annexure vii research report - colombo stock exchange · research report as at 23rd ... of mcrp in...

TRANSCRIPT

ANNEXURE VII – Research Report

1

Melstacorp Limited

Research Report As at 23rd September 2016

Prepared By:

CT CLSA Capital (Pvt) Ltd

A CT Holdings Group and CLSA Group Company The preparer of the research report possesses the requisite expertise to prepare research report to determine business

valuations of this nature involving a company quoted under Consumer Staples Sector

2

LIST OF ABBREVIATIONS

BBH BN BPL CIL CSE CTC DCF DIST EBITDA EV Ke LBL LION LKR LTE Ltr MADU

: : : : : : : : : : : : : : : : :

Browns Beach Hotel PLC Billion Balangoda Plantations PLC Continental Insurance Lanka Limited Colombo Stock Exchange Ceylon Tobacco Company PLC Discounted Cash Flow Distilleries Company of Sri Lanka PLC Earnings before Interest, Tax, Depreciation and Amortization Enterprise Value Cost of Equity Lanka Bell Limited Lion Brewery Ceylon PLC Sri Lankan Rupees Long Term Evolution Liters Madulsima Plantations PLC

MCRP MERF MHL NATA NBT NSA PCEYL PBT PBV PER PPE PSIP ROE SLIC SOTP

: : : : : : : : : : : : : :

Melstacorp Limited Melsta Regal Finance Limited Milford Holdings (Pvt) Limited National Authority on Tobacco and Alcohol Nation Building Tax National Sales Average Periceyl (Pvt) Ltd Profit Before Tax Price to Book Value Price to Earnings Property, Plant and Equipment Pelwatte Sugar Industries PLC Group Return on Equity Sri Lanka Insurance Corporation Sum of the Parts

SPEN VAT VWASP YoY

: : : :

Aitken Spence PLC Value Added Tax Volume Weighted Average Share Price Year over Year

3

TABLE OF CONTENTS

Table of Contents OBJECTIVE OF THE REPORT ........................................................................................................................... 4

1.0 THE COMPANY: MELSTACORP LIMITED................................................................................................ 5

1.1 Overview ................................................................................................................................ 5

1.2 Objective of the Restructure .................................................................................................. 5

1.3 Restructure: Sequence of Events ........................................................................................... 5

1.4 Group Structure Post-Restructure1 ........................................................................................ 6

1.5 MCRP: Group Operations ....................................................................................................... 7

2.0 DIST GROUP: HISTORICAL ANALYSIS OF POST-RESTRUCTURE MCRP GROUP FINANCIALS .................. 8

2.1 Income Statement Analysis .................................................................................................... 9

2.2 DIST Group: Quarterly Financial Analysis of Post-Restructure MCRP Group Financials ...... 15

2.3 Melstacorp Group (Prior to Restructure): Financial Analysis............................................... 16

3.0 BUSINESS SEGMENTS .......................................................................................................................... 17

3.1 Beverage Sector ................................................................................................................... 17

3.2 Plantation Sector .................................................................................................................. 20

3.3 Telecommunication Sector .................................................................................................. 23

3.4 Financial Services Sector ...................................................................................................... 25

3.5 Diversified Sector ................................................................................................................. 26

3.6 MCRP: Diversified Sector Analysis ....................................................................................... 28

3.7 Other Key Events .................................................................................................................. 30

4.0 MCRP GROUP: FORECASTS AND OUTLOOK POST-RESTRUCTURE ...................................................... 31

5.0 VALUATION ......................................................................................................................................... 40

5.1 Relative Price to Earnings Method (PE) ............................................................................... 41

5.2 Market Price Method (Sub Division of Shares) .................................................................... 42

5.3 Relative Price to Book Value Method (PBV) ........................................................................ 43

5.4 Sum of the Parts Method (SOTP) ......................................................................................... 44

6.0 RESEARCH TEAM - CT CLSA CAPITAL (PVT) LTD .................................................................................. 49

APPENDIX .................................................................................................................................................... 50

4

OBJECTIVE OF THE REPORT

The Distilleries Company of Sri Lanka PLC (DIST) made an announcement on 01st August 2016 of an Arrangement in

terms of Section X of the Companies Act No. 7 of 2007 to restructure the Group, making Melstacorp Limited (MCRP),

which is currently a 100% subsidiary of DIST, the parent company of the DIST Group. As such, DIST shares would be

suspended from trading from 30th September 2016. Shareholders of DIST Group as at 30th September 2016 will be

issued 1,200 Mn shares in MCRP in a ratio of 4:1 (4 shares of MCRP for each share in DIST) and 100% ownership of

DIST will be transferred to MCRP. Subsequently, it is proposed for MCRP to list 1,165 Mn shares on the Colombo

Stock Exchange (CSE) via an introduction. In this regard, the objective of this research report is to derive a Reference

Price for the introduction of MCRP in terms of Section 3.4.8 of the Listing Rules of the CSE.

5

1.0 THE COMPANY: MELSTACORP LIMITED

1.1 Overview

Melstacorp Limited (MCRP) is a diversified conglomerate domiciled in Sri Lanka with its business interests spanning

Beverage, Plantations, Telecommunication, Financial Services and Other Diversified Sectors. The Distilleries

Company of Sri Lanka PLC (DIST Alcohol Company), market leader in the hard alcohol segment in the country,

Balangoda Plantations PLC (BPL) and Browns Beach Hotel PLC (BBH) are subsidiaries of the MCRP Group, and are all

listed on the Colombo Stock Exchange (CSE). Furthermore, CSE listed conglomerate Aitken Spence PLC (SPEN) and

Madulsima Plantations PLC (MADU) are associate companies of MCRP. The Group employs a staff cadre of

approximately 12,700.

1.2 Objective of the Restructure

The Distilleries Company of Sri Lanka PLC (DIST Group) commenced operations as a distiller, manufacturer and

distributor of liquor products. Although it diversified its operations across a range of sectors over the years and as

such has changed its nature of business, the name of the holding company remained unchanged. With the

introduction of National Authority on Tobacco and Alcohol Act No. 27 of 2006 (NATA), using DIST as a corporate

brand name was made illegal. Branding for the Group came at a significant cost due to the need to market each

brand name independently. As a result, the DIST Group has decided to rebrand the Group under a common brand,

namely ‘MELSTA’. Furthermore, management believes that through the restructure, there would be a value

unlocking for DIST Company as a stand-alone listed entity by offering more visibility to the legacy beverage business.

1.3 Restructure: Sequence of Events

As part of the restructure process, Melstacorp Limited (MCRP), which is a fully owned subsidiary of DIST Group, will

become the ultimate parent of the Group through an Arrangement as per Part X of the Companies Act No. 7 of 2007.

As a result, DIST Alcohol Company would become a subsidiary of MCRP focusing purely on the legacy beverage

business.

The sequence of events for the Arrangement is as follows:

MCRP settling a sum of LKR 1,816,079,400 owing to DIST (out of an intercompany balance of

LKR 1,816,079,570) through the issue of 10,089,330 shares of MCRP to DIST at an issue price of LKR 180 per

share, representing the book value of MRCP at the time, which the Board of MCRP perceives is fair and

reasonable to MCRP and its sole shareholder, DIST

MCRP to issue 138,128,726 shares to DIST at an issue price of LKR 180 per share for a total consideration of

LKR 24,863,170,680. DIST to issue Promissory Notes to MCRP for the total consideration (Promissory Notes

will carry interest rate at the six months AWPLR of Licensed Commercial Banks of Sri Lanka plus 100bps)

Prior to the above, DIST held 265,450,000 shares in MCRP and post the issue of 148,218,056 shares

mentioned above, DIST would own a total of 413,668,056 shares of MCRP. These shares were consolidated

into 1,000 ordinary shares

6

100% ownership of DIST Company1 to be transferred to MCRP with shareholders of DIST as at 30th

September 2016 being issued shares in MCRP in the ratio of 04 shares of MCRP for every 01 share held in

DIST at a value of LKR 11.75 per share. On 30th September 2016, a total of 1.2 Bn shares of MCRP to be

issued for a total consideration of LKR 14.1 Bn for 300 Mn shares in DIST subsequent to which DIST would

be suspended from trading on CSE

The consolidated 1,000 ordinary shares are converted to 1,000 ordinary non-voting shares

Dissolve the Melstacorp Limited Employees Share Trust and repurchase the MCRP shares to be allotted to

the Trust through the settlement of a loan outstanding from the Trust to MCRP of LKR 1,392,132,049 as at

31st March 2016

Post-acquisition of DIST, MCRP Group would adopt a Common Control Accounting Policy for the said

Business Combination. Hence, goodwill on acquisition will not be recognized in MCRP consolidated financial

statements

MCRP to be the ultimate holding company, with a 100% stake in subsidiary DIST List MCRP on the Colombo Stock Exchange (CSE) through an Introduction of maximum of 1,165,397,072

shares at a price of LKR 69.0

DIST to recommence trading after meeting free float criteria as per the CSE (MCRP shareholders to receive

preferential allotment)

1.4 Group Structure Post-Restructure1

1 162,164 shares of DIST held by sixty four (64) deceased shareholders and three (3) shareholders who continued to hold their shares ‘in locked balance’ (which were excluded from the off-the-floor share transfer until the beneficiaries of the deceased are registered in the Register of DIST/ shares are transferred to the ‘trading balance’) are considered as held in trust for MCRP in consideration of the 648,656 MCRP shares allotted to those shareholders for the transfer of their DIST shares in terms of the ‘Arrangement’ (now held in trust).

7

1.5 MCRP: Group Operations

MCRP Group’s operations currently consist of five primary sectors (prior to restructure), namely:

Beverage (Excl. DIST Alcohol Company)

Plantations Telecommunication Financial Services Diversified

Historically, MCRP Group operations exclude the DIST Alcohol Company, which operates in the legacy alcohol

business. Prior to the restructure, MCRP Group was the only fully owned subsidiary of DIST Group, and held all other

subsidiaries. As such, DIST Group is a combination of DIST Alcohol Company and MCRP Group operations.

