analysis of the leased line markets - llv.li · pdf filemarket for terminating segments of...

TRANSCRIPT

O FFIC E FO R C O M M U N IC A TIO N S

PR IN C IPA LITY O F LIEC H TEN STEIN

Gerberweg 5 | P.O. Box 684 | 9494 Vaduz | Liechtenstein | T +423 236 64 88 | F +423 236 64 89 | [email protected] | www.ak.llv.li

Analysis of the leased line markets

Market for terminating segments of leased lines (wholesale market; M6)

Market for trunk segments of leased lines (wholesale market)

Final version

2/57

Vaduz, August 2012

3/57

TABLE OF CONTENTS

1 INTRODUCTION ...................................................................................................... 5

1.1 Legal basis ...................................................................................................................................... 5

1.2 Market analysis process ................................................................................................................. 6

1.3 National consultation ..................................................................................................................... 7

1.4 EEA-wide consultation .................................................................................................................... 8

1.5 Basic aspects of the market analysis ............................................................................................... 9

1.6 Composition of the market analysis ............................................................................................... 9

1.7 Time frame ................................................................................................................................... 10

1.8 Sources of data ............................................................................................................................. 10

1.9 Competition authority .................................................................................................................. 10

2 THE MARKETS TO BE INVESTIGATED ..................................................................... 12

2.1 The Liechtenstein fixed network sector in general ........................................................................ 12

2.2 Preliminary remarks on the market definition .............................................................................. 13

2.3 The leased line markets ................................................................................................................ 14

2.3.1 Definition of a leased line .............................................................................................................. 14

2.3.2 The material definition of the leased line markets ........................................................................ 15

2.4 Definition of the relevant product markets .................................................................................. 19

2.4.1 The Recommendation on Relevant Markets and the three-criteria test for ex ante regulation ... 19

2.4.2 The application of the three-criteria test to the trunk leased line market .................................... 20

2.4.3 The market for terminating segments of leased lines ................................................................... 22

2.4.4 The market for the minimum set of specific retail customer leased lines ..................................... 23

2.4.5 The materially relevant leased line markets � conclusion ............................................................. 23

2.5 The development of the leased line markets ................................................................................ 24

2.5.1 Providers ........................................................................................................................................ 24

2.5.2 Buyers............................................................................................................................................. 26

4/57

2.5.3 Leased line products offered.......................................................................................................... 26

2.5.4 Market sizes and development ...................................................................................................... 27

2.5.5 The sizes of the trunk segment market and the market for terminating segments ...................... 31

2.6 Definition of the relevant geographic market ............................................................................... 32

2.7 Regulation relevant to date for leased line services...................................................................... 32

3 MARKET POWER .................................................................................................. 35

3.1 Undertakings with significant market power ................................................................................ 35

3.1.1 Single dominance ........................................................................................................................... 35

3.1.2 Collective market power (joint dominance) .................................................................................. 36

3.2 Market shares............................................................................................................................... 38

3.2.1 The indicator's significance ............................................................................................................ 38

3.2.2 Assessment of the indicator ........................................................................................................... 40

3.3 Relevance of further SMP indicators............................................................................................. 44

3.4 Market barriers ............................................................................................................................ 45

3.4.1 The indicator's significance ............................................................................................................ 45

3.4.2 Control over infrastructure not easily duplicated .......................................................................... 46

3.4.3 Existence of economies of scale and scope ................................................................................... 48

3.4.4 Sunk costs ....................................................................................................................................... 49

3.4.5 Product diversification ................................................................................................................... 50

3.5 Joint market power ...................................................................................................................... 51

3.5.1 On the market for terminating segments of leased lines .............................................................. 51

3.5.2 On the market for trunk leased lines ............................................................................................. 52

3.6 Market power � conclusion .......................................................................................................... 53

3.6.1 On the market for terminating segments of leased lines .............................................................. 53

3.6.2 On the market for trunk segments of leased lines ......................................................................... 54

4 NO MEASURES OF SPECIAL REGULATION .............................................................. 57

5 ANNULMENT OF THE LEGACY LICENSING OBLIGATIONS ........................................ 57

5/57

1 Introduction

1.1 Legal basis

By virtue of Art. 20 of the Law concerning Electronic Communication (KomG)1 the Office for Communications (hereunder the "AK") is required to examine whether effective com-petition prevails on the electronic communication markets in Liechtenstein. If effective competition does not exist, that is, one or more providers possesses significant market power, the AK is to apply such measures of special regulation (under Art. 23 et seq. KomG) as are needed in order to remove or mitigate the competition problems that have been determined to exist. This procedure is termed market analysis.

The AK has defined the scope of the service and/or product markets that are to be investi-gated in the context of the market analysis in accordance with Art. 21(1) KomG. This was done taking into consideration the Recommendation on Relevant Markets by the EFTA Surveillance Authority.

The existence of significant market power � corresponding to a position of dominance in a market under general EEA competition law � has to be determined by taking into account in particular the criteria laid down in Art. 31 VKND.2

If the AK determines that one or more providers have significant market power in a de-fined market, it has the power to impose such measures of special regulation under Art. 34 to 43 VKND as are necessary and proportionate and suited to the removal or mitigation of the problems for competition obtaining on the market in question.

The following market analysis investigates in the first place the question of whether self-sustaining competition exists in an economic sense on the leased line markets in Liechten-stein or, as the case may be, whether self-sustaining competition would prevail in an eco-nomic sense without regulation. Such factors and competition problems as may stand in the way of such self-sustaining competition are identified. The presence of economic mar-ket power is investigated in this connection; in particular the criteria of Art. 31(1) to (3) VKND are considered according to their relevance for the market in question. Proceeding from the determination of providers having significant market power and the identifica-tion of relevant problems for competition on the leased line markets, the necessary measures of special regulation are assessed that are suited to redressing the problems for competition that have been determined.

1 Law of 17 March 2006 concerning electronic communication (Kommunikationsgesetz; KomG), LGBl. 2006 No. 91. 2 Ordinance of 3 April 2007 on electronic communication networks and services (VKND), LGBl. 2007 No. 67.

6/57

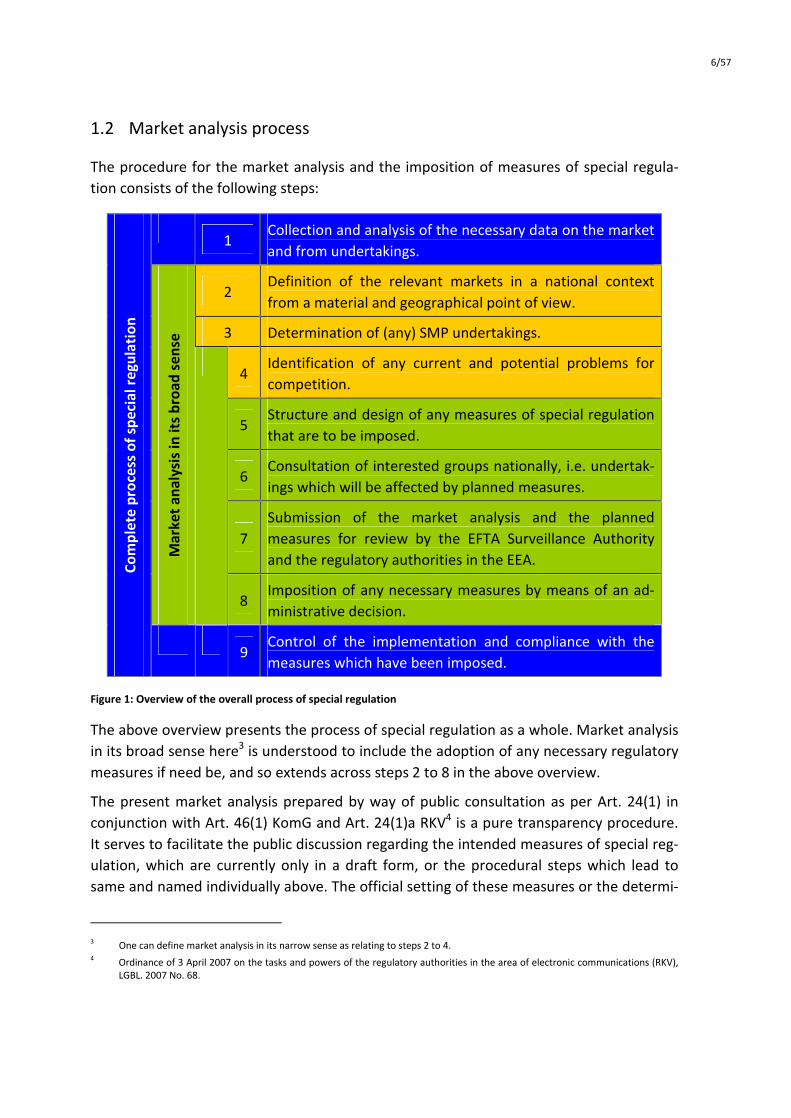

1.2 Market analysis process

The procedure for the market analysis and the imposition of measures of special regula-tion consists of the following steps:

Com

plet

e pr

oces

s of

spe

cial

reg

ulat

ion

1

Collection and analysis of the necessary data on the market and from undertakings.

Mar

ket

anal

ysis

in it

s br

oad

sens

e

2 Definition of the relevant markets in a national context from a material and geographical point of view.

3 Determination of (any) SMP undertakings.

4

Identification of any current and potential problems for competition.

5 Structure and design of any measures of special regulation that are to be imposed.

6 Consultation of interested groups nationally, i.e. undertak-ings which will be affected by planned measures.

7 Submission of the market analysis and the planned measures for review by the EFTA Surveillance Authority and the regulatory authorities in the EEA.

8 Imposition of any necessary measures by means of an ad-ministrative decision.

9

Control of the implementation and compliance with the measures which have been imposed.

Figure 1: Overview of the overall process of special regulation

The above overview presents the process of special regulation as a whole. Market analysis in its broad sense here3 is understood to include the adoption of any necessary regulatory measures if need be, and so extends across steps 2 to 8 in the above overview.

