annual financial report - city of port aransas, texas 2006-2007.pdf · annual financial report ......

TRANSCRIPT

ANNUAL FINANCIAL REPORT

FOR THE YEAR ENDED SEPTEMBER 30, 2007

CITY OF PORT ARANSAS, TEXASANNUAL FINANCIAL REPORT

FOR THE YEAR ENDED SEPTEMBER 30, 2007

TABLE OF CONTENTS

PageFINANCIAL SECTION:

Independent Auditors' Report 1

Management’s Discussion and Analysis 2

Basic Financial Statements:

Government-Wide Financial Statements:

Statement of Net Assets 15

Statement of Activities 16

Fund Financial Statements:

Balance Sheet – Governmental Funds 18

Statement of Revenues, Expenditures and Changes in Fund Balance – Governmental Funds 20

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Assets 22

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Revenues,

Expenditures and Changes in Fund Balance 23

Notes to the Financial Statements 24

Required Supplementary Information

Statement of Revenues, Expenditures and Changes in Fund Balance -Budget (GAAP Basis) and Actual – Major Governmental Funds:

General Fund 40Advertising Fund 41Beach Fund 42

Recreational Development Fund 43Port Aransas Recreational Development Corporation 44

SUPPLEMENTAL SECTION:COMBINING AND INDIVIDUAL FUND FINANCIAL STATEMENTS AND SCHEDULES:

GENERAL FUND:Comparative Balance Sheets 46Statement of Revenues, Expenditures and Changes in Fund Balance - Budget (GAAP Basis) and Actual 47Schedule of Revenues Compared to Budget (GAAP Basis) 48Schedule of Expenditures by Category 49

SPECIAL REVENUE FUNDS:

Municipal Airport Fund:Comparative Balance Sheets 50Statement of Revenues, Expenditures and Changes in Fund Balance - Budget (GAAP Basis) and Actual 51

Advertising Fund:Comparative Balance Sheets 52Statement of Revenues, Expenditures and Changes in Fund Balance - Budget (GAAP Basis) and Actual 53

TABLE OF CONTENTS - CONTINUED

Page

Beach Fund:Comparative Balance Sheets 54Statement of Revenues, Expenditures and Changes in Fund Balance - Budget (GAAP Basis) and Actual 55

Recreational Development Fund:Comparative Balance Sheets 56Statement of Revenues, Expenditures and Changes in Fund Balance - Budget (GAAP Basis) and Actual 57

Port Aransas Recreational Development Corporation:Comparative Balance Sheets 58Statement of Revenues, Expenditures and Changes in Fund Balance - Budget (GAAP Basis) and Actual 59

Port Aransas Library:Comparative Balance Sheets 60Comparative Statements of Revenues, Expenditures and Changes in Fund Balance 60

CAPITAL PROJECTS FUNDS:Combining Balance Sheet 61Combining Statement of Revenues, Expenditures and Changes in Fund Balances 62

OTHER SCHEDULES:Historical Statement of General Revenues 64Property Tax Collections 66Analysis of Ad Valorem Taxes Receivable by Year of Levy 68

FINANCIAL SECTION

INDEPENDENT AUDITORS’ REPORTMANAGEMENT’S DISCUSSION AND ANALYSIS

BASIC FINANCIAL STATEMENTSREQUIRED SUPPLEMENTARY INFORMATION

This Page Left Blank Intentionally

1

KOSAREK, DAVENPORT & CUDDCERTIFIED PUBLIC ACCOUNTANTS

A PROFESSIONAL LIMITED LIABILITY COMPANY5151 FLYNN PARKWAY - SUITE 604

CORPUS CHRISTI, TEXAS 78411-4394

WILLIE J. KOSAREK, CPA TELEPHONE 361-852-8223GARY R. DAVENPORT, CPA FAX 361-852-8688MARLEANA CUDD, CPA EMAIL [email protected]

INDEPENDENT AUDITORS’ REPORT

To the Honorable Mayor andMembers of the City Council

City of Port Aransas, Texas

We have audited the accompanying financial statements of the governmental activities, business-type activities, major funds and remaining fund information of the City of Port Aransas, Texas as of and for the year ended September 30, 2007, which collectively compromise the City's basic financial statements as listed in the table of contents. These financial statements are the responsibility of the City’s management. Our responsibility is to express opinions on these financial statements based on our audit.We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, therespective financial position of the governmental activities, the business-type activities, each major fund and the aggregate remaining fund information for the City of Port Aransas, Texas as of September 30, 2007, and the respective changes in financial position of those activities and funds for the year then ended in conformity with accounting principles generally accepted in the United States of America. The Management’s Discussion and Analysis and the other required supplementary information on pages 2 through 14 and pages 40 through 44 are not a required part of the basic financial statements but are supplementary information required by the Governmental Accounting Standards Board. We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the supplementary information. However, we did not audit the information and express no opinion on it.Our audit was conducted for the purpose of forming an opinion on the basic financial statements taken as a whole. The combining and individual fund financial statements and schedules listed in the table of contents are presented for purposes of additional analysis and are not a required part of the basic financial statements of the City of Port Aransas, Texas. This information has been subjected to the auditing procedures applied in the audit of the basic financial statements and, in our opinion, is fairlypresented in all material respects in relation to the basic financial statements taken as a whole.

Kosarek, Davenport & Cudd CPAs, PLLCApril 18, 2008

2

MANAGEMENT’S DISCUSSION AND ANALYSIS

This section of City of Port Aransas’ (City) annual financial report presents an overview, through management’s discussion and analysis (MD&A), of the City’s financial activities and performance during the fiscal year ended September 30, 2007. Please read it in conjunction with the independent auditors’ report and the City’s financial statements and disclosures, which follow this section.

FINANCIAL HIGHLIGHTS• The City’s total combined net assets were $23,829,053 and $22,899,789 as of September 30, 2007 and 2006,

respectively .• During the fiscal year ended September 30, 2007, the City’s net assets increased (decreased) by $1,779,115 for

governmental activities and by ($849,852) for business-type activities as compared to $1,143,409 and $358,231, respectively for the previous year ended September 30, 2006.

• Total expenditures in the City’s General Fund increased by $1,692 and $778,121 from 2006 and 2005, respectively.• Fund balances at September 30, 2007 and 2006, respectively are as follows: $2,365,065 & $3,186,478 - General

Fund; $781,702 & $560,432 - Beach Cleaning Fund; $446,474 & $1,258,549 - Recreational Development Fund and $206,072 & $267,359 - Port Aransas Recreational Development Corporation

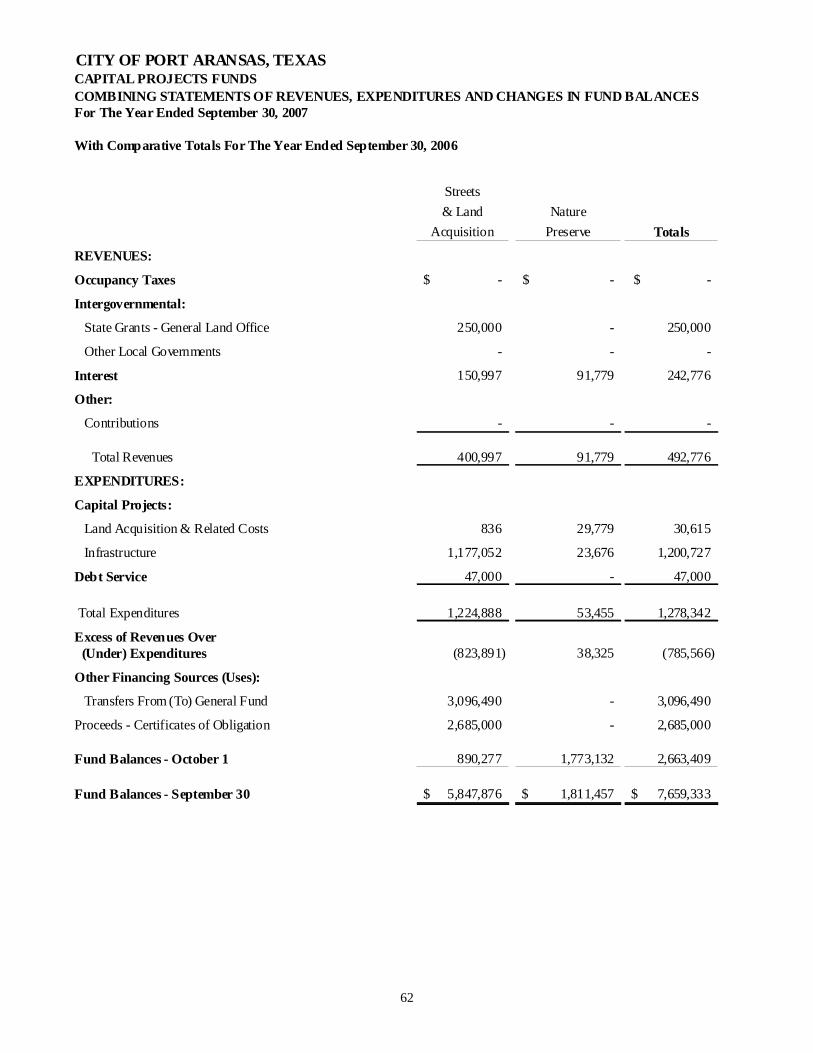

• The City issued certificates of obligation in the amount of $2,250,000 during the year ended September 30, 2004. The proceeds are being used to construct a nature preserve. At September 30, 2007 and 2006, the City has unexpended funds for this project totaling $1,811,457 and $1,773,132 respectively.

• The City issued general obligation bonds in the amount of $2,685,000 during the year ended September 30, 2007 for various street and drainage projects. The bond proceeds are accounted for in the Streets & Land Acquisition Fund. Along with transfers from other funds, the unexpended funds for these projects $5,847,876 and $890,277 at September 30, 2007 and 2006, respectively.

• The City has no authorized and unissued debt at September 30, 2007.

OVERVIEW OF THE FINANCIAL STATEMENTS

This annual report consists of three parts—management’s discussion and analysis (this section), the basic financial statements, and required supplementary information. Under GASB 34, basic financial statements include two kinds of statements that present different views of the City. Figure A-1 shows how the required parts of this annual report are arranged and related to one another. The remaining overview section of management’s discussion and analysis explains the structure and contents of each of the statements.

The first two statements are government-wide financial statements that provide both long-term and short-term information about the City’s overall financial status. The Statement of Net Assets and the Statement of Activities, which are the government-wide statements, report information about the City as a whole, and about its activities in a way that provides information helpful in determining whether the City’s financial condition has improved or deteriorated as a result of the current year’s activities.

The remaining statements are fund financial statements that focus on individual parts of the government, reporting the City’s operations in more detail than the government-wide statements. The funds are classified into three groups: Governmental Funds, Proprietary Funds and Fiduciary Funds.

