an overview on financial planning, investments and loans.docx

TRANSCRIPT

An Overview on Financial Planning, Investments and Loans

Financial Planning:

Introduction:

Some people claim that money isn’t important, yet most of us spend at least 45 to 55 hours a week working for money. The simple truth is that to fulfill our desires and needs we need money. Thus, the sooner we take control of our finances, the sooner we can start putting them to good use, which will improve the quality of our lives.

Financial Planning:

For some people financial planning may simply mean “Cash Flow Planning”, for some it may be restricted to “Tax Planning”, other may think that financial planning is about investments keeping in mind the tax planning issue.

But the simplest and most proper definition of financial planning may be as follows:

“Financial planning is the process of meeting life’s goals like buying a house, saving for child’s education or planning for retirement through the proper management of finances.” [As per CFP Board of Standards, Inc]

Benefits of Financial Planning :

Financial planning can achieve the following for an individual:

1. Organize their finances2. Improve cash flow3. Lower personal income taxes4. Plan for retirement5. Plan for education expenses6. Improve investment performance7. Lower investment risk8. Reduce insurance cost

Cash Flow and Budgeting:

Cash flow refers to the inflow and outflow of money. In simple terms, keeping a record of income and expenses.

The purpose of cash flow planning refers to the process of identifying the major expenditures in future (both short term and long term) and making planned investments so that the required amount is accumulated within the required time frame.

The income of an individual will be more or less within an anticipated range. Unless proper budgeting is done and expenditures are controlled, the individual might get in a debt trap. Budgeting is the best, most practical way to keep track of spending and more importantly to keep a grip on it. When we have a budget we can make sure our income and expenses match.

Process of making a budget:

Step 1:

List the source of income. Income that is regular counts the most. This includes money from a job, a pension, or other regular source.

There may be certain income which may not be accurately estimated on a monthly basis. For example, interest and dividend incomes, bonuses, income from business, etc. In these situations, an annual estimate should be made and divided by 12 to arrive at monthly figures.

Step 2:

Expenses should be divided into three categories: fixed, variable and discretionary.

1) Fixed expenses : Mandatory expense and one pays the same amount every month. Example- Mortgage or rent payments, insurance premiums, etc.

2) Variable expense : Mandatory expense but amounts vary each month. Example- Electricity bill3) Discretionary expenses : Optional expenses which should be considered if there is any surplus after

accounting for fixed and variable expenses. Example- Investments, entertainment, etc.

Step 3:

Emergency funds planning:

Emergency funds are an absolute necessary for financial security because they give us funds to fall back in moment of crisis. Building an emergency fund is healthy for financial well being. Success at building an emergency fund depends on consistency of saving money on a regular basis and resisting the urge to dip into this rainy day fund for non emergencies.

The minimum amount in emergency fund should be 3 to 6 months worth of basic living expenses . This money should be kept separate from the general savings account.

Step 4:

Monitoring, evaluation and compliance of Budgets:

Due to changes in circumstances and priorities, actual figures may change than budgeted. If it appears that the actual figures differ substantially from the allocation done in the budget then it’s time to relook at the budget more closely and take immediate action to make it more accurate. The following is suggested:

Control excessive expense not planned under budget. Check if expenses under a particular head are budgeted under any other head. Check if there is any one time non discretionary expense which resulted in mismatch of the budget. If necessary, curb discretionary expenses to adjust for increase in expenses not planned earlier in the

budget.

Compliance of a budget is extremely important for achievement of financial objectives. If the required investments are not being made due to mismatch in budgeted figures, it will impact the accumulation plans, thereby affecting the financial plan.

Investment Planning Overview:

Investing is an activity that is made from savings with a desire to earn a better return with some risk. The basic theory driving investment is the belief that the pleasure derived from future consumption will be more than the pleasure foregone today.

Characteristics of an Investment:

1) Return: The return expectation can be the amount received as interest, dividend received on stocks, capital appreciation on assets and many more. Different investments have different returns. Returns from an investment depend on rating, liquidity and time horizon of the investment. It is measured as Holding Period Return.

2) Risk: Risk is an inherent part of any investment activity. Some of the risk associated with an investment can bea) Loss of capital.b) Delay in repayment of capital,c) Non-payment of interest,d) Variability of returns

Risk and return are directly related. Higher the risk taken, higher can be the return, similarly low return comes with low risk.

3) Safety: An investment is considered to be safe, if there is a certainty of return of capital without any loss of the same.

4) Liquidity: The yield on any investment is, to a great extent, a function of liquidity provided by the specific investment. Liquidity in marketable assets are provided by the market, while non marketable assets like fixed deposits cannot be liquidated in market but can be offered for premature repayment to bank.

5) Tax efficiency: An ideal investment is that, which offers tax efficient return commensurate to risk with safety and liquidity.

Objectives of an Investment:

Every investment is considered after evaluating the five characteristics that have been discussed here in above with the following objective:

a) To maximize the returnb) To protect the purchasing power of the savingc) To minimize the risk

Types of Investment

Investment

Financial Investment Non-Financial Investment

a) Cash & Cash Equivalent a) Land & Buildingb) Small Savings Schemes b) Plant & Machineryc) Government Schemes c) Business & like thingsd) Bondse) Equity Sharesf) Mutual Fundsg) Insurance

a) Cash & Cash Equivalent:

Cash is not only physical money, but in the broader term is anything, which can be converted very fast in cash without loss of value.This definition of cash includes:

i. Bank Certificate of Deposits: It is a debt instrument issued by a “bank” in exchange for a deposit made by an investor for a specific term or period. Terms can range from 7 days to 5 years or more. It varies from bank to bank. The interest rates on these deposits are fixed by the respective banks, without any intervention from Reserve Bank of India (RBI), that is, banks are free to offer any interest rate on deposits mobilized. However to sustain and also operate competitively, it is generally based on prime lending rates prevailing in the economy.

ii. Money Market Mutual Funds: They are very short-term debt product offered by mutual fund. Funds collected in these schemes are invested in short-term debt instruments of high credit quality. Some of the money market instruments are:

i. Call money marketii. Treasury billiii. Commercial paperiv. Short term funding

The maturity of their investment portfolio is less than 1 year.

iii. Bank Savings Account: Money deposited in savings bank account are always money at call and can be withdrawn anytime without any loss of capital. The balance maintained in savings bank account also earns interest, though less than what is available on bank fixed deposits.

b) Small Saving Schemes

Small savings schemes are designed to provide safe and attractive investment options to the public and at the same time to mobilize resources for development. National Savings Organization (NSO) is responsible for national level promotion of small savings scheme. Over the years small savings schemes have grown big. These schemes are meant for small urban and rural investors. Institutions are not eligible to invest in major small savings schemes. Non-Resident Indians (NRIs) are also not eligible to invest in small savings schemes.

The following schemes come under small savings schemes:-

1) Post Office Savings Account2) 5 Year Post Office Recurring Deposit Account3) Post Office Time Deposit Account4) Kisan Vikas Patra5) National Savings Certificate6) Post Office Monthly Income Account7) Public Provident Fund (PPF)8) Senior Citizen Savings Scheme

1) Post Office Savings Account:-

Interest Payable, Rates, and Periodicity: 4.0%per annum on individual/ joint accounts.

Minimum Amount for opening of account and maximum balance that can be retained: Minimum INR 20/- for opening.

Salient features including Tax Rebate: 1) Account can be opened by cash only. 2) Minimum balance to be maintained in a non-cheque facility account is INR 50/-. 3) Cheque facility available if an account is opened with INR 500/- and for this purpose minimum balance of INR

500/-in an account is to be maintained.4) Cheque facility can be taken in an existing account also. 5) Interest earned is Tax Free up to INR 10,000/- per year from financial year 2012-13.6) Nomination facility is available at the time of opening and also after opening of account. 7) Account can be transferred from one post office to another. 8) One account can be opened in one post office. 9) Account can be opened in the name of minor and a minor of 10 years and above age can open and operate the

account.10) Joint account can be opened by two or three adults. 11) At least one transaction of deposit or withdrawal in three financial years is necessary to keep the account

active.12) Single account can be converted into Joint and Vice Versa. 13) Minor after attaining majority has to apply for conversion of the account in his name.14) Deposits and withdrawals can be done through any electronic mode in CBS Post offices.15) Inter Post office transactions can be done between CBS post offices. 16) ATM/Debit Cards can be issued to Savings Account holders (having prescribed minimum balance on the day of

issue of card) of CBS Post offices.

2) 5 Year Post Office Recurring Deposit Account:-

Interest Payable, Rates, and Periodicity:From 1.4.2014, interest rates are as follows:-

- 8.4% per annum (quarterly compounded)- On maturity INR 10/- account fetches INR 746.53. Can be continued for another 5 years on year to year basis.

Minimum Amount for opening of account and maximum balance that can be retained: - Minimum INR 10/- per month or any amount in multiples of INR 5/-.- No maximum limit.

Salient features including Tax Rebate: 1) Account can be opened by cash/cheque and in case of cheque the date of deposit shall be date of presentation

of cheque.2) Nomination facility is available at the time of opening and also after opening of account.3) Account can be transferred from one post office to another.4) Any number of accounts can be opened in any post office.5) Account can be opened in the name of minor and a minor of 10 years and above age can open and operate the

account.6) Joint account can be opened by two adults.7) Subsequent deposit can be made up to 15th day of next month if account is opened up to 15th of a calendar

month and up to last working day of next month if account is opened between 16th day and last working day of a calendar month.

