annual financial statements as per 31 december 2017 ... · sales of new machinery +3.7% y/y and...

TRANSCRIPT

Annual Financial Statementsas per 31 December 2017Analysts‘ Conference

Munich, 29 March 2018

Prof. Klaus Josef Lutz, CEO

Andreas Helber, CFO

29 March 2018BayWa AG Page 2

Agenda

1. Financial Year 2017

2. Performance of the Segments

3. Group Financials

4. Strategic Outlook for FY 2018

5. Operational Outlook for FY 2018

Appendix

BayWa AG

Financial Year 2017Prof. Klaus Josef Lutz

29 March 2018 Page 3

Positive earnings trend in all three core operating segments

Completion of the full refurbishment of the Group’s headquarters and relocation back to the building

Successful placement of a EUR 300 million hybrid bond

Dividend raised

Ongoing implementation of a speciality strategy through acquisitions: 100% Tracomex (Netherlands), 100% Premium Crops (UK)

Restructuring of grain trading activities in Southern and Eastern Europe completed

Expansion of Fruit: JV Al Dahra BayWa Agriculture, for cultivation of fruit and vegetables in UAE, developing according to plan; projects with investment of EUR 300 million planned (USA, Australia, Japan …)

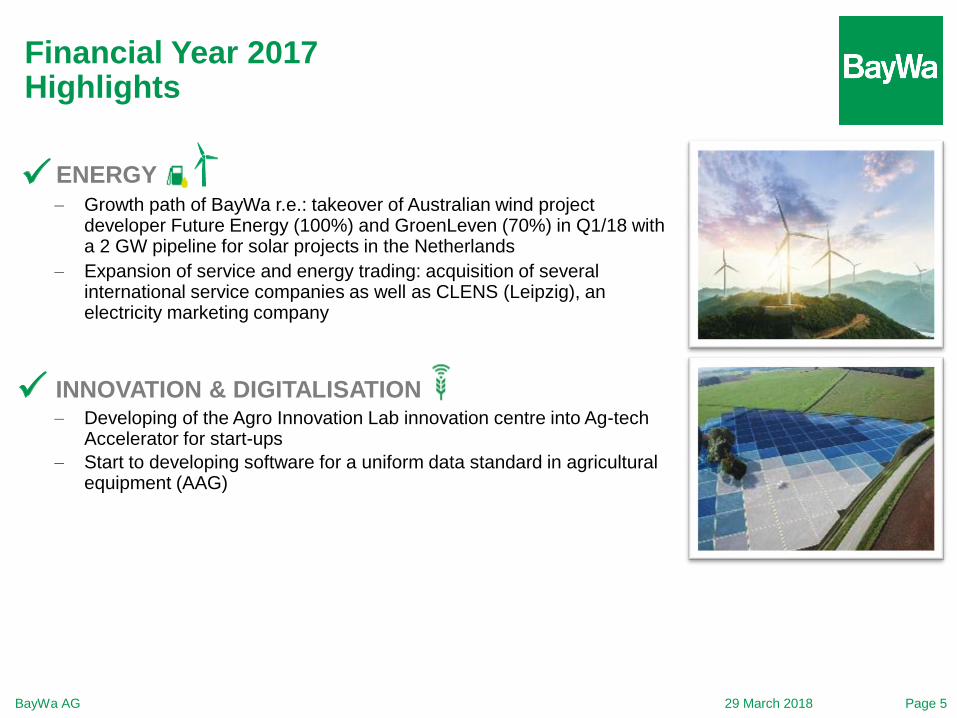

Financial Year 2017 Highlights

BayWa AG 29 March 2018 Page 4

GROUP

AGRICULTURE

Growth path of BayWa r.e.: takeover of Australian wind project developer Future Energy (100%) and GroenLeven (70%) in Q1/18 with a 2 GW pipeline for solar projects in the Netherlands

Expansion of service and energy trading: acquisition of several international service companies as well as CLENS (Leipzig), an electricity marketing company

Developing of the Agro Innovation Lab innovation centre into Ag-tech Accelerator for start-ups

Start to developing software for a uniform data standard in agricultural equipment (AAG)

Financial Year 2017 Highlights

BayWa AG 29 March 2018 Page 5

ENERGY

INNOVATION & DIGITALISATION

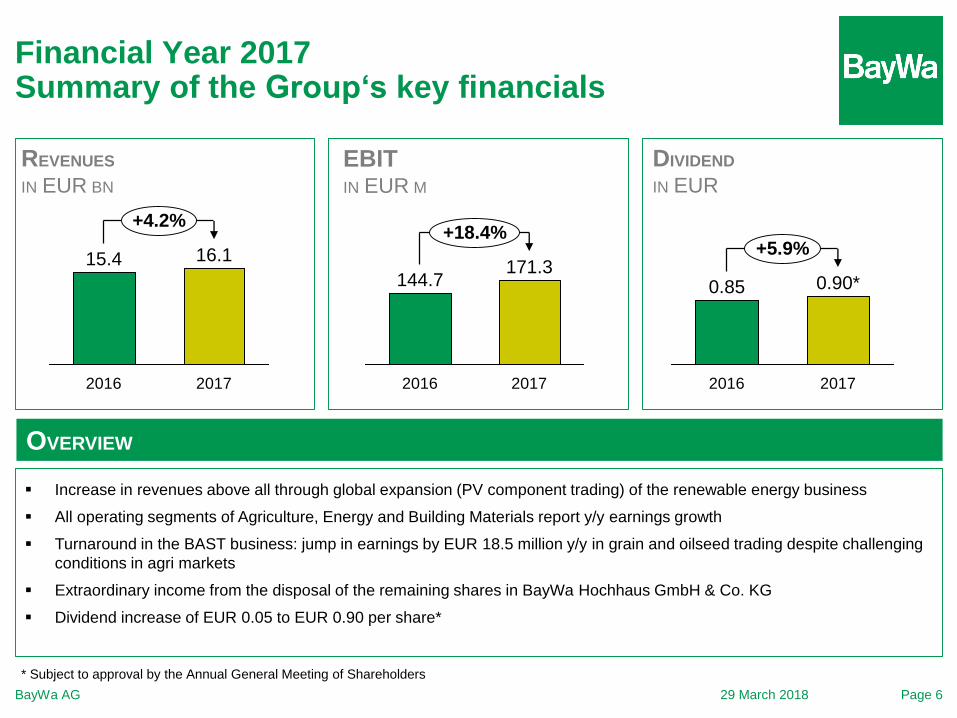

Financial Year 2017Summary of the Group‘s key financials

29 March 2018BayWa AG Page 6

+4.2%

2017

16.1

2016

15.4

2017

144.7

+18.4%

171.3

2016

+5.9%

0.85

2016

0.90*

2017

REVENUES

IN EUR BN

EBITIN EUR M

DIVIDEND

IN EUR

OVERVIEW

Increase in revenues above all through global expansion (PV component trading) of the renewable energy business

All operating segments of Agriculture, Energy and Building Materials report y/y earnings growth

Turnaround in the BAST business: jump in earnings by EUR 18.5 million y/y in grain and oilseed trading despite challenging

conditions in agri markets

Extraordinary income from the disposal of the remaining shares in BayWa Hochhaus GmbH & Co. KG

Dividend increase of EUR 0.05 to EUR 0.90 per share*

* Subject to approval by the Annual General Meeting of Shareholders

29 March 2018BayWa AG Page 7

Financial Year 2017 Multi-year comparison of operating EBIT

181.8

149.2

20142012 2016*

Ø 180.1

2017*

178.0

2013

194.8

169.5

2011

197.3190.4

2015

EBITIN EUR M

* Excluding Innovation & Digitalisation

29 March 2018BayWa AG Page 8

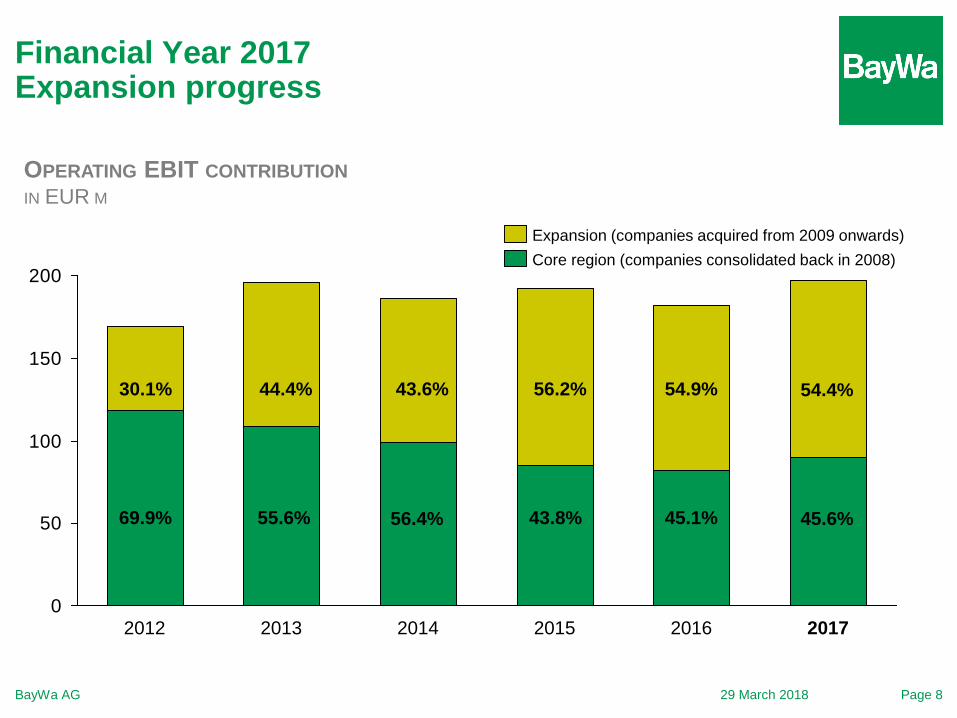

Financial Year 2017 Expansion progress

0

50

100

150

200

2012 20142013 2015 20172016

Expansion (companies acquired from 2009 onwards)

Core region (companies consolidated back in 2008)

30.1% 44.4% 43.6% 56.2% 54.9%

69.9% 55.6% 56.4% 43.8% 45.1%

OPERATING EBIT CONTRIBUTION

IN EUR M

54.4%

45.6%

BayWa AG

Performance of the SegmentsProf. Klaus Josef Lutz

29 March 2018 Page 9

Agriculture Segment 2017

GRAIN

OILSEED

SEED

FEEDSTUFF

CROP PROTECTION

FERTILISERS

FRUIT

AGRICULTURAL EQUIPMENT

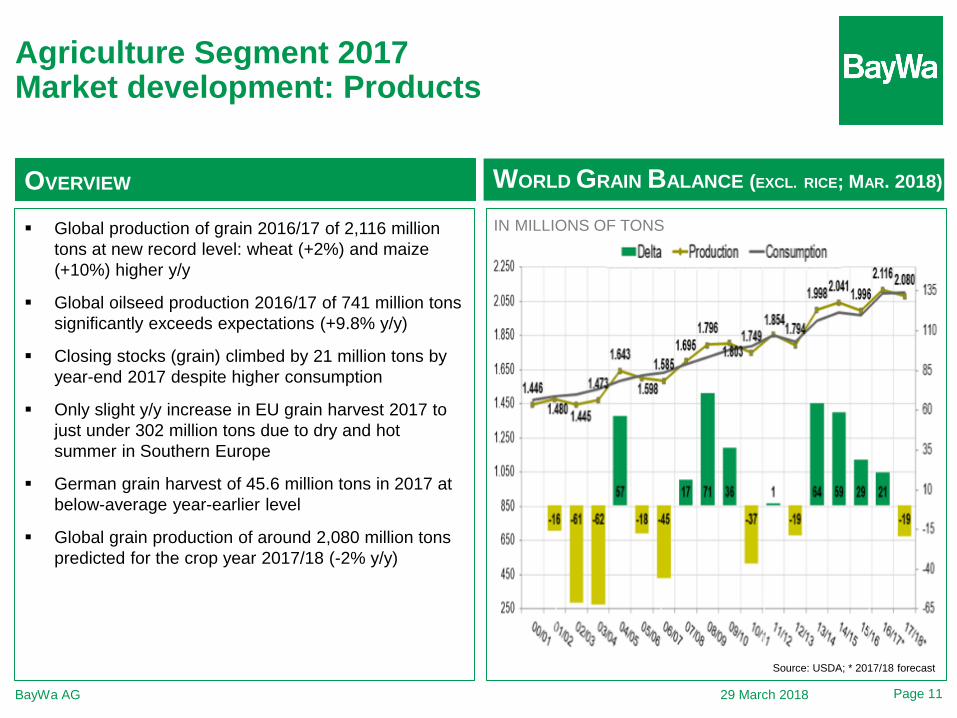

Agriculture Segment 2017Market development: Products

29 March 2018BayWa AG Page 11

Source: USDA; * 2017/18 forecast

WORLD GRAIN BALANCE (EXCL. RICE; MAR. 2018)