• The Governmental Funds statements tell how general government services were financed in the short term as well as what remains for future spending.

• Proprietary and Fiduciary funds are not applicable to the City. The gas utility, sanitation and the marina are business-type activities. However, they are accounted for in the City’s general fund.

The notes to the financial statements explain some of the information in the financial statements and provide more detailed data that are necessary for a full understanding of the financial statements.

The statements and notes are followed by a section of required supplementary information that includes budgetary comparisons of the City’s major funds, as defined by GASB 34.

Figure A-1, Required Components ofthe City’s Annual Financial Report

3

Government-wide StatementsThe government-wide statements report information about the City as a whole using accounting methods similar to those used by private-sector companies. The statement of net assets includes all of the City’s assets and liabilities. All of the current year’s revenues and expenses are accounted for in the statement of activities regardless of when cash is received or paid.

The two government-wide statements report the City’s net assets and how they have changed. Net assets—the difference between the City’s assets and liabilities—is one way to measure the City’s financial health or position.

• Over time, increases or decreases in the City’s net assets are an indicator of whether its financial health is improving or deteriorating, respectively.

• To assess the overall health of the City, you need to consider additional nonfinancial factors such as changes in the City’s tax base, which has increased significantly over the past several years.

The government-wide financial statements of the City include all Governmental and business-type activities. All of the City’s services are included here. These activities are financed primarily by taxes and user fees charged to customers.

Fund Financial StatementsThe fund financial statements provide more detailed information about the City’s most significant funds—not the City as a whole. Funds are accounting devices that the City uses to keep track of specific sources of funding and spending for particular purposes. Because most of the City’s funds qualify as major funds, all funds are presented as if they are major funds. Actual major funds, as defined by GASB 34, include: General Fund, Advertising Fund, Beach Fund, Recreational Development Fund, Nature Preserve Capital Projects Fund and Streets & Land Acquisition Capital Projects Fund. The remaining funds, though not “Major” funds by definition, include the Municipal Airport Fund, Port Aransas Recreational Development Corporation and the Port Aransas Library Fund.

• Some funds are required by State law and by covenants of bonds/certificates of obligation.

• The City Council establishes other funds to control and manage money for particular purposes or to show that it is properly using certain taxes, fees and grants.

The City has only one of the three categories of funds mentioned below.

• Governmental funds—All of the City’s services are included in governmental funds, which focus on (1) how cash and other financial assets that can readily be converted to cash flow in and out and (2) the balances left at year-end that are available for spending. Consequently, the governmental fund statements provide a detailed short-term view that helps one determine whether there are more or fewer financial resources that can be spent in the near future to finance the City’s services. Because this information does not encompass the additional long-term focus of the government-wide statements, we provide additional information at the bottom of the governmental funds statement, or on the subsequent page, that explains the relationship (or differences) between them.

• Proprietary Funds – Although some of the City’s operations are similar to those ordinarily accounted for in Proprietary Funds, the City has chosen to report the harbor and utility funds’ operations in the General Fund.

• Fiduciary Funds—The City has no Fiduciary Funds.

4

GOVERNMENT-WIDE FINANCIAL ANALYSISAssets, Liabilities and Net assets as of September 30, 2007 and 2006 are summarized in Table A-1. Changes in the City’s net assets and the net cost of functional expenses are reported in Table A-2.

Table A-1Summary Statement of Net Assets

September 30, 2007 and 2006Governmental Act ivit ies Busines s-Type Act ivi ties To tal

2007 2006 2007 2006 2007 2006ASSETS:Current and o ther assets 12 ,096,685$ 7,300 ,821$ 653,413$ 1,518,251$ 12 ,750,097$ 8,819,072$Cap ital Assets - Net 14 ,427,604 14,338 ,251 2,347,504 2,340,268 16 ,775,108 16,678,519

T otal Assets 26 ,524,289$ 21,639 ,072$ 3,000,917$ 3,858,519$ 29 ,525,206$ 25,497,591$LIABI LITIES:Current liabili ties 1 ,201,290$ 608 ,768$ 162,132$ 167,291$ 1 ,363,421$ 776,059$Long-term liab ilities 4 ,350,478 1,821 ,742 - - 4 ,350,478 1,821,742

T otal Liabil ities 5 ,551,768 2,430 ,510 162,132$ 167,291$ 5 ,713,899 2,597,801NET ASSETS:Invested in capital assets - Net 13 ,743,652 14,130 ,107 2,347,504 2,340,268 16 ,091,156 16,470,375Restricted 1 ,605,571 2,284 ,584 - - 1 ,605,571 2,284,584Unrest ricted 5 ,638,454 2,793 ,870 493,872 1,350,960 6 ,132,326 4,144,830

Total Net Assets 20 ,987,677$ 19,208 ,561$ 2,841,376$ 3,691,228$ 23 ,829,053$ 22,899,789$

Changes in net assets are presented in Table A-2.Table A-2

Changes in Net AssetsF or The Years Ended September 30, 2007 and 2006

Governmental Activities

Business-Type Activities Total

% of Total Revenue FYE 2006

Increase (Decrease)

Progra m Revenues:Charges for Services 1,385,506$ 1,977,918$ 3,363,424$ 29.1 6% 3,076,023$ 287,401$

Operat ing Grants and Contributions 389,788 - 389,788 3.3 8% 530,283 (140,496)Capital Grants and Contributions 283,193 - 283,193 2.4 6% 590,790 (307,597)

Total Program Revenues 2,058,487 1,977,918 4,036,405 35.0 0% 4,197,097 (160,692)

General Rev enues & Transfers:Property Taxes 3,009,120 - 3,009,120 26.0 9% 2,876,317 -Other taxes 3,810,343 - 3,810,343 33.0 4% 3,521,899 288,444State shared revenues 103,159 - 103,159 0.8 9% 98,489 4,670Gain (losss ) sale of assets - - - 0.0 0% 183,018 (183,018)Investment Earnings 529,778 45,411 575,188 4.9 9% 328,074 247,114Transfers 1,200,000 (1,200,000) - 0.0 0% - -

Total General Revenues & Transfers 8,652,400 (1,154,589) 7,497,811 65.0 0% 7,007,798 357,210

Total Revenues & Transfers 10,710,887 823,329 11,534,215 100.0 0% 11,204,895 196,518$ 2007

Expenses: Net Cost

General government 3,098,257 - 3,098,257 26.8 6% 3,142,744 (44,486)$ (3 ,017,334)$ Police, Fire & EMS 1,860,630 - 1,860,630 16.1 3% 1,735,456 125,174 (1 ,513,155) Inspect ions 297,512 - 297,512 2.5 8% 261,413 36,099 117,749 Public Works & St reets 1,584,035 - 1,584,035 13.7 3% 1,166,886 417,149 (1 ,584,035) Parks and recreation 1,173,382 - 1,173,382 10.1 7% 970,592 202,790 (266,089) Library 185,156 - 185,156 1.6 1% 156,879 28,277 (166,265) Public Bui ldings 441,520 - 441,520 3.8 3% 355,737 85,783 (407,426) Public transportation 152,198 - 152,198 1.3 2% 120,097 32,101 102,351 Interest on long-term debt 139,080 - 139,080 1.2 1% 77,388 61,692 (139,080) Gas util ity & sanitation - 1,342,678 1,342,678 11.6 4% 1,336,531 6,147 168,426 Marina - 330,503 330,503 2.8 7% 379,533 (49,030) 136,311

T otal Expenses 8,931,772 1,673,181 10,604,953 91.9 4% 9,703,255 901,697 (6 ,568,548)$

Increase (Decrease) in Net Assets 1,779,115$ (849,852)$ 929,263$ 8.0 6% 1,501,640$ (705,179)$

5

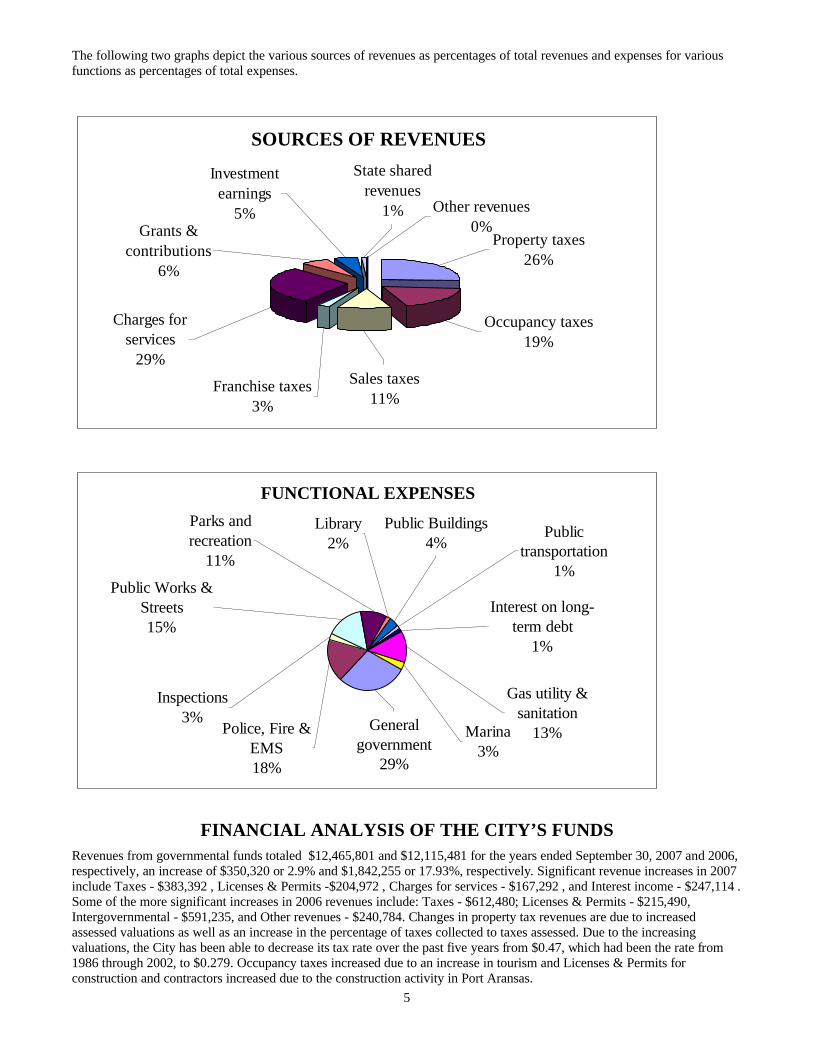

The following two graphs depict the various sources of revenues as percentages of total revenues and expenses for various functions as percentages of total expenses.

