an examination of momentum strategies in commodity futures markets

TRANSCRIPT

AN EXAMINATION OF

MOMENTUM STRATEGIES

IN COMMODITY FUTURES

MARKETS

QIAN SHENANDREW C. SZAKMARY*SUBHASH C. SHARMA

Commodity futures and equity markets differ in several importantrespects. Nevertheless, it was found that momentum profits in commodi-ties are highly significant for holding periods as long as 9 months,and returns to momentum strategies are roughly equal in magnitudeto those that have been reported in stocks. The profits documented aretoo large to be subsumed by transactions costs. Although the momen-tum strategies appear to be quite risky, their profitability cannot be fullyaccounted for in the context of a market factor model. Further, it is shownthat momentum profits eventually reverse if positions are maintainedlong enough after portfolio formation. © 2007 Wiley Periodicals, Inc.Jrl Fut Mark 27:227–256, 2007

*Correspondence author, Department of Finance, Robins School of Business, University ofRichmond, Richmond, VA 23173; e-mail: [email protected]

Received January 2006; Accepted April 2006

■ Qian Shen is an Assistant Professor in the Department of Economics, Finance andOSM in the School of Business at Alabama A&M University in Normal, Alabama.

■ Andrew C. Szakmary is an Associate Professor in the Department of Finance at RobinsSchool of Business at the University of Richmond in Richmond, Virginia.

■ Subhash C. Sharma is a Professor in the Department of Economics at Southern IllinoisUniversity at Carbondale in Carbondale, Illinois.

The Journal of Futures Markets, Vol. 27, No. 3, 227–256 (2007)© 2007 Wiley Periodicals, Inc.Published online in Wiley InterScience (www.interscience.wiley.com).DOI: 10.1002/fut.20252

228 Shen, Szakmary, and Sharma

Journal of Futures Markets DOI: 10.1002/fut

1The long horizon contrarian strategies have been examined by DeBondt and Thaler (1985, 1987),and Conrad and Kaul (1998) in U.S. markets, and by Richards (1997) in an international context.The momentum literature is reviewed in more detail below.

INTRODUCTION AND LITERATURE REVIEW

In recent years, many published studies have reported that relativelysimple trading strategies based on past cross-sectional stock returnsyield significant future abnormal returns. Both long-horizon (3–5 year)contrarian strategies that rely on return reversals, and intermediate hori-zon (1–12 month) momentum strategies based on return continuations,have been shown to be surprisingly profitable.1

Findings regarding the momentum strategies appear to be particu-larly robust with respect to different methodological approaches, peri-ods, and countries examined. Jegadeesh and Titman (1993) were thefirst to report significant intermediate horizon momentum profits in theU.S. stock market. Using a different methodological approach, Conradand Kaul (1998) nevertheless report similar findings. Conrad and Kaul,as well as Grundy and Martin (2001) show that the momentum strate-gies work in all subperiods they examine, being consistently profitable inthe U.S. stock market since the 1920s. Similarly, Jegadeesh and Titman(2001) find that in the 1990–1998 period (which was not included intheir original 1993 article) momentum strategies continue to be prof-itable to about the same degree as earlier; that is, the best strategies earnabnormal returns of approximately 1% per month, before trading costsare considered. Rouwenhorst (1998) examines individual stock returnsin 12 European markets, and finds momentum effects that are similar tothose documented in the U.S. Indeed, Chan, Hameed, and Tong (2000)provide statistically significant evidence of momentum profits even whenstrategies are implemented with international stock market indicesrather than individual stocks.

The causes of momentum and/or contrarian profits have been thesubject of considerable debate. Broadly speaking, three primary explana-tions have been advanced in the literature. The first is that the momen-tum profits simply represent fair compensation for risk. As Korajczyk andSadka (2004) note, the consensus in the literature is that risk factors failto completely explain intermediate horizon momentum profits in stocks.For example, Fama and French (1996) concede that their three-factorasset-pricing model does not explain returns to momentum portfolios.Similarly, Grundy and Martin (2001) confirm that the momentum strat-egy’s average profitability cannot be explained as a reward for bearing thedynamic exposure to the three factors of the Fama and French model,

Momentum Strategies 229

Journal of Futures Markets DOI: 10.1002/fut

2Another risk-based explanation of momentum profits is Chordia and Shivakumar’s (2002) claimthat momentum profits in U.S. stocks can be accounted for by exposure to macroeconomic risk fac-tors. However, Griffin, Ji, and Martin (2003) subsequently demonstrate that this linkage does notexist in an international context. Further, Cooper, Gutierrez, and Hameed (2004) show that Chordiaand Shivakumar’s macroeconomic multifactor model is not robust to common screens used to miti-gate microstructure-induced biases such as the removal of high trading-cost stocks or the skippingof time between formation and holding periods.

nor by exposure to industry factors.2 Nevertheless, some studies (e.g.,Conrad & Kaul, 1998) have indicated momentum profits could be a by-product of certain stocks being riskier than others in some unknown way,and thus having higher expected returns. This is because momentumstrategies take long (short) positions in stocks with high (low) pastreturns; if these past returns are high (low) because of unknown system-atic risk factors, then the same stocks should continue to earn relativelyhigh (low) returns in future periods. If this interpretation is correct, thenmomentum profits can be consistent with market efficiency.

Conrad and Kaul (1998) argue that the cross-sectional variationin the mean returns of individual securities plays an important rolein their profitability, and could potentially account for the profitabilityof momentum strategies. However, recent findings cast doubt on theConrad and Kaul hypothesis. If momentum profits were due primarily tocross-sectional differences in mean returns, then past winners (losers)should continue to be superior (inferior) performers indefinitely into thefuture, but Jegadeesh and Titman (2001) find that momentum portfolio(winners minus losers) returns are positive only during the first 12 monthsof portfolio formation. Taking a different tack, Chen and Hong (2002)and Jegadeesh and Titman (2002) decompose momentum profits, andargue that the profitability of momentum strategies is mostly due to timeseries dependence in realized returns rather than cross-sectional variationin expected returns.

Another explanation for the success of momentum strategies thathas been advanced in the literature is that market prices are drivenby irrational agents. Jegadeesh and Titman (1993) initially suggestedthat individual stock momentum might be driven by investor underreac-tion to firm-specific information. Furthermore, Chan, Jegadeesh, andLakonishok (1996) show that stock prices underreact to earnings newsand momentum profits concentrate on the subsequent earningsannouncements. In addition, several studies have introduced behavioralmodels that can explain the success of momentum strategies to at leastsome extent. Daniel, Hirshleifer, and Subrahmanyam (1998) develop atheory based on investor overconfidence and on changes in confidence

230 Shen, Szakmary, and Sharma

Journal of Futures Markets DOI: 10.1002/fut

resulting from biased self-attribution of investment outcomes. Their the-ory implies that investors overreact to private information signals andunderreact to public information signals. Barberis, Shlefier, and Vishny(1998) present a model based on psychological evidence and produce awide range of over- and underreaction values. Hong, Lim, and Stein(2000) find that momentum strategies work better among stocks withlow analyst coverage when holding firm size fixed. In addition, the effectof analyst coverage is greater for stocks that are past losers than it is forpast winners.

A final view suggested in several recent studies is that the momen-tum profits that have been documented in stocks are illusory. Korajczykand Sadka (2004) and Lesmond, Schill and Zhou (2004) both find thatonce the direct and indirect transactions costs associated with imple-menting momentum strategies are taken into account, it is doubtful thatthese strategies would have yielded abnormal returns in the stock marketprior to the recent decimalization of stock price quotes.

The purpose of this study is to conduct a comprehensive examina-tion of momentum strategies in commodity futures markets, using aresearch design that is typical of momentum studies applied to stockreturns. Because this is the first study that explicitly examines momen-tum strategies outside of equity markets—commodity futures differ fromstocks in important ways—this study makes a useful contribution to theliterature.

