anaging interest rate isk in a rising rate environment · deposit mix relationship between fixed...

TRANSCRIPT

Views expressed are those of the presenter and are not necessarily those of the Federal Reserve Bank of

San Francisco or the Board of Governors.

MANAGING INTEREST RATE RISK IN

A RISING RATE ENVIRONMENT

December 5, 2013

Wallace Young

Mr. Young is Director of the Risk Coordination Unit at the Federal Reserve Bank of San

Francisco. He joined the Reserve Bank in 1999. In his current capacity, Mr. Young

oversees a team of Risk Coordinators that are responsible for monitoring key banking

risks and supervisory issues, providing guidance and consultative services to

supervisory staff, and working with counterparts throughout the Federal Reserve System

to develop and deploy regulatory and examiner guidance.

Jeffrey Plaskett

Mr. Plaskett is a Senior Examiner and Market & Liquidity Risk Coordinator at the

Federal Reserve Bank of San Francisco. He has over fifteen years of regulatory

experience, covering market and liquidity risk issues at community, regional, and large

financial institutions. He also previously chaired the Federal Reserve’s Market Risk

Coordinator Affinity Group. In his current role, Mr. Plaskett is responsible for

monitoring emerging interest rate, market, and liquidity risks in the 12th District.

Call-the-Fed December 5, 2013 2

Today’s Presenters

Agenda

• Why is Interest Rate Risk a growing concern?

• Why are assumptions becoming more

important?

• What should bank management teams be doing

about this issue?

A Q&A Session will Follow the Prepared

Remarks

Call-the-Fed December 5, 2013 3

Why is Interest Rate Risk a

growing concern?

Call-the-Fed December 5, 2013 4

Short Term Rates Remain Low and Stable

Call-the-Fed December 5, 2013 5

Banks are Going Longer-Term in “Search for Yield”

Call-the-Fed December 5, 2013 6

Source: www.treasury.gov

Treasury Yield Curve

Long Term Interest Rates are Increasing

Call-the-Fed December 5, 2013 7

0.62%

1.41%

2.0% 1.5%

-0.4%

3.6%

2.7%

-0.1%

1.6%

1.0%

-1.2% -2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13

5-Year Treasury Rate

Small < $1B

Mid-Sized $1B - $10B

Large > $10B, excluding Wells Fargo

Unrealized Gains (Losses) on all

Securities / Equity – 12th District Banks in

Aggregate

Investment Portfolios are Declining in Value

Call-the-Fed December 5, 2013 8

Earnings-at-Risk

Measures extent to which a

change in interest rates will

reduce a bank’s Net Interest

Income.

Capital-at-Risk

Measures extent to which a

change in interest rates will

reduce a bank’s Economic

Value of Equity (EVE).

According to their own models, most

banks are positioned to benefit from

rising rates. But, this is largely

dependent on many important

assumptions.

Unrealized losses are only realized

when the bank sells the investment.

But, unrealized losses do limit the

bank’s flexibility and ability to

generate liquidity.

Call-the-Fed December 5, 2013 9

Why are assumptions becoming

more important?

Call-the-Fed December 5, 2013 10

Deposit Growth & Mix

December 5, 2013 11

0%

5%

10%

15%

20%

0%

20%

40%

60%

80%

100%

4Q1985 4Q1988 4Q1991 4Q1994 4Q1997 4Q2000 4Q2003 4Q2006 4Q2009 4Q2012

Fed

Fu

nd

s R

ate

(%

)

% o

f T

ota

l D

epo

sits

Deposit Mix

Recession

FF (right)

Time/Total

Deposits

NMD/Total

Deposits

Source: Call report

1985-2008 Average: 62%

1985-2008 Average: 38%

83%

17%

Call-the-Fed

Deposit Assumptions

• Deposit assumptions have a significant impact on Interest Rate

Risk measurements.

• The current environment may provide misleading data for banks

if data trends are not properly analyzed.

December 5, 2013 12

Assumption Definition

Beta Relative repricing rate assumed for deposits versus a benchmark

rate

Account Balance Projected balances assumed over a stated time horizon

Deposit Mix Relationship between fixed vs. floating interest bearing accounts

Call-the-Fed

Case Study

• Sample Bank has historically funded its operations with core deposits.

• Deposit mix has shifted dramatically toward non-maturity deposits over the last few years, which have seen above historical average deposit growth.

• Asset side of the balance sheet has seen growth in investment portfolio (primarily Mortgage Backed Securities) and fixed rate loan portfolio.

• The bank calculates its Earnings at Risk (E@R) exposure to a parallel 200 basis point rise in rates to be positive 5.8 percent (an increase to net interest income).

