amit nalin securities pvt. ltd.ansec.in/ansec/uploaded_files/ansec_ashok_leyland... · ashok...

TRANSCRIPT

AMIT NALIN SECURITIES PVT. LTD.

ANSec Research 19th MARCH 2012

Investment Case:

We recommend a buy on Ashok Leyland with a price target of Rs 33 per share

over the next 9-12 months. We expect central bank of India to start reducing

its key interest rate in the second half of CY2012 which should improve the

industrial growth and benefit the commercial vehicle industry. Ashok Leyland

which has market leadership in the Bus segment and 20% market share in the

truck segment should benefit from the interest rate cut. Specially, the bus

segment which has recorded degrowth over the last years should perform well

on account of improved government activities. Ashok Leyland’s JV with Nissan

has recently launched their first LCV- Dost; LCV segment which is less sensitive

to the interest rate is expected to grow at 20% over the next 2 years. We

expect the JV to capture a market share of 5% by FY2014.

Indian Commercial Vehicle (CV) segment which constitutes 4-5% of the total Automobile

Industry volume grew 30%+ during FY2009 to FY2011. During H1FY2012, the CV

growth has come down to 15-18%, led by de-growth in the Medium and Heavy

Commercial Vehicle passengers (M&HCV Bus) segment and slowdown in the M&HCV

goods carrier (Trucks) segment. But the Light Commercial Vehicle (LCV) segment has

bucked the industry trend by continuing its growth rate at 28-30%. The CV segment

was impacted due to high interest rate combined with high inflation and contracting

industrial activity. With the start of CY2012, RBI has cut CRR by 50bps and indicated

that it will focus on growth over inflation for the period ahead. With inflation inching

towards the acceptable level, we expect interest rate to come down this year. This

should improve the industrial output and ease the cost of borrowing; benefiting CV

industry.

M&HCV segment which had the major impact of interest rate hike and slowdown in the

industrial activity is expected to underperform the LCV segment during CY2012. We

expect CAGR of 6-7% for M&HCV and 18-20% for LCV segment during FY2013-2014.

ALL’s M&HCV passenger (Bus) segment which had seen a de-growth during CY2011 is

expected to improve in the H2FY2013. We expect ALL’s M&HCV segment to grow in line

with industry growth rate.

Ashok Leyland (ALL) through its JV with Nissan launched their first LCV (Dost) last year

and received a good response. Till December 2011, they were able to sell 3000 vehicles.

The management is confident of achieving a sales target of 50000 vehicles for FY2013

which translates into a market share of 10-12%, on incremental basis. We believe it will

be very difficult to capture such a huge market share within a short span of time due to

strong presence of players like Mahindra & Mahindra and Tata Motors. We expect ALL to

capture a market share of 5-6% over the next 2 years.

AMIT NALIN SECURITIES PVT. LTD.

Ashok Leyland CMP: Rs 27 Fair Value: Rs 33

AmitNalin Securities Pvt. Ltd.

Bloomberg Code AL.IN

Reuters Code ASOK.BO

Market Cap 7290cr.

52 W High 30.50

52 W Low 20.05

Average Volume 533383

Price 27

Sensex 17300

Company Information

Stock Data

Share Holding Pattern

Promoters 38.61

Institutions * 15.76

Foreign 29.96

Public 10.78

*includes corporate holding

Analysts

Vinod Malviya

Amit Nalin Securities Pvt. Ltd.

142/A, Mittal Tower, Nariman Point, Mumbai- 400021. Tel.: 40021601 Fax: 22854721 E-mail: [email protected]

Sensex vs ALL’s Mcap

Standalone (Rs in Crs.) 201003 201103 2012e 2013e 2014e

Net Sales 7407.2 11366.0 12502.6 14065.4 15472.0

EBIDTA 750.9 1204.4 1312.8 1462.8 1609.1

EBIT 546.8 937.0 967.8 1090.8 1217.1

EBT 544.8 801.8 741.1 830.1 930.3

PAT 423.7 631.3 601.0 672.4 753.5

EPS 1.6 2.4 2.3 2.5 2.8

PE (x)*

12.0 10.7 9.5

Mcap/Sales (x)*

0.6 0.5 0.5

EV/EBIDTA (x)*

6.8 5.8 4.9 *Ratios are calculated at current price.

