andreas stavrou, manager international business …uba.ua/documents/text/marfin_2010.pdfandreas...

TRANSCRIPT

1

2

Andreas Stavrou, Manager International Business Centre - Nicosia

The Cyprus Banking System

3

Cyprus

EU member since May 2004 &

Euro zone member since January 2008

Proven versatility in crisis

Milder effects from the economic crisis

Stable, conservative Central Banking

System and effective regulatory framework

The financial sector withstood the global crisis and no public recapitalization or government support was necessary

Cyprus is in the OECD white list

Ranked by Forbes as No.22 of “Best Countries for Business”

Economy dominated by the Services Sector – 78% of GDP

http://www.centralbank.gov.cy/

4

Cyprus ratings

The most recent 10-year CY bond which

was Issued in February 2010 is now

trading at 150 bps spread.

On 24 June 2010 Fitch affirmed Cyprus ratings

5

CBC Governor comments

“That said, I should point out that the budget deficit estimate for 2009 puts Cyprus in the middle of the range for the euro area as a whole. The situation is clearly not as dire as in some other euro area countries. To some degree this is because the recession we experienced in 2009 was not as deep as in other regions of the euro area.

A comparison with the Greek economy is not warranted. Our budget finances are in better shape and our debt to GDP ratio is considerably smaller.”

Athanasios Orphanides,

Governor of the Central Bank of Cyprus,

Interview with Bloomberg, 11 February 2010

6 6

Cyprus going strong in 2010

Total deposits ιn Cyprus increased by €8,8 billion during the first

6 months of 2010 (15,0% to €66,9 billion) - reflecting the "safe-

heaven" qualities of the market.

Property sales rising

Qatar agreement: a $500M joint project in hospitality/property

sectors confirming Cyprus economic potential

"Our decision to proceed with such a large investment in Cyprus is due to the fact that the

Cypriot economy has not been affected to a great extent by the (world) financial crisis. The

Cypriot economy has opportunities for growth."

Qatar's Emir, Sheikh Hamad bin Khalifa al-Thani Nicosia 21.4.2010

7 Cyprus Banking

8

Cyprus Banking

A market driven system based on English law, a legacy of the

British colonial rule

Marfin Laiki Bank, BOC – more than 100 years old

Legal and Banking structures (still) reflect British equivalents

Corporations Act 1925 - Marfin Laiki is number 1 on Register

of Companies

Open, competitive, multivariate, multidimensional, even

multicultural Banking Industry

Well capitalised and profitable banks

www.acb.com.cy

9

A Multitude of Banks of past and present

LISTED BANKS

1.Marfin Popular Bank Public Co Ltd

2.Bank of Cyprus Public Company Ltd

3.Hellenic Bank Public Company Ltd

4.USB Bank Plc

SUBSIDIARIES OF FOREIGN BANKS

Αlpha Bank Cyprus Ltd BNP Paribas Cyprus Ltd Emporiki Bank – Cyprus Limited Kommunalkredit International Bank

Ltd National Bank of Greece (Cyprus) Ltd Russian Commercial Bank (Cyprus)

Ltd Societe Generale Cyprus Ltd Piraeus Bank (Cyprus) Ltd Eurobank EFG Cyprus Ltd

OTHER BANKS

1. Co-operative Central Bank Ltd

2. The Cyprus Development Bank Public Company Ltd

3. Housing Finance Corporation

4. Mortgage Bank of Cyprus Ltd

BRANCHES OF BANKS OF EU COUNTRIES

1. Barclays Bank PLC

2. Banque SBA SA

3. First Investment Bank Ltd

4. Joint Stock Company “Trasta Komercbanka”

5. National Bank of Greece S.A.

6. Central Cooperative Bank PLC

7. Banca Transilvania S.A.

8. Joint Stock Company Akciju Komercbanka "Baltikums"

BRANCHES OF BANKS OF

COUNTRIES OTHER THAN EU

1. BankMed s.a.l.

2. Arab Jordan Investment Bank SA

3. BANQUE BEMO SAL

4. Bank of Beirut SAL

5. BBAC SAL

6. BLOM Bank SAL

7. Byblos Bank SAL

8. Credit Libanais SAL

9. FBME Bank Ltd

10.Open joint-stock company AvtoVAZbank

11.OJSC Promsvyazbank

12.Jordan Kuwait Bank PLC

13.Jordan Ahli Bank plc

14.Lebanon and Gulf Bank SAL

15.Lloyds TSB Offshore Limited

16.Privatbank Commercial Bank

17.IBL Bank sal

REPRESENTATIVE OFFICES 1. UBS AG 2. Atlasmont Banka A.D.

