an iintegrated marketing approach for a meinium …

TRANSCRIPT

AN IINTEGRATED MARKETING APPROACH

FOR A MEINIUM-SIIZEI)

S UTH AFRICAN AMILIN

IIN A ER GULATEID MARKET

N. LOUW MAY 1996

AN INTEGRATED MARKETING APPROACH FOR A MEDIUM-SIZED

SOUTH AFRICAN AIRLINE IN A DEREGULATED MARKET

by

NICOLAAS SALOMON LOUW

A dissertation submitted

in fulfilment of the requirements for the degree of

MAGISTER COMMERCII

in

MARKETING MANAGEMENT

of the

FACULTY ECONOMIC AND MANAGEMENT SCIENCES

at the

RAND AFRIKAANS UNIVERSITY

SUPERVISOR: PROF. J.A. BENNETT

MAY 1996

ACKNOWLEDGEMENTS

I would like to express my sincere appreciation and gratitude to the following persons and

organisations which contributed to this study:

Prof. J. A. Bennett, for his assistance and constructive criticism.

Comair, for granting me this study opportunity - may the next 50 years be

as successful as the previous.

Mary Smith, for proof-reading the dissertation.

My father, for his valued comments and assistance.

(i)

TABLE OF CONTENTS

LIST OF TABLES

LIST OF FIGURES

GOAL AND OBJECTIVES OF STUDY 1

1.1 INTRODUCTION

1.2 THE RESEARCH PROBLEM 4

1.3 GOAL AND OBJECTIVES 4

1.4 RESEARCH METHODOLOGY 5

1.5 DIVISION OF CHAPTERS 6

THE MACRO AND MARKET FORCES AFFECTING AIRLINES

IN SOUTH AFRICA 10

2.1 INTRODUCTION 10

2.2 THE MACRO ENVIRONMENT 12

2.2.1 The economic environment 13

2.2.1.1 The South African economy in a world and regional context 14

2.2.1.2 Economic indicators 17

2.2.1.2.1 Economic growth 17

2.2.1.2.2 Inflation 18

2.2.1.2.3 International capital flows 19

2.2.1.2.4 The exchange rate 19

2.2.1.2.5 Economic policy issues 20

2.2.1.3 Tourism and air travel 21

(ii)

2.2.2 The social environment 23

2.2.2.1 Demographics 24

2.2.2.2 Socio-cultural aspects 28

2.2.2.2.1 The changing role of women 28

2.2.2.2.2 The increasing importance of leisure 29

2.2.2.2.3 The rise of singles 29

2.2.2.2.4 Changing sexual attitudes 30

2.2.2.2.5 A growing interest in health consciousness 3 I

2.2.3 The physical environment 31

2.2.4 The international environment 33

2.2. 5 The institutional environment 34

2.2.6 The technological environment 41

2.3 THE MARKET ENVIRONMENT 47

2.3.1 The South African air travel industry 48

2.3.1.1 The South African air travel industry in a world context 48

2.3.1.2 The South African air travel industry in a regional context 51

2.3.1.3 The domestic South African air travel market 52

2.3.2 Comair - a medium-sized South African airline 55

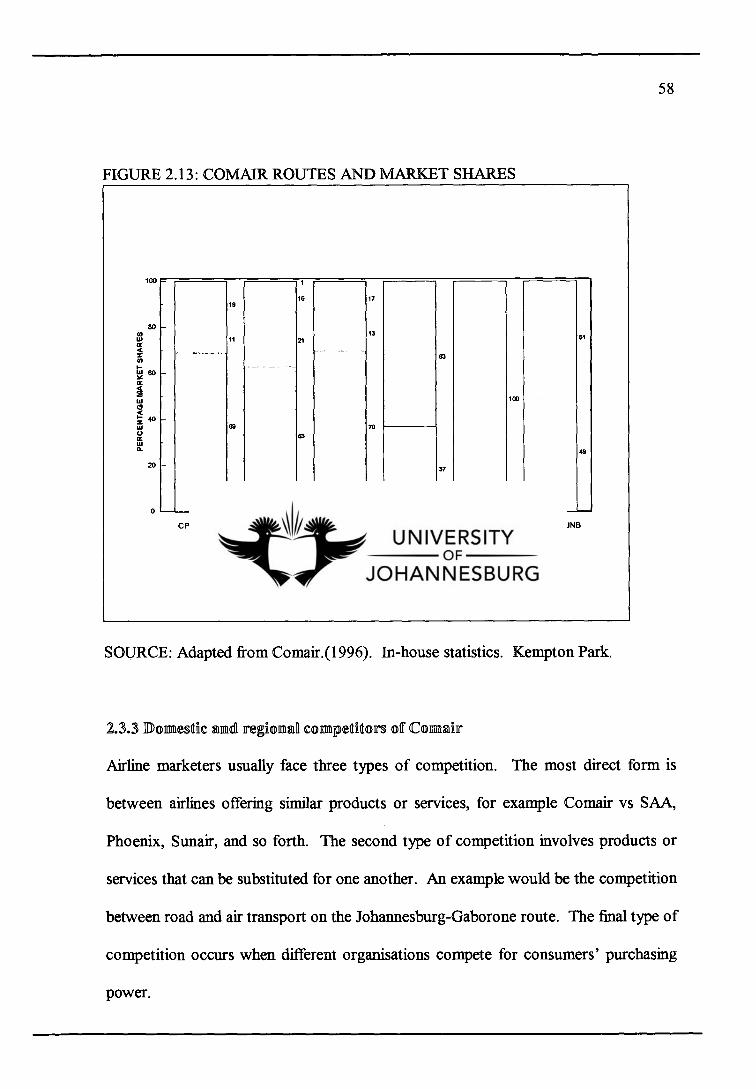

2.3.3 Domestic and regional competitors of Comair 58

2.3.3.1 Air Botswana (BP) 59

2.3.3.2 Air Namibia (SW) 60

2.3.3.3 Air Zimbabwe (UM) 60

2.3.3.4 Nationwide (CE) 61

2.3.3.5 Royal Swazi National Airways (ZC) 61

(iii)

2.3.3.6 SA Express (SAX) 62

2.3.3.7 South African Airways (SA) 62

2.3.3.8 Sunair (BV) 66

2.3.3.9 Zimbabwe Express (Z9) 67

2.4 SUMMARY 67

3. MARKET SEGMENTATION, MARKET TARGETING, MARKET

POSITIONING AND THE DEVELOPMENT OF A MISSION

STATEMENT 72

3.1 INTRODUCTION 72

3.2 MARKET SEGMENTATION 74

3.2.1 Advantages and disadvantages of market segmentation 75

3.2.2 Criteria for effective market segmentation 76

3.2.3 Segmentation of the domestic South African air travel market 77

3.2.3.1 Market segmentation sources for the domestic South African

air travel market 78

3.2.3.2 Segmentation based on purpose of trip 79

3.2.3.3 Segmentation based on demographic, geographic, and

economic characteristics 80

3.2.3.3.1 Demographic segmentation 81

Ethnic group 83

Gender 84

Age 84

Marital status 84

(iv)

(v) Home language 84

3.2.3.3.2 Geographic segmentation 85

Provincial distribution of the domestic South African

flyer 85

City distribution of the domestic South African flyer 86

3.2.3.3.3 Economic segmentation 88

Income 88

Lifestyle measurement (LSM) of the South African

flyer 90

3.2.3.4 Segmentation based on airline user status 92

3.2.3.5 Segmentation based on buyer needs and benefits sought 95

3.2.3.6 Segmentation based on psychographic characteristics and lifestyle 95

3.2.3.6.1 Responsibles

97

Characterising trends

97

Marketing implications

98

3.2.3.6.2 Brandeds

98

Characterising trends

99

Marketing implications

99

3.2.3.6.3 Innovatives

100

Characterising trends

100

Marketing implications

101

3.2.3.6.4 Self-motivateds

101

Characterising trends

101

Marketing implications

102

(v)

3.2.3.6. 5 Segmenting the South African air travel market

according to the 1992 White Sociomonitor 103

3.2.3.7 Segmentation based on price variables 104

3.3 MARKET TARGETING 105

3.3.1 Evaluating market segments 106

3.3.1.1 Segment size and growth 106

3.3.1.2 Segment structural attractiveness l07

3.3.1.3 Airline objectives and resources 107

3.3.2 Selecting market segments 108

3.4 MARKET POSITIONING 110

3.4.1 The importance of market positioning 111

3.4.2 Development of a positioning strategy 112

3.4.3 Anticipating competitive response 114

3.5 DEVELOPING A MISSION STATEMENT 115

3.6 SUMMARY 116

4. THE ROLE OF THE MARKETING MIX (PRODUCT AND DISTRIBUTION)

AS A COMPONENT OF AN INTEGRATED MARKETING APPROACH 120

4.1 INTRODUCTION 120

4.2 THE AIRLINE PRODUCT AS A COMPONENT OF THE MARKETING

MIX 123

4.2.1 Characteristics of the airline product 125

4.2.2 Developing a competitive airline product 128

4.2.2.1 The airline product and customer value 129

(vi)

