américa latina em cifras 2018 - alacero.org · américa latina em cifras latin america in figures...

TRANSCRIPT

América Latina em Cifras 2018LATIN AMERICA IN FIGURES2018

2. Alacero

_ _

Alacero - Latin American Steel Association - is the non-

profit civil association that brings together the steel value

chain of Latin America to promote the values of regional

integration, technological innovation, excellence in

human resources, safety at work, corporate responsibility

and socio-environmental sustainability.

Founded in 1959, it is integrated by more than 60

producing and related companies from 19 countries in

Latin America and the world, whose production is close

to 70 million tons per year.

Alacero is recognized as a Special Consultant

Organization by the United Nations.

América Latina em Cifras Latin America in Figures 3

_ _

COVER

Santa IfIgenIa VIaduct, São Paulo, BrazIl

CAPA

ViAduto SAntA ifigêniA São PAulo, BrASil

Alacero - Associação Latino-Americana do Aço -

é uma entidade civil sem fins lucrativos que reúne

a cadeia de valor do aço da América Latina. Seus

associados desenvolvem suas atividades em 19 países

do mundo e, sua produção é de aproximadamente 70

milhões de toneladas anuais, representando 95% do

aço fabricado na América Latina.

Fundada em 1959, a entidade busca fomentar os

valores de integração regional, inovação tecnológica,

excelência em recursos humanos, responsabilidade

empresarial e sustentabilidade socioambiental.

A Alacero é reconhecida como Organismo Consultor

Especial para as Nações Unidas.

© Alf Ribeiro / Shutterstock.com

4. Alacero

_ _

ConteúdoContent

_Alacero´s Vision is to be the regional institution representing the steel industry in Latin America to promote and support its sustain-ability on the basis of its key role in the development of the region.

_A visão da Alacero é ser a instituição regional que representa a indústria do aço na América Latina para promover a sustentabilidade com base em sua importância para o desenvolvimento da região.

© Fernando Romero Enterprise · Foster and Partners · AICM · Aerial.

Proporcionada por Grupo Aeroportuario de la Ciudad de México.

América Latina em Cifras Latin America in Figures 5

_ _

P. 06

P.08

P. 10

P.12

P. 18

P.26

P.30

P.34

IntroduçãoForeword

Sócios da Alacero Members of Alacero

3 Indicadores3 key figures

Produção de aço bruto Crude steel production

Produção e consumo de laminadosFinished steel production and consumption

Comércio siderúrgico latino-americanoLatin American steel trade

Indicadores econômicos e siderúrgicos da América Latina Latin America: Economic and steel indicators

Siderurgia chinesa: impacto sobre a América LatinaChinese steel industry: Impact on Latin America

01

02.

03.

04.

05.

06.

07.

08.

6. Alacero

_ _

01. IntroduçãoForeword

_Alacero has undertaken to encourage cooperation between companies and regional associations to combat unfair trade, favoring fair competition and good practices to all its participants.

_A Alacero comprometeu-se a incentivar a cooperação entre empresas e associações regionais para combater o comércio desleal, favorecendo a concorrência leal e boas práticas para todos os seus participantes.

_ _América Latina em Cifras Latin America in Figures 7

A economia latino-americana man-

tém a taxa de crescimento apresen-

tada no primeiro trimestre de 2017.

Apesar da incerteza política, das

crescentes tensões comerciais e da

forte crise financeira na Argentina,

a América Latina espera alcançar

um crescimento de 1,2% do PIB

em 2018, apoiada por um cresci-

mento global mais forte e pelos

altos preços das commodities.

Em 2018, o uso aparente de aço al-

cançará 68,5 milhões de toneladas

(Mt), enquanto a produção de aços

laminados alcançará 55,9 milhões,

1,3% e 5,6% maiores que em 2017,

respectivamente.

As previsões incluem um aumento

no consumo mundial de 3,9% e

6% na China.

As importações totais da América

Latina atingirão 23,5 Mt, o que

representa retração de 6,5% em

relação a 2017, porém o consumo

regional é suprido por 34% pelas

importações.

Desde 2015, os governos regionais,

em cooperação com empresas

siderúrgicas, fortaleceram seus

esforços para nivelar o campo

de atuação, estabelecendo ações

antidumping e salvaguardas, bus-

cando assegurar a competitividade

internacional do setor. Atualmente,

a América Latina tem 66 ações de

defesa comercial em vigor, 44 delas

contra a China.

The Latin American economy maintains the growth rate that began the first trimester of previous year. Despite the political uncertainty, the escalatory trade tensions, and the strong financial crisis in Argentina, Latin America expects to set a 1.2% GDP expansion in 2018 supported by stronger global growth and the high prices of commodities.In 2018, apparent steel use will reach to 68.5 million tons (Mt), while finished steel output will reach to 55.9 Mt, 1.3% and 5.6% higher than 2017, respectively.Forecasts includes an increase in world consumption of 3.9%, and 6.0% in China.Latin America total imports will reach 23.5 Mt, which represents a contraction of 6% compared to 2017, however regional consumption is supplied by 34% for these imports.Since 2015, the regional governments in cooperation with steel companies have strengthened their efforts to level the playing field, establishing antidumping actions and safeguards, pursuing to ensure international competitiveness in the industry. Currently, Latin America has 66 trade defense actions in force, 44 of these are against China.

Francisco Leal

Diretor Geral / General DirectorAlacero

8. Alacero

_ _ 8. Alacero

_ _

ArgentinaAcerbrag

Acindar Grupo AcelorMittal

Cámara Argentina del Acero

Gerdau

Instituto Argentino

de Siderurgia – IAS

Tenaris

Ternium

BrasilArcelorMittal Long Carbon

Americas

ArcelorMittal Tubarão. Aços

Planos

Companhia Siderúrgica

Nacional - CSN

Gerdau

Instituto Aço Brasil

Ternium

USIMINAS

Votorantim Siderurgia – VS

ChileAZA

CAP Acero

CAP Minería

Instituto Chileno del Acero

- ICHA

México Altos Hornos de México –

AHMSA

ArcelorMittal México

Autlán

Cámara Nacional de la

Industria del Hierro y del Acero

– CANACERO

Deacero

Gerdau

Grupo Villacero

Tenaris

Ternium

PeruCorporación Aceros Arequipa

Gerdau

República DominicanaAsociación Dominicana del

Acero – ADOACERO

Gerdau Metaldom

UruguaiGerdau

ColômbiaAcerías de Colombia – ACESCO

Acerías Paz del Río

ANDI-Cámara Fedemetal

Comité Colombiano de

Productores de Acero de ANDI

Gerdau

Tenaris

Ternium

Costa RicaMETALCO

EquadorAcerías Nacionales del Ecuador –

ANDEC

Federación Ecuatoriana

de Industrias del Metal –

FEDIMETAL

Novacero

02. Sócios ativos da AlaceroActive members of Alacero

América Latina em Cifras Latin America in Figures 9

_ __ _

Os sócios da Alacero produzem cerca de 70 milhões de toneladas por ano na região.

