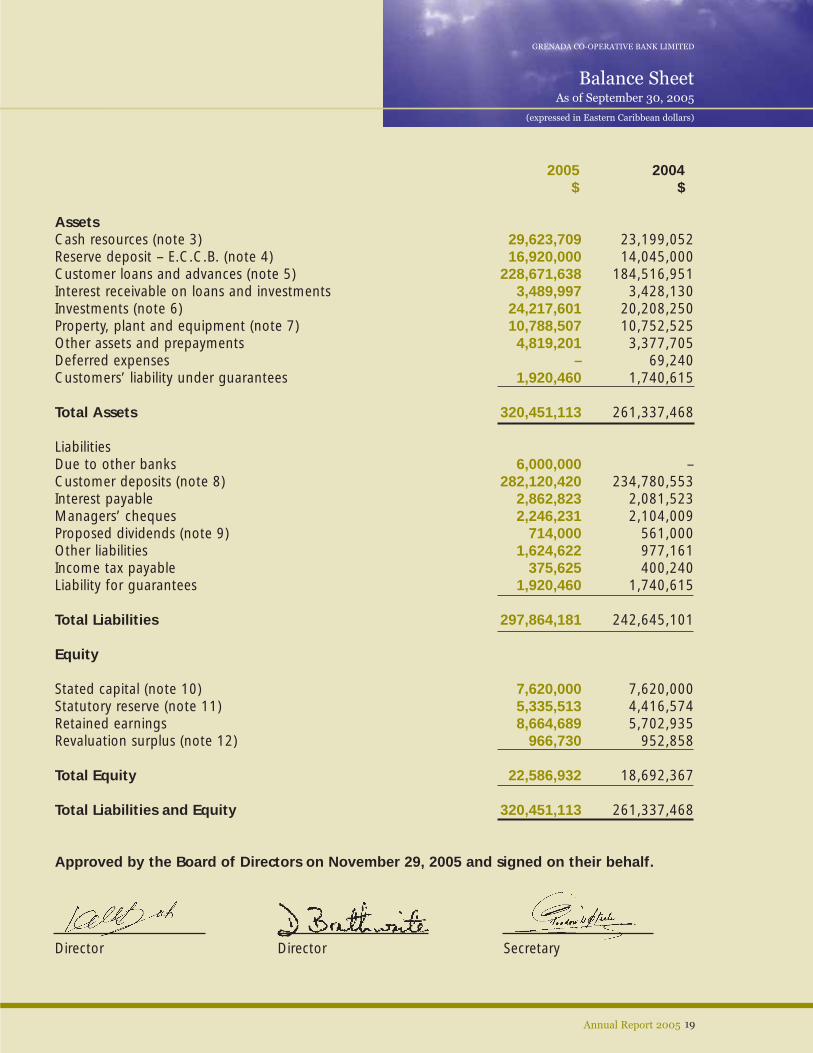

Balance SheetAs of September 30, 2005

(expressed in Eastern Caribbean dollars)

19Annual Report 2005

2005 2004$ $

AssetsCash resources (note 3) 29,623,709 23,199,052Reserve deposit – E.C.C.B. (note 4) 16,920,000 14,045,000Customer loans and advances (note 5) 228,671,638 184,516,951Interest receivable on loans and investments 3,489,997 3,428,130Investments (note 6) 24,217,601 20,208,250Property, plant and equipment (note 7) 10,788,507 10,752,525Other assets and prepayments 4,819,201 3,377,705Deferred expenses – 69,240Customers’ liability under guarantees 1,920,460 1,740,615

Total Assets 320,451,113 261,337,468

LiabilitiesDue to other banks 6,000,000 –Customer deposits (note 8) 282,120,420 234,780,553Interest payable 2,862,823 2,081,523Managers’ cheques 2,246,231 2,104,009Proposed dividends (note 9) 714,000 561,000Other liabilities 1,624,622 977,161Income tax payable 375,625 400,240Liability for guarantees 1,920,460 1,740,615

Total Liabilities 297,864,181 242,645,101

Equity

Stated capital (note 10) 7,620,000 7,620,000Statutory reserve (note 11) 5,335,513 4,416,574Retained earnings 8,664,689 5,702,935Revaluation surplus (note 12) 966,730 952,858

Total Equity 22,586,932 18,692,367

Total Liabilities and Equity 320,451,113 261,337,468

Approved by the Board of Directors on November 29, 2005 and signed on their behalf.

