america - vanguardinstitutional.vanguard.com/pdf/has_2002.pdfonce a minor player in the retirement...

TRANSCRIPT

®

S A V E S

How

A Report on Vanguard Defined Contribution Plans

2 0 0 2

America

Once a minor player in the retirement savings system, defined contribution plans, in

particular 401(k) plans, have taken center stage as the dominant form of retirement savings

for America’s workers. Today nearly 60 million employees participate in defined contribution

plans, and industry assets total $2.2 trillion. By 2030, researchers expect that defined

contribution plans will be paying more to the baby boom generation than Social Security.

The Vanguard Group is a leader in the defined contribution marketplace

with nearly $300 billion in retirement assets. We offer plan sponsors invest-

ment management, recordkeeping, and education services. Today we serve

more than 1,300 plan sponsors and nearly 3 million participants.

As an industry leader, Vanguard recognizes that it’s important to have a

detailed understanding of defined contribution plans and the role they play

in the U.S. retirement system. To this end, we’ve prepared the 2002 edition

of How America Saves: A Report on Vanguard Defined Contribution Plans. This

report provides an assessment of defined contribution plans and participant

behavior based on Vanguard recordkeeping data and other sources. It also

offers an update on the broader defined contribution savings system.

We hope our report will serve as a valuable reference tool, and that our

observations will prove useful as your organization continues to evaluate

its retirement offerings.

Sincerely,

F. William McNabb III

Managing Director

Institutional Investor Group

September 2002

4 Highlights

8 part one

Retirement Plans andthe U.S. Workforce

10 The U.S. Workforce

13 Plans, Participants, and Assets

17 Retirement Plan Coverage

22 The Incomes of Older Americans

26 part two

Vanguard Defined ContributionPlans: Current Features

28 Participation Rates

31 Savings Rates

33 Participant Investment Decisions

37 Account Balances

40 Plan Investment Options and Decisions

47 Exchange Activity

49 Participant Education and Advice

52 Access Methods and The Internet

55 Plan Loans

59 In-Service Withdrawals

60 Plan Distributions and Rollovers

64 part three

Insights and Strategies

66 Boosting Participation and Savings Rates

73 How Much Should Workers Be Saving?

78 Restrictions on Company Stock

83 “Money Attitudes” and RetirementCommunications

89 Participant Trading Behavior: A Longer-Term View

93 Methodology

94 References

96 Acknowledgments

see following pages for Highlights . . .

C O N T E N T S

Total private sector retirement plan assets reached $4.1 trillion in 2001 and will likely grow at single-digit rates through 2003 (assuming single-digit market returns).Defined benefit assets constituted 46% of the total; defined contribution assets,54%. At year-end 2001 there were 23 million participants in defined benefit plansand 57 million participants in defined contribution plans. Page 14.

401(k) plans now account for nearly three-quarters of all defined contribution planassets, more than 80% of all defined contribution plan participants, and nearly 40% of all private sector retirement assets. Page 15.

Just less than half of U.S. workers were covered by employer retirement plans atyear-end 2001: 6% had defined benefit plan coverage only; 28% had defined contri-bution plan coverage only; and 15% had coverage from both types of plans. Page18.

For older Americans, Social Security remains the most prevalent source of income:9 of 10 older Americans received Social Security income in 2000. Six of 10 olderhouseholds had income from savings; 4 of 10, income from employer plans. Forlow-income households, Social Security accounted for 8 of every 10 dollars ofincome; for high-income households, income came from a mix of Social Security, personal savings, employer plans, and work earnings. Page 22.

Vanguard average plan participation rates declined from 79% in 1999 to 76% in2001, a pattern similar to that reported by other industry sources. Likely reasonsinclude the slowdown in the U.S. economy and the impact of declining stock priceson new plan enrollment. Page 28.

Retirement Plansand the U.S.Workforce

Participation andSavings Behavior

Highlights

From 1999 to 2001, Vanguard average plan savings rates also declined by 1% to just more than 7%. As with participation rates, likely reasons include the economic slowdown and the impact of falling stock prices on savings behavior.Some data on participant deferral rates in the first half of 2002 suggested risingsavings rates, possibly in response to improved economic conditions and pension reform. Page 31.

The main tools for boosting plan participation and savings rates remain specificplan features (company match, loans) and participant communications. New strategies include plan design features such as automatic enrollment and automatic savings (SMarT) plans, as well as new education techniques such as personaliza-tion and “money attitudes” research. New studies also underscore the importanceof peer group dynamics in determining savings behavior. Page 66.

Despite a two-year decline in U.S. stocks of –20%, the average asset allocation toequities among Vanguard participants fell only slightly, from 78% in 1999 to 76% in 2001. Falling asset values were offset by ongoing contributions to equities.Contribution allocations to equities remain virtually unchanged, at 81% of new contributions in 2001. Pages 33 and 34.

Although Vanguard participants maintained high allocations to equities in the faceof a sharply declining stock market, the average Vanguard participant’s account balance fell by only 1% from 1999 to 2001. The typical (median) account balanceactually rose by 5% during the period. Again, new contributions offset the impact of declining asset values. These results may explain participants’ continuedcommitment to a buy-and-hold strategy, despite the worst decline in U.S. stockprices in a quarter century. Page 37.

Highlights

Impact of the Bear Market in U.S. Stocks

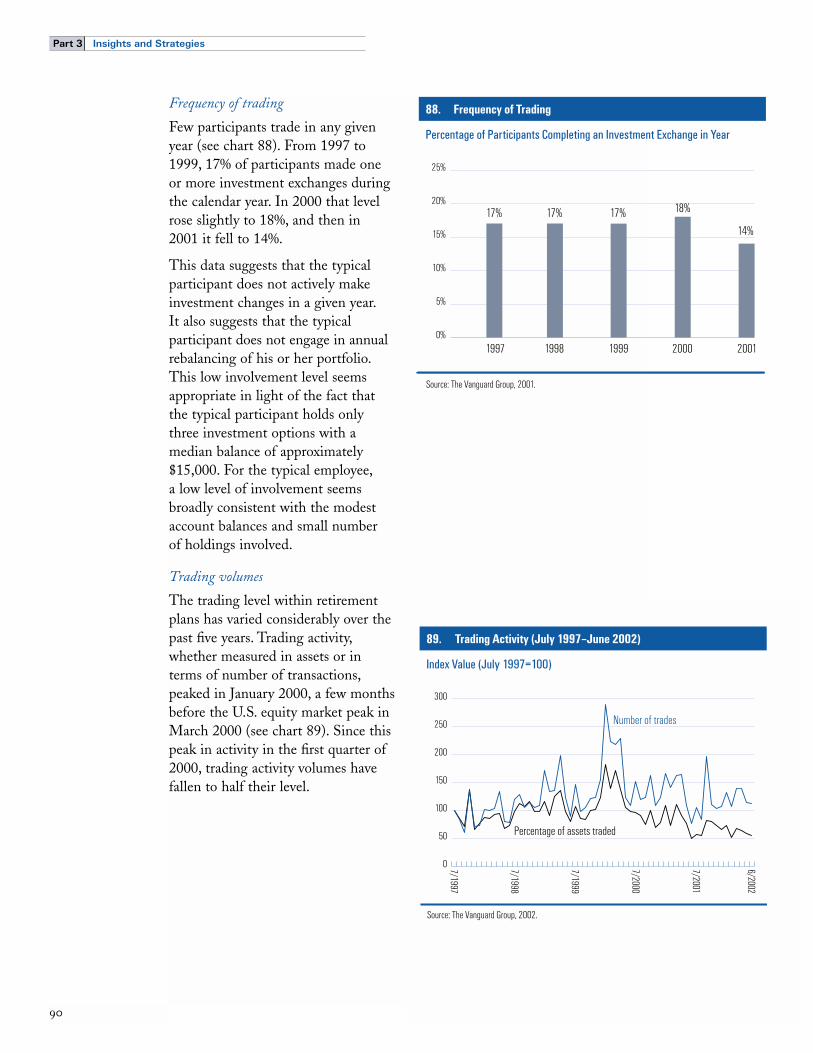

In any given year, few participants trade (i.e., exchange monies among investmentoptions in their employer’s plan). In 1999 only 17% of participants undertook anyinvestment exchange; in 2001 that number fell to 14% of participants. Page 47.

While fewer participants are trading, those who do trade are becoming increasinglylike-minded, with a preference for moving assets into fixed income investments.In 2001 an average of 2.5% of Vanguard net recordkeeping assets was shifted from equities to fixed income investments. While still modest, it was more than double the shift of 0.9% of average assets into fixed income investments in 1999. Page 48.

Company stock accounted for 14% of total defined contribution assets at Vanguard—and 25% of total assets among plans offering company stock as an investment option. These concentration levels remain somewhat below industry averages. Page 78.

The types of restrictions employers imposed on company stock are closely linkedwith the decision whether to make employer contributions in company stock or cash. Employers making stock contributions are more likely to impose restrictionson participants’ ability to diversify those contributions. Employers making cash con-tributions are more likely to have no restrictions at all or impose caps or maximumsin an effort to avoid concentrated stock holdings by participants. Pages 78 to

Vanguard participants are divided into three segments based on their degree ofinvolvement with their retirement accounts. Frequent contactors represented 22%of the Vanguard participant population in 2001; they contacted Vanguard an aver-age of 38 times per year, through the Web, a voice-response unit, or a telephoneassociate. Infrequent contactors constituted 30% of the plan population; they

Highlights

The Role ofCompany Stock

Participant Account Activity

Participant TradingActivity

81.

contacted Vanguard an average of four times per year. Just less than half of participants (48%) were noncontactors—they relied exclusively on quarterly accountstatements for information about their retirement plan accounts. Page 52.

Frequent contactors tend to be 45-year-old males with high account balances andhigh household incomes. According to Vanguard surveys of national plan partici-pants, these demographic elements are similar to those for frequent stock marketcheckers and frequent traders. Page 52.