AMIT NALIN SECURITIES PVT. LTD.

Valuation (Rs)

Value

EV

6.7x FY2013 EBIDTA 9800.8

Less: Debt

FY2013

3268.0

Add: Investment & Cash

FY2013

2019.5

Equity Value

8552.3

Equity Value per share

33

We have valued Ashok Leyland using relative valuation method and

arrived at a fair value of Rs 33 per share. We have assigned a multiple of

6.7x (Industry average) on FY2013 EBIDTA. The fair value provides an

upside of more than 20% from the current market price of Rs 27.

We expect sales to grow at a compounded rate of 11% during FY2012-2014. On a

conservative basis, we have assumed net profit margin to come down to 4.8%

from 5.6% during FY2011. This is due to current high interest rate environment

and increased in non-cash expenditure.

Due to slowdown in the commercial vehicle segment, working capital requirement

has increased substantially. Company has raised additional Rs 500 crore during the

9MFY2012 to meet the working capital. The overall debt has increased from Rs

2600 crore during FY2011 to Rs 3150 crore. We expect the working capital to

improve in the FY2012-2013- on account of interest rate cut and improved CV

growth rate.

Company had earmarked capital expenditure and Investment of Rs 900-1000 crore

for FY2012 out of which Rs 600-700 crore has already been incurred. Company

plans to incur Rs 900-1000 crore of investment in various subsidiaries over the

next 2 years. We believe 60-70% of the capital requirement will be met through

internal accrual and the remaining through debt.

During FY2011-2012, Ashok Leyland with its JV partner Nissan launched their first

LCV (Dost). Till date, the company has sold 3800 vehicles. Management is

targeting sales of 35000-40000 for FY2012-2013. The sales of Dost in Tamil Nadu

are carried out under JV banner in order to enjoy sales tax benefit from Tamil

Nadu government. On the other hand, in the case of sales of Dost outside Tamil

Nadu, ALL purchases Dost from JV. Out of the total Dost sales, 65-70% is outside

Tamil Nadu. Thus the above arrangement results in lower margins from Dost i.e.

impacts ALL gross margins.

The growth in the export market has been robust. During FY2011, export volume

grew by 72% from 5979 to 10306. The management expects the volume to grow

by 30% during FY2012 and contribute 15% towards the total volume sales. Till

December 2011, company had sold 9196 vehicles and thus the sales volume of

13000 would be easily achieved.

Hinduja Finance has an equity capital of Rs 325 crore out of which Ashok Leyland

share is Rs 129 crore (40% stake). The company has disbursed more than Rs

1000 crore of loan. Presently, 7% of the ALL’s sales are financed by NBFC and the

management is targeting sales of 10% by FY2013.

With increased ALL’s volume- Hinduja

Finance to benefit.

Robust growth seen in the export

market

Deleveraging product portfolio

AMIT NALIN SECURITIES PVT. LTD.

