annual financial statements - sa corporate real estate …

TRANSCRIPT

ANNUAL FINANCIALSTATEMENTS

SA CORPORATE REAL ESTATE FUND

SA CORPORATE REAL ESTATE FUNDContents To The Audited Annual Financial Statements

Page

DIRECTORS' RESPONSIBILITY............................................................................................................... 1

REPORT OF THE TRUSTEE..................................................................................................................... 2

INDEPENDENT AUDITOR'S REPORT......................................................................................................... 3

STATEMENTS OF FINANCIAL POSITION................................................................................................... 5

STATEMENTS OF COMPREHENSIVE INCOME............................................................................................ 6

STATEMENTS OF CHANGES IN UNITHOLDERS' FUNDS.............................................................................. 7

STATEMENTS OF CASH FLOWS.............................................................................................................. 9

NOTES TO THE ANNUAL FINANCIAL STATEMENTS.................................................................................... 10

APPENDIX A: STATUTORY INFORMATION.............................................................................................. 42

APPENDIX B: PROPERTY PORTFOLIO REVIEW......................................................................................... 43

APPENDIX C: PROPERTY PORTFOLIO.................................................................................................... 45

Cover pictures from left to right: Nampak, Denver, 530 Nicholson Road, Doornfontein, GautengCeltis Ridge Shopping Centre, CenturionWorld Trade Center, Sandton, Gauteng

SA CORPORATE REAL ESTATE FUND MANAGERS LIMITEDContents To The Audited Annual Financial Statements

Page

DIRECTORS' RESPONSIBILITY............................................................................................................... 49

DECLARATION BY THE SECRETARY........................................................................................................ 49

INDEPENDENT AUDITOR'S REPORT........................................................................................................ 50

REPORT OF THE AUDIT COMMITTEE....................................................................................................... 51

DIRECTORS' REPORT............................................................................................................................ 53

STATEMENT OF FINANCIAL POSITION.................................................................................................... 56

STATEMENT OF COMPREHENSIVE INCOME.............................................................................................. 57

STATEMENT OF CHANGES IN EQUITY...................................................................................................... 57

STATEMENT OF CASH FLOWS................................................................................................................ 58

NOTES TO THE ANNUAL FINANCIAL STATEMENTS.................................................................................... 59

ANNUAL FINANCIAL STATEMENTS 2013 1

RJ Biesman-SimonsChairman - Audit Committee

The directors of SA Corporate Real Estate Fund Managers Limited are responsible for the preparation and integrity ofthe annual financial statements and the related information included in the SA Corporate Real Estate Fund (“the Fund”)and all its subsidiaries (“the Group”) annual financial statements. In order for the Board to discharge its responsibilities,management has developed and continues to maintain a system of internal control. The Board has ultimate responsibilityfor the system of internal control and reviews its operation, primarily through the Risk and Compliance Committee andAudit Committee.

The internal controls include a risk-based system of internal accounting and administrative controls designed to providereasonable but not absolute assurance that the assets are safeguarded and that transactions are executed and recordedin accordance with generally accepted business practices and the Group and the Fund's policies and procedures. Thesecontrols are implemented by trained, skilled personnel with appropriate segregation of duties, are monitored by managementand the Risk, Audit and Compliance Committee, which was split into the Risk and Compliance Committee and AuditCommittee with effect from 1 January 2013, and include a comprehensive budgeting and reporting system operatingwithin an appropriate control framework.

The external auditors are responsible for reporting on the annual financial statements, and their opinion is included onpages 3 and 4. The annual financial statements are prepared in accordance with International Financial ReportingStandards and the requirements of the Collective Investment Schemes Control Act, No. 45 of 2002, and incorporatedisclosures in line with the accounting practices of the Group and the Fund. They are based on appropriate accountingpolicies consistently applied, except where otherwise stated, and are supported by reasonable judgements and estimates.

The directors believe that the Group and the Fund will be a going concern in the year ahead. Accordingly, in preparingthe annual financial statements, the going concern basis has been adopted.

The annual financial statements for the year ended 31 December 2013 as set out on pages 5 to 48 were approved bythe Board of Directors on 28 February 2014 and are signed on its behalf by:

J MolobelaIndependent Non-Executive Chairman

These annual financial statements have been prepared under the supervision of:AM BassonCA (SA)Financial Director

DIRECTORS’ RESPONSIBILITYFor And Approval Of The Annual Financial Statements

SA CORPORATE REAL ESTATE FUND2

To the unitholders of SA Corporate Real Estate Property FundAs Trustee to the SA Corporate Real Estate Trust Scheme (“the Scheme”), we are required, in terms of the CollectiveInvestment Schemes Control Act, 2002 (Act No. 45 of 2002) (“the CISCA”), to report to the unitholders on the administrationof the Scheme during each annual accounting period.

We advise, for the year 1 January 2013 to 31 December 2013, we reasonably believe that the Manager has administeredthe Scheme in accordance with:

i.) the limitations imposed on the investment and borrowing powers of the manager by the CISCA; and ii.) the provisions of the CISCA and the relevant deeds.

We confirm that, according to the records available to us, there were no material instances of compliance contraventionsand therefore no consequent losses incurred by the portfolio in the year.

Nelia De Beer Marian Rutters

First National Bank, a division of FirstRand Bank LimitedTrustee28 February 2014

1st Floor, 3 First Place, Bank CityCnr Simmons & Jeppe StreetsJohannesburg2001

REPORT OF THE TRUSTEEFor the year ended 31 December 2013

World Trade Center, Sandton, Gauteng

ANNUAL FINANCIAL STATEMENTS 2013 3

We have audited the consolidated and separate financial statements of SA Corporate Real Estate Fund set out on pages5 to 41, which comprise the statements of financial position as at 31 December 2013, and the statements of comprehensiveincome, statements of changes in unitholders' funds and statements of cash flows for the year then ended, and thenotes, comprising a summary of significant accounting policies and other explanatory information.

Directors' Responsibility for the Consolidated Financial StatementsThe Fund's directors are responsible for the preparation and fair presentation of these consolidated and separate financialstatements in accordance with International Financial Reporting Standards and the requirements of the CollectiveInvestment Schemes Control Act, No. 45 of 2002, and for such internal control as the directors determine is necessaryto enable the preparation of financial statements that are free from material misstatement, whether due to fraud orerror.

Auditor's ResponsibilityOur responsibility is to express an opinion on these consolidated and separate financial statements based on our audit.We conducted our audit in accordance with International Standards on Auditing. Those standards require that we complywith ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidatedand separate financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financialstatements. The procedures selected depend on the auditor's judgement, including the assessment of the risks of materialmisstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the entity's preparation and fair presentation of the financial statements in orderto design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinionon the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accountingpolicies used and the reasonableness of accounting estimates made by management, as well as evaluating the overallpresentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the consolidated and separate financial statements present fairly, in all material respects, the consolidatedand separate financial position of SA Corporate Real Estate Fund as at 31 December 2013, and its consolidated andseparate financial performance and consolidated and separate cash flows for the year then ended in accordance withInternational Financial Reporting Standards and the requirements of the Collective Investment Schemes Control Act,No. 45 of 2002.

INDEPENDENT AUDITOR’S REPORTTo The Unitholders Of SA Corporate Real Estate Fund

SA CORPORATE REAL ESTATE FUND4

Other reportsAs part of our audit of the consolidated and separate financial statements for the year ended 31 December 2013 wehave read the Report of the Trustee for the purpose of identifying whether there are material inconsistencies betweenthis report and the audited consolidated and separate financial statements. This report is the responsibility of the Trustee.Based on reading this report we have not identified material inconsistencies between this report and the auditedconsolidated and separate financial statements. However, we have not audited this report and accordingly do not expressan opinion on this report.

Deloitte & ToucheRegistered Auditors

Per: GG FortuinPartner28 February 20141st FloorThe SquareCape Quarter27 Somerset RoadCape Town8005

National Executive: LL Bam Chief Executive AE Swiegers Chief Operating Officer GM Pinnock Audit DL Kennedy RiskAdvisory NB Kader Tax TP Pillay Consulting K Black Clients & Industries JK Mazzocco Talent & Transformation CR BeukmanFinance M Jordan Strategy S Gwala Special Projects TJ Brown Chairman of the Board MJ Comber Deputy Chairman ofthe BoardRegional Leader: MN Alberts

A full list of partners and directors is available on request

B-BBEE rating: Level 2 contributor in terms of the Chartered Accountancy Profession Sector Code

Member of Deloitte Touche Tohmatsu Limited

INDEPENDENT AUDITOR’S REPORT (continued)To The Unitholders Of SA Corporate Real Estate Fund

Comaro Crossing, Oakdene, Gauteng

ANNUAL FINANCIAL STATEMENTS 2013 5

STATEMENTS OF FINANCIAL POSITIONas at 31 December 2013

Group Fund2013 2012 2013 2012

Notes R000 R000 R000 R000

Assets

Non-current assetsInvestment in subsidiary companies 7 - - 3 583 961 3 312 431 Shares - - 1 175 653 881 291 Loans - - 2 408 308 2 431 140 Investment property 8 8 654 251 7 733 791 5 084 554 4 352 314 Letting commissions and tenant installations 8 63 116 53 521 30 068 30 778 Interest rate swap derivatives 14 39 644 2 854 39 644 2 854 Rental receivable straight line adjustment 8 170 408 199 851 111 525 135 555

