annual regulatory report - transpower | we connect … · 2014/15 annual regulatory report ©...

TRANSCRIPT

2014/15 Annual Regulatory Report © Transpower New Zealand Limited 2015. All rights reserved. i

Annual Regulatory Report

on performance for the year ended 30 June 2015 and transmission pricing for the four years starting 1 April 2016

[Report Date]

2014/15 Annual Regulatory Report © Transpower New Zealand Limited 2015. All rights reserved. iii

Table of contents

Table of contents ................................................................................................................ iii

Table of figures .................................................................................................................... v

Table of tables .................................................................................................................... vi

Executive summary ............................................................................................................ vii

1 Introduction ............................................................................................................. 12

1.1 Maximum Allowable Revenue .............................................................................. 12

2 RCP2 revenue forecasts ......................................................................................... 14

2.1 Update to our revenue forecast ............................................................................ 14

2.2 Revenue in real terms .......................................................................................... 15

2.3 Interconnection Rate for 2016/17 ......................................................................... 16

2.4 HVDC Rate for 2016/17 ....................................................................................... 16

3 MAR wash-up .......................................................................................................... 17

3.1 Forecast and actual MAR for 2014/15 .................................................................. 17

3.2 MAR wash-up ...................................................................................................... 18

4 Network performance .............................................................................................. 20

4.1 RCP1 network performance measures and targets .............................................. 20

4.2 Interruptions greater than 1.0 system minute ....................................................... 21

4.2.1 Whirinaki Bus urgent remove from service (RFS) Event 11 July 2014 ........... 21

4.3 Historical network performance ............................................................................ 22

4.4 RCP2 revenue-linked network performance measures ........................................ 23

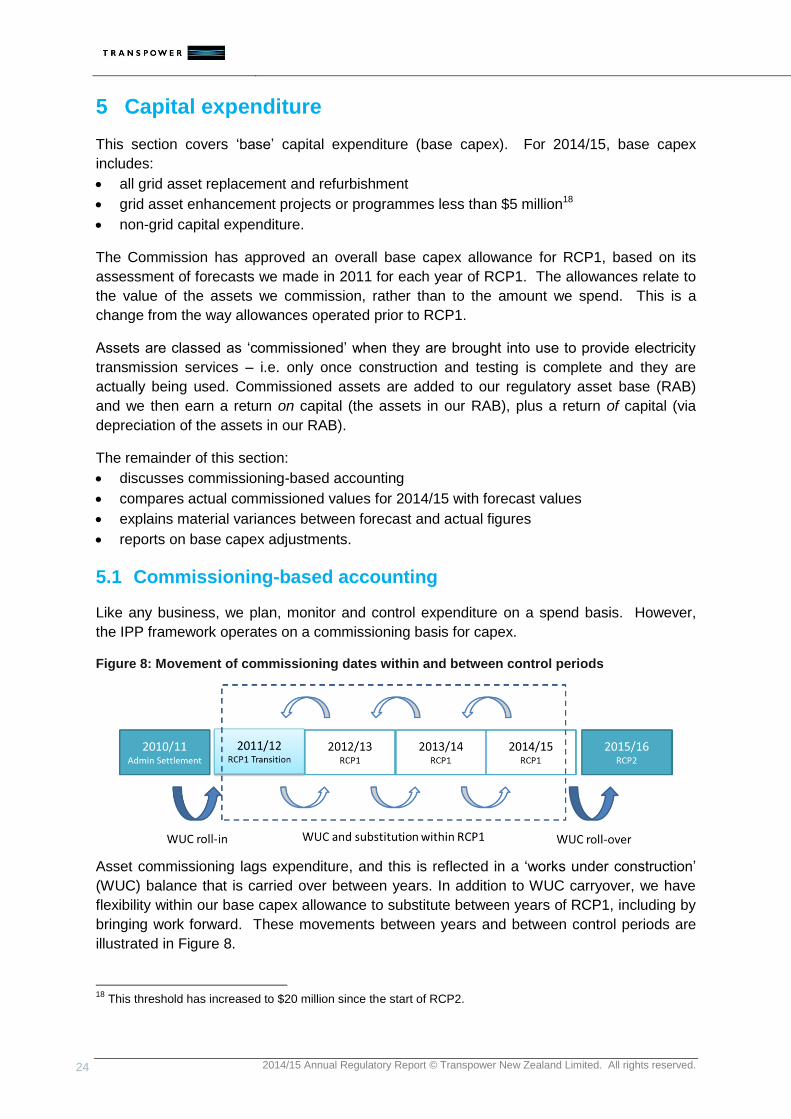

5 Capital expenditure ................................................................................................. 24

5.1 Commissioning-based accounting ....................................................................... 24

5.2 Comparison of actual with forecast base capex ................................................... 25

5.3 Base capex adjustments ...................................................................................... 26

5.4 Historical base capex ........................................................................................... 27

5.5 RCP2 base capex ................................................................................................ 28

6 Major projects .......................................................................................................... 29

6.1 Progress reports – costs ...................................................................................... 29

6.2 Progress reports – timing ..................................................................................... 31

6.3 Close-out reports ................................................................................................. 32

6.3.1 National Auto-synchronisation Points Project ................................................. 33

6.3.2 Wairakei Ring Project .................................................................................... 35

7 Controllable operating expenditure .......................................................................... 37

7.1 Historical operating expenditure ........................................................................... 38

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. iv

7.2 RCP2 opex allowance .......................................................................................... 39

8 Pass-through and recoverable costs ....................................................................... 40

8.1 2014/15 wash-up ................................................................................................. 40

8.2 Historical pass-through and recoverable costs ..................................................... 41

8.3 Forecast pass-through and recoverable costs ...................................................... 41

9 Other regulatory documents .................................................................................... 43

9.1 Initiatives Plan ...................................................................................................... 43

9.2 Integrated Transmission Plan .............................................................................. 43

A.1 RCP2 performance measures – Points of Service by category ................................ 44

A.2 RCP2 performance measures – selected circuits for HVAC availability measure .... 48

A.3 Detailed base capex variance explanation ............................................................... 49

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. v

Table of figures

Figure 1: Components of the year-on-year movement in HVAC revenue ............................ viii

Figure 2: Components of the year-on-year movement in HVDC revenue .............................. ix

Figure 3: Regulation of Transpower's activities ................................................................... 12

Figure 4: MAR building blocks and inputs ........................................................................... 13

Figure 5: Disclosure and update cycle ................................................................................ 13

Figure 6: Revenue in real terms .......................................................................................... 15

Figure 7: Simplified representation of main MAR building blocks ........................................ 17

Figure 8: Movement of commissioning dates within and between control periods ............... 24

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. vi

Table of tables

Table 1: Latest RCP2 revenue forecast (determined on 5 November 2015) ......................... vii

Table 2: Actual performance against target for four performance measures ......................... x

Table 3: HVAC updated revenue forecast (detail) ............................................................... 14

Table 4: HVDC updated revenue forecast (detail) ............................................................... 14

Table 5: Total updated revenue forecast ............................................................................. 15

Table 6: Summary calculation of the MAR wash-up for 2014/15 ......................................... 18

Table 7: Actual 2014/15 performance against targets for four network performance

measures ..................................................................................................................... 20

Table 8: Historical network performance ............................................................................. 22

Table 9: RCP2 network performance measures .................................................................. 23

Table 10: Forecast and actual 2014/15 base capital expenditure (commissioned basis) ..... 25

Table 11: Total RCP1 allowance and actual base capital expenditure (commissioned basis)

.................................................................................................................................... 26

Table 12: Adjustments that can apply to base capex .......................................................... 26

Table 13: Adjustment to base capex allowance for CPI movement ..................................... 27

Table 14: Historical base capex .......................................................................................... 27

Table 15: RCP2 base capex commissioning allowance ...................................................... 28

Table 16: Updated cost forecasts for partially completed major projects ............................. 29

Table 17: Updated timing forecasts for partially completed major projects .......................... 31

Table 18: Summary of possible adjustments to major projects ............................................ 32

Table 19: Actual operating expenditure for 2014/15 ........................................................... 37

Table 20: Historical and forecast operating expenditure ...................................................... 38

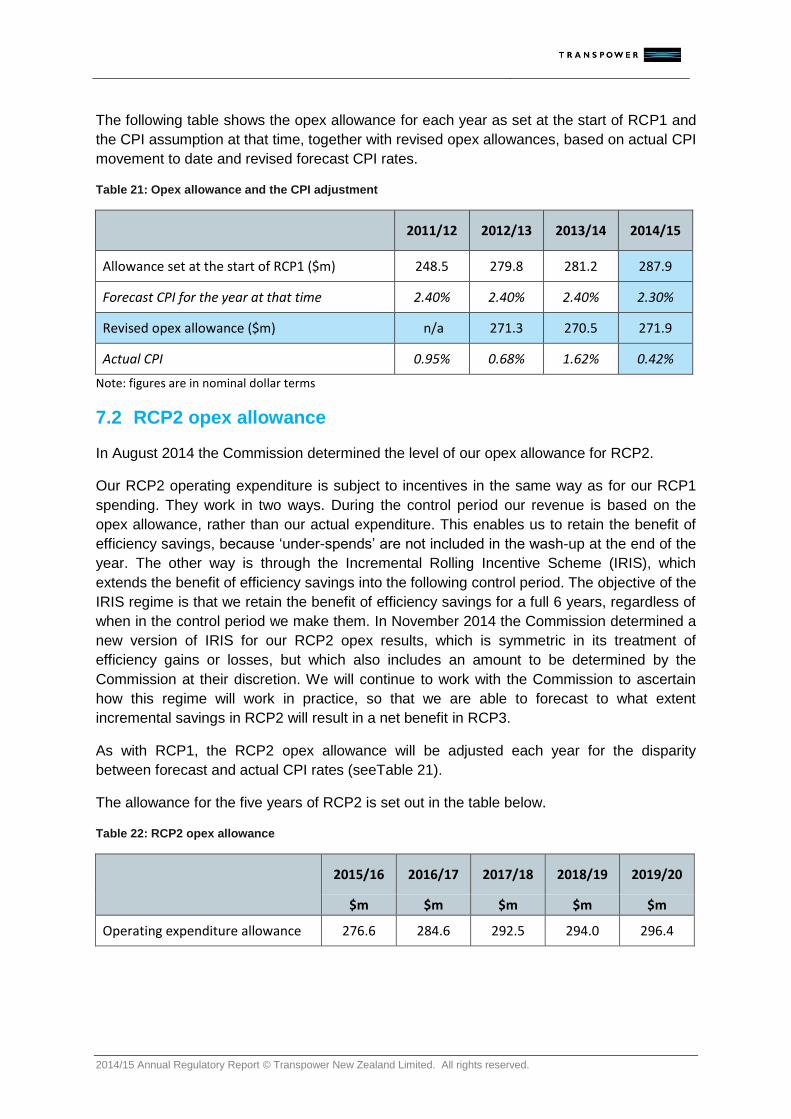

Table 21: Opex allowance and the CPI adjustment ............................................................. 39

