analyst presentation - final (2) - seneca college · introductory presentation 21 july 2011. ......

TRANSCRIPT

Introductory Presentation

21 July 2011

HighlightsOphir is a potential world class African resource play

/ 5th largest deepwater acreage holder in Africa

/ 5+ potential world scale oil and gas plays

/ 4.1Bnboe of net unrisked resources identified by RPS Energy Limited (RPS Energy)

/ Interest in 17 blocks, 8 jurisdictions

Diversified African exploration and appraisal portfolio

Diversified African exploration and appraisal portfolio

Proven technical, commercial and operating credentials

Proven technical, commercial and operating credentials

/ Portfolio actively managed to maximise value

/ Operator of majority wells to date

/ Commercial discoveries in 5 out of 8 operated wells to date

/ Material equity positions (pre and post farm downs)

/ Clear monetisation plans for gas discoveries

High impact High impact

/ 12+ wells1 drilling campaign over next 18 months

− Proven and frontier plays

/ Targeting 1.8Bnboe1 net unrisked resources

1

High impact

2011-12 exploration campaign

High impact

2011-12 exploration campaign

/ Targeting 1.8Bnboe net unrisked resources

− 56% gas; 44% oil

/ Tanzania and Equatorial Guinea now partially de-risked with >21Tcf and >6Tcf (gross) potential each

/ Gabon pre-salt is an oil play extension from recent major West African and Brazilian discoveries

/ Frontier oil exploration in AGC and Madagascar

Source: Ophir, RPS Energy for resource numbers1Includes AGC Kora-1 well

AGC

44

Tanzania

326

Gabon

223

Madagascar

10

Ophir’s African portfolio

Net risked prospective1 (MMboe) Diverse pan-African portfolio

SADR(4 blocks, 50% WI)

Somaliland

Equatorial

Guinea

320

Equatorial

Guinea

297

Net contingent1 (Bcf)

AGC(1 block, 36.7%4 WI)

Congo (B)2

(1 block, 48.5% WI)

Equatorial Guinea(1 block, 80% WI)

Gabon (4 blocks, Mbeli, Ntsina - 50%3 WI,

Manga, Gnondo - 100% WI)

Somaliland(1 block, 75% WI)

Tanzania(4 blocks, Blocks 1,3,4 - 40% WI,

East Pande - 70% WI)

Countries with discoveries

923MMboe

70% gas

Tanzania

835

2

Madagascar(1 block, 80% WI)

Countries with discoveries

Near-term upside

Medium-term upside

31.5% interest will be split pro-rata between Ophir and Kufpec3Post farm out of 50% interest in Mbeli and Ntsina blocks to Petrobras agreed on 17 June 20114Post farm out of 17.5% interest in AGC Profond block to Noble Energy agreed on 8 June 2011

1.1Tcf (189MMboe)

100% gas

Source: Ophir, RPS Energy for resource numbers

Aggregated resource figures represent mean estimates of probabilistic addition of the distributions of contingent and prospective resources

Net resource figures calculated based on post-Government back-in working interests where applicable, working interest shown on map are pre-Government back-in

Factor used for conversion from gas to oil equivalent - 6:11Excludes East Pande block in Tanzania2In October 2010, Premier Oil (Operator), elected not to participate in the 2nd PSC term; on 1 May 2011, PMO exited the license and the JOA stipulates that their

Oil plays

Gas plays

Both oil and gas plays

Board composition

Nicholas SmithChairman, Non Executive

Executive Deputy Chairman & Founder

Executive Director & FounderJonathan

Managing DirectorNick Cooper

Chief Financial OfficerB Yvonne

Independent Non ExecutiveDennis

Independent Non ExecutiveLyndon

Independent Non ExecutiveJohn Lander

Independent Non ExecutivePatrick Spink

Independent Non ExecutiveJohn Morgan

Independent Non ExecutiveRon Blakely

Non ExecutiveRajan

Tandon

Alan Stein, Executive Deputy Chairman & Founder

/ PhD, BSc (Hons)

/ 7 years with the Company

/ 23 years industry experience

/ Former Managing Director, Fusion Oil & Gas

Jonathan Taylor, Executive Director & Founder

/ MSc, BSc (Hons)

/ 7 years with the Company

/ 24 years industry experience

/ Former Technical Director, Fusion Oil & Gas

Executive team experience

Main Board Executives Independent Non Executive Non Executive

FounderAlan Stein

Jonathan

Taylor

B Yvonne

Holm

Dennis

McShane

Lyndon

Powell

John Lander Patrick Spink John Morgan Ron Blakely Tandon

3

/ Former Managing Director, IKODA / Former Team Leader, Clyde Petroleum

B Yvonne Holm, Chief Financial Officer

/ BA, MA

/ Joined the Company in February 2011

/ 15 years industry experience

/ Former General Manager, Mittal Investments

/ Former Senior Commercial Advisor, Amerada Hess

Nick Cooper, Managing Director

/ PhD, BSc (Hons), MBA

/ Joined the Company in June 2011

/ 20 years of industry experience

/ Former Chief Financial Officer, Salamander Energy plc

/ Previously Vice President, Goldman Sachs (Investment Banking), BG, AMOCO

Source: Ophir

2011-2012 the next phase of growing the resource base

First

Exploration and appraisal:

/ High-risk high-reward, rapid value accretion in the exploration and appraisal phase

/ Pre-appraisal monetisation opportunities via farm outs

Commercialisation:

/ Increased capital

requirements

/ Pre-development debt

funding

/ Pre-development

monetisation opportunities

Start-up:

/ First production: project

de-risked

/ Conventional RBL debt

funding; cash flow

positive

Equatorial

3D seismic

1st Discovery

Appraisal FID

First Production

Valu

e

Tanzania

Focus for use of proceeds

Oil new ventures

SADR

Somaliland

Gabon

Madagascar

Congo

AGC

East Pande

Equatorial Guinea

Value Realisation

Gas new ventures

4Source: Ophir

Potential for material near term net reserves and resources growth

Conventional “Mid-high” risk exploration

1,674MMboeTargeting

Prospective GPoS <50%3,555MMboe

Seismic attribute supported “Low risk” exploration

Adjacent to contingent resources

/ Discoveries

76MMboe

Prospective in existing discoveries198MMboe

Targeting 1,750MMboe1

net unriskedwith use of

proceeds Prospective GPoS >50%299MMboe

5

/ Discoveries

− Pweza-1− Chewa-1− Chaza-1− Fortuna-1− Lykos-1

Contingent 189MMboe

Source: Ophir, RPS Energy for resource numbers1Includes AGC Kora-1 well

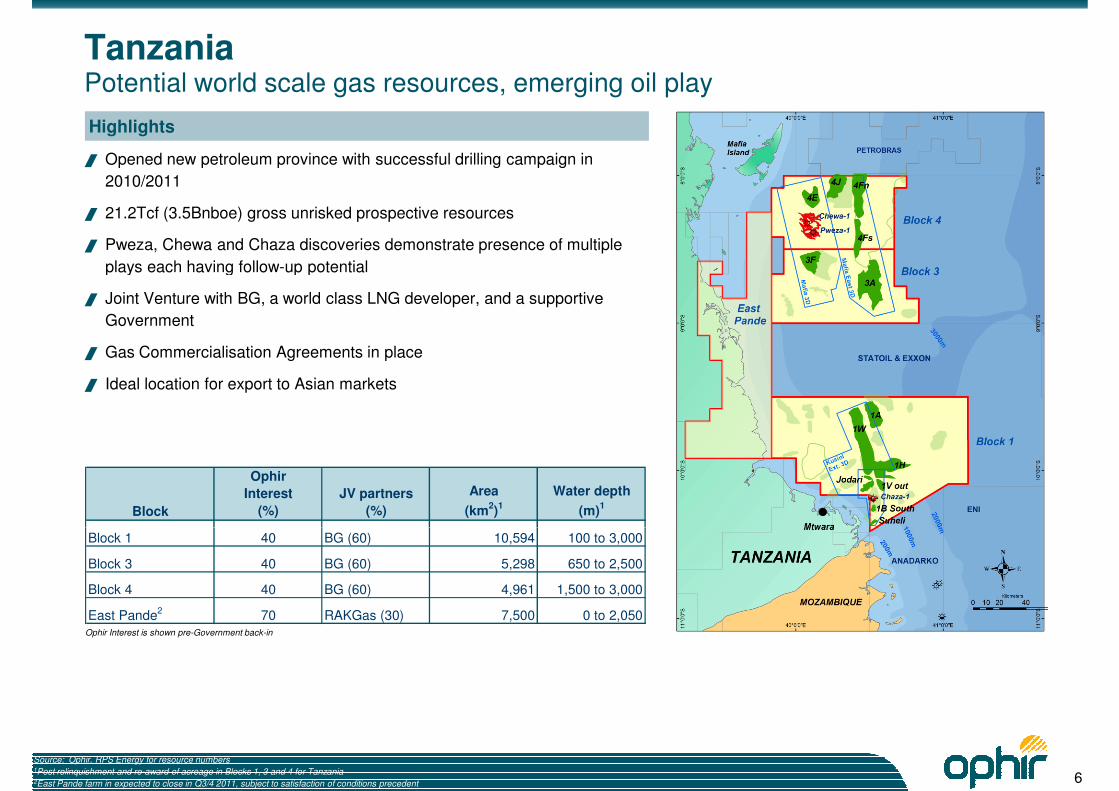

TanzaniaPotential world scale gas resources, emerging oil play

Highlights

/ Opened new petroleum province with successful drilling campaign in

2010/2011

/ 21.2Tcf (3.5Bnboe) gross unrisked prospective resources

/ Pweza, Chewa and Chaza discoveries demonstrate presence of multiple

plays each having follow-up potential

Block

Ophir

Interest

(%)

JV partners

(%)

Area

(km2)1

Water depth

(m)1

plays each having follow-up potential

/ Joint Venture with BG, a world class LNG developer, and a supportive

Government

/ Gas Commercialisation Agreements in place

/ Ideal location for export to Asian markets

Block 1 40 BG (60) 10,594 100 to 3,000

Block 3 40 BG (60) 5,298 650 to 2,500

Block 4 40 BG (60) 4,961 1,500 to 3,000

East Pande2 70 RAKGas (30) 7,500 0 to 2,050

6

Source: Ophir, RPS Energy for resource numbers 1Post relinquishment and re-award of acreage in Blocks 1, 3 and 4 for Tanzania2East Pande farm in expected to close in Q3/4 2011, subject to satisfaction of conditions precedent

Ophir Interest is shown pre-Government back-in

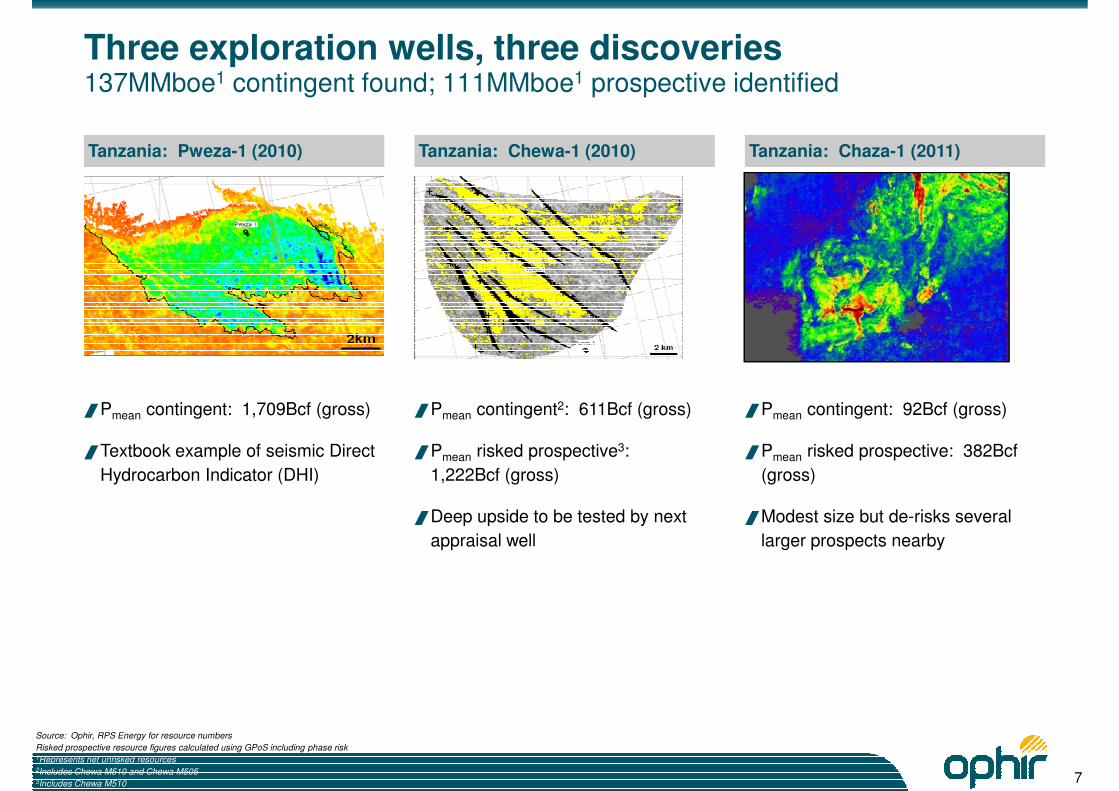

Three exploration wells, three discoveries137MMboe1 contingent found; 111MMboe1 prospective identified