4.2.2.2 The airline product and customer satisfaction 130

4.2.2.3 The airline product and quality 132

4.2.3 The airline product and branding 135

4.2.3.1 Brands as part of the booking process 136

4.2.3.2 The usage of differentiators in brand-building 138

4.2 . 4 Loyalty programmes as a component of the airline product 139

4.2.5 Future airline product trends 140

4.3 DISTRIBUTION AS A COMPONENT OF THE MARKETING MIX 142

4.3.1 Distribution channels in the air travel industry 143

4.3.2 The role of travel agencies in the airline distribution channel 145

4.3.3 The role of central reservations systems (CRSs) in the airline

distribution channel 148

4.3.4 New trends in the airline distribution channel 153

4.3.4. l Electronic ticketing and self-service ticketing machines 153

4.3.4.2 The changing role of travel agencies 157

4.3.4.3 The changing role of CRSs 157

4.3.4.4 The changing role of passengers 158

4.3.5 Direct marketing and the airline distribution channel 160

4.3.5.1 Major tools of direct marketing 160

4.3.5.2 Advantages of direct marketing 161

4.3.5.3 The development of integrated direct marketing 162

4.3.5.4 Developing a database marketing system 162

4.3.5.5 Major decisions in direct marketing 164

4.4 SUMMARY 165

(vii)

5. THE ROLE OF THE MARKETING MIX (PRICE AND PROMOTION)

AS A COMPONENT OF AN INTEGRATED MARKETING APPROACH 169

5.1 INTRODUCTION 169

5.2 PRICE AS A COMPONENT OF THE MARKETING MIX 169

5.2.1 Airline fare structures 171

5.2.2 Air travel pricing and demand 172

5.2.3 Airline costs and pricing 174

5.2.4 Airline productivity and pricing 175

5.2.5 The pricing process 176

5.2.5.1 Influences on the pricing of airline products 176

5.2.5.2 Pricing objectives 178

5.2.5.3 Pricing strategies 178

5.2.6 Air travel pricing and yield management 180

5.3 PROMOTION AS A COMPONENT OF THE MARKETING MIX 181

5.3.1 Advertising 182

5.3.1.1 Setting advertising objectives 183

5.3.1.2 Deciding on the advertising budget 184

5.3.1.3 Deciding on the advertising message 186

5.3.1.3.1 Message generation 186

5.3.1.3.2 Message evaluation and selection 189

5.3.1.3.3 Message execution 189

5.3.1.4 Deciding on media 190

5.3.1.4.1 Deciding on reach, frequency, and impact 190

5.3.1.4.2 Choosing amongst media types 191

(viii)

5.3.1.4.3 Selecting specific media vehicles 193

5.3.1.4.4 Deciding on media timing 194

5.3.1.4.5 Deciding on geographical media allocation 194

5.3.1.5 Evaluating advertising effectiveness 195

5.3.2 Public relations (PR) 196

5.3.2.1 Advantages and disadvantages of PR 196

5.3.2.2 Developing a PR plan 197

5.3.2.3 Implementing a PR programme 199

5.3.2.4 Measuring the effectiveness of PR 199

5.3.3 Sales promotion 200

5.3.3.1 The purpose of sales promotion 200

5.3.3.2 Sales promotion techniques used in air travel 201

5.3.3.3 Developing a sales promotion programme 202

5.3.3.3.1 Establishing sales promotion objectives 202

5.3.3.3.2 Selecting sales promotion tools 203

5.3.3.3.3 Planning a sales promotion programme 205

5.3.3.3.4 Implementing and controlling the sales promotion

programme 206

5.3.3.4 Evaluating sales promotion 207

5.3.4 Personal selling 207

5.3.4.1 Advantages and disadvantages of personal selling 208

5.3.4.2 Sales force objectives 209

5.3.4.3 Sales force size 209

5.3.4.4 Managing the sales force 210

(ix)

5.3.4.4.1 Recruiting and selecting sales representatives 210

5.3.4.4.2 Training sales representatives 211

5.3.4.4.3 Directing sales representatives 212

5.3.4.4.4 Motivating sales representatives 213

5.3.4.5 Evaluating sales representatives 214

5.4 SUMMARY 215

6. PRESENTATION OF FINDINGS OF EMPIRICAL RESEARCH 219

6.1 BACKGROUND 219

6.2 RESEARCH GOAL 220

6.3 RESEARCH METHODOLOGY 221

6.4 QUALITATIVE RESEARCH 224

6.4.1 Qualitative research objectives 224

6.4.2 Defining the qualitative research universe 224

6.4.3 Qualitative research findings 225

6.4.3.1 Decision-makers and influencers in choice of airline 225

6.4.3.2 Importance of airline attributes 226

6.4.3.3 Positioning of domestic airlines 229

6.4.3.4 Frequent flyer packages 230

6.4.3.5 Travel agents: Suggestions for improved service from airlines 231

6.5 QUANTITATIVE RESEARCH 232

6.5.1 Quantitative research objectives 233

6.5.2 Defining the quantitative research universe 233

6.5.3 Quantitative research findings 233

(x)

6.5.3.1 Profile of participants 234

6.5.3.2 Importance of airline attributes 237

6.5.3.3 Positioning of domestic airlines 239

6.5.3.4 Awareness and usage of domestic airlines 246

6.5.3.5 The role of price 250

6.5.3.6 Frequent flyer packages 252

6.6 SUMMARY 255

7. SUMMARY, CONCLUSIONS, AND RECOMMENDATIONS 261

7.1 INTRODUCTION 261

7.2 OVERVIEW OF STUDY 261

7.3 A SWOT ANALYSIS OF COMAIR 275

7.4 CONCLUSIONS AND RECOMMENDATIONS 277

7.4.1 The development of a customer-oriented approach 277

7.4.1.1 The role of Comair management 278

7.4.1.2 The role of Comair staff 280

7.4.1.3 Increased awareness of traveller needs 282

7.4.2 The development of a differentiated Comair product 283

7.4.3 The development of a coordinated market and communication strategy 285

LIST OF REFERENCES

APPENDIX

A: Quantitative research questionnaire

LIST OF TABLES

3.1 Demographic data of domestic South African flyers 82

4.1 The top four international computer reservations systems (CRSs) in

North America and Europe in 1992 148

5.1 Advertising media alternatives 191

5.2 Four difficulties facing sales managers 213

6.1 Participants according to organisation size 222

6.2 Participants according to region of origin 222

6.3 Participants according to airline used during previous 12 months 222

6.4 Demographic data of quantitative research participants 234

6.5 Frequency of travel, all participants versus Comair travellers 236

6.6 Area of residence and organisation size, all participants versus

Comair travellers 236

6.7 Importance of airline attributes 238

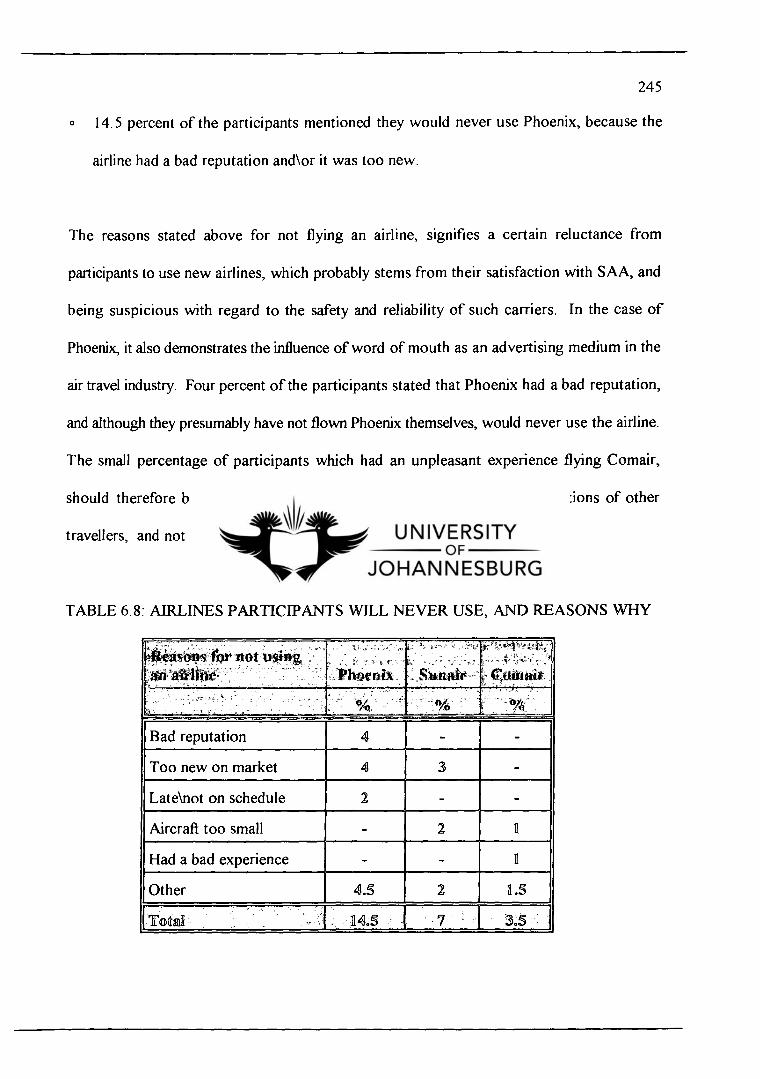

6.8 Airlines participants will never use, and reasons why 245

6.9 Awareness of domestic airlines 246

6.10 Usage of airlines 247

6.11 Number of airlines used by participants 248

6.12 Usual airline of Comair travellers 249

6.13 Awareness of price according to airline flown (Comair versus

non-Comair travellers) 250

6.14 Awareness of Johannesburg-Cape Town return fare 251

6.15 Loyalty created by SAA's Voyager programme 253

6.16 Awareness of frequent flyer programmes 253

6.17 Importance of frequent flyer incentives

255

7.1 An internal and external SWOT analysis of Comair (from a marketing

perspective)