Under the restructuring process being carried out, MCRP will become the ultimate holding company of the former

DIST Group, following a share swap. Hence, going forward, MCRP Group will also include the performance of DIST

Alcohol Company. For consistency, this report will analyze the historical Financial Statements for DIST Group, which

is the proforma Financial Statements of MCRP Group (post-restructure).

8

2.0 DIST GROUP: HISTORICAL ANALYSIS OF POST-RESTRUCTURE MCRP

GROUP FINANCIALS

Under the restructuring process being carried out, MCRP will become the ultimate holding company of the former

DIST Group, following a share swap. Hence, going forward, MCRP Group will also include the performance of DIST

Alcohol Company. For consistency, this report will analyze the historical Financial Statements for DIST Group, which

is the proforma Financial Statements of MCRP Group (post-restructure).

The Group operates in the following segments:

Beverage: DIST Alcohol Company and Periceyl (Pvt) Ltd (PCEYL). DIST is market leader in Sri Lanka’s legal

hard alcohol segment and focuses on the manufacture of arrack. PCEYL focuses on the premium alcohol

segment and manufactures foreign liquor brands while also importing well-known premium brands

Plantations: Includes operations of subsidiary, Balangoda Plantations PLC (BPL)

Telecommunication: Focuses on the telecommunication industry through Lanka Bell Ltd, Telecom Frontier

(Pvt) Ltd, Bell Solutions (Pvt) Ltd

Financial Services: Operates in the Insurance and Financial Services businesses through subsidiaries,

Continental Insurance Lanka Ltd and Melsta Regal Finance Limited

Diversified: Includes a range of industries including tourism, hydro power, real estate and media

9

2.1 Income Statement Analysis

(LKR Bn) FY12 FY13 FY14 FY15 FY16

Net Revenue 27.0 28.8 29.0 28.9 33.8

Gross Profit 12.2 12.9 13.8 12.7 13.0

EBIT 8.3 8.0 8.5 8.5 8.4

Profit before Tax 9.0 8.1 9.5 9.7 9.0

Net Profit attributable to Equity Holders 5.5 5.1 6.1 6.6 6.0

Gross Margin 45.3% 44.7% 47.5% 43.9% 38.5%

EBIT Margin 30.7% 27.9% 29.4% 29.3% 25.0%

PBT Margin 33.3% 28.1% 32.8% 33.6% 26.6%

Net Margin 20.5% 17.9% 21.1% 22.7% 17.6%

Segmental Net Revenue Beverages 16.8 19.5 18.9 19.1 24.2

Plantations 2.7 2.8 3.2 3.0 2.4

Telecommunication 4.0 4.0 3.6 3.4 3.3

Financial Services 0.0 0.0 0.0 1.4 2.0

Diversified 3.6 2.5 3.2 2.0 1.9

Segmental Profit before Tax Beverages 6.6 6.3 8.0 8.4 8.4

Plantations 0.1 0.1 0.1 -0.1 -0.4

Telecommunication 0.1 -0.2 -0.6 -0.7 -0.6

Financial Services 0.0 0.0 0.0 0.2 0.2

Diversified 0.8 0.5 0.5 0.5 0.7

Segmental PBT Margins Beverages 39.6% 32.6% 42.4% 43.9% 34.7%

Plantations 4.4% 4.0% 4.1% -3.5% -17.8%

Telecommunication 2.4% -3.8% -17.6% -20.5% -19.5%

Financial Services n/a n/a n/a 13.0% 11.5%

Diversified 21.3% 19.1% 16.5% 28.2% 36.4%

10

2.1.1 Revenue

DIST Group reported gross revenue of LKR 88.9 Bn in FY16, increasing 33.1% YoY and at a CAGR of 8.9% over the

period FY12-16. The Beverage sector constitutes majority of the Group’s net revenues, generating 71.5% of revenue

in FY16 and an average of 66.6% over FY12-16. Telecommunication was the second largest contributor to revenue,

accounting for 9.7% (average of 11.7% over FY12-16). Plantation, Financial Services and Diversified sectors

accounted for 7.1%, 6.0% and 5.6% of revenue in FY16, respectively. Revenue growth in FY16 was largely due to

higher volumes and increased prices in the Beverage sector. Despite a slowdown during 4QFY16 due to the excise

duty led price revisions, alcohol sales volumes recorded significant growth largely owing to cracking down of the

illicit un invoiced / tax unpaid local liquor segment under the current political regime and higher consumer

disposable income.

2.1.2 Gross Profit

Group gross profit for FY16 amounted to

LKR 13.0 Bn, implying a margin of 38.5%

(vs. margin of 43.9% in the prior year). The

declining trend of gross margins since a

high of 47.5% in FY14 was due to the Value

Added Tax (VAT) and Nation Building Tax

(NBT) being consolidated with excise

duties for the Alcohol Beverage sector in

October 2014. Prior to the amendment of

the tax regulation, Group gross profit

margins ranged between 44-48%.

30%

35%

40%

45%

50%

0

4

8

12

16

FY12 FY13 FY14 FY15 FY16

LKR

Bn

Gross Profit

Gross Profit Gross Margin (%) - RHS

Source: Company Financials

62%10%

15%

0%13%

72%

7%

10%

6%6%

Revenue Composition

Beverages

Plantations

Telecommunication

Financial Services

Diversified

FY12

FY16

Source: Company Financials

-5%

0%

5%

10%

15%

20%

0

5

10

15

20

25

30

35

FY12 FY13 FY14 FY15 FY16

LKR

Bn

Revenue Growth

Total Net Revenue

Growth (%) - RHS

Source: Company Financials

11

2.1.3 Other Operating Income

Meanwhile, DIST Group recorded other income of LKR 1.2 Bn in FY16, down 16.2% YoY due to the previous year

consisting of a refund on telecommunication development charge and a gain from disposal from investments. Other

operating income consists of dividend income from financial assets, gain on disposals and rent income. Other

operating income declined at a CAGR of 8.6% over the period FY12-16, while it averaged 4.3% of net revenue during

the same period.

2.1.4 Operating Expenses

Administration Expenses for the Group declined 6.0% YoY to LKR 3.6 Bn in FY16, while it grew at a CAGR of 3.2% over

the period FY12-16. The decline in FY16 was primarily owing to the cost reduction efforts taken by management in

order to reduce the losses incurred by the Telecommunication sector. Increasing 3.0% YoY, distribution expenses

amounted to LKR 1.8 Bn for FY16 and were 5.2% of net revenue, below the 5-year average of 6.2%. Other operating

expenses of LKR 350.5 Mn in FY16 increased significantly from that of the previous year due to impairment of loans

and advances and a loss on revaluation of property, plant and equipment.

2.1.5 EBIT

LKR Bn FY12 FY13 FY14 FY15 FY16

Reported EBIT 8.3 8.0 8.5 8.5 8.4

Reported EBIT Margin 30.7% 27.9% 29.4% 29.3% 25.0%

Non-Recurring Expenses

Loss on disposal of subsidiaries

-

-

0.6

-

- Loss on disposal of equity accounted investee

-

-

0.1

-

-

Impairment of Goodwill

-

0.8

-

-

-

Recurring EBIT 8.3 8.8 9.3 8.5 8.4

Recurring EBIT Margin 30.7% 30.6% 31.9% 29.3% 25.0%

Consequently, DIST Group EBIT amounted to LKR 8.4 Bn in FY16 marginally declining from that of the prior year. EBIT

margins declined to 25.0% in FY16 from 29.3% in FY15, largely due to the impact of lower gross margins. During the

period FY12-16, DIST Group recorded non-recurring expenses such as loss on disposal of subsidiaries and associates

and impairment of goodwill in FY13-14. The disposal was related to the de-recognition of Pelwatte Sugar Industries

PLC following the enactment of Underperforming Enterprises and Underutilized Assets Bill by the Government of Sri

Lanka.

2.1.6 Net Finance Cost

Refer Section 2.1.9 Balance Sheet Analysis

12

2.1.7 Share of Profit from Equity Accounted Investees

The share of profit from equity accounted investees amounted to LKR 0.7 Bn, down 46.2% YoY. The reasons for the

decline in profits are lower profits from Aitken Spence (SPEN) (lack of contribution from the 74% owned 100MW

thermal power plant, Ace Power Embilipitiya) and the widening loss of MADU. DIST’s share of profit during the year

from SPEN amounted to LKR 0.9 Bn declining from LKR 1.5 Bn in the previous year. Furthermore, the loss from MADU

widened to LKR 0.1 Bn.

2.1.8 Net Profit

Effective tax rate of 37.0% for the

year was above the 33.5%

recorded in FY15 and also

exceeded the four year average of

33.8%. The higher effective tax

rate was owing to the higher

contribution to PBT from the

Beverage sector, which is taxed at

a higher rate.

Consequently, DIST’s net profit

attributable to equity holders of

LKR 6.0 Bn in FY16 was down 9.0%

YoY and resulted in a net margin of

17.6%, approximately 500 bps below that of FY15. This implied an earnings per share of LKR 19.88 in FY16, declining

from LKR 21.84 in the previous year.

FY12 FY13 FY14 FY15 FY16

Recurring NP Margin 20.5% 20.6% 23.6% 22.7% 17.6%

Reported NP Margin 20.5% 17.9% 21.1% 22.7% 17.6%

Meanwhile, the Group’s shareholders’ funds for FY16 were LKR 63.2 Bn, leading to a return on equity of 9.6% for the

year on a recurring basis. During FY13-16, the Group’s recurring ROE averaged 11.9%.