Low levels of participant involvement—both reflected in account access data and in participant trading activity—seem appropriate in light of median account balances ($15,000) and a limited number of actual investment holdings (a median of three options). Page 42.

At a national level, an estimated 30% of preretirees are well prepared for retire-ment, 30% are potentially secure, and 40% are at risk. Page 74.

A participant earning $50,000 per year and covered only by a defined contributionplan would need to save 15% of income (both in employer and employee contribu-tions) over 30 years to ensure adequate retirement savings. For a participant withboth defined benefit and defined contribution coverage, the target savings ratewould be 9%. Based on these benchmarks, current defined contribution savingsrates appear to be too low. Page 77.

Other factors driving higher retirement savings include: a possible reduction inSocial Security benefits; the prospect for higher out-of-pocket Medicare and otherhealth care costs; increased life expectancy; and the additional savings needed to “self-fund” retirement income streams from lump-sum distributions. Page 75.

Highlights

Retirement Savings Adequacy

Retirement Plans and the U.S. Workforce

P A R T O N E

The U.S. retirement savings system rests on three legs. The first, Social Security, pro-vides income payments to older Americansand disability payments to workers. Thisdefined benefit program is mandatory andnearly universal. The system is publiclyfinanced through employer and employeepayroll taxes.

The second leg consists of an

extensive array of employer-

sponsored retirement plans.

Sponsorship of such plans is vol-

untary, and U.S. tax law provides

incentives to encourage plan

adoption. The principal sponsors

are private sector employers;

other important sponsors

include unions, nonprofit organi-

zations, and the public sector.

Defined contribution plans are

now the most prevalent type

of plan, though defined benefit

plans remain quite important for

employees of large companies,

union members, and public

sector workers.

The third leg of the U.S.

system is individually controlled

private retirement savings. Tax

incentives are granted to several

types of personal retirement

savings, including individual

retirement accounts (IRAs) and

fixed and variable annuities.

In this section we provide an

overview of key aspects of the

U.S. retirement system, with an

emphasis on employer-sponsored

retirement plans for private sec-

tor workers. This section covers:

• An overview of the U.S.

workforce in 2001.

• Size and scope of private

retirement plans.

• Retirement plan coverage.

• Income sources for today’s

older Americans.

The U.S. workforce has undergone

several dramatic changes over the past

quarter century. The changes outlined

below provide a broader context for

understanding retirement plan cover-

age and the shift from defined benefit

to defined contribution plans over

the period.

Employment

In 2001 the U.S. population totaled

285 million, and the U.S. workforce

reached 142 million (see chart 1).

Today, nearly 80% of jobs in the U.S.

workforce are in the private sector;

15% are in the public sector; and 2%

are in agriculture.

Over the past quarter century, private

sector employment has grown more

rapidly than public sector employ-

ment (see chart 2). From 1975 to

2001, private payrolls grew from 63

million to 110 million workers at an

annualized growth rate of 2.3%.

During the same period, government

payrolls expanded from 15 million to

21 million workers—an annualized

growth rate of 1.4%.

Part 1 Retirement Plans and the U.S. Workforce

1. Current U.S. Workforce 2001

Individuals

U.S. population

Civilian labor force

284.9

141.8

Source: U.S. Census, Department of Labor, 2001.

Composition of U.S. Workforce (in millions)

Individuals

Private sector (nonfarm)

Government

Agriculture

Unemployed

Other

110.2

21.1

3.1

6.7

0.7

Percentage

78%

15%

2%

5%

0%

Composition of Civilian Labor Force (in millions)

2. Growth of U.S. Workforce 1975–2001

Nonfarm Workers (in millions)

Public sector payrolls (+1.4% per year)

Private sector payrolls (+2.3% per year)

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

0

20

40

60

80

100

120

Source: Department of Labor, 2001.

The U.S. Workforce

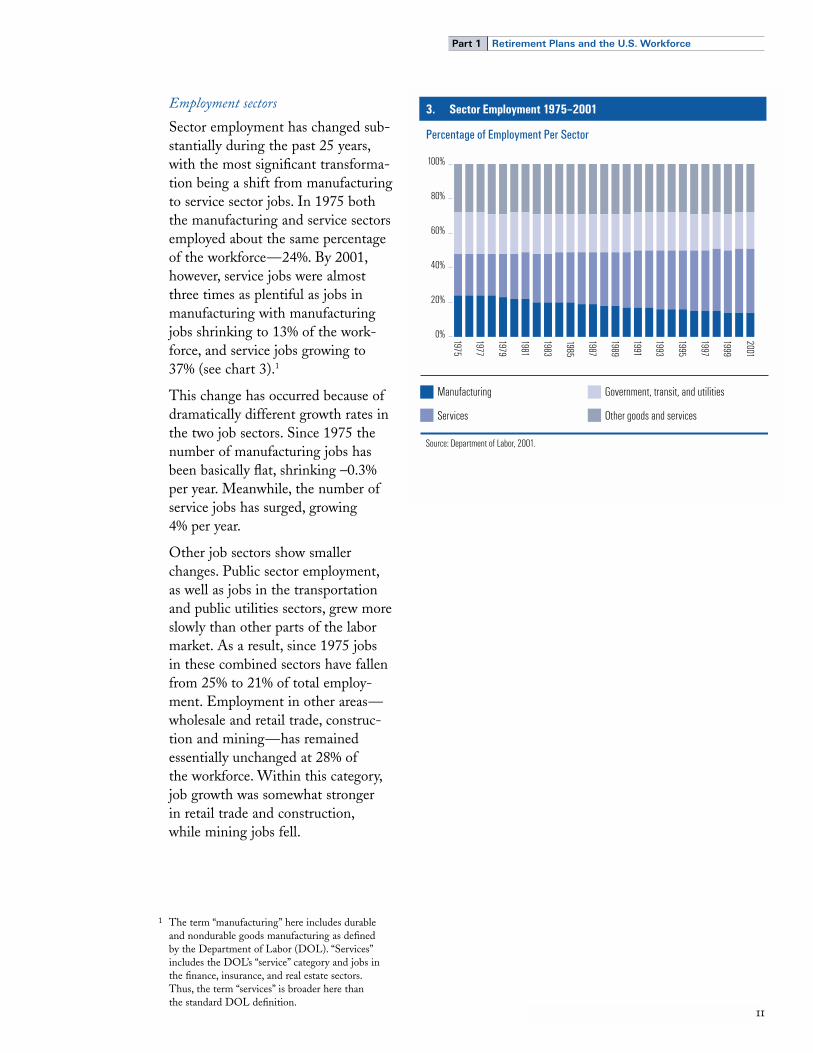

Employment sectors

Sector employment has changed sub-

stantially during the past 25 years,

with the most significant transforma-

tion being a shift from manufacturing

to service sector jobs. In 1975 both

the manufacturing and service sectors

employed about the same percentage

of the workforce—24%. By 2001,

however, service jobs were almost

three times as plentiful as jobs in

manufacturing with manufacturing

jobs shrinking to 13% of the work-

force, and service jobs growing to

37% (see chart 3).1

This change has occurred because of

dramatically different growth rates in

the two job sectors. Since 1975 the

number of manufacturing jobs has

been basically flat, shrinking –0.3%

per year. Meanwhile, the number of

service jobs has surged, growing

4% per year.

Other job sectors show smaller

changes. Public sector employment,

as well as jobs in the transportation

and public utilities sectors, grew more

slowly than other parts of the labor

market. As a result, since 1975 jobs

in these combined sectors have fallen

from 25% to 21% of total employ-

ment. Employment in other areas—

wholesale and retail trade, construc-

tion and mining—has remained

essentially unchanged at 28% of

the workforce. Within this category,

job growth was somewhat stronger

in retail trade and construction,

while mining jobs fell.

Part 1 Retirement Plans and the U.S. Workforce

3. Sector Employment 1975–2001

Percentage of Employment Per Sector

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

0%

20%

40%

60%

80%

100%

Manufacturing

Services

Government, transit, and utilities

Other goods and services

Source: Department of Labor, 2001.

1 The term “manufacturing” here includes durable

and nondurable goods manufacturing as defined

by the Department of Labor (DOL). “Services”

includes the DOL’s “service” category and jobs in

the finance, insurance, and real estate sectors.

Thus, the term “services” is broader here than

the standard DOL definition.

Work arrangements

Full-time work remains the most

common type of employment

arrangement in the U.S. Three-

quarters of workers are engaged

in full-time work (see chart 4).

An additional 15% are engaged

in traditional part-time work.

Nearly 13 million workers, or just

less than 10% of the workforce, are

employed in what are termed “alter-

native work arrangements” (see again

chart 4).2 These jobs are structured

somewhat differently than traditional

full-time or part-time work.

Workers in alternative work arrange-

ments include3:

Independent contractors (6.4% of

the workforce)—freelance workers

who typically acquire clients on their

own. Examples include management

consultants, freelance writers, or self-

employed trades people.

On-call workers (1.6%)—workers who

are called to a job as needed by vari-

ous employers. Their work may last a

day or two or extend to several weeks.

They include construction workers

hired through a union hall, substitute

teachers, or on-call nurses.

Temporary-help agency workers (0.9%)—

any workers paid by a temporary-

employment agency. The typical tem-

porary worker is the “temp” office sec-

retary, but this category also includes

jobs such as temporary accountants

or paralegals.

Contract workers (0.5%)—workers

employed by a contracting company,

which provides another organization

with workers on a long-term basis.

The workers of the contracting

company typically work for a single

client and often at the client’s work

site. Examples include employees

of food service, security, or computer

services companies—activities

typically “outsourced” by the client

organization to the contracting firm.

Part 1 Retirement Plans and the U.S. Workforce

4. Work Arrangements in 2001

Employed Workforce135.0 million

75.2% Full-time101.5 million

9.4% Alternative Work Arrangements12.7 million

Source: Department of Labor, 2001; Vanguard estimates.