The present market analysis prepared by way of public consultation as per Art. 24(1) in conjunction with Art. 46(1) KomG and Art. 24(1)a RKV4 is a pure transparency procedure. It serves to facilitate the public discussion regarding the intended measures of special reg-ulation, which are currently only in a draft form, or the procedural steps which lead to same and named individually above. The official setting of these measures or the determi-

3 One can define market analysis in its narrow sense as relating to steps 2 to 4. 4 Ordinance of 3 April 2007 on the tasks and powers of the regulatory authorities in the area of electronic communications (RKV),

LGBL. 2007 No. 68.

7/57

nation of the preconditions required for same occurs in the special regulation procedure following same, in which the individual undertakings concerned have individual, concrete measures in accordance with Art. 23 KomG imposed on them by means of an administra-tive decision.

1.3 National consultation

To the extent that the AK foresees the adoption of measures of special regulation that are likely to have significant effects on the market concerned, it is obliged to announce this to interested parties in conformity with Art. 24(1) KomG and to give such parties the oppor-tunity to make their position known within a reasonable period. The AK is for this purpose empowered to hold public consultations (Art. 46 KomG in conjunction with Art. 24(1)a RKV).

The consultation procedure in accordance with Art. 24(1) and Art. 46(1) KomG for the purpose of the market analysis is a non-adversarial administrative procedure sui generis. It serves to assess the conditions for competition and the promotion of transparency by means of early and public discussion of the measures planned by the AK. A differentiation is to be drawn between the consultation procedure of the subject matter and the adver-sarial special regulation procedure subsequent to same in accordance with Art. 23(1) KomG, in the context of which the AK imposes individual concrete "obligations by imposi-tion (measures of special regulation)" on an undertaking with significant market power.

On 31 May 2012, AK has published the present ex officio analysis of the leased line mar-kets in Liechtenstein pursuant to Art. 24(1) in conjunction with Art. 46(1) KomG and Art. 24(1) RKV and invited interested parties to submit comments on the analysis and the measures of special regulation proposed in it in the context of a public consultation.

The following undertakings submitted comments by the end of the consultation period on 31 July 2012: upc cablecom GmbH, Telecom Liechtenstein AG, Swisscom (Schweiz) AG, Or-ange (Liechtenstein) AG and Liechtensteinische Kraftwerke. None of the respondents disa-greed with the market definition or the lack of designation of undertakings with significant market power.

All comments are, in so far as they are not subject to confidentiality, published on the AK's website.5 In addition AK evaluated the submitted comments in the separate document "Evaluation of comments related to the national consultation on the analysis of the leased line markets" dated 9 August 2012, which was also published on the website of the AK.

The comments were taken into consideration when preparing the final version of the market analysis in so far as they are in the AK's view of importance and/or entail conse-

5 Accessible at: http://www.llv.li/amtsstellen/llv-ak-marktanalysen/llv-ak-marktanalysen-aktueller_stand.htm.

8/57

quences. In accordance with Art. 47(1) KomG the "participation in a public consultation [...] does not constitute any legal rights above and beyond it".

1.4 EEA-wide consultation

If the AK intends to adopt measures of special regulation which are likely to have effects on trade between EEA States, the AK thus has in addition to the national consultation ex-ercise to consult the EFTA Surveillance Authority and the other NRAs in the EEA before-hand in conformity with Art. 7 of the Framework Directive 2002/21/EC6,7 (Art. 24(2) KomG). This EEA-wide consultation of the draft measures serves to establish transparency and the consolidation of the single market.

During a first phase, the EFTA Surveillance Authority is given a period of one month to re-view the present draft analysis and the planned measures. If the Authority expresses a reasoned doubt as to the compatibility with the applicable EEA law of measures that have been submitted, it can extend this period by two months in order to allow further investi-gation of the matter. If no such doubts exist, the AK can adopt the measures that were submitted. On the other hand, if the EFTA Surveillance Authority comes to the conclusion within the extended period that the market definition submitted or the analysis of signifi-cant market power is contrary to applicable EEA law, it can forbid the AK from bringing the planned measures into force.

With regard to the structure and design of the concrete measures of special regulation per se, i.e. the obligations which are imposed on providers, the EFTA Surveillance Authority has solely the competence to comment on them, not to reject them. If the EFTA Surveil-lance Authority does comment on a draft measure submitted, then the AK has to take its comments into utmost account.

All relevant documents and published information related to the submission of planned measures of special regulation by the AK are accessible via the electronic portal8 of the EFTA Surveillance Authority. All public documents related to the national consultations are viewable on the AK's website.9

6 Directive 2002/21/EC of the European Parliament and of the Council of 7 March 2002 on a common regulatory framework for

electronic communications networks and services ("Framework Directive"; Liechtenstein Compendium of EEA Law ("EWR-Rechtssammlung"): Annex XI � 5cl.01).

7 For the details of the notification procedure according to Art. 7 of the Framework Directive see also: EFTA Surveillance Authority Recommendation of 2 December 2009 on notifications, time limits and consultations provided for in Article 7 of the Act referred to at point 5cl of Annex XI to the Agreement on the European Economic Area (Directive 2002/21/EC of the European Parliament and of the Council on a common regulatory framework for electronic communications networks and services), as adapted by Pro-tocol I thereto (Case No: 65615, Event No: 514868). Currently not available in German. Published in English at: http://www.eftasurv.int/media/internal-market/recommendation.pdf.)

8 https://eea.eftasurv.int/portal/ 9 http://www.ak.llv.li/

9/57

1.5 Basic aspects of the market analysis

From an economic viewpoint, the position of significant market power is related to an un-dertaking's power to increase prices without having to suffer significant sales losses. In accordance with the thesis of equivalence from the EFTA Surveillance Authority and the European Commission, effective competition prevails on a market when no undertaking on the market possesses a position of significant market power.10

In the following market analysis, the terms "effective competition", "functioning competi-tion", "competition that is effective" are used synonymously. Effective competition pre-supposes that the competition also exists without any ex ante regulation (anticipatory regulation) on this market, but taking into consideration ex ante regulations on other mar-kets of relevance for this market. If the competition on one market is also not dependant on regulations on other markets, not only is the competition effective, but also self-sustaining. Accordingly in the market analysis, the conditions for competition are to be assessed as if no ex ante regulations affecting this market exist (this is also termed the "greenfield approach"). Otherwise the danger exists that effective competition is ascer-tained for a market although the market outcome is primarily determined by existing regulation and not by competitive forces. The consequence of this would be that (at least over the medium term) structurally driven competition deficits arise and dominant market operators abuse their position to the detriment of the consumers.

1.6 Composition of the market analysis

The market analysis is composed as follows: After the general section in the present Chap-ter 1, an introduction to the subject matter under investigation is provided in Chapter 2. Initially, the essential developments in the markets under investigation are described be-fore, commencing with the definition of the relevant markets from a material and geo-graphical point of view, the products and services contained in them as well as the regula-tory situation to date are presented. The analysis of competition itself occurs in Chapter 3, in which the question of the effectiveness of the competition as well as the presence of market power is answered. Doing so, all aspects for the assessment of relevant market power indicators are examined. In section 3.6, the overall evaluation is conducted as to whether effective competition prevails on the markets under investigation, self-sustaining competition exists from an economic viewpoint without regulation, or which competition problems and factors are in conflict with this as the case may be. In the event that no ef-fective competition prevails, the most fundamental market power abuse potentials and competition problems are then analysed and the regulatory measures that are required

10 Cf. section 3.1.1.

10/57

for redressing the competition problems that have been ascertained as the case may be are discussed.

1.7 Time frame

Art. 21(2) KomG lays down that the conditions for competition in the defined markets are to be reviewed regularly by the AK. The time frame for the present market analysis amounts to two to three years. The AK will continue to keep the markets concerned under further observation during this period and, if necessary, initiate a fresh market analysis.

1.8 Sources of data

The essential data that provide the basis for the following market analysis were collected by the AK by means of an annual questionnaire to operators. The collection of market data takes place each year in the spring/summer in relation to the preceding calendar year. For reasons of proportionality, any collection of the requested data between these intervals is normally only conducted additionally if this seems to be indicated due to a rapid change in market conditions or by other special reasons.

To supplement the data gathered in the context of the annual questionnaires to opera-tors, data obtained under the previous legal framework is used as necessary. No further reference is made in the following market analysis to these data or to the data collected during the survey of operators; all other external sources of data are only referred to spe-cifically as necessary. Additionally, the AK keeps the markets in question, like other rele-vant markets, under constant observation. Hence the present analysis also relies on the AK's further current information and data.

1.9 Competition authority

Liechtenstein has no national competition law beyond the rules of competition applicable under the EEA Agreement. Nor does Liechtenstein have an independent competition au-thority at present. Legal recourse in competition cases is therefore to be sought in accord-ance with the applicable EEA law before the ordinary national courts or by referring the matter to the EFTA Surveillance Authority or the European Commission respectively. The exception to this is the Office for Trade and Transport by virtue of Art. 2(1) of the Law of 23 May 1996 on the Implementation of the Rules of Competition in the European Economic Area, LGBl. 1996 No. 113, under which that Office has responsibility for the implementa-tion of competition rules to the extent that the courts do not have jurisdiction. This re-sponsibility is however essentially directed towards supporting the EFTA Surveillance Au-

11/57

thority and the undertaking of actions by the State, and not towards the material applica-tion and enforcement of EEA competition rules.

For these reasons, cooperation with and consultation of a competition authority in the sense of the second sentence of Art. 16(1) of the Framework Directive 2002/21/EC11 is not possible in the case of the present market analysis in Liechtenstein.

11 Directive 2002/21/EC of the European Parliament and of the Council of 7 March 2002 on a common regulatory framework for

electronic communications networks and services ("Framework Directive"; Liechtenstein Compendium of EEA Law ("EWR-Rechtssammlung"): Annex XI � 5cl.01).