Tanzania: Pweza-1 (2010) Tanzania: Chewa-1 (2010) Tanzania: Chaza-1 (2011)

/Pmean contingent: 1,709Bcf (gross)

/Textbook example of seismic Direct

Hydrocarbon Indicator (DHI)

/Pmean contingent: 92Bcf (gross)

/Pmean risked prospective: 382Bcf

(gross)

/Modest size but de-risks several

/Pmean contingent2: 611Bcf (gross)

/Pmean risked prospective3:

1,222Bcf (gross)

/Deep upside to be tested by next

7

larger prospects nearbyappraisal well

Source: Ophir, RPS Energy for resource numbers

Risked prospective resource figures calculated using GPoS including phase risk1Represents net unrisked resources2Includes Chewa M510 and Chewa M5053Includes Chewa M510

TanzaniaPredictable, well constrained seismic

/ All three wells have discovered gas in soft, Tertiary sandstones

/ All gas intersections to-date are associated with a distinctive seismic signature - commonly referred to as a DHI

/ Data from the wells may now be used to calibrate or tune the seismic data to increase the confidence in predicting fluid fill

(oil/gas/water)

8

/ Seismic section and an opacity cube through an undrilled prospect in Block 1

demonstrating:

− Amplitude shut-off with depth

− A flat reflection from a potential GWC

Source: Ophir

East

TanzaniaRegional play concepts

Oil and gas potential

/ East Pande block recently

secured

De-risked significant gas play/ Wells drilled to date

− Pweza-1 (2010)− Chewa-1 (2010)− Chaza-1 (2011)

Oil and gas potential

/ 3D recently acquired

West

9Source: Ophir

In Place

(Pmean)

Gross

(Pmean)

unrisked

Net WI

(Pmean)

unrisked1

GPoS2

Gas (Bcf) Gas (Bcf) Gas (Bcf) (%)

Contingent resources

Pweza 2,278 1,709 581 100

Chewa M510 769 577 196 100

Chewa M505 57 34 12 100

Chaza Miocene 123 92 32 100

TanzaniaResources overview and forward work plan

Forward plan Contingent and prospective resources

/ 7 wells drilling campaign3 commencing 2H 2011

− Targeting 12.2Tcf gross (2.0Bnboe)

− Significant running room with multiple other targets (9.0Tcf gross)

Total Contingent resources 3,227 2,412 821

Prospective resources - targeted in the next 18 months

Jodari Miocene 247 185 65 59

Jodari Oligocene 1,477 1,108 390 62

Jodari Palaeocene 228 137 48 13

Jodari Campanian 201 121 43 8

Jodari Cenomanian 829 456 161 13

1H Palaeocene 2,516 1,510 532 19

1H Cretaceous 1,697 933 328 8

1W Campanian 4,078 2,651 933 21

1W Cenomanian 1,287 708 249 9

3A Cenomanian 3,657 2,011 684 9

Chewa M501 (Chewa-2) 975 731 249 42

Chewa M560 (Chewa-2) 465 326 111 27

Chewa M750 (Chewa-2) 1,139 626 213 6

4E 1,080 648 220 12

Subtotal - targeted in next 18m 19,876 12,151 4,226

Prospective resources - others

Chaza Miocene 697 523 184 73

1B South Upper Miocene 276 179 63 17

(9.0Tcf gross)

/ Interpretation of recently acquired 3D seismic outboard

starting - further prospectivity expected

/ 1,000km2 3D seismic to be acquired in inboard East

Pande block in Q3 2011 which has both oil and gas

prospectivity

1B South Lower Miocene 135 101 36 59

1B South Oligocene 236 153 54 59

Suheli 307 200 70 59

1A 1,420 852 300 11

1V Outboard Palaeocene 326 179 63 16

1V Outboard Upper Cretaceous 400 220 77 8

3F Lower Cretaceous 614 338 115 6

3F Deep 717 359 122 6

Chewa M510 (Chewa-1) 1,895 1,421 483 86

Pweza North 272 190 65 56

4F 2,498 1,499 510 8

4J 4,396 2,857 971 16

Subtotal 14,189 9,071 3,113

Total Prospective resources 34,065 21,222 7,339

10

Source: Ophir, RPS Energy for resource numbers1Based on post-Government back-in working interest2Probability of success of finding hydrocarbon of gas phase in trap3Based on Ophir's current intention in discussions with BG but subject to change number and identity of wells

Monetising Tanzanian gas

/ Innovative early commercial agreements: provide control and accelerate development

/ Farm out and collaboration with best-in-class LNG operator

/ Commercial certainty and bankability will attract mid-stream partners and gas customers

Control along value chain

Upstream Mid-stream(pipelines)

Mid-stream(liquefaction)

Marketing

/ BG operator (60%)

/ Ophir (40%)

/ BG operator (60%)

/ Ophir (40%)

/ BG operator (60%)

/ Ophir (40%)

/ LNG export either with BG

or independently

/ DMO for 10% after

threshold volume at

equivalent pricing

11

equivalent pricing

/ 7+ well drilling

campaign

/ Carry is expected to

continue for 2

more wells

/ Monetisation opportunities: Future partner to provide

mid-stream capital

/ Debt funding

Source: Ophir

GabonPotential world scale pre-salt oil play

Highlights

/ The Ogooué Delta is a proven oil and gas province - over 2,000MMbbl of oil

and 900Bcf of gas in post-salt sequences

/ 2,420MMboe gross unrisked prospective resources

/ Ophir’s focus in Gabon is on the pre-salt prospects in Ntsina and Mbeli

/ Plate reconstructions and analogue studies highlight the potential of pre-salt

prospectivity in Gabon

/ Reconstructs to the Sergipe Alagoas Basin in Brazil, with the pre-salt giant

Carmopolis field and one offshore Barra discovery in 2010

/ Farm out of 50% in the pre-salt blocks Mbeli and Ntsina to Petrobras,

industry leader in pre-salt exploration

Forward plan

/ Acquisition of 2,000km2 3D seismic targeting pre-salt in Mbeli and Ntsina

/ Drilling first pre-salt well anticipated in Q4 2012

Block

Ophir

Interest

(%)

JV partners

(%)

Area

(km2)

Water depth

(m)

