analysis of a local sales tax in the city of milwaukee

DESCRIPTION

Analysis of a Local Sales Tax in the City of Milwaukee. Carrie Hoback Michael O’Callaghan Alan Paberzs Allison Schill Samuel Wayne. Prepared for the Budget Office of the Division of Budget and Management (DBM) of the City of Milwaukee. Presentation Outline. - PowerPoint PPT PresentationTRANSCRIPT

1

Analysis of a Local Sales Tax in the City of Milwaukee

Carrie HobackMichael O’Callaghan

Alan PaberzsAllison Schill

Samuel Wayne

Prepared for the Budget Office of the Division of Budget and Management (DBM) of the City of Milwaukee

2

Presentation Outline

1. What is Milwaukee’s current fiscal situation?

2. What are other cities doing?

3. How will a sales tax affect the economy?

4. What is the tax incidence of a city sales tax?

5. Revenue estimates: how much can it raise?

3

Costs of providing public services are increasing at a faster rate than available

revenues creating a “fiscal gap”

Problem Statement

4

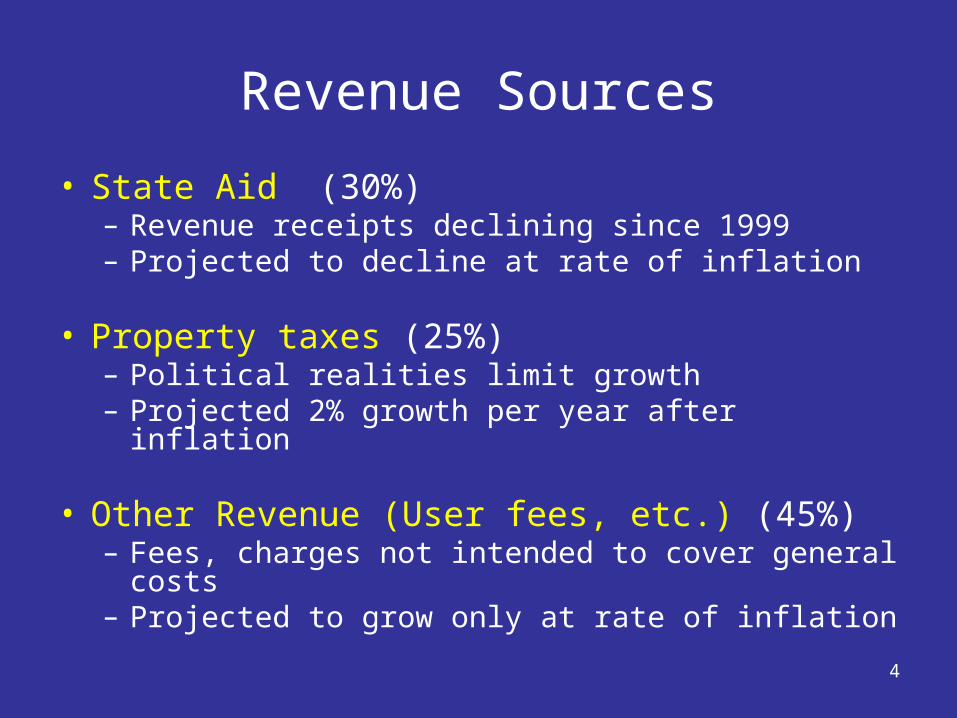

Revenue Sources

• State Aid (30%)– Revenue receipts declining since 1999 – Projected to decline at rate of inflation

• Property taxes (25%)– Political realities limit growth – Projected 2% growth per year after inflation

• Other Revenue (User fees, etc.) (45%)– Fees, charges not intended to cover general costs– Projected to grow only at rate of inflation

5

Expenditures

• Cost of maintaining current service levels projected to increase annually at 0.73%, after inflation

• Projections– 80% of the City budget is personnel related.

– Personnel cost increases 2006-2015:

Average difference of Consumer Price Index and Employment Cost Index from 1996-2004.