Table 22: RCP2 opex allowance ......................................................................................... 39

Table 23: Allocation of pass-through and recoverable wash-up amounts ............................ 40

Table 24: Historical pass-through and recoverable costs .................................................... 41

Table 25: Current forecast RCP2 pass-through and recoverable costs ............................... 42

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. vii

Executive summary

This report provides an overview of network and expenditure performance for our most

recent disclosure year (ended 30 June 2015) and information on transmission prices for the

coming pricing year (starting 1 April 2016).

The report complements more comprehensive and detailed spreadsheet-based disclosures,

which are available on our website:

https://www.transpower.co.nz/about-us/industry-information/revenue-and-pricing

This our fourth Annual Regulatory Report. It reports on the final year of our first regulatory

control period (RCP1). Next year’s report will introduce new performance measures that we

developed for our second control period (RCP2).

Updated revenue forecast

Following a thorough proposal and evaluation process, the Commerce Commission

published a determination in November 2014 setting forecast transmission revenue for the

five years of RCP2. These forecasts provide the basis for setting prices for the five years of

RCP2. Each year we update the revenue determination to take account of:

a wash-up of revenue inputs ( or “building blocks”) for the year just ended to ensure that

we do not under- or over-recover revenue from customers

costs associated with any newly-approved major capex projects

updated forecasts of pass-through and recoverable costs

financial incentives designed to promote ongoing performance improvements.

The table below presents updated revenue figures for all years of RCP2 (changes from the

previous forecast are detailed in Section 2.1).

Table 1: Latest RCP2 revenue forecast (determined on 5 November 2015)

2015/16 2016/17 2017/18 2018/19 2019/20

$m $m $m $m $m

HVAC 766.6 793.5 842.8 817.7 827.4

HVDC 149.9 152.8 151.4 152.3 150.0

Total transmission revenue 916.6 946.2 994.2 970.0 977.4

Note: figures are in nominal terms and may not add exactly due to rounding.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. viii

Year-on-Year Movement

The following charts analyse factors contributing to the year-on-year increase in

transmission revenue from 2015/16 to 2016/17. HVAC and HVDC1 are analysed separately.

We recover HVAC costs via three types of transmission fee:

connection ($128.6 million in 2016/17) – covers the cost of owning and operating assets

used to connect customers to the grid

prudent discount ($2.8 million in 2016/17) – customers who could avoid charges by

reconfiguring their connection to the grid can receive discounted transmission charges in

return for paying prudent discount fees

interconnection ($662.1 million in 2016/17) – the balance of costs are recovered from

offtake customers based on their contribution to regional demand peaks.

Figure 1: Components of the year-on-year movement in HVAC revenue

Movement explanations:

our HVAC regulatory asset base (RAB) is forecast to increase due to $233 million of

forecast base capex commissioning and $10 million of forecast major capex

commissioning during 2015/16

HVAC depreciation, write-offs and dismantling costs are forecast to be about $6 million

more in aggregate for the 2016/17 year than they were for the 2015/16 year. Of that

1 New Zealand’s transmission grid has a high voltage direct current (HVDC) link between Benmore (in the central South Island) and Haywards (near Wellington). The HVDC link connects the South Island and North Island high voltage alternating current (HVAC) grids. HVDC and HVAC costs are treated separately.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. ix

increase, $12 million is due to a higher Regulatory Asset Base (RAB), which is offset by

a $6 million decrease in the depreciation of our Pseudo Asset2

The operating expenses allowance is forecast to increase by about $8 million (or 3%)

from 2015/16 to 2016/17

The return to customers from the wash-up of the 2014/15 year is $4.5 million less than

from the wash-up of the 2013/14 year. That is principally because the over-estimate of

revenue building blocks for the year was about $14 million less than the previous year,

offset by the pass-through and recoverable costs wash-up, which was about $9 million

more than the previous year.

We recover HVDC revenue from customers who inject energy into the South Island grid.

Figure 2: Components of the year-on-year movement in HVDC revenue

Movement explanations (excluding items common to HVAC and HVDC):

our HVDC regulatory asset base (RAB) is forecast to decrease overall, because

depreciation in 2015/16 (reducing the RAB) is forecast to be $37.6 million whilst

commissioning (increasing the RAB) is forecast to be just $3.7 million

opex incentive credits contribute $5.7 million to HVDC revenue in 2016/17, up from $0.8

million in 2015/16

The additional charge to HVDC customers as a result of the 2014/15 wash-up is $3.5

million lower (at $3.4 million) than the wash-up for 2013/14, which was $6.9 million.

That’s principally because the under-estimate of revenue building blocks for the year was

about $5 million lower than the previous year, offset by an increase in the pass-through

and recoverable costs wash-up.

2 From 2011/12 to 2015/16 we had a pseudo asset on our RAB. That asset was depreciating at a rate of $6.4

million per year. This asset was fully depreciated at the end of 2015/16.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. x

Network Performance

We outperformed three of our four network performance targets during 2014/15.

Table 2: Actual performance against target for four performance measures

Performance measures Target Actual Target

achieved?

Number of loss of supply events greater than 0.05 system minutes3

21 13 Y

Number of loss of supply events greater than 1 system minute

3 1 Y

Unplanned HVAC circuit unavailability (%) 0.054 0.068 N

Unplanned HVDC bi-pole unavailability (%) (no target

set) 0.130 n/a

Total impact of interruptions (measured in system minutes) 16.69 12.21 Y

From 2015/16, we will be reporting against a new set of measures and will be subject to a

financial incentive linked to performance. The new measures cover the frequency and

duration of interruptions, and the availability of key market-sensitive circuits.

Detailed information on specific events that contributed to the missed HVAC unavailability

target can be found in the 2014/15 IPP disclosures on our website:

https://www.transpower.co.nz/about-us/industry-information/regulatory-control-

periods/rcp1/updates-rcp-1.

Other regulatory documents

Earlier this year we published two other sets of regulatory reports:

RCP2 Initiatives Plan – provides information on how we intend to develop service

measures and targets for our next control period (RCP3) and how we intend to improve

aspects of our asset planning and forecasting

2015 Integrated Transmission Plan (ITP) – an overview of our plans. Includes full

schedules of planned expenditure and information on what has changed since we

published our last ITP in 2013. The 2015 ITP is supported by a Transmission Planning

Report identifying backbone grid and regional development plans; a Service Report

defining our service offering and performance targets; and an Asset Management Plan

explaining our asset management framework, management of each asset class and

planning works.

The Improvement Plan and the ITP are available on our website:

https://www.transpower.co.nz/about-us/industry-information/regulatory-control-

periods/rcp2/updates. 3 A ‘system minute’ is a loss of supply equivalent to losing peak demand for one minute. For example, losing supply to a city the size of Hamilton for around 40 minutes during a peak winter night would be roughly equivalent to one system minute.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. xi

North Island Grid Upgrade (NIGU)

In August 2015 the Commission published its final decision on our application to amend the

allowance for the major North Island Grid Upgrade (NIGU) project we completed in 2012.

The decision permitted recovery of $876.3 million against a total project cost of $894 million.

We had previously built voluntary reductions into our revenues for the six years from

2014/15 that are consistent with this decision, so no further adjustments to revenue are

required.

Full details of the Commission’s decision can be found on the Commerce Commission

website4.

4 http://www.comcom.govt.nz/regulated-industries/electricity/electricity-transmission/transpower-major-capital-

proposal/amending-the-allowance-and-outputs-for-the-north-island-grid-upgrade-project/

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 12

1 Introduction

This report details Transpower’s regulated transmission revenue for the remaining four years

of RCP2 (from 1 April 2016 to 31 March 2020). This updated revenue forecast was

determined by the Commerce Commission on 5 November 20155.

The report also covers Transpower’s activities for the period from 1 July 2014 to 30 June

2015 (the ‘disclosure year’). It reviews capital and operating expenditure and the

performance of our transmission network.

Figure 3: Regulation of Transpower's activities

This is the fourth and final report from our first regulatory control period (‘RCP1’), which runs

from 2011/12 to 2014/15. We welcome any feedback you have on this report.

1.1 Maximum Allowable Revenue

The Commerce Commission (“the Commission”) has established rules that are used to set

the Maximum Allowable Revenue (“MAR”) for transmission services. The MAR is calculated

by adding together revenue ‘building blocks’.