Director Director Secretary

20 Annual Report 2005

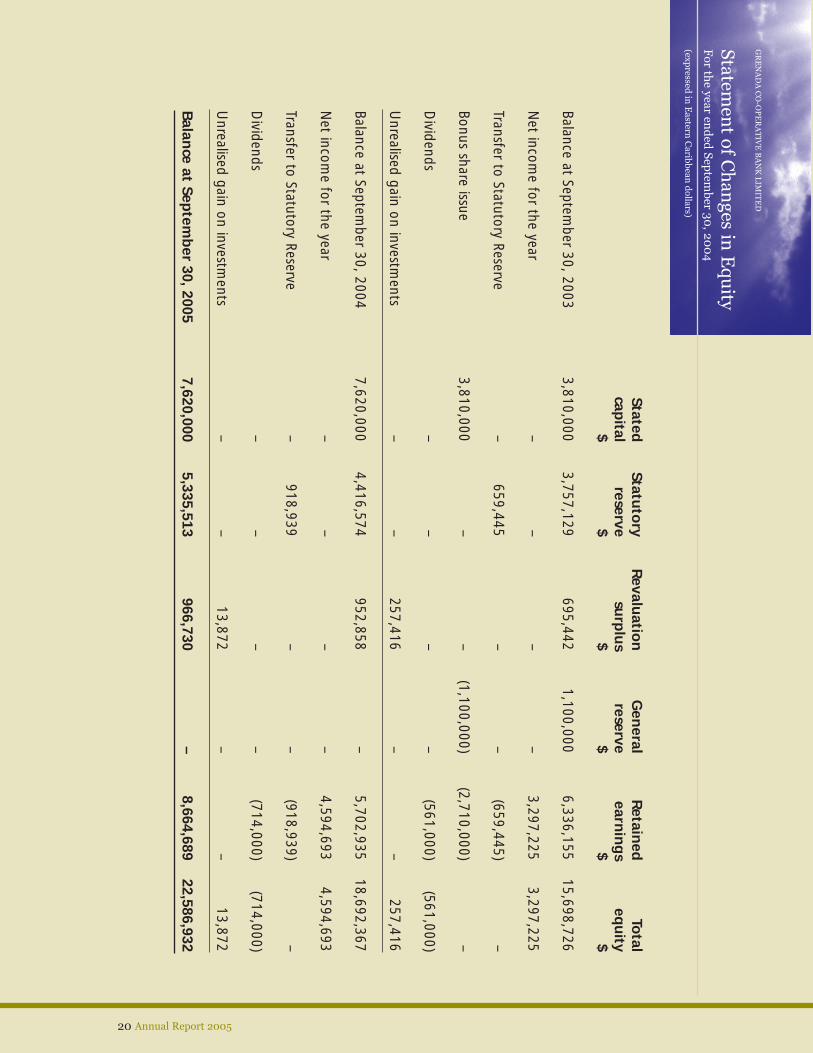

StatedStatu

tory

Revalu

ation

Gen

eral R

etained

Total

capital

reservesu

rplu

sreserve

earnin

gs

equ

ity$

$$

$$

$

Balance at September 30, 2003

3,810,0003,757,129

695,4421,100,000

6,336,15515,698,726

Net incom

e for the year–

––

–3,297,225

3,297,225

Transfer to Statutory Reserve–

659,445–

–(659,445)

–

Bonus share issue3,810,000

––

(1,100,000)(2,710,000)

–

Dividends

––

––

(561,000)(561,000)

Unrealised gain on investm

ents–

–257,416

––

257,416

Balance at September 30, 2004

7,620,0004,416,574

952,858–

5,702,93518,692,367

Net incom

e for the year–

––

–4,594,693

4,594,693

Transfer to Statutory Reserve–

918,939–

–(918,939)

–

Dividends

––

––

(714,000)(714,000)

Unrealised gain on investm

ents–

–13,872

––

13,872

Balan

ce at Septem

ber 30, 2005

7,620,0005,335,513

966,730–

8,664,68922,586,932

GR

EN

AD

A C

O-O

PE

RA

TIV

E B

AN

K L

IMIT

ED

Statemen

t of Ch

anges in

Equ

ityF

or the year en

ded

Septem

ber 30, 20

04

(expressed

in E

astern C

aribbean d

ollars)