IN MILLIONS OF TONS Global production of grain 2016/17 of 2,116 million

tons at new record level: wheat (+2%) and maize

(+10%) higher y/y

Global oilseed production 2016/17 of 741 million tons

significantly exceeds expectations (+9.8% y/y)

Closing stocks (grain) climbed by 21 million tons by

year-end 2017 despite higher consumption

Only slight y/y increase in EU grain harvest 2017 to

just under 302 million tons due to dry and hot

summer in Southern Europe

German grain harvest of 45.6 million tons in 2017 at

below-average year-earlier level

Global grain production of around 2,080 million tons

predicted for the crop year 2017/18 (-2% y/y)

OVERVIEW

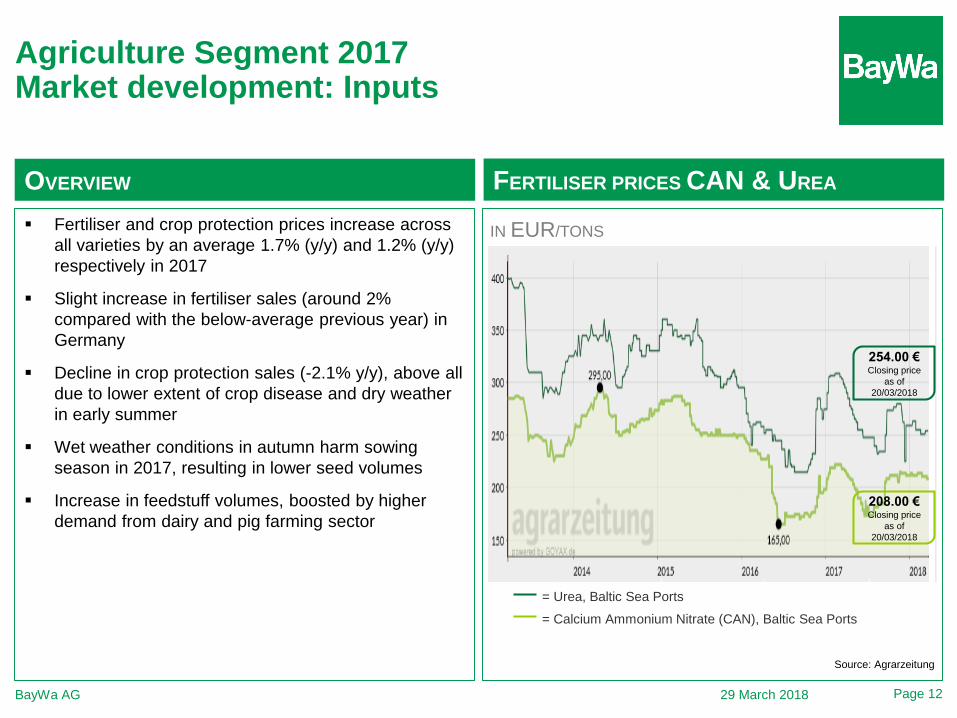

Agriculture Segment 2017Market development: Inputs

29 March 2018BayWa AG Page 12

Source: Agrarzeitung

OVERVIEW FERTILISER PRICES CAN & UREA

Fertiliser and crop protection prices increase across

all varieties by an average 1.7% (y/y) and 1.2% (y/y)

respectively in 2017

Slight increase in fertiliser sales (around 2%

compared with the below-average previous year) in

Germany

Decline in crop protection sales (-2.1% y/y), above all

due to lower extent of crop disease and dry weather

in early summer

Wet weather conditions in autumn harm sowing

season in 2017, resulting in lower seed volumes

Increase in feedstuff volumes, boosted by higher

demand from dairy and pig farming sector

= Urea, Baltic Sea Ports

= Calcium Ammonium Nitrate (CAN), Baltic Sea Ports

IN EUR/TONS

254.00 €Closing price

as of

20/03/2018

208.00 €Closing price

as of

20/03/2018

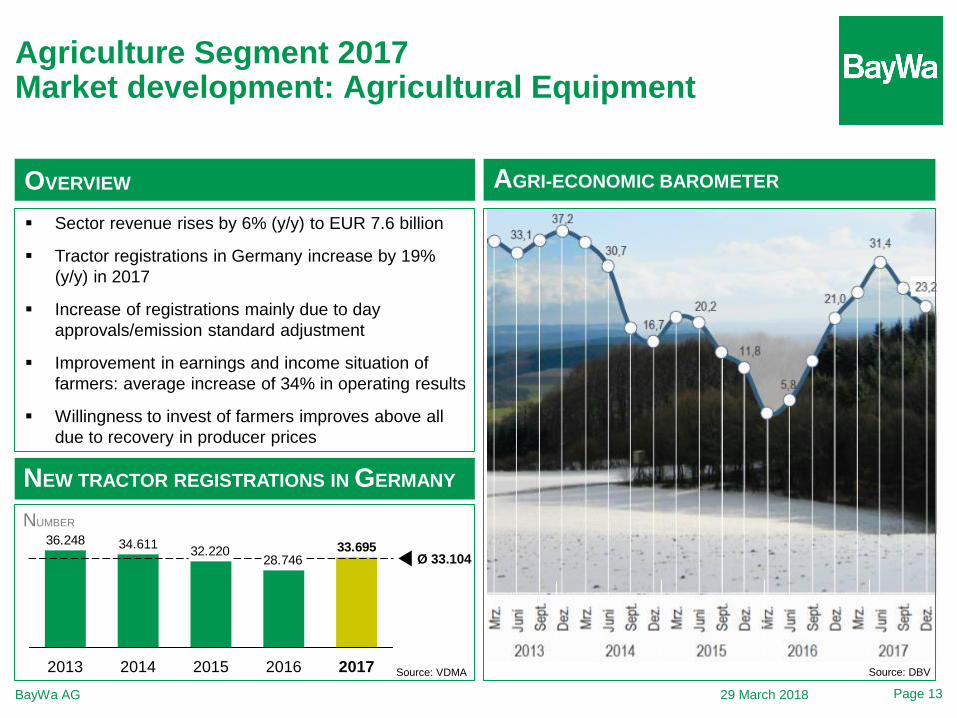

Agriculture Segment 2017Market development: Agricultural Equipment

29 March 2018BayWa AG Page 13

OVERVIEW

Sector revenue rises by 6% (y/y) to EUR 7.6 billion

Tractor registrations in Germany increase by 19%

(y/y) in 2017

Increase of registrations mainly due to day

approvals/emission standard adjustment

Improvement in earnings and income situation of

farmers: average increase of 34% in operating results

Willingness to invest of farmers improves above all

due to recovery in producer prices

33.69528.746

32.22034.61136.248

201520142013 2016

Ø 33.104

2017

AGRI-ECONOMIC BAROMETER

Source: VDMA

NEW TRACTOR REGISTRATIONS IN GERMANY

Source: DBV

NUMBER

Agriculture Segment 2017Market development: Fruit

29 March 2018BayWa AG Page 14

OVERVIEW

Fruit growing in Germany and in the EU badly

affected by poor weather conditions over the course

of the year: significant downturn in volumes and loss

of quality due to severe night frosts in spring and

summer heat in Southern & Eastern Europe

Apple harvest in Germany at around 597 thousand

tons, down 42% y/y; Lake Constance region reports

decline in harvest of up to 70%

Significant price increase for apples in Germany

(95% above the five-year average in October 2017)

NZ 2017 apple harvest delayed due to weather

conditions and, at 542 thousand tons, slightly lower

than the previous year (-1% y/y); declining export

volumes (-2% y/y), but export rate of 61% still high

Difficult market environment for NZA produce

(tomatoes, asparagus, berries, kiwis, etc.)

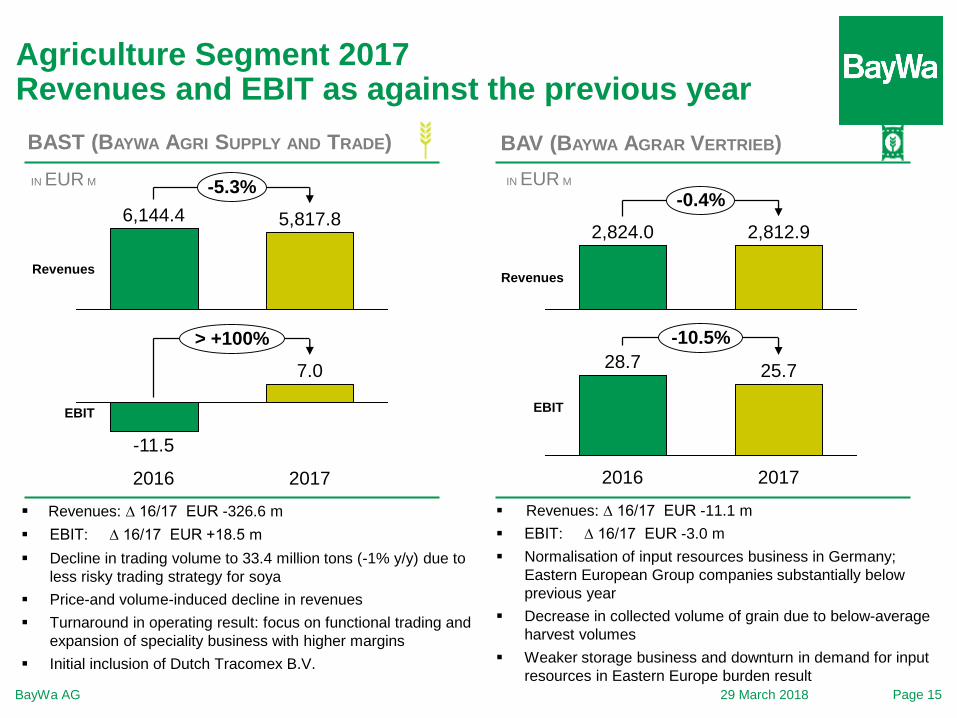

-11.5

> +100%

EBIT

2017

7.0

2016

Agriculture Segment 2017Revenues and EBIT as against the previous year

5,817.86,144.4

Revenues

-5.3%IN EUR M

Revenues: ∆ 16/17 EUR -326.6 m

EBIT: ∆ 16/17 EUR +18.5 m

Decline in trading volume to 33.4 million tons (-1% y/y) due to

less risky trading strategy for soya

Price-and volume-induced decline in revenues

Turnaround in operating result: focus on functional trading and

expansion of speciality business with higher margins

Initial inclusion of Dutch Tracomex B.V.

BayWa AG

2016

25.7

2017

EBIT

28.7

-10.5%

-0.4%

Revenues

2,824.0 2,812.9

Page 1529 March 2018

BAST (BAYWA AGRI SUPPLY AND TRADE)

Revenues: ∆ 16/17 EUR -11.1 m

EBIT: ∆ 16/17 EUR -3.0 m

Normalisation of input resources business in Germany;

Eastern European Group companies substantially below

previous year

Decrease in collected volume of grain due to below-average

harvest volumes

Weaker storage business and downturn in demand for input

resources in Eastern Europe burden result

IN EUR M

BAV (BAYWA AGRAR VERTRIEB)