SOURCES OF REVENUES

Investment earnings

5%Property taxes

26%

Occupancy taxes19%

Sales taxes11%

Franchise taxes3%

Charges for services

29%

Other revenues0%

State shared revenues

1%Grants &

contributions6%

FUNCTIONAL EXPENSES

Interest on long-term debt

1%

Marina3%

Public transportation

1%

Gas utility & sanitation

13%

Public Buildings4%

Library2%

Parks and recreation

11%

Public Works & Streets15%

Inspections3%

Police, Fire & EMS18%

General government

29%

FINANCIAL ANALYSIS OF THE CITY’S FUNDSRevenues from governmental funds totaled $12,465,801 and $12,115,481 for the years ended September 30, 2007 and 2006, respectively, an increase of $350,320 or 2.9% and $1,842,255 or 17.93%, respectively. Significant revenue increases in 2007include Taxes - $383,392 , Licenses & Permits -$204,972 , Charges for services - $167,292 , and Interest income - $247,114 . Some of the more significant increases in 2006 revenues include: Taxes - $612,480; Licenses & Permits - $215,490, Intergovernmental - $591,235, and Other revenues - $240,784. Changes in property tax revenues are due to increased assessed valuations as well as an increase in the percentage of taxes collected to taxes assessed. Due to the increasing valuations, the City has been able to decrease its tax rate over the past five years from $0.47, which had been the rate from 1986 through 2002, to $0.279. Occupancy taxes increased due to an increase in tourism and Licenses & Permits for construction and contractors increased due to the construction activity in Port Aransas.

6

General Fund Budgetary HighlightsOver the course of the year, the City revised its budget twice increasing expenditures and transfers by $27,500 in the General Fund and $9,500 in the Recreational Development Fund. Budget variances are “Favorable” if actual revenues exceed budgeted amounts and if actual expenditures are under budgeted amounts. Variances are “Unfavorable” if actual revenues are under budgeted amounts and if actual expenditures are over budgeted amounts. Favorable variances are indicated by showing amounts without brackets and unfavorable variances are indicated by bracketed amounts. The only departmental unfavorable variance is for the Public Works department where costs exceeded the budget by $1,014.

FY 2007 revenues were budgeted to increase by $125,485 or 1.48% and expenditures were budgeted to increase $1,431,864or 18.82%. Budget variances for the current year are as follows: Revenues - $33,762 and Expenditures - $1,430,172. The actual budget comparison is presented on page 40 and a more detailed comparison of revenues is presented on page 48. Also, graphs, which are presented at the end of this discussion and analysis, provide additional information regarding actual increases and decreases in various sources of revenues for all of the City’s funds.

CAPITAL ASSETS AND DEBT ADMINISTRATIONCapital Assets

At September 30, 2007 and 2006, the City had invested $16,775,108 and $16,678,519 , net of depreciation, in a broad range of capital assets, including land, buildings, infrastructure, machinery & equipment, and vehicles. In 2007, the City acquired assets totaling $950,550 for use in governmental activities and acquired assets totaling 138,692 for use in its business type activities. In 2006, the City acquired land totaling $765,424, other capital assets used in governmental activities totaling $1,148,843 and assets used in business-type activities totaling $84,065. More detailed information about the City’s capital assets is presented in the notes to the basic financial statements.

Long Term DebtPrincipal payments on the Certificates of Obligation of $125,000 and $120,000 were recorded in 2007 and 2006, respectively. The capitalized lease obligation decreased $54,721 and $32,458 in 2007 and 2006, respectively. Net increases in compensated absences for 2007 and 2006 were $17,999 and $4,416, respectively.

Bond Ratings - Standard & Poor’s assigned rating is “A-".

GRAPHS OF SELECTED DATA

Selected data from the Governmental funds are represented by the following charts and graphs. The time-lines presented in the accompanying charts and graphs present the most current year on the left-hand side of the graph and each preceding year is to the right. This presentation is necessary because this is the order that all of the City’s financial information is presented in the financial statements and other schedules.

7

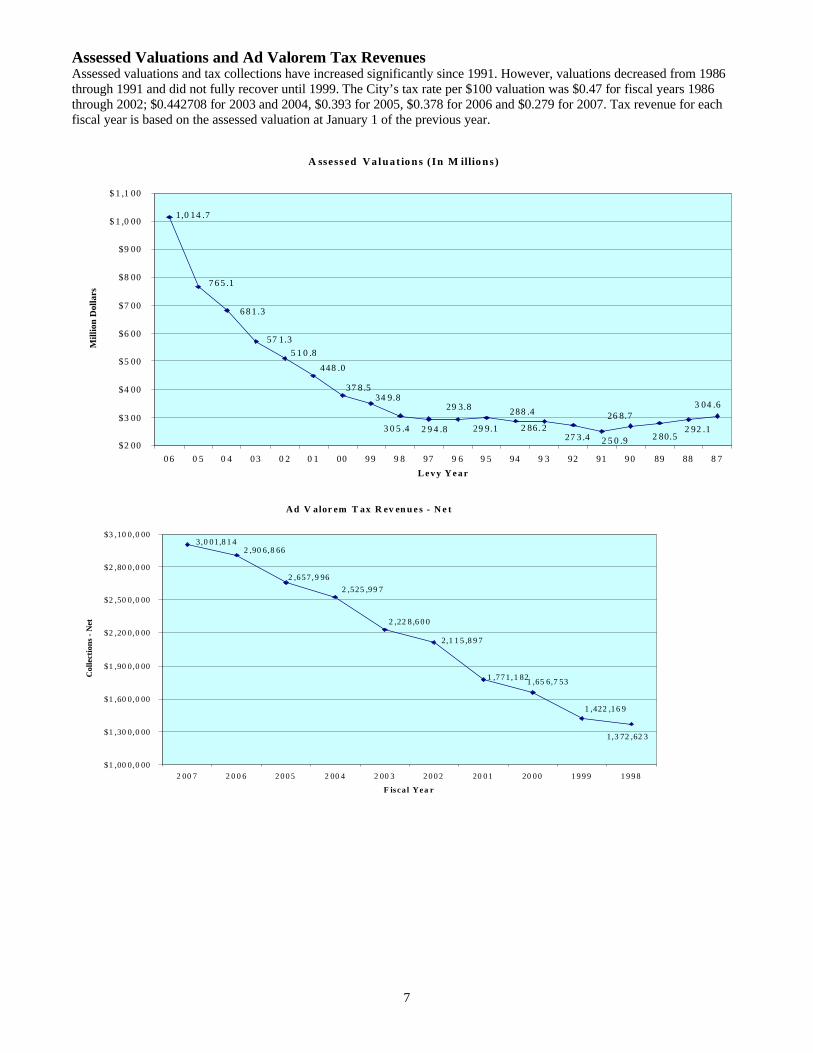

Assessed Valuations and Ad Valorem Tax RevenuesAssessed valuations and tax collections have increased significantly since 1991. However, valuations decreased from 1986through 1991 and did not fully recover until 1999. The City’s tax rate per $100 valuation was $0.47 for fiscal years 1986through 2002; $0.442708 for 2003 and 2004, $0.393 for 2005, $0.378 for 2006 and $0.279 for 2007. Tax revenue for each fiscal year is based on the assessed valuation at January 1 of the previous year.

A ssessed V a l u a t io n s (In M illio n s )

2 92 .129 9.1

288 .429 3.8

2 86. 227 3 .4 2 5 0 .9

26 8.7

2 80.53 0 5 .4

34 9.8

1,0 14 .7

57 1.3

2 9 4 .8

37 8 .5

448 .05 1 0 .8

6 8 1 .3

7 6 5 .1

3 04 .6

$2 00

$3 00

$4 00

$5 00

$6 00

$7 00

$8 00

$9 00

$ 1 ,0 00

$ 1 ,1 00

0 6 0 5 0 4 0 3 0 2 0 1 00 9 9 9 8 97 9 6 9 5 94 9 3 92 91 9 0 89 88 8 7L e v y Y e a r

Mill

ion

Dol

lars

Ad V alor em T ax R ev en u e s - N e t

2 ,22 8 ,6 0 0

2,1 1 5 ,8 9 7

2 ,90 6,8 66

1,3 72 ,62 3

1 ,422 ,16 9

1 ,65 6,7 531 ,771 ,1 82

2 ,525 ,99 72 ,657 ,9 96

3,0 01,8 1 4

$1 ,00 0,0 00

$1 ,30 0,0 00

$1 ,60 0,0 00

$1 ,90 0,0 00

$2 ,20 0,0 00

$2 ,50 0,0 00

$2 ,80 0,0 00

$3 ,10 0,0 00

2 00 7 2 0 0 6 2 0 0 5 2 00 4 2 00 3 2 0 0 2 20 01 20 00 1 9 9 9 1 9 9 8

F isca l Yea r

Col

lect

ions

- N

et

8

Various Taxes as a Percentage of Total TaxesThe make up of the various taxes as a % of total tax revenues each fiscal year have not changed significantly. The make up of tax collections has been approximately as follows: Ad valorem 40%; Sales 20%,Occupancy 30% & Franchise 10%.

Sales Tax RevenuesSales tax revenues have increased each year except for fiscal years 1998 and 2003. TheCity increased its sales tax rate from 1% to 1½% in 1996. The additional 1/2% sales tax has been recorded in the Port Aransas Recreational Development Corporation and is restricted to economic development.

Franchise Tax RevenuesThe primary franchise tax comes from the electric utility company. The increase in 2001 is due primarily to a one-time settlement with the electric utility company totaling $56,313. Franchise taxes from electric utilities have decreased from 2001 through 2005. The decreases are most likely due to the deregulation of the utility industry allowing customers to choose their utility providers. None of the other utility providers have submitted Franchise Tax reports or remitted any Franchise Tax payments. Franchise taxes from cable TV, telephoneand BFI/others have generally increased over the years.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998Fiscal Year

Percentages of Tax Revenues

Franchise TaxOccupancyCity Sales Ad valorem - Net

Sales Tax Revenues

1,070,234

818,553

916,334

674,355 611,687

967,883963,823

1,261,977

1,245,245

1,096,962

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000

$1,100,000

$1,200,000

$1,300,000

$1,400,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998Fiscal Year

Franchise Tax Revenue

358,881

374,905

390,781

361,100

389,591

389,621

454,150

310,751265,377

292,544

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

Fiscal Year

9

Franchise Tax - Electricity

200,000

225,000

250,000

275,000

300,000

325,000

350,000

375,000

400,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

Fiscal Year

Franchise Tax - Other Than Electricity

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998FISCAL YEAR

BFI &OtherPhoneCable TV

Hotel-Motel Occupancy Tax Revenues

Occupancy taxes continue to increase due to the growth in tourism. The rate was increased from 6% to 7% effective 1/1/99.

Occupancy Tax Revenues

1,702,446

1,369,3271,390,289

1,901,749

2,157,586

1,416,879

1,533,239

1,310,703

1,126,194

856,035

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998Fiscal Year

Construction PermitsAlthough there are a few years with decreases, revenues have steadily increased over the ten-year period.There have been significant increases since 2003 reflecting theincreased construction activity in Port Aransas.