GRENADA CO-OPERATIVE BANK LIMITED

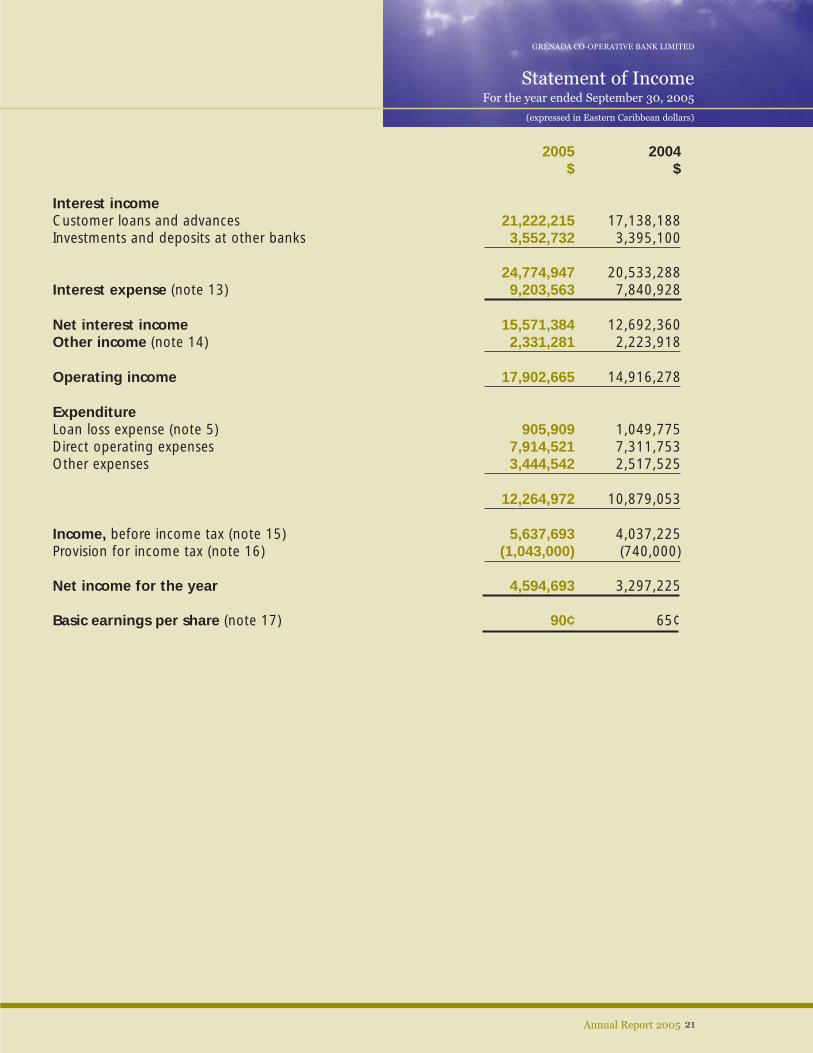

Statement of IncomeFor the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

21Annual Report 2005

2005 2004$ $

Interest incomeCustomer loans and advances 21,222,215 17,138,188Investments and deposits at other banks 3,552,732 3,395,100

24,774,947 20,533,288Interest expense (note 13) 9,203,563 7,840,928

Net interest income 15,571,384 12,692,360Other income (note 14) 2,331,281 2,223,918

Operating income 17,902,665 14,916,278

ExpenditureLoan loss expense (note 5) 905,909 1,049,775Direct operating expenses 7,914,521 7,311,753Other expenses 3,444,542 2,517,525

12,264,972 10,879,053

Income, before income tax (note 15) 5,637,693 4,037,225Provision for income tax (note 16) (1,043,000) (740,000)

Net income for the year 4,594,693 3,297,225

Basic earnings per share (note 17) 90¢ 65¢

2005 2004$ $

Cash flows from operating activitiesIncome before income tax 5,637,693 4,037,225

Items not affecting working capitalDepreciation 1,116,449 1,154,612Loss on disposal of property, plant and equipment 3,380 –

Operating profit before working capital changes 6,757,522 5,191,837

Net changes in operating assets and liabilities:Interest receivable and prepayments (1,503,363) (1,505,515)Customer loans and advances (44,154,687) (45,317,561)Customer deposits 47,339,867 33,743,929Interest payable 781,300 (492,787)Other liabilities 789,683 149,574Deferred expenses 69,240 90,794Due to other banks 6,000,000 –

16,079,562 (8,139,729)Net income tax paid (1,053,745) (396,308)

Net cash from/(used in) operating activities 15,025,817 (8,536,037)

Cash flows from investing activitiesPurchase/(sale) of investments (4,009,351) 402,101Purchase of property, plant and equipment (1,162,759) (998,479)Proceeds from sale of property, plant and equipment 6,950 –Increase in reserve deposit – E.C.C.B. (2,875,000) (1,945,000)

Net cash used in investing activities (8,040,160) (2,541,378)

Cash flows used in financing activitiesDividends paid (561,000) (557,400)

Net change in cash and cash equivalents 6,424,657 (11,634,815)

Cash and cash equivalents – beginning of year 23,199,052 34,833,867

Cash and cash equivalents – end of year (note 18) 29,623,709 23,199,052

GRENADA CO-OPERATIVE BANK LIMITED

Statment of Cash FlowsFor the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

22 Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

1 Incorporation and principal activity

The Bank was incorporated on July 26, 1932, and continued under the laws of Grenada. It isengaged in the business of banking. The registered office is situated on Church Street, St.George’s.

The bank employed 92 persons during the year (2004– 84 persons).

2 Significant accounting policies

a) Basis of accounting

These financial statements comply with International Financial Reporting Standards and areprepared under the historical cost convention except for land and buildings and certainavailable for sale investments which are at valuation.

b) Depreciation

Depreciation on property, plant and equipment is provided at the following rates, which areexpected to write off the cost or valuation of the assets over the period of their estimateduseful lives.

The annual rates used are as follows:-Furniture and equipment 10%Computer equipment 16 2/3%Motor vehicles 20%Freehold buildings 2 1/2%

Leasehold improvements are amortised over the term of the lease.