8) If subsequent deposit is not made up to the prescribed day, a default fee is charged for each default, default fee @ 5 paisa for every 5 rupee shall be charged. After 4 regular defaults, the account becomes discontinued and can be revived in two months but if the same is not revived within this period, no further deposit can be made.

9) If in any RD account, there is monthly default(s) the depositor has to first pay the defaulted monthly deposit with default fee and then pay the current month deposit. This will be applicable for both CBS and non CBS Post offices.

10) There is rebate on advance deposit of at least 6 installments.11) Single account can be converted into Joint and Vice Versa.12) Minor after attaining majority has to apply for conversion of the account in his name. 13) One withdrawal upto 50% of the balance allowed after one year. 14) Full maturity value allowed on R.D. Accounts restricted to that of INR. 50/- denomination in case of death of

depositor subject to fulfilment of certain conditions.15) In case of deposits made in RD accounts by Cheque, date of credit of Cheque into Government accounts shall be

treated as date of deposit.

3) Post Office Time Deposit Account:-

Interest Payable, Rates, and Periodicity:-Interest payable annually but calculated quarterly.

From 1.4.2014, interest rates are as follows:-

Period Rate1 Year A/c 8.40%2 Year A/c 8.40%3 Year A/c 8.40%5 Year A/c 8.50%

Minimum Amount for opening of account and maximum balance that can be retained: - Minimum INR 200/- and in multiple thereof. - No maximum limit.

Salient features including Tax Rebate:1) Account may be opened by individual. Account can be opened by cash/cheque and in case of cheque the date of

realization of cheque in Govt. account shall be date of opening of account.2) Nomination facility is available at the time of opening and also after opening of account.3) Account can be transferred from one post office to another. 4) Any number of accounts can be opened in any post office. 5) Account can be opened in the name of minor and a minor of 10 years and above age can open and operate the

account. 6) Joint account can be opened by two adults. 7) Single account can be converted into Joint and Vice Versa.8) Minor after attaining majority has to apply for conversion of the account in his name. 9) *In CBS Post offices, when any TD account is matured, the same TD account will be automatically renewed for the

period for which the account was initially opened e.g. 2 Years TD account will be automatically renewed for 2 Years. Interest rate applicable on the day of maturity will be applied.

10) Lock up period of 6 months for premature closer of TD accounts has been removed and as and when any TD accounts is closed before one Year, interest @ savings account applicable from time to time shall be payable. This will be applied for both CBS and non CBS Post offices.

11) The investment under 5 Years TD qualifies for the benefit of Section 80C of the Income Tax Act, 1961 from 1.4.2007.

4) Kisan Vikas Patra

Interest Payable, Rates, and Periodicity: Amount Invested doubles in 100 months (8 years & 4 months)

Minimum Amount for opening of account and maximum balance that can be retained: - Available in denominations of Rs. 1,000, 5000, 10,000 and Rs. 50,000. - Minimum deposit Rs 1000/- - No maximum limit.

Salient features including Tax Rebate:

1) Certificate can be purchased by an adult for himself or on behalf of a minor or by two adults.2) KVP can be purchased from any Departmental Post office.3) Facility of nomination is available.4) Certificate can be transferred from one person to another and from one post office to another.5) Certificate can be encashed after 2 & 1/2 years from the date of issue.

5) National Savings Certificates:- Interest Payable, Rates, and Periodicity:

From 1.4.2014, interest rates are as follows:-

5 Years National Savings Certificate (VIII Issue)- 8.5% compounded six monthly but payable at maturity. INR. 100/- grows to INR 151.62 after 5 years.

10 Years National Savings Certificate (IX Issue)- 8.80% compounded six monthly but payable at maturity. INR 100/- grows to INR 236.60 after 10 years.

Minimum Amount for opening of account and maximum balance that can be retained: - Minimum INR. 100/- No maximum limit available in denominations of INR. 100/-, 500/-, 1000/-, 5000/- & INR. 10,000/-.

Salient features including Tax Rebate:1) A single holder type certificate can be purchased by, an adult for himself or on behalf of a minor or by a minor.2) Deposits qualify for tax rebate under Sec. 80C of IT Act. 3) The interest accruing annually but deemed to be reinvested under Section 80C of IT Act.4) *In case of NSC VIII and IX issue, transfer of certificates from one person to another can be done only once from

date of issue to date of maturity. 5) *At the time of transfer of Certificates from one person to another, old certificates will not be discharged. Name of

old holder shall be rounded and name of new holder shall be written on the old certificate and on the purchase application (in case of non CBS Post offices) under dated signatures of the authorized Postmaster along with his designation stamp and date stamp of Post office.

6) Post Office Monthly Income Account:-

Interest Payable, Rates, and Periodicity:From 1.4.2014, interest rates are as follows:-- 8.40% per annum payable monthly.

Minimum Amount for opening of account and maximum balance that can be retained:

- In multiples of INR 1500/-- Maximum investment limit is INR 4.5 lakhs in single account and INR 9 lakhs in joint account. - An individual can invest maximum INR 4.5 lakh in MIS (including his share in joint accounts).- For calculation of share of an individual in joint account, each joint holder have equal share in each joint account.

Salient features including Tax Rebate:1) Account may be opened by individual.

2) Account can be opened by cash/cheque and in case of cheque the date of realization of cheque in Govt. account shall be date of opening of account.

3) Nomination facility is available at the time of opening and also after opening of account. 4) Account can be transferred from one post office to another. 5) Any number of accounts can be opened in any post office subject to maximum investment limit by adding balance

in all accounts. 6) Account can be opened in the name of minor and a minor of 10 years and above age can open and operate the

account. 7) Joint account can be opened by two or three adults. 8) All joint account holders have equal share in each joint account. 9) Single account can be converted into Joint and Vice Versa.

10) Minor after attaining majority has to apply for conversion of the account in his name. 11) Maturity period is 5 years from 1.12.2011. 12) Interest can be drawn through auto credit into savings account standing at same post office, through PDCs or

ECS./In case of MIS accounts standing at CBS Post offices, monthly interest can be credited into savings account standing at any CBS Post offices.

13) Can be prematurely en-cashed after one year but before 3 years at the discount of 2% of the deposit and after 3 years at the discount of 1% of the deposit. (Discount means deduction from the deposit.)

14) A bonus of 5% on principal amount is admissible on maturity in respect of MIS accounts opened on or after 8.12.07 and up to 30.11.2011. No bonus is payable on the deposits made on or after 1.12.2011.

7) Public Provident Fund 15 Year (PPF):-

Interest Payable, Rates, and Periodicity:From 1.4.2014, interest rates are as follows:-

- 8.70% per annum (compounded yearly).

Minimum Amount for opening of account and maximum balance that can be retained:- Minimum INR. 500/- Maximum INR. 1,50,000/- in a financial year. - Deposits can be made in lump-sum or in 12 installments.

Salient features including Tax Rebate:1) An individual can open account with INR 100/- but has to deposit minimum of INR 500/- in a financial year and

maximum INR 1,50,000/- 2) Joint account cannot be opened. 3) Account can be opened by cash/cheque and In case of cheque, the date of realization of cheque in Govt. account

shall be date of opening of account.4) Nomination facility is available at the time of opening and also after opening of account. Account can be

transferred from one post office to another. 5) The subscriber can open another account in the name of minors but subject to maximum investment limit by

adding balance in all accounts. 6) Maturity period is 15 years but the same can be extended within one year of maturity for further 5 years and so

on. 7) Maturity value can be retained without extension and without further deposits also. 8) Premature closure is not allowed before 15 years. 9) Deposits qualify for deduction from income under Sec. 80C of IT Act.10) Interest is completely tax-free.

11) Withdrawal is permissible every year from 7th financial year from the year of opening account. 12) Loan facility available from 3rd financial year. 13) No attachment under court decree order. 14) The PPF account can be opened in a Post Office which is double handed and above.

8) Senior Citizens Saving Scheme

Interest Payable, Rates, and Periodicity:

From 1.4.2015, interest rates are as follows:-

- 9.3% per annum, payable from the date of deposit of 31st March/30th Sept/31st December in the first instance & thereafter, interest shall be payable on 31st March, 30th June, 30th Sept and 31st December.

Minimum Amount for opening of account and maximum balance that can be retained:- There shall be only one deposit in the account in multiple of INR.1000/- maximum not exceeding INR 15 lakh.

Salient features including Tax Rebate:

1) An individual of the Age of 60 years or more may open the account.2) An individual of the age of 55 years or more but less than 60 years who has retired on superannuation or under

VRS can also open account subject to the condition that the account is opened within one month of receipt of retirement benefits and amount should not exceed the amount of retirement benefits.

3) Maturity period is 5 years. 4) A depositor may operate more than one account in individual capacity or jointly with spouse (husband/wife). 5) Account can be opened by cash for the amount below INR 1 lakh and for INR 1 Lakh and above by cheque only. 6) In case of cheque, the date of realization of cheque in Govt. account shall be date of opening of account. 7) Nomination facility is available at the time of opening and also after opening of account. 8) Account can be transferred from one post office to another. 9) Any number of accounts can be opened in any post office subject to maximum investment limit by adding balance

in all accounts. 10) Joint account can be opened with spouse only and first depositor in Joint account is the investor.11) Interest can be drawn through auto credit into savings account standing at same post office, through PDCs or

Money Order. 12) In case of SCSS accounts, quarterly interest shall be payable on 1st working day of April, July, October and January.