5 Technically the Commission determine our MAR, but the number most relevant to customers is our total

transmission revenue, which comprises our MAR, the forecast pass-through and recoverable costs together with voluntary reductions in our revenue. This is the figure applied to the TPM to calculate transmission charges.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 13

Figure 4: MAR building blocks and inputs

Some of the inputs to the building blocks are set by the Commission at the beginning of each

control period. These are:

operating expenditure allowances for each year

‘base’ capital expenditure for each year

cost of capital (WACC) for each control period.

The operating and base capital expenditure allowances for RCP2 were set by the

Commission on 29 August 2014 and the regulatory cost of capital for the period was set on

31 October 2014. We use these inputs to calculate an initial forecast of transmission

revenue, which is then updated each year to take account of actual expenditure and

performance.

Figure 5: Disclosure and update cycle

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 14

2 RCP2 revenue forecasts

This section presents details of our forecast revenue for the five years of RCP2, and

provides details of the main transmission pricing rates for 2016/17. Our regulated

transmission revenue consists of our MAR plus pass-through and recoverable costs and any

voluntary reductions.

2.1 Update to our revenue forecast

In November 2014 the Commerce Commission approved our revenue forecast for RCP2.

Every year we update6 this forecast for the remaining years of RCP2. This is our first such

update. The tables below show the revenue as determined last year, together with the

changes we have just made.

Table 3: HVAC updated revenue forecast (detail)

2016/17 2017/18 2018/19 2019/20

$m $m $m $m

Amount determined in November 2014 799.7 832.6 817.2 825.9

New major capex approval7 0.2 0.4 0.5 0.5

Wash-ups from 2014/15 (see Table 6) (16.1) - - -

Movement in the calculation of IRIS credits8 9.6 9.8 - 1.0

Updated amount 793.5 842.8 817.7 827.4

Table 4: HVDC updated revenue forecast (detail)

2016/17 2017/18 2018/19 2019/20

$m $m $m $m

Amount determined in November 2014 143.9 145.8 149.4 144.7

Wash-ups from 2014/15 (see Table 6) 3.4 - - -

Movement in the calculation of IRIS credits 5.5 5.6 2.9 5.2

Updated amount 152.8 151.4 152.3 150.0

6 We’re only permitted to update the revenue for certain changes, being new major or listed project approvals, the

effect of wash-ups from previous years and revised pass-through and recoverable costs. 7 Amendment to the Upper South Island Grid Upgrade.

8 IRIS (Incremental Rolling Incentive Scheme) is our opex incentive regime.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 15

Table 5: Total updated revenue forecast

2016/17 2017/18 2018/19 2019/20

$m $m $m $m

HVAC 793.5 842.8 817.7 827.4

HVDC 152.8 151.4 152.3 150.0

Total transmission revenue 946.2 994.2 970.0 977.4

2.2 Revenue in real terms

The graph below shows how the updated RCP2 revenue for HVAC and HVDC in Table 5

trends in real terms (2015/16 prices). The graph also shows our expected revenue, once

forecast wash-ups and other adjustments are included. 2015/16 is included for comparison.

Figure 6: Revenue in real terms

The revenue in 2015/16 includes the effect of wash-ups of the 2013/14 year ($20 million

reduction to HVAC and $6 million increase to HVDC). The revenue in 2016/17 includes

the effect of wash-ups of the 2014/15 year ($16 million reduction to HVAC and $3 million

increase to HVDC).

Major projects that are not yet approved by the Commerce Commission are excluded

from the inputs used to set our revenue path. The revenue numbers in Table 5 also

exclude forecast future wash-ups. The dotted lines show what our revenue path would

be if those were included.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 16

2.3 Interconnection Rate for 2016/17

Customers’ annual interconnection charge is determined by multiplying their contribution to

‘regional coincident peak demand’ (RCPD) by the Interconnection Rate. That rate is

calculated using the formula:

𝐼𝑅 =𝐴𝐶𝑟𝑒𝑣 − ∑ 𝐶𝑜𝑛𝑛𝑟𝑒𝑣 − ∑ 𝑃𝐷𝐴𝑟𝑒𝑣

∑ 𝑅𝐶𝑃𝐷𝑡𝑜𝑡𝑎𝑙

Where:

𝐴𝐶𝑟𝑒𝑣 = HVAC pricing revenue $ 793,434,669

∑ 𝐶𝑜𝑛𝑛𝑟𝑒𝑣 = revenue from connection charges $128,569,151

∑ 𝑃𝐷𝐴𝑟𝑒𝑣 = revenue from prudent discount agreements $2,794,513

∑ 𝑅𝐶𝑃𝐷𝑡𝑜𝑡𝑎𝑙 = regional coincident peak demand across all regions9 5,775,201 kW

The result is an Interconnection Rate for 2015/16 of $114.64 /kW

This is a 3.9% increase from the 2015/16 rate ($110.35 /kW), resulting from a 4.7% increase

in interconnection revenue, partially offset by a 0.8% increase in demand (total RCPD).

The 2015/16 rate was a 3.6% reduction from the 2014/15 rate ($114.47 /kW).

2.4 HVDC Rate for 2016/17

The HVDC charge on customers who inject energy into the South Island grid10 is determined

by multiplying their ‘historic anytime maximum injection’ (HAMI) by the HVDC Rate. That rate

is calculated using the formula:

𝐻𝑉𝐷𝐶 𝑅𝑎𝑡𝑒 =𝐷𝐶𝑟𝑒𝑣 − ∑ 𝑃𝐷𝐴𝑟𝑒𝑣

∑ 𝐻𝐴𝑀𝐼𝑡𝑜𝑡𝑎𝑙

Where:

𝐷𝐶𝑟𝑒𝑣 = HVDC pricing revenue $ 152,775,845

∑ 𝑃𝐷𝐴𝑟𝑒𝑣 = revenue from prudent discount agreements $491,018

∑ 𝐻𝐴𝑀𝐼𝑡𝑜𝑡𝑎𝑙 = total HAMI across all customers9 3,223,405 kW

The result is an HVDC Rate for 2015/16 of $47.24 /kW

This is a 1.6% increase from the 2015/16 rate ($46.49/kW), resulting from a 1.6% increase in

transmission pricing revenue.

The 2015/16 rate was a 4.2% increase from the 2014/15 rate ($44.60/kW).

9 Our TPM Operational Review will result in changes to the way RCPD and HAMI are calculated from April 2017

(see https://www.transpower.co.nz/about-us/industry-information/tpm-development#transpower-tpm). 10

Meridian Energy, Contact Energy and Genesis Energy account for 96% of South Island injection in 2015/16.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 17

3 MAR wash-up

This section covers the revenue ‘wash-up’ calculation included in forecast revenue for

2016/17 (and therefore prices for the pricing year starting April 2016).

The wash-up compares revenues we earned in 2014/15 with an ex post assessment of

revenue permitted under the Individual Price-Quality Path (IPP) framework. Any over- or

under-recovery from 2014/15 is returned to, or recovered from, customers via an adjustment

to our 2016/17 revenues (and prices).

3.1 Forecast and actual MAR for 2014/15

We calculated prices for our 2014/15 pricing year (starting 1 April 2014) based on forecasts

of the MAR ‘building blocks’ for the year11. The main building blocks are illustrated again

below.

Figure 7: Simplified representation of main MAR building blocks

Our forecast MAR for 2014/15 was determined by the Commission in October 2011 and was

updated in October 2013 to $934.6 million. Included in that forecast was a net reduction in

revenue of $12.2 million relating to net over-recovery in prior years. When we calculated

prices for 2014/15 we also applied a $4.0 million voluntary revenue reduction, relating to the

NIGU project overspend and cancellation of some RCP1 maintenance projects. That

reduced our target revenue for the year to $930.6 million.

We have now recalculated our MAR for 2014/15 to reflect the actual opening regulatory

asset base (RAB) value at 1 July 2014, the timing and value of assets commissioned during

2014/15, and actual CPI movement to the end of 2014/15.

11

Prices are set based on a forecast total revenue number that includes the forecast MAR, plus estimates of pass-through and recoverable costs. Pass-through and recoverable costs are covered in Section 7 of this report.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 18

3.2 MAR wash-up

The table below calculates our 2014/15 MAR wash-up by comparing HVAC and HVDC

revenues received in the pricing year with our actual MAR, broken down by revenue building

blocks.

Table 6: Summary calculation of the MAR wash-up for 2014/15

Building blocks (all in $m)

Forecast Revised Due (to) or from customers

A B B - A

Total Total Total HVAC HVDC

Return on assets 383.7 374.9 (8.7) (7.4) (1.3)

Tax 36.4 41.1 4.7 (0.9) 5.6

Depreciation 238.7 242.0 3.3 1.5 1.8

Opex allowance (CPI-adjusted) 287.9 271.9 (16.0) (14.6) (1.4)

Term Credit Spread Differential12 0.1 2.6 2.5 2.1 0.4

Building block revenue 946.8 932.5 (14.2) (19.3) 5.1

Historic EV adjustment13 12.2 12.2 - - -

Forecast MAR 958.9 944.7 (14.2) (19.3) 5.1

Subsequent EV adjustment14 (24.3) (24.3) - - -

Voluntary revenue reductions (4.0) (4.0) - - -

Charging variations in the year15 (6.1) 6.1 5.6 0.5

Tax on both EV adjustments 3.4 3.4 7.4 (4.0)

919.8

Revenue actually charged 924.5 924.5

Due (to) or from customers (4.7) (4.7) (6.3) 1.5

Other adjustments - prior year adjustments

- 0.3 (0.3)

(4.7) (6.0) 1.3

Interest for 2 years (2014/15 to 2016/17) (0.6) (0.8) 0.2

(5.4) (6.8) 1.5

Grossing up for tax at 28%

(2.1) (2.6) 0.6

Adjustment to the MAR for 2016/17 (7.4) (9.5) 2.0

RCP2 cash flow timing adjustment 0.2 0.3 (0.1)

(7.2) (9.2) 2.0

Pass-through and recoverable cost wash-up (5.5) (6.9) 1.4

Total 2014/15 wash-ups applied to 2016/17 revenue (12.7) (16.1) 3.4

Note: Figures may not add exactly due to rounding.