6

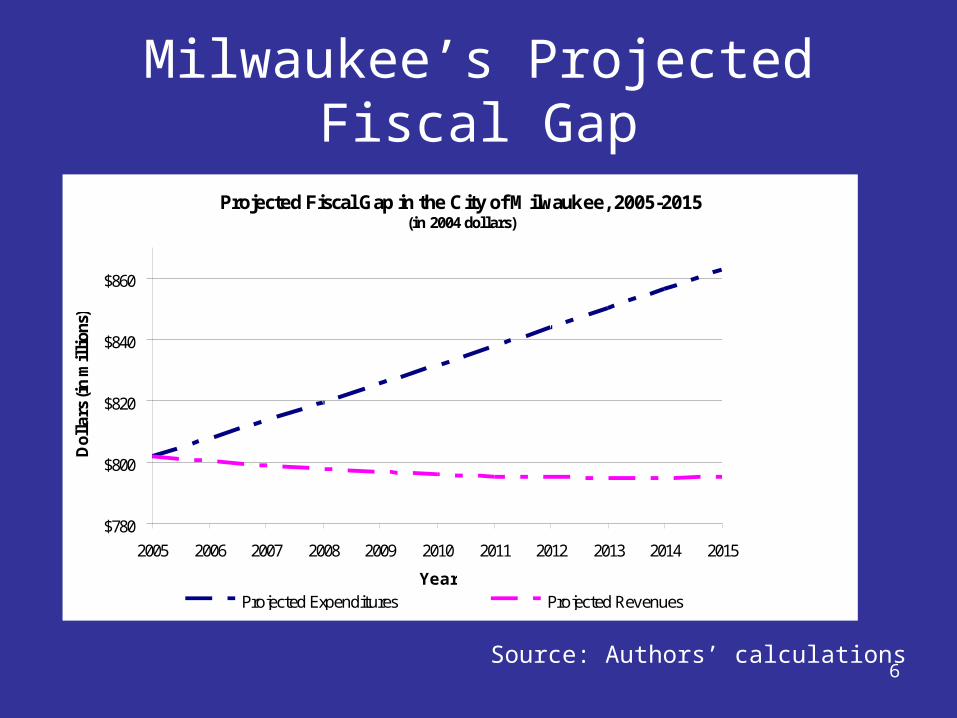

Milwaukee’s Projected Fiscal Gap

Projected Fiscal Gap in the City of Milwaukee, 2005-2015(in 2004 dollars)

$780

$800

$820

$840

$860

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Year

Dol

lars

(in

mil

lion

s)

Projected Expenditures Projected Revenues

Source: Authors’ calculations

7

Is a city sales tax a good way to close the fiscal gap?

Policy Question

8

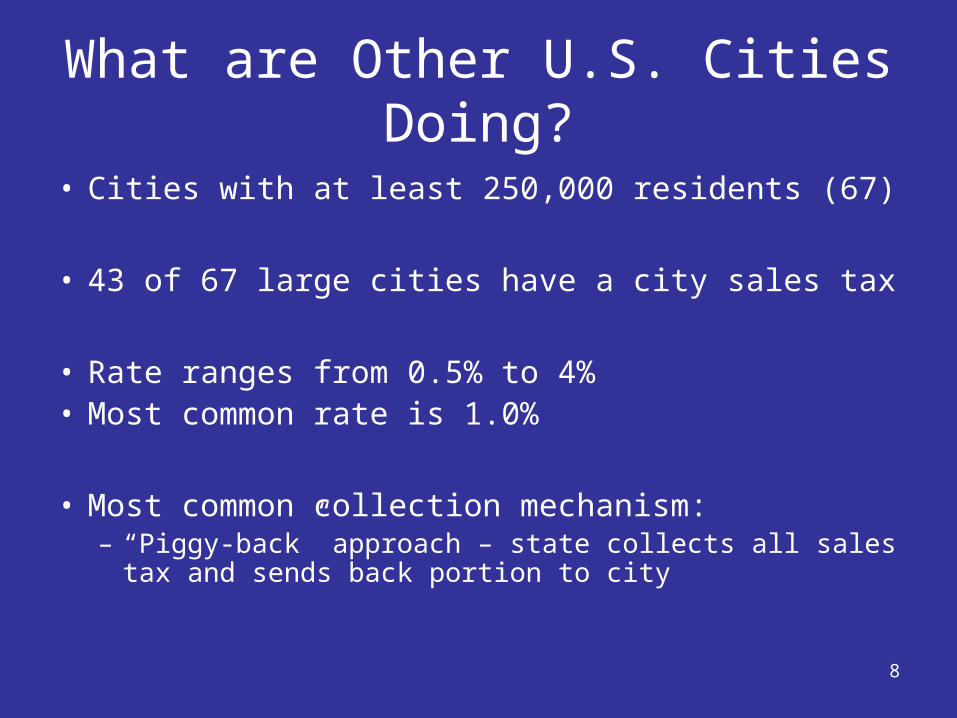

What are Other U.S. Cities Doing?