15.4% Part-time20.8 million

2 This information has been drawn from

Polivka, 1996.

3 Separate from the definition of full-time, part-

time, or alternative work; another 2% to 4% of

the workforce (three million to six million workers)

is classified as “contingent”—workers who expect

their employment to end in the foreseeable future.

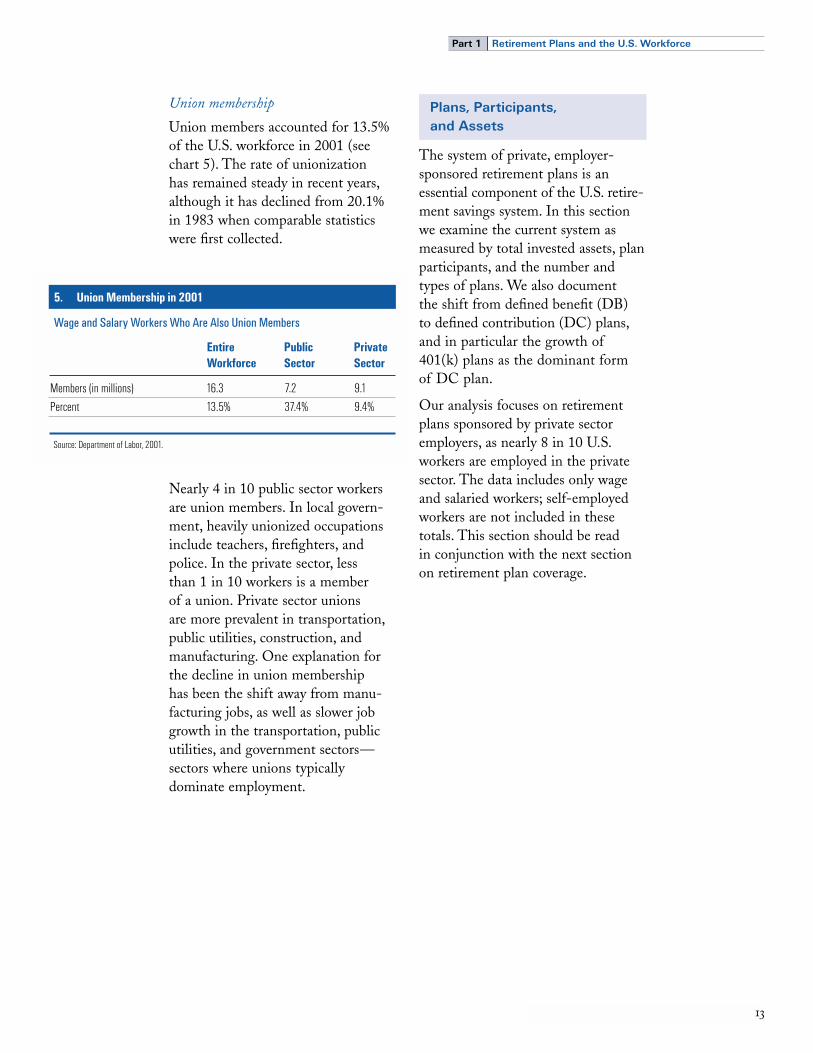

Union membership

Union members accounted for 13.5%

of the U.S. workforce in 2001 (see

chart 5). The rate of unionization

has remained steady in recent years,

although it has declined from 20.1%

in 1983 when comparable statistics

were first collected.

Nearly 4 in 10 public sector workers

are union members. In local govern-

ment, heavily unionized occupations

include teachers, firefighters, and

police. In the private sector, less

than 1 in 10 workers is a member

of a union. Private sector unions

are more prevalent in transportation,

public utilities, construction, and

manufacturing. One explanation for

the decline in union membership

has been the shift away from manu-

facturing jobs, as well as slower job

growth in the transportation, public

utilities, and government sectors—

sectors where unions typically

dominate employment.

The system of private, employer-

sponsored retirement plans is an

essential component of the U.S. retire-

ment savings system. In this section

we examine the current system as

measured by total invested assets, plan

participants, and the number and

types of plans. We also document

the shift from defined benefit (DB)

to defined contribution (DC) plans,

and in particular the growth of

401(k) plans as the dominant form

of DC plan.

Our analysis focuses on retirement

plans sponsored by private sector

employers, as nearly 8 in 10 U.S.

workers are employed in the private

sector. The data includes only wage

and salaried workers; self-employed

workers are not included in these

totals. This section should be read

in conjunction with the next section

on retirement plan coverage.

Part 1 Retirement Plans and the U.S. Workforce

5. Union Membership in 2001

Wage and Salary Workers Who Are Also Union Members

EntireWorkforce

Public Sector

Private Sector

Members (in millions)

Percent

16.3

13.5%

7.2

37.4%

9.1

9.4%

Source: Department of Labor, 2001.

Plans, Participants, and Assets

Overview

As of 2001, based on Vanguard esti-

mates4, private sector retirement assets

totaled $4.1 trillion, with $1.9 trillion

invested in DB plans and $2.2 trillion

in DC plans (see chart 6, top panel).

Although they are not formally part

of the employer-based retirement

system, IRAs are the recipients of

rollovers from both DC and DB

plans, and so a portion of IRA assets

comes from employer-sponsored

plans. As of 2001 IRA assets stood

at $2.6 trillion.5

Retirement Plans Overview

Based on our estimates (which

assume single-digit market returns

in 2002 and 2003), asset levels in

both DB and DC plans will continue

to grow at modest rates through

2003. Continuing the trend of the

past two decades, DC and IRA assets

are expected to grow at a faster rate

than DB assets.

As of 2001 there were about 80 mil-

lion workers participating in private

sector retirement plans (see chart 6,

second panel). A worker may be in

multiple plans, and so the actual

number of private sector workers cov-

ered by an employer-sponsored plan

is lower (see page 17). Of the private

sector workers in retirement plans,

about 70% of the total, or 57 million,

were in DC plans; about 30%, or 23

million, were in DB plans.

In 2001 there were more than

700,000 private sector DC plans,

compared with more than 50,000

DB plans (see chart 6, third panel).

Both in terms of active participants

and number of plans, DC plans

are expected to continue to grow,

while DB plans are expected to

stagnate or continue their historical

decline, albeit at a much slower

rate than in the past.

Part 1 Retirement Plans and the U.S. Workforce

4 Data through 1998 is drawn from DOL retirement

plans data, issued by the Pension Benefits and

Welfare Administration. Data for 1999 through

2003 is based on Vanguard estimates.5 While the percentage of IRA assets due to

employer rollovers is uncertain, 44% of IRA

account holders indicated that a portion of their

IRA assets are derived from an employer-

sponsored retirement plan. See ICI, 2002.

6. Retirement Plans Overview 2001–2003

2001Private Sector 2002 2003

AnnualGrowth

Rate

4%7%

5%

6%

0%4%

2%

–1%4%

4%

8%6%6%8%

1,894 2,166

4,060

2,602

23,000 57,100

80,100

52,000 736,000

788,000

1,603 45,900 70,600

392,800

$ $

$

$

$

1,951 2,275

4,226

2,732

22,900 58,900

81,800

51,000 765,500

816,500

1,706 47,700 73,400

424,200

$ $

$

$

$

2,044 2,457

4,501

2,951

22,800 61,200

84,000

50,500 796,100

846,600

1,867 51,500 79,200

458,200

$ $

$

$

$

Assets ($ billions)Defined BenefitDefined Contribution

Total

IRA Assets

Participants (thousands)Defined BenefitDefined Contribution

Total

PlansDefined BenefitDefined Contribution

Total

401(k) Plans* 401(k) Assets ($ trillions) 401(k) Participants (thousands) 401(k) Eligibles (thousands)** 401(k) Plans

* 401(k) data is subset of defined contribution data. ** 401(k) eligibles are estimated based on weighted participation rate of 65%. Source: Vanguard estimates; Department of Labor; Federal Reserve. 2002 and 2003 forecasts based on balanced index market return of 5% in 2002 and 8% in 2003.

Although they are already included

in the totals for DC plans, we have

separately estimated assets, partici-

pants, and 401(k) plans (see chart 6,

bottom panel). In 2001, 401(k) assets

stood at $1.6 trillion. Out of an esti-

mated 70 million workers eligible

for 401(k) plans, nearly 46 million

were active participants in their plans.

And the total number of 401(k)

plans approached 400,000.

By several measures, 401(k) plans

are now the dominant form of DC

retirement plan, more significant than

traditional DC plans such as stand-

alone profit-sharing, money purchase,

or employee stock ownership plans

(ESOPs). Today, 401(k) plans

account for:

• More than half of all DC plans.

• Nearly three-quarters of all DC

plan assets.

• More than 80% of all DC

plan participants.

Perhaps most significantly, 401(k)

plans now account for nearly 40%

of all private sector retirement plan

assets, DB and DC combined—a

total of $1.6 trillion in 401(k) plans

versus a combined $4.1 trillion in

all DB and DC plans.

Assets

Since 1985 DC plan assets have

grown at more than twice the rate

of DB plan assets (see chart 7).

DC plan assets have expanded at an

11% annualized rate, compared with

a 5% growth rate for DB plan assets.

Much of the growth in DC assets

has come from 401(k) plans, which

have surged at a compound rate

of 16% per year since 1985.

Similarly, IRA assets grew at double-

digit rates during the same period,

(see chart 8) expanding from $236

billion to $2.6 trillion since 1985.

This reflects an annualized growth

rate of 16% per year.

Part 1 Retirement Plans and the U.S. Workforce

7. Plan Assets 1985–2001

Assets of Private Sector Retirement Plans (in billions)

DB +5% per year

DC +11% per year

401(k) +16% per year

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Note: 401(k) is a subset of defined contribution data.Source: Department of Labor through 1998; Vanguard estimates thereafter.

$0

$500

$1,000

$1,500

$2,000

$2,500

8. IRAs 1985–2001

IRA Assets (in billions)

Source: Federal Reserve and Vanguard estimates.

