analysis of price volatility in energy commodities

TRANSCRIPT

0 | P a g e

ANALYSIS OF PRICE VOLATILITY IN ENERGY

COMMODITIES

A Dissertation Report Submitted in Partial Fulfillment of

Requirements

For

BBA (Oil and Gas marketing)

Batch 2010-2013

University of Petroleum and Energy Studies

Dehradun

SUBMITTED TO:

Mr. Sunil Bharthwal

Under guidance of

Dr.H .Roy

Assistant Professor

College of Management Studies

University of Petroleum and Energy Studies

SUMITTED BY

Vindyanchal Kumar (R170210052)

Enrollment NO: R170210052

Sap ID: 500011944

1 | P a g e

Acknowledgement

First and Foremost I wish to express my deep sense of gratitude and indebtedness to this

great institution of mine “University of Petroleum & Energy Studies” which has given me

privilege to imbibe ample technical and managerial knowledge.

I place on record my sincere sense of gratitude towards my mentor Dr. H. Roy, (Assistant

Professor, College Of Management Studies, UPES), BBA(Oil and Gas Marketing)and Faculty

of University of Petroleum & Energy Studies along with my colleagues for their cooperation

and most of all in making my post graduation a memorable experience.

Above all I would like to thank my parents and Family for giving me all the support.

Signature of Student

Vindyanchal Kumar

Place:

Date:

2 | P a g e

Certificate of Originality

This is to certify that the project titled “Analysis of Price Volatility in Energy

Commodities” is an original work of the student and is being submitted in partial

fulfillment of Bachelor Degree in Business Administration (BBA Oil and Gas

marketing) of University of Petroleum and Energy Studies, Dehradun for the

fulfillment of requirement of the course of study. This report has not been

submitted earlier to any other university/institution for the requirement of a

course of study.

Signature of Student

Vindyanchal Kumar

Place:

Date:

3 | P a g e

Bonafide Certificate

This is to certify that Mr. Vindyanchal Kumar, a student of „University of

Petroleum and Energy Studies, Dehradun, pursuing BBA (oil and gas

marketing), has successfully completed his dissertation report as a part of his

course curriculum. The project report entitled “Analysis of Price Volatility in

Energy Commodities”, submitted by the student to the undersigned is an

authentic record of his original work, which he carried out under my supervision

and guidance.

I wish him all the best.

Date:

Dr. H. Roy

Assistant Professor

University of Petroleum and Energy Studies

Dehradun, Uttrakhand

4 | P a g e

Abstract

In the recent years, India’s energy consumption has been increasing at one of the fastest

rates in the world due to population growth and economic development. To meet the demand

of the energy which is increasing at the rate of 6% and India is importing 76% crude oil, 22.5%

natural gas and 14.8% of coal to meet its energy demand. These energy commodities are also

influence the growth and development of the country. The import is increasing which leads to

the country fiscal deficit.

In 20th century energy market has tremendous growth recent studies shows the

speculation activities become one of the reason behind increased volatility. The example is the

Dec. 2008 when prices shoot up and touch the $147 and suddenly dropped down to $34 within

few months and now it’s between $70-80. Due to this many small players who did not react

accordingly and secure its position, have to bear a huge losses.

Looking at the crude oil crisis 1998, 2001, 2005 and 2008 many companies make losses.

Due to the price fluctuation many small players got bankrupt and many end up with huge

losses. We need to identify what are the factors affecting price of the energy commodities and

develop various precaution to reduce the risk exposure, so that the future losses can be reduce.

5 | P a g e

Table of Content:

Acknowledgement

Certificate of Originality

Bonafide Certificate

Abstract

List of Table

Chapter-1

1.1 Introduction

1.2Need for Research

1.3Objective of the study

1.4 Research Methodology

1.5 Literature Review

1.6 Scope for study

1.7 Limitations of the study

Chapter-2 Crude

2.1 Introduction to crude

2.2 Price volatility in crude oil

2.3 Price Trend analysis

2.4 Critical Price drivers of Crude Oil

6 | P a g e

Chapter -3 Coal

3.1 Introduction of Coal

3.2 Price Volatility in Coal

3.3 Supply Demand Fundamentals

Chapter -4 Natural Gas

4.1 Introduction to Natural Gas

4.2 Price volatility of Natural Gas

4.3 Relationship between oil and natural Gas Price

4.4 Price driving factors of natural Gas

4.5 Trend in natural gas price

Chapter – 5 Conclusion

Bibliography

7 | P a g e

Chapter - 1

1.1 Introduction

Crude oil, Coal and Natural Gas are the major source of energy for world economy since the last

century. These commodities had played a vital role in industrial development and growth of world

economy. The global economy is highly affected by the fluctuations in prices of these energy

commodities. There are several factors which affect the price of energy commodities, thus affecting

the world economy directly. The analysis shows that infrastructure; weather data, geopolitical

problem in Middle East countries, dollar index, unemployment rate etc. are the major fundamental

factors that affect the prices of energy commodities. For example. Analysis done on the crude oil

prices show that the price of crude oil shows high volatility in reference to change in Dollar value. It

shows an upward or downward trend depending on decrease or increase in Dollar value similarly the

Middle East countries also impacts the crude oil prices.

Some of the fundamental factors affecting the Natural Gas prices are weather condition such as

Katrina, Rita, and coming Richard in Gulf of Mexico affect the supply side of natural gas prices.

Also the seasonal demand shows that US consumes 1.5 times more in winters than other months

which leads to increase in price. There is a correlation between the price of natural gas and other

energy commodity such as crude oil and coal.

Demand of natural is increasing due to newly developed gas base power plant and economic

development of the countries and also concern toward the global warming. That is why the

consumption of natural gas increased.

Coal demand is highly dependent on energy demand, as the majority of power generation in several

countries (such as China, India and South Africa) comes from coal generation so the prices of coal

are correlated with price of electricity. Due to the weather condition and floods in Australia from

Richards Bay port not able to transport the coal leads to decrease in the supply to other nations as 1.8

million tonnes to 1.1 million tonnes. In India consumption is higher than production will leads to

price hike in near future. Due to the Global Warming problems in future some restrictions may take

place by the government agencies or environment protection agency. It will be macro-economic

factors such as GDP, trade deficit, national debt, inflation, interest rates that can indirectly influence

the price of coal.

8 | P a g e

The recent geo-political issues with producer and consumer countries are adversely affecting the

prices of energy commodities and Crude, Coal and Natural Gas prices showing upward trend.

Libyan rebel and the earthquake in Japan lead to huge volatility in the energy commodities, The

prices of crude oil is touching $115 from $80-$90.

1.2 Need for the Research:

To suggest relevant strategies to Producers, Consumers and Investors to protect from loss.

Effect of price volatility on GDP of countries

To know relationship between coal price and natural gas price

To find market force and factors driving the commodity price

Due to the price volatility in the commodity market producers, consumers, investors and the

government have to bear huge losses. To mitigate the price risk the derivative market provide the

platform to various players to indulge in the various contract but selection of the strategies become

irrelevant when you don‟t know the market direction where the market is going, is it following the

uptrend or downtrend within the given timeframe. So there is a need to find out the market force and

factors driving the commodity price that can be done by fundamental and technical analysis

sometimes known as techno-fundamental analysis. The fundamental analysis in simple term is

analysis of what is going on in the business environment and how it is affecting the basic demand

and supply factors of the physical energy market because the gap between the demand and supply

has direct relationship with price of the energy commodity. As a Simple statement of the head of

Saudi Arabian crude oil company that in case of price rise he will increase the production of oil leads

to decrease in the crude oil spot price from $88 to $79. Because single news in the market can leads

to heavy price fluctuation in the commodity market so we need to identify those factors and analyze

the intensity or magnitude of those factors.