Maintenance and repairs to buildings are charged to current operations and the cost ofimprovements are capitalised where such improvements would extend the remaining usefullife of the building.

The cost or valuation of property, plant and equipment replaced, retired or otherwise disposedof and the accumulated depreciation thereon are eliminated from the accounts and theresulting gain or loss reflected in the statement of income.

c) Provision for loan losses

Specific allowances are made against loans and advances where in the opinion ofManagement, after detailed appraisal of the loans portfolio, recovery is doubtful. Guidelinesissued by the Eastern Caribbean Central Bank are followed in this regard. Bad debts arewritten off against the provision when the extent of the loss is confirmed.

d) Revenue Recognition

The Bank classifies loans as non-productive when the loans have not been serviced for aperiod in excess of three months. No accrual is made for interest receivable on such loans.

23Annual Report 2005

Notes to Financial Statements For the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

2 Significant accounting policies …Continued

e) Foreign currencies

Assets and liabilities denominated in foreign currencies are translated to E.C. dollars at therates of exchange ruling at the end of the financial year. Transactions arising during the yearinvolving foreign currencies have been converted at the rates prevailing on the dates thetransactions occurred. Differences arising from fluctuations in exchange rates are included inthe statement of income.

f) Taxation

The company provides for income tax payable in accordance with Income Tax Act of 1994, asamended.

Deferred tax is provided where material, using the liability method at rates expected to applywhen settled or paid.

g) Investments

Debt and equity investments held for short-term liquidity purposes and or intended to be heldfor an indefinite period of time, which may be sold in response to needs for liquidity orchanges in interest rates are classified as available-for-sale. Investments with a fixed maturitywhere management has both the intent and the ability to hold to maturity are classified asheld-to-maturity and are carried at amortised cost. Equity investments are initially carried atcost and are subsequently remeasured at fair value. The unrealized gains or losses oninvestments are accounted for on the balance sheet as part of the revaluation surplus. Wherethe fair value of an equity investment cannot be reliably measured, the investment ismeasured at cost.

h) Pension

The Bank’s contributions to its Defined Contribution Pension Plan are charged to the incomestatement in the year to which they relate.

i) Cash and cash equivalents

For purposes of the cash flow statement, cash and cash equivalents comprise cash balances,deposits with the E.C.C.B. other than reserve deposit and amounts on deposit with otherbanks and other financial institutions.

j) Dividends

Dividends are recognised in equity in the period in which they are declared by the Directors.

GRENADA CO-OPERATIVE BANK LIMITED

24 Annual Report 2005

Notes to Financial StatementsFor the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

GRENADA CO-OPERATIVE BANK LIMITED

3 Cash resources

2005 2004$ $

Cash in hand 4,511,451 5,200,438Cash at other banks – current accounts 5,175,427 2,383,058Cash at other financial institutions 18,634,052 15,986,712E.C.C.B. 1,302,779 (371,156)

29,623,709 23,199,0524 Reserve deposit

This reserve is maintained in accordance with Article 33 of the E.C.C.B. Agreement 1983, and isbased on the level of deposit liabilities held from time to time. It is not available for use in thebank’s day-to-day operations.

5 Customer loans and advances

2005 2004$ $

Mortgages 194,085,208 148,425,520Promissory notes 16,204,289 16,171,411Other advances 22,621,161 23,771,887

232,910,658 188,368,818Provision for loan losses (4,148,439) (3,717,486)Special provision re. Trans-Nemwil (Finance) Ltd. (see note below) (90,581) (134,381)

228,671,638 184,516,951

Movement in provision for loan losses is as follows:-2005 2004

$ $

Balance beginning of year 3,717,486 3,151,386Bad debts written off (474,956) (483,675)Increase in provision 905,909 1,049,775

Balance end of year 4,148,439 3,717,486

The aggregate amount of non-performing loans on which interest was not being accruedamounted to $19,383,388 as at September 30, 2005 ($15,215,699 as at September 30, 2004).Uncollected interest accrued on impaired loans amounted to $6,565,588 as at September 30,2005 ($8,689,413 as at September 30, 2004).

25Annual Report 2005

Notes to Financial Statements For the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

Note:This amount represents the excess of assets over liabilities, purchase price, acquisition costs andprovision for loan losses arising from the 1999 purchase of the said assets and liabilities of Trans-Nemwil (Finance) Ltd. The amounts to be taken into income in any year is based on therealisation of principal balances of the purchased loans. During the year $43,800 (2004 -$14,028) was transferred to Income as per note 14.