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

1986

1985

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

IRAs +16% per year

Participants

Since 1985 DC plan participants have

grown from 33 million to 57 million,

a compound growth rate of about 3%

per year (see chart 9). Within this

category, 401(k) plan participants

have expanded at a 10% growth rate.

In 1985 3 in 10 DC plan participants

were in 401(k) plans; by 2001, nearly

8 in 10 were. The number of DB

plan participants fell from 29 million

in 1985 to 23 million in 2001—

a decline of 1% per year over the

period. This in part reflects the

shift in employment away from sec-

tors, such as manufacturing or the

government, where DB plans have

traditionally predominated.

Plans

Similar patterns are reflected in the

changing number of DB, DC, and

401(k) retirement plans (see chart

10). The number of DB plans has

fallen from more than 170,000 in

1985 to about 52,000 in 2001.

Meanwhile, the number of DC plans

has grown, and in particular 401(k)

plans have expanded at double-digit

rates. In 1985 only 6% of DC plans

were 401(k) plans; by 2001, more

than half were.

Part 1 Retirement Plans and the U.S. Workforce

9. Plan Participants 1985–2001

Private Sector Active Retirement Plan Participants (in thousands)

DB –1% per year

DC +3% per year

401(k) +10% per year1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Note: 401(k) data is a subset of defined contribution data.Source: Department of Labor through 1998; Vanguard estimates thereafter.

0

10,000

20,000

30,000

40,000

50,000

60,000

10. Plans 1985–2001

Number of Private Sector Retirement Plans

DB –7% per year

DC +3% per year

401(k) +17% per year

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Note: 401(k) data is a subset of defined contribution data.Source: Department of Labor through 1998; Vanguard estimates thereafter.

0

200,000

400,000

600,000

800,000

Coverage is the term used to describe

the number of workers eligible for,

and participating in, an employer-

sponsored retirement savings plan. It

is an important measure of the success

of the U.S. retirement savings system,

as the system relies on employment-

based retirement plans and private

savings to supplement benefits from

the Social Security system.

The term “pension coverage” is still

widely used, though it is now some-

thing of an anachronism given the

shift away from DB plans (pensions)

to DC plans (savings plans) over

the past quarter century. In this sec-

tion we summarize retirement plan

coverage both currently and histori-

cally, and offer some perspective

on how coverage varies across the

U.S. workforce.

Given that nearly 8 in 10 jobs are

in the private sector, our focus is on

private sector wage and salaried

workers (excluding the self-employed).

Pension coverage rates for the

public sector, as we note below, are

comparable to those found among

large private employers. Our analysis

addresses coverage rates, the number

of active workers covered by a private

plan—as opposed to sponsorship

rates, the number of employers

offering a retirement plan.6

Current coverage

According to our own estimates based

on historical data from the U.S.

Department of Labor, 49% of private

sector salaried and wage workers

were participating in a retirement

plan in 2001, and 51% were not

(see chart 11).

The dominant type of retirement

plan is a DC plan. More than 4 in 10

private sector workers participate in

a DC plan—28% participate solely

in a DC plan, and another 15% are

in both a DB and DC plan. In terms

of DB coverage, about 2 in 10 private

sector workers have such coverage—

6% of workers have only a DB plan,

and, again, 15% have both a DB

and a DC plan.

Part 1 Retirement Plans and the U.S. Workforce

6 The plan sponsorship rate, the percentage of

employers offering a retirement plan to workers, is

generally higher than plan coverage rates by more

than ten percentage points. The sponsorship rate

indicates only whether an employer has established

a retirement plan, regardless of eligibility rules or

participation by the employee. The coverage rate

reflects the actual number of employees who are

eligible for a plan and who are covered by it

(including, in voluntary 401(k) plans, those who

actually participate in the plan).

11. Current Private Sector Coverage 2001

15% DB and DC

Source: Department of Labor, 2001; Vanguard estimates.

51% Not covered

28% DC only% DC only

6% DB only

Retirement Plan Coverage

Historical coverage

Over the past quarter century, pen-

sion coverage has remained virtually

unchanged, at just under half of the

private sector workforce, despite

the dramatic shift from DB to DC

plans (see chart 12). In 1975 the

dominant form of pension plan cover-

age was DB-only. For 31% of the

private workforce, the only type of

retirement plan offered was a DB

plan. Another 8% of workers had

both DB and DC plans. At that time,

only 6% of private sector workers

were covered by DC-only plans,

which at the time did not include

401(k) plans.

With the introduction of 401(k)

plans in the early 1980s, coverage

by DC plans soared. The number

of workers covered by DC-only plans

nearly quintupled, from 6% to 28%

of the private sector workforce.

And the number of dual-coverage

participants—those covered by both

DB and DC plans—nearly doubled,

from 8% to 15%. Meanwhile,

coverage by stand-alone DB plans

declined sharply, from 31% to 6%

of the workforce.

In simple terms, over the past quarter

century, the rates of DB and DC

coverage have essentially traded

places. In 1975 about 4 in 10 private

sector workers (39%) had DB plan

coverage, either as a stand-alone DB

plan or in combined DB-DC cover-

age. By 2001, DC plans covered more

than 4 out of 10 (43%) workers.

In 1975, DC plans covered less than

2 out of 10 (14%) private sector

workers; by 2001, DB plans covered

2 in 10 workers (21%). The dominant

type of DC plan changed as well,

away from standalone profit-sharing

and ESOP programs to 401(k) plans,

sometimes in combination with

profit-sharing or ESOP features.

Part 1 Retirement Plans and the U.S. Workforce

12. Historical Private Sector Coverage 1975–2001

Percentage of Coverage

DB Only DC Only

DB and DC

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

Source: Department of Labor, 1999; Vanguard estimates.

5%

10%

15%

20%

25%

30%

35%

Variations in coverage

Pension coverage depends on a num-

ber of employment-related factors

(see chart 13). These include firm

size, employment sector, employee

skill grade, and the type of work

arrangement (full-time, part-time,

alternative). As a general rule,

coverage rates are higher among:

• Public sector and large private

sector firms.

• Manufacturing, transportation, pub-

lic utilities, and financial services.

• Professional/technical employees

and union members.

• Full-time workers.

At the other extreme, coverage

rates are lowest among small firms,

among sectors like construction and

retail sales, and among part-time,

on-call, temporary, and independent

contract workers.

Part 1 Retirement Plans and the U.S. Workforce

13. Variations in Coverage 1999

Percentage of Private Sector Salary and Wage Workers Participating in an Employer Retirement Plan—by Economic FactorOverall Average: 48%

Firm Size/Type* SectorType of Employees

Work Arrangement

Above-average coverage

Near-average coverage

Below-average coverage

Very large firms (81%)Public sector (80%)Large firms (70%)

Medium firms (57%)

Small firms (34%)

Manufacturing (68%)FIRE (62%)**Transportation and public utilities (59%)

Wholesale trade (53%)Services (45%)

Construction (39%)Retail trade (30%)

Full-time (56%)

Contract workers (48%)***R

On-call workers (31%)***Part-time (21%)Temp help (8%)***Independent contractors (2%)***

Union (79%)Professional/technical (69%)

Clerical/sales (45%)R

Blue collar/service (42%)

Economic Factor (Coverage Rate)

* Very large firms: 2,500 or more employees; large firms: 500–2,499 employees; medium firms: 100–499 employees; small firms: 1–99 employees. ** Finance, insurance, and real estate sector. *** 2001. Note: Below- and above-average defined as more than 10% below- or above-average. Source: Department of Labor, 1999, 2001.

Another way to look at variations

in pension coverage is by the

demographic characteristics of

workers (see chart 14).7 Not surpris-

ingly, workers who are older, have

average or above-average incomes,

or who have college or professional

training are more likely to be in jobs

with retirement plans. Meanwhile,

younger workers with low incomes

and less education are less likely

to be in jobs with retirement plans.

Coverage among women and men is

about equal—although, importantly,

this figure only measures those women

in the formal workforce. Because

more women than men work in the

home and fall outside the employ-

ment-based pension system, the

pension coverage rate for women in

the aggregate is lower than that for

men. White workers have somewhat

higher rates of coverage than black

workers or other races; perhaps the

most significant disparity is the low

rate of coverage for Hispanic workers.

Part 1 Retirement Plans and the U.S. Workforce

7 This demographic analysis is based on the public

and private sector workforce that is full-time and

full-year, age 18 to 64. Because full-time and public

sector employees have high rates of coverage, the

average coverage rate for this group is 61%. This

figure is used to make comparisons of above- and

below-average coverage.

14. Demographic Variations in Coverage 1999

Percentage of Public and Private Workers, Full-time and Full-year, Participating in an Employer Retirement Plan—by Demographic FactorOverall Average: 61%

Age Income Education

Race

Above-average coverage

Near-average coverageV

Below-average coverage

Age 45–54 (72%)Age 55–64 (68%)

Age 35–44 (61%)Age 25–34 (54%)V

Age 21–24 (33%)Age 20 and under (17%)

$50K+ (82%)$40–$49K (78%)$30–$39K (70%)

$20–$29K (50%)

$15–$19K (38%)$10–$14K (26%)

Gender

Male (61%)Female (60%)

White (65%)Black (56%)Other (55%)

Hispanic (38%)

Graduate/professional (81%)Bachelor’s degree (72%)

Some college (62%)High school (55%)

Less than high school (32%)

Demographic Factor (Coverage Rate)

Note: Below- and above-average defined as more than 10% below- or above-average. Source: Department of Labor, 1999; EBRI, 1999.

Boosting plan coverage

These statistics convey some of the

challenges involved in boosting cover-

age rates and strengthening the role

of employer-based plans in the U.S.

retirement savings system. For exam-

ple, small businesses (companies with

less than 100 employees) employ

more than 4 out of 10 private workers

in the U.S. But only a third or so of

small businesses are able to offer an

employer plan. Surveys of business

owners indicate that there are two

main reasons why they don’t offer a

retirement plan—uncertain company

revenues and workers’ preferences

for wages.8

When an employer offers an employ-

ee-voluntary program like a 401(k)

plan, coverage rates will also depend

on workers’ decisions to join the plan.