Mbeli 50 Petrobras (50) 3,384 180 to 2,200

Ntsina 50 Petrobras (50) 3,299 200 to 2,400

Manga 100 3,455 100 to 2,500

Gnondo 100 2,574 100 to 2,500

12

/ Secure farm in investment for Gnondo and Manga

Ophir Interest is shown pre-Government back-in of 10% in Mbeli, Ntsina and Gnondo blocks and 15% in Manga block, and post

farm out of 50% interest in Mbeli and Ntsina blocks to Petrobras agreed on 17 June 2011

Source: Ophir, RPS Energy for resource numbers

GabonReconstruction showing potentially analogous Brazilian fields and discoveries

Conjugate Brazilian and Gabonese basins

13Source: Ophir

GabonMbeli/Ntsina: pre-salt resource potential

/ Two pre-salt mega-closures have been mapped in Mbeli/Ntsina. Each mega-closure has a

number of sub-culminations

/ RPS has produced volume ranges for the following two models:

/ The mega-closure filled to spill

/ Only the sub-culminations filled

/ RPS has assigned probabilities to each model and consolidated a final volume estimate and PoS for each structure

In Place

(Pmean)

Gross

(Pmean)

unrisked

Net WI

(Pmean)

unrisked 1 GPoS

Oil (MMboe) Oil (MMboe) Oil (MMboe) (%)

Oil - post-salt

MB3 prospect 149 44 20 12

MB5 prospect 714 227 102 12

Tali 85 31 14 14

Sapeli 74 27 12 10Louvali 67 24 20 18

Pachg Liba 1,230 441 397 14Total 2,319 794 565

Padouck Area: Oil - pre-salt

Small Structures

Structure 1 3,639 1,401 630 10

Structure 2 516 199 90 8

Structure 3 968 373 168 8

Structure 4 454 175 79 8 Structure 4 454 175 79 8

Structure 5 121 47 21 8Total 2,776 1,069 481 18

Large Structures 21,881 8,424 3,791 2Total 3,246 1,250 563 18

4-5 Area: Oil - pre-salt

Small Structures

Structure 1 630 243 109 8

Structure 4 312 120 54 8

Structure 5 629 242 109 8Total 803 309 139 15

Large Structures 5,725 2,204 992 2Total 976 376 169

14

Model 2 cross section (small structure)

Model 1 cross section (large structure)

Wells targeted in the next 18 month drilling campaign

Source: Ophir, RPS Energy for resource numbers

Equatorial GuineaDe-risked gas play; significant further resource potential; active drilling campaign

Highlights

/ Block R is located in the south eastern part of the Niger Delta,

close to numerous significant oil and gas discoveries in the

Nigerian sector

/ 6.7Tcf (1.1Bnboe) gross unrisked prospective resources

/ Three deepwater wells drilled in 48 days; low drilling costs

/ Two gas discoveries have de-risked extensive portfolio

/ Gas is dry with no CO2 or H2S making it ideal for liquefaction

/ Sufficient resource potential to underpin export gas development

/ Finalised terms of a multi-party Memorandum of Understanding

(MoU) to participate in the planned second LNG train on Bioko

Island

Ophir

Interest JV partners Area Water depth

15

Block

Interest

(%)

JV partners

(%)

Area

(km2)

Water depth

(m)

Block R 80 GEPetrol (20) 1,674 1,050 to 1,950

Source: Ophir, RPS Energy for resource numbers

Three exploration wells, two discoveries 48MMboe1 contingent found; 87MMboe1 prospective identified

Equatorial Guinea: Fortuna-1 (2008) Equatorial Guinea: Lykos-1 (2008)

/ Pmean contingent2: 269Bcf (gross)

/ P risked prospective3: 572Bcf (gross)

/ Pmean contingent: 91Bcf (gross)

/ P risked prospective: 60Bcf (gross)

16

/ Pmean risked prospective3: 572Bcf (gross)

/ Opens up new play fairway in front of Niger Delta

thrust belt

/ Pmean risked prospective: 60Bcf (gross)

/ One of many similar features and drilled as "Proof

of Concept"

Source: Ophir, RPS Energy for resource numbers

Risked prospective resource figures calculated using GPoS including phase risk1Represents net unrisked resources2Includes Fortuna 5.5Ma (G1 and G2) channel, Fortuna 8.2Ma (G4) and Fortuna 10.5Ma (G3)3Includes Fortuna 5.5Ma prospective

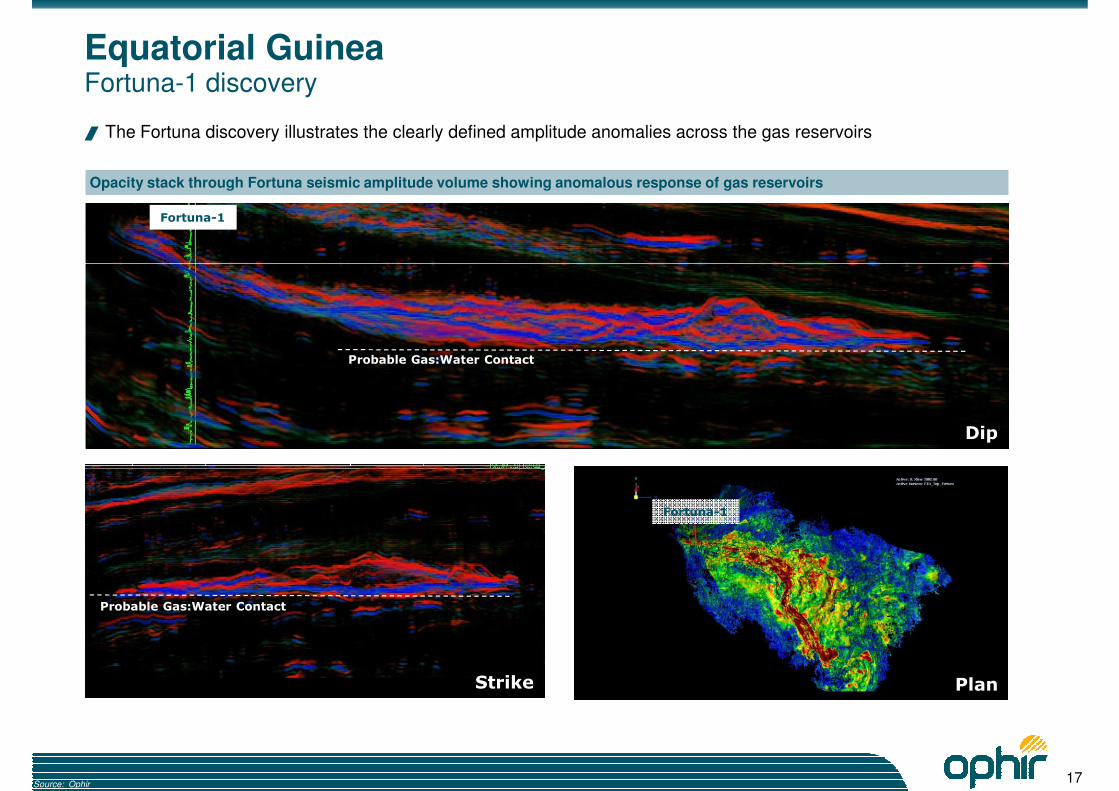

Equatorial GuineaFortuna-1 discovery

/ The Fortuna discovery illustrates the clearly defined amplitude anomalies across the gas reservoirs