• Cities with at least 250,000 residents (67)

• 43 of 67 large cities have a city sales tax

• Rate ranges from 0.5% to 4%• Most common rate is 1.0%

• Most common collection mechanism:– “Piggy-back” approach – state collects all sales tax

and sends back portion to city

9

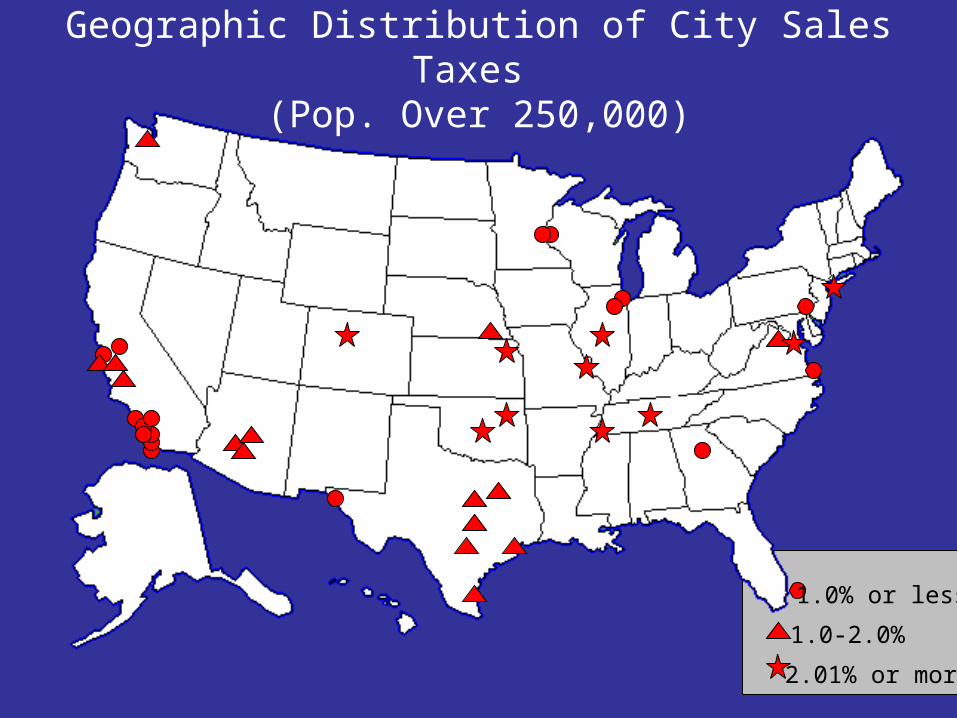

Geographic Distribution of City Sales Taxes (Pop. Over 250,000)

1.0% or less

1.0-2.0%

2.01% or more

10

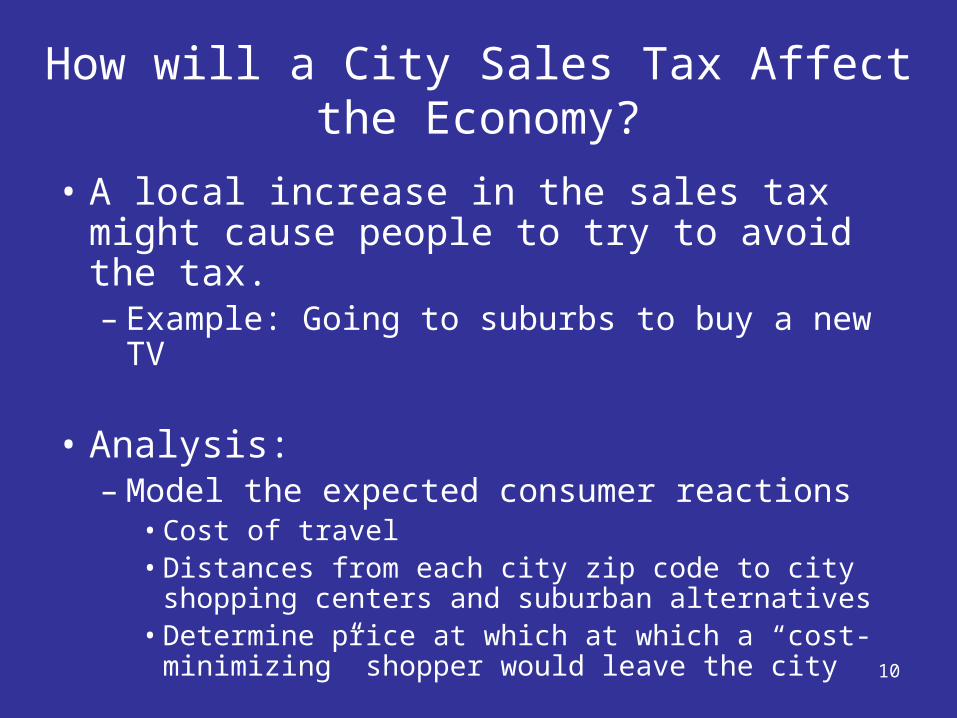

How will a City Sales Tax Affect the Economy?

