andrew d. cotlar your tool box for mortgage foreclosure

TRANSCRIPT

11

Andrew D. CotlarAndrew D. Cotlar

Your Tool Box for Mortgage Your Tool Box for Mortgage Foreclosure Defense V 2.0Foreclosure Defense V 2.0

Andrew D. Cotlar, Esq.Andrew D. Cotlar, Esq.Cotlar & CotlarCotlar & Cotlar23 West. Court St.23 West. Court St.Doylestown, PA 18901Doylestown, PA 18901

Tel: 215Tel: 215--345345--73107310Email: Email: [email protected]@hotmail.com

www.cotlarlaw.comwww.cotlarlaw.com

22

A Massive ReA Massive Re--Allocation of Allocation of WealthWealth

But a many a starving farmerBut a many a starving farmerThe same old story toldThe same old story toldHow the outlaw paid their mortgageHow the outlaw paid their mortgageAnd saved their little homes.And saved their little homes.……Yes, as through this world I've wanderedYes, as through this world I've wanderedI've seen lots of funny men;I've seen lots of funny men;Some will rob you with a sixSome will rob you with a six--gun,gun,And some with a fountain pen.And some with a fountain pen.

And as through your life you travel,And as through your life you travel,Yes, as through your life you roam,Yes, as through your life you roam,You won't never see an outlawYou won't never see an outlawDrive a family from their home.Drive a family from their home.

--Woody Guthrie, Pretty Boy FloydWoody Guthrie, Pretty Boy Floyd

33

TodayToday’’s Goalss Goals

Provide tools to handle a foreclosure Provide tools to handle a foreclosure defensedefense

Honorably and fairlyHonorably and fairly

Without losing money Without losing money

Based on my experience as general Based on my experience as general practitioner in Pennsylvaniapractitioner in Pennsylvania

44

Our Game Plan TodayOur Game Plan Today

Basic VocabularyBasic Vocabulary

Background/ overview of processBackground/ overview of process

Legal backgroundLegal background

How to get paidHow to get paid

Initial Interview; getting startedInitial Interview; getting started

Answer and CounterclaimsAnswer and Counterclaims

What if thereWhat if there’’s a default?s a default?

DiscoveryDiscovery

BankruptcyBankruptcy

Settled solutionsSettled solutions

HAMP Overview and Enforcing Loan ModificationsHAMP Overview and Enforcing Loan Modifications

55

DisclaimerDisclaimer

Limited to PA law and my experience Limited to PA law and my experience here. here.

No claim to provide legal analysis of your No claim to provide legal analysis of your local jurisdiction if not Pennsylvania.local jurisdiction if not Pennsylvania.

But, if itBut, if it’’s a judicial foreclosure state, your s a judicial foreclosure state, your laws may be similar to ours.laws may be similar to ours.

Know your own jurisdictionKnow your own jurisdiction’’s laws and s laws and procedures. procedures.

66

Basic VocabularyBasic Vocabulary

NotesNotes

MortgagesMortgages

DeedsDeeds

AssignmentsAssignments

Loan Modification AgreementLoan Modification Agreement

Reinstatement LetterReinstatement Letter

Payoff quotePayoff quote

Foreclosure Complaint (in rem action)Foreclosure Complaint (in rem action)

77

The Economic SituationThe Economic Situation

Woody Guthrie would be appalledWoody Guthrie would be appalled

Mortgages bought and sold on marketMortgages bought and sold on market

““TranchesTranches””

Foreclosures driven by hidden Foreclosures driven by hidden investors with minimal riskinvestors with minimal risk

Investments as a whole are insuredInvestments as a whole are insured

What triggered 2008 recessionWhat triggered 2008 recession

88

The Economic SituationThe Economic Situation

Many lenders use servicers as intermediariesMany lenders use servicers as intermediaries

Manage payments, escrow, and send delinquency Manage payments, escrow, and send delinquency noticesnotices

Foreclosure direction sent to specialist firmsForeclosure direction sent to specialist firms

Little direct contact with their client Little direct contact with their client

Lenders Processing Service and similar computer Lenders Processing Service and similar computer interactioninteraction

Source of frustration, delay and lack of communication Source of frustration, delay and lack of communication on unusual issueson unusual issues

Foreclosure firms get paid minimal amount per task Foreclosure firms get paid minimal amount per task

99

Why are homeowners Why are homeowners delinquent?delinquent?

Lost jobsLost jobs

Medical emergency and no insuranceMedical emergency and no insurance

DivorceDivorce

ProfligacyProfligacy

Unexpected sudden debtsUnexpected sudden debts

Predatory lending (more later)Predatory lending (more later)

1010

Foreclosure crisis: local Foreclosure crisis: local filings and national focusfilings and national focus

FederallyFederally--sponsored attempts to encourage loan sponsored attempts to encourage loan modifications have largely failedmodifications have largely failed

Troubled Asset Relief ProgramTroubled Asset Relief Program

HAMP HAMP

Positive and negative reports from different sidesPositive and negative reports from different sides

Thousands of local filings each year in Bucks County Thousands of local filings each year in Bucks County alonealone

Competing values: families v. investmentsCompeting values: families v. investments

No No ““pot of goldpot of gold”” for attorneysfor attorneys

Many defendants are pro seMany defendants are pro se

1111

The Foreclosure Process in PA If The Foreclosure Process in PA If You DefendYou Defend

2 months of arrearages2 months of arrearages

Act 91 NoticeAct 91 Notice

30 day extension if you consult with credit counselors and apply30 day extension if you consult with credit counselors and apply for for emergency loansemergency loans

Foreclosure Complaint filedForeclosure Complaint filed

Mediation program in various countiesMediation program in various counties

Answer filed (or default judgment if no answer)Answer filed (or default judgment if no answer)

Foreclosing attorney lists for trial if answer filedForeclosing attorney lists for trial if answer filed

Obtain judgment at trialObtain judgment at trial

Schedule SheriffSchedule Sheriff’’s sales sale

May be several adjournments of SheriffMay be several adjournments of Sheriff’’s sales sale

SheriffSheriff’’s sale held; deposits mades sale held; deposits made

SheriffSheriff’’s deed issued and transfer of property at Settlements deed issued and transfer of property at Settlement

Separate action in ejectment if necessarySeparate action in ejectment if necessary

1212

The Legal BackgroundThe Legal Background

Truth in Lending ActTruth in Lending Act, 15 USC 1601 et seq., 15 USC 1601 et seq.