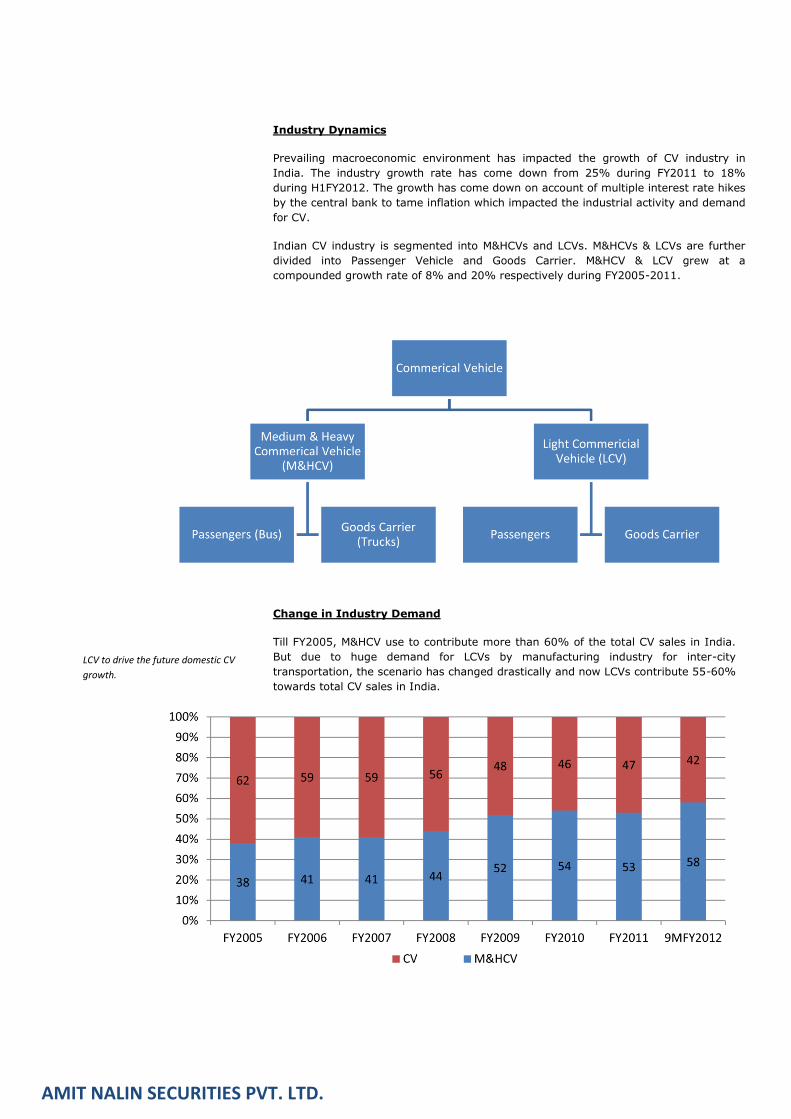

Industry Dynamics

Prevailing macroeconomic environment has impacted the growth of CV industry in

India. The industry growth rate has come down from 25% during FY2011 to 18%

during H1FY2012. The growth has come down on account of multiple interest rate hikes

by the central bank to tame inflation which impacted the industrial activity and demand

for CV.

Indian CV industry is segmented into M&HCVs and LCVs. M&HCVs & LCVs are further

divided into Passenger Vehicle and Goods Carrier. M&HCV & LCV grew at a

compounded growth rate of 8% and 20% respectively during FY2005-2011.

Change in Industry Demand

Till FY2005, M&HCV use to contribute more than 60% of the total CV sales in India.

But due to huge demand for LCVs by manufacturing industry for inter-city

transportation, the scenario has changed drastically and now LCVs contribute 55-60%

towards total CV sales in India.

LCV to drive the future domestic CV

growth.

AMIT NALIN SECURITIES PVT. LTD.