Regarding the differences between stocks and commodity futures,three considerations, in particular, stand out. First, the relatively lowtransactions costs in futures markets imply that momentum strategiescan be implemented at much lower cost than in the stock market.Numerous studies have estimated trading costs in futures markets; see,for example, Followill and Rodriguez (1991), Laux and Senchack (1992),Fleming, Ostdiek, and Whaley (1996), and Locke and Venkatesh (1997).All of these studies agree that effective bid-ask spreads in virtually allfutures are less than $40 per contract; in most cases, they are consider-ably less. The most accurate study to date is almost certainly that ofLocke and Venkatesh (1997). They obtained proprietary data from theChicago Mercantile Exchange (CME) and directly calculated averagecustomer transactions costs from the futures trade register for 12 differentcommodities over the period January 1, 1992, through June 30, 1992.Their results are partially reproduced in the second column of Table I.Based on the Locke and Venkatesh estimates of effective bid-askspreads, and assuming additional transactions costs of $10 per contractto reflect a typical discount broker commission that a representative

Momentum Strategies 231

Journal of Futures Markets DOI: 10.1002/fut

TABLE I

Estimated Round-Turn Transactions Costs in Futures Markets, January 1, 1992, through June 30, 1992

Effective Other Average Transactionsbid-ask transaction futures Contract Contract costs as % of

Commodity spreada costs price multiplier valueb contract valuec

Live Hogs 7.30 10 59.1180 400 $23,647 0.073Pork Bellies 10.32 10 34.7100 400 13,884 0.146Live Cattle 3.07 10 74.8270 400 29,931 0.044Lumber 15.92 10 236.6500 110 26,032 0.100Feeder Cattle 9.42 10 78.9580 500 39,479 0.049

aDirect estimates from Locke and Venkatesh (1997, Table II, p. 240).bEquals Average Futures Price � Contract Multiplier.cEquals (effective Bid-Ask Spread � Other Transactions Costs)�Contract Value.

investor might pay when trading multiple contracts, we calculate totalround-turn transactions costs as a percentage of contract value for thosefive CME commodities that are also included in our study. These esti-mates range from a low of 0.044% of notional contract value for LiveCattle futures to a high of 0.146% for Pork Bellies.

It is instructive to compare these estimates of transaction costs infutures to previously published estimates of round-turn transaction costsin stocks prior to the decimalization of stock quotes in early 2001. Thelatter range from 0.56% of transaction value for large institutionalinvestors buying S&P 500 stocks (Fleming et al., 1996) to greater than4% for trades in small capitalization/low price stocks (Bhardwaj & Brooks,1992; Stoll & Whaley, 1983). Given these transactions costs, it is hardlysurprising that Korajczyk and Sadka (2004) find that certain equallyweighted momentum strategies that look good on paper are difficult orimpossible to profitably implement in practice. Indeed, Lesmond et al.(2004) go further. They show that stocks used in momentum strategiesare disproportionately drawn from among stocks with high trading costs,and that it is doubtful that any such strategies are profitable in the stockmarket once transactions costs are fully and properly tallied.

An additional issue is that the implementation of momentum strate-gies requires a zero-cost trading strategy, whereby securities that are pre-dicted to earn relatively poor returns are sold short, with proceeds fromthese short sales used to finance the purchase of securities expected toearn superior returns. In futures markets, taking a short position (i.e.,contractually agreeing to deliver the underlying commodity at a futuredate) is as easy as taking a long position; there are no special restrictions

232 Shen, Szakmary, and Sharma

Journal of Futures Markets DOI: 10.1002/fut

on short positions, and transactions costs associated with them are iden-tical to those on long positions. In contrast, short-sellers in stock mar-kets generally do not receive use of (or interest on) the short-sale pro-ceeds, and the uptick rule prevents short sales whenever the latestrecorded transaction price is below the previously recorded price. Giventhat the majority of momentum strategy returns in the stock market areapparently generated by return continuation among poorly performingstocks, these short-sale constraints have a significant impact (Lesmondet al., 2004). Thus, in sum, it is clearly not an exaggeration to say thatthe ease of implementing momentum strategies, and transactions costsassociated with doing so, are orders of magnitude less in commodityfutures markets than in stock markets, and it is thus important to inves-tigate if momentum strategies work in commodities.

The third reason why examining momentum strategies in commodi-ty futures markets is likely to yield useful insights is that returns on com-modity futures are likely to have very different time-series properties.Unlike stocks, commodity futures prices are not driven by analystrecommendations or corporate earnings announcements. Moreover,commodities may have very dissimilar exposures to macroeconomicshocks. In the 1970s, for example, when inflation was high, stocks per-formed poorly, but the prices of most commodities rose by more thangeneral inflation would have warranted. On these grounds, also, webelieve that finding momentum profits in commodity futures couldtherefore point to broader, more general factors, as opposed to earningssurprises, institutional constraints, or other features unique to the stockmarket, as the ultimate causes of the momentum phenomenon.

The balance of the article is organized as follows. In the next section,the sample used, and the methodology for constructing unit value indicesis described. This is followed by a description of the basic momentum testsand results in the third section. Then the risk associated with momentumstrategies, as well as other tests designed to distinguish among alternativeexplanations for the causes of momentum profits in commodity futuresmarkets is the focus for the fourth section. A Conclusion is presented inthe last section of the article.

DATA AND CONSTRUCTION OF UNIT VALUE INDICES

From the Commodity Research Bureau (CRB) historical data CD, dailyclosing prices, trading volume, and open interest is extracted for 28 com-modity futures markets. In each case, the nearby contract is used, rolling

Momentum Strategies 233

Journal of Futures Markets DOI: 10.1002/fut

3This issue does not arise for trading volume or open interest, because the CRB reports total volumeand open interest across all contracts currently traded, i.e., volume and open interest are not specificto one expiration month.

over to the next contract on the last day of the month before contractexpiration. To avoid distortions caused by contract rollovers, we ensurethat percentage price changes are always calculated using data from thesame contract; thus, on rollover days prices are extracted for both thenearby and first-deferred contracts.3 Once a series of daily returns(adjusted for rollover) for each commodity have been obtained, we con-struct a daily unit value index from the daily returns.

For the purpose of constructing series used to measure formation-period returns for momentum strategies, we convert the data for each com-modity to a monthly frequency by sampling the daily unit value indexes onthe last trading day of each calendar month (although, when constructingmonthly volume and open interest measures, we average the daily volumeand open interest values within each calendar month). However, seriesused for the measurement of holding period returns are constructed differ-ently. This is primarily because some of the contracts included in thisstudy have price limits, whereby the maximum allowable price fluctuationper day is limited by the exchange. On days when price limits are reached,trading effectively shuts down, and traders must wait until the limits areno longer binding before trading activity resumes. Clearly, the implemen-tation of a momentum strategy requiring monthly rebalancing will beinhibited if some markets are closed due to price limits.

To ensure that the results we report are not an artifact of price limitsand that our strategies can actually be implemented, holding periodreturns are measured using a dataset from which price limit days areremoved. Specifically, we identify price limit days for each commodityfrom return and trading volume data, and we create a second monthlyunit value index for each commodity, which is sampled on the first day ofeach calendar month that is not a limit day. Thus, throughout the studywe use unadjusted monthly unit value indices (which are sampled on thelast day of each month) in the formation period to generate trading sig-nals, and the adjusted unit values to compute returns during the holdingperiod, which starts the following month. This procedure ensures thatthere is at least a 1-day lag between the generation of trading signals andthe taking of positions, and that both entry and exit trades are delayeduntil price limits are no longer binding.

The commodities in this study are traded on several differentexchanges, and have different start dates. We include all futures markets

234 Shen, Szakmary, and Sharma

Journal of Futures Markets DOI: 10.1002/fut

4In addition, we exclude the Commodity Research Bureau (CRB) Index futures; both because trad-ing volume in this market has been very thin and because, unlike all of the other markets includedin the study, the CRB index futures are cash-settled (i.e., the underlying “commodity” is a publishedindex that cannot be physically delivered).

carried on the CRB CD that have at least 10 years of available data; how-ever, we exclude financial futures (i.e., those on stock indices, bonds,interest rates, or currencies) because these are likely to have very differ-ent market dynamics and because we wish to focus this study on marketsthat have not been previously examined in a momentum context.4 Eightof the commodities included in our study begin on July 1, 1959. Ninebegin sometime in the 1960s, six in the 1970s, and the remaining fivecommodities start in 1980 or later. The last trading day for each com-modity is December 31, 2003. Table II lists the 28 sample commodities,along with their ticker symbols and start dates. We also provide in Table II,for each commodity futures market, summary statistics related tomean returns to long positions, standard deviation, skewness, excesskurtosis, minimum and maximum of returns, and, finally, average dailytrading volume broken down by time period (entire sample, prior toDecember 31, 1981, and after December 31, 1981). The trading volumefigures reported in Table II are not specific to the nearby contract, as thisinformation is not reported on the CRB CD. Rather, the figures are interms of the notional dollar value of contracts for all maturity months,defined as total number of contracts traded times nearby futures pricetimes contract multiplier.