Private right of action for actual damages and 2x Private right of action for actual damages and 2x finance charges, rights of rescissions, costs and finance charges, rights of rescissions, costs and attorneyattorney’’s fees.s fees.

1 year statute of limitation from closing, but you 1 year statute of limitation from closing, but you can assert it as a defense to foreclosure at any can assert it as a defense to foreclosure at any time.time.

Details are specified at Federal Reserve Board Details are specified at Federal Reserve Board Regulation ZRegulation Z

Basic concept: All fees must be disclosed and Basic concept: All fees must be disclosed and cannot be excessive.cannot be excessive.

33--day right of rescission must be givenday right of rescission must be given

1313

The Legal BackgroundThe Legal Background

Real Estate Settlement and Procedures Real Estate Settlement and Procedures ActAct, 12 U.S.C. 2601 et. seq., 12 U.S.C. 2601 et. seq.

Implemented by Federal Reserve Board Implemented by Federal Reserve Board Regulation XRegulation X

Private right of action for damages, attorneys Private right of action for damages, attorneys fees and costsfees and costs

3 year statute of limitations3 year statute of limitations

Prohibits kickbacks, unearned fees, etcProhibits kickbacks, unearned fees, etc

Requires HUD sheet to be accurateRequires HUD sheet to be accurate

1414

The Legal BackgroundThe Legal Background

Pennsylvania Act 91Pennsylvania Act 91, 35 P.S. , 35 P.S. 1690.401c et seq.1690.401c et seq.

Requires advance written notice of arrears with Requires advance written notice of arrears with name of lender, amount to cure, and list of name of lender, amount to cure, and list of credit counseling agencies in your county.credit counseling agencies in your county.

No private right of actionNo private right of action

Violations of notice provisions are a defense to Violations of notice provisions are a defense to foreclosure actionsforeclosure actions

Court will dismiss without prejudice to refileCourt will dismiss without prejudice to refile

Temporary delayTemporary delay

1515

The Legal BackgroundThe Legal Background

Pennsylvania Act 6,Pennsylvania Act 6, Loan Interest and Loan Interest and Protection Law of 1974, 41 PS 101 et seq.Protection Law of 1974, 41 PS 101 et seq.

Limited to home loans $50k and belowLimited to home loans $50k and below

AntiAnti--usury law requiring notices prior to usury law requiring notices prior to foreclosureforeclosure

Independent private right of actionIndependent private right of action

Plaintiff can recover excessive interest x3, costs Plaintiff can recover excessive interest x3, costs and attorney feesand attorney fees

Statute of limitations is 4 yearsStatute of limitations is 4 years

Lots of exceptions; big one is for national banks, Lots of exceptions; big one is for national banks, which follow more favorable federal lawwhich follow more favorable federal law

1616

The Legal BackgroundThe Legal Background

Pennsylvania Mortgage Bankers and Pennsylvania Mortgage Bankers and Brokers and Consumer Equity Brokers and Consumer Equity Protection ActProtection Act, 63 PS 456.101 et. seq., 63 PS 456.101 et. seq.

Lots of restrictions on balloon rates, Lots of restrictions on balloon rates, negative amortization, etc.negative amortization, etc.

Applies to principal less than $100kApplies to principal less than $100k

No private right of actionNo private right of action

DoesnDoesn’’t apply to assigns of the loanst apply to assigns of the loans

1717

The Legal BackgroundThe Legal Background

Fair Debt Collections Practices Act,Fair Debt Collections Practices Act, 15 U.S.C. 1692 15 U.S.C. 1692 et seq.et seq.

Prohibits abusive debt collection by debt collectorsProhibits abusive debt collection by debt collectors

PA Fair Credit Extension Uniformity ActPA Fair Credit Extension Uniformity Act

Nearly identical protections and covers debt collectors AND Nearly identical protections and covers debt collectors AND creditors in PA. 73 P.S. creditors in PA. 73 P.S. §§ 2270.2 et seq.2270.2 et seq.

PA Unfair Trade Practices and Consumer Protection PA Unfair Trade Practices and Consumer Protection LawLaw

Staple in litigation; 3x damages, costs and attorney feesStaple in litigation; 3x damages, costs and attorney fees

Applies to mortgage loansApplies to mortgage loans

Must prove elements of fraud or deceptionMust prove elements of fraud or deception

1818

The Legal BackgroundThe Legal Background

Common law torts,Common law torts, e.g. fraud, e.g. fraud, misrepresentation, etc.misrepresentation, etc.

Contract defenses (e.g. duty of good faith Contract defenses (e.g. duty of good faith and fair dealing)and fair dealing)

1919

The Legal Background:The Legal Background: special notespecial note

Federal Courts canFederal Courts can’’t issue injunctions (Antit issue injunctions (Anti-- injunction Act), so doninjunction Act), so don’’t bother to sue in t bother to sue in Federal Court and expect the court to enjoin Federal Court and expect the court to enjoin the foreclosure.the foreclosure.

2020

So a client is in your So a client is in your office...How to Get Paidoffice...How to Get Paid

UpUp--front payment is possible: flat rate or hourly drawn upon front payment is possible: flat rate or hourly drawn upon nonnon--refundable retainerrefundable retainer

Or combination of the two with credit for amounts paidOr combination of the two with credit for amounts paid

NB: FTC rules, 16 CFR 322.7: NB: FTC rules, 16 CFR 322.7:

Option 1: Collect an advance fee, place it in your escrow Option 1: Collect an advance fee, place it in your escrow account and draw upon it on an hourly basis.account and draw upon it on an hourly basis.

Option 2: Charge an advance flat fee and make it clear the fee Option 2: Charge an advance flat fee and make it clear the fee is earned upon receipt.is earned upon receipt.

No flat fees collected for not actually providing legal work.No flat fees collected for not actually providing legal work.

Therefore, BEWARE of companies that want to affiliate with Therefore, BEWARE of companies that want to affiliate with you to avoid the scope of state or federal regulations.you to avoid the scope of state or federal regulations.