FY12 FY13 FY14 FY15 FY16

Recurring Net Profit Attributable to Equity Holders 5.5 5.9 6.8 6.6 6.0

Shareholders' Funds 41.6 48.0 53.6 61.0 63.2

Recurring ROE (%) 13.2% 13.5% 11.4% 9.6%

Reported Net Profit Attributable to Equity Holders 5.5 5.1 6.1 6.6 6.0

ROE (%) 11.5% 12.0% 11.4% 9.6%

Group dividend per share was LKR 3.35 in FY16, implying a dividend payout ratio of 16.9%, above a 5-year average

of 16.3%.

FY12 FY13 FY14 FY15 FY16

Dividend per Share (LKR) 3.00 3.00 3.25 3.25 3.35

Dividend Payout (%) 16.3% 17.5% 15.9% 14.9% 16.9%

0%

7%

14%

21%

28%

35%

0

2

4

6

8

10

FY13 FY14 FY15 FY16

LKR

Bn

EBIT and Net ProfitRecurring EBIT Recurring Net Profit to Equity Holders

EBIT Margin (%) - RHS Net Profit Margin (%) - RHS

Source: Company Financials

13

2.1.9 Balance Sheet Analysis

MCRP Group reported Property, Plant and

Equipment (PPE) of LKR 22.3 Bn as at 31st

March 2016, increasing from LKR 18.5 Bn in

the previous year. Intangible Assets and

Investment Property for FY16 totaled LKR 3.7

Bn increasing from LKR 3.3 Bn in FY15. Capex

of LKR 3.7 Bn was 11.0% of net revenue in

FY16, declining from 35.5% in FY15. FY15

capex included the investment in a new plant

for DIST, in order to improve efficiencies. The

new plant-related capex totaled

approximately LKR 5.0 Bn over a period of 3

years. Over the period FY12-16, capex as a

percentage of revenue averaged at 16.1%. Depreciation and Amortization for FY16 amounted to LKR 2.4 Bn

increasing from LKR 1.5 Bn in FY15.

Working Capital (Days) FY12 FY13 FY14 FY15 FY16

Inventory 143 141 106 112 105

Trade and Other Receivables 111 99 122 127 122

Trade and Other Payables 282 257 210 230 210

Working Capital Cycle -28 -17 18 10 17

The Group reported inventory of LKR 6.0 Bn, while trade receivables and payables amounted to LKR 11.3 Bn and LKR

12.0 Bn, respectively. Inventory amounted to 28.9% of cost of sales, slightly below that of the previous year.

Meanwhile, trade receivables as a percentage of revenue amounted to 33.3%, down from 34.9% in FY15. Trade and

other payables as a percentage of cost of sales amounted to 57.6%, declining from 62.9% in the previous year as the

increased excise duty resulted in higher costs.

The working capital cycle for the period ending 31st March 2016 was 17 days, increasing from 10 days in FY15. During

the years FY12-13, the Group had a negative cash cycle while on average it has maintained a cash conversion cycle

of 15 days over the period FY14-16.

FY12 FY13 FY14 FY15 FY16

Total Debt 2.6 11.2 13.4 13.8 14.5

YoY Growth (%) 322.5% 20.1% 3.3% 5.0%

Debt to Equity (x) 0.06 0.23 0.25 0.23 0.23

Finance Income 0.7 0.7 0.6 0.4

Finance Cost (0.7) (2.0) (1.2) (0.7) (0.6)

Effective Finance Cost (%) 28.5% 9.9% 5.2% 4.3%

The Group’s balance sheet strength is reflected in its relatively low gearing levels, with a low debt to equity of 0.23x

in FY16 and a 5 year average of 0.20x. Total debt for FY16 amounted to LKR 14.5 Bn, increasing 5.0% YoY. Majority

0%

8%

16%

24%

32%

40%

0

2

4

6

8

10

12

FY12 FY13 FY14 FY15 FY16

LKR

Bn

Capex and Depreciation

CapexDepreciation & Amortization (Excl. Biological Assets)Capex as a % of Net Revenue

Source: Company Financials

14

of debt for the Group is in the form of short term borrowings and bank overdrafts (80.5% of total debt in FY16).

Excluding short term debt the Group’s debt to equity ratio would be even lower averaging 0.03x over the 5 year

period FY12-16. Finance cost for FY16 amounted to LKR 0.6 Bn, declining from LKR 0.7 Bn in the previous year.

Meanwhile, finance income declined 28.9% YoY to LKR 0.4 Bn. The effective finance cost for the year of 4.3% is below

5.2% recorded in FY15.

15

2.2 DIST Group: Quarterly Financial Analysis of Post-Restructure MCRP Group Financials

Quarterly Performance (LKR Bn) 1QFY16 1QFY17 YoY Growth

Net Revenue 7.6 9.3 23.3%

Gross Profit 3.3 4.0 21.3%

EBIT 2.2 2.8 29.9%

Profit before Tax 2.4 2.8 16.3%

Net Profit Attributable to Equity Holders 1.8 1.9 9.5%

EPS (LKR) 5.85 6.41 9.5%

Gross Profit Margin (%) 43.7% 43.0%

EBIT Margin (%) 28.8% 30.3%

Net Profit Margin (%) 23.2% 20.6%

DIST Group reported net revenue of LKR 9.3 Bn in 1QFY17, recording 23.3% YoY growth (-0.5% QoQ). Revenue

growth from 1QFY16 was largely owing to growth in the Beverage sector, which remained the largest contributor to

net revenue during the quarter (74.1% of net turnover). Group gross profit also increased at a significant 21.3% YoY

to LKR 4.0 Bn (+26.6% QoQ). However, gross margins declined from 43.7% in 1QFY16 to 43.0% in 1QFY17, as the

Group was affected by higher margins being provided to retailers by the Beverage sector and low tea and rubber

prices affecting the Plantation sector.

Administration Expenses amounted to LKR 1.0 Bn in FY16 up 12.2% YoY while distribution expenses were LKR 0.5 up

4.7% YoY. Other operating expenses were LKR 0.2 Bn for the year. Total operating expenses for the quarter thus

amounted to LKR 1.5 Bn, increasing from LKR 1.3 Bn in the previous year. Operating expenses as a percentage of net

revenue was 15.8% in 1QFY17 declining from 17.7% in 1QFY16. Consequently, the Group recorded 1QFY17 EBIT of

LKR 2.8 Bn, which implies a margin of 30.3%, an expansion of 150 bps from that of 1QFY16. Net finance cost

amounted to LKR 0.1 Bn in 1QFY17 against a net finance income of LKR 0.1 Bn in the previous year’s quarter. The

Group reported total debt of LKR 12.3 Bn in 1QFY17, declining slightly from the prior year quarter and as such debt

to equity for the quarter of 0.19x was broadly in line with that reported in 1QFY16. Meanwhile, share of profit from

equity accounted investees amounted to LKR 0.1 Bn, declining from the previous year mainly due to the decline in

the tourism sector. Effective tax for the quarter increased to 36.6% from 31.5% in 1QFY16. Net profit attributable to

equity holders grew 9.5% YoY to LKR 1.9 Bn in 1QFY17, implying a net margin of 20.6%. Reported EPS was LKR 6.41.

16

2.3 Melstacorp Group (Prior to Restructure): Financial Analysis

Melstacorp as a stand-alone company is an investment holding company which generates income through rent and

investment returns through its diversified portfolio of quoted and unquoted equity investments, corporate debt

securities, sovereign debt instruments and investment property. This section of the research report analyzes the

Melstacorp Group (prior to restructure), which excludes operations of DIST Alcohol Company.

Melstacorp Group, which was historically a fully owned subsidiary of DIST Group, held stakes in the following

companies:

Periceyl (Pvt) Ltd

Balangoda Plantations PLC

Bell Solutions (Pvt) Ltd

Lanka Bell Ltd

Telecom Frontier (Pvt) Ltd

Continental Insurance Lanka Limited

Melsta Regal Finance Ltd

Melsta Logistics (Pvt) Ltd

Timpex Ltd

Bellvantage (Pvt) Ltd

Bogo Power (Pvt) Ltd

Browns Beach Hotel PLC

Milford Holdings (Pvt) Ltd

Splendor Media (Pvt) Ltd

Texpro Industries Ltd

Melsta Properties (Pvt) Ltd

Melsta Technology (Pvt) Limited

Melsta Tower (Pvt) Limited

Prior to the restructure, MCRP Group recorded total net revenue of LKR 13.0 Bn in FY16, up 3.7% YoY. The largest

contributor to net revenue in FY16 was the Telecommunication Sector followed by Beverage and Diversified sectors

contributing 25.3%, 20.5% and 19.7% to revenue, respectively. The Group reported gross profit of LKR 4.3 Bn in FY16,

below that of FY15, and as such saw its gross margins decline by 150 bps to 33.0% primarily owing to weakness in

the Plantation sector. Consequently, EBIT for the Group also declined to LKR 1.3 Bn, down 4.8% YoY. On a segmental

basis, the Diversified sector generated profit before tax of LKR 1.2 Bn in FY16 while the Beverage sector earned LKR

1.0 Bn. Both Telecommunication and Plantation sectors however, reported a loss before tax. Net profit attributable

to equity-holders declined 22.8% YoY to LKR 2.0 Bn in FY16 resulting in the net margin narrowing to 15.1% from

20.3% in the prior year.

17

3.0 BUSINESS SEGMENTS

3.1 Beverage Sector

The Beverage sector comprises operations across

two companies, DIST Alcohol Company and

Periceyl (Pvt) Ltd (PCEYL) and is the largest

revenue generating segment for the Group (71.5%

of total Group net revenue in FY16).

The origin of DIST traces back to 1913, with the commencement of distillation and manufacture of liquor products

by the Excise Department of Ceylon. The State Distilleries Corporation which was incorporated to take over the

operations was converted to a limited company, and privatized in 1992 with the acquisition by the Stassens Group

of Companies.