In summary, we recovered $4.7 million more than permitted in 2014/15, comprising a

$6.0 million over-recovery from HVAC customers and a $1.3 million under-recovery from

12

This is an ‘allowance’ to compensate us for the extra cost of debt that has a tenor of more than 5 years. 13

This is the payment to/from customers to clear historical accumulated EV balances (see Appendix Error! Reference source not found.). 14

This is the wash-up of the 2012/13 disclosure year. 15

Changes to the configuration of the grid can lead to over- or under-recovery of our revenue in the year.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 19

HVDC customers. Other adjustments, including the addition of interest, tax and the wash-up

of our pass-through and recoverable costs, result in a total adjustment to revenues for

2016/17 of $12.7 million. That comprises a deduction of $16.1 million from HVAC revenue

and an addition of $3.4 million to HVDC revenue.

The Forecast revenue calculations for RCP1 assumed mid-financial year (i.e. December)

commissioning of all assets. If we actually commission assets earlier in the year, then the

forecast revenue figure will be too low. The wash-up allows us to make up for this shortfall.

Conversely, if we commission assets later in the year, then the wash-up allows us to return

our over-recovery to customers in the next pricing year. The wash-up similarly allows future

prices to be adjusted if we commission assets at a higher or lower cost than forecast.

The key drivers of the wash-up in 2014/15 are:

RAB assets at the start of the year were $98 million lower than forecast, resulting in an

$7.9 million over-recovery. That was partly offset by higher commissioning in the year,

which was $35 million higher than forecast. The higher-than-forecast commissioning

resulted in an under-recovery of $2.9 million and later-than-forecast commissioning

resulted in a $3.7 million over-recovery. The net effect is that our return on assets was

$8.7 million too high ($7.4 million for HVAC and $1.3 million for HVDC).

The operating expenditure allowance incorporates forecast CPI movement of 2.4% each

year on average over RCP1. Actual CPI movement has been less than forecast, so we

have over-recovered $16 million compared to the CPI-adjusted allowance.

The lower-than-forecast allowable tax deductions for the HVAC line of business has

resulted in a greater-than-forecast tax building block (an increase of $8 million). The

allowable opex was lower because of the CPI adjustment and the asset-based

allowances (tax depreciation and notional interest) were lower because of the lower

opening RAB.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 20

4 Network performance

This section reports on network performance measures that are monitored by the

Commission for RCP1.

A new suite of ‘grid output measures’ for RCP2 apply from 1 July 2015. These are the basis

of a financial incentive linked to network performance. There was no such arrangement for

RCP1.

4.1 RCP1 network performance measures and targets

The Commission has specified a set of measures, and target service quality levels for each

of those targets. The following table compares actual performance against the Commission

targets.

Table 7: Actual 2014/15 performance against targets for four network performance measures

Performance measures Target Actual Target

achieved?

Number of loss of supply events greater than 0.05 system minutes16

21 13 Y

Number of loss of supply events greater than 1 system minute

3 1 Y

Unplanned HVAC circuit unavailability (%) 0.054 0.068 N

Unplanned HVDC bi-pole unavailability (%) n/a 0.130 n/a

Total impact of interruptions (measured in system minutes) 16.69 12.21 Y

We met all of the network performance targets for 2014/15, except for the HVAC circuit

unavailability target. A detailed explanation of factors contributing to this missed target can

be found on our website in the 2014/15 IPP Disclosures document17.

16

A ‘system minute’ is a loss of supply equivalent to losing peak demand for one minute. For example, losing supply to a city the size of Hamilton for around 40 minutes during a peak winter night would be roughly equivalent to one system minute.

17

https://www.transpower.co.nz/about-us/industry-information/regulatory-control-periods/rcp1/updates-rcp-1

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 21

4.2 Interruptions greater than 1.0 system minute

There was one loss-of-supply event greater than 1.0 system minute in 2014/15, which

caused a loss of supply of 5.28 system minutes.

4.2.1 Whirinaki Bus urgent remove from service (RFS) Event 11 July 2014

Impact This event resulted in 5.28 system minutes of non-supply to Pan Pac.

Reason

On 11 July 2014, an urgent forced outage of the 11 kV Bus B at Whirinaki was required to investigate unusual noises from this switchgear and reports of the smell of ozone in the switchgear room. The decision was made to proceed with the urgent shutdown because of concerns about the possibility of a major failure occurring, with severe consequences for the supply to Pan Pac Forest Products Limited (Pan Pac). Pan Pac was advised that an urgent outage to Whirinaki 11kV Bus B was required to investigate an unusual noise. This resulted in interruptions to Pan Pac for 696 minutes (T3, average 11.2MW) and 764 minutes (T2, average 34.2MW).

Our response

While it cannot be conclusively proven, we consider that the most likely cause of the unusual noise was loose clamping arrangements of the vertically stacked current transformer assembly in the CB31 cubicle. Following this event, we completed an Incident Investigation Report and a number of remedial actions, including :-

1. Manufacturer of the Areva PIX switchgear has been advised of the defect in the CB2872 truck, and advice has been sought about an appropriate repair procedure.

2. A business case has been approved for a set of spare 11 kV voltage transformers to be procured that will cover the Whirinaki and Central Park substation Merlin Gerin switchgear.

The Investigation identified a number initiatives which are being implemented, including:-

1. Revise and clarify inspection requirements for metalclad switchgear 2. Research feasibility of a training resource on noises from indoor switchgear 3. Review the engineering on-site response to major failure incidents 4. Investigate decision support systems for reports of equipment in distress 5. Review the risk management approach for legacy indoor switchboards

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 22

4.3 Historical network performance

For comparison, the following table sets out performance against each of the Commission’s

targets, plus total outages in system minutes, from 2011/12 to 2014/15.

Table 8: Historical network performance

Measure 2011/12 2012/13 2013/14 2014/15

Events >0.05 system minutes 19 12 17 13

Events >1 system minute 2 2 2 1

Unplanned HVAC circuit unavailability (%) 0.064 0.032 0.051 0.068

Unplanned HVDC bi-pole unavailability (%) 0.109 0.684 0.071 0.130

Total impact of interruptions (in system minutes)

14.45 7.62 12.12 12.21

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 23

4.4 RCP2 revenue-linked network performance measures

The following table lists the details of the performance measures that will apply in RCP2. A

full list of the Points of Service in each of the categories (High Priority, Important, Standard,

Generator and N-security) is included in Appendix A.1 and the circuits included in the HVAC

availability measure are listed in Appendix A.2.

Table 9: RCP2 network performance measures

Measure and category Number of sites

RCP2 Targets

Incentive rate

($k per unit from

target) Target Cap Collar

Number of interruptions (p.a.)

High Priority 23 2 0 4 606

Important 43 9 4 14 242

Standard 78 26 21 31 133

Generator 40 11 6 16 133

N-security 46 56 38 74 10

Average duration of interruptions (min)

High Priority 23 70 30 110 15

Important 43 100 30 170 9

Standard 78 65 0 130 5

Generator 40 130 50 210 4

N-security 46 80 45 115 3

P90 Longest durations (min)

High Priority 23 120 80 160 15

Important 43 240 170 310 9

Standard 78 130 60 200 5

Generator 40 350 260 440 4

N-security 46 215 170 260 3

Availability (%)

HVDC - 98.5 99.5 97.5 1,000

HVAC - 99.6 100.0 99.2 2,500

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 24

5 Capital expenditure

This section covers ‘base’ capital expenditure (base capex). For 2014/15, base capex

includes:

all grid asset replacement and refurbishment

grid asset enhancement projects or programmes less than $5 million18

non-grid capital expenditure.

The Commission has approved an overall base capex allowance for RCP1, based on its

assessment of forecasts we made in 2011 for each year of RCP1. The allowances relate to

the value of the assets we commission, rather than to the amount we spend. This is a

change from the way allowances operated prior to RCP1.

Assets are classed as ‘commissioned’ when they are brought into use to provide electricity

transmission services – i.e. only once construction and testing is complete and they are

actually being used. Commissioned assets are added to our regulatory asset base (RAB)

and we then earn a return on capital (the assets in our RAB), plus a return of capital (via

depreciation of the assets in our RAB).

The remainder of this section:

discusses commissioning-based accounting

compares actual commissioned values for 2014/15 with forecast values

explains material variances between forecast and actual figures

reports on base capex adjustments.

5.1 Commissioning-based accounting

Like any business, we plan, monitor and control expenditure on a spend basis. However,

the IPP framework operates on a commissioning basis for capex.

Figure 8: Movement of commissioning dates within and between control periods

Asset commissioning lags expenditure, and this is reflected in a ‘works under construction’

(WUC) balance that is carried over between years. In addition to WUC carryover, we have

flexibility within our base capex allowance to substitute between years of RCP1, including by

bringing work forward. These movements between years and between control periods are

illustrated in Figure 8.

18

This threshold has increased to $20 million since the start of RCP2.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 25

5.2 Comparison of actual with forecast base capex

This section compares forecast and actual base capex at a ‘category’ level, and explains any

material variances.