8 927 419 7 990 017 8 849 752 7 833 932

Current assetsProperties classified as held for disposal 9 - 182 900 - 124 900 Trade and other receivables 10 162 780 129 142 94 186 62 044 Letting commissions and tenant installations 9 - 835 - 171 Current portion of loans to subsidiary companies 7 - - 77 726 96 234 Capital gains taxation in subsidiary companies - 824 - -Interest rate swap derivatives 14 382 - 382 - Rental receivable - straight line rental adjustment 8 40 566 33 233 26 421 20 681 Cash and cash equivalents 11 311 520 407 281 306 964 373 401

515 248 754 215 505 679 677 431

Total assets 9 442 667 8 744 232 9 355 431 8 511 363

Unitholders' funds and liabilities

Unitholders' funds 12 7 280 242 6 973 355 7 280 247 6 973 359

Non-current liabilitiesInterest-bearing borrowings 13 1 625 913 620 975 1 625 913 620 975 Deferred taxation 15 - 146 744 - -

1 625 913 767 719 1 625 913 620 975

Current liabilitiesTrade and other payables 16 198 506 171 317 111 024 85 189 Current portion of interest-bearing borrowings 13 - 520 000 - 520 000Current portion of loans from subsidiary companies 7 - - 241 - Capital gains taxation - 56 - 55 Distributions payable 17 326 030 305 475 326 030 305 475 Interest rate swap derivatives 14 11 976 6 310 11 976 6 310

536 512 1 003 158 449 271 917 029

Total unitholders' funds and liabilities 9 442 667 8 744 232 9 355 431 8 511 363

SA CORPORATE REAL ESTATE FUND6

STATEMENTS OF COMPREHENSIVE INCOMEfor the year ended 31 December 2013

Group Fund2013 2012 2013 2012

Notes R000 R000 R000 R000

Revenue 6 1 186 412 1 227 838 600 749 644 726

IncomeRent 878 077 893 877 508 008 524 810 Straight line rental adjustment 8 (24 419) 8 177 (19 537) 5 155 Recovery of property expenses 332 754 325 784 112 278 114 761 Income from associate company - 1 402 - 1 402 Interest income - 1 402 - 1 402 Interest income 20 811 30 547 19 170 29 506 Dividends from subsidiary companies - - 309 218 293 952

1 207 223 1 259 787 929 137 969 586ExpensesAccounting and secretarial fees (6 082) (5 893) (4 330) (3 296)Audit fees (1 845) (1 661) (1 845) (1 661)Administrative fees (10 460) (11 594) (9 599) (11 368)Interest expense (94 562) (139 202) (94 517) (139 117)Property administration fees (29 118) (35 200) (9 944) (12 740)Property expenses (412 714) (407 387) (163 597) (160 163)Service fees (37 435) (35 559) (25 314) (20 273)

(592 216) (636 496) (309 146) (348 618)

Operating income 615 007 623 291 619 991 620 968

Amortisation of debt restructure costs (10 504) (32 739) (10 504) (32 739)Revaluation of interest rate swap derivatives 14 31 506 (30 141) 31 506 (30 141)Capital loss on disposal of investmentproperties / investments (4 086) (20 075) (3 581) (6 538)Capital profit on disposal of investment in associate - - - 6 254 Revaluation of investment properties / investments 8 380 625 246 236 222 665 194 184 Revaluation of subsidiary companies - - 299 318 (9 101)

Profit before taxation 1 012 548 786 572 1 159 395 742 887

Taxation credit / (charge) 19 146 846 (49 939) - -

Profit after taxation attributable to unitholders 1 159 394 736 633 1 159 395 742 887

Other comprehensive income, net of taxation 10 516 27 473 10 516 27 473Amounts subsequently reclassified to profit or loss

Amortisation of hedge reserve arising on early derivativesettlements 10 516 27 473 10 516 27 473

Total comprehensive income attributable to unitholders 1 169 910 764 106 1 169 911 770 360

ANNUAL FINANCIAL STATEMENTS 2013 7

Non- distributable Distributable

Capital reserves reserves TotalR000 R000 R000 R000

GROUP

Unitholders' funds at 1 January 2012 7 076 649 (108 882) - 6 967 767

Total comprehensive income for the year - 27 473 736 633 764 106 Profit after taxation - - 736 633 736 633 Amortisation of hedge reserve - 27 473 - 27 473Capital items transferred to non-distributable reserves - 120 820 (120 820) - Revaluation of interest rate swap derivatives - (30 141) 30 141 - Revaluation of investment properties - 246 236 (246 236) - Capital loss on disposal of investment properties - (20 075) 20 075 - Taxation on property revaluation and disposals - (49 792) 49 792 - Straight line rental adjustment net of taxation - 7 331 (7 331) - Amortisation of hedge reserve - (27 473) 27 473 - Early debt settlement cost - (5 266) 5 266 - 42 879 535 units repurchased (142 489) - - (142 489)Unit repurchase cost (216) - - (216)Lapsed distribution on units repurchased - - 795 795

6 933 944 39 411 616 608 7 589 963Distributions attributable to unitholders - - (616 608) (616 608)

Unitholders' funds at 31 December 2012 6 933 944 39 411 - 6 973 355

Total comprehensive income for the year - 10 516 1 159 394 1 169 910 Profit after taxation - - 1 159 394 1 159 394 Amortisation of hedge reserve - 10 516 - 10 516Capital items transferred to non-distributable reserves - 519 866 (519 866) - Revaluation of interest rate swap derivatives - 31 506 (31 506) - Revaluation of investment properties - 380 625 (380 625) - Capital loss on disposal of investment properties - (4 086) 4 086 - Reversal of taxation on property revaluation - 124 929 (124 929) - Straight line rental adjustment net of taxation - (2 604) 2 604 - Amortisation of hedge reserve - (10 516) 10 516 - Other - 12 (12) -58 896 063 units repurchased (222 986) - - (222 986)Unit repurchase cost (509) - - (509)Lapsed distribution on units repurchased - - 8 823 8 823

6 710 449 569 793 648 351 7 928 593Distributions attributable to unitholders - - (648 351) (648 351)

Unitholders' funds at 31 December 2013 6 710 449 569 793 - 7 280 242

STATEMENTS OF CHANGES IN UNITHOLDERS’ FUNDSfor the year ended 31 December 2013

SA CORPORATE REAL ESTATE FUND8

STATEMENTS OF CHANGES IN UNITHOLDERS’ FUNDS (continued)for the year ended 31 December 2013

Non- distributable Distributable

Capital reserves reserves TotalR000 R000 R000 R000

FUND

Unitholders' funds at 1 January 2012 7 076 615 (115 098) - 6 961 517

Total comprehensive income for the year - 27 473 742 887 770 360 Profit after taxation - - 742 887 742 887 Amortisation of hedge reserve - 27 473 - 27 473 Capital items transferred to non-distributable reserves - 127 074 (127 074) - Revaluation of interest rate swap derivatives - (30 141) 30 141 - Revaluation of investment properties / investments - 185 083 (185 083) - Capital loss on disposal of investment properties - (6 538) 6 538 - Capital profit on disposal of associate - 6 254 (6 254) - Straight line rental adjustment - 5 155 (5 155) - Amortisation of hedge reserve - (27 473) 27 473 - Early debt settlement cost - (5 266) 5 266 -42 879 535 units repurchased (142 489) - - (142 489)Unit repurchase cost (216) - - (216)Lapsed distribution on units repurchased - - 795 795

6 933 910 39 449 616 608 7 589 967 Distribution attributable to unitholders - - (616 608) (616 608)

Unitholders' funds at 31 December 2012 6 933 910 39 449 - 6 973 359

Total comprehensive income for the year - 10 516 1 159 395 1 169 911 Profit after taxation - - 1 159 395 1 159 395 Amortisation of hedge reserve - 10 516 - 10 516 Capital items transferred to non-distributable reserves - 519 867 (519 867) - Revaluation of interest rate swap derivatives - 31 506 (31 506) - Revaluation of investment properties / investments - 521 983 (521 983) - Capital loss on disposal of investment properties - (3 581) 3 581 - Straight line rental adjustment - (19 537) 19 537 - Amortisation of hedge reserve - (10 516) 10 516 - Other - 12 (12) -58 896 063 units repurchased (222 986) - - (222 986)Unit repurchase cost (509) - - (509)Lapsed distribution on units repurchased - - 8 823 8 823

6 710 415 569 832 648 351 7 928 598 Distribution attributable to unitholders - - (648 351) (648 351)