19.9

EBIT

20172016

+87.6%

10.6

Agriculture Segment 2017

Revenues and EBIT as against the previous year

Revenues

1,400.3

+11.4%

1,256.8

Revenues: ∆ 16/17 EUR +143.5 m

EBIT: ∆ 16/17 EUR +9.3 m

Volume-induced increase in revenues and earnings:

sales of new machinery +3.7% y/y and used machinery

+12.6% y/y

Higher machine sales enhance demand for service

Positive development of Dutch subsidiary Agrimec

29 March 2018BayWa AG Page 16

5,000

2,500

1,500

500

0

2,000

1,000

4,500

4,000

3,500

3,000

3,659

2016

3,529

2015

3,986

20172009 2012

3,168

2,832

2008

2,967

2007 2011

4,661

3,038

2010

4,855

4,366

2014

3,850

2013

Ø 3,179

AGRICULTURAL EQUIPMENT

IN EUR M

NEW TRACTOR SALES 2007-2017

QUANTITY

181194

236

206

256

19

22

21

25

14

45

54

59

82

58

18

18

19 19

20

0

50

100

150

200

250

300

350

400

2013 2014 2015 2016 2017

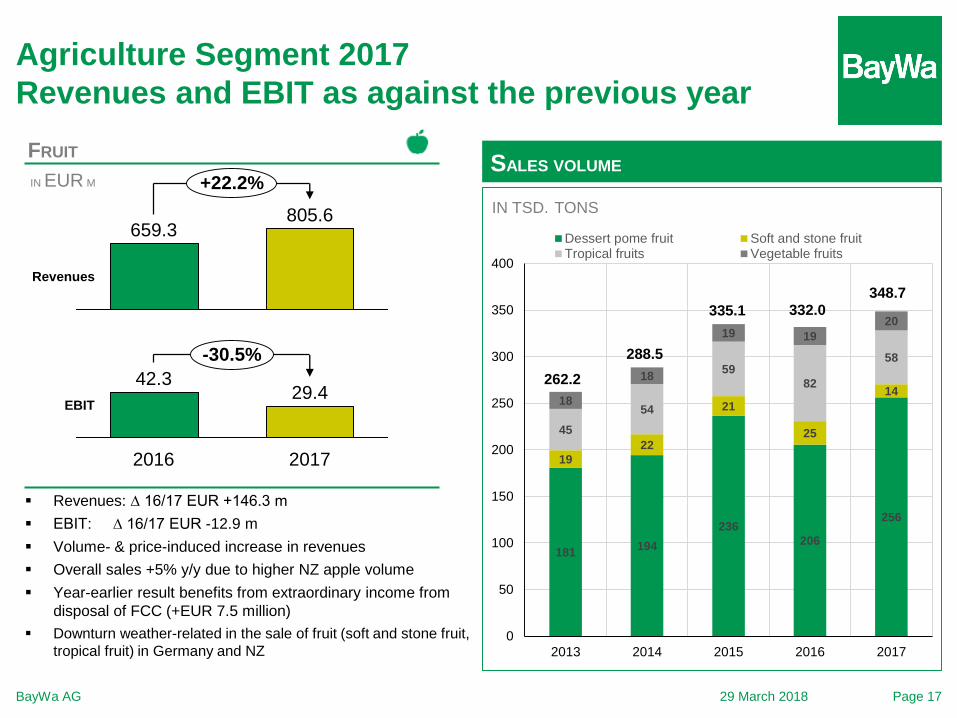

Dessert pome fruit Soft and stone fruitTropical fruits Vegetable fruits

29.4

20172016

42.3

-30.5%

EBIT

Agriculture Segment 2017

Revenues and EBIT as against the previous year

+22.2%

805.6

Revenues

659.3

Revenues: ∆ 16/17 EUR +146.3 m

EBIT: ∆ 16/17 EUR -12.9 m

Volume- & price-induced increase in revenues

Overall sales +5% y/y due to higher NZ apple volume

Year-earlier result benefits from extraordinary income from

disposal of FCC (+EUR 7.5 million)

Downturn weather-related in the sale of fruit (soft and stone fruit,

tropical fruit) in Germany and NZ

29 March 2018BayWa AG Page 17

FRUIT

IN EUR M

SALES VOLUME

262.2

288.5

335.1 332.0348.7

IN TSD. TONS

Energy Segment 2017

BAYWA R.E.

HEATING OIL

LUBRICANTS

SOLID BIOFUELS

FUELS

Energy Segment 2017Market development

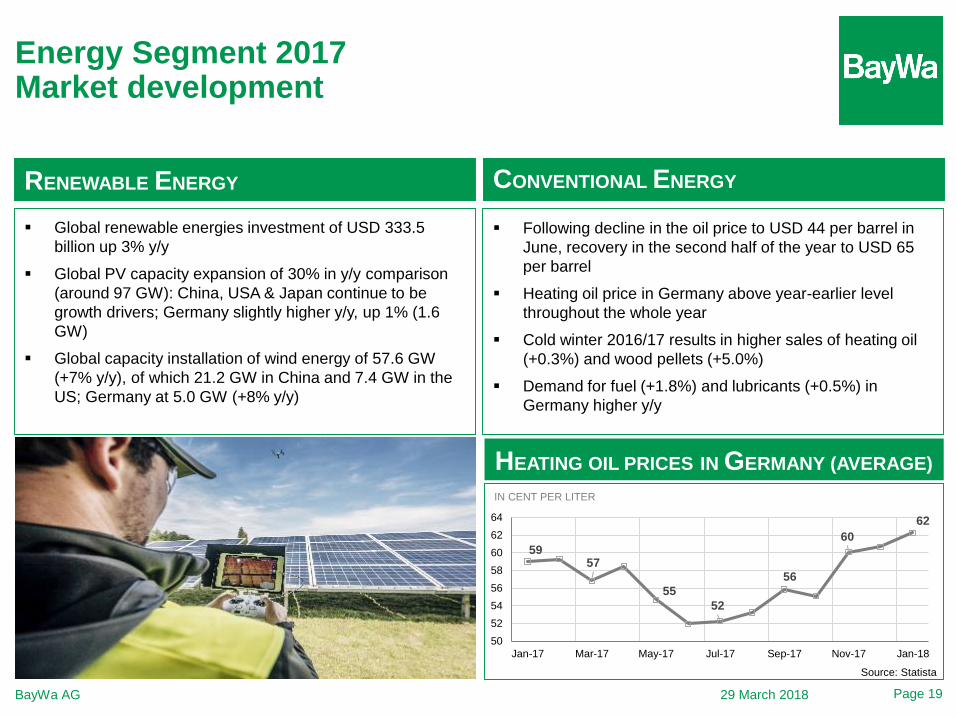

29 March 2018BayWa AG Page 19

RENEWABLE ENERGY

Global renewable energies investment of USD 333.5

billion up 3% y/y

Global PV capacity expansion of 30% in y/y comparison

(around 97 GW): China, USA & Japan continue to be

growth drivers; Germany slightly higher y/y, up 1% (1.6

GW)

Global capacity installation of wind energy of 57.6 GW

(+7% y/y), of which 21.2 GW in China and 7.4 GW in the

US; Germany at 5.0 GW (+8% y/y)

CONVENTIONAL ENERGY

Following decline in the oil price to USD 44 per barrel in

June, recovery in the second half of the year to USD 65

per barrel

Heating oil price in Germany above year-earlier level

throughout the whole year

Cold winter 2016/17 results in higher sales of heating oil

(+0.3%) and wood pellets (+5.0%)

Demand for fuel (+1.8%) and lubricants (+0.5%) in

Germany higher y/y

HEATING OIL PRICES IN GERMANY (AVERAGE)

IN CENT PER LITER

5957

55

52

56

60

62

50

52

54

56

58

60

62

64

Jan-17 Mar-17 May-17 Jul-17 Sep-17 Nov-17 Jan-18

Source: Statista

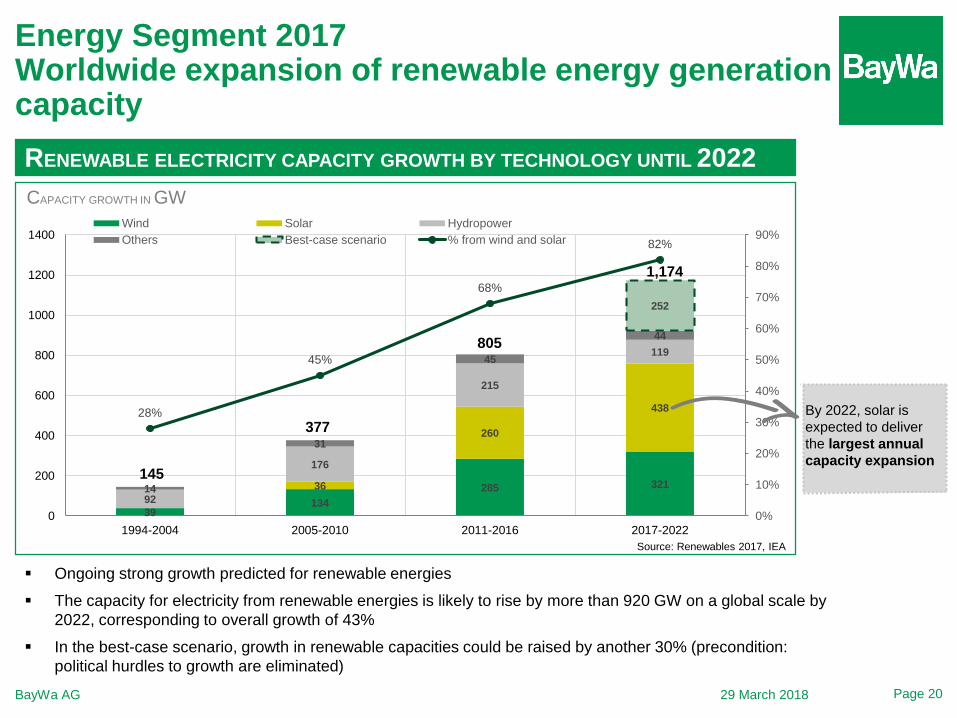

39134

285 32136

260

438

92

176

215

119

14

31

45

44

252

28%

45%

68%

82%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

200

400

600

800

1000

1200

1400

1994-2004 2005-2010 2011-2016 2017-2022

Wind Solar Hydropower

Others Best-case scenario % from wind and solar

Energy Segment 2017Worldwide expansion of renewable energy generation capacity

29 March 2018BayWa AG

RENEWABLE ELECTRICITY CAPACITY GROWTH BY TECHNOLOGY UNTIL 2022

Ongoing strong growth predicted for renewable energies

The capacity for electricity from renewable energies is likely to rise by more than 920 GW on a global scale by

2022, corresponding to overall growth of 43%

In the best-case scenario, growth in renewable capacities could be raised by another 30% (precondition:

political hurdles to growth are eliminated)

Source: Renewables 2017, IEA

By 2022, solar is

expected to deliver

the largest annual

capacity expansion

1,174

805

377

145

CAPACITY GROWTH IN GW

Page 20

2016

EBIT

15.8

2017

18.5

+17.1%

Energy Segment 2017 Revenues and EBIT as against the previous year

2,228.1

Revenues

+9.7%

2,030.1

Revenues: ∆ 16/17 EUR +198.0 m

EBIT: ∆ 16/17 EUR +2.7 m

Price-and volume-induced increase in revenues (crude

oil price higher on average than previous year)

Volume growth in fuel (+1.5% y/y), lubricants (+5.5% y/y)

and heating oil (+1.1% y/y)

Improved margins in the fuel business

67.3

EBIT

66.6

20172016

-1.0%

Revenues

+44.5%

1,366.7945.9

Revenues: ∆ 16/17 EUR +420.8 m

EBIT: ∆ 16/17 EUR -0.7 m

Jump in revenues through significant sales growth in PV

trade (+56% y/y)

International growth in the project business and energy

trade: all in all, 16 wind and solar farms with an output of

407.4 MW sold; in addition, sale of 2 biogas plants (6.6 MW)

Result almost at high year-earlier level; In 2016 extra-

ordinary income from sale of geothermal plants (EUR 14 m)

IN EUR M

CONVENTIONAL ENERGYRENEWABLE ENERGY

IN EUR M

29 March 2018 Page 21BayWa AG

Building Materials Segment 2017

BUILDING MATERIALS

Building Materials Segment 2017Market development

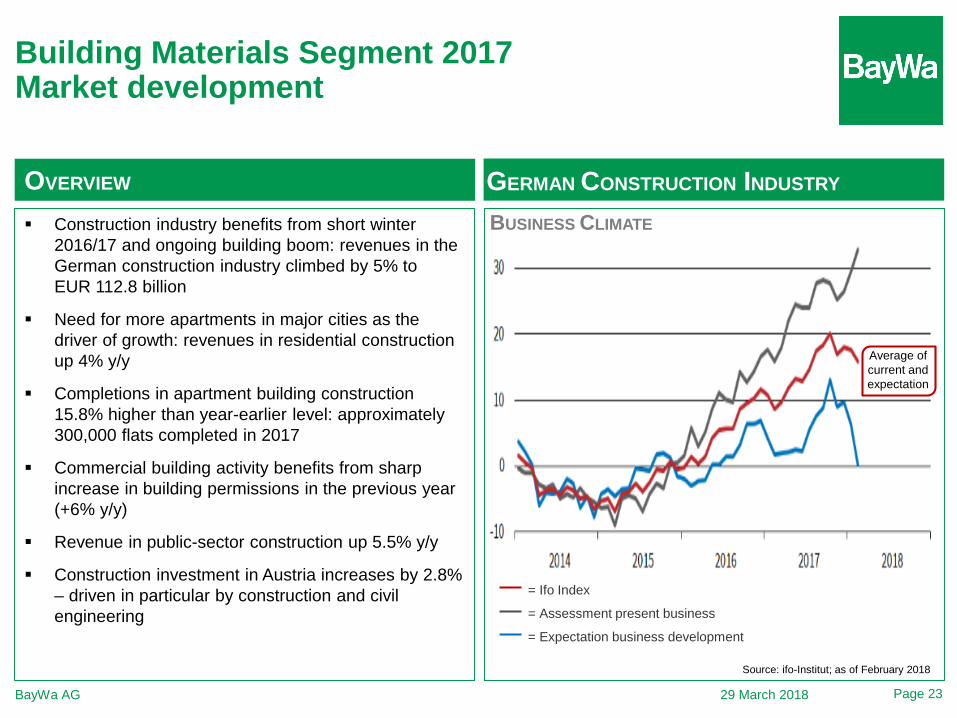

29 March 2018BayWa AG Page 23

OVERVIEW GERMAN CONSTRUCTION INDUSTRY

Construction industry benefits from short winter

2016/17 and ongoing building boom: revenues in the

German construction industry climbed by 5% to

EUR 112.8 billion

Need for more apartments in major cities as the

driver of growth: revenues in residential construction

up 4% y/y

Completions in apartment building construction

15.8% higher than year-earlier level: approximately

300,000 flats completed in 2017

Commercial building activity benefits from sharp

increase in building permissions in the previous year

(+6% y/y)