10

Central Bank of Cyprus (CBC)

Cyprus joined euro area on 1 January 2008

Interest rate management is now the responsibility of the European Central Bank (ECB)

Governor is a member of the Board of ECB

The primary objective of the ECB is to ensure price stability, which means keeping inflation rates below, but close to, 2%

The CBC has supervision over the commercial banks

http://www.centralbank.gov.cy

11

An Effective Supervisory Mechanism

Proven track record in setting Monetary Policy and safeguarding the Banking system

IMF’s Assessment of Financial Sector Supervision Report: “Supervision is strong, effective and in compliance with International Standards”

Full adoption of European Regulation

Use of non-interest rate tools proactively:

Tight(er) liquidity requirements – only 30% of FX deposits can be lend out by Banks – increases funding cost

Managed “cooling off” of the property market: tightened LVRs since mid 2007, to 70%.

Large credit exposures are discouraged to avoid concentration risk.

12

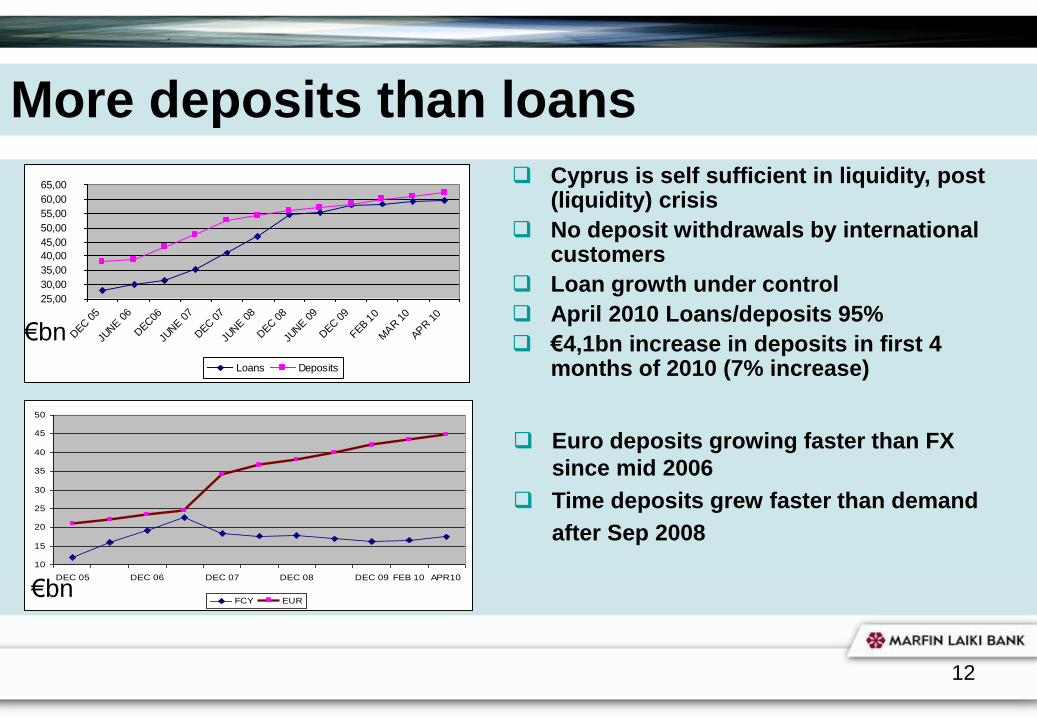

More deposits than loans

10

15

20

25

30

35

40

45

50

DEC 05 DEC 06 DEC 07 DEC 08 DEC 09 FEB 10 APR10

FCY EUR

Euro deposits growing faster than FX

since mid 2006

Time deposits grew faster than demand

after Sep 2008

Cyprus is self sufficient in liquidity, post (liquidity) crisis

No deposit withdrawals by international customers

Loan growth under control

April 2010 Loans/deposits 95%

€4,1bn increase in deposits in first 4 months of 2010 (7% increase)