12/57

2 The markets to be investigated

2.1 The Liechtenstein fixed network sector in general

The fixed network sector in Liechtenstein was characterised until the end of 2007 by three separate undertakings: LTN Liechtenstein TeleNet AG (LTN; for wholesale services), Tele-com FL AG (TFL; for retail services) and LIE-COMTEL AG (for CATV services).12 On 1 January 2008, all three undertakings were merged into Telecom Liechtenstein AG (hereunder called "TLI") and now exist only under this name.

Before then, the provision of telecommunications in Liechtenstein took place up to 1998 under the PTT Treaty of 1978 between Liechtenstein and Switzerland. The network in Liechtenstein was an integral part of the Swiss telephone network (Schweizerische Post-, Telefon- und Telegrafenbetriebe or the subsequent Swisscom AG). The network components situated in Liechtenstein, and especially the copper pair based access net-work as well, were provided, maintained and operated by Swisscom in the name and on the account of the Liechtenstein State. Their owner was the Liechtenstein State. In 1998, separation from the Swiss telephone network took place upon the liberalisation of the tel-ecommunications sector and with the founding of the former LTN.

LTN was only entrusted with the operation of the network. The retail customer relation-ship was transferred to the former Telecom FL AG, which belonged to Swisscom, following an invitation for tenders in relation to the provision of basic services. Telecom FL was then taken over 100% by LTN in 2003 following an increase in LTN's capital. The full merger of the two undertakings as "Telecom Liechtenstein AG" took place on 1 January 2008. TLI remains under complete State ownership.

Before integration into TLI at the beginning of 2008 under the name LIE-COMTEL, the ca-ble television (and internet) provider for the majority of Liechtenstein13 belonged to Liechtensteinische Kraftwerke (LKW) until the end of 2006. LKW, which is also 100% State-owned, is also responsible for the development and maintenance of the copper, optical fibre and cable TV infrastructure in Liechtenstein.

In 2006, LTN and LKW signed a so-called "consolidation agreement". The agreement's purpose is to concentrate all retail customer relationships and "intelligent" network com-ponents in the hands of LTN (now TLI) and to combine all passive network components, including in particular the access network, transmission lines, cable ducts, etc., in LKW's

12 Lie-COMTEL AG was originally founded by Liechtensteinische Kraftwerke (LKW) as a stand-alone undertaking but existed at the

time of the transfer to LTN only as a brand name and business that was part of LKW. The CATV network remained with LKW also after the transfer of the services platform and customers to TLI.

13 LKW operates a cable TV network (CATV) in nine of the eleven Liechtenstein municipalities: Balzers, Triesen, Triesenberg, Vaduz, Schaan, Planken, Gamprin-Bendern, Ruggell and Schellenberg. The CATV network in Schellenberg belongs to the municipality but is operated by LKW. Hereunder, LKW is always regarded as being inclusive of the municipality of Schellenberg's CATV network.

13/57

hands. LKW should henceforth no longer be active on the retail customer market, but ra-ther only on the wholesale market. The agreement was put into effect on 1 January 2007 through the transfer of LTN's passive network infrastructure to LKW. At the same point in time LIE-COMTEL was integrated into the former LTN by transferring the customer rela-tionships and taking over the services platform as well as the active network components; the passive (and a few active) CATV network components remained in LKW's hands.

LKW has thus been the owner of the above named fixed access networks in Liechtenstein since 1 January 2007. In addition to copper pair (TPCW) based subscriber connections, these also consist of optical fibre (fibre access) and CATV (coaxial access). Furthermore, LKW also operates copper and fibre optic based infrastructure for the core network and leased lines (dark copper and dark fibre). LKW uses this infrastructure to provide whole-sale services to carriers and providers. By contrast, only TLI is active on the retail customer market.14

In addition to LKW, TV-COM AG (formerly Matt Antennentechnik AG15) is active in Liech-tenstein as a further cable network operator in the municipalities of Mauren/Schaanwald and Eschen/Nendeln). There is no overlap between the area supplied by TV-COM AG and that of LKW's CATV network. Both firms taken together cover practically 100% of the households in Liechtenstein.

2.2 Preliminary remarks on the market definition

In accordance with the Guidelines (hereunder called the "SMP Guidelines") of the EFTA Surveillance Authority on market definition and the assessment of significant market power,16 the basis for the definition of the materially relevant market is a test of substi-tutability on the demand and supply sides of the product or service in question. Those products all belong to the same market when both consumers and providers see them as sufficiently interchangeable. A generally acknowledged procedure for determining this is provided by the so-called SSNIP test (small but significant non-transitory increase in price � SSNIP) or the test of the hypothetical monopolist.17

The EFTA Surveillance Authority in its 2008 Recommendation on Relevant Markets18 has identified in accordance with Art. 15 of the Framework Directive 2002/21/EC those mate-

14 As per the implementing arrangement to the merger agreement of 05.10.2007 (not public) and actual range of services. 15 The former Matt Antennentechnik AG changed its name on 09.03.2011 to TV-COM AG with its registered office in Eschen. 16

Guidelines of the EFTA Surveillance Authority of 14 July 2004 on market analysis and the assessment of significant market power under the common regulatory framework for electronic communications networks and services referred to in Annex XI of the Agreement on the European Economic Area, OJ C 101, 27.04.2006, page 1.

17 The SSNIP test examines whether the consumer as a reaction to a 5 to 10% increase in the price of a good by a hypothetical mo-

nopolist (HM) increasingly demands a substitute product instead so that the price increase is no longer profitable for the HM due to the induced reduction in the volume caused by the elasticity of the demand.

18 EFTA Surveillance Authority Recommendation of 5 November 2008 on relevant product and service markets within the electronic communications sector to be considered for ex ante regulation in accordance with the Act referred to at point 5cl of Annex XI to

14/57

rially relevant product and service markets which can be considered for ex ante (anticipa-tory) regulation. It is to be assumed that for these markets � because the EFTA Surveil-lance Authority has already examined whether the applicable criteria are fulfilled � ex ante regulation will also be considered in Liechtenstein. Hence, the AK does not have to repeat this examination as the competent regulatory authority, unless it has reasonable doubt as to the criteria's specific concordance with the national context or the definition of the rel-evant national product market deviates from that which has been recommended.19

The AK is to define, to a material and geographical extent, the service or product markets respectively that are to be investigated in accordance with Art. 21(1) KomG in the context of the AK market analysis, while taking into consideration to the greatest degree possible the Recommendation on Relevant Markets by the EFTA Surveillance Authority. If and to the extent that the AK defines markets which deviate from the Recommendation on Rele-vant Markets by the EFTA Surveillance Authority, it has to ensure in advance in accordance with the same stipulation that the following three criteria are cumulatively fulfilled (here-under called the "three-criteria test"):

a) Significant entry barriers of a structural, legal or regulatory nature persist.

b) The market does not tend towards effective competition within the relevant timeframe. When assessing this criterion, the level of competition behind the bar-riers to entry is to be examined.

c) Competition law by itself is insufficient to adequately address the market failure concerned.

2.3 The leased line markets

2.3.1 Definition of a leased line

Commencing with the legal definition of Art. 3(1)(24) KomG, leased lines are understood hereunder to be facilities which provide a precisely defined transparent transmission ca-pacity between two network termination points20 (symmetric bi-directional) located in Liechtenstein. A further characteristic of leased lines is the lack of switching functionality, i.e. the user does not have any controlling options available to them (lack of an on-demand switching function). This definition is applicable for both leased lines on the retail level, as well as for those on the wholesale level.

the EEA Agreement (Directive 2002/21/EC of the European Parliament and of the Council on a common regulatory framework for electronic communication networks and services), as adapted by Protocol 1 thereto and by the sectional adaptations contained in Annex XI to that Agreement, OJ C 156, 09.07.2009, page 18.

19 Cf. comments of the EFTA Surveillance Authority of 6 September 2005 on the submission of the first Norwegian decision on mo-bile termination markets, section 3.2.

20 With leased lines on the wholesale level, the network termination point is also understood to mean the point of interconnection (POI) between the contractual partners.

15/57

In line with this definition, there are three characteristics which have to exist cumulatively in order to classify a leased line as a transmission facility:

A leased line is a symmetric bi-directional point-to-point connection with a fixed capacity capable of data and voice traffic.

A leased line is a transparent transmission facility: Transparency describes the property whereby payload data bits are transmitted unchanged from a transmis-sion facility.

A leased line is a transmission facility without switching functionality: This means that the user has no option for controlling the connection.21

It is fundamentally irrelevant for the classification of a transmission facility as a leased line via which technology its establishment occurs. The decisive factor is the function for the user and not the kind of technical establishment between the two customer interfaces or the product description on the market respectively. As a rule, internet access types pro-vide on-demand switching functionality � regardless of the kind of connection technology utilised e.g. xDSL, coaxial cable (CATV), WLAN � and are thus not to be classified as a leased line.

Leased lines are used by both retail customers for a connection from locations or to estab-lish private networks, as well as by operators as a wholesale service product to provide communication services to retail customers. Thus, retail and wholesale markets may fun-damentally be defined in parallel.

On the wholesale level, a differentiation can be drawn between markets for trunk (long distance) line segments on the one hand and terminating segments of leased lines on the other hand. The exact extent to which the differentiation is to be undertaken between these two markets in a national context depends on the given network topography and is at the discretion of the regulatory authority.22 The differentiation of these two markets in accordance with the circumstances in Liechtenstein occurs in the next section.

2.3.2 The material definition of the leased line markets

At the wholesale level leased lines are provided for use by other communication network operators or service providers. A differentiation may be drawn between two relevant wholesale markets: The market for trunk segments on the one hand and the market for

21 The lack of switching functionality results from the fact that no connection control information is analysed from the bitstream at

the user interface within the transmission facility. 22 Cf. Commission Staff Working Document (Explanatory Note) accompanying the Commission Recommendation on Relevant Prod-

uct and Service Markets within the electronic communications sector susceptible to ex ante regulation in accordance with Di-rective 2002/21/EC of the European Parliament and of the Council on a common regulatory framework for electronic communi-cations networks and services (Second edition) � SEC (2007) 1483, hereunder called "Commission Explanatory Note", page 38.