In Technical analysis we follow the assumption that history repeats itself so by analysing the

historical databases. we will try to identify the trend of market for particular commodity, at the same

time try to find out the market direction or market forces, who is influencing the market is that

buyers or sellers who is controlling and driving the market who actually define the market price of

9 | P a g e

the particular commodity. For analysing the Volatility we can use ATR (Average True Range) which

tell us what might be the volatility or movement in a particular energy commodity in a particular day.

1.3 Objective of study:

1. To study Price Volatility

2. To analyse Fundamental factors influencing Price of Energy Commodities.

3. To analyse price volatility using technical tools.

4. To suggest relevant strategies to Producers, Consumers and Investors.

5. To identify time periods at which we will definitely see the price volatility in the market.

6. To determine the price trend of crude oil in relationship with prices of alternative fuels.

7. To know the consequences and there possible remedies .

1.4 Research Methodology

Type of research: Descriptive

Sampling technique:

Non probabilistic method of convenience sampling will be used. The data will be collected from

easily available and cost effective sources.

Data Source:

Secondary Data will be collected by visiting various Internet sites such as Bloomberg, Reuters,

and Ticker Plant, Website of Commodity Exchanges e.g. Nymex, MCX, ICE, Ministry of Petroleum

and Natural Gas; various global futures exchange websites, Platts, IMF, EIA, and MCX etc.

10 | P a g e

Data Analysis:

Data collected from different sources will be tabulated and analyzed using different analytical tools

as:

Average True Range

Standardeviation

1.5 Literature Review

There is adequate literature available for the reference for the project. Extensive usage has been

made of all the available literature for the information. The books on derivatives and risk

management have been of great help for the understanding of the concept of derivatives. Oil Trading

Manual by David Long, Energy Price Risk by Tom James, Energy hedging in Asia by PETER C.

FUSARO, technical analysis of financial market by john j. Murphy needs special mention as these

books has been extensively used.

Also for the understanding of the concept many research papers both international as well as

national will be studied. These research papers are very helpful as these bring the clarity about the

subject of the topics. They help in showing the correct direction for the project work and how one

shall proceed with it. Over the study of different research papers, it has been found that every paper

has different aspect to work out, as the papers are written on problems faced by importers, refiners,

producers due to price volatility.

Research paper

1. Coal Price Projection

Author-

Date-oct 2011

Place-EU,CHINA, RUSSIA,COLUMBIA

No pages-42

11 | P a g e

This paper set out key consideration used by DECC in creating price assumption for the coal market

over the next 20 years.

It is done by external agencies like EIA, IEA.

It uses mainly demand, supply, and analysis of long run marginal costs models.

Results

a) It is find that price of coal largely depend on china.

b) Price of coal directly depends on price of gas.

c) Demand of coal will decrease n 2050 because coal eliminates double carbon than the gas, so

company have to paid more tax.

2. OIL in charge

Author- ABE COFNAS

1. This research paper is about effect of price volatility in oil exporting and importing countries.

2. Effect of price volatility on developing and developed countries.

3. Analysis of “Impact of high oil price on the global economy “in may 2004.

Finding

a) Economy of developing countries like Asia, Africa is affected because their economy depend

more on imported oil.

b) Oil importing countries uses more than twice petroleum product to produce one unit of output than

developed countries.

c) US economy less effected by price hike because one and another way there dollar return to them.

12 | P a g e

3. Natural gas

Analysis of change in market price

Author –GAO

Date – Dec 2002

No .of page- 97

Why did GAO do this survey?

During the winter of 2000-2001, the wholesale price of natural gas peaked at a level four times

greater than its usual level.

Responding to the congressional interest and concern caused by these high prices,

GAO undertook a study to

1) Factors that influence natural gas price volatility and the high prices of 2000-2001;

2) Federal government‟s role in ensuring that natural gas prices are determined in a competitive,

informed market place .

.

3) Choices available to gas utility companies that want to mitigate the effects of price spikes on their

residential customers.

What GAO found;

a) Price spikes occur periodically in natural gas markets because supplies cannot quickly adjust to

demand changes.

b) While market forces make natural gas prices susceptible to price volatility, investigations are

underway to determine if natural gas prices were manipulated in the Western United States during

the winter of 2000-2001

4. Oil price volatility and U.S macroeconomic Activity

Author- Hui GUA and Kevin L. Kliesen

Place- St. Lousis

No of pages-16

This research paper distinguishes two most important channel through which change in oil price

affect aggregate economic activities.

13 | P a g e

I. The change in the dollar price of crude oil

II. The change in the uncertainty about future price.

Result:

a) Oil price volatility has negative and significant effect on future GDP growth.

b) This volatility effect becomes more significant after we control oil price change.

c) Both the oil price change and its volatility lose their significance after we control non linear oil

shock measure

5. Price volatility ,hedging and variable risk premium in the crude oil market

Author –Ahmad R. Jalali-Naini and Maryam Kazemi Manesh

No of pages-17

Date –Jan 2006

Place-New York, Texas

In this research paper author compare OHR (optimal hedge ratio) for the crude oil. This research is

done in New York and Texas.

It is done by using different model like GARCH and ARCH model. It also tested the variable

existing risk premium in the crude oil market

Finding

Research finds that there is zero risk premium with helping GARCH model.

6. NEW evidence on the asymmetry in gasoline price: volatility versus margin?

Author: Salah Abosedra and Stanislav Radchenko

Place-Beirut, USA

Date – Sept 2006

No of pages-27

14 | P a g e

This paper examine recent evidence on the role that gasoline margins and volatility play in the

asymmetric response of gasoline prices to change in oil price to change in oil price at different stages

of distribution process.

This research paper has used regression model with margin

Finding

a) Margin is statistically significant in explaining asymmetry between crude oil and spot gasoline

prices,

b) Spot gasoline prices and wholesale gasoline price etc and it has same finding in volatility of price.

7. Volatility Relationship between Crude Oil and Petroleum Products

Author-Thomas K. Lee & John Zyren

No pages-17

Date -17 Jan 2007

This paper utilizes calculated historical volatility and GARCH models to compare the historical price

volatility behavior of crude oil, motor gasoline and heating oil in U.S. markets since 1990. We

incorporate a shift variable in the GARCH/TARCH models to capture the response of price volatility

to a change in OPEC‟s pricing behavior.

Finding

a) There was an increase in volatility as a result of a structural shift to higher crude oil prices after

April 1999.

b) Volatility shocks from current news are not important since GARCH effects dominate ARCH

effects in the variance equation.

c) Persistence of volatility in all commodity markets is quite transitory, with half-lives normally

being a few weeks.

15 | P a g e

Reports and Journals

“Methodology and Specifications Guide” published by Platt‟s

The crude specifications mentioned in this guide contain the primary specifications and

methodologies for Platt‟s crude oil cargo and pipeline assessments throughout the world. These

methodologies are used by oil producers, traders, refiners and final consumers for pricing of crude

oil throughout the world. The Platt‟s prices are considered benchmark for crude oil pricing. So this

report helps in finding out the factors which affect the price of crude oil.

Ahuja N.L. (2005): “Commodity Derivatives Market in India: Development, Regulation and

Future Prospects” published in „„International Research Journal of Finance and Economics‟‟

This paper analyzes the evolution of Indian commodity market and how did India pull it off in

such a short time since 2002? Is this progress sustainable and what are the obstacles that need urgent

attention if the market is to realize its full potential? Why are commodity derivatives important and

what could other emerging economies learn from the Indian mistakes and experience?

Shah Ash Narayan: “Price Discovery in Cash and Futures Market: The Case of Nymex Crude

and Heating Oil” published in Contemporary Issues in Energy Sector, 1st Edition, 2009.