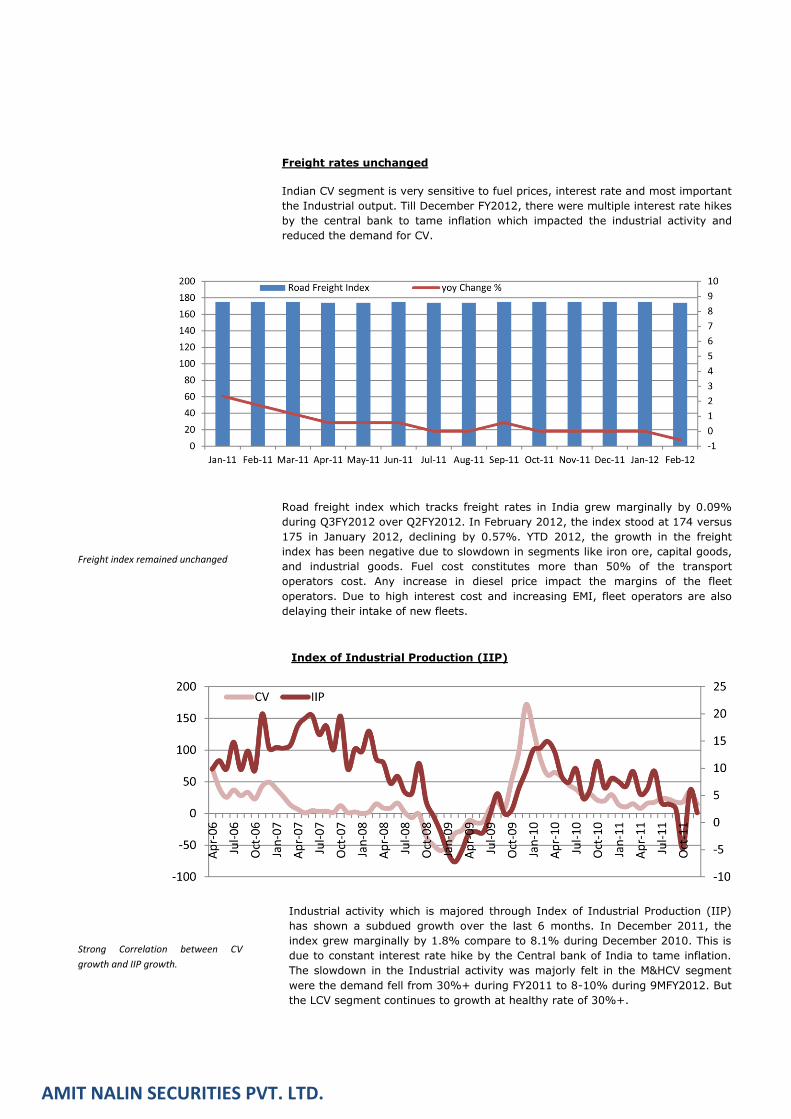

Freight rates unchanged

Indian CV segment is very sensitive to fuel prices, interest rate and most important

the Industrial output. Till December FY2012, there were multiple interest rate hikes

by the central bank to tame inflation which impacted the industrial activity and

reduced the demand for CV.

Road freight index which tracks freight rates in India grew marginally by 0.09%

during Q3FY2012 over Q2FY2012. In February 2012, the index stood at 174 versus

175 in January 2012, declining by 0.57%. YTD 2012, the growth in the freight

index has been negative due to slowdown in segments like iron ore, capital goods,

and industrial goods. Fuel cost constitutes more than 50% of the transport

operators cost. Any increase in diesel price impact the margins of the fleet

operators. Due to high interest cost and increasing EMI, fleet operators are also

delaying their intake of new fleets.

Index of Industrial Production (IIP)

Industrial activity which is majored through Index of Industrial Production (IIP)

has shown a subdued growth over the last 6 months. In December 2011, the

index grew marginally by 1.8% compare to 8.1% during December 2010. This is

due to constant interest rate hike by the Central bank of India to tame inflation.

The slowdown in the Industrial activity was majorly felt in the M&HCV segment

were the demand fell from 30%+ during FY2011 to 8-10% during 9MFY2012. But

the LCV segment continues to growth at healthy rate of 30%+.

Freight index remained unchanged

Strong Correlation between CV

growth and IIP growth.

AMIT NALIN SECURITIES PVT. LTD.

Company Overview

Ashok Leyland Limited is a Chennai based company. The Company is engaged in

the manufacturing of commercial vehicles and related components. The

Company’s products include buses, trucks, engines, defense and special vehicles.

From 18 seater to 82 seater double-decker buses, from 7.5 ton to 49 ton in

haulage vehicles, from numerous special application vehicles to diesel engines for

industrial, marine and gensets applications, Ashok Leyland offers a range of

products. During the fiscal year ended March 31, 2011 (fiscal 2011), the Company

produced 95,337 numbers of commercial vehicles and 17,603 numbers of engines

and gensets.

Bus Volume Q1FY2012 Q2FY2012 H1FY2012 Q1FY2011 Q2FY2011 H1FY2011 Q2 YoY HY1 YoY

Private 3749 4581 8330 4028 4855 8883 -6 -6

STU 3134 3030 6164 3477 4800 8277 -37 -26

ICV 4026 4197 8223 4223 3469 7692 21 7

10909 11808 22717 11728 13124 24852 -10 -9

During H1FY2012, volume sales of Buses recorded degrowth of 9% on yoy basis.