Alacero´s members produce about 70 million tons a year in the region.

RepúblicaDominicana

Uruguai

Brasil

Colômbia

México

Costa Rica

Equador

Peru

Chile

Argentina

10. Alacero

_ _

3 key figures to understand the steel industry today

Global Overcapacity

tons is the estimated global overcapacity installed, in which China is responsible for 50%, with 280 million tons. This level is equivalent to 4.1 times the steel consumption in Latin America.

Chinese Steel Industry

tons was the Chinese´s production of crude steel in 2017. Meanwhile, China’s apparent steel consumption recorded 737 million tons, while total exports reached 73 million tons.

Unfair Trade

in force antidumping resolutions and/or safeguards related to steel products in Latin America are against China.

560 million

832 million

44 out of 66

© Marco Mendizábal

América Latina em Cifras Latin America in Figures 11

_ _

3 indicadores para entender a indústria do aço hoje

Excesso de Capacidade Global

de toneladas é a estimativa sobre capacidade instalada a nível global,

na qual a China é responsável por 50%, com 280 milhões de toneladas.

O que representa 4,1 vezes o consumo de aço na América Latina.

Siderurgia Chinesa

de toneladas foi a produção de aço bruto da China em 2017. Por sua

vez, o consumo aparente de laminados registrou 737 milhões de

toneladas, enquanto as exportações totais atingiram 73 milhões de

toneladas.

Comércio Desleal

ações de defesa comercial e/ou antidumping relacionadas ao aço, em

vigor na América Latina, são contra a China.

560 milhões

832 milhões

44 de 66

12. Alacero

_ _

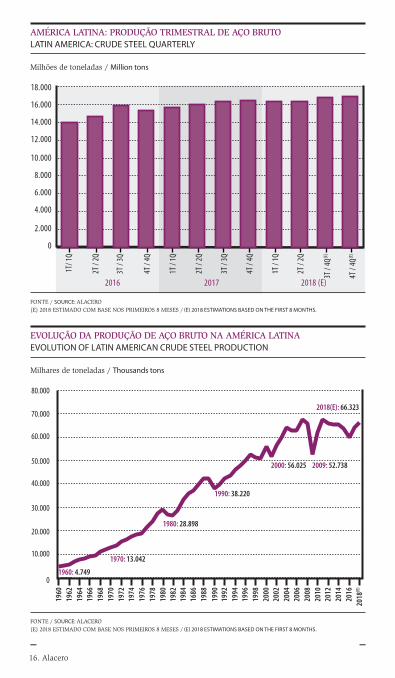

04. Produção de aço brutoCrude steel production

12. Alacero

_The steel industry is fundamental for the metal-mechanic chain’ s development

_A indústria do aço é fundamental para o desenvolvimento da cadeia metal-mecânica

América Latina em Cifras Latin America in Figures 13

_ _

O ano de 2017 foi um ponto

decisivo para a indústria, apoiado

em condições mais favoráveis para

a recuperação produtiva e um

moderado aumento nos preços do

mercado siderúrgico. O ano de 2018

começou com expectativas muito

boas, que se mantêm apesar das

adversidades internas e externas

que ocorreram até o momento.

Até o final de 2018, a produção

de aço bruto deverá atingir 66,3

milhões de toneladas, o que

representaria um aumento de 3,2%

em relação ao ano anterior.

The recovery continues

The year 2017 was a turning point for the industry supported by better conditions for the productive recovery and a moderate rise in the prices of the steel market. 2018 began with very good expectations, which have remained despite internal and external adversities that have been faced so far this year.By the end of 2018, crude steel production is expected to reach 66.3 million tons, which represents an increase of 3.2% over the previous year.

Ritmo de recuperação é mantido

14. Alacero

_ _

China

Japão / Japan

Índia

Estados Unidos / United States

Rússia

Coreia do Sul / South Korea

Alemanha / Germany

Turquia / Turkey

Brasil / Brazil

Itália / Italy

Taiwan - China

Ucrânia / Ukraine

Irã / Iran

México / Mexico

França / France

Espanha / Spain

Canadá

Vietnã

Polônia / Poland

Austria

Bélgica / Belgium

Reino Unido / United Kingdom

Egito / Egypt

Holanda / The Netherlands

África do Sul / South Africa

Austrália

Eslovaquia / Slovak Republic

Paquistão / Pakistan

Arábia Saudita / Saudi Arabia

Indonésia

Outros / Other

Total Mundial / World Total

1

2

3

4

5

6

7

8

9

11

12

10

14

13

15

16

17

19

18

22

20

21

28

23

24

27

29

36

25

29

807,6

104,8

95,5

78,5

70,5

68,6

42,1

33,2

31,3

23,4

21,8

24,2

17,9

18,8

14,4

13,6

12,6

7,8

9

7,4

7,7

7,6

5

6,9

6,1

5,3

4,8

3,6

5,5

4,7

66,8

1.627,0

2016

Ranking Volume

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

831,7

104,7

101,4

81,6

71,3

71

43,4

37,5

34,4

24,1

22,4

21,3

21,2

19,9

15,5

14,5

13,6

11,5

10,3

8,1

7,8

7,5

6,9

6,8

6,3

5,3

5

5

4,8

4,8

69,8

1.689,4

2017

VolumeRanking

FONTE / SOURCE: WORLDSTEEL IN FIGURES 2018

País / Country

MUNDO: RANKING DE PRODUÇÃO DE AÇO BRUTOWORLD: RANKING OF CRUDE STEEL PRODUCTION

Milhões de toneladas / Million tons

REPARTICIÓN REGIONAL DE LAPRODUCCIÓN DE ACERO CRUDO 2018(E)

REGIONAL SHARE OF CRUDE STEELPRODUCTION 2018(E)

Brasil/Brazil (55%)Argentina (8%)Chile (2%)

México/Mexico (32%)Peru (2%)Outro/Other (4%)

2%

4%2%

8%

32% 55%

América Latina em Cifras Latin America in Figures 15

_

PRODUÇÃO LATINO-AMERICANA DE AÇO BRUTO 2018(E)