It will be applicable at all CBS Post Offices.13) *Quarterly interest of SCSS accounts standing at CBS Post offices can be credited in any savings account standing at

any other CBS post offices. 14) Premature closure is allowed after one year on deduction of an amount equal to1.5% of the deposit & after 2 years

1% of the deposit. 15) After maturity, the account can be extended for further three years within one year of the maturity by giving

application in prescribed format. In such cases, account can be closed at any time after expiry of one year of extension without any deduction.

TDS is deducted at source on interest if the interest amount is more than INR 10,000/- p.a. 16) Investment under this scheme qualifies for the benefit of Section 80C of the Income Tax Act, 1961 from 1.4.2007.

c) Government Schemes

1) Pradhan Mantri Jan-Dhan Yojana (PMJDY)

It is National Mission for Financial Inclusion to ensure access to financial services, namely, Banking / Savings & Deposit Accounts, Remittance, Credit, Insurance, Pension in an affordable manner.

Account can be opened in any bank branch or Business Correspondent (Bank Mitr) outlet.

PMJDY accounts are being opened with Zero balance. However, if the account-holder wishes to get cheque book, he/she will have to fulfil minimum balance criteria.

Special Benefits under PMJDY Scheme

a) Interest on depositb) Accidental insurance cover of Rs.1 lacc) No minimum balance requiredd) Life insurance cover of Rs.30,000/-e) Easy Transfer of money across Indiaf) Beneficiaries of Government Schemes will get Direct Benefit Transfer in these accounts.g) After satisfactory operation of the account for 6 months, an overdraft facility will be permittedh) Access to Pension, insurance productsi) Accidental Insurance Cover, RuPay Debit Card must be used at least once in 45 daysj) Overdraft facility upto Rs.5000/- is available in only one account per household, preferably lady of the household

Documents required to open an account under Pradhan Mantri Jan-Dhan Yojana

If Aadhaar Card is not available, then any one of the following Officially Valid Documents (OVD) is required: Voter ID Card, Driving License, PAN Card, Passport & NREGA Card. If these documents also contain your address, it can serve both as “Proof of Identity and Address”

Highlights:

Scheme for comprehensive financial inclusion launched by the Prime Minister of India, Narendra Modi on 28 August 2014

Run by Department of Financial Services, Ministry of Finance Inauguration day, 1.5 Cr. bank accounts were opened under this scheme By 28 January 2015, 12.58 Cr. accounts were opened, with around ₹10,590 Cr.

2) Pradhan Mantri Suraksha Bima Yojana

Highlights of the Pradhan Mantri Suraksha Bima Yojana (PMSBY – Accidental Death Insurance) are

Eligibility: Available to people in age group 18 to 70 years with bank account. Premium: Rs. 12 per annum. Payment Mode: The premium will be directly auto-debited by the bank from the subscribers account. This is the

only mode available. Risk Coverage: For accidental death and full disability – Rs 2 Lakh and for partial disability – Rs 1 Lakh. Eligibility: Any person having a bank account and Aadhaar number linked to the bank account can give a simple

form to the bank every year before 1st of June in order to join the scheme. Name of nominee to be given in the form.

Terms of Risk Coverage: A person has to opt for the scheme every year. He can also prefer to give a long-term option of continuing in which case his account will be auto-debited every year by the bank.

Who will implement this Scheme? : The scheme will be offered by all Public Sector General Insurance Companies and all other insurers who are willing to join the scheme and tie-up with banks for this purpose.

The premium paid will be tax-free under section 80C and also the proceeds amount will get tax-exemption u/s 10(10D).But if the proceeds from insurance policy exceed Rs.1 lakh , TDS at the rate of 2% from the total proceeds if no Form 15G or Form 15H is submitted to the insurer.

3) Pradhan Mantri Jeevan Jyoti Bima Yojana

Highlights of the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY - For Life Insurance Cover)

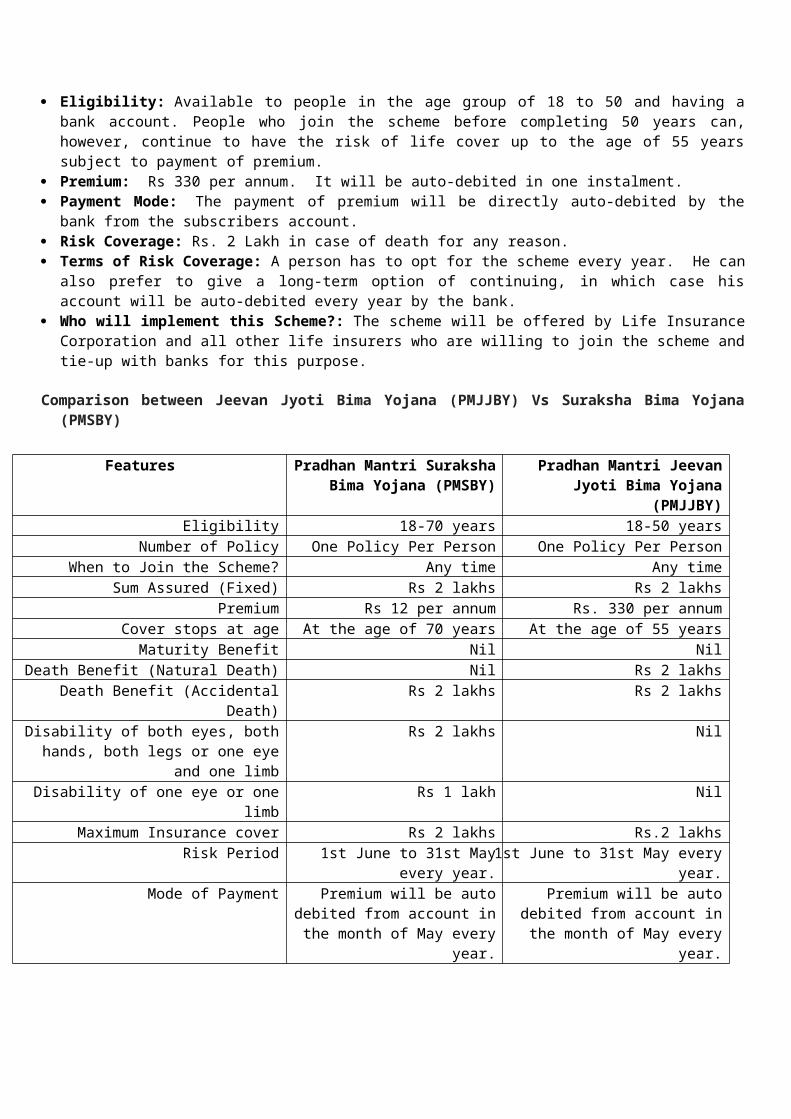

Eligibility: Available to people in the age group of 18 to 50 and having a bank account . People who join the scheme before completing 50 years can, however, continue to have the risk of life cover up to the age of 55 years subject to payment of premium.

Premium: Rs 330 per annum. It will be auto-debited in one instalment. Payment Mode: The payment of premium will be directly auto-debited by the bank from the subscribers account. Risk Coverage: Rs. 2 Lakh in case of death for any reason. Terms of Risk Coverage: A person has to opt for the scheme every year. He can also prefer to give a long-term

option of continuing, in which case his account will be auto-debited every year by the bank. Who will implement this Scheme?: The scheme will be offered by Life Insurance Corporation and all other life

insurers who are willing to join the scheme and tie-up with banks for this purpose.

Comparison between Jeevan Jyoti Bima Yojana (PMJJBY) Vs Suraksha Bima Yojana (PMSBY)

Features Pradhan Mantri Suraksha Bima Yojana (PMSBY)

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

Eligibility 18-70 years 18-50 yearsNumber of Policy One Policy Per Person One Policy Per Person

When to Join the Scheme? Any time Any timeSum Assured (Fixed) Rs 2 lakhs Rs 2 lakhs

Premium Rs 12 per annum Rs. 330 per annumCover stops at age At the age of 70 years At the age of 55 years

Maturity Benefit Nil NilDeath Benefit (Natural Death) Nil Rs 2 lakhs

Death Benefit (Accidental Death) Rs 2 lakhs Rs 2 lakhs

Disability of both eyes, both hands, both legs or one eye and one limb

Rs 2 lakhs Nil

Disability of one eye or one limb Rs 1 lakh Nil

Maximum Insurance cover Rs 2 lakhs Rs.2 lakhsRisk Period 1st June to 31st May every year. 1st June to 31st May every year.

Mode of Payment Premium will be auto debited from account in the month of May

every year.

Premium will be auto debited from account in the month of May every

year.

4) Atal Pension Yojna (APY)

The scheme will be launched on June 1 2015 and focus is on the unorganised sector. A pension provides people with a monthly income when they are no longer earning.

The scheme is administered by the Pension Fund Regulatory and Development Authority (PFRDA) through NPS Architecture.

Under the APY, there is guaranteed minimum monthly pension for the subscribers ranging between Rs. 1000 and Rs. 5000 per month.

The benefit of minimum pension would be guaranteed by the GOI.

GOI will also co-contribute 50% of the subscriber’s contribution or Rs. 1000 per annum, whichever is lower. Government co-contribution is available for those who are not covered by any Statutory Social Security Schemes and is not income tax payer.

GOI will co-contribute to each eligible subscriber, for a period of 5 years who joins the scheme between the period 1st June, 2015 to 31st December, 2015. The benefit of five years of government Co-contribution under APY would not exceed 5 years for all subscribers including migrated Swavalamban beneficiaries.

All bank account holders may join APY.

Eligibility for APY: Atal Pension Yojana (APY) is open to all bank account holders who are not members of any statutory social security scheme.

Age of joining and contribution period: The minimum age of joining APY is 18 years and maximum age is 40 years. One needs to contribute till one attains 60 years of age.