This paper analyzes the role of futures exchanges in price discovery of crude oil and heating oil

using monthly data of prices at Nymex. It uses co-integration and error correction model for analysis

of prices. The findings of study prove that there exists a long term relationship between spot and

future prices of crude oil and heating oil. Further, error correction model establishes a feedback

relation between spot and future prices of crude and heating oil. This relationship study will help in

determining the role of spot markets in price discovery of crude oil.

Dr. Diwan Parag: “Energycopia”, First Edition, 2008

This book covers crude oil trading and natural gas trading. It examines the principal issues

concerning energy sector. These contemporary issues include concepts of energy economics, the

regulation and policy framework, the conservation issues, the global energy trade and finally the idea

of achieving energy security. The book will help in finding out current scenario of energy sector and

understanding the trading mechanism of crude oil and natural gas.

16 | P a g e

Murphy, john j. “technical analysis of financial market” prentice hall direct, 1999

This book covers Technical analysis tools which are widely used by the traders to trade in the

exchanges. It briefly explains the various tools, how to use them and the importance of those tools.

This book will help in finding the strategies with tools to trade and manage price risk by telling when

to enter the market and when to exit or say when to buy and when to sell.

1.6 Scope of Study

My research will cover whole world and can be used both individually or group.

It will be used by managers of oil companies to forecast future price.

My research will be helpful for the oil company like HPCL, BPCL, and IOCL etc.

It will be also helpful for the company whose work somehow related with petroleum product.

1.7 Limitations of the Study

1. Data is collected from secondary sources so there are chances of error.

2. The strategies have to be implemented in real market conditions to find out their efficacy.

3. Availability of time and budget constraints.

4. Technical analysis will be used to forecast crude oil prices but sometimes it may not yield

effective results.

17 | P a g e

Chapter-2

2.1 Introduction of crude oil

Crude oil is a mixture of about 5oo organic chemicals, predominantly hydrocarbons (molecules

made of carbon and hydrogen). It is recovered from underground reservoirs, normally 1000 - 5000

meters down the earth. Crude oil can be of wide variety and characteristics. It could be very fluid,

very viscous or semisolid. The colour could be black, dark brown, amber or light brown. It is also

called Petroleum.

Classification of Crude Oil

Various crude oils are often referred by their API Gravity. API Gravity is expressed as (141.5/

Sp. Gravity - 131.5). As specific gravity is in the denominator, API Gravity is higher for lighter

crude and lower for heavier crude. A comparative idea of this gravity unit can be obtained by

comparison with water: Water: 10 API Typical API Gravity figures for crude oil are

Mumbai High Crude: 40 API - Light Crude

Arabian Crude: 34 API - Medium Crude

Venezuelan Crude: 15 API - Heavy Crude

There could be sub-categorization as Medium Heavy or Light Medium. Another common

classification is based on Characterization Factor, which depends on API Gravity and Boiling Point.

Types of Crude oil

Light crude has low density making it easier to transport and refine. Most refiners prefer the

light sweet crude oil because it contains low sulfur content. Light crude is chemically "closer" to

many desired finished products such as gasoline and diesel fuel and usually it requires less refining

and processing and therefore is typically more valuable and more expensive than "heavy" oil.

Heavy crude has high density, making it more difficult to transport and refine. Heavy crude is

cheaper to buy and usually cheaper to extract though heavy crude produced from tar sands can cost

twice as much as conventional drilling.

18 | P a g e

Crude oil Bench marks

Brent Crude Oil

Brent Crude oil is used as a bench mark for deciding the price of crude oil. It is light and sweet

crude oil but not as much sweet as WTI. The API gravity of the Brent crude oil is near about the

38.o6 and the specific gravity is near about the 0.835. Sulfur content in the Brent crude oil is

approximately the O.37%. Mostly it is use for the distillation of gasoline and middle distillate

product.

Future and option contracts of the Brent crude oil are traded on the ICE (Inter Continental

Exchange), NYMEX (New York Mercantile Exchange). The symbol of the Brent crude oil is CL4 in

the commodity trading market. Earlier the Brent crude oil was traded on the open outcry on the IPE

but now it is to be traded electronically on the ICE. One contract of the Brent crude oil is 1000 barrel

of crude oil. The contract price of the Brent crude oil is to be quoted in the dollar per barrel.

West Texas Intermediate (WTI) crude oil is of very high quality and is excellent for the Refining.

Its API gravity is 39.6 degrees and it contains only about 0.24 percent of sulfur. Most WTI crude oil

gets refined in the Midwest region of the country, with some more refined with in the Gulf Coast

region. Although the production of WTI crude oil is on the decline, it still is the major benchmark of

crude oil in the America.

Tapis

Tapis is a Malaysian crude oil used as pricing marker crude in Singapore. It is not only traded on

market like Brent and WTI, it is often used as oil marker for Asia.

19 | P a g e

Dubai and Oman

Dubai crude is a light sour crude oil. It is used as benchmark in Middle East.

• It has API gravity of 31 and sulphur content of 2%

• It is considerably more heavy and viscous and sourer, making sweet crude marker is an

inadequate tool with which to manage sour crude price risk.

Hence introduction to exchange traded Middle East sour crude facilitates risk management of sour

crude in Middle East, Asia and beyond also.

Dubai Oman crude uses by the Middle Eastern Countries for determining the price of their crude oil.

In early days the Middle Eastern Countries decide their price on the basis of Brent crude but Brent

crude oil is light sweet crude oil while the Middle Eastern countries crude oil contains high sulfur

content and the API gravity near about the 15 to 17 API. So the price is not determined on the base

of a Brent crude oil. Dubai Oman crude traded on the Dubai Mercantile Exchange. In July 2007

DME launched the future contract of the Dubai Oman Crude oil.

Introduction to Global Crude oil market

Over the last three decades oil has become the biggest commodity market in the world. During this

period, oil trading has evolved from a primarily physical activity into a sophisticated financial

market. It has attracted the interest of a wide range of participants including banks, governments,

financial institutions, fund managers as well as the airlines, traditional oil majors, independents and

physical oil traders.

Prior to 1970s, oil trading was a marginal activity for most companies who only used the market to

resolve any imbalances in supply and demand that might emerge. The industry was dominated by

large integrated oil companies and as a result trading volumes were typically small and usually spot

and the prices were much less transparent than they are today.

As the nationalization of oil companies took place in 1970 in the Middle East and elsewhere, the

major oil companies were forced to buy huge amount of crude oils from their former host

20 | P a g e

governments and trading eventually became an integral part of any oil company‟s supply and

marketing operations. With more oil being traded, external market began to set the price for internal

transfers as well as third‐party sales, fuelling the growth of the market.

The driving force behind the rapid growth in oil trading is the huge variability in the price of oil. The

daily price movements of $2/barrel are not uncommon and prices frequently change by up to 50

cents/barrel. Since there is no obvious upper or lower bound to oil prices, the value of a barrel of oil

can double or halve within the space of a few months.

As a result, everyone involved in the industry is exposed to the risk of very large changes in the

value of any oil that they are producing, transporting, refining or purchasing, and a range of new

markets have evolved in order to provide effective hedging instruments against the elaborate

combination of absolute and relative price risks that characterize the oil business.

Trading Horizons

The most important change to the oil market has been the gradual extension of trading horizons.

Before the introduction of forward and futures contracts, oil companies had no effective means

setting prices for future delivery. As a result, the spot market was forced to bear the brunt of trading

decisions that might relate to time periods ranging anywhere from a day to a year ahead, which could

only have added to price volatility.

However, the time horizon of the oil market has been extended much further forward as can be seen.