16/57

terminating segments on the other hand. Both markets fundamentally cover leased lines without any bandwidth restrictions.

The differentiation between a trunk and a terminating segment occurs on the basis of the physical line routing: With trunk segments it concerns leased lines or leased line sections23 on the wholesale level which connect two points of interconnection (POI) � as a rule at the main distribution frame (MDF) or at the intermediate distribution frame (IDF) of two ac-cess network areas � of the operator providing same. It is characteristic of trunk segments that as a rule they do not reach the network termination point of the retail customer.

Terminating segments are regarded as all leased lines or leased line segments at whole-sale level, which are not classified as trunk segments. As a rule, these are (at least for bandwidths of < 8 Mbit/sec)24 twisted pair copper wires (TPCW) or a multiple of them that extend from the main distribution frame (MDF) to the network termination point of the retail user.

Thus, trunk segments of leased lines are as a rule assigned to the core network, while ter-minating segments are assigned to the access network. While the user receives exclusive access to the complete connection line available with the terminating segment of a leased line, as a rule trunk leased lines transmit the data streams of several users together (with a fixed capacity provided permanently for each user) and transport larger volumes of infor-mation.

The LKW's twisted pair copper based access network in Liechtenstein currently consist of a total of 30 access domains and thus trunk segment points of interconnection.25

The differentiation between trunk segments and terminating segments may also be un-dertaken in the same way for leased lines established via optical fibre (fibre optic cable � FOC). Terminating segments of FOC leased lines as a rule also converge in the same TPCW access domains in optical distribution frames (ODF),26 which can be found as a rule in the same places as the main distribution frame (MDF) or intermediate distribution frame for TPCW lines. The number of optical distribution frames (ODF) will increase further over the coming years with the progressive expansion of the FOC access network (fibre to the home � FTTH).27 Thus, there are trunk segment points of interconnection at the points named for leased lines provided via optical fibre. Consequently, trunk segments of leased lines run between these points.

23 For the purpose of defining the market at the wholesale level, it is necessary to introduce the term "leased line section". A

wholesale leased line which falls in both the market for trunk segments as well as in that for terminating segments due to its line routing is separated into sections which are assigned to the respective markets.

24 TLI establishes customer connections up to a capacity of 2,048 kbit/sec (E1 lines) via TPCW lines or optical fibre (FOC) and higher bandwidths fundamentally via an STM-1 FOC connection.

25 Source: LKW "Approved Reference Offer and Cost Accounting Model" dated 20.04.2012. 26 Also called "E2000 optical distribution frame" or splice box. 27 Cf. the Government press release dated 29.06.2010: "Ambitious broadband supply aim for Liechtenstein / supply planned across

the complete country by 2020".

17/57

Moreover, the line sections located in Liechtenstein of cross-border leased lines, i.e. so-called international half circuits, are to be assigned to the trunk segments.

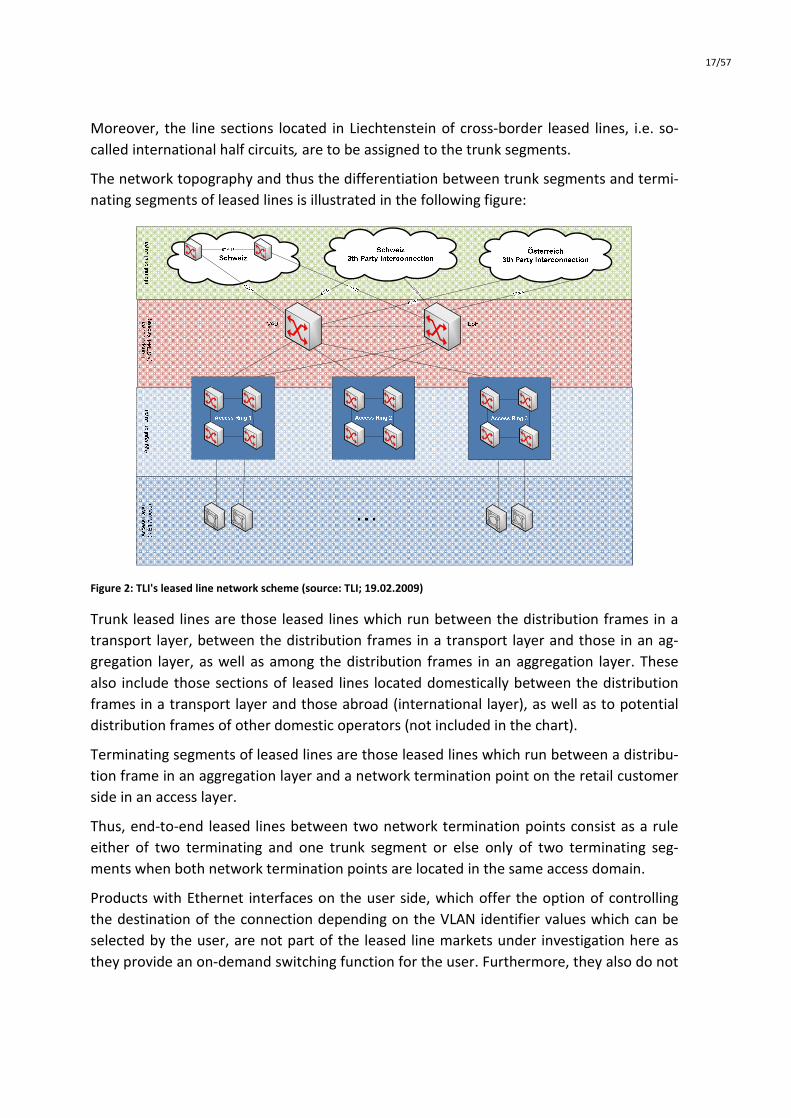

The network topography and thus the differentiation between trunk segments and termi-nating segments of leased lines is illustrated in the following figure:

Figure 2: TLI's leased line network scheme (source: TLI; 19.02.2009)

Trunk leased lines are those leased lines which run between the distribution frames in a transport layer, between the distribution frames in a transport layer and those in an ag-gregation layer, as well as among the distribution frames in an aggregation layer. These also include those sections of leased lines located domestically between the distribution frames in a transport layer and those abroad (international layer), as well as to potential distribution frames of other domestic operators (not included in the chart).

Terminating segments of leased lines are those leased lines which run between a distribu-tion frame in an aggregation layer and a network termination point on the retail customer side in an access layer.

Thus, end-to-end leased lines between two network termination points consist as a rule either of two terminating and one trunk segment or else only of two terminating seg-ments when both network termination points are located in the same access domain.

Products with Ethernet interfaces on the user side, which offer the option of controlling the destination of the connection depending on the VLAN identifier values which can be selected by the user, are not part of the leased line markets under investigation here as they provide an on-demand switching function for the user. Furthermore, they also do not

670��

18/57

include products with user-side X.25, Frame Relay, ATM and IP interfaces at the network termination points which offer the option to control the destination of the connection de-pending on the values of a connection control parameter (examples of connection control parameters are: Logical channel number, data link connection identifier (DLCI), virtual connection identifier (VCI), virtual path identifier (VPI) or destination IP address), as well as products with user-side Ethernet interfaces to more than two network termination points, which terminate an Ethernet frame sent at one customer interface to several or all other customer interfaces of this product.

Unlit optical fibre as well as twisted pair copper lines not in service are not part of the rel-evant leased line markets because they provide no specific transparent transmission ca-pacity. To the extent that these unlit cables or not switched on lines are located in the ac-cess network domain, they are to be assigned instead to the already defined market for physical access to network infrastructures at fixed locations (M4). With regard to unlit op-tic fibre in core networks (dark fibre/fibre channels), these are to be assigned to an sepa-rate wholesale market still to be defined as the case may be for the physical access to network infrastructures for high capacity transmission routes in a core network. The AK is currently assessing the conditions for the definition and regulation of such a market and will conduct an independent consultation process in this respect as required.

In addition to those services which are provided to third parties, self provided services (self supply) which are used for the internal provision of retail customer leased lines or for own use are also taken into consideration in the present leased line markets on the wholesale level. Thus, self supply is part of the market, as the market power of a hypo-thetical monopolist on the wholesale level is also restricted by such undertakings which also or solely provide the wholesale service concerned internally. As a 5 to 10% increase in the prices on the wholesale market also in general leads to an increase in the prices on the retail market,28 it is always then unprofitable when sufficiently large numbers of custom-ers switch to vertically integrated providers as a reaction to the price increase. Moreover, self supply is also relevant to the extent that an undertaking which provides leased lines internally can also offer these externally (or actually does this) and thus the internally pro-vided capacities of this undertaking potentially restrict the external provider of leased lines competitively.

28 For providers of leased lines to retail customer markets, which purchase the leased lines on a wholesale market, wholesale

leased lines represent a very high share of the complete costs.

19/57

2.4 Definition of the relevant product markets

2.4.1 The Recommendation on Relevant Markets and the three-criteria test for ex ante regulation

The 2004 Recommendation on Relevant Markets29 by the EFTA Surveillance Authority, which has been amended in the meantime, still defined three relevant leased line mar-kets:

The market for the minimum set of leased lines with specific types of leased lines up to and including 2 Mbit/sec (retail market)

The market for trunk segments (wholesale market)

The market for terminating segments (wholesale market).

In its revised and currently applicable 2008 Recommendation on Relevant Markets,30 the EFTA Surveillance Authority removed the retail market for the minimum set of leased lines as well as the wholesale market for trunk segments of leased lines from the list of markets to be considered for ex ante regulation. The wholesale market for terminating segments was the sole leased line market (as Market No. 6 of the applicable Recommendation) to be retained. Thus, after a separate EEA/EFTA-wide consultation, the Authority for its part fol-lowed without exceptions the revised 2007 market recommendation31 of the European Commission, which is applicable in the EU. With respect to the revision of its Recommen-dation, by its own admission the EFTA Surveillance Authority did not align itself to the lev-el of the market development in the EEA/EFTA states, but rather to that in the complete EEA, and thus predominantly to the level of the market development in the EU Member States.32

The AK presented, in its statement dated 27 June 2008 as well as on the occasion of the workshop dated 16 September 2008 held in this respect in the context of the consulta-tions conducted by the EFTA Surveillance Authority on the revision of the Market Recom-mendations, the special national (market) circumstances worthy of consideration which, in the opinion of the AK, spoke for the retention of the wholesale market for trunk segments of leased lines in the revised Recommendation.