Unitholders' funds at 31 December 2013 6 710 415 569 832 - 7 280 247

ANNUAL FINANCIAL STATEMENTS 2013 9

Group Fund2013 2012 2013 2012

Notes R000 R000 R000 R000

Cash flows from operating activitiesProfit after taxation 1 159 394 736 633 1 159 395 742 887 Adjustments for: Interest income (20 811) (30 547) (19 170) (29 506) Income from associate company - (1 402) - (1 402) Interest expense 94 562 139 202 94 517 139 117 Allowance for doubtful debt movement 692 (14 427) 3 794 (3 990) Provision for VAT 5 717 5 925 5 717 5 925 Amortisation of letting commissions and tenant installations 25 369 30 687 15 010 14 260 Taxation (credit) / charge (146 846) 49 939 - - Revaluation of investment properties / investments (excluding straight line adjustment) (356 206) (254 413) (502 446) (190 238) Interest rate swap revaluation derivatives and amortisation of debt restructure costs (20 990) 62 880 (20 990) 62 880 Capital loss on disposal of investment properties / investments 4 086 20 075 3 581 6 538 Capital profit on disposal of associate - - - (6 254)

Operating profit before working capital changes 744 967 744 552 739 408 740 217

Working capital changes (19 333) 31 663 (22 296) 6 202 (Increase) / Decrease in trade and other receivables (34 667) 49 843 (36 276) 22 284 Increase / (Decrease) in trade and other payables 15 334 (18 180) 13 980 (16 082)

Cash generated from operations 725 634 776 215 717 112 746 419

Interest received 21 148 30 547 19 510 29 506 Interest income from associate company - 1 402 - 1 402 Interest paid (90 215) (139 202) (89 840) (139 117)Taxation refund received / (paid) 870 (1 742) (55) - Distributions paid 17 (627 796) (612 544) (627 796) (612 561)Net cash inflow from operating activities 29 641 54 676 18 931 25 649

Cash flows from investing activitiesSettlement of interest rate swap derivatives 14 - (59 230) - (59 230)Increase in investment properties / investments 8 (591 201) (117 946) (551 115) (58 404)Proceeds on disposal of investment properties / investments 230 497 754 034 163 244 513 538 Increase in letting commissions and tenant installations 8 (34 964) (43 929) (14 300) (22 266)Proceeds on disposal of investment in associate - 175 208 - 175 208Decrease in loans to subsidiary companies - - 46 537 207 3701

Net cash (outflow) / inflow from investing activities (395 668) 708 137 (355 634) 756 216

Cash flows from financing activitiesRepurchase of units (222 986) (142 489) (222 986) (142 489)Unit repurchase cost (509) (216) (509) (216)Lapsed distribution on units repurchased 8 823 795 8 823 795 Early debt settlement cost - (5 266) - (5 266)Increase / (Decrease) in interest-bearing borrowings 484 938 (582 007) 484 938 (582 007)Net cash inflow / (outflow) from financing activities 270 266 (729 183) 270 266 (729 183)

Net (decrease) / increase in cash and cash equivalents (95 761) 33 630 (66 437) 52 682 Cash and cash equivalents at the beginning of the year 407 281 373 651 373 401 320 719 Cash and cash equivalents at the end of the year 11 311 520 407 281 306 964 373 401

1This amount was included in “Proceeds on disposal of investments” and is now disclosed separately.

STATEMENTS OF CASH FLOWSfor the year ended 31 December 2013

SA CORPORATE REAL ESTATE FUND10

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTSfor the year ended 31 December 2013

1. General informationSA Corporate Real Estate Fund (“the Fund”), established in the Republic of South Africa, is a collective investmentscheme in property established in terms of the Collective Investment Schemes Control Act, No. 45 of 2002. TheFund is listed on the JSE Limited. The Fund is managed by SA Corporate Real Estate Fund Managers Limited, acompany approved by the Registrar of Collective Investment Schemes to manage the Fund.

2. Adoption of new and revised International Financial Reporting StandardsIn the current year the Group and the Fund has adopted all of the new and revised Standards and Interpretationsissued by the International Accounting Standards Board (“the IASB”) and the IFRS Interpretations Committee(“IFRIC”) of the IASB that are relevant to its operations and effective for accounting periods beginning on or before1 January 2013. The adoption of these standards and interpretations has not resulted in any adjustment to theamounts previously reported in the Annual Financial Statements for the year ended 31 December 2012.

3. Accounting policiesThe Annual Financial Statements have been prepared in accordance with International Financial Reporting Standards(“IFRS”). The accounting policies used in the preparation of the financial statements are consistent with thoseapplied in the prior year. The financial statements have been prepared on the going concern and historical costbases, except where otherwise stated.

The principal accounting policies are set out below:

3.1 Basis of consolidationThe Group Annual Financial Statements incorporate the results and financial position of the Fund and all itssubsidiaries. The results of subsidiaries are included from the effective dates of gaining control and up to the effectivedates of relinquishing control. All inter-entity transactions and balances between Group entities are eliminated.

The accounting policies of the subsidiaries are consistent with those of the Fund.

3.2 Business combinationsThe purchase method of accounting is used to account for the acquisition of subsidiaries by the Group. The costof an acquisition is measured as the aggregate of the fair value of the underlying assets acquired, equity instrumentsissued and liabilities incurred or assumed at the date of exchange. Cost directly attributable to the acquisition isrecognised in profit or loss. Identifiable assets acquired and liabilities and contingent liabilities assumed in a businesscombination are measured initially at their fair values at the acquisition date. The excess of the cost of the acquisitionover the fair value of the Group's share of the identifiable net assets acquired is recorded as goodwill. Goodwill isnot amortised and is tested for impairment on an annual basis.

If the cost of the acquisition is less than the fair value of the net assets of the subsidiary acquired, the differenceis recognised directly in profit or loss. An impairment loss recognised for goodwill is not reversed in a subsequentperiod. On disposal of a subsidiary, attributable goodwill is included in the determination of the profit or loss ondisposal.

3.3 Investment in subsidiariesInvestments in subsidiary companies are revalued to fair value at each reporting date. Surpluses or deficits onrevaluation or disposal are reflected in profit or loss and transferred to capital in the statement of changes inunitholders' funds.

3.4 Investment propertiesInvestment properties are properties held to earn rentals and appreciate in capital value. Investment propertiesare initially recognised at cost, including transaction costs on acquisition, and are stated at their fair value at eachreporting date. These fair values of property exclude accrued operating lease income. Gains or losses arising fromchanges in the fair values are reflected in profit or loss in the year in which they arise and are transferred to non-distributable reserves in the statement of changes in unitholders' funds.

ANNUAL FINANCIAL STATEMENTS 2013 11

3.4 Investment properties (continued)Properties purchased by the Group and settled by the issuing of units are recorded at the fair value of the propertiesacquired, unless that fair value cannot be reliably measured, in which case they are measured at the fair value ofthe units granted in terms of IFRS 2: Share Based Payments. This excludes purchases of properties which areregarded as business combinations as described in note 3.2.

New buildings that are acquired and developed for future use as investment property as well as existing investmentproperty that is redeveloped for continued future use as investment property are carried at fair value.

Properties held under long term operating leases are classified and accounted for as investment properties.

Partially held investment property is treated as a jointly controlled asset as the co-owners jointly control the property.The following is therefore recognised in the annual financial statements:� the undivided share of the jointly controlled assets, classified according to the nature of the assets;� any liabilities incurred;� any income from the sale or use of the undivided share of the output of the partially held investment property, together with the share of any expenses incurred by the partially held investment property; and� any expenses incurred in respect of the interest held in the partially held investment property.

3.5 Borrowing costsWhere a fixed property company undertakes a major development or refurbishment of its property, interest iscapitalised to the cost of the property concerned during the construction period. Where a property, owned by theFund, undertakes a major development or refurbishment, interest is capitalised to the extent that it is directlyincurred in the course of development.

All other borrowing costs are recognised in profit or loss in the period in which they are incurred.

3.6 Assets held for saleProperties and other non-current assets which have been earmarked for sale and have met the recognition criteriain terms of IFRS 5: Non-Current Assets Held for Sale and Discontinued Operations are classified as non-currentassets held for sale. Properties held for sale are measured at fair value in terms of IAS 40: Investment Property.Other assets held for sale are measured at their fair value less costs to sell.

3.7 TaxationThe Fund is treated as a trust for income taxation purposes and no liability for taxation arises on its profits to theextent that it is distributed by the Fund. The Fund's capital profit is exempt from capital gains taxation.

The subsidiary companies are subject to taxation. For these companies the income tax expense comprises the sumof current taxation payable and deferred taxation. Taxable profit differs from accounting profit as it excludes incomeor expenses that are taxable or deductible in other years and it excludes items never deductible or taxable.

Deferred taxation is provided for using the liability method based on temporary differences. Temporary differencesare differences between the carrying amounts of assets and liabilities for financial reporting purposes and theirtaxation bases. Deferred taxation is charged to profit or loss, except to the extent that it relates to a transactionthat is recognised directly in equity, or a business combination that is an acquisition. A deferred taxation asset isrecognised to the extent that it is probable that future taxable profits will be available against which the associatedunused tax losses and deductible temporary differences can be utilised. Deferred taxation assets are reduced tothe extent that it is no longer probable that the related tax benefit will be realised.