Revenue in public-sector construction up 5.5% y/y

Construction investment in Austria increases by 2.8%

– driven in particular by construction and civil

engineering

Source: ifo-Institut; as of February 2018

BUSINESS CLIMATE

= Ifo Index

= Expectation business development

= Assessment present business

Average of

current and

expectation

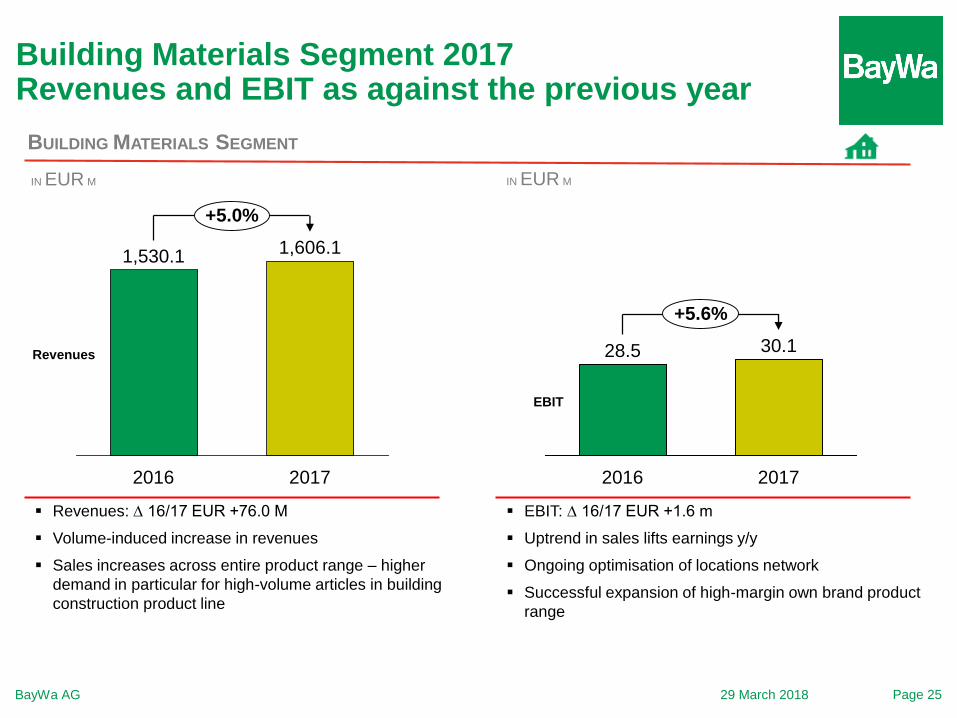

+5.0%

Revenues

2017

1,606.1

2016

1,530.1

Building Materials Segment 2017Revenues and EBIT as against the previous year

IN EUR M

Revenues: ∆ 16/17 EUR +76.0 M

Volume-induced increase in revenues

Sales increases across entire product range – higher

demand in particular for high-volume articles in building

construction product line

BayWa AG

+5.6%

EBIT

2017

30.1

2016

28.5

Page 2529 March 2018

BUILDING MATERIALS SEGMENT

EBIT: ∆ 16/17 EUR +1.6 m

Uptrend in sales lifts earnings y/y

Ongoing optimisation of locations network

Successful expansion of high-margin own brand product

range

IN EUR M

INNOVATION & DIGITALISATION

Innovation & Digitalisation Segment 2017

Innovation & Digitalisation Segment 2017Market development

BayWa AG

OVERVIEW

The market for digital applications in the agriculture industry

comprises the areas of Precision Farming (focus on

automation of processes and optimisation of deploying input

resources) and Smart Farming (networking of all areas of

operations)

Digitalisation in the agricultural industry in the top third of all

sectors: capital expenditure rate of around 10% of annual

revenues

The optimisation of the value chain is the strongest driver of

digitalisation

53% of German farmers are already using digital

technologies

High-tech agricultural machinery, automatic feeding

machines and intelligent control software are most widely

used

Germany is the largest single market in Europe in the area

of Precision Farming with 35% in capital expenditure

(around USD 394 million) in 2017

The market volume in interactive trading and e-commerce in

Germany grew by 7.9% to around EUR 78.1 billion in 2017

29 March 2018 Page 26

Innovation & Digitalisation Segment 2017Revenues and EBIT as against the previous year

29 March 2018BayWa AG Page 27

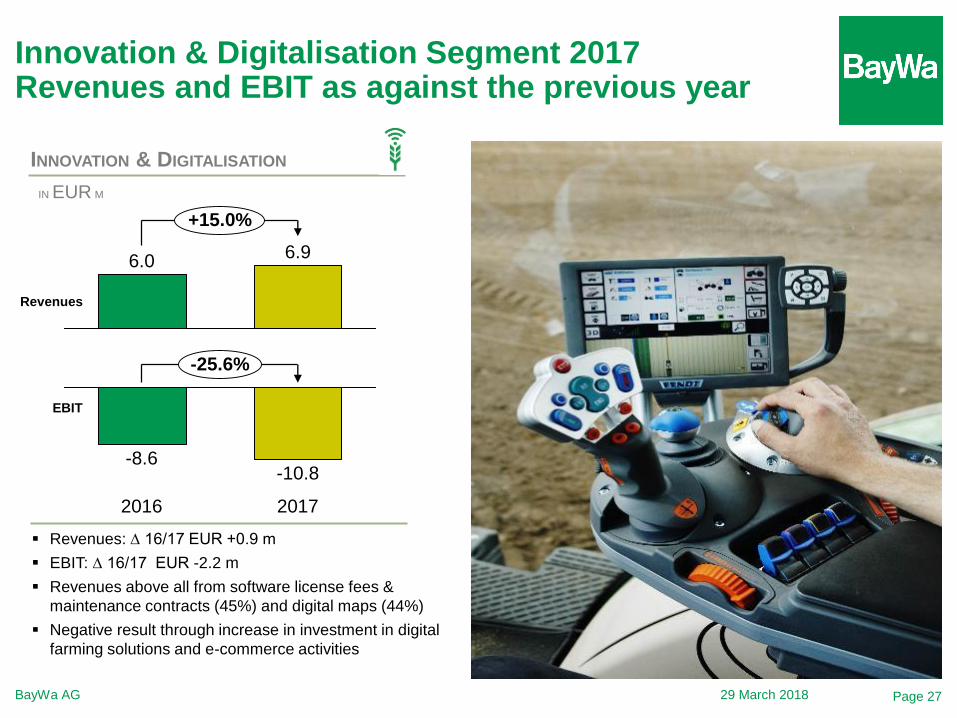

-25.6%

2017

EBIT

-10.8

2016

-8.6

+15.0%

6.9

Revenues

6.0

INNOVATION & DIGITALISATION

IN EUR M

Revenues: ∆ 16/17 EUR +0.9 m

EBIT: ∆ 16/17 EUR -2.2 m

Revenues above all from software license fees &

maintenance contracts (45%) and digital maps (44%)

Negative result through increase in investment in digital

farming solutions and e-commerce activities

BayWa AG

Group FinancialsAndreas Helber

29 March 2018 Page 28

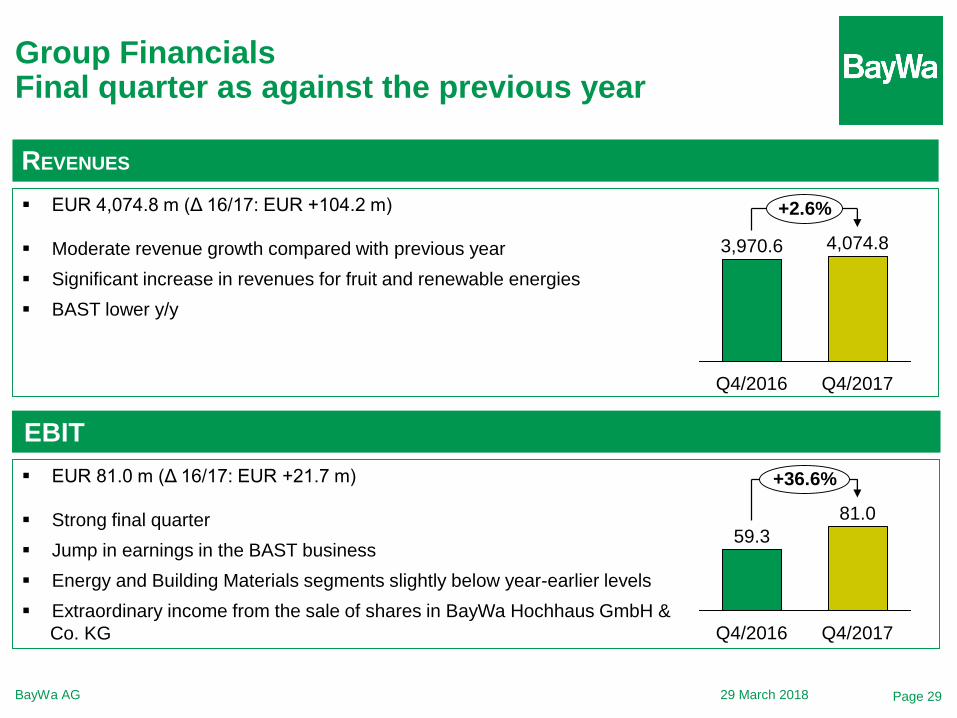

Group FinancialsFinal quarter as against the previous year

29 March 2018BayWa AG

EBIT

EUR 81.0 m (Δ 16/17: EUR +21.7 m)

Strong final quarter

Jump in earnings in the BAST business

Energy and Building Materials segments slightly below year-earlier levels

Extraordinary income from the sale of shares in BayWa Hochhaus GmbH &

Co. KG

59.3

Q4/2017Q4/2016

81.0

+36.6%

EUR 4,074.8 m (Δ 16/17: EUR +104.2 m)

Moderate revenue growth compared with previous year

Significant increase in revenues for fruit and renewable energies

BAST lower y/y

+2.6%

Q4/2017Q4/2016

3,970.6 4,074.8

REVENUES

Page 29

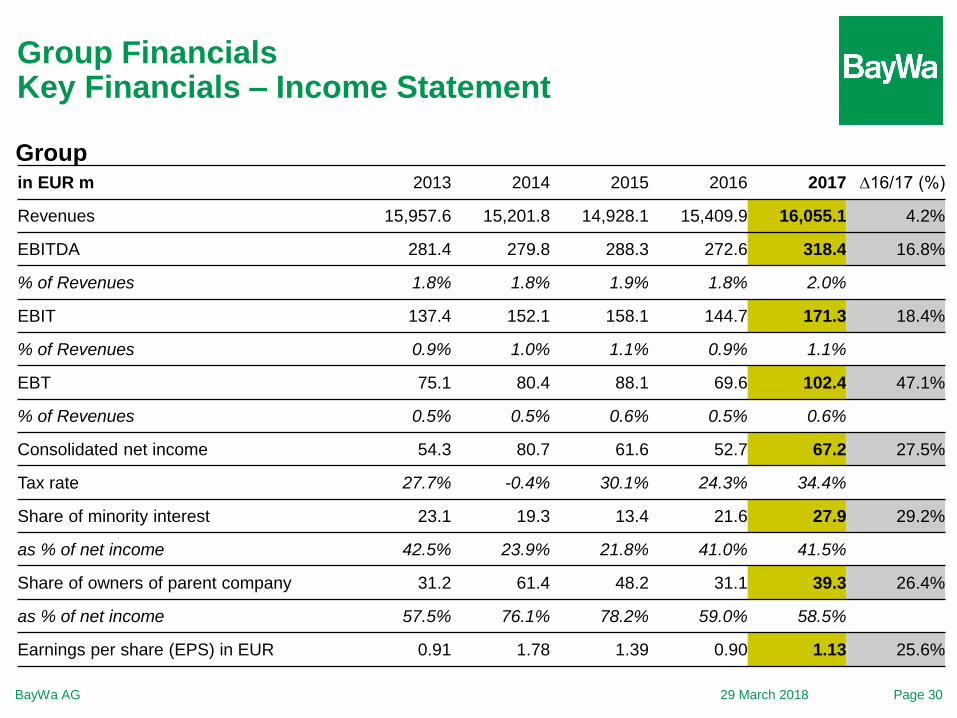

Group FinancialsKey Financials – Income Statement

29 March 2018 Page 30BayWa AG

Groupin EUR m 2013 2014 2015 2016 2017 ∆16/17 (%)