Degrowth was due to no orders from State Transport Undertakings (STU) and

Private Players. Intermediate commercial vehicle (ICV) recorded a fair growth of

7% on yoy basis. On account of improving road facility -intercity travel by road

should improve, and demand from niche segments like IT, BPO, schools, and

corporates should boost the demand for buses in the coming years.

Domestic Market Share

The M&HCV passenger segment grew at a compounded rate of 11% during

FY2005-2011. The segment is dominated by 2 players –Tata Motors and Ashok

Leyland- both of them together hold more than 84% of the domestic market

share. Eicher Motors along with its JV partner Volvo has done considerable value

by increasing its market share from merely 4% in FY2010 to ~9% in 9MFY2012.

Ashok Leyland is the market leader in the domestic Bus segment with more than

40% market share. The volume sales for ALL in the bus segment have grown at

a compounded rate of 12% during FY2005-2011. The growth was led by good

amount of orders from STUs and Private Players. ALL offers variety of buses

from 18 seaters to 80 seaters which fits almost every requirement like City Bus,

Sub-Urban Bus, Inter-City Bus, School & Staff Bus etc.

Medium & Heavy Commercial Vehicle (M&HCV)

The growth in the M&HCV segment has been very robust over the last 2 years.

During FY2010 and FY2011, M&HCV segment grew by more than 30%, 4x GDP

growth rate. But due to constant interest rate hike and contracting industrial

activity the growth is expected to narrow down to 6-7% during FY2012, 1x of

GDP growth rate. Growth in the sub-category has been negative for M&HCV

passenger vehicle (Buses) and 8-10% for M&HCV carrier vehicle (Trucks). We

expect overall M&HCV segment to grow in line with GDP growth i.e. 7-8% during

FY2013-FY2014.

Stagnant Government impacted the

bus segment.

Ashok Leyland has a leadership

position in the bus segment.

AMIT NALIN SECURITIES PVT. LTD.

Trucks

Demand for Truck is majorly influenced by the industrial activity. The demand

has shrunk from 30%+ during FY2011 & FY2010 to 9% during the H1FY2012.

This is due to slowdown in the core industries like steel, coal & mining etc. The

core industry growth has been very slow over the last 6 months on account of

multiple interest rate hikes, delay in government policy and mining ban in the

South India.

Volume Q1FY2012 Q2FY2012 H1FY2012 Q1FY2011 Q2FY2011 H1FY2011 Q2 YoY HY1 YoY

Haulage (16T) 6586 7835 14421 8007 9129 17136 -14 -16

Tippers (16T-31T) 10396 14729 25125 7816 10137 17953 45 40

Tractor Trlrs (30T-49T) 6344 7190 13534 6065 8035 14100 -11 -4

MAV (22T-31T) 27294 27706 55000 26222 27492 53714 1 2

ICV (9T-15T) 13471 16267 29738 11510 12105 23615 34 26

Total 64091 73727 137818 59620 66898 126518 10 9

In the sub-category, Tippers have witnessed a huge growth of 40% on yoy

basis, due to strong replacement demand. Tipper segment in FY2007 & FY2008

witnessed volumes which have been historical peaks so far and the

replacement volumes of the historical highs are likely to support near term

tipper demand. During the H1FY2011, the demand for MAV stood flat whereas

demand for Haulage and Tractor Trailer was negative. The demand for trucks is

expected to revive in the H2CY2012, once RBI starts reducing the key interest

rate, industrial activity and investment sentiment should change.

Domestic Market Share

The M&HCV goods career segment grew at a compounded rate of 8% during

FY2005-2011. The segment is dominated by Tata motors with 66% market

share and Ashok Leyland with 20% market share. Eicher Motors along with

its JV partner Volvo has done considerably well by increasing their market

share by 130bps to ~12% during 9MFY2012.