Retirement plan coverage is lower for

workers who are younger, who have

less income, or who are less educated.

One reason is that these workers are

more likely to be in jobs that lack

retirement plan coverage. But another

reason is that workers may choose not

to participate—whether because of

low income and an inability to save,

or a lack of understanding or aware-

ness of the plan and its benefits.

There are two challenges to boosting

private pension coverage in the

U.S.: encouraging firms, particularly

medium- and small-sized businesses,

to take on the costs of plan sponsor-

ship; and, in the case of voluntary

programs like 401(k) plans, encouraging

workers, particularly lower-income

workers, to take on the costs of

contributing to their plan.

Part 1 Retirement Plans and the U.S. Workforce

8 EBRI, 2002.

Another way to examine the U.S.

retirement savings system is from the

perspective of the benefits paid today

to older Americans. In 2001 more

than 35 million Americans—about

12% of the population—were age 65

or older. Not all of these individuals

were “retired” in the traditional

sense—that is, individuals who had

left their primary occupation. But age

65 remains a traditional demarcation

point between the active workforce

and the retired population in the U.S.

In this section we look at the current

incomes of those age 65 and older

in 2000. This data is drawn from

an analysis conducted by the Social

Security Administration based on

a survey by the U.S. Census Bureau.9

Sources of income

Social Security remains the most

prevalent form of income earned

by older Americans. Nine out of 10

older Americans received benefits

under the program in 2000, the latest

year for which data is available

(see chart 15). Six out of 10 older

Americans reported income from

their personal savings; about 4 in 10

said they received income from an

employer retirement plan, both public

and private sector. About 1 in 5

older Americans had salary or wages

from work.

Two caveats about these results:

First, with the shift from DB to DC

plans, the distinction between person-

al savings and employer plans has

become blurred. The category

“employer plans” includes pension

payments received from a DB plan.

But it may not capture DC plan

savings, depending on how the indi-

vidual replied to the Census Bureau

survey. Workers who roll over DC

plan savings (or DB lump sums)

to IRAs may classify these monies

as savings. Thus, the finding that

4 out of 10 older Americans receive

money from an employer plan may

refer largely to DB pension payments

and some, but not all, DC monies.

Part 1 Retirement Plans and the U.S. Workforce

15. Income Sources for Older Americans in 2000

Percentage of Older Americans Receiving Income from a Given Source

90%

5%

22%

41%

4%

59%

SocialSecurity

Personal Savings

EmployerPlans

Veterans’Benefits

PublicAssistance

WorkEarnings

Source: Social Security Administration, 2002.

Source

0%

20%

40%

60%

80%

100%

9 See Social Security Administration, 2002. This data

is based on Social Security “aged units”—married

couples with at least one member 65 and older or

single individuals age 65 and older. Throughout

this section we use informal terms like “older

Americans” or “households age 65 and older”

instead of the more technical “aged units.”

The Incomes of Older Americans

Second, this survey includes all

Americans 65 and older, whether they

are working or retired. So, for an item

like “work earnings,” the results shown

include individuals still in the work-

force, as well as individuals who con-

sider themselves retired, but who also

have chosen to work in retirement.

Shares of income

Another way to look at retiree income

is to examine the total income earned

in aggregate by all older Americans

(see chart 16). Social Security again

tops the list, accounting for about 4

out of every 10 dollars of income paid

to individuals age 65 and over. Work

earnings represent nearly a quarter

of total income. Both income from

savings and retirement plans amount

to nearly a fifth each.

Income distribution

Social Security is the dominant

source of income for lower-income

households, while higher-income

households rely on multiple sources

(see chart 17 on page 24). In 2000

the bottom quintile of households,

ranked by income, earned less than

$9,000 per year; the second quintile

earned from $9,000 to $15,000.

For both groups, Social Security

accounted for 82% of their incomes.

For the middle-income group, with

income from $15,000 to $24,000 in

2000, Social Security was still a domi-

nant source of earnings, accounting

for 64% of income. But more than

one-third came from other sources—

including employer plans (16%), per-

sonal savings (9%), and work earnings

(7%). In the fourth quintile—those

older Americans earning $24,000 to

$40,000—Social Security accounted

for less than half (46%) of income.

Employer plans provided nearly

a quarter of income (23%). Personal

savings and work earnings were

also important sources of income.

The top-income segment—those

earning more than $40,000 in 2000—

was unique because of the dominance

of work earnings, which accounted

for 35% of total income. Personal

savings were the second most impor-

tant source of income (24%), with

employer plans and Social Security

making up the balance (19% each).

Part 1 Retirement Plans and the U.S. Workforce

16. Components of Total Income in 2000P

Percentage of Total Income, Age 65 and Older, from Source

38% Social Security

23% Work earnings

18% Employer plans

18% Personal savings

Source: Social Security Administration, 2002.

3% Other

The role of Social Security

Social Security is the sole retirement

income for about one-third of older

Americans, accounting for 90% to

100% of their total income (see chart

18). In fact, for 1 in 5 recipients,

Social Security is their entire income.

Another one-third of Social Security

recipients derive the majority of their

income from Social Security; Social

Security ranges from 50% to 89% of

their income. Slightly more than a

third rely on Social Security for less

than half of their income.

The future of Social Security

In 2001 Social Security covered a

total of 153 million workers for both

old-age and disability benefits. Nearly

39 million individuals received old-

age income benefits under the pro-

gram. The average annual retirement

payment equaled about $10,100.

Social Security retirement benefits

are designed to replace about 40%

of the average American’s preretire-

ment income. This level of benefit is

about half that paid by the public

systems in continental Europe, but

on par with programs in the United

Kingdom, Canada, Australia, and

the Netherlands.

Social Security faces a well-documented

financial crisis because of demograph-

ics. The system is largely financed on

a “pay as you go” basis, meaning that

taxes on current workers are used to

pay benefits to current retirees. As the

baby boom ages, there will be a surge

in the number of Social Security

recipients, but a much smaller growth

in the number of workers paying

taxes to the system. Today there are

3.4 workers paying taxes for every

Social Security recipient; by 2030,

when the baby boom is retired, there

will be 2.1 workers for each retiree.

Part 1 Retirement Plans and the U.S. Workforce

17. Income Distribution for Older Americans, 2000

Percentage of Income from Various Sources, by Income Quintiles

Social Security

Work Earnings

Top 20%

Fourth 20%

19% 19% 24% 35% 3%

Employer Plans

Other

Personal Savings

Source: Social Security Administration, 2002.

0% 20% 40% 60% 80% 100%

46% 23% 13% 14% 4%

Middle 20%

Second 20%

Bottom 20%

64% 16% 9% 7% 4%

82% 7% 5% 3% 3%

82% 3%3%

1% 11%

18. Role of Social Security, 2000P

Percentage of Older Americans Deriving Given Percent of Income from Social Security

100% of income: 20%

90–99% of income: 11%

50–89% of income: 33%

Source: Social Security Administration, 2002.

Less than 50% of income: 36%

The trustees of the Social Security

system estimate that the system

will be fiscally insolvent by 2041.

At that point, to restore financial

health, benefits would need to be

reduced by about 30%, or tax rates

increased by half, in order to maintain

benefits. Possible reform strategies

include combinations of benefit

reductions, tax increases, or the

greater use of prefunded investments

(whether invested centrally or

through individual private accounts).

Today Social Security accounts for

half or more of income for 6 out of

10 older Americans. Regardless of the

direction taken by reform proposals,

Social Security is likely to remain

an essential component of retirement

income for the baby boom generation.

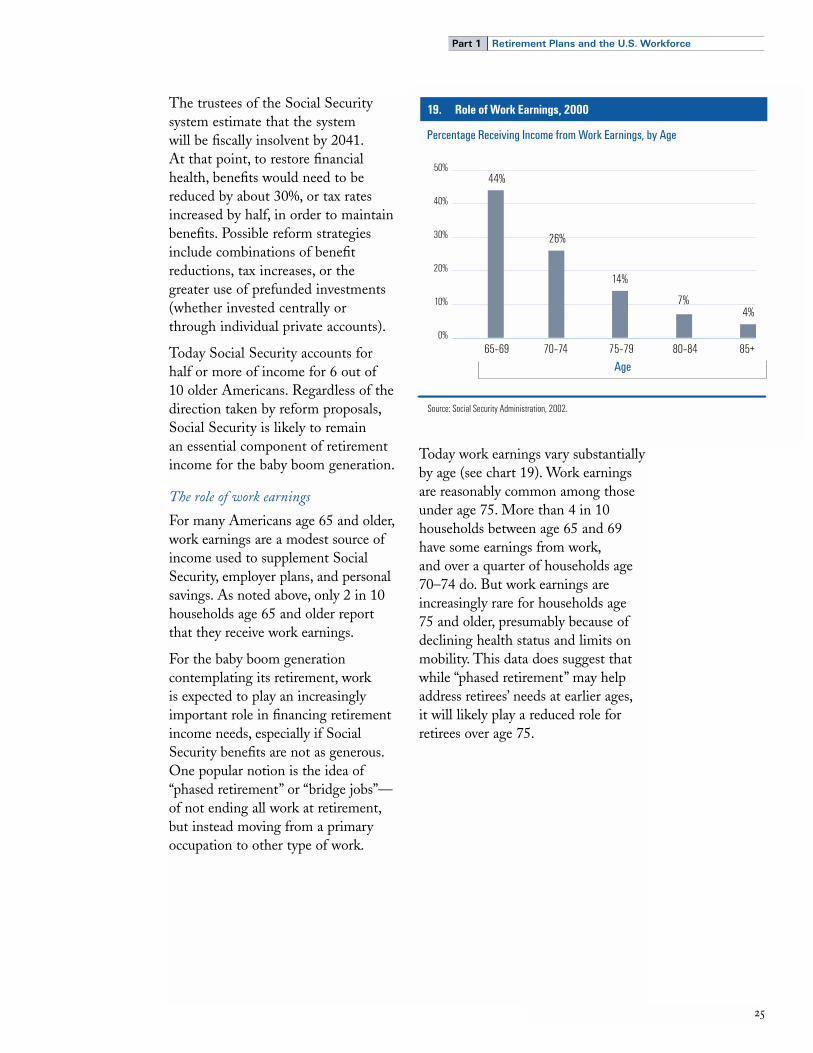

The role of work earnings

For many Americans age 65 and older,

work earnings are a modest source of

income used to supplement Social

Security, employer plans, and personal

savings. As noted above, only 2 in 10

households age 65 and older report

that they receive work earnings.