Revenues 15,957.6 15,201.8 14,928.1 15,409.9 16,055.1 4.2%

EBITDA 281.4 279.8 288.3 272.6 318.4 16.8%

% of Revenues 1.8% 1.8% 1.9% 1.8% 2.0%

EBIT 137.4 152.1 158.1 144.7 171.3 18.4%

% of Revenues 0.9% 1.0% 1.1% 0.9% 1.1%

EBT 75.1 80.4 88.1 69.6 102.4 47.1%

% of Revenues 0.5% 0.5% 0.6% 0.5% 0.6%

Consolidated net income 54.3 80.7 61.6 52.7 67.2 27.5%

Tax rate 27.7% -0.4% 30.1% 24.3% 34.4%

Share of minority interest 23.1 19.3 13.4 21.6 27.9 29.2%

as % of net income 42.5% 23.9% 21.8% 41.0% 41.5%

Share of owners of parent company 31.2 61.4 48.2 31.1 39.3 26.4%

as % of net income 57.5% 76.1% 78.2% 59.0% 58.5%

Earnings per share (EPS) in EUR 0.91 1.78 1.39 0.90 1.13 25.6%

in EUR m 2013 2014 2015 2016 2017 ∆16/17 (%)

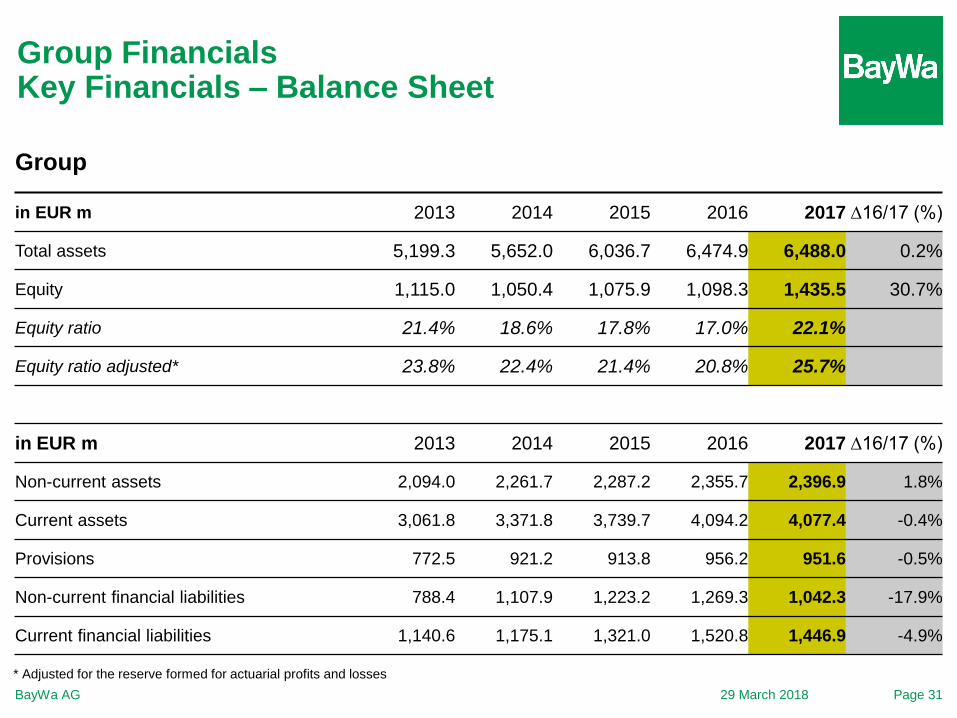

Total assets 5,199.3 5,652.0 6,036.7 6,474.9 6,488.0 0.2%

Equity 1,115.0 1,050.4 1,075.9 1,098.3 1,435.5 30.7%

Equity ratio 21.4% 18.6% 17.8% 17.0% 22.1%

Equity ratio adjusted* 23.8% 22.4% 21.4% 20.8% 25.7%

in EUR m 2013 2014 2015 2016 2017 ∆16/17 (%)

Non-current assets 2,094.0 2,261.7 2,287.2 2,355.7 2,396.9 1.8%

Current assets 3,061.8 3,371.8 3,739.7 4,094.2 4,077.4 -0.4%

Provisions 772.5 921.2 913.8 956.2 951.6 -0.5%

Non-current financial liabilities 788.4 1,107.9 1,223.2 1,269.3 1,042.3 -17.9%

Current financial liabilities 1,140.6 1,175.1 1,321.0 1,520.8 1,446.9 -4.9%

Group FinancialsKey Financials – Balance Sheet

29 March 2018 Page 31BayWa AG

* Adjusted for the reserve formed for actuarial profits and losses

Group

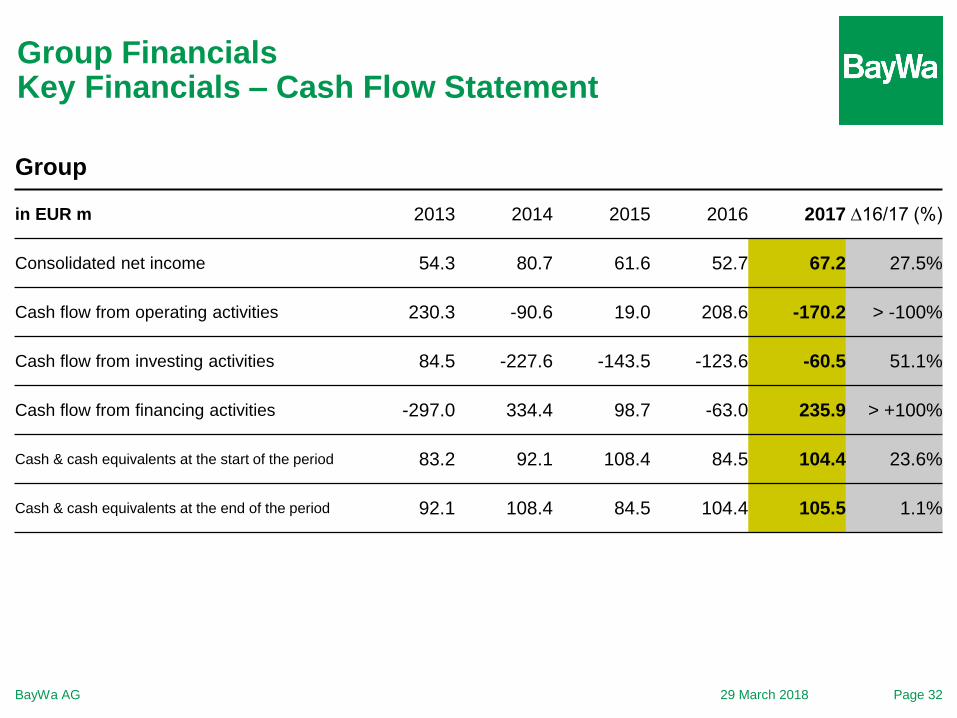

Group FinancialsKey Financials – Cash Flow Statement

29 March 2018 Page 32BayWa AG

Group

in EUR m 2013 2014 2015 2016 2017 ∆16/17 (%)

Consolidated net income 54.3 80.7 61.6 52.7 67.2 27.5%

Cash flow from operating activities 230.3 -90.6 19.0 208.6 -170.2 > -100%

Cash flow from investing activities 84.5 -227.6 -143.5 -123.6 -60.5 51.1%

Cash flow from financing activities -297.0 334.4 98.7 -63.0 235.9 > +100%

Cash & cash equivalents at the start of the period 83.2 92.1 108.4 84.5 104.4 23.6%

Cash & cash equivalents at the end of the period 92.1 108.4 84.5 104.4 105.5 1.1%

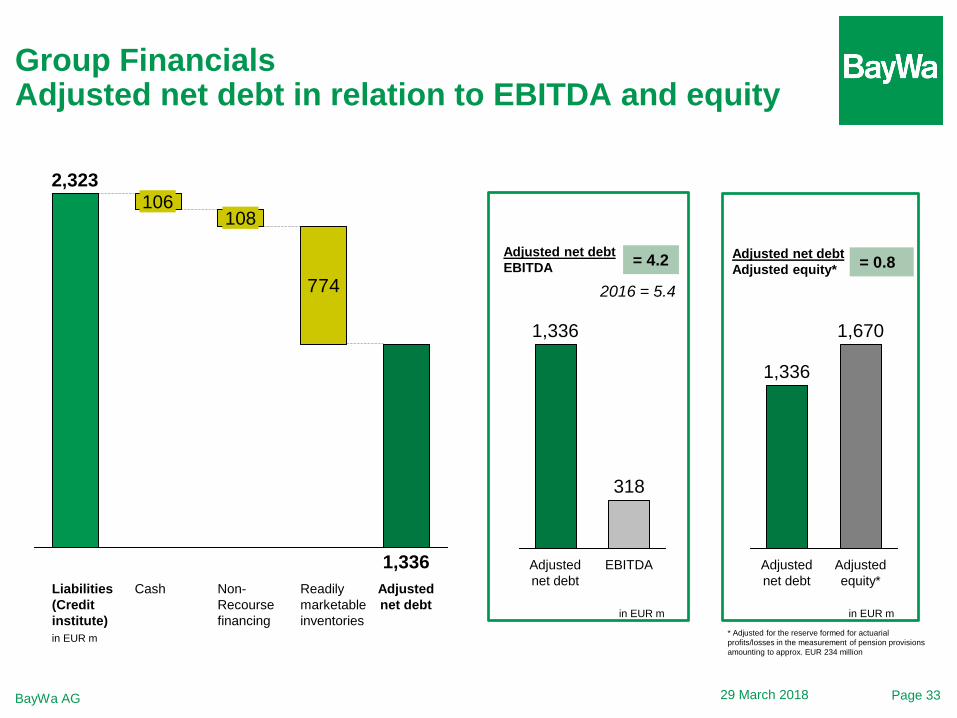

774

Readily

marketable

inventories

Non-

Recourse

financing

Adjusted

net debt

1,336

108

Cash

106

Liabilities

(Credit

institute)