Actual and forecast values are set out below. The Commerce Commission has specified

‘material variance’ to be a variance that is both greater than $10 million and more than 10%

of the category forecast.

Table 10: Forecast and actual 2014/15 base capital expenditure (commissioned basis)

Category Allowance Actual Variance

$m $m $m

Asset Enhancement 7.3 4.9 (2.4)

Asset Refurbishment and Replacement 175.4 229.9 54.5

TOTAL GRID CAPEX 182.7 234.8 52.1

Information Services and Technology (IST) 67.4 72.4 5.0

Business Support 14.1 10.2 (3.8)

TOTAL 264.1 317.4 53.3

Note: Figures may not add exactly due to rounding.

Asset refurbishment and replacement

Overall we commissioned $54 million more than the allowance, primarily driven by a completion of works initially scheduled for earlier in the RCP1 period. The main contributors to this are:

Refurbishment of Haywards Synchronous Condensers: $24 million more than forecast

due to commissioning two refurbished Synchronous Condensers (C9 &C10) and other

refurbishment work related to the condensers. We initially forecast completion in

2012/13. However commissioning was rearranged to align with the completion of Pole 3,

which was later than planned.

Buildings, Grounds and Seismic: We commissioned $13 million more than forecast due

to the need to catch up after a slower start to the programme than anticipated in the early

part of RCP1. This was due to a review of the programme and further assessment of

seismic strengthening requirements in the early part of RCP1. Over the RCP1 period the

programme has remained within the allowance.

Outdoor to indoor conversion: $8 million more due to the commissioning of five

conversions versus the four we forecast in the allowance.

Information Services and Technology (IST)

We commissioned $5 million more on the data centre because we decided to implement a

hybrid approach, resulting in higher initial expenditure of $5 million over the RCP1

allowance. This will be offset by future benefits delivered through more cost efficient data

facility upgrades.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 26

Business support

A $4 million under-spend. The RCP1 allowance assumed a move of the Wellington Head

office to a new location. This is now planned to occur in 2017/18. This underspend was

partially offset by completion of new office in Auckland at Transpower's Otahuhu site which

was not planned in the RCP1 allowance.

The table below is a summary of the CPI-adjusted base capex allowance for the full RCP1

period, compared to the actual commissioning over that period.

Table 11: Total RCP1 allowance and actual base capital expenditure (commissioned basis)

Category Allowance Actual Variance Variance

$m $m $m %

Asset Enhancement 20.9 12.8 (8.1) (38.8)

Asset Refurbishment and Replacement 737.8 693.1 (44.7) (6.1)

TOTAL GRID CAPEX 758.8 705.9 (52.8) (7.0)

Information Services and Technology (IST) 209.6 229.2 19.6 9.3

Business Support 32.2 31.0 (1.3) (3.9)

TOTAL 1,000.6 966.1 (34.5) (3.5)

Appendix A.3 sets out forecast variances and explanations for base capex over the full

RCP1 period.

5.3 Base capex adjustments

The following table summarises the adjustments relating to base capex that can apply

through RCP1 or at the end of the period.

Table 12: Adjustments that can apply to base capex

Description When it applies

Unapproved amount

Revenue is adjusted to remove the benefit of any base capex that has not been through our internal approval processes.

Each year

Conversion Expenditure that was included in the base capex allowance may instead be covered by a new major project. The base capex allowance is reduced accordingly.

Each year

CPI The base capex allowance is adjusted to account for any disparity between forecast and actual consumer price index (CPI) rates.

Each year, from 2012/13

Excess amount

Revenue is adjusted to remove the revenue benefit of any base capex that exceeds the overall allowance for RCP1.

End of RCP1

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 27

All base capex for 2014/15 has been through internal processes, so no ‘unapproved amount’

adjustment to revenue is required this year.

The Kawerau Generation Export Enhancement project was previously included in the base

capex allowance and has now been designated as a major capex project. We have reduced

our 2013/14 base capex allowance by $4.2 million accordingly.

The following table shows the base capex allowance for each year as set at the start of

RCP1, and compares CPI forecasts made at the time with actual CPI to date. This data is

used to produce an adjusted base capex allowance for 2014/15 and an updated forecast

allowance for 2014/15.

Table 13: Adjustment to base capex allowance for CPI movement

2011/12 2012/13 2013/14 2014/15

Allowance set at the start of RCP1 ($m) 208.6 301.9 240.3 278.4

Forecast CPI for the year at that time 2.40% 2.40% 2.40% 2.30%

CPI-adjusted base capex allowance ($m) n/a 295.3 232.6 264.1

Actual CPI 0.95% 0.68% 1.62% 0.42%

Note: figures are in nominal dollar terms

5.4 Historical base capex

For comparison with the figures in Table 10, the following table sets out historical base

capex for the four years of RCP1.

Table 14: Historical base capex

Category 2011/12 2012/13 2013/14 2014/15

$m $m $m $m

Basis Commissioned Commissioned Commissioned Commissioned

Enhancement and Development 4.9 3.0 - 4.9

Refurbishment and Replacement 168.9 145.9 148.5 229.8

IST 46.2 50.2 60.4 72.4

Business support 1.7 7.9 11.1 10.2

Total 221.7 207.0 220.0 317.4

Note: figures are in nominal dollar terms and may not add exactly due to rounding.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 28

5.5 RCP2 base capex

In August 2014 the Commission determined the level of our base capex ‘allowance’ for

RCP2. In RCP1 the total base capex allowance for the period was a hard threshold, above

which we would have had to repay 100%19 of the excess.

In contrast, the RCP2 allowance is more of a ‘benchmark’ against which base capex

incentive rewards or penalties are calculated. In each year of RCP2 our actual base capex

spending will be compared to the allowance for that year and our revenue for the next pricing

year will be adjusted up or down by an amount equal to 33% of the base capex under- or

over-spend. There will be no hard, full-RCP threshold, but we are incentivised year-on-year

to minimise costs.

As with RCP1, the RCP2 base capex allowance will be adjusted each year for the disparity

between forecast and actual CPI rates (see Table 13). In addition, the allowance will be

adjusted for any disparity between the forecast and actual foreign exchange rates.

The allowance for the 5 years of RCP2 is set out in the table below.

Table 15: RCP2 base capex commissioning allowance

2015/16 2016/17 2017/18 2018/19 2019/20

$m $m $m $m $m

Base capex allowance (commissioning basis)

235.2 249.5 242.0 231.6 213.1

19

100% of the future benefit we would get from the excess assets on our RAB.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 29

6 Major projects

Grid enhancement projects and programmes expected to cost more than $5 million were

approved by the Commission individually, based on an assessment of the market benefit of

the project compared to other viable alternatives. Each of these ‘major projects’ has an

approved allowance, timeframe and ‘outputs’.

This section covers:

progress reports on major projects partially commissioned during 2014/15 and close-out

reports on completed major projects

major projects newly approved by the Commission

other variations and adjustments.

6.1 Progress reports – costs

Table 16 compares the current expected cost of our partially-completed projects to the

expected cost at the time the projects were approved.

Table 16: Updated cost forecasts for partially completed major projects

Title

Major Capex

Allowance

Expected cost Expected cost

variance

Expected cost

variance Current Forecast

Original Forecast

$m $m $m $m (%)

Bunnythorpe-Haywards Reconductoring

161.0 136.7 151.0 (14.3) (9.5)

Clutha Upper Waitaki Lines Programme

196.9 45.7 147.2 (101.5) (69.0)

Upper North Island Dynamic Reactive Support20

98.2 52.9 91.4 (38.5) (42.1)

Lower South Island Reliability 62.4 31.6 55.6 (24.0) (43.2)

Upper South Island Grid Upgrade 8.0 6.6 6.6 - -

Wanganui-Stratford Transmission 44.1 25.8 42.3 (16.5) (39.0)

North Auckland and Northland grid upgrade

418.9 353.0 333.6 19.4 5.8

TOTAL 989.5 652.3 827.7 (175.4) (21.2)

Note: Figures may not add exactly due to rounding.

As with base capex, the Commerce Commission has specified ‘material variance’ as being

both more than $10 million and greater than 10% of the forecast value. Explanations for

material variances are provided below.

20

Excluding amounts in relation to demand response initiatives.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 30

Bunnythorpe-Haywards Reconductoring

We have reduced the forecast cost of the conductors (mainly sections 1 and 2) as a result of the tendering process for those portions of the project. Clutha Upper Waitaki Lines Programme (CUWLP)

The reduction on the programme forecast cost is in the context that three of the five projects of the CUWLP programme are on hold and under review. The forecast expenditures are a considered anticipation of the results of that review, but should not be taken as prejudging the circumstances that prevail at the time, and hence the outcome. Upper North Island Dynamic Reactive Support

The reduction in costs from the original budget can be attributed to two main factors. The first being for the Marsden and Penrose STATCOMs where the main contract for design, supply and installation was lower than budgeted due to contract efficiencies achieved by working in conjunction with the HVDC project and due to favourable foreign exchange rates. The second main factor has been a reduction in the forecast for the Auckland Reactive Power Controller where alternative solution approaches have been evaluated to provide outcomes at a cost $27.8 million below the original budget estimate. Lower South Island Reliability Transmission Investment

The expected cost in the approval includes $16.7 million for a 220 kV series capacitor at Three Mile Hill that is now not expected to be required until 2020 or later. This cost is excluded from the forecast end cost and we will review it before completing all remaining components of the project, and prepare a variation to the regulatory approval for the project and close it out. Other savings include the cost of two transformers and a pair of shunt capacitors being less than the forecast, and having successfully avoided draw down of $4 million of the contingencies provision. Wanganui-Stratford Transmission Investment

Construction costs were forecast to be $25.8 million including contingencies. Successful management of most construction risks meant that there was limited draw-down of contingencies and actual construction costs were $16 million. This also reflects a successful procurement strategy of awarding all line sections to a single contractor. Other savings against forecast included $2.3 million on procurement and $4.8 million on property. North Auckland and Northland Grid Upgrade

The cost increase of 6% arises principally from additional unforeseen costs in relation to cabling, together with some general cost increases caused by delayed commissioning.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 31

6.2 Progress reports – timing

The following table compares the current forecast commissioning date for partially

completed major projects with the forecast made in the last Annual Regulatory Report or at

the time the projects were approved. Material variances are explained below.