Construction Permits & Contractor Licenses

161,090

409,810

276,132

181,159

252,396

133,067

151,423

130,368 94,714 127,462

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998Fiscal Year

10

Food and Beverage PermitsPermit fees are as follows: Food -$3.50; Beer & Wine (on premise) -$87.50 and mixed beverage -$375.00. At these rates, there has to be substantial growth or decline to significantly affect total income. Fluctuations are more likely due to the fact that the mixed beverage permit is a multiyear permit and some years have more of these permits due than others.

Food & Beverage Permits

7,242

5,412

6,439

7,880

6,9966,535

11,374

7,027 6,974

8,554

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

$12,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

Fiscal Year

Beach Parking PermitsPermit sales fluctuate based not only on the level of tourism on the island; but also, due to the level of enforcement of the parking permitrules. Sales increased to over $200,000 from 1999 through 2002. In 2003, the City entered into an agreement with the City of Corpus Christi and Nueces County to sell beach parking permits that would be valid on all beaches governed by the three entities. This agreement benefited the many visitors to Port Aransas, Mustang Island and North Padre Island. Revenues have fluctuated up and down each year since the agreement was approved. The agreement provided that the City would be reimbursed for any loss of revenue in 2003. The reimbursement was not determined

or received until 2004.

Beach Parking Permits

271,403

159,543

214,123

418,245

351,790

138,601

217,467 219,814

172,473215,046

$130,000

$180,000

$230,000

$280,000

$330,000

$380,000

$430,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

Fiscal Year

11

Intergovernmental Revenues

Regular intergovernmental revenues are made up of the following: Federal Emergency Management Assistance, Texas Beach Cleaning Grant, State Shared Beverage Tax and various grants and reimbursements from county and local governmental agencies. The most significant grants and reimbursements received during the ten-year period include: 1998 - Park Grant from the Texas Parks & Wildlife - $472,969; First Phase of the Coastal Erosion Project - $491,982 in 2001 and $795,665 in 2002. The first phase of the Coastal Erosion Project was completed in 2002 at a total cost of $1,329,258. This project was financed by the Texas General Land Office (GLO) ($998,147), Port of Corpus Christi Authority ($124,500), Nueces County WC&ID #4 ($165,000) and the City ($41,611). The second phase of the Coastal Erosion Project, which cost $883,639, was completed in 2003. This project was financed by the Texas General Land Office ($551,835), Port of Corpus Christi Authority ($150,000), and the City ($181,804). In 2003, the City also received a $427,100 block grant from the Texas Department of Transportation for renovation to the Port Aransas Municipal Airport. The renovations were completed in 2003. FY’s 2004 through 2006 include grants from the Texas General Land Office for land acquisition in Charlie’s Pasture, which will be used for the nature preserve. FY 2006 also includes $200,000 from the Port of Corpus Christi (Bulkhead); $151,117 for Equipment, $18,163 for the Airport; $15,755 for the Hike & Bike Trail.

Inter gove rnm enta l Re venue s

1 ,23 7,4 46

7 7 3 ,98 4

5 5 1 ,27 7

1,1 42 ,51 2

6 3 2 ,76 6

1,5 01,346

331,027

863,022

310,592

7 8 5 ,99 1

$100 ,0 00

$300 ,0 00

$500 ,0 00

$700 ,0 00

$900 ,0 00

$1 ,10 0,0 00

$1 ,30 0,0 00

$1 ,50 0,0 00

$1 ,70 0,0 00

20 07 200 6 200 5 2 0 0 4 2 0 0 3 20 02 20 01 20 00 19 99 19 98

F iscal Year

Sanitation RevenuesSanitation revenues include regular trash pick-up and fees charged at the collection station. Except for 2003 and 2001, revenues have generally increased. Collection Station fees have been as follows:2006-07 - $43,0152005-06 - $36,7062004-05 - $31,6562003-04 - $32,4632002-03 - $42,8812001-02 - $57,3722000-01 - $28,1081999-00 - $71,025The decreases in revenues have been due to the decreases in the Collection Station revenues.

Sanitation Revenues

336,252

297,891286,640

400,695

480,773

319,552

285,362

251,284

271,821

237,853

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

Fiscal Year

12

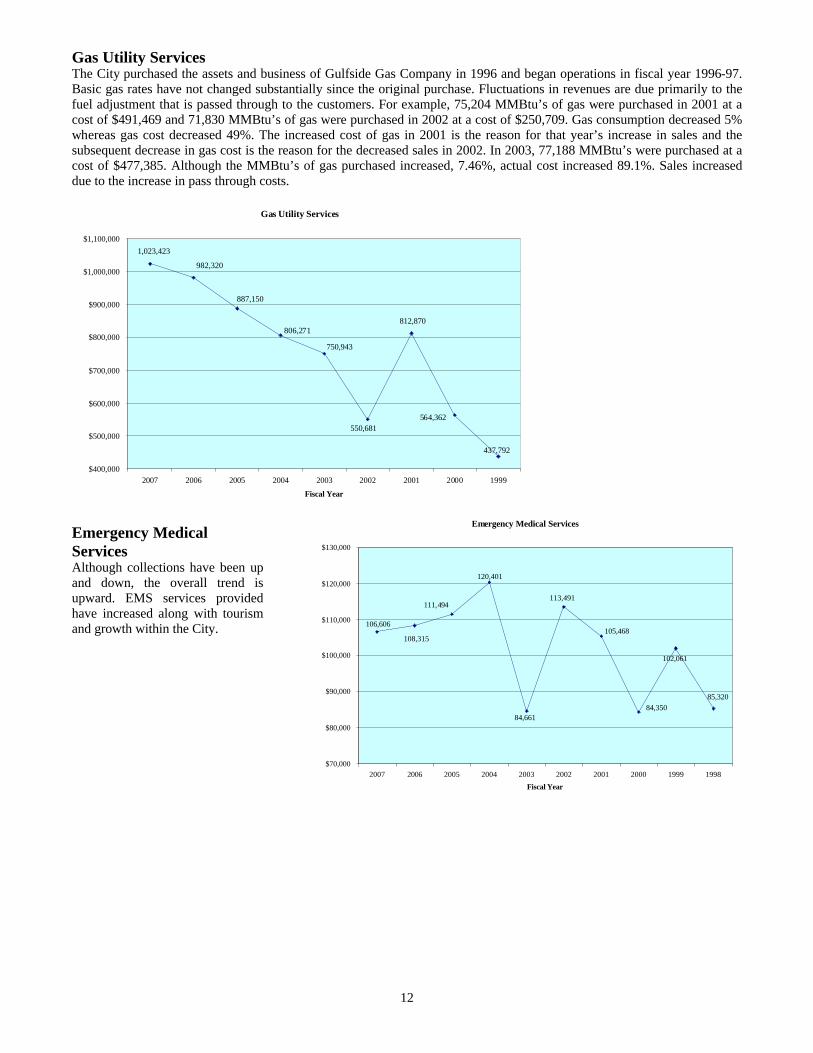

Gas Utility ServicesThe City purchased the assets and business of Gulfside Gas Company in 1996 and began operations in fiscal year 1996-97. Basic gas rates have not changed substantially since the original purchase. Fluctuations in revenues are due primarily to the fuel adjustment that is passed through to the customers. For example, 75,204 MMBtu’s of gas were purchased in 2001 at a cost of $491,469 and 71,830 MMBtu’s of gas were purchased in 2002 at a cost of $250,709. Gas consumption decreased 5% whereas gas cost decreased 49%. The increased cost of gas in 2001 is the reason for that year’s increase in sales and the subsequent decrease in gas cost is the reason for the decreased sales in 2002. In 2003, 77,188 MMBtu’s were purchased at a cost of $477,385. Although the MMBtu’s of gas purchased increased, 7.46%, actual cost increased 89.1%. Sales increased due to the increase in pass through costs.

Gas Utility Services

437,792

564,362

1,023,423

550,681

812,870

982,320

750,943

806,271

887,150

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000

$1,100,000

2007 2006 2005 2004 2003 2002 2001 2000 1999

Fiscal Year

Emergency Medical ServicesAlthough collections have been up and down, the overall trend is upward. EMS services provided have increased along with tourism and growth within the City.

Emergency Medical Services

102,061

108,315

106,606105,468

84,350

111,494

120,401

84,661

113,491

85,320

$70,000

$80,000

$90,000

$100,000

$110,000

$120,000

$130,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998Fiscal Year

13

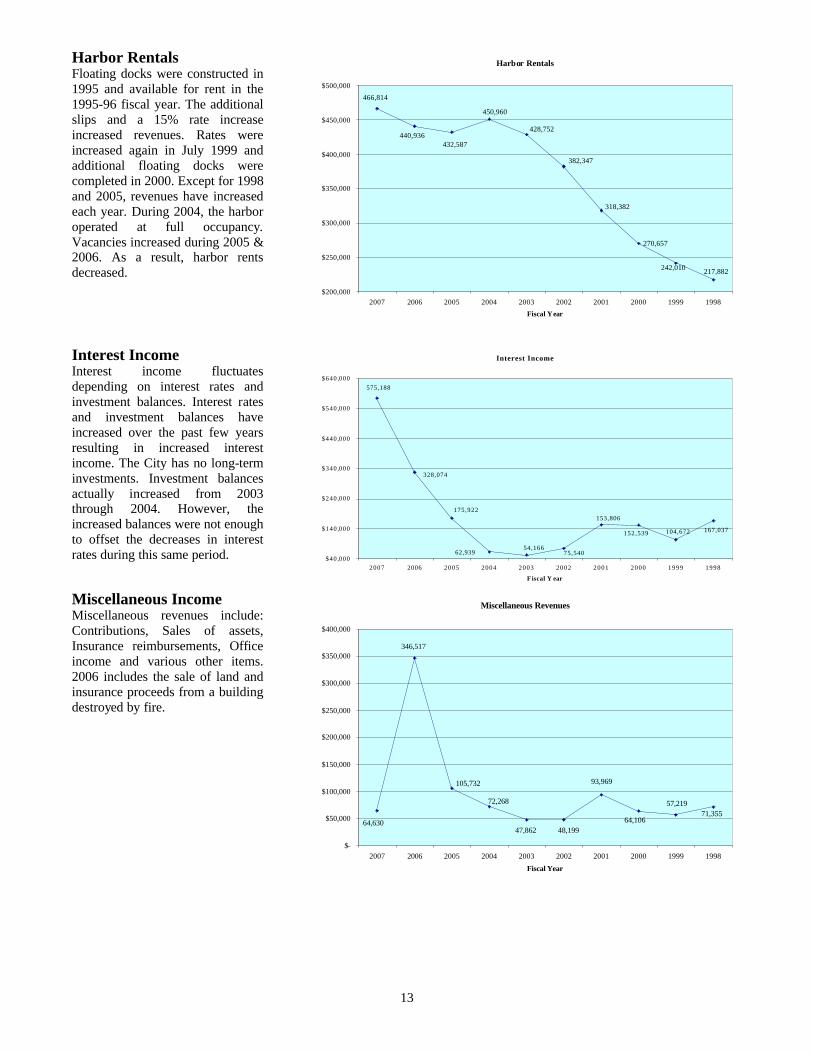

Harbor RentalsFloating docks were constructed in 1995 and available for rent in the 1995-96 fiscal year. The additional slips and a 15% rate increaseincreased revenues. Rates were increased again in July 1999 and additional floating docks were completed in 2000. Except for 1998and 2005, revenues have increasedeach year. During 2004, the harbor operated at full occupancy. Vacancies increased during 2005 & 2006. As a result, harbor rents decreased.