LATIN AMERICAN CRUDE STEELPRODUCTION 2018(E)

milhões de

toneladas

million tons66,3

da produção

mundial

of global production

3,7% vai aumentar a

produção vs. 2017

production willincrease vs. 2017

3,2%

Brasil / Brazil

México / Mexico

Argentina

Peru

Chile

Colômbia / Colombia

Equador / Ecuador

Guatemala

Cuba

Venezuela

El Salvador

Uruguai / Uruguay

Outros / Other Latam

Total

33.897

18.930

5.488

1.078

1.118

1.079

667

395

256

1.485

121

94

638

65.247

33.256

18.228

5.028

1.082

1.358

1.112

720

403

284

1.345

124

97

639

63.676

31.275

18.811

4.126

1.168

1.272

1.153

576

314

244

553

100

61

70

59.723

34.365

19.924

4.624

1.207

1.253

1.158

561

294

221

444

96

58

24

64.229

35.209

20.694

5.458

1.240

1.157

1.098

583

300

225

173

99

60

25

66.323

2%

4%

18%

3%

-8%

-5%

4%

2%

2%

-61%

3%

4%

4%

3%

201620152014 2017 2018(E) Var.́ 18/́ 17

AMÉRICA LATINA: PRODUÇÃO DE AÇO BRUTO POR PAÍSESLATIN AMERICA: CRUDE STEEL PRODUCTION BY COUNTRY

País / Country

FONTE / SOURCE: ALACERO(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHSOUTROS LATAM INCLUEM A PARAGUAI E TRINIDAD & TOBAGO / OTHER LATAM INCLUDES PARAGUAY AND TRINIDAD & TOBAGO

Milhares de toneladas / Thousand tons

FONTE / SOURCE: ALACERO(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

DISTRIBUIÇÃO REGIONAL DA PRODUÇÃO DE AÇO BRUTO 2018(E)

REGIONAL SHARE CRUDE STEELPRODUCTION 2018(E)

REPARTICIÓN REGIONAL DE LAPRODUCCIÓN DE ACERO CRUDO 2018(E)

REGIONAL SHARE OF CRUDE STEELPRODUCTION 2018(E)

Brasil/Brazil (55%)Argentina (8%)Chile (2%)

México/Mexico (32%)Perú/Peru (2%)Otros/Other (4%)

2%

4%2%

8%

32% 55%

16. Alacero

_ _

1960: 4.749

1970: 13.042

1980: 28.898

1990: 38.220

2000: 56.025 2009: 52.738

2018(E): 66.323

1962

1960

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1686

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

(E)

FONTE / SOURCE: ALACERO(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS BASED ON THE FIRST 8 MONTHS.

2016 2017 2018 (E)

18.000

16.000

14.000

12.000

10.000

8.000

6.000

4.000

2.000

0

AMÉRICA LATINA: PRODUÇÃO TRIMESTRAL DE AÇO BRUTOLATIN AMERICA: CRUDE STEEL QUARTERLY

Milhões de toneladas / Million tons

EVOLUÇÃO DA PRODUÇÃO DE AÇO BRUTO NA AMÉRICA LATINAEVOLUTION OF LATIN AMERICAN CRUDE STEEL PRODUCTION

Milhares de toneladas / Thousands tons

FONTE / SOURCE: ALACERO(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS BASED ON THE FIRST 8 MONTHS.

América Latina em Cifras Latin America in Figures 17

_ _

AMÉRICA LATINA: PRODUÇÃO DE FERRO PRIMÁRIO(A) LATIN AMERICA: PRIMARY IRON PRODUCTION (A)

Brasil / Brazil

México / Mexico

Argentina

Chile

Venezuela

Colômbia / Colombia

Paraguai / Paraguay

Trinidad & Tobago

Peru

América Latina /

Latin America

27.016

11.095

4.427

584

1.402

234

71

2.168

88

47.086

27.803

10.074

3.934

644

1.356

240

73

2.199

72

46.396

26.036

9.782

2.914

677

659

225

50

129

11

40.482

28.426

10.256

3.402

670

491

203

38

-

-

43.486

28.362

10.373

3.951

664

491

213

39

-

-

44.093

0%

1%

16%

-1%

0%

5%

4%

nd

nd

1%

201620152014 2017 2018(E) Var.́ 18/́ 17País / Country

Milhares de toneladas / Thousand tons

FONTE / SOURCE: ALACERO (A) FERRO PRIMÁRIO INCLUI FERRO GUSA E FERRO ESPONJA / (A) PRIMARY IRON INCLUDES PIG IRON AND SPONGE IRON.(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS BASED ON THE FIRST 8 MONTHS.

PRODUÇÃO DE FERRO PRIMÁRIO 2018(E)

PRIMARY IRON PRODUCTION 2018(E)

milhões de

toneladas

million tons44,1

do ferro primário regional é produzido no Brasil

of the primary iron production comes from Brazil

64%

vai aumentar a

produção vs. 2017

production increase vs. 2017

1,4%

DISTRIBUIÇÃO DA PRODUÇÃO DE FERRO PRIMÁRIO POR PAÍSPRIMARY IRON PRODUCTION DISTRIBUTION BY COUNTRIES

DISTRIBUCIÓN DE LA PRODUCCIÓN DE HIERRO PRIMARIO POR PAÍSES

PRIMARY IRON PRODUCTION DISTRIBUTION BY COUNTRIES

Brasil/Brazil (65%)Argentina (9%)Chile (1%)

México/Mexico (24%)Venezuela (2%)Outro/Other (0%)

1%2% 1%

65%

24%

9%

FONTE / SOURCE: ALACERO

DISTRIBUCIÓN DE LA PRODUCCIÓN DE HIERRO PRIMARIO POR PAÍSES

PRIMARY IRON PRODUCTION DISTRIBUTION BY COUNTRIES

Brasil/Brazil (65%)Argentina (9%)Chile (1%)

México/Mexico (24%)Venezuela (2%)Otros/Other (0%)

1%2% 1%

65%

24%

9%

18. Alacero

_ _

05. Produção e consumo de laminados Finished steel production and consumption

_O aço está presente em todas as atividades diárias, tornando a vida diária mais fácil e prazerosa

_Steel is present in all our everyday activities, making our life easier and more enjoyable.

América Latina em Cifras Latin America in Figures 19

_ _

2018: Um bom ano apesar das adversidades

Em 2018, a demanda por laminados

na América Latina deve crescer

1,3% em relação a 2017, atingindo

68,5 milhões de toneladas,

crescendo abaixo do potencial da

região devido a fatores internos; a

incerteza política latente no Brasil,

no México e na Colômbia devido

ao ciclo eleitoral, bem como a

crise financeira na Argentina e

fatores externos; as crescentes

tensões comerciais causadas pelo

protecionismo dos Estados Unidos.

Além disso, prevê-se um aumento

no consumo global de 3,9% e 6,0%

na China. A produção de laminados

na região, em 2018, alcançará

52,8 milhões de toneladas, o que

representa um aumento de 3,2%

em relação a 2017.

2018: A good year despite the adversities

In 2018, the apparent finished steel use in Latin America is expected to increase 1.3% versus 2017, reaching 68.5 million tons, growing below the potential of the region due to internal factors; the political uncer-tainty latent in Brazil, Mexico and Colombia due to the electoral cycle, and the financial crisis in Argentina, and external factors; the escalatory trade tensions caused by the United States protectionism.Additionally, an increase in global consumption of 3.9% and 6.0% in China is forecast. The production of finished steel in the region will reach 52.8 million tons in 2018, which represents an increase of 3.2% compared to 2017.