2121

How to Get Paid: How to Get Paid: What Not to DoWhat Not to Do

DonDon’’t take an adverse interest in your clientt take an adverse interest in your client’’s s property (ethics)property (ethics)

Example: forcing your client to take out a Example: forcing your client to take out a second mortgage to guaranty payment second mortgage to guaranty payment (Florida attorney)(Florida attorney)

Example: client sells property to straw buyer Example: client sells property to straw buyer with whom you have any relationship with whom you have any relationship (Bennett and Dougherty PA criminal (Bennett and Dougherty PA criminal conviction)conviction)

DonDon’’t make promises you cant make promises you can’’t keept keep

Give client a reality checkGive client a reality check

2222

A Client Walks into Your A Client Walks into Your Office... What you need to Office... What you need to collectcollect

All correspondenceAll correspondence

All notes re any All notes re any conversationsconversations with lender with lender representatives:representatives:

All settlement documentsAll settlement documents

Copy of complaint and attachmentsCopy of complaint and attachments

Mortgage & noteMortgage & note

Other recorded mortgages and Other recorded mortgages and

Any assignments referenced in complaintAny assignments referenced in complaint

Other loans not in foreclosureOther loans not in foreclosure

Other possible liensOther possible liens

Paystubs and taxesPaystubs and taxes

2323

Review the ComplaintReview the Complaint

Does Plaintiff have Does Plaintiff have standingstanding??

E.g. Bank of NY, Deutsche Bank, Trustees E.g. Bank of NY, Deutsche Bank, Trustees for investment trustsfor investment trusts

Assignment dates, names, places, etc.Assignment dates, names, places, etc.

Websites with lists of robosignersWebsites with lists of robosigners

Statement that assignments are in process Statement that assignments are in process of being formalized is allowed. of being formalized is allowed. U.S. Bank U.S. Bank v. Malloryv. Mallory, 2009 PA Super 182; 982 A.2d , 2009 PA Super 182; 982 A.2d 986 (Pa. Super. 2009)986 (Pa. Super. 2009)

2424

Review the ComplaintReview the Complaint

Who verified the complaint?Who verified the complaint?

Party?Party?

Attorney?Attorney?

Helps you focus on who to depose if need Helps you focus on who to depose if need bebe

2525

Review the ComplaintReview the Complaint

Mortgage Electronic Registration Systems (MERS). Mortgage Electronic Registration Systems (MERS). What is it?What is it?

See Michael Powell and Gretchen Morgenson, See Michael Powell and Gretchen Morgenson, ““MERS? It MERS? It May Have Swallowed Your Loan,May Have Swallowed Your Loan,”” New York Times (March New York Times (March 5, 2011).5, 2011).

Nothing inherently wrong with MERS being assignor. See Nothing inherently wrong with MERS being assignor. See See See Mortg. Elec. Registration Sys. v. RalichMortg. Elec. Registration Sys. v. Ralich, 982 A.2d 77, , 982 A.2d 77, 81 (Pa. Super. 2009).81 (Pa. Super. 2009).

But through discovery you may want to explore whether But through discovery you may want to explore whether MERS vice presidents really exist as a matter of fact (robo MERS vice presidents really exist as a matter of fact (robo signers)signers)

Lenders, servicers and foreclosure firms pay for staff to be Lenders, servicers and foreclosure firms pay for staff to be Vice President with MERS on temporary basisVice President with MERS on temporary basis

2626

Review the ComplaintReview the Complaint

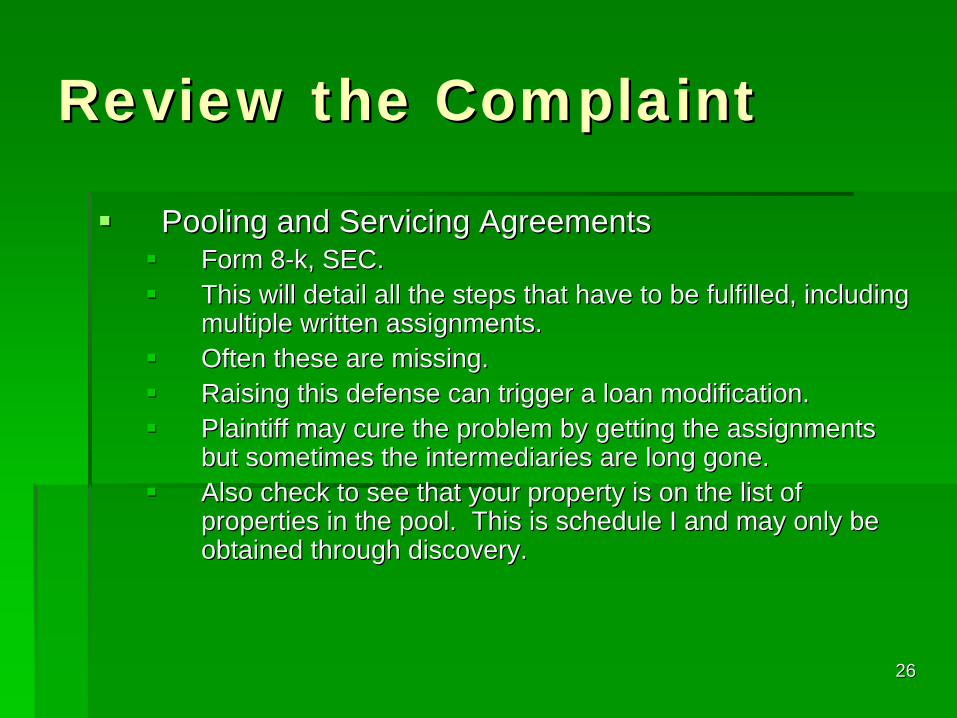

Pooling and Servicing AgreementsPooling and Servicing Agreements

Form 8Form 8--k, SEC. k, SEC.

This will detail all the steps that have to be fulfilled, includThis will detail all the steps that have to be fulfilled, including ing multiple written assignments. multiple written assignments.

Often these are missing. Often these are missing.

Raising this defense can trigger a loan modification. Raising this defense can trigger a loan modification.