2,323

in EUR m

Page 33BayWa AG 29 March 2018

318

Adjusted

net debt

EBITDA

1,336

Adjusted net debt

EBITDA = 4.2

1,670

1,336

Adjusted

net debt

Adjusted

equity*

in EUR m

Group FinancialsAdjusted net debt in relation to EBITDA and equity

= 0.8

* Adjusted for the reserve formed for actuarial

profits/losses in the measurement of pension provisions

amounting to approx. EUR 234 million

in EUR m

Adjusted net debt

Adjusted equity*

2016 = 5.4

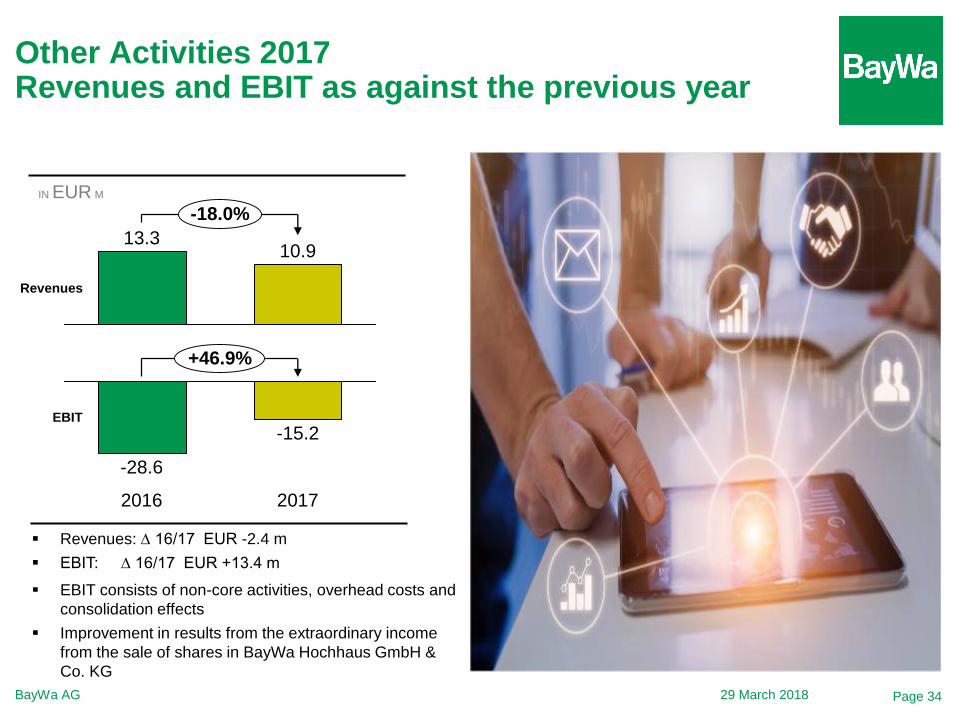

Other Activities 2017Revenues and EBIT as against the previous year

29 March 2018BayWa AG Page 34

EBIT

+46.9%

2017

-15.2

-28.6

2016

-18.0%

Revenues

10.913.3

IN EUR M

Revenues: ∆ 16/17 EUR -2.4 m

EBIT: ∆ 16/17 EUR +13.4 m

EBIT consists of non-core activities, overhead costs and

consolidation effects

Improvement in results from the extraordinary income

from the sale of shares in BayWa Hochhaus GmbH &

Co. KG

BayWa AG

Strategic Outlook for FY 2018Prof. Klaus Josef Lutz

29 March 2018 Page 35

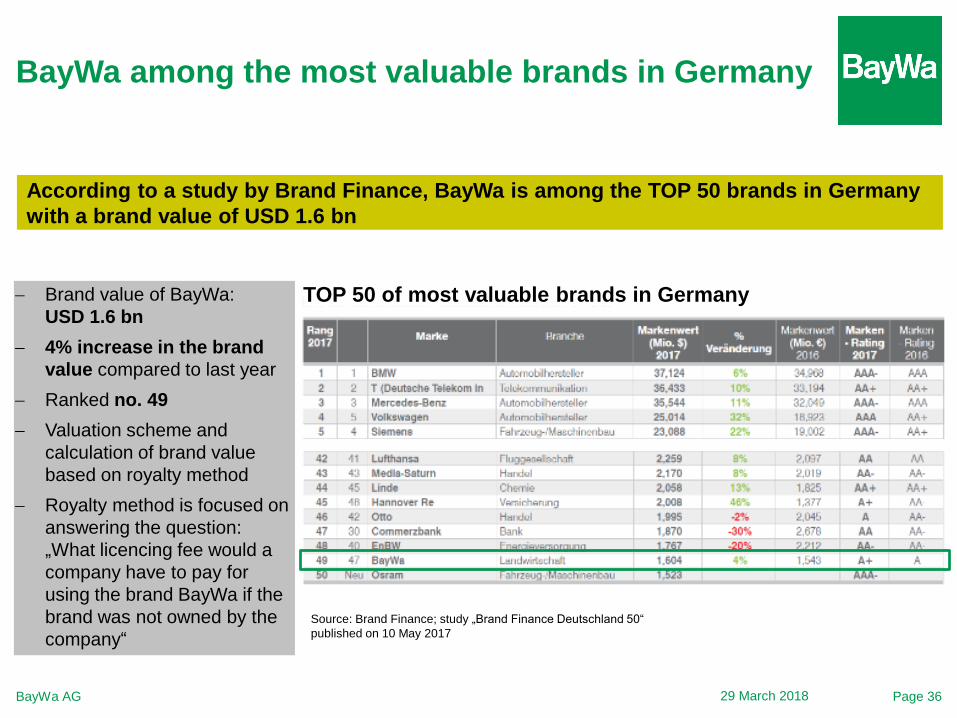

BayWa among the most valuable brands in Germany

Brand value of BayWa:

USD 1.6 bn

4% increase in the brand

value compared to last year

Ranked no. 49

Valuation scheme and

calculation of brand value

based on royalty method

Royalty method is focused on

answering the question:

„What licencing fee would a

company have to pay for

using the brand BayWa if the

brand was not owned by the

company“

Source: Brand Finance; study „Brand Finance Deutschland 50“

published on 10 May 2017

According to a study by Brand Finance, BayWa is among the TOP 50 brands in Germany

with a brand value of USD 1.6 bn

TOP 50 of most valuable brands in Germany

29 March 2018BayWa AG Page 36

Group strategy: project business as a driver

throughout the whole Group

From system supplier of dessert pome fruit

for food wholesalers and retailers ...

... to international project development

of greenhouses

From building materials trader ...

... to cooperation partner for

innovative building projects

From the supplier

of energy and heating ...

... to project developer

for renewable energies

... to full-line equipping and

management planning of farming operations

From wholesaler ...

BayWa will concentrate

increasingly on more profitable

customer and project solutions

in the future as well

ENERGY

BUILDING

MATERIALS

GLOBAL

PRODUCE

FARMING

BUSINESS

29 March 2018BayWa AG Page 37

BayWa Agrar Strategy: Specialties / Grains

29 March 2018

Goal: 50% specialties/

50% other products

Trend

Internationalisation

2012 - 2015

Since 2016

STRATEGIC DIRECTION:

PORTFOLIO ENRICHMENT THROUGH SPECIALTIES

KEY

CRITERIA

Growingmarket

Lowervolatilities

Stablemargins

Long-term businessrelationships

BAST Group Grains, Co-products, By-products: Thegra Tracomex Group

Grains, Oilseeds, Co-Products: Premium Crops Ltd. (an agricultural

supply chain manager that provides to customers long-term solutions for

niche crops with specialty traits)

CURRENT INITIATIVES:

By-products of

barley, cocoa,

linseed, malt, oat,

rapeseed, etc

Organic

grains

Pulses:

horsebeans,

lupines,

peas

National

Business

Functional Margin

International

Business

Trade Margin

Specialties and

services

Functional Margin

Development of regional and international

emerging markets

Reallocation of resources(capital) into moreprofitable business

activities

Portfolio Optimisation

Trend Specialties

BayWa AG Page 38

Pipfruit

Local apple

trader

BayWa Fruit T&G GlobalTropical Fruit

CompanyAl Dahra BayWa

Pipfruit

Exotics

„ready to eat“

Diversified Portfolio

Pipfruit

Diversified Portfolio

Internationalization Specialization

premium & club

varieties

Exotics

„ready to eat“

Pipfruit

Diversified Portfolio

Industrialization

Greenhouse

„seed project“

Exotics

„ready to eat“

Pipfruit

Diversified Portfolio

Greenhouse

Project Development

Global Produce

Global Produce

Product Knowledge

2002 – 2012 2012 2016 2017 2018

Leading fruit trader in

Germany

Largest German

supplier of organic

pome fruits

Access to Asia

Exclusive trademark

rights

Global trading

network – delivery to

40 countries

Year round availability

of exotics

Global sourcing from

over 40 countries

„ready to eat“ premium

products

Premium products

from local and

protected production

Global project

development

Increase self-suffiency

rate – reduction of

import dependency

Ac

ce

ss

To

Gro

wth

Ma

rke

ts

29 March 2018

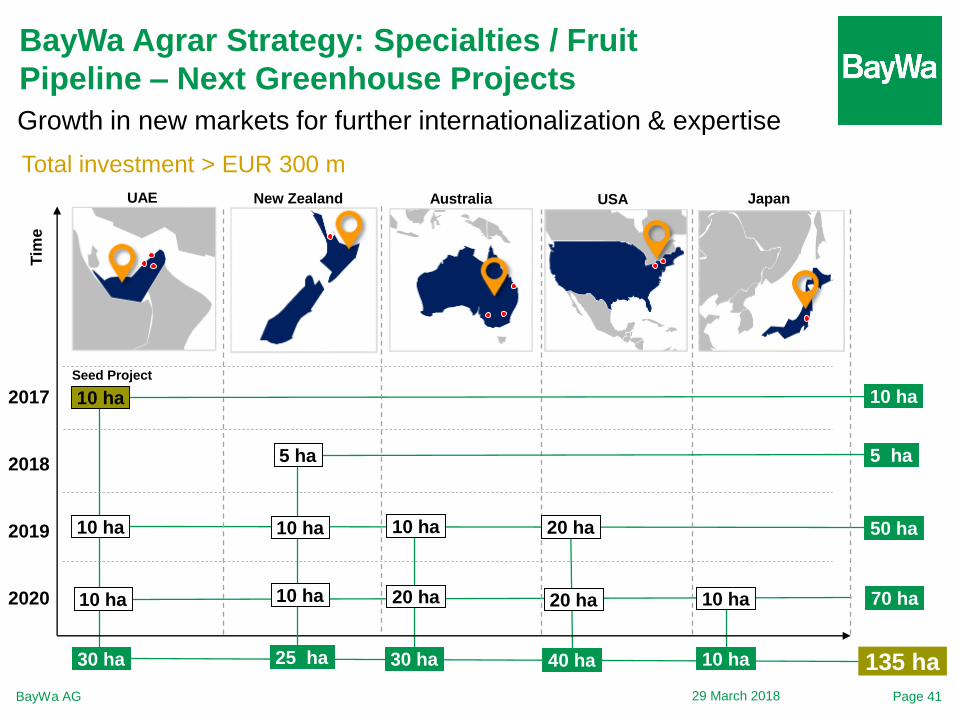

BayWa Agrar Strategy: Specialties / Fruit

From Local Trader To Global Produce

BayWa AG Page 39

BayWa Agrar Strategy: Specialties / Fruit

Vegetable Fruit Cultivation

29 March 2018

JOINT VENTURE IN THE UAE:STRATEGIC RATIONALE:

Reduce the volatility of product availability through

production in glasshouses – to increase self-suffiency rate

Reduction of import dependency and efficient design of

supply chain

Further diversification of the product portfolio

of the fruit division - focus on specialties

State-of-the-art greenhouse technology enables

cultivation in almost all climates

Supply security for growing global food needs through

high yield per hectare

Pilot Project 10 ha climate-controlled greenhouse

Location Al Ain, United Arab Emirates

ProductConventional tomatoes - high end (vine, cocktail

& cherry tomatoes)

Volume 5,000 ton/ year (50kg / m2 per year)

Sales Local for local

Start of

productionQ1 2018/5 ha

Investment EUR 28.3 m

Country Rent-free lease for 20 years with Al-Dahra Group

Financing

Shareholder loan from BayWa, until repayment

loan, BayWa has 100% claim on dividend –

following 51% BayWa / 49% Al-Dahra

BayWa AG Page 40

UAE JapanUSAAustralia

2017

2018

2019

2020

10 ha

10 ha

10 ha

20 ha

20 ha

10 ha

10 ha

30 ha 40 ha 30 ha 10 ha

50 ha

70 ha

5 ha

10 ha

Tim

e

135 ha

Seed Project

20 ha

New Zealand

5 ha

25 ha

10 ha

10 ha

Total investment > EUR 300 m

BayWa Agrar Strategy: Specialties / Fruit

Pipeline – Next Greenhouse Projects

Growth in new markets for further internationalization & expertise

29 March 2018BayWa AG Page 41

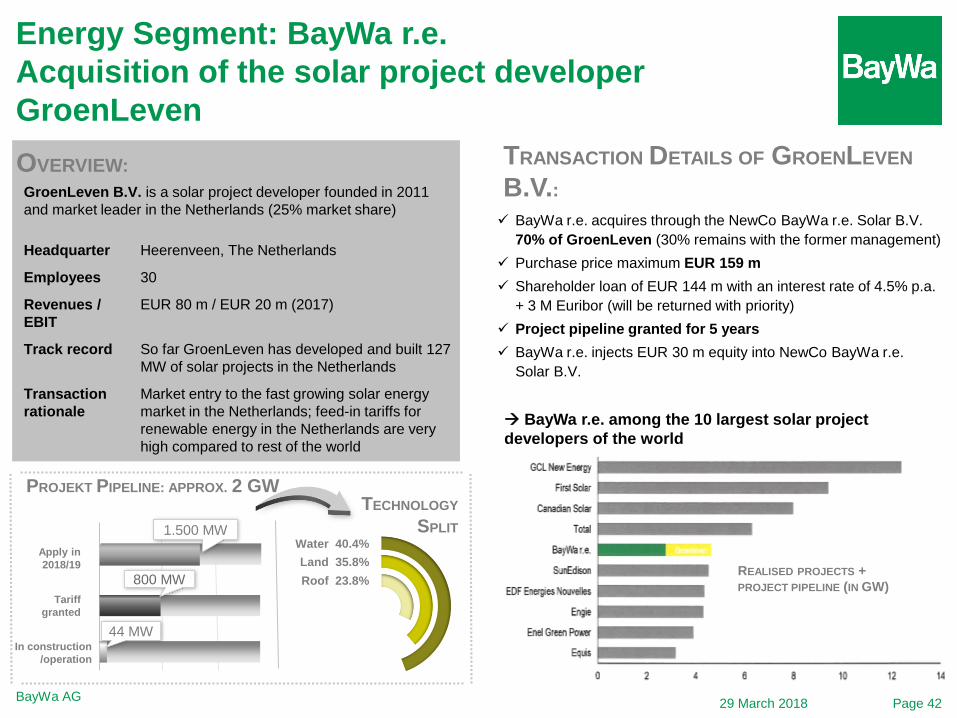

Energy Segment: BayWa r.e.