20. Alacero

_ _

Argentina

Brasil / Brazil

Chile

Colômbia / Colombia

México / Mexico

Peru

Venezuela

Outros / Other

América Latina /

Latin America

14.895

8.803

13.549

6.089

9.674

6.150

7.923

5.223

8.378

12.709

8.701

13.738

5.800

8.815

6.178

7.688

5.282

8.000

14.463

9.896

15.068

6.380

9.319

6.732

6.890

5.536

8.722

10.667

9.127

16.143

6.761

9.614

7.118

3.300

5.744

8.196

-26%

-8%

7%

6%

3%

6%

-52%

4%

-6%

20162015 2017 2018E) Var.́ 18/́ 17

AMÉRICA LATINA: PRODUTO INTERNO BRUTO PER CAPITA (US$)LATIN AMERICA: GROSS DOMESTIC PRODUCT PER CAPITA (US$)

País / Country

FONTE / SOURCE: IMF WEO OCTOBER 2018. CEPAL / ECLAC (E) 2018 ESTIMADO / (E) 2018 ESTIMATED.OUTROS INCLUEM O RESTO DOS PAÍSES DA AMÉRICA LATINA / OTHERS INCLUYE THE RESTO OF LATIN AMERICAN´S COUNTRIES

FONTE / SOURCE: IMF WEO OCTOBER 2018. CEPAL / ECLAC (E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS BASED ON THE FIRST 8 MONTHS.

2016

140

2015

2014

2013

2012

2011

2010

2009

2008

120

140

80

60

40

Kg

12.000

10.000

8.000

6.000

4.000

US$

2017

107

85

113 113118 119 118

114

104 107

7.711

9.9449.776

8.3788.000

8.722

9.9149.983

8.674

7.016

2018

(E)

107

8.196

AMÉRICA LATINA: RELAÇÃO ENTRE CONSUMO DE AÇO E PIB (PER CAPITA)LATIN AMERICA: RELATIONSHIP BETWEEN ASU (PER CAPITA) AND GDP (PER CAPITA)

Consumo de aço per capita / ASU per capitaPIB per cápita / GDP per capita

US$ - precios corrientes / US$ current prices

Kg uS$

13.209

12.112

14.620

7.999

10.981

6.563

7.030

5.242

9.776

2014

América Latina em Cifras Latin America in Figures 21

_ _

Aço e crescimento

A indústria siderúrgica é um

dos pilares do desenvolvimento

econômico e social da América

Latina, registrando uma alta

proporção de consumo aparente

de aço per capita com o Produto

Interno Bruto per capita (PIB pc).

Os níveis atuais de consumo de

aço per capita continuam bem

abaixo da média mundial, um sinal

do caminho que ainda precisa ser

percorrido.

Steel and growth

The steel industry is one of the pillars of the economic and social development of Latin America, showing a high correlation between Apparent Steel Consumption per capita (ASU pc) and GDP pp. The current ASU pp levels remain well below the world average, sign that we still have a long way to go.

Argentina

Brasil / BrazilChile

Colômbia / Colombia

México / MexicoPeru

Venezuela

Outros Latam /

Other LatamAmérica Latina /

Latin AmericaUnião Européia

(28) / Europea Union (28)*Estados Unidos /

United States*Coreia do Sul /

South Korea*Mundo / World*

117

124

148

83

191

94

68

59

118

294

337

1.102

212

201620152014 2017 2018(E) Var.́ 18/́ 17

AMÉRICA LATINA: CONSUMO APARENTE DE AÇO LAMINADO PER CAPITALATIN AMERICA: APPARENT STEEL USE PER CAPITA

País / Country

FONTE / SOURCE: ALACERO - CEPAL/ECLAC - WORLDSTEEL (PRELIMINAR SRO OCT. 2018 / PRELIMINARY SRO OCT. 2018)OUTROS INCLUI O RESTO DOS PAÍSES DA AMÉRICA LATINA / OTHER LATAM INCLUDES REST OF LATIN AMERICA(E) ESTIMADO / (E) ESTIMATED

KgS

121

102

156

84

200

111

60

59

114

303

300

1.103

204

96

87

153

75

202

103

24

56

104

310

285

1.124

204

112

91

152

73

207

114

16

56

107

320

301

1.106

211

111

95

152

74

200

116

16

57

107

327

306

1.057

217

0%

4%

0%

2%

-3%

2%

-1%

2%

0%

2%

2%

-4%

3%

22. Alacero

_

Ásia

China

União Europeia (28)

/ European Union (28)

América do Norte/

North America

América Latina /

Latin America

Oriente Médio /

Middle East

Países CIS /

CIS Countries

Outros Europa /

Others Europe

África

Austrália & N.Z.

Mundo / World

1.011,1

710,8

148,9

122,7

72,3

54,5

57,7

37,0

37,4

7,6

1.550

977,5

672,3

153,7

109,5

70,5

53,8

52,4

40,1

38,7

7,4

1.504

1.000,6

681,0

157,6

106,9

64,9

53,1

50,9

40,7

37,6

6,9

1.520

1.058,5

736,8

163,0

114,3

67,6

53,3

54,0

42,6

34,9

6,6

1.595

1.110,5

781,0

166,8

117,3

68,5

54,5

54,8

41,9

36,0

7,3

1.658

4,9%

6,0%

2,3%

2,6%

1,3%

2,1%

1,4%

-1,6%

3,1%

11,2%

3,9%

201620152014 2017 Var.́ 18/́ 17

MUNDO: CONSUMO APARENTE DE PRODUTOS LAMINADOS WORLD: APPARENT FINISHED STEEL USE

Região / Region

Milhões de toneladas / Million tons

Consumo aparente de aço

Estima-se que o consumo aparente

de aço em 2018 na América Latina

cresça 1,3% em relação a 2017,

ante uma média mundial que

registrará um crescimento de 3,9%.

Por outro lado, o consumo da

China crescerá 6%, e o da América

do Norte crescerá 2,6%. Enquanto

isso, a União Europeia (28) terá um

crescimento de 2,3% em 2018.

Apparent steel use

The steel industry is one of the pillars of the economic and social development of Latin America, showing a high correlation between Apparent Steel Consumption per capita (ASU pc) and GDP pp. The current ASU pp levels remain well below the world average, sign that we still have a long way to go.