ALL has a market share of 20% in the domestic Truck segment. ALL’s Truck

segment grew at a compounded growth rate of 9% during FY2005-2011. The

growth was led by robust industrial activity. During FY2012, RBI hiked

interest rate to tame the inflation which has impacted the industry growth

rate significantly. The industry growth rate has come down to 6-7%, Whereas

ALL’s volumes sales has shown a negative growth rate of 10%. We expect

volume sales of 7-8% during FY2012-2014.

ALL offers comprehensive range of trucks for a variety of applications: long-

haul, distribution, construction, and mining. The demand for trucks in the

neighboring countries has been robust. Export volume sales registered a

growth of 70% during FY2011. Management expects the demand for truck to

remain robust in the neighboring countries like Sri Lanka, Bangladesh, and

Middles East Countries and has provided guidelines of 30-35% growth rate

during FY2012.

Replacement demand for tippers

drives the growth.

ALL has 20% market share (2nd

largest) in domestic truck segment.

30% growth expected the export

markets.

AMIT NALIN SECURITIES PVT. LTD.

Light Commercial Vehicle (LCV)

LCV segment which is less influenced by interest rate & industrial activity

grew at a compounded rate of 20% during FY2005-2011. The demand for

sub 1 tonne has very been robust due to emergence of Hub and Spoke

model and increasing demand for last mile connectivity. We expect the LCV

goods carrier segment to grow by 20% during FY2012-2014.

Domestic Market Share

The segment is dominated by Tata Motors and Mahindra & Mahindra with

60% and 31% market share respectively. Since 2005, the LCV goods

carrier segment has grown by 20% every year, except for FY2009. Due to

such an impressive growth rate, new players are entering the market and

intensifying the competition. To keep the market share intact, existing

players are offering discounts and launching new variants in sub

categories of LCVs. We expect players with strong brand equity, wide

distribution network and good understanding of the domestic market

should be able to snatch market share from weak players and from

incremental sales.

50:50 JV with Nissan for LCVs

First LCV product called ’Dost‘ was launched in July 2011 with a payload

capacity of 1.25 tons. Sales of Dost within Tamil Nadu will be booked in

the joint venture company and sales outside Tamil Nadu will be booked in

Ashok Leyland. Total sales till January 2012 of Dost were more than 3000

units. LCVs will be marketed through a separate dealer network. The

company has added 20 dealers so far and plans to sell 12,000 vehicles in

FY2012E. New products in <4 ton range will be launched over the next

few years. The company will invest Rs 500 crore in the joint venture. Till

date, Rs 290 crore has already been invested.

Less sensitive to the macroeconomic

environment.

Hub & spoke model drives LCV

growth.

JV eying a market share of 5-10% in

the next 2 years.

AMIT NALIN SECURITIES PVT. LTD.

AmitNalin Securities Pvt. Ltd.

50:50 JV with John Deere for construction equipment

The company launched the 435 backhoe loader in November 2011. The

company will be launching wheeler loader in CY2013E from its

Gummidipoondi facility. The facility has a production capacity of 10,000

units and the company will be investing Rs400 crore in the joint venture.

The joint venture has received an investment of Rs140 crore till date of

which Ashok Leyland has invested Rs51 crore. The company will also

supply engines for the backhoe loader. The company targets to sell 500

backhoe loaders in FY2012E and scale up volumes to >8,500 over the

next few years.

JV with Alteams for casings and housings

The joint venture was established to manufacture gear box casings, case

oil coolers and connection housings to Ashok Leyland’s trucks and

telecom gensets. The company will also manufacture cylinder heads and

inlet manifold in future from this joint venture. The total project cost is

Rs160 crore of which Ashok Leyland will invest Rs35 crore.

Hinduja Leyland finance

Hinduja Leyland Finance has disbursed ~Rs950 crore till Sep 2011 and

has financed 2,150 vehicles in 1HFY12. Equity capital in the company is

Rs325 crore of which Ashok Leyland has invested Rs129 crore and the

rest has been invested by group companies of the Hinduja group.

Operations have been spread to 394 locations with manpower strength of

over 850.