Harbor Rentals

466,814

440,936432,587

428,752

382,347

450,960

318,382

242,010

270,657

217,882

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998Fiscal Year

Interest IncomeInterest income fluctuates depending on interest rates and investment balances. Interest ratesand investment balances have increased over the past few years resulting in increased interest income. The City has no long-term investments. Investment balances actually increased from 2003 through 2004. However, the increased balances were not enough to offset the decreases in interest rates during this same period.

Interest Income

175,922

328,074

54,166

153,806

152,539

75,540

575,188

62,939

167,037104,672

$40 ,000

$140,000

$240,000

$340,000

$440,000

$540,000

$640,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

F iscal Y ear

Miscellaneous IncomeMiscellaneous revenues include: Contributions, Sales of assets, Insurance reimbursements, Office income and various other items. 2006 includes the sale of land and insurance proceeds from a building destroyed by fire.

Miscellaneous Revenues

346,517

72,268

47,86264,630

105,732

48,199

93,969

64,106

57,21971,355

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2007 2006 2005 2004 2003 2002 2001 2000 1999 1998Fiscal Year

14

CONTACTING THE CITY’S FINANCIAL MANAGEMENTThis financial report is designed to provide our citizens, taxpayers, customers, and investors and creditors with a general overview of the City’s finances and to demonstrate the City’s accountability for the money it receives. If you have questions about this report or need additional financial information, contact the City’s Business Office, at 710 West Avenue A, Port Aransas, Texas 78373 or call 1-361-749-4111. Some additional information is also available on the City’s web-site @www.cityofportaransas.org

15

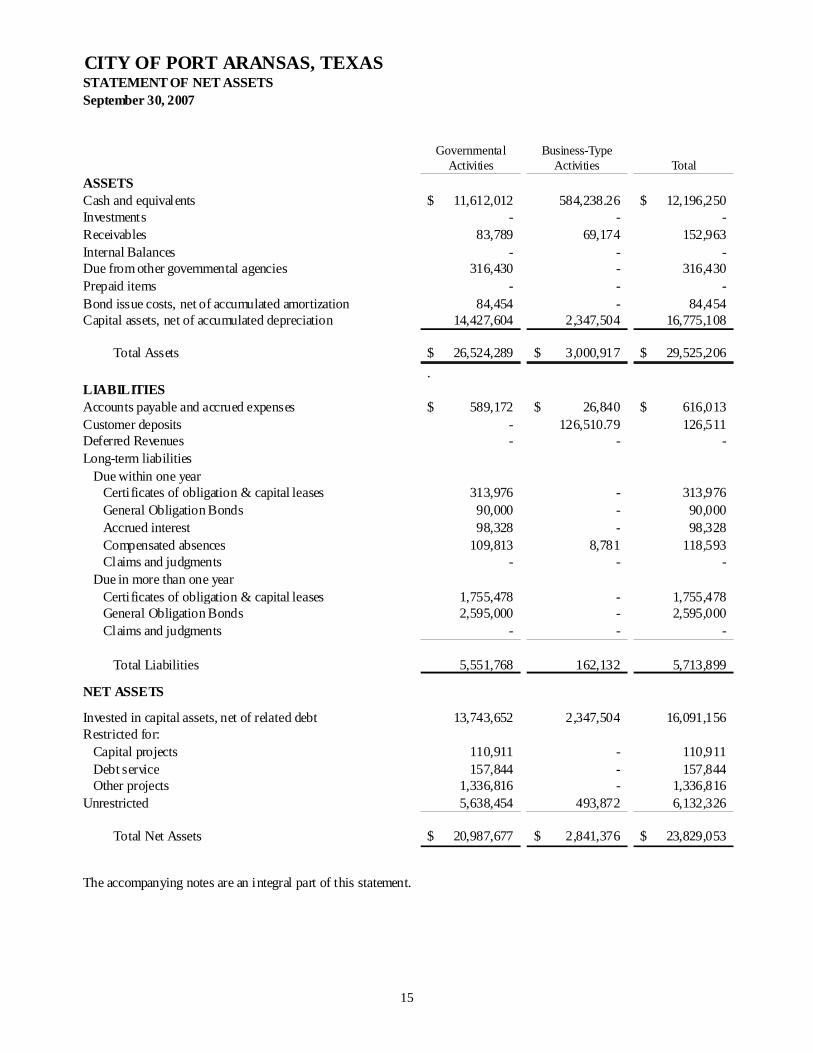

CITY OF PORT ARANSAS, TEXASSTATEMENT OF NET ASSETSSeptember 30, 2007

Governmental Activities

Business-Type Activities Total

ASSETSCash and equivalents 11,612,012$ 584,238.26 12,196,250$ Investments - - - Receivables 83,789 69,174 152,963 Internal Balances - - - Due from other governmental agencies 316,430 - 316,430 Prepaid items - - - Bond issue costs, net of accumulated amortization 84,454 - 84,454 Capital assets, net of accumulated depreciation 14,427,604 2,347,504 16,775,108

Total Assets 26,524,289$ 3,000,917$ 29,525,206$ .

LIABILITIESAccounts payable and accrued expenses 589,172$ 26,840$ 616,013$ Customer deposits - 126,510.79 126,511 Deferred Revenues - - - Long-term liabilities

Due within one yearCertificates of obligation & capital leases 313,976 - 313,976 General Obligation Bonds 90,000 - 90,000 Accrued interest 98,328 - 98,328 Compensated absences 109,813 8,781 118,593 Claims and judgments - - -

Due in more than one yearCertificates of obligation & capital leases 1,755,478 - 1,755,478 General Obligation Bonds 2,595,000 - 2,595,000 Claims and judgments - - -

Total Liabilities 5,551,768 162,132 5,713,899

NET ASSETS

Invested in capital assets, net of related debt 13,743,652 2,347,504 16,091,156 Restricted for:

Capital projects 110,911 - 110,911 Debt service 157,844 - 157,844 Other projects 1,336,816 - 1,336,816

Unrestricted 5,638,454 493,872 6,132,326

Total Net Assets 20,987,677$ 2,841,376$ 23,829,053$

The accompanying notes are an integral part of this statement.

16

CITY OF PORT ARANSAS, TEXASSTATEMENT OF ACTIVITIESFor the Year Ended September 30, 2007

Functions/Programs ExpensesCharges for

ServicesOperating Grants & Contributions

Capital Grants & Contributions

Primary governmentGovernmental Activities

General government 3,098,257$ 74,465$ 6,459$ -$ Police 1,259,178 217,388 23,481 - Fire 157,246 - - - Emergency medical services 444,207 106,606 - - Inspections 297,512 415,261 - - Public works & streets 1,584,035 - - - Parks and recreation 1,173,382 520,519 103,581 283,193 Library 185,156 17,174 1,717 - Public buildings 441,520 34,094 - - Public transportation 152,198 - 254,550 - Interest on long-term debt 139,080 - - -

Total governmental activities 8,931,772 1,385,506 389,788 283,193

Business-type activitiesGas utility & sanitation 1,342,678 1,511,103 - - Harbor 330,503 466,814 - -

Total business-type activities 1,673,181 1,977,918 - -

Total primary government 10,604,953$ 3,363,424$ 389,788$ 283,193$

General revenues:Taxes:

Property taxes, levied for general purposesProperty taxes, levied for debt serviceFranchise taxesOccupancy taxesSales & use taxesState shared beverage tax

Unrestricted investment earningsMiscellaneous

Transfers

Total general revenues, special items, and transfers

Change in net assets

Net assets - beginning

Net assets - ending

The accompanying notes are an integral part of this statement.

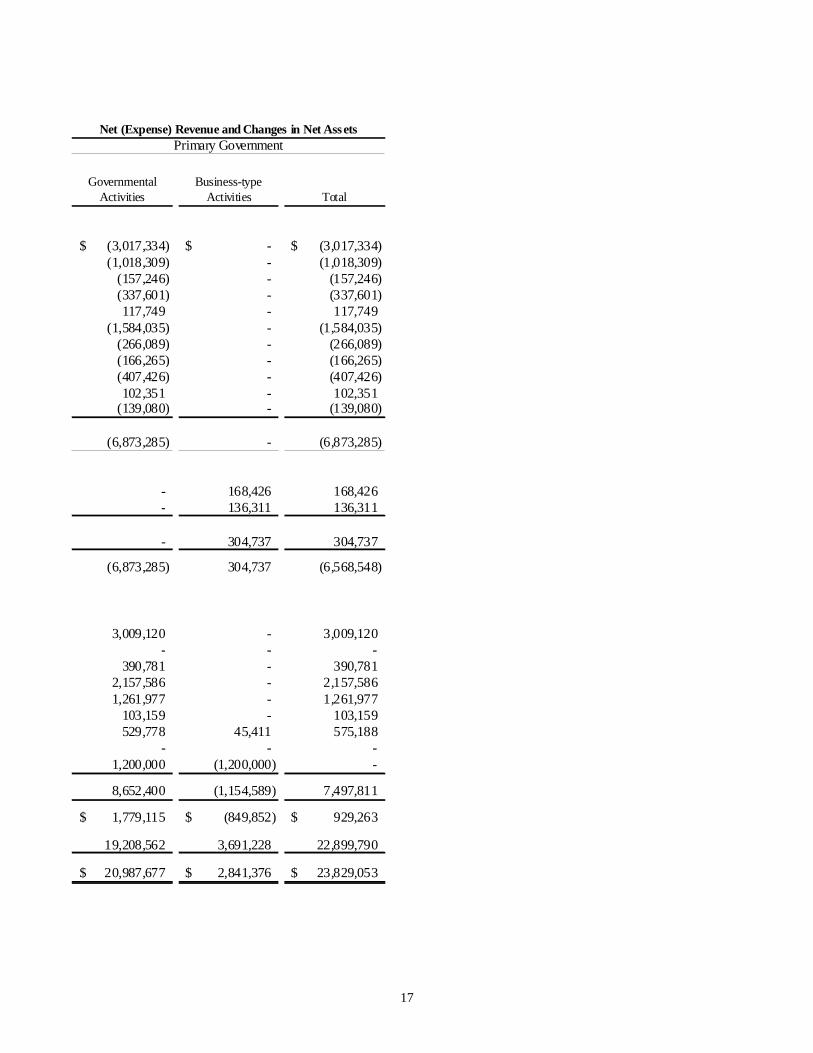

Program Revenue

17

Governmental Activities

Business-type Activities Total

(3,017,334)$ -$ (3,017,334)$ (1,018,309) - (1,018,309)