2018(E)

FONTES: ALACERO PARA AMÉRICA LATINA E WORLDSTEEL PRELIMINAR SRO OCTUBRE 2018 PARA RESTO DO MUNDO /SOURCE: ALACERO FOR LATIN AMERICA AND WORLDSTEEL PRELIMINARY SRO OCTOBER 2018 FOR ROW(E) 2018 ESTIMADO / (E) 2018 ESTIMATED

América Latina em Cifras Latin America in Figures 23

_ _

Argentina

Brasil / Brazil

Chile

Colômbia / Colombia

México / Mexico

Peru

Venezuela

Outros / Other

América Latina /

Latin America

5,0

25,6

2,6

4,0

23,5

2,9

2,0

6,7

72,3

5,3

21,3

2,8

4,0

25,0

3,5

1,8

6,9

70,5

4,2

18,2

2,8

3,7

25,5

3,3

0,7

6,6

64,9

4,9

19,2

2,8

3,6

26,4

3,7

0,5

6,6

67,6

5,0

20,1

2,8

3,7

25,9

3,8

0,5

6,8

68,5

0,8%

4,9%

1,1%

2,5%

-1,9%

3,3%

0,0%

2,7%

1,3%

201620152014 2017 2018(E) Var.́ 18/́ 17

AMÉRICA LATINA: CONSUMO APARENTE DE PRODUTOS LAMINADOS LATIN AMERICA: APPARENT FINISHED STEEL USE

País / Country

Milhões de toneladas / Million tons

FONTE / SOURCE: ALACERO. INFORMAÇÃO FORNECIDA PELAS SECRETARIAS REGIONAIS / ALACERO. DATA SUBMITED BY REGIONAL SECRETARIES. NOTA / NOTE: 2018 SÃO PROJEÇÕES FEITAS COM BASE NO SRO DA AMÉRICA LATINA / 2018 ARE FORECASTS BASED ON THE LATIN AMERICA SRO.OUTROS INCLUEM CUBA, EQUADOR, EL SALVADOR, GUATEMALA, HONDURAS, PANAMA, PARAGUAI, REPÚBLICA DOMINICANA E URUGUAI / OTHERS INCLUDE CUBA, DOMINICAN REPUBLIC, ECUADOR, EL SALVADOR, GUATEMALA, HONDURAS, PANAMA, PARAGUAY, AND URUGUAY.

FONTE / SOURCE: ALACERO

Construção/Construction (51%) Electrodomesticos/Domestic Appliances (1%)Equipamentos Elétricos/Electrical Equipment (2%)

Maquinaria Mecânica/Mechanical Machinery (14%)

Produtos Métalicos/Metal Products (18%)

Automotive/Automotive (12%)Outro Transporte/Other Transport (1%)

51%

12%

18%

14%

1%

1%2%

AMÉRICA LATINA: USO DE AÇO POR SETORES EM 2017LATIN AMERICA: STEEL USE BY SECTORS 2017

24. Alacero

México / Mexico

Brasil / Brazil

Peru

Argentina

Colômbia / Colombia

Chile

Ecuador / Equador

Guatemala

Costa Rica

Rep. Dominicana /

Dominican Rep.

Venezuela

Cuba

El Salvador

Uruguai / Uruguay

Outros / Others

América Latina /

Latin America

Brasil / Brazil

México / Mexico

Argentina

Colômbia / Colombia

Venezuela

Peru

Rep. Dominicana /

Dominican Rep.

América Latina /

Latin America

8.084

10.688

1.725

1.312

1.394

1.017

707

574

516

460

726

105

83

79

425

27.894

14.229

8.594

2.546

410

635

60

-

26.474

8.301

9.253

1.656

1.291

1.420

1.035

761

591

426

474

504

126

85

81

438

26.442

13.388

8.533

2.556

440

756

52

-

25.725

8.742

8.647

1.333

1.360

1.326

1.081

696

474

436

382

305

130

97

75

19

25.102

12.273

9.154

2.274

447

225

57

46

24.476

8.731

8.734

1.594

1.462

1.414

1.062

710

454

417

378

158

114

90

66

21

25.406

13.688

9.023

2.374

482

246

55

54

25.922

9.227

9.365

1.885

1.503

1.397

1.112

754

476

463

401

138

120

95

70

23

27.029

14.417

9.682

2.351

421

95

58

60

27.084

5%

7%

-1%

-13%

-61%

5%

10%

4%

2016

2016

2015

2015

2014

2014

2017

2017

2018(E)

2018(E)

Var.́ 18/́ 17

Var.́ 18/́ 17

AMERICA LATINA: PRODUÇÃO DE AÇOS LONGOSLATIN AMERICA: LONG STEEL PRODUCTION

AMÉRICA LATINA: PRODUÇÃO DE AÇO PLANOLATIN AMERICA: FLAT STEEL PRODUCTION

País / Country

País / Country

FONTE / SOURCE: ALACERO. INFORMAÇÃO FORNECIDA PELAS SECRETARIAS REGIONAIS / ALACERO. DATA SUBMITED BY REGIONAL SECRETARIES OUTROS INCLUI PARAGUAI E TRINIDAD & TOBAGO / OTHERS INCLUDE PARAGUAY AND TRINIDAD Y TOBAGO(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2017 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

FONTE / SOURCE: ALACERO. INFORMAÇÃO FORNECIDA PELAS SECRETARIAS REGIONAIS / ALACERO. DATA SUBMITED BY REGIONAL SECRETARIES. (E) 2018 ESTIMADO EN BASE A LOS 8 PRIMEROS MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

Milhares de toneladas / Thousand tons

Milhares de toneladas / Thousand tons

6%

7%

18%

3%

-1%

5%

6%

5%

11%

6%

-13%

5%

5%

5%

6%

6%

América Latina em Cifras Latin America in Figures 25

_ __ __ _

Argentina

Brasil / Brazil

México / Mexico

Venezuela

América Latina /

Latin America

750

657

1.064

-

2.471

360

388

739

-

1.486

376

391

801

-

1.568

621

384

939

-

1.944

736

427

1.000

-

2.164

19%

11%

7%

0%

11%

201620152014 2017 2018(E) Var.́ 18/́ 17

AMÉRICA LATINA: PRODUÇÃO DE TUBOS SEM COSTURALATIN AMERICA: SEAMLESS TUBES PRODUCTION

País / Country

Milhões de toneladas / Million tons

PRODUÇÃO LATINO-AMERICANA

DE LAMINADOS 2018

LATIN AMERICAN FINISHED STEEL PRODUCTION 2018

Milhões de toneladas

Million tons55,8 FONTE / SOURCE: ALACERO. INFORMAÇÃO FORNECIDA PELAS SECRETARIAS REGIONAIS / ALACERO. DATA SUBMITED BY REGIONAL SECRETARIES(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

2016 2017 2018(E)