The results in Table II are of most interest in revealing the large dif-ferences in volatility and trading volume among the 28 commodities.Although monthly return standard deviations range from 2.39% (fordomestic sugar) to 13.91% (Natural Gas), there are few obvious patternsor linkages between seemingly related markets. For example, the stan-dard deviation for world sugar is 5 times as high as for domestic sugar,the standard deviations for both silver and platinum are nearly twice ashigh as for gold, and hog futures (Lean Hogs, Pork Bellies) appear to beconsiderably more volatile than cattle futures. We should also note thatfew of these markets exhibit normality in their monthly returns.Although return skewness is positive in some markets and negative inothers, all of the return series have positive excess kurtosis, indicatingthat most of these markets, similar to other financial markets, have fat-tailed distributions. Indeed, Jarque–Bera (Jarque & Bera, 1987) tests(not reported) reject the normality assumption at the 5% level for allbut two of the commodities (the exceptions are lumber and natural gas,

TA

BL

E I

I

Sum

mar

y S

tati

stic

s

Exc

ess

retu

rns

on lo

ng p

osit

ions

Avg.

tra

ding

vol

ume

($ m

illi

ons)

Sym

bol

Com

mod

ity

Sta

rt D

ate

MS

DS

kew

ness

Kur

tosi

sM

inim

umM

axim

umO

vera

llP

re-1

981

Post

-198

1

BO

Soy

bean

Oil

07/0

1/19

590.

0030

0.08

610.

8953

3.32

62�

0.30

100.

4187

157.

2664

.94

251.

69C

-C

orn

07/0

1/19

59�

0.00

430.

0613

0.88

716.

2665

�0.

2104

0.42

2140

6.13

174.

8864

2.63

CC

Coc

oa07

/01/

1959

�0.

0007

0.08

840.

4539

1.46

21�

0.34

600.

4189

52.5

216

.17

89.7

0C

LC

rude

Oil

03/3

0/19

830.

0060

0.09

36�

0.05

802.

2742

�0.

3670

0.37

1020

92.2

9N

A20

92.2

9C

TC

otto

n07

/01/

1959

�0.

0009

0.05

79�

0.20

191.

5373

�0.

2418

0.19

6515

9.01

66.3

125

3.82

FC

Fee

der

Cat

tle11

/30/

1971

0.00

050.

0508

�0.

5813

3.28

39�

0.22

720.

1708

72.1

746

.24

84.1

6G

CG

old

12/3

1/19

74�

0.00

340.

0549

0.15

416.

6527

�0.

2771

0.31

8211

55.9

872

8.94

1293

.48

HG

Cop

per

Hig

h G

rade

11/0

1/19

69�

0.00

080.

0768

�0.

1722

4.38

49�

0.46

230.

3330

161.

9373

.18

211.

01H

OH

eatin

g O

il11

/14/

1978

0.00

460.

0912

0.36

562.

6833

�0.

3131

0.44

2161

5.24

64.1

669

4.57

HU

Gas

olin

e12

/03/

1984

0.00

990.

0976

0.52

702.

3467

�0.

2975

0.41

1868

9.74

NA

689.

74JO

Ora

nge

Juic

e02

/01/

1967

0.00

080.

0908

1.31

406.

7254

�0.

2909

0.56

8422

.30

8.53

31.6

3K

CC

offe

e08

/01/

1972

0.00

110.

1100

0.78

661.

8853

�0.

2701

0.45

1921

5.61

68.1

127

8.74

KW

Whe

at, N

o. 2

Win

ter

01/0

5/19

700.

0007

0.06

791.

0646

10.1

210

�0.

3476

0.51

3786

.72

46.0

310

8.91

LBLu

mbe

r10

/01/

1969

�0.

0049

0.08

520.

0638

0.58

06�

0.26

330.

3236

30.4

528

.75

31.4

0LC

Live

Cat

tle11

/30/

1964

0.00

370.

0529

�0.

2627

2.57

76�

0.22

630.

2159

337.

3120

1.04

443.

63LH

*Li

ve/L

ean

hogs

a02

/28/

1966

0.00

420.

0806

�0.

2217

1.37

97�

0.28

170.

3030

156.

8388

.21

206.

48N

GN

atur

al G

as04

/04/

1990

�0.

0001

0.13

910.

2529

0.01

90�

0.28

720.

3767

1450

.11

NA

1450

.11

O-

Oat

s07

/01/

1959

�0.

0059

0.07

981.

0868

8.85

95�

0.27

940.

6345

7.56

3.78

11.4

1P

AP

alla

dium

01/0

3/19

77�

0.00

030.

1088

0.69

549.

2693

�0.

4988

0.73

777.

242.

138.

40P

BP

ork

Bel

lies

11/1

5/19

64�

0.00

290.

1079

�0.

2019

2.17

82�

0.58

750.

4106

101.

3010

9.79

94.6

8P

LP

latin

um03

/04/

1968

�0.

0041

0.09

42�

3.06

8229

.734

7�

0.94

970.

3814

47.2

515

.27

67.3

6R

RR

ough

Ric

e08

/20/

1986

�0.

0091

0.08

670.

8889

4.63

77�

0.33

470.

4319

6.71

NA

6.71

S-

Soy

bean

s07

/01/

1959

0.00

010.

0739

0.34

497.

8908

�0.

4283

0.46

7210

38.8

758

1.88

1391

.99

SB

Sug

ar #

11/W

orld

01/0

4/19

61�

0.00

280.

1270

0.31

712.

0659

�0.

5236

0.49

2212

7.40

57.7

319

3.91

SE

Sug

ar #

14/D

om.

07/0

7/19

87�

0.00

090.

0239

0.23

523.

5606

�0.

1018

0.09

3012

.85

NA

12.8

5S

IS

ilver

03/1

2/19

67�

0.00

340.

1067

�1.

7642

39.5

975

�1.

1570

0.78

3440

0.18

211.

9752

7.07

SM

Soy

bean

Mea

l07

/01/

1959

0.00

320.

0844

0.16

378.

1150

�0.

5057

0.48

9621

9.77

67.6

737

5.33

W-

Whe

at, N

o. 2

Sof

t07

/01/

1959

�0.

0038

0.06

681.

1137

11.1

672

�0.

3406

0.56

1719

8.76

112.

1628

7.33

Not

e.D

olla

r tr

adin

g vo

lum

e is

the

notio

nal v

alue

of c

ontr

acts

for

all m

atur

ity m

onth

s tr

aded

on

an a

vera

ge d

ay, d

efine

d as

tota

l tra

ding

vol

ume

�fu

ture

s pr

ice

�co

ntra

ct m

ultip

lier.

a We

switc

h to

Lea

n H

ogs

in p

lace

of L

ive

Hog

s on

Nov

. 1, 1

996.

236 Shen, Szakmary, and Sharma

Journal of Futures Markets DOI: 10.1002/fut

5To facilitate return calculations over longer horizons and for consistency with other studies, wedefine the monthly return as ln(UVt�UVt�1), where UV is the unit value index of a particular futurescontract at the end of month t, constructed as previously described. Given this log definition of thereturn, it is possible to obtain a return that is less than �100%, as is the case for the minimum valuefor silver futures reported in Table II.6Margins in futures markets can be posted using Treasury Bills. Consequently, the “return” as wecalculate it is an excess return that would be earned by an investor who uses no leverage (i.e., postsT-bills with a market value equal to the full contract value of the futures contract) and takes a longposition.

the two with the lowest excess kurtosis).5 In terms of average tradingvolume, there is an even larger degree of variation among these mar-kets, ranging from over 2,092 million dollars per day in crude oil allthe way down to 6.71 million dollars daily in rough rice. The large dif-ferences in trading volume across markets underscore the need forrobustness checks in which strategies are implemented with differentsubsets of the 28 commodities. If one considers market impact costs,it is not clear that trading volume in some of these markets is sufficientto profitably implement in practice some strategies that look goodon paper.