The most active futures contracts, such as NYMEX WTI, now trade for delivery up to nine years

ahead and the industry has acquired a new set of trading instruments that enable participants to

establish prices even further into the future. Instead of being limited to a time horizon of only a few

months, prices can now be reliably obtained for periods from one to ten years ahead. This has been

made possible by the introduction of financial instruments such as OTC options, which have created

a liquid market that enables companies to trade the price of oil over a time frame that is appropriate

for producers investing in new oil fields or for consumers building new power stations. And for

physical traders who frequently use financial instruments to fix price independently of delivery.

21 | P a g e

2.2 Price Volatility in Crude oil:-

The price volatility in the crude oil can be because of two factors one is the investor‟s sentiments

and the other is known as fundamentals of crude oil. The first factor is investors sentiments is the

price when the investor like to invest or exit from the market. These investor‟s sentiments can be

predicted by using the technical and statistical analysis. One of the tools is ATR (Average True

Range).

ATR(Average True Range)

The average true range (ATR) determines Commodities volatility over a given period. That is,

the tendency of a commodity to move, in either direction.

More specifically, the average true range is the average of the true range for a given period. The true

range is the greatest of the following:

The difference between the current high and the current low

The difference between the current high and the previous close

The difference between the current low and the previous close

The ATR is mainly used to have stop loss or to exit from the trade while trading. Because they

expect that the commodity price will not move more than this level in a particular day.

Other statistical method we can use is by finding the Standard deviation from the expected price

of the commodity.

22 | P a g e

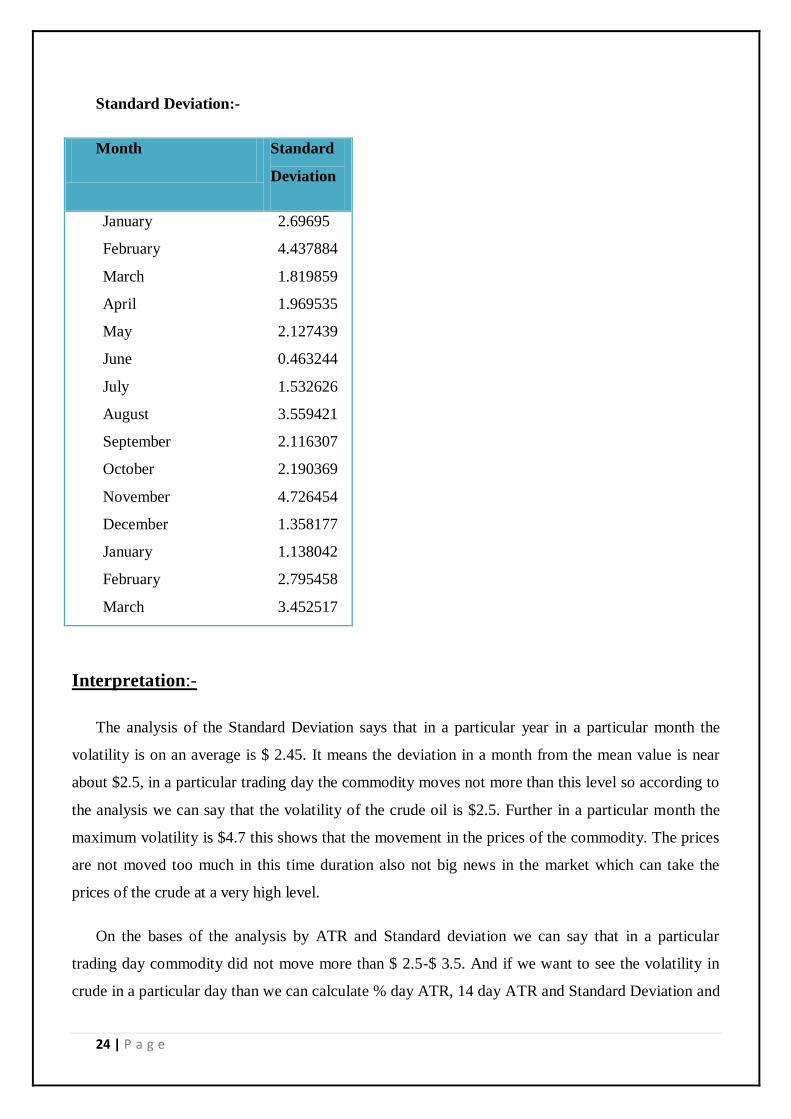

Standard Deviation:-

Standard deviation is a widely used measurement of variability or diversity used in statistics and

probability theory. It shows how much variation there is from the average. A low standard deviation

indicates that the data points tend to be very close to the mean, whereas high standard deviation

indicates that the data are spread out over a large range of values.

The second major factor is fundamentals of crude oil. The market react according to the news is

coming in to the market. The market players are sensitive about market news. Whenever there is a

news in a market, the market participants try to grab that opportunities and react accordingly but at

the same time there are some big players who tried to trap the other players and move the market in a

opposite direction and make their stop loss triggered and the others end up with the losses. So we

have to very careful while trading and finally market always moves in the way it should move. So we

have to analyse at what time and which side the market will move and accordingly we can trade. For

that purposes we can actually see the market past news when they come how the market move in

shorter duration and in the longer duration.

ATR calculation of the Crude oil

Calculation

The Average True Range (ATR) is based on 14 periods and can be calculated on an daily, weekly

or monthly basis. For this example, the ATR will be based on daily data. Because there must be a

beginning, the first TR value is simply the High minus the Low, and the first 14-day ATR is the

average of the daily TR values for the last 14 days.

ATR value from NYMEX

Given

Long term ATR for the Coal is = $ 0.8023385

The 14 days ATR is = $ 3.74951683

The 5 days ATR is = $3.8286829

23 | P a g e

The 5 days ATR and 14 days ATR is commonly used ATR for trading activities. It is considered

that the price in a particular day might move to this range and then will stop moving. But we cannot

assure that the price will not move more than that because the price is unpredictable and it can move

further but chances of moving not more than this is very less.

The all time ATR or say ATR from 1983 to 2013 says that the average movement in a particular

day is $0.8023385. The crude oil price will not move more than this but the observation is related to

the long term and in the initial days the prices are not much volatile and now a days the market is

much more volatile than ever. The conditions are changing and the market is becoming more

dynamic.

If we analyse the past prices then we will find that market is not moving more than is value when

the market conditions are normal or say the investors are not in panic. But if there is adverse news

then in that case the market may move more than this value so in this case we can take more 5 days

ATR or 14 days ATR to know the volatility in short term or can say current volatility in the market.

In this report there is 14 days ATR and we find that the max. Value of the ATR is $ 3.74951683.

Means in the time duration of the 14 days the average movement of the crude was $ 3.74 and the

average value is somewhere around the $ 3.5 so we can say that according to the current market the

price will generally move $3.5 and in the adverse condition the value can be move by $ 3.74.

In 5 days ATR we find that the max Value is $3.8286829. in this case we can also take the 5 days

ATR because it tells the current market volatility and if the volatility according to the 14 days and 5

days are approx. Same in this case we can say that the market might move near to the ATR value but

if both the ATR is not equal then we can say that the market will move the higher value of the ATR.

After doing the calculation of the ATR we found that the 5 days and the 14days ATR are

showing the nearly same values in this case we can consider the both the ATR‟s. And then we can

take the position in the market.

The analysis shows that the average value of the ATR of the crude oil is $ 3.74 to $3.82. so in the

general market condition when there is no opposite news in the market or small news in the market

the market will not move more than $ 3 in a trading day so if the market already moves this much in

a particular trading day we can trade considering the market will go side wave or will show the

retracement.