Plaintiff may cure the problem by getting the assignments Plaintiff may cure the problem by getting the assignments but sometimes the intermediaries are long gone.but sometimes the intermediaries are long gone.

Also check to see that your property is on the list of Also check to see that your property is on the list of properties in the pool. This is schedule I and may only be properties in the pool. This is schedule I and may only be obtained through discovery.obtained through discovery.

2727

Review the ComplaintReview the Complaint

Proper Act 91 Notices? List of credit Proper Act 91 Notices? List of credit counseling agencies in the county.counseling agencies in the county.

Needs to be attached to complaint in PANeeds to be attached to complaint in PA

This This waswas a jurisdictional requirement! a jurisdictional requirement!

Beneficial v. Vukmam, 2012 PA Super 18; 37 A.3d 596 (Pa. Super. 2012) (superseded by statute)

But see Act 70, 2012, S.B. 1433: not jurisdictional But see Act 70, 2012, S.B. 1433: not jurisdictional but still a good defense and case can be dismissed but still a good defense and case can be dismissed w/o prejudice until notice is providedw/o prejudice until notice is provided

Good for delay onlyGood for delay only

2828

Review the ComplaintReview the Complaint

Review the numbers for inaccuraciesReview the numbers for inaccuracies

Amount of arrearsAmount of arrears

Excessive attorney feesExcessive attorney fees

Mysterious other fees/costsMysterious other fees/costs

Dates of arrearsDates of arrears

Interest rate, interest rate capsInterest rate, interest rate caps

Compare to mortgage and noteCompare to mortgage and note

2929

Answering the Complaint:Answering the Complaint: Duty of good faith and fair Duty of good faith and fair dealingdealing

Gather information on clientGather information on client--lender interactionslender interactions

See, e.g. NV and AZ AG complaints against Bank of See, e.g. NV and AZ AG complaints against Bank of America. Great detailed examples of bad faith:America. Great detailed examples of bad faith:

Assurances of no foreclosure pending loan modification Assurances of no foreclosure pending loan modification discussions when proceeding with foreclosure anyway;discussions when proceeding with foreclosure anyway;

Falsely telling customers they must be in default to obtain a Falsely telling customers they must be in default to obtain a modification;modification;

Promising to make loan modifications permanent only to Promising to make loan modifications permanent only to renege on the deal;renege on the deal;

Conjuring bogus reasons for denying modifications. Conjuring bogus reasons for denying modifications. (Andrew Martin and Michael Powell, (Andrew Martin and Michael Powell, ““Two States Sue Bank Two States Sue Bank of America Over Mortgages,of America Over Mortgages,”” New York Times, Dec. 17, New York Times, Dec. 17, 2010)2010)

3030

Answering the Complaint:Answering the Complaint: Duty of good faith and fair Duty of good faith and fair dealingdealing

Inherent in every PA contract:Inherent in every PA contract:

““Section 205 of the Restatement (Second) of ContractsSection 205 of the Restatement (Second) of Contracts suggests suggests that "[e]very contract imposes upon each party a duty of good fathat "[e]very contract imposes upon each party a duty of good faith ith and fair dealing in its performance and its enforcement." and fair dealing in its performance and its enforcement." Creeger Creeger Brick and Building Supply, Inc. v. MidBrick and Building Supply, Inc. v. Mid--State BankState Bank, 385 Pa. Super. , 385 Pa. Super. 30; 560 A.2d 151, 153 (Pa. Super. 1989).30; 560 A.2d 151, 153 (Pa. Super. 1989).

Fleet Real Estate Funding Corp. v. SmithFleet Real Estate Funding Corp. v. Smith, 530 A.2d 919 (Pa. , 530 A.2d 919 (Pa. Super. 1987) (lenderSuper. 1987) (lender’’s refusal to cooperate with homeowners refusal to cooperate with homeowner’’s s request to negotiate payments constitutes breach of duty of goodrequest to negotiate payments constitutes breach of duty of good faith and fair dealing when HUD guidelines for FHA insured faith and fair dealing when HUD guidelines for FHA insured mortgage not followed); mortgage not followed);

Commonwealth School EmployeeCommonwealth School Employee’’s Retirement Fund v. Terrells Retirement Fund v. Terrell, , 582 A.2d 367 (Pa. super, 1990) (lender582 A.2d 367 (Pa. super, 1990) (lender’’s failure to properly s failure to properly service loan was breach of duty of good faith and fair dealing);service loan was breach of duty of good faith and fair dealing); Union National Bank of Little Rock v. CobbsUnion National Bank of Little Rock v. Cobbs, 567 A.2d 719 (Pa. , 567 A.2d 719 (Pa. Super, 1989) (same). Super, 1989) (same).

3131

Answering the Complaint:Answering the Complaint: Duty of good faith and fair Duty of good faith and fair dealingdealing

HAMP participating lenders have additional dutiesHAMP participating lenders have additional duties

See their service agreement and HAMP guidelines (U.S. See their service agreement and HAMP guidelines (U.S. Treasury)Treasury)

For latest version of Making Home Affordable Handbook, see For latest version of Making Home Affordable Handbook, see https://www.hmpadmin.com/portal/programs/guidance.jsphttps://www.hmpadmin.com/portal/programs/guidance.jsp. (now . (now v 5.0)v 5.0)

Frequently updated.Frequently updated.

Prohibits moving forward with foreclosure while evaluating loss Prohibits moving forward with foreclosure while evaluating loss mitigation measures like loan modificationsmitigation measures like loan modifications

Rules on how to evaluate a loan modificationRules on how to evaluate a loan modification

No private right of action to enforce, but this may be good basiNo private right of action to enforce, but this may be good basis s for establishing an implied duty contractuallyfor establishing an implied duty contractually

3232

Answering the ComplaintAnswering the Complaint

REMEMBER: just filing an answer will REMEMBER: just filing an answer will buy your client lots of time. buy your client lots of time.

The file goes to the bottom of the very The file goes to the bottom of the very busy foreclosure attorneybusy foreclosure attorney’’s pile.s pile.

If you donIf you don’’t file an answer, you risk t file an answer, you risk default and malpractice.default and malpractice.