25,00

30,00

35,00

40,00

45,00

50,00

55,00

60,00

65,00

DEC

05

JUNE 0

6

DEC

06

JUNE 0

7

DEC

07

JUNE 0

8

DEC

08

JUNE 0

9

DEC

09

FEB 10

MAR 1

0

APR 1

0

Loans Deposits

€bn

€bn

13

A Competitive Banking Market

Commercial Banking

8 local Banks and other credit Institutions

9 subsidiaries of Foreign Banks

27 International Banks operate branches

Very open & automatic for EU Banks

462 branches plus 33 IBUs

Supervised by the Central Bank of Cyprus

Large Cooperative sector

111 co-ops

Supervised by the Cooperative Central Bank

14

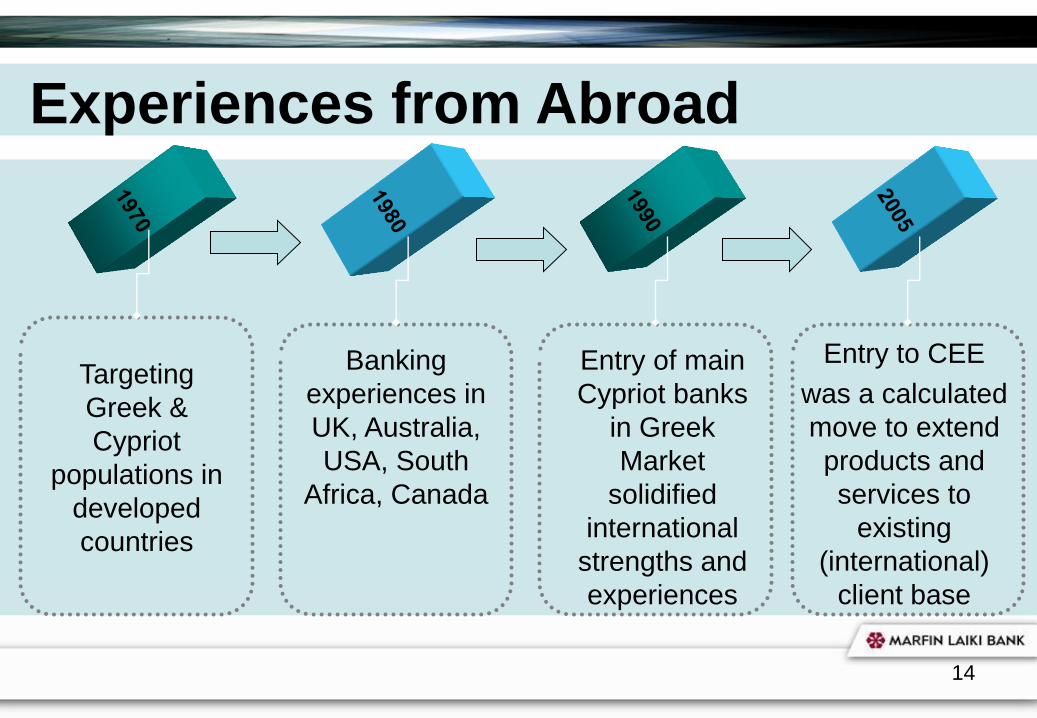

Experiences from Abroad

Targeting

Greek &

Cypriot

populations in

developed

countries

Banking

experiences in

UK, Australia,

USA, South

Africa, Canada

Entry of main

Cypriot banks

in Greek

Market

solidified

international

strengths and

experiences

Entry to CEE

was a calculated

move to extend

products and

services to

existing

(international)

client base

15

Commercial Banking

Highly educated human resources

Strong Banking Fundamentals

Adoption of Basel II

Conservative Lending Practices

Good breakdown of operations

between markets

Very good profitability record

No exposure to “Toxic Assets”

Healthy Capital and Liquidity positions

EU-wide stress testing results indicate ability

of domestic banking sector to withstand shocks

Limited exposure to CEE

16 16

Deutsche Bank ranks MLB as the least exposed in CEE

amongst peers

17

Solid Financial Package attracts International businesses

Benign low tax environment

Extensive Array of Double Taxation treaties

Mature Legal and Accounting practices

Strong Banking Sector

Euro

shields against currency crisis

provides access to ECB arsenal of support

expands the attractiveness of the Banking system for foreign

deposits and transactions Attraction of International Businesses expands banking client base

18

Government Crisis Support

Was not needed for Cyprus Banks given their strengths and reasonable

risk exposures

In fact, the Cyprus Government did not have to “bail out” or provide

direct support to any private organisation.