24 | P a g e

Standard Deviation:-

Month Standard

Deviation

January

February

March

April

May

June

July

August

September

October

November

December

January

February

March

2.69695

4.437884

1.819859

1.969535

2.127439

0.463244

1.532626

3.559421

2.116307

2.190369

4.726454

1.358177

1.138042

2.795458

3.452517

Interpretation:-

The analysis of the Standard Deviation says that in a particular year in a particular month the

volatility is on an average is $ 2.45. It means the deviation in a month from the mean value is near

about $2.5, in a particular trading day the commodity moves not more than this level so according to

the analysis we can say that the volatility of the crude oil is $2.5. Further in a particular month the

maximum volatility is $4.7 this shows that the movement in the prices of the commodity. The prices

are not moved too much in this time duration also not big news in the market which can take the

prices of the crude at a very high level.

On the bases of the analysis by ATR and Standard deviation we can say that in a particular

trading day commodity did not move more than $ 2.5-$ 3.5. And if we want to see the volatility in

crude in a particular day than we can calculate % day ATR, 14 day ATR and Standard Deviation and

25 | P a g e

we will get the value which will tell us that in that day what is the rage of the commodity and how

much it may move.

2.3 Price Trend Analysis of Crude Oil:-

Period: Dec 1996 – Dec 1998

Price range (% Change): 26.80 - 10.35 (-61.38)

Factors: -

Rise in inventories 300 – 325 million barrels

Oct-96 – Jun‟97

Fall in Natural gas prices 4.71 – 1.8 USD/MMBTU, 1.04 USD/MMBTU

Jan‟97 – Mar‟97, Dec‟98

Asian Financial Crisis

1997-98

Period: Dec 1998 – Sept 2000

Price range (% Change): 10.35 - 37.80 (+265.22)

Factors: -

Later season cold snap

Feb‟99

Cut in refinery runs 40.05 – 37.33

Dec‟98 – May‟99

26 | P a g e

Increased seasonal gasoline demand 7.83 – 9.08 Mbpd

Apr‟99 – July‟99

Fall in peak season inventories 284 (334) million

Period: Sept 2000 – Jan 2002

Price range (% Change): 37.80 - 17.85 (-52.78)

Reasons:

OPEC production cut 1 MBpd (25.2-24.2 MBpd)

Apr‟01

Concerns over US and global economy

Period: Jan 2002 – July 2006

Price range (% Change): 17.85 - 79.86(+347.39)

Reasons:

OPEC output cut 1.5 MBpd (23.2-21.7 MBpd)

Dec‟01

Global supply shortfall 0.8 MBpd (76.9 MBpd supply vs. 77.7 MBpd demand) 2002

Decline in inventories (Cold weather) 10.55 percent (311.06 – 278.25 million barrels) 2002

Geopolitical tensions

Nigeria, Iran

Early 2007

27 | P a g e

Feud between Venezuela and Exxon-Mobil

Jan-Feb‟08

Incursion of Turkish forces into northern Iraq

Nov‟07, Feb‟08

Possibility of a third round of sanctions on Iran

Feb‟08

Period: July2008 – Till Date

Price range (% Change): $78-$110(+70%)

Reasons:

Global Recession

Recessionary impact led to sharp fall in demand

Jan- Sep‟09

Milder Hurricane Season No supply disruptions

Geopolitical Tensions Sanctions on Iran

Jan‟10

Increased non-OPEC supply from Brazil and China

28 | P a g e

2.4 Critical price drivers of Crude oil: -

From the above analysis of crude oil price trend, the following factors are identified as crucial in

determining the movement and direction in crude oil prices on a regular basis:

Seasonal patterns in prices

World demand and supply of crude oil

Demand and supply trends of crude oil at the US front

Natural gas prices

Weather conditions

Fluctuations in the value of dollar

Policy/ regulatory aspects

Inventories of Crude oil and products (mainly at the US front)

Performance of end use sectors

Trend in other global markets (inter-product (derivatives) and intra-product)

These factors can further be classified into short term and medium term based on their

significance and horizon of influence on price movement.

Short-Term Factors

Weekly US crude and product demand

Weekly crude and product inventories

Weekly crude oil and product imports

Weekly refinery production of crude oil and products etc

Weather conditions

Natural gas prices

Trend in other global markets

Currency movements

Political/geopolitical issues

29 | P a g e

Medium Term Factors

Monthly IEA (International energy agency) and OPEC (Organization of petroleum exporting

countries) reports covering petroleum products demand and supply scenario at OECD

countries

Seasonal patterns in demand and supply of crude oil

Performance of end used sectors

Global demand and supply scenario

Political/geopolitical issues

Economic scenario

30 | P a g e

Chapter -3

3.1 INTRODUCTION TO COAL:-

Coal is a combustible black or brownish-black sedimentary rock normally occurring in rock strata in

layers or veins called coal beds or coal seams. The harder form of the coal is anthracite coal. Coal is

composed primarily of carbon along with variable quantities of other elements, chiefly sulfur,

hydrogen, oxygen and nitrogen.

Types OF COAL:

There are various types of coal available in the market. Different type of coal having different

Peat, The peat coal is considered to be a precursor of coal; it has industrial importance as a fuel in

some regions, for instance, Ireland and Finland. In its dehydrated form, peat is a highly effective

absorbent for fuel and oil spills on land and water.

Lignite, the Lignite coal is referred as brown coal, it is the lowest rank of coal, and it is used

exclusively as fuel for electric power generation.

Bituminous coal, The Bituminous coal is dense sedimentary rock, black but sometimes dark brown,

often with well-defined bands of bright and dull material. The Bituminous Coal is used primarily as

fuel in steam-electric power generation, with substantial quantities also used for heat and power

applications in manufacturing and to make coke.

Anthracite, It is the highest rank of coal and contains 86 to 97 percent carbon. It is used for

residential and commercial space heating. Otherwise called as hard coal it contains a high percentage

of fixed carbon and low percentage of volatile matter. It is the cleanest burning fuel and the most

efficient among the varieties.

Graphite, it is mostly used in pencils and, when powdered, as a lubricant.

31 | P a g e

Coal as a Traded Commodity

Coal futures contracts are currently traded on the New York Mercantile Exchange. The trading unit

is 1,550 short tons (1,410 t) per contract, and is quoted in U.S. dollars and cents per ton. Since coal is

the principal fuel for generating electricity in the world, the coal futures contracts also provides coal

producers and consumers an important tool for hedging and risk management.

In addition to the NYMEX contract, the InterContinental Exchange (ICE) has European (Rotterdam)

and South African (Richards Bay) coal futures available for trading. The trading unit for these

contracts is 5,000 tones (5,500 short tons), and are also quoted in U.S. dollars and cents per ton.

The price of coal increased from around $30.00 per short ton in 2000 to around $150.00 per short ton

as of September 2008.

Economic aspects:

Estimates of the cost of producing liquid fuels from coal suggest that domestic U.S. production of

fuel from coal becomes cost-competitive with oil priced.

China is by far the largest producer of coal in the world. It has now become the world's largest

energy consume but relies on coal to supply about 70% of its energy needs. An estimated 5 million

people work in China's coal-mining industry.

Pricing of Coal

Coal is mainly priced on

1. GCV

2. Moisture

Congestion at Load Port & Discharge Port

Freight

Weather

Inventory

Currency

32 | P a g e

Finished product price

Government policies

Prices of alternatives

New technology development

3.2 Price Volatility in Coal:-

Coal is another energy which is used from the past long time in the world for various purposes.