Table 17: Updated timing forecasts for partially completed major projects

Title

Forecast commissioning date

(at approval or in the 2012/13 ARR)

Forecast commissioning date

(updated)

Bunnythorpe-Haywards Reconductoring 2014 to 2020 2014 to 2020

Clutha Upper Waitaki Lines Programme 2012 to 2017 2014 to 2016

Upper North Island Dynamic Reactive Support 2011 to 2015 2011 to 2017

Lower South Island Reliability 2012 to 2015 April 2017

Upper South Island Grid Upgrade June 2018 June 2018

Wanganui-Stratford Transmission 2011 December 2017

North Auckland and Northland grid upgrade 2014 June 2016

Upper North Island Dynamic Reactive Support

The programme was affected by resource constraints caused by the HVDC project. Once the HVDC project was completed, the final component of the program (Auckland Reactive Power Controller) was deferred so an assessment could be made into alternative solution options to deliver the required solution options at lower cost. This assessment and planning is now complete, saving $27.8 million. The programme is now forecast to complete in June 2017. Lower South Island Reliability Transmission Investment

The forecast end date has been revised to April 2017 due to delay in securing designation and easements to construct a 2.25 km long 220 kV double circuit line from the 220 kV North Makarewa – Three Mile Hill A line to Gore Substation, for the new 220/110 kV interconnection at Gore. The designation over the chosen line route was obtained in late 2013. However, efforts to acquire easements through negotiations were not successful due to the 3 landowners' unwillingness to grant easements and strong preference for an outright sale of their farms to Transpower. Easements are now being pursued through the compulsory acquisition process, which is being led by Land Information New Zealand (LINZ). Wanganui-Stratford Transmission Investment

Commissioning of individual lines sections was phased more slowly than originally forecast to better manage outages and to fit with contractor resourcing. The first, second and third sections were completed in 2010, early 2012 and 2013.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 32

Substation work at Stratford and Waverly has been completed, but work at Hawera is scheduled to be completed by December 2017 so that we can minimise disruption and avoid major outages. North Auckland and Northland Grid Upgrade

The forecast end date has been affected by delays in completing the required works at Penrose substation. The delays were caused by the October 2014 fire event, installation challenges for the 220 kV Ring Bus Cable during November 2015 to March 2015 and discovery of asbestos contamination inside the old Penrose control and relay room in March 2015.

6.3 Close-out reports

Two major projects were commissioned in 2014/15.

When a project is commissioned, several revenue or allowance adjustments may occur.

The following table summarises these potential adjustments.

Table 18: Summary of possible adjustments to major projects

Adjustment Description

CPI and FX The approved allowance may be updated to account for differences between CPI and foreign exchange rates anticipated when the project was approved, and the rates that actually occurred during the project.

Excess amount If the actual cost of a project exceeds the relevant approved allowance, then a revenue adjustment is made to remove the value of the ‘excess amount’.

Output If a project does not deliver the relevant approved outputs, then a revenue adjustment may be made to remove one-third of the value of the project.

In addition to these adjustments, we may apply to the Commission for approval of an

amended allowance, and/or agreement to vary agreed project outputs.

The following tables provide close out reports for each major project completed in 2014/15:

National Auto-synchronisation Points Project

Wairakei Ring Project

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 33

6.3.1 National Auto-synchronisation Points Project

Project Description

The project is for the installation of auto synchronisation points at ten substations across the National Grid. The substations have been selected on the basis of their significance in restoring the supply to consumers and return the grid to a secure event after low probability high impact system event. The benefits of the project relate to the reduction in system average restoration times for those consumers disconnected and also avoids the need to disconnect generation and/or load in order to tie the power system together again after such an event.

Commissioned values

Final End

Cost P50 cost at approval

Variance Material?

Project costs $5.6m $9.1m ($3.5m) Y

Commissioning dates

Output Actual Approved

date Variance Material?

Designing, procuring, installing and commissioning auto synchronisation capability at ten locations: 1. Invercargill 2. Clyde 3. Bunnythorpe 4. Whakamaru 5. Whakamaru (Bay of Plenty) 6. Waitaki 7. West Coast 8. Redclyffe 9. Tuai 10. Hamilton

May 2013 to

May 2015

In parts over 2011 through

2013

Y Y

Project Outputs

Achieved Outputs Variance to Approved

Outputs?

Designing, procuring, installing and commissioning auto synchronisation capability at nine locations: 1. Invercargill 2. Clyde 3. Bunnythorpe 4. Whakamaru 5. Whakamaru/Wairakei (Bay of Plenty) 6. Waitaki 7. West Coast 8. Tuai 9. Hamilton

Y

Output adjustment

17 points were installed at 9 locations, rather than 24 points installed at 10 locations.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 34

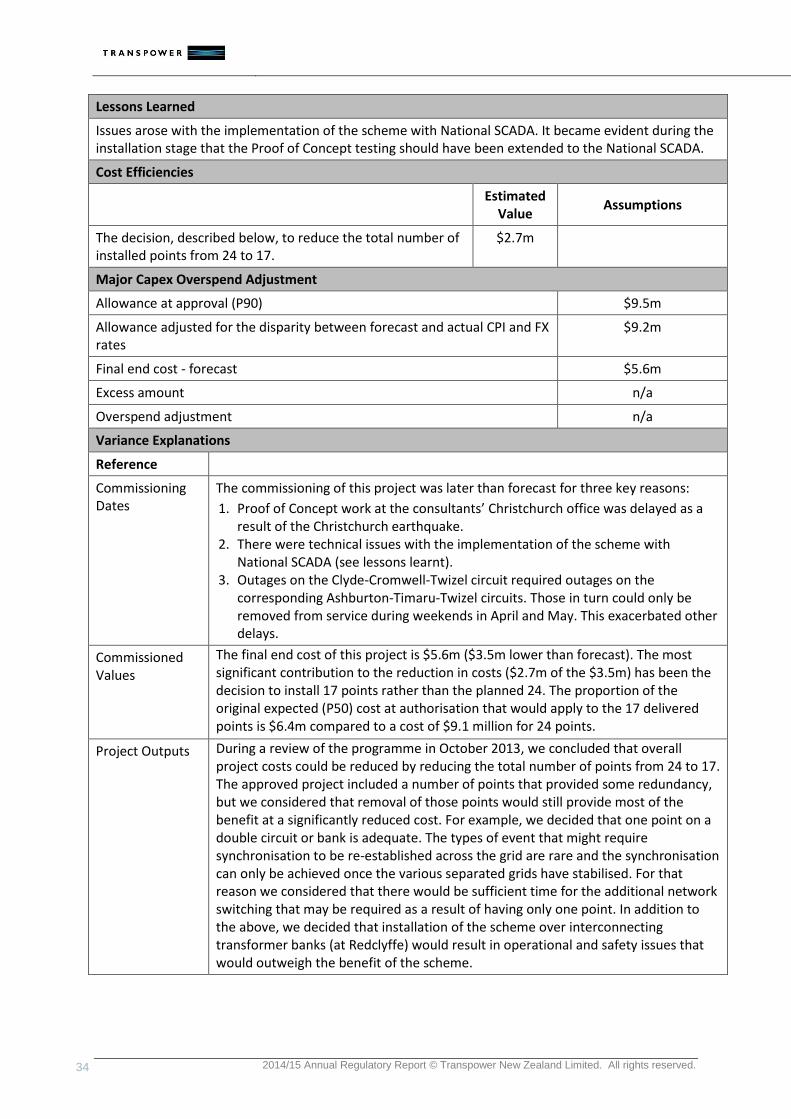

Lessons Learned

Issues arose with the implementation of the scheme with National SCADA. It became evident during the installation stage that the Proof of Concept testing should have been extended to the National SCADA.

Cost Efficiencies

Estimated

Value Assumptions

The decision, described below, to reduce the total number of installed points from 24 to 17.

$2.7m

Major Capex Overspend Adjustment

Allowance at approval (P90) $9.5m

Allowance adjusted for the disparity between forecast and actual CPI and FX rates

$9.2m

Final end cost - forecast $5.6m

Excess amount n/a

Overspend adjustment n/a

Variance Explanations

Reference

Commissioning Dates

The commissioning of this project was later than forecast for three key reasons:

1. Proof of Concept work at the consultants’ Christchurch office was delayed as a result of the Christchurch earthquake.

2. There were technical issues with the implementation of the scheme with National SCADA (see lessons learnt).

3. Outages on the Clyde-Cromwell-Twizel circuit required outages on the corresponding Ashburton-Timaru-Twizel circuits. Those in turn could only be removed from service during weekends in April and May. This exacerbated other delays.

Commissioned Values

The final end cost of this project is $5.6m ($3.5m lower than forecast). The most significant contribution to the reduction in costs ($2.7m of the $3.5m) has been the decision to install 17 points rather than the planned 24. The proportion of the original expected (P50) cost at authorisation that would apply to the 17 delivered points is $6.4m compared to a cost of $9.1 million for 24 points.