29 EFTA Surveillance Authority Recommendation No. 194/04/KOL of 14 July 2004 on relevant product and service markets within

the electronic communications sector to be considered for ex ante regulation in accordance with the common regulatory frame-work for electronic communication networks and services in the Agreement on the European Economic Area Directive 2002/21/EC of the European Parliament and of the Council), OJ L 113, 27.04.2006, page 18.

30 Cf. footnote 17. 31 Commission Recommendation 2007/879/EC of 17 December 2007 on relevant product and service markets within the electronic

communications sector to be considered for ex ante regulation in accordance with Directive 2002/21/EC of the European Parlia-ment and of the Council on a common regulatory framework for electronic communications networks and services, OJ L 344, 28.12.2007, page 65.

32 Cf. Recital 18, second sentence, 2008 Recommendation on Relevant Markets by the EFTA Surveillance Authority.

20/57

The EFTA Surveillance Authority explicitly clarified in Recital 21 of its 2008 Market Rec-ommendations that the removal of a market from the Recommendation does not neces-sarily mean that effective competition prevails on the market in question in each EEA/EFTA state and that ex ante regulation is no longer justified for this market. In this connection, it referred especially to the comments received in the context of the consulta-tions.

The EFTA Surveillance Authority further stated that: "For markets not listed in this Rec-ommendation national regulatory authorities should apply the three-criteria test to the market concerned. For the markets in the Annex to Recommendation No 194/04/COL of 14 July 2004, which are not listed in the Annex to this Recommendation, national regulatory authorities should have the power to apply the three-criteria test in order to assess wheth-er, on the basis of national circumstances, a market is still susceptible to ex ante regula-tion."33

Commencing with the recommendatory character of the Recommendation on Relevant Markets by the EFTA Surveillance Authority, a regulatory authority thus continues to be free to consider as required markets as relevant for the ex ante regulation which are not listed (anymore) in the Recommendation on Relevant Markets by the EFTA Surveillance Authority, provided it demonstrates the cumulative fulfilment of the three-criteria test under the specific national circumstances: The existence of significant persistent barriers to entry, the lack of a tendency towards effective competition and the insufficiency of the means under general competition law to redress the market failure ascertained. This three-criteria test can also be found in Art 21(1) second sentence KomG.

2.4.2 The application of the three-criteria test to the trunk leased line market

The AK continues to regard the three criteria stipulated in Art 21(1) second sentence KomG to be fulfilled with respect to the wholesale market for trunk segments of leased lines in Liechtenstein for the following reasons:

Unlike numerous other EEA states, Liechtenstein has to date not been able to ascertain any duplication34 of trunk segments of leased lines by alternative operators. While it is true that the mobile network operators have partly established radio link connections in order to connect parts of their network to their gateway-MSCs, however this is often only for redundancy purposes and geographically limited to their own antenna sites. A cable connection alternative trunk infrastructure also only exists to an isolated extent, as well as in the form of short and customer-specific line sections with only a sporadic geographic

33 Recital 22, second and third sentence, 2008 Recommendation on Relevant Markets by the EFTA Surveillance Authority. 34 The determination of the progressive duplication of trunk leased line connections in numerous EEA states moved the European

Commission, and consequently the EFTA Surveillance Authority, to remove the market for trunk leased lines designated as rele-vant previously for ex ante regulation from the revised 2008 Market Recommendations (cf. Commission Explanatory Note, page 38).

21/57

presence as a rule. Likewise, the network of the sole alternative CATV network operator, TV-COM AG, is limited to the area of the two Eschen and Mauren municipalities.

Thus, apart from these exceptions, no general duplication of the national trunk leased line routes can be observed in Liechtenstein. In other words, alternative operators have not established their own leased line capacities in a core network, and especially between the main distribution frames (MDF), intermediate distribution frames (IDF) and optical distri-bution frames (ODF), which represent the points of interconnection (POI) to the access network or to the terminating segments respectively.

This lack of alternative capacities can be traced back to the low traffic volume and income on these routes and the high line construction sunk costs linked to such a duplication, which represent persistent barriers to entry onto this market. For these reasons, the AK also does not expect any duplication of trunk leased line routes in the foreseeable future. Consequently, it can be ascertained that on the wholesale market for trunk leased lines, no tendency to develop (self-sustaining) competition will occur in the anticipated period under consideration of this market analysis and that high and persistent market entry bar-riers will continue to exist.

Following the sale of the passive network infrastructure from TLI (previously LTN) to LKW, there were initially two undertakings, TLI and LKW, which offered leased line products ex-ternally on the wholesale level. However since 2010, LKW has not offered leased lines on the wholesale level anymore, but rather only dark fibre or dark copper respectively. Thus, TLI is currently the de facto sole provider of leased lines to external wholesale service buyers. All other operators only provide leased line services for self supply or for their own retail customers. However, as TLI is also dependent for the provision of leased lines in the access network and the core network on the wholesale inputs of LKW in the form of unlit optical fibre and copper lines (dark fibre and dark copper), ultimately only LKW can or could respectively provide by its own means cable based leased lines across the complete country.35

LKW does not itself offer leased lines on the retail market. Even though LKW on the one hand currently does not de facto provide leased lines on the wholesale level and on the other side guarantees access to its infrastructure under non-discriminatory conditions, it is still correct that LKW itself also could be active on the wholesale market for trunk leased lines as a provider and thus a competitor, and consequently incentives fundamentally ex-ist for anti-competitive behaviour, and especially to charge excessive (or allocation ineffi-cient) prices or to practice margin squeezes. The access conditions and prices for trunk

35 The access to not switched on/unlit TPCW or FOC is currently not subject to special regulation. The LKW has unilaterally guaran-

teed non-discriminatory access to these wholesale service inputs. The obligation to provide access to not switched on/unlit ca-bles by means of measures of special regulation in other markets than the present one, and especially the wholesale market for the (physical) access to network infrastructures (Market No. 4 of the market definitions announced) and a wholesale market still to be defined as the case may be for physical access to the core network, remains reserved.

22/57

leased lines are not currently subject to regulation. There is no relevant wholesale regula-tion for the trunk leased line market at present � unlike the wholesale regulation for ac-cess to the physical infrastructure in the access network (M4 Market). In accordance with the greenfield approach, in any case the competitive conditions are to be assessed by the AK in such a way as though there is no relevant regulation for the present market on the market itself or on upstream markets.

Consequently, it must be concluded that high and insurmountable market entry barriers continue to exist on the wholesale market for trunk leased lines. No tendency towards ef-fective competition can be observed. The lack of an independent competition authority in Liechtenstein and the fact that any legal action in accordance with general EEA competi-tion law has to be brought before the ordinary national courts or the EFTA Surveillance Authority � should it have jurisdiction � coupled with the probable requirement of an on-going and detailed intervention in cases of competition problems on this market (and es-pecially to fight the problem of excessive prices) make it obvious that general competition law is inadequate for successfully countering potential competition problems on the trunk leased line market.36

For these reasons, the AK has ascertained that the three-criteria test as per Art. 21(1) sen-tence two KomG is (still) fulfilled with respect to the wholesale market for trunk segments in Liechtenstein and ex ante regulation of this market is still to be considered.

2.4.3 The market for terminating segments of leased lines

With respect to terminating segments of leased lines, there are also clearly high and in-surmountable barriers to market entry. A tendency towards effective competition cannot be observed, nor is it to be expected in the foreseeable future. This is the case for the rea-son that the provision of terminating segments of leased lines continues to be dependent in one form or another on access to the fixed access network across the complete country. While it is true that simplified access options to the infrastructure in the access domain are available due to the measures of special regulation imposed on the market for physical access (M4), however the circumstances on the market for terminating segments of leased lines are to be assessed, in the sense of the greenfield approach to be applied, in such a way as though there were no relevant regulation for same on the market itself or on upstream markets.

Also with respect to terminating leased lines, general competition law is to be categorised as insufficient, for the reasons described already in section 2.4.3 concerning trunk leased lines, in order to redress the competition problems arising on this market. Hence, ex ante

36 Even if a competition authority was able to successfully deal with the competition infringements, general competition law would

not be suitable for handling the persistent access and price setting or cost accounting problems respectively, as well as the con-tinuous monitoring of the access conditions, including the technical parameters.

23/57

regulation is to still be considered for this market, also in Liechtenstein, as provided for by the 2008 Recommendation on Relevant Markets by the EFTA Surveillance Authority.

2.4.4 The market for the minimum set of specific retail customer leased lines

The demand for retail customer leased lines with a bandwidth of less than 2 Mbit/sec, and thus those leased lines subject to date to a minimum provision obligation, has decreased significantly over the last few years due to the fact that other substitution technology (and especially xDSL) can be utilised for this and the general requirement for bandwidth has grown drastically.

Apart from that, effective special regulation can secure functioning competition on the upstream wholesale level and protect the consumers on the retail customer markets. This is also true for retail customer leased lines with a bandwidth of more than 2 Mbit/sec, which were not subject to any minimum provision obligation up to then.

Thus, if the required measures of special regulation are taken on the leased line wholesale markets, there only remain low barriers to the market entry of alternative providers on the leased line retail market. For these reasons, it is no longer appropriate to envisage the provision of a minimum set of retail leased lines and the obligations which exist in this re-spect should be rescinded accordingly. Apart from that, the European Commission has de-leted the list of the minimum set of retail leased lines to be provided without any re-placement, and thus there is also no need for regulation anymore for the same reason.37 Ultimately, this approach corresponds to the "wholesale service regulation before regula-tion on the retail markets" premise.