276

LIST OF FIGURES

2.1 The external environment of an airline 12

2.2 GNP per capita, South Africa and other countries 15

2.3 Projection of overseas visitors 1990-1999 23

2.4 Human Development Index, worldwide (1994) 27

2.5 Racial composition of South Africa, SAA, and Comair 39

2.6 Primary cause factors of accidents 45

2.7 World shares of aviation 49

2.8 Air travel maturity per trip 50

2.9 The African air travel market 51

2.10 Share of capacity - domestic airlines January 1996 53

2.11 Domestic air routes - January 1996 54

2.12 Percentage business generated by Comair's routes 57

2.13 Comair routes and market shares 58

3.1 Steps in market segmentation, targeting, and positioning 73

3.2 Provincial distribution of domestic South African flyers 86

3.3 City distribution of domestic South African flyers 87

3.4 Income grouping of domestic South African flyers 89

3.5 Frequency of travel amongst domestic South African flyers 94

3.6 Psychographic segmentation of the domestic South African market 103

3.7 Five forces determining segment structural attractiveness 108

4.1 The marketing mix in context of the marketing system 121

4.2 The different levels of the airline product 124

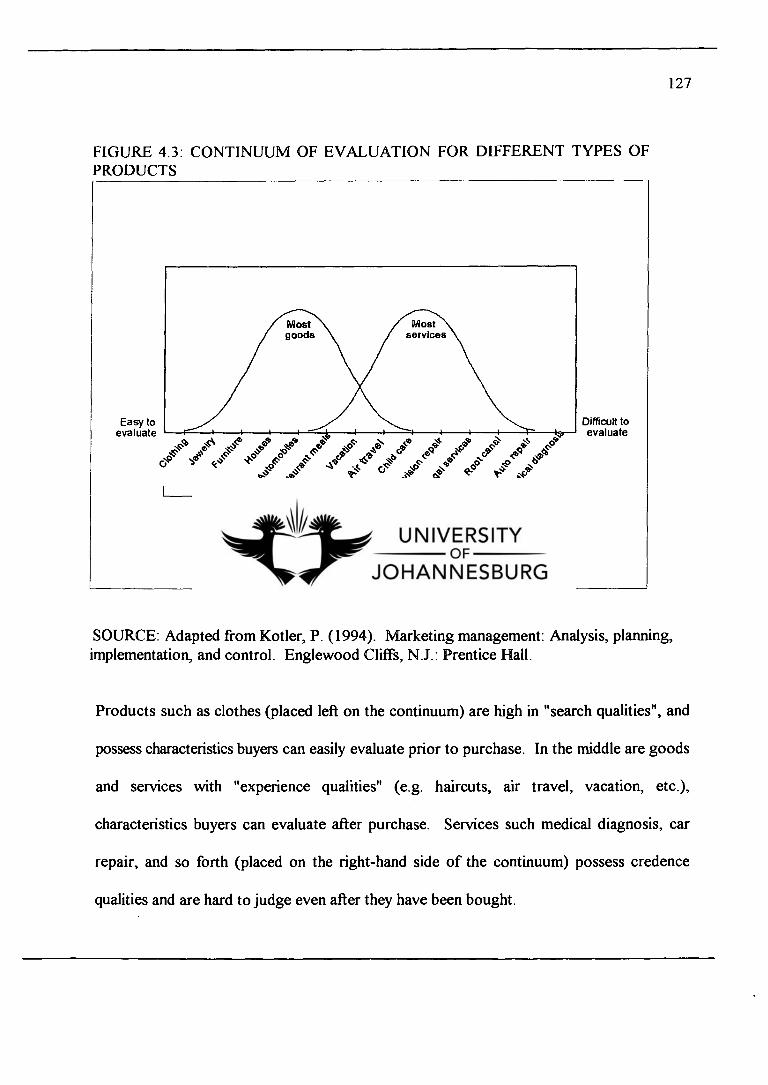

4.3 Continuum of evaluation for different types of products 127

4.4 The five distribution channels of the airline product 143

5.1 The pricing tripod 170

5.2 Forces of and barriers to communication 188

5.3 Sales promotion techniques used in air travel 204

6.1 Average market shares on domestic jet routes (1\1995-6\1995) 223

6.2 Attribute associated with airlines 241

6.3 Domestic airlines in relation to weighted airline attributes 242

6.4 Personification of domestic airlines 244

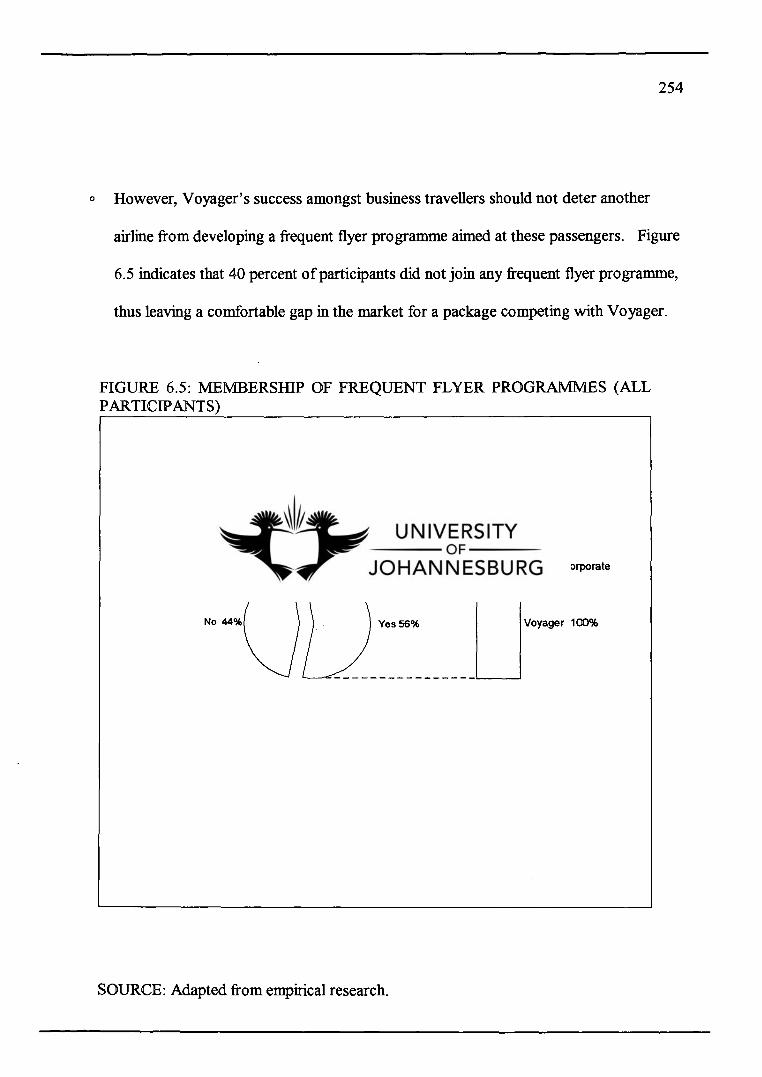

6.5 Membership of frequent flyer programmes 254

7.1 The current and proposed role of marketing in Comair 279

GOAL AND OBJECTIIVES OF STUDY

1.1 11NTRODUCT11ON

The deregulation of the American air transport industry in 1978 created a turning point

for air travel worldwide. As a growing number of governments endorsed the policy of

deregulation, national airlines in those countries now had to face competition, and could

no longer rely on protective legislation to ensure their survival (Meyer, Oster, and

Clippinger 1984:3). A major effect of deregulation was the sudden importance passengers

gained. Travellers in countries with a deregulated air travel industry now often had an

option of two or more airlines serving destinations they wished to travel to, and airlines

in such an environment were forced to find innovative ways of persuading travellers to use

their services, instead of competitors (Shaw, 1990:2).

The importance of marketing in ensuring an airline's survival thus grew, as successful

airlines realized that they should ideally design airline products around the needs and

expectations of travellers; that easy access to the airline product needs to be provided;

that the airline product should represent value for money; and that the benefits offered by

a specific airline has to be communicated to the market. Deregulated air travel markets

were, as a result, quickly propelled into a stage where airline brands; differentiated

products; and passenger loyalty; became important survival tools (Rapp and Collins,

1990:218). However, these variables relate more to the external perceptions of an airline

product and many airlines had to change internal aspects of their operations, to facilitate

the perceptional changes they desired in their market environments.

Deregulation thus required successful airlines to review both market perceptions of their

products, and internal organisational components supporting these views, through

developing a fully "integrated" marketing approach that could assist them in surviving the

volatile dynamics of a competitive environment.