BASIC MOMENTUM TESTS AND RESULTS

We conduct basic momentum tests as follows. At the end of eachcalendar month, from July 1959 to December 2003, we rank all eligi-ble commodities independently on the basis of past holding periodreturns, where the return for each commodity in each month is mea-sured as the log percentage change in the unit value index relative tothe reference month.6 We form 10 different formation periods J, whereJ ranges from 1 month to 60 months. Based on each commodity’s pastreturns, we then group it into one of three portfolios (P1 to P3), whereP1 consists of past “winners” (top one third of commodities, based onformation-period return) and P3 of past “losers” (bottom one thirdof commodities). We then measure K-period holding period returnsfor each commodity using a different unit value series, which is sam-pled on the first trading day of each calendar month that is not a pricelimit-impacted day.

To test the significance of momentum profits in each portfolio,we use t-statistics that are asymptotically distributed as N(0, 1), under thenull hypothesis that the true profits are zero. Because in general we useoverlapping data, we correct our standard errors for heteroskedasticity

Momentum Strategies 237

Journal of Futures Markets DOI: 10.1002/fut

7The use of unadjusted average P1 � P3 returns, along with Newey and West standard errors toassess statistical significance, has been criticized in some studies on the grounds that there may be adownward bias in small samples in computing the P1 � P3 returns, and because statistical infer-ences may be invalid if the returns are not normally distributed. Mostly, however, these issues pertainto assessing the profitability of long-horizon contrarian strategies, which are not the main focus ofour study. Nevertheless, following Richards (1997), we conducted a bootstrap experiment on a sam-ple of 18 commodities for the 1982–2003 period. Briefly, the procedure consisted of a temporallyrandom resampling of the monthly logarithmic returns in our dataset 1000 times, and then compar-ing the mean returns resulting from the momentum strategies applied to the actual data to thoseobtained using the randomized data. Heeding the warning of Jegadeesh and Titman (2002), we con-ducted each resampling without replacement, and we preserved the contemporaneous relations inthe monthly data across commodities. The results of this exercise (not reported) revealed no evi-dence of substantial bias in calculating mean P1 � P3 returns at any horizon, and gave no indicationthat the inferences based on Newey and West standard errors were misleading.

and autocorrelation using the Newey and West (1987) adjustment. Inevery case, the number of lags used in the adjustment equals the numberof months of overlap.7

To provide an initial indication of the robustness of returns tomomentum strategies, their performance is examined in two separatetime periods, the pre-1981 (July 1959–December 1981) and post-1981(January 1982–December 2003) subperiods of approximately equallength. The year 1981 represents a convenient break point between aperiod of generally rising inflation (1960–1981) and falling inflation(1982–2003). Further, Irwin and Yoshimaru (1999) argue that invest-ments in managed futures funds (which combine investors’ moneys forthe purpose of speculating in futures and options markets) have explodedsince the early 1980s, growing from $200 million in 1980 to $19 billionin 1994, and that these funds tend to engage in positive feedback tradingstrategies. Fung and Hsieh (1997) also show that trend-following strate-gies dominate among CTA (Commodity Trading Advisor) funds. If moretraders are pursuing trend-following strategies, we might intuitivelyexpect momentum profits to be lower in our second subperiod.

To begin the analysis, we first implement strategies for which thelength of the formation period and the future holding period is identical,i.e., J � K. Similar in spirit to Jegadeesh and Titman’s (1993, 2001)approach, we divide our sample commodities into three portfolios basedon their past returns, and P1 � P3 is the difference in realized profitsbetween winner and loser portfolios, i.e., profits accruing to a strategy oftaking long positions in past relative winners and short positions in pastlosers. Table III summarizes average realized profits for momentumstrategies implemented with all commodities in the entire sample period,as well as broken down by pre- versus post-1981. Table III also reports

TA

BL

E I

II

Ave

rage

Mom

entu

m P

rofit

s fo

r A

ll S

ampl

e C

omm

odit

ies

Pane

l A: E

ntir

e sa

mpl

e pe

riod

Pane

l B: P

re-1

981

peri

odPa

nel C

: Pos

t-19

81 p

erio

d

J/K

P1

P2

P3

P1

�P

3P

1P

2P

3P

1�

P3

P1

P2

P3

P1

�P

3

1 m

onth

0.00

68�

0.00

16�

0.00

510.

0118

0.00

81�

0.00

03�

0.00

310.

0113

0.00

54�

0.00

28�

0.00

700.

0124

(3.2

268)

**(�

.867

8)(�

2.59

68)*

*(5

.160

2)**

(2.4

58)*

(�.1

01)

(�1.

0094

)(3

.451

1)**

(2.1

011)

*(�

1.49

46)

(�2.

974)

**(3

.853

2)**

2 m

onth

s0.

0097

0.00

01�

0.01

070.

0204

0.01

640.

0018

�0.

0102

0.02

650.

0031

�0.

0016

�0.

0112

0.01

43(2

.482

6)*

(.02

27)

(�2.

8491

)**

(5.2

038)

**(2

.490

7)*

(.38

88)

(�1.

6678

)(4

.507

9)**

(.75

5)(�

.541

1)(�

2.57

89)*

(2.8

192)

**

3 m

onth

s0.

0142

�0.

0029

�0.

0131

0.02

730.

0217

0.00

56�

0.01

470.

0364

0.00

71�

0.01

10�

0.01

120.

0183

(2.4

56)*

(�.6

532)

(�2.

5292

)*(4

.874

)**

(2.1

969)

*(.

7496

)(�

1.78

19)

(4.1

992)

**(1

.221

7)(�

2.34

74)*

(�1.

7869

)(2

.638

2)**

6 m

onth

s0.

0158

0.00

39�

0.02

450.

0403

0.03

330.

0099

�0.

0161

0.04

94�

0.00

090.

0001

�0.

0293

0.02

83(1

.450

9)(.

4127

)(�

2.23

47)*

(3.8

46)*

*(1

.915

6)(.

6268

)(�

.929

8)(3

.155

9)**

(�.0

742)

(.00

84)

(�2.

2705

)*(2

.072

9)*

9 m

onth

s0.

0171

0.01

14�

0.03

470.

0519

0.04

410.

0317

�0.

0243

0.06

84�

0.00

66�

0.00

37�

0.03

660.

0301

(.95

49)

(.74

91)

(�2.

1127

)*(3

.336

8)**

(1.5

126)

(1.2

376)

(�.9

699)

(3.2

195)

**(�

.328

4)(�

.237

9)(�

1.87

06)

(1.3

689)

12 m

onth

s0.

0014

0.01

14�

0.02

240.

0238

0.03

480.

0556

�0.

0136

0.04

84�

0.02

36�

0.02

33�

0.01

75�

0.00

62(.

0578

)(.

5068

)(�

.997

9)(1

.159

2)(.

8565

)(1

.534

3)(�

.394

2)(1

.553

9)(�

.941

1)(�

1.04

17)

(�.6

606)

(�.2

313)

24 m

onth

s�

0.05

290.

0082

0.01

25�

0.06

540.

0178

0.11

660.

0875

�0.

0698

�0.

0609

�0.

0571

�0.

0371

�0.

0238

(�.9

876)

(.17

89)

(.26

77)

(�1.

5311

)(.

2067

)(1

.794

3)(1

.271

2)(�

1.30

46)

(�1.

8232

)(�

1.29

32)

(�.6

393)

(�.4

091)

36 m

onth

s�

0.04

03�

0.00

530.

0117

�0.

0520

0.10

390.

1283

0.21

32�

0.10

93�

0.07

29�

0.04

92�

0.11

120.

0383

(�.5

191)

(�.0

813)

(.15

15)

(�.9

362)

(.82

4)(1

.364

6)(2

.104

6)*

(�1.