Mainly Coal is used in Iron and Steel industry and Power generation. The change in the prices of

coal affects the Industry which is actually backbone of the country as power sector. As other

commodities coal is also a most traded commodity but coal is mainly traded in OTC (Over-the-

counter (OTC) or off-exchange) market and less traded in the exchanges so the speculation

activities are very less. There is not much volatility in the prices of the coal but there are several

factors affecting the price of coal. Coal is traded mainly in long term contracts so the prices are

determined by the market and the players but sometimes due change in the demand of the coal the

prices started changing so it affect the cash market or say the spot market, So the companies who

cannot store good quantity of the Coal face the problems because they have to purchase it from the

spot market they need to monitor the price and have to hedge their position in the future.

33 | P a g e

ATR of COAL

ATR value from NYMEX

Given

Long term ATR for the Coal is = $ 1.43655

The 14 days ATR is = $ 3.4563

The 5 days ATR is = $ 2.35646

On the bases of the we can say that in the general condition of the market the price movement in

a particular trading day is $ 1.5 which is the long term ATR but we cannot rely only on the long term

analysis we have to know the current volatility as well so we consider the 5 days ATR and 14 Days

ATR which tells us that now days the average movement in the coal prices are near about $ 2.6. So

when we trade in the coal we can say that the expected movement will be near $ 2.5 - $ 3 .but if there

is any news related to the Demand and Supply of the Coal then the prices will more than the ATR

value.

34 | P a g e

Standard Deviation:-

SD is another tool to check the volatility in which we can check the volatility and the price

movement in a particular time duration we are using the same for coal.

The long term 1 year standard deviation is = $ 5.675741

Month wise SD table

Month Standard Deviation

April

May

June

July

August

September

October

November

December

January

February

March

1.89786

3.45644

2.45345

1.75532

3.372067

1.882181

1.438301

1.078546

2.139523

2.471605

3.152573

3.28046

On the bases of the analysing the monthly SD we can say that volatility in the prices is from $ 2.1

to $ 3.1 which means in a particular month the movement of the commodity will be between these

values but again we can say that the coal is mainly based on a fundamental factors so need to

combine the both of the thing then try to find the trend of the Coal.

On the bases of the two of the analysis ATR and SD says that in a particular normal trading day

when there is no news in the market the Coal prices will move up to the $ 2 to $ 3 and in case of the

market news the Coal price can move up to $ 5 in a particular trading day.

35 | P a g e

3.4 Supply-demand fundamentals for Coal:-

As it is mainly (almost 70% on a global level) used for power generation, coal is competing with

other energy sources and therefore strongly linked to their availability (e.g. hydro conditions, nuclear

plant outages, wind conditions). Retirements and new additional coal-fired power plants are also

fundamental in determining future changes of steam coal demand.

Production is linked to timely and adequate investments in new expansions, productivity rates and

depletion rates of existing reserves, as well as strikes, availability of mining service equipment and

skilled labor, low water levels in inland transportation.

36 | P a g e

Chpter-4

4.1 INTRODUCTION TO NATURAL GAS:-

Natural gas is consisting primarily of methane, with 0-20% hydrocarbons. It is found associated with

other hydrocarbons. It is an important fuel source and a major feedstock for fertilizers.

Most natural gas is created by biogenic, thermogenic and abogenic process. Biogenic gas is created

by methanogenic organisms in marshes, bogs, landfills, and shallow sediments. Deeper in the earth,

at greater temperature and pressure, thermogenic gas is created from buried organic material.

Before natural gas can be used as a fuel, we must remove almost all materials other than methane.

The by-products of that processing include ethane, propane, butanes, pentanes, and higher molecular

weight hydrocarbons, elemental sulfur, carbon dioxide, water vapor, and sometimes helium and

nitrogen.

Natural Gas is colorless, shapeless, and odorless in its pure form. Natural gas is clean burning and

emits lower levels of harmful byproducts into the air. We require energy constantly, to heat our

homes, cook our food, and generate our electricity.

Typical Composition of Natural Gas

Methane CH4 70-90%

Ethane C2H6 0-20%

Propane C3H8

Butane C4H10

Carbon Dioxide CO2 0-8%

Oxygen O2 0-0.2%

Nitrogen N2 0-5%

Hydrogen sulfide H2S 0-5%

Rare gases A, He, Ne, Xe, trace

37 | P a g e

The natural gas that is delivered to your home, it is almost pure methane. Methane is a molecule

made up of one carbon atom and four hydrogen atoms, and is referred to as CH4. Mercaptan aids in

detecting any leaks.

Natural gas has many uses, generally it is found underneath of earth with other hydrocarbons.

Production companies search for presence of these reservoirs by using technology that helps to find

the location of the natural gas, and drill wells in the earth where it is likely to be found. The natural

gas is refined to remove water, other gases, sand, and other compounds. Propane and Butane are

removed and sold separately. Other impurities are also removed, such as hydrogen sulfide. Then

clean natural gas is transmitted through a network of pipelines.

4.2 Price Volatility in Natural Gas:-

The price volatility in the natural gas can be analyzed in the short term and long term. As we had

the ATR and Standard Deviation for analyzing the price volatility of crude oil and it is also an energy

commodity so we are applying the same method for the coal also. The natural gas is less volatile then

the Crude Oil because the Natural Gas market is not that much developed as the Crude Oil market.

Natural Gas has correlation with Crude oil. If the prices of the crude oil will increase the prices of the

Natural Gas increase the price of Natural Gas will also increase. Initial Days crude oil was the only

source of energy but after the development of the natural gas sector it is also considered as a major

energy commodity. Because of the wide Industrial use of natural gas now small change in the price

hampers the growth of the industry and the economy. The only way to secure ourselves is to do

hedging of the commodity in the crude oil market. For that we need to know how much Natural Gas

price can move according to that the companies try to hedge their position in the market.

38 | P a g e

ATR of NATURAL GAS:-

ATR value from NYMEX

Given

All time average ATR is = 0.1498101

Maximum value of the 14 days ATR = 0.64708

Maximum value of the 5 days ATR = 1.0535879

5 day ATR and the 14 days ATR can be use for the research work and for trading but all time

ATR is also good for the analysis.

As the all time ATR is showing that the movement is around $ .15 which means in a general

market the price of the Natural Gas moves either side of the market by $ .15. But we know that it is

considering a long term so the data will not be sufficient in the current market because it is more

volatile than last decade.

The 5 days ATR is showing the value of $ 1.06 that means according to the current market

volatility and the time of the energy shocks the price of the Natural Gas may move up to the $ 1 so at

the time of the important news in the market we can expect the price will change up to $ 1 in one

trading day.

The 14 days ATR is showing the value of $ .65 that means in a 14 trading day the maximum

volatility was $.65. On the bases of the average of the last month 5 days and 14 days ATR the values

are near about the $ .15 so we can say that in a particular trading day the price of the Natural Gas can

move up to $ .15 and then we can expect the market will retrace the price or will go to the side wave.

Again it is better to have all three ATR for the trading of Natural Gas because there are many

factors which are influencing the price and in that condition we can use these values as levels for the

trading as support and resistance level.

39 | P a g e

Standard Deviation:-

Month Standard Deviation

value

January

February

March

April

May

June

July

August

September

October

November

December

January

February

March

0.205596

0.195777

0.105677

0.885451

0.185215

0.140683

0.088427

0.290022

0.163761

0.215118

0.143578

0.121659

0.28379

0.262

0.228274

Now if we look at the SD on month bases then we find that the average SD for the Natural Gas is

$ .25 so we can say that the average movement in the Natural Gas in a particular trading day is $.25-

$.30, In case of the huge volatility the movement can be change but in last few days there is no such

news in the market so we can say that the movement will not high but in particular time of the day

the expected movement will be$ .25.

Now if analyze the both values ATR and the SD then we will find that the volatility of the

Natural Gas is $.15 - $.25, and in case of adverse condition or big market news the market can move

up to $ 1.