3333

Answer the Complaint: Answer the Complaint: what not to dowhat not to do

Do NOT use the following language regarding the arrears paragrapDo NOT use the following language regarding the arrears paragraph, h, taken from Pa. R.C.P. 1029(c), if you can help it:taken from Pa. R.C.P. 1029(c), if you can help it:

After reasonable investigation, Defendant is without knowledge oAfter reasonable investigation, Defendant is without knowledge or information r information sufficient to form a belief as to the truth or accuracy of the asufficient to form a belief as to the truth or accuracy of the allegation/averment and llegation/averment and therefore said allegation/averment is denied. Strict proof is rtherefore said allegation/averment is denied. Strict proof is required at trial.equired at trial.

First Wis. Trust Co v. StrausserFirst Wis. Trust Co v. Strausser, 653 A.2d 688, 692 (Pa. Super 1995). , 653 A.2d 688, 692 (Pa. Super 1995). General denials of factual matters in foreclosure will be considGeneral denials of factual matters in foreclosure will be considered ered admissions if the Defendant should have this information. admissions if the Defendant should have this information.

See note to Pa.R.C.P. 1029(c).See note to Pa.R.C.P. 1029(c).

Note: Reliance on subdivision (c) does not excuse a failure to aNote: Reliance on subdivision (c) does not excuse a failure to admitdmit or deny a factual allegation when it is clear that the pleader mor deny a factual allegation when it is clear that the pleader mustust know whether a particular allegation is true or false. See Cercoknow whether a particular allegation is true or false. See Cerconene v. v. Cercone, 254 Pa.Super. 381, 386 A.2d 1 (1978).Cercone, 254 Pa.Super. 381, 386 A.2d 1 (1978).

Time and time again people lose on appeal because of this becausTime and time again people lose on appeal because of this because e they should know how much they owe.they should know how much they owe.

3434

Answer the Complaint: Answer the Complaint: proper denialsproper denials

Pick apart the breakdown of arrears and look for inconsistenciesPick apart the breakdown of arrears and look for inconsistencies or or inaccuracies that allow you to deny the allegations, e.g. date iinaccuracies that allow you to deny the allegations, e.g. date interest nterest started on arrearsstarted on arrears

Highlight any discrepancies between complaint and Act 91 notice Highlight any discrepancies between complaint and Act 91 notice descriptiondescription

Use the following language to demonstrate why Defendant should nUse the following language to demonstrate why Defendant should not ot have the kind of information needed to affirm or deny:have the kind of information needed to affirm or deny:

After reasonable investigation, Defendant is without knowledge oAfter reasonable investigation, Defendant is without knowledge or r information sufficient to form a belief as to the truth or accurinformation sufficient to form a belief as to the truth or accuracy of the acy of the allegation/averment and therefore said allegation/averment is deallegation/averment and therefore said allegation/averment is denied. Strict nied. Strict proof is required at trial. Further, pursuant to Pa. R.C.P. 102proof is required at trial. Further, pursuant to Pa. R.C.P. 1029(c), 9(c), Defendant avers that the information forming the substance of thDefendant avers that the information forming the substance of this is allegation is not information to which she has access, because [allegation is not information to which she has access, because [her her departed husband dealt exclusively with servicer Bank of Americadeparted husband dealt exclusively with servicer Bank of America and the and the matter of arrears and that information was not shared with her.]matter of arrears and that information was not shared with her.] [the proper [the proper calculation of interest, escrow advances, penalties and propertycalculation of interest, escrow advances, penalties and property inspection inspection fees are matters within the exclusive knowledge of the servicer,fees are matters within the exclusive knowledge of the servicer, not not Defendant]Defendant]

3535

Answer the Complaint: Answer the Complaint: new matter and defensesnew matter and defenses

File with the answer New Matter and File with the answer New Matter and defensesdefenses

Tell the story of arrears in new matterTell the story of arrears in new matter

Violation of specific statuteViolation of specific statute

Breach of contractBreach of contract

Breach of implied contractual duty of good Breach of implied contractual duty of good faith and fair dealingfaith and fair dealing

Fraud, misrepresentation, etc.Fraud, misrepresentation, etc.

3636

CounterclaimsCounterclaims

Not generally available for foreclosuresNot generally available for foreclosures

Because its in remBecause its in rem

Rearick v. Elderton State BankRearick v. Elderton State Bank, 2014 PA , 2014 PA Super 157, 97 A.3d 374, 383 (Pa. Super Super 157, 97 A.3d 374, 383 (Pa. Super 2014). 2014).

Counterclaims are allowed if they arise Counterclaims are allowed if they arise from the execution of the underlying note from the execution of the underlying note or mortgage (e.g. fraud in the execution)or mortgage (e.g. fraud in the execution)

3737

Counterclaims: TILA and Counterclaims: TILA and RESPARESPA

Look at settlement docs for Look at settlement docs for inaccuracies or inconsistenciesinaccuracies or inconsistencies

Examine HUD sheetExamine HUD sheet

Proper notices given? (e.g. right to Proper notices given? (e.g. right to rescind)rescind)

3838

Counterclaims: predatory Counterclaims: predatory lendinglending

NOT usually successfulNOT usually successful

What to look forWhat to look for

Lender provides loan to applicant when it knew or Lender provides loan to applicant when it knew or should have known repayment was not possibleshould have known repayment was not possible

Compare loan app and credit historyCompare loan app and credit history

Look at appraisals Look at appraisals

Discovery: request entire file and look at Discovery: request entire file and look at underwriting comments, especially for any underwriting comments, especially for any ““overridesoverrides””

3939

Counterclaims: predatory Counterclaims: predatory lendinglending

Note on abusive lending practices. [PA Banking Note on abusive lending practices. [PA Banking Dept.]Dept.]