3009

)(�

2.16

63)*

(�.8

719)

(�1.

5063

)(.

5654

)

48 m

onth

s0.

0138

�0.

0291

�0.

0048

0.01

850.

2907

0.12

740.

3326

�0.

0419

�0.

0920

�0.

0408

�0.

1555

0.06

35(.

1276

)(�

.304

2)(�

.039

8)(.

2727

)(1

.933

5)(.

7862

)(2

.155

6)*

(�.3

013)

(�1.

7542

)(�

.771

3)(�

2.62

92)*

*(.

8749

)

60 m

onth

s0.

0272

�0.

0183

0.01

210.

0151

0.45

040.

2542

0.53

49�

0.08

46�

0.12

55�

0.03

71�

0.18

330.

0578

(.17

47)

(�.1

444)

(.06

76)

(.17

71)

(2.1

159)

*(1

.420

9)(2

.729

8)**

(�.5

121)

(�1.

8953

)(�

.869

3)(�

4.05

69)*

*(.

7107

)

Not

e.T

he ta

ble

prov

ides

mea

ns o

f hol

ding

per

iod

(K)

retu

rns

for

vario

us p

ortfo

lios.

The

P1

port

folio

s co

ntai

n co

mm

oditi

es r

anke

d in

the

top

third

, acr

oss

all 2

8 co

mm

oditi

es, i

n te

rms

offo

rmat

ion

perio

d (J

) re

turn

, the

P2

port

folio

s co

mm

oditi

es r

anke

d in

the

mid

dle

third

, and

the

P3

port

folio

s co

mm

oditi

es r

anke

d in

the

botto

m th

ird. F

igur

es in

par

enth

eses

are

t-st

atis

tics

base

d on

New

ey a

nd W

est (

1987

) st

anda

rd e

rror

s.

*,**

Sig

nific

ance

at t

he 5

% a

nd 1

% le

vels

, res

pect

ivel

y.

Momentum Strategies 239

Journal of Futures Markets DOI: 10.1002/fut

8A negative return to a momentum strategy that buys past winners and sells past losers naturallyimplies a corresponding positive return to a contrarian strategy that buys past losers and sells pastwinners.

the t-statistics in parentheses for testing the statistical significance of theaverage profits (losses).

Panel A in Table III contains the realized profits for our entire sam-ple period. These results show that momentum strategies with forma-tion and holding periods of up to 9 months earn significant positiveabnormal returns. If we divide the total holding period returns bythe length of the holding period, then it appears that the intrinsicprofitability is highest at the shortest horizons, e.g., 1–2 months. Thet-statistics are also greatest at these horizons, but they do remain highlysignificant out through 9 months. These findings, both in terms of themagnitude of momentum profits and their significance, are similar towhat have been reported in equity markets by Jegadeesh and Titmanand others, although the horizon over which momentum strategies areprofitable appears to be slightly shorter than when momentum strategiesare implemented with individual stocks. In this respect, our findingsmore closely parallel Chan, Hameed, and Tong’s (2000) study ofmomentum effects in international stock market indexes. We should alsonote that, in contrast to findings in equity markets, our results show nofirm evidence of long-horizon contrarian profits. Although P1 � P3returns do tend to be negative at 24- and 36-month horizons, indicatingthat contrarian strategies are profitable, these findings are not statisticallysignificant.8

Panels B and C in Table III report profits from two subsample peri-ods: pre- and post-1981. Not surprisingly, in light of the fact that the firstperiod was characterized by rising inflation and commodity prices, andthe second period by the opposite effects, we see that in panel B, theprofits in general (for all portfolios and horizons) tend to be higher thanin panel C. Generally, at shorter horizons during the pre-1981 period,the past winner portfolios post significantly positive subsequent returnswhile the past losers show only small losses. Conversely, post-1981, thepast winners earn only small positive returns, while the past losers showsignificant losses in the postformation period. However, momentumstrategies that simultaneously take long positions in past relative winnersand short positions in past losers (P1 � P3) are significantly profitable inboth periods, although the profitability appears lower, and slightly lesssignificant, post-1981. Another difference appears to be that, in the pre-1981 period, the significance of the momentum profits extends out to

240 Shen, Szakmary, and Sharma

Journal of Futures Markets DOI: 10.1002/fut

9Consistent with momentum studies in the stock market, the past winners and losers are defined inrelative rather than absolute terms; thus, in Table III, the one third of commodities that had thehighest returns over some past formation period are grouped into the P1 portfolio (i.e., the winnerscategory) even if some (or all) of these commodities had negative returns. We also implementedmomentum strategies using an alternate procedure whereby, to be placed in the P1 (P3) portfolio, acommodity had to rank in the top (bottom) one third during the formation period and had to have apositive (negative) FP return in an absolute sense. Although this alternate strategy generally result-ed in slightly higher P1 � P3 mean returns for formation and holding periods of 9 months or less,the results (not reported) are not materially different from those in Table III.

formation and holding periods of 9 months, whereas post-1981 the sig-nificance ends after 6 months.9

We next examine whether momentum profits persist when thestrategies are implemented only with various subsets of the 28 commodi-ties used in Table III. Aggregate subset results, i.e., results for winner� loser (P1 � P3) portfolios only, are reported in Table IV. We examinethe following subsets of commodities. First, we implement the momen-tum strategies across 25 commodities from which full carry markets havebeen excluded (EFC). In the three full carry markets that are excluded(all precious metals), the underlying commodities are easily and cheaplystorable, and the futures price approximately equals the spot price multi-plied by one plus the periodic interest rate. In the remaining non-fullcarry markets (i.e., energy, foodstuffs, grains/oilseeds, and livestock/meats), storing and delivering the underlying commodity are not neces-sarily cheap, supply and/or demand are seasonal, and the futures pricecan fluctuate much more freely relative to the spot price. Next, we exam-ine momentum strategies across 20 markets with relatively high tradingvolume (HV), where the momentum strategies are much more likely tobe implementable on a large scale in practice. This subset excludes theeight commodities with the lowest overall trading volumes reported inTable II, i.e., cocoa, orange juice, lumber, oats, palladium, platinum,rough rice, and domestic sugar. With these exclusions, each remainingcommodity has average daily trading volume of at least 72.17 milliondollars overall, $46.03 million pre-1981, and $84.16 million post-1981.The last subset we examine (HVEFC) represents the intersection of theEFC and HV subsets, i.e., a group of 18 commodities that exclude bothfull carry markets and those with low trading volume.

The results in Table IV indicate that the profitability of momentumstrategies remains significant when these strategies are implementedwith only subsets of commodities, but the results are sensitive to theparticular sets with which they are implemented. Comparing the resultsin panel A of Table IV with those in panel A of Table III, the only note-worthy difference appears to be that, for the HV and HVEFC subsets,

TA

BL

E I

V

Ave

rage

Agg

rega

te P

rofit

s of

Mom

entu

m S

trat

egie

s Im

plem

ente

d W

ith

Sub

grou

ps o

f C

omm

odit

ies

Pane

l A: E

ntir

e sa

mpl

e pe

riod

Pane

l B: P

re-1

981

peri

odPa

nel C

: Pos

t-19

81 p

erio

d

J/K

EF

CH

VH

VE

FC

EF

CH

VH

VE

FC

EF

CH

VH

VE

FC

1 m

onth

0.01

170.

0117

0.01

140.

0109

0.01

260.

0120

0.01

250.

0108

0.01

08(4

.904

4)**

(4.4

311)

**(4

.121

9)**

(3.1

657)

**(3

.302

8)**

(3.1

231)

**(3

.790

9)**

(2.9

569)

**(2

.710

5)**

2 m

onth

s0.

0216

0.02

000.

0216

0.02

910.

0316

0.03

390.

0143

0.00

850.

0095

(5.4

660)

**(4

.383

5)**

(4.5

766)

**(5

.045

3)**

(4.4

849)

**(4

.803

6)**

(2.7

109)

**(1

.530

0)(1

.577

4)

3 m

onth

s0.

0263

0.02

640.

0234

0.03

630.

0461

0.04

290.

0165

0.00

670.