Deferred taxation assets and liabilities are not recognised if the temporary differences arise from goodwill, or fromthe initial recognition (other than business combinations) of other assets and liabilities in a transaction which affectsneither the taxable profit nor the accounting profit.

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

SA CORPORATE REAL ESTATE FUND12

3.8 Impairment (excluding goodwill)The carrying amount of the Group's assets is reviewed at each reporting date to determine whether there is anyindication of impairment. An impairment loss is recognised in profit or loss whenever the carrying amount of anasset exceeds its recoverable amount, which is the higher of an asset's net selling price and value in use. Wheneveran impairment loss is subsequently reversed, the carrying amount of the asset is increased to the extent that theincreased carrying amount does not exceed the original carrying amount. A reversal of impairment loss is recognisedimmediately in profit or loss.

3.9 Financial instrumentsA financial asset or financial liability is recognised for as long as the Group or Fund is party to the contractualprovisions of the instrument.

3.9.1 Non-derivative financial instrumentsNon-derivative financial instruments recognised on the statement of financial position include cash and cashequivalents, trade and other receivables, investments, unitholders' funds, interest- bearing borrowings and tradeand other payables.

a. Financial assets

i. Initial recognitionFinancial assets are initially measured at fair value plus, for instruments not at fair value through profit orloss (“FVTPL”), any directly attributable transaction costs. Subsequent to initial recognition, non-derivativefinancial instruments are measured as described below.

Financial assets are classified into the following specified categories: 'at FVTPL', 'held to maturity' investments,'available for sale' and 'loans and receivables'. The classification depends on the nature and purpose of thefinancial assets and is determined at the time of initial recognition.

ii. Financial assets at FVTPLA financial asset is classified as at FVTPL if it is held for trading or is designated as such upon initial recognition.

A financial asset is classified as held for trading if:� it has been acquired principally for the purpose of selling in the near future; or� it is a part of an identified portfolio of financial instruments that the Group manages together and has a recent actual pattern of short-term profit-taking; or� it is a derivative that is not designated and effective as a hedging instrument.

A financial asset other than a financial asset held for trading may be designated as at FVTPL upon initialrecognition if:� such designation eliminates or significantly reduces a measurement or recognition inconsistency that would otherwise arise; or� the financial asset forms part of a group of financial assets or financial liabilities or both, which is managed

and its performance is evaluated on a fair value basis, in accordance with the Group's documented risk management or investment strategy, and information about the grouping is provided internally on that basis; or� it forms part of a contract containing one or more embedded derivatives, and IAS 39 Financial Instruments:

Recognition and Measurement permits the entire combined contract (asset or liability) to be designatedas at FVTPL.

Financial assets at FVTPL are measured at fair value, and changes therein are recognised in profit or loss.

Investments in fixed property companies have been designated as at FVTPL.

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

ANNUAL FINANCIAL STATEMENTS 2013 13

3.9.1 Non-derivative financial instruments (continued)iii. Held-to-maturity investments

Held-to-maturity investments are recorded at amortised cost using the effective interest method less anyimpairment losses.

The Group and the Fund does not currently have any held-to-maturity investments.

iv. Available for sale financial assetsGains and losses arising from changes in fair value of available for sale financial assets, other than impairmentlosses, are recognised directly in equity. Where the investment is disposed of, the cumulative gain or losspreviously recognised in equity is transferred to profit or loss.

v. Loans and receivablesTrade receivables, loans, and other receivables that have fixed or determinable payments that are not quotedin an active market are classified as loans and receivables. Loans and receivables are measured at amortisedcost using the effective interest method, less any impairment.

vi. Derecognition of financial assetsThe Group and Fund derecognises a financial asset only when the contractual rights to the cash flows fromthe asset expire; or it transfers the financial asset and substantially all the risks and rewards of ownershipof the asset to another entity. If the Group and Fund neither transfers nor retains substantially all the risksand rewards of ownership and continues to control the transferred asset, the Group and Fund recognisesits retained interest in the asset and an associated liability for amounts it may have to pay. If the Group andFund retains substantially all the risks and rewards of ownership of a transferred financial asset, the Groupand Fund continues to recognise the financial asset and also recognises a collateralised borrowing for theproceeds received.

b. Financial liabilities

Financial liabilities are classified as either financial liabilities at FVTPL or other financial liabilities.

i. Financial liabilities at FVTPLFinancial liabilities are classified as at FVTPL where the financial liability is either held for trading or it isdesignated as at FVTPL.

ii. Other financial liabilitiesOther financial liabilities, including borrowings, are initially measured at fair value, net of transaction costs.

Other financial liabilities are subsequently measured at amortised cost using the effective interest method,with interest expense recognised on an effective yield basis.

The effective interest method is a method of calculating the amortised cost of a financial liability and ofallocating interest expense over the relevant period. The effective interest rate is the rate that exactlydiscounts estimated future cash payments through the expected life of the financial liability, or, whereappropriate, a shorter period.

iii. Derecognition of financial liabilitiesThe Group and Fund derecognises financial liabilities when, and only when, the Group's and Fund's obligationsare discharged, cancelled or they expire.

3.9.2 Derivative financial instrumentsThe Group and Fund use derivative financial instruments to manage its exposure to interest rate risk exposures.At inception, these instruments are either designated as cash flow hedges, or not, on an item by item basis.

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

SA CORPORATE REAL ESTATE FUND14

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

3.9.2 Derivative financial instruments (continued)Derivative financial instruments designated as a hedge:Changes in the fair value of designated cash flow hedging instruments are recognised in other comprehensiveincome and accumulated in equity to the extent that the hedge is effective. The ineffective portion of any gainor loss is recognised immediately in profit or loss.

If the hedging instrument no longer meets the criteria for hedge accounting, expires, or is sold, terminated orexercised then hedge accounting is discontinued prospectively. The cumulative gain or loss previously recognisedin equity remains there until the forecast transaction occurs. When the hedged item is a non-financial asset, theamount recognised in equity is transferred to the carrying amount of the asset when it is recognised. In othercases the amount recognised in equity is transferred to profit or loss in the same period that the hedged itemsaffects profit or loss.

Derivative financial instruments not designated as a hedge:Derivative financial instruments not designated as cash flow hedging instruments are accounted for as financialinstruments at FVTPL.

The fair value of the interest rate swaps is the estimated amount that the Group and Fund would receive or payto terminate the swap at the reporting date, taking into account current interest rates and the current creditworthiness of the swap counterparties.

3.10 ProvisionsProvisions are recognised when the Group and Fund have a present legal or constructive obligation as a result ofpast events, for which it is probable that an outflow of economic benefits will occur, and where a reliable estimatecan be made on the settlement amount of the obligation.

3.11 Revenue recognitionRevenue comprises gross rental income, including all recoveries from tenants. Variable operating cost recoveriesare recognised on the accrual basis. Rental income and fixed operating costs recoveries are recognised on thestraight line basis in accordance with IAS 17: Leases. Turnover rental income is recognised on the accrual basisand measured at fair value.

Interest income is recognised at the effective rates of interest on a time related basis.

Dividends are recognised when the right to receive them is established.

3.12 LeasesInvestment properties leased out under operating leases are reflected as investment properties on the statementof financial position. Where there are fixed increments in rental, the income is recognised on a straight line basisin accordance with IAS 17: Leases.

3.13 Deferred expensesDeferred expenses comprise tenant installation costs and letting commissions which are amortised on a straightline basis over the lease period to which they relate. The tenant installations and letting commissions are separatelydisclosed. As at date of disposal, the unamortised deferred expense is included in the capital profit or loss of theproperty.

3.14 DistributionsIn terms of the Collective Investment Schemes Act, No. 45 of 2002 the Fund is obliged to distribute to its unitholdersall net revenue profit earned and received. The Fund has elected to use its annual distributable income growth asits measurement to evaluate if a Trading Statement is required in accordance with the JSE Listings requirements.

3.15 Segment reportingInformation reported to the Group's chief operating decision makers, being the executive directors, for the purposesof resource allocation and assessment of its performance, is based on the economic sectors in which the investmentproperties operate.

ANNUAL FINANCIAL STATEMENTS 2013 15

3.15 Segment reporting (continued)On a primary basis the Group operates in the following reportable segments:� Retail� Industrial� Commercial

3.16 Unitholders' fundsUnitholders' funds represent the residual interest in the Group's and Fund's assets after deducting all of its liabilitiesand have been accounted for as equity. Units issued by the Group and Fund are recognised at the proceeds received,net of direct issue cost. Units repurchased by the Group and Fund are recognised and deducted directly in equity.No gain or loss is recognised in profit or loss on the purchase, sale, issue or cancellation of the Fund's own units.

4. Critical accounting estimates and judgementsEstimates and judgements are continually evaluated and are based on historical experience as adjusted for currentmarket conditions and other factors.

The Group and Fund makes estimates and assumptions concerning the future. The resulting accounting estimateswill, by definition, seldom equal the related actual results. The estimates or assumptions that have a significantrisk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial yearare discussed below.