AMÉRICA LATINA: PRODUCCIÓN Y CONSUMO TRIMESTRAL DE LAMINADOSLATIN AMERICA: QUARTERLY FINISHED STEEL PRODUCTION AND USE

21.000

18.000

15.000

12.000

9.000

6.000

3.000

0

AMÉRICA LATINA: PRODUÇÃO E CONSUMO TRIMESTRAL DE LAMINADOSLATIN AMERICA: QUARTERLY FINISHED STEEL PRODUCTION AND USE

Milhões de toneladas / Million tons

2016 2017 2018(E)

AMÉRICA LATINA: PRODUCCIÓN Y CONSUMO TRIMESTRAL DE LAMINADOSLATIN AMERICA: QUARTERLY FINISHED STEEL PRODUCTION AND USE

21.000

18.000

15.000

12.000

9.000

6.000

3.000

0

Produção / Production Consumo / Consumption

FONTE / SOURCE: ALACERO. INFORMAÇÃO FORNECIDA PELAS SECRETARIAS REGIONAIS / DATA SUBMITED BY REGIONAL SECRETARIES (E) 3T Y 4T 2018 ESTIMADO EN BASE A LOS 8 PRIMEROS MESES / (E) 3Q AND 4Q 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

26. Alacero

_ _

06. Comércio siderúrgico latino-americano Latin American steel trade

_O aço é essencial paraalcançar uma economia circular: Reduzir, Reutilizar, Recuperar, Repensar.

_Steel is fundamental to achievinga circular economy:Reduce, Reuse, Recover, Rethink.

América Latina em Cifras Latin America in Figures 27

_ __ __ _

As importações ainda são uma ameaça

As importações totais de aço

realizadas pela América Latina

reduziram em relação a 2017

principalmente devido ao menor

saldo exportador da China, mas

a participação das importações

sobre o consumo permanece

elevada, e estima-se que atinja

34% até o final de 2018. Esta

situação ocorre e se agrava ano

após ano, gerando desincentivos

para a indústria local, atritos

comerciais e ameaças de desem-

prego. Além disso, em muitos

casos, esses produtos entram

na região a preços de dump-

ing, de países com economias

“não-mercantis”, que subsidiam

a produção de aço e fornecem

facilidades financeiras, fora das

diretrizes da OMC para suas

indústrias. Em 2017, a China

embarcou 7,0 milhões de tonela-

das de aço para a região.

Desde 2015, os governos locais e

as empresas siderúrgicas têm

fortalecido seus esforços para

nivelar o campo de atuação,

seguindo os procedimentos

permitidos pela OMC, por meio

do estabelecimento de ações

antidumping e salvaguardas, bus-

cando garantir a competitividade

internacional do setor.

Imports are still a threat

Total steel imports received by Latin America have contracted with re-spect to 2017, mainly due to China lower export balance, however the share of imports over consumption remains high, and it is estimated to reach 34% by the end of 2018. This situation remains or aggravated year after year, generating disincen-tives for the local industry, trade frictions and threatens jobs. In addi-tion, in many cases these products enter the region at dumping prices, from countries with ‘non-market’ economies, which subsidize steel production and provide financial fa-cilities, outside the WTO guidelines for their industries. In 2017, China shipped 7.0 million tonnes of steel to the region.Since 2015, local governments and steel companies have strengthened their efforts to level the playing field, following the procedures allowed by the WTO, through the establishment of anti-dumping and safeguard actions, seeking to ensure the international competi-tiveness of the industry.

28. Alacero

_ _

Argentina

Brasil / Brazil

Chile

Colômbia / Colombia

México / Mexico

Peru

Venezuela

Outros / Other

América Latina /

Latin America

Argentina

Brasil / Brazil

Chile

Colômbia / Colombia

México / Mexico

Peru

Venezuela

Outros / Other

América Latina /

Latin America

790

3.389

82

85

3.579

162

20

431

8.538

762

3.921

1.561

2.645

8.716

2.054

732

4.327

24.719

394

4.905

67

49

2.910

162

72

491

9.050

1.054

2.825

1.854

2.661

10.217

1.593

956

4.427

25.587

391

4.717

78

60

3.134

203

41

576

9.200

573

1.398

1.604

2.392

9.925

1.750

189

4.455

22.286

706

5.455

99

79

3.349

236

0

699

10.623

1.021

1.995

1.719

2.200

11.086

2.378

108

4.587

25.095

722

5.246

146

114

3.749

217

-

750

10.944

1.302

2.103

1.835

2.428

9.304

1.659

55

4.782

23.467

2%

-4%

48%

44%

12%

-8%

-100%

7%

3%

28%

5%

7%

10%

-16%

-30%

-49%

4%

-6,5%

2016

2016

2015

2015

2014

2014

2017

2017

2018E)

2018(E)

Var.́ 18/́ 17

Var.́ 18/́ 17

AMÉRICA LATINA: EXPORTAÇÕES DE AÇO LAMINADOLATIN AMERICA: FINISHED STEEL EXPORTS

AMÉRICA LATINA: IMPORTAÇÃO DE AÇO LAMINADOLATIN AMERICA: FINISHED STEEL IMPORTS

País / Country

País / Country

FONTE / SOURCE: ALACERO, INFORMAÇÃO FORNECIDA PELAS SECRETARIAS REGIONAIS / INFORMATION SUBMITED BY REGIONAL SECRETARIESOUTROS INCLUEM CUBA, EQUADOR, EL SALVADOR, GUATEMALA, HONDURAS, PANAMÁ, PARAGUAI, REPÚBLICA DOMINICANA E URUGUAI / OTHERS INCLUDE CUBA, DOMINICAN REPUBLIC, ECUADOR, EL SALVADOR, GUATEMALA, HONDURAS, PANAMA, PARAGUAY, AND URUGUAY(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

FONTE / SOURCE: ALACERO, INFORMAÇÃO FORNECIDA PELAS SECRETARIAS REGIONAIS/ INFORMATION SUBMITED BY REGIONAL SECRETARIESOUTROS INCLUEM CUBA, EQUADOR, EL SALVADOR, GUATEMALA, HONDURAS, PANAMÁ, PARAGUAI, REPÚBLICA DOMINICANA E URUGUAI / OTHERS INCLUDE CUBA, DOMINICAN REPUBLIC, ECUADOR, EL SALVADOR, GUATEMALA, HONDURAS, PANAMA, PARAGUAY, AND URUGUAY. (E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

Milhares de toneladas / Thousand tons

Milhares de toneladas / Thousand tons

América Latina em Cifras Latin America in Figures 29

_ _

DÉFICIT COMERCIAL DE AÇO NA AMÉRICA LATINA 2018LATIN AMERICA STEEL TRADE DEFICIT 2018

milhões de toneladas

million tons

é a participação

das importações

sobre o consumo

is the share of imports over consumption

12,5

34%

0

-2.000

-4.000

-6.000

-8.000

-10.000

-12.000

-14.000

-16.000

-18.0002018(E)2017201620152014

2018(E)2017201620152014

25

24

23

22

21

20

34%

25

36%

26

34%

22

37%

25

34%

23

38%

36%

34%

32%

26

AMÉRICA LATINA: BALANÇA COMERCIAL DE LAMINADOS(E)