Making a loan without regard to the borrowerMaking a loan without regard to the borrower’’s ability to repay;s ability to repay;

Loan flipping;Loan flipping;

Excessive fees and packing;Excessive fees and packing;

Aggressive and deceptive marketing;Aggressive and deceptive marketing;

Home improvement scams;Home improvement scams;

Prepayment penaltiesPrepayment penalties

Balloon paymentsBalloon payments

Negative Amortization (paying less than interest and principal/ Negative Amortization (paying less than interest and principal/ month)month)

4040

Counterclaims: predatory Counterclaims: predatory lendinglending

Hallmarks of Predatory Lending:Hallmarks of Predatory Lending:

““One of the clearest indicators of a predatory One of the clearest indicators of a predatory and unfair loan is one which exceeds the and unfair loan is one which exceeds the borrowerborrower’’s needs and repayment capacity.s needs and repayment capacity.”” Girard Finance v. Pa Hum. rel. CommGirard Finance v. Pa Hum. rel. Comm, 2012 , 2012 Pa. Commw. LEXIS 223, 13 (Pa. Comw. Pa. Commw. LEXIS 223, 13 (Pa. Comw. 2012) (reverse redlining case)2012) (reverse redlining case)

““high interest rates, high upfront fees, high high interest rates, high upfront fees, high late fees, hidden fees, hidden costs, and a late fees, hidden fees, hidden costs, and a lack of disclosure to the borrower.lack of disclosure to the borrower.”” 1414

4141

Counterclaim: RESPACounterclaim: RESPA Set it up early with opening Set it up early with opening letterletter

““We believe that the calculation of principal We believe that the calculation of principal and interest owed may be incorrect. and interest owed may be incorrect. Pursuant to the 12 U.S.C. Pursuant to the 12 U.S.C. §§2605(e) and 2605(e) and implementing Regulation X, we demand a implementing Regulation X, we demand a written response to this inquiry detailing the written response to this inquiry detailing the calculation of principal and interest for the calculation of principal and interest for the above accounts within 20 days of the date of above accounts within 20 days of the date of this letter. The reason why we are seeking this letter. The reason why we are seeking this information is that _______ is ready and this information is that _______ is ready and willing to negotiate a loan modification but willing to negotiate a loan modification but wishes to ensure that the amount due is wishes to ensure that the amount due is accurate.accurate.””

4242

Counterclaim: RESPACounterclaim: RESPA

““You are further warned that pursuant to 12 You are further warned that pursuant to 12 U.S.C. U.S.C. §§2605(e)(3), you may not provide any 2605(e)(3), you may not provide any information regarding any overdue payment information regarding any overdue payment owed by __________ to any consumer owed by __________ to any consumer reporting agency as the term is defined by 15 reporting agency as the term is defined by 15 U.S.C. U.S.C. §§1681a, for a 601681a, for a 60--day period day period commencing with the date of this letter. commencing with the date of this letter. Failure to comply with this request within the Failure to comply with this request within the applicable deadline will subject you to applicable deadline will subject you to potential liability under the Real Estate potential liability under the Real Estate Settlement Procedures Act of 1974 as Settlement Procedures Act of 1974 as amended.amended.””

4343

Set up Debt Collection Set up Debt Collection claimclaim

Request reinstatement quoteRequest reinstatement quote

Could trigger information for suit under FDCPA if it is Could trigger information for suit under FDCPA if it is inaccurate.inaccurate.

See See Allen v. LaSalle Bank, NAAllen v. LaSalle Bank, NA, 2011 U.S. App. LEXIS 587 , 2011 U.S. App. LEXIS 587 (3d Cir. 2011) (holding that reinstatement letter from (3d Cir. 2011) (holding that reinstatement letter from foreclosing attorney to defense attorney claiming fees and foreclosing attorney to defense attorney claiming fees and costs in excess of those authorized by New Jersey law costs in excess of those authorized by New Jersey law violated Fair Debt Collections Practices Act 1692(f)(1) violated Fair Debt Collections Practices Act 1692(f)(1) because such amounts were not authorized by agreement or because such amounts were not authorized by agreement or permitted by law).permitted by law).

But see But see Wright v. Phelan, Hallinan & SchmiegWright v. Phelan, Hallinan & Schmieg, 2010 U.S. , 2010 U.S. Dist. LEXIS 21977 (3d Cir. 2010) (holding that FDCPA does Dist. LEXIS 21977 (3d Cir. 2010) (holding that FDCPA does not apply to attorneynot apply to attorney--toto--attorney communications)attorney communications)

4444

Aggressive preemptive Aggressive preemptive action ?action ?

DonDon’’t bothert bother

Rooker Feldman doctrine and AntiRooker Feldman doctrine and Anti-- Injunction Act prohibits Federal Injunction Act prohibits Federal injunctions issued against state courtsinjunctions issued against state courts

DonDon’’t double your workloadt double your workload

4545

Is it too Late?Is it too Late? Petition to Open Judgment Petition to Open Judgment vs. Petition to Strike vs. Petition to Strike

UU.S. Bank v. Mallory.S. Bank v. Mallory, 2009 Pa. Super, 182, 982 A.2d , 2009 Pa. Super, 182, 982 A.2d 986 (Pa. Super. 2009) (held for lender)986 (Pa. Super. 2009) (held for lender)

Petition to Strike: granted only for a Petition to Strike: granted only for a ““fatal defect or fatal defect or irregularity appearing on the face of the record.irregularity appearing on the face of the record.””

Petition to Open (used for factual matters not Petition to Open (used for factual matters not apparent on face of record):apparent on face of record):

10 day automatic open, Pa. R.C.P. No. 237.3. 10 day automatic open, Pa. R.C.P. No. 237.3.

OtherwiseOtherwise……

Prompt filing of petition (82 day delay is too much time; withinPrompt filing of petition (82 day delay is too much time; within a a month preferred)month preferred)

Reasonable excuse or explanation (lack of sophistication not Reasonable excuse or explanation (lack of sophistication not an excuse)an excuse)

A meritorious defense (see above)A meritorious defense (see above)

4646

DiscoveryDiscovery

Ask for entire account fileAsk for entire account file

Were payments applied to principal & interest or Were payments applied to principal & interest or first to penalties. Compare with note & mortgagefirst to penalties. Compare with note & mortgage

Look at underwriting criteria and commentsLook at underwriting criteria and comments

Look at activity log (computerized)Look at activity log (computerized)

Look at conversation log (computerized)Look at conversation log (computerized)

Pay special attention to amounts and datesPay special attention to amounts and dates

Look for assignmentsLook for assignments

4747

Discovery: Examine the Discovery: Examine the NoteNote

Possession of note vs assignment of Possession of note vs assignment of mortgagemortgage

If Plaintiff is claiming right to foreclose If Plaintiff is claiming right to foreclose based on possession of original note.based on possession of original note.