(a) Estimate of the fair value of investment propertiesThe best evidence of fair value is current prices in an active market for similar leases and other contracts. Inthe absence of such information, the Group and Fund determines the amount within a range of reasonablefair value estimates. In making its judgment the Group and Fund considers information from a variety ofsources including:

� Current prices in an active market for properties of different nature, condition or location (or subject to different lease or other contracts), adjusted to reflect those differences;� Recent prices of similar properties in less active markets, with adjustments to reflect any changes in economic conditions since the date of the transactions that occurred at those prices; and� Discounted cash flow projections based on reliable estimates of future cash flows, derived from the terms

of any existing leases and other contracts and (where possible) from external evidence such as current market rents for similar properties in the same location and condition, and using discount rates that reflect

current market assessments of the uncertainty in the amount and timing of the cash flows.

Principal assumptions of management's estimation of fair valueIf information on current or recent prices is not available, the fair values of investment properties are determinedusing discounted cash flow valuation techniques. The Group and Fund used assumptions that are mainly basedon market conditions existing at each reporting date.

The principal assumptions underlying management's estimation of fair value are those related to:The receipt of contracted rentals, expected future market rentals, lease renewals, maintenance requirementsand appropriate discount and capitalisation rates. These valuations are regularly compared to actual marketyield data, actual transactions by the Group and the Fund and those reported by the market.

The expected future market rentals are determined with reference to current market rentals for similarproperties in the same location and condition.

(b) Doubtful debt provisionAll legal arrears that have been summonsed, as well as tenants with arrears older than 90 days, have beenprovided against. Exceptions are applied based on an assessment of the individual debtor.

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

SA CORPORATE REAL ESTATE FUND16

5. New accounting standards and IFRIC interpretationsCertain new accounting standards and IFRIC interpretations have been published that are applicable for futureaccounting periods. These new standards and interpretations have not been early adopted by the Group and Fund.The directors do not expect that the adoption of the standards and interpretations will have a material impact onfuture financial statements. The amended and new standards and interpretations in issue, but not yet effective,that are relevant to the Group and Fund are:

IFRS 7 Financial Instruments: Disclosures (effective 1 July 2015);IFRS 9 Financial Instruments (effective 1 January 2015);IFRS 10 Consolidated Financial Statements (effective 1 January 2014);IFRS 12 Disclosure of Interests in Other Entities (effective 1 January 2014);IAS 27 Separate Financial Statements (effective 1 January 2014);IAS 32 Financial Instruments: Presentation (effective 1 January 2014);IAS 36 Impairment of Assets (effective 1 January 2014); andIFRIC 21 Levies (effective 1 January 2014)

The Group and Fund adopted the following new and revised accounting standards and circular in the current year:

IFRS 7 Financial Instruments: Disclosures;IFRS 10 Consolidated Financial Statements;IFRS 11 Joint Arrangements;IFRS 12 Disclosure of Interests in Other Entities;IFRS 13 Fair Value Measurement;IAS 1 Presentation of Financial Statements;IAS 32 Financial Instruments: Presentation; andCircular 2/2013 Headline Earnings

The adoption of these new and revised accounting standards and circular has not resulted in any restatement ofinformation previously presented but has resulted in increased disclosure.

Group Fund2013 2012 2013 2012R000 R000 R000 R000

6. RevenueOperating lease income 861 528 876 136 507 277 520 691Turnover based operating lease income 16 549 17 741 731 4 119Total operating lease income 878 077 893 877 508 008 524 810

Straight line rental adjustment (24 419) 8 177 (19 537) 5 155 Recovery of property expenses 332 754 325 784 112 278 114 761

1 186 412 1 227 838 600 749 644 726

7. Investment in subsidiary companiesThe Fund has pledged and ceded the shares and loan accounts of certain of its subsidiary companies, to secureloan facilities of R500m by Old Mutual Specialised Finance Proprietary Limited (2012: R500m). At 31 December2013 the balance owing to Old Mutual Specialised Finance Proprietary Limited was R500m (2012: R500m). Referto note 13 for details of borrowings.

The Fund's claims against Madison Park Properties 24 Proprietary Limited and Jrad Investments Proprietary Limitedhave been subordinated in favour of outside creditors to the extent of the deficit on shareholder funds in thesecompanies. The total deficit on the shareholder funds in these companies amount to R93 680 000 (2012:R98 636 000).

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

ANNUAL FINANCIAL STATEMENTS 2013 17

7. Investment in subsidiary companies (continued)

The following property owning subsidiaries, incorporated in South Africa, are wholly owned by SA Corporate RealEstate Fund Nominees Proprietary Limited, as nominee of the Fund:

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

Fund Fund Fund2013 2012 2013 2012 2013 2012R000 R000 R000 R000 R000 R000

Current loans Non-current loans Investment

Fixed property companies Blue Heron Proprietary Limited 559 740 8 563 8 560 40 238 35 444 Dune Lark Investments Proprietary Limited 467 188 6 686 6 686 20 214 18 059 Erf 84-85-86 Shakas Head Proprietary Limited 907 (278) 14 968 13 665 11 709 10 538 Grey Heron Investments Proprietary Limited 120 402 4 273 4 273 19 227 15 651 Jrad Investments Proprietary Limited 117 (233) 34 806 31 063 - -1

Madison Park Properties 24 Proprietary Limited (211) 14 588 - 36 171 - -2

Rock Kestrel Investments Proprietary Limited 406 466 1 801 1 801 5 899 5 349 SA Retail Properties Proprietary Limited 63 981 66 751 2 229 124 2 224 061 911 485 653 940 Stondell Investments Proprietary Limited (30) (5) 1 489 1 489 5 299 4 440 Umlazi Mega City Proprietary Limited 8 450 8 793 65 153 65 153 63 835 52 557 Whirlprops 25 Proprietary Limited 1 696 4 457 36 133 32 906 53 857 47 200 Wood Ibis Investments Proprietary Limited 1 023 365 5 312 5 312 43 890 38 113

77 485 96 234 2 408 308 2 431 140 1 175 653 881 291

Current portion of loans to subsidiary companies 77 726 96 234Current portion of loans from subsidiary companies (241) -

77 485 96 234

The intercompany loans are unsecured, interest free and have no fixed repayment terms.

1 After reclassification of R10m impairment of investment to non-current loan in the prior year.2 After reclassification of R89m impairment of investment to non-current loan in the prior year.

PWC, 102 Essenwood Road, Durban, KwaZulu-Natal

SA CORPORATE REAL ESTATE FUND18

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

Group Fund2013 2012 2013 2012R000 R000 R000 R000

8. Investment property and lettingcommissions and tenant installationsCarrying value at beginning of year 7 733 791 7 812 992 4 352 314 4 350 282 at valuation 7 903 575 7 178 125 4 445 250 4 194 700 straight line rental adjustment (233 084) (210 833) (156 236) (137 118) property under development 63 300 845 700 63 300 292 700

Acquisitions and improvements 592 992 117 946 552 576 58 404 at valuation 591 201 111 053 551 115 52 729 property under development - 5 375 - 5 375

capitalised interest# 1 791 1 518 1 461 300

Disposals (81 848) - (41 754) -

Fair value adjustment 380 625 246 236 222 665 194 184 at valuation 356 206 253 788 203 128 198 714 straight line rental adjustment 24 419 (8 177) 19 537 (5 155) property under development - 625 - 625

Net transfer from property under development (79 800) (788 400) (41 800) (235 400)Net transfer to investment property 79 800 788 400 41 800 235 400

Transfer of properties classified as held for disposal 28 691 (443 383) (1 247) (250 556) at valuation 31 000 (429 309) - (236 593) straight line rental adjustment (2 309) (14 074) (1 247) (13 963)

Carrying value at end of year 8 654 251 7 733 791 5 084 554 4 352 314 at valuation 8 722 125 7 903 575 5 117 400 4 445 250 straight line rental adjustment (210 974) (233 084) (137 946) (156 236) property under development 143 100 63 300 105 100 63 300

Letting commissions and tenant installations

Carrying value at beginning of year 53 521 41 114 30 778 22 943 Amortisation during the year (25 369) (30 687) (15 010) (14 260)Additions during the year 34 964 43 929 14 300 22 266 Transfer to property held for disposal * - (835) - (171)Carrying value at end of year 63 116 53 521 30 068 30 778

# As detailed in note 18.* As detailed in note 9.

The fair value of the entire portfolio of investment properties, excluding properties subject to unconditional contracted sales,was determined by independent registered valuers, ACRES, based on the discounted cash flow method and approved on 28February 2014 by the Board of Directors.

ANNUAL FINANCIAL STATEMENTS 2013 19

2013 2012

Terminal TerminalDiscount capitalisation Discount capitalisation

rates (%) rates (%) rates (%) rates (%)

Industrial 13.75 - 15.50 8.25 - 10.00 14.25 - 16.25 8.75 - 10.75Retail 13.50 - 16.25 8.00 - 10.75 13.50 - 17.50 8.00 - 12.00Commercial 14.50 - 16.00 9.00 - 10.50 14.50 - 16.00 9.00 - 10.50

Certain properties are subject to mortgage bonds in favour of Absa Bank Limited, Old Mutual Specialised Finance ProprietaryLimited and Rand Merchant Bank, a division of FirstRand Bank Limited as detailed in note 13.