Acquisition of the solar project developer

GroenLeven

BayWa AG

OVERVIEW: TRANSACTION DETAILS OF GROENLEVEN

B.V.: BayWa r.e. acquires through the NewCo BayWa r.e. Solar B.V.

70% of GroenLeven (30% remains with the former management)

Purchase price maximum EUR 159 m

Shareholder loan of EUR 144 m with an interest rate of 4.5% p.a.

+ 3 M Euribor (will be returned with priority)

Project pipeline granted for 5 years

BayWa r.e. injects EUR 30 m equity into NewCo BayWa r.e.

Solar B.V.

Water 40.4%

Land 35.8%

Roof 23.8%

Apply in

2018/19

Tariff

granted

In construction

/operation

1.500 MW

800 MW

44 MW

GroenLeven B.V. is a solar project developer founded in 2011

and market leader in the Netherlands (25% market share)

Headquarter Heerenveen, The Netherlands

Employees 30

Revenues /

EBIT

EUR 80 m / EUR 20 m (2017)

Track record So far GroenLeven has developed and built 127

MW of solar projects in the Netherlands

Transaction

rationale

Market entry to the fast growing solar energy

market in the Netherlands; feed-in tariffs for

renewable energy in the Netherlands are very

high compared to rest of the world

BayWa r.e. among the 10 largest solar project

developers of the world

REALISED PROJECTS +

PROJECT PIPELINE (IN GW)

TECHNOLOGY

SPLIT

PROJEKT PIPELINE: APPROX. 2 GW

29 March 2018 Page 42

BayWa AG

Operational Outlook for FY 2018Prof. Klaus Josef Lutz

29 March 2018 Page 43

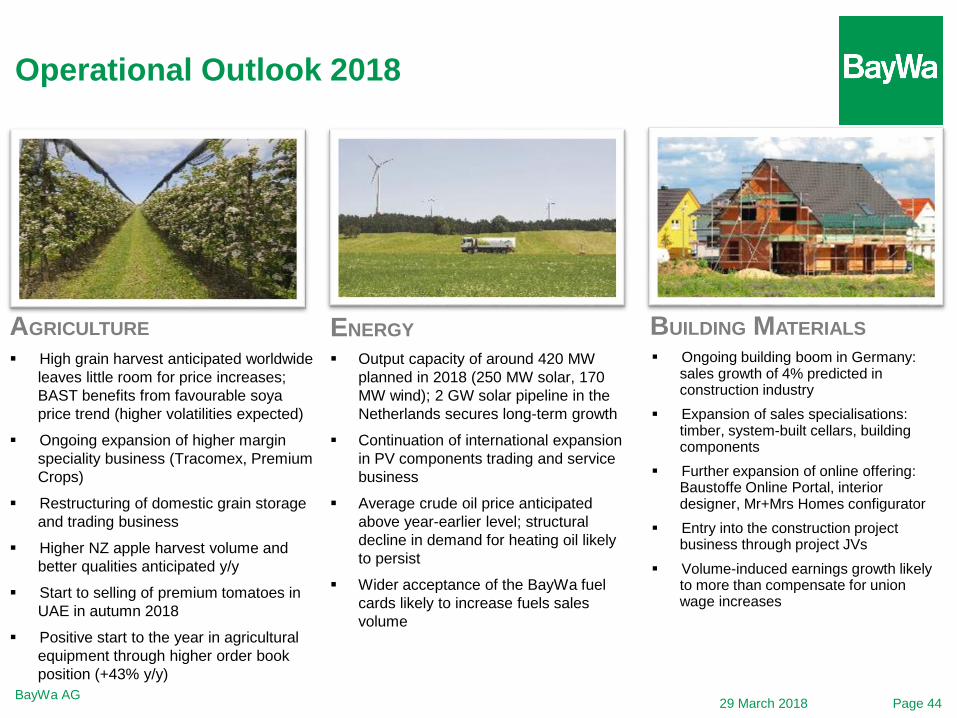

Operational Outlook 2018

BayWa AG

BUILDING MATERIALSENERGY

High grain harvest anticipated worldwide

leaves little room for price increases;

BAST benefits from favourable soya

price trend (higher volatilities expected)

Ongoing expansion of higher margin

speciality business (Tracomex, Premium

Crops)

Restructuring of domestic grain storage

and trading business

Higher NZ apple harvest volume and

better qualities anticipated y/y

Start to selling of premium tomatoes in

UAE in autumn 2018

Positive start to the year in agricultural

equipment through higher order book

position (+43% y/y)

Output capacity of around 420 MW

planned in 2018 (250 MW solar, 170

MW wind); 2 GW solar pipeline in the

Netherlands secures long-term growth

Continuation of international expansion

in PV components trading and service

business

Average crude oil price anticipated

above year-earlier level; structural

decline in demand for heating oil likely

to persist

Wider acceptance of the BayWa fuel

cards likely to increase fuels sales

volume

Ongoing building boom in Germany: sales growth of 4% predicted in construction industry

Expansion of sales specialisations: timber, system-built cellars, building components

Further expansion of online offering: Baustoffe Online Portal, interior designer, Mr+Mrs Homes configurator

Entry into the construction project business through project JVs

Volume-induced earnings growth likely to more than compensate for union wage increases

AGRICULTURE

29 March 2018 Page 44

Thank you for your attention The information in this presentation is partly made up of forward-looking statements which are based on assumptions and are subject to unforeseeable risks.In as much as the assumptions on the successful integration of acquisitions and on the internal growth of the company should prove to be inaccurate, or should other unforeseeable risks occur, the possibility of the assets, financial position and results of operations of the Group diverging negatively from the target figures cited in this presentation should not be discounted.BayWa AG can therefore undertake no guarantee that the actual development of the net worth, financial position and results of operations of the Group will concur with the target figures described in this presentation.

Appendix

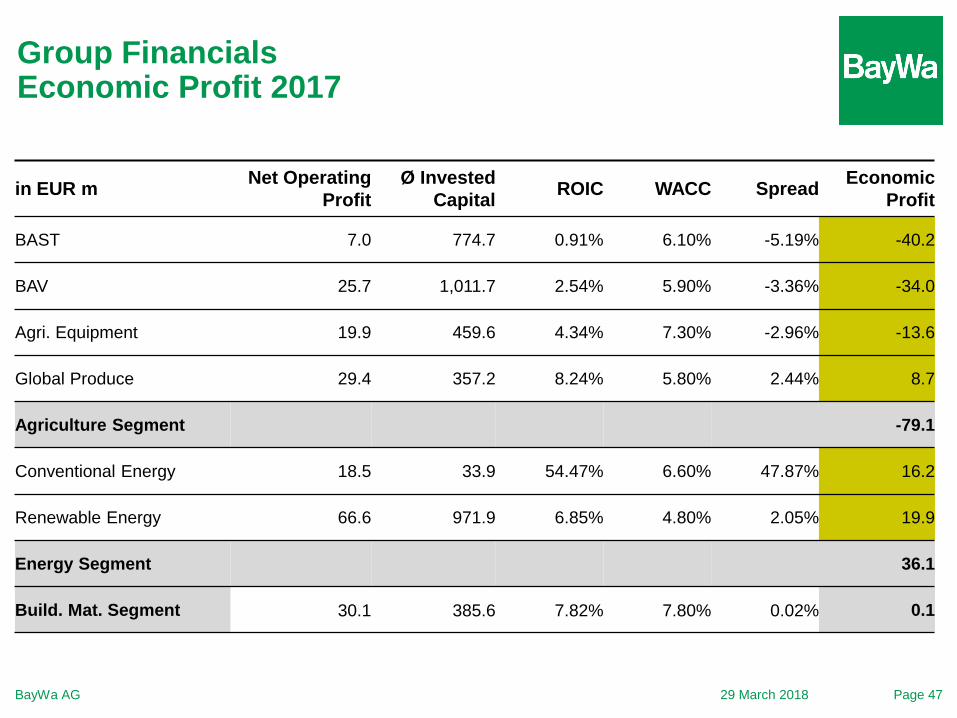

29 March 2018 Page 47BayWa AG

in EUR mNet Operating

Profit

Ø Invested

CapitalROIC WACC Spread

Economic

Profit

BAST 7.0 774.7 0.91% 6.10% -5.19% -40.2

BAV 25.7 1,011.7 2.54% 5.90% -3.36% -34.0

Agri. Equipment 19.9 459.6 4.34% 7.30% -2.96% -13.6

Global Produce 29.4 357.2 8.24% 5.80% 2.44% 8.7

Agriculture Segment -79.1

Conventional Energy 18.5 33.9 54.47% 6.60% 47.87% 16.2

Renewable Energy 66.6 971.9 6.85% 4.80% 2.05% 19.9

Energy Segment 36.1

Build. Mat. Segment 30.1 385.6 7.82% 7.80% 0.02% 0.1

Group FinancialsEconomic Profit 2017

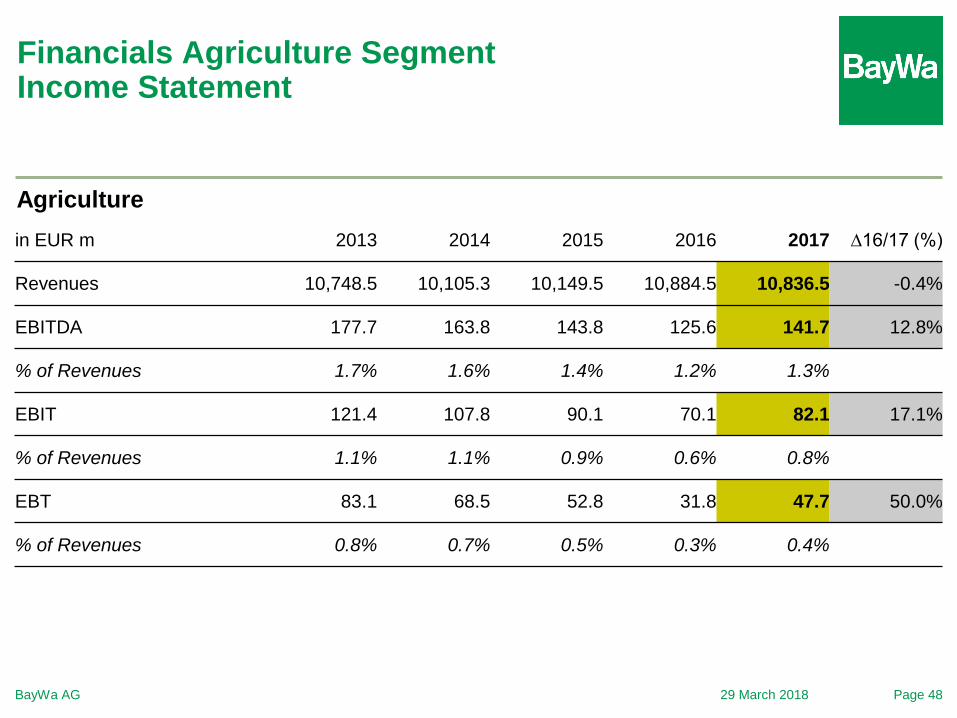

Financials Agriculture SegmentIncome Statement

29 March 2018 Page 48BayWa AG

Agriculture

in EUR m 2013 2014 2015 2016 2017 ∆16/17 (%)