Opacity stack through Fortuna seismic amplitude volume showing anomalous response of gas reservoirs

Fortuna-1

Dip

Probable Gas:Water Contact

Fortuna-1

17

StrikeStrike

Probable Gas:Water ContactProbable Gas:Water Contact

Strike

Probable Gas:Water Contact

Plan

Source: Ophir

Equatorial Guinea Resources overview and forward work plan

Prospective resources

In Place

(Pmean)

Gross

(Pmean)

unrisked

Net WI

(Pmean)

unrisked GPoS

Gas (Bcf) Gas (Bcf) Gas (Bcf) (%)

Contingent resources

Fortuna 5.5Ma (G1 and G2 channel) 226 170 136 100

Fortuna 8.2Ma (G4) 21 16 13 100

Fortuna 10.5Ma (G3) 111 83 66 100

Lykos Shallow 121 91 73 100

Total Contingent resources 479 360 288

Prospective resources - targeted in the next 18 months

Forward plan

/ 2+ well exploration drilling campaign commencing Q4

2011

− Targeting over 2.0Tcf gross (338MMboe)

− Significant running room with multiple other targets Prospective resources - targeted in the next 18 months

Fortuna East (Fortuna 2.4Ma) 520 364 291 24

Fortuna 10.5Ma 791 593 474 11

Fortuna East (Fortuna 13.8Ma) 727 545 436 11

Juturna 749 524 419 19

Subtotal - targeted in the next 18m 2,787 2,026 1,620

Prospective resources - others

Aphros H800 Gas1 278 195 156 4

Delphin H800 Gas1 114 80 64 3

Euthenia H800 Gas1 13 9 7 3

Helius H800 Gas1 21 15 12 4

Lykos H800 Gas1 53 37 30 4

Metis H800 Gas1 329 230 184 4

Nike H800 Gas1 92 64 51 3

Pandora H800 Gas1 13 9 7 4

Rhodes H800 Gas1 106 74 59 3

Silenus H800 Gas1 153 107 86 3

Uranus H800 Gas 1 22 15 12 4

Fortuna-1 (Fortuna 5.5Ma prospective) 779 584 467 98

Lykos prospective 89 67 54 89

Fortuna 8.2Ma 100 70 56 33

Fortuna 9.2Ma 25 19 15 24

Volturnas 288 202 162 18

Iambe 681 511 409 13

− Significant running room with multiple other targets (4.7Tcf gross)

/ Conclude negotiations with Government regarding

enhanced gas terms and commercialisation structure

/ Potential to introduce partners to accelerate and broaden

the drilling campaign

18

Iambe 681 511 409 13

Chronos 557 390 312 12

Northwest channels 494 370 296 11

Aphros 46 34 27 35

Bythos North 244 183 146 40

Delphin 57 43 34 83

Euthenia 62 46 37 77

Helius 215 161 129 85

Metis 216 162 130 73

Nike 82 62 50 85

Pandora 255 191 153 63

Rhodes 65 49 39 77

Silenus East 424 318 254 73

Silenus West 255 191 153 81

TBG 1 117 88 70 69

TBG 3 30 23 18 69

Uranus 80 60 48 66

Subtotal 6,355 4,659 3,727

Total Prospective resources 9,142 6,685 5,347

Source: Ophir, RPS Energy for resource numbers

Monetising Equatorial Guinea gas

/ Expected commercialisation via Equatorial Guinea LNG2, but floating LNG provides alternative, if required

Upstream Mid-stream(pipelines)

Mid-stream(Liquefaction)

Marketing

Multi-party MoU governs development of Equatorial Guinea LNG2

(pipelines) (Liquefaction)

/ Ophir (100% and non-

Government equity)

/ 3G consortia / Marathon + partners / LNG to be sold via arms

length international tenders

/ Combined feedstock

with Noble provides

critical mass

/ No mid-stream capital required assuming Equatorial Guinea

LNG2

19

/ Enhanced gas terms

/ 2+ well drilling campaign

/ Scope to accelerate

drilling and secure

development via farm

outs from high existing

equity

Source: Ophir

AGCNear term, frontier oil exploration Highlights

/ Kora-1 well targeting 165MMboe net unrisked resources in June/July 2011

− 1 in 5 chance of drilling success

/ Structural style in the AGC dominated by toe thrust and salt diapirism provides a

target-rich environment for both structural and stratigraphic plays

/ 735MMboe gross unrisked prospective resources

/ Potential reservoirs deposited by the Casamance River delta are predominantly

Cretaceous in ageCretaceous in age

/ Hydrocarbon potential is demonstrated by the neighbouring near-shore Dome Flore

and Dome Gea fields (STOIIP >1Bnbbl)

/ Extensive 3D seismic data available over the block

/ Multiple prospects identified - Kora, the best prospect to test the petroleum system,

will be drilled first

/ High impact play finder that could open a major new petroleum province

Forward plan

/ Contracted semi-submersible rig Maersk Deliverer to drill the Kora-1 prospect in

June 2011

/ Depending on the success, further seismic and drilling will be performed

Prospective resources

Block

Ophir

Interest

(%)

JV partners

(%)

Area

(km2)

Water depth

(m)

AGC Profond 36.7 Noble (30)

Rocksource (12.5)

Entreprise (12)

FAR (8.8)

9,838 75 to 3,500

Ophir currently has a 44.2% participating interest, FAR an 8.8% participating interest, Rocksource a

5% participating interest and Noble Energy a 30% participating interest. Should Rocksource and

Noble Energy participate through the drilling of the second exploration well, Noble Energy will retain

a 30% participating interest and Rocksource and the Group’s interests will be 8.75% and 40.45%

In Place

(Pmean)

Gross

(Pmean)

unrisked

Net WI

(Pmean)

unrisked GPoS

Oil (MMboe) Oil (MMboe) Oil (MMboe) (%)

Oil

Kora 1,586 476 165 19

Sabar 245 74 26 9

Xalam 618 185 64 8

Total 2,449 735 254

20

Prospective resources

Source: Ophir, RPS Energy for resource numbers

Wells targeted in the next 18 month drilling campaign

a 30% participating interest and Rocksource and the Group’s interests will be 8.75% and 40.45%

respectively. Should Rocksource and Noble Energy continue to participate in petroleum operations

after the drilling of the second exploration well, Noble Energy will retain a 30% participating interest

and Rocksource and the Group’s interests will be 12.5% and 36.7% respectively. L'Entreprise holds

a 12% participating interest (subject to further back-in rights to acquire pro rata from the other

members of the joint venture a further 5% participating interest. Participating interests are shown

pre-L'Entreprise back-in.