Government has the means for direct support but their use has been

unnecessary in the global crisis of 2008/09

Fiscal stimulus package being implemented

The Central Bank of Cyprus offers and operates a Deposit Protection

Scheme up to €100.000 per person or legal entity per Bank.

19

Update on Cyprus Banking System

“Despite negative developments in the real economy, our banking system remains in very good condition. Our banks are healthy, robust and have a strong capital base with a capital adequacy ratio of 11.9% at December 21, 2009, well above the minimum requirement of 8%.

The ratio of non-performing loans, which was declining steadily over

time, may have increased in 2009 but is still within acceptable levels. Please note that satisfactory provision for bad debts has been set aside for these loans. Regarding the profitability of banks, this has been satisfactory in 2009. During the year under review, which was a difficult year, banks have remained profitable, but with a smaller profit than that of 2008”

Athanasios Orphanides, Governor of Central Bank of Cyprus,

Press Conference, Nicosia 3 May 2010

20 Marfin Laiki Bank

A good Example

21

Group Profile – 109 Years Old

Marfin Laiki Bank (MLB) is strategically positioned as an

emerging regional player with two home markets, Greece &

Cyprus, and operations spanning in 11 countries in

Emerging Europe, UK, Australia, Malta, Russia & Ukraine

Regional bank with focus on corporate banking, wealth

management and international business banking

Ten years of robust growth both organically and through a

series of mergers & acquisitions and strategic alliances

Successful management track record and entrepreneurial

culture

Head-Office in Cyprus

507 branches, over 9.500 staff

http://www.marfinlaiki.com.cy/

22

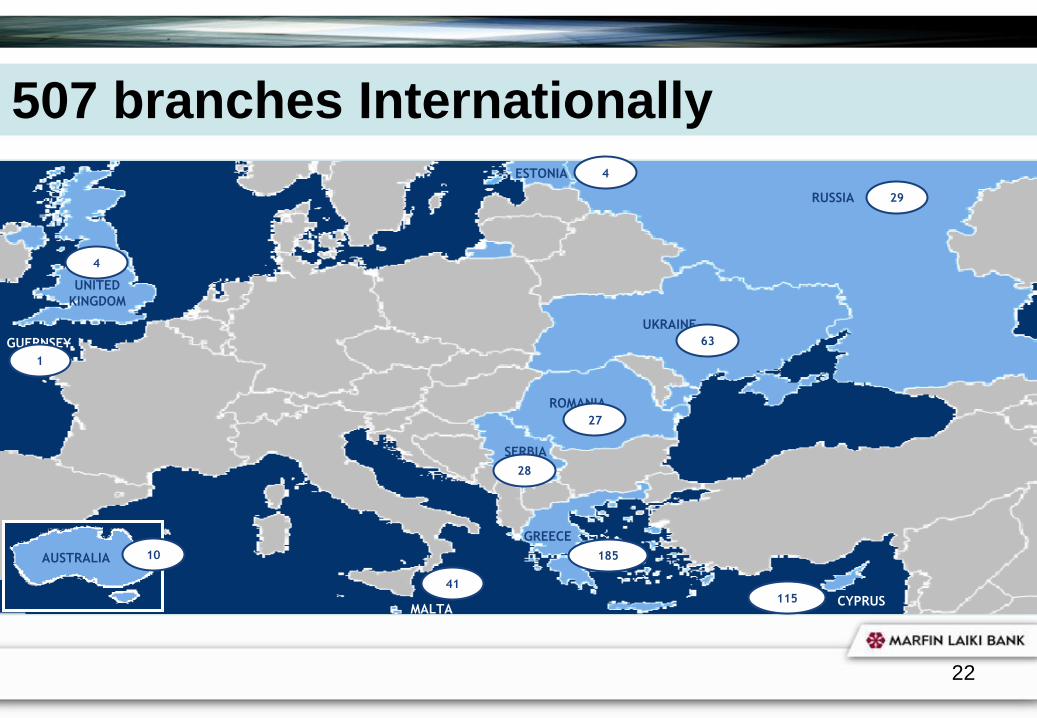

507 branches Internationally

GREECE

CYPRUS MALTA

GUERNSEY

SERBIA

ROMANIA

UKRAINE

RUSSIA

ESTONIA

UNITED

KINGDOM

AUSTRALIA 10

41

115

185

1

4

4

29

63

27

28

23

Credit Ratings

Capital Raising 7.7.2010

“…Marfin Popular Bank Public Co Ltd (“Bank”)

announces that it has successfully

completed on June 25, 2010, the issue of

the second Tranche of Capital Securities

2010 through a public offer, …

Overall, through the two Tranches the

amount of €295.524.000 was raised by the

issue of 295.524 Capital Securities of

nominal value €1.000 each. The Capital

Securities will be included to the Hybrid Tier

I Capital of the Bank, following the already

obtained relevant approval by the Central

Bank of Cyprus, further enhancing the

strong capital base of the Marfin Popular

Bank Group.