For the baby boom generation

contemplating its retirement, work

is expected to play an increasingly

important role in financing retirement

income needs, especially if Social

Security benefits are not as generous.

One popular notion is the idea of

“phased retirement” or “bridge jobs”—

of not ending all work at retirement,

but instead moving from a primary

occupation to other type of work.

Today work earnings vary substantially

by age (see chart 19). Work earnings

are reasonably common among those

under age 75. More than 4 in 10

households between age 65 and 69

have some earnings from work,

and over a quarter of households age

70–74 do. But work earnings are

increasingly rare for households age

75 and older, presumably because of

declining health status and limits on

mobility. This data does suggest that

while “phased retirement” may help

address retirees’ needs at earlier ages,

it will likely play a reduced role for

retirees over age 75.

Part 1 Retirement Plans and the U.S. Workforce

19. Role of Work Earnings, 2000

Percentage Receiving Income from Work Earnings, by Age

44%

4%7%

14%

26%

65–69 70–74 75–79 85+80–84

Source: Social Security Administration, 2002.

Age

0%

10%

20%

30%

40%

50%

Vanguard Defined ContributionPlans: Current Features

P A R T T W O

Defined contribution plans have become the dominant type of retirement savings plan sponsored by private sector employers in the U.S. and a critical component of the U.S. savings system.

Over the past 20 years, both

participation and savings rates

in such plans have grown.

Participants today hold high

allocations to equity investments

in pursuit of their long-term

retirement goals. DC plans in

the United States offer a com-

prehensive range of services—

including, for participants,

an array of investment choices,

financial educational materials,

and account access services.

The success of DC plans can

be measured in three key ways—

the rate at which employees

participate in their plan, the rate

at which they contribute to the

plan, and the way in which they

choose to invest their savings.

In this section we look at each

of these three metrics using data

from Vanguard’s universe of

DC recordkeeping clients.

In addition, we examine other

DC plan characteristics

using data from Vanguard

clients, including:

• Average and median

account balances.

• Investment options offered

by sponsors, and their use

by participants.

• Education and advice trends.

• Preretirement access to

savings via loans and in-

service withdrawals.

• Participant distribution

behavior when changing

jobs or retiring.

For plan sponsors and industry

providers, participation rates in DC

plans remain the most visible metric

of success. A number of factors drive

sponsor interest in participation rates:

• Employees perceive retirement

savings plans as a positive benefit,

and sponsors view savings plans as

an integral part of total compensa-

tion. Encouraging participation is

therefore a means of promoting

employee retention and loyalty.

• Under nondiscrimination testing

rules, sponsors must achieve ade-

quate participation by lower-paid

employees if higher-paid workers

are to take maximum advantage

of a 401(k) plan.

• DC plans are an ever-increasing

component of retirement wealth

for American workers. Sponsors

seek to encourage high participation

rates in an effort to promote

retirement security.

Among Vanguard DC plans with

a voluntary employee component,

the average plan participation rate

in 2001 was 76% (see chart 20).

This figure is comparable to other

industry-reported figures for average

plan participation rates.

At both the plan and participant

level, based on both Vanguard and

other industry sources, participation

rates dropped by 3% to 4% between

1999 and 2001. Although there have

been no formal studies on why rates

dropped, we suspect that it is the

result of two factors. First, the eco-

nomic slowdown in 2001 may have

caused some participants to exit

their plans because of economic wor-

ries.10 Second, strong stock market

returns in the late 1990s encouraged

workers to join their savings plans.

In the subsequent bear market, lower

stock returns may have discouraged

newly eligible workers from joining

their retirement savings plan.

Part 2 Vanguard Defined Contribution Plans—Current Features

20. Plan Participation RatesI

Unweighted Average Participation Rate

79% 76%83%80%

1999

Vanguard Profit Sharing/401(k) Council of America

2001

Source: The Vanguard Group, 2001; Greenwich Associates, 2001; Profit Sharing/401(k) Council of America, 2001a.

80% 74%

Greenwich Associates0%

20%

40%

60%

80%

100%

10 Note that participants laid off during the

economic slowdown would not have contributed to

the decline in participation rates, as laid-off workers

would be no longer eligible for plan membership

and so would be excluded from the participation

rate calculation. But currently eligible workers who

temporarily elect not to participate—because a

spouse was laid off or because of worries about

their own financial future—would contribute to

lower participation rates.

Participation Rates

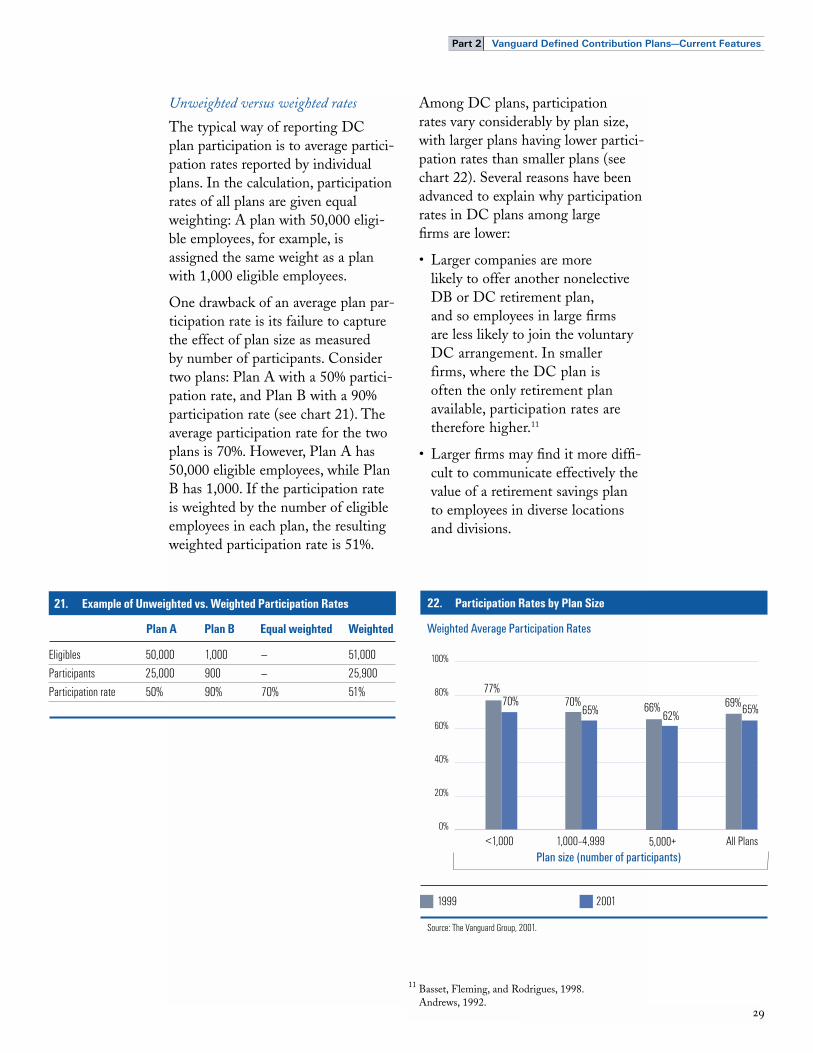

Unweighted versus weighted rates

The typical way of reporting DC

plan participation is to average partici-

pation rates reported by individual

plans. In the calculation, participation

rates of all plans are given equal

weighting: A plan with 50,000 eligi-

ble employees, for example, is

assigned the same weight as a plan

with 1,000 eligible employees.

One drawback of an average plan par-

ticipation rate is its failure to capture

the effect of plan size as measured

by number of participants. Consider

two plans: Plan A with a 50% partici-

pation rate, and Plan B with a 90%

participation rate (see chart 21). The

average participation rate for the two

plans is 70%. However, Plan A has

50,000 eligible employees, while Plan

B has 1,000. If the participation rate

is weighted by the number of eligible

employees in each plan, the resulting

weighted participation rate is 51%.

Among DC plans, participation

rates vary considerably by plan size,

with larger plans having lower partici-

pation rates than smaller plans (see

chart 22). Several reasons have been

advanced to explain why participation

rates in DC plans among large

firms are lower:

• Larger companies are more

likely to offer another nonelective

DB or DC retirement plan,

and so employees in large firms

are less likely to join the voluntary

DC arrangement. In smaller

firms, where the DC plan is

often the only retirement plan

available, participation rates are

therefore higher.11

• Larger firms may find it more diffi-

cult to communicate effectively the

value of a retirement savings plan

to employees in diverse locations

and divisions.

Part 2 Vanguard Defined Contribution Plans—Current Features

11 Basset, Fleming, and Rodrigues, 1998.

Andrews, 1992.

21. Example of Unweighted vs. Weighted Participation Rates

Plan BPlan A Equal weighted Weighted

Eligibles

Participants

Participation rate

1,000

900

90%

—

—

70%

50,000

25,000

50%

51,000

25,900

51%

22. Participation Rates by Plan SizeI

Weighted Average Participation Rates

70%65%

69%65%

1999

1,000–4,999 All Plans

2001

Source: The Vanguard Group, 2001.