The table below analyses the investment properties that are measured at fair value, subsequent to initial recognition andprovides information about the fair value hierarchy.

Level 3 (defined in note 26):Group Fund

2013 2012 2013 2012R000 R000 R000 R000

Investment properties: at valuation 8 722 125 7 903 575 5 117 400 4 445 250 property under development 143 100 63 300 105 100 63 300

8. Investment property and letting commissions and tenant installations (continued)

The independent valuers applied current market related assumptions to the risks in rental streams of properties. Discount ratesin the respective sectors ranged as follows:

9. Properties classified as held fordisposalCarrying value at beginning of year 182 900 527 700 124 900 422 050 Net transfer (to) / from investment properties (31 000) 429 309 - 236 593 Transfer (to) / from investment properties (31 000) 413 309 - 226 705 Revaluation adjustment of buildings disposed or classified as held for disposal - 16 000 - 9 888 Disposal (151 900) (774 109) (124 900) (533 743)Carrying value at end of year - 182 900 - 124 900 Straight line rental adjustment - (2 309) - (1 246)

Straight line rental adjustment - 2 309 - 1 246 Carrying value at end of year - 182 900 - 124 900

Letting commissions and tenant installationsCarrying value at beginning of year 835 - 171 - Transfer from investment property * - 835 - 171 Disposals (835) - (171) -Carrying value at end of year - 835 - 171

* As detailed in note 8

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

SA CORPORATE REAL ESTATE FUND20

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

Group Fund2013 2012 2013 2012R000 R000 R000 R000

10. Trade and other receivables Trade receivables 44 558 47 415 15 486 14 978 Allowance for doubtful debts (27 921) (27 229) (10 010) (6 216)Trade receivables net of allowance for doubtful debts * 16 637 20 186 5 476 8 762 Other receivables and accrued interest 146 143 108 956 88 710 53 282

162 780 129 142 94 186 62 044 * As detailed in note 26.

11. Cash and cash equivalents Cash and cash equivalents include cash on hand and in banks.

Cash and bank balances 24 098 27 248 19 501 11 339 Money markets investments and call accounts 254 482 345 124 254 482 345 124 Distributions account 181 316 181 316 Tenant deposit 32 759 34 593 32 800 16 622

311 520 407 281 306 964 373 401

The tenant deposit and distributions accounts are not availablefor use by the Group and Fund, as it relates to the tenant depositand unclaimed distributions liabilities included in payables

12. Unitholders' funds Capital 1 980 093 014 (2012: 2 038 989 077) units 6 710 449 6 933 944 6 710 415 6 933 910 Non-distributable reserves 569 793 39 411 569 832 39 449

7 280 242 6 973 355 7 280 247 6 973 359

Nampak, Denver, 530 Nicholson Road, Doornfontein, Gauteng

ANNUAL FINANCIAL STATEMENTS 2013 21

12. Unitholders' funds (continued) The non-distributable reserves include items of a capital nature which may not be distributed to the unitholders in terms ofthe Trust Deed.

The statement of changes in unitholders' funds reflects a detailed analysis of movements in unitholders' funds.

The Board approved the implementation of a unit repurchase programme for which approval was given by the unitholders atthe annual general meeting in 2012. In terms of the programme, a portion of the proceeds from the sale of the properties canbe used to repurchase units in the open market which would then be cancelled. During January 2013 and February 2013, theprogramme was concluded by the repurchase of 58 896 063 units at an average price of 378.61 cents per unit (2012: 42 879535 units at an average price of 332.30 cents per unit).

Group Fund2013 2012 2013 2012R000 R000 R000 R000

13. Interest bearing borrowingsAbsa Bank Limited 1 124 787 619 835 1 124 787 619 835 Loan bearing interest at 6.775% per annum. Refer # for repayment dates. 399 831 399 835 399 831 399 835

Loan bearing interest at 6.775% per annum.Refer # for repayment dates. 299 957 220 000 299 957 220 000

Loan bearing interest at 6.375% per annum.Refer # for repayment dates. 359 999 - 359 999 -

Loan bearing interest at 6.375% per annum.Refer # for repayment dates. 65 000 - 65 000 -

Old Mutual Specialised Finance Proprietary Limited 500 000 500 000 500 000 500 000 Loan bearing interest at 6.833% per annum. Thisloan is repayable on 30 September 2018. 270 000 270 000 270 000 270 000

Loan bearing interest at 6.833% per annum. Thisloan is repayable on 30 September 2018. 30 000 30 000 30 000 30 000

Loan bearing interest at 7.642% per annum. Thisloan is repayable on 29 April 2015. 200 000 200 000 200 000 200 000

Rand Merchant Bank, a division of FirstRand Bank LimitedLoan bearing interest at 7.154% per annum.This loan is repayable on 25 July 2016 1 126 21 140 1 126 21 140

1 625 913 1 140 975 1 625 913 1 140 975 Non-current borrowings 1 625 913 620 975 1 625 913 620 975 Current borrowings - 520 000 - 520 000

1 625 913 1 140 975 1 625 913 1 140 975

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

SA CORPORATE REAL ESTATE FUND22

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

13. Interest bearing borrowings (continued)

# These loans were restructured as at 31 December 2013 as follows and changes are effective in September 2014.Previous structure - Effective at December 2013

2013 Total facility RepaymentR000 R000 date

Facility A 399 831 400 000 11 September 2014Facility B 299 957 300 000 31 December 2014Facility C 359 999 360 000 30 June 2014Facility D 65 000 390 000 30 June 2014

1 124 787 1 450 000

New structure - Effective September 2014Total facility Repayment

R000 dateFacility A 500 000 31 December 2016Facility B 300 000 31 December 2015Facility C 650 000 30 June 2015

1 450 000

Interest rate risk is mitigated by interest rate swap derivatives for all loans as detailed in note 14.

The fair value of the interest-bearing borrowings excluding the effect of interest rate swaps as at 31 December 2013 amountsto R1 626m (2012: R1 141m).

These loans are secured by first mortgage bonds over a portion of the property portfolio to the value of R4 399m (2012:R3 692m), as listed below and in note 8, as well as the cession of shares and loan accounts of certain of the Fund's propertycompanies as indicated in note 7.

Property

ABSA Bank Limited199 North Ridge Road - Durban21 Fricker Road - Illovo37 Yaldwyn Road - Jet Park40 Electron Avenue - Isando57 Sarel Baard Crescent - Centurion88 Loper Avenue - Aeroport9 Milner Road - Paarden Eiland (Tableview Industrial Park)90 Electron Avenue - IsandoAtterbury Décor - PretoriaCheckers - Somerset WestCnr Rudo Nel & Tudor Streets - Jet ParkCnr Staal & Stephenson Road - PretoriaEast Rand Galleria - DurbanMidway Mews - MidrandMusgrave Centre - Durban

Old Mutual Specialised Finance Proprietary Limited111 Mimets Road - Denver112 Yaldwyn Road - Jet Park2 Fobian Street - Boksburg27 Jet Park Road - Jet Park5 Yaldwyn Road - Jet ParkBeryl Street - Jet ParkBluff Shopping Centre - Durban

ANNUAL FINANCIAL STATEMENTS 2013 23

13. Interest bearing borrowings (continued)

Old Mutual Specialised Finance Proprietary Limited (continued)Cnr Handel & Crownwood Roads - OrmondeMontana Crossing - PretoriaStellenbosch Square - StellenboschWhirlprops 25 P Proprietary Limited - Durban

Rand Merchant Bank, a division of FirstRand Bank Limited1 Baltex Road - Isipingo1 Holwood Park La Lucia10 Yarborough Road - Pietermaritzburg11 Columbine Place - Red Hill36 Wierda Rd West - Sandton6 - 9 Mahogany Road - Mahogany Ridge6 Cedarfield Close - DurbanComaro Crossing - OakdeneLebombo Road - PretoriaNobel Street Office Park - Bloemfontein

The Fund is subject to, and is in compliance with, the following covenants:

2013 2012Covenants Ratio Ratio

ABSA Bank Limited� Interest cover ratio >2.00 >2.00� Transactional interest cover ratio >1.60 >1.60 � Total loan to value <0.40 <0.30� Transactional loan to value (excluding mark to market values) <0.65 -� Transactional loan to value (including mark to market values) <0.75 -� Total borrowings to total assets (excluding negative mark to market values) - <0.60 � Total borrowings to total assets (including negative mark to market values) - <0.65

Old Mutual Specialised Finance Proprietary Limited� Interest cover ratio >2.00 >2.00 � Security portfolio loan to value <0.50 <0.50 � Total loan to value <0.30 <0.30 � Security tenancy level >0.90 >0.90 � Vacancy level <0.10 <0.10 � Hedging - total debt <0.15 <0.15

Rand Merchant Bank, a division of FirstRand Bank Limited� Interest-bearing debt asset ratio <0.30 <0.30 � Facility outstandings mortgaged asset value ratio <0.35 <0.35 � Interest cover ratio >2.50 >2.50 � Facility interest cover ratio >2.50 >2.50 � Net asset value >R 3.5bn >R 3.5bn