• A local increase in the sales tax might cause people to try to avoid the tax.– Example: Going to suburbs to buy a new TV

• Analysis:– Model the expected consumer reactions

• Cost of travel• Distances from each city zip code to city shopping

centers and suburban alternatives• Determine price at which at which a “cost-

minimizing” shopper would leave the city

11

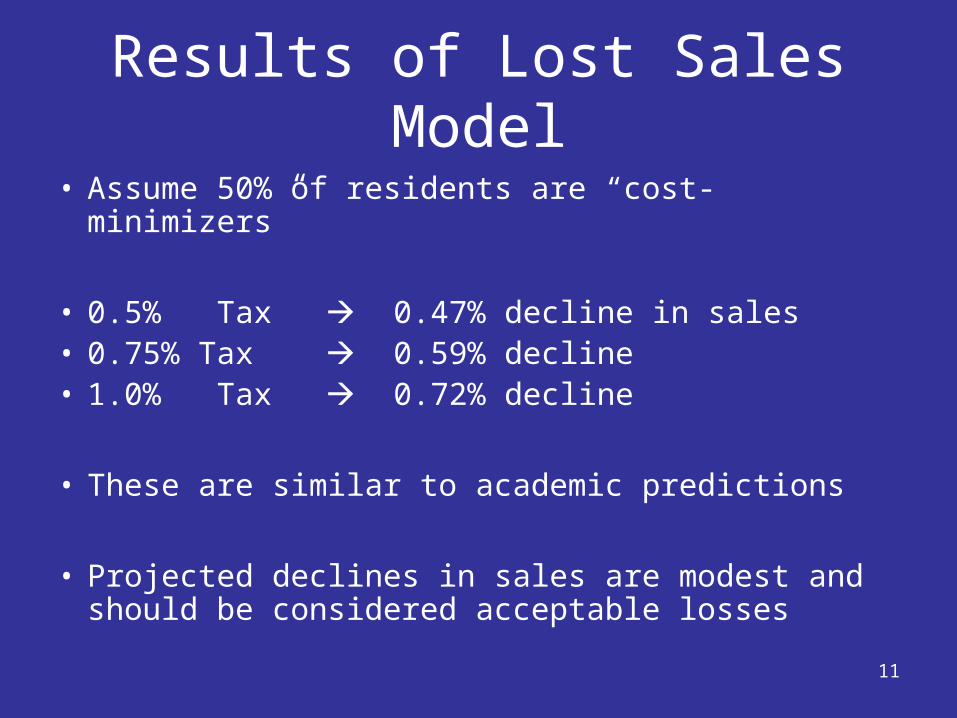

Results of Lost Sales Model

• Assume 50% of residents are “cost-minimizers”

• 0.5% Tax 0.47% decline in sales• 0.75% Tax 0.59% decline• 1.0% Tax 0.72% decline

• These are similar to academic predictions

• Projected declines in sales are modest and should be considered acceptable losses

12

• If not solved with sales tax, then what?

• We assume that the alternative to a city sales tax is an increase in the property tax