LATIN AMERICA: FINISHED STEEL TRADE BALANCE(E)

Milhares de toneladas / Thousand tons

AMÉRICA LATINA: EVOLUÇÃO DA PARTICIPAÇÃO DAS IMPORTAÇÕES NO CONSUMO DE LAMINADOSLATIN AMERICA: EVOLUTION OF THE SHARE OF IMPORTS IN THE FINISHED STEEL CONSUMPTION

Milhares de toneladas / Thousand tons

Importações / Imports from ChinaÍndice de importação - Consumo / Imports - Use ratio (%)

2018(E)2017201620152014

25

24

23

22

21

20

34%

25

36%

26

34%

22

37%

25

34%

23

38%

36%

34%

32%

26

FONTE / SOURCE: ALACERO. INFORMAÇÃO FORNECIDA PELAS SECRETARIAS REGIONAIS / DATA SUBMITED BY REGIONAL SECRETARIES. (E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

FONTE / SOURCE: ALACERO, INFORMAÇÃO FORNECIDA PELAS SECRETARIAS REGIONAIS / INFORMATION SUBMITED BY REGIONAL SECRETARIES(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

30. Alacero

_ _

07. Indicadores econômicos e siderúrgicos da América Latina Latin America: Economic and steel indicators

_Uma adequada infraestrutu-ra viária é essencial para a competitividade da indústria siderúrgica e o desenvolvi-mento sustentável na América Latina.

_An appropriate road instructure is essential for the Latin American steel industry and the sustainable development of the region.

América Latina em Cifras Latin America in Figures 31

_ _

Crescimento moderado

Apesar da incerteza política

causada pelos momentos eleitorais

nas principais economias da região,

as crescentes tensões comerciais

geradas pelo protecionismo dos

Estados Unidos e a forte crise

financeira que vem sido mantida

na Argentina desde o segundo

trimestre, a América Latina tem

se beneficiado com o crescimento

econômico global e os altos níveis

de preços das commodities.

Segundo o Fundo Monetário

Internacional (FMI), o crescimento

em 2018 será de 1,2%, mantendo

praticamente o mesmo ritmo do

ano passado. Seria o segundo

ano consecutivo de recuperação

moderada no período recessivo

2015-2016.

Até 2019, é esperado um

crescimento de 2,1% na região,

principalmente como resultado

de recuperações econômicas

mais amplas no Brasil, México e

Colômbia.

Moderate growth

Despite the political uncertainty caused by the electoral cycles in the main economies of the region, the escalatory trade tensions due to United States protectionism, and the strong financial crisis that is facing Argentina since second tri-mester, Latin America has benefited from world economic growth and high levels of commodity prices.According to the International Mon-etary Fund (IMF), growth in 2018 will be 1.2%, maintaining almost the same pace of last year. It would be the second consecutive year of moderate recovery of the recessive period 2015-2016.By 2019, a 2.1% growth is observed in the region, mainly due to of broader economic recoveries in Brazil, Mexico, and Colombia.

32. Alacero

_ _

Argentina

Brasil / Brazil

Chile

Colômbia / Colombia

México / Mexico

Peru

Venezuela

Outros / Other

América Latina /

Latin America

Argentina

Brasil / Brazil

Chile

Colômbia / Colombia

México / Mexico

Peru

Venezuela

América Latina /

Latin America

-2,5%

0,5%

1,8%

4,7%

2,8%

2,4%

-3,9%

4,7%

1,3%

2,7%

-3,5%

2,3%

3,0%

3,3%

3,3%

-6,2%

3,2%

0,3%

-1,8%

-3,5%

1,3%

2,0%

2,9%

4,0%

-16,5%

4,3%

-0,6%

2,9%

1,0%

1,5%

1,8%

2,0%

2,5%

-14,0%

4,6%

1,3%

-2,6%

1,4%

4,0%

2,8%

2,2%

4,1%

-18,0%

4,3%

1,2%

201620152014 2017 2018(E)

AMÉRICA LATINA: EVOLUÇÃO DO PRODUTO INTERNO BRUTOLATIN AMERICA: GROSS DOMESTIC PRODUCT EVOLUTION

AMÉRICA LATINA: EVOLUÇÃO DA PRODUÇÃO INDUSTRIALLATIN AMERICA: INDUSTRIAL PRODUCTION EVOLUTION

País / Country

País / Country

Taxa de variação anual (%) / Annual variation rate (%)

Taxa de variação anual em % / Yearly % variation rate

FONTES / SOURCE: IMF WEO OCTOBER 2018(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

FONTE / SOURCE: ALACERO. DATOS DE SECRETARÍAS REGIONALES / ALACERO. DATA BY REGIONAL SECRETARIES*CIFRA DE AMÉRICA LATINA CONSIDERA SOLO LOS PAÍSES LISTADOS. LATIN AMERICAN NUMBER CONSIDERER ONLY LISTED COUNTRIES.(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

-4,2%

-3,0%

0,4%

0,7%

2,6%

-3,6%

-7,2%

-1,6%

0,3%

-8,3%

0,8%

1,2%

1,1%

-1,5%

-6,8%

-3,1%

-5,7%

-6,4%

-1,5%

3,0%

0,4%

-1,4%

nd

-3,7%

2,1%

2,5%

-0,6%

-2,0%

-0,6%

-0,2%

nd

0,8%

0,5%

2,8%

3,1%

2,7%

0,4%

5,1%

nd

1,3%

201620152014 2017 2018(E)

América Latina em Cifras Latin America in Figures 33

_ _

INDICADORES MACROECONÔMICOSMACROECONOMIC INDEXES

expandirão o PIB mundial em 2018 will expand the world GDP in 2017

3,7% expandirão o PIB da América Latina em 2018

will expand the Latin American GDP in 2018

1,2%

de crescimento da

produção industrial

em 2018

will grow industrial production in 2018

1,3%

FONTE / SOURCE: DADOS DE SECRETARIAS REGIONAIS/ ALACERO. DATA BY REGIONAL SECRETARIES. *NÚMEROS DA AMÉRICA LATINA CONSIDERAM APENAS OS PAÍSES LISTADOS / LATIN AMERICAN NUMBER CONSIDERER ONLY LISTED COUNTRIES.(E) 2018 ESTIMADO COM BASE NOS PRIMEIROS 8 MESES / (E) 2018 ESTIMATIONS ARE BASED ON THE FIRST 8 MONTHS

2017

12%

2015201420132012201120102009

8%

4%

0%

-4%

-8%

2016 2018(E)

PIB / GDP % Produção industrial / Industrial Production (%)

AMÉRICA LATINA: RELAÇÃO CRESCIMENTO DO PIB E DA PRODUÇÃO INDUSTRIAL.LATIN AMERICA: RELATIONSHIP BETWEEN GPD GROWTH AND INDUSTRIAL PRODUCTION

34. Alacero

_ _

08. Siderurgia chinesa: impacto sobre a América Latina Chinese steel industry: impact on Latin America

_560 million tons is the estimated global overcapacity installed, in which China is responsible for 50%, with 280 million tons.