Project Outputs During a review of the programme in October 2013, we concluded that overall project costs could be reduced by reducing the total number of points from 24 to 17. The approved project included a number of points that provided some redundancy, but we considered that removal of those points would still provide most of the benefit at a significantly reduced cost. For example, we decided that one point on a double circuit or bank is adequate. The types of event that might require synchronisation to be re-established across the grid are rare and the synchronisation can only be achieved once the various separated grids have stabilised. For that reason we considered that there would be sufficient time for the additional network switching that may be required as a result of having only one point. In addition to the above, we decided that installation of the scheme over interconnecting transformer banks (at Redclyffe) would result in operational and safety issues that would outweigh the benefit of the scheme.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 35

6.3.2 Wairakei Ring Project

Project Description

The transmission lines north of Lake Taupo comprising the Wairakei Ring are a critical part of New Zealand’s National Grid. The Wairakei Ring:

enables transfer of electricity northwards into the Auckland and Bay of Plenty regions;

helps supply the Hawkes Bay region;

supports southward transfer out of the Auckland and Bay of Plenty regions during low South Island hydro periods;

transports existing geothermal generation out of the Wairakei area; and

connects to the southern end of the new 220/400 kV line at Whakamaru. Accordingly, upgrading the Wairakei Ring assists in facilitating competition and security of supply by removing constraints.

Commissioned values

Final End

Cost P50 cost at approval

Variance Material?

Project costs $140.0m $124.9m $15.1m Y

Commissioning dates

Output Actual Approved

date Variance Material?

procuring, constructing and commissioning a new double circuit line that: is capable of 220kV operation;

has a continuous rating of around 2300A per circuit;

includes the termination of both circuits at Wairakei substation;

includes the termination of one circuit into Whakamaru North substation and the other circuit into Whakamaru substation; and

has a single circuit diversion into Te Mihi substation.

From October 2013 to July

2014

Mid

2013

Y Y

procuring, constructing and commissioning substation facilities to facilitate the above connections and equipment.

From Jan 2012 to July

2014

Mid

2013 Y Y

decommissioning and dismantling components of existing connections, circuits and substations made redundant by these works.

Dec 2013 to

July 2015 April 2013 Y Y

obtaining designations, easements, resource consents and property purchases for these works.

Completed by Sept 2014

April 2013 Y Y

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 36

Project Outputs

Achieved Outputs Variance to Approved

Outputs?

procuring, constructing and commissioning a new double circuit line that: is capable of 220kV operation;

has a continuous rating of around 2300A per circuit;

includes the termination of both circuits at Wairakei substation;

includes the termination of one circuit into Whakamaru North substation and the other circuit into Whakamaru substation; and

has a single circuit diversion into Te Mihi substation.

N

procuring, constructing and commissioning substation facilities to facilitate the above connections and equipment.

N

decommissioning and dismantling components of existing connections, circuits and substations made redundant by these works.

N

obtaining designations, easements, resource consents and property purchases for these works.

N

Output adjustment n/a

Lessons Learned

Effective co-ordination of substation and line design consultants is required to ensure the design at the point of interface is practical and considers the physical aspects of the site.

Increase the level of quality assurance on site particularly in the earlier stages of individual work packages to enable discrepancies to be identified and addressed early in the process.

Ensure landowners understand what type of work activity is intended to be undertaken to minimise the risk of disputes and limit pre-construction activity to surveying and geotech activity.

Cost Efficiencies

Est. value Assumptions

n/a

Major Capex Overspend Adjustment

Allowance at approval (P90) $141.0m

Allowance adjusted for the disparity between forecast and actual CPI and FX rates

$120.5m

Final end cost - forecast $140.0m

Excess amount n/a

Overspend adjustment n/a

Variance Explanations

Commissioning dates

The final property agreements were not secured until September 2014. This combined with the decision to avoid undertaking stringing works during winter delayed the commissioning of the new circuits.

Project costs The decision to alter the transmission route to address concerns raised by the community during the consenting phase of the project resulted in an increase in civil and property costs.

Project outputs n/a

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 37

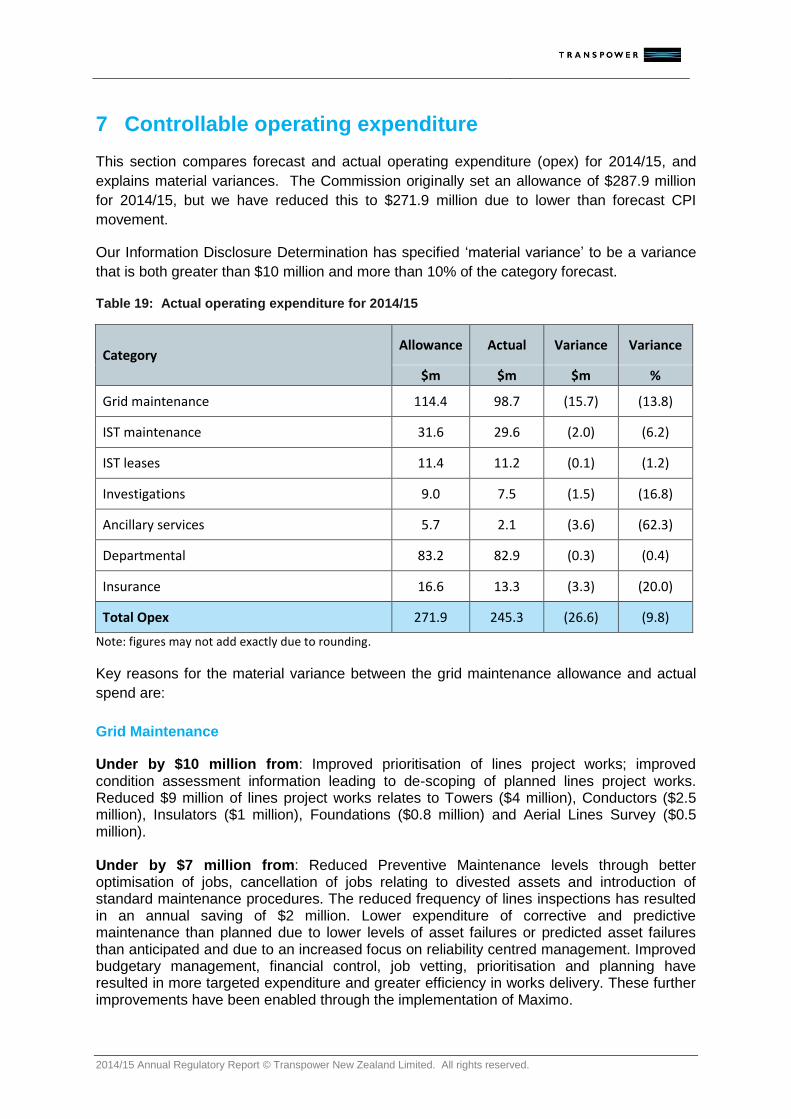

7 Controllable operating expenditure

This section compares forecast and actual operating expenditure (opex) for 2014/15, and

explains material variances. The Commission originally set an allowance of $287.9 million

for 2014/15, but we have reduced this to $271.9 million due to lower than forecast CPI

movement.

Our Information Disclosure Determination has specified ‘material variance’ to be a variance

that is both greater than $10 million and more than 10% of the category forecast.

Table 19: Actual operating expenditure for 2014/15

Category Allowance Actual Variance Variance

$m $m $m %

Grid maintenance 114.4 98.7 (15.7) (13.8)

IST maintenance 31.6 29.6 (2.0) (6.2)

IST leases 11.4 11.2 (0.1) (1.2)

Investigations 9.0 7.5 (1.5) (16.8)

Ancillary services 5.7 2.1 (3.6) (62.3)

Departmental 83.2 82.9 (0.3) (0.4)

Insurance 16.6 13.3 (3.3) (20.0)

Total Opex 271.9 245.3 (26.6) (9.8)

Note: figures may not add exactly due to rounding.

Key reasons for the material variance between the grid maintenance allowance and actual

spend are:

Grid Maintenance

Under by $10 million from: Improved prioritisation of lines project works; improved condition assessment information leading to de-scoping of planned lines project works. Reduced $9 million of lines project works relates to Towers ($4 million), Conductors ($2.5 million), Insulators ($1 million), Foundations ($0.8 million) and Aerial Lines Survey ($0.5 million). Under by $7 million from: Reduced Preventive Maintenance levels through better optimisation of jobs, cancellation of jobs relating to divested assets and introduction of standard maintenance procedures. The reduced frequency of lines inspections has resulted in an annual saving of $2 million. Lower expenditure of corrective and predictive maintenance than planned due to lower levels of asset failures or predicted asset failures than anticipated and due to an increased focus on reliability centred management. Improved budgetary management, financial control, job vetting, prioritisation and planning have resulted in more targeted expenditure and greater efficiency in works delivery. These further improvements have been enabled through the implementation of Maximo.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 38

Over by $1 million from: Lower capitalisation levels of SCADA modelling team than expected. Additional modelling resources were employed in the second half of the year to deliver the large volume of project work. Over by $3 million from: Unbudgeted Service Provider transition costs associated with our service provider reset programme. Core Grid Service Provides will reduce from 5 to 4 in 15/16 resulting in future savings in service provider overhead costs. Investigations

Lower number of investigation projects, particularly in our grid development and grid performance divisions. Ancillary Services

We have a provision of $2m for HVDC outages extending beyond 14 days (where only 50% of costs would be recoverable). There were no HVDC events in 2014/15. Insurance

Uncalled provision of $0.9 million for self-insurance in the allowance. General decrease in insurance costs.

7.1 Historical operating expenditure

For comparison, the table below shows actual operating expenditure for 2011/12 to 2014/15.

Expenditure is broken down by categories for each year.