DIST Company markets a wide range of products including, Old Arrack, Coconut Arrack, Double Distilled Arrack,

V.S.O.A and Extra Special. Meanwhile, PCEYL’s key brands include Periceyl Black Opal, Franklin and Galerie. The price

range for several key brands of DIST Co. and PCEYL are highlighted below.

Prices of Key Brands of DIST Company and PCEYL per 750ml bottle

DIST Company Rs.* PCEYL Rs.*

Extra Special 1,200 Periceyl Lemon Arrack 1,320

Special Arrack 1,080 Flinton London Dry Gin 1,650

White Label Arrack 1,250 Franklin Brandy 1,630

Old Arrack 1,400 Petroff Vodka 1,700

V.S.O.A Premium 1,500 Balmora Rum 1,670

D.D.A 1,500 House of Tilbury Whisky 2,000

Sri Lanka Arrack 1,700 Galerie Brandy 1,950

Source: CT CLSA * w.e.f 23 Nov 2015

18

DIST Company has continued to maintain its position as market leader in the industry over the years. In terms of

Coconut and Processed Arrack, the Beverage sector accounted for 70.3% market share in 2014, while in the Total

Arrack market the sector had a market share of 71.7%.

One of the primary reasons for the decline in DIST Company market share is the increasing presence of cheap illicit

alcohol. However, the current political regime has taken a firm stance on the illicit local liquor segment in Sri Lanka,

particularly of un-invoiced and tax unpaid products, which liberally entered the market at significantly lower prices.

In FY16, the Beverage sector paid 69.4% of its gross revenue as direct turnover related taxes, up from 66.4% in the

previous year. The direct turnover related taxes for FY16 amounted to LKR 55.0 Bn, increasing from LKR 37.8 Bn in

the previous year. The industry faces another challenge due to the prohibition of advertising and promoting alcoholic

brands (NATA Act).

Meanwhile, the increasing taxes on hard alcohol over the recent years has also affected performance. The hard

liquor market continued to decline, and with it the market for DIST Alcohol Company, primarily due to the impact of

substitution, resulting from strong beer (above 5% alcohol content) being priced relatively lower. In November 2015

however, the GoSL increased the duty on strong beer, thus ending the comparative advantage of purchasing cheaper

strong beer versus more expensive hard liquor. Given these challenges, the beverage sector has continued to lose

market share from 80.5% in 2012 to 71.7% in 2014.

Tax Structure on Alcohol Beverages

Segment 2011 2012 2013 2014 2015

Jan Oct Mar Oct Jul Oct Oct* Oct Nov

Beer - Alcohol % < 5% (LKR / Ltr) 80 85 90 100 110 120 150 190 190

Beer - Alcohol % >/=5% (LKR / Ltr) 96 101 106 116 130 145 185 245 315

Molasses & Arrack (LKR / Proof Ltr) 863 923 983 1,043 1,120 1,210 1,485 1,595 1,850

Foreign Liquor (LKR / Proof Ltr) 1,003 1,063 1,123 1,183 1,250 1,370 1,700 1,860 2,030

As a result of the differing tax structure for hard liquor and malt beer (prior to the amendment in November 2015),

there has been a shift in production of liquor. The chart below indicates that production of hard liquor has continued

to decline while production of malt liquor (beer) has been on an upward trajectory. Over the period 2010-2014, hard

liquor production declined at a CAGR of 2.7%, while malt liquor production grew at a CAGR of 15.0%.

0

20

40

60

80

100

120

140

2008 2009 2010 2011 2012 2013 2014

Liquor Production

Hard Liquor (Proof Litres Mn) Malt Liquor (Beer) (Bulk Liters Mn)

Source: Excise Department

Source: Excise Department of Sri Lanka

* Consolidation of Duties

19

The segment earned net revenue of LKR 24.2

Bn in FY16, up 26.4% YoY primarily driven by

higher volumes (+11.8%) and increased

prices (+13.1%). Volume growth was largely

owing to the cracking down of the illicit local

liquor segment in Sri Lanka, while higher

disposable income also supported the

recovery. Revenue growth was however,

slightly hampered by the sharp excise duty

led price revisions. Volume growth in proof

liters declined 14.7% and 9.2% in FY14 and

FY15 against a growth in net revenue per

proof liter of 14.1% and 11.4% in the same

periods, respectively.

Despite significant revenue growth however, the

segment’s profit before tax declined marginally to

LKR 8.4 Bn in FY16 due to the adverse impact of

exchange rate movements and raw material price

increases. The average exchange rate for LKR

against the USD declined approximately 6% in

FY16, thus resulting in import of raw materials

being more expensive. Given that majority of the

sector’s ethanol requirement is imported

(approximately 70% of cost of sales), a depreciating

rupee has a negative impact on sector

performance.

Furthermore, import duties on ethanol were raised in 2015, while global sugar and ethanol prices also increased,

which also had a negative impact on sector performance. given that sugarcane is a primary raw material in the

production of ethanol, sugar prices broadly track ethanol prices.

Earnings were also impacted by the end of PCEYL’s partnership with Pernod Ricard, for distribution of imported

brands.

The sector recorded strong financial performance in 1QFY17. Net revenue from Beverages increased 30.1% YoY to

LKR 6.9 Bn during the quarter while profit before tax recorded growth of 30.3% YoY to LKR 2.8 Bn. Revenue growth

was largely due to higher volumes and product prices. PBT margins remained broadly flat during the quarter at

39.9%. On a QoQ basis, revenue growth was 1.2% while profit before tax grew 12.3%.

In FY16, DIST Alcohol Company recorded net revenue of LKR 21.5 Bn increasing 27.3% YoY driven by higher volumes

as well as prices. Gross profit for the year amounted to LKR 9.2 Bn implying a gross margin of 42.8%, decreasing from

52.2% primarily owing to the consolidation of VAT and NBT with excise duties. Margins were further hampered by

increasing competition and the resulting higher margins provided to retailers. During 1QFY17, DIST Alcohol Company

recorded net revenue of LKR 6.2 Bn increasing 31.8% YoY. Gross profit during the quarter amounted to LKR 2.9 Bn,

implying a gross margin of 46.4%, down from 47.9% in 1QFY16, given the consolidation of duties and increased

competition.

-10%

-1%

8%

17%

26%

35%

44%

0

5

10

15

20

25

FY12 FY13 FY14 FY15 FY16

LKR

Bn

Beverage - Revenue

Revenue YoY Growth (%) - RHS

0%

10%

20%

30%

40%

50%

0

2

3

5

6

8

9

FY12 FY13 FY14 FY15 FY16

LKR

Bn

Beverage - Profit before Tax

Profit before Tax PBT Margin (%) - RHS

Source: Company Financials

-20.0%

-10.0%

0.0%

10.0%

20.0%

FY14 FY15 FY16

Beverage Sector: Net Revenue per Proof Liter and Volume Growth

Volume Growth (Proof Liters) (%)

Growth in Net Revenue per Proof Liter (%)

Source: Company Financials

20

3.2 Plantation Sector

MCRP’s exposure to the Plantation sector stems from its subsidiary (effective stake of

43.2%), Balangoda Plantations PLC (BPL), which primarily focuses on the cultivation and

processing of tea and rubber. The Group is also exposed to the Plantation industry through

its associate, Madulsima Plantations PLC (MADU), of which it has an effective stake of

45.9%. The Plantation sector of the Group includes the performance of BPL, while the

performance of MADU is recorded under share of associate profits.

The Plantation sector earned net revenue of LKR

2.4 Bn in FY16 (accounted for 7.1% of Group net

revenue) declining significantly due to weak

demand for tea from export destinations such as

Russia, Ukraine, Turkey and the Middle East

combined with the impact of low prices. Revenue

from rubber plantations also declined owing to the

unfavorable weather conditions that persisted and

continued global weakness. The sector generated a

net loss before tax of LKR 0.4 Bn in FY16, increasing

from a loss of LKR 0.1 Bn in the previous year. The

Group’s Plantation sector, similar to the industry at

large, was affected by continued labour issues and trade action for wage increases. A ‘go-slow’ was launched by

estate workers in July 2015, demanding a wage hike which had an adverse impact on the sector’s performance.

Furthermore, the withdrawal of the fertilizer subsidy and the ban of certain chemicals being used have also affected

the industry at large. However, BPL continued its replanting strategy, where unproductive tea areas were diversified

into rubber, while new planting was also conducted in Balangoda and Badulla.

The sector generated revenue of LKR 0.6 Bn during 1QFY17 increasing 5.9% YoY, while the loss before tax narrowed

to LKR 35.3 Mn from LKR 102.4 Mn in the same quarter of the previous year. Improvement in sector financial

performance was largely owing to a recovery in tea prices fetched at the auctions. On a QoQ basis, revenue increased

5.2% while the loss before tax declined.

BPL was incorporated in 1992 and was listed on the CSE in 1998. The company has 06 tea estates, 12 tea cum rubber

estates and 04 rubber estates. In 2015, approximately 90% of its total crop was tea, while the remaining 10%

comprised rubber. BPL’s tea crop (primarily in Uva Medium and Low elevations) declined 6.4%, down for the second

consecutive year in 2015, while rubber crop grew 13.9% YoY.

-40%

-20%

0%

20%

0

1

2

3

4

FY12 FY13 FY14 FY15 FY16

LKR

Bn

Plantation - Revenue

Revenue YoY Growth (%) - RHS

Source: Company Financials

-20%

-15%

-10%

-5%

0%

5%

10%

-500

-400

-300

-200

-100

0

100

200

FY12 FY13 FY14 FY15 FY16

LKR

'00

0s

Plantation - Profit before TaxProfit before Tax PBT Margin (%) - RHS

Source: Company Financials

21

BPL’s National Sales Average (NSA) for tea declined 15.2% YoY while the NSA for rubber declined 16.4% YoY in FY16.