_Estima-se que 560 milhões de toneladas seja a sobrecapacidade instalada a nível global, na qual a China é responsável por 50%, com 280 milhões de toneladas.

América Latina em Cifras Latin America in Figures 35

_ _

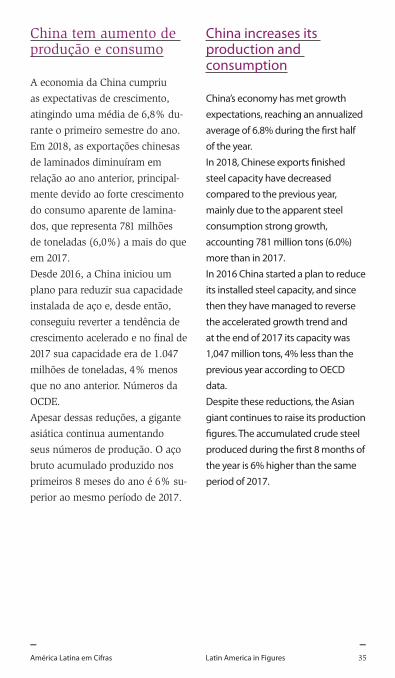

China tem aumento de produção e consumo

A economia da China cumpriu

as expectativas de crescimento,

atingindo uma média de 6,8% du-

rante o primeiro semestre do ano.

Em 2018, as exportações chinesas

de laminados diminuíram em

relação ao ano anterior, principal-

mente devido ao forte crescimento

do consumo aparente de lamina-

dos, que representa 781 milhões

de toneladas (6,0%) a mais do que

em 2017.

Desde 2016, a China iniciou um

plano para reduzir sua capacidade

instalada de aço e, desde então,

conseguiu reverter a tendência de

crescimento acelerado e no final de

2017 sua capacidade era de 1.047

milhões de toneladas, 4% menos

que no ano anterior. Números da

OCDE.

Apesar dessas reduções, a gigante

asiática continua aumentando

seus números de produção. O aço

bruto acumulado produzido nos

primeiros 8 meses do ano é 6% su-

perior ao mesmo período de 2017.

China increases its production and consumption

China’s economy has met growth expectations, reaching an annualized average of 6.8% during the first half of the year.In 2018, Chinese exports finished steel capacity have decreased compared to the previous year, mainly due to the apparent steel consumption strong growth, accounting 781 million tons (6.0%) more than in 2017.In 2016 China started a plan to reduce its installed steel capacity, and since then they have managed to reverse the accelerated growth trend and at the end of 2017 its capacity was 1,047 million tons, 4% less than the previous year according to OECD data.Despite these reductions, the Asian giant continues to raise its production figures. The accumulated crude steel produced during the first 8 months of the year is 6% higher than the same period of 2017.

36. Alacero

_ _

650

700

750

120

100

80

60

40

20

0

2013 2014 2015 2016 2017

Producción / Production Consumo / Consumption Exportaciones / Exports

60

110

800

850

900

73

FONTE / SOURCE: WORLDSTEEL (SRO OCTOBER 2018) / ALACERO / ALFÂNDEGA CHINESA / CHINESE CUSTOMS SERVICE

FONTE / SOURCE: BASE DE DADOS DE EXCESSO DE CAPACIDADE DE PRODUÇÃO DA OCDE / OECD STEELMAKING CAPACITY DATABASE.

SOBRECAPACIDAD DE CHINA Y EL MUNDO

0

100

200

300

400

500

Millones de toneladas / Million tons

2013 2015 2017

Mundo sem China / World without China China

OVERCAPACITY IN THE WORLD AND CHINA

287264 280 280

450

334

PRODUÇÃO, CONSUMO E EXPORTAÇÕES DE AÇO CHINA: PRODUCTION, CONSUMPTION AND EXPORTS OF STEEL

Milhões de toneladas / Million tons

650

700

750

120

100

80

60

40

20

0

2013 2014 2015 2016 2017

Produção / Production Consumo / Consumption Exportações / Exports

60

110

800

850

900

73

EXCESSO DE CAPACIDADE NO MUNDO E NA CHINAOVERCAPACITY IN THE WORLD AND CHINA

Milhões de toneladas / Million tons

SOBRECAPACIDAD DE CHINA Y EL MUNDO

0

100

200

300

400

500

Millones de toneladas / Million tons

2013 2015 2017

Mundo excluyendo China / World without China China

OVERCAPACITY IN THE WORLD AND CHINA

287264 280 280

450

334

América Latina em Cifras Latin America in Figures 37

_ _

2013 2014 2015 2016 2017(E)

6,3

15,7 15,4

9,3 9,4

16,2

7,6

14,7

7,0

18,1

FONTE / SOURCE: ALACERO - ALFÂNDEGA CHINESA / CHINESE CUSTOMS SERVICE

AMÉRICA LATINA: EVOLUÇÃO DE IMPORTAÇÕES DE AÇO LAMINADOLATIN AMERICA: EVOLUTION OF FINISHED STEEL IMPORTS

2013 2014 2015 2016 2017(E)

6,3

15,7 15,4

9,3 9,4

16,2

7,6

14,7

7,0

18,1

Importações da china / Imports from ChinaImportações do resto do mundo / Imports from ROW

Milhões de toneladas / Million tons

AMÉRICA LATINA: EVOLUÇÃO DO ÍNDICE DE IMPORTAÇÕES/CONSUMO DE AÇO LATIN AMERICA: EVOLUTION OF STEEL IMPORTS/USE RATIO

2012 2013 2014 2015 2016

33%

30% 31%

34%37%

20172010 201|1

36%30%

25%

20%

5%

0%

34%

9%

31%

11%12%11%

7%6%5%6%

15%

10%

FONTE / SOURCE: ALACERO - ALFÂNDEGA CHINESA / CHINESE CUSTOMS SERVICE

Importações chinesas / Chinese imports Resto do mundo / ROWÍndice de importação da China - Consumo (%) / Importsfrom China - Use ratio (%)Índice total de importações - Consumo (%) / Importsfrom China - Use ratio (%)

Associação Latino-Americana de Aço

Alameda Santos 2.300, conjunto 62

CEP: 01418-200 - São Paulo, SP, Brasil

[email protected] | www.alacero.org

Tel: (+55) 11 3195 5491

@RedAlacero Alacero Alacero