The domestic South African air travel market, partly as a result of the impetus created by

the American deregulation experience, was deregulated in 1991, followed shortly by the

deregulation of the international South African air travel market. Marked differences exist

between the South African and American air travel markets. Apart from an obvious

difference in size (the South African air travel market represents a mere 1 percent the size

of the American market - UN Civil Aviation statistics, 1992), only one government-

owned carrier, South African Airways (SAA), had been allowed to operate on major

domestic and all international routes for more than 60 years. The result is that five years

after deregulation, SAA still dominates the domestic air travel market as well as virtually

all international routes, and it is questionable whether deregulation has succeeded in

creating a really free and competitive air travel environment. Of the six airlines (serving

major domestic routes) that entered the domestic air transport market after deregulation,

two privately-owned airlines (Flitestar - April 1994, and Phoenix - September 1995) had

to close down, the demise of Flitestar (accusing SAA of anti-competitive behaviour)

probably being a more serious blow to the goals of deregulation. Flitestar was the only

new entrant that challenged SAA's supremacy head-on. The remaining four airlines, SA

Express, Sunair, Nationwide, and Comair, have up to now, been successful to various

degrees.

Both Sunair and SA Express, however, are either fully or partly owned by the government

(with the inherent advantages), whilst Nationwide has an almost insignificant presence (+-

2 percent market share) on the Johannesburg-Cape Town route alone. This leaves Comair

as SAA's only large, fully privately-owned, competitor'.

Q

The discrepancies that exist between the goals of deregulation and the current structure

of the South African air travel market, however, are usually not noticed by domestic air

travellers, who have become more sophisticated consumers with a growing awareness of

travel options available. This trend has forced all domestic South African airlines intent

on surviving to become consumer driven. SAA managed to build a brand valued in the

marketplace during the years of its monopoly, gained a wealth of airline expertise,

provides an extensive domestic route network as well as frequency, and has vast

(compared to the other domestic airlines) funds available to spend on marketing and

product enhancement. These advantages that SAA has, increases the importance of other

domestic airlines, and especially privately owned airlines, to focus on traveller needs and

expectations. The current dynamics of the deregulated air travel market therefore requires

domestic, and especially privately-owned airlines, to fully embrace an integrated marketing

approach (with traveller needs and expectations as the focal point), to be able to survive

in an increasingly sophisticated consumer market against the backdrop of an "uneven"

playing fields.

1) For the purposes of this study, Comair will represent a medium-sized South African

airline .

1.2 THE RESEARCH PROBLEM

The research problem is that Comair has yet failed to develop an integrated marketing

approach, and that such an approach, because of market dynamics, has become a prime

tool in ensuring the airline's long-term survival.

1.3 GOAL AND OBJECTRVIES

The overall goal of this study is to provide a medium-sized South African airline with the

theoretical framework and necessary research and analyses, in developing an integrated

marketing approach in a deregulated environment.

The objectives of the study are :

to analyse the macro and market variables that could impact on the marketing

efforts of a medium-sized South African airline.

to assess a medium-sized South African airline's marketing efforts (in response to

external variables) using existing theories and the airline's own set objectives.

to link the marketing efforts of a medium-sized South African airline to internal

variables, to be able to provide a truly "integrated" analysis of all marketing

activities.

to provide broad guidelines for future marketing activities undertook by a

medium-sized South African airline.

5

1.4 RESEARCH. METHODOLOGY

To assist in achieving the goal and objectives of this study, empirical research was

undertaken in May 1995, to establish information necessary for Comair to act upon

prevailing market conditions, and facilitate a change in the airline's then marketing efforts.

The goal of the research, set by Comair's top management was to determine how

frequent SAA economy class business travellers could be persuaded to switch to Comair.

The universe of the research, as a result, was defined as frequent (six or more annual

trips) domestic business travellers, travelling economy class. The research methodology

viewed as most appropriate was the following:

O

A qualitative phase comprising five focus group sessions (including one session

consisting of travel agents). A trained and experienced moderator led the group

discussions using a specific guideline and agenda. The qualitative phase was

completed first to assist in developing a stage two (quantitative leg) questionnaire.

O A quantitative phase involving 200 personal in-home interviews, conducted in

Johannesburg, Cape Town, and Durban, by experienced field workers using a set

questionnaire.

A spread of participants working for small, medium, and large companies, during both the

qualitative and quantitative research legs were ensured.

6

Secondary research comprising literature such as newspaper articles, books, local and

international magazines, and other publications were included in the study, as well as

statistics obtained from Comair, the All Media and Product Survey (AMPS),

Sociomonitor, Department of Civil Aviation, United Nations, International Air Transport

Association, and the Central Statistical Services.

1.5 DIVISION OF CHAPTERS

This study has been divided into seven chapters. A brief synopsis regarding the contents

of each chapter follows .

Chapter 2

Chapter 2 is divided into two sections, each investigating the main components of the

external environment of a medium-sized South African airline. The first section analyses

the six megatrends comprising an airline's macro environment: the economic; socio-

cultural; physical; international; institutional; and technological environments. The impact

and relevance of these megatrends to a medium-sized South African airline, as well as

current trends, are discussed.

The second section examines the market environment of a medium-sized South African

airline.

7

The South African air travel industry is discussed in a world, regional, and domestic

context, the reasons behind choosing Comair as the focal point of the study are explained,

and the carrier's history as well as its competitors are reviewed. Due to space constraints,

both air travellers and travel agents are studied in separate chapters (chapter 3 and 4

respectively).

Chapter 3

This chapter analyses, and applies where possible, the different methods of segmenting the

South African air travel industry .

A geographic, demographic, and psychographic profile, of the South African air traveller

are given, and flyer characteristics such as travel frequency, as well as purpose of trip -

both important air travel segmentation variables, are studied.

The second section of chapter 3 deals with criteria airlines need to employ when selecting

target segments, and the third section with the importance of an airline "fitting" itself to

the selected target segments in such a way as to set it meaningfully apart from other

airlines - in other words, the "positioning" of the airline in the marketplace.

Chapter 3 lastly reviews the role of a mission statement in communicating the airline's

"positioning" to both air travellers and airline employees, and its function as a logical

conclusion of the process of segmentation, targeting and positioning.

8

Chapter 4

The first section of this chapter examines the role of the airline product as a component

of the marketing mix. The different levels of the airline product, its characteristics, and

the importance of customer value, customer satisfaction, and quality, when designing the

airline product, are discussed. The section concludes with an analysis of the importance

of airline "branding", and a look at future airline product trends.

The second part of the chapter peruses the role of distribution as a component of the

marketing mix, with specific reference to the role of travel agencies and central

reservations systems. New trends currently impacting on the airline distribution channel,

thus changing the current roles of travel agencies, central reservation systems and

passengers, are then considered. This is followed by a review of the function of direct

marketing in the airline distribution system, its advantages, and the development of

integrated direct marketing and a database marketing system.

Chapter 5

The remaining two components of the marketing mix, price and promotion, are analysed

in, this chapter. The first section of the chapter discusses air travel demand, the costs in

providing air transport, productivity, and other influences in air travel pricing. Pricing

objectives and strategies are then deliberated, followed by examining the role of yield

management in air travel pricing.

9

The second section of the chapter analyses the fourth component of the marketing mix:

promotion. Promotion in turn comprises four variables: advertising, public relations, sales

promotion, and personal selling. Each of these promotion "tools" is analysed discussing

the function, investigating related advantages and disadvantages, examining the setting

of objectives and choice of strategies, studying the development of an action plan, and

reviewing the necessity of evaluating results.

Chapter 6

Chapter 6 comprises a presentation of the findings of the empirical research.

Chapter 7

This chapter gives a brief summary on each of the preceding chapters, followed by a

SWOT analysis applied to the internal environment of Comair. The research findings

(representing external perceptions of the Comair product) are then related to the internal

analysis to offer "integrated" conclusions and recommendations.

10

THE MACRO AND MARKET FORCES AFFECTING

AI LINES IN SOUTH AFRICA

2.1 INT ODUCTION

An airline and the external environment which in it operates, are open systems, and they

influence each other reciprocally. It follows then that an airline cannot exist successfully

if it is out of pace with its external environment. Any alteration in the present status quo

of an airline's external environment can be considered as a change, a movement towards

instability, and a shift towards the unpredictable. Changes usually cannot be measured,

it causes insecurity, and originates from a number of interrelated external factors. These

shifts and changes are often also occurring rapidly, and an airline is therefore constantly

exposed to change. The result is that an airline continuously encounters a "new" external

environment, with the following types of trends:

Trends which represent opportunities for the airline.

Trends which pose particular threats to the airline.

Trends which may appear but which hold no implications for the airline (Marx and

van der Walt, 1989:33).

Unfortunately, most of the difficulties experienced by airlines when responding to the

external environment are not related to the actual adjusting, but are for management to

change preconceived ideas and beliefs. These ideas and beliefs have the potential to

render a specific airline product irrelevant to the needs of its target market when

circumstances change.

11

Management specialist Drucker (Kotler, 1994:2) encapsulates the importance of airline

managers being open-minded and receptive in a changing environment, when he stated

that an organisation's winning formula in one decade might be its undoing in the next.