Credit Ratings

Baa2

BBB+

24

Strong Shareholders-Allies

MLB shares are listed on the Athens and the Cyprus Stock Exchanges

Biggest shareholder is Dubai Investment Fund with 18,81% No exposure to Dubai fund or Dubai economy – confirmed by press

release and Rating Agencies comments Other key shareholders proposed purchase of stake http://www.dubaigroup.com/

2nd biggest is Marfin Investment Group (MIG) with 9,55% Listed in Athens Stock Exchange €5,19bn capital raising through private placement completed in July

2007 Most recent investment: Olympic Airlines April 2010 sold Chipita for €730m and is accumulating cash for new

investment opportunities http://www.marfininvestmentgroup.com/

25 25

Financial Information

Key balance sheet items (€m) FY08 FY09 1H10

Loans to customers (net) 23.427 25.082 27.513

Total assets 38.367 41.828 43.287

Customer deposits 24.828 23.886 25.344

Total equity 3.430 3.636 3.563

Tangible equity 2.165 2.358 2.270

Key ratios FY08 FY09 1H10

Tier 1 8,6% 9,7% 9,8%

Capital adequacy ratio 10,6% 11,8% 11,5%

Cost/income 54,5% 58,1% 60,4%

NIM 2,4% 1,72% 1,80%

Loans/Deposits 94,4% 104,0% 104,9%

NPLs 4,3% 6,1% 6,6%

Provisioning 61 bps 105 bps 105 bps

26

CEO comments on 1H10 Results

31.08.10 Mr. Efthimios Bouloutas, CEO of Marfin Popular Bank Group, made the following statement:

“The Group’s strong operating performance during 1H 2010 reflects the success of our strategy

established on both prudent balance sheet management and rigorous risk management culture, in

conjunction with strong focus on client service. In this exceptionally challenging business environment,

the Group succeeded to further increase its operating profitability, while maintaining its solid capital

and comfortable liquidity position. The quality of the Group’s revenues combined with pre-provision

organic profitability demonstrated significant improvement compared with 1H 2009, while NPL

formation marked a meaningful decline. The combination of the above together with additional

provisions led to the further improvement of the provision coverage ratio and the strengthening of the

Group’s balance sheet against future developments.

Our Group, appreciating the social role it has to play in these adverse conditions globally, and especially

in Greece, has continued the uninterrupted supply of credit to its clients. In 1H 2010, the Group’s

market shares in new loan disbursements exceeded 25% in Cyprus (highest rank) and 21% in Greece

(second highest rank).

With these actions we consider that we contribute practically and materially to the efforts of our clients

and the communities we operate as they undergoing the adjustment process and reposition for growth.”

26

27 27

2010 EU Wide Stress Test Exercise

□ The exercise was conducted using the scenarios,

methodology and key assumptions provided by CEBS.

□ As a result of the assumed shock under the adverse

scenario, the estimated consolidated Tier 1 capital ratio

would change to 8,5% in 2011 compared to 9,4% as of end

of 2009.

□ An additional sovereign risk scenario would have a further

impact of 1,4 percentage point on the estimated Tier 1

capital ratio, bringing it to 7,1% at the end of 2011,

compared with the CRD regulatory minimum of 4%.

□ Additional buffer of €302m exists!

28 28

Marfin Laiki Bank Achievements

“Best Investment

Services Provided,

Cyprus 2008” Awarded by “World

Finance of Reuters” –

(first time awarded to

a Cypriot Bank)

“Best Bank

in Cyprus in

2009” Awarded by

“World

Finance”

“Best Internet

Bank, Consumer

Bank in Cyprus,

2009” and

“Best Sub

Custodian Bank

in Cyprus, 2009” Awarded by

“Global Finance”

“Innovation

Award- Cyprus” Awarded by

“Money Markets 2008

International Custody

Awards”

“Special 10 Year

Recognition

Award for the

period 2000-

2009” For the quality of US

payments Awarded by

“JP Morgan” –

(first time awarded to

a Cypriot Bank)