Go to foreclosure firm law officesGo to foreclosure firm law offices

Bring a witness who can sign an affidavit Bring a witness who can sign an affidavit that they examined the documentthat they examined the document

Look for evidence of originalityLook for evidence of originality

4848

Discovery: Depositions of Discovery: Depositions of Plaintiff WitnessPlaintiff Witness

There mere threat often triggers a There mere threat often triggers a request for a loan modificationrequest for a loan modification

Examine means of possession of note Examine means of possession of note and assignmentsand assignments

Examine amounts and how calculatedExamine amounts and how calculated

Examine their knowledge of the fileExamine their knowledge of the file

4949

BankruptcyBankruptcy

Not a long term solution, as lenders get Not a long term solution, as lenders get exempted by petitionexempted by petition

Lender can go after the security (the land) as Lender can go after the security (the land) as foreclosure is against the landforeclosure is against the land

Bankruptcy reflects on credit rating, which Bankruptcy reflects on credit rating, which makes loan modification more difficultmakes loan modification more difficult

But it does take care of the consumer debt But it does take care of the consumer debt load that often gets people into troubleload that often gets people into trouble

5050

SettlementSettlement

Forbearance (temporary) (beware of waivers) (interest on Forbearance (temporary) (beware of waivers) (interest on arrears still accrues) arrears still accrues)

Home Affordable Modification Program (Home Affordable Modification Program (““Obama PlanObama Plan””).).

ALWAYS APPLY: foreclosure canALWAYS APPLY: foreclosure can’’t go forward with a pending t go forward with a pending application.application.

Tier 2 allows multiple tries if previously rejected.Tier 2 allows multiple tries if previously rejected.

Countrywide & Citibank agreement with PA attorney general Countrywide & Citibank agreement with PA attorney general with principal reduction (beware of tax consequences for with principal reduction (beware of tax consequences for principal forgiveness)principal forgiveness)

Short sale; must be by consent of all interested partiesShort sale; must be by consent of all interested parties

Deed in lieu of foreclosure, possibility of $3Deed in lieu of foreclosure, possibility of $3--4K payment 4K payment ((““Deeds for KeysDeeds for Keys””))

Transfer deed with lease back (e.g. Fannie Mae program)Transfer deed with lease back (e.g. Fannie Mae program)

Reverse mortgage for older adults with equity in property.Reverse mortgage for older adults with equity in property.

5151

Enforcing Loan Enforcing Loan ModificationsModifications-- HAMPHAMP

HAMP regulationsHAMP regulations

U.S. Treasury polices and HAMP servicer U.S. Treasury polices and HAMP servicer handbook that compiles all policy updates, handbook that compiles all policy updates, V. 5.0: V. 5.0:

https://www.hmpadmin.com/portal/programs/https://www.hmpadmin.com/portal/programs/ guidance.jspguidance.jsp

5252

Enforcing Loan Enforcing Loan ModificationsModifications

Frequent problemFrequent problem

HAMP loan modification HAMP loan modification

Proposal is to reduce payments to affordable rate per month by Proposal is to reduce payments to affordable rate per month by reducing interest rate, deferring arrears or principal to ballooreducing interest rate, deferring arrears or principal to balloon payment, n payment, so that monthly amount is less than 31% of gross incomeso that monthly amount is less than 31% of gross income

Client must qualify and fill out long Request for Modification fClient must qualify and fill out long Request for Modification formorm

Details in HAMP handbookDetails in HAMP handbook

Temporary Trial Plan to requires client to make 3 payments over Temporary Trial Plan to requires client to make 3 payments over 3 3 monthsmonths

Once client complies, permanent loan modification document is Once client complies, permanent loan modification document is presented for signature.presented for signature.

Financials must remain sameFinancials must remain same

What if lender does not honor the agreement?What if lender does not honor the agreement?

5353

Enforcing Loan Enforcing Loan ModificationsModifications-- HAMPHAMP

TPP not converting to permanent status: VERY frequently TPP not converting to permanent status: VERY frequently litigated. Typical excuses:litigated. Typical excuses:

applicant applicant ““not qualifiednot qualified”” despite going through predespite going through pre--qualification qualification proceduresprocedures

applicant did not pay 3 paymentsapplicant did not pay 3 payments

applicant did not submit documentsapplicant did not submit documents

Frequently lost, sometimes allegedly on purposeFrequently lost, sometimes allegedly on purpose

ApplicantApplicant’’s financials have changeds financials have changed

Agreed among all courts, no private right of action to enforce Agreed among all courts, no private right of action to enforce HAMP U.S. Treasury RulesHAMP U.S. Treasury Rules

BUT, is the TPP contract enforceable on its own terms pursuant tBUT, is the TPP contract enforceable on its own terms pursuant to o state contract law? YES.state contract law? YES.

Wigod v. Wells Fargo BankWigod v. Wells Fargo Bank, 7th Cir. 2011., 7th Cir. 2011.

No controlling appellate Pennsylvania law yetNo controlling appellate Pennsylvania law yet