A well-known example of an airline (and its management) that responded positively to its

external environment, is Carlzon's "marketising" of SAS airlines. When he took over as

president of SAS in 1980, the airline was failing to satisfy the needs of its target market.

Within four months, major changes initiated by Carlzon, including major product

adjustments, were implemented within the airline, leading to a marked increase in full-fare

traffic on SAS, at a time that price cutting and zero growth were taking place in the air

travel market (Kotler, 1994:25).

Marketing plays a very important role in the adjustment of an airline to its external

environment, but examples unfortunately abound of organisations that suffered "marketing

myopia" when viewing their external environment. In the 1970's, the most powerful US

organisations included General Motors (GM); Sears; RCA; and IBM. Today, all four are

struggling to remain profitable. GM kept on producing large cars despite smaller sizes

being desired; Sears was caught between fashionable boutiques and discount department

stores; RCA never mastered the art of marketing; and IBM ignored new customer needs

(Kotler, 1994:2). Corey (Kotler, 1994:1) summarises the function of marketing in a

changing external environment by stating: "Marketing consists of all activities by which

a company adapts itself to its environment - creatively and profitably".

ACRO-ENVIRONMENT

Physical Environment

Economic Environment

Institutional Environment

ARKET ENVIRONMENT

International Environment AIRLINE

Competitors

Air travellers

Technologica Environment

Travel agents

Socio-cultural Environment

12

The external environment of an airline consists of two "sub-environments", as illustrated

in figure 2.1, displaying an interplay of forces with potential powerful impact on air travel.

Airlines should therefore be aware of trends and happenings in their external environment,

as these could affect their survival in a volatile industry.

FIGURE 2.1: THE EXTERNAL ENVIRONMENT OF AN AIRLINE

SOURCE: Adapted from Middleton, V.T.C. (1993). Marketing in travel and tourism. Oxford:Butterworth and Heineman.

The next section is devoted to an analysis of these two important environments which a

medium-sized South African airline operates in.

2.2 THE MACRO ENVIRONMENT

The variables that exist in an airline's macro-environment, are often fittingly referred to

as "megatrends".

13

The individual airline has very little control over these, despite their potentially severe

impact on its existence. Because of an airline's lack of power over these variables,

awareness of changes and trends in this environment is particularly important.

Adjustments necessary for an airline to survive, can only be made once a macro

environment trend has been perceived and acknowledged. The following six "sub-

environments" constitute the macro environment of an airline:

the economic environment.

the socio-cultural environment.

the physical environment.

the international environment.

the institutional environment.

the technological environment.

Each of these "environments" is subject to a more detailed discussion in the ensuing

sections.

2.2.1 The economic environment

No product can be bought without the necessary monetary means. The purchasing power

of an airline's customers is largely a by-product of a country's economy. Due to the

expenses involved, and being a derived demand, air travel especially, is very sensitive to

the economic climate of a country.

It is therefore important that any airline marketing activity should seriously consider the

forces at work in this environment and be aware of major trends.

14

Specific attention needs to be given to macro-economic conditions that influence the state

of the economy such as the Gross Domestic Product (GDP), whether the economy is in

an inflationary or recessionary period, interest rates, unemployment levels, and so forth,

as the economic environment can and does change very rapidly. The effects of these

changes could be far-reaching and could frequently require changes in an airline's

marketing strategy. Even a well-planned marketing strategy can fail in the event of a rapid

business-decline cycle (McCarthy and Perreault, 1993:122). Airline marketers should, in

addition, be aware of trends in consumer buying patterns as leisure travellers' purchasing

power provides the broad framework for, and eventually translates into ticket sales

(Kotler and Armstrong, 1991:66).

2.2.11.1 The South African economy in a world and regional context

South Africa is considered to be a higher middle-income country, with a Gross National

Product (GNP) per capita in 1994 of 3 010 US Dollars (higher middle income group: $2

896 - $8 955). Figure 2.2 compares the GNP per capita of South Africa with those of

other countries (Luxembourg - $39 850, and Mozambique - $80, respectively being the

world's richest and poorest country, based on 1994 GNP per capita). In 1994, South

Africa had the sixth highest income per capita in Africa, after the Seychelles ($6 210),

Gabon ($3 550), Mauritius ($3 180), and possibly Libya and Reunion - statistics

unavailable, but estimated to be upper middle-income countries (World Bank, 1996:18).

However, with regard to the size of its economy, South Africa can be considered a

regional giant.

30 000

25 860

25 030 -

21 650

20 000 - 18 410

15 000 - 13 190

10 000 - 8 060

5 000 - 4 010 3 520 3 010

2 650

USA UK Argentina Malaysia Russian Federation

Hong Kong New Zealand Mexico South Africa

US

DO

LL

AR

S 1

994

15

The South African economy contributes 77 percent to the SADC region's GDP

(comprising the economies of Angola, Mozambique, Botswana, Lesotho, Namibia,

Malawi, Swaziland, Tanzania, Zambia and Zimbabwe), whilst Angola and Zimbabwe, the

region's two second largest economies, contribute 6 and 5 percent respectively (South

African Development Bank, 1990).

FIGURE 2.2: GNP PER CAPITA, SOUTH AFRICA AND OTHER COUNTRIES

SOURCE: Adapted from World Bank.(1996). World Bank Atlas. Washington D.C.

Income per capita and the size of a country's economy, however, does not always reveal

the full economic picture regarding the cost of living in a certain country.

16

Several barometers could be used in this regard. In a study quoted by the South African

Institute for Race Relations (April 1995:6), it is mentioned that one kilogram of bread

based on the weighted average of 12 occupations) requires 10 minutes of work (to be able

to buy it) and a hamburger and a large portion of chips (comparable to MacDonald's

BigMac) 45 minutes, in Johannesburg. The average time for 47 cities ranging from

Lagos, to Toronto, Bangkok, and Zurich, is 23.9 minutes (bread) and 69.2 minutes

(hamburger and chips) respectively. New Yorkers would have to work 14 minutes for

one kilogram of bread and 23 minutes for a BigMac, while inhabitants of Nairobi 44 and

177 minutes respectively. Based on these statistics, the cost of living in South Africa

compares favourably with other countries worldwide. Although the above statistics

exclude other important expenses such as transport and accommodation (and stops short

from a full-scale comparative economic study), it could possibly indicate that South

Africa's cost of living allows the higher income groups more disposable income to spend

on air transport than for example Kenyans, but less than New Yorkers.

Another prominent characteristic of the South African economy that should be

highlighted, is the country's racial disparity in income distribution - considered by most a

legacy of the "apartheid" era. Although the gap has narrowed between 1980 and 1990,

it is still huge: The average income per White household in the metropolitan areas of

South Africa in 1990 was R71 598 per annum, the corresponding figure for Asians was

R26 918, Coloureds R22 642, and Blacks R11 682 (Bennett, 1995:199). This

discrepancy has given rise to South Africa's economy - having both First and Third world

characteristics - being described as a "dual economy", with mainly the White community

falling in the former, and the Black community in the latter category.

17

The Coloured and Indian communities fall somewhere in between. Apart from being the

least educated and least wealthy population group, the Black community is also the worst

afflicted by unemployment - 41 percent of Blacks are estimated to be without a job

(Stengel, R. 1995:40).

The following section discusses certain of the economic indicators most often used, when

analysing a country's economy.

2.2.1.2 Economic indicators

Airline marketers should be aware of the economic indicators discussed below, as they

reflect changing economic trends with a potential impact on air transport.

2.2.1.2.1 Economic growth

Every country's economy has a natural cycle which is not determined by politics.

Economic policies and politics, however, do determine the range of this economic cycle.

South Africa has a +-3 percent growth ceiling, due to a high import propensity and a lack

of foreign direct investment (FDI). This means that imports from abroad increase during

a time of economic growth and eventually exceed South African exports. When this point

is reached (at a +-3 percent growth rate), the economy, as a result, slows down again. In

order to attain a higher growth ceiling, the South African economy needs to be

restructured, so that it can lower its dependence on imports while increasing exports

through producing competitive products (De Wet:1995).

18

South Africa is presently drawing close to the upper turning point of its economic cycle.

The growth rate for 1995 was +-3 percent, while 1996 in all probability will still be a good

year, with a growth rate similar (or higher) to that of 1995. However, the South African

economy is predicted to start entering a cyclical downturn again in 1997, with a projected

economic growth rate of 1 to 2 percent during that period. The lower turning point of the

South African economic cycle is estimated to occur in 1999 (De Wet:1995). It is the

experience of the South African air travel industry that both leisure and business travel

decline during periods of recession. A higher growth ceiling (and therefore a higher,

lower turning point), will contribute to sustained air travel even during cyclical troughs.

2.2.11.2.2 Ikillataon

The average inflation rate for South Africa during the 1985-1994 period was 14.2 percent

(World Bank, 1996:18), whilst the inflation rates for our main trading partners, most

notably the USA and UK, were 3.3 percent and 5.7 percent respectively. World inflation

(including the inflation rates of our main trading partners) currently appears to have

slowed down, and is presently below 3 percent. Although South Africa's inflation rate has

decreased to a low of +-6.5 percent (November 1995), it will have to drop even further

to be on par with those of our main trading partners (De Wet:1995).