Timing Prospect Country

Gross

(Pmean)

unrisked

Gross

(Pmean)

risked

Working

interest

Net

(Pmean)

unrisked

Net

(Pmean)

risked

Weighted average

GPoS

(MMboe) (MMboe) (%) (MMboe) (MMboe)

Exploration and appraisal programme12+4 high impact exploration and appraisal wells anticipated before end 2012

/ Campaign targeting 1.8Bnboe4 net unrisked at average GPoS of 1 in 5

Q3 2011 Kora AGC 476 90 34.6% 165 31 19%

Jodari Tanzania 335 147 35.2% 118 52 44%

Fortuna E1 Equatorial Guinea 250 35 80.0% 200 28 14%

1W Tanzania 560 103 35.2% 197 36 18%

Pweza2 Tanzania NM

Juturna Equatorial Guinea 87 17 80.0% 70 13 19%

Q2 2012 Chewa3 Tanzania 281 72 34.0% 95 25 26%

1H Tanzania 407 60 35.2% 143 21 15%

4E Tanzania 108 13 34.0% 37 4 12%

Q4 2011

AppraisalQ1 2012

Q3 2012 4E Tanzania 108 13 34.0% 37 4 12%

Anjohibe Madagascar 61 7 80.0% 49 6 12%

3A Tanzania 335 30 34.0% 114 10 9%

Padouck deep Gabon 1,250 225 45.0% 563 101 18%

TOTAL 4,150 801 1,750 329

Q4 2012

Q3 2012

21

Source: Ophir, RPS Energy for resource numbers

Note: Net resource figures calculated based on post-Government back-in working interest1Fortuna E well will de-risk Iambe, and in an up-side case may prove gas at Iambe at the Fortuna East location

2Pweza-2 appraisal well not targeting additional prospective resources3Chewa-2 appraisal well targeting new additional prospective resources4Includes AGC Kora-1 well

2011 2012 Likely

Q3 Q4 Q1 Q2 Q3 Q4 ($ million)

TanzaniaBlocks 1,3

and 4199 Operator has secured a +300 day rig commitment

East Pande 10 Assumes 3D 1,000km2 programme

Equatorial Guinea Block R 65 Assumes Ophir 100% paying

PermitCountry Comments

$375m IPO proceeds used across 5+ plays targeting 1.8Bnboe1 net unrisked resources

Potential for further drilling

Gabon Mbeli 0 Commitment firm seismic - carried by expected farminee

Ntsina 4 Pre-salt well with Petrobras carrying part of Ophir

Manga 0 Minimum work programme

Gnondo 1 PSC obligation of minor 2D seismic programme

AGC Profond 2 Future work and balance of Kora-1 costs

Madagascar Marovoay 27 Enter new term and well commitment

New Ventures 44 Discretionary funding for new opportunities

Admin/Corporate/

Other exploration23 Based on historical/projections and other exploration costs

Total 375

22

Well drilled Spending cap for BG carry agreement reachedGeophysical acquisition (offshore)

476 585 647 281 576 1,585Gross unrisked resources targeted (MMboe)1

165 318 267 95 229 677Net unrisked resources targeted (MMboe)1

Source: Ophir, RPS Energy for resource numbers1Includes AGC Kora-1 well

Excludes existing cash resources and any proceeds from any exercise of the over-allotment option granted in the IPO

4,150

1,750

HighlightsOphir is a potential world class African resource play

/ 5th largest deepwater acreage holder in Africa

/ 5+ potential world scale oil and gas plays

/ 4.1Bnboe of net unrisked resources identified by RPS Energy Limited (RPS Energy)

/ Interest in 17 blocks, 8 jurisdictions

Diversified African exploration and appraisal portfolio

Diversified African exploration and appraisal portfolio

Proven technical, commercial and operating credentials

Proven technical, commercial and operating credentials

/ Portfolio actively managed to maximise value

/ Operator of majority wells to date

/ Commercial discoveries in 5 out of 8 operated wells to date

/ Material equity positions (pre and post farm downs)

/ Clear monetisation plans for gas discoveries

High impact High impact

/ 12+ wells1 drilling campaign over next 18 months

− Proven and frontier plays

/ Targeting 1.8Bnboe1 net unrisked resources

23

High impact

2011-12 exploration campaign

High impact

2011-12 exploration campaign

/ Targeting 1.8Bnboe net unrisked resources

− 56% gas; 44% oil

/ Tanzania and Equatorial Guinea now partially de-risked with >21Tcf and >6Tcf (gross) potential each

/ Gabon pre-salt is an oil play extension from recent major West African and Brazilian discoveries

/ Frontier oil exploration in AGC and Madagascar

Source: Ophir, RPS Energy for resource numbers1Includes AGC Kora-1 well

DisclaimerThis document has been prepared and issued by and is the sole responsibility of Ophir Energy plc (the “Company”) and its subsidiaries.

This document is an advertisement and not a prospectus or an offer or invitation to subscribe for or purchase any securities and nothing contained herein shall form the basis of any contract or commitment whatsoever. Investors should not subscribe for or purchase any shares referred to in this document. Investors are referred to the prospectus published by the Company on 8 July 2011 in connection with its admission to the premium listing segment of the Official List of the Financial Services Authority and to trading on the main market for listed securities of the London Stock Exchange plc (together “Admission”) and the issue and sale of ordinary shares. Copies of the prospectus are available from the Company’s registered office and from www.ophirenergy.com.

This document does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any shares in the Company nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract commitment or investment decision in relation thereto nor does it constitute a recommendation regarding the securities of the Company.

THIS DOCUMENT IS NOT AN OFFER FOR SALE OF SECURITIES IN THE UNITED STATES OR ANY OTHER JURISDICTION. THE ORDINARY SHARES OF THE COMPANY HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE US SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR THE SECURITIES LAWS OF ANY STATE OF THE UNITED STATES OR OTHER JURISDICTION AND MAY NOT BE OFFERED AND SOLD WITHIN THE UNITED STATES EXCEPT TO QUALIFIED INSTITUTIONAL BUYERS (AS DEFINED IN RULE 144A) IN RELIANCE ON RULE 144A OR ANOTHER EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND ANY APPLICABLE STATE OR LOCAL SECURITIES LAWS. NO PUBLIC OFFER OF OPHIR SECURITIES IS BEING MADE IN REQUIREMENTS OF THE SECURITIES ACT AND ANY APPLICABLE STATE OR LOCAL SECURITIES LAWS. NO PUBLIC OFFER OF OPHIR SECURITIES IS BEING MADE IN THE UNITED STATES.