Enrolment agencies: All Points of Presence (Service Providers) and Aggregators under Swavalamban Scheme would enrol subscribers through setup of National Pension System.

Indicative Monthly Contribution Chart

Age of Entry Monthly pension of Rs. 1000

Monthly pension of

Rs.2000

Monthly pension of

Rs.3000

Monthly pension of

Rs.4000

Monthly pension of

Rs.500018 42 84 126 168 21020 50 100 150 198 24825 76 151 226 301 37630 116 231 347 462 57735 181 362 543 722 90240 291 582 873 1164 1454

Charges for default

In Atal Pension Yojna monthly contribution would automatically be deducted from Subscriber’s bank account. Subscriber should ensure that the Bank account to be funded enough for auto debit of contribution amount. If there is delay in contributions then Bank would levy penalty. The fixed amount of interest/penalty will remain as part of the pension corpus of the subscriber.

Rs 1 per month for contribution upto Rs. 100 per month. Rs 2 per month for contribution upto Rs. 101 to 500 per month. Rs 5 per month for contribution between Rs 501 to 1000 per month. Rs 10 per month for contribution beyond Rs 1001 per month.

Discontinuation of payments of contribution amount shall lead to following:

After 6 months account will be frozen. After 12 months account will be deactivated. After 24 months account will be closed.

Exiting from Atal Pension Yojna

On attaining the age of 60 years: The exit from APY is permitted at the age with 100% annuitisation of pension wealth. On exit, pension would be available to the subscriber.

In case of death of subscriber pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension corpus would be returned to his nominee.

Exit Before the age of 60 Years: Exit before 60 years of age is not permitted however it is permitted only in exceptional circumstances, i.e., in the event of the death of beneficiary or terminal disease.

5) Sukanya Samridi Account

Sukanya Samriddhi Account is another welcome step from Govt of India. Honorable Prime Minister of India, Sh. Narendra Modi Ji launched Sukanya Samriddhi Account “A Small Savings Scheme” on 22nd January, 2015. It is part of “Beti Bachao – Beti Padhao” initiative of Government of India (GOI) also known as BBB.

Objective:

Sukanya Samriddhi Account, Govt is trying to give a social message that Girl Child is not a financial burden if parents of a Girl child secure their future through proper financial planning.

Benefits:

1) Highest Interest Rate among all Small Savings Schemes offered by Govt of India: Sukanya Samriddhi Account will offer interest rate of 9.1% for current financial year i.e. FY 2014-15. It is highest among all Small Savings Schemes.

2) Tax Savings: In order to encourage people to open Sukanya Samriddhi Account, Govt has exempted contribution to this account u/s 80C of the Income Tax Act, 1961.

3) Lock-in Period: The maturity of account is 21 years from the date of opening of the account or Marriage of the Girl Child, Whichever is earlier. For Marriage, Girl should be of 18 years at the time of marriage. The operation of account is not permitted beyond date of marriage.

4) Purpose of Sukanya Samriddhi Account: It is quite evident that Sukanya Samriddhi Account is launched with sole objective of financial planning for the marriage of Girl Child. Social Message is that Marriage or Education of a Girl Child is not a financial burden if parents plan well in advance.

5) Maturity Proceeds to be Paid to Girl Child: On maturity of Sukanya Samriddhi Account, the account balance along with accrued interest will be paid directly to the account holder i.e. Girl Child. It gives financial independence to Girl child which is currently missing in India.

6) Interest to be paid even after Maturity: Unlike other financial schemes where interest is not paid after maturity of the deposit / investment scheme. Unique feature of Sukanya Samriddhi Account is that even after maturity, if the account is not closed by the account holder, Interest shall be payable in the account till final closure of the account.

7) Flexibility to operate Sukanya Samriddhi Account: Based on past experience, Government of India has given lot of flexibility in terms of account operations.

(a) Account can be opened with initial deposit of Rs 1000 and thereafter any amount in multiple of Rs 100 can be deposited subject to max limit of 1.5 lakh during financial year. Every FY, a min sum of Rs 1000 should be deposited to keep account operative.

(b) On attaining age of 10 years, a girl child can operate her account.(c) Account can be closed if it is proved that account is causing undue hardship to the account holder.(d) Account can be transferred anywhere in India.

6) Kisan Vikas Patra (KVP) (Re-introduced)

INTEREST RATE - 8.7%

- The re-launched Kisan Vikas Patra (KVP) will be available to the investors in the denomination of Rs. 1000, 5000, 10,000 and 50,000, with no upper ceiling on investment.

- The certificates can be issued in single or joint names and can be transferred from one person to any other person / persons, multiple times. The facility of transfer from one post office to another anywhere in India and of nomination will be available. The certificate can also be pledged as security to avail loans from the banks and in other case where security is required to be deposited. Initially the certificates will be sold through post offices, but the same will soon be made available to the investing public through designated branches of nationalised banks.

- Kisan Vikas Patras have unique liquidity feature, where an investor can, if he so desires, en cash his certificates after the lock-in period of 2 years and 6 months and thereafter in any block of six months on pre-determined maturity value. The investment made in the certificate will double in 100 months.

- Reintroduction of Kisan Vikas Patra (KVP) is a welcome step not only in the direction of providing safe and secure investment avenues to the small investors but will also help in augmenting the savings rate in the country. The scheme will also safeguard small investors from fraudulent schemes. With a maturity period of 8 years 4 months, the collections under the scheme will be available with the Govt. for a fairly long period to be utilized in financing developmental plans of the Centre and State Governments and will also help in enhancing domestic household financial savings in the country.

d) Bonds:

A bond is a debt investment in which an investor loans money to an entity (typically corporate or governmental) which borrows the funds for a defined period of time at a variable or fixed interest rate. Bonds are used by companies, municipalities, states and sovereign governments to raise money and finance a variety of projects and activities. Owners of the bonds are debtholders, or creditors, of the issuer.

Characteristics of Bonds:

Most bonds share some common basic characteristics including:

Face value is the money amount the bond will be worth at its maturity, and is also the reference amount the bond issuer uses when calculating interest payments.

Coupon rate is the rate of interest the bond issuer will pay on the face value of the bond, expressed as a percentage.

Coupon dates are the dates on which the bond issuer will make interest payments. Typical intervals are annual or semi-annual coupon payments.

Maturity date is the date on which the bond will mature and the bond issuer will pay the bond holder the face value of the bond.

Issue price is the price at which the bond issuer originally sells the bonds.

Varieties of Bonds:

Zero-Coupon Bonds do not pay out regular coupon payments, and instead are issued at a discount and their market price eventually converges to face value upon maturity. The discount a zero-coupon bond sells for will be equivalent to the yield of a similar coupon bond.

Convertible Bonds are debt instruments with an embedded call option that allows bondholders to convert their debt into stock (equity) at some point if the share price rises to a sufficiently high level to make such a conversion attractive.

Some corporate bonds are callable, meaning that the company can call back the bonds from debtholders if interest rates drop sufficiently. These bonds typically trade at a premium to non-callable debt due to the risk of being called away and also due to their relative scarcity in today's bond market. Other bonds are putable, meaning that creditors can put the bond back to the issuer if interest rates rise sufficiently.

The majority of corporate bonds in today's market are so-called Bullet Bonds, with no embedded options whose entire face value is paid at once on the maturity date.

e) Equity Shares:

Equity is a part of a company, also known as stock or share. When you buy shares of a company, you basically own a part of that company. A company`s stockholders or shareholders all have equity in the company, or own a fractional portion of the whole company. They buy the shares because they expect to profit when the company profits. There are two basic types of shares that any company issues: equity shares and preference shares.

Both public and private corporations issue equity shares. Equity shareholders are the owners of a company and initially provide the equity capital to start the business. Equity share ownership in a public company offers many benefits to investors.

The following are some of its main advantages: Capital appreciation Dividends Voting privileges Liquidity - shares can easily be bought or sold Dividend tax credit and capital gains tax

Types of Equity Shares:

There are two types of shares under Indian Company Law:-

1) Common Share (Equity): Common share represents an ownership claim on the earnings and the assets of a company. After holders of debt claims are paid, the management of the company can either pay out the remaining earnings to stock holders in the form of dividends or reinvest part or all of the earnings. The holder of a common stock has limited liability upto the amount of share capital contributed.

2) Preference Share : Preference share means shares which fulfil the following two conditionsa. It carries preferential rights in respect of dividend payable at fixed amount or at fixed rate. This dividend

must be paid before the holders of the equity shares can be paid dividend.b. It also carries preferential right in regard to payment of capital on winding up or otherwise. It means the

amount paid on preference share must be paid back to preference share holders before anything in paid to the equity shareholders. In other words, preference share capital has priority both in payment of dividend as well as repayment of capital.

Risks in Investing in Equity

Macro-economic risks: Share prices are sensitive to the developments in the economy, such as a change in interest rates, value of currency, inflation rate, government policies, tax rates, and central bank policies. All these tend to influence the prices of equity securities. For instance, an increase in inflation rate leads to a rise in equity risk premium, which depress the equity markets. Similarly, a weakening currency dampens the equity markets.

Liquidity risks: The liquidity of a stock is a function of its trading volume. A constriction in the volume of securities could affect the fund manager's ability to transact, which in turn, could affect the fund's overall NAV. The funds that invest in small-cap or unlisted stocks are more prone to such risks. The inability to sell securities due to a lack of volumes could lead to substantial losses for the mutual fund.