Top 1000 World Banks

2009 2010

Rank 240 209

FT Banker magazine

29 Contact Us

30

Contact Us

International Business Banking Tel: +357 22 363923, Fax: +357 22 363900 e-mail: [email protected]

Mailing Address: PO Box 22032, CY-1598 Nicosia, Cyprus

Nicosia International Business Centre 1 (178) Tel: +357 22 363737, Fax: +357 22 363750 e-mail: [email protected]

Nicosia International Business Centre 2 (168) Tel: +357 22 363737, Fax: +357 22 363700 e-mail: [email protected]

Limassol International Business Centre 1 (179) Tel: +357 25 815959, Fax: +357 25 815972 e-mail: [email protected]

Limassol International Business Centre 2 (158) Tel: +357 25 815959, Fax: +357 25 815637 e-mail: [email protected]

31

Contact Us cont…

Larnaca International Business Centre

Tel: +357 24 814291, Fax: +357 24 814290

e-mail: [email protected]

Paphos International Business Centre

Tel: +357 26 816522, Fax: +357 26 911334

e-mail: [email protected]

International Lending

Tel: +357 22 363718, Fax: +357 22 312878

e-mail: [email protected]

International Corporate Banking Unit

Tel: +357 22 363903, Fax: +357 22 363900

e-mail: [email protected]

Moscow Representative Office

Tel: +74959670185, Fax: +74959670186,

e-mail:[email protected]

32

DISCLAIMER Recipients of this presentation in jurisdictions outside the UK or the US should inform themselves about and observe any applicable legal requirements. This presentation is only being made available to interested parties on the basis that: (A) if they are UK persons, they are (i) persons who are "Investment Professionals", as described in Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the "Financial Promotion Order"), (ii) persons falling within any of the categories of persons described in Article 49 of the Financial Promotion Order, (iii) persons to whom this Memorandum may otherwise lawfully be made available; (B) if they are United States persons, they are „accredited investors‟ as defined under Rule 501(a) promulgated under the United States Securities Act of 1933, as amended; or (C) are outside the United Kingdom and the United States and eligible under local law to receive this Memorandum (all such persons collectively being referred to as “Relevant Persons”). By accepting this document you represent and warrant that you are such a person. This document must not be acted on or relied on and should be returned to Marfin Popular Bank by persons who are not Relevant Persons. Any investment or investment activity to which this communication relates is available only to Relevant Persons and will be engaged in only with Relevant Persons. Each person that receives a copy, by acceptance thereof, represents and agrees that he/she will not distribute or otherwise make available this document to any other person.

This presentation contains forward-looking statements, which include comments, statements and opinions with respect to our objectives and strategies, and the results of our operations and our business, considering environment and risk conditions.

However, by their nature, these forward-looking statements involve numerous assumptions, uncertainties and opportunities, both general and specific. We caution that these statements represent the Group‟s judgments and future expectations and that we have based these forward-looking statements on our current expectations and projections about future events. The risk exists that these statements may differ materially from actual future results or events and may not be fulfilled. We caution readers of this presentation not to place undue reliance on these forward-looking statements as a number of factors could cause future Group results to differ materially from these targets.

Forward-looking statements may be influenced in particular by factors such as movements in local and international securities markets, fluctuations in interest rates and exchange rates, the effects of competition in the areas in which we operate, general market, macroeconomic, governmental and regulatory trends and changes in economic, regulatory and technological conditions. We caution that the foregoing list is not exhaustive.

When relying on forward-looking statements to make decisions, investors should carefully consider the aforementioned factors as well as other uncertainties and events. Any statements regarding past trends or activities should not be taken as a representation that such trends or activities will continue in the future. All forward - looking statements are based on information available to Marfin Popular Bank Public Co Ltd. on the date of this presentation and Marfin Popular Bank Public Co Ltd. assumes no obligation to update such statements, unless otherwise required by applicable law.

Nothing on this presentation should be construed as a solicitation or offer, or recommendation, to acquire or dispose of any investment or to engage in any other transaction. Neither this presentation nor a copy of it may be taken or transmitted into Australia, Canada or Japan, or distributed, directly or indirectly, in Australia, Canada or Japan. Any failure to comply with this restriction may constitute a violation of Australian, Canadian or Japanese securities law. The distribution of this presentation in other jurisdictions may be restricted by law and persons into whose possession this presentation comes should inform themselves about, and observe, any such restrictions.