December 5, 2013 13 Call-the-Fed

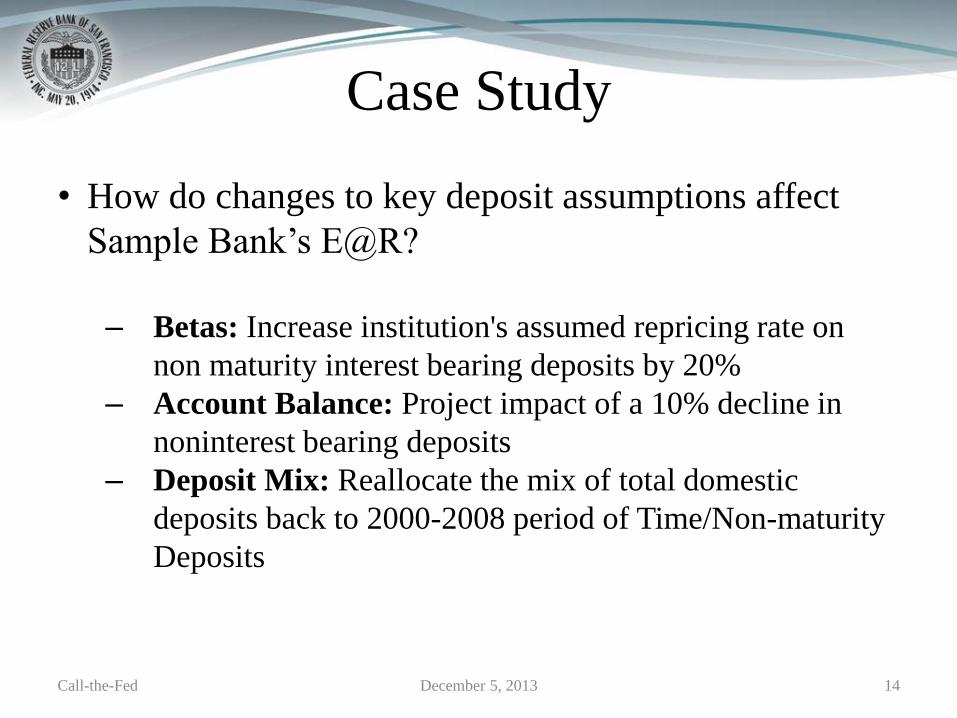

• How do changes to key deposit assumptions affect

Sample Bank’s E@R?

– Betas: Increase institution's assumed repricing rate on

non maturity interest bearing deposits by 20%

– Account Balance: Project impact of a 10% decline in

noninterest bearing deposits

– Deposit Mix: Reallocate the mix of total domestic

deposits back to 2000-2008 period of Time/Non-maturity

Deposits

December 5, 2013 14

Case Study

Call-the-Fed

December 5, 2013 15

Case Study

5.8%

3.6%

-0.4%

-1.5%

E@R at + 200 bps E@R with Beta adjustment

E@R with Deposit Mix adjustment E@R with Deposit Decay Adjustment

Earnings at Risk Analysis

Call-the-Fed

What should bank management

teams be doing about this issue?

Call-the-Fed December 5, 2013 16

1. Conduct critical reviews of assumptions used

in interest rate risk measurement process.

Focus on non-maturity deposits.

How will “surge”

deposits behave?

Call-the-Fed December 5, 2013 17

2. Stress test your assumptions.

Pay more attention to those assumptions that

are more significant to the outcome.

If we changed this

assumption “X%” what is

impact on overall

exposure?

Call-the-Fed December 5, 2013 18

3. Evaluate impact to interest rate risk when

making investment decisions.

Determine if the proposed security will

increase or decrease interest rate risk, prior to

making the purchase decision.

Is that small, additional

yield worth the extra

interest rate risk?

Call-the-Fed December 5, 2013 19

4. Validate your interest rate risk modeling

process.

Important models and risk management

systems should be subject to ongoing,

periodic validation and audit. How confident are you

that your interest rate risk

measurement process is

working?

Call-the-Fed December 5, 2013 20

5. Ensure robust discussions with the Board.

Ensure the Board of Directors fully

understand the institution’s risk exposure.

Do the directors understand

how interest rate changes

will impact the institution’s

earnings and financial

condition?

Call-the-Fed December 5, 2013 21

For further information and resources:

• Joint Policy Statement on Interest Rate Risk (May 23, 1996)

• Interagency Advisory on Interest Rate Risk Management (January 6, 2010)

• Interagency Advisory on Interest Rate Risk Management Frequently Asked Questions (January 12, 2012)

http://www.federalreserve.gov/bankinforeg/topics/market_risk_mgmt.htm

Call-the-Fed December 5, 2013 22

Let’s Take Some Questions …

Call-the-Fed December 5, 2013 23

Thank you!

Call-the-Fed December 5, 2013 24