As with other products, inflation causes the price of air fares to rise in response to

spiralling fuel, catering, and salary costs.

19

2.2.1.1.3 international capital flows

Despite short-term capital inflow into South Africa, the possibility exists that little foreign

direct investment is likely to happen. South African investments currently have a low

return on investment due to low productivity, a rigid labour situation, low profits, and

high risks. International capital currently favours countries such as the USA, China, and

other places in the Far East. Barring foreign investment, virtually no aid and little

development finance are given to developing countries these days - the majority of what

is given being channelled through to Russia and Eastern Europe (De Wet:1995).

Foreign investment, through stimulating job creation and contributing to the economy, has

a benign effect on air travel (being a derived demand product). The transport of

professionals, consultants, and executives, to investment sites and between major cities,

could often grow a route substantially (e.g. Richards Bay and the ALUSAF project).

2.2.1.2.4 The exchange rate

The Rand's current decline against other currencies is likely to continue until South

Africa's inflation rate reaches 3 percent (De Wet:1995). At the time of writing (26 April

1996) the Rand Dollar exchange rate was R4,44; whilst the Rand Pound exchange rate

was R6,673. A weaker Rand has the following effect on the South African air travel

industry:

It becomes cheaper for foreign visitors to visit the country when the exchange rate

favours them, and this aspect has the potential to attract more foreign visitors.

20

O A poor local currency serves as a stimulant for the domestic tourism market as it

becomes too expensive for the local market to travel overseas. Domestic travel

is then often considered a viable option.

O

Overseas marketing of South Africa, by the South African Tourism Board

(SATOUR) and local businesses (e.g. hotels and game resorts), becomes more

expensive with an unfavourable exchange rate (Bennett, 1995:200).

O The cost of leasing and buying aircraft becomes more expensive, as in many cases

the payments have to be made in international currencies such as the Dollar or

Pound (Flitestar's leasing payments had to be made in US dollars, hastening the

demise of the airline due to a progressively weaker Rand).

0

Aircraft fuel becomes more expensive, increasing the cost of air fares.

2.2.1.2.5 Economic policy issues

The South African government, from an economist's point of view, presently has both

positive and negative trends with regard to economic policies. The positive trends (April

1996) can contribute to a restructuring of the South African economy, thus raising the

lower turning point of the economic cycle. The current positive trends are:

A maintenance of monetary discipline through high real rates of interest, and

slowly declining nominal rates.

An attempt at fiscal discipline - although difficult, the situation is unlikely to get

out of hand.

The government is favourably disposed towards privatisation.

21

O Less protection is provided to South African goods due to agreements reached at

GATT (General Agreement on Trade and Tariffs) and the World Trade

Organisation.

An attempt to uplift the level of literacy, education, and training, across the board.

A consistency and stability in policy (De Wet:1995).

The current (April 1996) negative trends that could adversely affect the South African

economy are:

Socialistic undertones with regard to education, health, land, and labour issues.

An inability to curb crime and violence.

A standstill in many areas of the civil service.

Taxes and government expenditure are still too high.

A strong desire to act against big business.

Several state and semi-state monopolies still exist.

An inability to implement RDP projects (De Wet:1995).

As a derived demand product, air travel growth is dependant on a healthy and growing

economy. Since economic growth is facilitated by sound governmental policies, the air

travel industry will be affected by the government's treatment of and solutions to the

country's economic problems.

2.2.1.3 Tourism and air travel

This section deals with tourism as an individual component of the South African economy,

due to the industry's interrelationship with air transport. Tourism is currently one of the

22

major contributors to the South African economy (the fourth biggest forex earner in 1993,

after manufactured goods, gold exports, and mining), and the government is increasing

its efforts directed at stimulating this industry as a source of revenue. Tourism constituted

6 percent of the world GNP in 1993, compared to only 3 percent in South Africa

(SATOUR, 1994a). The Explore South Africa campaign launched by SATOUR in 1995,

and the World Rugby Cup (June 1995), contributed to South Africa's growing popularity

as a tourist destination, and are followed by more promotional campaigns in 1996 and

1997. Cape Town, in addition, is a contender in a bid to host the Olympics in 2004.

SATOUR predicts that overseas visitors to South Africa will increase to two million by

the year 2000 as presented in figure 2.3, due to a growing interest in the country after the

lifting of sanctions. An increase in tourism will have a beneficial effect on air travel both

to and within South Africa: SATOUR's annual report (1993) records that 82 percent of

all overseas visitors in 1992 used air transport as a travel mode to South Africa. These

travellers often utilise domestic air transport to reach favourite South African tourist

destinations such as Cape Town and game reserves in Mpumalanga from Johannesburg.

An increase in tourism arrivals will therefore have a positive result on the traffic volumes

of domestic airlines.

The promising future of tourism in this country, however, will have to be supported by

maintaining political stability, curbing violence, and resolving certain other industry issues

such as the improvement of service standards.

1991 1992 1993 1994 1995 1996 1997 1998 1999

8 000 000

7 000 000

6 000 000

LL 0

5 w

000 000

D D 0 4 000 000 Z

3 000 000

2 000 000

23

FIGURE 2.3: PROJECTION OF OVERSEAS VISITORS 1990-1999

SOURCE: Adapted from SATOUR(b). (1994). Projection of overseas visitors. Pretoria .

2.2.2 The social environment

Kotler and Armstrong (1991:62) define demography as: "the study of human population

in terms of size, density, location, age, sex, race, occupation, and other statistics". The

demographic environment is of major interest to airline marketers because it involves

people, and people make up air travel markets.

24

2.2.2.1 Demographics

The South African population comprised 40 435 300 individuals in 1994. The average

annual growth rate of the population during 1991-1994 was +-2 percent, while illegal

emigrants from neighbouring countries grow the population a further 0.5 to 1 percent

annually (De Wet:1995). Almost half the population resides in urban areas, whilst 33

percent of the population participates in the country's economy. The median age of the

population is a young 21 years (South African Development Bank, 1990).

One of the most prominent features of the South African population is its cultural

diversity. Four main racial groupings exist: Blacks, comprising 76.1 percent of the

population; Whites 12.8 percent; Coloureds 8.5 percent; and Asians, 2.6 percent (Central

Statistical Services, 1994:3). However, even within these main ethnic groupings, several

diverse cultures can be found. The Black community is divided between nine major tribes;

the White community consists of a 57.5 percent Afrikaans majority, a 38.7 percent English

component and several other smaller communities (e.g. Greek, Portuguese, Jewish,

German, etc.). The Coloured community is divided between the Griquas (mainly of

Hottentot-European descent) and the Cape Malays (with diverse Far East origins - slaves

brought to the Cape); while the Asian community consists of Indian Tamils, Hindus, and

Muslims, originally from several parts in India (five different languages are still spoken by

older generation Indians). A small (+-20 000) Chinese community is found in the country,

the majority of whom were born here (Central Statistical Services, 1994:7, and Bureau

for Information 1995:5,6).

25

As a result of this cultural diversity several languages are spoken in the country, 11 of

which are now officially recognised, although English and to a lesser extent Afrikaans,

is widely used as the lingua franca between the various communities.

With regard to religion the nation appears to be more homogenous. The majority (+-70

percent) of the population are affiliated to one or other Christian church, while the

remainder do not profess any religious involvement except for small minorities supporting

the Hindu, Islamic, and Jewish faiths. However, the Christian umbrella covers numerous

churches with widely diverse views such as the staunch Calvinistic Dutch Reformed

church, and independent Black churches blending traditional beliefs with Christian

doctrine (Central Statistical Services, 1994:9).

Apart from the above linguistic and other cultural aspects, the South African racial

communities also differ with regard to average age, urbanisation, growth rate, human

development and other variables. The level of education as well as the human

development in South Africa are cases in point:

Education is an important facilitator of economic growth and has become a

priority for the new government. Since the April 1994 election, more funds have

been allocated to education whilst segregated schooling has been abolished in an

attempt to provide equal education opportunities for all children. The

government's recent focus on education is warranted, statistics show that the

country's education level is in dire need of attention.

26

In 1991 only 11.3 percent of the South African population qualified for a Matric,

any higher certificate, or a degree. This percentage is spread unevenly between

the different population groups: The White community is the most educated - 44.7

percent having a Matric or higher qualification, followed by the Indian community

- 21.8 percent, the Coloured community - 7.8 percent, and lastly, the Black

community - 5.9 percent (South African Institute for Race Relations, April

1995:5). While only 3.2 percent of the South African population has a degree or

similar education, 20 percent of United States citizens are college-educated - the

highest college-educated citizenry in the world as well as the most powerful global

economy (Kotler, 1994:157).

Human development is a measurement of individuals' ability to live a long and

healthy life, to communicate, to participate in a community, and to have sufficient

means to be able to afford a decent living. The Human Development Index (HDI)

is often used to measure human development in a given country. Any

measurement above 0.8 is considered to be a high level of human development

(HHD), 0.5-0.8 is considered to be the medium human development range

(MHD), and below 0.5 indicates low human development (LHD). Figure 2.4

compares the level of human development in South Africa with that of other

countries (also depicting the FEDI of each South African racial community).