(157,246) - (157,246) (337,601) - (337,601) 117,749 - 117,749

(1,584,035) - (1,584,035) (266,089) - (266,089) (166,265) - (166,265) (407,426) - (407,426) 102,351 - 102,351

(139,080) - (139,080)

(6,873,285) - (6,873,285)

- 168,426 168,426 - 136,311 136,311

- 304,737 304,737

(6,873,285) 304,737 (6,568,548)

3,009,120 - 3,009,120 - - -

390,781 - 390,781 2,157,586 - 2,157,586 1,261,977 - 1,261,977

103,159 - 103,159 529,778 45,411 575,188

- - - 1,200,000 (1,200,000) -

8,652,400 (1,154,589) 7,497,811

1,779,115$ (849,852)$ 929,263$

19,208,562 3,691,228 22,899,790

20,987,677$ 2,841,376$ 23,829,053$

Net (Expense) Revenue and Changes in Net AssetsPrimary Government

18

CITY OF PORT ARANSAS, TEXASBALANCE SHEETGOVERNMENTAL FUNDSSeptember 30, 2007

BeachGeneral Airport Advertising Cleaning

ASSETSCash and Temporary Investments $ 2,387,600 $ (7,542) $ 125,897 $ 733,150 Receivables - Net of Allowances:

Accounts 68,474 485 - - Governmental Units 191,478 33,193 - 48,552 Ad Valorem Taxes - Net 76,281 - - - Other 7,611 - - -

Prepaid Expenses - - - -

Total Assets $ 2,731,444 $ 26,136 $ 125,897 $ 781,702

LIABILITIESAccounts Payable $ 126,035 $ 737 $ - $ - Accrued Liabilities 37,553 - - - Matured Bonds & Interst Payable - - - - Customer Deposits 126,511 - - - Deferred Revenues 76,281 - - -

Total Liabilities 366,380 737 - -

FUND BALANCESReserved For:

Approved Projects - - - - Unreserved:

Designated For Harbor 205,345 - - - Designated For Gas Utility 294,716 - - - Designated For Specific Projects - - - Undesignated 1,865,003 25,399 125,897 781,702

Total Fund Equity 2,365,065 25,399 125,897 781,702

Total Liabilities And Fund Equity $ 2,731,444 $ 26,136 $ 125,897 $ 781,702

The accompanying notes are an integral part of this statement.

19

Port AransasRecreational Streets Total

Recreational Development Nature & Land GovernmentalDevelopment Corporation Library Preserve Acquisition Funds

$ 604,221 $ 172,767 $ 79,054 $ 1,811,457 $ 6,289,647 $ 12,196,250

- - - - - 68,960 - 43,208 - - - 316,430 - - - - - 76,281

111 - - - - 7,723 - - - - - -

$ 604,332 $ 215,975 $ 79,054 $ 1,811,457 $ 6,289,647 $ 12,665,643

$ 14 $ 7,838 $ - $ - $ 441,771 $ 576,394 - 2,065 - - - 39,618

157,844 - - - - 157,844 - - - - - 126,511 - - - - - 76,281

157,858 9,903 - - 441,771 976,648

- - - - 1,679,677 1,679,677

- - - - - 205,345 - - - - - 294,716 - - - 1,811,457 - 1,811,457

446,474 206,072 79,054 - 4,168,199 7,697,800

446,474 206,072 79,054 1,811,457 5,847,876 11,688,995

$ 604,332 $ 215,975 $ 79,054 $ 1,811,457 $ 6,289,647 $ 12,665,643

20

CITY OF PORT ARANSAS, TEXASSTATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCEGOVERNMENTAL FUNDSFor The Year Ended September 30, 2007

BeachGeneral Airport Advertising Cleaning

REVENUES:Taxes $ 4,233,912 $ - $ 924,680 $ 616,453 Licenses and Permits 421,183 - - 418,245 Intergovernmental 393,686 33,193 - 97,104 Charges For Services 2,580,704 85,808 - - Fines and Penalties 232,993 - - - Rentals 500,908 - - - Interest Income 217,378 1,593 10,148 28,359 Other 56,539 - - -

Total Revenues 8,637,304 120,594 934,827 1,160,161EXPENDITURES:Current:

Central Operating 822,619 - - - Mayor and Council 176,911 - 968,830 - CityCourt 72,942 - - - CityAttorney 78,286 - - - CityManager 229,991 - - - CitySecretary 175,949 - - - Finance 154,403 - - - Parks and Recreation 405,021 125,211 - 938,891 Police 1,244,202 - - - Fire 117,169 - - - Emergency Medical Services 428,496 - - - Public Works 960,837 - - - Building Codes & Planning 296,068 - - - Library 185,182 - - - Public Buildings 370,368 - - - Harbor 270,677 - - - Public Transportation 151,782 - - - Gas Utility & Sanitation 1,403,591 - - -

Capital Projects - - - - Debt Service 67,388 - - -

Total Expenditures 7,611,883 125,211 968,830 938,891 Excess of Revenues

Over (Under) Expenditures 1,025,421 (4,617) (34,003) 221,270

OTHER FINANCING SOURCES (USES):Proceeds From Sale of Bonds - - - - Transfers From (To) Other Funds (1,846,834) - - -

Fund Balances - October 1 3,186,478 30,016 159,900 560,432

Fund Balances - September 30 $ 2,365,065 $ 25,399 $ 125,897 $ 781,702 The accompanying notes are an integral part of this statement.

21

Port AransasRecreational Streets Total

Recreational Development Nature & Land GovernmentalDevelopment Corporation Library Preserve Acquisition Funds

$ 616,453 $ 420,659 $ - $ - $ - $ 6,812,157 - - - - - 839,429 - - - - 250,000 773,984 - - - - - 2,666,513 - - - - - 232,993 - - - - - 500,908

62,099 10,135 2,701 91,779 150,997 575,188 - - 8,091 - - 64,630

678,552 430,794 10,792 91,779 400,997 12,465,801$

- - - - - 822,619 - - - - - 1,145,741 - - - - - 72,942 - - - - - 78,286 - - - - - 229,991 - - - - - 175,949 - - - - - 154,403 - 492,081 - - - 1,961,205 - - - - - 1,244,202 - - - - - 117,169 - - - - - 428,496 - - - - - 960,837 - - - - - 296,068 - - 1,417 - - 186,598

49,884 - - - - 420,252 - - - - - 270,677 - - - - - 151,782 - - - - - 1,403,591 - - - 53,455 1,177,888 1,231,342

191,088 - - - 47,000 305,475 240,971 492,081 1,417 53,455 1,224,888 11,657,627

437,580 (61,287) 9,376 38,325 (823,891) 808,174

- - - - 2,685,000 2,685,000 (1,249,656) - - - 3,096,490 - 1,258,549 267,359 69,678 1,773,132 890,277 8,195,821

$ 446,474 $ 206,072 $ 79,054 $ 1,811,457 $ 5,847,876 $ 11,688,995

22

CITY OF PORT ARANSAS, TEXASRECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEETTO THE STATEMENT OF NET ASSETSSeptember 30, 2007

Total Fund Balance - Governmental Funds 11,688,995$

Amounts reported in the governmental activities in the statement of net assets are different because:

1 - Capital assets used in governmental activities are not current financial resources and therefore are not reported in the governmental funds. The cost of the assets is $28,494,935 and the accumulated depreciation is $11,719,827 16,775,108

2 - Other long-term assets, including delinquent taxes receivable, net of allowance are not available for current period expenditures and are, therefore, deferred in the funds. 76,281

3 - Some liabilities are not due and payable in the current period and therefore are not reported in funds. A detail of these liabilities follows:

Compensated absences (118,593)$ Capitalized lease obligations (159,454) General Obligation Bonds (2,685,000) Certificates of obligation (1,785,000) (4,748,048)

4 - Various other reclassifications and eliminations are necessary to convert from the modified accrual of accounting to the accrual basis of accounting. These include recording bond issue cost net of amortization of $84,454 as an asset and accrued interest of $65,485 as a liability. The net effect of these reclassifications and recognitions is to increase (decrease) net assets. 18,969

Net Assets of Governmental Activities 23,829,053$

23

CITY OF PORT ARANSAS, TEXASRECONCILIATION OF THE GOVERNMENTAL FUNDS STATEMENT OF REVENUES, EXPENDITURESAND CHANGES IN FUND BALANCE TO THE STATEMENT OF ACTIVITIESFor The Year Ended September 30, 2007

Change in Fund Balance - Governmental Funds 3,493,174$

Amounts reported in the governmental activities in the statement of activities are different because:

1 - Governmental funds report capital outlays as expenditures. However, in the statement of activities the cost of capital assets is allocated over their estimated useful lives and reported as depreciation expense. Capital outlays and depreciation expense for the current period are as follows:

Capital outlays 1,089,242$ Depreciation expense (1,141,602) (52,360)

2 - Revenues in the statement of activities that do not provided current financial resources are not reported as revenues in funds. Adjustment necessary to report property tax revenues on the accrual basis. 7,306

3 - Debt proceeds provide current financial resources to governmental funds, but issuing debt increases long-term liabilities in the statement of net assets. Repayment of debt principal is an expenditure in the governmental funds, but the repayment reduces long-term liabilities in the statement of net assets. This is the amount by which proceeds exceeded repayment.

Compensated absences (253)$ Capitalized lease obligations 55,721 General Obligation Bonds Issued (2,685,000) Certificates of obligation paid 125,000 (2,504,532)

4 - Various other reclassifications and eliminations are necessary to convert from the modified accrual of accounting to the accrual basis of accounting. These include reclassifying bond issue costs, recording amortization of bond issue cost, writing off net book value of assest sold or disposed and adjusting accrued interest on long-term debt. The net effect of these reclassifications and recognitions is to increase (decrease) net assets.