Revenues 10,748.5 10,105.3 10,149.5 10,884.5 10,836.5 -0.4%

EBITDA 177.7 163.8 143.8 125.6 141.7 12.8%

% of Revenues 1.7% 1.6% 1.4% 1.2% 1.3%

EBIT 121.4 107.8 90.1 70.1 82.1 17.1%

% of Revenues 1.1% 1.1% 0.9% 0.6% 0.8%

EBT 83.1 68.5 52.8 31.8 47.7 50.0%

% of Revenues 0.8% 0.7% 0.5% 0.3% 0.4%

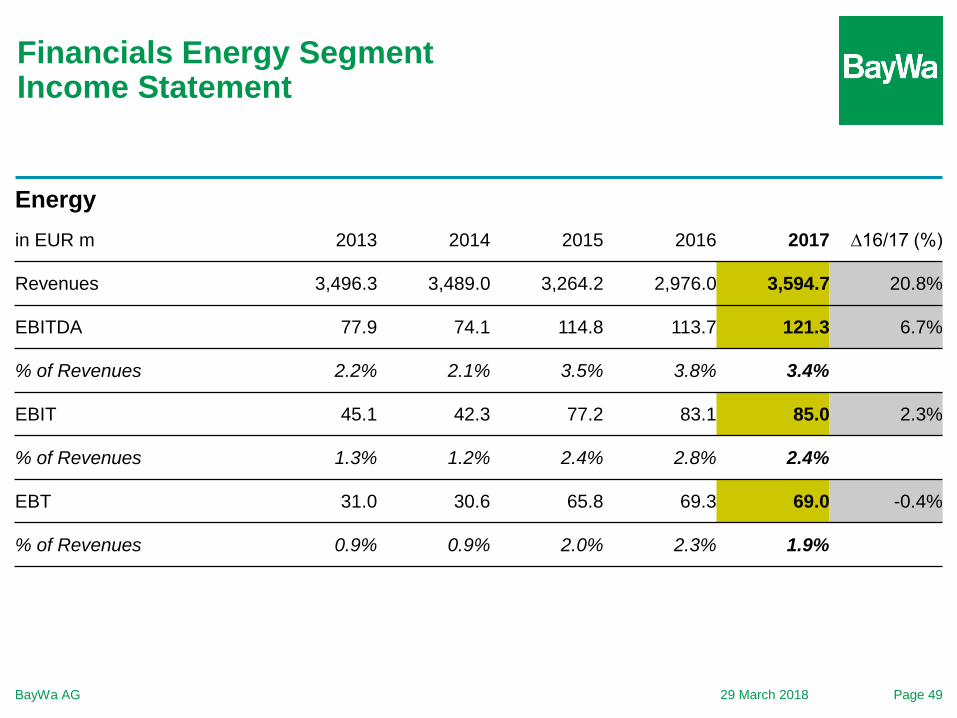

Financials Energy SegmentIncome Statement

29 March 2018 Page 49BayWa AG

Energy

in EUR m 2013 2014 2015 2016 2017 ∆16/17 (%)

Revenues 3,496.3 3,489.0 3,264.2 2,976.0 3,594.7 20.8%

EBITDA 77.9 74.1 114.8 113.7 121.3 6.7%

% of Revenues 2.2% 2.1% 3.5% 3.8% 3.4%

EBIT 45.1 42.3 77.2 83.1 85.0 2.3%

% of Revenues 1.3% 1.2% 2.4% 2.8% 2.4%

EBT 31.0 30.6 65.8 69.3 69.0 -0.4%

% of Revenues 0.9% 0.9% 2.0% 2.3% 1.9%

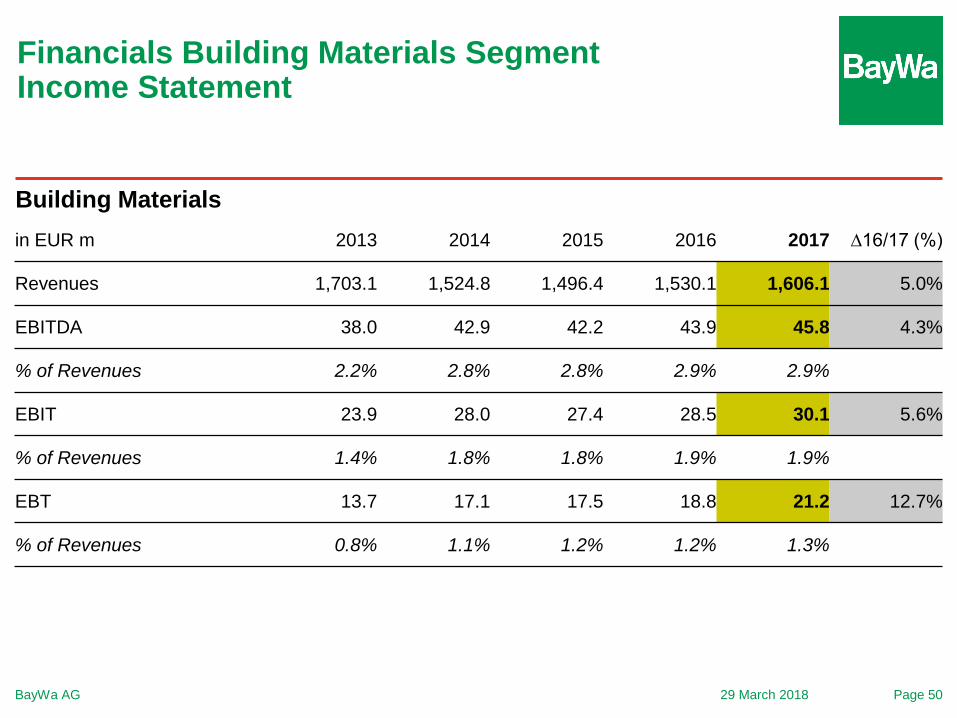

Financials Building Materials SegmentIncome Statement

29 March 2018 Page 50BayWa AG

Building Materials

in EUR m 2013 2014 2015 2016 2017 ∆16/17 (%)

Revenues 1,703.1 1,524.8 1,496.4 1,530.1 1,606.1 5.0%

EBITDA 38.0 42.9 42.2 43.9 45.8 4.3%

% of Revenues 2.2% 2.8% 2.8% 2.9% 2.9%

EBIT 23.9 28.0 27.4 28.5 30.1 5.6%

% of Revenues 1.4% 1.8% 1.8% 1.9% 1.9%

EBT 13.7 17.1 17.5 18.8 21.2 12.7%

% of Revenues 0.8% 1.1% 1.2% 1.2% 1.3%

BayWa AG

BayWa Share 2017

29 March 2018 Page 51

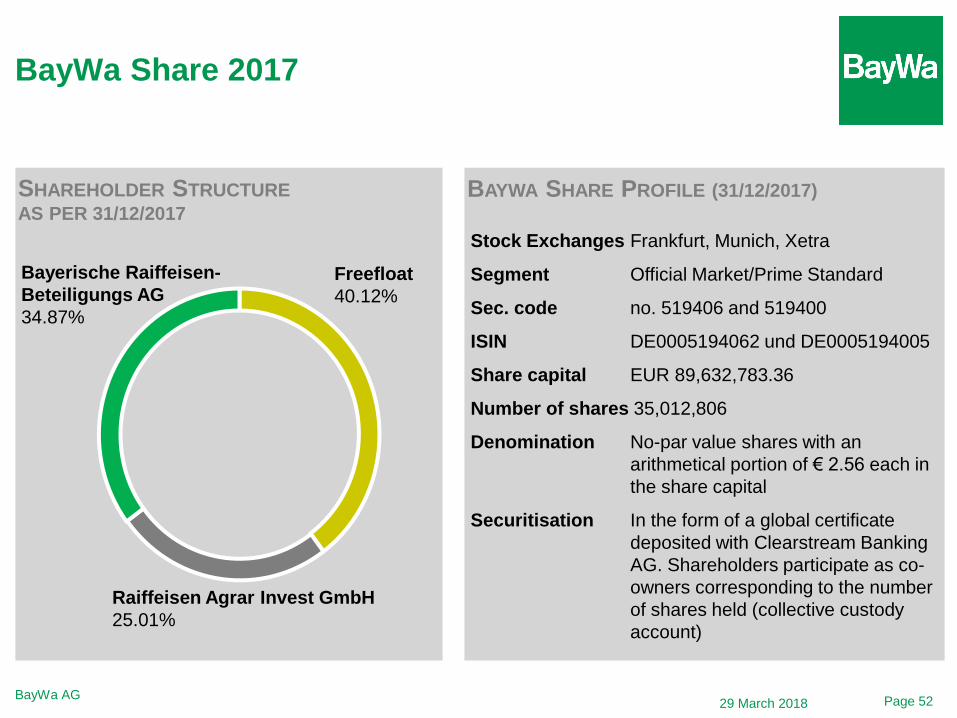

BayWa Share 2017

SHAREHOLDER STRUCTURE

AS PER 31/12/2017

Stock Exchanges Frankfurt, Munich, Xetra

Segment Official Market/Prime Standard

Sec. code no. 519406 and 519400

ISIN DE0005194062 und DE0005194005

Share capital EUR 89,632,783.36

Number of shares 35,012,806

Denomination No-par value shares with an

arithmetical portion of € 2.56 each in

the share capital

Securitisation In the form of a global certificate

deposited with Clearstream Banking

AG. Shareholders participate as co-

owners corresponding to the number

of shares held (collective custody

account)

BAYWA SHARE PROFILE (31/12/2017)

Freefloat

40.12%

Raiffeisen Agrar Invest GmbH

25.01%

Bayerische Raiffeisen-

Beteiligungs AG

34.87%

BayWa AG29 March 2018 Page 52

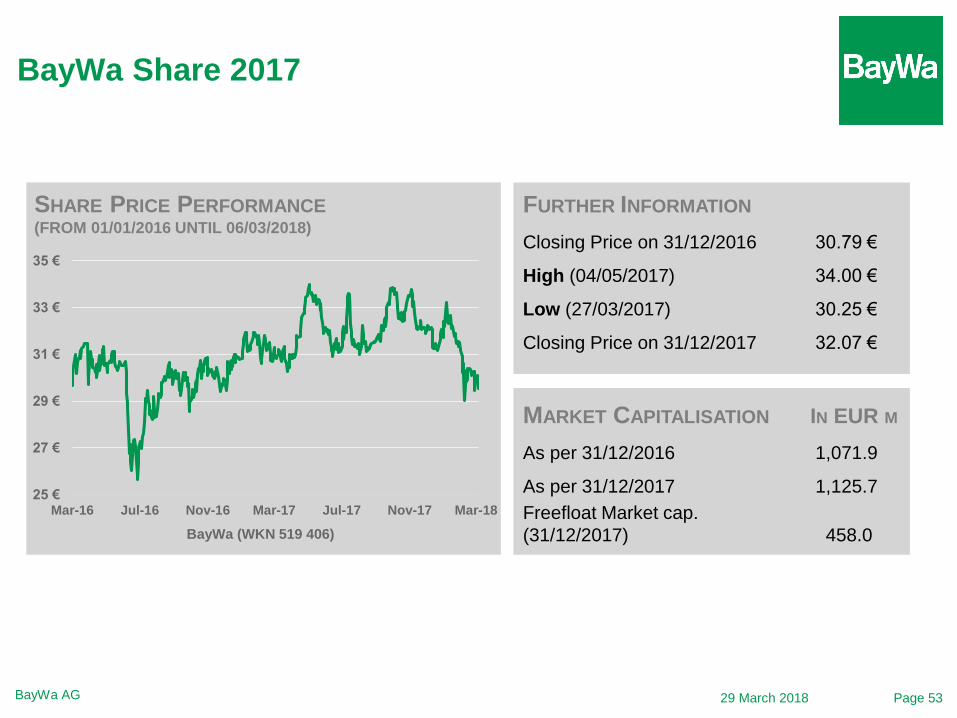

BayWa Share 2017

FURTHER INFORMATION

Closing Price on 31/12/2016 30.79 €

High (04/05/2017) 34.00 €

Low (27/03/2017) 30.25 €

Closing Price on 31/12/2017 32.07 €

MARKET CAPITALISATION IN EUR M

As per 31/12/2016 1,071.9

As per 31/12/2017 1,125.7

Freefloat Market cap.

(31/12/2017) 458.0

SHARE PRICE PERFORMANCE(FROM 01/01/2016 UNTIL 06/03/2018)

BayWa AG

25 €

27 €

29 €

31 €

33 €

35 €

Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Nov-17 Mar-18

BayWa (WKN 519 406)

29 March 2018 Page 53

Investor Relations Contact

JOSKO

RADELJIC

JULIUS

BLERSCH

Head of Investor Relations

Telefon +49 (089) 92 22 3887

Mobil +49 162 2828671

RAPHAELA

DA COSTA VON GEHLEN

Investor Relations Manager

Telefon +49 (089) 92 22 3151

Mobil +49 162 2828410

Junior Investor Relations Manager

Telefon +49 (089) 92 22 2873

Mobil +49 151 44024858

BAYWA AG

Arabellastraße 4

81925 Munich, Germany

Homepage: www.baywa.com

Financial Calendar 2018MARCH 2018

29/03 Analysts‘ Conference, BayWa AG in Munich

MAY 2018

09/05 Analysts‘ Conference Call Q1

JUNE 2018

05/06 Annual General Meeting, ICM Munich

RENATE

LORENZ

Assistant

Telefon +49 (089) 92 22 3881