Non-diversification risks: A mutual fund aims at eliminating or minimising internal, or company-specific, risks through diversification. However, at times, a particular sector or segment of capital market may acquire a sizeable proportion in the fund's total assets and expose it to the risk of non-diversification. For example, if mid-cap stocks acquire a majority stake in an equity diversified fund's corpus, the fund could be at substantial risk if the markets were to turn bearish in the near future. This is because mid-cap stocks are the first to bear the brunt when the market declines.

Corporate performance risks: Fund managers look for undervalued companies with strong fundamentals that are likely to show improved operational performance over time. However, companies may not perform as per the investors' expectations due to the increase in costs or reduced revenue. The radically changing consumer preferences can also lead to a lack of demand for a company's products and result in underperformance. This could drastically affect the NAV of a fund as the stocks of underperforming companies are hammered on the stock exchanges.

In addition to these, an equity fund that invests in overseas securities is subject to the following risks:

Currency risks: If a fund invests a proportion of its corpus in stocks, whose prices are denominated in foreign currencies, it is exposed to the risk of currency movement. The distribution of income and, correspondingly, the value of the fund are adversely affected by any changes in the value of foreign currencies relative to the Indian rupee.

Country and political risks: These are the risks associated with the deteriorating relationships between countries. Some of the possibilities include immobilisation of overseas financial assets and introduction of extraordinary exchange controls. Such risks also include a country's inability to meet its financial obligations that could adversely affect the value of the fund.

f) Mutual Funds

An investment instrument that is made up of a pool of funds collected from many investors for the purpose of investing in securities such as stocks, bonds, money market instruments and other similar assets.

Mutual funds are operated by fund managers, who invest the fund's capital and attempt to produce capital gains and income for the fund's investors. A mutual fund's portfolio is structured and maintained to match the investment objectives stated in its prospectus.

Mutual Fund is a suitable investment option for the common man as it offers an opportunity to invest in a diversified, professionally managed basket of securities at a relatively low cost.

Why do people invest in Mutual Funds?

Mutual funds offer investors an affordable way to diversify their investment portfolios. Mutual funds allow investors the opportunity to have a financial stake in many different types of investments. These investments include: stocks, bonds, money markets, real estate, commodities, etc. Individually, an investor may be able to own stock in a few companies, a few bonds, and have money in a money

market account. Participation in a mutual fund, however, allows the investor to have much greater exposure to each of these asset classes.

Most mutual funds are professionally managed by an investment expert known as a portfolio manager. This individual makes all of the buying and selling decisions for the fund. This provides investors with many options to help them achieve their investment objectives.

How does a Mutual Fund work?

Different Types of Mutual Funds?1) By StructureA) Open ended fundsB) Close ended funds2) By Investment ObjectiveA) Equity FundsB) Debt Funds

C) Balanced FundsD) Money Market Funds

Open ended funds These funds buy and sell units on a continuous basis and, hence, allow investors to enter and exit as per their

convenience. The units can be purchased and sold even after the initial offering (NFO) period (in case of new funds). The units are bought and sold at the net asset value (NAV) declared by the fund. Open ended schemes are offered for sale at a pre-specified price, say INR 10, in the initial offer period. After the

pre-specified period, say 30 days, the fund is declared open for further sales and repurchases.

Close ended funds

The unit capital of closed-ended funds is fixed and they sell a specific number of units. Unlike in open-ended funds, investors cannot buy the units of a closed-ended fund after its NFO period is over. This

means that new investors cannot enter, nor can existing investors exit till the term of the scheme ends. However, to provide a platform for investors to exit before the term, the fund houses list their closed-ended schemes on a stock exchange.

A) Equity Funds Equity or Growth Funds normally invest a majority of their corpus in equities. The aim of Growth/ Equity Funds is to provide capital appreciation over medium to long term. Types of Equity Funds1) Large Cap Funds- These are stocks of usually large and well-established companies that have a strong market

presence and are generally considered as safe investments. Their stocks are publicly traded and have large market capitalizations. One important fact about large caps is that information regarding these companies is readily available in newspapers and magazines. Most of the large cap companies have good disclosures and therefore there is no dearth of information for an investor looking into them. Ex:- Infosys, TCS, Wipro

2) Mid Cap Funds- Mid caps lie between large cap stocks and small cap stocks. These represent mid-sized companies that are relatively more risky than large cap as investment options yet, they are not considered as risky as small cap companies.

3) Small Cap Funds- Lying at the lowest end of market capitalisation, Small cap stocks are generally viewed under the misconception of being hazardous or 'quick rich' stocks. However, both these labels are untrue. Small cap companies have smaller revenue and client bases, and usually include the start-ups or companies in the early stage of development.

4) Sector Funds- A mutual fund which invests entirely or predominantly in a single sector. Sector funds tend to be riskier and more volatile than the broad market because they are less diversified, although the risk level depends on the specific sector.

B) Income/Debt Funds

Income or Debt Funds generally invest in fixed income securities (debt securities) such as bonds, corporate debentures and Government securities.

The aim of Income Funds is to provide regular and steady income to investors. Income Funds are ideal for capital stability and regular income. Capital appreciation in debt funds may be limited, though risks are typically lower than that in an equity fund.

Funds those invest only in government securities are called Gilt Funds and do not carry any credit risk.

Types of Debt Funds

1) Liquid Funds / Money Market Funds

These funds invest in highly liquid money market instruments and provide easy liquidity. The period of investment in these funds could be as short as a day. They aim to earn money market rates and could serve as an alternative to corporate and individual investors, for parking their surplus cash for short periods. Returns on these funds tend to fluctuate less when compared with other funds.

2) Ultra Short Term Funds

Earlier known as Liquid Plus Funds, they invest in very short term debt securities with a small portion in longer term debt securities. Most ultra short term funds do not invest in securities with a residual maturity of more than 1 year. Also referred to as Cash or Treasury Management Funds, Ultra Short Term Funds are preferred by investors who are willing to marginally increase their risk with an aim to earn commensurate returns. Investors who have short term surplus for a time period of approximately 1 to 9 months should consider these funds.

3) Floating Rate Funds

These funds primarily invest in floating rate debt securities, where the interest paid changes in line with the changing interest rate scenario in the debt markets. The periodic interest rate of the securities held by these products is reset with reference to a market benchmark. This makes these funds suitable for investments when interest rates in the markets are increasing.

4) Short Term & Medium Term Income Funds

These funds invest predominantly in debt securities with a maturity of upto 3 years in comparison to a Regular Income Fund. These funds tend to have a average maturity that is longer than Liquid and Ultra Short Term Funds but shorter than pure Income Funds. These funds tend to perform when short term interest rates are high and could potentially benefit from capital gains as liquidity comes back to the market and interest rates go down. These funds are suitable for conservative investors who have low to moderate risk taking appetite and an investment horizon of 9 to 12 months.

5) Income Funds, Gilt Funds and other dynamically managed debt funds

These funds comprise of investments made in a basket of debt instruments of various maturities & issuers. These funds are suitable for investors who willing to take a relatively higher risk as compared to corporate bond funds, and have longer investment horizon. These funds tend to work when entry and exit are timed properly; investors can consider entering these funds when interest rates have moved up significantly to benefit from higher accrual and when the outlook is that interest rates would decrease. As interest rates go down, investors can potentially benefit from capital gains as well. A few types of dynamically managed debt funds are mentioned below -

Income funds invest in corporate bonds, government bonds and money market instruments. However, they are highly vulnerable to the changes in interest rates and are suitable for investors who have a long term investment horizon and higher risk taking ability. Entry and exit from these funds needs to be timed appropriately. The correct time to invest in these funds is when the market view is that interest rates have touched their peak and are poised to reduce.

Gilt Funds invest in government securities of medium and long term maturities issued by central and state governments. These funds do not have the risk of default since the issuer of the instruments is the government. Net Asset Values (NAVs) of the schemes fluctuate due to change in interest rates and other economic factors.

These funds have a high degree of interest rate risk, depending on their maturity profile. The higher the maturity profiles of the instrument, higher the interest rate risk.

Dynamic Bond Funds invest in debt securities of different maturity profiles. These funds are actively managed and the portfolio varies dynamically according to the interest rate view of the fund managers. These funds Invest across all classes of debt and money market instruments with no cap or floor on maturity, duration or instrument type concentration.

6) Corporate Bond Funds

These funds invest predominantly in corporate bonds and debentures of varying maturities that offer relatively higher interest, and are exposed to higher volatility and credit risk. They seek to provide regular income and growth and are suitable for investors with a moderate risk appetite with a medium to long term investment horizon.

7) Close Ended Debt Funds

Fixed Maturity Plans (FMPs) are closed ended Debt Mutual Funds that invest in debt instruments with a specific date of maturity that is less than or equal to the maturity date of the scheme. Securities are redeemed on or before maturity and proceeds are paid to the investors.

FMPs are similar to passive debt funds, where the portfolio manager buys and holds the debt securities for the entire duration of the product. FMPs are a good option for conservative investors, as they do not carry any interest rate risk provided the investor stays invested until the maturity of the product. They are also a tax efficient investment option.

C) Balanced Funds Balanced Funds invest both in equities and fixed income securities in the proportion indicated in their offer

documents. This proportion affects the risks and the returns associated with the balanced fund - in case equities are allocated a

higher proportion, investors would be exposed to risks similar to that of the equity market. The aim of Balanced Funds is to provide both growth and regular income. These funds periodically distribute a part of their earning Balanced funds with equal allocation to equities and fixed income securities are ideal for investors looking for a

combination of income and moderate growth.

Monthly Income Plans (MIPs) strive to offer the benefit of diversification across asset classes by investing a proportion of the portfolio in debt securities (70% to 95%) with a smaller allocation in equity securities (5 % to 30 %).