Amortization of bond issue costs (4,309)$ Bond issue costs 47,000 Decrease (Increase) - Accrued interest on long-termdebt (57,017)

(14,326)

Change in Net Assets of Governmental Activities 929,263$

24

CITY OF PORT ARANSAS, TEXASNOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED SEPTEMBER 30, 2007

A. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES: The City of Port Aransas, Texas (the "City") was incorporated as a general law city in November 1955. In August 1978 the City adopted the Mayor-Council-Manager form of government. The principal services accounted for as general governmental functions include public safety, health, streets, sanitation, park and recreation, planning, zoning and general administrative services. The financial statements of the City have been prepared in accordance with accounting principles generally accepted in the United States of America (GAAP) as applied to governmental units. The Governmental Accounting Standards Board (GASB) is the standard setting body for governmental accounting and financial reporting. The GASB periodically updates its codification of the existing Governmental Accounting and Financial Reporting Standards, which along with subsequent GASB pronouncements (Statements and Interpretations), constitutes GAAP for governmental units.The more significant accounting principles and practices are discussed in subsequent sections of these Notes.

REPORTING ENTITY:The financial statements of the reporting entity include those of the City (the primary government) and its component units, entities for which the City is considered financially accountable. In evaluating how to define the City, for financial reporting purposes, management has considered all potential component units. The City is financially accountable if it appoints a voting majority of the organization’s governing board and it is able to impose its will on the organization, or there is a potential for the organization to provide specific financial benefits to or burdens on the City. Additionally, the City is required to consider other organizations for which the nature and significance of their relationship with the City are such that exclusion would cause the City’s financial statements to be misleading or incomplete. Blended component units, although legally separate entities are, in substance, part of the City operations and so data from these units are combined with data of the City. If applicable, each discretely presented component unit is reported in a separate column in the government-wide financial statements to emphasize it is legally separate from the City.

Blended Component Units:The Port Aransas Recreational Development Corporation (PARDC) was chartered on November 27, 1995. The public purposes for which the Corporation is organized and for which it may issue bonds are as follows: construction, development, expansion, maintenance, operation and promotion of recreational and sports fields and stadiums, swimming pool, sports complexes, and related facilities and improvements. The Board of Directors consisting of seven members is appointed by the City Council. PARDC's main source of revenue is the additional one-half cent sales tax approved by voters.Discretely Presented Component Units - There are no component units requiring discrete presentation.

Related Organizations and Jointly Governed Organizations that are administered by separate boards or commissions provide services within the City. However, the City is not financially accountable for these organizations. Therefore, they are not component units of the City, even if the City Council could appoint a voting majority of the organizations' board. Consequently, financial information for the Coastal Bend Council of Governments, the Regional Transit Authority and the Port Aransas Chamber of Commerce are not included in these financial statements.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED…

25

The PARDC is audited in conjunction with the audit of the City’s general-purpose financial statements. PARDC does not issue separate stand-alone financial statements.

Basic Financial Statements:The basic financial statements include both government-wide (based on the City as a whole) and fund financial statements. While the previous model emphasized fund types (the total of all funds of a particular type), in the new reporting model the focus is on either the City as a whole or major individual funds (within the fund financial statements). Both the government-wide and fund financial statements categorize activities as either governmental activities or business-type activities. In the government-wide statement of net assets, both the governmental and business-type activities columns are presented on a consolidated basis by column and reflected on a full accrual, economic resource basis, which incorporates long-term assets and receivables as well as long-term debt and obligations.The government-wide statement of activities reflects both the gross and net cost per functional category (police, fire, operations, etc.) which are otherwise being supported by general government revenues (e.g., property taxes, sales taxes and certain intergovernmental revenues). The statement of activities reduces gross expenses, including depreciation, by related program revenues, operating and capital grants. The program revenues must be directly associated with the function or a business-type activity. Program revenues include revenues form charges for services, franchise fees, fines and penalties, licenses and permit fees and service assessments. The operating grants include operating-specific and discretionary (either operating or capital) grants while the capital grants column reflects capital-specific grants.

The net costs (by government or business-type activity) are normally covered by general revenue. Historically, the previous model did not summarize or present net cost by function or activity. This government-wide presentation focuses more on the substantiality of the City as an entity and the changes in aggregate financial position resulting from the activities of the fiscal period.

The fund financial statements are similar to the financial statements presented in the previous model. Emphasis here is on the major funds in either the governmental or business type categories. Non-major funds (by category) or fund type are summarized into a single column.The governmental funds major fund statements in the fund financial statements are presented on a current financial resource and modified accrual basis of accounting. This is the manner in which these funds are normally budgeted. This presentation demonstrates: legal and covenant compliance, source and use of liquid resources and how the City’s actual experience conforms to the budget or fiscal plan. Since the governmental fund statements are presented on a different measurement focus and basis of accounting than the government-wide statements, reconciliations are presented following the statementsthat briefly explain the adjustments necessary to transform the fund based financial statements into the government-wide statements.

Basis of Presentation:The City’s financial transactions are recorded in individual funds, each of which is considered a separate accounting entity. The operations of each fund are accounted for with a separate set of self-balancing accounts that comprise its assets, liabilities, fund equity, revenues and expenditures. Resources are allocated to and accounted for in individual funds based upon the purposes for which they are to be spent and the means by which spending activities are controlled. GASB 34 establishes criteria(percentage of the assets, liabilities, revenues or expenditures/expenses of either fund category or the governmental and enterprise combined) for the determination of major funds. The nonmajor funds can be combined in a single column in the fund financial statements. However, management determined that reporting all funds in the basis financial statements as if they were major funds would provide a more simple and meaningful presentation. Actual major funds, as defined by GASB 34, for the year ended

NOTES TO THE FINANCIAL STATEMENTS CONTINUED…

26

September 30, 2007 are as follows: General Fund (always a major fund), Recreational Development Fund, Nature Preserve Capital Project Fund and the Streets & Land Acquisition Capital Projects Fund. Funds not meeting the definition but reported as major funds on the balance sheet and statements of revenues, expenditures and changes in fund balance include: Municipal Airport Fund, Advertising Fund, Beach Fund, Port Aransas Recreational Development Corporation and the Library Fund.

The General Fund (GF) accounts for all financial resources except those required to be accounted for in another fund. The Advertising Fund accounts for the portion of Occupancy taxes that are required to be spent for advertising and promoting the City. The Beach Fundaccounts for the portion of Occupancy taxes required to provide beach cleaning and safety. The Recreational Development Fund accounts for the portion of Occupancy taxes that the Council requires to be set aside for recreational development. The Nature Preserve Capital Projects Fund was established to account for the proceeds of the Certificates of Obligation that were issued during the year ended September 30, 2004. Certificates of Obligation will be used to provide a nature preserve. The Streets and Land Acquisition Fund accounts for bond proceeds, grants from other governmental agencies and transfers from the General Fund that are used for streets, miscellaneous projects and land acquisitions other than for the nature preserve.

GASB 34 eliminates the presentation of account groups, but provides for these records to be maintained and incorporates the information into the Governmental column in the government-wide statement of net assets.

Basis of Accounting: Basis of accounting refers to the point at which revenues or expenditures/expenses are recognized in the accounts and reported in the financial statements. It relates to the timing of the measurements made, regardless of the measurement focus applied. The government-wide statements are presented on accrual basis of accounting. The governmental funds in the fund financial statements are presented on a modified accrual basis. Accrual means that revenues are recognized when earned and expenditures/expense are recognized when incurred. All governmental funds use the modified accrualbasis of accounting. Under this basis of accounting, revenues are recognized when susceptible to accrual (i.e., when they become both measurable and available). "Measurable" means the amount of the transaction can be determined and "available" means collectible within the current period or soon enough thereafter to be used to pay liabilities of the current period. The City considers property taxes and franchise taxes as available if they are collected within 60 days after year-end. A one-year availability period is used for revenue recognition for all other governmental fund revenues. Expenditures are recorded when the related fund liability is incurred. Principal and interest on general long-term debt are recorded as fund liabilities when due or when amounts have been accumulated in therequired fund for payments to be made early in the following year.

Revenues susceptible to accrual are property taxes, franchise taxes, grants earned, interest revenue, harbor rentals and charges for sanitation and gas utility services. Receivable amounts are reported net of allowances for uncollectibles where appropriate. As of September 30, 2007, the City recorded allowances of $23,000 for utilities and $19,070 for ad valorem taxes in the General Fund. No other allowances are considered necessary. Sales taxes collected and held by the state at year-end on behalf of the City also are recognized as revenue. Occupancy taxes, fines, permits, and miscellaneous revenues are not susceptible to accrual because generally they are not measurable until received in cash.In applying the “susceptible to accrual” concept to intergovernmental revenues pursuant to GASB No. 33 “Accounting and Financial Reporting for Nonexchange Transactions”, the revenue provider recognizes liabilities and expenses and the revenue recipient recognizes receivables and revenue when

NOTES TO THE FINANCIAL STATEMENTS CONTINUED…

27

the applicable eligibility requirements, including time requirements, are met. Resources transmitted before the eligibility requirements are met are reported as advances by the provider and as deferred revenue by the recipient/Encumbrances are supported by purchase orders or contracts and represent commitments related to unperformed contracts for goods or services. Under Texas law, appropriations lapse at year-end and encumbrances outstanding at that time are to be canceled or appropriately provided for in the subsequent year’s budget. The only significant encumbrances outstanding at September 30, 2007 totaled $1,679.677 for contracts in process for the 2007 street and drainage program.

Cash and cash equivalents of all City funds, except for the Library and Seized Drug money, are pooled and each fund has equity in the pooled amount. Cash and cash equivalents include currency on hand, demand deposits with banks, amounts included in pooled cash and liquid investments with a maturity of three months or less when purchased. City funds are deposited and invested under the terms of a depository contract. The depository bank deposits for safekeeping and trust with a third-party bankapproved pledged securities as authorized by Chapter 2257 Collateral for Public Funds of the Government Code in an amount sufficient to protect City funds on a day-to-day basis during the period of the contract. The pledge of such securities is waived only to the extent of the depository bank's dollar amount of Federal Deposit Insurance Corporation ("FDIC") Insurance. Texas statutes authorize the City to invest in 1) obligations of the U.S. Treasury or its agencies and instrumentalities; 2) direct obligations of the State of Texas or its agencies; 3) other obligations, the principal of and interest on which are unconditionally guaranteed or insured by the State of Texas or the United States; 4) obligations of states, agencies, counties or cities rated A or better by a national investment rating firm; 5) certificates of deposit that are insured by the Federal Deposit Insurance Corporation or secured by obligations having a market value of at least the principal amount of the certificates; and 6) fully collateralized direct repurchase agreements. The City’s investments are stated at fair value, which is determined using selected bases. Short-term investments are reported at cost, which approximates fair value. Securities traded on a national or international exchange are valued at the last reported sales price at current exchange rates. Cash deposits are reported at carrying amount, which reasonably estimates fair value. The net change in fair value of investments is recognized and reported as investment income in the financial statements. Accrued interest, if material, is shown under the caption accrued interest receivable. Other wise it is included with the value of the investment. Additional cash and investment information and fair values are presented in Note C. Interest earned on pooled cash is allocated to each fund based on the funds’ participation in that investment. Aside from accounts clearly identified as belonging to a specific fund, any unrealized gain/loss resulting from the valuation is allocated to each fund based on the fund’s participation in that investment.