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

SA CORPORATE REAL ESTATE FUND24

Group Fund2013 2012 2013 2012R000 R000 R000 R000

13. Interest bearing borrowings (continued)Debt funding capacityLoan and guarantee facilities 1 625 913 1 140 975 1 625 913 1 140 975 Unutilised facility 523 917 258 860 523 917 258 860 Overdraft facility 38 000 38 000 38 000 38 000 Total facilities in place 2 187 830 1 437 835 2 187 830 1 437 835 Difference between facility and debt funding capacity 471 738 1 007 098 453 653 945 929 Total debt funding capacity 2 659 568 2 444 933 2 641 483 2 383 764 Plus / (Less): Net interest rate swap asset / (liability) 28 050 (3 456) 28 050 (3 456)Less: Facility utilised (1 625 913) (1 140 975) (1 625 913) (1 140 975)

Debt funding capacity available at end of year 1 061 705 1 300 502 1 043 620 1 239 333 Adjusted for future capital commitments and proceeds ondisposal (34 323) 78 544 (13 119) 57 715 Total capital commitments (34 323) (31 284) (13 119) (25 518) Expected proceeds on disposal - 109 828 - 83 233

Anticipated available debt capacity 1 027 382 1 379 046 1 030 501 1 297 048

14. Interest rate swap derivatives Designated and accounted for at fair value through profit or loss

Non-current asset 39 644 2 854 39 644 2 854Current asset 382 - 382 - Current liability (11 976) (6 310) (11 976) (6 310)Carrying amount of net asset / (liability) 28 050 (3 456) 28 050 (3 456)

Carrying value at beginning of year (3 456) (32 545) (3 456) (32 545)Fair value adjustment 31 506 (30 141) 31 506 (30 141)Settlement - 59 230 - 59 230Carrying value at end of year 28 050 (3 456) 28 050 (3 456)

Interest rate swap agreements, for 3 - 7 years linked to JIBAR,have been concluded to convert floating rates to fixed rates. Thetotal nominal value of the swaps is R1 375m (2012: R720m).

The Fund carries the derivatives as financial assets and liabilitiesat fair value through profit or loss.

The following table indicates the periods in which the netundiscounted cash flows are expected to occur and impact profitor loss:

Expected cash inflow / (outflow) 39 269 (945) 39 269 (945)Not later than 1 year (11 872) (6 517) (11 872) (6 517)Later than 1 year and not later than five years 44 301 (816) 44 301 (816)More than 5 years 6 840 6 388 6 840 6 388

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

ANNUAL FINANCIAL STATEMENTS 2013 25

Group Fund2013 2012 2013 2012R000 R000 R000 R000

15. Deferred taxationBalance at the beginning of year 146 744 95 363 - - (Credited) / Charged to the statement of comprehensiveincome (146 744) 51 381 - -

Balance at the end of year - 146 744 - -

Comprising:Revaluation of investment properties - 146 744 - -

During the year, the JSE Limited approved the Fund's applicationfor the Real Estate Investment Trust (“REIT”) status. SACorporate will qualify as a REIT with effect from thecommencement of its next financial year, being 1 January 2014.In determining the aggregate capital gain or capital loss of aREIT or a controlled property company for purposes of theEighth Schedule of the Income Tax Act of 1958, as amended,any capital gain or capital loss determined in respect of thedisposal of immovable property; or a share in a controlledproperty company, must be disregarded. This resulted in areversal of the Group's deferred taxation liability.

16.Trade and other payablesTrade and other payables 197 160 170 283 109 721 84 197 Unclaimed distributions 1 346 1 034 1 303 992

198 506 171 317 111 024 85 189

The Group and Fund have cash management policies in place to ensure that all amounts are paid within the credit time frame.

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

Davenport Square Shopping Centre, Bulwer Road, Durban, KwaZulu-Natal

SA CORPORATE REAL ESTATE FUND26

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

Group Fund2013 2012 2013 2012R000 R000 R000 R000

17. Distributions payableBalance at the beginning of year 305 475 301 411 305 475 301 428 Distribution attributable to unitholders 648 351 616 608 648 351 616 608 Distributions paid (627 796) (612 544) (627 796) (612 561)Balance at the end of year 326 030 305 475 326 030 305 475

18. Capitalisation of interestInterest capitalised during development phases 1 791 1 518 1 461 300

Interest was capitalised at annual rates ranging from 7.1% to9.9% (2012: 8.3% to 8.8%)

The capitalised interest is included in the investment propertyas detailed in note 8

19. TaxationCurrent income taxation 102 1 442 - - Deferred taxation 146 744 (51 381) - - Deferred capital gains taxation * 124 929 (50 535) - - Deferred taxation on straight line rental adjustment 21 815 (846) - -

Total taxation credited / (charged) 146 846 (49 939) - -

Deferred taxation is not provided on the revaluation of propertiesowned by fixed property companies (2012: 18.7% which wasthe capital gains taxation rate). Refer note 15.

* Excluded from headline earnings

Taxation rate reconciliation % % % %

Standard rate 18.7 18.7 - -Change in capital gain taxation inclusion rate - 4.0 - -Non-taxable income (6.7) (3.0) - -Distributions vested in beneficiary (12.0) (14.6) - -Deferred taxation asset not recognised - 0.1 - -Reversal of deferred taxation balance on conversion to a REIT (14.5) - - -Utilisation of assessed losses - 1.1 - -

Effective rate (14.5) 6.3 - -

The taxation credit in the current year is primarily attributable to the revaluation adjustment credited through profit or loss.

ANNUAL FINANCIAL STATEMENTS 2013 27

19. Taxation (continued)

No taxation is provided for against operating profit, to the extent that it is declared as a tax deductible distribution in terms ofsection 11(s) of the Income Tax Act. Therefore the Group reconciles the capital gains tax rate to the effective taxation rate.

Deductible temporary differences and unutilised tax losses for which no deferred tax asset has been raised.

Group Fund2013 2012 2013 2012R000 R000 R000 R000

Deferred taxation on investment property - 18 302 - - Estimated taxation losses 14 377 16 185 - -

14 377 34 487 - -

20. Earnings and diluted earnings per unitThe calculation of earnings and diluted earnings per unit are based on a net profit of R1 159 394 000 (2012: R736 633 000)of the Group and 1 985 702 979 (2012: 2 057 569 388) weighted number of units in issue during the year. Earnings and dilutedearnings per unit are 58.39 cents (2012: 35.80 cents).

21. Headline earnings per unitThe calculation of headline earnings per unit is based on headline earnings of R657 824 000 (2012: R559 565 000) of the Groupand 1 985 702 979 (2012: 2 057 569 388) weighted number of units in issue during the year.

Reconciliation of headline earnings and distribution attributable to unitholders:

Group Group2013 2013 2012 2012R000 CPU R000 CPU

Profit after taxation 1 159 394 58.39* 736 633 35.80* Adjustments for: Capital loss on disposal of investment properties 4 086 20 075 Taxation on capital profit on disposal of investment properties (102) (1 442) Revaluation of investment properties (no taxation effect) (380 625) (245 611) Revaluation of investment property under development - (625) (Reversal of taxation) / taxation on revaluation (124 929) 50 535 Headline earnings 657 824 33.13* 559 565 27.20* Straight line rental adjustment 24 419 (8 177)Taxation on straight line rental adjustment (21 815) 846 Amortisation of debt restructure costs 10 504 32 739 Other 102 699 Revaluation of interest rate swap derivatives (31 506) 30 141 Lapsed distribution on units repurchased 8 823 795 Distributable income attributable to unitholders 648 351 32.75 616 608 30.15

Interim 322 315 16.28 311 133 15.17 Final 326 036 16.47 305 475 14.98

* Weighted average cents per unit

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

SA CORPORATE REAL ESTATE FUND28

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

Group Fund2013 2012 2013 2012R000 R000 R000 R000

22. DistributionAvailable for distribution 648 351 616 608 648 351 616 608

cents cents cents centsper unit per unit per unit per unit

No. 35 declared 20 August 2012, paid 01 October 2012 15.17 15.17 No. 36 declared 22 February 2013, paid 25 March 2013 14.98 14.98No. 37 declared 26 August 2013, paid 30 September 2013 16.28 16.28 No. 38 declared 28 February 2014, paid 31 March 2014 16.47 16.47Distributions declared 32.75 30.15 32.75 30.15

23. Operating lease arrangements The minimum future lease payments receivable under

non-cancellable operating leases are as follows: R000 R000 R000 R000

Not later than 1 year 882 695 842 384 524 627 464 638 Later than one year and not later than 5 years 1 735 469 1 878 632 1 011 174 1 059 813 Later than 5 years 251 669 321 962 172 008 241 462

2 869 833 3 042 978 1 707 809 1 765 913

24. Operating lease expense andcommitmentsRent paid recognised as an expense:

Minimum rental expense 9 656 2 457 34 12 Contingent rental expense 666 2 563 - - Total rental expense 10 322 5 020 34 12

The minimum future lease payments payable undernon-cancellable operating leases are as follows:

Not later than 1 year 12 042 3 269 - - Later than 1 year and not later than 5 years 43 096 14 148 - - Later than 5 years 217 572 238 600 - - 272 710 256 017 - -The minimum future sub-lease payments receivable undernon-cancellable operating leases are as follows:

Not later than 1 year 70 511 58 795 - - Later than 1 year and not later than 5 years 724 295 164 159 - - Later than 5 years 79 661 3 024 - - 874 467 225 978 - -

Operating lease expense relates to leases of land with leases expiring between 2025 and 2054.