As the correlation between prices of equity and debt is low, this product endeavors to give an investor returns that are relatively higher than debt market returns. MIPs can be classified as debt oriented hybrids that seek to -

Generate income from the debt securities Maximise the benefits of long term growth from equity securities Aim for periodic distribution of dividends

However, an important point to be noted is that monthly income is not assured and it is subject to the availability of distributable surplus in the fund.

Capital Protection Oriented Funds are closed ended funds that are hybrid in nature; they allocate money to debt and equity securities. The allocation to debt securities is done in such a way that at the end of the term of the

product, the value of debt investment is equal to the original investment in the fund. The equity portion aims to add to the returns of the product at maturity. These funds are oriented towards protection of capital and do not offer guaranteed returns.

Say, for example, AAA bonds are quoting at interest rate of 10% p.a. for a 5 year term.

This means that at the end of 5 years, the investment of Rs. 100 in such bonds would be worth Rs. 161.05, assuming reinvestment of the interest.

On the other hand, if one invests Rs. 62.09 in such bonds, the value of the bonds at the end of 5 years would be Rs. 100.

In such a case, the allocation between equity and debt would be 38 : 62 respectively. So, if the equity value reduces to zero, the investor gets back the original amount invested.

The asset allocation is a function of prevailing interest rates on high quality (AAA rated) bonds. It is mandatory for the fund to be rated by at least one rating agency in order to be called a capital protection oriented fund. Debt securities held in the portfolio must be of highest rating.

Multiple Yield Funds are close ended income funds that aim to optimize income from debt securities and potential growth from equity. They aim to limit the downside by investing in rated debt instruments of reputed issuers. Through a limited equity exposure, they aim to provide capital appreciation by investing in shares of companies without any sector or market capitalization bias. This exposure will help to participate in the growth of these companies thus seeking to provide the portfolio with an element of potential long term capital appreciation.

D) Money Market Funds These funds generally invest in safer short-term (less than a year) money market instruments such as Treasury

Bills, Certificates of Deposit, Commercial Paper and Inter-Bank Call Money. The aim of Money Market Funds is to provide easy liquidity, preservation of capital and moderate income. Returns on these schemes may fluctuate depending upon the interest rates prevailing in the market. Ideal for corporate and individual investors as a means to park their surplus funds for short periods. The investment portfolio is very liquid and enables investors to hold their investments for very short horizons of a

day or more.

Various Options in Mutual Funds: 1) Growth Option: Dividend is not paid-out and the investor realizes only the capital appreciation on the investment

(by an increase in NAV).2) Dividend Payout Option: Dividends are paid-out to investors. However, the NAV of the scheme falls to the extent

of dividend payout. 3) Dividend Re-investment Plan: Dividend accrued is automatically re-invested in purchasing additional units in open-

ended funds.

Different Modes in Mutual Funds

1) Lumpsum Investment: A lump sum investment means investing the entire amount at one go.

2) Systematic Investment Plan (SIP):

- SIP is a disciplined way of investing where investors invest a regular sum every month in mutual funds.- A Systematic Investment Plan or SIP is a smart and hassle free mode for investing money in mutual funds.- SIP allows you to invest a certain pre-determined amount at regular interval- weekly, monthly, quarterly etc.- SIP is a planned approach towards investments and helps you inculcate the habit of saving and building wealth for

the future.- For example: you start to invest Rs 5,000 every month in a mutual fund. If you do it via SIP, this money will be taken

from your account every month and invested in the mutual fund that you have selected for SIP.

How does it work?

A SIP is a flexible and easy investment plan. Your money is auto-debited from your bank account and invested into a specific mutual fund scheme.

You are allocated certain number of units based on the ongoing market rate (called NAV or net asset value) for the day.

Every time you invest money, additional units of the scheme are purchased at the market rate and added to your account. Hence, units are bought at different rates and investors benefit from Rupee-Cost Averaging and the Power of Compounding.

Importance of SIP:

1) Disciplined Saving - Discipline is the key to successful investments. When you invest through SIP, you commit yourself to save regularly. Every investment is a step towards attaining your financial objectives.

2) Flexibility - While it is advisable to continue SIP investments with a long-term perspective, there is no compulsion. Investors can discontinue the plan at any time. One can also increase/ decrease the amount being invested.

3) Long-Term Gains - Due to rupee-cost averaging and the power of compounding SIPs have the potential to deliver attractive returns over a long investment horizon.

4) Convenience - SIP is a hassle-free mode of investment. You can issue a standing instruction to your bank to facilitate auto-debits from your bank account.

3) Systematic Transfer Plan (STP): STP is a variant of SIP. STP is essentially transferring investment from one asset or asset type into another asset or asset type. The transfer happens gradually over a period.

Systematic Transfer Plan is of two types:-

I. Fixed STP: A fixed STP is where investors take out a fixed sum from one investment to another. II. Capital appreciation STP: A capital appreciation STP is where investors take the profit part out of one investment

and invest in the other.

4) Systematic Encashment Plan (SEP): This allows the investor the facility to withdraw a pre-determined amount / units from his fund at a pre-determined interval. The investor's units will be redeemed at the applicable NAV as on that day.

5) Systematic Withdrawal Plan (SWP): A Systematic Withdrawal Plan (SWP) is a facility that allows an investor to withdraw money from an existing mutual fund at predetermined intervals. The money withdrawn through a systematic withdrawal plan can be reinvested in another fund or retained by the investor in cash.

When is SWP generally used?Systematic withdrawal plans are used by investors to create a regular flow of income from their investments. Investors looking for income at periodical intervals for e.g. funding a travel plan during the children’s summer vacations, also set up their withdrawals in such a way that the cash is available when most required.

SWP is available in two options: Fixed Withdrawal: Where you specify amounts you wish to withdraw from your investment on a

monthly/quarterly basis. Appreciation Withdrawal: Where you can withdraw your appreciated amount on a monthly/quarterly basis.

Risk Profile of Fund Categories

1) Equity Funds: High Level of Return, but as high level of risk too2) Debt Funds: Returns comparatively less risky than equity funds3) Money Market Funds: Provide stable but low level of return

Note: Investors have to face the risk-return trade off

Investor Categories eligible to buy MF Units

• Resident Individuals• Indian Companies• Indian trusts and charitable institutions• Banks• Non-banking Financial Companies (NBFC) • Insurance companies• Provident funds• Non-resident Indians (NRI) • Overseas Corporate Bodies (OCB) • SEBI registered FII’s

Risk in MF Investments

• Market Risk: At times the prices or yields of all the securities in a particular market rise or fall due to broad outside influences affecting stock prices. This change in price is due to "market risk".

• Inflation Risk: Also referred to as "loss of purchasing power”, this risk emerges whenever the rate of inflation exceeds the earnings on investment.

• Credit Risk: This arises from the credibility and reliability of the company associated. • Interest Rate Risk: Changing interest rates affect both equities and bonds. Generally, when interest rates rise,

prices of the securities fall and vice versa.

• Investment Risks: NAV of sectoral schemes are linked to the equity performance of such companies and may be more volatile than a more diversified portfolio of equities.

• Liquidity Risk: Thinly traded securities carry the risk of not being easily saleable at or near their real values. Liquidity risk is characteristic of the Indian fixed income market.

• Changes in the Government Policy: Policy changes, especially in regard to the tax benefits may impact the business prospects of the companies leading to an impact on the investments made by the fund.

Net Assets of Mutual Funds

The net assets represent the market value of assets which belong to the investors, on a given date. Net Assets = Market Value of Investments + Current Assets and Other Assets + Accrued Income - Current

Liabilities and Other Liabilities - Accrued Expenses

Net Asset Value Net Asset Value (NAV) is the market value of the assets of the scheme minus its liabilities. The per unit NAV is the net asset value of the scheme divided by the number of units outstanding on the Valuation

Date. Typically, NAV is calculated by summing the current market values of all securities held by the fund, adding in cash

and any accrued income, then subtracting liabilities and dividing the result by the number of units outstanding.Example:-

Total Value of Securities(Equity, Bonds, Debentures etc.)

INR 1,000

Cash INR 1,500Liabilities INR 500

Total outstanding units 100NAV = [(1000+1500-500)/100] INR 20 per unit

Risk and Return Measures of Mutual Fund Schemes: Sharpe Ratio: It is used to measure the risk-adjusted performance of a portfolio. The Sharpe ratio is calculated by

subtracting the risk-free rate from the rate of return for a portfolio and dividing the result by the standard deviation of the portfolio returns. The Sharpe ratio tells us whether a portfolio's returns are due to smart investment decisions or a result of excess risk. The greater a portfolio's Sharpe ratio, the better its risk-adjusted performance has been. A negative Sharpe ratio indicates that a risk-less asset would perform better than the security being analyzed.

Alpha: A measure of performance on a risk-adjusted basis. Alpha takes the volatility (price risk) of a mutual fund and compares its risk-adjusted performance to a benchmark index. The excess return of the fund relative to the return of the benchmark index is a fund's alpha. A positive alpha of 1.0 means the fund has outperformed its benchmark index by 1%. Correspondingly, a similar negative alpha would indicate an underperformance of 1%.

Beta: A measure of the volatility, or systematic risk, of a security or a portfolio in comparison to the market as a whole. A beta of 1 indicates that the security's price will move with the market. A beta of less than 1 means that the security will be less volatile than the market. A beta of greater than 1 indicates that the security's price will be more volatile than the market.

Tax Reckoner 2015-16The rates are applicable for the financial year 2015-16.