77%70%

<1,000

66%62%

5,000+0%

20%

40%

60%

80%

100%

Plan size (number of participants)

While the average plan participation

rate at Vanguard was 76% in 2001,

the weighted participation rate was

65%. One way to interpret these

different figures is that the average

employer is able to attract 3 out

of 4 eligible participants to join a

voluntary DC arrangement—i.e.,

the average plan participation rate is

76%. However, the average employee

across all plans is likely to join a

voluntary DC arrangement in 2 out

of 3 cases—i.e., the weighted plan

participation rate is 65%. The lower

weighted rate is due to the fact that

employees at larger firms are less

likely to join a voluntary DC plan.

As with the unweighted participation

rates, weighted participation rates

fell by 3% to 4% from 1999 to 2001

(see chart 23).

Participation by income and age

Participant rates also vary substan-

tially by income and age. Income

is a key determinant of participation

(see chart 24). Among low-income

employees earning less than $15,000,

about 1 in 5 (19%) employees

participate; among high-income

employees earning more than

$75,000, 9 in 10 (89%) participate.

Part 2 Vanguard Defined Contribution Plans—Current Features

23. Vanguard Unweighted vs. Weighted Participation Rates

Average Participation Rate

79%69%

1999

65%

76%

2001

Unweighted Weighted

Source: The Vanguard Group, 2001.

0%

20%

40%

60%

80%

100%

24. Participation Rates by Income

Weighted Average Participation Rate

19%

89%80%

67% 65%

47%

<$15,000 $15,000–$30,000

$30,001–$50,000

All>$75,000$50,001–$75,000

Source: The Vanguard Group, 2001.

Income

0%

20%

40%

60%

80%

100%

Age is also an important element in

the participation decision. Less than

1 in 3 employees under age 25

participate, while three-quarters of

participants between the ages of 55

and 64 join their employer’s savings

plan (see chart 25).

Defined contribution plans are

intended principally as a savings vehi-

cle for retirement. Along with plan

participation, a critical measure of

success is whether participants are

saving enough to fund an adequate

standard of living during retirement.

Vanguard participants are currently

saving an average of 7.2% of their

incomes in employer-sponsored DC

plans. The corresponding median

savings rate is 6%, meaning that half

of participants are saving above this

rate, and half below (see chart 26).

Both the average and the median

rates have fallen by a full percentage

point since 1999. As with participa-

tion rates, while no formal research

has been done on the reasons for

the decline, we believe that the eco-

nomic slowdown and poor stock

returns may have discouraged savings

behavior, particularly among newly

eligible employees.

Part 2 Vanguard Defined Contribution Plans—Current Features

25. Participation Rates by Age

Weighted Average Participation Rate

31%

75%

60%

75%

65%73%

60%

<25 25–34 35–44 55–64 65+ All45–54

Source: The Vanguard Group, 2001.

Age

0%

20%

40%

60%

80%

100%

Source: The Vanguard Group, 2001.

26. Savings Rates

8.31%

7%7.20%

6%

1999 20011999 20010%

2%

4%

6%

8%

MedianMean

Savings Rates

Distribution of savings rates

Savings rates among participants vary

widely around the average of 7.2%

and the median of 6%. One in 4

participants save between 5% and 6%

of salary. This may be due in part to

the fact that the most common

employer match is 50 cents for each

dollar contributed up to 6%. One in

10 participants saves 2% or less, while

2 in 10 participants save more than

10% of salary (see chart 27).

Demographic influences

As with participation rates, both

income and age are determinants of

savings rates. Not surprisingly, high-

income employees find it easier to

save than do low-income employees.

The most affluent save a median of

7% of income, while less affluent save

5% (see chart 28). This gap would be

greater if not for IRS dollar limits on

contributions ($11,000 in 2001); this

dollar cap effectively prevents very

high income households from saving

at higher percentage rates.

Besides income, savings rates vary

by age, with older workers not sur-

prisingly saving more than younger

workers (see chart 29).

Savings versus deferral rates

A participant’s savings rate measures the

actual contributions made by the partici-

pant in a given year divided by the

participant’s income. Calculating savings

behavior in this way provides the best

measure of actual economic savings.

Another method for calculating

savings behavior is to take an average

of participants’ deferral rates—the

rate at which participants are having

contributions deducted from their

pay. This figure is more readily calcu-

lated from recordkeeping systems

than savings rates. But the average

deferral rate is not a perfect measure

of savings behavior; in fact, it is more

reflective of anticipated or expected

rather than actual savings behavior.

Why would savings and deferral rates

differ? Participants may sign up for

a given deferral rate, but then reduce

or increase it during the year. Other

participants may be capped by IRS

dollar limits. Still others might

Part 2 Vanguard Defined Contribution Plans—Current Features

Source: The Vanguard Group, 2001.

27. Distribution of Savings Rates

Percentage of Participants

15% 16%14%

4%

9%–10% 11%–15% >15%7%–8%

27%

5%–6%

15%

3%–4%

9%

1%–2%

Savings Rates

0%

5%

10%

15%

20%

25%

30%

28. Savings Rates by Income

Median Savings Rate

5.71%

6.93%7.00%

6.00% 6.00%

5.00%

<$15,000 $15,000–$30,000

$30,001–$50,000

All>$75,000$50,001–$75,000

Source: The Vanguard Group, 2001.

Income

0.00%

2.00%

4.00%

6.00%

8.00%

receive additional income at year-end,

such as bonuses, which effectively

reduces their percentage savings rate.12

In 2001 the average Vanguard deferral

rate for participants contributing to

their plan was 8.1%, versus an average

savings rate of 7.2%. Vanguard defer-

ral rates typically run about a percent-

age point or so higher than average

savings rates.

Interestingly, for the first six months

of 2002, Vanguard average deferral

rates rose from 8.1% in 2001 to 8.3%

for the first six months of 2002. This

increase in savings behavior may

be the result of a number of factors,

such as improving economic condi-

tions or the impact of pension reform

legislation, which allows much higher

percentage-of-income contributions

to DC plans. Over time, measuring

actual savings rates as well as deferral

rates will help determine whether this

trend in savings behavior will persist.

A third factor in gauging the success

of a defined contribution plan is

whether participants are taking

appropriate levels of equity market

risk in pursuit of their long-term

goals. Despite the recent bear market

in U.S. stocks, participant equity

holdings are only marginally lower;

participants do not appear to have

significantly shifted their portfolios

away from the equity market over

the past two years.

Asset and contribution allocations

For the average plan, nearly two-

thirds of assets (63%) are invested

directly in equities (see chart 30).

This total includes both diversified

common stock funds and company

stock. If balanced and life-cycle

funds are included in the mix, 3 in 4

plan dollars (76%) are invested in

equity-linked investments, compared

with 78% in 1999.

Part 2 Vanguard Defined Contribution Plans—Current Features

29. Savings Rates by Age

Median Savings Rate

4.62%

6.18%

8.35%7.71%

6.00%6.00%5.84%

<25 25–34 35–44 55–64 65+ All45–54

Source: The Vanguard Group, 2001.

Age

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

30. Plan Asset AllocationP

Vanguard—Defined Contribution PlansTotal equity/balanced: 76%

49% Stock funds

18% Money market/stable value

6% Bond funds

13% Balanced funds

14% Company stock

Source: The Vanguard Group, 2001.

12 Average deferral and savings rates will also differ

because the two rates may be drawn from different

samples of participants.

Participant Investment Decisions

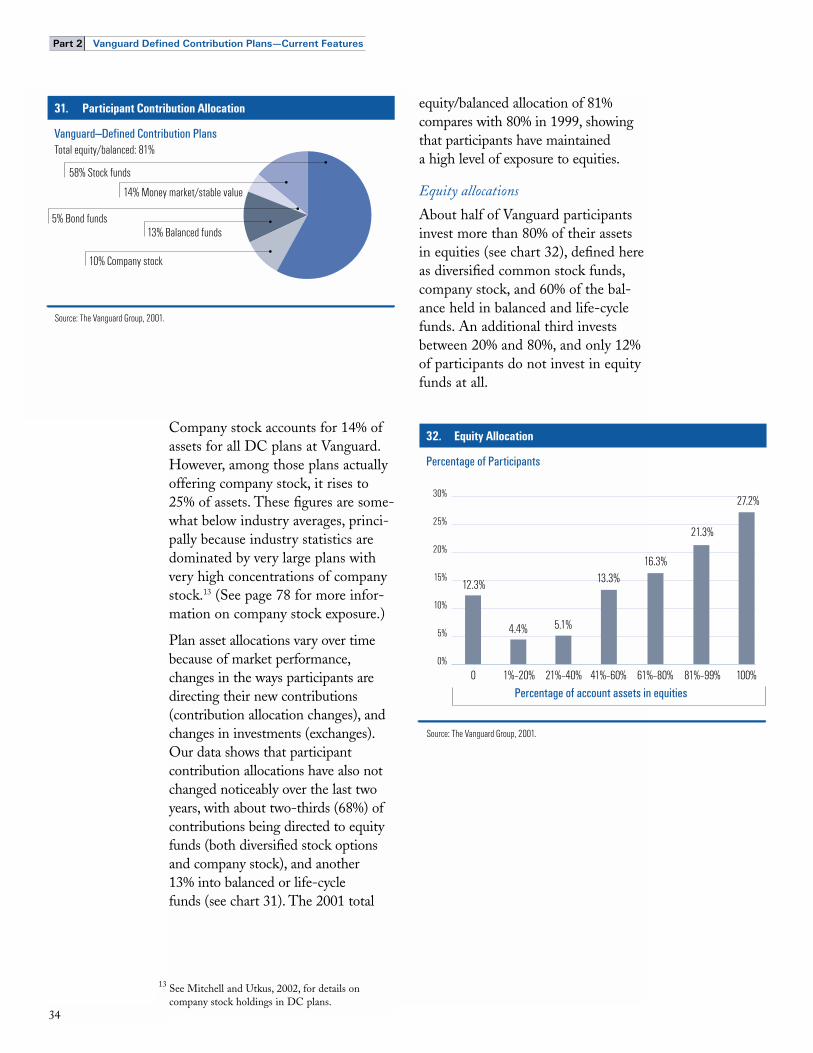

Company stock accounts for 14% of

assets for all DC plans at Vanguard.