2.4.5 The materially relevant leased line markets � conclusion

On the basis of the explanations provided above and under consideration of the circum-stances in Liechtenstein, two material markets in the leased line area are to be defined for ex ante regulation consideration:

a) The wholesale market for terminating segments of leased lines

b) The wholesale market for trunk segments of leased lines.

The market for terminating segments of leased lines under a) corresponds to Market No. 6 of the Recommendation on Relevant Markets by the EFTA Surveillance Authority:

"Wholesale terminating segments of leased lines, irrespective of the technology used to provide leased or dedicated capacity" (wholesale market).38

37 Decision 2008/60/EC of the Commission dated 21 December 2007 on the amendment to Decision 2003/548/EC concerning the

deleting of certain kinds of leased lines from the minimum set of leased lines, OJ L 15, 18.1.2001, page 32. 38 The European Commission has described the underlying material product markets in its explanatory remarks to the market rec-

ommendation, Explanatory Note (Commission staff working document SEC2007/1483) to Commission Recommendation

24/57

Due to the fulfilment of the three-criteria test as per Art. 21(1) second sentence KomG, the AK has additionally defined the following wholesale market for trunk leased lines as a material market for ex ante regulation consideration and assumes this in the market anal-ysis hereunder:

Wholesale trunk segments of leased lines, irrespective of the technology used to provide leased or dedicated capacity (wholesale market).

2.5 The development of the leased line markets

The undertakings active on the materially relevant leased line markets and their products as well as the market shares and their development are presented and investigated here-under.

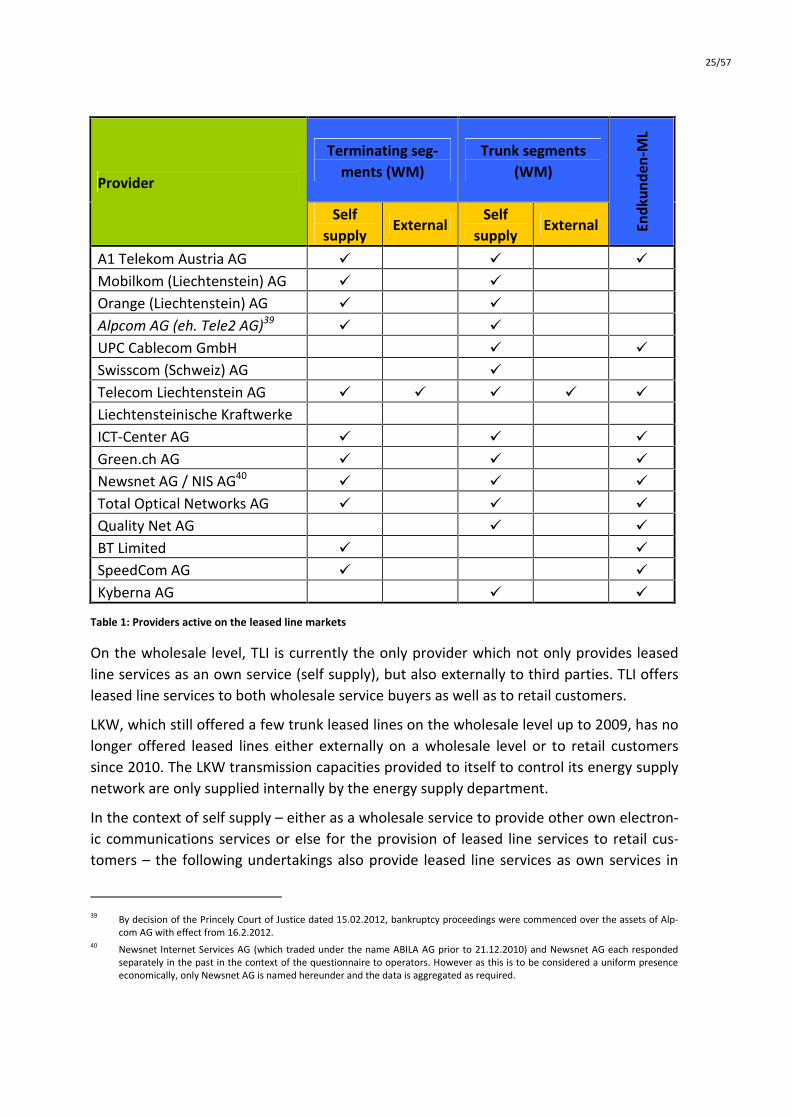

2.5.1 Providers

Initially, the providers active on the two relevant leased line wholesale markets are identi-fied. In this connection, a differential is also to be drawn between the (pure) provision of own services (self supply) and the external provision of leased line capacities to third par-ties.

The providers of retail leased line products are not relevant for the present market analy-sis, as this market is not under consideration (anymore) for ex ante regulation. However it is also included hereunder for the sake of completeness and to allow for a better differen-tiation.

2007/879/EC of 17 December 2007 on Relevant Product and Service Markets within the electronic communications sector to be considered for ex ante regulation in accordance with Directive 2002/21/EC of the European Parliament and of the Council on a common regulatory framework for electronic communications networks and services, OJ L 344, 28.12.2007, page 65.

25/57

Provider

Terminating seg-ments (WM)

Trunk segments (WM)

Endk

unde

n-M

L

Self supply

External Self

supply External

A1 Telekom Austria AG Mobilkom (Liechtenstein) AG

Orange (Liechtenstein) AG

Alpcom AG (eh. Tele2 AG)39

UPC Cablecom GmbH Swisscom (Schweiz) AG

Telecom Liechtenstein AG Liechtensteinische Kraftwerke

ICT-Center AG Green.ch AG Newsnet AG / NIS AG40 Total Optical Networks AG Quality Net AG BT Limited SpeedCom AG Kyberna AG

Table 1: Providers active on the leased line markets

On the wholesale level, TLI is currently the only provider which not only provides leased line services as an own service (self supply), but also externally to third parties. TLI offers leased line services to both wholesale service buyers as well as to retail customers.

LKW, which still offered a few trunk leased lines on the wholesale level up to 2009, has no longer offered leased lines either externally on a wholesale level or to retail customers since 2010. The LKW transmission capacities provided to itself to control its energy supply network are only supplied internally by the energy supply department.

In the context of self supply � either as a wholesale service to provide other own electron-ic communications services or else for the provision of leased line services to retail cus-tomers � the following undertakings also provide leased line services as own services in

39 By decision of the Princely Court of Justice dated 15.02.2012, bankruptcy proceedings were commenced over the assets of Alp-

com AG with effect from 16.2.2012. 40 Newsnet Internet Services AG (which traded under the name ABILA AG prior to 21.12.2010) and Newsnet AG each responded

separately in the past in the context of the questionnaire to operators. However as this is to be considered a uniform presence economically, only Newsnet AG is named hereunder and the data is aggregated as required.

26/57

Liechtenstein as per the 2010 questionnaire to the operators: A1 Telekom Austria AG (Austria), UPC Cablecom GmbH (Switzerland), ICT-Center AG, Green.ch AG (Switzerland), Newsnet AG, Total Optical Networks AG (Switzerland), Quality Net AG, BT Switzerland Ltd. (Switzerland), SpeedCom AG and Kyberna AG.41 With the exception of A1 Telekom Austria AG and UPC Cablecom GmbH � which utilise either solely or predominantly their own in-frastructure (i.e. cable-based or radio transmission systems) to provide their leased line services � the provision of leased line capacities by the other providers named is based in the overwhelming number of cases on infrastructure wholesale inputs provided by LKW.42 Although these providers are thus dependent on wholesale inputs from other providers in order to provide leased line services, their leased line capacities are to be taken into con-sideration on the supply side � due to their provision by themselves.

In addition to the providers named above, the licensed mobile communications providers in Liechtenstein, Mobilkom (Liechtenstein) AG, Orange (Liechtenstein) AG, Alpcom AG and Swisscom (Schweiz) AG, provide leased line services as self supply on the wholesale level in the context of operating their mobile communication networks. As a rule, they utilise their own radio transmission systems (radio links) for this, which serve on the one hand for connecting the mobile communication base stations (BTS/Node B) to the core network and on the other hand for interconnection with other domestic and foreign operators. These capacities are to be taken into consideration on the supply side as self supply.

2.5.2 Buyers

Buyers of leased line wholesale products are other domestic and foreign communications network operators and providers of communications services (incl. internet service pro-viders � ISP) for their own requirements or as wholesale input for the provision of retail leased lines.

In addition to the leased lines which are provided for external parties ("external services"), those leased lines on the market which are used for the internal provision of retail leased lines or for other internal purposes ("self supply") are also included.

2.5.3 Leased line products offered

The following published leased line products are currently offered externally on the mar-ket on a wholesale level, i.e. not as pure self supply:

41 TV-COM AG provides infrastructure wholesale services for the provision of leased lines, however it does not provide leased lines

itself at present. 42 And only to a limited extent on the infrastructure of other operators (where available).

27/57

Provider Product43 Relevant leased line market

TLI

Virtual leased lines (VLL) based on MPLS44 standard (with Ethernet inter-face) for bandwidths of 2 Mbit/sec to 1,000 Mbit/sec.45

- Trunk leased lines;

- Terminating segments.

TLI Private line national (PLN) with band-widths of 64 kbit/sec to 622 Mbit/sec (higher bandwidths on request).46

- Trunk leased lines;

- Terminating segments.

TLI

Private line international (PLI) with bandwidths of 2 Mbit/sec to 155 Mbit/sec.47

- Trunk leased lines;

- Terminating segments;

(Each in domestically located section).