Neither this document nor any copy of it may be taken, distributed or transmitted into the United States, (including its territories or possessions, any state of the United States or the District of Columbia). Neither this document nor any copy of it may be taken or transmitted into Australia, Canada or Japan or to Australian, Canadian or Japanese persons or any securities analyst or other person in any of those jurisdictions. Any failure to comply with this restriction may constitute a violation of US, Australian, Canadian or Japanese securities law. The distribution of this document in other jurisdictions may be restricted by law and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions. The securities referred to herein have not been and will not be registered under the applicable securities law of Canada, Australia or Japan and, subject to certain exceptions, may not be offered or sold within Canada, Australia or Japan or to any national, resident or citizen of Canada, Australia or Japan.

This document and any materials distributed in connection with this document may include certain forward-looking statements, beliefs or opinions, including statements with respect to the Company’s business, financial condition and results of operations. These statements, which contain the words “anticipate”, “believe”, “intend”, “estimate”, “expect” and words of similar meaning, reflect the Directors’ beliefs and expectations and involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. No representation is made that any of these statements or forecasts will come to pass or that any forecast results will be achieved. There are a number of risks, uncertainties and factors that could cause actual results and developments to differ materially from those expressed or implied by these statements and forecasts. Past performance of the Company cannot be relied on as a guide to future performance. Information in this document of the price at which ordinary shares have been bought or sold in the past cannot be relied upon as a guide to future performance. Forward-looking statements speak only as at the date of this document and each of the Company, its advisers and each of their respective members, directors, officers and employees expressly disclaims any obligations or undertaking to release any update of, or revisions to, any forward-looking statements in this document. No statement in this document is intended to be a profit forecast. As a result, you are cautioned not to place any undue reliance on such forward-looking statements.

Certain data in this document was obtained from various external data sources, and the Company has not verified such data with independent sources. Accordingly, the Company the Company does not make any representations as to the accuracy or completeness of that data, and such data involves risks and uncertainties and is subject to change based on various factors.

24

factors.

The Company, its advisers and each of their respective members, directors, officers and employees are under no obligation to update or keep current information contained in this document, to correct any inaccuracies which may become apparent, or to publicly announce the result of any revision to the statements made herein except where they would be required to do so under applicable law, and any opinions expressed in them are subject to change without notice. No representation or warranty, express or implied, is given by the Company or any of its respective subsidiary undertakings or affiliates or directors, officers or any other person as to the fairness, accuracy or completeness of the information or opinions contained in this document, nor have they independently verified such information, and any reliance you place thereon will be at your sole risk. Without prejudice to the foregoing, no liability whatsoever for any loss howsoever arising, directly or indirectly, from any use of this document or its contents or otherwise arising in connection therewith is accepted by any such person in relation to such information.

Any securities, financial instruments or strategies mentioned herein or relating to the Company may not be suitable for all investors. The recipient of this document must make its own independent decision regarding any securities or financial instruments mentioned herein or relating to the Company.

By accepting a copy of this document, you agree to be bound by the foregoing limitations and conditions and, in particular, will be taken to have represented, warranted and undertaken that (i) you have read and agree to comply with the contents of this notice; and (ii) you will not at any time have any discussion, correspondence or contact concerning the information in this document or the prospectus with any of the directors or employees of the Company or its subsidiaries without the prior written consent of the Company.