Total operating expenditure for RCP1 was $986.4 million, compared to a CPI-adjusted

allowance of $1,062.2 million.

Table 20: Historical and forecast operating expenditure

2011/12 2012/13 2013/14 2014/15

$m $m $m $m

Grid maintenance 96.6 91.1 92.9 98.7

IST maintenance 26.6 26.1 29.1 29.6

IST leases 12.4 13.3 13.1 11.2

Investigations 12.2 10.4 8.3 7.5

Ancillary services 1.8 2.1 2.0 2.1

Departmental 80.4 94.1 90.4 82.9

Insurance 11.2 13.2 13.8 13.3

Total operating expenditure 241.3 250.2 249.6 245.3

Note: figures are in nominal dollar terms and may not add exactly due to rounding

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 39

The following table shows the opex allowance for each year as set at the start of RCP1 and

the CPI assumption at that time, together with revised opex allowances, based on actual CPI

movement to date and revised forecast CPI rates.

Table 21: Opex allowance and the CPI adjustment

2011/12 2012/13 2013/14 2014/15

Allowance set at the start of RCP1 ($m) 248.5 279.8 281.2 287.9

Forecast CPI for the year at that time 2.40% 2.40% 2.40% 2.30%

Revised opex allowance ($m) n/a 271.3 270.5 271.9

Actual CPI 0.95% 0.68% 1.62% 0.42%

Note: figures are in nominal dollar terms

7.2 RCP2 opex allowance

In August 2014 the Commission determined the level of our opex allowance for RCP2.

Our RCP2 operating expenditure is subject to incentives in the same way as for our RCP1

spending. They work in two ways. During the control period our revenue is based on the

opex allowance, rather than our actual expenditure. This enables us to retain the benefit of

efficiency savings, because ‘under-spends’ are not included in the wash-up at the end of the

year. The other way is through the Incremental Rolling Incentive Scheme (IRIS), which

extends the benefit of efficiency savings into the following control period. The objective of the

IRIS regime is that we retain the benefit of efficiency savings for a full 6 years, regardless of

when in the control period we make them. In November 2014 the Commission determined a

new version of IRIS for our RCP2 opex results, which is symmetric in its treatment of

efficiency gains or losses, but which also includes an amount to be determined by the

Commission at their discretion. We will continue to work with the Commission to ascertain

how this regime will work in practice, so that we are able to forecast to what extent

incremental savings in RCP2 will result in a net benefit in RCP3.

As with RCP1, the RCP2 opex allowance will be adjusted each year for the disparity

between forecast and actual CPI rates (seeTable 21).

The allowance for the five years of RCP2 is set out in the table below.

Table 22: RCP2 opex allowance

2015/16 2016/17 2017/18 2018/19 2019/20

$m $m $m $m $m

Operating expenditure allowance 276.6 284.6 292.5 294.0 296.4

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 40

8 Pass-through and recoverable costs

Our operating expenditure allowance is intended to be limited to controllable expenditure.

This helps to ensure that regulatory incentives to pursue efficiencies and reduce ongoing

expenditure can operate as intended.

Costs that are not controllable are treated separately and classed as either ‘pass through’ or

‘recoverable’. In both cases, we forecast costs annually and wash-up any over- or under-

recovery. These costs comprise:

Pass-through costs Recoverable costs

Local government rates

Commerce Commission levies

Electricity Authority levies.

instantaneous reserves (IR) charges21

non-transmission solutions (NTS)22.

8.1 2014/15 wash-up

The table below shows the wash up of 2014/15 pass-through and recoverable costs,

calculated by comparing the forecast costs used for pricing with the actual costs we incurred.

Table 23: Allocation of pass-through and recoverable wash-up amounts

Description TOTAL HVAC HVDC

$m $m $m

Forecast pass through costs 16.2 16.1 0.1

Actual pass-through costs 13.7 13.7 -

Wash-up amount due (to) from customers (2.5) (2.4) (0.1)

Forecast recoverable costs 6.1 5.1 1.0

Actual recoverable costs 3.1 0.6 2.5

Wash-up amount due (to) from customers (3.0) (4.5) 1.5

Total wash-up due (to) from customers (5.5) (6.9) 1.4

Note: Figures may not add exactly due to rounding.

21

We purchase back up supply (or demand interruption) from the IR market to cover the risk of a failure of the HVDC link causing an under-frequency event in the island receiving supply from the link.

22

Most major grid upgrade projects are designed to improve the reliability of the grid. In some cases, it is possible to achieve similar reliability improvements by non-transmission means (i.e., by use of a ‘non-transmission solution). For example, paying some customers to reduce their consumption at times of peak demand may defer the need for a grid upgrade.

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 41

Pass-through costs were $2.5 million lower than forecast as a result of local government

rates being $3.9 million lower than forecast, offset by Commerce Commission and Electricity

Authority levies that were $1.4 million more than forecast.

HVDC recoverable costs comprise just instantaneous reserves charges. They were $1.5

million higher than forecast.

HVAC recoverable costs comprise just non-transmission solution costs. They were $4.5

million less than we had forecast.

8.2 Historical pass-through and recoverable costs

For comparison, this section presents forecast and actual pass-through and recoverable

costs for RCP1.

Table 24: Historical pass-through and recoverable costs

2011/12 2012/13 2013/14 2014/15

$m $m $m $m

Pass-through costs

Forecast 13.4 13.4 13.0 16.2

Actual 10.1 11.0 14.2 13.7

HVAC wash-up (3.3) (2.4) 1.5 (2.4)

HVDC wash-up - - (0.3) (0.1)

Recoverable costs

Forecast 25.8 9.7 3.2 6.1

Actual 18.5 9.1 3.0 3.1

HVAC wash-up (6.7) 0.7 0.6 (4.5)

HVDC wash-up (0.7) (1.3) (0.9) 1.5

Note: figures are in nominal dollar terms and may not add exactly due to rounding.

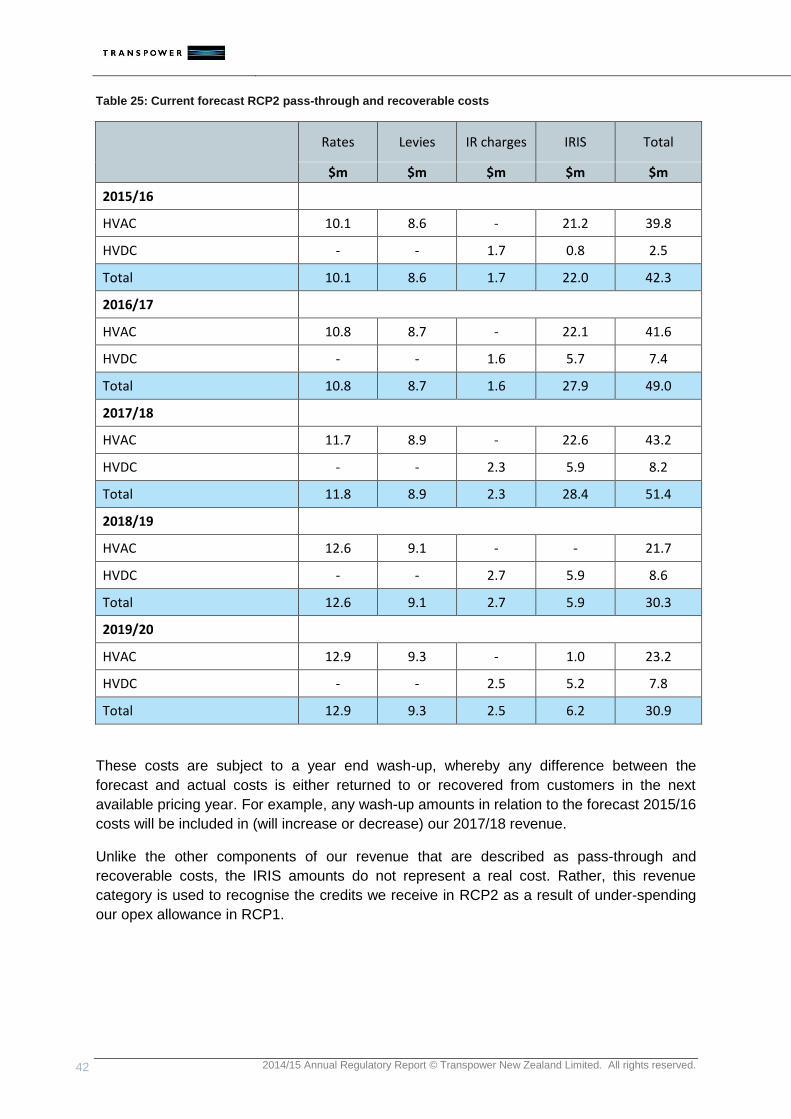

8.3 Forecast pass-through and recoverable costs

The table below shows the forecast of the pass-through and recoverable costs that has been

included in our recent revenue forecast (see Section 2.1).

2014/15 Annual Regulatory Report © Transpower New Zealand Limited. All rights reserved. 42

Table 25: Current forecast RCP2 pass-through and recoverable costs

Rates Levies IR charges IRIS Total

$m $m $m $m $m

2015/16

HVAC 10.1 8.6 - 21.2 39.8

HVDC - - 1.7 0.8 2.5

Total 10.1 8.6 1.7 22.0 42.3

2016/17

HVAC 10.8 8.7 - 22.1 41.6

HVDC - - 1.6 5.7 7.4

Total 10.8 8.7 1.6 27.9 49.0

2017/18

HVAC 11.7 8.9 - 22.6 43.2

HVDC - - 2.3 5.9 8.2

Total 11.8 8.9 2.3 28.4 51.4

2018/19

HVAC 12.6 9.1 - - 21.7