0040

(4.5

373)

**(3

.926

7)**

(3.3

447)

**(4

.185

6)**

(4.3

351)

**(4

.154

8)**

(2.1

771)

*(0

.898

6)(0

.454

0)

6 m

onth

s0.

0412

0.03

730.

0347

0.05

190.

0577

0.05

540.

0275

0.01

470.

0118

(3.7

896)

**(3

.161

9)**

(2.8

096)

**(3

.132

1)**

(3.2

253)

**(3

.007

9)**

(2.0

201)

*(1

.006

7)(0

.756

1)

9 m

onth

s0.

0434

0.03

220.

0262

0.06

300.

0441

0.04

050.

0198

0.01

450.

0082

(2.7

118)

**(1

.703

6)(1

.335

4)(2

.838

7)**

(1.4

917)

(1.3

444)

(0.8

930)

(0.6

327)

(0.3

367)

12 m

onth

s0.

0114

�0.

0117

�0.

0183

0.03

66�

0.00

49�

0.00

95�

0.01

77�

0.02

30�

0.02

82(0

.546

1)(�

0.49

16)

(�0.

7296

)(1

.136

7)(�

0.12

46)

(�0.

2376

)(�

0.67

05)

(�0.

8189

)(�

0.92

34)

24 m

onth

s�

0.09

11�

0.10

36�

0.11

99�

0.11

08�

0.15

69�

0.18

39�

0.03

77�

0.01

86�

0.02

81(�

2.08

16)*

(�1.

7389

)(�

2.05

40)*

(�1.

8503

)(�

1.54

72)

(�1.

8841

)(�

0.66

28)

(�0.

2948

)(�

0.44

25)

36 m

onth

s�

0.06

48�

0.05

61�

0.06

28�

0.12

19�

0.12

63�

0.12

430.

0153

0.04

320.

0197

(�1.

1431

)(�

0.77

56)

(�0.

8263

)(�

1.39

94)

(�1.

0179

)(�

0.92

72)

(0.2

100)

(0.5

055)

(0.2

132)

48 m

onth

s0.

0262

0.05

360.

0491

�0.

0296

0.09

850.

0972

0.04

480.

0060

�0.

0360

(0.3

659)

(0.5

799)

(0.4

890)

(�0.

2211

)(0

.535

8)(0

.524

4)(0

.522

5)(0

.055

5)(�

0.31

01)

60 m

onth

s0.

0664

0.06

600.

0695

�0.

0612

0.08

120.

1245

0.08

550.

0035

�0.

0508

(0.6

557)

(0.6

111)

(0.5

911)

(�0.

3889

)(0

.456

1)(0

.805

6)(0

.911

4)(0

.023

1)(�

0.32

90)

Not

e.T

he t

able

pro

vide

s m

eans

of

hold

ing

perio

d (K

) re

turn

s fo

r w

inne

r �

lose

r (P

1�

P3)

por

tfolio

s fo

r m

omen

tum

str

ateg

ies

impl

emen

ted

with

var

ious

sub

grou

ps o

f co

mm

odity

futu

res.

The

EF

C,

HV,

and

HV

EF

C g

roup

ings

rep

rese

nt,

resp

ectiv

ely,

25

com

mod

ities

tha

t ex

clud

e fu

ll ca

rry

mar

kets

, 20

com

mod

ities

with

rel

ativ

ely

high

tra

ding

vol

ume,

and

18

high

-vo

lum

e co

mm

oditi

es e

xclu

ding

full

carr

y m

arke

ts. F

igur

es in

par

enth

eses

are

t-st

atis

tics

base

d on

New

ey a

nd W

est (

1987

) st

anda

rd e

rror

s.

*,**

Sig

nific

ance

at t

he 5

% a

nd 1

% le

vels

, res

pect

ivel

y.

242 Shen, Szakmary, and Sharma

Journal of Futures Markets DOI: 10.1002/fut

the time horizon for significant profitability of momentum strategiesis limited to 6 months or less. However, when focusing on the post-1981 period in panel C of the two tables, we find momentum strate-gies that are restricted to high volume commodities earn lower returnseven at short horizons. At 2-, 3-, and 6-month horizons, momentumprofits are no longer significant, post-1981, for the HV and HVEFCsubsets, while for all commodities and the EFC subset they remain sig-nificant at these horizons. At the 1-month horizon, however, momen-tum profits remain significant (at the 1% level) for every subset weexamine in the post-1981 period. In general, the results in Table IVindicate that the key distinction among commodities is trading volumerather than full carry status. Consequently, throughout the remainderof the study, our robustness checks concentrate on ascertaining howresults differ between strategies that are implemented with the full setof 28 commodities and those that are implemented only with theHV subset.

The momentum tests conducted in Tables III and IV are similar inspirit to those that have been conducted in stocks, and demonstrate thatsimilar strategies work in commodity futures markets. However, if wewere to tailor a strategy to exploit momentum in commodity futures effi-ciently, it would almost certainly employ a shorter holding period thanmomentum strategies applied to stocks. In the latter environment, givenrelatively high transactions costs and longer persistence in returns, itmakes sense to limit portfolio reformation to once every 6–12 months. Incontrast, in commodity futures, most markets have monthly or bimonthlyexpiration cycles and only the nearby contracts tend to be liquid. If con-tracts must be rolled over anyway (and transactions costs incurred) every1–2 months, it makes little sense to limit reformation of positions toonce every 6–12 months. Consequently, to provide a better indication ofthe profit potential of momentum strategies in commodities, we nextfocus on 1-month holding periods. Table V reports mean returns andNewey and West t-statistics associated with momentum strategies inwhich the formation period varies from 1 to 12 months, but where theportfolios are held for only one month after their formation. As before,each month the P1 portfolios contain commodities in which a long posi-tion is taken (i.e., in the top third in terms of formation-period return),the P2 portfolios contain those commodities in which no position istaken, and the P3 portfolios contain those commodities in which a shortposition is taken (i.e., those in the bottom third in terms of formation-period return). We report results for all three portfolios as well as theP1 � P3 momentum portfolio, for the entire sample, and the pre- and

TA

BL

E V

Ave

rage

Pro

fits

of M

omen

tum

Str

ateg

ies,

One

-Mon

th H

oldi

ng P

erio

ds

Form

atio

nPa

nel A

: Ent

ire

sam

ple

peri

odPa

nel B

: Pre

-198

1 pe

riod

Pane

l C: P

ost-

1981

per

iod

peri

odP

1P

2P

3P

1�

P3

P1

P2

P3

P1

�P

3P

1P

2P

3P

1 �

P3

Mom

entu

m s

trat

egie

s im

plem

ente

d w

ith

all

28

com

mod

itie

s

1 m

onth

0.00

68�

0.00

16�

0.00

510.

0118

0.00

81�

0.00

03�

0.00

310.

0113

0.00

54�

0.00

28�

0.00

700.

0124

(3.2

268)

**(�

.867

8)(�

2.59

68)*

*(5

.160

2)**

(2.4

58)*

(�.1

01)

(�1.

0094

)(3

.451

1)**

(2.1

011)

*(�

1.49

46)

(�2.

974)

**(3

.853

2)**

2 m

onth

s0.

0070

�0.

0001

�0.

0070

0.01

390.

0112

�0.

0007

�0.

0064

0.01

760.

0027

0.00

04�

0.00

750.

0102

(3.1

521)

**(�

.088

9)(�

3.61

58)*

*(5

.964

7)**

(3.1

071)

**(�

.256

6)(�

2.18

46)*

(5.2

564)

**(1

.067

3)(.

2396

)(�

3.01

68)*

*(3

.156

1)**

3 m

onth

s0.

0078

�0.

0026

�0.

0057

0.01

350.

0093

�0.

0004

�0.

0054

0.01

470.

0063

�0.

0050

�0.

0060

0.01

23(3

.636

6)**

(�1.

5821

)(�

2.99

80)*

*(5

.910

5)**

(2.5

657)

*(�

.132

)(�

1.83

24)

(4.1

474)

**(2

.755

4)**

(�2.

6026

)**

(�2.

5027

)*(4

.274

9)**

6 m

onth

s0.