5.1 Maturity profile – Loans and advances

2005 2004$’000 $’000

Within 1 year 51,624 55,811

Within 1 to 3 years 17,606 14,771Within 3 to 5 years 16,486 13,942Over 5 years 147,195 103,845

232,911 188,369

5.2 Loans by Sector

2005 2004$’000 $’000

Agriculture 591 366Fisheries 483 455Manufacturing 10,144 10,213Utilities (electricity, water, telephone & media) 396 370Construction and land development 3,920 4,715Distributive trades 13,008 6,341Tourism 2,440 2,210Entertainment and catering 981 1,162Transportation and storage 22,432 8,647Financial institutions 239 26Professional and other services 9,275 7,728Public administration 7,085 7,191Personal 161,917 138,945

Total 232,911 188,369

GRENADA CO-OPERATIVE BANK LIMITED

26 Annual Report 2005

Notes to Financial StatementsFor the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

GRENADA CO-OPERATIVE BANK LIMITED

27Annual Report 2005

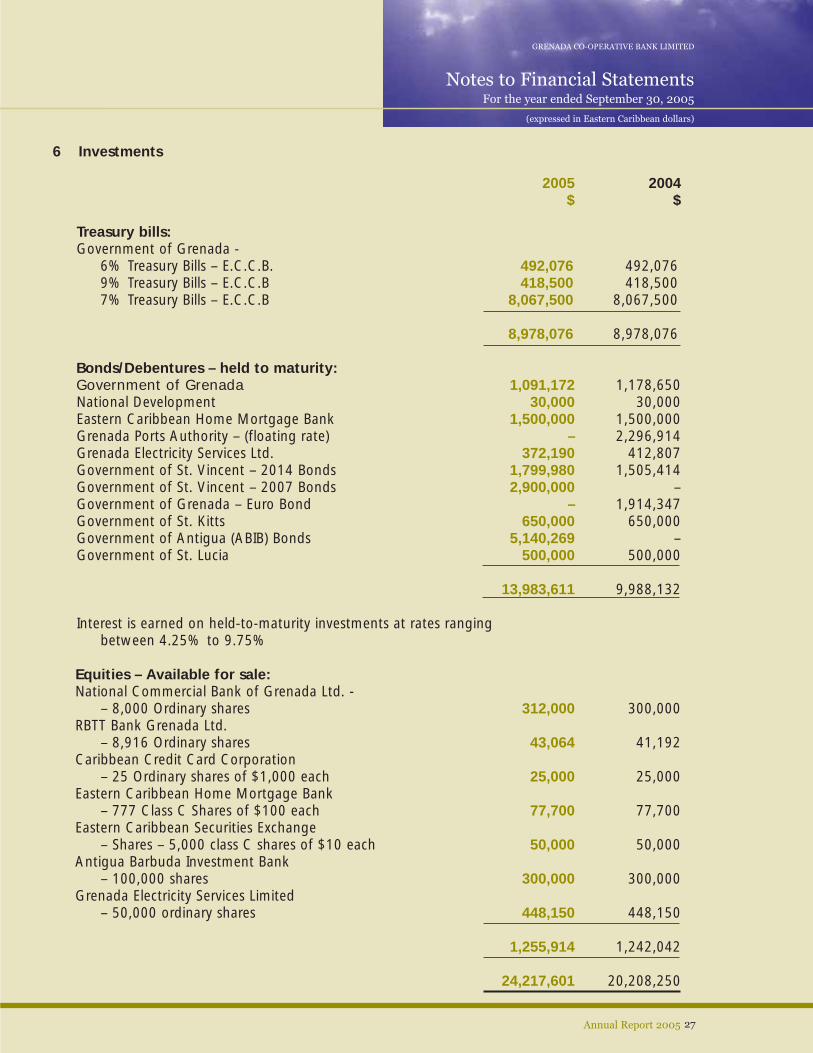

6 Investments

2005 2004$ $

Treasury bills:Government of Grenada -

6% Treasury Bills – E.C.C.B. 492,076 492,0769% Treasury Bills – E.C.C.B 418,500 418,5007% Treasury Bills – E.C.C.B 8,067,500 8,067,500

8,978,076 8,978,076

Bonds/Debentures – held to maturity:Government of Grenada 1,091,172 1,178,650National Development 30,000 30,000Eastern Caribbean Home Mortgage Bank 1,500,000 1,500,000Grenada Ports Authority – (floating rate) – 2,296,914Grenada Electricity Services Ltd. 372,190 412,807Government of St. Vincent – 2014 Bonds 1,799,980 1,505,414Government of St. Vincent – 2007 Bonds 2,900,000 –Government of Grenada – Euro Bond – 1,914,347Government of St. Kitts 650,000 650,000Government of Antigua (ABIB) Bonds 5,140,269 –Government of St. Lucia 500,000 500,000

13,983,611 9,988,132

Interest is earned on held-to-maturity investments at rates rangingbetween 4.25% to 9.75%

Equities – Available for sale:National Commercial Bank of Grenada Ltd. -

– 8,000 Ordinary shares 312,000 300,000RBTT Bank Grenada Ltd.