40 | P a g e

4.3 Relation between Crude Oil and Natural Gas Prices: -

The availability of natural gas supplies act as a demand dampener for crude oil in the form of

competition for residual crude oil in electricity generation and with distillate crude‟s for space

heating applications. Thus, there stands a relationship between the prices of natural gas and crude oil.

Despite the substitution effect of natural gas prices on crude oil prices, prices were found to have a

positive correlation

While there is a strong stable long-run price relationship between oil and natural gas prices,

seasonal fluctuations and other factors such as abrupt changes in weather, supply disruptions and

inventory trends can alter this price relationship in the short-term.

41 | P a g e

4.4 price driving factors of natural gas

Factors Affecting Short Term Demand for Natural Gas: -

Demand for natural gas has been cyclical in nature. Demand for natural gas depends highly on the

time of year, and changes from season to season. In the past, the cyclical nature of natural gas is:

demand was highest during the coldest months of winter and lowest during the warmest months of

summer. The driver for this cycle of natural gas demand is the need for residential and commercial

heating. This has resulted in demand for natural gas showing spikes in January and February, and

Low during the months of July and August.

The recent change in the use of natural gas for the generation of electricity has resulted in an

deviation in this traditional cyclical behavior. Requirements of natural gas for heating decrease

during the summer months demand for space cooling increases during this warmer season. As we

know Electricity is the primary source of energy for residential and commercial cooling

requirements, it is leading to an increase in demand for electricity. Because natural gas is used to

generate a large portion of electricity, simply increased electrical demand often means increased

natural gas demand. This results in a smaller spike in natural gas demand during the warmest months

of the year. Thus, natural gas demand experiences its most pronounced increase in the coldest

months, but as the use of natural gas for the generation of electricity increases, the magnitude of the

smaller summer peak in demand for natural gas is expected to become more pronounced.

There are two primary drivers that determine the demand for natural gas in the short term:

Weather – as we know that natural gas demand peaks during the coldest months of the year and

tapers off during the warmest months of the year, with a slight increase during the summer to meet

the demands of electric generators. The weather during any particular season has effect on cyclical

demand for natural gas. The colder the weather during the winter, the more pronounced will be the

winter peak. A warm winter may result in a less winter peak. Extremely hot winter can result in even

greater cooling demands, which in turn increase summer demand for natural gas.

Fuel Switching - demand and supply in the marketplace determine the short term price of natural

gas. This can work in reverse as well; the price of natural gas can affect its demand. This is

particularly true for those consumers who have the capacity to switch the fuel upon which they rely.

While most residential and commercial customers rely solely on natural gas to meet many of their

energy requirements, some industrial and electric generation consumers have the capacity to switch

42 | P a g e

between different fuels. For example, during a period of extremely high natural gas prices, many

electric generators may switch from using natural gas to using cheaper coal, thus decreasing the

demand for natural gas.

Economy - The state of the economy in general can have a considerable effect on the demand for

natural gas in the short term. If the economy is developing then output from industrial sectors will

also increasing at the same rate. If the economy is in recession, output from industrial sectors will

drops. These fluctuations in industrial output accompanying economic upswings and downturns

affects the amount of natural gas needed by these industrial users. For Example, during the economic

downturn of 2001, industrial natural gas consumption fell by 6%. Thus we can say that the short term

status of the economy has an effect on the amount of natural gas consumed.

Factors Affecting Long Term Demand for Natural Gas

It is the long term demand factors that reflect the basic trends for natural gas use into the future. In

order to analyze those factors that affect the long term demand for natural gas, we can examine

natural gas demand by sector. It is useful to have an understanding where and how the natural gas

can be used in different sector.

Transportation Sector Demand

Natural gas use in the transportation sector is still in its in starting stage, Demand from the

transportation sector accounts for 3 % of total world natural gas demand. Natural gas supplies barely

a fraction of the total energy used in the transportation sector.

The demand for alternative fuel vehicles is expected to increase in the future primarily due to new

legislation and regulation about the emissions from the transportation sector. As more stringent

emissions standards are adopted.

43 | P a g e

Electric Generation Demand

The demand for electricity is increase by an average rate of 1.8 % per year through to 2025. In order

to meet this growing demand, 335 Giga watts of new electric generation capacity are expected to be

needed by 2025. Relatively low capital requirements for building natural gas fired combined cycle

generation plants, and the reduction of emissions that can be earned from using natural gas as

opposed to other dirtier hydrocarbons like coal, we expects 57 % of new electric generation capacity

built by 2025 will be natural gas combined-cycle or combustion turbine generation. Natural gas fired

electricity generation accounted for 16 percent of all generation in 2002.

Residential and Commercial Demand

We expect residential energy demand to increase 25 percent between 2002 and 2025. Residential use

of natural gas is expected to increase by 1.5 percent per year from 2002 to 2010 and 0.9 percent from

2010 to 2025, increasing 25.5 percent from 2002 to 2025. Residential natural gas consumption

accounts for 12 percent of all consumption in the world.

The analyses of factors that affect long term demand across all sectors are complicated. The actual

demand for any source of energy relies on a variety of interrelated factors, and it is very difficult to

predict how these factors will combine to shape overall demand.

Hurricanes can impact both the supply of and demand for natural gas. For example, as hurricanes

approach the Gulf of Mexico, offshore natural gas platforms are shut down as workers evacuate,

thereby shutting in production. In addition, hurricanes can also cause severe destruction to offshore

(and onshore) production facilities. For example, Hurricane Katrina (2005) resulted in massive shut-

ins of natural gas production.

Hurricane damage can also reduce natural gas demand. The destruction of power lines interrupting

electricity produced by natural gas to distribute , can result in significant reduction in demand for a

given area (e.g., Florida).

44 | P a g e

Factors Affecting the Supply of Natural Gas: -

The production of natural gas in the world is based on competitive market forces: inadequate supply

at any one time leads to price increases, and it signal to production companies that they need to

increase the supply of natural gas to the market. Supplying natural gas in the world in order to meet

this demand, however, is dependent on a number of factors: -

Short Term Supply Barriers

Price signals would be recognized and acted upon immediately, and there would be little lag time

between increased demand for natural gas, and an increase in supplies reaching the market. In reality,

this lag time does exist.

Availability of Skilled Workers – it is very difficult to find the skilled workers and to train them, it

requires time and money. So in that time the production is low and the demand is increasing

according to the market. For example, from 1991 to 1999, relatively low prices indicated adequate

supplies of natural gas existed, and the exploration and production industry contracted in response. In

this period, the U.S. Bureau of Labor Statistics recorded a 26 percent average decrease in

employment in the oil and gas extraction industry. Some of these workers left the industry altogether

rather than remain unemployed. The production companies began to react to higher prices in late

1999. So the companies have to pay higher wages to the workers.

Natural Gas Prices and Drilling Rig Operation:

Availability of Equipment - Drilling rigs are very expensive. Price volatility in the industry makes it

very difficult for producers, as well as production equipment suppliers, to plan the construction and

placement of drilling rigs far in advance. Low prices results in reduction of the number of available

rigs. If prices respond to increase demand, and drilling activity increases, time is required to build

and place an adequate number of drilling rigs. For this reason, drilling rig counts are a good

indication of the status of the oil and natural gas production industry.

Inclement Weather Can Disrupt Offshore Operations

Weather and Delivery Disruptions - weather patterns may have a significant impact on natural gas

production. For instance, hurricanes can have an impact on the offshore production of natural gas, as

safety measures require the temporary shutdown of offshore drilling and production platforms. While

45 | P a g e

the safety record of the natural gas industry is extremely good, malfunctions and accidents may occur

from time to time that disrupt the delivery of natural gas.