0039

0.00

21�

0.00

660.

0105

0.00

820.

0020

�0.

0067

0.01

49�

0.00

030.

0023

�0.

0064

0.00

61(1

.779

6)(1

.320

8)(�

3.40

69)*

*(4

.631

8)**

(2.1

878)

*(.

7766

)(�

2.19

87)*

(4.1

958)

**(�

.129

0)(1

.174

6)(�

2.72

6)**

(2.1

901)

*

9 m

onth

s0.

0043

0.00

21�

0.00

670.

0110

0.00

710.

0023

�0.

0057

0.01

280.

0016

0.00

18�

0.00

770.

0093

(1.9

367)

(1.2

056)

(�3.

4965

)**

(4.6

231)

**(1

.885

6)(.

8032

)(�

1.90

45)

(3.5

291)

**(.

6630

)(.

9747

)(�

3.18

19)*

*(2

.990

9)**

12 m

onth

s0.

0053

0.00

12�

0.00

670.

0121

0.00

730.

0035

�0.

0065

0.01

380.

0035

�0.

0011

�0.

0069

0.01

03(2

.357

5)*

(.69

45)

(�3.

4440

)**

(5.1

661)

**(1

.891

1)(1

.258

)(�

2.10

64)*

(3.9

289)

**(1

.419

6)(�

.617

3)(�

2.88

85)*

*(3

.361

2)**

Mom

entu

m s

trat

egie

s im

plem

ente

d w

ith

20 h

igh-

vol

ume

com

mod

itie

s

1 m

onth

0.00

730.

0004

�0.

0044

0.01

170.

0089

0.00

26�

0.00

370.

0126

0.00

58�

0.00

17�

0.00

500.

0108

(3.0

959)

**(.

2202

)(�

2.04

35)*

(4.4

311)

**(2

.324

1)*

(.77

72)

(�1.

1231

)(3

.302

8)**

(2.0

733)

*(�

.776

6)(�

1.87

05)

(2.9

569)

**

2 m

onth

s0.

0088

0.00

01�

0.00

530.

0141

0.01

440.

0001

�0.

0067

0.02

110.

0031

0.00

01�

0.00

400.

0070

(3.4

885)

**(.

0418

)(�

2.50

24)*

(5.1

966)

**(3

.488

5)**

(.01

65)

(�2.

0498

)*(5

.318

4)**

(1.0

921)

(.04

92)

(�1.

4501

)(1

.926

9)

3 m

onth

s0.

0085

�0.

0007

�0.

0050

0.01

350.

0121

0.00

19�

0.00

690.

0189

0.00

50�

0.00

33�

0.00

300.

0080

(3.3

673)

**(�

.376

8)(�

2.34

58)*

(4.9

054)

**(2

.827

)**

(.62

48)

(�2.

0812

)*(4

.454

8)**

(1.8

420)

(�1.

4872

)(�

1.15

43)

(2.3

188)

*

6 m

onth

s0.

0049

0.00

31�

0.00

490.

0098

0.00

990.

0038

�0.

0066

0.01

65�

0.00

010.

0024

�0.

0031

0.00

30(1

.937

3)(1

.713

4)(�

2.24

39)*

(3.6

246)

**(2

.280

1)*

(1.3

26)

(�1.

9785

)*(4

.022

1)**

(�.0

412)

(1.0

868)

(�1.

1322

)(.

8807

)

9 m

onth

s0.

0049

0.00

27�

0.00

410.

0091

0.00

930.

0031

�0.

0048

0.01

410.

0007

0.00

24�

0.00

340.

0041

(1.9

21)

(1.4

579)

(�1.

942)

(3.2

947)

**(2

.101

5)*

(.99

44)

(�1.

5277

)(3

.413

5)**

(.24

75)

(1.1

276)

(�1.

2075

)(1

.132

5)

12 m

onth

s0.

0064

0.00

08�

0.00

390.

0103

0.00

810.

0039

�0.

0043

0.01

240.

0047

�0.

0021

�0.

0035

0.00

82(2

.449

4)*

(.46

68)

(�1.

8386

)(3

.900

3)**

(1.8

087)

(1.2

807)

(�1.

3045

)(3

.089

6)**

(1.7

36)

(�1.

0505

)(�

1.30

53)

(2.3

957)

*

Not

e.F

igur

esin

par

enth

eses

are

t-st

atis

tics

base

d on

New

ey a

nd W

est (

1987

) st

anda

rd e

rror

s.

*,**

Sig

nific

ance

at t

he 5

% a

nd 1

% le

vels

, res

pect

ivel

y.

244 Shen, Szakmary, and Sharma

Journal of Futures Markets DOI: 10.1002/fut

10In a recent study, George and Hwang (2004) estimate returns to a momentum-like strategy inwhich the formation-period criterion is a security’s nearness to its 52-week high, and claim that thiscriterion dominates and improves upon the forecast power of past returns for future returns. Weapplied their trading rule to the commodity data used in this study, and found that the profitabilityof this nearness to the 52-week high strategy for forecasting 1-month returns was similar to, thoughslightly below, the profitability of traditional momentum strategies.11Jegadeesh and Titman (1993) report that momentum profits in stocks are seasonal. In January, thestrategies earn significant negative returns, but mean profitability is positive in all other months.Consequently, we also tested for monthly seasonality in aggregate returns to 1-, 2-, 3- and 6-monthformation-period momentum strategies. We found no evidence of monthly seasonality in the returnsgenerated by these strategies in commodity futures markets.

post-1981 periods. We also segregate our results by whether the momen-tum strategies are implemented with all 28 commodities, or with a subsetof 20 high-volume commodities.

For the full 1959–2003 sample period in panel A, the results inTable V strongly indicate that, for any length formation period used tomeasure past returns, momentum strategies are quite profitable, earningexcess returns of about 1% per month or slightly more when used with-out leverage. Regardless of whether the strategies are implemented withall commodities or only within the HV subset, performance tends to beslightly better for the shorter (1–3 month) formation periods, but forboth sets and all formation periods, the P1 � P3 returns are significantlypositive at the 1% level. We observe similar results for the pre-1981period in panel B, but in the post-1981 period (panel C), we observesome differences in the results depending on whether or not we limitimplementation of momentum strategies to the HV subset. For allformation-period lengths post-1981, momentum profits are lower (andless significant) if we limit implementation to the HV subset wheretransactions costs are likely to be lower. In the case of shorter 1–3 monthformation periods, the momentum portfolios have monthly excessreturns in the 1.02–1.24% range when implemented with all commodi-ties, but these drop to 0.70–1.08% when restricted to HV commodities,and in a few cases the momentum profits are no longer significant.10,11

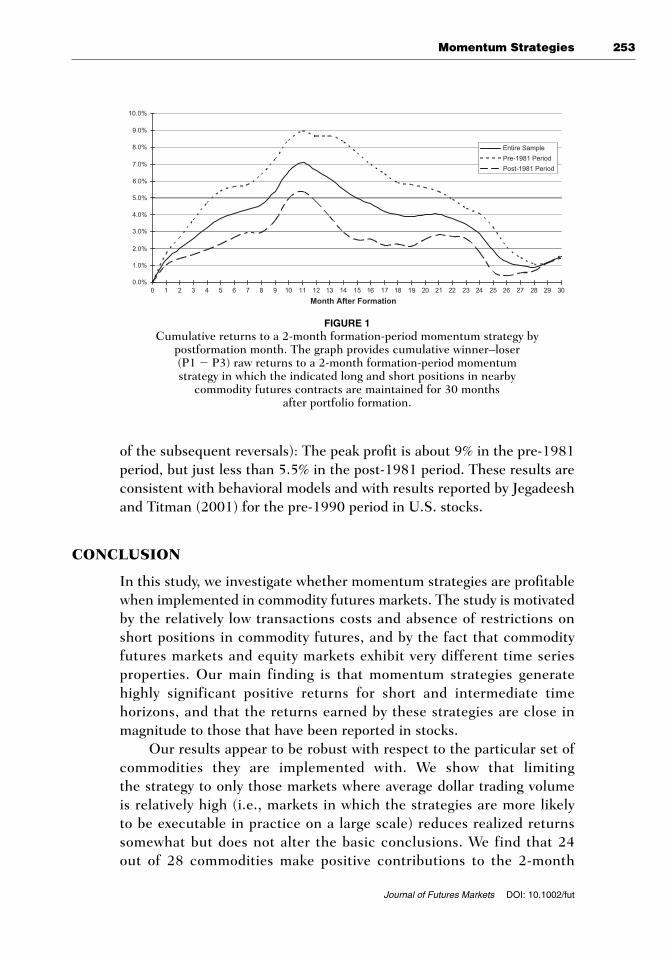

DISTINGUISHING AMONG ALTERNATIVEEXPLANATIONS FOR THE PROFITABILITYOF MOMENTUM STRATEGIES

Thus far we have examined the mean returns accruing to momentumstrategies, and we have demonstrated that the profitability of thesestrategies is fairly robust over time and to the set of commodities withwhich they are implemented. We next explore whether the momentum