Return to the Problem: Fiscal Gap

13

Tax Incidence

• Property Tax vs. Sales Tax

• Residents and Nonresidents

14

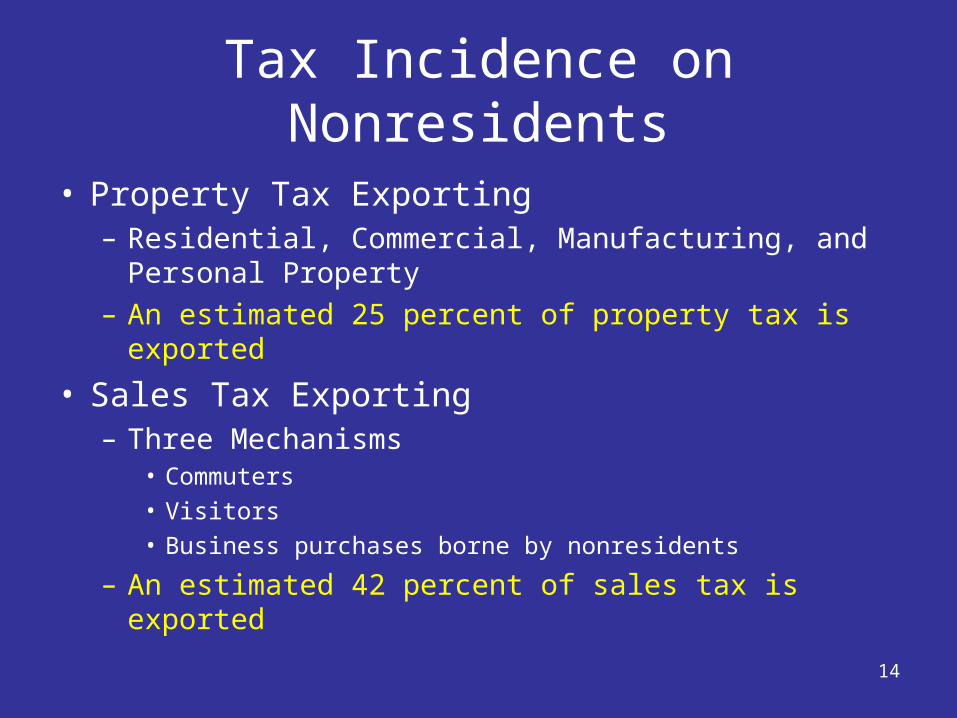

Tax Incidence on Nonresidents

• Property Tax Exporting– Residential, Commercial, Manufacturing, and

Personal Property– An estimated 25 percent of property tax is exported

• Sales Tax Exporting– Three Mechanisms

• Commuters• Visitors• Business purchases borne by nonresidents

– An estimated 42 percent of sales tax is exported

15

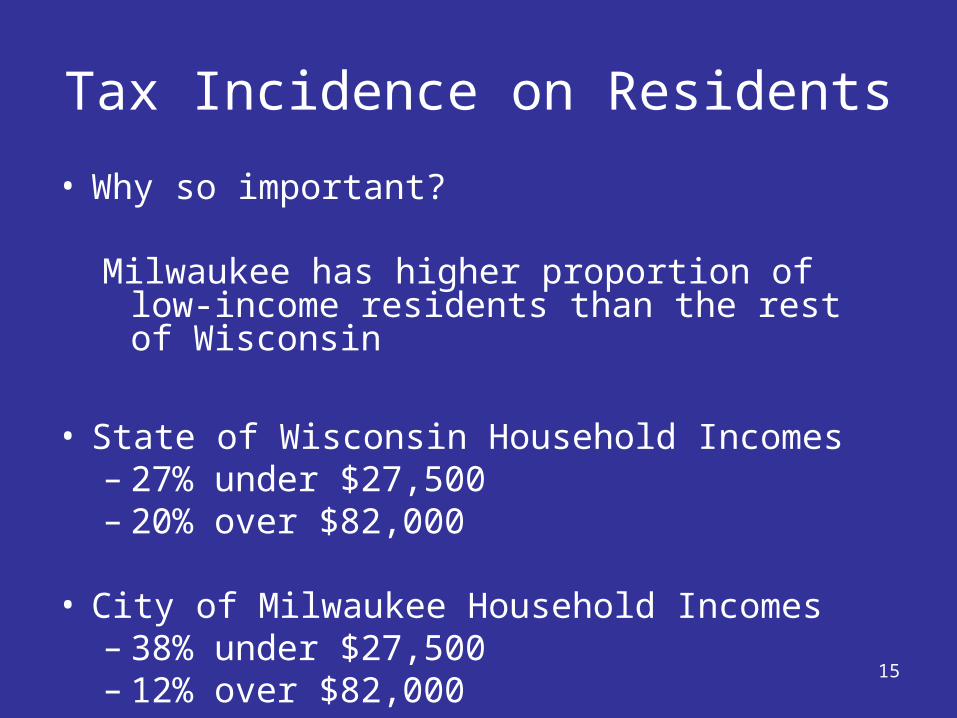

Tax Incidence on Residents

• Why so important?