– 8,916 Ordinary shares 43,064 41,192Caribbean Credit Card Corporation

– 25 Ordinary shares of $1,000 each 25,000 25,000Eastern Caribbean Home Mortgage Bank

– 777 Class C Shares of $100 each 77,700 77,700Eastern Caribbean Securities Exchange

– Shares – 5,000 class C shares of $10 each 50,000 50,000Antigua Barbuda Investment Bank

– 100,000 shares 300,000 300,000Grenada Electricity Services Limited

– 50,000 ordinary shares 448,150 448,150

1,255,914 1,242,042

24,217,601 20,208,250

Notes to Financial Statements For the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

GRENADA CO-OPERATIVE BANK LIMITED

28 Annual Report 2005

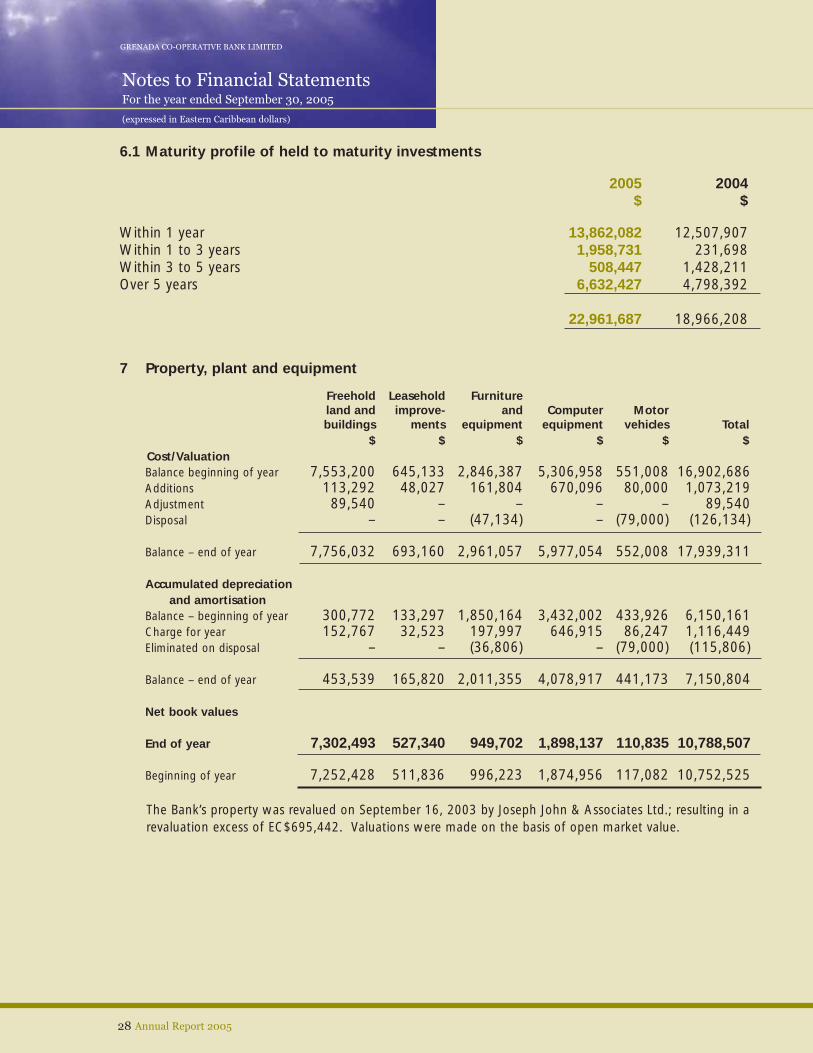

6.1 Maturity profile of held to maturity investments

2005 2004$ $

Within 1 year 13,862,082 12,507,907Within 1 to 3 years 1,958,731 231,698Within 3 to 5 years 508,447 1,428,211Over 5 years 6,632,427 4,798,392

22,961,687 18,966,208

7 Property, plant and equipment

Freehold Leasehold Furnitureland and improve- and Computer Motorbuildings ments equipment equipment vehicles Total

$ $ $ $ $ $Cost/ValuationBalance beginning of year 7,553,200 645,133 2,846,387 5,306,958 551,008 16,902,686Additions 113,292 48,027 161,804 670,096 80,000 1,073,219Adjustment 89,540 – – – – 89,540Disposal – – (47,134) – (79,000) (126,134)

Balance – end of year 7,756,032 693,160 2,961,057 5,977,054 552,008 17,939,311

Accumulated depreciationand amortisation

Balance – beginning of year 300,772 133,297 1,850,164 3,432,002 433,926 6,150,161Charge for year 152,767 32,523 197,997 646,915 86,247 1,116,449Eliminated on disposal – – (36,806) – (79,000) (115,806)

Balance – end of year 453,539 165,820 2,011,355 4,078,917 441,173 7,150,804

Net book values

End of year 7,302,493 527,340 949,702 1,898,137 110,835 10,788,507

Beginning of year 7,252,428 511,836 996,223 1,874,956 117,082 10,752,525

The Bank’s property was revalued on September 16, 2003 by Joseph John & Associates Ltd.; resulting in arevaluation excess of EC$695,442. Valuations were made on the basis of open market value.