Receivables and Payables – Amounts reported as interfund receivables and payables are eliminated in the government-wide statement of net assets. All trade and property tax receivables are shown net of an allowance for uncollectibles. Trade accounts receivable in excess of 120 days comprise the trade accounts receivable allowance for uncollectibles. The property tax receivable allowance is equal to 20% of outstanding property taxes at the end of the fiscal year. Utility revenue is recorded when billed at the end of the month. The estimated value of services provided but unbilled is not considered significant because meters are read near the end of the month. As such, no unbilled services are included in the accompanying financial statements. Net property tax receivable of $76,281 is fully deferred at year-end because delinquent collections received within the following sixty days are not considered significant. Inventories are not considered significant and are not reported in the accompanying financial statements. As a result, costs of inventories are recorded as expenditures when purchased.Capital Assets - All capital assets, including public domain ("infrastructure") general fixed assets, purchased or constructed are valued at historical cost or estimated historical cost if actual historical cost

NOTES TO THE FINANCIAL STATEMENTS CONTINUED…

28

is not available. Donated assets are valued at their estimated market value on the date donated. Maintenance repairs and renewals, which neither materially add to the value of the property nor appreciably prolong its life, are charged to expense as incurred. Leases that meet the criteria of a capital lease, as defined by Statement of Financial Accounting Standards No. 13, are capitalized. Depreciation on capital assets is calculated on the straight-line basis over the following estimated useful lives: Gas pipelines – 50 years; Infrastructure - 30 to 50 years, Runways and related improvements - 15 to 20 years; Buildings - 30 to 40 years; Improvements other than buildings 10 to 20 years; Vehicles – 5 years; Machinery and equipment - 5 to 15 years and Office furniture – 7 years. Interest is capitalized on assets, other than infrastructure assets, acquired with tax-exempt debt. The amount of interest capitalized is the net interest expense incurred (interest expense less interest income) from the date of the borrowing until completion of the project. Restricted Assets – When an expense is incurred for purposes for which both restricted and unrestricted net assets are available, it is the city’s policy to apply restricted net assets first.Accumulated Unpaid Compensated Absences - The City allows employees to accumulate up to a maximum of 130 days of unused sick leave. However sick days do not vest, and accordingly, employees can be paid sick leave only when sick. Since an employee's right to receive compensation for future absences is contingent upon the absences being caused by future illnesses and since amounts cannot be reasonably estimated, a liability for unused sick leave is not recorded in the financial statements. Earned vacation time generally must be used within one year of accrual. Up to 10 days of accumulated earned vacation will be paid to an employee upon termination. Accumulated unpaid vacation pay is reported in the government-wide statement of net assets. Expenditures are recorded in the governmental funds as employees resign or retire. The amount expected to be paid from current resources is not considered to be significant. Long-Term Obligations – In the government-wide financial statements, long-term debt and other long-term obligations are reported as liabilities in the applicable governmental activities and business-type activities. Bond premiums and discounts, as well as issuance costs, are deferred and amortized over the life of the bonds using the effective interest method. Bonds payable are reported net of the applicable bond premium or discount. Bond issuance costs incurred on the issuance of the Certificates of Obligation are reported as assets, net of amortization on the Statement of Net Assets. In the fund financial statements, governmental funds recognize bond premiums and discounts, as well as bond issuance costs, during the current period. The face amount of debt issued is reported as other financing sources. Premiums received on debt issuances are reported as other financing sources while discounts on debt issuances are reported as other financing uses. Issuance costs, whether or not withheld from the actual debt proceeds received, are reported as debt service expenditures in the governmental funds, bond discounts and issuance costs are treated as period costs in the year issued. Interfund Transactions - During the course of normal operations, the City has numerous transactions between funds including expenditures and transfers of resources to provide services. The accompanying fund financial statements generally reflect such transactions as operating transfers, which are included in the results of operations of the individual funds. Nonrecurring transfers of equity between funds are treated as residual equity transfers and are reported as additions or deductions to the fund balance of the individual funds. The General Fund charges the Beach Fund for vehicles and equipment used to provide beach safety, police patrols and cleaning. The General Fund also charges other funds for services as provided. Since these charges are considered "Quasi External" transactions, they are recorded as revenues by the General Fund and expenditures by the other funds. During the year ended September 30, 2007 the General Fund charged the Beach Fund $938,891. Charges in excess of a fund’s available resources are not recorded as due from that fund because it can not be determined if that fund will receive sufficient resources to enable repayment of the excess amounts. If sufficient funds become

NOTES TO THE FINANCIAL STATEMENTS CONTINUED…

29

available in future years, a reimbursement may be made. In years prior to 2007, charges to the Beach Fund exceeded the resources in that fund by $32,584. Reimbursements have not been made to the General Fund for these prior year charges. The “Quasi External” transactions are eliminated for the government-wide statements.

Fund Equity - In the fund financial statements, governmental funds report reservations of fund balance for amounts that are not available for appropriation or are legally restricted by outside parties for use for a specific purpose. Designations represent tentative management plans that are subject to change.Use of Estimates – The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect certainreported amounts and disclosures. Accordingly, actual results could differ from those estimates.

B. BUDGETS AND BUDGETARY ACCOUNTING:The City Charter requires adoption of an annual budget. This budget is prepared in accordance with the basis of accounting utilized by the various funds. The Capital Projects Funds adopt project-length budgets. The City Manager is authorized to transfer budgeted amounts within departments; however, any revisions that alter the total expenditures of a department must be approved by the City Council. The following procedures are used by the City in establishing the budgetary data reflected in the financial statements: 1) Prior to October 1, the beginning of the fiscal year, the City Manager submits a proposed budget to the City Council. This budget includes proposed expenditures and the means of financing them; 2) Advertised public hearings are conducted; 3) Budget and tax levy are enacted through the passage of ordinances; 4) Budget is amended as considered necessary. Both original and amended budgets for the General and major Special Revenue Funds are presented in the required supplementary information following these notes. All unencumbered budget appropriations except project budgets, lapse at the end of each fiscal year.

C. Cash and Temporary Investments:Cash in Depository Banks - At September 30, 2007, the carrying amount of the City's deposits at its depository banks totaled $64,294 at American bank, $91,987 at Value bank and $21,084 at Herndon, Plant, Oakley LTD and the banks’ balances totaled $173,482, $91,987 and $21,084, respectively. All deposits were entirely covered by FDIC insurance and by pledged collateral held by a third party bank in the City's name. The City's cash deposits during the year ended September 30, 2007 were entirely covered by FDIC insurance and by pledged collateral held by the City's agent bank in the City's name.Custodial credit risk is the risk that in the event of a bank failure, the City’s deposits may not be returned or the City may not be able to recover collateral securities in the possession of an outside party. The City’s policy requires all invested funds to be fully collateralized or insured consistent with federal and state law and the current bank depository contract. Also, all securities pledged as collateral shall be deposited in trust with the Federal Reserve Bank or an independent investment institution under an appropriate legal contract. The amount of securities pledged shall be determined by their market value.

Temporary Investments - The City maintains accounts at TexPool, which is duly chartered and administrated by the State Treasurer's Office and its portfolio consists of U.S. Treasury bills and notes, collateralized certificates of deposit and repurchase agreements. The objective of TexPool is to maintain a stable $1.00 price of the fund. All securities owned by TexPool are marked to market daily and if the ratio of the market value of the portfolio divided by its book value is less than 0.995 or greater than 1.005, TexPool will sell portfolio holdings as required to maintain the ratio between 0.995 and 1.005. However, the $1.00 price is not guaranteed or insured by the State of Texas or the Treasury. Accounts at Herndon Plant Oakley are used to invest primarily in securities of the U.S. or its agencies.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED…

30

Investments - Credit risk is the risk that an issuer or other counterparty to an investment will not fulfill its obligations. Investments that are represented by specific identifiable investment securities are classified as to credit risk by three categories described as follows: 1) insured or registered, or securities held by the City or its agent in the City's name; 2) uninsured and unregistered, with securities held by the counterparty's trust department or agent in the City's name; 3) uninsured and unregistered, with securities held by the counterparty, or by its trust department or agent but not in the City's name. Investments held in mutual funds are not assigned risk categories since the City has not been issued securities, but rather owns an undivided beneficial interest in the investments. All of the City’s investments, other than investments in mutual funds, are in category 1. During the year ended September 30, 2005, the City changed its investment strategy from investing solely in TexPool to investing in a variety of temporary investments such as US Treasuries, quasi governmental agencies, mutual funds, certificates of deposits and money market accounts. During the year ended September 30, 2007, the City changed its investment strategy back to investing primarily at TexPool. The City reports certain investments at fair value in the balance sheet and recognizes the corresponding change in the fair value of investments in the year in which the change occurred. Fair value fluctuates with interest rates and increasing rates could cause fair value to decline below original cost. Fair values of the City’s investments are equal to their respective carrying amounts. City management believes the liquidity of the portfolio is more than adequate to meet cash flow requirements and to preclude the City from having to sell investments below original cost for that purpose. Interest rate risk is the risk that changes in interest rates will adversely affect the fair value of an investment. Investments held for longer periods are subject to increased risk of adverse interest rate changes. The City’s investment policy provides the guideline that maturity of securities should not exceed more than five years and that pooled funds’ average dollar-weighted maturity allowed based on the stated maturity date for the portfolio is one year. Investments are diversified to minimize the risk of loss resulting from over-concentrations of assets in a specific maturity period. The net increase (decrease) in the fair value of investments held during the year ended September 30, 2007 was $23,786. This amount takes into account all changes in fair value, including purchases and sales that occurred during the year. The City has no unrealized loss at September 30, 2007. Investments and temporary investments held by the City at September 30, 2007 are as follows:

CarryingAmounts

Tempora ry Inv estments - Substantia lly al l mature within 1 year:Investments in U. S. Agencies -$

Tempora ry Inv estments not catego rized (Mutual Funds)Thornburg LTD Term US Govt-A - TexPo ol 12,017,062

Total Temp orary Inv estments not categorized (Mutual Funds) 12,017,062

Certificates of Deposits and Money Ma rket AccountsMM - Tamarack Inv es tment Funds 21,084 Certi ficates of Depos it - ValueBank 64,618

To tal Cert ificates o f D ep osit and Money Market Acco unts 85,702

Tota l Inv estments, Mutual Funds, Certificatesof D epost a nd Money Market Accounts 12,102,764$

D. Property Taxes:Property Taxes attach as an enforceable lien on property as of January 1. Property taxes are levied on October 1 based on 100% of appraised value of property as determined on the previous January 1. Appraised values are determined by the Nueces County Appraisal District; approved by the Nueces

NOTES TO THE FINANCIAL STATEMENTS CONTINUED…

31