0.932

0.840

0.90

0.836

0.679 0.677 0.670 0.663 0.644

0.513 0.500

0.425

0.252

cr so, v p- 4, 4, c.,° 4 .‘ + 4, * t 0 cot'

._:_,0 `fit` ,.‘ 9 _ • b 0.4 e

co A,

0 4 ,,, * .0P Nqf' 0 0 b e

4' co co

4,

0.8

High Human Development

Modium Human Development

0.4

0.2

0

a°tee 41,

0 4. gb

° e q <0° yo

Humon Development

0.6

o Ola ,.- ----0.47.0

27

FIGURE 2.4: HUMAN DEVELOPMENT INDEX, WORLDWIDE (1994 )

SOURCE: Adapted from Central Statistical Services(a).(1995). October Household Surve y. Pretoria.

Several cultural issues have influenced the South African air travel industr y in the recent

past, such as the usage of languages, SAA is now using Black languages on board whilst

using less Afrikaans (antagonising many Afrikaners), the promotion of SAA's "ubuntu"

corporate culture, and so forth. This is onl y the beginning of a trend. A long-term growth

in the non-White component of the air travel market is projected, while affirmative action

efforts will contribute to a more culturall y diverse airline staff component.

28

These trends will increasingly require airline marketers to become sensitive to cultural

issues, necessitating a multi-cultural approach both internally (e.g. a more "open"

environment) and externally (e.g. more complicated media and advertising strategies).

2.2.2.2 Socio-chhural aspects

Belch and Belch (1990:57) state the following with regard to socio-cultural aspects:

"Marketers must take into account the core cultural beliefs and values that exist in the

countries or regions that compose their marketplace. Marketers must constantly monitor

the socio-cultural environment in order to spot new opportunities or to identify new

threats. They must monitor social trends and changes in consumer values and respond to

these through their marketing and promotional programmes".

As part of the international community, South Africa (and domestic air travel) is affected

by global as well as Western socio-cultural trends. The following are some of the more

important worldwide trends.

2.2.2.2.1 The changing role of women

Worldwide, women are demanding and experiencing greater opportunities in all spheres

of life: at work, at home, and in social settings. They are increasingly seeking independent

lifestyles, wanting fewer children, more fulfilling careers, and a recognition of their

individual capabilities (Allvine, 1987:116). In 1960, women comprised 23 percent of the

South African work force, growing to 37 percent in 1987. During 1969 to the early

eighties, the number of White women filling managerial posts increased from 6.75 percent

to 14 percent (Marx and van der Walt, 1993:63).

29

Women played a major role in South Africa's transition to democracy, are now well-

represented in Parliament, and are progressively earning and controlling more purchasing

power than in the past. Due to the growing number of female travellers, airline marketers

will increasingly have to focus on this segment, designing products and packages that suit

the tastes of these flyers.

2.2.2.2.2 The increasing importance of leisure

With growing prosperity and improved standards of living, a new work ethic is developing

in the Western world. Workers are looking for interesting and dignified jobs, and would

rather have a shorter working week, more holidays, and longer paid vacations. As a

result, leisure has become a huge growth industry in the USA (Allvine, 1987:120). Partly

due to greater affluence, and partly due to an increase in the importance of leisure, touring

foreign countries have become a popular holiday option for many Europeans, North

Americans, and Asians. South Africa is currently one of the most popular African

destinations, and the resultant increase in tourists has had a positive impact on the

domestic air travel industry.

2.2.2.2.3 The rise of singles

Similarly to women, singles are a growing market segment, especially in the Western

world. Partly a product of sexual freedom and expanding career opportunities for women,

the new singles generation primarily comprises people in the 20-34 age group. Many

within this group feel no immediate need to get married and desire, for the time being, to

concentrate on their careers (Allvine, 1987:124).

30

The growing importance of this segment is reflected by the fact that the traditional

household (husband, wife , children) is no longer the dominant household pattern in the

United States. People are now choosing not to many, marrying later, or marrying without

having children (Kotler, 1994 - 157). Airline marketers have to consider this growing

segment when designing traditional airline products such as spouse fares, family packages,

and so forth.

2.2.2.2.4 Changing sexual attitudes

Since the sexual revolution in the 1960's and 1970's, individuals' attitudes towards

morality, sex, and divorce, have been changing. Divorce is now an acceptable method of

ending an unpleasant marriage, while pre and extra marital sex are more acceptable than

before (Allvine, 1987:122). This change in attitude is very evident in the marketing

environment. Some organisations are even using previous sexual "taboos" as modern

market segmentation and positioning tools. TIME magazine (25 September 1995:20)

reports that Miami Beach (Florida, USA), has recently decided to market itself as "the gay

and lesbian destination of the 90's" as research has revealed that gays "typically have far

more disposable income than do straights" and that gays "clearly spend disproportionately

more on travel than any other group". Certain American airlines, for similar reasons,

already provide packages to gay and lesbian couples (TIME, 25 September 1995:20),

while a Cape Town-based travel agency (Gay esCape), caters for gay and lesbian clientele,

offering tours, advice, and a list of "gay-friendly" places and businesses to overseas gay

visitors.

31

2.2.2.2.5 A growing interest in health consciousness

People in the Western world are increasingly becoming more health conscious, which has

led to a worldwide growth in health products and healthier lifestyles. The South African

society has experienced similar trends in health consciousness. The Health and Racquet

Club (a chain of upper class gyms), was listed on the Johannesburg Stock Exchange in

April 1994. In 1995 the organisation's turnover increased by 34 percent to R120 million

(Nel, N. 1995:70).

The growing interest in health has led to South African airlines receiving more requests

for healthy food such as vegetarian meals; Appletiser; mineral water; brown bread; and

so forth. Many airlines across the globe have banned smoking, as nonsmokers are

increasingly concerned about the effect that smoke fumes have on their health. Smoking

on all domestic SAA, Comair, and Sunair flights, is banned. SAA plans to extend this

policy in the near future to all Boeing 737 flights in Africa, domestic sectors of

international flights, and two of the eleven weekly international flights to London (Natal

Witness, 22 January, 1996).

2.2.3 The physical environment

Across the globe, people are increasingly concerned about the deteriorating physical

environment, and environmentalism has grown from a grass-roots movement into a

political and business force to be reckoned with. Kotler defines environmentalism as "an

organised movement of concerned citizens and governments to protect and enhance

peoples' living environment" (1994:160).

32

Airline marketers should be aware of the threats and opportunities associated with three

trends in the physical environment:

Increased cost of energy. The price of oil created serious problems for the world

economy when it shot up from $2.23 a barrel in 1970 to $34 a barrel in 1982. The

development of alternative energy sources, however, has led to a decline in oil

prices by 1986. Still, oil reserves are finite, and even air transport will have to use

alternative energy sources in the distant future.

Increased levels of pollution. The public's concern with pollution provides

marketing opportunities for organisations. Resourceful organisations will initiate

environment-friendly actions to show their communities that they care about the

well-being of the environment.

The changing role of governments in environmental protection. Governments

vary in their concern for the environment. The German government on the one

hand is vigorous in its pursuit of environmentally conscious policies, while many

poor nations are doing little. The hope is that organisations around the world will

accept more social responsibility and that less expensive devices are found to

control pollution (Kotler, 1994:159).

Environment-related constraints are becoming increasingly common in the air travel

industry (e.g. the banning of stage two aircraft in Europe, restricted airport operational

hours due to noise pollution, etc.). In response to environmental legislation and efforts,

the International Air Transport Association (IATA) provides a "clearing house" for such

information, monitors international environmental debate, and promotes common industry

positions on environmental problems.

33

These include support for a coordinated phase-out of old aircraft types, and noise-

compatible land-use planning. IATA also publishes an "Environmental Review", and is

currently building a data bank containing environmental information (IATA, 1995:8).

2.2.4 The international environment

Due to trade agreements such as the General Agreement on Trade and Tariffs (GATT),

the world is fast becoming one big marketplace. Economic realities seem to have become

more important to countries, while international boundaries have become less significant.

The integration of the European community, the North Atlantic Free Trade Agreement

between the USA, Canada, and Mexico, the collapse of Communism in Eastern Europe,

indicate a trend towards global integration. Closer to home, consensus exists that the

Southern African economies are interrelated and interdependent. Closer integration and

cooperation of the regional economies are therefore advocated (Bennett, 1995:208).

The GATT annex on air transport services came into force for the majority of signatory

countries (including South Africa), on 1 January 1995. Though insufficient time has

elapsed to assess its impact on the air travel industry, a vigorous debate continues whether

in time, GATT will become the primary multilateral instrument to open world air transport

markets. At present, only aircraft repair and maintenance services; the selling and

marketing of air transport services; and computer reservation systems fall within the scope

of the accord. The GATT agreement excludes traffic rights and makes an explicit

commitment that a member's obligations under current bilateral or multilateral agreements

will not in any way be reduced.

34

However, proponents of GATT point out that the agreement calls for "progressive

liberalisation", and some countries (Australia, New Zealand, Singapore, Malaysia, and the

Nordic countries) have already asked for a working party to look at broadening GATT's

coverage of other aviation issues. The eventual effect of GATT and other trade

agreements on air travel could be summarised by quoting a World Trade Organisation

councillor (Marconini): "Aviation cannot escape broad-based economic disciplines

forever, it is no longer the unique, glamorous sector it used to be" (Airline Business,

September 1995:81-82).