Notes to Financial StatementsFor the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

GRENADA CO-OPERATIVE BANK LIMITED

8 Customer deposits

2005 2004$ $

Savings accounts 116,198,699 101,377,836Fixed deposit accounts 110,912,367 96,126,323Treasure Chest accounts 20,060,020 15,448,177Chequing accounts 19,115,159 14,323,087Current accounts 15,834,175 7,505,130

282,120,420 234,780,553

All deposits mature within one year. Effective interest rate ranged from 1.5% to 5%.

9 Proposed dividends

2005 2004$ $

Common shares 714,000 561,000

10 Stated capital

2005 2004$ $

Authorised:-An unlimited number of common shares with no par value

Issued:-5,100,000 common shares 7,620,000 7,620,000

29Annual Report 2005

Notes to Financial Statements For the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

11 Statutory reserve

The Banking Act of 1993 under Sub-section 14 (1) requires that a minimum of 20% of net aftertax profits in each year be transferred to a Statutory Reserve Fund until the balance of this fundis equal to the issued Share Capital. This reserve is not available for distribution as dividends orany form of appropriation.

The transfer for the year was $918,939 (2004 - $659,445).

12 Revaluation surplusEquity

Property investments Total$ $ $

Balance at beginning of year 695,442 257,416 952,858Revaluation surplus – unrealized gain on

available for sale investments – 13,872 13,872

Balance at end of year 695,442 271,288 966,730

13 Interest expense2005 2004

$ $

Savings deposits 3,877,281 3,125,512Other time deposits 5,110,171 4,578,572Chequing account 216,111 136,844

9,203,563 7,840,928

GRENADA CO-OPERATIVE BANK LIMITED

30 Annual Report 2005

Notes to Financial StatementsFor the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

GRENADA CO-OPERATIVE BANK LIMITED

14 Other income2005 2004

$ $

Sundry fees 2,166,948 2,137,657Miscellaneous 120,533 72,233Transfer from Trans-Nemwil special provision – (note 4) 43,800 14,028

2,331,281 2,223,918

15 Income before income tax

Income before income tax is arrived at after charging the following:-2005 2004

$ $

Depreciation 1,116,449 1,154,612Staff costs 4,043,571 4,010,251

16 Taxation

2005 2004$ $

Current tax 1,043,000 740,000

The tax on the income before tax differs from the theoretical amount that would arise using thebasic tax rate as follows:

2005 2004$ $

Income before income tax 5,637,693 4,037,225

Tax calculated at corporation tax rate of 30% 1,691,308 1,211,168Income not subject to tax (799,561) (608,676)Expenses not deductible for tax purposes 65,703 109,389Depreciation on items not eligible for capital allowances 81,887 24,689Over-provision in accounts – current year 3,663 3,430

1,043,000 740,000

31Annual Report 2005

Notes to Financial Statements For the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

17 Basic earnings per share

Basic earnings per share is calculated by dividing the income attributable to commonshareholders by the weighted average number of common shares in issue during the year.

2005 2004$ $

Net income attributable to common shareholders 4,594,693 3,297,225Weighted average number of common shares in issue 5,100,000 5,100,000Basic earnings per share 90¢ 65¢

The Bank has no potential common shares in issue which would give rise to a dilution of thebasic earnings per share. Therefore diluted earnings per share would be same as basic earningsper share.

18 Cash and cash equivalents2005 2004

$ $

This is comprised of:-Cash resources (note 3) 29,623,709 23,199,052

19 Leasehold commitments

At September 30, 2005, the bank was committed to annual leasehold payments as follows:-

2005 2004Lease expiry date $ $

Under one year 247,763 182,250One to five years 854,250 –

1,102,013 182,250

20 Undrawn commitments

Undrawn commitments on loans and advances at September 30, 2005 amounted to$30,755,000 (2004 - $20,017,000).

21 Capital commitments

The bank has commitments of $89,083 in respect of the improvement of electronic informationsystems.

GRENADA CO-OPERATIVE BANK LIMITED

32 Annual Report 2005

Notes to Financial StatementsFor the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

GRENADA CO-OPERATIVE BANK LIMITED

33Annual Report 2005

22 Defined contribution scheme

The bank maintains a superannuation plan into which both employer and employee pay 5% ofgross salary. The bank’s contribution to the Scheme was $199,406 (2004- $160,224).