Tax Implications on Dividend received by Unit holders from a Mutual Fund

Individual/ HUF Domestic Company NRI

DividendAll schemes Tax Free

Tax on distributed income (payable by the scheme) rates**Equity oriented Nil Nil Nilschemes*Infrastructure Debt 25% + 12% Surcharge + 3% Cess 30% + 12% Surcharge + 3% Cess 5% + 12% Surcharge + 3% CessFund (‘IDF’)

= 28.84% = 34.608% = 5.768%

Other than equity 25% + 12% Surcharge + 3% Cess 30% + 12% Surcharge + 3% Cess 25% + 12% Surcharge + 3% Cessoriented schemes andIDF

= 28.84% = 34.608% = 28.84%

* Securities transaction tax (STT) will be deducted on equity oriented scheme at the time of redemption/ switch to the other schemes/ sale of units. Mutual Fund

would also pay securities transaction tax wherever applicable on the securities sold.

* For the purpose of determining the tax payable, the amount of distributed income be increased to such amount as would, after reduction of tax from such

increased amount, be equal to the income distributed by the Mutual Fund. The impact of the same has not been reflected above.

Capital Gains TaxationIndividual/ HUF $ Domestic Company @ NRI $/ #

Long Term Capital GainsEquity oriented Units held for more than 12 monthsschemes

Nil Nil Nil

Otherthan equity Units held for more than 36 monthsoriented schemesListed 20% with indexation + 12% 20% with indexation + Surcharge as 20% with indexation + 12%

Surcharge + 3% Cess applicable + 3% Cess Surcharge + 3% Cess

= 23.072% = 22.042% or 23.072% = 23.072%Unlisted 20% with indexation + 12% 20% with indexation + Surcharge as 10% without indexation + 12%

Surcharge + 3% Cess applicable + 3% Cess Surcharge + 3% Cess

= 23.072% = 22.042% or 23.072% = 11.536%

Short Term Capital GainsEquity oriented schemes Units held for 12 months or less

15% + Surcharge as applicable + 3%15%+ 12% Surcharge + 3% Cess Cess 15% + 12% Surcharge + 3% Cess

= 17.304% = 17.304% or 16.5315% = 17.304%Other than equity oriented Units held for 36 months or lessschemes

30% + Surcharge as applicable + 3%30%^ + 12% Surcharge + 3% Cess Cess 30%^+ 12% Surcharge + 3% Cess

= 34.608% = 34.608% or 33.063% =34.608%

Tax Deducted at Source (Applicable only to NRI Investors)

Short term capital gains Long term capital gainsEquity oriented schemes 17.304% Nil

Other than equity oriented schemes (Listed) 34.608%^ 23.072%

Other than equity oriented schemes (Unlisted) 34.608%^ 11.536%

$ - Surcharge at the rate of 12% is levied in case of individual/ HUF unit holders where their income exceeds Rs 1 crore.

@ - Surcharge at the rate of 7% is levied for domestic corporate unit holders where the income exceeds Rs 1 crore but less than Rs 10 crores and at the rate of 12% where income exceeds Rs 10 crores.

# - Short term/ long term capital gain tax will be deducted at the time of redemption of units in case of NRI investors only.

^ - Assuming the investor falls into highest tax bracket.

Education Cess at the rate 3% will continue to apply on tax plus surcharge

The Finance Act, 2015 provides tax exemption to unit holders upon consolidation or merger of mutual fund schemes, provided consolidation is of two or more schemes of equity oriented fund or two or more schemes of a fund other than equity oriented fund.

Dividend Stripping: The loss due to sale of units in the schemes (where dividend is tax free) will not be available for setoff to the extent of the tax free dividend declared; if units are:(A) bought within three months prior to the record date fixed for dividend declaration; and (B) sold within nine months after the record date fixed for dividend declaration.

Bonus Stripping: The loss due to sale of original units in the schemes, where bonus units are issued, will not be available for set off; if original units are: (A) bought within three months prior to the record date fixed for allotment of bonus units; and (B) sold within nine months after the record date fixed for allotment of bonus units. However, the amount of loss so ignored shall be deemed to be the cost of purchase or acquisition of such unsold bonus units.

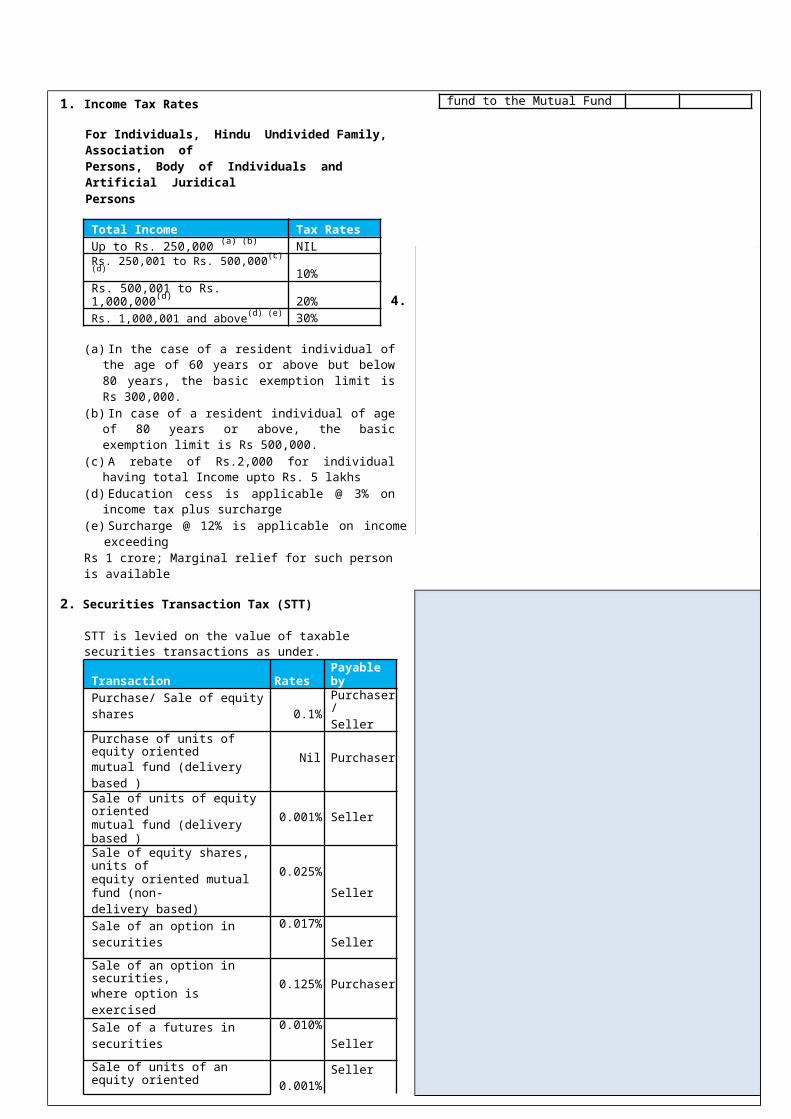

1. Income Tax Rates

For Individuals, Hindu Undivided Family, Association ofPersons, Body of Individuals and Artificial JuridicalPersons

Total Income Tax RatesUp to Rs. 250,000 (a) (b) NILRs. 250,001 to Rs. 500,000(c) (d) 10%

4.Rs. 500,001 to Rs. 1,000,000(d) 20%Rs. 1,000,001 and above(d) (e) 30%

(a) In the case of a resident individual of the age of 60 years or above but below 80 years, the basic exemption limit is Rs 300,000.

(b) In case of a resident individual of age of 80 years or above, the basic exemption limit is Rs 500,000.

(c) A rebate of Rs.2,000 for individual having total Income upto Rs. 5 lakhs

(d) Education cess is applicable @ 3% on income tax plus surcharge

(e) Surcharge @ 12% is applicable on income exceeding Rs 1 crore; Marginal relief for such person is available

2. Securities Transaction Tax (STT)

STT is levied on the value of taxable securities transactions as under.

Transaction Rates Payable by

Purchase/ Sale of equity shares 0.1%Purchaser/Seller

Purchase of units of equity orientedNil Purchaser

mutual fund (delivery based )Sale of units of equity oriented

0.001% Sellermutual fund (delivery based )Sale of equity shares, units of

0.025%equity oriented mutual fund (non- Sellerdelivery based)