5454

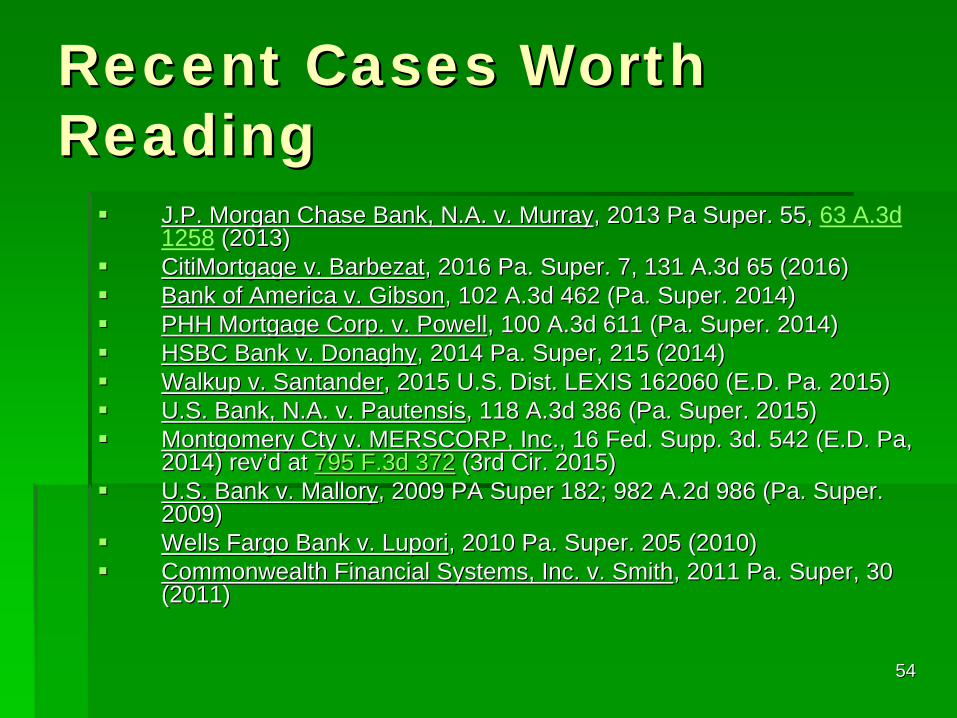

Recent Cases Worth Recent Cases Worth ReadingReading

J.P. Morgan Chase Bank, N.A. v. MurrayJ.P. Morgan Chase Bank, N.A. v. Murray, 2013 Pa Super. 55, , 2013 Pa Super. 55, 63 A.3d 1258 (2013)(2013)

CitiMortgage v. BarbezatCitiMortgage v. Barbezat, 2016 Pa. Super. 7, 131 A.3d 65 (2016) , 2016 Pa. Super. 7, 131 A.3d 65 (2016)

Bank of America v. GibsonBank of America v. Gibson, 102 A.3d 462 (Pa. Super. 2014) , 102 A.3d 462 (Pa. Super. 2014)

PHH Mortgage Corp. v. PowellPHH Mortgage Corp. v. Powell, 100 A.3d 611 (Pa. Super. 2014) , 100 A.3d 611 (Pa. Super. 2014)

HSBC Bank v. DonaghyHSBC Bank v. Donaghy, 2014 Pa. Super, 215 (2014) , 2014 Pa. Super, 215 (2014)

Walkup v. SantanderWalkup v. Santander, 2015 U.S. Dist. LEXIS 162060 (E.D. Pa. 2015), 2015 U.S. Dist. LEXIS 162060 (E.D. Pa. 2015)

U.S. Bank, N.A. v. PautensisU.S. Bank, N.A. v. Pautensis, 118 A.3d 386 (Pa. Super. 2015) , 118 A.3d 386 (Pa. Super. 2015)

Montgomery Cty v. MERSCORP, IncMontgomery Cty v. MERSCORP, Inc., 16 Fed. Supp. 3d. 542 (E.D. Pa, ., 16 Fed. Supp. 3d. 542 (E.D. Pa, 2014) rev2014) rev’’d at d at 795 F.3d 372795 F.3d 372 (3rd Cir. 2015)(3rd Cir. 2015)

U.S. Bank v. MalloryU.S. Bank v. Mallory, 2009 PA Super 182; 982 A.2d 986 (Pa. Super. , 2009 PA Super 182; 982 A.2d 986 (Pa. Super. 2009)2009)

Wells Fargo Bank v. LuporiWells Fargo Bank v. Lupori, 2010 Pa. Super. 205 (2010) , 2010 Pa. Super. 205 (2010)

Commonwealth Financial Systems, Inc. v. SmithCommonwealth Financial Systems, Inc. v. Smith, 2011 Pa. Super, 30 , 2011 Pa. Super, 30 (2011)(2011)

5555

U.S. Consumer Financial U.S. Consumer Financial Protection Bureau Protection Bureau January 2014 RulesJanuary 2014 Rules

Foreclosure initiated only after 120 days of delinquency.Foreclosure initiated only after 120 days of delinquency.

No dualNo dual--tracking, i.e. proceeding with foreclosure while homeowner tracking, i.e. proceeding with foreclosure while homeowner has submitted a loan modification application.has submitted a loan modification application.

Must notify homeowners about foreclosure alternatives.Must notify homeowners about foreclosure alternatives.

Direct and ongoing access to servicing personnel (i.e. single poDirect and ongoing access to servicing personnel (i.e. single point of int of contact)contact)

Homeowners must be considered for all available loss mitigation,Homeowners must be considered for all available loss mitigation, not not just injust in--house loan modshouse loan mods

No sheriffNo sheriff’’s sales if loan mod arrives at least 37 days before sale date.s sales if loan mod arrives at least 37 days before sale date.

Clear monthly mortgage statementsClear monthly mortgage statements

Prior warning before interest rate adjustmentsPrior warning before interest rate adjustments

Prior warning before purchasing forcedPrior warning before purchasing forced--place insuranceplace insurance

Restrictions on placing partial payments in Restrictions on placing partial payments in ““suspense accountssuspense accounts””

Respond to payoff requests in 7 daysRespond to payoff requests in 7 days

Respond to notices of error in calculation from homeowner in 30 Respond to notices of error in calculation from homeowner in 30 daysdays

Store loan information in an accessible way.Store loan information in an accessible way.

NO private right of action.NO private right of action.

www.consumerfinance.govwww.consumerfinance.gov

5656

Final ThoughtsFinal Thoughts

Use these tools to take these casesUse these tools to take these cases

You can make moneyYou can make money

Make it clear you cannot guaranty that Make it clear you cannot guaranty that youyou’’ll save someonell save someone’’s home; but you can s home; but you can give them lots of time and possibly give them lots of time and possibly resolve the matterresolve the matter

You will have a grateful client for lifeYou will have a grateful client for life

Any questions? EAny questions? E--mail me or call me. mail me or call me.

5757

Thank You and Good LuckThank You and Good Luck

Andrew D. Cotlar, Esq.Andrew D. Cotlar, Esq.

Law Office of Cotlar & CotlarLaw Office of Cotlar & Cotlar23 West Court St.23 West Court St.Doylestown, PA 18901Doylestown, PA 18901

Tel: 215Tel: [email protected]@hotmail.comwww.cotlarlaw.comwww.cotlarlaw.com