23 Financial instruments

Interest rate riskNon-

Up to Between Between Over interest1 year 1-3 years 3-5 years 5 years bearing Total

As at 09.30.05 $’000 $’000 $’000 $’000 $’000 $’000

Assets

Cash and short-term funds 29,624 – – – 16,920 46,544Loans and advances 47,476 17,606 16,486 147,195 – 228,763Investments 13,862 1,959 508 6,633 1,256 24,218Other assets – – – – 20,926 20,926

Total assets 90,962 19,565 16,994 153,828 39,102 320,451

Liabilities

Customers’ deposits 282,120 – – – – 282,120Other liabilities – – – – 15,744 15,744

Total liabilities 282,120 – – – 15,744 297,864

Interest Sensitivity Gap (191,158) 19,565 16,994 153,828

As at 09.30.04

Assets

Cash and short-term funds 23,199 – – – 14,045 37,244Loans and advances 51,959 14,771 13,942 103,845 – 184,517Investments 12,508 232 1,428 4,798 1,242 20,208Other assets – – – – 19,368 19,368

Total assets 87,666 15,003 15,370 108,643 34,655 261,337

Liabilities

Customers’ deposits 234,781 – – – – 234,781Other liabilities – – – – 7,864 7,864

Total liabilities 234,781 – – – 7,864 242,645

Interest Sensitivity Gap (147,115) 15,003 15,370 108,643

Notes to Financial Statements For the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

23 Financial instruments ...Continued

Liquidity risk

Maturity of assets and liabilitiesUp to Up to Over

1 year 5 years 5 years Total($000’s) ($000’s) ($000’s) ($000’s)

As at September 30, 2005

Assets

Cash resources 46,544 – – 46,544Investments 13,862 2,467 7,888 24,217Loans and advances 47,476 34,092 147,195 228,763Other assets 6,739 6,149 8,038 20,926

Total assets 114,621 42,708 163,121 320,450

Liabilities

Customers’ deposits 282,120 – – 282,120Other liabilities 15,744 – – 15,744

Total liabilities 297,864 – – 297,864

Net liquidity gap (183,243) 42,708 163,121 22,586

As at September 30, 2004

Total assets 106,880 37,319 117,138 261,337Total liabilities (242,645) – – (242,645)

Net liquidity gap (135,765) 37,319 117,138 18,692

The maturity profile of the bank’s deposits and other borrowings is not directly matched by thematurity profile of its advances. Past experience has however indicated that deposits aretraditionally reinvested at maturity.

GRENADA CO-OPERATIVE BANK LIMITED

34 Annual Report 2005

Notes to Financial StatementsFor the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

GRENADA CO-OPERATIVE BANK LIMITED

23 Financial instruments ...Continued

Fair value of financial assets and liabilities

Financial assets and liabilities are carried at amounts which approximate their fair values at thebalance sheet date. The following methods and assumptions have been used to estimate theirvalues.

Assets

Cash resources

The fair values of these financial instruments are assumed to approximate their carrying valuesdue to their short-term nature.

Loans and advances

The carrying amounts, net of allowances for loan losses are assumed to reflect their fair values.

Investments

The valuation policy for investments is disclosed in note 2(g).

Liabilities

Customers’ deposits and other borrowings

Deposit liabilities payable on demand are assumed to equal their fair value.

24 Unauthorised transactions

Certain unauthorised transactions were discovered and reported in 2004. The total loss of$1.7m. resulting from these transactions have been reported in these financial statements.

35Annual Report 2005

Notes to Financial Statements For the year ended September 30, 2005

(expressed in Eastern Caribbean dollars)

Branch Designation Names

Head Office:No. 8 Church Street Managing Director Gordon V. Steele, Esq.St. George’s Internal Auditor J.G. Lawrence (Miss), B.S., MBA-IBFGrenada, West Indies Manager, Finance & Corporate Affairs R.W. Duncan, Esq., B.Sc., MA., CGA, AICBP.O. Box 135 Manager, Credit F.A. Williams (Mrs.), B.S.

Manager, Banking Operations F. Dowden, Esq., AICBSenior Credit Officer J. Gulston-Gittens (Mrs.), B.S.Senior Information Technology Officer D. Flemming, Esq.Human Resources Officer M. Squires-Francis (Mrs.) B.Sc.Marketing Officer S. Ince-John (Mrs.) B.Sc.

Telephone: Senior Operations Officer S. Regis, Esq., AICBSenior Programme & Research Officer P. Antoine, Esq., B.Sc, AICB

(473)-440-2111/3549Fax: Consultants:-

(473)-440-6600 Credit Consultant D. De Freitas, Esq.E-mail:

Grenville:Victoria Street Branch Manager A.C. Williams (Miss)Grenville, St. Andrew’s

Telephone:(473)-442-7748/7708

Fax:(473)-442-8400

Sauteurs:Main Street Branch Manager C. Bhola, Esq., AICBSauteurs, St. Patrick’s

Telephone:(473)-442-9247/1188

Fax:(473)-442-9888

Spiceland Mall:Morne Rouge Branch Manager C. Davidson (Mrs.)St. George’s

Telephone:(473)-440-2111Fax:(473)-439-0776

GRENADA CO-OPERATIVE BANK LIMITED

Offices

36 Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

Notes

37Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

Notes

38 Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

Notes

39Annual Report 2005

GRENADA CO-OPERATIVE BANK LIMITED

Notes

40 Annual Report 2005