Momentum Strategies 245

Journal of Futures Markets DOI: 10.1002/fut

12We chose the 2-month formation-period momentum strategy for further analysis because it wasthe best-performing specification in the pre-1981 period. On this basis, one can interpret the post-1981 results from this specification as an out-of-sample test, somewhat ameliorating data miningconcerns.

profits can be attributed to risk premia, or if they are better explained asarising from behavioral causes. Recall that the momentum strategies wehave implemented involve simultaneously taking long positions in com-modity futures that have had relatively high returns (to long positions)over some previous interval, and short positions in those markets thathave had relatively low returns. We therefore begin our risk assessmentby comparing the total risk (as measured by the standard deviation andhigher moments of the return distribution) associated with the returns torepresentative momentum strategies to those of a “control” strategy inwhich, each month, equal numbers of commodities are assigned to longand short portfolios randomly, rather than on the basis of their pastreturns. To obtain an empirical distribution of mean returns, return stan-dard deviations and higher moments, we construct the control portfolios1000 times, and compare the moments of momentum strategy returns tothe entire distribution of control portfolios obtained using the 1000replications.

The moments of P1 � P3 1-month holding period returns resultingfrom 2-month formation-period momentum strategies are reported inpanel A of Table VI. As in Table V, we report results for the entire sample,pre- and post-1981, and we report results for implementation with allcommodities and with HV commodities only.12 As a basis for comparison,in panel B of Table VI, we report the empirical distributions for the mean,standard deviation, skewness, excess kurtosis, and Sharpe ratio across1000 replications in which, each month, one third of commodities withavailable returns that month are randomly assigned to the P1 (long) port-folio and one third of commodities to the P3 (short) portfolio.

The mean returns to the momentum strategies examined in Table VIhave been reported previously; the main findings of interest pertain to thehigher moments of the momentum strategy returns. The results clearlyshow that the 2-month FP momentum strategy produces very high returnstandard deviations when compared with control strategies in which com-modities are assigned to portfolios randomly. For example, when themomentum strategy is implemented with all 28 commodities over theentire sample period, the standard deviation of monthly returns is found tobe 0.0538, as compared to a median (50th percentile) standard deviationfor control strategies of 0.0418 when implemented with a similar universe

TA

BL

E V

I

Sum

mar

y S

tati

stic

s an

d B

oots

trap

Res

ults

for

Mon

thly

Ret

urns

to

a R

epre

sent

ativ

e M

omen

tum

Str

ateg

y

Str

ateg

ies

impl

emen

ted

wit

h al

l com

mod

itie

sS

trat

egie

s im

plem

ente

d w

ith

HV

com

mod

itie

s on

ly

Ent

ire

sam

ple

Pre

-198

1 pe

riod

Post

-198

1 pe

riod

Ent

ire

sam

ple

Pre

-198

1 pe

riod

Post

-198

1 pe

riod

Pane

l A: P

1�

P3

Res

ults

for

a 2-

mon

th fo

rmat

ion

peri

od m

omen

tum

str

ateg

yM

ean

Ret

urn

0.01

390.

0176

0.01

020.

0141

0.02

110.

0070

SD

0.05

380.

0547

0.05

270.

0626

0.06

490.

0595

Ske

wne

ss�

0.01

630.

0717

�0.

1321

0.01

94�

0.16

020.

1878

Kur

tosi

s0.

4289

0.52

160.

2923

0.83

281.

3664

0.28

40M

inim

um�

0.14

64�

0.13

41�

0.14

64�

0.23

83�

0.23

83�

0.17

05M

axim

um0.

1847

0.18

360.

1847

0.20

830.

2083

0.18

57S

harp

e ra

tio0.

8958

1.11

230.

6716

0.78

051.

1254

0.41

00

Pane

l B: P

1�

P3

Res

ults

(ac

ross

100

0 re

plic

atio

ns)

whe

n co

mm

odit

ies

are

assi

gned

to

port

foli

os r

ando

mly

eac

h m

onth

Mea

n R

etur

n:

P�

0.00

5�

0.00

40�

0.00

75�

0.00

55�

0.00

60�

0.00

82�

0.00

63P

�0.

025

�0.

0033

�0.

0055

�0.

0043

�0.

0041

�0.

0062

�0.

0047

Mdn

0.00

010.

0000

0.00

000.

0000

0.00

000.

0001

P�

0.97

50.

0034

0.00

570.

0041

0.00

410.

0063

0.00

48P

�0.

995

0.00

450.

0086

0.00

560.

0049

0.00

860.

0058

SD

:P

�0.

005

0.03

850.

0413

0.03

250.

0429

0.04

620.

0356

P�

0.02

50.

0393

0.04

240.

0333

0.04

350.

0475

0.03

71M

dn0.

0418

0.04

620.

0365

0.04

700.

0522

0.04

08P

�0.

975

0.04

460.

0506

0.04

030.

0503

0.05

720.

0449

P�

0.99

50.

0456

0.05

200.

0415

0.05

130.

0583

0.04

65

Ske

wne

ss:

P�

0.00

5�

0.61

74�

0.70

62�

1.05

18�

0.74

75�

0.77

68�

1.34

76P

�0.

025

�0.

4485

�0.

5334

�0.

7704

�0.

5729

�0.

6385

�0.

8735

Mdn

0.00

720.

0195

�0.

0020

�0.

0209

�0.

0143

�0.

0169

P�

0.97

50.

4143

0.52

940.

7399

0.49

080.

6280

0.63

93P

�0.

995

0.57

130.

6835

1.00

330.

6271

0.80

221.

1551

Kur

tosi

s:P

�0.

005

0.20

46�

0.02

33�

0.30

060.

4851

0.22

28�

0.24

31P

�0.

025

0.46

460.

1880

�0.

1267

0.72

510.

4476

�0.

1095

Mdn

1.32

780.

9986

0.94

131.

8129

1.67

090.

7950

P�

0.97

53.

1959

2.70

055.

1335

4.11

163.

7533

5.88

98P

�0.

995

4.33

643.

8290

9.32

955.

2998

4.99

869.

5156

Sha

rpe

ratio

:P

�0.

005

�0.

3267

�0.

5453

�0.

5248

�0.

4330

�0.

5945

�0.

5442

P�

0.02

5�

0.27

74�

0.40

12�

0.41

26�

0.30

83�

0.41

74�

0.40

87M

dn0.

0056

0.00

15�

0.00

270.

0022

�0.

0032

0.01

07P

�0.

975

0.28

150.

4448

0.39

350.

3068

0.43

760.

4150

P�

0.99

50.

3843

0.60

610.

5120

0.37

210.

5723

0.52

75

Not

e.P

anel

Are

port

s m

onth

ly r

etur

n su

mm

ary

stat

istic

s fo

r P

1 �

P3

mom

entu

m p

ortfo

lios,

whi

ch ta

ke lo

ng p

ositi

ons

in p

ast w

inne

r an

d sh

ort p

ositi

ons

in p

ast l

oser

com

mod

ities

. Pan

el B

prov

ides

key

dis

trib

utio

n po

ints

for

each

sum

mar

y st

atis

tic a

cros

s 10

00 b

oots

trap

ped

repl

icat

ions

in w

hich

com

mod

ities

are

ass

igne

d to

the

P1

and