Table 2: Overview of leased line products offered on the wholesale level

2.5.4 Market sizes and development

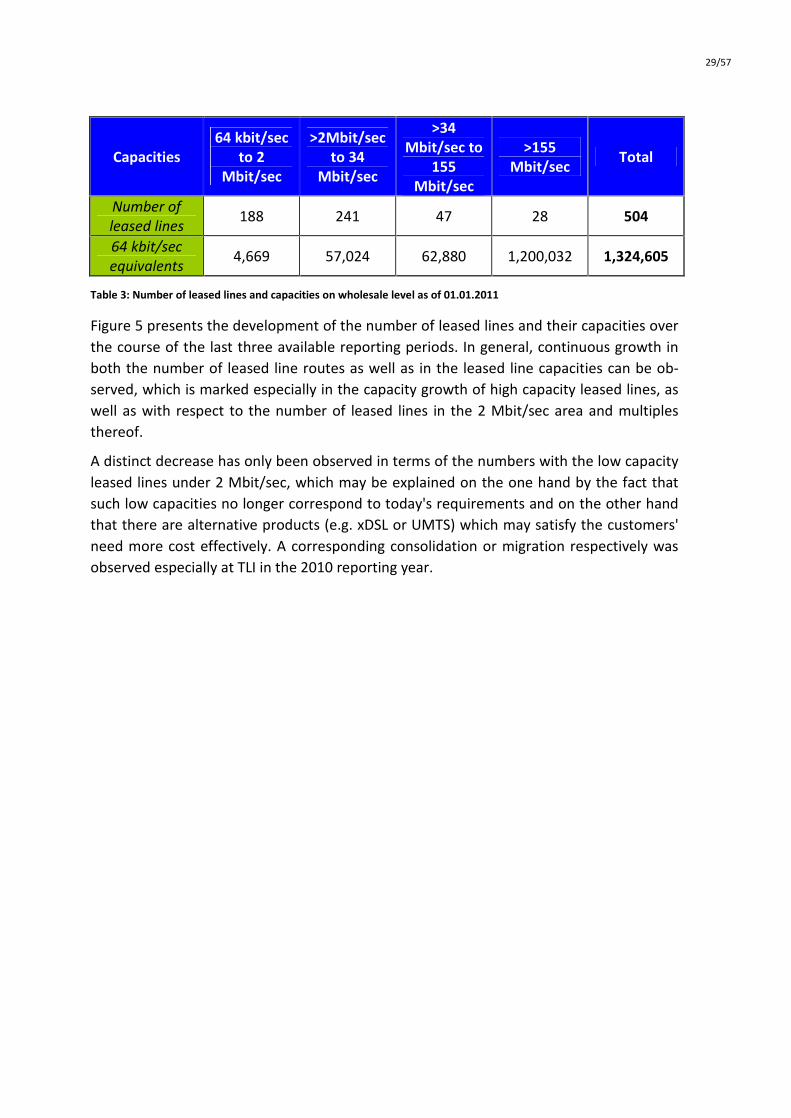

The leased line wholesale markets of relevance for the investigation are presented in Fig-ure 3, measured on the one hand in the number of trunk as well as terminating leased line routes and on the other hand in capacities provided (in 64 kbit/sec equivalents48).

43 For the TLI products, see the wholesale product descriptions on its website, as well as the "Product Description - Virtual Leased

Line VLL" dated 23.05.2006 (http://www.telecom.li/CFDOCS/cms3/admin/cms/download.cfm?FileID=2490&GroupID=171), last accessed on 16.02.2012.

44 Multi protocol label switching. 45 Distance dependent pricing per line type and bandwidth, whereby all of Liechtenstein (incl. half-circuits to Feldkirch/AUT and

Buchs SG/CH) is priced as a uniform national zone. 46 TLI provides the customer-side modem (CPE) to the wholesale service buyer (service provider). 47 PLI extends to the point of presence (POP) abroad; from there, the terminating segment has to be provided by the wholesale

service buyer. 48 For comparison purposes, the leased lines of the most varied capacities shown were provided at the largest common factor of 64

kbit/sec (also termed hereunder "64 kbit/sec equivalents" or "64 kbit/sec EQ"). For reasons of practicability (the respective line lengths could not be surveyed at a reasonable effort by the providers), the line lengths were not independently considered.

28/57

Figure 3: Overall view of leased lines on wholesale levels as of 01.01.2011

The unequal distribution of the number of leased lines across the differing capacities can already be recognised here. The presentation hereunder provides a more precise over-view of the distribution of the capacities and the number of leased lines across the differ-ent leased line capacities.

Figure 4: Distribution of capacities and number of leased lines as of 01.01.2011

As of 01.01.2011, leased line capacities of 81 Gbit/sec49 were provided overall in Liechten-stein, distributed across 504 individual leased line routes on the wholesale level.

49 This corresponds to 1,324,605 64 kbit/sec equivalents.

0

200'000

400'000

600'000

800'000

1'000'000

1'200'000

1'400'000

0

50

100

150

200

250

300

64Kbit/s bis 2Mbit/s >2Mbit/s bis 34 Mbit/s >34 Mbit/s bis 155 Mbit/s >155 Mbit/s

Num

ber

ofl

ease

dlin

ero

utes

64kbit/secequivalents

64 kbit/sec equivalents Number of leased line routes

0%

10%

20%

30%

40%

50%

60%

RF 64kb

it/s

RF 8M

bit/s

RF 16M

bit/s

RF 34M

bit/s

RF 155 M

bit/s

Analog

64 kbit/

s PDH

128 kbit/

s PDH

256 kbit/

s PDH

384 kbit/

s PDH

512 kbit/

s PDH

1 Mbit/

s PDH

2 Mbit/

s PDH

n x2 M

bit/s P

DH

10 Mbit/

s VLL

20 Mbit/

s VLL

50 Mbit/

s VLL

100 Mbit/

s VLL

500 Mbit/

s VLL

1000 Mbit/

s VLL

34 Mbit/

s PDH

140 Mbit/

s PDH

155 Mbit/

s SDH (S

TM-1

)

622 Mbit/

s SDH (S

TM-4

)

2.5 Gbit/

s SDH (S

TM-1

6)

10 Gbit/

s SDH (S

TM-6

4)

Distribu on capaci es Distribu on number of routes

29/57

Capacities 64 kbit/sec

to 2 Mbit/sec

>2Mbit/sec to 34

Mbit/sec

>34 Mbit/sec to

155 Mbit/sec

>155 Mbit/sec

Total

Number of leased lines

188 241 47 28 504

64 kbit/sec equivalents

4,669 57,024 62,880 1,200,032 1,324,605

Table 3: Number of leased lines and capacities on wholesale level as of 01.01.2011

Figure 5 presents the development of the number of leased lines and their capacities over the course of the last three available reporting periods. In general, continuous growth in both the number of leased line routes as well as in the leased line capacities can be ob-served, which is marked especially in the capacity growth of high capacity leased lines, as well as with respect to the number of leased lines in the 2 Mbit/sec area and multiples thereof.

A distinct decrease has only been observed in terms of the numbers with the low capacity leased lines under 2 Mbit/sec, which may be explained on the one hand by the fact that such low capacities no longer correspond to today's requirements and on the other hand that there are alternative products (e.g. xDSL or UMTS) which may satisfy the customers' need more cost effectively. A corresponding consolidation or migration respectively was observed especially at TLI in the 2010 reporting year.

30/57

Figure 5: Development of the leased line capacities on the wholesale level

Although, in the context of the market power analysis conducted in the next chapter, the intention is to break down the market shares in accordance with the two defined product markets, Figure 6 hereunder is still intended to illustrate the aggregated market conditions on the wholesale level as of 01.01.2011.

Figure 6: Distribution of the market shares across the complete leased line market on the wholesale level

0

200'000

400'000

600'000

800'000

1'000'000

1'200'000

1'400'000

0

50

100

150

200

250

300

350

400

64Kbit/s bis 2Mbit/s >2Mbit/s bis 34 Mbit/s >34 Mbit/s bis 155 Mbit/s >155 Mbit/s