However, among those plans actually

offering company stock, it rises to

25% of assets. These figures are some-

what below industry averages, princi-

pally because industry statistics are

dominated by very large plans with

very high concentrations of company

stock.13 (See page 78 for more infor-

mation on company stock exposure.)

Plan asset allocations vary over time

because of market performance,

changes in the ways participants are

directing their new contributions

(contribution allocation changes), and

changes in investments (exchanges).

Our data shows that participant

contribution allocations have also not

changed noticeably over the last two

years, with about two-thirds (68%) of

contributions being directed to equity

funds (both diversified stock options

and company stock), and another

13% into balanced or life-cycle

funds (see chart 31). The 2001 total

equity/balanced allocation of 81%

compares with 80% in 1999, showing

that participants have maintained

a high level of exposure to equities.

Equity allocations

About half of Vanguard participants

invest more than 80% of their assets

in equities (see chart 32), defined here

as diversified common stock funds,

company stock, and 60% of the bal-

ance held in balanced and life-cycle

funds. An additional third invests

between 20% and 80%, and only 12%

of participants do not invest in equity

funds at all.

Part 2 Vanguard Defined Contribution Plans—Current Features

31. Participant Contribution AllocationP

Vanguard—Defined Contribution PlansTotal equity/balanced: 81%

58% Stock funds

14% Money market/stable value

5% Bond funds13% Balanced funds

10% Company stock

Source: The Vanguard Group, 2001.

32. Equity Allocation

Percentage of Participants

12.3% 13.3%

21.3%

16.3%

27.2%

5.1%4.4%

0 1%–20% 21%–40% 61%–80% 81%–99% 100%41%–60%

Source: The Vanguard Group, 2001.

Percentage of account assets in equities

0%

5%

10%

15%

20%

25%

30%

13 See Mitchell and Utkus, 2002, for details on

company stock holdings in DC plans.

The percentage of participants with

more than 80% of their account in

equities has declined over the past

two years, from about 60% to less

than 50% of participants, in line with

the decline in the U.S. equity mar-

kets. Overall this appears to be the

result of two effects: falling stock

market values and modest shifts by

some participants out of equities and

into fixed income investments.

Total equity holdings remain fairly

constant across plan size (see

chart 33). However, among larger

plans there is a substitution of com-

pany stock holdings for diversified

equity funds. Large plans are much

more likely to offer company stock,

and when they do are also more

likely to restrict participants’

ability to diversify out of that stock.

(See page 78 for more information

on company stock exposure.)

Demographic influences

Participant income and age are key

factors influencing investment deci-

sions. Higher-income participants

take on somewhat more equity

market risk, while lower-income par-

ticipants do not. However, at least

among Vanguard clients, the differ-

ence in equity exposure by income

level is not dramatically different. In

2001 participants earning more than

$75,000 had an average of 73% of

assets invested in equities, while par-

ticipants earning less than $15,000

had 64% of account assets in equities

(see chart 34).

Part 2 Vanguard Defined Contribution Plans—Current Features

33. Asset Allocation by Plan Size

StockFunds

CompanyStock

BalancedFunds

TotalEquity

BondFunds

Number of participants

Money Market/Stable Value

<1,000

1,000–4,999

5,000+

All Plans

17%

20%

18%

18%

7%

5%

6%

6%

70%

68%

72%

71%

18%

15%

11%

13%

1%

7%

19%

14%

58%

52%

46%

49%

*Stock, company stock, and 60% of balanced funds. Source: The Vanguard Group, 2001.

Asset Allocation

*

34. Asset Allocation by Income

StockFunds

CompanyStock

BalancedFunds

TotalEquity

BondFunds

Income

Money Market/Stable Value

<$15,000

$15,000–$30,000

$30,001–$50,000

$50,001–$75,000

>$75,000

All (mean)

24%

25%

22%

19%

16%

18%

6%

6%

6%

5%

5%

6%

64%

63%

66%

70%

73%

71%

14%

14%

14%

14%

12%

13%

15%

13%

13%

14%

15%

14%

41%

42%

45%

48%

51%

49%

*Stock, company stock, and 60% of balanced funds. Source: The Vanguard Group, 2001.

Asset Allocation

*

Younger participants generally take

on more equity market exposure than

older participants (see chart 35).

(The data for participants under age

25 is an anomaly undoubtedly due to

a very small sample size.) As a whole,

participants appear to have taken the

“time diversification” principle to

heart—namely, the longer your time

horizon, the higher your commitment

to equities.

It remains a topic of debate as to how

older participants end up with more

conservative allocations. One explana-

tion is that, as they age, participants

gradually shift monies from equities

to fixed income. This is a common

financial education principle.

A second theory is the so-called

“demographic cohort” effect.

Participants of a given age belong to

a generational cohort, and that cohort

develops similar investment risk

preferences based on its shared life

experiences. In other words, younger

investors may hold more in equities

because of common generational per-

ceptions—e.g., greater awareness of

the returns of equities, the influence

of the bull market, greater acceptance

of risk-taking. Although research has

not resolved the debate between the

two theories, it’s likely that both fac-

tors—the lower risk tolerance of older

investors and common demographic

cohort experiences—play a role.

Part 2 Vanguard Defined Contribution Plans—Current Features

35. Asset Allocation by Age

StockFunds

CompanyStock

BalancedFunds

TotalEquity

BondFunds

Age

Money Market/Stable Value

<25

25–34

35–44

45–54

55–64

65+

All (mean)

21%

10%

12%

17%

24%

34%

18%

6%

4%

5%

6%

7%

9%

6%

64%

80%

79%

72%

64%

51%

71%

23%

12%

13%

13%

13%

13%

13%

9%

13%

15%

15%

13%

9%

14%

41%

60%

56%

49%

43%

34%

49%

*Stock, company stock, and 60% of balanced funds. Source: The Vanguard Group, 2001.

Asset Allocation

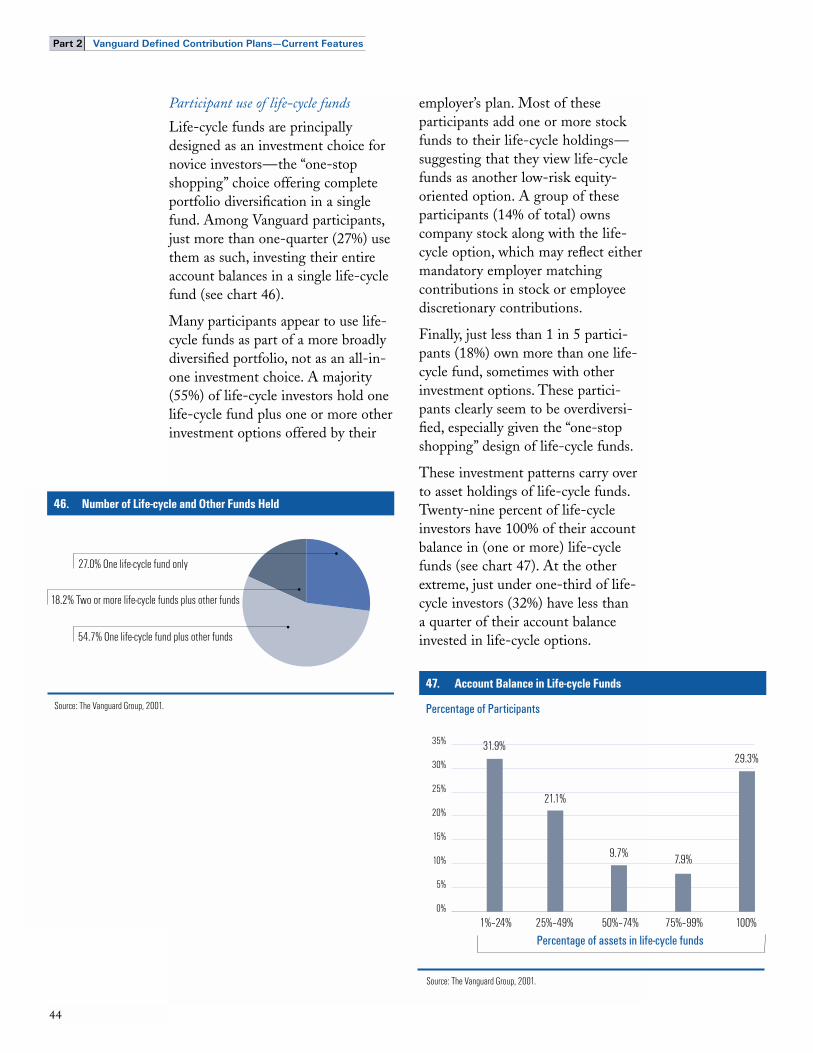

*

Defined contribution plan account

balances are important on two counts:

• Retirement savings adequacy.

Account balances measure how

much workers have accumulated

for retirement at their current

employer, and thus influence

an important policy question—

Are workers saving enough

for retirement?

• Economics of retirement providers.

Average balances are also of interest

to retirement services providers

and sponsors negotiating plan fees.

Most revenues for providers are

typically generated through asset-

based fees. The economics of

the retirement services business

is therefore directly linked to

average balances.

On both of these questions, current

DC plan balances only tell part

of the story. In the United States,

DC plans are not a closed system;

when employees change jobs or retire,

monies are frequently rolled over to

IRAs.14 As a result, because of job

changes, participants’ current balances

do not reflect lifetime DC savings.

Job changes are reasonably com-

mon—among Vanguard recordkeep-

ing participants, median plan tenure

is six years and median employment

tenure is ten years.

A complete analysis of retirement

savings adequacy must reflect not only