Consequently, BPL’s revenue from tea amounted to LKR 2.2 Bn, down 20.6% YoY and rubber revenue declined 4.8%

YoY to LKR 177 Mn during the year. The yield / hectare for tea declined to 867 Kg/Ha in FY16, down from 940 Kg/Ha

in the previous year. The rubber sector was adversely affected by the continued decline in global demand and large

stock piles accumulated in major consuming countries. The rubber yield / hectare however increased to 647 Kg / Ha

from 577 Kg / Ha in the previous year.

Tea Industry

Tea production continued to decline in 2015, for the second consecutive year, primarily due to supply side factors

such as unfavorable weather conditions and labour issues. The sector’s concerns were however further exacerbated

by lower demand from major export destinations owing to declining oil prices (Middle East) and geo-political

uncertainties (Russia and Ukraine). Lower demand led to the declining trend in tea prices to continue in 2015.

Production declined 2.7% YoY in 2016 continuing a downward trajectory for the second consecutive year. In 2015,

the average NSA for tea in Sri Lanka declined 11.8% YoY to LKR 387.6 per kg. However, prices started increasing

towards the end of 2015. By September 2016, prices increased to LKR 499.1 per kg, up 36.3% YoY. Sri Lanka is also

expected to benefit from the removal of economic sanctions on Iran, which is one of the country’s major export

-

50

100

150

200

250

2012 2013 2014 2015

Mn

Kg

Tea Crop Output in Sri Lanka

High Medium Low

Source: Sri Lanka Tea Board

0

100

200

300

400

500

600

2012 2013 2014 2015 2016 YTMAugust

LKR

/ K

g

National Sales Average by Elevation

Low Medium High

Source: Sri Lanka Tea Board

-

100

200

300

400

500

600

-

500

1,000

1,500

2,000

2,500

3,000

3,500

FY12 FY13 FY14 FY15 FY16

LKR

/ K

g

LKR

Mn

BPL: Tea vs. Rubber

Tea Revenue Rubber Revenue

Tea NSA - RHS Rubber NSA - RHS

Source: BPL

500

600

700

800

900

1,000

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

FY12 FY13 FY14 FY15 FY16

Kg

/ h

a

Mn

Kg

Cropwise BreakdownTotal Tea Crop Total Rubber Crop

Tea - Yield kg/ha Rubber - Yield kg/ha

Source: BPLL

22

destinations for tea. Although tea prices showed signs of recovery in 1QFY16, the outlook still remains relatively

bleak on the back of a global economic slowdown coupled with political unrest in the Middle East and Russia.

Rubber Industry

Natural rubber production declined 10.1% YoY to 88.6

MT ‘000s in 2015, continuing the downtrend

experienced since 2012, as smallholders slowed their

tapping operations in response to lower rubber

prices, globally. The industry was further affected by

adverse weather conditions and the high cost of

production, poor management of the fields and over

aged trees. Sri Lankan rubber prices (average of Latex

Crepe No. 1X, RSS1 and Brown Crepe 1X) was down

4.3% YoY to LKR 245.1 per Kg. Prices have continued

to decline following the trend of international rubber

price decline. The downtrend is due to the primary

substitute, synthetic rubber prices also being low due

to its positive correlation with crude oil prices.

180

270

360

450

0

40

80

120

160

2012 2013 2014 2015LK

R /

Kg

MT

'00

0s

Rubber Production and NSA in Sri Lanka

Natural Rubber Production

Average Rubber NSA

Source: Rubber Development Department of Sri Lanka

23

3.3 Telecommunication Sector

The Group’s telecommunication sector

consists of Lanka Bell (LBL), Bell Solutions

and Telecom Frontier. Lanka Bell is the

pioneer of fixed wireless telephony who

introduced CDMA technology to Sri Lanka

and currently provides a range of telecommunication services to corporate and residential customers. The Sri Lankan

telecommunication industry consists of two operators with the ability to offer mobile, fixed, data & television. LBL

has clearance to offer just one or two of the services. The Company also introduced Bell4G home broadband services

via 4G Long Term Evolution (LTE) technology. LBL has a subscriber base of approximately 0.9 Mn subscribers.

The sector generated LKR 3.3 Bn in FY16 (accounted for 9.7% of Group net revenue) while it recorded a net loss

before tax of LKR 0.6 Bn, which narrowed from a loss of LKR 0.7 Bn in the previous year. The primary reason for the

consistent net losses incurred by the sector is the significant depreciation costs, although management stated LBL is

EBITDA positive with a positive operating Cashflow. The sector recorded revenue of LKR 0.8 Bn during the quarter

declining from that of the prior year, while the loss before tax increased to LKR 0.3 Bn. On a QoQ basis, revenues

declined 2.3%.

The Sri Lankan telecommunications industry is dominated by

mobile services, which accounted for over 90% of the market,

while fixed access services accounted for less than 10%. In

2015, the number of fixed lines declined 4.0% YoY to 2.6 Mn

as a decline in wireless services offset a marginal increase in

wireline services. Cellular phone connections however, have

increased at a CAGR of 7.1% over the period 2010-2015 to

reach 24.4 Mn connections by 2015.

0

9,000

18,000

27,000

2010 2011 2012 2013 2014 2015

No

.

Fixed Services Vs. Mobile Services in Sri Lanka

Fixed Access Services ('000) Cellular Phones ('000)

Source: Central Bank of Sri Lanka

-14%

0%

14%

0

1

2

3

4

FY12 FY13 FY14 FY15 FY16

LKR

Bn

Telecommunication - Revenue

Revenue YoY Growth (%) - RHS

Source: Company Financials

-25%

-20%

-15%

-10%

-5%

0%

-800

-600

-400

-200

0

200

FY12 FY13 FY14 FY15 FY16

LKR

Mn

Telecommunication - Profit before Tax

Profit before Tax

PBT Margin (%) - RHSSource: Company Financials

24

Moreover, telephone penetration (connections per

100 persons) continued to increase in Sri Lanka

reaching 128.7 in 2015 from 117.0 in 2012 with

growth from cellular phone penetration of 116.3

more than compensating for lower penetration

levels of fixed lines of 12.4. Internet penetration in

Sri Lanka also has continued to grow reaching 19.5%

in 2015 from 6.7% in 2012. Primarily driven by higher

demand for high speed internet services in Sri Lanka,

LBL also rolled out 4G/ Long Term Evolution (LTE) to

enhance the services provided to their customers.

0 40 80 120

2012

2013

2014

2015

Telephone Penetration in Sri Lanka

Cellular Fixed

Source: Central Bank of Sri Lanka

25

3.4 Financial Services Sector

The Financial Services sector contributed 6.0% to

Group net revenue in FY16, slightly increasing

from 5.0% contribution in FY15. The Financial

Services sector consists of Continental Insurance

Lanka Limited (CIL), which operates in the general

insurance business, and Melsta Regal Finance Limited (MERF), which focuses on financing, leasing, hire purchasing

and factoring. While historically, these two business lines were segmented under Diversified Sector the Group split

the categorization of CIL and MERF as Financial Services in FY16.

CIL, which operates in the general insurance business, accounts for approximately 4% market share. The industry

has recently been intensely scrutinized by regulatory authorities and several reforms were introduced in an effort

to strengthen the framework and ensure insurance policyholders’ safety and protection. The company’s product

portfolio includes categories such as automobile, home-owners, travel, marine, general accident and property

insurances. CIL has a branch network of 40 and continues to expand its network. CIL was the first insurance company

under 5 years of operations to be rated A- (lka) by Fitch Ratings Lanka.

MERF has a rating of A+ (lka) by Fitch Ratings, and has continued to focus on penetrating the market over the last

four years of operations. The company has seven branches across the island and continues to expand its geographical

footprint. The company hopes to expand its product range to include housing loans and micro leasing products.

The sector generated revenue of LKR 2.0 Bn in FY16, increasing a significant 40.9% YoY from LKR 1.4 Bn in FY15.

Profit before Tax also grew 2.8% YoY in FY16 to LKR 0.2 Bn. Financial Services recorded revenue growth of 44.1% YoY

to reach LKR 0.7 Bn in 1QFY17, although profit before tax remained relatively flat YoY, owing to the significant claims

stemming from the recent floods. On a QoQ basis however, revenues improved 7.6% while the profit before tax

increased a significant 162.8%.

0.0

0.7

1.4

2.1

FY15 FY16

LKR

Bn

Financial Services - Revenue and Profit before Tax

Revenue Profit before Tax

Source: Company Financials

26

3.5 Diversified Sector

DIST’s Diversified sector consists of a range of industries:

Milford Holdings : 98.4% Holdings : An Investment Holding Company

Browns Beach Hotels : 53.9% Holdings : Operates in the Leisure Business

Texpro Industries : 41.8% Holdings : Dyeing and Printing Fabric

Timpex : 51.0% Holdings : An Investment Holding Company

Melsta Logistics : 100.0% Holdings : Automobile Servicing & Logistics

Splendor Media : 100.0% Holdings : Media Buying & Creative Services

Bogo Power : 99.3% Holdings : Hydro Power Generation

Bellvantage : 100.0% Holdings : BPO, KPO & Call Centre Services

Melsta Properties : 100.0% Holdings : Management of Real Estate

Melsta Towers : 100.0% Holdings : Real Estate Company

Melsta Technologies : 100.0% Holdings : Information Technology

The Diversified sector contributed 5.6% to

Group net revenue in FY16, declining from

6.7% in the previous year. The sector

generated revenue of LKR 1.9 Bn in FY16,

declining 2.5% YoY. Despite lower revenue

however, sector earnings before tax

increased 25.9% YoY to LKR 0.7 Bn in FY16

implying a PBT margin of 36.4%. Margins

expanded over 800 bps during the year.

Margin improvement was owing to higher

return on investments, an increase in rent

income and higher profits from Bogo Power.