Milwaukee has higher proportion of low-income residents than the rest of Wisconsin

• State of Wisconsin Household Incomes– 27% under $27,500– 20% over $82,000

• City of Milwaukee Household Incomes– 38% under $27,500– 12% over $82,000

16

Tax Incidence: Property vs. Sales(Drawing local conclusions from state data)

0%

1%

2%

3%

4%

5%

6%

7%

8%

poorest 20% 2nd 20% 3rd 20% 4th 20% Next 10% Next 9% Top 1%

Household Group

Eff

ecti

ve T

ax R

ate

Sales TaxProperty Tax With Refundable CreditsProperty Tax Without Refundable Credits

Source: DOR Tax Incidence Study

17

Tax Incidence Conclusions

– Sales tax is similarly regressive to a property tax

– More exporting potential with sales tax

18

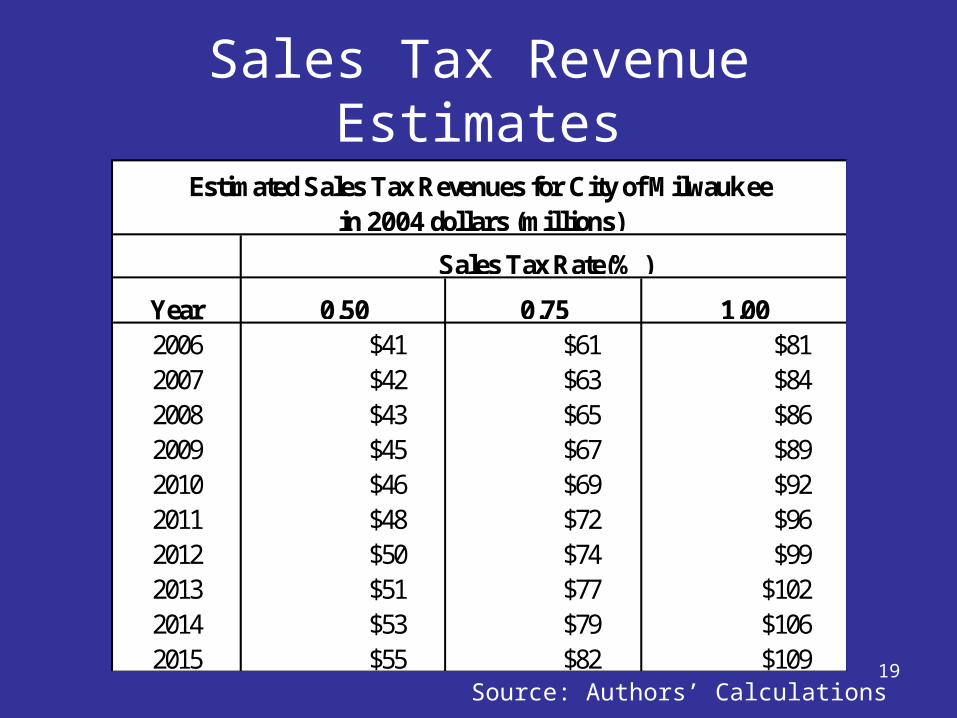

Estimating Sales Tax Revenue for the City of Milwaukee

• Choosing a Reasonable Range– 0.50, 0.75, and 1.00%

• Forecasting Sales Tax Revenues– Methodology

• Milwaukee County Sales Tax Revenues• Consumer Expenditures by Zip Code • Annual Growth in Real Personal Income• Accounting for Economic Competitiveness

19

Sales Tax Revenue Estimates

Year2006 $41 $61 $812007 $42 $63 $842008 $43 $65 $862009 $45 $67 $892010 $46 $69 $922011 $48 $72 $962012 $50 $74 $992013 $51 $77 $1022014 $53 $79 $1062015 $55 $82 $109

Estimated Sales Tax Revenues for City of Milwaukee in 2004 dollars (millions)

Sales Tax Rate(% )

0.50 1.000.75

Source: Authors’ Calculations

20

Closing the Fiscal GapProjected City of Milwaukee Revenue with a Sales Tax and Currently

Projected City Expenditures and Revenues, 2005 to 2015

$780

$800

$820

$840

$860

$880

$900

$920

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Year

2004

con

stan

t dol

lars

(i

n m

illi

ons)

City Expenditures City Revenues City Revenue with 0.5% Sales Tax Revenue

City Revenue with 0.75% Sales Tax Revenue

City Revenue with 1.0% Sales Tax Revenue

Source: Authors’ Calculations

21

Conclusions

• A city sales tax of 0.75% would fill the fiscal gap

• Small decrease in total city sales (0.6%)

• Larger exporting potential than property tax

• Burden on low income residents similar to a property tax