Traffic rights and GATT aside, the air travel industry has already been strongly influenced

in recent decades by other international trends. The rise of mega-carriers is one such

example. Airline mergers, takeovers, and alliances, are increasing, and it is predicted that

by early in the next century, five as opposed to the current eight major West European

airlines will exist, four major US trunk carriers (presently 7); and seven other major

airlines (currently 8). The resulting 16 mega-carriers will have an estimated 75 percent

share of world traffic (IATA, September 1995).

2.2.5 The institutional environment

An airline's institutional environment includes components ranging from laws governing

its operations and government agencies enforcing those laws, to the political climate of

the country. Although laws affecting air transport and government agencies dealing with

airlines are the most visible component of an airline's institutional environment, the

influence exerted on an airline by a country's political climate should not be

underestimated, and is often very powerful and prescriptive.

35

This section firstly deals with direct government involvement in the air travel industry

(worldwide, but also in South Africa). The impact of South Africa's political climate on

its air travel industry is then discussed .

One of the main purposes of government regulation in the air travel industry is (or should

be), to protect passengers and society from unfair business practices. The institutional

environment is therefore probably the most restrictive of the "megatrends". Most of an

airline's marketing mix components (e.g. product - aircraft, promotion - advertising, price

etc.), is affected in some way or another by government regulation (Belch and Belch,

1990:57). However, government involvement in the air travel industry has in the past

often exceeded the mere protection of passengers. This is particularly the case in Africa,

where the World Bank and the African Regional Airline Association (AFRAA) have

criticized governments for operating airlines as extensions of their various foreign affairs

departments. They allege that African governments are reluctant to let go of airlines as

they are sources of national pride and often provide free VIP flights. This lack of political

will to reorganize airlines into business units, renders them unattractive to other alliance-

seeking airlines (Finance Week, 26 August 1993). Africa, however, is not the only

continent still struggling with the issue of state involvement in the air travel industry. The

1994 round of state aid approvals in Brussels has given the French, Greek, and Portuguese

governments, authority to support their struggling flag carriers with government aid. Air

France was awarded the biggest aid package ever to an airline - 3.7 billion US Dollars,

one of the conditions being that the French government should not interfere again with

the management of the airline (Airline Business, September 1994:29).

36

The situation in South Africa is fortunately different. In 1987 the White Paper on

Privatisation and Deregulation advocated that the air travel industry be deregulated (based

on the American experience which initiated a worldwide trend). The thinking was that

competition will lead to more efficient airlines, resulting in lower fares, while benefitting

the country's economy in the long term. The recommendation was included in the

Domestic Air Transport Policy, published by the Department of Transport in May 1990,

and subsequently embodied in the Air Services Licensing Act, Act 115, 1990. The South

African air travel industry was, as a result, deregulated on the first of July 1991. SAA,

no longer the official national carrier, now had to operate as a business unit. In response

to deregulation, two airlines initially, Flitestar and Comair, took to the air to exploit the

new opportunity of "open skies". On 29 April 1992, Welgemoed, then Minister of

Transport, announced that the Cabinet had approved a new liberal international air travel

policy for South Africa, which has since become the International Air Services Act of

1993. The new act allowed for more than one designated South African carrier on

international and regional routes (Department of Civil Aviation, January 1996). Comair

has since been designated as the second South African carrier on both the Johannesburg

to Harare, Johannesburg to Windhoek, Johannesburg to Victoria Falls, and Cape Town

to Windhoek, routes.

In response to the elections, a new transport policy is currently taking form, and will be

published as a White Paper by the end of 1996. In line with views held by the present

government, many of its objectives come from the RDP .

37

Some of the issues addressed are meeting basic needs; creating wider ownership of the

South African economy; organising private-sector capital; reducing trade debt; and

promoting fair competition (Financial Mail, 26 January 1996).

As mentioned above, laws and regulations are often not the only institutional force with

which an airline has to deal with. The political climate and government of a country can

often have a powerful impact on airline operations, and South Africa particularly has

numerous examples supporting this statement.

One of the most telling examples currently, is the increasing number of tourists visiting the

country. This, and the high increase in airlines operating to and from South Africa, could

at least be partly attributed to South Africa's first ever democratic elections, held in April

1994. As the majority of overseas visitors use air transport to arrive in South Africa,

while also utilising domestic air transport, the benefits to the South African air travel

industry are obvious. However, the increase in tourists visiting the country is not the only

impact which the country's current political climate had on the air travel industry. Black

economic empowerment, for instance, being one of the present government's main

objectives, is another example. Although no law has been passed in South Africa giving

legal impetus to Black economic empowerment, the following examples illustrate the

subtle yet powerful force which a country's political environment can exert on the air

transport:

0

According to Myburgh (SAA), "Black economic empowerment was undoubtedly

one of the more important reasons" why SAA agreed to help bring SA Express

about (Mazwai, T. 1994:12).

38

SAA decided to acquire a 20 percent share in the airline, while Thebe Investment

Corporation - a Black owned investment giant - holds a 51 percent stake. An

umbilical link exists between Thebe Investment Corporation and the Batho-Batho

trust, headed by Nelson Mandela and (previously) Walter Sisulu, but allegations

of Thebe being an investment arm of the ANC have been vehemently denied by

all parties concerned (Sunday Finance, 6 February 1994:3).

Black economic empowerment is one of the main reasons why the government

also supports affirmative action. SAA and other state-owned enterprises afford

the government with the necessary means to achieve this goal. All appointments,

transfers, and promotions of White SAA employees, for example, currently have

to be approved by a "Turn Strategy Council", which sets racial quota goals and

targets to be achieved by certain dates (De Villiers, 1994:1). The objective of

both Transnet and SAA, is a fundamental shift in race and gender profiles by the

year 2000. Other South African airlines are responding to affirmative action in

various ways. Both SA Express and Sunair have a relatively high non-White staff

component (Sunair, +- 50 percent), and are either partly or wholly owned by the

government. At Comair, the only large, privately-owned airline in South Africa,

most of the junior, middle, and top management positions, apart from a Black

board member, are still filled by Whites (January 1996) - the majority of the non-

White staff employed by the airline in the past two years have filled positions in

the organisation's front-line departments. Although the government has thus far

refrained from forcing private organisations to endorse racial quotas, Comair's

aim is to increase its number of non-White employees.

39

Figure 2.5 reflects the racial composition of the country, SAA, and Comair, at the

end of 1994.

FIGURE 2.5: RACIAL COMPOSITION OF SOUTH AFRICA, SAA, AND COMAIR

1W

79

❑ Bleck

0 White

0 Coloured

0 Asian

76

70

1 6° 0 ce 0.

40

23

13 13

2

COMAIR

SOUTH AFRICA

SAA

SOURCE: Adapted from SAA News. De Villiers, A.(1994). New turn for turn strategy. August p1. South African Advertising Research Foundation.(1994). All Media

and Products Survey. Johannesburg. Comair.(1995). Personnel. Johannesburg.

One of the most publicised issues concerning Black economic empowerment in the air

travel industry, is the privatisation of state assets.

40

The government and unions, unfortunately, have conflicting views on the role of

privatisation with regard to Black economic empowerment. The government is in favour

of partial (e.g. SAA) and total privatisation (e.g. Sunair) of state assets, due to the belief

that privatisation will increase the efficiency and expertise of state assets; earn money for

the government to pay off debt; and grow the economy in the long run. The unions, on

the other hand, feel obliged to protect their members' jobs, and believe that job losses due

to privatisation are inevitable. The issue is far from being resolved, but the latest

indications given by Maharaj (Financial Mail, 26 January 1996) are that "Sunair can be

privatised (now) and the workers would support it". However, Maharaj is not sure who

to sell it to. With regard to SAA, Maharaj is more vague. He states that SAA is not for

sale yet, but that he intends explaining to the unions that privatisation might lead to long-

term growth in employment opportunities (SAA now employs more people than when it

was "rightsized" by Myburgh two years ago). Maharaj is more definitive on the issue of

Black economic empowerment, indicating that both Sunair and SAA (if partially

privatised), will be sold to owners that are fully committed to Black economic

empowerment (Financial Mail, 26 January 1996).

SAA's acquisition of seven Boeing 777-200's and two Boeing 747-400's is

another example reflecting the extent to which the government's Black economic

empowerment drive affects the air travel industry. SAA had to choose between

three different aircraft manufacturers, one of the criteria being contributions to the

RDP through local contracts, as a result of the order. SAA's choice of Boeing

will lead to offset contracts valued at R2.8 billion being placed in South Africa

(Business Report, 6 November 1995).

41

Airlines will continue to be influenced by the political climate of a country, as long as air

transport is perceived to be a high-profile industry. The pressure on an airline to behave

politically correctly might differ from one country to another, and in some cases will even

be exerted by the airline's passengers rather than a country's government. A case in point

is the recent charges of racism which has been levelled at British Airways (BA). In

November 1995, a British-born Black probation officer accused BA of racism, after his

passport was photocopied without his consent - BA eventually apologised. In the latest

race row, BA payed 2 000 pounds in compensation to a 16-year-old schoolgirl who

believed that check-in staff tried to stop her from taking a flight because she was Black.