During 1QFY17 revenue from Diversified Sector declined 3.0% YoY to LKR 0.4 Bn, while profit before tax declined

58.1% YoY to LKR 0.1 Bn. On a QoQ basis, revenues were down 32.3% while a loss before tax in the previous quarter

turned profitable. The weak performance is primarily attributable to the slowdown in equity markets.

0.0

0.5

1.0

1.5

2.0

FY15 FY16

LKR

Bn

Diversified Sector - Revenue and Profit before Tax

Revenue Profit before Tax

Source: Company Financials

27

The hydro power project, Bogo Power however, is likely to have contributed positively to the sector, due to high

rainfall levels. The Group re-launched Browns Beach Hotels PLC as Heritance Negombo in April 2016, in an effort to

capitalize on the booming tourism industry in Sri Lanka. Meanwhile, the Group’s Collision Repair Centre, Melsta

Logistics, expects to continue investing in advanced technology to enhance efficiencies as well as expand its facility.

Owing to increasing competition and lower demand for woven fabric, the Group’s textiles company, Texpro

experienced a marginal decline in revenue.

Bogo Power (Pvt) Ltd. was formed to set up a mini hydro plant in Bogowantalawa. A Power Purchase Agreement has

been entered into with the Ceylon Electricity Board for the sale of electricity generated over a period of 20 years.

The project was commissioned in December 2011, with power capacity of 4 MW and annual energy generated of

15.2 GWH. The Group’s Business Process Outsourcing Company, Bellvantage, is a leading brand in the industry.

Splendor Media meanwhile offers marketing communication solutions to its customers and is currently exploring

new opportunities in the industry.

Within the Diversified Sector, the Group also maintains a large investment portfolio which includes strategic and

non-strategic equity, the market value of which amounted to LKR 18.1 Bn, using Volume Weighted Average Share

Price from 15/08/2016 to 23/09/2016 and the shareholdings as at 30th June 2016 (no materials changes to the

shareholdings have taken place as at 23rd September 2016).

Company Shareholdings

(No.'000) WA Price*

(Rs.) Value

(Rs.'000)

ACL Cables PLC 63 62.22 3,920

Aitken Spence Hotel Holdings PLC 23 51.44 1,188

Bukit Darah PLC 72 282.00 20,360

Carson Cumberbatch PLC 29 206.35 6,067

Ceylon Hospitals PLC - Non Voting 136 81.18 11,033

Commercial Bank of Ceylon PLC 28,295 140.16 3,965,900

Commercial Bank of Ceylon PLC - Non Voting 1 117.32 78

CT Holding PLC 1,476 128.19 189,149

DFCC Bank PLC 17,043 130.61 2,226,034

Free Lanka Capital Holdings PLC 2,851 1.27 3,633

Hatton National Bank PLC 10,179 226.75 2,308,044

Haycarb PLC 74 159.07 11,752

Hemas Holdings PLC 100 100.07 10,007

The Kingsbury Hotel PLC 824 16.24 13,376

John Keells Holdings PLC 49,848 153.53 7,653,051

John Keells Holdings PLC - Warrant 2015 2,176 3.69 8,030

John Keells Hotels PLC 529 11.76 6,219

Lanka IOC PLC 30 39.38 1,181

Lanka Milk Foods (CWE) PLC 6,710 123.15 826,360

Nation Trust Bank PLC 50 81.21 4,061

National Development Bank PLC 0 165.41 0

Nestle Lanka PLC 4 2,267.73 9,064

Renuka Agri Foods PLC 6,119 3.25 19,909

SeyLan Bank PLC 10 95.01 950

Softlogic Capital PLC 40,000 6.03 241,226

Softlogic Holdings PLC 380 14.76 5,607

Textured Jersey Lanka PLC 13,512 42.57 575,137

Tokyo Cement PLC 100 55.06 5,506

Vallibal One PLC 121 21.68 2,625

Total 18,129,467

28

3.6 MCRP: Diversified Sector Analysis

The Diversified sector on the Colombo Stock Exchange comprises over 15 listed companies with a total market

capitalization of LKR 456.7 Bn as at 23rd September 2016, accounting for approximately 17% of the total market

capitalization. Sector earnings for the trailing twelve months ending 30th June 2016 amounted to LKR 27.8 Bn and

contributed 13.1% to total earnings during the period.

LKR Mn Market

Cap

Earnings FY16/

FY2016

Shareholder Funds FY16/

FY2016

John Keells Holdings 204,064 14,070 154,982

Transportation, Leisure, Property, Consumer, Financial, IT & Plantation

Hemas Holdings 60,117 2,653 21,992

FMCG, Healthcare, Leisure &Transportation

Carson Cumberbatch 37,471 2,373 41,084

Beverage, Plantation, Oils & Fats, Asset Mgmt, Real Estate, Leisure &Investment Holdings

Aitken Spence 28,298 2,027 36,646

Tourism, Maritime &Logistics, Strategic Investments & Services

C T Holdings 23,345 1,626 18,860

FMCG, Retail &Wholesale Distribution, Restaurants, Real Estate, Entertainment &Banking

Hayleys 21,375 3,004 30,855

Eco Solutions, Hand Protection, Purification, Textiles, Construction Materials, Plantations, Transportation &Logistics, Leisure, Consumer, Power &Energy, Industry Inputs

Vallibel One 22,383 4,228 38,091

Investment, Tiles and Sanitary-ware, Lifestyle & Consumer, Plantation, Banking, Tourism, Healthcare

Richard Pieris And Company 17,094 2,148 10,873

Retail, Plantations, Tyre, Plastic & Furniture, Rubber, Financial Services

Expolanka Holdings 13,293 1,113 11,854

Freight & Logistics, Investments & Services, International Trading & Manufacturing, Leisure

Softlogic Holdings 11,296 722 9,400

Retail, Healthcare, ICT, Financial Services, Automobile, Leisure

Sunshine Holdings 7,298 587 5,782

Healthcare, FMCG, Agribusiness, Power & Energy, Packaging

Browns Investments 4,836 -943 13,991

Leisure, Plantation, Renewable Energy, Construction, Real Estate, Investments

Taprobane Holdings 4,512 -1,742 3,673

Investments, Leisure, Finance, Stock &Money Brokering, Manufacturing, Property, Services

The Colombo Fort Land & Building 3,960 -321 7,611

Trading of Consumer Products & Industrial Products, Leisure, Planations

Dunamis Capital 3,186 -439 781

29

Financial Services, Manufacturing, Real Estate

F L C Holdings 1,642 -216 5,223

Plantation, Power, Leisure &Real Estate

Adam Investments 1,033 -1 1,019

Apparel, Metal, Network Communication & Automobile

Adam Capital 454 2 589

Activated Carbon, Micro Credit

Diversified Sector 456,657 30,891 413,306

* Market capitalization calculated based on 23rd September 2016 share prices

30

3.7 Other Key Events

Amount due from the Secretary to the Treasury on account of Sri Lanka Insurance Corporation (SLIC)

Shares

The Supreme Court of Sri Lanka declared and directed that the shares of SLIC purported to have been sold to

Distilleries Consortium in 2003 along with any shares purchased from employees shall be deemed to have been

held for and on behalf of the Secretary of the Treasury. Consequently, the money that was paid by the Group

subsidiary, Milford Holdings (Pvt) Limited (MHL) to purchase shares from SLIC has been returned. MHL was also

entitled to retain the profits of SLIC derived by MHL during its period of ownership. However, since the value of

profits has not been determined by MHL, no adjustments were made to the financial statements.

Pelwatte Sugar Industries PLC Group (PSIP) affected by the revival of Underperforming Enterprises

and Underutilized Assets Bill

Following the enactment of the Underperforming Enterprises and Underutilized Assets Bill in November 2011,

the state officials occupy the land leased to PSIP and are currently running its operations and related companies.

Subsequently, a compensation tribunal was formed as required by the Act. Without assuming any liability or

without any prejudice to, or impact on its rights, PSIP has submitted a claim to the tribunal. Management is

currently awaiting instructions by the Secretary to the Treasury. Financial results of PSIP up to 30 September

2011 were consolidated to the full year results ending 31 March 2012 however; consolidation has been

suspended due to non-accessibility of the information. The investment in PSIP is classified as a fully impaired

long term investment in the group.

Rights Issue of Shares for Browns Beach Hotels PLC

Browns Beach Hotel PLC (BBH) ceased its operations in March 2011 for the construction of a new resort. The

new resort commenced its operations in April 2016, under Negombo Beach Resorts (Pvt) Ltd, a fully owned

subsidiary of BBH.

The Board of Directors of BBH decided on 23rd August 2016, to issue 54,000,000 ordinary shares by way of a

rights issue subject to the approval of the CSE and shareholders of the Company. The shares are to be issued in

the ratio of 5 new ordinary shares for every 12 ordinary shares held at a consideration of LKR 25.85 per share.

The Company expects to raise approximately LKR 1,395,900,000 as equity capital to invest in its subsidiary,

Negombo Beach Resorts (Private) Limited. The subsidiary would in turn use these funds to reduce the existing

debt levels and finance the project and construction costs of the hotel in Negombo (Heritance Negombo). The

current share price of BBH as of 23rd September 2016 is Rs. 25.00 per share.

31

4.0 MCRP GROUP: FORECASTS AND OUTLOOK POST-RESTRUCTURE

Under the restructuring process being carried out, MCRP will become the ultimate holding company of the former

DIST Group with a 100% stake2, following a share swap. Hence, going forward, MCRP Group will also include the

performance of DIST Alcohol Company.

Hence, FY15 and FY16 figures in this section are of DIST Group while the forecasts are estimates for post-

restructure financials of MCRP Group, which is equivalent to the former DIST Group. Further, it is assumed DIST

Alcohol Company was a fully owned subsidiary of Melstacorp for the entire FY17E (for comparative purposes).