Sale of an option in securities0.017%

Seller

Sale of an option in securities,0.125% Purchaser

where option is exercised

Sale of a futures in securities0.010%

Seller

Sale of units of an equity oriented0.001% Seller

fund to the Mutual Fund

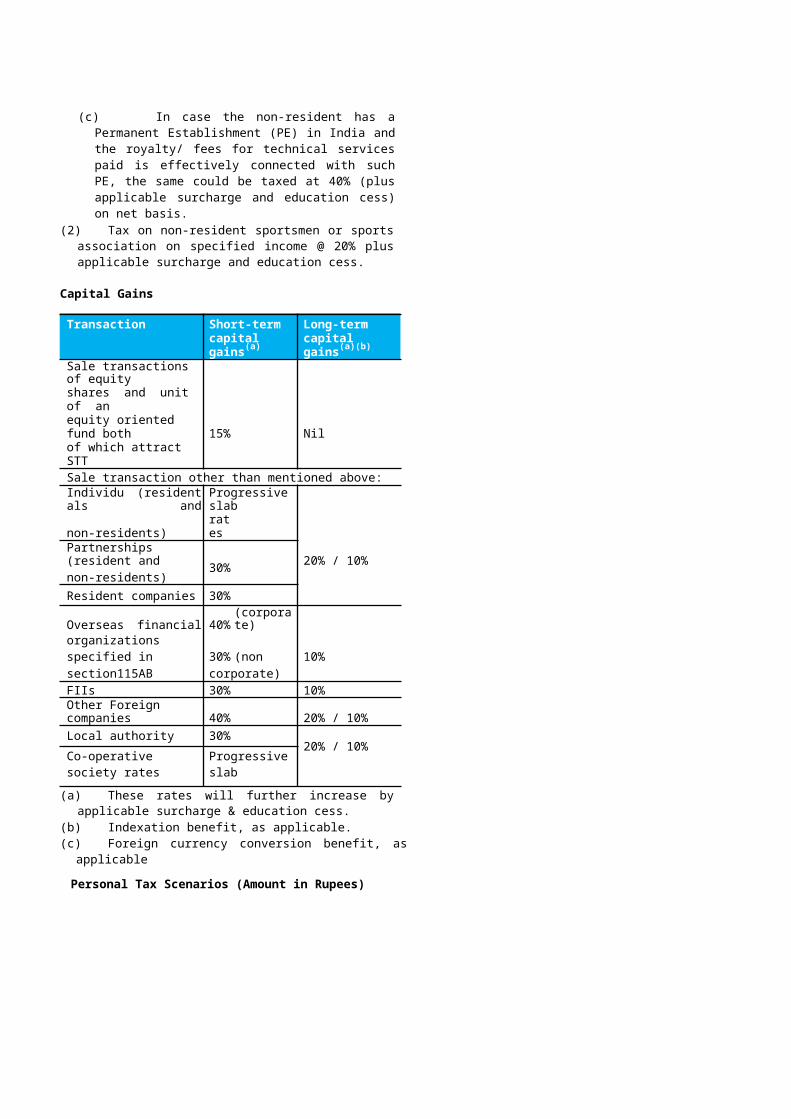

(c) In case the non-resident has a Permanent Establishment (PE) in India and the royalty/ fees for technical services paid is effectively connected with such PE, the same could be taxed at 40% (plus applicable surcharge and education cess) on net basis.

(2) Tax on non-resident sportsmen or sports association on specified income @ 20% plus applicable surcharge and education cess.

Capital Gains

Transaction Short-term Long-termcapital gains(a) capital gains(a)(b)

Sale transactions of equityshares and unit of anequity oriented fund both 15% Nilof which attract STTSale transaction other than mentioned above:Individuals (resident and Progressive slabnon-residents) ratesPartnerships (resident and 30% 20% / 10%non-residents)Resident companies 30%Overseas financial 40% (corporate)organizations specified in 30% (non 10%section115AB corporate)FIIs 30% 10%Other Foreign companies 40% 20% / 10%Local authority 30%

20% / 10%Co-operative society rates Progressive slab

(a) These rates will further increase by applicable surcharge & education cess.

(b) Indexation benefit, as applicable. (c) Foreign currency conversion benefit, as applicable

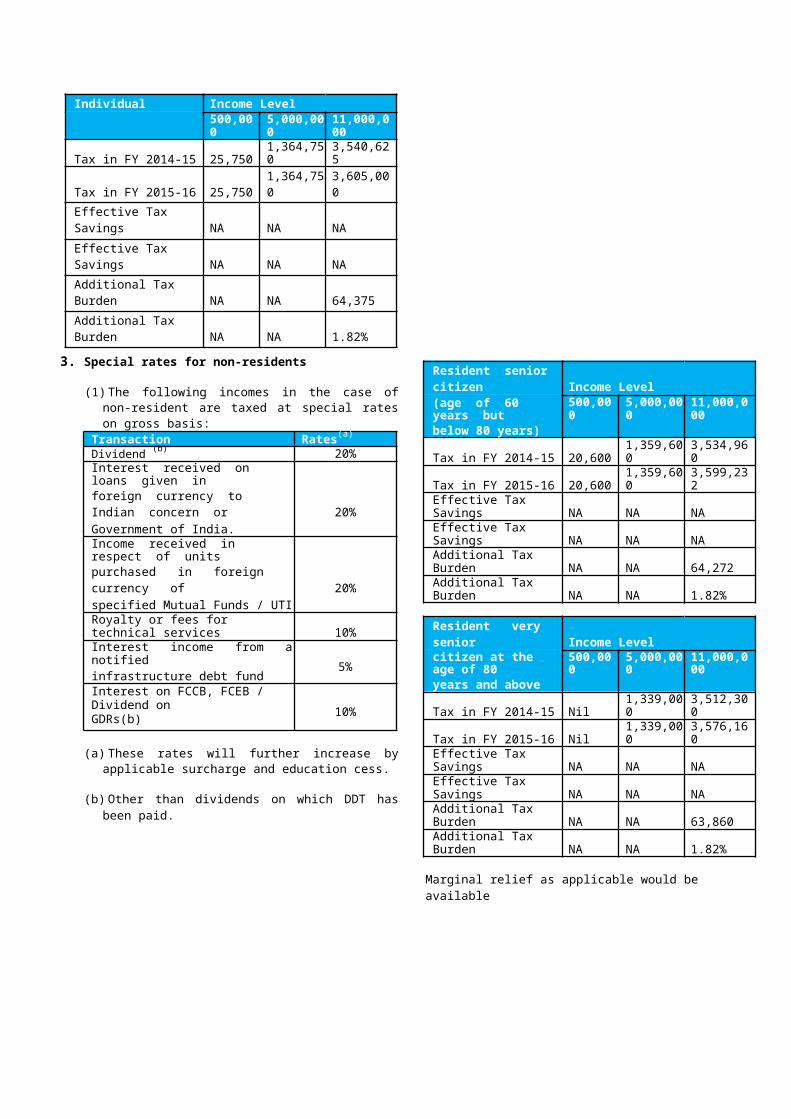

Personal Tax Scenarios (Amount in Rupees)

Individual Income Level500,000 5,000,000 11,000,000

Tax in FY 2014-15 25,750 1,364,750 3,540,625Tax in FY 2015-16 25,750 1,364,750 3,605,000

Effective Tax Savings NA NA NA

Effective Tax Savings NA NA NA

Additional Tax Burden NA NA 64,375

Additional Tax Burden NA NA 1.82%

3. Special rates for non-residents

(1) The following incomes in the case of non-resident are taxed at special rates on gross basis:

Transaction Rates(a)

Dividend (b) 20%Interest received on loans given inforeign currency to Indian concern or 20%Government of India.Income received in respect of unitspurchased in foreign currency of 20%specified Mutual Funds / UTIRoyalty or fees for technical services 10%Interest income from a notified

5%infrastructure debt fundInterest on FCCB, FCEB / Dividend on

10%GDRs(b)

(a) These rates will further increase by applicable surcharge and education cess.

(b) Other than dividends on which DDT has been paid.

Resident senior citizen Income Level(age of 60 years but 500,000 5,000,000 11,000,000below 80 years)Tax in FY 2014-15 20,600 1,359,600 3,534,960Tax in FY 2015-16 20,600 1,359,600 3,599,232Effective Tax Savings NA NA NAEffective Tax Savings NA NA NAAdditional Tax Burden NA NA 64,272Additional Tax Burden NA NA 1.82%

Resident very senior Income Levelcitizen at the age of 80 500,000 5,000,000 11,000,000years and aboveTax in FY 2014-15 Nil 1,339,000 3,512,300Tax in FY 2015-16 Nil 1,339,000 3,576,160Effective Tax Savings NA NA NAEffective Tax Savings NA NA NAAdditional Tax Burden NA NA 63,860Additional Tax Burden NA NA 1.82%

Marginal relief as applicable would be available

NOTES:

1) The tax rates mentioned above are those provided in the Income tax Act, 1961 and amended as per Finance Act, 2015, applicable for the financial year 2015-16 relevant to assessment year 2016-17. In the event of any change, we do not assume any responsibility to update the tax rates consequent to such changes. The tax rates mentioned above may not be exhaustive rates applicable to all types of assesses /taxpayers.

2) The tax rates mentioned above are only intended to provide general information and are neither designed nor intended to be a substitute for professional tax advice. Applicability of the tax rates would depend upon nature of the transaction, the tax consequences thereon and the tax laws in force at the relevant point in time. Therefore, users are advised that before making any decision or taking any action that might affect their finances or business, they should take professional advice.

3) A non-resident tax payer has an option to be governed by the provisions of the Income tax Act, 1961 or the provisions of the relevant DTAA, whichever is more beneficial. As per the provisions of the Income tax Act, 1961, submission of tax residency certificate (“TRC”) along with From No. 10F will be necessary for granting DTAA benefits to non-residents. A taxpayer claiming DTAA benefit shall furnish a TRC of his residence obtained by him from the Government of that country or specified territory. Further, in addition to the TRC, the non-resident may be required to provide such other documents and information subsequently, as may be prescribed by the Indian Tax Authorities.

Insurance

i. Life Insurance Life Insurance is the key to good financial planning. On one hand, it safeguards your money and on the

other, ensures its growth, thus providing you with complete financial well being. Insurance is the transfer of risk by an individual, such as yourself, or an organisation, such as your

business, to the insurance company. You or your organisation will thus be known as the policy owner. The insurance company receives payment in the form of premium and will compensate you in the event of insured individual's or individuals' death or other event, such as terminal illness, critical illness or maturity of the policy.

Types of Life Insurance

1) Term Plan: Term Insurance helps the customers in safeguarding their families from financial worries that arise due

to unfortunate circumstances. Term plans are pure risk cover plans with or without maturity benefits. These pure risk plans cover your