Operating lease income relates to leases expiring between 2014 and 2029.

The contingent rental expense is calculated as a percentage of either the valuation or the net rental income generated by the property.

ANNUAL FINANCIAL STATEMENTS 2013 29

Industrial Retail Commercial Corporate GroupR000 R000 R000 R000 R000

25. Segment results2013 Information on reportable segments

Revenue 472 533 611 248 102 631 - 1 186 412

Rental income (excluding straight line rentaladjustment) 416 930 374 746 86 401 - 878 077Net property expenses (45 084) (47 785) (16 209) - (109 078) Property administration fees (5 611) (21 649) (1 858) - (29 118) Property expenses (104 099) (274 537) (34 078) - (412 714) Recovery of property expenses 64 626 248 401 19 727 - 332 754

Net property income 371 846 326 961 70 192 - 768 999Straight line rental adjustment (9 023) (11 899) (3 497) - (24 419)Income from associate company - - - - -Interest income - - - 20 811 20 811 Interest expense - - - (94 562) (94 562)Amortisation of debt restructure costs - - - (10 504) (10 504)Group expenses - - - (55 822) (55 822)Capital loss on disposal of investment properties (619) (1 575) (1 892) - (4 086)Revaluation of investment properties 165 273 198 739 16 613 - 380 625 Investment properties 156 250 186 840 13 116 - 356 206 Straight line rental adjustment 9 023 11 899 3 497 - 24 419Revaluation of interest rate swap derivatives - - - 31 506 31 506 Taxation 22 700 124 146 - - 146 846

Net profit / (loss) attributable to unitholders 550 177 636 372 81 416 (108 571) 1 159 394

Properties 3 781 276 3 832 793 1 040 182 - 8 654 251 At valuation 3 796 600 3 866 125 1 059 400 - 8 722 125 Straight line rental adjustment (120 424) (71 332) (19 218) - (210 974) Under development 105 100 38 000 - - 143 100

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

Stellenbosch Square, Western Cape

SA CORPORATE REAL ESTATE FUND30

STATUTORY INFORMATION AND

NOTES TO THE ANNUAL FINANCIAL STATEMENTS (continued)for the year ended 31 December 2013

Industrial Retail Commercial Corporate GroupR000 R000 R000 R000 R000

25. Segment results (continued)

2012 Information on reportable segments

Revenue 473 486 654 095 100 257 - 1 227 838

Rental income (excluding straight line rentaladjustment) 389 648 421 518 82 711 - 893 877Net property expenses (34 092) (64 945) (17 766) - (116 803) Property administration fees (5 973) (27 477) (1 750) - (35 200) Property expenses (84 468) (288 190) (34 729) - (407 387) Recovery of property expenses 56 349 250 722 18 713 - 325 784

Net property income 355 556 356 573 64 945 - 777 074Straight line rental adjustment 27 489 (18 145) (1 167) - 8 177Income from associate company - - - 1 402 1 402Interest income - - - 30 547 30 547 Interest expense - - - (139 202) (139 202)Amortisation of debt restructure costs - - - (32 739) (32 739)Group expenses - - - (54 707) (54 707)Capital loss on disposal of investment properties (1 044) (17 865) (1 134) (32) (20 075)Revaluation of investment properties 178 919 66 073 619 - 245 611 Investment properties 206 408 47 928 (548) - 253 788 Straight line rental adjustment (27 489) 18 145 1 167 - (8 177)Revaluation of investment properties underdevelopment 625 - - - 625Revaluation of interest rate swap derivatives - - - (30 141) (30 141)Taxation (5 689) (44 088) (162) - (49 939)

Net profit / (loss) attributable to unitholders 555 856 342 548 63 101 (224 872) 736 633

Properties 3 495 654 3 747 343 671 385 - 7 914 382 At valuation 3 556 400 3 688 075 659 100 - 7 903 575 Straight line rental adjustment (129 446) (83 232) (22 715) - (235 393) Under development 63 300 - - - 63 300 Classified as held for disposal 5 400 142 500 35 000 - 182 900

Revenue reported above represents revenue, from external tenants, generated in South Africa. The Fund does not place significantreliance on any single tenant. No single tenant contributed 10% or more to the Fund's revenue for both 2013 and 2012.

ANNUAL FINANCIAL STATEMENTS 2013 31

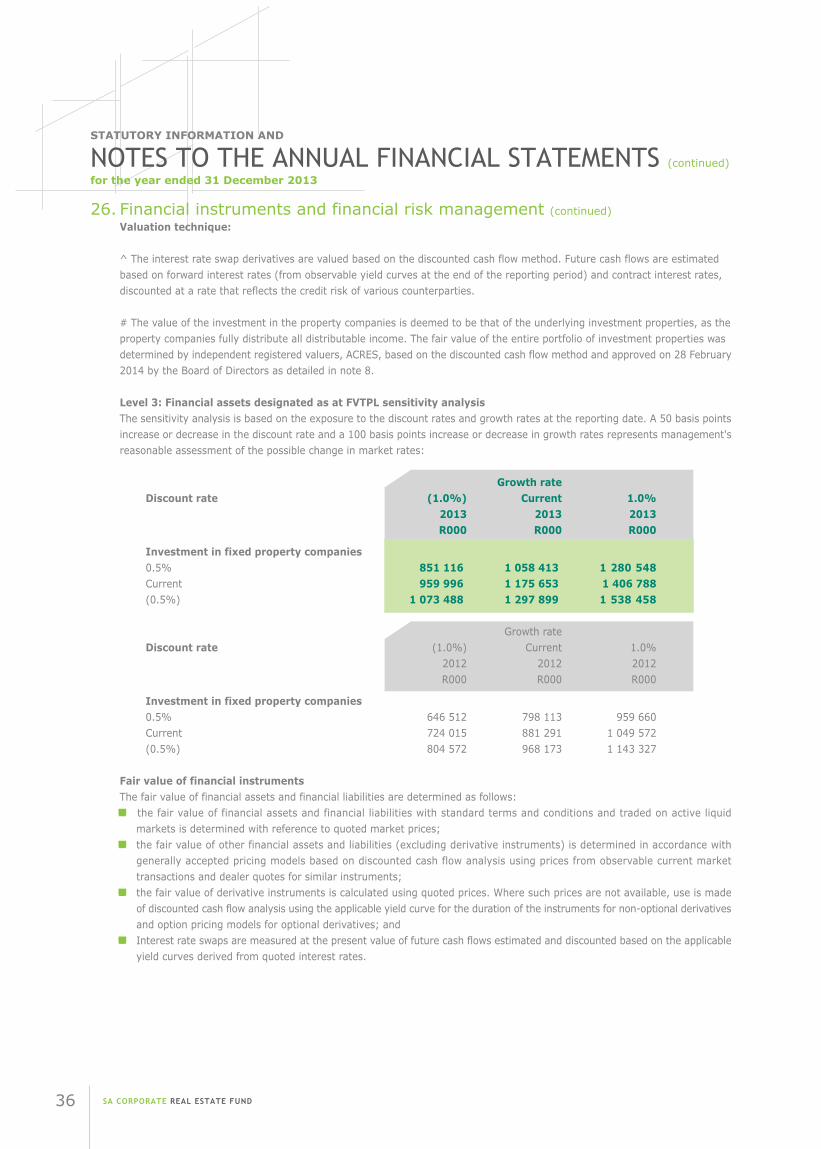

26. Financial instruments and financial risk managementThe Group and Fund is exposed to strategic and business risk, financial risk, regulatory and compliance risk.

This note deals with certain financial analyses relating to the financial risks.

Capital risk managementThe Group's and Fund's capital comprises unitholders' funds and interest-bearing borrowings. Capital is actively managed toensure that the Group and Fund is properly capitalised and funded at all times, having regard to its regulatory needs, prudentmanagement and the needs of its stakeholders.

The Group and Fund has a business planning process that runs on an annual cycle with regular updates to projections. It isthrough this process, which includes risk and sensitivity analyses of forecasts, that the Group's and Fund's capital is managed.Specifically, the Group and Fund has adopted the following capital management policies:

� Maintenance, as a minimum, of capital sufficient to meet the statutory requirements and such additional capital as management believes is necessary.� Maintenance of an appropriate level of liquidity at all times. The Group and Fund further ensures that it can meet its expected capital and financing needs at all times, having regard to the business plans, forecasts and any strategic initiatives.� Maintenance of an appropriate level of issued units based on approval from the unitholders and the Board.

The Group and Fund has both qualitative and quantitative risk management procedures to monitor the key risks and sensitivitiesof the business. This is achieved through scenario analyses and risk assessments. From an understanding of the principal risks,appropriate risk limits and controls are defined.