4.1 Revenue

Group (LKR Bn) FY15 FY16 FY17E FY18E FY19E

Gross Revenue 66.8 88.9 98.2 108.3 119.6

YoY Growth (%) 33.1% 10.5% 10.3% 10.4%

Net Revenue 28.9 33.8 37.6 41.5 45.9

YoY Growth (%) 17.0% 11.0% 10.4% 10.7%

Segmental Net Revenue Composition

Beverage 66.2% 71.5% 71.0% 70.9% 70.7%

Plantation 10.4% 7.1% 6.8% 6.8% 6.7%

Telecommunication 12.3% 10.2% 9.3% 8.8% 8.5%

Financial Services 5.0% 6.0% 6.9% 7.6% 8.4%

Diversified 6.1% 5.1% 6.0% 5.9% 5.8%

Segmental Net Revenue YoY Growth

Beverage 26.4% 10.2% 10.2% 10.2%

Plantation -19.6% 6.5% 9.5% 9.5%

Telecommunication -2.7% 0.5% 4.8% 6.6%

Financial Services 40.9% 27.4% 22.1% 21.8%

Diversified -2.2% 30.1% 8.4% 8.6%

We forecast net revenue for the Group of LKR 37.6 Bn in FY17E, up 11.0% YoY, driven by growth in Beverage,

Diversified and Financial Services sectors. Revenue growth over the forecast period is expected at a CAGR of 10.7%

during FY16-19E. On a segmental basis, we expect the Beverage sector to be the largest contributor to revenue in

FY17E, followed by the Telecommunication Sector, accounting for 71.0% and 9.3% of net revenue, respectively.

However, given the changing dynamics within the industries, we expect contribution from Telecommunication

sector to decline to 8.5% of net revenue by FY19E, while we expect the Financial Services sector to increase its

contribution to 8.4% by FY19E, from 6.9% in FY17E.

2 162,164 shares of DIST held by sixty four (64) deceased shareholders and three (3) shareholders who continued to hold their shares ‘in locked balance’ (which were excluded from the off-the-floor share transfer until the beneficiaries of the deceased are registered in the Register of DIST/ shares are transferred to the ‘trading balance’) are considered as held in trust for MCRP in consideration of the 648,656 MCRP shares allotted to those shareholders for the transfer of their DIST shares in terms of the ‘Arrangement’ (now held in trust).

32

4.2 Beverage Sector

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Net Revenue 19.1 24.2 26.7 29.4 32.4

YoY Growth (%) 1.1% 26.4% 10.2% 10.2% 10.2%

Volume Growth (Proof Liters) (%) -9.2% 11.8% 4.0% 4.0% 4.0%

Growth in Net Revenue per Proof Liter (%) 11.4% 13.1% 6.0% 6.0% 6.0%

Direct Turnover Taxes as a % of Gross Revenue 66.4% 69.4% 69.4% 69.4% 69.4%

The Beverage sector is expected to generate net revenue of LKR 26.7 Bn in FY17E, increasing 10.2% YoY. Growth in

FY17E is owing to volume growth of 4.0% and net revenue per proof liter growth of 6.0%. Revenue is expected to

reach LKR 32.4 Bn in FY19E, as it grows at a CAGR of 10.2%. We expect volume growth to continue at a moderate

level of 4.0% on average during FY17E-19E, while we assume growth in net revenue per proof liter would be at 6.0%

during the same period. We have not explicitly forecasted the increase in direct turnover related taxes, however, it

is expected that the current tax structure would continue.

The DIST Alcohol Company is expected to generate net revenue of LKR 23.7 Bn in FY17E increasing 10.2% YoY. We

expect DIST’s market share to remain at its current level of approximately 68.0% throughout the forecast period.

We expect DIST Alcohol Company to report net revenue of LKR 28.9 Bn in FY19E, growing at a CAGR of 10.2% during

the period FY16-19E.

4.3 Plantation Sector

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Net Revenue 3.0 2.4 2.6 2.8 3.1

YoY Growth (%) -19.6% 6.5% 9.5% 9.5%

Tea Revenue 2.8 2.2 2.4 2.6 2.9

Rubber Revenue 0.2 0.2 0.2 0.2 0.2

The Plantation sector recorded a significant decline in revenue of 19.6% YoY to LKR 2.4 Bn in FY16 continuing the

downward trend for the second consecutive year. We estimate revenue of LKR 2.6 Bn in FY17E an increase of 6.5%

YoY. Tea accounted for approximately 93.0% of total revenue for the sector in FY16, while the remainder was a

contribution from Rubber. In our forecasts, we assume the contribution from Tea would continue to increase while

the contribution from Rubber is expected to decline.

Revenue growth is expected to be driven by a 5.8% YoY increase in Tea to LKR 2.4 Bn in FY17E combined with a

15.8% YoY increase in Rubber to LKR 0.2 Bn. Growth in the Tea segment is owing to a potential recovery in NSA,

given the upward trend seen during the latter half of 2016. Total net revenue is estimated to grow at a CAGR of 8.5%

over the period FY16-19E with revenue from Tea and Rubber expected to record growth at a CAGR of 8.7% and 5.6%,

respectively.

33

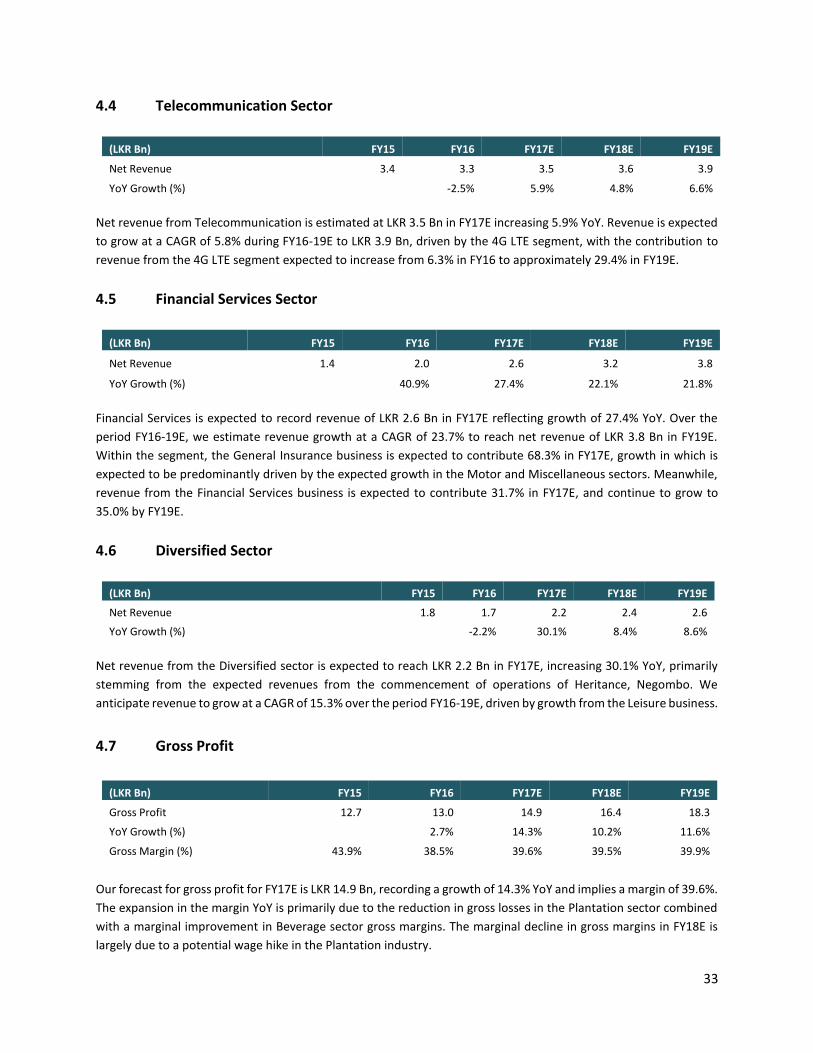

4.4 Telecommunication Sector

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Net Revenue 3.4 3.3 3.5 3.6 3.9

YoY Growth (%) -2.5% 5.9% 4.8% 6.6%

Net revenue from Telecommunication is estimated at LKR 3.5 Bn in FY17E increasing 5.9% YoY. Revenue is expected

to grow at a CAGR of 5.8% during FY16-19E to LKR 3.9 Bn, driven by the 4G LTE segment, with the contribution to

revenue from the 4G LTE segment expected to increase from 6.3% in FY16 to approximately 29.4% in FY19E.

4.5 Financial Services Sector

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Net Revenue 1.4 2.0 2.6 3.2 3.8

YoY Growth (%) 40.9% 27.4% 22.1% 21.8%

Financial Services is expected to record revenue of LKR 2.6 Bn in FY17E reflecting growth of 27.4% YoY. Over the

period FY16-19E, we estimate revenue growth at a CAGR of 23.7% to reach net revenue of LKR 3.8 Bn in FY19E.

Within the segment, the General Insurance business is expected to contribute 68.3% in FY17E, growth in which is

expected to be predominantly driven by the expected growth in the Motor and Miscellaneous sectors. Meanwhile,

revenue from the Financial Services business is expected to contribute 31.7% in FY17E, and continue to grow to

35.0% by FY19E.

4.6 Diversified Sector

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Net Revenue 1.8 1.7 2.2 2.4 2.6

YoY Growth (%) -2.2% 30.1% 8.4% 8.6%

Net revenue from the Diversified sector is expected to reach LKR 2.2 Bn in FY17E, increasing 30.1% YoY, primarily

stemming from the expected revenues from the commencement of operations of Heritance, Negombo. We

anticipate revenue to grow at a CAGR of 15.3% over the period FY16-19E, driven by growth from the Leisure business.