64kbit/seceq

uivalentsN

umbe

rof

leas

edli

ner

oute

s

2007 2008 2009 2010

31/57

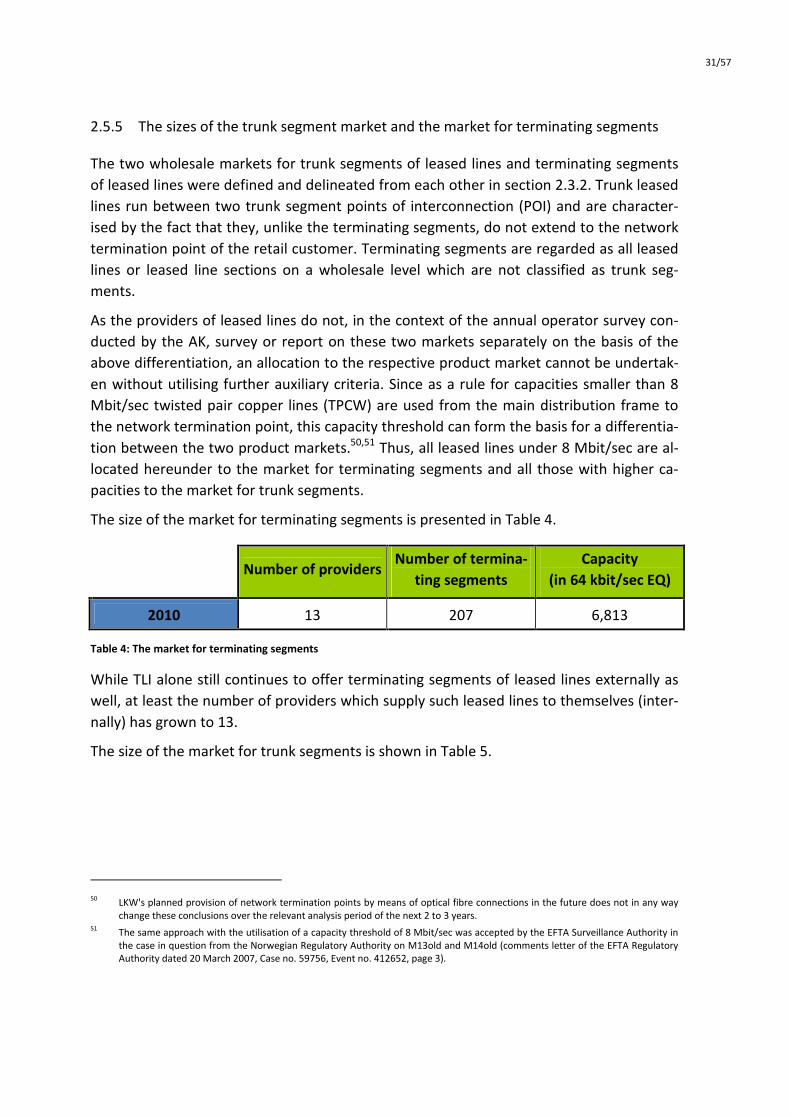

2.5.5 The sizes of the trunk segment market and the market for terminating segments

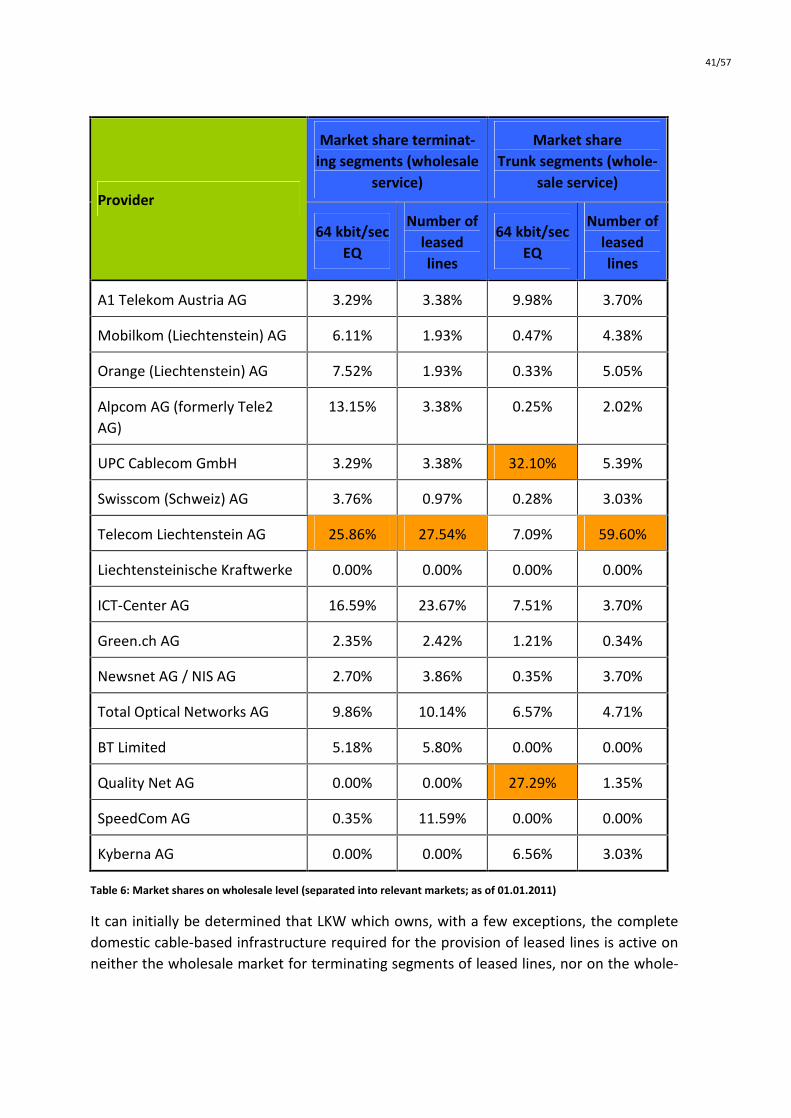

The two wholesale markets for trunk segments of leased lines and terminating segments of leased lines were defined and delineated from each other in section 2.3.2. Trunk leased lines run between two trunk segment points of interconnection (POI) and are character-ised by the fact that they, unlike the terminating segments, do not extend to the network termination point of the retail customer. Terminating segments are regarded as all leased lines or leased line sections on a wholesale level which are not classified as trunk seg-ments.

As the providers of leased lines do not, in the context of the annual operator survey con-ducted by the AK, survey or report on these two markets separately on the basis of the above differentiation, an allocation to the respective product market cannot be undertak-en without utilising further auxiliary criteria. Since as a rule for capacities smaller than 8 Mbit/sec twisted pair copper lines (TPCW) are used from the main distribution frame to the network termination point, this capacity threshold can form the basis for a differentia-tion between the two product markets.50,51 Thus, all leased lines under 8 Mbit/sec are al-located hereunder to the market for terminating segments and all those with higher ca-pacities to the market for trunk segments.

The size of the market for terminating segments is presented in Table 4.

Number of providers Number of termina-

ting segments Capacity

(in 64 kbit/sec EQ)

2010 13 207 6,813

Table 4: The market for terminating segments

While TLI alone still continues to offer terminating segments of leased lines externally as well, at least the number of providers which supply such leased lines to themselves (inter-nally) has grown to 13.

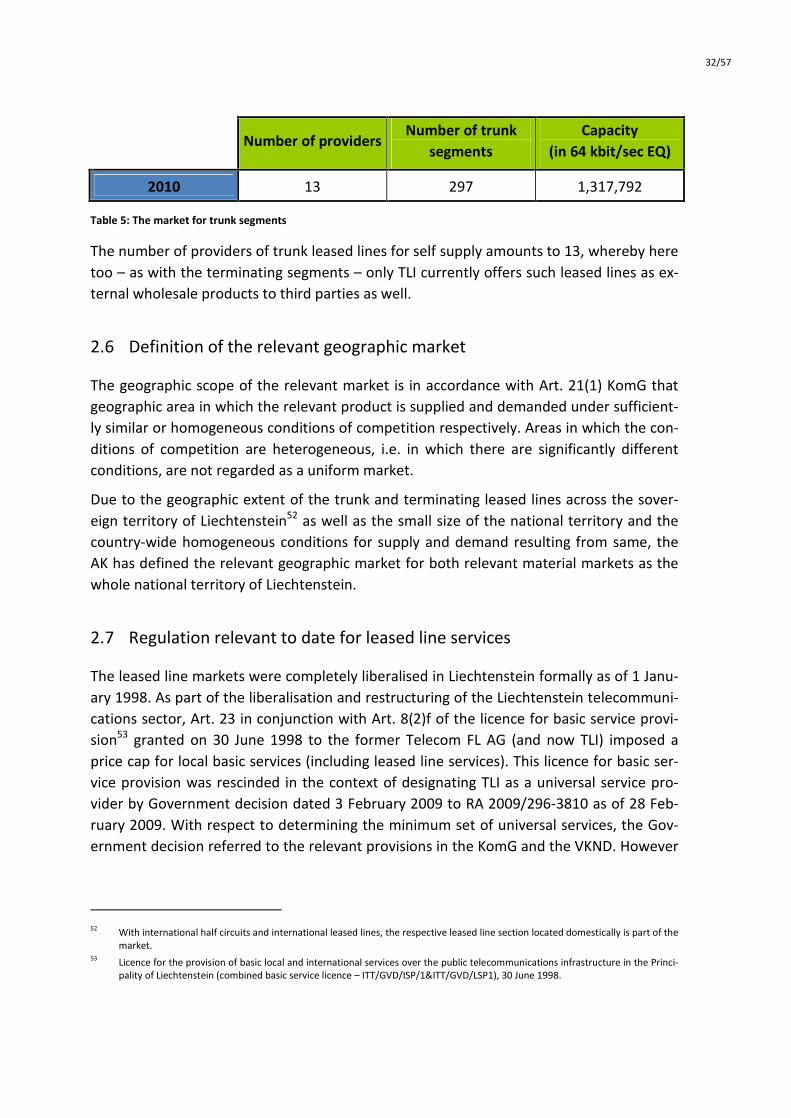

The size of the market for trunk segments is shown in Table 5.

50 LKW's planned provision of network termination points by means of optical fibre connections in the future does not in any way

change these conclusions over the relevant analysis period of the next 2 to 3 years. 51 The same approach with the utilisation of a capacity threshold of 8 Mbit/sec was accepted by the EFTA Surveillance Authority in

the case in question from the Norwegian Regulatory Authority on M13old and M14old (comments letter of the EFTA Regulatory Authority dated 20 March 2007, Case no. 59756, Event no. 412652, page 3).

32/57

Number of providers Number of trunk

segments Capacity

(in 64 kbit/sec EQ)

2010 13 297 1,317,792

Table 5: The market for trunk segments

The number of providers of trunk leased lines for self supply amounts to 13, whereby here too � as with the terminating segments � only TLI currently offers such leased lines as ex-ternal wholesale products to third parties as well.

2.6 Definition of the relevant geographic market

The geographic scope of the relevant market is in accordance with Art. 21(1) KomG that geographic area in which the relevant product is supplied and demanded under sufficient-ly similar or homogeneous conditions of competition respectively. Areas in which the con-ditions of competition are heterogeneous, i.e. in which there are significantly different conditions, are not regarded as a uniform market.

Due to the geographic extent of the trunk and terminating leased lines across the sover-eign territory of Liechtenstein52 as well as the small size of the national territory and the country-wide homogeneous conditions for supply and demand resulting from same, the AK has defined the relevant geographic market for both relevant material markets as the whole national territory of Liechtenstein.

2.7 Regulation relevant to date for leased line services

The leased line markets were completely liberalised in Liechtenstein formally as of 1 Janu-ary 1998. As part of the liberalisation and restructuring of the Liechtenstein telecommuni-cations sector, Art. 23 in conjunction with Art. 8(2)f of the licence for basic service provi-sion53 granted on 30 June 1998 to the former Telecom FL AG (and now TLI) imposed a price cap for local basic services (including leased line services). This licence for basic ser-vice provision was rescinded in the context of designating TLI as a universal service pro-vider by Government decision dated 3 February 2009 to RA 2009/296-3810 as of 28 Feb-ruary 2009. With respect to determining the minimum set of universal services, the Gov-ernment decision referred to the relevant provisions in the KomG and the VKND. However

52 With international half circuits and international leased lines, the respective leased line section located domestically is part of the