On the bases of the previous analysis we can say that:-

The demand for natural gas is mainly driven by the following factors:

Weather

Demographics

Economic growth

Fuel competition

Storage

Exports

The supply for natural gas is mainly driven by the following factors:

Pipeline capacity

Storage

Gas drilling rates

Natural phenomena

Technical issues

Imports

International Trade of Natural Gas

26.3% of total world marketed natural gas production was internationally traded. LNG tankers trade

accounted for 21% of total international trade. The low share of international trade is due to the high

transportation costs. Natural gas is complex to transport and requires large investments, while many

gas resources are far from consuming centers. The construction and management of pipelines also

poses legal and logistical problems. Most LNG trade takes place in Asia-Pacific, with Indonesia,

Malaysia and Australia as exporting countries and Japan as the main importing country. Algeria and

Qatar are also major exporters of LNG.

46 | P a g e

4.5 Trends in natural gas prices

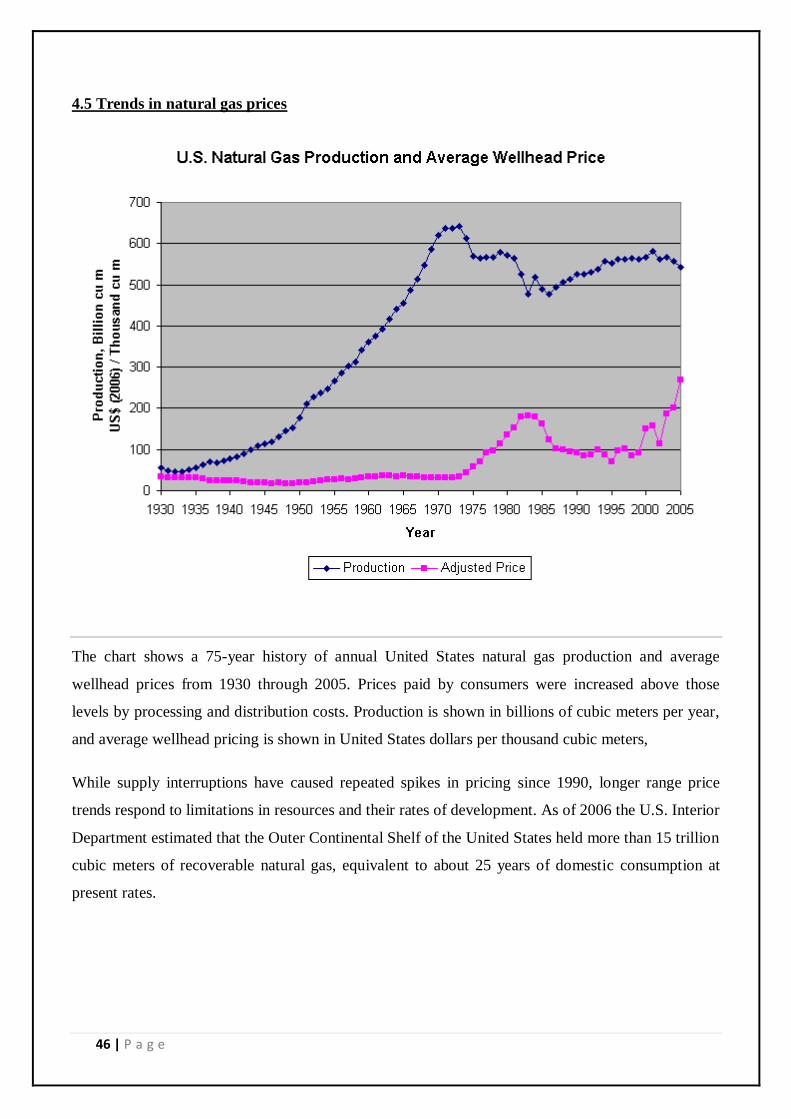

The chart shows a 75-year history of annual United States natural gas production and average

wellhead prices from 1930 through 2005. Prices paid by consumers were increased above those

levels by processing and distribution costs. Production is shown in billions of cubic meters per year,

and average wellhead pricing is shown in United States dollars per thousand cubic meters,

While supply interruptions have caused repeated spikes in pricing since 1990, longer range price

trends respond to limitations in resources and their rates of development. As of 2006 the U.S. Interior

Department estimated that the Outer Continental Shelf of the United States held more than 15 trillion

cubic meters of recoverable natural gas, equivalent to about 25 years of domestic consumption at

present rates.

47 | P a g e

Chapter - 5

Conclusion:-

Energy commodities play an important role in the economy. Small change in the price of these

commodities leads to big losses to the consumers. In the research we tried to find the factors

affecting the price and the movement of the price in a particular day. The study carried out by the

technical and statistical tools followed by analysis of the factors affecting the price of Crude oil,

Natural gas and Coal.

These three commodities are the major commodities which having influence in all the

sectors. And we find that in a particular trading day in normal condition the prices of crude

oil moves between $ 2- $ 3 and if there is any news in the market it may become more

volatile and move according to the news in the market. The factors which are affecting the

crude oil are Weekly US crude and product demand, Weekly crude and product inventories,

Weekly crude oil and product imports, Weekly refinery production of crude oil and products

etc, Weather conditions, Natural gas prices, Trend in other global markets, Currency

movements and Political/geopolitical issues.

Natural Gas market is developing now as these days and the demand is increasing

continuously. In the study we find that in general conditions it moves between$.15- $ .25 and

in adverse condition it can move up to $1. Natural gas having a very good correlation with

crude oil. Crude oil and the demand in power sector and transportation sector influence the

price of natural gas with majorly considering the factors affecting the supply.

Coal is another prominent commodity used mainly in the power generation so the industrial

demand and the demand in the power sector having influence in the price of coal. Majorly the

coal is not traded in exchanges it is traded in OTC market. Analysis says that the movement

in the price of coal is between $ 2- $ 3 and the other market condition it can be reach up to

$5.5.

There are still many factors which are affecting the prices such as the correlation between the

commodities and the effect of the change in the price currency value in which the commodity

traded.

48 | P a g e

Bibliography

1)Cofnas ABE, ”Ol in charge”

2) GAO, “ Natural gas analysis of hang in maet prce”

3) Gua Hui & Kliesen Kivin, “ Oil price volatility and US micro economic activity”

4) Ahmad R Jalali & Naini, Kazimi Mariyam, “Price volatility and hedging variables risk premium

in crude oil market”

5) Abosedra Salah, Radcheneso Stanislav, “New evidence on the asymmetric gasoline price:

volatility vs margin?”

6) Lie Thomas K, “ Volatility relationship between crude oil & petroleum product”

Websites:

http://weatherbugbrowserbar.mysearch.com/search/redirect.jhtml?qid=0FEAEA5868BE6FC

84B42FF8E556E677D&action=click&p=AJmain&ss=sub&ptnrS=&st=bar&cb=WB&pg=AJ

main&ord=18&searchfor=Descriptive+Research&tpr=jrel3&redirect=AJmain.jhtml&ct=RR

http://www.onlinetradingconcepts.com/TechnicalAnalysis/MovingAverageEnvelopes.html

http://www.geocities.com/dancoman/TA/gannangles.html

http://chartschool.wordpress.com

http://ask.reference.com/related/Descriptive+Research?

http://answers.yahoo.com/question/index?qid=

http://www.powermin.nic.in/

http://www.globalcoal.com/

http://www.coalspot.com/

http://www.mccloskeycoal.com/

http://www.coalindia.in/

http://seekingalpha.com/search/articles/?q=crude&cx=00151423756733

49 | P a g e

http://www.marketoracle.co.uk/

http://www.marketwatch.com/