4.7 Gross Profit

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Gross Profit 12.7 13.0 14.9 16.4 18.3

YoY Growth (%) 2.7% 14.3% 10.2% 11.6%

Gross Margin (%) 43.9% 38.5% 39.6% 39.5% 39.9%

Our forecast for gross profit for FY17E is LKR 14.9 Bn, recording a growth of 14.3% YoY and implies a margin of 39.6%.

The expansion in the margin YoY is primarily due to the reduction in gross losses in the Plantation sector combined

with a marginal improvement in Beverage sector gross margins. The marginal decline in gross margins in FY18E is

largely due to a potential wage hike in the Plantation industry.

34

We forecast a gross margin of 42.8% for DIST Alcohol Company in FY17E, stable from that of the previous year and

improve to 43.0% by FY19E. Average gross profit growth over the forecast period for MCRP Group and DIST Alcohol

Company are 12.0% and 10.4% respectively, over the period FY17-19E. Gross margin over FY17-19E is expected to

average 39.7% for MCRP Group over the forecast period.

4.8 Other Operating Income

We have not forecasted dividend income from financial assets and gains/losses from disposal of financial assets. The

current market value of the respective financial assets has instead been considered for our Sum-of-the-Parts (SOTP)

valuation. Our forecast with the exception of the above amounts to LKR 0.4 Bn in FY17E, which is broadly in line with

that of the previous year. Other operating income is expected to remain at the same levels over the forecast period,

with operating income as a percentage of net revenue is assumed at 1.0%.

4.9 Operating Expenses

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Distribution Expenses 1.7 1.8 1.9 2.0 2.2

As a % of Net Revenue 5.9% 5.2% 4.9% 4.8% 4.7%

Administrative Expenses 3.8 3.6 4.2 4.6 4.7

YoY Growth (%) -6.0% 17.9% 7.1% 3.9%

Other Operating Expenses 0.0 0.4 0.1 0.2 0.2

As a % of Net Revenue 0.1% 1.0% 0.3% 0.4% 0.5%

Distribution costs are expected to increase 4.7% YoY to reach LKR 1.9 Bn in FY17E and expected to grow to LKR 2.2

Bn in FY19E. We assume distribution costs would average 4.8% of net revenue over the forecast period, declining

from 5.2% in FY16. Administration costs for FY17E are estimated at LKR 4.2 Bn, increasing 17.9% from the previous

year mainly due to the commencement of operations of Heritance Negombo, while it is expected to grow at a 3-year

CAGR of 9.5% to LKR 4.7 Bn in FY19E. Other Operating Expenses amounted to LKR 0.4 Bn in FY16, and we expect this

to decline to LKR 0.1 Bn in FY17E. Operating expenses as a percentage of net revenue is expected to average 0.4%

during FY17-21E.

35

4.10 EBIT

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Recurring EBIT 8.5 8.4 9.0 10.1 11.7

YoY Growth (%) -0.4% 7.0% 11.9% 15.2%

EBIT Margin (%) 29.3% 25.0% 24.1% 24.4% 25.4%

Comparable EBIT 7.7 7.7 9.0 10.1 11.7

YoY Growth (%) -0.1% 17.7% 11.9% 15.2%

EBIT Margin (%) 26.6% 22.7% 24.1% 24.4% 25.4%

Our estimate for recurring EBIT is LKR 9.0 Bn in FY17E, implying a margin of 24.1%, while we expect EBIT to grow at

a CAGR of 11.3% over the period FY16-19E. Margin decline in FY17E is owing to losses stemming from the newly

commenced hotel, Heritance Negombo. EBIT margin for the forecast period is expected to average 24.6%. Margin

expansion in FY19E is from Heritance Negombo generating profits coupled with improvement in Beverage sector

gross margins.

Comparable EBIT excludes investment income from the Group’s investment portfolio, and is expected to amount to

LKR 9.0 Bn in FY17E and increase to LKR 11.7 Bn by FY19E. Comparable EBIT margins are expected to average 24.6%

over the period FY17-19E, increasing from 22.7% in FY16.

4.11 Net Finance Costs

(LKR Bn) FY17E FY18E FY19E

Finance Income 0.3 0.5 0.7

Finance Cost (1.0) (1.3) (1.5)

Net Finance Cost (0.7) (0.7) (0.7)

Total Debt 17.8 21.0 24.2

Equity attributable to Shareholders 67.7 73.4 79.8

Debt to Equity (x) 0.25 0.28 0.29

Effective Finance Cost (%) 6.5% 6.5% 6.5%

Net finance cost for FY16 amounted to LKR 0.2 Bn, and we expect this to increase to LKR 0.7 Bn in FY17E due to

higher effective finance cost and debt. Total debt for the Group is forecasted to be LKR 17.8 Bn in FY17E, increasing

to LKR 24.2 Bn by FY19E. Net debt for the Group is estimated at LKR 11.5 Bn in FY17E declining to LKR 9.1 Bn by

FY19E, given the generation of operating cash flow. We expect the effective finance cost would remain at 6.5%

throughout the forecast period. Our forecast for debt to equity for FY17E is 0.25x, and we estimate an average debt

to equity of 0.27x over the forecast period.

36

4.12 Share of Associate Profits

We expect the share of associate profits to amount to LKR 1.1 Bn in FY17E, increasing from LKR 0.7 Bn in the previous

year, primarily driven by a renewed power purchasing agreement with the Ceylon Electricity Board for one year

through SPEN (Ace Power Embilipitiya (Pvt) Ltd). The contribution from SPEN is forecasted at LKR 1.1 Bn for the year

increasing from LKR 0.9 Bn, while we expect a negative contribution from MADU, owing to weakness in the

plantation industry. The contribution from SPEN is expected to increase to LKR 1.4 Bn by FY19E, driven by the tourism

sector. Total share of associate profits is expected to increase to LKR 1.3 Bn by FY19E.

4.13 Profit before Tax

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Share of Associate Profits 1.4 0.7 1.1 1.1 1.3

Profit Before Tax 9.7 9.0 9.4 10.5 12.3

YoY Growth (%) -7.6% 4.6% 11.7% 16.8%

PBT Margin (%) 33.6% 26.6% 25.0% 25.3% 26.8%

Comparable PBT 8.9 8.2 9.4 10.5 12.3

YoY Growth (%) -1.2% -7.9% 14.4% 11.7% 16.8%

PBT Margin (%) 30.9% 24.3% 25.0% 25.3% 26.8%

Segmental PBT (excl. associate profits)

Beverage 8.4 8.4 8.9 10.2 11.5

Plantation (0.1) (0.4) (0.2) (0.3) (0.3)

Telecommunication (0.7) (0.6) (0.8) (0.9) (0.9)

Financial Services 0.2 0.2 0.3 0.4 0.5

Diversified 0.5 0.7 0.1 0.1 0.0

The Group is forecasted to record PBT of LKR 9.4 Bn in FY17E, up 4.6% YoY. PBT is expected to grow at a CAGR of

10.9% to reach LKR 12.3 Bn in FY19E. We expect PBT margins to range from 25.0% – 26.8% during the forecast period

FY17-19E, and average 25.7%. Comparable PBT for FY17E is expected to amount to LKR 9.4 Bn increasing from LKR

8.2 Bn in the previous year, with PBT margins improving to 25.0% in FY17E from 24.3%. Growth in PBT is driven by

the leisure business turning profitable in FY19E.

On a segmental basis, the Beverage sector is expected to earn PBT of LKR 8.9 Bn in FY17E, increasing from LKR 8.4

Bn in the previous year. The Beverage sector PBT margin is expected to be 33.5% in FY17E declining from 34.7% in

the previous year as other operating income has not been forecasted. We expect Beverage sector PBT to grow at a

3-year CAGR of 11.2% during FY16-19E to reach LKR 11.5 Bn by FY19E based on improvement in gross margins which

benefited from lower depreciation and lower growth in administration expenses following the recently completed

restructure. PBT margins are expected to range between 33.5% - 35.6% over this period. The DIST Alcohol Company

is forecasted to record PBT of LKR 7.0 Bn in FY17E and increase to LKR 10.5 Bn in FY19E. The PBT margins for DIST

Alcohol Company are expected to range from 33.9% - 36.2% during FY17-19E.

37

Given the weak supply side factors, we do not expect a turnaround in the Plantations sector in the near term. As

such, we forecast a loss before tax of LKR 0.19 Bn in FY17E and expect it to record an average loss before tax of LKR

0.27 Bn over the period FY17-19E. It is expected that there would be a wage hike in FY18E, which would not be paid

in arrears, which is likely to hamper profitability further.

Despite the expectation of the Telecommunication sector recording growth in revenue, we believe the sector losses

before tax would continue to expand during the forecast period. We estimate a loss before tax of LKR 0.77 Bn in

FY17E, while a loss of LKR 0.85 Bn is expected on average over the years FY17-19E due to increasing operating and

finance costs. We do not expect the company to record a turnaround during the forecast period.

Profit before tax for Financial Services is estimated at LKR 0.3 Bn for FY17E, reflecting growth of 9.4% YoY. We expect

PBT to continue to record growth at a CAGR of 27.8% over the forecast period. The General Insurance business is

expected to contribute 57.9% to PBT in FY17E, while the financial services company is expected to contribute the

remaining. Continental Insurance is expected to record underwriting profits by FY18E. PBT margin for FY17E is

expected to be 9.9%, declining from the prior year due to the increased claims stemming from the floods which took

place in May 2016. Margins are expected to average 11.3% during FY17-19E.

The Diversified sector income consists of dividend and gains/losses on disposal of financial investments, which we

have not forecasted and instead have used the current market value for our SOTP valuations. Over our forecast

period, we expect the profit before tax to average LKR 0.06 Bn.

4.14 Net Profit attributable to Equity Holders

(LKR Bn) FY15 FY16 FY17E FY18E FY19E

Taxation 3.3 3.3 3.5 3.9 4.5