NBFC has already disbursed more

than Rs 1000crore of loan.

Foray into construction equipment.

AMIT NALIN SECURITIES PVT. LTD.

Balance Sheet

Standalone (Rs in Crs.) 201003 201103 2012e 2013e 2014e

SOURCES OF FUNDS:

Share Capital 133.0 133.0 266.1 266.1 266.1

Reserves Total 3535.7 3829.9 4160.5 4530.3 4944.7

Total Shareholders’ Funds 3668.8 3963.0 4426.5 4796.3 5210.8

Total Debt 2280.4 2658.2 3568.0 3822.0 3526.5

Total Liabilities 5949.2 6621.2 7994.5 8618.3 8737.3

APPLICATION OF FUNDS : Gross Block 6018.6 6691.9 7649.1 8119.1 8648.1

Less : Accumulated Depreciation 1769.1 2058.1 2403.1 2775.1 3167.1

Net Block 4249.6 4633.8 5246.0 5344.0 5481.0

Investments 326.2 1230.0 1530.0 1730.0 1830.0

Inventories 1638.2 2208.9 2327.0 2600.0 2689.0

Sundry Debtors 1022.1 1185.2 1165.0 1407.0 1340.0

Cash and Bank 518.9 179.5 315.0 289.5 528.0

Loans and Advances 972.9 793.6 961.4 1157.0 1173.0

Total Current Assets 4152.1 4367.2 4768.4 5453.5 5730.0

Current Liabilities 2592.1 3037.9 3493.6 3843.0 4227.3

Provisions 368.7 490.3 500.1 510.1 520.3

Total Current Liabilities 2960.8 3528.3 3993.8 4353.1 4747.6

Net Current Assets 1191.4 839.0 774.6 1100.4 982.4

Total Assets 5949.2 6621.2 7994.5 8618.3 8737.3

Income Statement

Standalone (Rs in Crs.) 201003 201103 2012e 2013e 2014e

Net Sales 7407.2 11366.0 12502.6 14065.4 15472.0

Raw Material 5211.6 8113.2 8939.4 10056.8 11062.4

Power & Fuel Cost 44.5 65.2 75.0 84.4 92.8

Employee Cost 667.3 969.7 1062.7 1195.6 1315.1

Other Manufacturing Expenses 90.4 169.7 187.5 211.0 232.1

COGS 6013.7 9317.7 10264.6 11547.7 12702.5

Gross Profit 1393.5 2048.3 2238.0 2517.7 2769.5

Selling and Administration Expenses 642.6 843.9 925.2 1054.9 1160.4

EBIDTA 750.9 1204.4 1312.8 1462.8 1609.1

Depreciation 204.1 267.4 345.0 372.0 392.0

EBIT 546.8 937.0 967.8 1090.8 1217.1

Interest 101.9 188.9 226.7 260.7 286.8

EBT 544.8 801.8 741.1 830.1 930.3

Tax 121.1 170.5 140.1 157.7 176.8

PAT 423.7 631.3 601.0 672.4 753.5

AMIT NALIN SECURITIES PVT. LTD.

Disclaimer:

This document has been prepared for private publication on the basis of publicly available information,

internally developed data and other sources believed to be reliable. Whilst we are not soliciting any action

based upon this information, all care has been taken to ensure that the facts are accurate and opinions

given fair and reasonable. Neither Amit Nalin Securities Pvt. Ltd., nor any of its employees, shall be

responsible for the contents. The securities discussed and opinions expressed in this report may not be

suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. The recipient should independently evaluate

the investment risks. The value and return of investment may vary because of changes in interest rates,

foreign exchange rates or any other reason. Past performance is not necessarily a guide to future

performance. Actual results may differ materially from those set forth in projections.

Amit Nalin Securities Pvt. Ltd may have issued other reports that are inconsistent with and reach different

conclusion from the information presented in this report. Amit Nalin Securities Pvt. Ltd, its affiliates or

individuals connected therewith may have used the information before publication and may have positions

in, may trade in or otherwise may be materially interested in any of the securities mentioned therein.