Appendix

25

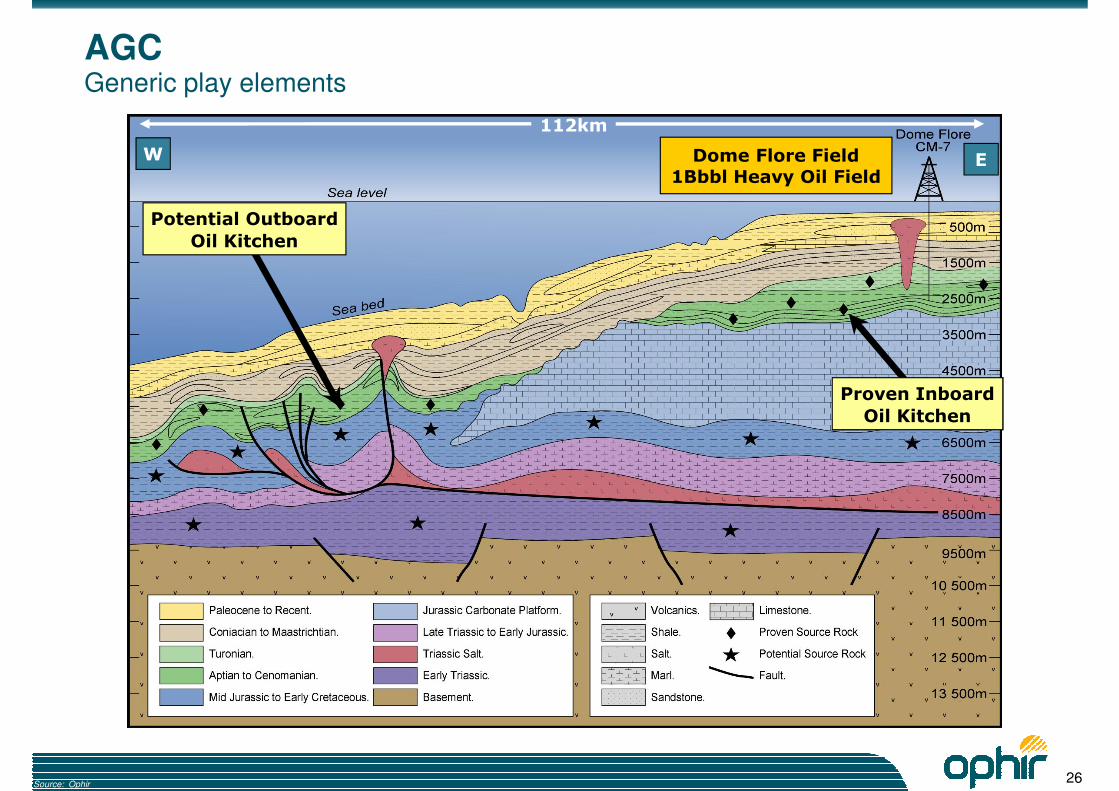

AGC Generic play elements

112km112km

WW

Potential Outboard

Oil Kitchen

Potential Outboard

Oil Kitchen

EEDome Flore Field

1Bbbl Heavy Oil Field

Dome Flore Field

1Bbbl Heavy Oil Field

112km

W

Potential Outboard

Oil Kitchen

EDome Flore Field

1Bbbl Heavy Oil Field

Proven Inboard

Oil Kitchen

Proven Inboard

Oil Kitchen

Proven Inboard

Oil Kitchen

26Source: Ophir

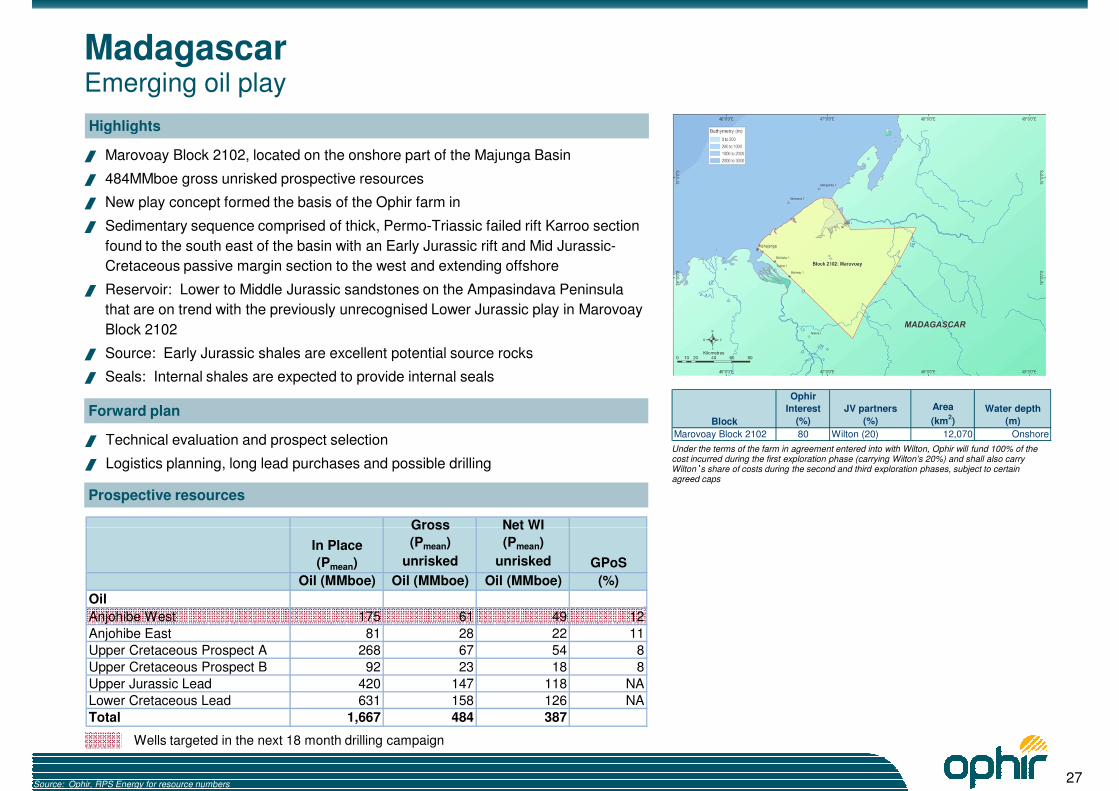

MadagascarEmerging oil play

Highlights

/ Marovoay Block 2102, located on the onshore part of the Majunga Basin

/ 484MMboe gross unrisked prospective resources

/ New play concept formed the basis of the Ophir farm in

/ Sedimentary sequence comprised of thick, Permo-Triassic failed rift Karroo section

found to the south east of the basin with an Early Jurassic rift and Mid Jurassic-

Cretaceous passive margin section to the west and extending offshore

Block

Ophir

Interest

(%)

JV partners

(%)

Area

(km2)

Water depth

(m)

Marovoay Block 2102 80 Wilton (20) 12,070 Onshore

Cretaceous passive margin section to the west and extending offshore

/ Reservoir: Lower to Middle Jurassic sandstones on the Ampasindava Peninsula

that are on trend with the previously unrecognised Lower Jurassic play in Marovoay

Block 2102

/ Source: Early Jurassic shales are excellent potential source rocks

/ Seals: Internal shales are expected to provide internal seals

Forward plan

/ Technical evaluation and prospect selection

/ Logistics planning, long lead purchases and possible drillingUnder the terms of the farm in agreement entered into with Wilton, Ophir will fund 100% of the cost incurred during the first exploration phase (carrying Wilton’s 20%) and shall also carry Wilton’s share of costs during the second and third exploration phases, subject to certain agreed caps

Prospective resources

Gross Net WI

27

Wells targeted in the next 18 month drilling campaign

In Place

(Pmean)

Gross

(Pmean)

unrisked

Net WI

(Pmean)

unrisked GPoS

Oil (MMboe) Oil (MMboe) Oil (MMboe) (%)

Oil

Anjohibe West 175 61 49 12

Anjohibe East 81 28 22 11

Upper Cretaceous Prospect A 268 67 54 8

Upper Cretaceous Prospect B 92 23 18 8

Upper Jurassic Lead 420 147 118 NA

Lower Cretaceous Lead 631 158 126 NA

Total 1,667 484 387

Source: Ophir, RPS Energy for resource numbers

Congo, SADR, SomalilandAssets overview

SomalilandCongo (B) SADR

Block

Ophir

Interest

(%)

JV partners

(%)

Area

(km2)

Water depth

(m)

Berbera 75 RAKGas (22.5)

Government of

Somaliland (2.5)

16,270 0 to 1,425

Block

Ophir

Interest

(%)

JV partners

(%)

Area

(km2)

Water depth

(m)

Marine IX 1 48.5 Ophir and Kufpec 1,044 400 to 1,600

Block

Ophir

Interest

(%)

JV partners

(%)

Area

(km2)

Water depth

(m)

Daora; Haouza;

Mahbes; Mijek

50 Premier SADR (50) 74,327 200 to 2,500

28

/ Discussions with the Government of

Somaliland are underway to reconfigure

the terms of the Berbera PSA to allow for

the acquisition of new seismic data

/ Forward plan on hold until sovereign

status of the SADR is resolved

/ Forward plan to be determined following

a conclusion of negotiations with the

Government regarding Premier’s

withdrawal

Forward planForward plan Forward plan

SADR and Somaliland subject to uncertainty related to sovereignty issues. Title to assets in Congo (B) pending agreement with government regarding fiscal terms1In Oct ober 2010, Premier Oil (Operator), elected not to participate in the 2nd PSC term; on 1 May 2011, PMO exited the license and the JOA stipulates that their 31.5% interest will be split pro-rata between Ophir

and Kufpec

Source: Ophir